Embed Size (px)

Citation preview

Investments, 8th edition

Bodie, Kane and Marcus

Slides by Susan Hine

McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 1 The Investment

Environment

1-2

Real Assets Versus Financial Assets

• Essential nature of investment

– Reduced current consumption

– Planned later consumption

• Real Assets

– Assets used to produce goods and

services

• Financial Assets

– Claims on real assets

1-3

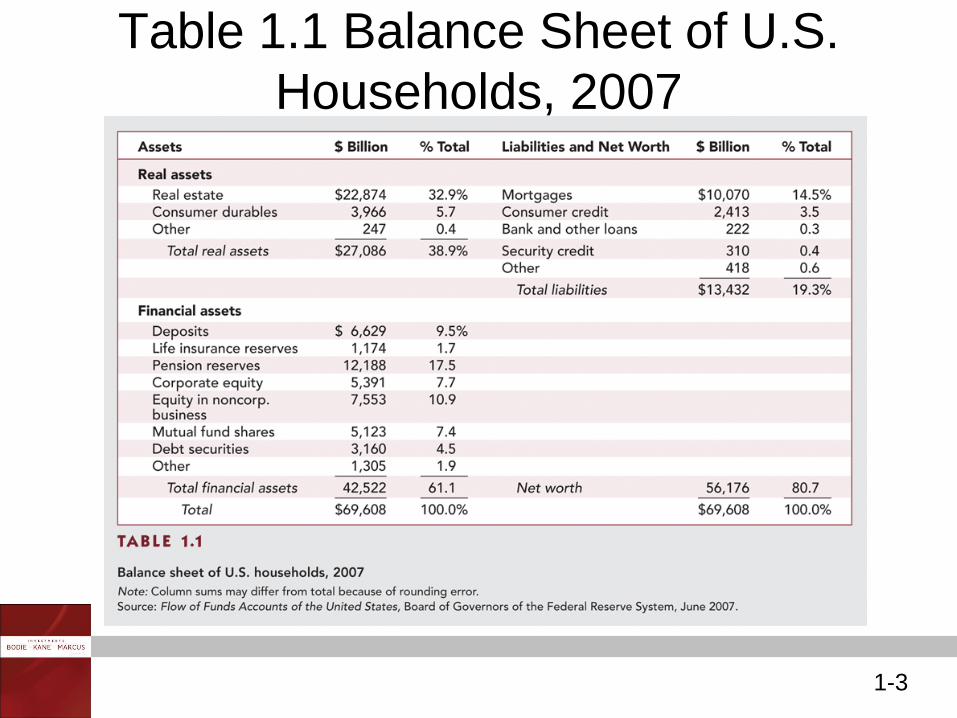

Table 1.1 Balance Sheet of U.S.

Households, 2007

1-4

Table 1.2 Domestic Net Worth

1-5

A Taxonomy of Financial Assets

• Fixed income or debt

– Money market instruments

• Bank certificates of deposit

– Capital market instruments

• Bonds

• Common stock or equity

• Derivative securities

1-6

Financial Markets and the Economy

• Information Role

– The Google effect

• Consumption Timing

• Allocation of Risk

• Separation of Ownership and

Management

– Agency Issues

1-7

Financial Markets and the

Economy Continued

• Corporate Governance and Corporate Ethics

– Accounting Scandals

• Examples – Enron, Rite Aid, HealthSouth

– Auditors—watchdogs of the firms

– Analyst Scandals

• Arthur Andersen

– Sarbanes-Oxley Act

• Tighten the rules of corporate governance

1-8

The Investment Process

• Asset allocation

– Choice among broad asset classes

• Security selection

– Choice of which securities to hold within

asset class

• Security analysis

1-9

Markets are Competitive

• Risk-Return Trade-Off

• Efficient Markets

– Active Management

• Finding mispriced securities

• Timing the market

– Passive Management

• No attempt to find undervalued

securities

• No attempt to time the market

• Holding a highly diversified portfolio

1-10

The Players

• Business Firms– net borrowers

• Households – net savers

• Governments – can be both borrowers and

savers

• Financial Intermediaries

– Investment Companies

– Banks

– Insurance companies

– Credit unions

1-11

The Players Continued

• Investment Bankers

– Perform specialized services for

businesses

– Markets in the primary market

1-12

Table 1.3 Balance Sheet of

Commercial Banks, 2007

1-13

Table 1.4 Balance Sheet of Nonfinancial

U.S. Business, 2007

1-14

Recent Trends—Globalization

• American Depository Receipts (ADRs)

• Foreign securities offered in dollars

• Mutual funds that invest internationally

• Instruments and vehicles continue to

develop (WEBs)

• Exchange Traded Funds (ETFs)

