Embed Size (px)

Citation preview

0

INVESTMENT OPPORTUNITIES IN ITALY

FOR TURKISH COMPANIES

ANKARA ▪ ISTANBUL ▪ IZMIR

October 2015

TURKISH-ITALIAN COOPERATION MEETING

1ST FDI ATTRACTION ROADSHOW

THE ITALIAN GOVERNMENT

1

2

SAMPLES OF INVEST OPPORTUNITIES: INDEX

• Food and Beverage 27 • Fashion Industry 23 • Real Estate 20 • Automotive and Components 8 • Construction Material 7 • Industrial Machinery 6 • Textile Industry 6 • Pharmaceutical Industry 3 • Metallurgic Industry 2 • Chemical Industry 1 • Components Industry 1 • Electronic Equipment 1 • Flat Glass 1 • Furniture & Crafts 1 • ICT 1 • Petrochemical Industry 1 • Pharmaceutical equipment 1 • Railway 1 • Retail 1 • Software Engineering 1 • Tourism 1 • Transportation 1 • White Goods Industry 1

... and in 23 sectors 116 projects in 17 Regions…

25

1

10 12

11

14

5

3

8

7

8

3

1

1

2

2

1

3

4

CONTENT OF THE DOCUMENT

• M&A OPPORTUNITIES

• OTHER PROJECTS

5

6

COMPANY 31 - AUTOMOTIVE AND COMPONENTS M&A

OPPORTUNITIES

TURNOVER From 20 to 30

NUMBER OF EMPLOYEES From 50 to 100

COMPANY OVERVIEW

• The company, based in the centre of Italy and founded in

1976, is a leader in the field of design and production of

printed circuit boards. The Company is active in printed

circuits boards, flexible, rigid and electronic components

for automotive in particular, but also for other sectors

(audio-visual, healthcare, white goods, energy,

telecommunications, energy and banking). The company

is focused on research & development, technological

innovation and continuous training of his highly

specialised staff.

• Certifications: ISO TS 16949:2009; ISO 9001:2008

• The company created some partnership and joint-projects

with its customers. The company is able to develop a

wide range of products with high standards at

internationally competitive prices.

• Transnational Activity: 20 to 49% of the turnover.

• The owner is available for cooperation with foreign

partners and for both solutions:

- Financial partner: in the minority stake

- Industrial partner: sell the majority stake

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

Euro Mln, Number, 2013

7

COMPANY OVERVIEW

COMPANY 54 - AUTOMOTIVE AND COMPONENTS

MARKETS & COMPANY STRUCTURE

• The Company, founded in the ’70s, offers its customers,

such as Tier 1 automotive clients, a broad product

portfolio in both steel and aluminum, producing doors,

hatches, sliding door systems, structural assemblies, and

modules for structural body parts for light commercial

vehicles (LCV) and cars. The Group has 10

manufacturing facilities strategically located close to

major customers and 740 employees.

• In May 2013, the Group started 2 operating JVs (both in

Canada and in Europe) with a North American

manufacturer of structural body parts for cars and other

motor vehicles, focused on hydro forming technology

• In March 2014, the Group started a marketing JV in

China with a Chinese conglomerate, one of the main

players operating in the steel industry worldwide

M&A

OPPORTUNITIES

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• The owner is available to a sell the majority stake.

2010 2011 2012

TURNOVER 121,3 132,4 143,7

EBITDA 10,1 8,4 9,2

Euro Mln

8

COMPANY OVERVIEW

COMPANY 55 - AUTOMOTIVE AND COMPONENTS

MARKETS & COMPANY STRUCTURE

• The Company is a family-owned business, among global

leaders in the manufacture of high precision

machined metal products for the Auto industry

worldwide, and primarily a Tier 2 supplier. The Company

makes critical small parts in high volume to very high

precision. It operates at the micron level of tolerance and

produces an average 170 million parts per year with a

defect rate of 4ppm or less. The Company is focused on

critical high-precision components primarily for

automotive powertrain and chassis applications e.g.

components of gasoline and diesel fuel injectors, starter

motors, AC compressors and shock absorbers.

• The Company serves a broad range of sophisticated

customers and sells globally. Automotive accounts for

about 90% of total revenues, followed by Aerospace and

Appliances. Approximately 85% of sales are in Europe,

10% in the Americas and 5% in Asia (China, India).

Germany is the largest market for HPM (36% of sales).

Top 5 Customers in 2012 were Bosch, Delphi, Eaton,

Sanden and Continental

M&A

OPPORTUNITIES

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• The Owners are open to consider selling the majority or

even the totality of their shares.

• The Company is managed by a strong CEO and

Executive Team committed to continue growing the

business

• 2014 revenues are about 95 mln euro with EBITDA of

about 16 mln euro and net debt close to 36 mln euro;

• 2015 budget indicates sales of 99 euro mln, EBITDA of

18 mln euro , net debt of 34 mln euro.

9

COMPANY 58 - AUTOMOTIVE AND COMPONENTS M&A

OPPORTUNITIES

COMPANY OVERVIEW

• The Company is an Italian group that designs and

manufactures customized metal components (i.e.

tubes and brackets for exhaust systems) mainly for the

automotive industry. The Company owns state of the art

and flexible production plants for bending, welding

punching and press of metal components. The Group

develops its activity in 4 plants, one of which is

located abroad, with a total surface of some 15,000

sqm and owns international standard certifications like

ISO UNI EN ISO 9002, UNI EN ISO 14000 and ISO TS

16949.

• The Group’s main customers are well-known Tier 1 and

OEM operators. 80% of the turnover is generated abroad

(EU countries). The Comapny is able to assists its

customers, during all the production steps from the

fulfillment of the idea to the delivery of the final products

• The Company employs approximately 380 people

• The owner is available to a sell the majority stake.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

Euro Mln, Number, 2014

2012 2013 2014

TURNOVER 49 55 57

EBITDA 3,6 5,3 5,8

10

COMPANY OVERVIEW

COMPANY 52 - AUTOMOTIVE AND COMPONENTS

MARKETS & COMPANY STRUCTURE

• The company is the result of two companies founded by

the same entrepreneur. Both companies operate in two

different niches of the value chain of brake aftermarket

automotive components.

• Due to a thirty year-old experience, the company is an

European leader in the brake parts production thanks

to the quality of its products and the continuous research

of new technical solutions.

• Following requests by racing car sector, the company

R&D department together with tuning firms, developed a

Racing friction material only for competition with highly

performances.

• Company products range includes: shoes, pads, shoes

kits, discs, wheel cylinders, pressure regulating valves,

master/slave cylinders, clutch master cylinders.

• The company is certified: UNI ENI ISO 9001:2008, ECE

R-90, AAMVA.

M&A

OPPORTUNITIES

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• The company is looking for an investor to sell the existing

share. 2010 2011 2012

TURNOVER 24,6 24,0 24,8

EBITDA 5,7 5,0 5,4

Euro Mln

11

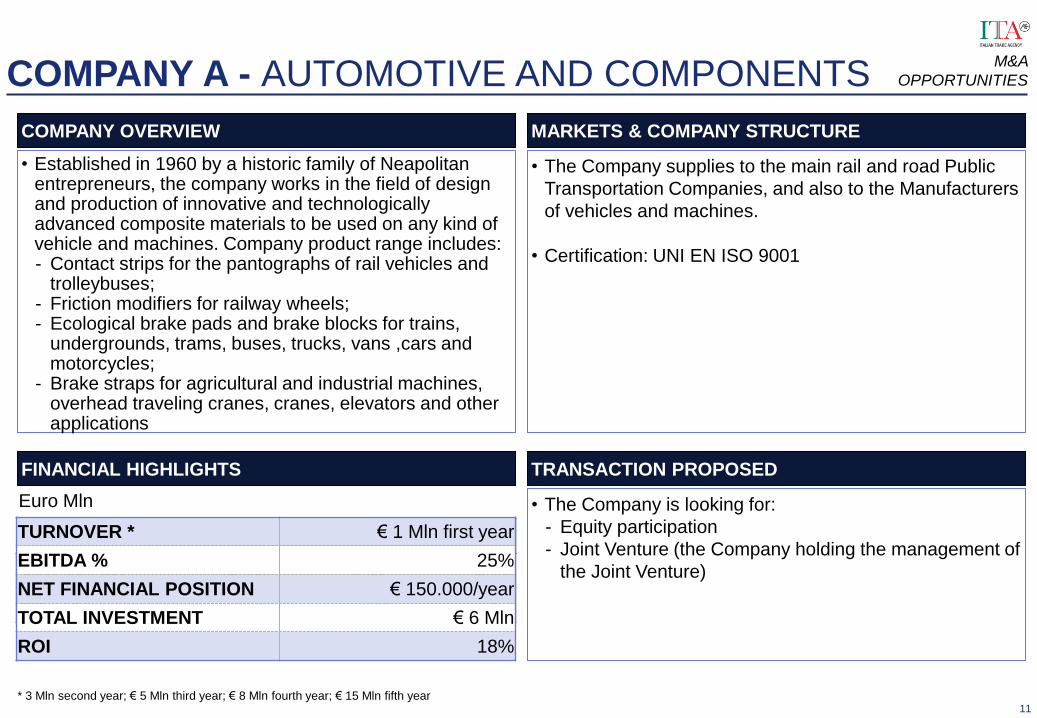

• The Company supplies to the main rail and road Public

Transportation Companies, and also to the Manufacturers

of vehicles and machines.

• Certification: UNI EN ISO 9001

COMPANY A - AUTOMOTIVE AND COMPONENTS M&A

OPPORTUNITIES

COMPANY OVERVIEW

• Established in 1960 by a historic family of Neapolitan entrepreneurs, the company works in the field of design and production of innovative and technologically advanced composite materials to be used on any kind of vehicle and machines. Company product range includes: - Contact strips for the pantographs of rail vehicles and

trolleybuses; - Friction modifiers for railway wheels; - Ecological brake pads and brake blocks for trains,

undergrounds, trams, buses, trucks, vans ,cars and motorcycles;

- Brake straps for agricultural and industrial machines, overhead traveling cranes, cranes, elevators and other applications

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• The Company is looking for:

- Equity participation

- Joint Venture (the Company holding the management of

the Joint Venture)

2010 2011 2012

TURNOVER 24,6 24,0 24,8

EBITDA 5,7 5,0 5,4

Euro Mln

TURNOVER * € 1 Mln first year

EBITDA % 25%

NET FINANCIAL POSITION € 150.000/year

TOTAL INVESTMENT € 6 Mln

ROI 18%

* 3 Mln second year; € 5 Mln third year; € 8 Mln fourth year; € 15 Mln fifth year

12

COMPANY F - AUTOMOTIVE AND COMPONENTS M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• The Company is engaged in the design and manufacture

of bodies (coachwork) for motor vehicles as well as

trailers and semi-trailers

• One of the largest producers of trucks and towing trucks

in Italy and among the largest in Europe

• Production capacity is over 15,000 per year

• The average revenue of the top-20 Italian companies in

this sector is € 60 mln per year

Asset Profile

• Plant based in central Italy

WHY INVEST

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• STRENGTHS: very competitive and effective post-sale

service, state-of-the-art equipment, wide product-offer and

highly-qualified workforce. The company has a long term

track record of production and high-standing relations with

local stakeholders

• CHALLENGES: due to declining domestic demand the

company needs to open up to new international markets

• The Company is looking for an Industrial investor

• Company/plant acquisition

FIANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 45 ~ 27 ~ 37

EBITDA ~ -6 ~- 5 ~ -4

Employees ~ 350

Net Financial Position ~ 36 ~ 38 ~ 35

Euro Mln

13

COMPANY G - AUTOMOTIVE AND COMPONENTS M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• Leading Company in the tyre production in Italy.

• Average revenues top-10 Italian companies € ~30 mln

Asset Profile • Plant for the manufacture of rubber tyres and tubes

located in northern Italy wholly controlled by the parent company

• Retreading and rebuilding of rubber tyres (commercial tyres, car tyres, industrial tyres, earthmover tyres, design and R&D, tyres machinery, retreading system)

WHY INVEST

TRANSACTION PROPOSED

• STRENGTH POINTS: highly qualified workforce; plants

covers 40,000 sq. Leading tyre production in Italy with

positive relations with local stakeholders

• POTENTIAL MARKETS: 50% of the production is

exported to Europe, mainly to Germany and the UK

• CHALLENGES: the plant is facing strong price

competition from producers in Europe and East Asia.

