Embed Size (px)

Citation preview

PPFAS Asset Management Private Limited[Investment Manager to PPFAS Mutual Fund]

Investor Education InitiativeFrom PPFAS Mutual FundSponsor: Parag Parikh Financial Advisory Services Private Limited

Scan this code to visit our website.

www.amc.ppfas.com

‘’You have to do very few things

right in your life so long as you don’t

do too many things wrong.”

Inside...

The magic of compounding

Nominal vs Real Return

True investors are the real winners in the long term

Owning a business vs owning Shares in a business

Financial Planning and Asset Allocation

Skin in the game

Which is the ‘best’ time to enter the market?

Systematic Investment Plans

4

5

6

8

11

13

17

19

Investor Protection = Regulation plus Education. 5

Booklet Date : October 24, 2020

Albert Einstein the renowned scientist had said...

Compound interest is the eighth wonder of the world.He who understands it earns it and.....

he who does not, pays it.

Luckily for us, we do not need the intelligence of Albert Einstein to understand the power of compound interest! This simple concept is taught in high school.

Here is an example : Ÿ Imagine you invest ̀ 10,000 for 10 years. The rate of interest is 10% per yearŸ At the end of Year 1, you will earn ̀ 1,000/-. Thus your invested amount will grow to ̀ 11,000/-Ÿ At the end of Year 2, you will earn ̀ 1,100/-... and so on. Ÿ Finally, at the end of year 10, you will earn ̀ 2,358/- for that year, while the initial sum of ̀ 10,000 will

grow to around ̀ 25,940.

Basically it means that when you invest for long periods of time, you start earning interest on interest. On the other hand, if you were earning , you would have only earned a flat sum of ̀ 1,000/- per year for 10 years and the total amount would have only grown to ̀ 20,000/-.

The difference of ̀ 5,940/- is because you have earned interest on interest.

In a nutshell,

Amazing, isn’t it?

simple interest

compound interest is the magic of earning interest on interest.

Here is an example of how compound interest can convert small savings into large numbers :

Just imagine this: You are a young 20 year old 'branded' coffee lover.

Now, assume one day you opted to drink the neighbourhood Udipi restaurant coffee, costing ̀ 25/- over the fancy one, costing ̀ 125/-

Further, you invested this difference of ` 100 at 15% per year for the next 40 years. Can you estimate how much this ̀ 100/- would grow to?

The answer is : ̀ 26,786!!

Now imagine you saved and invested ` 100/- everyday. Do you still desire that fancy coffee?

There is a simple and sure formula to get rich. Save & invest early and let the magic of compounding do the rest.

4

Stock prices are influenced by innumerable factors, many of whom are unrelated to a company's earnings. Often, these movements are random and difficult to forecast. However, over time, this apparent randomness slowly fades away, and we can observe a sustained uptick in stock prices in line with the underlying companies’ performance. That is why long-term investors emerge as true winners, beating, both day-traders and the ever-present danger of inflation. The graph below shows that if you had invested in stocks (as measured by the BSE Sensex) onJanuary 1, 1990 and stayed invested till , 2020, you would have earned compounded annual returns of 13.56% p.a., which means Rs. 10,000 invested on January 1, 1990, would have compounded to Rs. 4,96,099 on August 31, 2020. The returns drop drastically if you missed the 10, 20, 30 and 40 best days.

A prudent investor is one who always remains invested for the long term and allows his money to compound.

But how long is long-term ? While there is no concrete definition, we define it as a minimum period of five years.

Equities can help you fulfil your long-term financial aspirations, provided you are willing to stay the course and not sell in panic during market downturns. You could also choose to invest in equities through equity mutual fund schemes via the Systematic Investment Plan (SIP) route. We also suggest you consult your Financial Adviser before beginning.

August 31

True investors are the real winners in the long term

Equity investors who are not terrified of short term fluctuations can benefit from the power of compounding

5

Source: Value Research

Daily Returns from January 1, 1990 to Jan 31, 2019

Retu

rns

(%)

CAGR

All days invested Missing best 10 days Missing best 20 days Missing best 30 days Missing best 40 days

0

2

4

6

8

10

12

14

16

Column F

13.56

9.43

7.17

5.604.39

(`4,96,099)

(`1,59,046)

(`83,984)

(`53,343)(`37,367)

What are Shares/Stocks ?