1-15

Figure 1.1 Globalization: A Debt Issue

Denominated in Euros

1-16

Recent Trends—Securitization

• Mortgage pass-through securities

• Other pass-through arrangements

– Car, student, home equity, credit card

loans

• Offers opportunities for investors and

originators

1-17

Figure 1.2 Asset-backed Securities

Outstanding

1-18

Recent Trends—Financial Engineering

• Use of mathematical models and computer-

based trading technology to synthesize new

financial products

• Bundling and unbundling of cash flows

1-19

Figure 1.3 Building Creates a Complex

Security

1-20

Figure 1.4 Unbundling of Mortgages into

Principal- and Interest-Only Securities

1-21

Recent Trends—Computer Networks

• Online information dissemination

• Information is made cheaply and widely

available to the public

• Automated trade crossing

– Direct trading among investors

Investments, 8th edition

Bodie, Kane and Marcus

Slides by Susan Hine

McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 2 Asset Classes and Financial Instruments

1-23

Major Classes of Financial Assets or

Securities

• Money market

• Bond market

• Equity Securities

• Indexes

• Derivative markets

1-24

The Money Market

• Treasury bills

– Bid and asked price

– Bank discount method

• Certificates of Deposits

• Commercial Paper

• Bankers Acceptances

1-25

The Money Market Continued

• Eurodollars

• Repurchase Agreements (RPs) and Reverse

RPs

• Brokers’ Calls

• Federal Funds

• LIBOR Market

1-26

Figure 2.1 Rates on Money Market Securities

1-27

Table 2.1 Major Components of the

Money Market

1-28

Figure 2.2 Treasury Bill Yields

1-29

Figure 2.3 The Spread between 3-month

CD and Treasury Bill Rates

1-30

The Bond Market

• Treasury Notes and Bonds

• Inflation-Protected Treasury Bonds

• Federal Agency Debt

• International Bonds

• Municipal Bonds

• Corporate Bonds

• Mortgages and Mortgage-Backed Securities

1-31

Treasury Notes and Bonds

• Maturities

– Notes – maturities up to 10 years

– Bonds – maturities in excess of 10 years

– 30-year bond

• Par Value - $1,000

• Quotes – percentage of par

1-32

Figure 2.4 Lisiting of Treasury Issues

1-33

Federal Agency Debt

• Major issuers

– Federal Home Loan Bank

– Federal National Mortgage Association

– Government National Mortgage

Association

– Federal Home Loan Mortgage Corporation

1-34

Municipal Bonds

• Issued by state and local governments

• Types

– General obligation bonds

– Revenue bonds

• Industrial revenue bonds

• Maturities – range up to 30 years

1-35

Figure 2.5 Tax-exempt Debt Outstanding

1-36

Municipal Bond Yields

• Interest income on municipal bonds is not

subject to federal and sometimes not to state

and local tax

• To compare yields on taxable securities a

Taxable Equivalent Yield is constructed

1-37

Table 2.2 Equivalent Taxable Yields

Corresponding to Various Tax-Exempt

Yields

1-38

Figure 2.6 Ratio of Yields on Tax-Exempt to Taxable Bonds

1-39

Corporate Bonds

• Issued by private firms

• Semi-annual interest payments

• Subject to larger default risk than government

securities

• Options in corporate bonds

– Callable

– Convertible

1-40

• Developed in the 1970s to help liquidity of

financial institutions

• Proportional ownership of a pool or a

specified obligation secured by a pool

• Market has experienced very high rates of

growth

Mortgages and Mortgage-Backed

Securities

1-41

Figure 2.7 Mortgage-backed Securities

Outstanding, 1979-2007

1-42

Equity Securities

• Common stock

– Residual claim

– Limited liability

• Preferred stock

– Fixed dividends -limited

– Priority over common

– Tax treatment

• Depository receipts

1-43

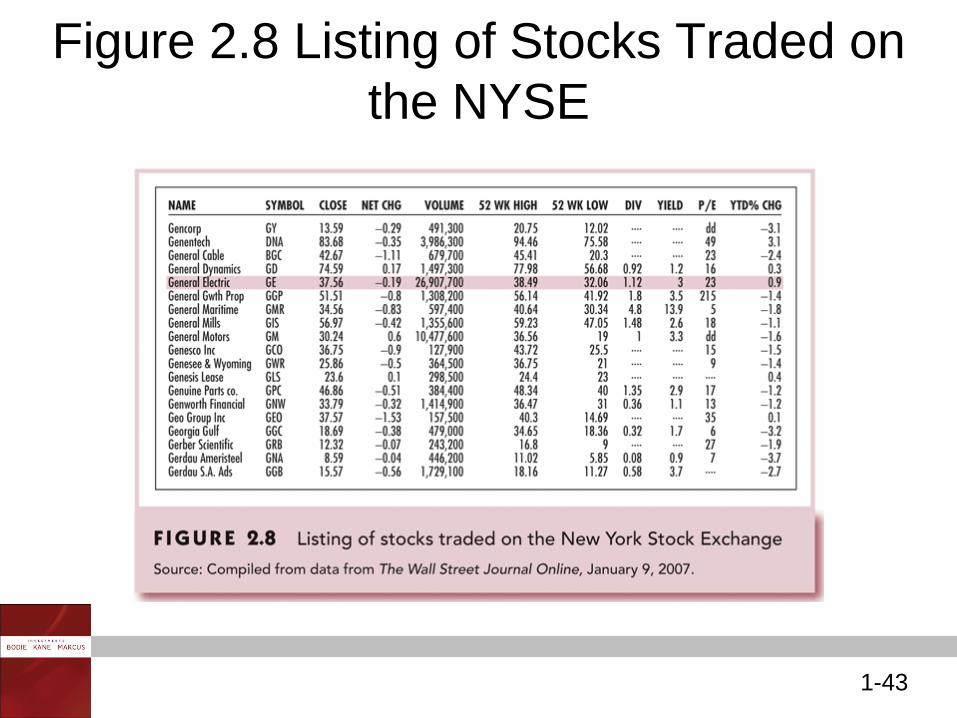

Figure 2.8 Listing of Stocks Traded on

the NYSE

1-44

• There are several broadly based indexes

computed and published daily

• There are several indexes of bond market

performance

• Others include:

– Nikkei Average

– Financial Times Index

Stock Market Indexes

1-45

Dow Jones Industrial Average

• Includes 30 large blue-chip corporations

• Computed since 1896

• Price-weighted average

1-46

Example 2.2 Price-Weighted Average

Portfolio: Initial value $25 + $100 = $125

Final value $30 + $ 90 = $120

Percentage change in portfolio value

= 5/125 = -.04 = -4%

Index: Initial index value (25+100)/2 = 62.5

Final index value (30 + 90)/2 = 60

Percentage change in index -2.5/62.5

= -.04 = -4%

1-47

• Broadly based index of 500 firms

• Market-value-weighted index

• Index funds

• Exchange Traded Funds (ETFs)

Standard & Poor’s Indexes

1-48

Other U.S. Market-Value Indexes

• NASDAQ Composite

• NYSE Composite

• Wilshire 5000

1-49

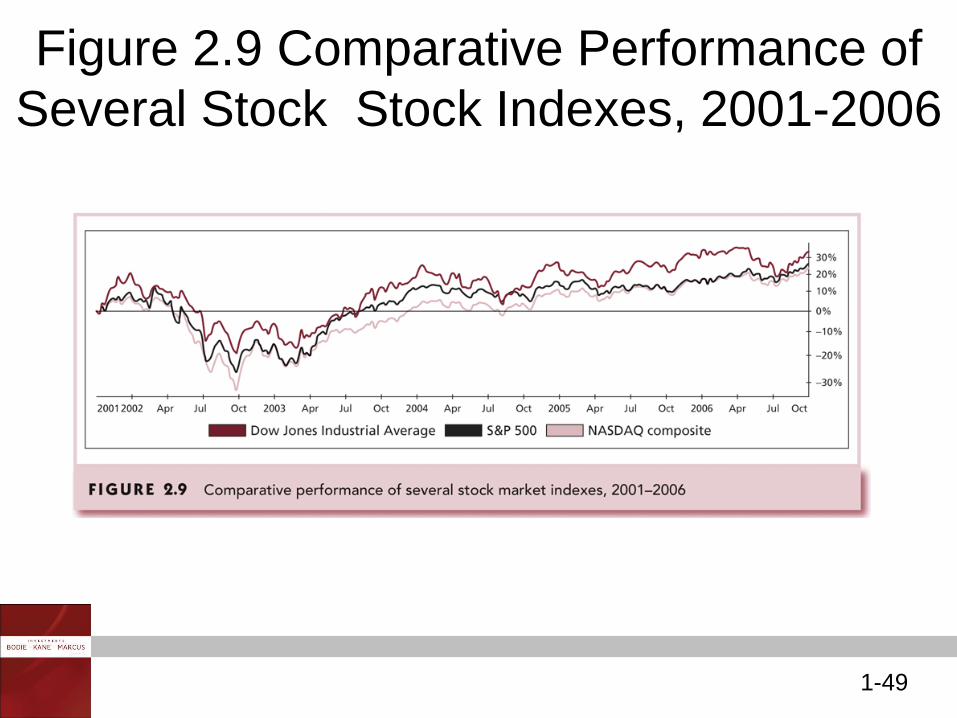

Figure 2.9 Comparative Performance of

Several Stock Stock Indexes, 2001-2006

1-50

Foreign and International

Stock Market Indexes

• Nikkei (Japan)

• FTSE (Financial Times of London)

• Dax (Germany)

• MSCI (Morgan Stanley Capital International)

• Hang Seng (Hong Kong)

• TSX (Canada)

1-51

Derivatives Markets

Options

• Basic Positions

– Call (Buy)

– Put (Sell)

• Terms

– Exercise Price

– Expiration Date

– Assets

Futures

• Basic Positions

– Long (Buy)

– Short (Sell)

• Terms

– Delivery Date

– Assets

1-52

Figure 2.10 Trading Data on GE Options

1-53

Figure 2.11 Listing of Selected

Futures Contracts

Investments, 8th edition

Bodie, Kane and Marcus

Slides by Susan Hine

McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 3 How Securities

are Traded

1-55

How Firms Issue Securities

• Primary

– New issue

– Key factor: issuer receives the proceeds

from the sale

• Secondary

– Existing owner sells to another party

– Issuing firm doesn’t receive proceeds

and is not directly involved

1-56

How Firms Issue Securities Continued

• Investment Banking

• Shelf Registration

• Private Placements

• Initial Public Offerings (IPOs)

