Embed Size (px)

Citation preview

Investment Opportunities for Japanese Capital Securities

Toshiyasu OhashiMD & Head of Credit ResearchFixed Income, Currency and Commodities Research Dept.

November 2015

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1

1. Japanese Capital Securities

2. Increasing Investment Opportunities

3. Product Features of Different Capital Securities

4. Credit Valuation on Issuers

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

2

Summary

Japanese firms (banks, insurers, non-financial firms) watching for further utilization/issuance of capital securities

First, they will likely plan to issue yen-denominated bonds. However, issuance of USD-denominated bonds also expected in the case of (1) limited domestic demand and/or (2) overseas market being more attractive.

Attractiveness of Japanese capital securities— stable creditworthiness at issuers

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

33

1. Capital Securities: Method to Procure Regulatory Capital and Quasi Capital

Banks (financial holding companies)

(Tier2 securities) Basel III-compliant Tier 2 subordinated bonds: B3T2(Additional Tier1 securities) B3AT1 with debt claim

Non-financial firms Subordinated bonds with equity credit (quasi capital)Simple subordinated bonds (mezzanine fundraising)

Insurers (Subordinated bonds) Term debt/superlong/perpetual(Capital of mutual companies)Foundation fund bonds

Source: Compiled by Daiwa Securities.

1-1. Banks: Regulations on capital adequacy ratio (Basel Ⅲ)

1-2. Insurers: Solvency margin regulations

※Incl. securities firms’ ultimate parent companies (Daiwa Securities Group, Nomura Holdings).

1-3. Non-financial companies: Quasi capital, mezzanine fundraising

Assets

Common shares, etc.(CET1)

Additional Tier 1 securities

Subordinated bonds (Tier 2)

DepositsSenior debt

Regulated capital

Contingency reservesPrice fluctuation reserves

Common shares・foundation funds, etc.

Liability reserves

Subordinated bonds

Assets

Regulated capital

Common shares, etc

Senior debt

Subordinated bonds

Assets

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

4

2-1. Banks: Transition Period from Basel II to Basel III

Some banks (such as Mitsubishi UFJ Financial Group [MUFG] and Sumitomo Mitsui Trust Holdings [SMTH]) started to raise returns to shareholders via share buybacks Banks shifting capital policy from CET1 to AT1 & T2

Capital Adequacy Ratio at Japanese Major Financial Groups

Source: Financial Services Agency, company materials; compiled by Daiwa Securities.

AT1, 1.4 %AT1, 1.6 %

AT1, 1.7 % AT1, 1.2 %

Tier2, 3.0 %

Tier2, 3.9 %

Tier2, 3.1 %Tier2, 3.7 %

Tier 1 (e.g., common equity )

(CET1), 10.4 %

Tier 1(e.g., common equity )

(CET1), 9.7 %

Tier 1(e.g., common equity )

(CET1), 11.7 %

Tier 1 (e.g., common equity )

(CET1), 11.0 %Tier 1

(e.g., common equity )(CET1) 4.5 %

Capital conserv ation buffer

(CET1) 2.5 %

Additional Tier 1

(AT1), 1.5 %

Tier2 2.0 %

0.0

1.5

3.0

4.5

6.0

7.5

9.0

10.5

12.0

13.5

15.0

16.5

18.0

19.5

Basel Ⅲ MUFG SMFG Mizuho FG SMTH

(Minimum requirement lev el +capital conserv ation buffer)

End-Jun 2015

(%)

Required capital adequacy ratioudder full implementation

Based on transitional arrangements

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

5

Eligible Tier 2 Capital Instruments Subject to Transitional Arrangements, Issuance of B3T2

Eligible Tier 1 Capital Instruments Subject to Transitional Arrangements, Issuance of AT1

Source: Company materials; compiled by Daiwa Securities.

Eligible Tier 1/Tier 2 capital instruments subject to transitional arrangements to decline Replacement to B3AT1/B3T2 just started Market potential is significant (B3AT1:Y3~4tn, B3T2:Y4~5tn)

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

MUFG SMFG Mizuho FG SMTH

(Y bn) AT1

Inclusion of eligible Tier 1 capital instruments subject to transitional arrangements in AT1

Cap on inclusion of eligible Tier 1 capital instruments subject to transitional arrangements in AT1

0

500

1,000

1,500

2,000

2,500

3,000

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

End-FY12

End-FY13

End-3Q

FY13

End-FY14

End-1Q

FY15

End-2Q

FY15

End-3Q

FY15

End-FY15

MUFG SMFG Mizuho FG SMTH

(Y bn) B3T2 (eligible Tier 2)

Inclusion of eligible Tier 2 capital instruments subject to transitional arrangements in Tier 2

Cap on inclusion of eligible Tier 2 capital instruments subject to transitional arrangements in Tier 2

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

6

Strong needs for capital reinforcement due to growth-oriented policy, indicating significant scope to utilize capital securities Replacement demand for already issued capital securities anticipated

Procurement/redemption of Insurers’ Hybrid Debt

2-2. Insurers:Significant Scope to Utilize Capital Securities

Solvency Margin Components (end-Dec 2014)

933.8

917.3

1041.9

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Nippon Life Insurance Dai-ichi Life Insurance Meiji Yasuda Life Insurance

(Y bn)

840

860

880

900

920

940

960

980

1000

1020

1040

1060 (%)

Foundation funds, v arious reserv es Hy brid debt capital instrumentsNet unrealized gains on av ailable-for-sale securities (*90%) OthersSolv ency margin ratio (%)

981.0

1319.4

989.9

1176.0

639.0

775.5

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Sumitomo LifeInsurance

Daido Life Insurance Taiy o Life Insurance Fukoku Mutual LifeInsurance

Asahi Mutual LifeInsurance

Mitsui Life Insurance

0

200

400

600

800

1000

1200

1400(%)

Foundation funds, v arious reserv es Hy brid debt capital instruments

Net unrealized gains on av ailable-for-sale securities (*90%) OthersSolv ency margin ratio (%)

(Y bn)

Source: Company materials; compiled by Daiwa Securities.