Costs reduction represents one of the key challenge

• The Company is looking for an Industrial investor

• Company/plant acquisition (€ 140 mln revenues,

EBITDA/turnover 9.5%)

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 110 ~ 85 ~ 50

EBITDA ~ 3 ~ 0,7 ~ -7

Employees 420

Net Financial Position ~ 30 ~ 18 ~ 13

Euro Mln, Number

14

COMPANY T - CHEMICAL INDUSTRY M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• The company operates in wholesale and manufacturing

of plastic materials, synthetic resins and other related

products

• Engaged in the wholesale distribution of chemicals and

chemical products.

Asset Profile

• Plants for the production of chemical product, nitrogen

fertilizers, plastic materials and rubber is located in the

South of Italy.

WHY INVEST

TRANSACTION PROPOSED

• STRENGTHS: The plant is in perfect conditions and has

a production capacity of 250-300,000 tons per year, out

of 1 mln tons per year of potential market in Italy

• POTENTIAL MARKETS: further expanding in the Italian

market and increase the penetration in the European

market.

• The Company is looking for an Industrial investor

• Asset acquisition

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 1.5 ~ 1.2 ~ 1

EBITDA ~ -1.3 ~ 1.1 ~ -0.89

Employees 82

Net Financial Position ~ 1,600 ~ 790 ~ -24

Euro Mln, Number

15

COMPANY I – COMPONENTS INDUSTRY M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• The Company operates in the manufacturing and

distribution of wires in Italy and abroad, steel wiredrawing,

steel nails and spikes, cold drawing of wire

• The Company also manufactures strands for reinforced

concrete, wire ropes, ties and lifting equipment

• The company is wholly owned by foreign European

companies

Asset Profile

• Production plants based in northern Italy, in liquidation

WHY INVEST

TRANSACTION PROPOSED

• POTENTIAL MARKETS: wide possibility to increase the

penetration into the European markets

• CHALLENGES: the first problems emerged in 2010-2011

due to financial crisis

• The Company is looking for an Industrial investor

• Company merger & acquisition

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 56 ~ 37 ~ 1

EBITDA ~ 3 ~ -5 ~ -8

Employees 105

Net Financial Position ~ 13 ~ 5 ~ 2

Euro Mln

16

COMPANY 1 - CONSTRUCTION MATERIALS

COMPANY OVERVIEW PRODUCT RANGE

• The Company was founded 70 years ago by the aggregation of different companies active in the hydraulic binding business.

• One of the main Italian player for the cement market, the Company is organized into a major group active in two other business: concrete and transportation.

• The Company has production facilities in Italy in the following locations: Testi-Greve in Chianti (FI), Castelraimondo (MC), Cagnano Amiterno (AQ), Tavernola Bergamasca (BG) e Pescara (PE).

• The Company has a Turnover of €105,3 m.

FINANCIAL HIGHLIGHTS NOTE

• The Company received an offer from a major Italian

group, back in the first quarter of 2015, but was turned

down by the company’s creditor banks.

• Currently the Company may attract other offers.

Cement

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 148,6 154,2 133,2 105,3

EBITDA 12,1 15,3 5,1 (6,1)

EBITDA margin 8,1% 9,9% 3,9% n.m.

Net Profit (21,5) (23,4) (63,4) (33,6)

Fixed Assets 396,5 361,8 327,7 350,7

NFP 296,3 305,1 305,9 325,3

Shareholder's funds 126,3 122,8 59,4 69,9

17

COMPANY 2 - CONSTRUCTION MATERIALS

COMPANY OVERVIEW PRODUCT RANGE

• The Company was founded in 2001 in the Modena area from the idea of its founder, who stepped into the ceramic market with an innovative patent to manufacture ceramic slabs of large surface area and minimum thickness.

• The Company products are not only used for construction purpose such as architecture and coatings for interior and exterior, but as well as new sectors such as furniture and technologies of energy generation from renewable sources.

• The Company has a Turnover of around €40 m.

FINANCIAL HIGHLIGHTS NOTE

• In May 2015 the Company’s CEO announced that the

Company is looking to expand into new markets through

JV partnerships.

Large Minimum Thickness Ceramic Surface

M&A

OPPORTUNITIES

Key financial data (€/m) 2011 2012 2013 2014

Revenues 25,0 24,1 29,8 39,4

EBITDA 3,6 3,5 6,2 8,2

EBITDA margin 14,5% 14,5% 20,9% 20,9%

Net Profit 2,2 0,5 2,5 3,6

Fixed Assets 9,6 8,5 7,6 6,5

NFP 0,0 0,0 0,0 0,0

Shareholder's funds 10,1 10,6 14,2 17,8

18

COMPANY 3 - CONSTRUCTION MATERIALS

COMPANY OVERVIEW PRODUCT RANGE

• The Company was established in the 1960’s and is a family run business.

• The Company specializes in wooden houses and also produces laminated wood structures.

• The business is divided into structures, living and panels, according to its product range.

• The Company consolidated turnover for 2014 is €30 m according to Company information.

FINANCIAL HIGHLIGHTS NOTE

• The Company is looking for an external investor (Aug.

2015), the advisor has been already appointed.

• According to the Company management an ideal would

be an international player active in the Company’s

industry interested in accelerating expansion.

Precast Wood Panels

M&A

OPPORTUNITIES

Laminated Beams

Wooden Houses

Key financial data (€/m) 2010 2011 2012 2013

Revenues 10,3 9,8 14,6 12,6

EBITDA 0,7 0,8 (0,2) 1,8

EBITDA margin 6,3% 8,4% n.m. 14,1%

Net Profit 0,1 (0,3) (1,4) 0,0

Fixed Assets 11,7 12,0 12,7 12,3

NFP 9,9 10,8 13,9 12,7

Shareholder's funds 5,0 6,6 5,2 5,2

Note: The financial data are unconsolidated. According to the Company the turnover amounted

to €30 m in 2014

19

COMPANY 15 - CONSTRUCTION MATERIALS M&A

OPPORTUNITIES

COMPANY OVERVIEW

• The group is an Italian producer of paints for the construction

industry private Italian commercial refrigeration company.

• The company is looking for acquisition targets in the Middle

East.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• In 2014, the company posted a turnover of EUR 70m, with a

20% EBITDA margin. It forecasts a 10% revenue bump in

2015, due to a recent acquisition and new manufacturing

capacity, obtained pursuant to a EUR 3.5m investment to

enlarge its production premises in a village, near Venice.

• The company is also pursuing M&A deals in Europe, namely

in Germany and Turkey,.

• The company has been funding its M&A plans with internal

cash resources, and intends to continue doing so in the near

future. However, it could consider taking on an investor

through the sale of a minority stake, should midterm projects

require extra funds.

20

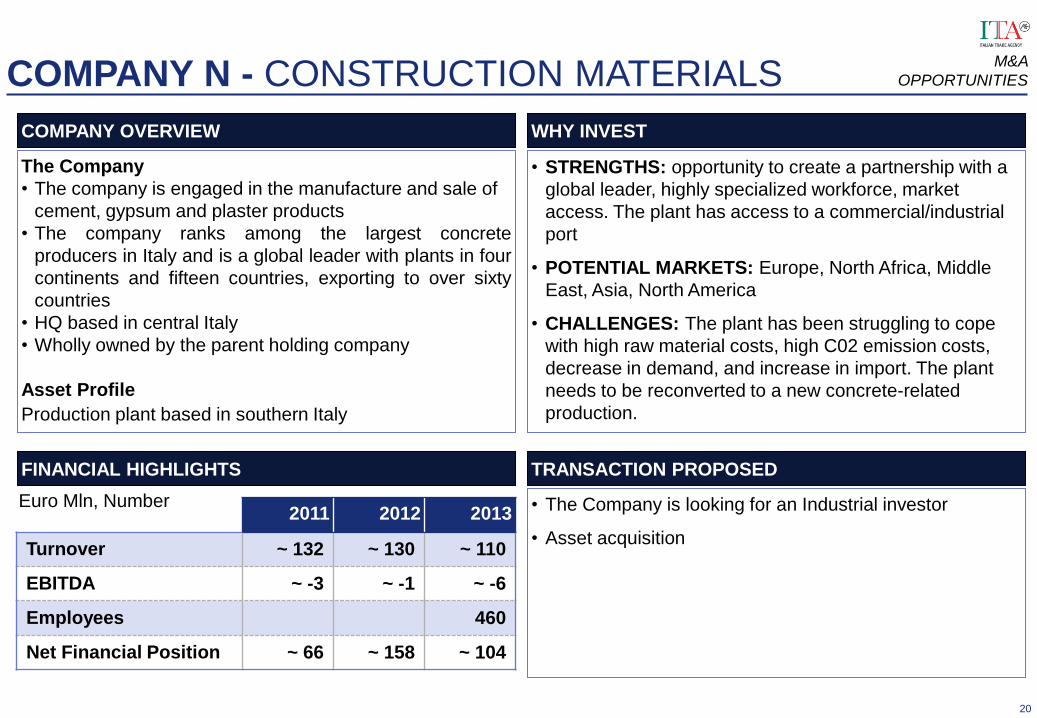

COMPANY N - CONSTRUCTION MATERIALS M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• The company is engaged in the manufacture and sale of

cement, gypsum and plaster products

• The company ranks among the largest concrete

producers in Italy and is a global leader with plants in four

continents and fifteen countries, exporting to over sixty

countries

• HQ based in central Italy

• Wholly owned by the parent holding company

Asset Profile

Production plant based in southern Italy

WHY INVEST

TRANSACTION PROPOSED

• STRENGTHS: opportunity to create a partnership with a

global leader, highly specialized workforce, market

access. The plant has access to a commercial/industrial

port

• POTENTIAL MARKETS: Europe, North Africa, Middle

East, Asia, North America

• CHALLENGES: The plant has been struggling to cope

with high raw material costs, high C02 emission costs,

decrease in demand, and increase in import. The plant

needs to be reconverted to a new concrete-related

production.

• The Company is looking for an Industrial investor

• Asset acquisition

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 132 ~ 130 ~ 110

EBITDA ~ -3 ~ -1 ~ -6

Employees 460

Net Financial Position ~ 66 ~ 158 ~ 104

Euro Mln, Number

21

COMPANY B - CONSTRUCTION MATERIALS M&A

OPPORTUNITIES

COMPANY OVERVIEW

• Established in 1960 the company works in the design,

production, trade and assembling of prefabricated

metallic constructions. Started as individual firm, since

1979 is a shared capital enterprise.

• Products range: Container, Modular Componable, Shelter

and Metallic Parking System

• Supplier of shelters mainly in electric, radar,

telecommunication, petrolchemical sectors, partner of

Enel spa, Gruppo Eni spa, Telecom Italia Mobile spa,

Alenia Marconi System spa, ABB spa, Ericsson

Telecomunicazioni spa, Telecom Italia spa and many

others international companies.

• The Company internal structure is composed of single

directions (technical, production, commercial and

administrative)

• Production plant on a surface of over 30.000 sqm is

located in Campania Region

• Among Italian first companies to obtain a UNI EN ISO

9001 Quality System certification in 1997

• Patented a Metallic Parking System, capable of doubling

car parking surfaces

• The Owners are considering selling the majority of the

stakes

• They are looking not only for a financial partner but for an

investor committed to expanding the business

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• Annual Turnover 7.5 ml in the last 4 years.

