Embed Size (px)

DESCRIPTION

Citation preview

Investment Banking Division

2006

2

Abelmann Bank Divisions

Fixed Income, Currency and Commodities

Division EquitiesDivision

Investment BankingDivision

Merchant BankingDivision

Investment ManagementDivision

Legal, Compliance andManagement Controls

Division

Executive Office

Human CapitalManagement Division

Global InvestmentResearch Division

Operations, Technologyand Finance Division

Management Committee

3

Investment Banking Mission Statement

“Abelmann Bank’s Investment Banking Division identifies, structures and executes diverse and innovative public and private market transactions for corporations, financial institutions and governments.”

4

Investment Banking Organizational Structure

Investment Banking DivisionInvestment Banking DivisionInvestment Banking DivisionInvestment Banking Division

InvestmentInvestment Banking Banking

InvestmentInvestment Banking Banking

Consumer / Retail

Financial Institutions

Financial Sponsors Group

Healthcare

Industrials

Latin America

Natural Resources

Real Estate

Telecom, Media & Technology

Equity CapitalEquity CapitalMarketsMarkets

Equity CapitalEquity CapitalMarketsMarkets

Investment GradeInvestment GradeCapital MarketsCapital Markets

Investment GradeInvestment GradeCapital MarketsCapital Markets

Leveraged Leveraged FinanceFinance

Leveraged Leveraged FinanceFinance

Municipal Municipal FinanceFinance

Municipal Municipal FinanceFinance New ProductsNew ProductsNew ProductsNew Products DerivativesDerivativesDerivativesDerivatives

