Embed Size (px)

Citation preview

Price ` 368

Target 460

Upside 25%

Div Yield -

Tenure 1 Year

Sensex 33904.44

Nifty 10205.10

Group/Index

M.cap (` in cr) 74112

Equity (` In cr) 2013.91

52 wk H/L ` 547.25/307.65

Face Value ` 10.00

NSE code HDFCLIFE

BSE code 540777

IN `

EV(` in Cr)** 15690

NW(`in cr) 5110

NB SA* 123440

AUM 109630

** Embedded Value

* New Business Sum Assured

Return on EV 18.40%

Return on IV * 65.30%

ROE 31.00%

Solvency ratio 197.00%

* Return on Invested capital

Source: Google

Has 26 partners across non traditional ecosystem, who offers tremendous growth potential (4 partners

added in Q1 FY19).

Also, launched specialised "Agency LIFE" program last year, it registered a growth of 26% over last year. As

on June,2018 HDFC has 83,128 individual agents – net addition of 6,080 during the quarter. Moreover, it

would continue to implement enhanced technology and mobile solutions to drive agent productivity.

The Robust online and digital sub-channel contributes 7% of Individual APE. 1,500+ frontline sales staff

across direct sales channels including branch, group sales (B2B), online and digital sub-channels. Aim to

emphasize cross selling and up selling by leveraging analytical tools.

87%/50%

Equitable Buiness mix

Reimagining Insurance- Focus on Digital platform

Entrust with Worthy Corporate Governance

Stock Details

Key Metrics

Key Ratios

Persistency

(13M/61M)

HDFC Life continues to benefit from its increased presence across the country having a wide reach with 414

branches and additional distribution touchpoints through several new tie-ups and partnerships comprising

163 bancassurance partners including NBFCs, MFIs, SFBs, etc (14 partners added in Q1 FY19) and Top 15

bancassurance partners have over 15,000 branches, Well positioned to capitalise on opportunities provided

by open architecture.

Bancassurance gains highest share of 65% in revenues. HDFC group entities sourced 13% of total group

business and 29% of total new business in Q1 FY19.

More than 85% of servicing requests are now serviced in less than 8 hours with over 70% serviced in less than 4

hours, have deployed advance analytics and predictive technologies for claim processing leading to an average

turnaround time of 3 days for claim settlement.

Profitable growth to be in Limelight

HDFC has always differentiated itself with new product offerings, innovative product models etc. Focus on

profitable growth will be something that the management is eyeing on in future. With new partners

widening the customer base for the bank such as the SFBs & NBFC's, rural innovators, payment apps etc &

Integration with new ecosystems such as Consumer insights from social media, app & mobile usage, Payment

banks to provide physical access, UPI, wallets for ease of payment & E-commerce players, aggregators and

other new-age start-ups as new sales platforms will drive growth & bring in healthy profits.

Wide access through 163 bancassurance and 26 non-traditional

ecosystem partnerships provides opportunity to increase

customer base & to cross-sell

BUY Investment Rationale

Share Holding Pattern

Dated : 31st Oct. 2018

INVESTMENT RESEARCH

FUNDAMENTAL COVERAGE -HDFC STANDARD LIFE INSURANCE COMPANY LTD

A / S&P BSE

100

Entrust with worthy corporate governance in its bucket, a market leader in product innovation,positions itself 1st among other private players terms of AUM, with balanced business mix,differentiate HDFC amongst others.

HDFC have leveraged new age technological capabilities like artificial intelligence, natural language

processing and robotics, enjoying ownership of e-product space. Given its focus and investment in the digital

platform, the company is uniquely positioned to capitalise on rising digitalisation of India’s economy.

Revamped customer service portal- MY ACCOUNT, Elle-The CHATBOX, Neo- TWITTER BOT, SPOK- Email

Bot, Net banking etc., all these initiatives have lead ease customers & save time.

Company is entrusted with Seasoned and stable senior management team, with decades of experience in

financial services. Having a track record of delivering consistent results across business cycles, Active

well-informed and independent Board oversees how the management serves and protects the interests

of all stakeholders. The superior, extensive, well equiped management distinguishes HDFC from others.

