Embed Size (px)

Citation preview

Investment in Mining

Keith LockwoodTIPS Annual Forum

14 June 2016

THE GLOBAL CONTEXT

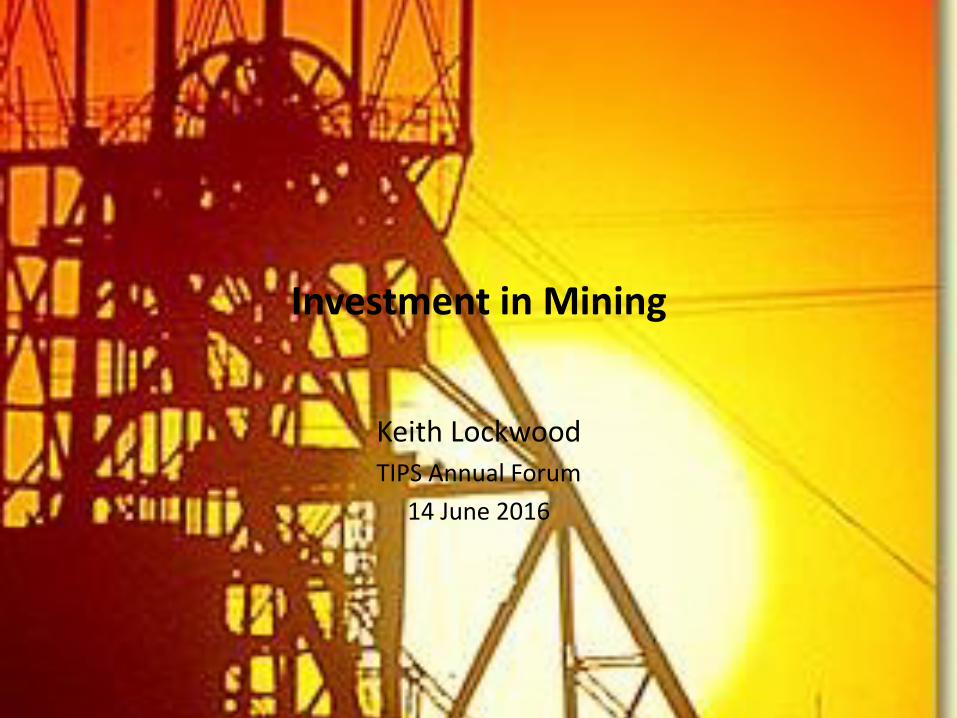

Key commodity price trends

0

100

200

300

400

500

600

700

800

900

19

95

M0

1

19

96

M0

2

19

97

M0

3

19

98

M0

4

19

99

M0

5

20

00

M0

6

20

01

M0

7

20

02

M0

8

20

03

M0

9

20

04

M1

0

20

05

M1

1

20

06

M1

2

20

08

M0

1

20

09

M0

2

20

10

M0

3

20

11

M0

4

20

12

M0

5

20

13

M0

6

20

14

M0

7

20

15

M0

8

Pri

ce In

de

x: J

anu

ary

19

95

= 1

00

Crude Oil

Coal

Iron Ore

Copper

Gold

Platinum

43

51

39

58

76

69

0

20

40

60

80

100

120

20

12

M0

1

20

12

M0

4

20

12

M0

7

20

12

M1

0

20

13

M0

1

20

13

M0

4

20

13

M0

7

20

13

M1

0

20

14

M0

1

20

14

M0

4

20

14

M0

7

20

14

M1

0

20

15

M0

1

20

15

M0

4

20

15

M0

7

20

15

M1

0

20

16

M0

1

20

16

M0

4

Pri

ce In

de

x: J

anu

ary

20

12

= 1

00

Crude Oil

Coal

Iron Ore

Copper

Gold

Platinum

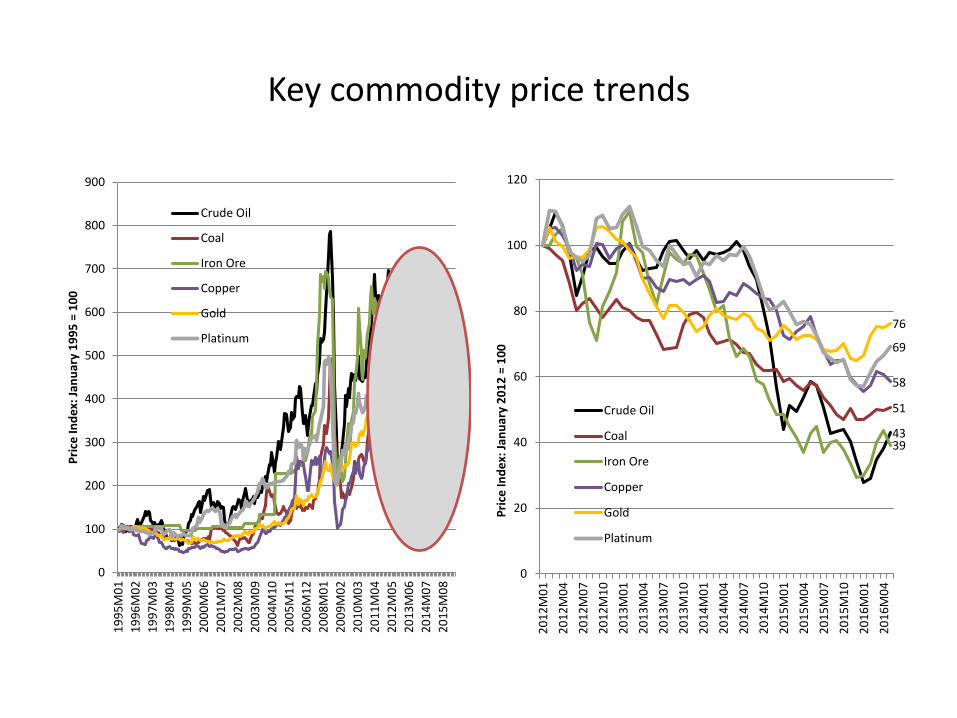

Waiting for the bear market to end