• Annual Turnover in 2014: 8 ml

22

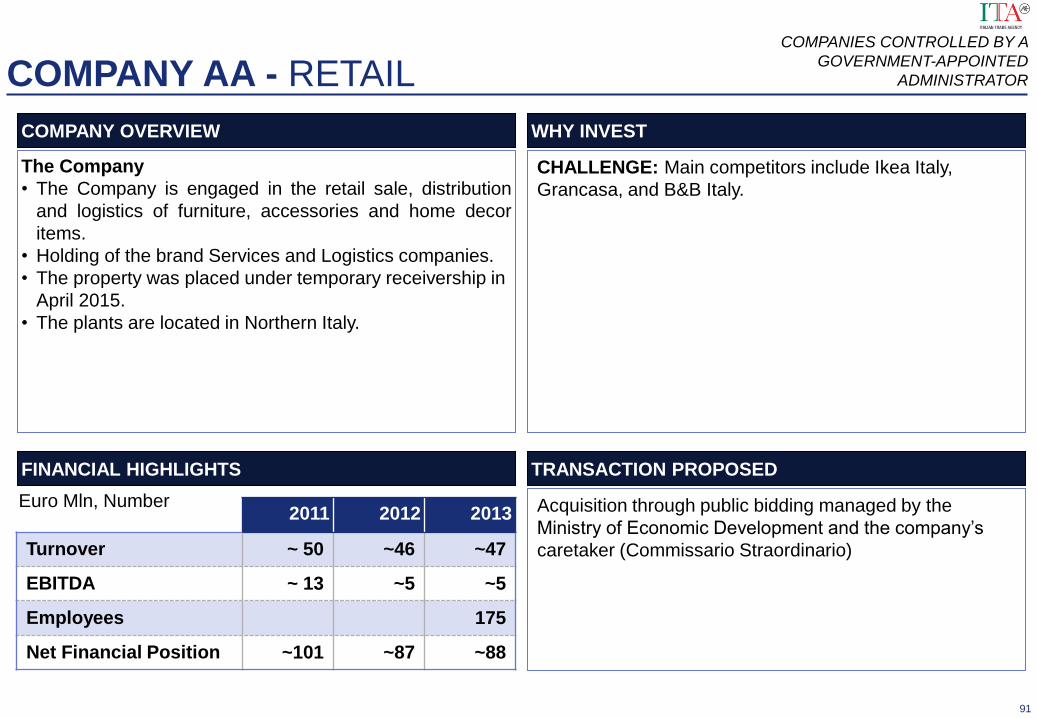

COMPANY Z - CONSTRUCTION MATERIAL

COMPANY OVERVIEW

The Company

• The Company is engaged in the production of pre-

fabricated structural metal, precast concretes, metal

structures and photovoltaic panels.

• The Company was placed under temporary receivership

since February 2014.

WHY INVEST

TRANSACTION PROPOSED

• STRENGTHS: The Company also owns subsidiaries that produce pre-fabricated concrete buildings in Spain and photovoltaic panels in Italy.

• POTENTIAL MARKETS: it needs to expand into new markets beyond the stagnant building sector in Italy and Spain

• CHALLENGES: the company’s decision to increase production capacity and diversify its activities in a downward market was not successful. It resulted in high indebtedness and lack of capitalization. Lack of professional management (family-owned firm) has also been an issue in the past. Strong competition from producers in East Europe.

• Looking for industrial/financial investor.

• Company/branch acquisition through public bidding

managed by the Ministry of Economic Development and

the company’s caretaker (Commissario Straordinario).

• Non essential assets are to be liquidated.

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~59 ~19 n.a.

EBITDA ~-13 ~-21 n.a.

Employees 230 n.a.

Net Financial Position ~53 ~50 n.a.

Euro Mln, Number

COMPANIES CONTROLLED BY A

GOVERNMENT-APPOINTED

ADMINISTRATOR

23

COMPANY K - ELECTRONIC EQUIPMENT M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• Engaged in the manufacturing of electronic equipment for

telecommunication and biomedical. Specialized in

diagnostic equipment (MDI), rehabilitation, health and

wellness (RGMD), biomedical equipment (OMS Ratto,

Lorenz Lifetech), complex electromechanical products

(Esacontrol)

WHY INVEST

TRANSACTION PROPOSED

• STRENGTHS: the company has solid fundamentals (though

it faced a management/financial crisis); this asset could be a

strong entry point for a new investor in this sector; specialized

workforce;

• POTENTIAL MARKETS: current buyers include Alcatel

Lucent, Esaote, Centervue, Framos, Ami Italia, Elt, Selex ES,

Elman, Telco, Micro TLC, Bitron

• CHALLENGES: companies in this sector face high price

(labour costs) and non-price competition (technological

innovation). Demand for these products is sustained but BTP

Tecno lost an important customer (Alcatel Lucent). The

company needs to regain market shares through a new

management and new investments in technology innovation.

• The Company is looking for an Industrial investor

• Company acquisition

• PUBLIC INCENTIVES: national and local government

may provide support for a plant reconversion

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 77 ~ 104 ~ 52

EBITDA ~ 3.4 ~5 ~ 4.2

Employees 102

Net Financial Position ~ 5 ~ 9.8 ~ 7.7

Euro Mln, Number

24

COMPANY OVERVIEW

COMPANY 37 - FASHION INDUSTRY

MARKETS & COMPANY STRUCTURE

• The company is part of a group of companies specialized

in Technical high-end sportswear jacket.

• The company brand was founded in 2002 inspired by

mountains with the mission to review a practical and

versatile timeless sportswear concept: a mix between

high quality and technique.

• Starting from the jacket, a total look wardrobe was

developed since foundation the company collection

includes men, women and child.

• Besides the usual Spring/Summer and Autumn/Winter

collections, the company also produces capsule

collections driven by design content.

• Sales channel are wholesale and retail.

• Recently the shareholders of the group controlling the

company have reshuffled the group’s governance and

nowadays the company is a new legal entity with a single

brand and a single business model.

M&A

OPPORTUNITIES

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• Major interest are for Asian potential investors and for the

support to international expansion.

• The owner is available to a minority investment 2010 2011 2012

TURNOVER 99.4 108.0 83.4

EBITDA 20.4 22.8 11.5

Euro Mln

25

COMPANY 46 - FASHION INDUSTRY M&A

OPPORTUNITIES

COMPANY OVERVIEW

• Founded in the seventies the company is specialized in

the frozen fish food sector, and operated in all phases

of the value chain, starting from the fishing to retail

distribution.

• 90% of the revenues comes from the core business- fish

food, the remaining part from meat and vegetables frozen

food.

• The storage capacity of the company is based in 13

logistics hubs (9 of which are owned by the company),

allowing the company to cover the the entire country.

The company sales channel is composed by:

• Direct operated stores (that represent the 35-40 % of total

revenues)

• Wholesalers (60-65%)

• Outlet channel (5%)

• The expected growth rate for the next years is estimated

around 5-10%

• The owners want to sell the existing share, around 40%.

• Amount of the investment: less than 100 mln. Euro.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

2010 2011 2012

TURNOVER 83 98 105

EBITDA 7.3 9.5 11.5

Euro Mln

26

COMPANY 1 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Group was founded in 1958 in a small workshop in San Mauro Pascoli, where the founding family created the first collection of sandals designed for tourists holidaying on the Italian Riviera

• Its shoes are designed as must-have objects of desire, never as solely designer label accessories, but as true masterpieces of design.

• In the recent year, the business boasts a growth rate of + 20% per year, with 16 flagship stores, a new showroom in New York, the opening of corners and shop-in shops in Russia as well as expansion towards China and the Middle East.

FINANCIAL HIGHLIGHTS NOTE

• The company is open to selling a stake to outside

investors.

Shoes collection

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 25,9 33,6 35,7 36,1

EBITDA 1,7 2,7 4,7 3,6

EBITDA margin 6,4% 8,1% 13,1% 10,0%

Net Profit 0,4 0,9 2,5 1,5

Fixed Assets 9,3 9,8 10,3 10,6

NFP 5,2 4,8 3,8 4,8

Shareholder's funds 6,5 7,4 9,6 10,5

27

COMPANY 2 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• Established in 1952 by an Italian entrepreneur the

company is now held by his children and the third

generation of its family.

• The company is a leader in the luggage and travel bags

industry, with products recognized for their image and

functionality, with a positive quality/price ratio. Is known

also for its wallets and accessories.

• The company sells its products also in the emerging

markets; the Management plans to open ten more stores

in Asia and in Usa.

FINANCIAL HIGHLIGHTS NOTE

• The company is receptive to offers for minority stake

sale, strategic investors preferred, says executive.

Travel & accessories

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 34,9 37,6 37,4 33,6

EBITDA 1,4 2,3 0,9 0,9

EBITDA margin 4,1% 6,2% 2,3% 2,8%

Net Profit (0,2) 0,2 (0,8) (0,0)

Fixed Assets 9,9 9,6 9,4 9,6

NFP 15,3 16,1 16,4 13,4

Shareholder's funds 5,9 6,2 5,5 5,9

28

COMPANY 3 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Group was founded in the first half of the 1950s by an Italian entrepreneur who decided to open a small dressmaker’s shop for children in Marche region.

• Today, the Group is a leading company in the children fine clothing market. Their focused orientation towards new ideas and technology is the true driving force of their development.

• In 2010 the Group started its partnership with an international fashion company for the design, the production and distribution of its kids and baby collection.

• In the coming months, the company plans to open ten branded concessions and shop-in-shops. The Group aims to expand in the Asia market.

FINANCIAL HIGHLIGHTS NOTE

• The company is looking for a suitable bidder interested in

investing in the company - General Manager said.

Collections

M&A

OPPORTUNITIES

28

Key financial data (€/m) 2011 2012 2013 2014

Revenues 39,9 42,6 42,4 45,6

EBITDA 2,1 2,0 2,3 2,9

EBITDA margin 5,3% 4,7% 5,3% 6,3%

Net Profit 5,1 4,8 6,9 7,4

Fixed Assets 5,1 5,5 7,3 8,1

NFP 19,6 18,9 15,8 15,9

Shareholder's funds 5,1 4,8 6,9 7,4

29

COMPANY 4 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company is one of the main Italian players in women

apparel and accessories.

• The Company produces and distributes its products under

its brand, mainly through its proprietary (franchising) retail

distribution network.

• In September 2013, the company has a network of 158

shops in Italy (out of which 63 DOS) 199 shops in Europe

(out of which 103 DOS) and 48 shops in the rest of the

world (out of which 2 DOS).

• In October 2010 it has sold its 50% interest in a fashion

group.

FINANCIAL HIGHLIGHTS NOTE

• According to our intelligence, the company has

restructuring plans and the option to go to market.

Apparel

M&A

OPPORTUNITIES

Knitwear & Cachemere

Leather Goods Accessories

Key financial data (€/m) 2011 2012 2013 2014

Revenues 193,6 186,6 168,5 155,9

EBITDA (21,4) (3,2) (8,7) 0,4

EBITDA margin n.m. n.m. n.m. 0,2%

Net Profit 14,6 (20,1) (23,8) (7,7)

Fixed Assets 90,7 76,7 63,9 55,0

NFP 37,5 68,0 76,5 74,0

Shareholder's funds 65,9 44,9 19,0 10,8

30

COMPANY 5 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• Founded in 1977, the company is an Italian fashion

group, owned by the two founding families,

• The company owns several brands. China, South Est

Asia and the US are the main areas of interest to start

a series of partnership deals, in order to better penetrate

international markets.

• Today, its brands are sold in about 800 retail locations.

The most famous brand is present in 324 select multi

brand stores and 45 mono brand boutiques/ shop- in-

shops worldwide.

FINANCIAL HIGHLIGHTS NOTE

• The management would be interested in offers for a

minority stake - the founder said.

Collections

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 54,1 63,2 61,1 66,5

EBITDA 5,7 12,7 11,7 14,3

EBITDA margin 10,5% 20,0% 19,1% 21,5%

Net Profit 1,7 5,5 6,6 4,0

Fixed Assets 30,1 29,4 29,0 45,5

NFP (0,7) (7,6) (13,3) (2,6)

Shareholder's funds 58,9 62,8 69,5 73,1

31

COMPANY 6 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Group founded in 1996, is an Italian women’s apparel

manufacturer.

• The Group is headquartered in a small city close to

Naples. The Group is specialized in producing girl’s

clothing. The company has 21 stores across Italy. It is

currently focused in strengthening its retail network within

Europe and the Middle East, particularly in the UAE.

• The Group is going to open its second flagship store in

Milan by the end of the year.

FINANCIAL HIGHLIGHTS NOTE

• The Group has already received two bids from parties

interested in investing in the company. The management

is keen on receiving offers for a 60% stake sale.

Collections

M&A

OPPORTUNITIES

Key financial data (€/m) 2011 2012 2013 2014

Revenues 32,9 39,1 47,6 49,4

EBITDA 2,4 2,9 5,2 7,9

EBITDA margin 7,4% 7,5% 10,8% 16,0%

Net Profit 1,1 1,5 3,0 4,7

Fixed Assets 2,3 2,1 1,9 1,5

NFP (2,7) (3,1) (2,2) (4,4)

Shareholder's funds 6,4 7,9 10,6 13,7

32

COMPANY 7 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company was founded in 1921 but expanded into the

sportswear business after 1970.

