Embed Size (px)

Citation preview

Investor PresentationIstanbul, Turkey – March 2018

2

Agenda

1. Turkey at a Glance

2. Our Markets

• Private Pension System

• Life Insurance

3. Corporate Profile

4. Financial Results

Turkey at a Glance

4

Turkey at a GlanceA Fast Growing Economy

0%

1%

2%

3%

4%

5%

6%

1990-1999 2000-2009 2010-2016

GDP Average Annual Growth*

Turkey OECD Euro-15

Source: *OECD National Accounts Data, **IMF, ***Turkish Statistics Institute, ****World Bank National Accounts Data

Over the last decade and half, Turkey

successfully stabilized its macro economy.

After the 1999–2001 economic crisis, Turkey

maintained a highly successful policy of

macroeconomic stabilization.

-6%

-5%

-4%

-3%

-2%

-1%

0%

2011 2012 2013 2014 2015 2016 2017

Budget Balance (% of GDP)**

Euro Area EM Turkey

0%

5%

10%

15%

20%

25%

CPI*** and Interest Rates****

CPI Interest Rates

5

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2011 2012 2013 2014 2015 2016 2017

Current Account Balance (% of GDP)*

Euro Area EM Turkey

Turkey at a GlanceUrgent Need to Increase Domestic Savings

Source: *IMF, except for Turkey’s domestic saving rate which is from Ministry of Development

**CBT Financial Stability Report: All data represents 3rd quarter figures, except for 2012 which

shows the year-end figures

0%

1%

2%

3%

4%

5%

6%

7%

0

250

500

750

1.000

1.250

2011 2012 2013 2014 2015 2016 2017

Weight of Pension Funds in Household Savings (TRY billion)**

Pension Funds Total Household Savings Weight of Pension Funds

Republic of Turkey – Medium Term Programme

Article 81: “Charging ratio will be converged

to international levels in the private pension

system and “auto enrolment system” will be

implemented. Life insurance and long-term

(over one year) private health insurance will

be developed.”

Medium Term Programme (2016-2018), prepared by Ministry

of Development was adopted by Cabinet Decree No.

2015/8355, 29.12.2015 and published in Official Gazette No.

29590, 11.01.2016.

10%

15%

20%

25%

30%

35%

2011 2012 2013 2014 2015 2016 2017

Domestic Saving Rate (% of GDP)*

Euro Area EM Turkey

6

Turkey at a GlanceDemographic Opportunity Window

2017 2050

Population (millions) : 80.8 93.5

Median Age : 31.7 43

Fertility : 2.10 1.65

Proportion of Elderly Population : 8.5% 20.8%

2018

January

Population 15 Years And Over (thousands) : 60,360

Labor Force (thousands) : 31,438

Employed (thousands) : 28,029

Labor Force Participation Rate : 52.1%

Unemployment Rate : 10.8%

Non-Agricultural Unemployment Rate : 12.7%

Source: Turkish Statistics Institute – The World Bank - IMF

Decreasing fertility and increasing longevity means a demographic transition.

• 47 percent of the population is under 30 years old.

• Only 9 percent of the population is over 64 years old.

• The youth dependency ratio is relatively high.

• More people are living off retirement savings, thus a decrease in the saving rate

is a common issue.

• In the interim period when the youth dependency ratio is falling fast and the old-

age dependency ratio is only increasing modestly; larger potential labor force and

higher private saving to fund investment is a major demoghraphic advantage.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Population By Age

2017 2050

Our Markets

Private Pension System

Life Insurance

8

Our MarketsPrivate Pension System: Positioned in Pillar III

Three-Pillar System

Pillar I

State Pension

Mandatory

Securing a minimum

standard of living

Retirement, health,

disability and

unemployment

Pillar II

Occupational

Pension

Workplace Pensions

with Auto Enrolment

starting by 2017

Maintenance of

current living

standards in terms of

replacement rate

Pillar III

Private Pension

Voluntary

Opportunity to

increase retirement

income

Available since 2003

9

Our MarketsPillar III Private Pension System: Important Features

Defined contribution and

voluntary participation.

Funds are managed by

asset management

companies.

Minimum retirement age: 56

Completion of 10 years.

Started in 2003.

17 companies in 2018.

Participants can switch funds,

pension plans and transfer

between companies.

Incentives for both

participant and employer.

10

Pillar III Private Pension System: Well Designed Structure

Pension

Monitoring Center

(EGM)

ISE Settlement

and Custody

Bank

(Takasbank)

Capital Markets

Board (SPK)

Undersecretariat

of Treasury

Ministry of Labor

and Social

Security

Ministry of

Finance

Pension

Accounts

Administered by

Pension

Companies

Pension Funds

Managed by

Asset

Management

Companies

Our Markets

Regulation Administration Monitoring

11

Our MarketsPillar III Private Pension System: Incentives

For Participants For Employers

• Contributions with a cap of

annual legal minimum wage is

subject to 25% state

contribution.

• Vesting Period:

% 15 at the end of 3 years

% 35 at the end of 6 years

% 60 at the end of 10 years

% 100 at retirement date or

death/disability cases

• Investment income of

pension funds are tax

exempt.

• Transaction of pension

funds are exempt of fees

and taxes.

• Withholding tax applies only

on the investment income:

5% (completion of 10 years in

the system & 56 years of age)

10% (completion of 10 years in

the system)

15% (early leave, before

completion of 10 years in the

system)

Contribution Stage Investment Stage Benefit Payments Employer contributions are

tax deductible up to 15% of

gross salary with a cap of

annual legal minimum wage.