Source: Compiled by Daiwa Securities.Note: Based on company disclosures.

▲ 600

▲ 400

▲ 200

0

200

400

600

FY2

004

FY2

005

FY2

006

FY2

007

FY2

008

FY2

009

FY2

010

FY2

011

FY2

012

FY2

013

FY2

014

FY2

015

FY2

016

FY2

017

FY2

018

FY2

019

FY2

020

FY2

021

FY2

022

FY2

023

FY2

024

(Y bn)

RdemptionIssuance

※Initial call date consdiered as redemption. Assuming Y120/US$ and Y130/€.

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

7

2-3. Non-financial Companies:Abenomics to Boost Utilization Third arrow of Abenomics requires ROE improvement at companies Adjustment to debt/capital structure (recapitalization) is financial strategy to improve ROE Some firms (e.g., Softbank) started to utilize subordinated bonds to improve debt structure

Utilization to adjust debt/capital structure (ROE improvement)

Utilization to improve debt structure (improvement in creditworthiness of senior debt )

Utilization of subordinated bonds with equity content

Utilization of subordinated bonds as mezzanine fundraising

While implementing share buybacks,

① Recapitalization via senior debt ② Recapitalization via CB ③Recapitalization via subordinated bonds(adjustment to debt/capital structure)

ROE should rise Rise in ROE Simple rise but CB conversion to shares No increase in real D/E ratio in ROE may lower ROE as some subordinated bonds

are assessed as equity content

Assets

Equity

Liabilities

Assets

Liabilities

Equity

Senior debt

Assets

Liabilities

Equity

CB

Assets

Liabilities

Equity

Subordinated bonds

Source: Compiled by Daiwa Securities.

Source: Compiled by Daiwa Securities.

Assets

Equity

LiabilitiesAssets

Equity

Subordinated bonds

Liabilities

Improvement inleveraged debtstructure

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

8

1.Bank capital securitiesB3AT1: Issuance of USD-denominated bonds yet to beginB3T2: Two USD-denominated bonds issued

Many USD-denominated B2-compliant capital securities issued

2. Insurer capital securitiesSome USD-denominated bonds issued

3. Non-financial companies’ capital securitiesIssuance of USD-denominated bonds yet to begin

USD-denominated Japanese Capital Securities

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

9

3. Product Features of Different Capital Securities

Comparison of Characteristics of Capital Securities

Source: Compiled by Daiwa Securities.Notes: 1) ◎, ○, △ denote attractive, reasonable, less attractive, respectively.

2) Above assessment based on my subjective opinion.

※In case ofinvestment by

financial institutionsProbability of redemption

Absolute value vs. product risk (vs. expected redemption date)

◎ ※Bullet type

○ ※ With call option

Banks: Additional Tier 1 capital instruments (B3AT1) ◎ △ △ △ △ △

Insurers: Subordinated bonds ○ ○ ○ ○ △ △

Insurers: Foundation fund bonds △ △ ○ ○ ○ △

△ ※With call option △ ※With call option

◎ ※Bullet type ◎ ※Bullet type

Market liquidity

◎

Interest rate Probability of interestpayment

○

Risk weighting

△

Non-financial firms: Subordinated bonds ○ ○ ◎

◎

△

Banks: Tier 2 capital instruments (B3T2) △

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1010

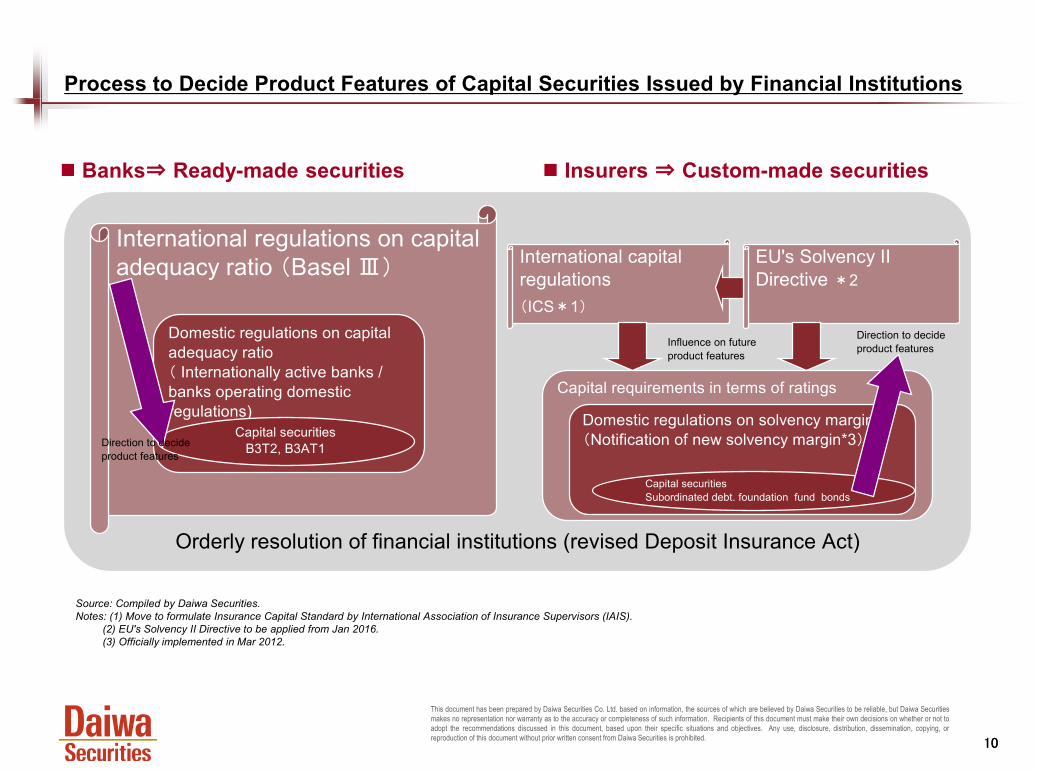

Process to Decide Product Features of Capital Securities Issued by Financial Institutions

Banks⇒ Ready-made securities Insurers ⇒ Custom-made securities

Source: Compiled by Daiwa Securities.Notes: (1) Move to formulate Insurance Capital Standard by International Association of Insurance Supervisors (IAIS).