• Its brand gained an image of elegant apparel for sailing,

golfing and outdoor situations.

• Nowadays, it offers a total-look, luxury range of: apparel;

accessories, travelling goods and technical products for

sailing, golf and skiing.

• Current products include men, women, cadet and

accessories collections which are sold in more than 200

international single-brand stores in every continent.

FINANCIAL HIGHLIGHTS NOTE

• no recent news.

Menswear

M&A

OPPORTUNITIES

Womenswear Accessories

Key financial data (€/m) 2009 2010 2011 2012

Revenues 145.9 152.1 170.7 n.a.

EBITDA 44.2 45.9 46.1 n.a.

EBITDA margin 30.3% 30.2% 27.0% n.a.

Net Profit 28.9 30.5 30.2 n.a.

Fixed Assets 28.9 36.9 41.9 n.a.

NFP (106.8) (110.6) (42.4) n.a.

Shareholder's funds 195.0 212.2 206.2 n.a.

33

COMPANY 8 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company founded in 1971 in Bologna, is a leading

producer of active sportswear.

• The Company operates in three business area:

teamwear, merchandising and leisurewear for football,

basket, rugby, volley, running, handball and baseball.

• It operates through three subsidiaries: two commercial

stores in Bologna and Monza and a company in China

and distributes its products through mono - brand stores

located in Central Europe, Turkey and Canada.

• In 2011, a PE fund has acquired a majority stake (50,1%)

in the company for € 23m.

FINANCIAL HIGHLIGHTS NOTE

• The Company is interested in acquisitions in Germany

and Eastern Europe in order to shorten the time to market

in those countries where it is not yet present.

• The Company may look to an investor to enter in these

markets.

M&A

OPPORTUNITIES

Teamwear Merchandising Leisurewear

Key financial data (€/m) 2011 2012 2013 2014

Revenues 52,3 60,0 62,2 64,2

EBITDA 3,5 4,1 5,7 6,8

EBITDA margin 6,7% 6,8% 9,2% 10,6%

Net Profit 1,1 1,7 2,0 2,6

Fixed Assets 1,9 2,1 2,8 4,4

NFP 18,5 19,3 14,9 19,4

Shareholder's funds 15,6 17,3 19,3 21,9

34

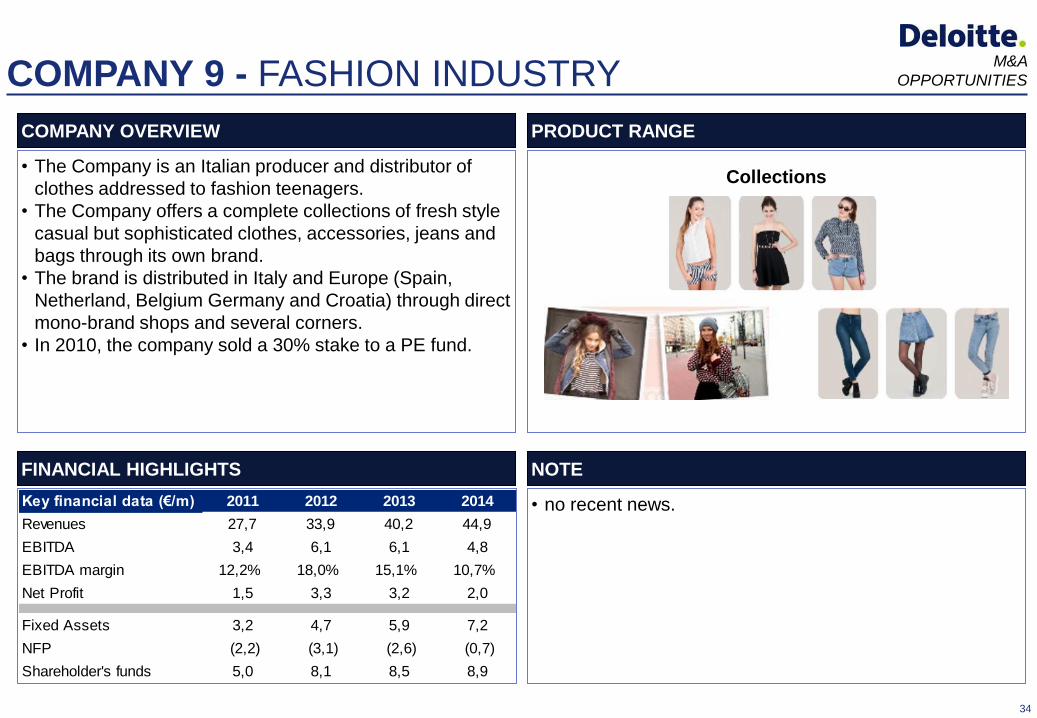

COMPANY 9 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company is an Italian producer and distributor of

clothes addressed to fashion teenagers.

• The Company offers a complete collections of fresh style

casual but sophisticated clothes, accessories, jeans and

bags through its own brand.

• The brand is distributed in Italy and Europe (Spain,

Netherland, Belgium Germany and Croatia) through direct

mono-brand shops and several corners.

• In 2010, the company sold a 30% stake to a PE fund.

FINANCIAL HIGHLIGHTS NOTE

• no recent news.

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2011 2012 2013 2014

Revenues 27,7 33,9 40,2 44,9

EBITDA 3,4 6,1 6,1 4,8

EBITDA margin 12,2% 18,0% 15,1% 10,7%

Net Profit 1,5 3,3 3,2 2,0

Fixed Assets 3,2 4,7 5,9 7,2

NFP (2,2) (3,1) (2,6) (0,7)

Shareholder's funds 5,0 8,1 8,5 8,9

35

COMPANY 10 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company is an Italian producer and distributor of

fashion clothes. The company was founded in the 40’s as

a tailored clothes shop.

• The Company offers a complete collection of elegant

men’s and women’s knitwear including: suits, shirts and

pants, dresses and accessories.

• The brand is distributed worldwide in Europe, USA and

Japan; wholesale is the favorite retailing channel, as well

as for well-known multi-brand stores (like Barneys and

Berdgorf in NYC).

• In 2013, the Company was fully acquired by a PE Fund.

FINANCIAL HIGHLIGHTS NOTE

• no recent news.

M&A

OPPORTUNITIES

Key financial data (€/m) 2011 2012 2013 2014

Revenues - - 23,2 24,0

EBITDA - - (2,8) 1,0

EBITDA margin - - n.m. 4,1%

Net Profit - - (3,1) (0,5)

Fixed Assets - - (3,1) (0,5)

NFP - - 21,3 14,0

Shareholder's funds - - 9,1 21,3

Menswear Womenswear Accessories

36

COMPANY 11 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company is an Italian fashion group established in

1982 in Bologna

• The creator of the Company was aimed at building a

sportswear brand designed to become a symbol of

extreme research on fibres and textiles, applied to an

innovative design.

• Under the Brand the Company manufactures and

distributes menswear and womenswear apparel,

accessories and kidswear.

FINANCIAL HIGHLIGHTS NOTE

• The Company sale process called off (January 2014)

• According to our intelligence, the Company is looking for

an investor.

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2011 2012 2013 2014F

Revenues 53,7 62,0 69,8 79,5

EBITDA 3,9 5,8 9,6 11,8

EBITDA margin 7,3% 9,4% 13,8% 14,8%

Net Profit 1,5 1,9 5,3 n.a.

Fixed Assets 11,7 10,6 18,0 n.a.

NFP 7,6 7,9 13,4 n.a.

Shareholder's funds 29,9 31,0 33,9 n.a.

37

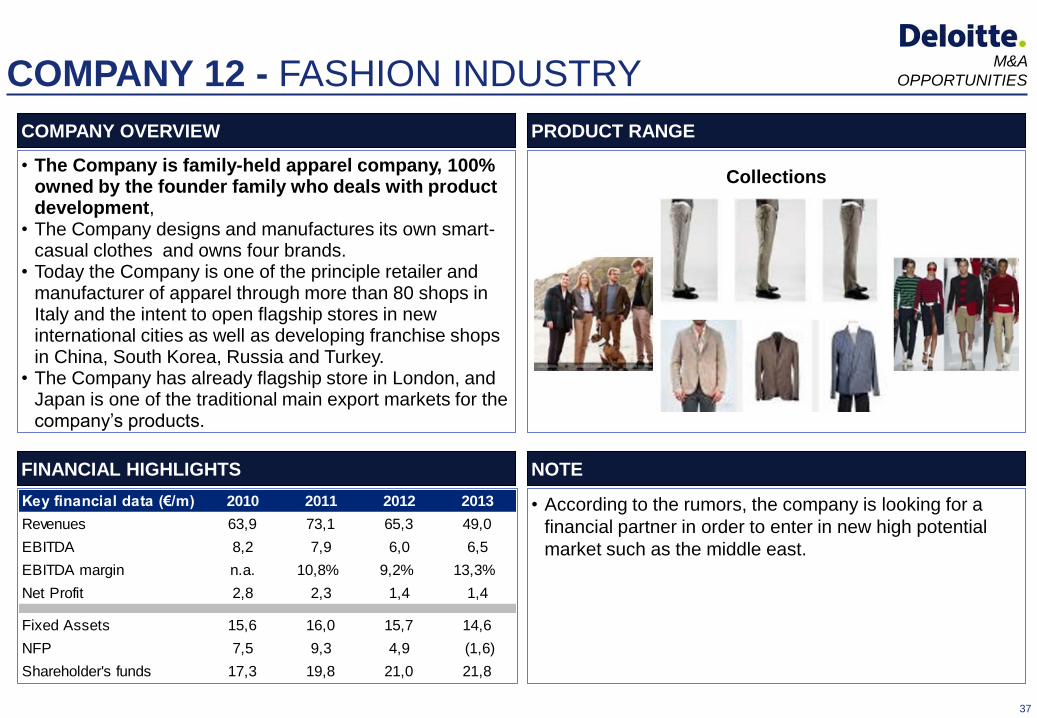

COMPANY 12 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company is family-held apparel company, 100% owned by the founder family who deals with product development,

• The Company designs and manufactures its own smart-casual clothes and owns four brands.

• Today the Company is one of the principle retailer and manufacturer of apparel through more than 80 shops in Italy and the intent to open flagship stores in new international cities as well as developing franchise shops in China, South Korea, Russia and Turkey.

• The Company has already flagship store in London, and Japan is one of the traditional main export markets for the company’s products.

FINANCIAL HIGHLIGHTS NOTE

• According to the rumors, the company is looking for a

financial partner in order to enter in new high potential

market such as the middle east.

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2010 2011 2012 2013

Revenues 63,9 73,1 65,3 49,0

EBITDA 8,2 7,9 6,0 6,5

EBITDA margin n.a. 10,8% 9,2% 13,3%

Net Profit 2,8 2,3 1,4 1,4

Fixed Assets 15,6 16,0 15,7 14,6

NFP 7,5 9,3 4,9 (1,6)

Shareholder's funds 17,3 19,8 21,0 21,8

38

COMPANY 13 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company was established in 1939 in the province of Milan.

• The Company distributes its products under its well known brand and thanks to its know - how in shirt manufacturing it produces for several important brands and designer worldwide.

• Today the company produces womenswear, menswear and accessories that are distributed all over the world thanks to its flagship stores and the wholesale distribution channel.

FINANCIAL HIGHLIGHTS NOTE

• no recent news.