12

Our MarketsPillar III Private Pension System: Charging Structure

Management Fee / Entrance Fee Fund Management Fee

First 5 years of the contracts No change in fund management

fee levels. A new rebate structure

will be implemented by 2021.

Maximum limit: 8.5% of the

monthly legal minimum wage

• Applicable for the first 5 years of

the contract.

• One common cap for entrance fee

and management fee.

Fund Management Fees

• Money market funds: 1.09%

• Fixed income & index funds: 1.91%

• Equity and managed funds: 2.28%

• State contribution funds: 0.36%

Rebate Structure

• Beginning with 2.5% by the 6th

year of the contract.

• 2.5% gradual increase each year.

• Maximum 25% after the 15th year.

• Rebate is not applicable below

1.1% of pension assets.

13

Our MarketsPillar III Private Pension System: Growth Accelerated with Increased Government Support

Und

er

Dis

cu

ssio

n

Imp

lem

ente

d

• 25% State Contribution since 2013

• Withholding tax limited to capital gains

• Pension fund transfers from provident

funds* by the end of 2017

• Fee Structure Efficiency

• Auto-Enrolment started in 2017

• Deconcentration of asset managers

(effective by 2018)

• Severance Payments

* Funds from associations, foundations, provident funds and other organizations with retirement provisions.

Source: Pension Monitoring Center as of 31.03.2018

0

10

20

30

40

50

60

70

80

90

AUM State Contribution

Pension AUM Growth(TRY billion)

0

1.000

2.000

3.000

4.000

5.000

6.000

7.000

8.000

Number of Participants(Thousands)

14

Our MarketsPillar III Private Pension System: Big Growth Potential

125,7%

49,5%

4,8%

0% 25% 50% 75% 100% 125% 150% 175% 200%

Netherlands

United States

Weighted average

United Kingdom

Finland

Israel

Simple Average

Japan

Spain

Slovak Republic

Portugal

Poland

Slovenia

Belgium

Germany

Austria

Turkey

Hungary

Pension Funds as a Percentage of GDP

Turkey

OECD Simple Average

OECD Weighted Average

Big Growth Potential

The Turkish pension market has a very low level of GDP

penetration compared to other countries with similar GDP

per capita.

This illustrates a huge growth potential when combined

with the demographic opportunity window.

Pension Participants

6.9 MillionSocial Security Participants

22 Million

Work Force

31.4 Million

Working-Age Population

60.4 MillionTotal Population

80.8 Million

Source: OECD Pension Markets in Focus 2017; Turkish Statistics Institute as of 31.01.2018; Social Security Institution as of 28.02.2018;

Pension Monitoring Center as of 31.03.2018

15

Our MarketsAttractive Market

109

6 65

4 4 4

1314

1718

19 1918 18

2010 2011 2012 2013 2014 2015 2016 2017

Life Private Pension

The Number of Companies*

61%

73% 74%69%

65% 65% 63%

36% 37% 39%

45%

52%54% 53%

2010 2011 2012 2013 2014 2015 2016

Paid-In Capital GWP

Foreign Investment Share

The pension system started with 11 companies in 2003.

Due to strong growth expectations and government support,

the system attracted more local and international groups.

Source: Undersecretariat of Treasury, Insurance and Private Pensions Annual Reports

* Active companies

16

Our MarketsPillar III Private Pension System: Key Highlights

Key Figures

Participants : 6.9 Million

Participant Funds : TRY 70.3 Billion

State Contribution Funds : TRY 10.3 Billion

Assets Under Management : TRY 80.7 Billion

Intermediaries : 45,104

Pension Companies : 17

5,6%

27,4%

33,8%

23,8%

9,4%

0-25 25-34 35-44 45-55 56+

Participant Age Distribution

Individual75,5%

Non-Sponsored

Groups20,1%

Employer Sponsored Groups 4,4%

Contributions Total Amount by

Contract Type

Bank72%

Other; 2%

Direct Sales11%

Corporate Sales4%

Agent11%

Distribution of Contributions

by Marketing Channel(2016 total)

1.000

1.500

2.000

2.500

3.000

2008 2009 2010 2011 2012 2013 2014 2015 2016

Average of Total Amount of Regular Contributions per Year (TRY)

Source: Pension Monitoring Center

As of 31.03.2018

17

Our MarketsPrivate Pension System: Pension Funds*

Equity11,5%

Repo and Money Market Instruments

6,1%

International Securities

2,0%

Government Bonds46,5%

Corporate Bonds12,9%

Time Deposits21,0%

Asset Allocation of Pension Funds

Number of Funds : 402

Total AUM : TRY 83.0 Billion

Return on Pension Funds (2004-2018Q1)

Nominal : 423.0%

Real : 61.9%

23,9%

19,6%

11,1%

18,4%

9,5%

23,3%

9,6%

0,1%

17,9%

-0,2%

14,5%

3,0%

10,9%

15,4%

2,0%

13,3%11,0%

1,3%

9,2%

-0,5%

15,8%

3,0%

-9,4%

11,0%

-7,1%

5,9%

-5,4%

2,2% 3,1%

-0,7%

Nominal & Real Investment Return of Pension Funds

Nominal Return Real Return

As of 31.03.2018 * Includes Auto Enrolment funds

18

Our MarketsPrivate Pension System: New Frontiers

Auto

Enrolment

Severance

Payments

Simplification

of Fund

Choices

Deconcentration

of Asset

Managers

19

Our MarketsAuto Enrolment: Basic Features*

Automatic

enrolment of

current and new

employees under

age 45

Gradual

implementation

based on

company

scale

Minimum

contribution

amount

set as

%3 of

monthly

wage

State contribution:• 25% on contributions

• 1,000 TRY initial bonus

• 5% of assets at

annuity phase

Simplified

fund menu

Simplified and

automated

enrolment and

collection

process

2 months of call

back period.