81%

19%

Promoter Others

Page 1 www.rudrashares.com

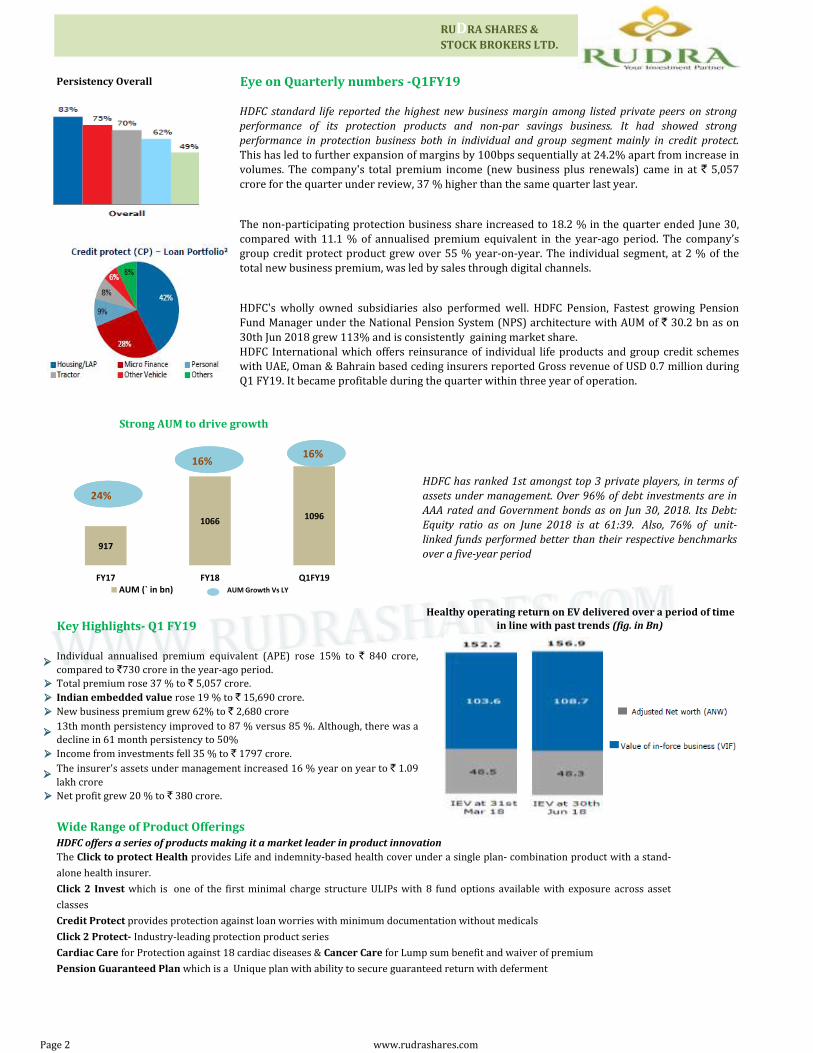

Persistency Overall Eye on Quarterly numbers -Q1FY19

Strong AUM to drive growth

Key Highlights- Q1 FY19

Total premium rose 37 % to ` 5,057 crore.

Indian embedded value rose 19 % to ` 15,690 crore.

New business premium grew 62% to ` 2,680 crore

Income from investments fell 35 % to ` 1797 crore.

Net profit grew 20 % to ` 380 crore.

Wide Range of Product OfferingsHDFC offers a series of products making it a market leader in product innovation

The Click to protect Health provides Life and indemnity-based health cover under a single plan- combination product with a stand-

alone health insurer.

Click 2 Invest which is one of the first minimal charge structure ULIPs with 8 fund options available with exposure across asset

classes

Credit Protect provides protection against loan worries with minimum documentation without medicals

Click 2 Protect- Industry-leading protection product series

Cardiac Care for Protection against 18 cardiac diseases & Cancer Care for Lump sum benefit and waiver of premium

Pension Guaranteed Plan which is a Unique plan with ability to secure guaranteed return with deferment

Individual annualised premium equivalent (APE) rose 15% to ` 840 crore,

compared to `730 crore in the year-ago period.

13th month persistency improved to 87 % versus 85 %. Although, there was a

decline in 61 month persistency to 50%

The insurer's assets under management increased 16 % year on year to ` 1.09

lakh crore

HDFC standard life reported the highest new business margin among listed private peers on strongperformance of its protection products and non-par savings business. It had showed strongperformance in protection business both in individual and group segment mainly in credit protect.This has led to further expansion of margins by 100bps sequentially at 24.2% apart from increase involumes. The company's total premium income (new business plus renewals) came in at ` 5,057

crore for the quarter under review, 37 % higher than the same quarter last year.