A share/stock of a company represents a small stake in a company's underlying business. In the past, many investors remained invested in a company for long periods aiming to participate in that company's growth across business cycles and earn dividends along the way.

However, today the distinction between investors and traders is narrowing. Holding periods have reduced to a matter of days rather than years. This has contributed to share prices becoming more volatile. Other factors include:

Owning a business vs owning Shares in a business

- Warren Buffett

However, for long-term investors willing to hold on for several years, volatility is a blessing in disguise as they can take advantage of sudden, unexplained plunges in stock prices to purchase stocks of good companies at attractive valuations.

Investors may also opt to invest through equity mutual fund schemes which invest according to the principles of . The fund managers of many such schemes view their portfolio as a collection of businesses and not just stocks.

Their portfolio will usually comprise of companies having all/a combination of the following characteristics :

• Low debt burden • Strong franchises • Relatively low earnings volatility• Run by competent managements who consider the interests of minority shareholders

value investing

6

The advent of online trading and plummeting brokerage rates.

Increased information flow, which facilitates quick decisions.

Growing importance of the

financial media.

Increased information flow, which facilitates quick decisions.

Also, such schemes will have very low portfolio turnover ratios, as the fund manager will prefer to hold on to the underlying companies as long as the business fundamentals are intact.

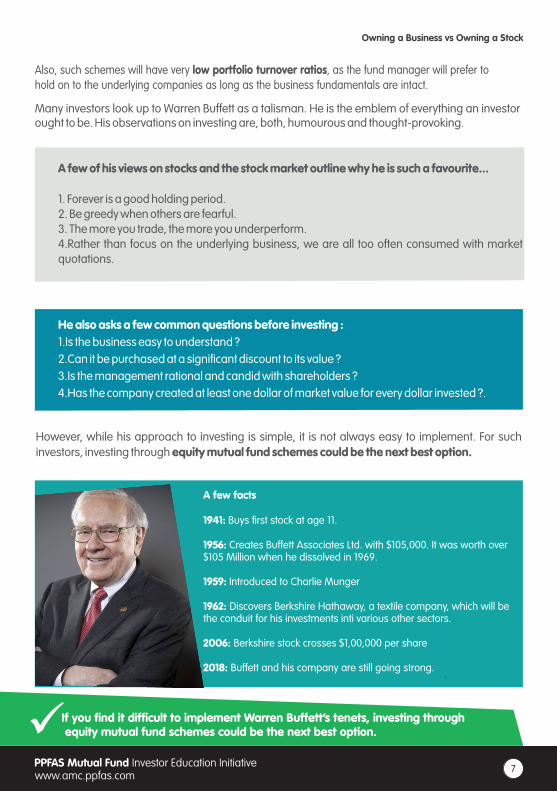

Many investors look up to Warren Buffett as a talisman. He is the emblem of everything an investor ought to be. His observations on investing are, both, humourous and thought-provoking.

A few of his views on stocks and the stock market outline why he is such a favourite...

1. Forever is a good holding period.2. Be greedy when others are fearful.3. The more you trade, the more you underperform.4.Rather than focus on the underlying business, we are all too often consumed with market quotations.

He also asks a few common questions before investing : 1.Is the business easy to understand ?2.Can it be purchased at a significant discount to its value ? 3.Is the management rational and candid with shareholders ?4.Has the company created at least one dollar of market value for every dollar invested ?.

However, while his approach to investing is simple, it is not always easy to implement. investors, investing through equity mutual fund schemes could be the next best option.

For such

If you find it difficult to implement Warren Buffett’s tenets,

investing through equity mutual fund schemes could be the next best option.

A few facts

1941: Buys first stock at age 11.

1956: Creates Buffett Associates Ltd. with $105,000. It was worth over$105 Million when he dissolved in 1969.

1959: Introduced to Charlie Munger

1962: Discovers Berkshire Hathaway, a textile company, which will bethe conduit for his investments inti various other sectors.

2006: Berkshire stock crosses $1,00,000 per share

2018: Buffett and his company are still going strong.

7

Why should we prepare a Financial Plan ? 1. It helps us to know where we stand currently 2. It helps us to determine our goal 3. It provides options on how to reach there. 4. It helps us know what is possible and what is not.