Voluntary opt-out

at any time

Law enacted in 2016,

in force by 2017.

First three phases

are completed.

Structural changes

in marketing, sales

and service model

SME & Corporate

* Based on the Law enacted in August 2016 and the complementary legislation.

No

employer

contribution

20

Our MarketsAuto Enrolment System: Incentives

For Participants

• Contributions with a cap of annual legal

minimum wage is subject to 25% state

contribution. This limit is set independently

of Pillar III contracts.

• Initial 1,000 TRY bonus if the employee

stays in the system.

• Vesting Period For State Contribution

% 15 at the end of 3 years

% 35 at the end of 6 years

% 60 at the end of 10 years

% 100 at retirement date or death/disability

cases

• State contributions are booked in a separate

account as a commitment and will be

subject to revaluation indexed to CPI. The

accrued amounts will be funded gradually

according to the vesting schedule.

• Investment income of auto enrolment funds

are tax exempt.

• Additional state contribution equal to 5% of

savings at retirement date is provided in

case of transfer into an annuity contract with

a minimum term of ten years.

Contribution Stage Investment Stage Retirement Stage

21

Our MarketsAuto Enrolment System: Charging Structure

Management Fee / Entrance Fee Fund Management Fee

No management or entrance fee. Fund management fee level is

capped.

According to the Law enacted in

August 2016, no management or

entrance fee is allowed in Auto

Enrolment System.

Fund Management Fee is capped at

a maximum of 0.85%.

22

Our MarketsAuto Enrolment - New Target Market

DatePrivate

Sector

Public

Sector

Number of

Employees***%

2017 January 1,000+ - 2.2 Million 15.4

2017 April 250 – 999 Public administrations 4.0 Million 28.3

2017 July 100 – 249 - 1.5 Million 10.7

2018 January 50 – 99Public enterprises +

local administrations1.3 Million 9.1

2018 July 10 – 49 - 2.7 Million 19.1

2019 January 5 - 9 - 2.5 Million 17.4

Total 14.2 Million 100

WORKFORCE*

* Social Security Institution February 2018, Turkish Statistics Institute, January 2018

** Estimated as 75% of the 4a and 4c participants *** Target market estimated by Undersecretariat of Treasury

Eligible Employees

(age less than 45)**

12.8 Million

Social Security Participants

(4a&4c)

17.1 Million

Social Security Participants

22 MillionEmployed

28.03 MillionWork Force

31.4 Million

3,0 Million (4c public sector)

13,3 Million(4a private sector)

0,9 Million (4a public sector)

SOCIAL SECURITY PARTICIPANTS (4A&4C)

Staging Process

Staging process defined in the complementary legislation

Public sector in 2017

Gradual staging for private sector beginning with large scale

companies (+1,000 employees)

23

Our MarketsAuto Enrolment – Market Preview

Market Size*

Number of Employees 3,836,070

Number of Certificates 3,955,076

Total Funds (TRY) 2,427,149,445

*Source: Pension Monitoring Center as of 31.03.2018

Staging Process

Fourth phase of Auto Enrolment have been

started.

The employees of private companies over 50

employees and public administrations has been

enrolled in one of auto enrolment plans.

Date Target

2017 January Private companies with 1,000+ employees

2017 AprilPrivate companies with 250-999 employees

Public administrations

2017 July Private companies with 100-249 employees

2018 JanuaryPrivate companies with 50-99 employees

Public enterprises and local administrations

2018 July Private companies with 10-49 employees

2019 January Private companies with 5-9 employees

24

Our MarketsLife Insurance: Underpenetrated Market

21

144 164

962

658

1.620

353285

638

Life Insurance Non Life Insurance Total Insurance

Turkey Europe World

Insurance Premium per Capita (USD)

Global Comparison (2016)

Source: Sigma, SwissRe

Country /

Region

Life GWP

(in % of GDP)

Share of World Market

(in %)

Turkey 0.2 0.06

Europe 4.0 32.8

OECD 4.0 75.7

World 3.5 100

Life insurance market has great potentials in Turkey.

Turkey’s life insurance market is extremely

underpenetrated as life premiums’ weight in GDP is only

1/20 of OECD average.

Low penetration level - when combined with favorable

demographics and strong government support for saving

and annuity products - demonstrates high growth

potential.

