Embed Size (px)

Citation preview

is the grass greener?

Property | international opportunities

40

Investing in New Zealand —

is the grass greener?The advantages of investing in New Zealand are clear: no stamp duty, strong rental demand and enormous potential for capital growth. But how easy is it to buy property in New Zealand? And is it worth the hassle of managing a foreign property?

Property | international opportunities

41

Investing in New Zealand —

New Zealand offers an attractive lifestyle, with clean air, close-knit communities and thriving

metropolitan centres set against a backdrop of sprawling landscapes.

With a growing population and increasing rental demand, the country is attracting Australian investors in droves; in regional areas, at least, Australians are proving to be the dominant force in the property market.

“We had a number of Australian investors, when the market was down six or seven months ago, coming into the market and buying in our provincial towns,” says Murray Cleland, president of the Real Estate Institute of New Zealand (REINZ).

“Now that values have shot up, that activity has flattened off a bit, but I imagine the investors that got in there earlier will be making some good capital gains if they chose to sell now.”

About New ZealandStatistics NZ estimates that there are 4.18 million people living in New Zealand, in approximately 1.47 million residential dwellings (up from 1.27m in

1996). According to the New Zealand Property Investors Federation, around 170,000 investors own 400,000 of these properties.

Unemployment rates are steady at a low 3.8%, which, together with strong domestic demand and foreign investment, has been underpinning a strong economy.

The Reserve Bank of New Zealand is increasing cash rates to try and dampen growth – most recently, and largely unexpectedly, in June this year – but it has had little effect so far.

“I think it’s too early to see the effect of the interest rate rises we’ve had this year,” Cleland says. “The housing market in New Zealand traditionally slows through the winter period, but I think in the next month or two we will start to see the real effects of these interest rate rises.”

Strong growthAccording to REINZ, median property prices have more than doubled nationally in the last decade, climbing steadily from just NZ$164,000 in May 1997 to NZ$350,000 in May this year.

42

Property | international opportunities

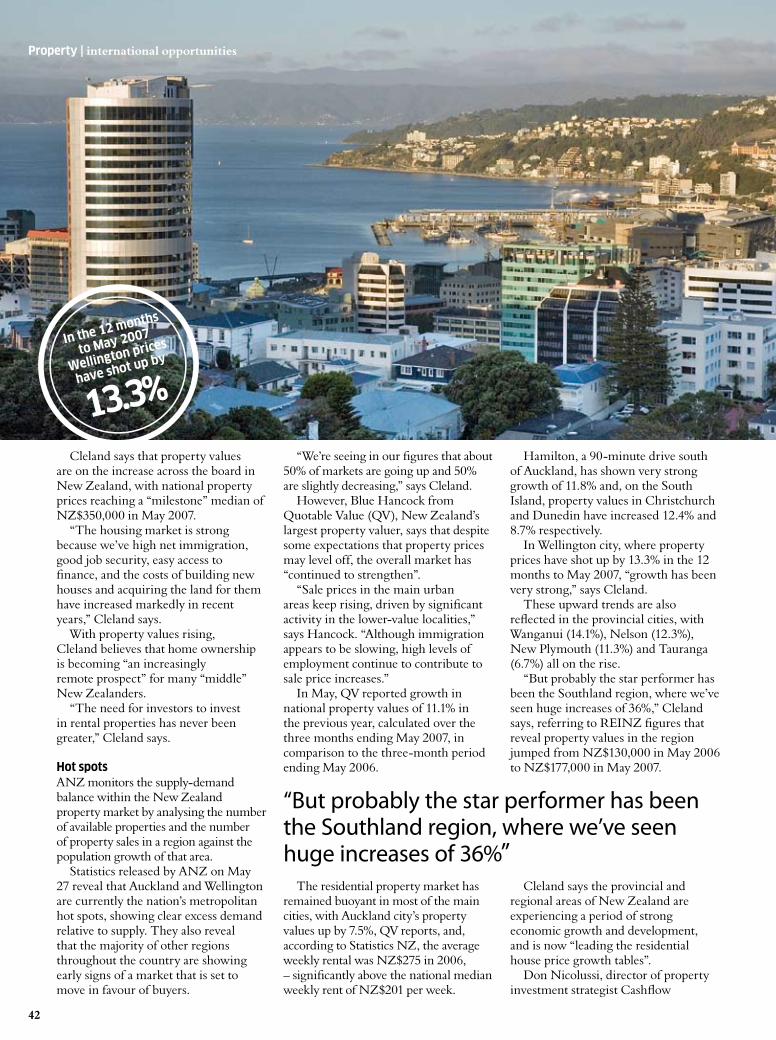

Cleland says that property values are on the increase across the board in New Zealand, with national property prices reaching a “milestone” median of NZ$350,000 in May 2007.