Adapted from material by SNL Metals and Mining

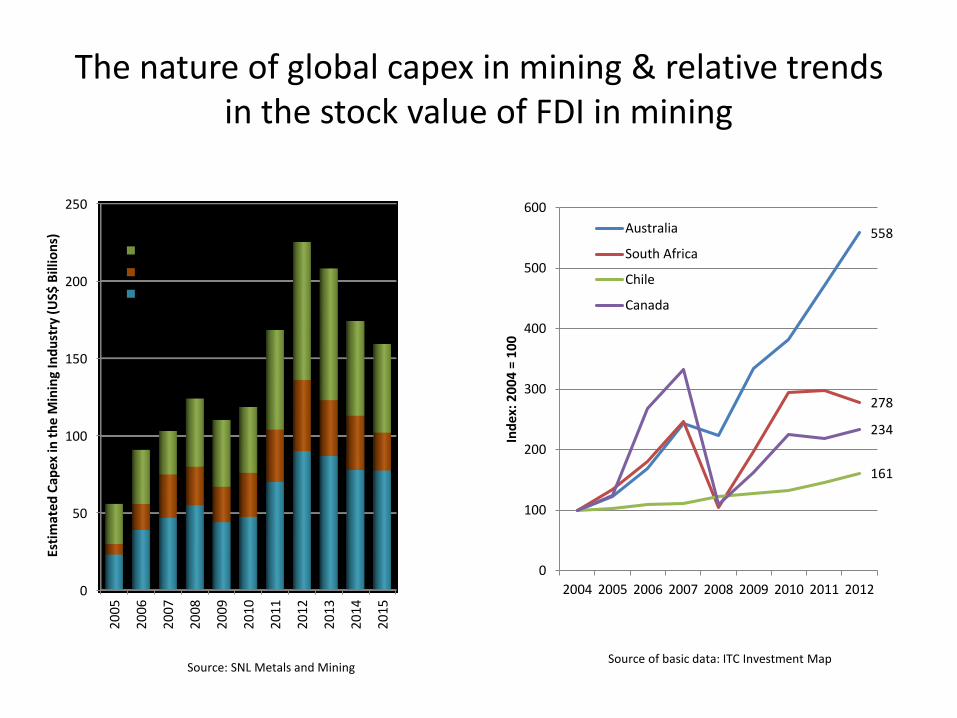

Problem seems to be due to historical global over-investment and excess supply, rather

than deficient demand

The nature of global capex in mining & relative trends in the stock value of FDI in mining

558

278

161

234

0

100

200

300

400

500

600

2004 2005 2006 2007 2008 2009 2010 2011 2012

Ind

ex: 2

00

4 =

10

0

Australia

South Africa

Chile

Canada

Source of basic data: ITC Investment Map

0

50

100

150

200

250

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

201

5

Esti

mat

ed C

ape

x in

th

e M

inin

g In

du

stry

(U

S$ B

illio

ns)

Greenfield

Brownfield

Sustaining Capex

Source: SNL Metals and Mining

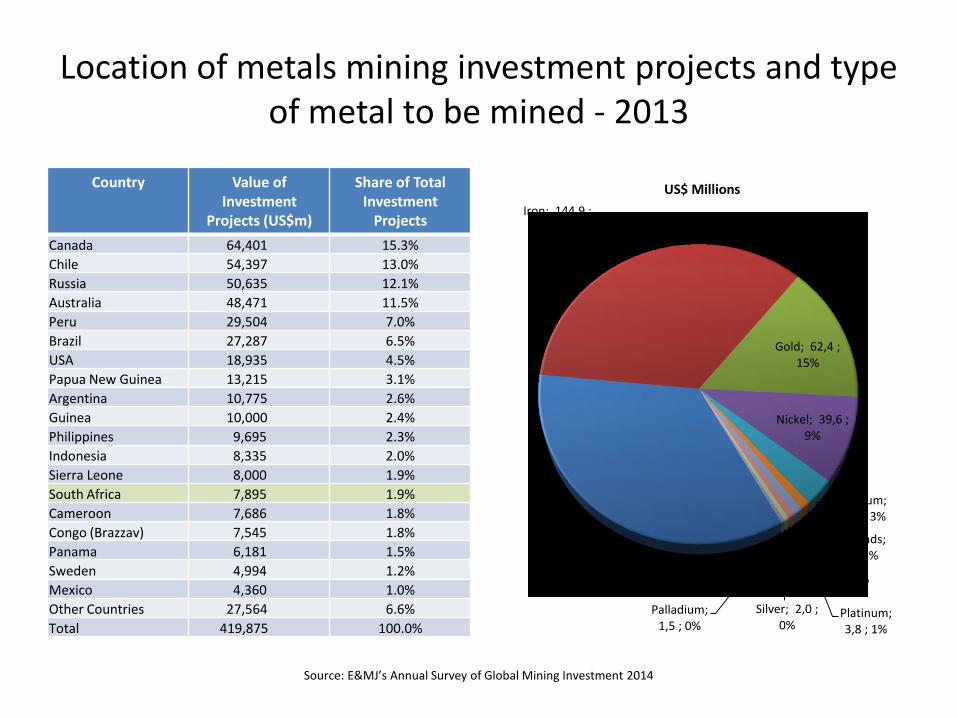

Location of metals mining investment projects and type of metal to be mined - 2013

Copper; 146,3 ; 35%

Iron; 144,9 ; 35%

Gold; 62,4 ; 15%

Nickel; 39,6 ; 9%

Uranium; 12,6 ; 3%

Diamonds; 4,0 ; 1%

Platinum; 3,8 ; 1%

Zinc; 2,8 ; 1%

Silver; 2,0 ; 0%

Palladium; 1,5 ; 0%

US$ MillionsCountry Value of Investment

Projects (US$m)