25

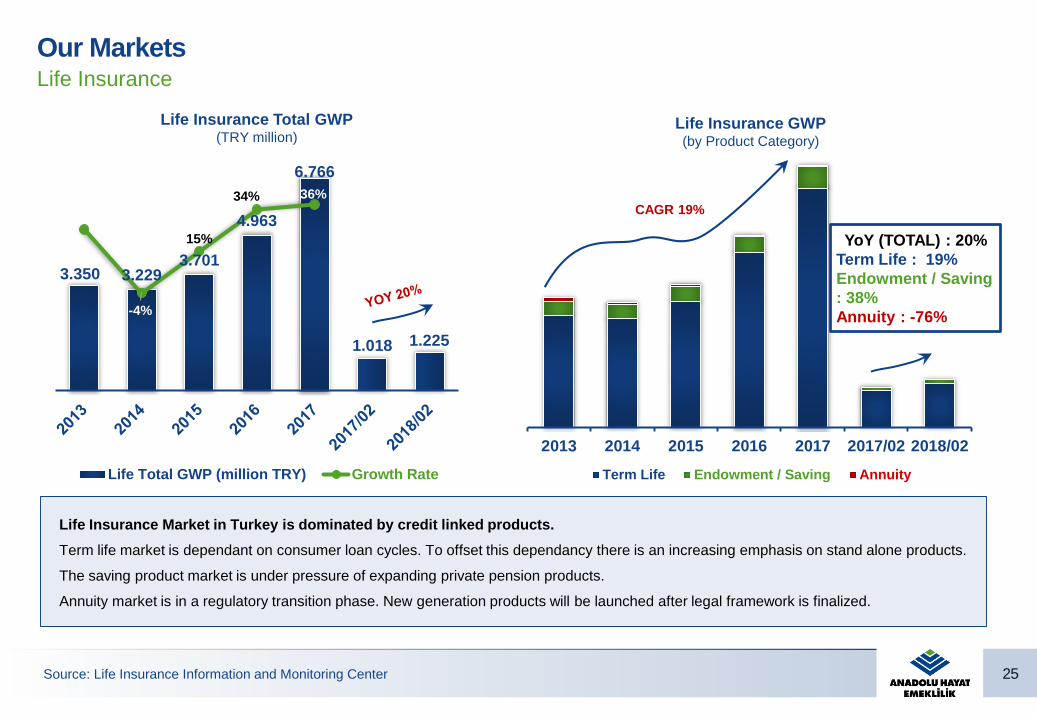

Our Markets

Life Insurance Total GWP(TRY million)

3.350 3.2293.701

4.963

6.766

1.018 1.225

-4%

15%

34% 36%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

-100,00

900,00

1.900,00

2.900,00

3.900,00

4.900,00

5.900,00

6.900,00

Life Total GWP (million TRY) Growth Rate

2013 2014 2015 2016 2017 2017/02 2018/02

Term Life Endowment / Saving Annuity

CAGR 19%

Life Insurance GWP(by Product Category)

Life Insurance Market in Turkey is dominated by credit linked products.

Term life market is dependant on consumer loan cycles. To offset this dependancy there is an increasing emphasis on stand alone products.

The saving product market is under pressure of expanding private pension products.

Annuity market is in a regulatory transition phase. New generation products will be launched after legal framework is finalized.

Source: Life Insurance Information and Monitoring Center

Life Insurance

YoY (TOTAL) : 20%

Term Life : 19%

Endowment / Saving

: 38%

Annuity : -76%

Anadolu Hayat Emeklilik

Corporate Profile

27

Anadolu Hayat EmeklilikAt a Glance

Free Float15%

İşbank64% Anadolu

Sigorta20%

Milli Reasürans

1%

Ownership Structure*

Established in 1990 as a subsidiary of İşbank

First life insurance company in Turkey

The first publicly traded Life & Pension Company since 2000

Operating in pension business since 2003

Strong market position in life insurance and private pension

businesses

Strong shareholder structure

Sector’s leader in total assets with TRY 18.4 billion

SECTOR’S

LEADERLife and Private

Pension Funds

TRY 17 Billion

SECTOR’S

LEADERPrivate Pension

Contracts

1.3 Million

* The rate of publicly traded shares is 17%. As at 23 February 2017, İşbank owns the 1.89% of the publicly traded shares.

28

Anadolu Hayat EmeklilikAt a Glance

I OrganizationHeadquartered in Istanbul

11 District Sales Offices

Branch Office in TRNC

IIHuman

Resources

HQ and Regions :

Direct Sales Team :

Total :

534

506

1,040

IIIFinancial

Metrics

Total Assets :

Shareholders’ Equity :

Gross Profit :

Market Value :

TRY 18,446 million

TRY 819 million

TRY 93 million

TRY 3,204 million

IV Brand Value First remembered private pension company 35% *

VMarket

Position

Private Pension

Contracts :

Participants :

Assets Under Management :

#1 – 16%

#2 – 16%

#2 – 19%

Life Insurance

AUM (Mathematical Reserves) :

Gross Written Premium :

#1 – 26% **

#4 – 8%

* Source: TNS, as of February 2018

** As of February 2018

29

Anadolu Hayat EmeklilikFinancial Highlights(Million TRY) 2016 2017 Change 2017Q1 2018Q1 Change

