Embed Size (px)

Citation preview

INVESTMENT MANAGEMENT AND PRIVATE FUNDS:Private Placement Life Insurance and Variable Annuities

VIRTUAL ROUNDTABLEOctober 27, 2020

These materials and commentary are intended for educational purposes only. No portion may be construed as rendering legal advice for specific cases, or as creating an attorney-client relationship between the audience and the author. The opinions expressed herein are solely those of the author.

We will start at 4pm ET.

All lines are muted.

We will be starting momentarily.

All lines are muted.

4

Firm Overview Top10%

of all law firms for innovative approach and anticipating client needs. – BTI Client Service A-Team 2018 list

Troutman Pepper is a national law firm known for its higher commitment to client care. With more than 1,100 attorneys in 23 U.S. offices, the firm partners with clients across every industry sector to help them achieve their business goals. Read more about the firm’s litigation, transactional, and regulatory practices at troutman.com.

5

1,100+combined attorneys

47thprojected Am Law ranking

Our National ReachAtlanta | Berwyn | Boston | Charlotte | Chicago | Detroit | Harrisburg | Los Angeles | New YorkOrange County | Philadelphia | Pittsburgh | Portland | Princeton | Raleigh | Richmond | RochesterSan Diego | San Francisco | Silicon Valley | Virginia Beach | Washington, D.C. | Wilmington

Top 10%of all law firms for innovative approach and anticipating client needs. – BTI Client Service A-Team 2018 list

23U.S. cities

CLE Available

There will be an online survey available after the webinar to submit the two CLE Code words provided during today’s session. Contact [email protected] for the survey if you do not receive it after today’s session.

7

Gregory Nowak is sought after for advice on complex securities law matters, particularly on issues arising out of the Investment Company Act of 1940; the Investment Advisers Act of 1940; federal and state securities laws and regulations; broker dealer, FINRA, CFTC and NFA regulatory matters; and corporate and M&A transactions.

Greg also represents many hedge funds and other alternative investment funds in fund formation and investment and compliance matters, including compliance audits and preparation work. Greg has represented a broad range of investment funds, from funds that use the traditional broad investment charters and invest globally in virtually any financial asset that can be readily traded to specialty niche funds.

Greg writes and speaks frequently on issues involving alternative lending, blockchain, initial coin offerings (ICOs), investment management, health care and other matters and is the author of five books on hedge funds.

Gregory J. Nowak215.981.4893

[email protected]/New York

Investment Funds

Insert Photo Here

8

Justin Brown focuses his practice on estate and tax planning, estate and trust administration, and estate litigation. He is a fellow of the American College of Trust and Estate Counsel.

Justin advises clients on wealth transfer, asset protection, and business succession strategies. Justin also counsels fiduciaries on their duties and obligations in connection with the administration of estates and trusts. In his probate and Orphans’ Court litigation practice, Justin represents both fiduciaries and beneficiaries in will contests, fiduciary accountings, and guardianship proceedings. He is a Fellow of the American College of Trust and Estate Counsel.

Justin serves as an adjunct professor at Temple University’s James E. Beasley School of Law. He is the co-host of “The Digital Planning Podcast,” which educates individuals about all things digital in estate planning, business planning, and estate administration

Justin H. Brown215.981.4022

Tax

Insert Photo Here

9

Brian is an insurance and estate planning professional, with 38 years experience in the industry. After a short career with Coopers and Lybrand, Brian joined Northwestern Mutual in 1982.

His 38 years have covered many levels within the insurance industry, including Pension Estate and Family Legacy Planning. A multiple Million Dollar Round table qualifier. Brian has been part of the leaders group and executive council for many of the top companies in the industry.

As President and founder of the PPLI Group, Brian markets to the HNW and family office markets and their advisors.

Brian [email protected]

Insert Photo Here

10

Harvey Feinberg spent the first 30 years of his career as the owner and president of Finesse Promotions LTD. He was a leader in this industry becoming president of the association and eventually being inducted into the industry “Hall of Fame”.

During the years as an entrepreneur Harvey was president of his local Rotary Club and received the honor of Paul Harris Fellow.

Upon leaving the promotion industry Harvey worked as a consultant to various startup companies, eventually gravitating to the life insurance field. He has worked with some of the highest respected individuals in the insurance field, collaborating with them, delivering innovative concepts in estate and legacy planning for HNW families.