Common Stock

Convertibles

Private Placements

Emerging Markets

Financial Institutions / FIG Structured Finance

Investment Grade

Liability Management

Bank Loan Capital Markets

Commodity Finance

High Yield Capital Markets

Leveraged Finance

Liability Management

Restructuring / Distressed Finance

Corporate Related

Energy and Public Power

Healthcare and Higher Education

Housing

Infrastructure

Public / Private Partnerships

Equity Derivatives

Municipal Derivatives

Swaps Marketing

5

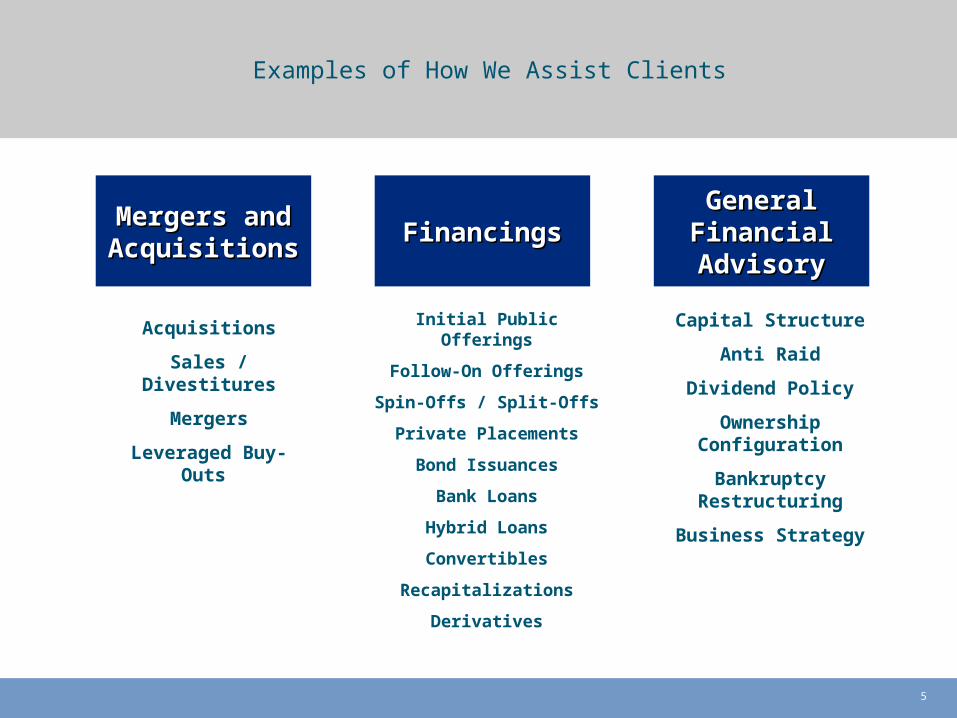

Examples of How We Assist Clients

Acquisitions

Sales / Divestitures

Mergers

Leveraged Buy-Outs

Mergers and Mergers and AcquisitionsAcquisitions

Capital Structure

Anti Raid

Dividend Policy

Ownership Configuration

Bankruptcy Restructuring

Business Strategy

Initial Public Offerings

Follow-On Offerings

Spin-Offs / Split-Offs

Private Placements

Bond Issuances

Bank Loans

Hybrid Loans

Convertibles

Recapitalizations

Derivatives

FinancingsFinancingsGeneral General

Financial Financial AdvisoryAdvisory

6

FinancingFinancingFinancingFinancingMergers & Acquisitions

Equity IssuanceEquity Issuance

Review capital requirementsReview capital requirements

Due diligence, developing the storyDue diligence, developing the storyPreliminary valuationPreliminary valuation

Drafting the prospectusDrafting the prospectusRoadshow preparationRoadshow preparation

Investor targetingInvestor targetingRoadshowRoadshow

Indicative ordersIndicative ordersBuilding the order bookBuilding the order book

PricingPricingClosingClosing

Investment Banking DivisionThe Job Experience

Phases

Planning

Investigation & assessment

Preparation

Marketing the company

Determining value

Completion

Sale of a Business

Review of owners’ objectives

Business due diligencePreliminary valuation

Writing the selling memoPrepare mgmt presentation

Buyer contactsBuyer visits

Preliminary bidsFormal bids, negotiationsFairness opinion

Merger agreementClosing

7

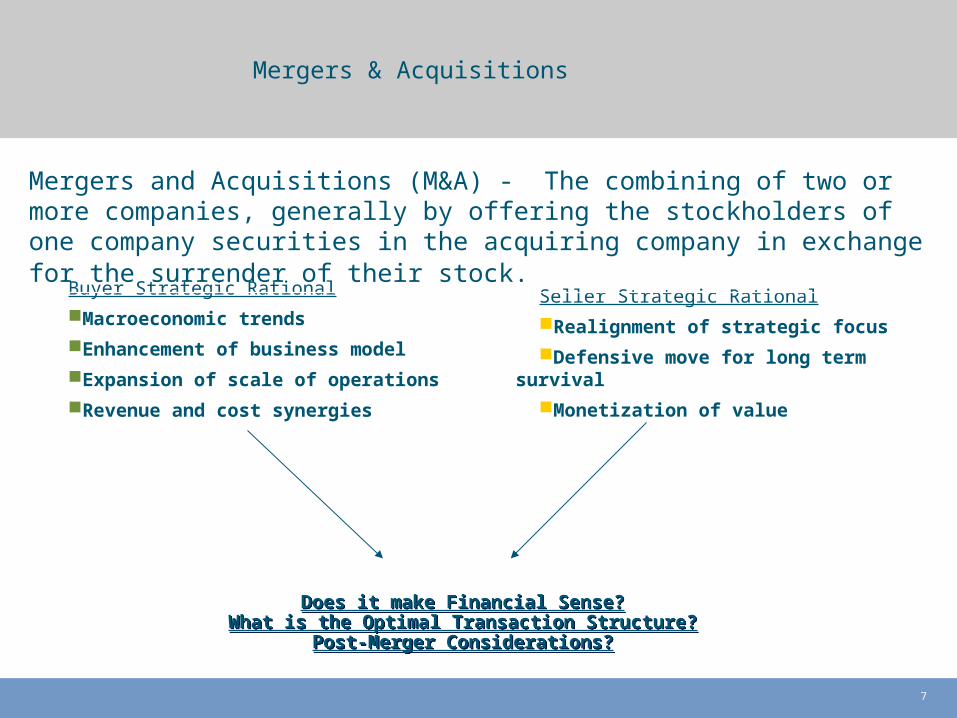

Mergers & Acquisitions

Buyer Strategic Rational

Macroeconomic trends

Enhancement of business model

Expansion of scale of operations

Revenue and cost synergies

Seller Strategic Rational

Realignment of strategic focus

Defensive move for long term survival

Monetization of value

Mergers and Acquisitions (M&A) - The combining of two or more companies, generally by offering the stockholders of one company securities in the acquiring company in exchange for the surrender of their stock.

Does it make Financial Sense?What is the Optimal Transaction Structure?

Post-Merger Considerations?

Does it make Financial Sense?What is the Optimal Transaction Structure?