Total GWP and Net Contributions 1,859.3 2,203.7 19% 458.5 619.9 35%

Life Mathematical Provisions 1,682.4 1,725.7 3% 1,703.1 1,709.7 0.4%

Pension AUM 11,359.4 14,712.8 30% 12,173.8 15,314.5 26%

Total Assets 14,391.7 17,877.2 24% 15,170.2 18,445.6 22%

Shareholders Equity 860.9 926.6 8% 766.3 819.1 7%

Total Technical Profit 133.0 199.2 50% 43.0 65.2 52%

Non Life -0.57 -0.55 -4% 0.0 -0,3 -

Life 112.5 132.6 18% 31.2 40.8 31%

Private Pension 21.1 67.1 218% 11.8 24.7 108%

Financial Income 123.4 124.3 1% 32.6 39.7 22%

Profit for the Period 229.8 279.8 22% 63.4 92.7 46%

Net Profit 190.3 224.7 18% 51.7 74.0 43%

Key Financial Metrics 2016 2017

ROAE 23% 25%

Expense Ratio 17.2% 16.0%

P/E Ratio 11.2 15.8

P/B Ratio 2.5 3.8

Earnings per Share 0.44 0.52

2017Q1 2018Q1

25% 28%

17.5% 16.1%

10.8 13.0

2.8 3.9

0.47 0.57

30

Anadolu Hayat EmeklilikLines of Business

Private

Pension

Individual

Plans

Non-

Sponsored

Group Plans

Employer

Sponsored

Group Plans

Income

Drawdown

Plans

Life

InsuranceAnnuities Term Life

Savings &

Endowment

Personal

Accident

Insurance

Group

Accident

Insurance

Personal

Accident

Insurance

Low RiskMedium

RiskHigh Risk

Money Market

Conservative Flexible

Private Sector DebtInstruments

Group Conservative

Initial

Initial Participation

Auto EnrolmentConservative

Bond Fund

First Debt Instruments

Second Debt

Instruments

Developed Countries

Flexible

Balanced Flexible

Participation Standard

Contribution

Participation

Contribution

Group Bond

Group Debt

Instruments

HSBC Asset Mngt.

Debt Instruments

Standard

Auto Enrolment

Balanced

Auto Enrolment

Standard

Auto Enrolment

Participation Standard

Equity Fund

Dynamic Flexible

BRIC Plus

Aggressive Flexible

Gold

Group Equity

Second Equity

Isbank Subsidiaries

Index

Auto Enrolment

Aggressive

Auto Enrolment

Dynamic

Auto Enrolment

Aggressive

Participation

Auto Enrolment

Dynamic Participation

Lines of Business Pension Funds

Auto

Enrolment

Auto

Enrolment

Plans

31

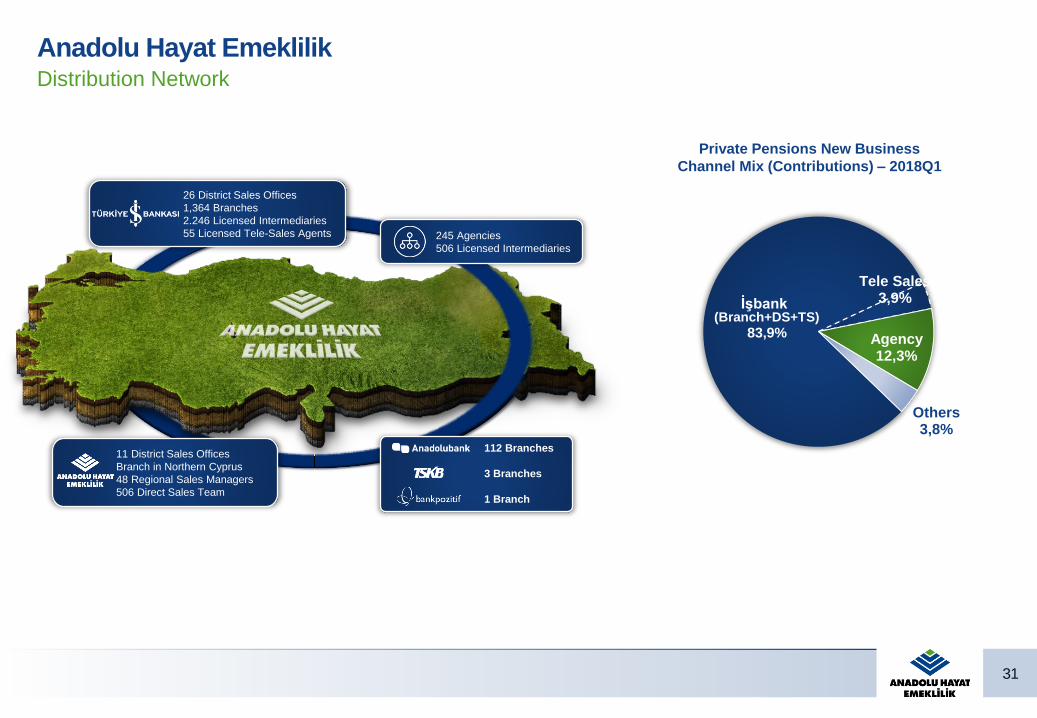

Anadolu Hayat EmeklilikDistribution Network

26 District Sales Offices

1,364 Branches

2.246 Licensed Intermediaries

55 Licensed Tele-Sales Agents

11 District Sales Offices

Branch in Northern Cyprus

48 Regional Sales Managers

506 Direct Sales Team

245 Agencies

506 Licensed Intermediaries

112 Branches

3 Branches

1 Branch

Private Pensions New Business

Channel Mix (Contributions) – 2018Q1

(Branch+DS+TS)

83,9%

Tele Sales3,9%

Agency12,3%

Others3,8%

İşbank

32

Anadolu Hayat EmeklilikDeep Bench with Lots of Talent

Total Number

of Employees: 1,040

4%

24%

35%

21%

9%

4%

2%

18-24

25-29

30-34

35-39

40-44

45-49

50+

Young & Energetic

0,4%

3%

89%

8%

Primary Level

High School

University

Graduate

Educated

62%

38%

Female

Male

Diverse

33

Anadolu Hayat EmeklilikCorporate Strategy

Finance

Become the market leader among private

pension and life insurance companies

Customer

Optimize customer and product portfolio to

make the best use of sales potential

Process

Design cost oriented simple processes for

top-notch customer experience

Improvement

and Learning

Continuously develop business model and human

resources to become the leader in all arenas

Become both the private

pension and life insurance

market leader

Optimize operational

profitability and efficiency

Optimize ROE and risk

portfolio

Utilize the Bancassurance

channel in the most

effective way

Make the best use of up

and cross selling

opportunities

Extend quality customer

base

Develop integrated, agile

and solution focused

systems

Optimize acquisition and

service related costs by

digitalization

Become a superb service

provider

Differentiate through new

infrastructure and

business model

Enhance collaboration and

interaction within teams

Become the first choice for

employees through high

performance teams

34

Anadolu Hayat EmeklilikStrong Infrastructure

Core System Transformation

Project

The first phase of the

transformation project to serve

private pension operations

established in February 2017

including a huge migration from

the old legacy system. Second

phase of the project covering life

insurance operations has started

in 2017.