Why don't we plan ? 1. We get overwhelmed by the process 2. We fear that things will not go according to plan 3. Procrastination

The chief constituents of a Financial Plan are : 1. Cash Flow Management 2. Insurance 3. Asset Allocation 4. Estate Planning

8

Financial Planing

Goal Sett

ing

Data

Gath

eri

ng

Pla

n P

repara

tion

Pla

n Im

ple

menta

tion

Pla

n R

evi

ew

Cours

e C

orr

ect

ions

Asset Allocation involves spreading your investments across various financial asset classes such as fixed deposits, equities, real estate, gold etc.

Why this is desirable :

1. It helps to reduce risk of capital loss, as different assets usually perform differently at the same point in time.

2. It prevents us from getting unduly worried or ecstatic. 3. It helps in bringing about balance in our financial life.

How do we go about it ?

1. Arrive at the optimum allocation 2. Re-balance periodically

The share of various assets will depend :

1. Our current financial situation 2. Our financial goals 3. Certain 'soft' factors like our attitude towards certain assets.

Source: Value Research

Performance of Asset Classes since 2009

9

Debt: IncomeGoldS&P BSE Sensex Index

* as on 31 August, 20204.61

23.3417.43

7.98

-24.6410.09

12.5125.54

5.20

8.9812.89

-7.4129.89

7.04-6.08

-5.0311.84

10.101.95

4.964.66

27.914.87

8.175.87

7.6723.74

14.386.52

30.59-6.36

-4.43

31.65

2020 (YTD*)

2019

2018

2017

2016

2015

2014

2013

2012

2011

2010

Asset Allocation is only one part of the Financial Planning Process. It should be done, keeping the other aspects in mind.

Mutual funds provide a good way to undertake asset allocation. A few examples are :

All this can be undertaken at a reasonable cost, without, usually, sacrificing liquidity.

The Financial Planning and Asset Allocation process may appear to be easy, but it is not always simple. Hence, outsource this function to a competent Financial Planner, if you lack confidence or ability to do it yourself.

42.50%

46.70%

10.70%

Real EstateStocks Gold

Specimen Asset Allocation

Type of Fund Underlying Asset

Debt Fund Debt instruments issued by Corporates and Governments

Equity Fund Indian as well as foreign equities

Gold Fund Gold

Real Estate Investment Trust Commercial Real Estate

Asset Allocation is only one part of the Financial Planning Process. It should be done keeping the other aspects in mind.

10

Have you ever come across this notice in a restaurant : “The owner eats here...”

Does this not make you feel more assured, about the quality of food ?

The same could be extended to money management.

11

There are two kinds of money managers :

1. The first kind manages your money for a fixed fee, without investing along with you. In other words, he does not lose, even if you lose.

2. The second kind strongly believes in the scheme that he is managing, and hence invests his own money in it. Hence, he usually wins only if you win. This is known as having 'Skin In The Game'.

Don’t you feel more reassured while you are entrusting money to the second manager?

Having ‘Skin In The game’ results in:

1. Your fund manager behaving more prudently. 2. His financial interest being aligned with yours. 3. Him having less incentive to cut corners. 4. Him having more than merely reputation, at stake.

Before choosing a mutual fund, do not go merely by past performance statistics. Choose one where the interests of the fund house are aligned with yours...

Around 18th Century BC lived a King named Hammurabi who instituted a social law now known as the Hammurabi's Code. It is the one of the first evidence of law ever written down.

One of the principle features of the code was about the builder - If a builder built a house for a man & the house collapses to cause the death of the owner, then the builder has to be put to death.

In a mutual fund's context, a Fund Manager is said to have 'Skin In The Game' if he / she owns units in the Scheme he / she is managing.

The greater the holding, the greater the implicit commitment of the Manager. It demonstrates a willingness to link their financial well-being with the unitholders' well-being.

It also places an onus on them to make optimum use of their time & abilities in order to enhance the scheme's performance and avoid reckless behaviour.

Money management acquires a different dimension when one has ‘Skin In The Game'.

12

The Hammurabi Code

A good question...Unfortunately, there is no 'one' right answer.

One thumb rule which often works is :‘'The best time to buy is when stock prices are falling sharply and you least feel like buying'.