In addition to the honors Harvey received during his career, he spent 20 years on the Arthritis Board of Directors receiving many awards and recognition for outstanding contributions to the foundation.

Harvey received his bachelor’s degree in business administration from New York Institute of Technology. He has a degree as a Certified Family Business Specialist from the American College, Bryn Mawr, Pennsylvania.

Harvey [email protected]

11

Robert D. Stuchiner is the president of Synergy Life Brokerage Group, LLC. Synergy specializes in designing and implementing cost-effective strategies to mitigate risk, maximize flexibility and reduce taxes. Synergy has been recognized by Private Asset Management as best high-net-worth insurance agency in both 2013 and 2014.

Robert’s knowledge of estate planning, executive benefits and planned charitable giving as well as his ability to perform “due diligence” on Insurance products and carriers makes him a resource to Industry professionals seeking to implement Insurance strategies in the affluent markets.

Mr. Stuchiner has worked for some of the largest Insurance companies, most recently AIG where he was a senior vice president in charge of product development and market strategy for the corporate and affluent markets group. In his industry experience, Robert was a pioneer in life insurance and annuity products as well as senior life settlements. Robert is the co-creator and founder of the Insuring A Better World Fund, a public charity whose mission is to raise funds for other charities by directing the value of unneeded or unaffordablelife insurance to the charity of the donor’s choosing. Robert is the 2015 recipient of the Stephen A. Kramer Humanitarian Award granted by the UJA-Federation of New York.

Robert D. [email protected]

1. McCarran-Ferguson Act of 1945, 59 Stat. 33 15 USC §1011 effectively delegates the regulation of insurance to the states.

2. In SEC v. VALIC, 359 US 65 (1959), the U.S. Supreme Court definitively stated that:• “The concept of insurance involves some investment risk-taking on the part of

company.”• “[In the variable annuity arrangement presented in the case, t]here is no true

entrusting of risks, the one landmark of insurance as it has commonly been conceived of in popular understanding and usage.”

CONCLUSION: Variable annuities are securities and subject to the ‘33 Act and ‘40 Act.

LEGAL FRAMEWORK

A. Contract must be issued by an insurance company

B. State law allows insurance companies to segregate risk away from their general accounts into so-called segregated accounts of the insurance company – Do not confuse this with an SMA. They are different animals.

C. The segregated account must be owned 100% by the insurance company.

D. The insurance company can create an “insurance dedicated fund” to comply with the diversification rules of the regulations and act as the investment vehicle.

SECTION 817(h) OF THE IRS & APPLICABLE REGULATIONS

A. No more than 55% of the values of the segregated account is represented by any one investment.

B. No more than 70% by any two investments.

C. No more than 80% by any three investments.

D. No more than 90% by any four investments.

• There are safe harbors and alternative tests

• Treas. Reg. 1.817-5(f) provides a look-through rule for certain RICs, REITs, partnerships and certain trusts – must be owned exclusively by insurance company segregated accounts. These entities must be “insurance dedicated funds” – “IDFs”

DIVERSIFICATION

• GP Interest –

A. Only allowed in connection with the creation or management of the partnership

B. No carry or performance allocations [can have a performance fee].

IDFs

Insurance Company General

Account

SegregatedAccount

DEATH BENEFIT & INTERNAL BUILD UP

Policy Information Wall –NO INVESTOR

CONTROL

FEES

Accredited Investor

SMA-DIVERSIFIED

POOL

RIA

Services

Policy Holder

‘40 ACT 3(c)(1) or (7)

FUND

CONTRACT

IDFLP

INVESTMENTGP/RIA

DIVERSFIEDPOOL OF ASSETS

Estate Planning with Private Placement Life Insurance

18

• Estate Tax• 2020 Exemption: $11.58 million per individual• 2026 Exemption: $5 million (adjusted for inflation)• Portability

• Gift Tax• 2020 Exemption: $11.58 million per individual• 2026 Exemption: $5 million (adjusted for inflation)• Deceased Spouse Unused Exemption• Annual Exclusion: $15,000

• Generation Skipping Transfer Tax• 2020 Exemption: $11.58 million per individual• 2026 Exemption: $5 million (adjusted for inflation)• NO Portability• Annual Exclusion $15,000 (but be careful about trusts!)