The non-participating protection business share increased to 18.2 % in the quarter ended June 30,compared with 11.1 % of annualised premium equivalent in the year-ago period. The company’sgroup credit protect product grew over 55 % year-on-year. The individual segment, at 2 % of thetotal new business premium, was led by sales through digital channels.

HDFC's wholly owned subsidiaries also performed well. HDFC Pension, Fastest growing PensionFund Manager under the National Pension System (NPS) architecture with AUM of ` 30.2 bn as on

30th Jun 2018 grew 113% and is consistently gaining market share.HDFC International which offers reinsurance of individual life products and group credit schemeswith UAE, Oman & Bahrain based ceding insurers reported Gross revenue of USD 0.7 million duringQ1 FY19. It became profitable during the quarter within three year of operation.

HDFC has ranked 1st amongst top 3 private players, in terms ofassets under management. Over 96% of debt investments are inAAA rated and Government bonds as on Jun 30, 2018. Its Debt:Equity ratio as on June 2018 is at 61:39. Also, 76% of unit-linked funds performed better than their respective benchmarksover a five-year period

Healthy operating return on EV delivered over a period of time

in line with past trends (fig. in Bn)

RUDRA SHARES &

STOCK BROKERS LTD.

917

1066 1096

FY17 FY18 Q1FY19 AUM (` in bn)

24%

16% 16%

24%

16% 16%

AUM Growth Vs LY

Page 2 www.rudrashares.com

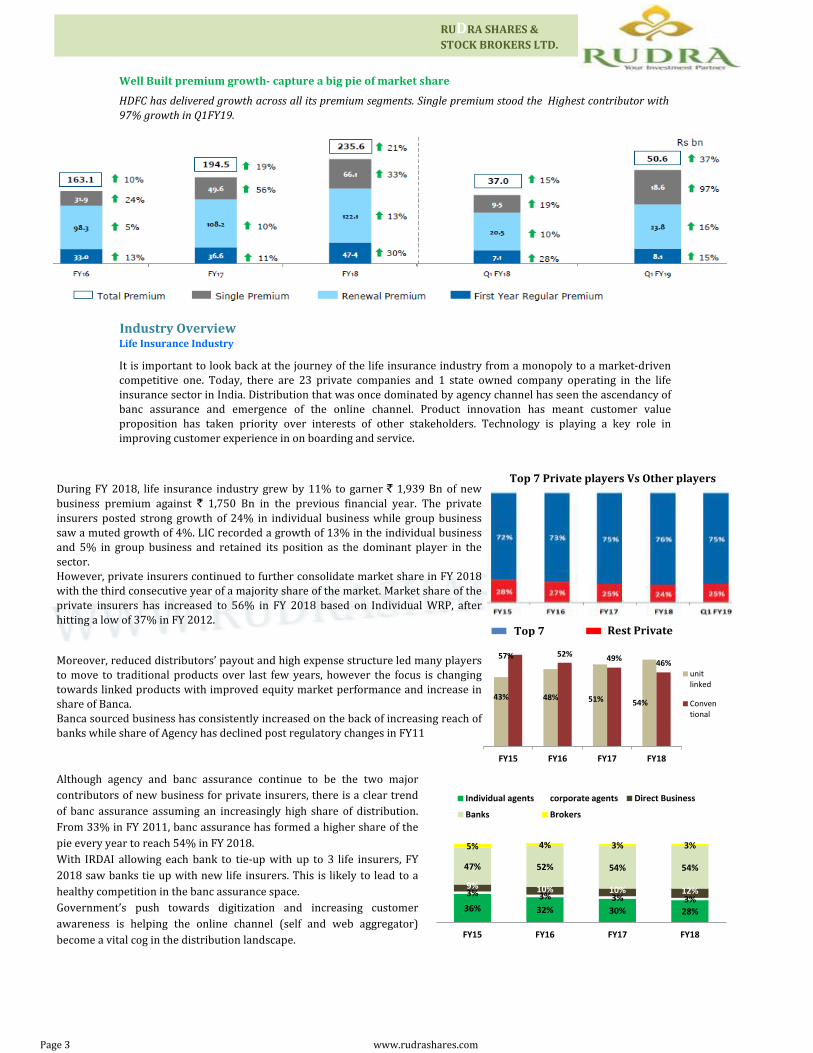

Well Built premium growth- capture a big pie of market share

Industry OverviewLife Insurance Industry

Top 7 Rest Private

HDFC has delivered growth across all its premium segments. Single premium stood the Highest contributor with97% growth in Q1FY19.