Most often, we ask this question because we are terrified of the unknown. What if I purchase today and...

oil prices or interest rates start rising?Europe slips back into recession? There is a war, etc...

Here is one statistic that may reassure you...The BSE Sensex was 100 on April 1, 1979. It is around 26,000 currently. This amounts to an annualised return of nearly 17% p.a.

During this period, most of what could possibly go wrong, did go wrong, both on the local and global front. Yet, those who invested at that time and held on, have multiplied their wealth by over 260 times. They have also comprehensively beaten inflation. Those who tried to time the market were often left frustrated...and poorer.

For those who worry about losses due to stock market fluctuations, here are two charts. From these it is evident that the longer you stay invested, the lower the chance of losses and even if you had invested on days when the Sensex was at its highest value, you would not have lost money, had you held on.

Source: Value Research

13

Monthly SIPs made on the best day of the BSE Sensex 30

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

0

50,00,000

1,00,00,000

1,50,00,000

2,00,00,000

2,50,00,000

3,00,00,000 Monthly SIPs made on the worst day of the BSE Sensex 30 `2,84,45,543

`2,62,69,793

Worth of `10,000 monthly SIP

Also, often, the risk of not being in the market is higher than the risk of being in it.

Sensex Returns

Source: Value Research

Source: Value Research

14

1 yr 3 yr 5 yr 7 yr 10 yr 12 yr 15 yr

30 28 26 24 21 19 16

8 4 3 1 NIL NIL NIL

26.67 14.29 11.54 4.17 NIL NIL NIL

17.39 9.28 10.32 11.14 13.31 11.33 13.39

18.72 14.26 12.58 11.97 12.13 12.11 13.18

82.09 49.76 43.13 26.46 20.45 19.10 16.66

-52.45 -12.29 -1.80 -2.61 2.59 6.09 7.31

32.35 16.55 11.73 7.55 5.31 3.55 2.29

Summary since January 1990

Loss Probability (%)

Minimum Return (%)

Missing 10 days

49,60,995

15,90,462

20,54,65023,55,882

29,65,135

36,02,219

Missing 8 days Missing 6 days Missing 4 days Missing 2 days All days invested0

10,00,000

20,00,000

30,00,000

40,00,000

50,00,000

60,00,000

Source: Value Research

15

BSE Sensex

S&P BSE Sensex Index (1991 to 2019)

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

1990

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2012

2013

2014

2015

2016

2017

2018

2019

2020

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Ketan Parekh scamdivulged & techboom goes bust

y

Prices at LME crashed,Fed increased interestrates

Exuberant bull phase withplenty of NFOs, IPOs

U.S. sub-prime crisis emergLehman Bros.

Recovery withglitches

Coming of the NDA government

The big bull-HarshadMehta scam divulg

Tech boom

Blackmonda

Coming of the

NDA government

Recovery with

glitchesverhangDebt o

in Euro zone

dot.com crash(2000)

Financial crisis(2008)

The bottomline :

There is enough evidence to prove that equities have beaten other asset classes over the long term. If you find it difficult to invest in stock markets on your own, opt for a mutual fund and invest through the Systematic Investment Plan (SIP) route.

16

Long term performance of asset classes(Current value of `100 invested in FY 1990-91)

Nifty 50 Index Gold (1 gram) PPF

Source: Value Research

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

0

1,000

2,000

3,000

4,000

S&P BSE Sensex

Gold

PPF

Nominal vs Real Return...