Share of Total Investment

Projects

Canada 64,401 15.3%

Chile 54,397 13.0%

Russia 50,635 12.1%

Australia 48,471 11.5%

Peru 29,504 7.0%

Brazil 27,287 6.5%

USA 18,935 4.5%

Papua New Guinea 13,215 3.1%

Argentina 10,775 2.6%

Guinea 10,000 2.4%

Philippines 9,695 2.3%

Indonesia 8,335 2.0%

Sierra Leone 8,000 1.9%

South Africa 7,895 1.9%

Cameroon 7,686 1.8%

Congo (Brazzav) 7,545 1.8%

Panama 6,181 1.5%

Sweden 4,994 1.2%

Mexico 4,360 1.0%

Other Countries 27,564 6.6%

Total 419,875 100.0%

Source: E&MJ’s Annual Survey of Global Mining Investment 2014

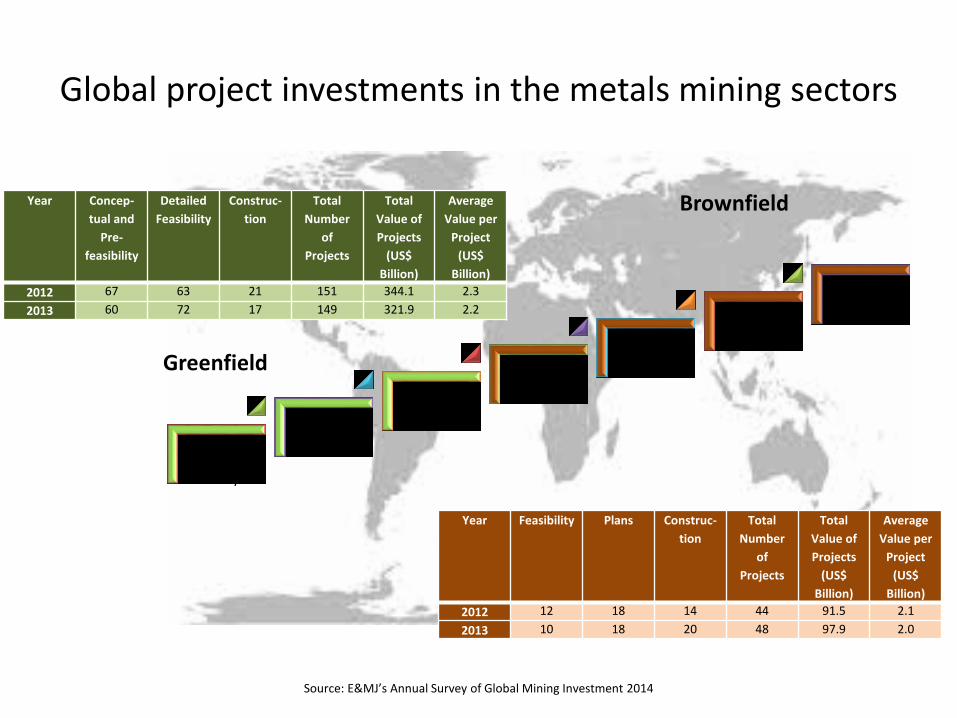

Global project investments in the metals mining sectors

Conceptual & Pre-feasibility

Feasibility

Construction

Operating -Feasibility

Operating –Plans

Operating –Construction

Other Brownfields

Source: E&MJ’s Annual Survey of Global Mining Investment 2014

Year Concep-

tual and

Pre-

feasibility

Detailed

Feasibility

Construc-

tion

Total

Number

of

Projects

Total

Value of

Projects

(US$

Billion)

Average

Value per

Project

(US$

Billion)

2012 67 63 21 151 344.1 2.3

2013 60 72 17 149 321.9 2.2

Year Feasibility Plans Construc-

tion

Total

Number

of

Projects

Total

Value of

Projects

(US$

Billion)

Average

Value per

Project

(US$

Billion)

2012 12 18 14 44 91.5 2.1

2013 10 18 20 48 97.9 2.0

Greenfield

Brownfield

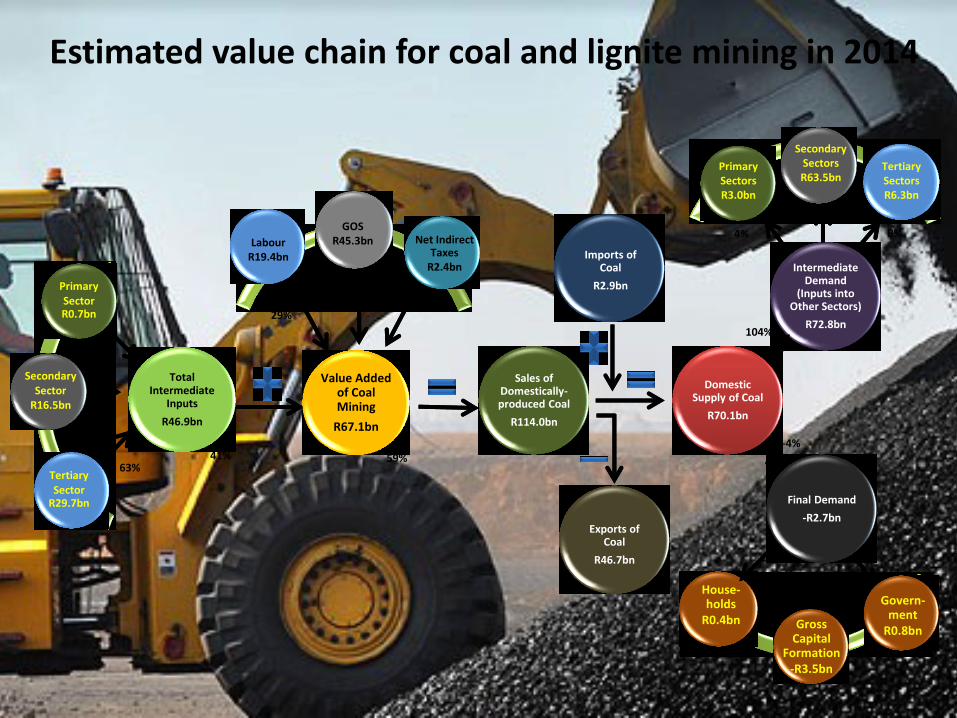

INVESTMENT IN SOUTH AFRICANMINING

Total Intermediate

Inputs

R46.9bn

Primary Sector R0.7bn

Secondary Sector

R16.5bn

Tertiary Sector

R29.7bn

Value Added of Coal Mining

R67.1bn

LabourR19.4bn

GOSR45.3bn Net Indirect

TaxesR2.4bn

Sales of Domestically-produced Coal

R114.0bn

Exports of Coal

R46.7bn

Imports of Coal

R2.9bn

Domestic Supply of Coal

R70.1bn

Final Demand

-R2.7bn

Intermediate Demand

(Inputs into Other Sectors)

R72.8bn

Primary SectorsR3.0bn

Secondary SectorsR63.5bn

Tertiary SectorsR6.3bn

Gross Capital

Formation-R3.5bn

63%

35%

2%

29%

67%

4%

41% 59%

House-holds

R0.4bn

104%

-4%

9%

87%

4%

Govern-ment

R0.8bn

Estimated value chain for coal and lignite mining in 2014

Total Intermediate

Inputs

R13.2bn

Primary Sector R0.3bn

Secondary Sector R9.5bn

Tertiary Sector R3.3bn

Value Added of Gold &

Uranium Ore Mining

R49.9bn

LabourR31.6bn

GOSR16.5bn Net Indirect

TaxesR1.8bn

Sales of Domestically-

produced Gold & Uranium

Ore

R63.1bn

Exports of Gold &

Uranium

R62.7bn

Imports of Gold &

Uranium

R0bn

Domestic Supply of Gold

& Uranium

R0.4bn

Final Demand

-R2.5bn

Intermediate Demand

(Inputs into Other Sectors)