New IT infrastructure is flexible,

modular and state of the art which

will reduce reliance on IT

resources, reduce the time to

market for new products, gain

process efficiencies with

automation for a unique

customer experience, reduce

operational risk, increase the

ability to deal with regulatory

change.

CRM

Hardware Architecture

Transformation(Exadata)

Payment and Collection

Processes Module(Payment HUB)

Commission and

Intermediary Campaigns

Rule Engine

Mechanization of

Operational Processes

Digital Corporate Identity(AHEŞUBE, AHEMOBİL, AHEPAD)

Financial Systems

Transformation(GL / FAH)

Insurance Applications

Transformation

Integrated BI and

Reporting Platform(Atlas)

35

Anadolu Hayat EmeklilikFocus on Customer Retention

97

98

99

100O

ct-

03

Jan

-04

Ap

r-04

Jul-0

4

Oct-

04

Jan

-05

Ap

r-05

Jul-0

5

Oct-

05

Jan

-06

Ap

r-06

Jul-0

6

Oct-

06

Jan

-07

Ap

r-07

Jul-0

7

Oct-

07

Jan

-08

Ap

r-08

Jul-0

8

Oct-

08

Jan

-09

Ap

r-09

Jul-0

9

Oct-

09

Jan

-10

Ap

r-10

Jul-1

0

Oct-

10

Jan

-11

Ap

r-11

Jul-1

1

Oct-

11

Jan

-12

Ap

r-12

Jul-1

2

Oct-

12

Jan

-13

Ap

r-13

Jul-1

3

Oct-

13

Jan

-14

Ap

r-14

Jul-1

4

Oct-

14

Jan

-15

Ap

r-15

Jul-1

5

Oct-

15

Jan

-16

Ap

r-16

Jul-1

6

Oct-

16

Jan

-17

Ap

r-17

Jul-1

7

Oct-

17

Jan

-18

Continuity Index (%)

AHE System Sector Average

* Pension Monitoring Center data as of February 2018 (last 12 months’ average)

• Key account management

• Consultancy through investment managers

• Exclusive customer service on call center

• Special customer loyalty programs

• Premium gifts for special days

Lowest churn rate in

peer group• 1% monthly churn rate* (1.2% sector

average)

Extensive use of CRM• Campaign, lead and customer

complaints management, key account

management

Predictive Modeling

• Churn risk ratios based warning & action

processes

• Customer profiling

• Offers based on customer behaviors

VIP segment

focus

• Campaigns to raise regular and additional

contributions

• Automated collection warning mechanisms.

Collections

Performance

• Customer experience program

• Customer satisfaction surveys & researches

• Actions based on the results of customer

focus group feedback

• Customer journeys based on different

personas

Customer

Experience

ManagementOutbound retention

calls

• Reduce churns, increase cross-selling,

improve customer interaction and keep it

alive, inform, raise regular contributions,

avoid non payment

• Emphasis of benefits in outbound calls

36

Anadolu Hayat EmeklilikA Strong Brand Name

*Celent is a global research and advisory firm for the financial services industry.

**SocialBrands Data Analytics Awards evaluate brands’ performance according to the SocialBrands social media brand index which is

consolidated from independent data

First and only

UNEP-FI member of

Turkish insurance

sector

Received golden prize in

2017 SocialBrands Data

Analytics Awards among

private pension and life

insurance firms **

financial services industry.

«Best corporate

transformation» award

by International Data

Corporation (IDC) Turkey

Turkey’s first company to

receive the prestigious

«Customers’ Friend»

award by ICERTIAS in

customer relationship

management

Anadolu Hayat Emeklilik has

been recognized by Celent as

a winner of a Model Insurer

2018 award for «Legacy and

Ecosystem Transformation».*

37

Anadolu Hayat EmeklilikStrong Market Positioning in Private Pensions

733.137

863.365

1.026.5931.120.505 1.148.227 1.126.904 1.146.723

0,00

200.000,00

400.000,00

600.000,00

800.000,00

1.000.000,00

1.200.000,00

1.400.000,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

18% 17% 17%

Market Share

Participants

Technical Profit (TRY million)

5.243

7.394

8.945

11.366

14.581

12.185

15.126

0,00

2.000,00

4.000,00

6.000,00

8.000,00

10.000,00

12.000,00

14.000,00

16.000,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

20% 20% 19% 19%

Market Share

Assets Under Management (TRY million)

4.3335.497

6.831

8.189

9.6488.507

10.053

0,00

2.000,00

4.000,00

6.000,00

8.000,00

10.000,00

12.000,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

Contributions (TRY million)

Source: Pension Monitoring Center

20% 19% 18% 18%

Market Share

17% 17% 19%

18%

-11,1

3,7

22,0 21,1

67,1

11,8

24,7

-20,00

-10,00

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

CAGR 106%

17% 16% 19% 19%

18% 18%

38

394,2365

402,1

500,6

574,7

140,8 151,0

0,00

100,00

200,00

300,00

400,00

500,00

600,00

700,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

Anadolu Hayat EmeklilikStrong Market Positioning in Life Insurance

12% 11% 11% 10%

Market Share

Life Insurance GWP (TRY million)