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 30,5 34,7 35,4 31,2

EBITDA 0,3 0,7 1,7 1,6

EBITDA margin n.a. n.a. 4,7% 5,0%

Net Profit (0,5) (0,2) 0,1 (0,1)

Fixed Assets 19,2 19,6 19,8 19,5

NFP 12,2 n.a. 5,5 7,3

Shareholder's funds 15,9 15,7 15,8 15,7

Menswear Womenswear Accessories

39

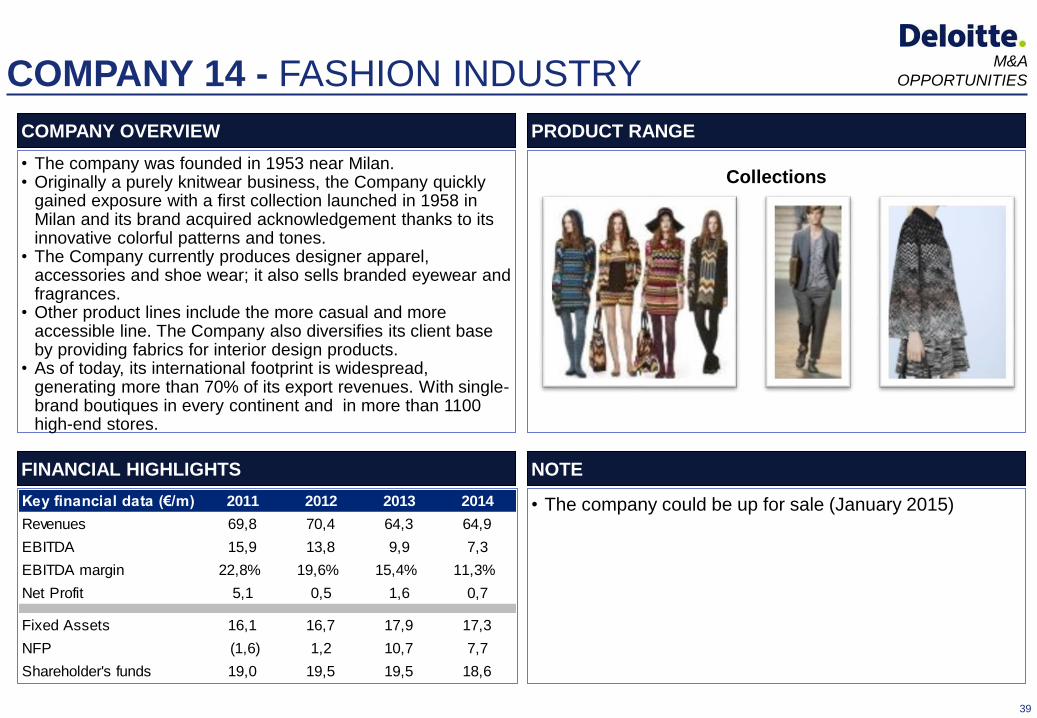

COMPANY 14 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The company was founded in 1953 near Milan. • Originally a purely knitwear business, the Company quickly

gained exposure with a first collection launched in 1958 in Milan and its brand acquired acknowledgement thanks to its innovative colorful patterns and tones.

• The Company currently produces designer apparel, accessories and shoe wear; it also sells branded eyewear and fragrances.

• Other product lines include the more casual and more accessible line. The Company also diversifies its client base by providing fabrics for interior design products.

• As of today, its international footprint is widespread, generating more than 70% of its export revenues. With single-brand boutiques in every continent and in more than 1100 high-end stores.

FINANCIAL HIGHLIGHTS NOTE

• The company could be up for sale (January 2015)

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2011 2012 2013 2014

Revenues 69,8 70,4 64,3 64,9

EBITDA 15,9 13,8 9,9 7,3

EBITDA margin 22,8% 19,6% 15,4% 11,3%

Net Profit 5,1 0,5 1,6 0,7

Fixed Assets 16,1 16,7 17,9 17,3

NFP (1,6) 1,2 10,7 7,7

Shareholder's funds 19,0 19,5 19,5 18,6

40

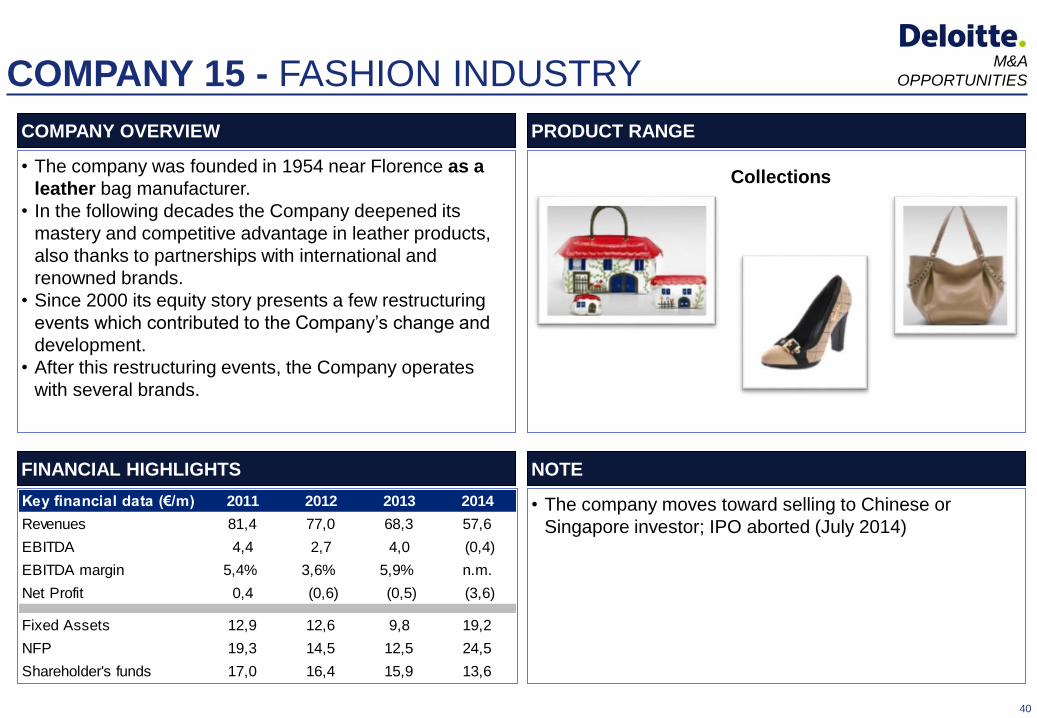

COMPANY 15 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The company was founded in 1954 near Florence as a

leather bag manufacturer.

• In the following decades the Company deepened its

mastery and competitive advantage in leather products,

also thanks to partnerships with international and

renowned brands.

• Since 2000 its equity story presents a few restructuring

events which contributed to the Company’s change and

development.

• After this restructuring events, the Company operates

with several brands.

FINANCIAL HIGHLIGHTS NOTE

• The company moves toward selling to Chinese or

Singapore investor; IPO aborted (July 2014)

M&A

OPPORTUNITIES

Key financial data (€/m) 2011 2012 2013 2014

Revenues 81,4 77,0 68,3 57,6

EBITDA 4,4 2,7 4,0 (0,4)

EBITDA margin 5,4% 3,6% 5,9% n.m.

Net Profit 0,4 (0,6) (0,5) (3,6)

Fixed Assets 12,9 12,6 9,8 19,2

NFP 19,3 14,5 12,5 24,5

Shareholder's funds 17,0 16,4 15,9 13,6

Collections

41

COMPANY 16 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The company was founded in 1923 in Monza, began producing felt hats, later moving on to gaiters and workwear.

• The products range includes sky collection, as jackets, pants, topwear and accessories for men, women and kids and also a golf collection, that includes polo, gilet, jackets and pants.

• The company is going to introduce also beachwear collection.

• The company sells its products through 7 boutiques in Italian alps and two shops in Seoul, and also through sportswear and casualwear shops.

• The company is fully owned by the founder Family.

FINANCIAL HIGHLIGHTS NOTE

• The company could consider acquisitions of fashion

jacket producers (January 2015).

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 48,0 52,8 64,2 82,4

EBITDA 3,0 2,9 7,9 12,3

EBITDA margin 6,4% 5,5% 12,3% 14,9%

Net Profit 0,7 0,7 2,6 6,3

Fixed Assets 21,7 19,8 18,7 18,8

NFP (9,7) (13,1) (14,4) (8,2)

Shareholder's funds 77,1 77,4 79,5 85,0

Collections

42

COMPANY 17 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Group is a leading player in the international

wintersport and outdoor market.

• The Group was established in 2003 through the

acquisition of several brands; the other strategic

acquisitions were made aiming at building a leading group

for sports equipment and apparel.

• The Groups brands include winter and outdoor sports

goods: ski-boots, winter footwear and equipment, ski, ski-

boots and accessories, winter footwear and accessories,

shoes and equipment for alpinism, backpacking, outdoor

fitness, trekking, hunting ice skates ski and outdoor

shoes, winter equipment roller skate and accessories.

FINANCIAL HIGHLIGHTS NOTE

• The Company recently sold one of its brands.

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2010 2011 2012 2013

Revenues 394,7 404,4 335,2 325,7

EBITDA 36,2 35,1 16,3 17,4

EBITDA margin 9,2% 8,7% 4,9% 5,3%

Net Profit 2,8 0,9 (15,9) (21,2)

Fixed Assets 100,0 95,0 87,5 79,9

NFP 177,5 194,8 184,2 171,8

Shareholder's funds 69,6 69,3 49,1 25,2

43

COMPANY 18 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• Established in 1978, the Company is a private held Italian

menswear producer headquartered in a small city in the

middle of Italy.

• The Company produces 1500 items of clothing every day

thanks to 900 employees both internal and external. The

result is that the brand is now recognized as a brand of

“Made in Italy” excellence.

• In its collections, the experience of the Italian sartorial

tradition is combined with the innovation, research and

experimentation

• On April 2014, its new enlarged showroom was opened in

Milano, in the heart of the fashion quarter.

FINANCIAL HIGHLIGHTS NOTE

• Starting from 2016, the management could take into

consideration potential bidders, but it needs to see a real

long term interest in sharing the company’s development

plan, said the CEO ( January 2015)

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2011 2012 2013 2014

Revenues 53,3 53,0 54,2 71,1

EBITDA 3,2 3,5 5,4 9,2

EBITDA margin 6,0% 6,6% 10,0% 13,0%

Net Profit 1,0 1,1 2,4 5,2

Fixed Assets 8,5 11,5 10,7 12,5

NFP 18,0 14,2 13,1 14,5

Shareholder's funds 5,3 8,1 10,2 14,1

44

COMPANY 19 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The Company is headquartered in Naples and has 130 employees, The brand is an international menswear brand, and it produces several collections including footwear, bags and leather accessories’ collections.

• Born in 2007 form the vision and talent of its founder, the Company stands immediately out for the ability to develop its own design language, conceived for a new generation of consumers.

• Nowadays the brand is distributed in 3200 multi- brand stores over 70 countries around the world and is sold in 70 mono-brand stores located in strategic areas of Europe, Asia and South America. Exports last year accounted for 65% of sales.

• The Company intends to open around 10-15 flagship stores this year (2015) in Germany, Belgium and Spain, the executive said.

FINANCIAL HIGHLIGHTS NOTE

• The company would take offers for up to a 49% stake, the

founder said, adding that he would prefer to maintain

some operational control over the business (January

2015)

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2011 2012 2013 2014

Revenues - - 74,8 76,1

EBITDA - - 9,1 7,0

EBITDA margin - - 12,2% 9,1%

Net Profit - - 3,7 3,0

Fixed Assets - - 7,9 11,1

NFP - - (5,3) (0,7)

Shareholder's funds - - 14,5 16,5

45

COMPANY 20 - FASHION INDUSTRY

COMPANY OVERVIEW PRODUCT RANGE

• The company is headquartered in Campi Bisenzio (FI), is a well-know player in the swimsuit industry.

• The brand was born in San Francisco producing a small line of nylon or cotton-nylon shorts especially designed for surfing

• In 1979 the Company holds the permanent license to produce in Europe and sale worldwide products branded in order to make its main product, the “boardshort”, successful also in Italy.

• The brand is basically addressed to young people that want to be ensured about wearing a quality product as well as a recognized brand. Thanks to several sponsorships and to communication strategies the company is leader in the Italian market. Moreover the brand is already globally spread, with its showroom in NYC, and the presence in multi-brand luxury stores in France, Spain, Greece and Italy.

• The company is fully owned by a Italian PE Fund

FINANCIAL HIGHLIGHTS NOTE

• No recent news

M&A

OPPORTUNITIES

Collections

Key financial data (€/m) 2011 2012 2013 2014

Revenues 23,8 22,3 20,2 20,5

EBITDA 4,9 3,4 3,6 3,8

EBITDA margin 20,4% 15,2% 17,6% 18,6%

Net Profit 0,1 (1,5) (2,9) (1,3)

Fixed Assets 28,8 27,9 27,5 25,3

NFP 22,4 22,2 19,0 18,3

Shareholder's funds 14,7 13,2 10,3 14,3

46

COMPANY P - FASHION INDUSTRY M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• The Company deals with licensed production and

distribution of clothing apparels.