It is important to look back at the journey of the life insurance industry from a monopoly to a market-drivencompetitive one. Today, there are 23 private companies and 1 state owned company operating in the lifeinsurance sector in India. Distribution that was once dominated by agency channel has seen the ascendancy ofbanc assurance and emergence of the online channel. Product innovation has meant customer valueproposition has taken priority over interests of other stakeholders. Technology is playing a key role inimproving customer experience in on boarding and service.

RUDRA SHARES &

STOCK BROKERS LTD.

Moreover, reduced distributors’ payout and high expense structure led many playersto move to traditional products over last few years, however the focus is changingtowards linked products with improved equity market performance and increase inshare of Banca.Banca sourced business has consistently increased on the back of increasing reach ofbanks while share of Agency has declined post regulatory changes in FY11

Although agency and banc assurance continue to be the two major

contributors of new business for private insurers, there is a clear trend

of banc assurance assuming an increasingly high share of distribution.

From 33% in FY 2011, banc assurance has formed a higher share of the

pie every year to reach 54% in FY 2018.

With IRDAI allowing each bank to tie-up with up to 3 life insurers, FY

2018 saw banks tie up with new life insurers. This is likely to lead to a

healthy competition in the banc assurance space.

Government’s push towards digitization and increasing customer

awareness is helping the online channel (self and web aggregator)

become a vital cog in the distribution landscape.

During FY 2018, life insurance industry grew by 11% to garner ` 1,939 Bn of new

business premium against ` 1,750 Bn in the previous financial year. The private

insurers posted strong growth of 24% in individual business while group businesssaw a muted growth of 4%. LIC recorded a growth of 13% in the individual businessand 5% in group business and retained its position as the dominant player in thesector.However, private insurers continued to further consolidate market share in FY 2018with the third consecutive year of a majority share of the market. Market share of theprivate insurers has increased to 56% in FY 2018 based on Individual WRP, afterhitting a low of 37% in FY 2012.

Top 7 Private players Vs Other players

43% 48% 51% 54%

57% 52% 49% 46%

FY15 FY16 FY17 FY18

unit linked

Conventional

36% 32% 30% 28%

3% 3% 3% 3%

9% 10% 10% 12%

47% 52% 54% 54%

5% 4% 3% 3%

FY15 FY16 FY17 FY18

Individual agents corporate agents Direct Business

Banks Brokers

Page 3 www.rudrashares.com

The widespread adoption of Smartphone and the affordability of data usage are speeding up the realization ofopportunity. Company has been at the forefront of technology investments and it has made significant

progress on its digital insurer journey. The Company continues to build its distribution network of agents,deepen its Bancassurance relationships and open new partnerships with NBFCs, Fin techs and non-traditionalplayers (e-commerce, payments, loyalty etc.).

On the back of new ties, wide rang of product offerings, strong positioning, entrust with strong corporatesboard, widespread adoption of Smartphone and bank to deepen its banc assurance relationships, it is wellpoised for future growth.

We estimate VNB to grow at 20-25 % CAGR in the next year. We value HDFC life at Rs 430, whichcorresponds to 5.5x of Q1FY19 embedded value.Owing to strong corporate governance and its strong position, HDFC Life enjoys higher valuation.

RUDRA SHARES &

STOCK BROKERS LTD.

Valuation Conclusion

Company Overview

Established in 2000, HDFC Standard Life Insurance Company Limited is a leading long-term life insurancesolutions provider, offering a range of individual and group insurance solutions that meet various customer needssuch as Protection, Pension, Savings, Investment, and Health.The HDFC Life is a joint venture between Housing Development Finance Corporation Limited (HDFC Ltd.),India’s leading housing finance institution and Standard Life Aberdeen, a global investment company.During the year under review, HDFC Life completed its Initial Public Offer by way of an offer for sale of 14.92% ofthe fully diluted post-offer paid-up equity share capital of the Company. The shares of HDFC Life are listed onNational Stock Exchange of India Limited and BSE Limited w.e.f. November 17, 2017.

Page 4 www.rudrashares.com

Disclosures :

1) Business Activity :

2)

3)

4)

Sr. No. Yes/No

a) No

b) No

c) No

5)

Sr. No. Yes/No

a) No

b) No

c) No

6) Other Disclosures:

Yes/No

Sr. No.

a) No

b) No

c) No

Rudra or its associates have received any compensation or other benefits from the subject

company or third party in connection with the research report .