(2) EU's Solvency II Directive to be applied from Jan 2016.(3) Officially implemented in Mar 2012.

Orderly resolution of financial institutions (revised Deposit Insurance Act)

International regulations on capitaladequacy ratio (Basel Ⅲ)

Domestic regulations on capitaladequacy ratio( Internationally active banks /banks operating domesticregulations)

Capital securitiesB3T2, B3AT1

International capitalregulations(ICS*1)

EU's Solvency IIDirective *2

Influence on futureproduct features

Capital requirements in terms of ratings

Domestic regulations on solvency margin(Notification of new solvency margin*3)

Capital securitiesSubordinated debt, foundation fund bonds

Direction to decideproduct features

Direction to decideproduct features

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1111

3-1. Capital Securities Issued by Banks

Source: Various materials; compiled by Daiwa Securities.Note: Bold letters indicate changes from requirements under Basel II.

Requirements for Tier2 Subordinated Bonds and Additional Tier 1 Capital Securities Under Basel III

Basel III-based requirements

Requirements for Capital Adequacy Ratio Under Full Implementation of Basel III

Source: Financial Services Agency; compiled by Daiwa Securities.Note: Countercyclical capital buffers and capital surcharge for G-SIBs not considered.

Common equity Tier 1 (CET1)4.5 %

Capital conservation buffer(CET1)

2.5 %

Additional Tier11.5 %

Tier22.0 %

0.0

1.5

3.0

4.5

6.0

7.5

9.0

10.5

12.0

Basel Ⅲ(Minimum requirement + Capital conservation buffer)

(%)Tier 2 securities

(B3T2)Additional Tier 1 securities

(B3AT1)Maturity date ・At least five years ・No maturity date (Perpetual)

Dividend/coupon ・To be paid, irrespective of credit conditions

・Full discretion for payment cancelation("Dividend pusher" clause prohibited)

・Non-cumulative・Within distributable amount

Premature redemption

Going-concern loss absorbency "Benefit of time" not lost in cases other thanbankruptcy/liquidation

・Principle reduction and conversion to commonstocks needed at trigger point (CET1 ratio of 5.125%

and above)

Loss absorbency at point of non-viability

Priority in payment of residual property ・Inferior to deposits and senior debt・Inferior to deposits, senior debt, and subordinated debt・Not included in debt under Bankruptcy Act's insolvencytest

・Approved from fifth year・However, special clauses that raise redemption probability (step-up interest rates) not approved

・Necessitates to maintain sufficient capital and prior approval by Financial Services Agency

・Necessitates clauses for principle reduction and conversion to common stocks at point of non-viability

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1212

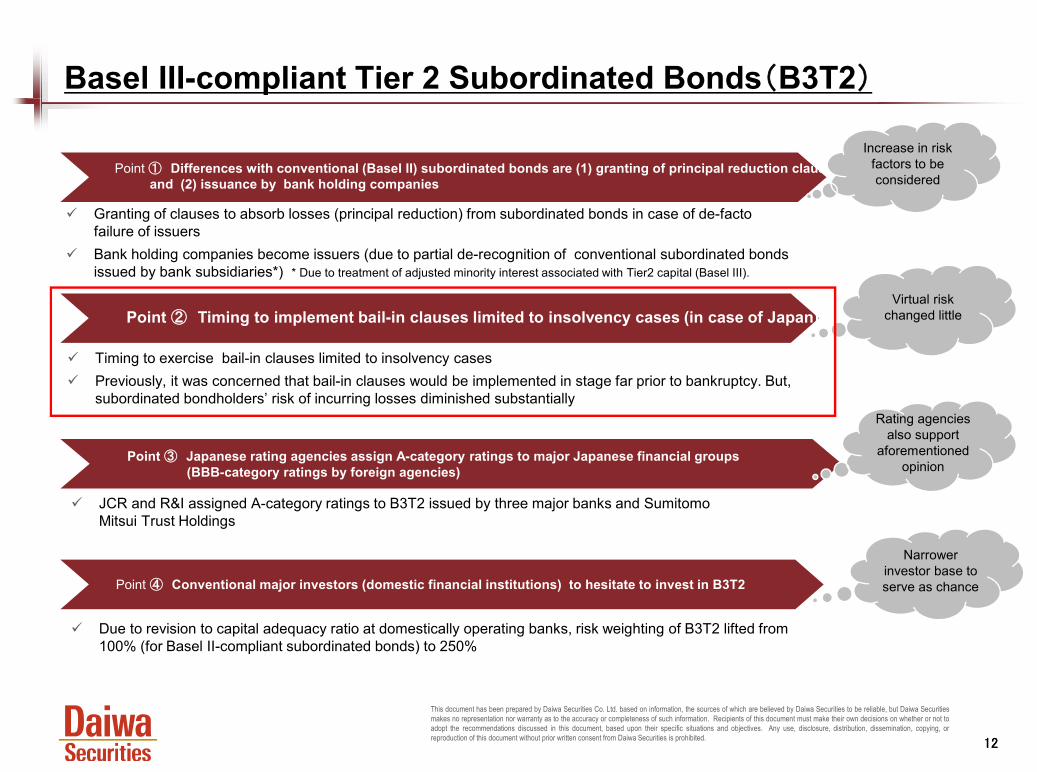

Basel III-compliant Tier 2 Subordinated Bonds(B3T2)

Timing to exercise bail-in clauses limited to insolvency cases Previously, it was concerned that bail-in clauses would be implemented in stage far prior to bankruptcy. But,

subordinated bondholders’ risk of incurring losses diminished substantially

Due to revision to capital adequacy ratio at domestically operating banks, risk weighting of B3T2 lifted from 100% (for Basel II-compliant subordinated bonds) to 250%

Granting of clauses to absorb losses (principal reduction) from subordinated bonds in case of de-facto failure of issuers

Bank holding companies become issuers (due to partial de-recognition of conventional subordinated bonds issued by bank subsidiaries*) * Due to treatment of adjusted minority interest associated with Tier2 capital (Basel III).