“The housing market is strong because we’ve high net immigration, good job security, easy access to finance, and the costs of building new houses and acquiring the land for them have increased markedly in recent years,” Cleland says.

With property values rising, Cleland believes that home ownership is becoming “an increasingly remote prospect” for many “middle” New Zealanders.

“The need for investors to invest in rental properties has never been greater,” Cleland says.

Hot spotsANZ monitors the supply-demand balance within the New Zealand property market by analysing the number of available properties and the number of property sales in a region against the population growth of that area.

Statistics released by ANZ on May 27 reveal that Auckland and Wellington are currently the nation’s metropolitan hot spots, showing clear excess demand relative to supply. They also reveal that the majority of other regions throughout the country are showing early signs of a market that is set to move in favour of buyers.

“We’re seeing in our figures that about 50% of markets are going up and 50% are slightly decreasing,” says Cleland.

However, Blue Hancock from Quotable Value (QV), New Zealand’s largest property valuer, says that despite some expectations that property prices may level off, the overall market has “continued to strengthen”.

“Sale prices in the main urban areas keep rising, driven by significant activity in the lower-value localities,” says Hancock. “Although immigration appears to be slowing, high levels of employment continue to contribute to sale price increases.”

In May, QV reported growth in national property values of 11.1% in the previous year, calculated over the three months ending May 2007, in comparison to the three-month period ending May 2006.

The residential property market has remained buoyant in most of the main cities, with Auckland city’s property values up by 7.5%, QV reports, and, according to Statistics NZ, the average weekly rental was NZ$275 in 2006, – significantly above the national median weekly rent of NZ$201 per week.

Hamilton, a 90-minute drive south of Auckland, has shown very strong growth of 11.8% and, on the South Island, property values in Christchurch and Dunedin have increased 12.4% and 8.7% respectively.

In Wellington city, where property prices have shot up by 13.3% in the 12 months to May 2007, “growth has been very strong,” says Cleland.

These upward trends are also reflected in the provincial cities, with Wanganui (14.1%), Nelson (12.3%), New Plymouth (11.3%) and Tauranga (6.7%) all on the rise.

“But probably the star performer has been the Southland region, where we’ve seen huge increases of 36%,” Cleland says, referring to REINZ figures that reveal property values in the region jumped from NZ$130,000 in May 2006 to NZ$177,000 in May 2007.

Cleland says the provincial and regional areas of New Zealand are experiencing a period of strong economic growth and development, and is now “leading the residential house price growth tables”.

Don Nicolussi, director of property investment strategist Cashflow

“But probably the star performer has been the Southland region, where we’ve seen huge increases of 36%”

13.3%

In the 12 months

to May 2007

Wellington prices

have shot up by

43

Properties, says there are excellent investment opportunities available to those who are willing to look in regional locations.