Estate/Gift/Generation Skipping Transfer Tax

19

• Estate/Gift/GST Tax• 2021 Exemption:

o Trump Victory: $11.70 million per individual ($23.4 million per couple)o Biden Victory: $3.5 million? $5 million? $11.7 million?

• Interest Rates• Applicable Federal Rate (October)

o Short Term: 0.14%o Mid Term: 0.38%o Long Term: 1.12%

• Applicable Federal Rate (January)o Can it get any lower!?

How Will Estate/Gift/GST Taxes Changes After the Election?

20

• IRC Section 2042• The life insurance death benefit received by the executor is subject to estate tax.• The life insurance death benefit received by a beneficiary is subject to estate tax if the decedent possessed at the

time of his/her death any incidents of ownership, exercisable either alone or in conjunction with any other person.

• Irrevocable Life Insurance Trust (ILIT)• Trust owns life insurance policy (rather than the insured) so that the insured has no “incidents of ownership” in the

policy.o Insured should not be a trustee of the ILITo Insured should not be a beneficiary of the ILITo Insured should not have the ability to designate the beneficiaries of the ILITo Insured should not retain any interests in the ILIT

• Premium Payments:o Insured makes a gift of the premium to the ILITo Beneficiaries receive Crummey noticeo Trustee pays premium

Life Insurance Planning

21

• Payment Strategy when Insured Does Not Have Sufficient Gift Tax Exemption• Insured loans funds to the ILIT and takes back a promissory note at the AFR rate.• Trustee uses the loaned funds to pay the policy premium.• Policy internal value builds and the trustee may borrow funds from the policy to pay

off the insured’s note.

Premium Financing

ILITInsured

PPLI

Loan to ILIT

Premium Payment

NoteBorrow from

Growth in PolicyPay off Note

22

• Spousal Limited Access Trusts (SLAT)• Grantor Trust as to settlor for income tax purposes• Assets not subject to estate tax• Funded through gift or sale

• Beneficiary Defective Inheritance Trust (BDIT)• Grantor Trust as to the beneficiary for income tax purposes• Assets not subject to estate tax• Funded through gift or sale

• Domestic Asset Protection Trust (DAPT)• Grantor Trust as to settlor for income tax purposes• Assets subject to estate tax if retained interests• Funded by incomplete gift• Creditor Protection

Other Year End Planning Opportunities with PPLI

PPLIPrivate Placement Life

Insurance 2.0“The All-Seasons Advantage"

October 2020

Presented byRobert D. Stuchiner

Strategic Advisor and Founder Synergy Life Brokerage Group, LLC

Agenda

Value proposition PPLI explained The investment opportunities The current market The cost New innovations Introducing Private Mortality Coverage (PMC)

24

PPLI Value Proposition

One of the best, last remaining tax management devicesavailable of any kind

For many buyers of life insurance, PPLI is the lowest costway to pay for needed life insurance death benefit

25

What is PPLI?

Private Placement Life Insurance (PPLI), is a flexiblepremium, flexible death benefit, variable universal lifepolicy (VUL) that is only available to “accreditedinvestors” and “qualified purchasers”

Policy is exempt from SEC registration Accredited Investors - $1M of net worth or $200K of household income

each of the last three years ($300K combined with spouse) Qualified purchasers- $5M of investable assets

26

PPLI Continued A low-load, institutionally priced variable universal life

policy (i.e. no surrender charges) Filed with various state jurisdictions (Departments of Insurance) and

offshore FINRA Registered

Complies with all IRC regulations and various state lawsregulating insurance when applicable IRC Sections 101, 72, 817 & 7702

All client assets are held in PPLI Carrier’s separateaccount and are not chargeable with any liability arisingfrom any other business of the carrier. Separate account neutralizes credit risk of carrier.

27

PPLI Investment Options

Qualifying Wealth Managers can manage PPLI assets butwithin PPLI

Access to vast array of non-retail investment choices,which expands further through use of SMA managed byWealth Manager.