• 11th largest producer in Italy.

Asset Profile

Production plants based in central Italy

WHY INVEST

TRANSACTION PROPOSED

• STRENGTHS: over 5 million of high-quality fashion items

are in storage and ready for immediate sale. High-quality

and producer well integrated in the global fashion supply

chain. The company supplies Versace, Polo Ralph

Lauren, Thierry Mugler, Tommy Hilfiger Collection etc.

• POTENTIAL MARKETS: current market share in Europe

is around 5%

• CHALLENGES: the company needs to improve its

responding capacity to market trends, and needs to

maximize operation efficiency by reducing inventories and

fixed costs

• The Company is looking for an Industrial investor

• Acquisition of the newco (under insolvency procedure)

• PUBLIC INCENTIVES: public support is available in the

form of economic incentives for investments in the so

called "Area di Crisi” (economic crisis area)

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 125 ~ 120 ~ 60

EBITDA (€ ‘000) ~ 2.6 ~ 1 ~ -77

Employees 600

Net Financial Position ~ 0.1 ~ 17 ~ 11

Euro Mln, Number

47

COMPANY Q - FLAT GLASS M&A

OPPORTUNITIES

COMPANY OVERVIEW

The Company

• The Company manufactures over 1,300 tons/day of float

glass (35% of all float glass in Italy). Glass for thermic and

acoustic isolation, design, solar control

• The Company is among the largest producers of flat glass

in Italy.

WHY INVEST

TRANSACTION PROPOSED

• STRENGTHS: high quality production lines: more than

300 millions euro have been invested in different

production lines over the last 10 years; direct

management of design, construction, start up and

production set up. Italy is worldwide acknowledged

leading producer of high quality glass

• POTENTIAL MARKETS: Europe and the world

(especially for the construction sector and transformation

industries)

• CHALLENGES: the company is undercapitalized and is

seeking a buyer/new partner for future development.

• The Company is looking for an Industrial investor

• Company/asset acquisition

FINANCIAL HIGHLIGHTS

2011 2012 2013

Turnover ~ 88 ~ 80 ~ 74

EBITDA ~ 16 ~ 2.2 ~ -3.5

Employees 195

Net Financial Position ~ 28 ~ 36 ~ 38

Euro Mln, Number

48

COMPANY 44 - FOOD AND BEVERAGE M&A

OPPORTUNITIES

COMPANY OVERVIEW

• The company is specialized in shoes production for

women. The same was founded in 1910 and operated

as a family company till 2001, when the majority of the

share capital was acquired. Over the years the company

has extended the product range from shoes

production, in particular for women, to handbags,

perfumes and eyewear. The price-quality positioning of

the product is in the mid-high range of luxury sectors. The

design, prototyping, quality control phases are operated in

house, instead the production is executed by Italian

suppliers.

The distribution channel is based on Horeca, GDO

sectors, shops channel, (150 directly operated) shop-in-

shop (106 directly operated) and wholesalers. The

suppliers are:

• 35%, joint-venture partners, from different countries:

Argentine, Chile, Morocco, Senegal, Thailand;

• 65% external companies.

• The 80% of the fish food supplied is prepared and freezed

by the suppliers, in the company plant, recently renewed.

• Major interest in selling the existing shares – 100%.

• Amount of the investment: around 100/150 mln. euro

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

2011 2012 2013

TURNOVER 220.0 203.8 179.9

EBITDA 10.3 8.6 10.5

Euro Mln

49

COMPANY 60 - FOOD AND BEVERAGE M&A

OPPORTUNITIES

COMPANY OVERVIEW

• The company creates and distributes Made in Italy

craftsmanship ice cream of high quality. The product will

be marketed by a multitude of economic operators and in

different locations (bars, restaurants, structures sports

and recreation, shopping centers, etc. ) .

• The company sells in the national market 100% of the

product.

• The ice cream sector does not suffer from the consumer

crisis and is the driving force in agribusiness field.

Household spending to buy Italian ice cream reached

2.026 billion euro in 2013 (1% a/a).

• The owner of the company wishes to ensure the business

continuity by selling quotes of the company.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

2012 2013 2014

TURNOVER 2,4 3,8 6,7

EBIT 0,4 0,7 1,4

Euro Mln

50

COMPANY 46 - FOOD AND BEVERAGE M&A

OPPORTUNITIES

COMPANY OVERVIEW

• Founded in the seventies the company is specialized in

the frozen fish food sector, and operated in all phases

of the value chain, starting from the fishing to retail

distribution.

• 90% of the revenues comes from the core business- fish

food, the remaining part from meat and vegetables frozen

food.

• The storage capacity of the company is based in 13

logistics hubs (9 of which are owned by the company),

allowing the company to cover the the entire country.

The company sales channel is composed by:

• Direct operated stores (that represent the 35-40 % of total

revenues)

• Wholesalers (60-65%)

• Outlet channel (5%)

• The expected growth rate for the next years is estimated

around 5-10%

• The owners want to sell the existing share, around 40%.

• Amount of the investment: less than 100 mln. Euro.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

2010 2011 2012

TURNOVER 83 98 105

EBITDA 7.3 9.5 11.5

Euro Mln

51

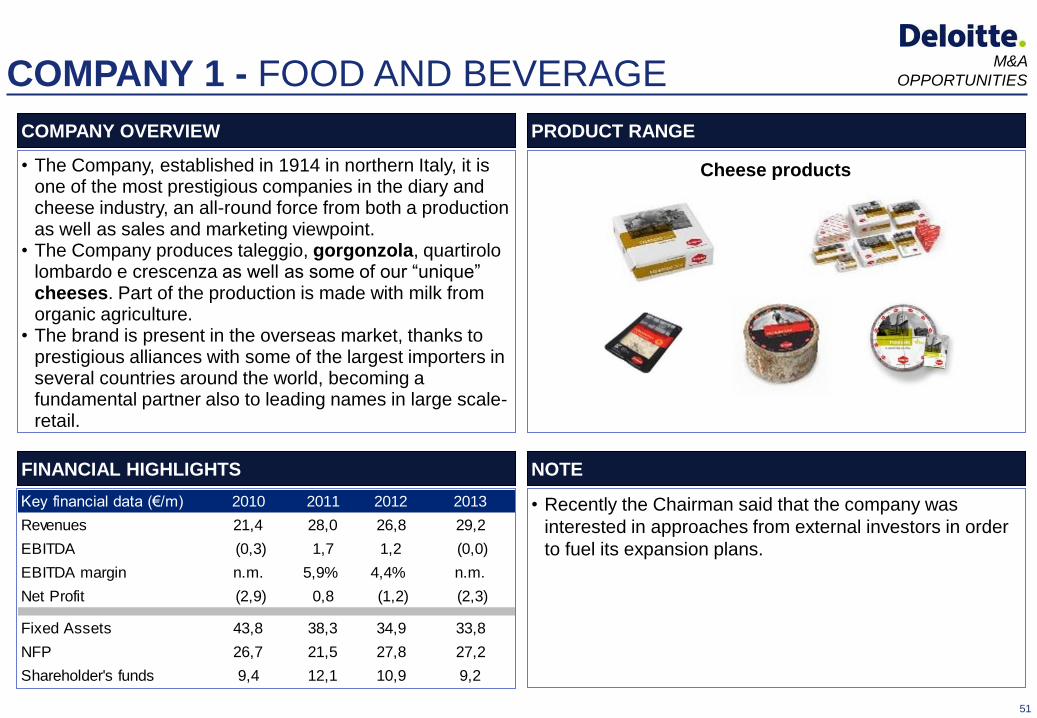

COMPANY 1 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company, established in 1914 in northern Italy, it is one of the most prestigious companies in the diary and cheese industry, an all-round force from both a production as well as sales and marketing viewpoint.

• The Company produces taleggio, gorgonzola, quartirolo lombardo e crescenza as well as some of our “unique” cheeses. Part of the production is made with milk from organic agriculture.

• The brand is present in the overseas market, thanks to prestigious alliances with some of the largest importers in several countries around the world, becoming a fundamental partner also to leading names in large scale-retail.

FINANCIAL HIGHLIGHTS NOTE

• Recently the Chairman said that the company was

interested in approaches from external investors in order

to fuel its expansion plans.

Cheese products

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 21,4 28,0 26,8 29,2

EBITDA (0,3) 1,7 1,2 (0,0)

EBITDA margin n.m. 5,9% 4,4% n.m.

Net Profit (2,9) 0,8 (1,2) (2,3)

Fixed Assets 43,8 38,3 34,9 33,8

NFP 26,7 21,5 27,8 27,2

Shareholder's funds 9,4 12,1 10,9 9,2

52

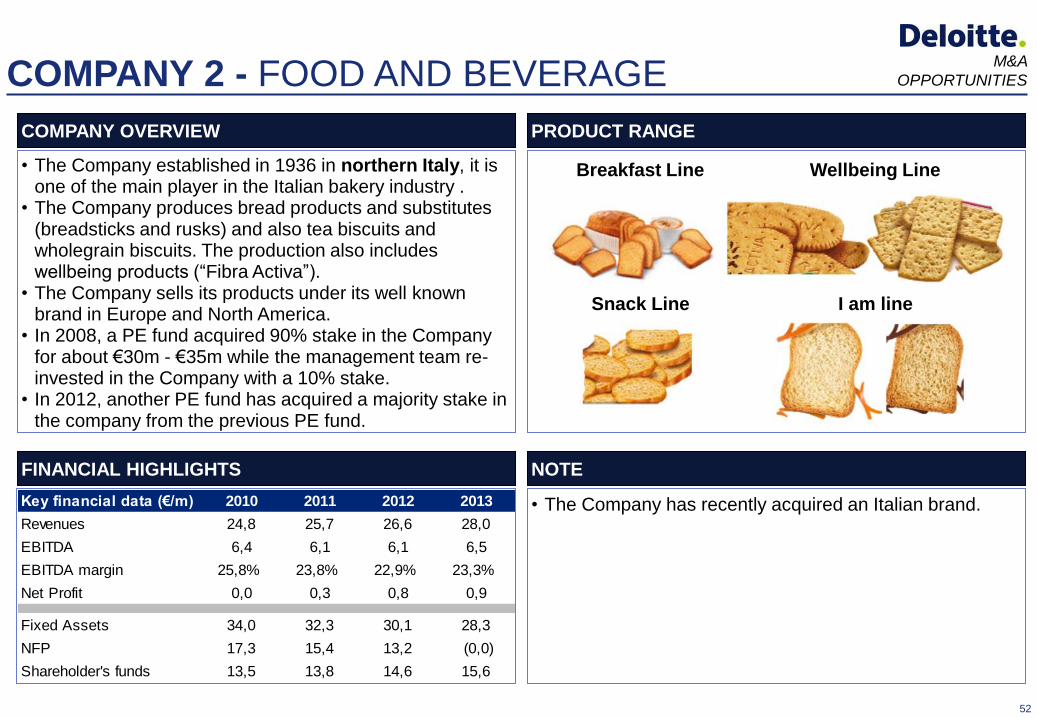

COMPANY 2 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company established in 1936 in northern Italy, it is one of the main player in the Italian bakery industry .

• The Company produces bread products and substitutes (breadsticks and rusks) and also tea biscuits and wholegrain biscuits. The production also includes wellbeing products (“Fibra Activa”).

• The Company sells its products under its well known brand in Europe and North America.

• In 2008, a PE fund acquired 90% stake in the Company for about €30m - €35m while the management team re-invested in the Company with a 10% stake.

• In 2012, another PE fund has acquired a majority stake in the company from the previous PE fund.

FINANCIAL HIGHLIGHTS NOTE

• The Company has recently acquired an Italian brand.

Wellbeing Line

M&A

OPPORTUNITIES

Breakfast Line

I am line Snack Line

Key financial data (€/m) 2010 2011 2012 2013

Revenues 24,8 25,7 26,6 28,0

EBITDA 6,4 6,1 6,1 6,5

EBITDA margin 25,8% 23,8% 22,9% 23,3%

Net Profit 0,0 0,3 0,8 0,9

Fixed Assets 34,0 32,3 30,1 28,3

NFP 17,3 15,4 13,2 (0,0)

Shareholder's funds 13,5 13,8 14,6 15,6

53

COMPANY 3 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company is a privately owned Italian producer of

vinegar, was founded in 1867 in northern Italy.