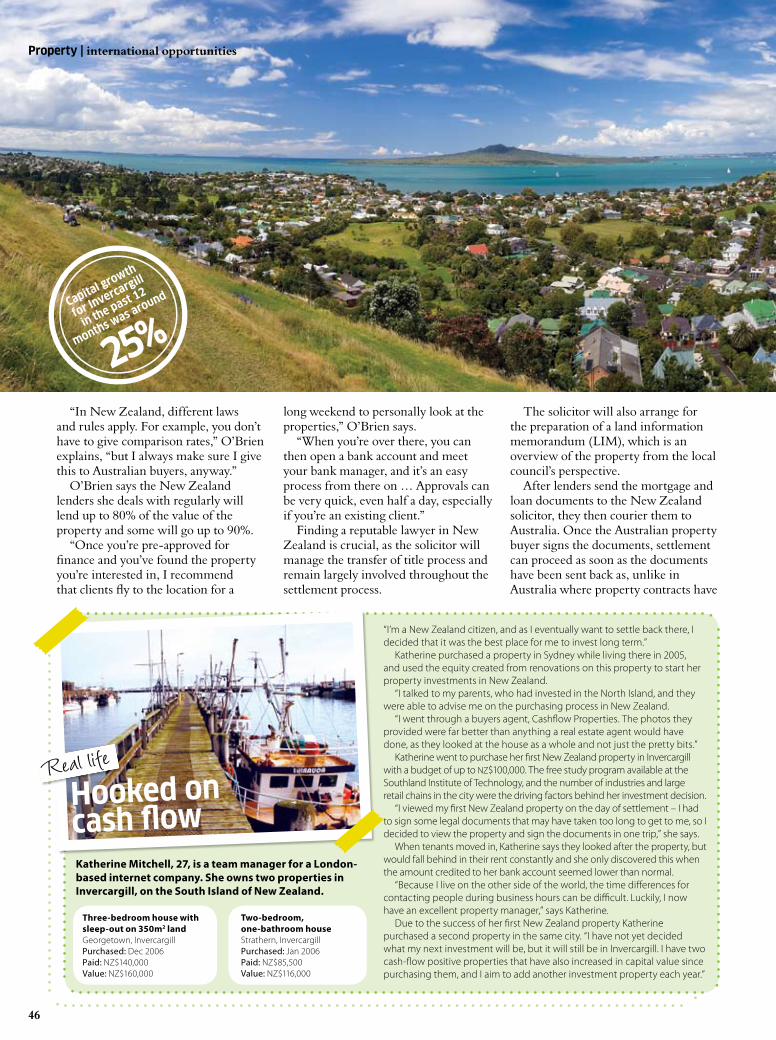

“We try to focus on regions with strong economic fundamentals,” says Nicolussi. “We live in Invercargill, and we’re surrounded by some great opportunities. Annualised capital growth for Invercargill was around 25% in the past 12 months and there’s no sign of a slow-down.”

Investing in InvercargillInvercargill, New Zealand’s southern-most town, is the commercial hub of the agricultural region Southland. In the growing regional city, population 50,000, investors can still access genuine cash-flow positive opportunities.

“Even though there has been significant growth in property here in New Zealand, there’re still plenty of opportunities available, such as in Invercargill,” says Nicolussi. “Rental yields are a lot higher than in Australia at the moment.”

A two-bedroom unit in the city centre is currently on the market for NZ$95,000 and a three-bedroom house in tidy condition is NZ$160,000. Just a 20-minute drive south of Invercargill, a three-bedroom house is asking NZ$101,000, while a two-and-a-half-bedroom house in nearby Bluff will set you back just NZ$86,000 – with a rental assessment of NZ$140 per week.

Property values in Invercargill are sharply moving upwards after the town fought back from a declining population in the 1990s and transformed itself, using innovative ideas and community funding to attract residents and

visitors to the city. “In the early 1990s, Invercargill had the highest rate of population decline of any city in New Zealand or Australia,” says Tim Shadbolt, Mayor of Invercargill.

In the 1960s, Keith Richards of The Rolling Stones made the infamous comment, when passing through Invercargill, that it was the “arsehole of the world”. Shadbolt, however, has employed drastic measures to reverse the negative view of the region.

The combined coffers of the Invercargill City Council, the Invercargill Licensing Trust and the Community Trust of Southland unlocked an “unprecedented, incredibly high level of community wealth”, Shadbolt says, and the

Property | international opportunities

$Exchange rateThe Australian dollar is currently worth NZ$1.1043*, which effectively gives you a 10% discount when purchasing a property in New Zealand. Keep in mind, however, that your investment is vulnerable to dollar fluctuations – so if the Kiwi dollar weakens, so does the effective value of your property. Visit the Reserve Bank of Australia website (www.rba.gov.au) to access up-to-date currency rates.

*Source: Reserve Bank of Australia as at 10 July, 2007

Median property prices have more than doubled nationally in the last decade!

44

Property | international opportunities

that he has seen reverse a negative population trend.

And, according to Nicolussi, the growth is set to continue. “A New Zealand company is currently drilling for oil just outside town, and the tenders for drilling rights in the south sea basin just off the coast near Bluff are soon to be announced,” says Nicolussi. “The Invercargill property market has just really started to boom.”

The buying process

Although New Zealand is a foreign country, similar legal, banking and regulatory environments allow Australians to invest in property without too much trouble.

Most Australian financial institutions are reluctant to let you borrow against a New Zealand property, although there are some Australian lenders and banks – particularly those with partner companies in New Zealand – who may be willing to finance your purchase.

However, it is relatively easy to secure finance with one of the New Zealand banks, says mortgage broker Mary O’Brien from New Zealand Mortgage Solutions.

She warns that investors should protect themselves by finding a broker that understands the state laws in Australia and applicable New Zealand laws.

unique, integrated structure of Invercargill’s “Big Three” has since been instrumental in “everything that’s happened in this city”.

The Southern Institute of Technology (SIT) began offering free tertiary education to New Zealand citizens under their Zero Fees scheme in 2001, boosting student numbers from around 1,400 in 2000 to 4,500 in 2004. It has been a huge drawcard for Invercargill that, due to funding provided by the Big Three, no other education provider in New Zealand could match.

“The zero-fee tertiary education scheme brings about 4,000 students – and potential tenants – to the city each year,” says Nicolussi.

With the city’s investment in top-notch facilities, such as the world-class Splash Palace aquatic centre in 1997, Southland Stadium in 2000, the recent NZ$16m Civic Theatre upgrade and completion of the final stage of the NZ$9.5m Rugby Park expected this year, Invercargill now has more resources and facilities than any other town of its size in the country.