Post-Merger Considerations?

8

What Is Our Role in an M&A Transaction?

Preparation Phase

Transaction Initiation

Design Phase

Negotiation Phase

Approvals/Closing

Preparation Transaction Initiation

Design Negotiation Approvals/Closing

Possible Problem

Identification

Strategic and Key Decision

Preparation

Communication Strategy

Development

Strategic and Key Decision

Preparation

Legal, Tax and structuring

Analyses

Valuation and Due Diligence Preparation

Deal and Legal Structuring

Initial Contact

Strategic Plan

Due Diligence

Valuation Refinement

PricingStructure

Preliminary Internal

Approvals

Negotiation and

Due Diligence

Documentation

Preliminary Regulatory Approvals

Others

Final Approvals and

Communications

Final External Approvals and

Communications

9

Leveraged Buyout (LBO)

Debt $25

Equity $75

5 years later$100

Debt $75

Equity $25

Today$100

Use little equity and borrowed funds (leverage) to buy asset

Pay down debt over time

All excess returns accrue to the equity

IRR = 25%

Leveraged Buyout (LBO) - The acquisition of a business utilizing both debt and equity financing sources, with the debt component representing the more significant amount. The equity component is often contributed from a financial sponsor or private equity firm with the debt component raised in the bank loan and / or high yield financing markets.

10

What Is Capital Markets?

Capital Markets seeks to balance the interests of investors and issuers to achieve successful offerings

Sellers/IssuersSellers/Issuers

AT&T Wireless

Freescale

Deutsche Telekom

General Electric

State of New York

Prudential

Buyers/InvestorsBuyers/Investors

Alliance

Capital

Fidelity

Janus

PIMCO

Putnam

Investment Investment BankingBanking

Sales and Sales and TradingTrading

Chinese WallChinese Wall

High Price Low Price

Capital MarketsCapital Markets

Advice and Judgment

Products

Solicitation

Allocation

Pricing

Marketing

Aftermarket Support

11

Financing: Initial Public Offering (IPO)

IPO (Initial Public Offering) - Transfers a portion of a company’s ownership from a few private stakeholders to many public shareholders

Strategic Advantages

New Capital

Future Capital

Liquidity

Cashing Out

Employee Compensation

Strategic Disadvantages

Profit-sharing/Loss of Control

Loss of Confidentiality

Reporting and Fiduciary Responsibilities

IPO Expenses

Legal Liability

12

What Is Our Role in an IPO?

Solicitation

Internal ApprovalDue Diligence

Preliminary Filing

StructuringRoadshow Preparation

Roadshow / Marketing

Pricing and Offering

Aftermarket Trading

13

The Investment Grade Bond New Issue ProcessA Multi-Pronged Approach

Morning Market Update Call with

Client to Decide “Go or No-Go”

Announce Deal to the Market

Hold Investor Conference Call(If Necessary)

Release Price Talk and Confirm Orders

Price Transaction and Cross Treasuries with

Investors

A High Yield Offering follows a similar process although after the deal is announced there is typically a multi-day roadshow to market to investors