1-57

Investment Banking

• Underwritten: firm commitment on proceeds

to the issuing firm

• Red herring

• Prospectus

1-58

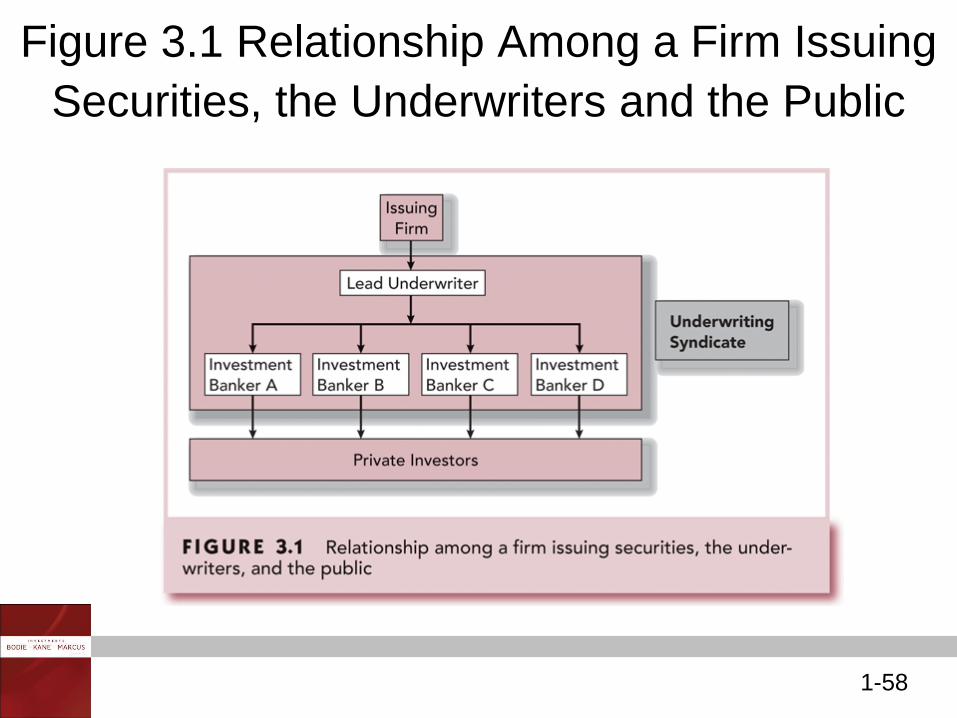

Figure 3.1 Relationship Among a Firm Issuing

Securities, the Underwriters and the Public

1-59

Shelf Registrations

• SEC Rule 415

• Introduced in 1982

• Ready to be issued – on the shelf

1-60

• Sale to a limited number of sophisticated

investors not requiring the protection of

registration

• Allowed under Rule 144A

• Dominated by institutions

• Very active market for debt securities

• Not active for stock offerings

Private Placements

1-61

Initial Public Offerings

• Process

– Road shows

– Bookbuilding

• Underpricing

– Post sale returns

– Cost to the issuing firm

1-62

Figure 3.2 Average Initial Returns for

IPOs in Various Countries

1-63

Figure 3.3 Long-term Relative

Performance of Initial Public Offerings

1-64

How Securities are Traded

• Types of Markets

– Direct search

• Least organized

– Brokered

• Trading in a good is active

– Dealer

• Trading in a particular type of asset increases

– Auction

• Most integrated

1-65

Types of Orders

• Market—executed immediately

– Bid Price

– Ask Price

• Price-contingent

– Investors specify prices

– Stop orders

1-66

Figure 3.4 The Limit Order Book for Intel on the Archipelago Market,

January 19, 2007

1-67

Figure 3.5 Price-Contingent Orders

1-68

Trading Mechanisms

• Dealer markets

• Electronic communication networks (ECNs)

• Specialists markets

1-69

U.S. Security Markets

• Nasdaq and NYSE have evolved in response

to new information technology

• Both have increased their commitment to

automated electronic trading

1-70

Nasdaq

• National Market System

• Nasdaq Small Cap Market

• Levels of subscribers

– Level 1 – inside quotes

– Level 2 – receives all quotes but they can’t

enter quotes

– Level 3 – dealers making markets

1-71

Table 3.1 Partial Requirements for Listing

on NASDAQ Markets

1-72

New York Stock Exchange

• Member functions

– Commission brokers

– Floor brokers

– Specialists

• Block houses

• SuperDot

1-73

Table 3.2 Some Initial Listing

Requirements for the NYSE

1-74

Table 3.3 Block Transactions on the

New York Stock Exchange

1-75

Other Systems

• Electronic Communication Networks

– Private computer networks that directly link

buyers with sellers

• National Market System

– Securities Act of Amendments of 1975

• Bond Trading

– Automated Bond System (ABS)