Technical Profit (TRY million)

186,2 198,2

259,0

395,0

459,4

114,0 114,7

0,00

50,00

100,00

150,00

200,00

250,00

300,00

350,00

400,00

450,00

500,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

6% 7% 8% 9%

Market Share

Term Life GWP (TRY million)

Mathematical

Reserves –

Life Insurance

Fund Size

Market Share*

AHE26%

Others; 74%

Market

Leader with

1.7 billion

TRY AUM

*As of 28.02.2018

9% 7.4%

Term Life76%

Saving21%

Annuity3%

2018Q1

63,4 63,8

86,5

112,5

132,6

31,240,8

0,00

20,00

40,00

60,00

80,00

100,00

120,00

140,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

8% 8% 6%*

Source: Insurance Association of Turkey , Life Insurance Information and Monitoring Center

39

Anadolu Hayat EmeklilikStatutory Financials

99,0

134,8

175,9

229,8

279,8

63,4

92,7

0,00

50,00

100,00

150,00

200,00

250,00

300,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

52,367,5

108,3

133,0

199,2

43,0

65,2

0,00

50,00

100,00

150,00

200,00

250,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

Gross Profit for the Period (mio TRY)

Technical Profit (mio TRY)

124 128 184 215 249

620710

789877

949

0

200

400

600

800

1000

1200

1400

2013 2014 2015 2016 2017

Required Capital Total Capital

500% 553% 430% 408%

Capital Adequacy Ratio

Shareholders’ Equity and Capital Adequacy Ratio (mio TRY)

2013 2014 2015 2016 2017

ROAE 15% 16% 20% 23% 25%

381%

40

Anadolu Hayat EmeklilikStatutory Financials

Net Distributable Profit / Dividend to Shareholders (mio TRY) Dividend Payout Ratio (%)

8290

142

186

221

5060

100

140

170

0

50

100

150

200

250

2013 2014 2015 2016 2017

Net Distributable Profit Dividend to Shareholders

61

6770

7577

2013 2014 2015 2016 2017

Cash Dividend / Net Distributable Profit (%)

0.14 0.16 0.24 0.33 0.40

Dividend per Share Gross (TRY)

41

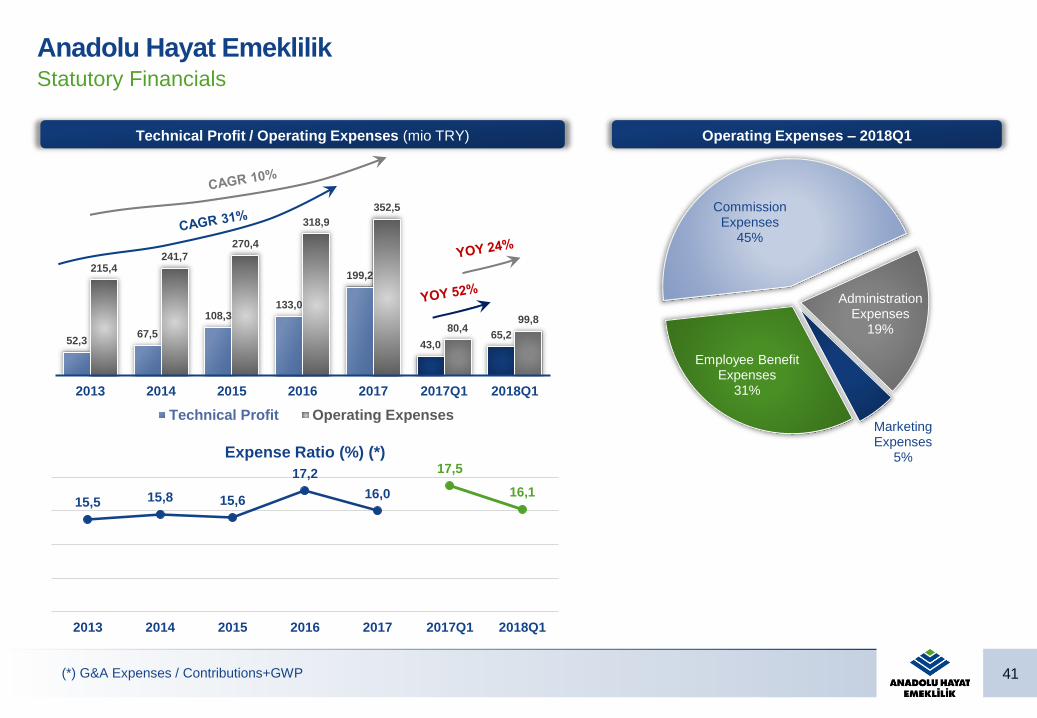

Anadolu Hayat EmeklilikStatutory Financials

52,367,5

108,3133,0

199,2

43,065,2

215,4241,7

270,4

318,9

352,5

80,499,8

0,00

50,00

100,00

150,00

200,00

250,00

300,00

350,00

400,00

2013 2014 2015 2016 2017 2017Q1 2018Q1

Technical Profit Operating Expenses

Technical Profit / Operating Expenses (mio TRY)

MarketingExpenses

5%

Employee BenefitExpenses

31%

Commission Expenses

45%

Administration Expenses

19%

Operating Expenses – 2018Q1

15,5 15,8 15,6

17,2

16,0

17,5

16,1

2013 2014 2015 2016 2017 2017Q1 2018Q1

Expense Ratio (%) (*)

(*) G&A Expenses / Contributions+GWP

42

Anadolu Hayat EmeklilikStatutory Financials

Summary of Income Statement

*Four period (2014-2017) of Pension Technical Profit is used in the calculation of CAGR because of the technical loss in 2013.