KPMG Australasian demographer Bernard Salt lauds Invercargill as a unique success story, being the only Australasian local authority area in his 27 years of tracking population trends

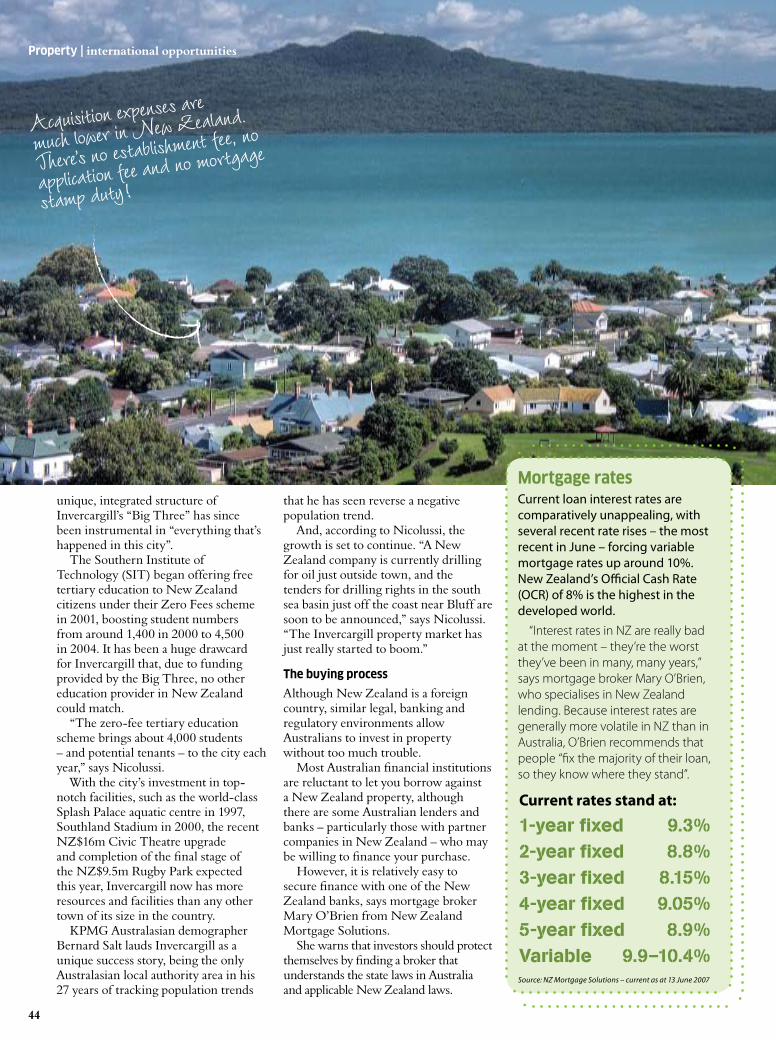

Current rates stand at:

1-year fixed 9.3%2-year fixed 8.8%3-year fixed 8.15%4-year fixed 9.05%5-year fixed 8.9%Variable 9.9–10.4%

Mortgage ratesCurrent loan interest rates are comparatively unappealing, with several recent rate rises – the most recent in June – forcing variable mortgage rates up around 10%. New Zealand’s Official Cash Rate (OCR) of 8% is the highest in the developed world.

“Interest rates in NZ are really bad at the moment – they’re the worst they’ve been in many, many years,” says mortgage broker Mary O’Brien, who specialises in New Zealand lending. Because interest rates are generally more volatile in NZ than in Australia, O’Brien recommends that people “fix the majority of their loan, so they know where they stand”.

Property | international opportunities

Source: NZ Mortgage Solutions – current as at 13 June 2007

Acquisition expenses are

much lower in New Zealand.

There’s no establishment fee, no

application fee and no mortgage

stamp duty!