R2.9bn

Primary SectorsR0bn

Secondary SectorsR1.8bn

Tertiary SectorsR1.1bn

Gross Capital

Formation-R2.5bn

25%

72%

3%

63%

33%

4%

21% 79%

House-holdsR0bn

38%

62%

0%

Govern-mentR0bn

Estimated value chain for gold and uranium ore mining in 2014

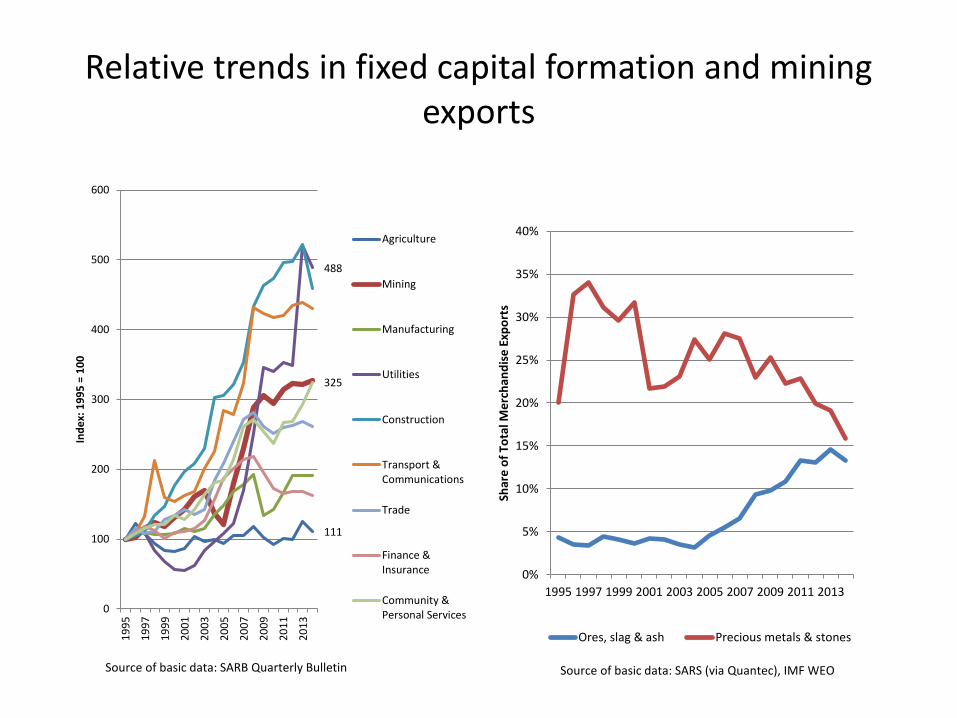

Relative trends in fixed capital formation and mining exports

0%

5%

10%

15%

20%

25%

30%

35%

40%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Shar

e o

f To

tal M

erc

han

dis

e E

xpo

rts

Ores, slag & ash Precious metals & stones

111

488

325

0

100

200

300

400

500

600

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

Ind

ex:

19

95

= 1

00

Agriculture

Mining

Manufacturing

Utilities

Construction

Transport &Communications

Trade

Finance &Insurance

Community &Personal Services

Source of basic data: SARB Quarterly Bulletin Source of basic data: SARS (via Quantec), IMF WEO

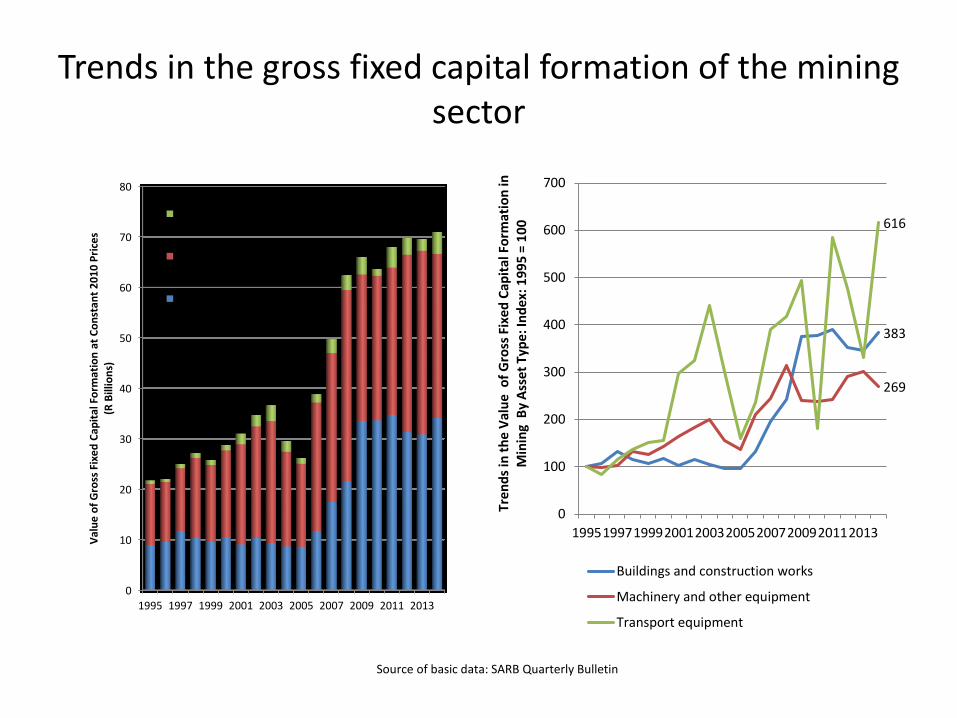

Trends in the gross fixed capital formation of the mining sector

0

10

20

30

40

50

60

70

80

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Val

ue

of

Gro

ss F

ixe

d C

apit

al F

orm

atio

n a

t C

on

stan

t 2

01

0 P

rice

s (R

Bill

ion

s)

Transport equipment

Machinery and otherequipment

Buildings and constructionworks

383

269

616

0

100

200

300

400

500

600

700

1995199719992001200320052007200920112013

Tren

ds

in t

he

Val

ue

of

Gro

ss F

ixed

Cap

ital

Fo

rmat

ion

in

Min

ing

By

Ass

et

Typ

e: I

nd

ex:

19

95

= 1

00

Buildings and construction works

Machinery and other equipment

Transport equipment

Source of basic data: SARB Quarterly Bulletin

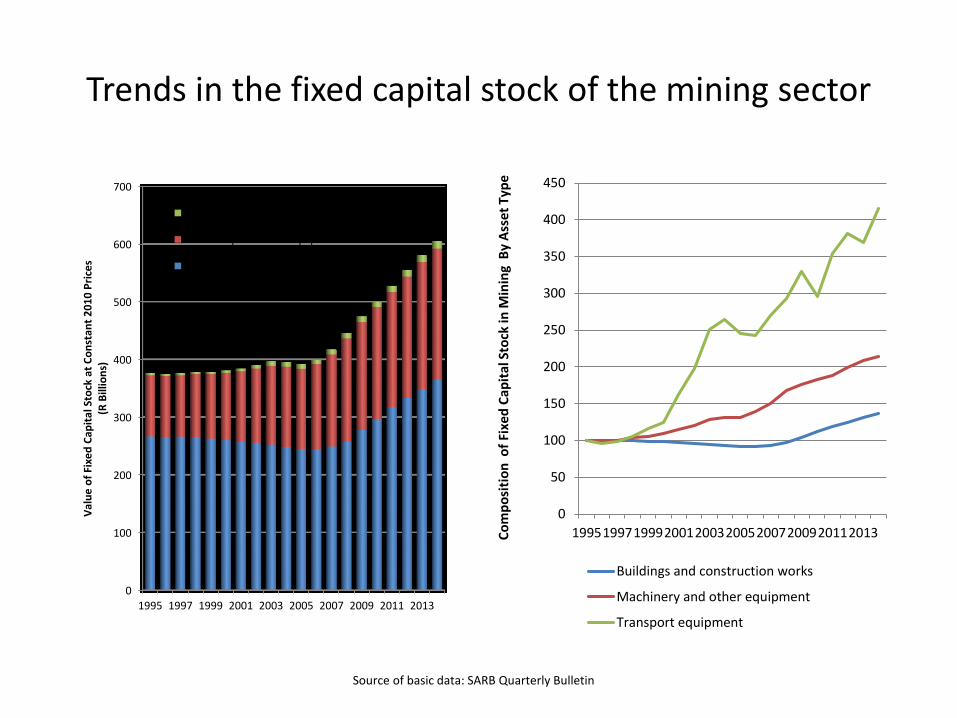

Trends in the fixed capital stock of the mining sector

0

100

200

300

400

500

600

700

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Val

ue

of

Fixe

d C

apit

al S

tock

at

Co

nst

ant

20

10

Pri

ces

(R B

illio

ns)

Transport equipment

Machinery and other equipment

Buildings and construction works

0

50

100

150

200

250

300

350

400

450

1995199719992001200320052007200920112013Co

mp

osi

tio

n o

f Fi

xed

Cap

ital

Sto

ck in

Min

ing

By

Ass

et

Typ

e

Buildings and construction works

Machinery and other equipment

Transport equipment

Source of basic data: SARB Quarterly Bulletin

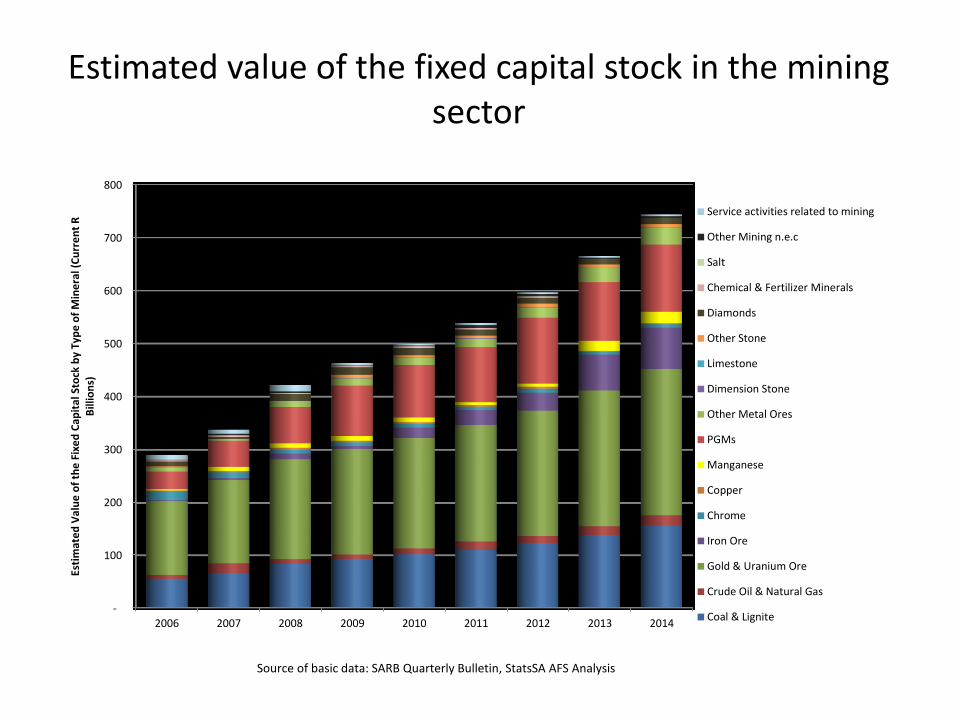

Estimated value of the fixed capital stock in the mining sector

-

100

200

300

400

500

600

700

800

2006 2007 2008 2009 2010 2011 2012 2013 2014

Esti

mat

ed

Val

ue

of

the

Fix

ed

Cap

ital

Sto

ck b

y Ty

pe

of

Min

era

l (C

urr

en

t R

B

illio

ns)