Point ① Differences with conventional (Basel II) subordinated bonds are (1) granting of principal reduction clausesand (2) issuance by bank holding companies

Point ② Timing to implement bail-in clauses limited to insolvency cases (in case of Japan)

Point ③ Japanese rating agencies assign A-category ratings to major Japanese financial groups (BBB-category ratings by foreign agencies)

JCR and R&I assigned A-category ratings to B3T2 issued by three major banks and Sumitomo Mitsui Trust Holdings

Point ④ Conventional major investors (domestic financial institutions) to hesitate to invest in B3T2

Increase in risk factors to be considered

Virtual risk changed little

Rating agencies also support

aforementioned opinion

Narrower investor base to serve as chance

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

13

Bail-in Risk Relatively Limited in Japan

Source: Financial Services Agency, Proposal to revise Deposit Insurance Act; compiled by Daiwa Securities.

Financial Safety Net Based on Revised Deposit Insurance Act

Contractual bail-in clauses Basel III-compliant securities have limited bail-in risk Preemptive capital injections do not serve as PONV triggers PONV triggers occur in case of negative equity

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1414

Ratings of Basel III-compliant Tier 2 Subordinated Bonds(B3T2)

As of Oct. 20thSource: Methodologies at rating agencies; compiled by Daiwa Securities.

Note: Rating in red circle indicates actual one.

Ratings of Basel III-compliant Subordinated Bonds (actual, forecast)

Except for Moody’s ratings, no major difference between ratings of conventional (Basel II-compliant) subordinated bonds and those of Basel III-compliant subordinated bonds(B3T2)

Issued by bank holding companies

Bail-in trigger is simple—when prime minister approves “Special measures under Item 2 under Article 102 of Deposit Insurance Act” (note: actual bonds extinguished on any day within ten days after approval)

Bail-in clause indicates full principal reduction

10-year bullet type, 10NC5 type

No clause for advance redemption, but there are clauses for early redemption when Tier 2 requirements lost

Product Features of B3T2

JCR R&I S&P MDYSenior debt A+ A BBB Baa1

B3T2 A- A- BB+ -Senior debt AA- A+ BBB+ Baa1

B3T2 A A BB+ -

Daiwa Securities Group

Nomura Holdings

JCR R&I S&P MDYSenior debt AA AA- A+ A1Conventional subordinated bonds AA- A+ A A2

MUFG B3T2 A+ A+ A- Baa2Senior debt AA AA- A A1Conventional subordinated bonds AA- A+ A- A2

SMFG B3T2 A+ A+ BBB+ Baa2Senior debt AA AA- A A1Conventional subordinated bonds AA- A+ A- A2

Mizuho FG B3T2 A+ A+ BBB+ Baa3Senior debt AA- A+ A A1Conventional subordinated bonds A+ A A- A2

Sumitomo Mitsui Trust Holdings B3T2 A+ A BBB+ Baa2

Bank of Tokyo-Mitsubishi UFJ

Sumitomo Mitsui BankingCorporation

Mizuho Bank

Sumitomo Mitsui Trust Bank

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1515

Basel III-compliant Additional Tier1 Securities (B3AT1)

B3AT1 in forefront in securing soundness at banks

Point ① Going-concern loss absorbency

Losses (principal reduction, conversion to common shares) occur when CET1 ratio is 5.125% and lower

Point ② Uncertainty on maturity date

Callable perpetual bonds but step-ups not approved

Point ③ Full discretion for coupon payment

Non-cumulative coupons, issuer has full discretion on coupon payment

Point ④ Loss absorbency at point of non-viability

Similar to B3T2

Point ⑤ Inferiority in distribution of residual property

Inferior to other debt such as subordinated bonds (= little hope for collection of money in case of issuer entering bankruptcy procedures)

Timing of Loss Generation for Capital Securities

Source: Compiled by Daiwa Securities.Note: When assets are accepted as being in excess of liabilities, preventive injection of public fund does not fall into PONV in Japan.

Tier 1 such as common shares (CET1)

Depositors

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1616

Product Features of B3AT1

Source: Company materials; compiled by Daiwa Securities.

Product Features of First B3AT1 Issued by MUFG and Mizuho FG

As B3AT1 is regulatory capital in forefront in securing soundness at banks, overall risk exposure increases Meanwhile, respective L+240bp/L+245bp spreads on A- rated bonds(JCR) attractive “Bond-like view vs. equity-like view” could be applied

Issuer Mitsubishi UFJ Financial Group (MUFG) Mizuho FG

Name First series of unsecured perpetual subordinated bonds with optional-redemption clauseand write-down clause for qualified institutional investors only

First series of unsecured perpetual subordinated bonds with optional-redemption clauseand write-down clause for qualified institutional investors only

Term Perpetual NC5 Perpetual NC5

Issue amount Y100bn Y300bn

Coupon rate Initial five years: 2.70% (L+240bp) Initial five years: 2.75% (L+245bp)After five years: 6-month euro-yen LIBOR + 2.40% After five years: 6-month euro-yen LIBOR + 2.45%

Rating A- (JCR) A- (JCR)

① Going-concern loss absorbency Partial principal reduction when consolidated CET1 ratio falls below 5.125%(Write-down of principal necessary to recover CET ratio to 5.125%)

Partial principal reduction when consolidated CET1 ratio falls below 5.125%(Write-down of principal necessary to recover CET ratio to 5.125%)※With reinstatement clause (after prior confirmation of Financial Services Agency)