Property | international opportunities

45

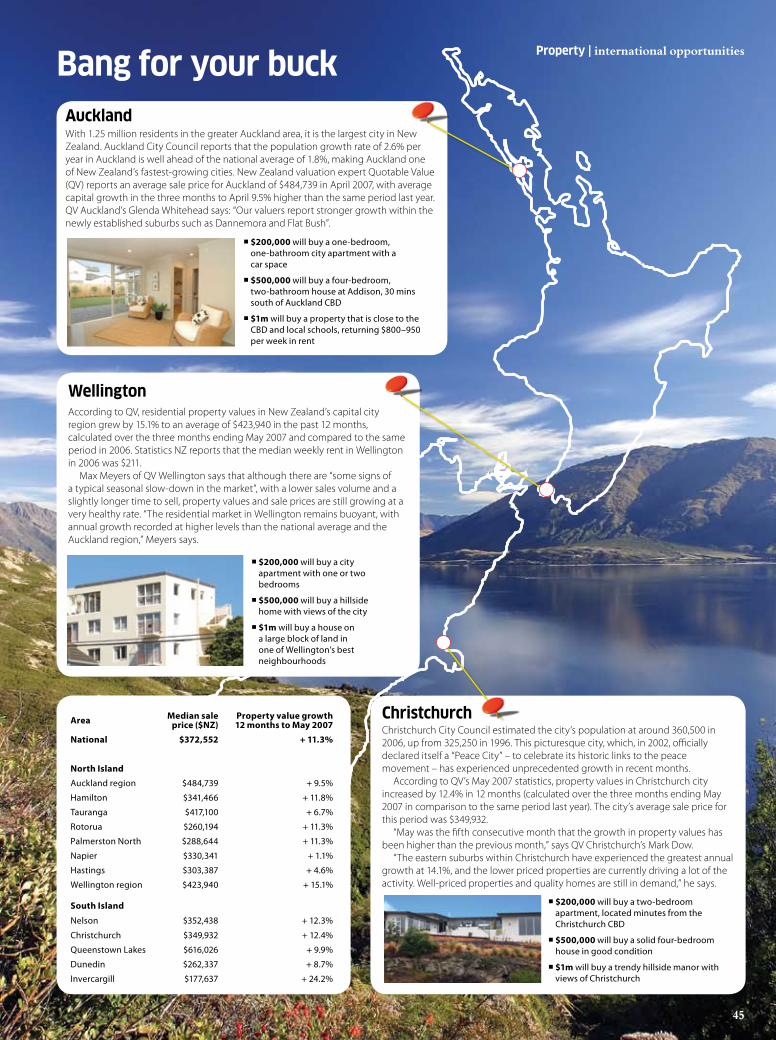

Bang for your buckAucklandWith 1.25 million residents in the greater Auckland area, it is the largest city in New Zealand. Auckland City Council reports that the population growth rate of 2.6% per year in Auckland is well ahead of the national average of 1.8%, making Auckland one of New Zealand’s fastest-growing cities. New Zealand valuation expert Quotable Value (QV) reports an average sale price for Auckland of $484,739 in April 2007, with average capital growth in the three months to April 9.5% higher than the same period last year. QV Auckland’s Glenda Whitehead says: “Our valuers report stronger growth within the newly established suburbs such as Dannemora and Flat Bush”.

ChristchurchChristchurch City Council estimated the city’s population at around 360,500 in 2006, up from 325,250 in 1996. This picturesque city, which, in 2002, officially declared itself a “Peace City” – to celebrate its historic links to the peace movement – has experienced unprecedented growth in recent months.

According to QV’s May 2007 statistics, property values in Christchurch city increased by 12.4% in 12 months (calculated over the three months ending May 2007 in comparison to the same period last year). The city’s average sale price for this period was $349,932.

“May was the fifth consecutive month that the growth in property values has been higher than the previous month,” says QV Christchurch’s Mark Dow.

“The eastern suburbs within Christchurch have experienced the greatest annual growth at 14.1%, and the lower priced properties are currently driving a lot of the activity. Well-priced properties and quality homes are still in demand,” he says.

$200,000 will buy a one-bedroom, one-bathroom city apartment with a car space

$500,000 will buy a four-bedroom, two-bathroom house at Addison, 30 mins south of Auckland CBD

$1m will buy a property that is close to the CBD and local schools, returning $800–950 per week in rent

$200,000 will buy a two-bedroom apartment, located minutes from the Christchurch CBD

$500,000 will buy a solid four-bedroom house in good condition

$1m will buy a trendy hillside manor with views of Christchurch

WellingtonAccording to QV, residential property values in New Zealand’s capital city region grew by 15.1% to an average of $423,940 in the past 12 months, calculated over the three months ending May 2007 and compared to the same period in 2006. Statistics NZ reports that the median weekly rent in Wellington in 2006 was $211.

Max Meyers of QV Wellington says that although there are “some signs of a typical seasonal slow-down in the market”, with a lower sales volume and a slightly longer time to sell, property values and sale prices are still growing at a very healthy rate. “The residential market in Wellington remains buoyant, with annual growth recorded at higher levels than the national average and the Auckland region,” Meyers says.