Rudra or its research analysts, or his/her relative or associates have actual/beneficial

ownership of one per cent or more securities of the subject company.

Rudra or its associates have managed or co-managed public offering of securities for the

subject in the past twelve months.

Disclosures

Rudra or its associates have received any compensation from the subject company in the

past twelve months.

Rudra or its research analysts, or his/her relative or associate has any direct or indirect

financial interest in the subject company.

Disclosures with regard to receipt of compensation :

The Research report is issued to the registered clients. The Research Report is based on the facts, figures and

information that are considered true, correct and reliable. The information is obtained from publicly available media or

other sources believed to be reliable. The report is prepared solely for informational purpose and does not constitute an

offer document or solicitation to buy or sell or subscribe for securities or other financial instruments for clients.

Disclosures with regard to ownership and material conflicts of interest :

RUDRA SHARES &

STOCK BROKERS LTD.

Rudra or its research analysts, or his/her relative or associate has any other material

conflict of interest at time of publication of the research report.

Disclosures

Rudra Shares & Stock Brokers Limited is engaged in the business of providing broking services & distribution of

various financial products. RUDRA is also registered as a Research Analyst under SEBI(Research Analyst) Regulations,

2014. SEBI Reg. No. INH100002524.

Disclosures & Disclaimers

Terms & Conditions of issuance of Research Report:

There has been no instance of any Disciplinary action, penalty etc. levied/passed by any regulation/administrative

agencies against RUDRA and its Directors. Pursuant to SEBI inspection of books and records of Rudra, as a Stock Broker,

SEBI has not issued any Administrative warning to Rudra.

Disciplinary History :

Disclosures

The research analyst has served as an officer,director,employee of the subject company.

Rudra or its research analyst has been engaged in market making activity for the subject

company.

Rudra or its or associates have received any compensation from the subject company in the

past twelve months.

Page 5 www.rudrashares.com

RUDRA SHARES & STOCK BROKERS LTD.

Phone: +91 – 512 – 67011001

Disclaimers:

This Research Report (hereinafter called report) has been prepared and presented by RUDRA SHARES & STOCK BROKERS

LIMITED, which does not constitute any offer or advice to sell or does solicitation to buy any securities. The information presented in

this report, are for the intended recipients only. Further, the intended recipients are advised to exercise restraint in placing any

dependence on this report, as the sender, Rudra Shares & Stock Brokers Limited, neither guarantees the accuracy of any information

contained herein nor assumes any responsibility in relation to losses arising from the errors of fact, opinion or the dependence placed

on the same.

Despite the information in this document has been previewed on the basis of publicly available information, internal data , personal

views of the research analyst(s)and other reliable sources, believed to be true, we do not represent it as accurate, complete or

exhaustive. It should not be relied on as such, as this document is for general guidance only. Besides this, the research analyst(s) are

bound by stringent internal regulations and legal and statutory requirements of the Securities and Exchange Board of India( SEBI)

and the analysts' compensation was, is, or will be not directly or indirectly related with the other companies and/or entities of Rudra

Shares & Stock Brokers Ltd and have no bearing whatsoever on any recommendation, that they have given in the research report.

Rudra Shares & Stock Brokers Ltd or any of its affiliates/group companies shall not be in any way responsible for any such loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Rudra Shares & Stock

Brokers Ltd has not independently verified all the information, which has been obtained by the company for analysis purpose, from

publicly available media or other sources believed to be reliable. Accordingly, we neither testify nor make any representation or

warranty, express or implied, of the accuracy, contents or data contained within this document. Rudra Share & Stock Brokers Ltd and

its affiliates are engaged in investment advisory, stock broking, retail & HNI and other financial services. Details of affiliates are

available on our website i.e. www.rudrashares.com.

We hereby declare, that the information herein may change any time due to the volatile market conditions, therefore, it is advised to

use own discretion and judgment while entering into any transactions, whatsoever.

Individuals employed as research analyst by Rudra Shares & Stock Brokers Ltd or their associates are not allowed to deal or trade in

securities, within thirty days before and five days after the publication of a research report as prescribed under SEBI Research

Analyst Regulations.

Subject to the restrictions mentioned in above paragraph, we and our affiliates, officers, directors, employees and their relative may:

(a) from time to time, have long or short positions acting as a principal in, and buy or sell the securities or derivatives thereof, of

Company mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or profits.

RUDRA SHARES &

STOCK BROKERS LTD.

Page 6 www.rudrashares.com