1-76

Market Structure in Other Countries

• London - predominately electronic trading

• Euronext – market formed by combination of

the Paris, Amsterdam and Brussels

exchanges

• Tokyo Stock Exchange

• Globalization and consolidation of stock

markets

1-77

Figure 3.6 Market Capitalization of Major

World Stock Exchanges, 2007

1-78

Trading Costs

• Commission: fee paid to broker for making

the transaction

• Spread: cost of trading with dealer

– Bid: price dealer will buy from you

– Ask: price dealer will sell to you

– Spread: ask - bid

• Combination: on some trades both are paid

1-79

Buying on Margin

• Using only a portion of the proceeds for an

investment

• Borrow remaining component

• Margin arrangements differ for stocks and

futures

1-80

Stock Margin Trading

• Margin is currently 50%; you can borrow up to

50% of the stock value

– Set by the Fed

• Maintenance margin: minimum amount equity

in trading can be before additional funds must

be put into the account

• Margin call: notification from broker that you

must put up additional funds

1-81

Margin Trading - Initial Conditions

Example 3.1

X Corp $100

60% Initial Margin

40% Maintenance Margin

100 Shares Purchased

Initial Position

Stock $10,000 Borrowed $4,000

Equity $6,000

1-82

Margin Trading - Maintenance Margin

Example 3.1

Stock price falls to $70 per share

New Position

Stock $7,000 Borrowed $4,000

Equity $3,000

Margin% = $3,000/$7,000 = 43%

1-83

Margin Trading - Margin Call Example 3.2

How far can the stock price fall before a

margin call?

(100P - $4,000)* / 100P = 30%

P = $57.14

* 100P - Amt Borrowed = Equity

1-84

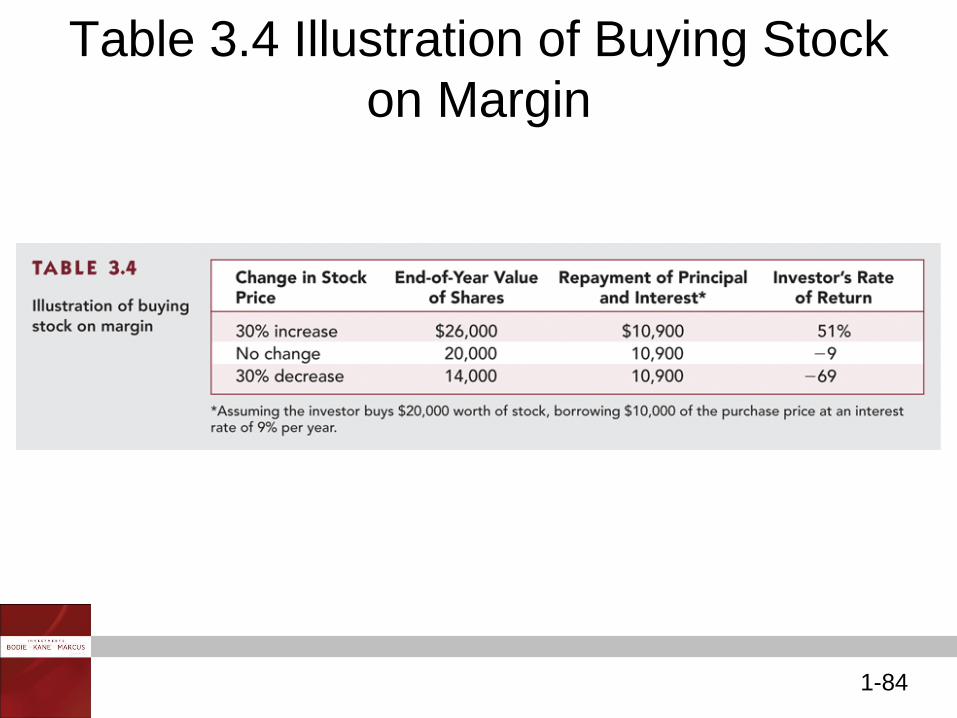

Table 3.4 Illustration of Buying Stock

on Margin

1-85

Short Sales

• Purpose: to profit from a decline in the price of a stock or security

• Mechanics

– Borrow stock through a dealer

– Sell it and deposit proceeds and margin in an account

– Closing out the position: buy the stock and return to the party from which is was borrowed