$200,000 will buy a city apartment with one or two bedrooms

$500,000 will buy a hillside home with views of the city

$1m will buy a house on a large block of land in one of Wellington’s best neighbourhoods

Area Median sale price ($NZ)

Property value growth12 months to May 2007

National $372,552 + 11.3%

North Island

Auckland region $484,739 + 9.5%

Hamilton $341,466 + 11.8%

Tauranga $417,100 + 6.7%

Rotorua $260,194 + 11.3%

Palmerston North $288,644 + 11.3%

Napier $330,341 + 1.1%

Hastings $303,387 + 4.6%

Wellington region $423,940 + 15.1%

South Island

Nelson $352,438 + 12.3%

Christchurch $349,932 + 12.4%

Queenstown Lakes $616,026 + 9.9%

Dunedin $262,337 + 8.7%

Invercargill $177,637 + 24.2%

46

Property | international opportunitiesProperty | international opportunities

long weekend to personally look at the properties,” O’Brien says.

“When you’re over there, you can then open a bank account and meet your bank manager, and it’s an easy process from there on … Approvals can be very quick, even half a day, especially if you’re an existing client.”

Finding a reputable lawyer in New Zealand is crucial, as the solicitor will manage the transfer of title process and remain largely involved throughout the settlement process.

The solicitor will also arrange for the preparation of a land information memorandum (LIM), which is an overview of the property from the local council’s perspective.

After lenders send the mortgage and loan documents to the New Zealand solicitor, they then courier them to Australia. Once the Australian property buyer signs the documents, settlement can proceed as soon as the documents have been sent back as, unlike in Australia where property contracts have

25%Capital growth

for Invercargill

in the past 12

months was around

“In New Zealand, different laws and rules apply. For example, you don’t have to give comparison rates,” O’Brien explains, “but I always make sure I give this to Australian buyers, anyway.”

O’Brien says the New Zealand lenders she deals with regularly will lend up to 80% of the value of the property and some will go up to 90%.

“Once you’re pre-approved for finance and you’ve found the property you’re interested in, I recommend that clients fly to the location for a

Three-bedroom house with sleep-out on 350m2 landGeorgetown, InvercargillPurchased: Dec 2006Paid: NZ$140,000Value: NZ$160,000

“I’m a New Zealand citizen, and as I eventually want to settle back there, I decided that it was the best place for me to invest long term.”

Katherine purchased a property in Sydney while living there in 2005, and used the equity created from renovations on this property to start her property investments in New Zealand.

“I talked to my parents, who had invested in the North Island, and they were able to advise me on the purchasing process in New Zealand.

“I went through a buyers agent, Cashflow Properties. The photos they provided were far better than anything a real estate agent would have done, as they looked at the house as a whole and not just the pretty bits.”

Katherine went to purchase her first New Zealand property in Invercargill with a budget of up to NZ$100,000. The free study program available at the Southland Institute of Technology, and the number of industries and large retail chains in the city were the driving factors behind her investment decision.

“I viewed my first New Zealand property on the day of settlement – I had to sign some legal documents that may have taken too long to get to me, so I decided to view the property and sign the documents in one trip,” she says.

When tenants moved in, Katherine says they looked after the property, but would fall behind in their rent constantly and she only discovered this when the amount credited to her bank account seemed lower than normal.

“Because I live on the other side of the world, the time differences for contacting people during business hours can be difficult. Luckily, I now have an excellent property manager,” says Katherine.

Due to the success of her first New Zealand property Katherine purchased a second property in the same city. “I have not yet decided what my next investment will be, but it will still be in Invercargill. I have two cash-flow positive properties that have also increased in capital value since purchasing them, and I aim to add another investment property each year.”

Hooked on cash flowKatherine Mitchell, 27, is a team manager for a London-based internet company. She owns two properties in Invercargill, on the South Island of New Zealand.

Real life

Two-bedroom, one-bathroom houseStrathern, InvercargillPurchased: Jan 2006Paid: NZ$85,500Value: NZ$116,000

a fixed settlement date, the NZ solicitor can settle the transaction “any time he or she likes”, says O’Brien.

“The solicitor decides when you settle – it can be within 24 hours,” says O’Brien. “The average is about four weeks, but it depends on the vendor. Many times I’ve had clients with coastal properties that are being subdivided and it can be 12 months just for title transfer.”

Acquisition costsAcquisition expenses are generally much lower in New Zealand than in Australia. “There’s no establishment fee, no application fee and no mortgage stamp duty, so the entry costs are usually around NZ$1,000, including legal fees and title registrations,” O’Brien says.

“Often banks will even contribute towards the legal fees, if you’re a long-standing customer and you have a good relationship with the bank. I had a loan approved for a client recently that included NZ$400 towards legal costs.”

An additional cost the client might face is a property valuation, which costs roughly NZ$350–450, O’Brien explains.

It is an expense that lenders generally cover in Australia; however, O’Brien says that banks often don’t need a valuation on an 80% loan with a 20% deposit. Even if the valuation is required, O’Brien views this as a positive.