(mio TRY) 2013 2014 2015 2016 2017 CAGR 2017Q1 20178Q1 YOY

Non-Life Technical Profit / Loss 0.02 -0.03 -0.24 -0.57 -0.54 - 0.01 -0.24 -

Life Technical Profit / Loss 63.41 63.80 86.48 112.49 132.61 20% 31.16 40.79 31%

Pension Technical Profit / Loss -11.14 3.69 22.02 21.09 67.12 163%* 11.83 24.66 108%

General Technical Profit / Loss 52.29 67.46 108.26 133.01 199.19 40% 43.00 65.21 52%

Net Investment Income 48.39 69.61 72.07 101.88 98.20 19% 25.79 32.70 27%

Other Income/Expenses -2.20 -2.30 -4.48 -5.09 -17.58 68% -5.43 -5.23 -4%

Profit Before Taxes 98.48 134.77 175.85 229.80 279.81 30% 63.36 92.67 46%

43

Anadolu Hayat EmeklilikStatutory Financials

Pension Technical Profit

*Four period (2014-2017) of Pension Technical Profit is used in the calculation of CAGR because of the technical loss in 2013.

(mio TRY) 2013 2014 2015 2016 2017 CAGR 2017Q1 2018Q1 YOY

Pension Technical Income 132.00 166.57 209.06 236.76 300.55 23% 65.55 87.34 33%

1- Fund Management Income 90.76 113.57 144.26 173.82 216.74 24% 49.20 61.60 25%

2- Management Fee 17.77 21.58 26.38 21.20 32.96 17% 6.03 11.17 85%

3- Entrance Fee Income 20.24 26.13 32.05 37.08 42.60 20% 9.16 11.81 29%

4- Other Technical Income 3.23 5.29 6.37 4.66 8.25 26% 1.16 2.76 138%

Pension Technical Expense -143.14 -162.88 -187.04 -215.67 -233.43 13% -53.72 -62.68 17%

1- Total Fund Expenses -16.30 -16.99 -22.34 -24.57 -31.08 18% -7.32 -7.26 -1%

2- Operating Expenses -125.96 -144.11 -157.26 -181.71 -187.91 11% -43.24 -51.03 18%

3- Other Technical Expenses -0.88 -1.78 -7.44 -9.39 -14.44 101% -3.16 -4.39 39%

Pension Technical Profit -11.14 3.69 22.02 21.09 67.12 163%* 11.83 24.66 108%

44

Anadolu Hayat EmeklilikStatutory Financials

Life Technical Profit

Technical Margin

(Technical Profit / Earned Premiums)16.6% 18.1% 22.1% 23.7% 24.4%

*Technical results of four year (2013-2016) are taken into consideration in this calculation, since the result of 2017 is negative.

(mio TRY) 2013 2014 2015 2016 2017 CAGR 2017Q1 2018Q1 YOY

Life Technical Income 598.51 550.43 602.51 700.85 741.97 6% 190.27 218.17 15%

1- Earned Premiums (Net of Reinsurer Share) 382.88 353.32 391.78 475.43 544.07 9% 132.13 152.47 15%

2- Investment Income 206.89 188.62 202.87 214.83 190.80 -2% 55.90 62.80 12%

3- Other Technical Income 8.74 8.49 7.86 10.59 7.10 -5% 2.24 2.90 29%

Life Technical Expense -535.10 -486.63 -516.03 -588.36 -609.36 3% -159.11 -177.38 11%

1- Incurred Losses (Net of Reinsurer Share) -527.63 -542.81 -426.60 -448.86 -403.40 -6% -114.97 -103.20 -10%

2- Change in Provision for Bonus and Discounts 0.13 -0.03 -0.15 -0.14 0,16 - 0.00 -0.02 -

3- Change in Life Mathematical Provisions 83.43 155.52 26.54 2.27 -36.53 -59%* -5.70 -24.17 -

4- Change in Other Technical Provisions -2.00 -2.19 -3.11 -4.96 -5,81 31% -1.44 -1.43 -

5- Operating Expenses -89.03 -97.12 -112.71 -136.67 -163.78 16% -37.00 -48.56 31%

Life Technical Profit 63.41 63.80 86.48 112.49 132.61 20% 31.16 40.79 31%

23.6% 26.8%

45

DISCLAIMER

The information in this document has been obtained by Anadolu Hayat Emeklilik A.Ş. from sources believed to

be reliable, however, Anadolu Hayat Emeklilik A.Ş. cannot guarantee the accuracy, completeness or

correctness of such information. This document has been issued for information purposes only. The financial

reports and statements announced by Anadolu Hayat Emeklilik A.Ş. to the public and relevant corporations are

accepted to be the sole material. Anadolu Hayat Emeklilik A.Ş. does not accept any liability whatsoever for any

direct or consequential loss arising from any use of this document or its contents due to the misleading

information in this document. All estimations contained in this document are opinions of Anadolu Hayat

Emeklilik A.Ş. and can be subject to change without notice. This document cannot be interpreted as an advice

to the investors and Anadolu Hayat Emeklilik A.Ş. cannot be held responsible for the results of investment

decisions made on account of this document. This document has been issued specially to the person, whom

the document is concerned and may not be reproduced, distributed or shared with third parties for any purpose.

www.anadoluhayat.com.tr