1-86

Short Sale – Initial Conditions Example 3.3

Dot Bomb 1,000 Shares

50% Initial Margin

30% Maintenance Margin

$100 Initial Price

Sale Proceeds $100,000

Margin & Equity 50,000

Stock Owed 100,000

1-87

Short Sale - Maintenance Margin

Stock Price Rises to $110

Sale Proceeds $10,000

Initial Margin 5,000

Stock Owed 11,000

Net Equity 4,000

Margin % (4000/11,000) 36%

1-88

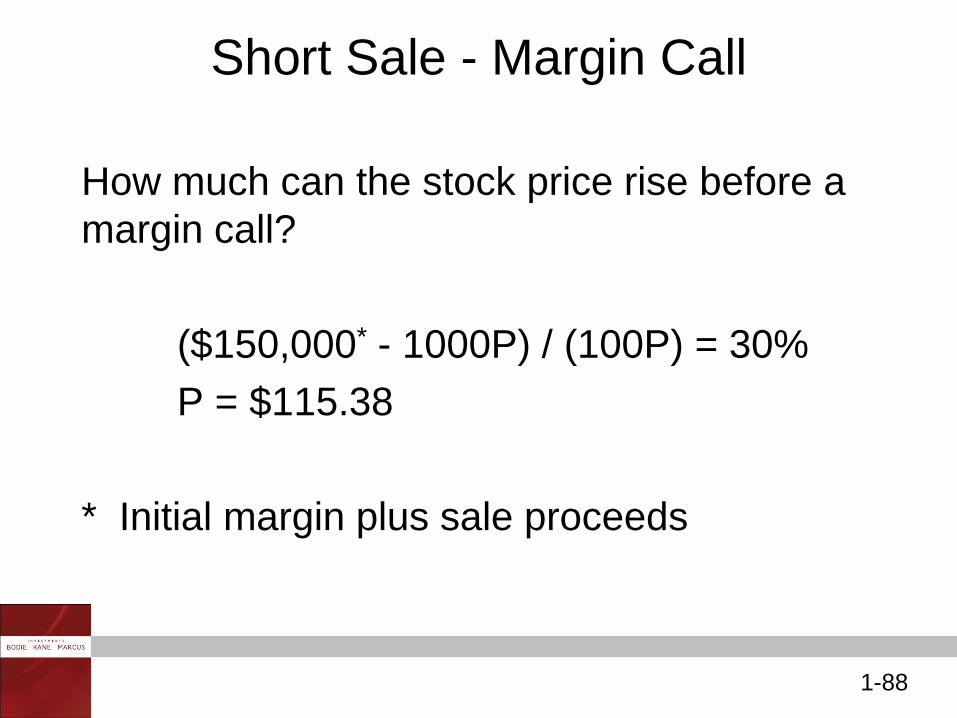

Short Sale - Margin Call

How much can the stock price rise before a

margin call?

($150,000* - 1000P) / (100P) = 30%

P = $115.38

* Initial margin plus sale proceeds

1-89

Regulation of Securities Markets

• Major regulations

– Securities Act of 1933

– Securities Act of 1934

– Securities Investor Protection Act of 1970

• Self-Regulation

– Stock markets are largely self-regulating

1-90

Regulation Securities Markets Continued

• Regulatory Responses to Recent Scandals

– Public Company Accounting Oversight

Board

– Financial experts to serve on audit

committees of boards of directors

– CEOs and CFOs personally certify firms’

financial reports

– Boards must have independent directors

– Sarbanes-Oxley Act

1-91

Circuit Breakers

• Trading halts

• Collars

1-92

Insider Trading

• Officers, directors, major stockholders must

report all transactions in firm’s stock

• Insiders do exploit their knowledge

• Leakage of useful information to some

traders

Investments, 8th edition

Bodie, Kane and Marcus

Slides by Susan Hine

McGraw-Hill/Irwin Copyright © 2009 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 4 Mutual Funds

and Other

Investment

Companies

1-94

Investment Companies

• These companies perform several

important functions for investors:

– Administration & record keeping

– Diversification & divisibility

– Professional management

– Reduced transaction costs

1-95

Net Asset Value

• Used as a basis for valuation of investment

company shares

– Selling new shares

– Redeeming existing shares

Calculation

Market Value of Assets - Liabilities

Shares Outstanding

1-96

Types of Investment Companies

• Unit Trusts

• Managed Investment Companies

– Open-End

• Open-end: shares outstanding change when new shares are sold or old shares are redeemed

• Priced at Net Asset Value(NAV)