“It’s actually great, because the client and I can see the valuation before I give it to the bank,” O’Brien says. “The client can then see the description of the property and comparison sales of all

the streets around them, and that gives buyers the confidence to go ahead.”

Property taxes According to New Zealand Inland Revenue, no stamp duty is payable – ever. And land tax was abolished in 1992. Capital gains tax doesn’t exist in New Zealand; however, the Australian Tax Office requires all foreign income to be declared when you file your Australian tax return.

Depreciation Depreciation in New Zealand is more generous than in Australia. Firstly, and importantly, depreciation commences on the date of purchase, not the date of construction – as is the case in Australia – meaning a 30-year-old property has the same depreciation values as a brand-new house.

You can also choose between the diminishing value (3% pa) and straight-line (2% pa) methods of depreciation.

The diminishing value method causes the amount to decrease proportionally each year. So a NZ$100,000 asset will depreciate NZ$2,985 the first year, NZ$2,895 the second year, down to NZ$1,623 in 20 years’ time, and just NZ$1,197 after 30 years.

Straight-line depreciation will allow NZ$2,000 per year to be depreciated on a NZ$100,000 asset, regardless of how long the property is owned, which can be more suitable for buy-and-hold investors.

Naomi Ferguson, deputy commissioner – service delivery of NZ Inland Revenue, says that property

Jodene (27) and Neil (28) Young own a property in the trendy Auckland suburb of Onehunga.

Taking the plunge

“We bought our place in June 2005 and paid NZ$410,000. Lucky for us, the previous owner was elderly and needed a quick sale.”

The couple have family and friends living nearby. The area is close to One Tree Hill – with a large park and domain – and the shopping area in Onehunga is currently being upgraded.

“The drive into the city, where we both work, only takes 20–30 minutes on a busy day, and we are local to all amenities,” says Jodene.

After researching the property market casually for around six months, they began to get more serious about their future investment decision.

“We decided to buy a property because we wanted to get on the property ladder... plus we were ready for that financial commitment,” she says.

“At the time, we had recently returned from living in the UK and we had saved a small deposit, but in order to save more, we lived with my parents until we had a bigger chunk of money to play with.”

Since purchasing the place two years ago, the Youngs have done work on the garden, minor work to the interior, and plan to give the kitchen and bathroom a freshen up within the next year.

“To date, we’ve spent approximately NZ$5,000 on materials and envisage at least another NZ$10,000 before we could put it back on the market.

“We plan to stay here for at least another two years. Once we start a family, we will look for a ‘family’ home.”

Real life

47

In the last three years, property investor Randall Vlietstra has owned 19 properties in New Zealand. The Sydney-based carpenter, who is originally from New Zealand, says his property journey has been “a lot of fun”.

“I was working on a client’s property at Vaucluse [NSW] one day, overlooking the water with a mate, and I said: ‘How do people do this? How do they get wealthy?’ ”

Originally from New Zealand, Randall had heard about opportunities to get positively geared properties and started his research into the New Zealand property market.

“Houses were on the market in Invercargill for NZ$30,000 and NZ$40,000, and returning NZ$150 a week. I’d only been to the place twice in my life. Personally, I wouldn’t live there because it’s too cold! But it has a good population, with good infrastructure.

“The first property we bought there was in March 2004, and we paid NZ$40,000. It was returning NZ$130 a week. After that, I started looking at properties around NZ$60–70,000, and I could always get a good rental yield at around 11% or 12%.”

At one point, Randall had 19 properties in his portfolio but has been selling them gradually. He aims to end up with nine properties, mortgage-free. “Basically, we want to keep them so we have their income for our retirement,” he says.

As for leasing properties from abroad, Randall says that aside from one incident with a tenant, he has never had problems.

“We did have trouble getting a tenant on one property once, so after about two months, we jumped on a plane and flew over to see what was wrong. It turned out it was on a big, exposed block on a corner, and there was no privacy.

“A quote for a fence came back at about NZ$4,000, so we went out and bought about 50 NZ$5 pine trees and planted them around the perimeter. It rented out straightaway – in fact, the same tenant is still in there,” he says.

Randall says there are still opportunities for investors in Invercargill, but it’s with more value-add properties now, because the yields are not like they used to be.

“It’s still very affordable for Australians – you can still buy homes down there for NZ$125,000 returning NZ$160 per week. So, you can still hunt out an 8% return and get the positive cash flow, but it’s really hard to get that 10% yield now.

“The top end of the market at NZ$300,000 and NZ$400,000 is not moving at all, but the bottom end is still going up. Because so many people are buying now, it’s got to the stage where it’s a bit frenzied. Every time I sell a house it only takes about three or four days to sell.