② Uncertainty on maturity date Discretionary call option available if five years pass after issuance (on interest payment date)(Note: no granting of stepped-up interest rate)

Discretionary call option available if five years pass after issuance (on interest payment date)(Note: no granting of stepped-up interest rate)

③ Full discretion for coupon payment Interest payments can be cancelled based on issuer's full discretion (non-cumulative) Interest payments can be cancelled based on issuer's full discretion (non-cumulative)‧ Interest payments should not exceed distributable amount ‧ Interest payments should not exceed distributable amount‧ With dividend stopper clause (when interest payments on the bonds are cancelled, stockdividend should not be paid

‧ With dividend stopper clause (when interest payments on the bonds are cancelled, stockdividend should not be paid

④ Loss absorbency at point of non-viability Write-down of full principal when "specified item 2 measures" under Article 126-2 of DepositInsurance Act are set in motion

Write-down of full principal when "specified item 2 measures" under Article 126-2 of DepositInsurance Act are set in motion

⑤ Inferiority in distribution of residual propertyIn case of legal bankruptcy: The bonds rank senior to common shares, pari passu withpreferred shares and preferred securities, and junior to general creditors and datedsubordinated creditors

In case of legal bankruptcy: The bonds rank senior to company's shares and existingpreferred securities issued by its overseas special purpose subsidiaries, and junior togeneral creditors and subordinated creditors of Tier 2 liabilities of company

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

17

Ratings on B3AT1

Our Estimates for Ratings on B3AT1

As of Oct.20thSource: Rating agencies; compiled by Daiwa Securities*Actual rating.

MUFG SMFG Mizuho FG SMTHJCRIssuer rating (core bank) AA AA AA AA-

Standard notch-down 3 3 3 3Notch-down in terms of holding company 1 1 1 -

Total notch-down 4 4 4 3Rating on B3AT1 (our estimate) A- * A- * A- * A- *

R&IIssuer rating (core bank) AA- AA- AA- A+

Standard notch-down 3~4 3~4 3~4 3~4Notch-down in terms of holding company 1 1 1 1

Total notch-down 4~5 4~5 4~5 4~5Rating on B3AT1 (our estimate) ( BBB+ ~ BBB ) ( BBB+ ~ BBB ) ( BBB+ ~ BBB ) ( BBB ~ BBB- )

MDYAdjsuted BCA a3 a3 baa1 a3

Standard notch-down 3 3 3 3Notch-down in terms of holding company 1 1 1 1

Total notch-down 4 4 4 4Rating on B3AT1 (our estimate) ( Ba1 ) ( Ba1 ) ( Ba2 ) ( Ba1 )

S&PStandalone assessment a+ a a a

Standard notch-down 3 3 3 3Notch-down in terms of holding company 1 1 1 1

Total notch-down 4 4 4 4Rating on B3AT1 (our estimate) ( BBB ) ( BBB- ) ( BBB- ) ( BBB- )

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1818

【Reference】 Mega Financial Groups to Issue Senior Debt to Cope with TLAC

G-SIBs (three mega financial groups) need to cope with TLAC, in addition to compliance to Base III Purpose is to have sufficient loss absorbency and avoid usage of public funds in worst case of bankruptcy procedures They need to issue certain amount of TLAC-eligible debt (TLAC ratio of 16-20%?) In case of Japan, senior debt issued by financial holding companies can be recognized as TLAC-eligible debt

Breakdown of Capital Adequacy Ratio at Japanese Mega Financial Groups (end-FY14 transitional arrangements) and Estimates for TLAC Requirements

Source: Company materials; compiled by Daiwa Securities.Note: Capital conservation buffer (2.5%) cannot be included in TLAC, but we assume corresponding amount can be included given deposit insurance system in Japan. As G-SIB surcharge cannot be included in TLAC, we deducted 1.5% for MUFG and 1% each for SMFG and Mizuho FG. Required TLAC ratio assumed at 18%, midpoint of proposed 16-20% range.

MUFG: Slightly above Y4tnMizuho FG: Slightly below Y3tnSMFG: Y1.5tn

Will this trigger revival of banks’ senior debt market?

AT1, 1.5 % AT1, 1.6 %

AT1, 2.1 %

Tier 2, 3.1 %Tier 2, 3.7 %

Tier 2, 3.1 %

TLAC bonds, 2.4%

TLAC bonds, 4.4%

Tier 1(e.g., common equity )

(CET1), 9.4 %

Tier 1 (e.g., common equity )

(CET1), 11.3 %

Tier 1(e.g., common equity )

(CET1), 11.1 %

Tier 1 (e.g., common equity )

(CET1) 4.5 %

Capital conserv ation buffer

(CET1) 2.5 %

AT1, 1.5 %

Tier2 2.0 %

TLAC bonds, 3.8%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Basel Ⅲ MUFG MUFG (TLAC) SMFG SMFG (TLAC) Mizuho FG Mizuho FG (TLAC)

(Minimum requirement lev el +capital conserv ation buffer)

End-FY2014

Required capital adequacy ratioudder full implementation

TLAC ratio (%)

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

1919

3-2. Insurers’ Capital Securities (subordinated bonds)

Capital requirement under new solvency margin regulationsFirst considerationTaiyo Life Insurance(Fixed-term subordinated bonds: 10NC5)

Capital requirement in terms of ratings Second considerationNippon Life Insurance(Dollar-/yen-denominated fixed-term subordinated bonds: 30NC10)

Sumitomo Life Insurance( Dollar-denominated fixed-term subordinated bonds:60NC10)

Future capital requirementThird considerationFukoku Mutual Life Insurance(Dollar-denominated perpetual subordinated debt: NC10)

(Perpetual subordinated debt: NC5)

Product design of fixed-term subordinated bonds considers only capital requirements under solvency margin regulations

Specified hybrid debt capital instruments (perpetual subordinated debt) also issued given requirements for inclusion in solvency margins

Issuance of super long-term subordinated bonds also considers requirements in ratings

Some firms prefer perpetual subordinated debt, in anticipation of tighter regulations in future

Source: Compiled by Daiwa Securities.