Service activities related to mining

Other Mining n.e.c

Salt

Chemical & Fertilizer Minerals

Diamonds

Other Stone

Limestone

Dimension Stone

Other Metal Ores

PGMs

Manganese

Copper

Chrome

Iron Ore

Gold & Uranium Ore

Crude Oil & Natural Gas

Coal & Lignite

Source of basic data: SARB Quarterly Bulletin, StatsSA AFS Analysis

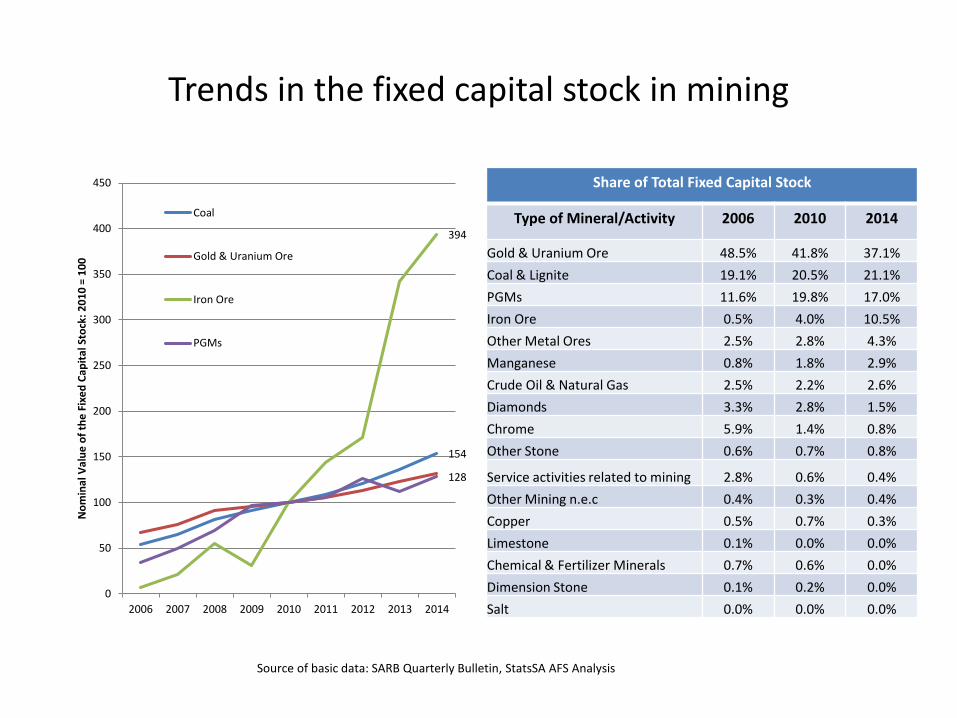

Trends in the fixed capital stock in mining

154

394

128

0

50

100

150

200

250

300

350

400

450

2006 2007 2008 2009 2010 2011 2012 2013 2014

No

min

al V

alu

e o

f th

e F

ixe

d C

apit

al S

tock

: 2

01

0 =

10

0

Coal

Gold & Uranium Ore

Iron Ore

PGMs

Share of Total Fixed Capital Stock

Type of Mineral/Activity 2006 2010 2014

Gold & Uranium Ore 48.5% 41.8% 37.1%

Coal & Lignite 19.1% 20.5% 21.1%

PGMs 11.6% 19.8% 17.0%

Iron Ore 0.5% 4.0% 10.5%

Other Metal Ores 2.5% 2.8% 4.3%

Manganese 0.8% 1.8% 2.9%

Crude Oil & Natural Gas 2.5% 2.2% 2.6%

Diamonds 3.3% 2.8% 1.5%

Chrome 5.9% 1.4% 0.8%

Other Stone 0.6% 0.7% 0.8%

Service activities related to mining 2.8% 0.6% 0.4%

Other Mining n.e.c 0.4% 0.3% 0.4%

Copper 0.5% 0.7% 0.3%

Limestone 0.1% 0.0% 0.0%

Chemical & Fertilizer Minerals 0.7% 0.6% 0.0%

Dimension Stone 0.1% 0.2% 0.0%

Salt 0.0% 0.0% 0.0%

Source of basic data: SARB Quarterly Bulletin, StatsSA AFS Analysis

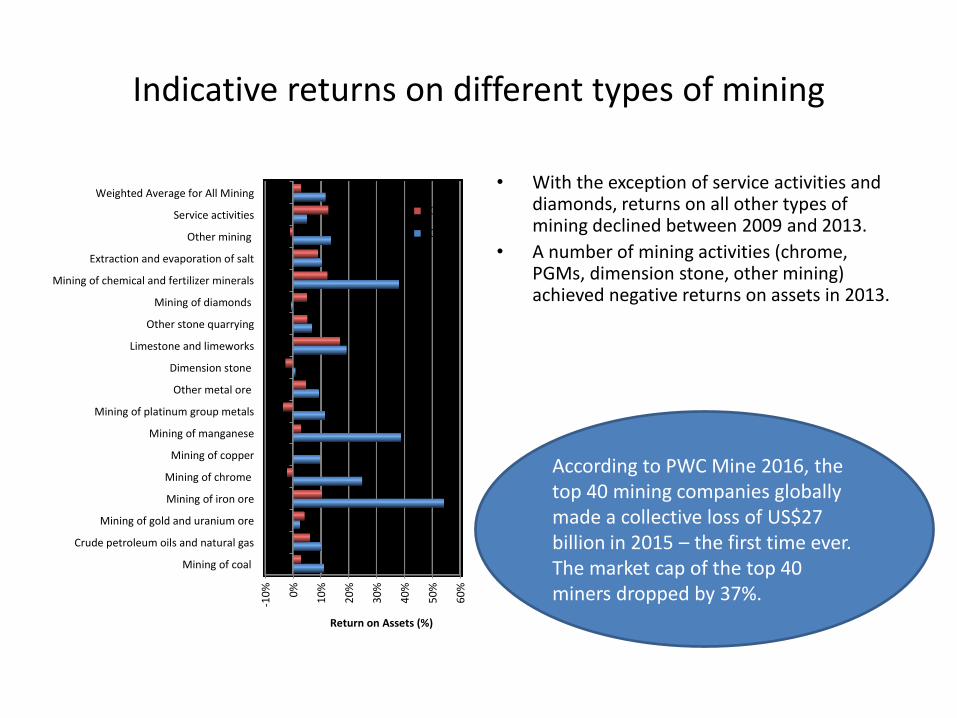

Indicative returns on different types of mining

-10

%

0%

10

%

20

%

30

%

40

%

50

%

60

%

Mining of coal

Crude petroleum oils and natural gas

Mining of gold and uranium ore

Mining of iron ore

Mining of chrome

Mining of copper

Mining of manganese

Mining of platinum group metals

Other metal ore

Dimension stone

Limestone and limeworks

Other stone quarrying

Mining of diamonds

Mining of chemical and fertilizer minerals

Extraction and evaporation of salt

Other mining

Service activities

Weighted Average for All Mining

Return on Assets (%)

2013

2009

• With the exception of service activities and diamonds, returns on all other types of mining declined between 2009 and 2013.