• The Company is a world leader in the production of

vinegar, pickles, vegetable preserves in oil, condiments

and ready-made sauces.

• The Company produces the balsamic vinegar of Modena

and is the result of a delighted blend between selected

grape musts and precious wine vinegar, followed by a

certified maturation period in different wooden core casks

• In 2008, the company acquired an organic producer

established in 1980 and located at the foot of the Alps

near Torino.

FINANCIAL HIGHLIGHTS NOTE

• The Company is receptive to approaches from interested

investors - Chairman said.

M&A

OPPORTUNITIES

• Balsamic vinegar of Modena

• Olives & Pickles

Key financial data (€/m) 2010 2011 2012 2013

Revenues 111,2 113,9 113,7 115,8

EBITDA 13,5 14,1 12,0 14,1

EBITDA margin 12,1% 12,4% 10,6% 12,1%

Net Profit 5,6 5,8 4,1 5,8

Fixed Assets 44,3 44,3 44,2 44,7

NFP 24,6 26,9 28,8 10,2

Shareholder's funds 53,2 54,5 58,6 58,5

54

COMPANY 4 - FOOD AND BEVERAGE

COMPANY OVERVIEW Product range

• The Company founded in 1960s, was originally focused

on the processing of tomatoes.

• The Company today offers frozen vegetables, grilled

vegetables, herbs, natural vegetables, potatoes, ready

side dish, steam precooked vegetables and semi- finished

products.

• The Company also offers frozen food service products

such as pizza as well as pasta and ready meals.

• In 2011, the company attempted a sale process. At that

time, the management has mandated an advisor to

handle the sale process, a source said.

FINANCIAL HIGHLIGHTS Note

• The Company has recently attracted the interest from

private equity firms.

M&A

OPPORTUNITIES

Key financial data (€/m) 2009 2010 2011 2012

Revenues 136,3 139,5 142,6 147,6

EBITDA 18,0 15,2 12,9 11,5

EBITDA margin 13,2% 10,9% 9,1% 7,8%

Net Profit 5,9 4,0 2,2 2,6

Fixed Assets 51,0 51,4 51,8 52,6

NFP (13,0) (11,6) (33,5) (16,8)

Shareholder's funds 97,0 100,9 100,9 103,5

Pasta & ready meal frozen

Vegetable frozen

55

COMPANY 5 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company established in 1925 in southern Italy, and

is wholly held by the founding family and is now managed

by the fourth generation.

• The Company, is an Italian based producer of tomatoes

sauce. From the field to the point of sale, the tomato is

grown, processed and packed, continuously trying to

diversify the range of products, in order to meet the needs

of any consumer.

• Exports accounted for 65% of sales pointing to the UK,

Germany, France; Libya, Nigeria, Ghana, Senegal; South

Africa and Kenya as its key markets.

FINANCIAL HIGHLIGHTS NOTE

• The Group wants to take an investor on board ahead of a

potential IPO.

M&A

OPPORTUNITIES

• Mashed tomatoes

• Chopped tomatoes

• Peeled tomatoes

• The delicacies

Key financial data (€/m) 2011 2012 2013 2014

Revenues 164,7 178,5 177,9 159,9

EBITDA 4,6 6,5 6,7 6,6

EBITDA margin 2,8% 3,6% 3,7% 4,1%

Net Profit (0,3) 0,5 0,3 0,1

Fixed Assets 28,6 29,7 32,2 31,1

NFP 47,5 49,9 48,4 36,6

Shareholder's funds 23,5 23,9 24,2 24,3

56

COMPANY 6 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company is an Italian company specialized in the production of frozen pizza

• In 2008 the founding family took over the company after the bankruptcy of the previous owner who had acquired years before the pizza division from a Group owned by another Italian food company.

• The Company sells its products to the private label market in Italy as well as in other European markets including UK, Germany, Denmark, Spain, Portugal and Hungary.

• In 2008 an Italian PE firm acquired a minority stake in the Company (33%); the majority stake (53%) is currently owned by the holding company 100% owned by the founding family.

FINANCIAL HIGHLIGHTS NOTE

• Unsourced report says the Company could be interested

in expanding its share of the pizza segment in Germany,

showing interest in a private German frozen pizza

company up to sale.

Pizzeria

M&A

OPPORTUNITIES

Snacks

Key financial data (€/m) 2011 2012 2013 2014

Revenues 47,6 49,4 56,1 78,4

EBITDA 0,3 3,3 2,9 4,5

EBITDA margin 0,6% 6,7% 5,2% 5,7%

Net Profit (1,3) 0,5 0,1 0,9

Fixed Assets 11,2 8,4 8,8 9,9

NFP 10,9 8,9 11,1 11,0

Shareholder's funds 3,7 4,2 4,3 5,3

57

COMPANY 7 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company is an Italian company specialized in the

production of frozen and fresh potatoes.

• The Company could look beyond its national borders and

offer the quality of its Italian-made products to the world.

Gnocchi were introduced for the first time to Asia,

especially Japan.

• The Group recently invested EUR 40m through a mix of

its own resources and bank debt to start the construction

of a new plant in the province of Bologna.

• The company has struck a deal with McDonald’s to

supply its 500 Italian restaurants with 2.000 tons of

products a year, equivalent to 10% of its output.

FINANCIAL HIGHLIGHTS NOTE

• The company welcomes strategic partnership or PE

investments to accelerate the company’s expansion in

overseas market, CEO said.

Potatoes product

M&A

OPPORTUNITIES

Key financial data (€/m) 2011 2012 2013 2014

Revenues 70,8 68,7 76,5 72,6

EBITDA 6,5 4,0 4,7 4,2

EBITDA margin 9,2% 5,8% 6,2% 5,8%

Net Profit 1,3 (0,1) 0,3 (0,0)

Fixed Assets 26,1 24,4 23,1 24,2

NFP 20,2 17,9 12,7 12,1

Shareholder's funds 18,4 18,2 18,5 18,7

58

COMPANY 8 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company is and Italian producer of bakery products

with a particular focus on the production of bakery

products typical of the Italian Veneto region.

• The Company is specialized in the production of a wide

variety of bread; in 2009 the company also acquired a

majority stake in an Italian player active in the market of

dry bread substitutes.

• In 2000 the company was partially acquired by an

international group but in 2006 it went back to the family

through an FBO operation backed by a Private equity

house active in Italy, which currently own a 25% stake.

FINANCIAL HIGHLIGHTS NOTE

• In 2012 a private equity fund has acquired a 55% stake in

the Company.

Bakery products

M&A

OPPORTUNITIES

Key financial data (€/m) 2008 2009 2010 2011

Revenues n.a. 49,0 49,7 53,8

EBITDA n.a. 9,6 9,9 8,5

EBITDA margin n.a. 19,6% 19,8% 15,8%

Net Profit n.a. 1,7 2,7 1,1

Fixed Assets n.a. 57,7 56,2 53,2

NFP n.a. 28,8 25,3 22,9

Shareholder's funds n.a. 25,0 27,6 28,7

59

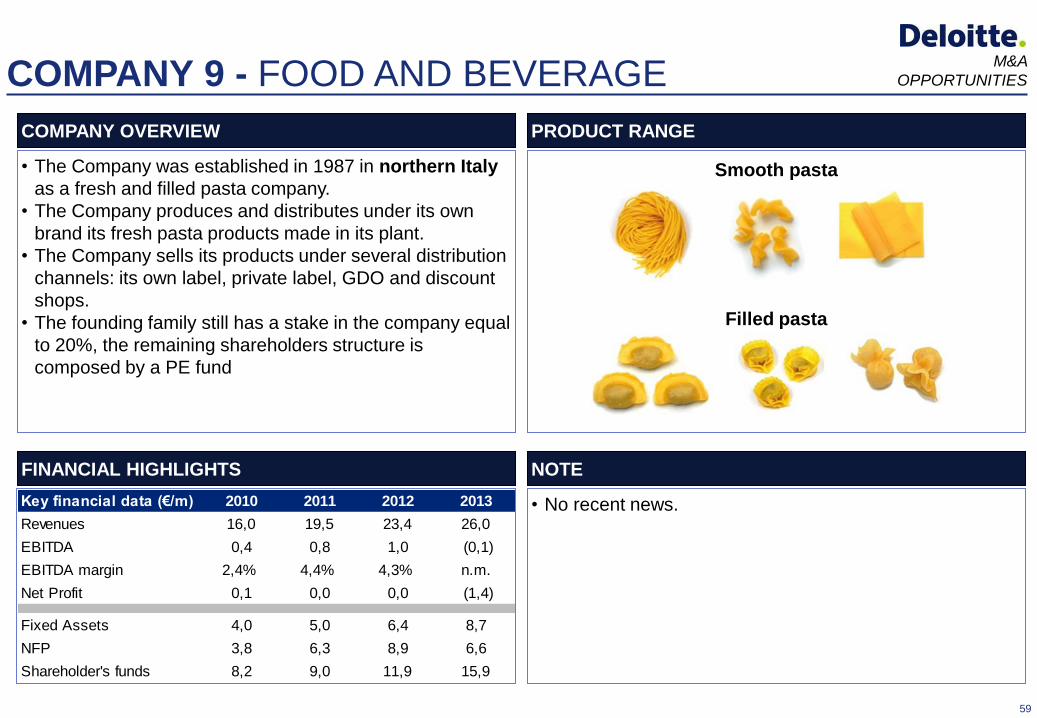

COMPANY 9 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company was established in 1987 in northern Italy

as a fresh and filled pasta company.

• The Company produces and distributes under its own

brand its fresh pasta products made in its plant.

• The Company sells its products under several distribution

channels: its own label, private label, GDO and discount

shops.

• The founding family still has a stake in the company equal

to 20%, the remaining shareholders structure is

composed by a PE fund

FINANCIAL HIGHLIGHTS NOTE

• No recent news.

Smooth pasta

M&A

OPPORTUNITIES

Filled pasta

Key financial data (€/m) 2010 2011 2012 2013

Revenues 16,0 19,5 23,4 26,0

EBITDA 0,4 0,8 1,0 (0,1)

EBITDA margin 2,4% 4,4% 4,3% n.m.

Net Profit 0,1 0,0 0,0 (1,4)

Fixed Assets 4,0 5,0 6,4 8,7

NFP 3,8 6,3 8,9 6,6

Shareholder's funds 8,2 9,0 11,9 15,9

60

COMPANY 10 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company established in 1990; it is Italy's premier

health food company providing an innovative product

ranges including: drinks, desserts, ice creams, soya

yoghurts, biscuits, veggie burgers and cutlets.

• The Company offers its products through four main

brands.

• The company is based in center of Italy, and distributes its

products across Europe including Austria, Germany,

Greece, Slovenia, Spain and Switzerland.

• In November 2011, the Company acquired an Italian jam

producer that today accounts for 32% of total revenues

FINANCIAL HIGHLIGHTS NOTE

• Recently, the Chairman said the company was interested

in buying niche companies in their respective markets.

M&A

OPPORTUNITIES

• Plant based drinks and yogurt

• Soya Ice cream and dessert

• Vegan and vegetarian meals

• Biscuits and snacks

Key financial data (€/m) 2011 2012 2013 2014

Revenues 57,0 93,3 100,4 114,0

EBITDA 5,9 9,8 12,8 18,0

EBITDA margin 10,3% 10,5% 12,7% 15,8%

Net Profit 2,6 4,5 6,9 10,3

Fixed Assets 34,3 36,2 34,2 34,3

NFP 18,8 11,4 n.a n.a

Shareholder's funds 24,2 27,0 35,6 44,3

Note: FY 2013, FY 2014 Consolidated Data; FY2011, FY2012 Unconsolidated Data

61

COMPANY 11 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company, founded in 1980, is based in northern

Italy.

• The Company is specialized in the production of

mozzarella cheese by lactic fermentation, and now it is a

fast-growing market leader and trusted partner for Private

Labels in large scale retail trade and dairy factories, both

in Italy and abroad.

• At the end of 2011, the company has been acquired by a

private equity firm.