14

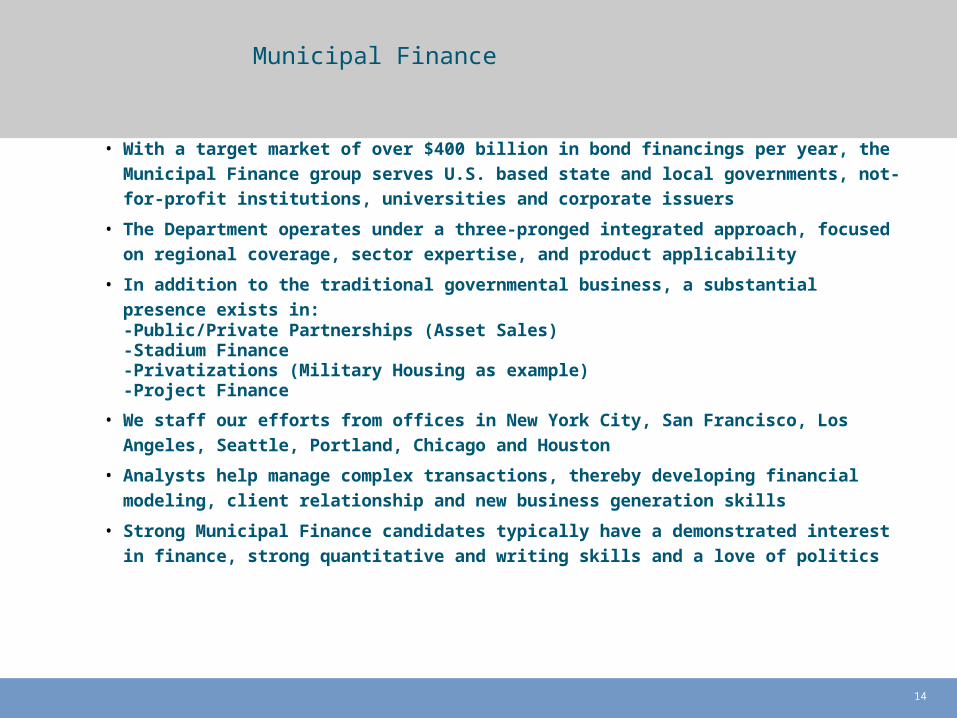

• With a target market of over $400 billion in bond financings per year, the Municipal

Finance group serves U.S. based state and local governments, not-for-profit

institutions, universities and corporate issuers

• The Department operates under a three-pronged integrated approach, focused on

regional coverage, sector expertise, and product applicability

• In addition to the traditional governmental business, a substantial presence exists

in:-Public/Private Partnerships (Asset Sales)-Stadium Finance-Privatizations (Military Housing as example)-Project Finance

• We staff our efforts from offices in New York City, San Francisco, Los Angeles,

Seattle, Portland, Chicago and Houston

• Analysts help manage complex transactions, thereby developing financial

modeling, client relationship and new business generation skills

• Strong Municipal Finance candidates typically have a demonstrated interest in

finance, strong quantitative and writing skills and a love of politics

Municipal Finance

15

Role of an Investment Banker

Investment Bankers Are Not… But We Do…

Consultants that are tasked with analyzing market share, generating new product ideas, etc.

Analyze a company’s strategic position relative to peers and assess its viability going forward

Accountants that audit a company’s financial statements and sign-off on their validity

“Sanity check” a company’s financials and use them to derive a valuation

Lawyers who understand every comma and “whereas” in a merger agreement or covenant package

Understand all of the major items in legal agreements that will affect our clients

Operators who analyze internal processes and suggest opportunities for improvement

Compare a client’s operations to that of its peers and communicate major differences

16

Roles & Responsibilities

AssociateAssociate

Vice Vice PresidentPresident

Managing DirectorManaging Director

AnalystAnalyst

OwnsOwnsthe Analytics/the Analytics/

ProcessProcess

Leads the ProjectLeads the Project

Becomes Becomes the Trusted the Trusted Advisor to Advisor to the Clientthe Client