Can invest in long-short strategies, private credit, realestate and private equity funds

Premium and death benefit can in certain circumstancesbe paid “in kind”

28

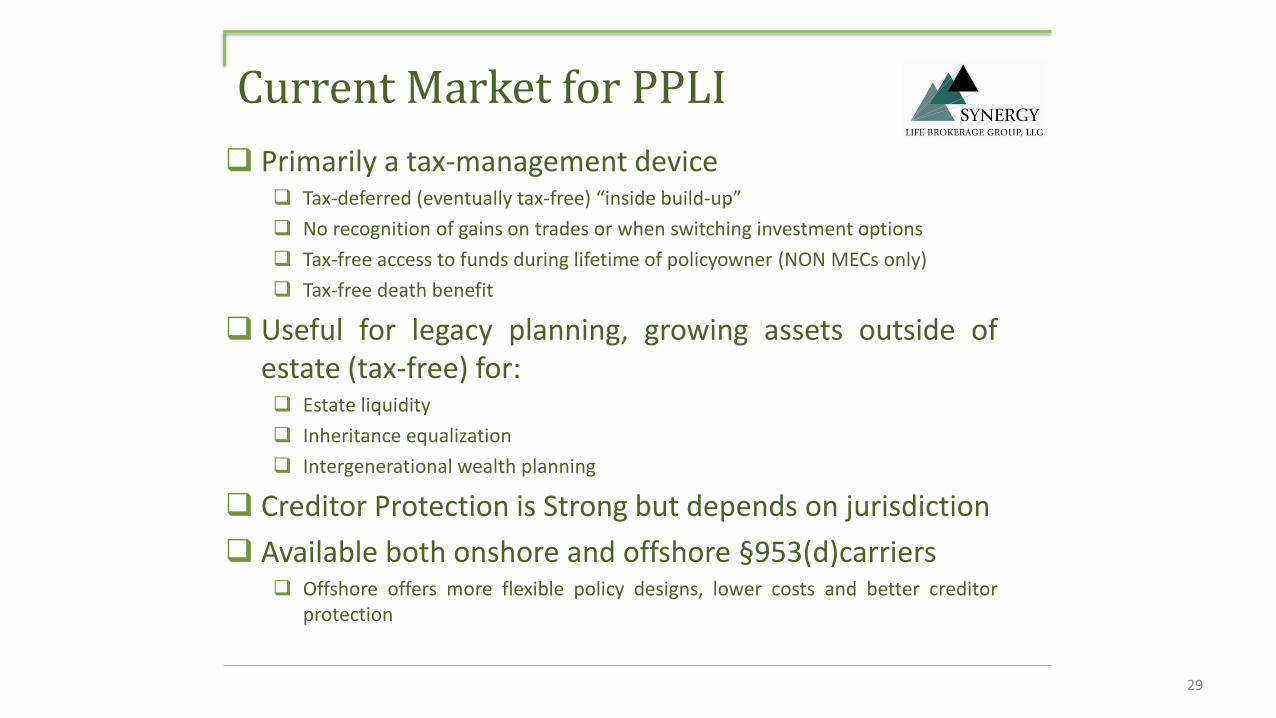

Current Market for PPLI Primarily a tax-management device

Tax-deferred (eventually tax-free) “inside build-up” No recognition of gains on trades or when switching investment options Tax-free access to funds during lifetime of policyowner (NON MECs only) Tax-free death benefit

Useful for legacy planning, growing assets outside ofestate (tax-free) for: Estate liquidity Inheritance equalization Intergenerational wealth planning

Creditor Protection is Strong but depends on jurisdiction Available both onshore and offshore §953(d)carriers

Offshore offers more flexible policy designs, lower costs and better creditorprotection

29

What is the cost of PPLI?

Depends on age, sex, and health status Largest cost is for the purchase of the “pure” insurance death benefit, known as

the “Net Amount at Risk”, (NAR). The cost of NAR, is a function of the age, health,and sex.

Net amount at risk can be reduced over time (Option A) orkept level (Option B). Traditional PPLI using a level NAR (Option B) becomes prohibitively expensive at

older ages since such contracts are facultatively reinsured using annuallyrenewable term rate.

IRC permits the reduction of NAR to zero or close to zero at age 95

When NAR is optimized, the total cost for a typical PPLIpolicy is approximately 100 basis points over lifetime

In other words, you get tax avoidance for life at a cost of100 basis points!