Several factors result in “custom-made” product features

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

2020

Requirements for Subordinated Bonds Under New Solvency Margin Regulations

Source: Financial Service Agency; compiled by Daiwa Securities.Note: Core payment capacity = Net assets (excl. valuation gains/losses) + Reserve for price fluctuation + Contingency reserve - Net unrealized gains on available-for-sale securities.

Outline of Requirements for Subordinated Bonds Under New Solvency Margin Regulations

Solvency margin ratio =Total margin amount (incl. equity capital, reserves, subordinated bonds)

1/2 × Total risk amount (incl. risk of increase in insurance claims payment, asset investment-related risk)

Hybrid debt capital instruments Specified hybrid debt capital instruments

Redemption period ・At least five years

Dividend/interest payment ・To be paid, irrespective of creditconditions

① Coupon payment can be postponed① Coupon payment can be postponed② Coupon payment should be non-cumulative or cumulative, with no limitationon postponement of coupon payment

Premature redemption

Stepped-up interest rateAvailable if five years pass after

issuance and rate is not excessive (up to150bp)

Available if five years pass afterissuance and rate is not excessive (up

to 150bp)

Available if five years pass after issuanceand rate is not excessive (up to 100bp)

Loss absorbency at point of non-viability All amount can be included

・Up to 50% of core payment capacity -Cap on inclusion in capital ・Total amount is upper limit of inclusion (within core payment capacity)

Subordinated term debtPerpetual subordinated debt

・No limitation (perpetual)

・Discretional redemption available by issuers・Necessitates advance confirmation by Financial Services Agency and sufficient capital holding

No loss absorbency

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

2121

Criteria for Equity Content Assessment at Rating Agencies

Most strict standard among guidelines at rating agencies

Source: Rating agencies, interviews with rating agencies; compiled by Daiwa Securities.

R&I JCR Moody's S&P

Class 350%

Medium equity content50%

Basket "C"50%

Medium equity content (cap on inclusion: 25% of capital)

Above 50 years (as ofissuance)

At least 40 years (residualmaturity)

At least 60 years (as of issuance)At least 10 years (residual maturity) At least 20 years (residual maturity)

After five years After five years No rules No rulesNecessary Necessary Unnecessary Unnecessary

Timing After five years After five years After ten yearsAfter ten years

(below 25bp step-up available after fiveyears)

Degree Up to 100bp Around 100bp Up to 100bp At least 25bp and up to 100bp

Discretionary cancellation Discretionary cancellation Discretionary cancellation Discretionary cancellation

Cumulative Cumulative Cumulative Cumulative

Most inferior among debt Most inferior among debt Most inferior in capital composition(excl. common shares)

Strong subordination (no clear definition)

Criteria for equity content assessment

Existence or non-existence of maturity

(perpetuity)

Obligation to continueinterest payment

Clause to cancel interestpayment

Cumulativeness of deferredinterest

Ranking of claim(subordination)

Equity content assessment

Stepped-up

Term

Call optionRefinance clause

Criteria for Equity Content Assessment at Rating Agencies

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

2222

Final maturity tend to be long, but effective maturity shortened by granting callable clauses

Due to regulation/rating requirements, final maturity tends to be long However, issuers shorten effective maturity by granting product feature of callable clauses available when five/ten years pass after issuance Granted stepped-up interest rate indicates probability of issuer exercising call※In case of banks’ bonds, granting of stepped-up interest rates (which indicate probability of issuer exercising call) not allowed under Basel III, which is major difference

Insurers’ subordinated bonds

Banks’ subordinated bonds (Basel III-compliant)

※When residual maturity becomes shorter than five years, amount that can be included in capital declines, which serves as incentive for issuer to exercise call provision

Step-up interest rate

First call dateYears after issuance

Premiumvs. base interest rate

Effective maturity (5, 10 years)

Final maturity (30 years, etc.)

First call dateYears after issuance

Premiumvs. base interest rate

Effective maturity? (5 years, etc.)

Final maturity (10 years, etc.)

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

2323

Insurers’ Subordinated Bonds

Point ① Terms tend to be super long with callable clauses

Because issuers need to consider capital requirements in terms of rating, not limited to requirements for regulatory capital(= solvency margin ratio regulations)

Point ② Redemption risk:Period until first call date can be regarded as effective redemption period

Unlike banks’ capital securities, insurers can indicate probability of call by granting stepped-up interest rates

Point ③ Risk of suspension of interest payment: Low probability of discretionary/compulsory suspension of interest payment

Due to rating requirements, clauses for discretionary/compulsory suspension of interest payment could be granted. However, discretionary suspension is like “nuclear button.” Given current business conditions of domestic insurers, risk of compulsory suspension (such as solvency margin ratio less than 200%) limited.

Point ④ Mechanical rating methodology

Two notches down (vs. issuer rating) general, resulting from one notch down due to subordination in collection and one notch down caused by risk of deferral of interest payment

Seemingly unattractive investment targets, but practical risks not so high Carrying high yields in proportion to inferior marketability and liquidity; attractive amid low-interest rate and tight-spread environment

Point ⑤ Substantially factoring in credit enhancement via gov’t support is risk

Revision to Deposit Insurance Act enabled preemptive capital injection to insurers. However, we should think that it is possible only in the case of serious market collapse such as Lehman crisis. As witnessed by past bankruptcies of life insurers (Chiyoda, Kyoei, Tokyo, Yamato), gov’t unlikely to support firms’ failed management.

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

2424

3-3. Capital Securities Issued by Non-financial Firms Mitsubishi Corporation issued three-tranche publicly offered subordinated bonds amounting to Y200bn

Source: Company materials; compiled by Daiwa Securities.

Strongly reflecting equity content assessment by foreign rating agencies

Note: Tax event means cases of the bonds not allowed to be included in losses for tax reasons, event of equity credit change indicates cases of rating agencies’ changes in standards for equity content assessment (currently 50% at all rating agencies).