“I think it might flatten out a little, but in saying that, because there’s a huge oil exploration going on in the southern basin, if it all comes off, they’ll be building a NZ$5bn refinery and an international airport. So we’ll see what comes of that. It will keep ticking away quite nicely, regardless, because it’s a sustainable little area.”

Finding solid investments in Invercargill

Invercargill is a city that is raining riches these days...

owners are also “able to depreciate chattels such as carpets, drapes, light fittings, whiteware and so on, as separate assets”, at a rate of 33% per year over three years.

“There is also provision to depreciate separately items such as water heaters, clothes lines and other fittings that are not part of the building,” Ferguson says.

Double taxAs a result of the Closer Economic Relations (CER) trade agreement struck between Australia and New Zealand in 1988, Australians can purchase property and enter into mortgages in New Zealand without difficulty.

Australia has a double tax agreement with New Zealand, meaning that Australians who earn rental income from properties in New Zealand pay tax only once – in Australia – but investors will still need to report to the New Zealand tax office, says Mary O’Brien.

“You must do a tax return on 31 March with the New Zealand Inland Revenue department,” says O’Brien and adds, “then you show that to your Australian accountant.

“I recommend you get an accountant in both New Zealand and Australia. Then the accountants can talk to each other and make sure everything is running smoothly.”

Other tax issuesAs in Australia, expenses related to your New Zealand investment properties, such as interest incurred on borrowings, council rates and maintenance relating to the properties, can be negatively geared against income received.

However, because your only income in New Zealand is rent, any losses will accumulate in New Zealand, as you are not able to negatively gear New Zealand property losses against Australian income.

On the plus side, keep in mind that visiting your investment property in New Zealand could be a tax deduction – check with your accountant.

Source: New Zealand Inland Revenue www.ird.govt.nz

48

49

Buying the big blocks

“Initially, I decided to invest in property in New Zealand because there was no stamp duty. Also, high interest rates equal high rents, and the relatively low cost of purchasing properties was also attractive.”

Simon found a property sourcing company online that pointed to Invercargill. “They found me some properties, so I flew over to New Zealand to look at these and other properties. They were also kind enough to spend the entire weekend with me and show me around town and teach me the good and bad points of the area.”

The high recommendation, affordable prices, growth potential and low vacancy rates were all reasons why Simon decided to invest there.

“I wanted something close to major facilities with good road access, and large blocks with houses located at the front or back of the block for future sub-dividing. I also wanted three to four bedrooms so it would be suitable for the average family.”

He bought two three-bedroom houses in May 2006 and paid NZ$155,000 for one and NZ$170,000 for the other.

Resources To search properties in New Zealand for sale online, go to: www.allrealestate.co.nz www.trademe.co.nz www.realestate.co.nz The following industry websites will also give you a better understanding of the New Zealand property market:

Real Estate Institute of New Zealand (REINZ)Access market trends, news, facts and statistics direct from the professional body for the real estate industry in New Zealand www.reinz.co.nz

NZ Property Investors Federation (NZPIF)The umbrella organisation for 20 local property investors’ associations throughout New Zealand www.nzpif.org.nz

Quotable ValueValuation services and online reports, including sales history figures and demographic profiles, for various New Zealand markets www.qv.co.nz

Property Council of New ZealandIndustry association focused on the commercial property sector www.propertynz.co.nz

Statistics NZEconomic and statistical information www.statisticsNZ.govt.nz

“With one of my houses, I’ve had trouble with rent not being paid, but this was sorted out with minimal hassle. However, I’ve not been happy with the performance of the property manager dealing with this property and I plan to change soon.

“I don’t find it difficult to manage my property from a distance. I have property in Australia and New Zealand, but live in Japan.

“I have very good contacts in both locations and it is relatively easy.

“I still have plans to continue to expand my portfolio in New Zealand. My next step would be to build on the back of my existing blocks.”

Simon recommends being highly selective when choosing property managers – because if you choose the right one, he says owning property can be a very “hands off” investment.

“My biggest recommendation to investors who don’t live in the area is to choose your contacts carefully. There are some very good property sourcing companies that charge a reasonable fee.”

“I also strongly suggest that if you’re buying in a new town, then fly over there to check it out. You only have to do it once, but actually being there allows you to get a true feel for the area – and will leave you confident to buy there again and again.”

Real life

Three-bedroom house InvercargillPurchased: May 2006Paid: NZ$155,000Rent: NZ$220 per week

Three-bedroom house InvercargillPurchased: May 2006Paid: NZ$170,000Rent: NZ$220 per week

Simon Bruce is a 32-year-old Australian living in Japan. He works as a recruitment consultant and currently has investment properties in both New Zealand and Australia.

Property | international opportunities