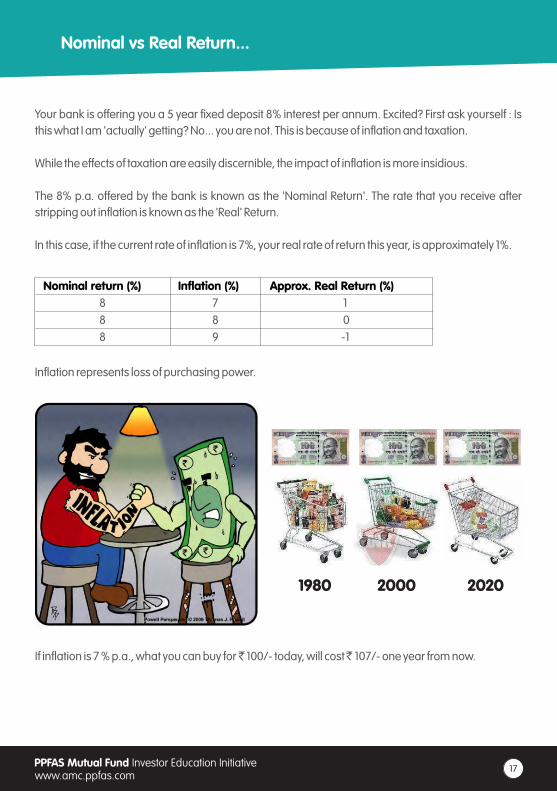

Your bank is offering you a 5 year fixed deposit 8% interest per annum. Excited? First ask yourself : Is this what I am 'actually' getting? No... you are not. This is because of inflation and taxation.

While the effects of taxation are easily discernible, the impact of inflation is more insidious.

The 8% p.a. offered by the bank is known as the 'Nominal Return'. The rate that you receive after stripping out inflation is known as the 'Real' Return.

In this case, if the current rate of inflation is 7%, your real rate of return this year, is approximately 1%.

Nominal return (%) Inflation (%) Approx. Real Return (%)8 7 18 8 08 9 -1

Inflation represents loss of purchasing power.

If inflation is 7 % p.a., what you can buy for ̀ 100/- today, will cost ̀ 107/- one year from now.

17

1980 2000 2020

Investment options offering you minuscule or negative real returns, mean that your investments are actually making you poorer. In fact, the longer you remain invested, the poorer you may become. Time is the enemy of fixed income investors. Historically, investment in equities has offered higher real returns compared to fixed deposits. Hence, it seen as a good hedge against inflation.

Nominal vs Real Return...

When we invest in equities we are purchasing a small portion of the underlying business. As consumers, we often complain that companies are constantly raising the prices of products and services. By investing in those very businesses, we can benefit along with these companies.

If you find it difficult to choose the right companies for investing, you could opt to invest through mutual fund schemes, preferably through the Systematic Investment Plan (SIP) route.

Sensex Fixed DepositGold Cost Inflation Index

Sensex Vs Gold Vs FD Vs Cost Inflation Index

Do not get swayed by nominal returns. It is the 'real' return that counts...

Value of Rs. 100/- invested on 1st Apr 1980. ( )adjusted for inflation

18

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

0

5000

10000

15000

20000

25000

30000

35000

40000

45000

Systematic Investment Plans

What is a SIP?You could view it as a recurring deposit in a mutual fund scheme wherein you invest a fixed amount periodically on any particular day (say, on the 10th of every month). This process could be automated either by investing online or by issuing standing instructions to your bank, just as you would in the case of your electricity / telephone bill. Yes... It really is this simple.

Why should you register a SIP? ...

SIP: It is like an EMI you pay to yourself.

19

You do not have to worry about the 'right time'.The longer you invest through a SIP, the more you will be convinced that the benefit of just remaining invested is more than eternally searching for that one right moment to invest.

SIP = DIP By removing the emotional element from the investment process, the SIP doubles up as a Disciplined Investing Plan. You could also call this the Auto-Pilot mode of investing.

The power of compounding You could begin with amounts as low as ` 1000/- per month. The power of compounding will ensure that small contributions can grow into large sums over time.

Befriend volatility Yes... equities are volatile. However, the auto-debit feature of your SIP means that you will keep investing during fearful times. Over time, you will be happy that you were bold when the others were scared. Continuously investing over a long period, helps you to actually take advantage of market fluctuations.

PPFAS Asset Management Private Limited81/82, 8th Floor, Sakhar Bhavan, Ramnath Goenka Marg, 230, Nariman Point,

Mumbai - 400 021. INDIA.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

www.amc.ppfas.com

Visit our Knowledge Centre at www.amc.ppfas.com.

SystematicTransfer Plans

Parag’s Views

Tortoise Speaks (Blog)

AMFI Booklet

Liquid Fund

Calendars

Mutual FundsSahi Hai

Short TakesSEBI Videos

Mutual Fund 101+

Investor Lessons

Call: 91 22 61406538 / 8291979349 / 8291979350, Email: [email protected]