FINANCIAL HIGHLIGHTS NOTE

• In 2013 a company controlled by it (80%) has acquired a

milk processing subsidiary of a Slovenian private wine

producer

Fresh Cheese

produced using selected lactic ferments

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues n.a. 56,9 n.a. 52,4

EBITDA n.a. 2,2 (0,1) 0,9

EBITDA margin n.a. 3,9% n.a. 1,8%

Net Profit n.a. 0,7 (0,3) (1,8)

Fixed Assets n.a. 4,5 16,8 20,2

NFP n.a. 5,8 4,1 6,4

Shareholder's funds n.a. 3,8 11,7 9,8

62

COMPANY 12 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company was established in 1968 in the Province of Pordenone; it is a leading company in the private label market, specialized in the fresh cheese processing products.

• The products offered by the Company are stracchino, mozzarella, mascarpone and cream cheese.

• Its products are available on the whole national territory and abroad in United Kingdom, Austria, Sweden and Spain.

• Amongst the Company’s clients are some of the major mass-market chains in Italy and Europe, such as: Trentina, Coop Italia, Despar, Conad, PAM, Centrale del Latte di Firenze, Granarolo, Caplac, Latte Busche, Abit etc.

FINANCIAL HIGHLIGHTS NOTE

• On 2012, a listed Swiss dairy group, has increased its

shareholding in these Italian fresh cheese company to

26% from 10%.

Mozzarella and stracchino

M&A

OPPORTUNITIES

Cream cheese and mascarpone

Key financial data (€/m) 2010 2011 2012 2013

Revenues 24,0 33,7 37,8 47,6

EBITDA 0,9 2,0 1,6 1,2

EBITDA margin 3,9% 6,0% 4,3% 2,6%

Net Profit 0,1 1,1 0,1 (0,5)

Fixed Assets 14,7 16,5 17,1 18,0

NFP 8,3 11,6 10,2 12,4

Shareholder's funds 3,1 4,3 4,6 4,6

63

COMPANY 13 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company is part of an Italian Group, one of the

Italian leading winery group, with a production of nearly

13 million bottles.

• The Company distributes wine under several brands/

labels.

• The Company operates through seven companies in the

south of Italy and several commercial outlets spread in 74

countries all over the world.

• In 2012, 45% of the Company’s revenues arises from the

production of DOC wine, while the IGT wine represents

43% of revenues.

FINANCIAL HIGHLIGHTS NOTE

• In 2013, an Italy based private equity fund, has acquired a

majority stake in the company

• Today the PE fund owns and controls the whole group.

Wine

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 26,4 30,0 34,9 38,4

EBITDA 4,5 4,7 3,9 4,4

EBITDA margin 17,0% 15,6% 11,2% 11,5%

Net Profit 2,5 2,7 1,7 0,0

Fixed Assets 5,4 5,0 4,8 6,8

NFP 4,0 5,4 5,6 8,9

Shareholder's funds 9,9 11,9 12,9 13,4

64

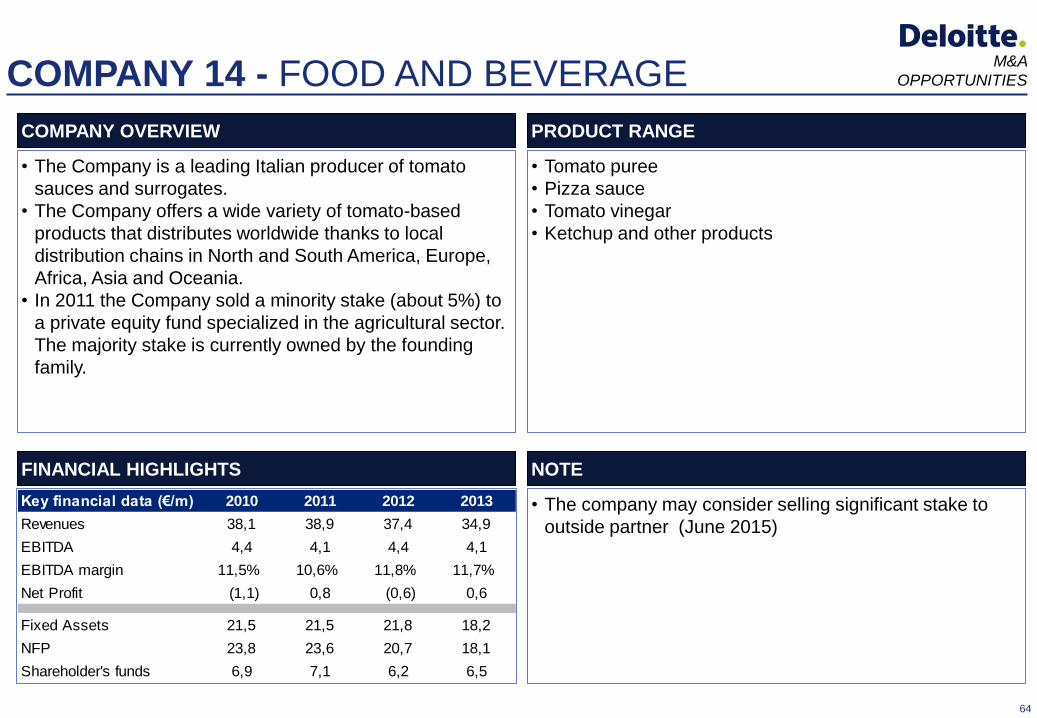

COMPANY 14 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company is a leading Italian producer of tomato

sauces and surrogates.

• The Company offers a wide variety of tomato-based

products that distributes worldwide thanks to local

distribution chains in North and South America, Europe,

Africa, Asia and Oceania.

• In 2011 the Company sold a minority stake (about 5%) to

a private equity fund specialized in the agricultural sector.

The majority stake is currently owned by the founding

family.

FINANCIAL HIGHLIGHTS NOTE

• The company may consider selling significant stake to

outside partner (June 2015)

M&A

OPPORTUNITIES

• Tomato puree

• Pizza sauce

• Tomato vinegar

• Ketchup and other products

Key financial data (€/m) 2010 2011 2012 2013

Revenues 38,1 38,9 37,4 34,9

EBITDA 4,4 4,1 4,4 4,1

EBITDA margin 11,5% 10,6% 11,8% 11,7%

Net Profit (1,1) 0,8 (0,6) 0,6

Fixed Assets 21,5 21,5 21,8 18,2

NFP 23,8 23,6 20,7 18,1

Shareholder's funds 6,9 7,1 6,2 6,5

65

COMPANY 15 - FOOD AND BEVERAGE

COMPANY OVERVIEW PRODUCT RANGE

• The Company was founded in the far-off 1800s in

Piemonte region, in the north of Italy, from the founder

that in 1878 opened its first own chocolate shop.

• Over the years, the artisan workshop turned into an

increasingly structured business and today, it produces

over 350 specialty chocolates, exporting them worldwide,

and since 2006, it has also included ice creams in its

range.

• The Company sells its products through several own

shops in main Italian cities, but also in Europe, Asia and

Latin America.

FINANCIAL HIGHLIGHTS NOTE

• no recent news

Chocolate and Candies

M&A

OPPORTUNITIES

Key financial data (€/m) 2010 2011 2012 2013

Revenues 31,4 36,6 39,2 39,7

EBITDA 7,2 8,8 9,1 9,8

EBITDA margin 23,1% 24,1% 23,1% 24,7%

Net Profit (0,3) 0,9 3,3 3,9

Fixed Assets 17,2 13,4 16,2 17,2

NFP 13,2 10,0 8,7 5,2

Shareholder's funds 12,9 13,8 17,1 20,1

66

COMPANY 6 - FOOD AND BEVERAGE M&A

OPPORTUNITIES

COMPANY OVERVIEW

• The company was established in 1988 and is the world's

third largest manufacturer of Modena balsamic Vinegar.

The company is based the center of Italy.

• The company is a market leader in Germany, Benelux

and the Scandinavian region. A company owns 60% while

the remainder is shared by the founding family each

holding a 13.3% stake.

• The company has mandated UBS to consider strategic

options, including the sale of Italian vinegar manufacturer.

• Non-binding offers have yet to be submitted but are

expected between the last week of February and the first

week of March.

• Two Spanish and one Turkish corporate, alongside

several private equity firms are among the interested

parties.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• Turnover 2013 €26.4m with EBITDA of EUR 3m

67

COMPANY 7 - FOOD AND BEVERAGE M&A

OPPORTUNITIES

COMPANY OVERVIEW

• The company is a

producer of licorice

candies. The company is

headquartered in a small

city of the northern part

of Calabria, southern

Italy.

• The company's management would like to talk with investors that can provide financial

resources and direct expertise in setting up retail chains. An ideal interlocutor would be a

private equity firm interested in sharing an industrial project. Specifically, the company will

consider approaches offering new business development projects adding that her family is

thinking of setting up its own retail or coffee chain. The management is interested in forging

alliances with distributors in the US and Australia, where consumers are very interested in

organic products. The United Arab Emirates were also mentioned as another region of

interest. The company has already distributed its products there, the chairman said,

pointing to the potential for growth on these markets. Ideal counterparts would be importers

specializing in the distribution of high-end Italian food.

MARKETS & COMPANY STRUCTURE

FINANCIAL HIGHLIGHTS TRANSACTION PROPOSED

• Revenues 2014 €5m,

with exports accounting

for 25% of overall sales,

pointing to Denmark,

Norway, Sweden and

Germany as key

markets.

• Recently, the company has started producing typical Neapolitan cookies, taralli, flavored

with licorice, in order to start product diversification ahead of the retail project. In the city,

where the company is based, the company has already opened its first coffee bar,

launching coffee and chocolate flavored with licorice. The management is considering

replicating this format in some Italian cities and also abroad. The company is a historical

Italian company; it was established in 1871 and is wholly owned by the founding family. It

produces four tons of licorice every three to four days. The whole family works for the

company, with the thirteenth generation now running the business.

68

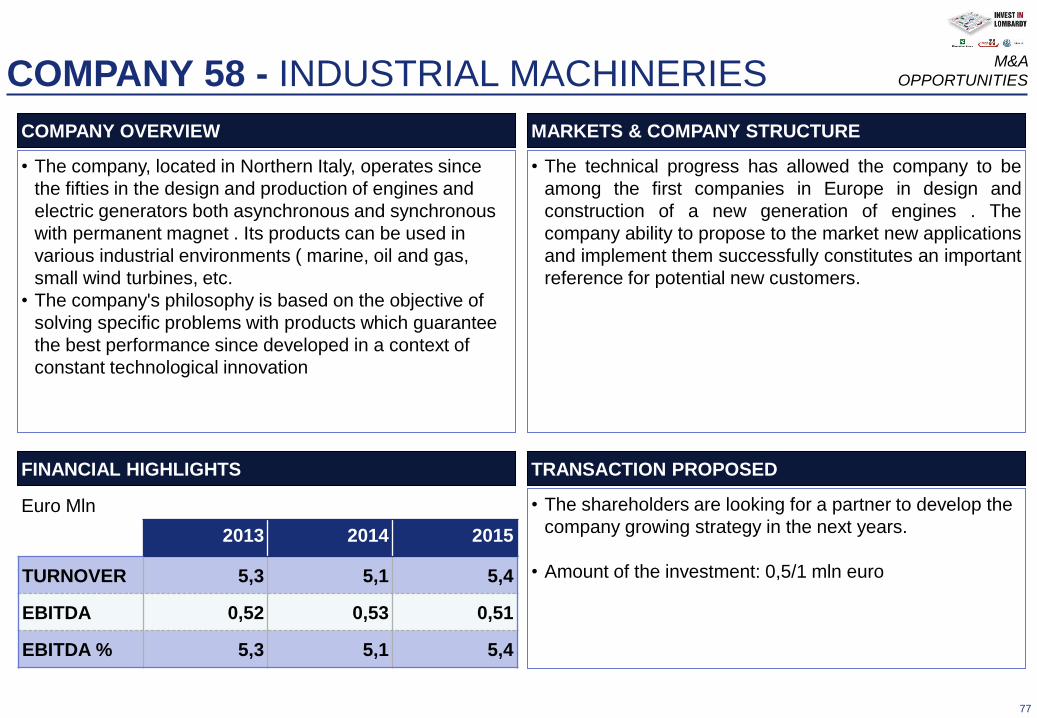

COMPANY 8 - FOOD AND BEVERAGE M&A

OPPORTUNITIES