– Closed-End

• no change in shares outstanding unless new stock is offered

• Priced at Premium or discount to NAV

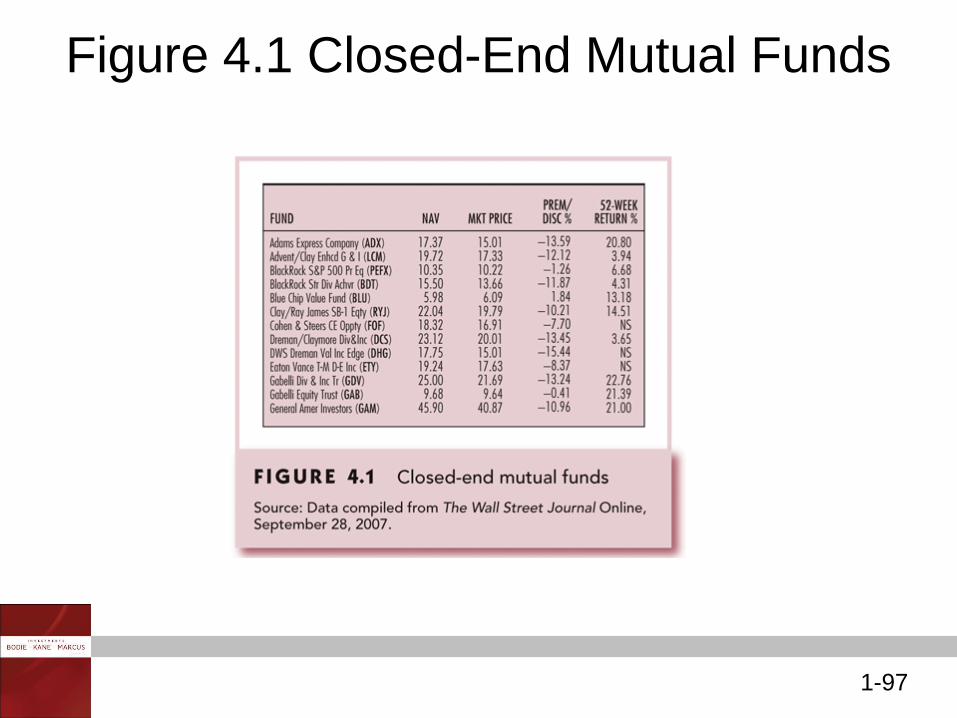

1-97

Figure 4.1 Closed-End Mutual Funds

1-98

Types of Investment

Companies Continued

• Other investment organizations

– Commingled funds

– REITs

– Hedge Funds

1-99

Mutual Funds—Investment Policies

• Money Market

• Equity

• Sector

• Bond

• Balanced

• Asset Allocation and Flexible

• Index

• International

1-100

Table 4.1 U.S. Mutual Funds by

Investment Classification

1-101

How Funds Are Sold

• Direct-marketed funds

• Sales force distributed

• Revenue sharing on sales force distributed

– Potential conflicts of interest

• Financial Supermarkets

1-102

Costs of Investing in Mutual Funds

• Fee Structure

– Operating expenses

– Front-end load

– Back-end load

– 12 b-1 charges

• distribution costs paid by the fund

• Alternative to a load

1-103

Fees and Mutual Fund Returns

1 0

0

NAV NAV Income and capital gain distributionsRate of return =

NAV

0

10

20

30

40

50

60

70

80

90

1st Qtr 2nd Qtr 3rd Qtr 4th Qtr

East

West

North

1-104

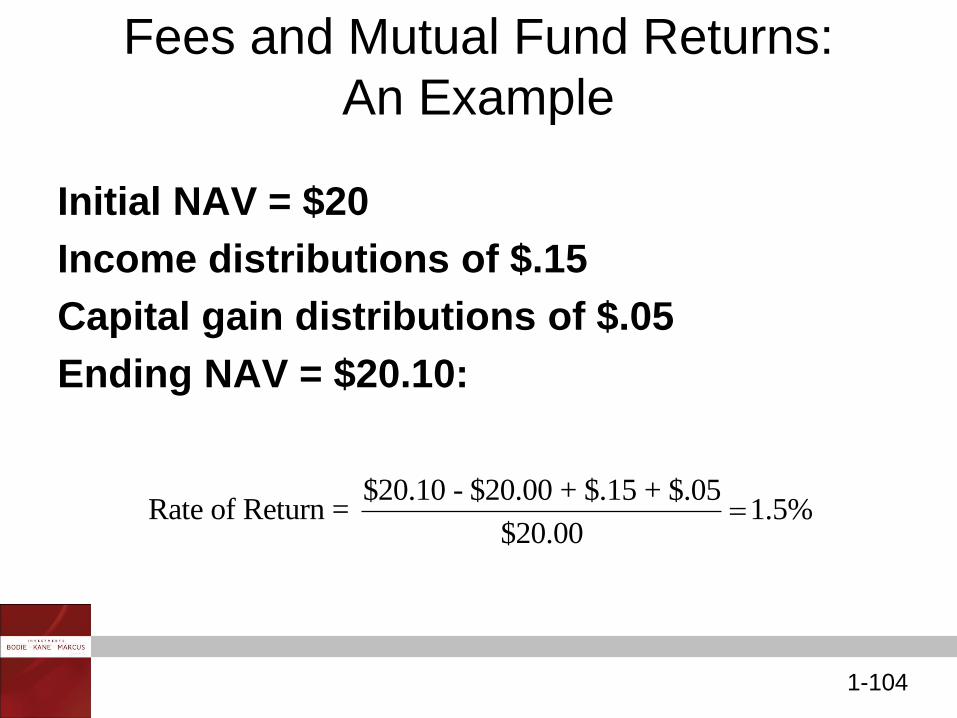

Fees and Mutual Fund Returns:

An Example

Initial NAV = $20

Income distributions of $.15

Capital gain distributions of $.05

Ending NAV = $20.10:

$20.10 - $20.00 + $.15 + $.05Rate of Return = 1.5%

$20.00

1-105

Table 4.2 Impacts of Costs on

Investment Performance

1-106

Trading Scandal with Mutual Funds

• Late trading – allowing some investors to

purchase or sell later than other investors

• Market timing – allowing investors to buy or

sell on stale net asset values

– International

• Net effect is to transfer value from other

shareholders to privileged traders

– Reduction in the rate of return of the

mutual fund

1-107

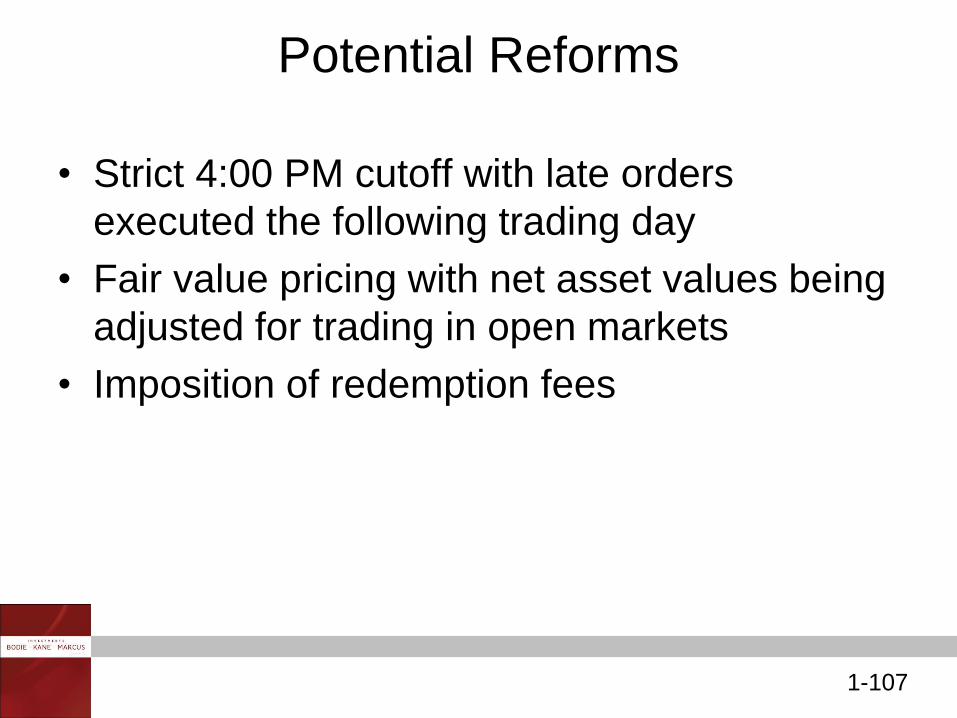

Potential Reforms

• Strict 4:00 PM cutoff with late orders

executed the following trading day

• Fair value pricing with net asset values being

adjusted for trading in open markets

• Imposition of redemption fees

1-108

Taxation on Mutual Fund Income

• Pass-through status under the U.S. tax code

– Taxes are paid only by the investor

• High turnover leads to tax inefficiency

1-109

Exchange Traded Funds

• ETF allow investors to trade index portfolios like shares of stock

• Examples - SPDRs and WEBS

• Potential advantages

– Lower taxes

– Trade continuously

– Lower costs

• Potential disadvantages

– Prices can depart by small amounts from NAV

1-110

Table 4.3 EFT Sponsors and Products

1-111

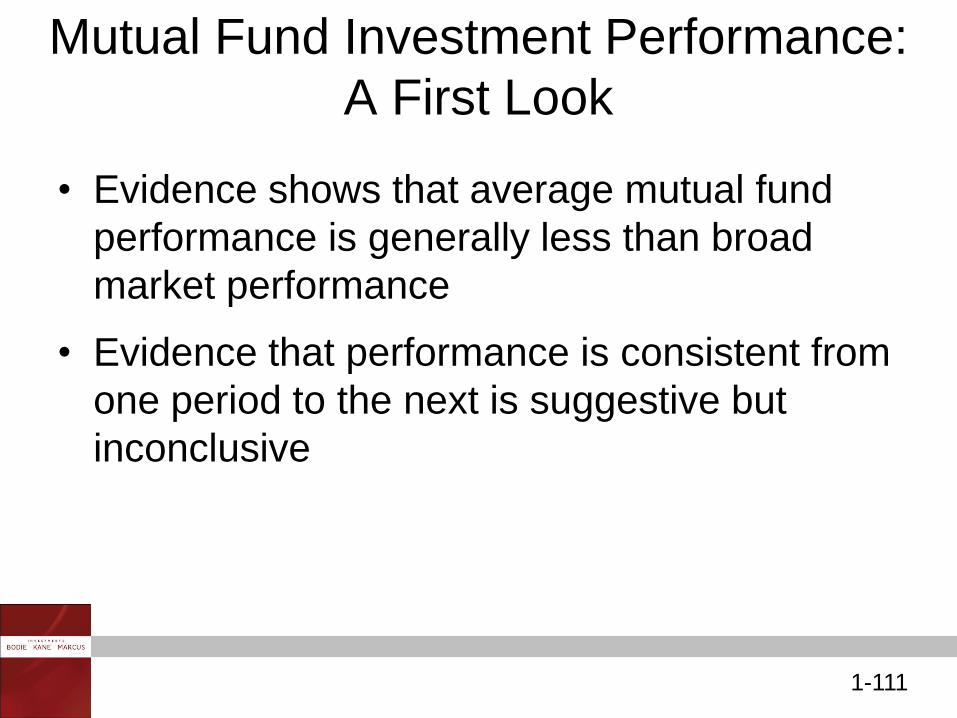

Mutual Fund Investment Performance:

A First Look

• Evidence shows that average mutual fund

performance is generally less than broad

market performance

• Evidence that performance is consistent from

one period to the next is suggestive but

inconclusive

1-112

Figure 4.2 Diversified Equity Funds

versus Wilshire 5000 Index

1-113

Table 4.4 Consistency of

Investment Results

1-114

Information on Mutual Funds

• Wiesenberger’s Investment Companies

• Morningstar (www.morningstar.com)

• Yahoo (biz.yahoo.com/funds)

• Investment Company Institute (www.ici.org)

• Directory of Mutual Funds