No. 1 bonds60NC5 (variable rate)

Premium vs. base interest rate 3mL+200bp

Final redemption date+75bp3mL+125bp

3mL+100bp+25bpFirst call

3mL+200bp

+75bp3mL+125bp

5YL+100bp3mL+100bp

+25bp1.31% First call

3mL+200bp

+75bp3mL+125bp10YL+100bp

+25bp1.68%

2015 (issuance) 2020 2025 2040 2045 2075

2015 (issuance) 2020 2025 2040 2045 2075

2015 (issuance) 2020 2025 2040 2045 2075

No. 2 bonds60NC5 (fixed rate)

No. 3 bonds60NC10 (fixed rate)

Final redemption date

Final redemption date

Premium vs. base interest rate

Premium vs. base interest rate

First call

No. 1 bonds60NC5 (variable rate)

Premium vs. base interest rate 3mL+200bp

Final redemption date+75bp3mL+125bp

3mL+100bp+25bpFirst call

3mL+200bp

+75bp3mL+125bp

5YL+100bp3mL+100bp

+25bp1.31% First call

3mL+200bp

+75bp3mL+125bp10YL+100bp

+25bp1.68%

2015 (issuance) 2020 2025 2040 2045 2075

2015 (issuance) 2020 2025 2040 2045 2075

2015 (issuance) 2020 2025 2040 2045 2075

No. 2 bonds60NC5 (fixed rate)

No. 3 bonds60NC10 (fixed rate)

Final redemption date

Final redemption date

Premium vs. base interest rate

Premium vs. base interest rate

First call

IssuerName Unsecured subordinated bonds No.1 Unsecured subordinated bonds No.2 Unsecured subordinated bonds No.3Term 60NC5 60NC5 60NC10Issue amount Y68bn Y92bn Y40bnInterest rate Initial ten years: 3mL+100bp Initial five years: 1.31% (5YL+100bp Initial ten years: 1.68% (10YL+100bp)

10-25 years: 3mL+125bp 5-10 years: 3mL+100bp 10-30 years: 3mL+125bpAfter 25 years: 3mL+200bp 10-25 years: 3mL+125bp After 30 years: 3mL+200bp After 25 years: 3mL+200bp

Rating

① Uncertainty on interest payments

② Uncertainty on maturity date Discretionary call option available if five yearspass after issuance (on interest payment date)

Discretionary call option available if five yearspass after issuance (on interest payment date)

Discretionary call option available if tenyears pass after issuance (on interestpayment date)

Can be redeemed before maturity uponoccurrence of tax event or event of equitycredit change*

Can be redeemed before maturity uponoccurrence of tax event or event of equitycredit change*

Can be redeemed before maturity uponoccurrence of tax event or event ofequity credit change*

⑤ Inferiority in distribution of residualproperty

In case of legal bankruptcy: The bonds rank junior to priority claims (such as senior debt) and pari passu with the most preferred stock

A (R&I), A3 (Moody's), A- (S&P)Issuer can defer interest payments at discretion and deferred interest is cumulative (However, accrued and unpaid interest should becompulsory paid by interest payments/dividend on securities inferior to the most preferred stock and subordinated debt ranking pari passu withthe bonds)

Mitsubishi Corporation

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

25

4. Credit Valuation

Japanese financials

Japan’s financial system has been maintaining stability. Financial intermediation has operated more smoothly than before. Extract from BOJ’s “Financial System Report, October 2015”

In monitoring Japanese financial system, (1) BOJ’s “Financial System Report” (semiannual) and (2) Financial Services Agency’s “Financial Monitoring Report” (annual) are useful

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

26

Japanese investors do not worried about credit risk at major banks1. Stable financial system/ solid financial safety net 2. Steady earnings 3. Adequate capital

Capital Adequacy Ratios (internationally active banks)Profit from Core Business (major banks)

Source: Extract from BOJ’s Financial System Report, April 2015.

Banks

Source: Extract from BOJ’s Financial System Report, October 2015.

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

27

Focal points in terms of credit risk valuationExpansion of international operations led to

1. Deterioration in balance between risk and capital 2. Higher risk of foreign currency liquidity

Overseas Loans Outstanding of Three Major Banks Stability Gap (Between Illiquid Loans and Stable Funding) Among Major Banks

Source: Extract from BOJ’s Financial System Report, October 2015.Source: Extract from BOJ’s Financial System Report, October 2015.

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

28

InsurersCreditworthiness of Japanese life insurers: Stable/improving1. Steady core profit driven by improved investment spread 2. Improving soundness (solvency margin ratio)

Core Profit and Solvency Margin Ratio at Major Life Insurers

Source: Company materials; compiled by Daiwa Securities.

-200

-100

0

100

200

300

400

500

600

700

800

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

FY02

12

FY20

13

FY20

14

N ippon Life Insurance Dai-ichi Life Insurance Meiji Yasuda LifeInsurance

Sumitomo LifeInsurance

Daido Life Insurance Taiyo Life Insurance Fukoku Mutual LifeInsurance

Asahi Mutual LifeInsurance

(Y bn)

0

200

400

600

800

1000

1200

1400(%)Investment spread (left)

Mortality & morbidity savings (left)Expense sav ings (left)

"Core profit - Investment spread" used for Daido and Taiyo (left)Solvency margin ratio (right)

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

29

Focal points in terms of credit risk valuation1. Success and failure of overseas M&As2. Risk control of foreign currency-denominated

assets under investmentRecent Investment in Overseas Insurers by Major Life Insurers Investment in Foreign Securities by Life Insurers

Source: Company materials; compiled by Daiwa Securities.

Source: Life Insurance Association of Japan; compiled by Daiwa Securities.