Analytics / WritingAnalytics / Writing

17

• Internal Meetings

• Client Meetings

• Financial Modeling

• Competitive/Market Analysis

• Due Diligence

• Presentation Books

• Memorandums / Proposals

• Marketing Materials

• Road Shows

The Role of an Analyst Day to Day Tasks

18

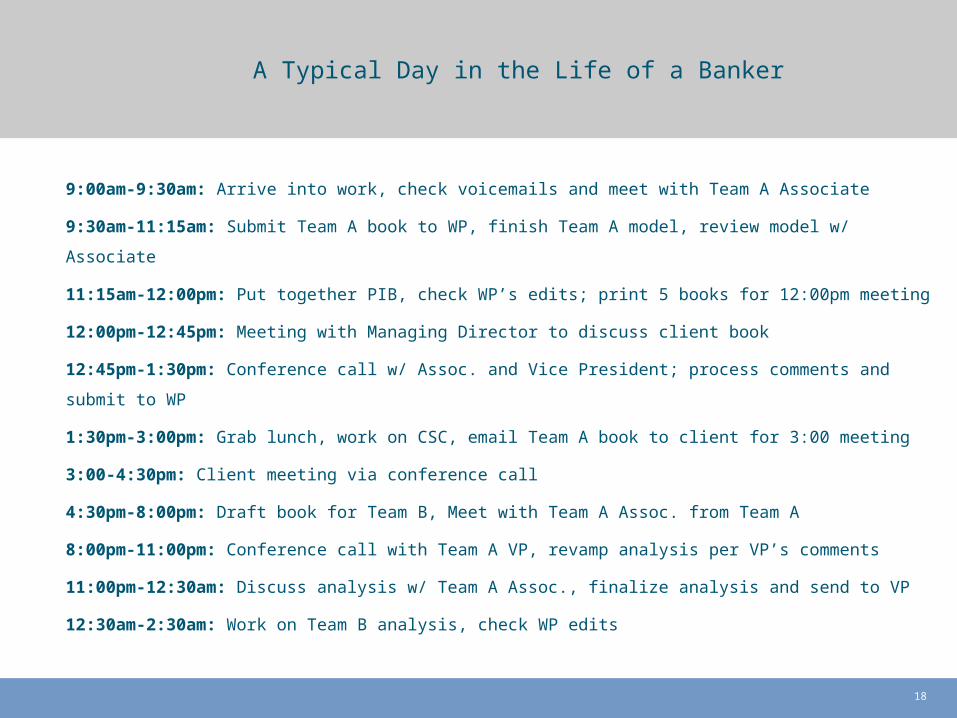

A Typical Day in the Life of a Banker

9:00am-9:30am: Arrive into work, check voicemails and meet with Team A Associate

9:30am-11:15am: Submit Team A book to WP, finish Team A model, review model w/ Associate

11:15am-12:00pm: Put together PIB, check WP’s edits; print 5 books for 12:00pm meeting

12:00pm-12:45pm: Meeting with Managing Director to discuss client book

12:45pm-1:30pm: Conference call w/ Assoc. and Vice President; process comments and submit to WP

1:30pm-3:00pm: Grab lunch, work on CSC, email Team A book to client for 3:00 meeting

3:00-4:30pm: Client meeting via conference call

4:30pm-8:00pm: Draft book for Team B, Meet with Team A Assoc. from Team A

8:00pm-11:00pm: Conference call with Team A VP, revamp analysis per VP’s comments

11:00pm-12:30am: Discuss analysis w/ Team A Assoc., finalize analysis and send to VP

12:30am-2:30am: Work on Team B analysis, check WP edits

19

A Day in the Life . . . No Day is the Same!Capital Markets

Arrive between 7:00 and 7:30am. Breakfast! CCM: Attend IG/HY morning meetings to get

update on current business activity, new issue calendar, trading activity

ECM: Listen to morning call – updates on current business activity, research comments and ECM deal updates

Read news and sports headlines, check Treasury levels, Futures and economic releases for the day

Make out-going calls to clients, update them on market activity and discuss their current financing plans

CCM: Due diligence call for bond deal. Talk with syndicate desk to get updated pricing for potential acquisition financing

ECM: Confirm roadshow schedules / begin gathering feedback. Attend block trade meeting to discuss upcoming trade

Draft executive summary for upcoming pitch

Early Morning: 7:00am – 9:30amEarly Morning: 7:00am – 9:30am

Evening: 5pm to ??Evening: 5pm to ??

Mid-Morning: 9:30am – 12:00pmMid-Morning: 9:30am – 12:00pm

Afternoon: 12:00pm – 5:00pmAfternoon: 12:00pm – 5:00pm The real work begins! Continue working on client presentations Go to gym and grab dinner

Attend meeting with banking team to review presentation for meeting later in the week

CCM: Post clients via email/calls on Bernanke testimony and Treasury market reaction. Finalize term sheet for leveraged loan financing pitch. Work with Liability Management desk on tender/refinancing analysis

ECM: Continue calls to salesforce to further flush out valuation feedback. Work with traders to come up with bid for block trade after the close. Work with sales / sales traders on allocations for transaction that is pricing

20

Solving Clients’ Most Important Strategic and Financial Issues

Exposure to Top-Level Decision Making/Senior Client Exposure

Fast-Paced Environment With Immediate Tangible Results

Ability to Make an Impact Early in One’s Career

Dynamic/Diverse Colleagues

Solid Business Foundation for Future Endeavors

Work Hard/Play Hard

Why Investment Banking?

21

Academics Grades Not Just Econ Majors Test Scores

Extracurriculars Leadership Initiative Energy Level

Job Experience Responsibilities Purpose What Did You Learn

We look for well-rounded candidates who have excelled in three main categories:

Personal Characteristics Mature Team Oriented Self Motivated Detail Oriented Analytical “Passion”

Questions we ask ourselves Is this person a good fit for

Abelmann Bank? Is Abelmann Bank the right

environment for this person? Will this person grow and thrive at

Abelmann Bank?

What We Look For