• A number of mining activities (chrome, PGMs, dimension stone, other mining) achieved negative returns on assets in 2013.

According to PWC Mine 2016, the top 40 mining companies globally made a collective loss of US$27 billion in 2015 – the first time ever.The market cap of the top 40 miners dropped by 37%.

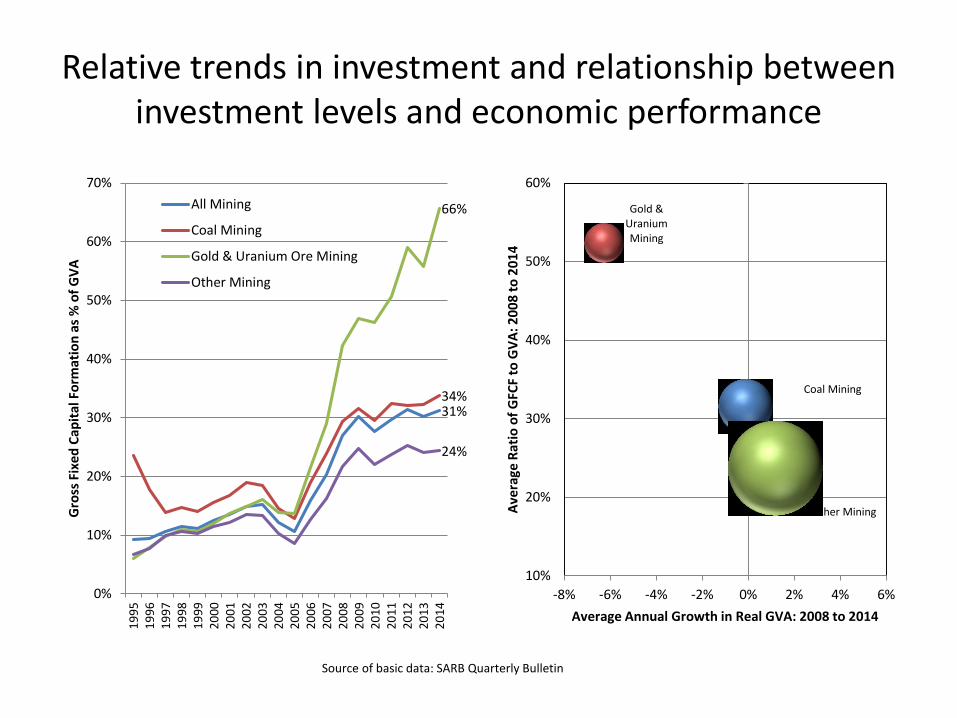

Relative trends in investment and relationship between investment levels and economic performance

31%34%

66%

24%

0%

10%

20%

30%

40%

50%

60%

70%

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Gro

ss F

ixed

Cap

ital

Fo

rmat

ion

as

% o

f G

VA

All Mining

Coal Mining

Gold & Uranium Ore Mining

Other Mining

Other Mining

Coal Mining

Gold & Uranium Mining

10%

20%

30%

40%

50%

60%

-8% -6% -4% -2% 0% 2% 4% 6%

Ave

rage

Rat

io o

f G

FCF

to G

VA

: 20

08

to

20

14

Average Annual Growth in Real GVA: 2008 to 2014

Source of basic data: SARB Quarterly Bulletin

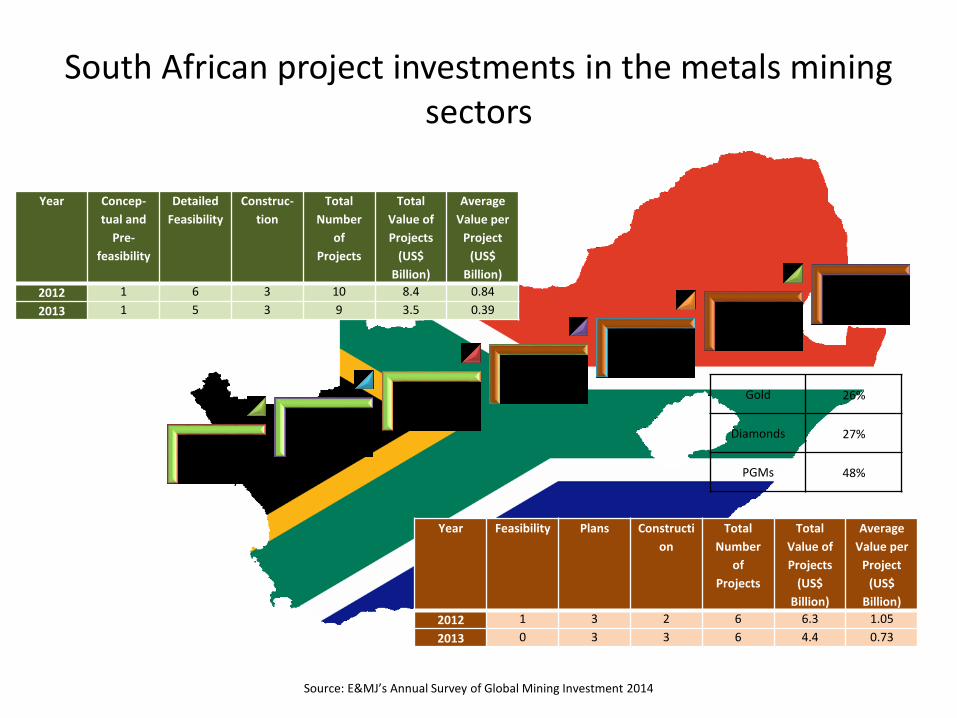

South African project investments in the metals mining sectors

Conceptual & Pre-feasibility

Feasibility

Construction

Operating -Feasibility

Operating –Plans

Operating –Construction

Other Brownfields

Source: E&MJ’s Annual Survey of Global Mining Investment 2014

Gold 26%

Diamonds 27%

PGMs 48%

Year Concep-

tual and

Pre-

feasibility

Detailed

Feasibility

Construc-

tion

Total

Number

of

Projects

Total

Value of

Projects

(US$

Billion)

Average

Value per

Project

(US$

Billion)

2012 1 6 3 10 8.4 0.84

2013 1 5 3 9 3.5 0.39

Year Feasibility Plans Constructi

on

Total

Number

of

Projects

Total

Value of

Projects

(US$

Billion)

Average

Value per

Project

(US$

Billion)