Nation Company name Announced in Investmentamount (Y bn)

Meiji Yasuda Life Insurance US StanCorp Financial Group Jul-15 624.6Dai-ichi Life Insurance US Protective Life Jun-14 582.2Sumitomo Life Insurance US Symetra Financial Aug-15 466.4Nippon Life Insurance Indonesia Sequis Life May-14 43.0Sumitomo Life Insurance Indonesia BNI Life Insurance Dec-13 38.2Dai-ichi Life Insurance Indonesia Panin Life Jun-13 34.3Sumitomo Life Insurance Vietnum Bao Viet Holdings Dec-12 28.0

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

FY2009 FY2010 FY2011 FY2012 FY2013

(Y bn)

24.0

24.5

25.0

25.5

26.0

26.5

27.0

27.5

28.0

28.5(%)

Foreign securities (left)

Share to total securities under investment (right)

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

30

Favorable credit fundamentals at Japanese firms 1. Profit uptrend in corporate earnings2. Healthy balance sheet3. Credit ratings in upgrade cycle

Non-financial Firms

Capital Adequacy Ratio and Financial Debt at Japanese FirmsRecurring Profit at Japanese firms (Nikkei 225 basis)

Source: Financial Statements Statistics of Corporations by Industry (survey targets: companies with capital of Y1 bn or over, excl. financials); compiled by Daiwa Securities.Source: Nikkei, Toyo Keizai, etc.; compiled by Daiwa Securities.

E: Estimates.

0

5

10

15

20

25

30

35

40

45

FY20

03

FY20

04

FY20

05

FY20

06

FY20

07

FY20

08

FY20

09

FY20

10

FY20

11

FY20

12

FY20

13

FY20

14

FY20

15 E

FY20

16 E

(Y tn) Nikkei 225

Nikkei 225 (excl. financials)

0.0

50.0

100.0

150.0

200.0

250.0

Jun-

10

Oct-1

0

Feb-

11

Jun-

11

Oct-1

1

Feb-

12

Jun-

12

Oct-1

2

Feb-

13

Jun-

13

Oct-1

3

Feb-

14

Jun-

14

Oct-1

4

Feb-

15

Jun-

15

(Y tn)

39

40

41

42

43

44

45

46

Borrow ings from financial institutions (left) Corporate bonds (left)

Other borrow ings (left) Capital adequacy ratio (right) (%)

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

31

Source: Rating agencies; compiled by Daiwa Securities. Notes: 1) Universe is ratings of domestic corporations by four major rating agencies.

2) Downgrades expressed as negatives. 3) Technical factors mean rating actions triggered by changes in sovereign ratings and rating agency's valuation methodology.

No. of Upgrades and Downgrades

-70

-60

-50

-40

-30

-20

-10

0

10

20

30

4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7 8 91011121 2 3 4 5 6 7

'10 '11 '12 '13 '14 '15

Downgrade(technical factors)

Upgrade(technical factors)

Downgrade

Upgrade

Upgrade-Downgrade(exclusive of technical factors)

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

32

Summary

Japanese firms (banks, insurers, non-financial firms) watching for further utilization/issuance of capital securities

First, they will likely plan to issue yen-denominated bonds. However, issuance of USD-denominated bonds also expected in the case of (1) limited domestic demand and/or (2) overseas market being more attractive.

Attractiveness of Japanese capital securities— stable creditworthiness at issuers

This document has been prepared by Daiwa Securities Co. Ltd. based on information, the sources of which are believed by Daiwa Securities to be reliable, but Daiwa Securitiesmakes no representation nor warranty as to the accuracy or completeness of such information. Recipients of this document must make their own decisions on whether or not toadopt the recommendations discussed in this document, based upon their specific situations and objectives. Any use, disclosure, distribution, dissemination, copying, orreproduction of this document without prior written consent from Daiwa Securities is prohibited.

IMPORTANTThis report is provided as a reference for making investment decisions and is not intended to be a solicitation for investment. Investment decisions should be made at your own discretion and risk. Content herein is based on information available at the time the report was prepared and may be amended or otherwise changed in the future without notice. We make no representations as to the accuracy or completeness. Daiwa Securities Co. Ltd. retains all rights related to the content of this report, which may not be redistributed or otherwise transmitted without prior consent.

Notification items pursuant to Article 37 of the Financial Instruments and Exchange LawIf you decide to enter into a business arrangement with our company based on the information described in materials presented along with this cover letter, we ask you to pay close attention to the following items. • In addition to the purchase price of a financial instrument, our company will collect a trading commission* for each transaction as agreed beforehand with you. Since commissions may be included in the purchase price or may not be charged for certain transactions, we recommend that you confirm the commission for each transaction. In some cases, our company also may charge a maximum of ¥ 2 million (including tax) per year as a standing proxy fee for our deposit of your securities, if

you are a non-resident. • For derivative and margin transactions etc., our company may require collateral or margin requirements in accordance with an agreement made beforehand with you. Ordinarily in such cases, the amount of the transaction will be in excess of the required collateral or margin requirements. • There is a risk that you will incur losses on your transactions due to changes in the market price of financial instruments based on fluctuations in interest rates, exchange rates, stock prices, real estate prices, commodity prices, and others. In addition, depending on the content of the transaction, the loss could exceed the amount of the collateral or margin requirements. • There may be a difference between bid price etc. and ask price etc. of OTC derivatives handled by our company. • Before engaging in any trading, please thoroughly confirm accounting and tax treatments regarding your trading in financial instruments with such experts as certified public accountants.

* The amount of the trading commission cannot be stated here in advance because it will be determined between our company and you based on current market conditions and the content of each transaction etc.When making an actual transaction, please be sure to carefully read the materials presented to you prior to the execution of agreement, and to take responsibility for your own decisions regarding the signing of the agreement with our company.

Corporate Name: Daiwa Securities Co. Ltd.Financial instruments firm:chief of Kanto Local The Finance Bureau (Kin-sho) No.108Memberships: Japan Securities Dealers AssociationThe Financial Futures Association of JapanJapan Investment Advisers AssociationType Ⅱ Financial Instruments Firms Association