30

Chart of Typical PPLI with Investment Orientation

31

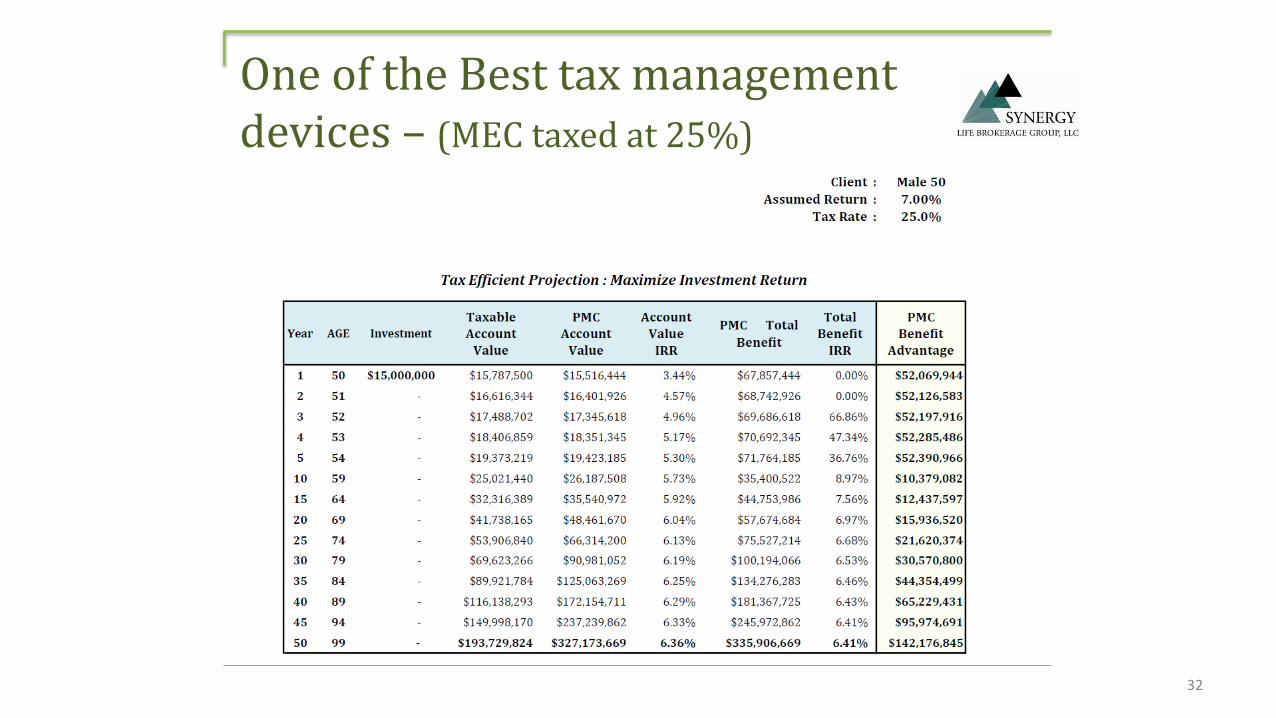

One of the Best tax management devices – (MEC taxed at 25%)

32

One of the Best tax management devices (Non-MEC taxed at 40%)

33

Introducing Private Mortality Coverage (PMC) A fresh look at PPLI

PMC replaces typical facultative reinsurance - based on ART which is difficult tounderwrite and extremely expensive at later ages

Utilizes guaranteed level premium universal life Less expensive over lifetime Guaranteed vs non-guaranteed

Option B using PMC is now affordable and providesguaranteed level NAR for lifetime death benefit Estate Planning Special Needs funding Business continuation planning Capital needs, etc.

Option B using PMC permits lifetime funding of the PPLIPolicy not just for initial 7 years

34

$84,613,435

$13,057,360

Total ULPremium

Charges vs.Facultative

Reinsurance

Guaranteed UL Facultative Reinsurance

Total Premium of GUL vs

Total PPLI Facultative COI Rates

35

Graphic Overview of PMC VS Facultative Reinsurance (COI)

Male 60, Super Preferred, $20M Face Amount40 Year Cumulative Totals for same amount of

Death Benefit Coverage

Notes: UL Policies are level DB and designed to limit cash value. PPLI illustrates constant $20M NAR reflecting Option B

This extraordinarily high facultative cost explains why PPLI has devalued the death benefit

Example 1A New Look at PPLI

For certain high net-worth investors, PPLI with PMC is thelowest cost method for acquiring needed life insurance(death benefit) on the market

The cost of death benefit can now be paid from “insidebuild-up,” which is equivalent to using tax free dollars

Thereby reducing the cost of carrying desired amount oflife insurance by owner’s marginal tax bracket