2012 1 3 2 6 6.3 1.05

2013 0 3 3 6 4.4 0.73

LOOKING FOR REASONS FOR SOUTH AFRICA’S DETERIORATING INVESTMENT PERFORMANCE

• SA still has attractive known reserves – so primary reason for location choice should still hold

• So why losing ground i.t.o. investment?– Licensing/royalty arrangements/policy uncertainty

– Energy constraints (new projects need to be self sufficient)

– High cost producer during extended commodity price downturn

– Ease of doing business

– Logistics

– Proximity to major consumer markets

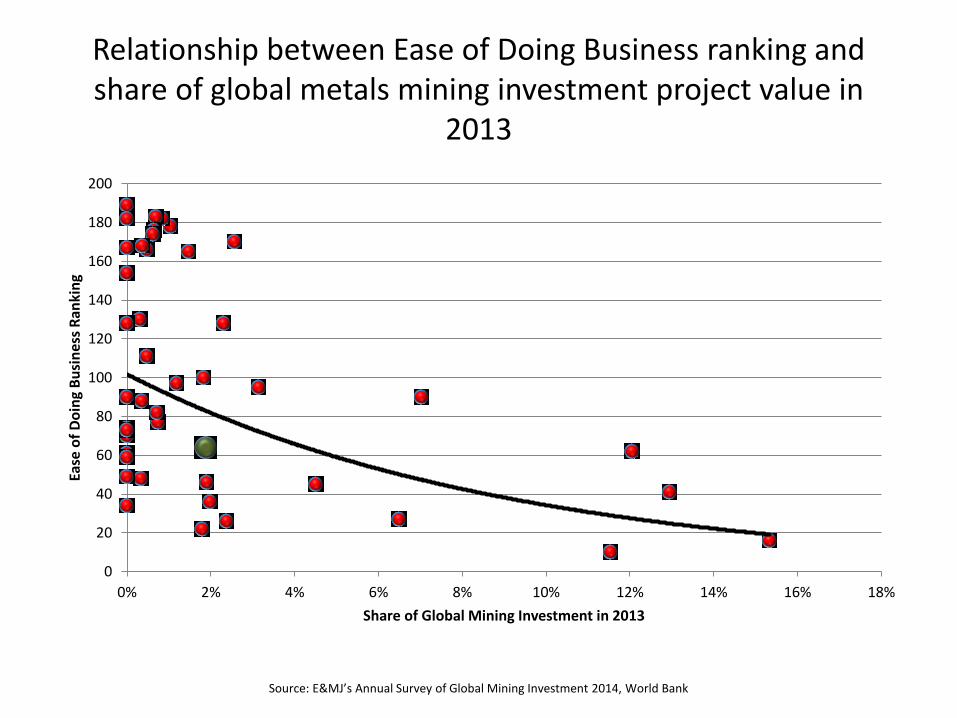

Relationship between Ease of Doing Business ranking and share of global metals mining investment project value in

2013

0

20

40

60

80

100

120

140

160

180

200

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Ease

of

Do

ing

Bu

sin

ess

Ran

kin

g

Share of Global Mining Investment in 2013

Source: E&MJ’s Annual Survey of Global Mining Investment 2014, World Bank

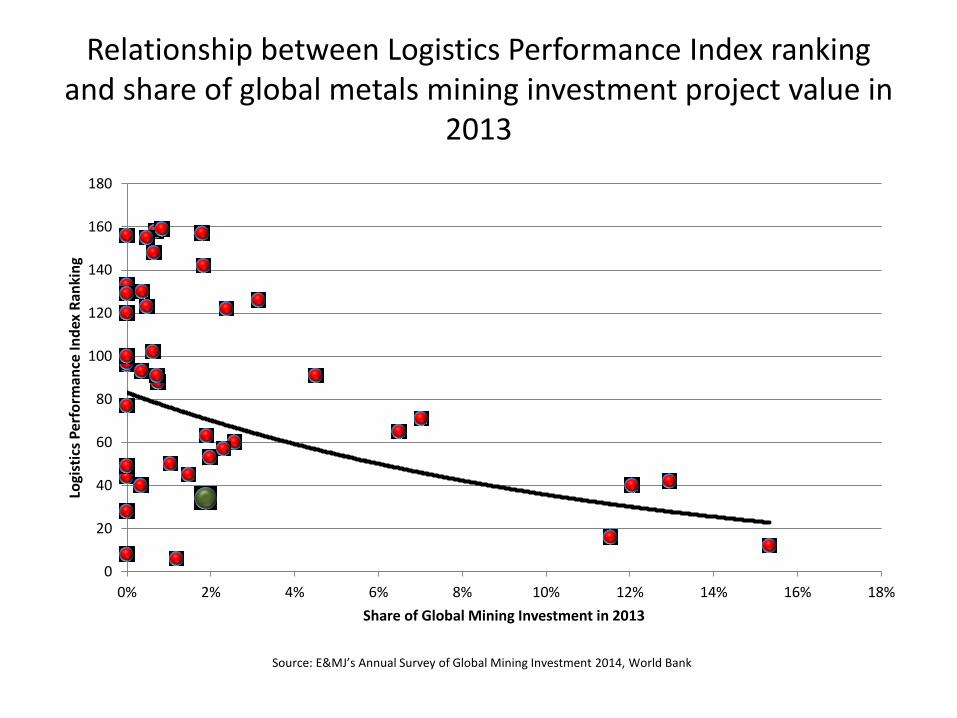

Relationship between Logistics Performance Index ranking and share of global metals mining investment project value in

2013

0

20

40

60

80

100

120

140

160

180

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Logi

stic

s P

erfo

rman

ce In

dex

Ran

kin

g

Share of Global Mining Investment in 2013

Source: E&MJ’s Annual Survey of Global Mining Investment 2014, World Bank

Conclusion

• The nascent uptick in some commodity prices seems unlikely to gain significant momentum over the medium term: the bear market seems likely to remain intact.

• A sustainable price turnaround will depend largely on supply cuts rather than a dramatic recovery in demand

• A significant recovery in global mining investment therefore still seems some years off. The nature of investment will continue to shift to sustaining investment, rather than new mines.

• Even within the context of a gloomy global environment, South Africa’s mining sector has underperformed.

• While proximity to major markets is a factor, the main reasons for the underperformance appear to have been largely self-inflicted (policy uncertainty, electricity constraints, fractious labour relations).

• Given depressed output levels, investment has been high (in some cases unsustainably so), but there is still little indication that the nature of investment is consistent with a radically changed, mechanised mining sector.