36

Example 1 continued

Situation: Male, age 50, seeks $20M of guaranteed level deathbenefit to age 121 – Premium is approximately $200K per yearfor life Solution: Purchase $20M of no lapse universal life plus a PPLI policy to

“wrap the GUL” policy On a non-MEC basis, the PPLI policy can absorb $1M/yr, or on a single

premium MEC basis can deposit $8M in year one Assuming 6% net investment return, client can fund $3.33M into a PPLI

policy and inside build-up (tax-free) pays the cost of insurance for theinsured on the GUL ($3.33M x 6% =$200K)

Assuming insured is in the 35% marginal tax bracket, reduces cost from$307,692 ($200k premium divided by .65%) vs $200k cost with PPLI orapproximately a 50% savings in cost

37

Example 2A New look at PPLI

Situation: Male, age 54, sophisticated Wall St investor with$20M whole life policy with cash value of $5.0M expected tobe done with premiums but latest dividend reduction adds 3more years of premium that he wasn’t expecting to pay. Solution #1: Purchase $20M of guaranteed no-lapse universal life

coverage ($250k per year) and roll in via 1035 exchange $5M of cashvalue. Total death benefit of $25M ($20M of NAR + $5M of cash value) Paying no additional premium and assuming 6.5% net rate of return, policy continues

to grow modestly above the $25M for life

Solution #2: Same as solution above except pay-in the three additionalpremiums to take advantage of tax-free inside build-up rights. Produces a net death benefit that is $5.0M higher than the whole life policy at life

expectancy

38

Example 3 Add inside build-up Rights

Situation: Male 60, owns $20M of guaranteed life insurancepurchased 10 years ago with policy performing as expected.

Would like to continue the coverage but add substantial premium which can grow tax-free in high growth investment options to morph the policy so that it includesinvestment tax advantages as well as death benefit

Solution: Purchase new PPLI policy and utilize existing guaranteed no-lapse policy to provide the net amount at risk.

On MEC basis can deposit $8M immediately, wait six years and thencan deposit $1.48M/yr for life , i.e. years 7-40

On non-MEC basis can deposit $1.48M/yr for life i.e. years 1-40 Result: Can dramatically improve an in-force policy to add tax-free

inside build-up for tens of millions of dollars over lifetime into a hugevariety of non-retail, sophisticated investment options

39

Example 4Rescue in-force Policy

Situation: Male, now aged 65 purchased $25M of universal life20 years ago with a premium for life of $250k. Due to lowinterest rates and/or skipping of premium new projectedpremium to carry coverage for life is $400k/yr Solution: Purchase new PPLI policy and contribute existing universal life

to provide the necessary net amount at risk. Through tax savings frominside build-up, can lower the cost of premium back to its originalamount ($250k)

Assuming marginal tax bracket of 35% and a 7% net investment rate ofreturn, need to invest an additional $6M one-time or over several years,which will generate $150K/yr tax savings ($6,142,857 x 7% = $434K ofinvestment x 35%= $150k of tax savings)

Can deposit substantially more as in example 3 above

40

Conclusions

PPLI is an extremely attractive tax management device offering awide variety of investment options on an institutionally priced basis

Opens new investment opportunities for Wealth Managers, which inturn allows for deploying innovative investment strategies usingSMAs. These features are not found in retail policies or inconventional PPLI

With the introduction of PMC (Private Mortality Coverage) , PPLI cannow be used to acquire needed death benefit at a lower cost thanconventional insurance

PMC can be used as either new coverage or provide the fundingmechanism for current in-force coverage

PMC can add huge income tax advantages to both new and existingcoverages

41

Synergy is a national life brokerage. This briefing is for informational purposes onlyand should not be construed as legal or tax advice and is not intended to replace theadvice of a qualified attorney or an accountant. Nothing herein is intended as an offeror solicitation for the purchase or sale of any financial investment nor for the purchaseor sale of any insurance policy. Synergy Life Brokerage Group is not engaged inrendering tax, legal, investment or actuarial services. The recipient agrees to maintainthis information in strict confidence.

42

PRIVATE AND CONFIDENTIAL – NOT FOR PUBLIC DISSEMINATION

43

For a Copy of the PowerPoint/Additional Information Contact:Harvey [email protected](516)359-8800

CLE Available

There will be an online survey available after the webinar to submit the two CLE Code words provided during today’s session. Contact [email protected] for the survey if you do not receive it after today’s session.