Embed Size (px)

Citation preview

INVESTING IN ASIA -

DIVIDEND MATTERS

Ashish Goyal, CFA, B Engg, PGDM

June 2013

Investing in Asia – Dividend Matters……………………………………………………………………….…. 03

Section I : Dividend Investing

Long and successful history ............................................................................................................... 04

Making a comeback............................................................................................................................ 06

Section II : Investment Opportunities in Asia

Growing and consolidating.................................................................................................................. 08

Companies have higher propensity to pay dividends ........................................................................ 10

Robust Asian growth is supportive of higher dividends...................................................................... 11

Section III : Valuation and Risks

Favourable valuations......................................................................................................................... 13

Risks................................................................................................................................................... 13

Conclusion………………………………………………………………………………………………………. 15

2

TABLE OF CONTENTS

1 Our thought piece “Investing in Asia – The Next 10 Years” argued for the investment case for Asian equities. We reiterate

some of the arguments in the third section of this white paper.

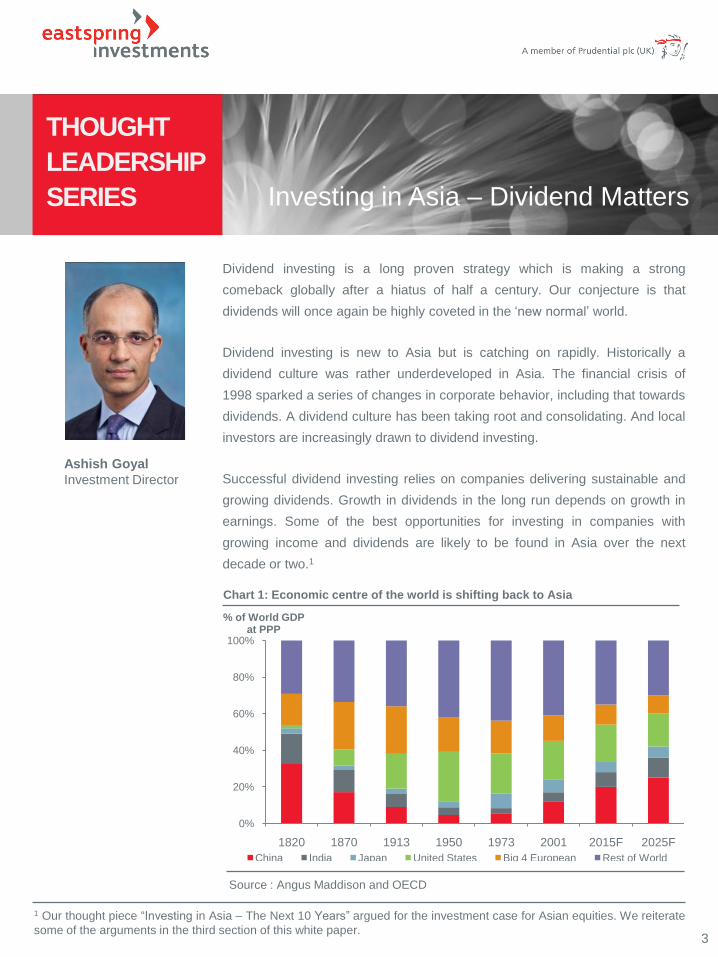

Investing in Asia – Dividend Matters

Dividend investing is a long proven strategy which is making a strong

comeback globally after a hiatus of half a century. Our conjecture is that

dividends will once again be highly coveted in the „new normal‟ world.

Dividend investing is new to Asia but is catching on rapidly. Historically a

dividend culture was rather underdeveloped in Asia. The financial crisis of

1998 sparked a series of changes in corporate behavior, including that towards

dividends. A dividend culture has been taking root and consolidating. And local

investors are increasingly drawn to dividend investing.

Successful dividend investing relies on companies delivering sustainable and

growing dividends. Growth in dividends in the long run depends on growth in

earnings. Some of the best opportunities for investing in companies with

growing income and dividends are likely to be found in Asia over the next

decade or two.1

THOUGHT

LEADERSHIP

SERIES

3

Chart 1: Economic centre of the world is shifting back to Asia

0%

20%

40%

60%

80%

100%

1820 1870 1913 1950 1973 2001 2015F 2025F

% of World GDP at PPP

China India Japan United States Big 4 European Rest of World

Source : Angus Maddison and OECD

Ashish Goyal

Investment Director

2 The history of the Dutch East India Company (Dutch: Vereenigde Oost-Indische Compagnie, VOC) is a fascinating storyabout the immense success and the subsequent decline of the world‟s first listed multinational corporation over 200 yearsof changing political, economic, and trade conditions during the 17th and the 18th century. It is highly recommendedreading for the student of economic and corporate history.

Section I Dividend Investing

Since the dawn of stock markets, dividends

have played a very important role in delivering

returns to investors.

The first ever listed company was the Dutch East

India Company established in 1602. It ran a very

successful spice trading business and paid an 18%

annual dividend for nearly 200 years.2 As stock

markets grew, inevitably they went through

speculative periods where stock prices lost any

rational relationship with underlying economics. In

these periods, dividends became less important.

Speculative investing has a nasty habit of

penalising investors when the bubble bursts or the

excessive valuation deflates. Dividends tend to

reassert themselves in these post speculative

periods.

Since the 1950’s, ‘growth investing’ has

dominated investor psyche and ‘dividend

investing’ has taken a back-seat.

These past 5-6 decades have been an extraordinary

period of economic and stock market growth. During

this growth period, companies have reduced their

payout ratios and chosen to reinvest capital

pursuing growth.

From the charts below it can be seen how there was

a distinct shift away from dividends in the US from

around the mid-50‟s as companies cut their payout

ratios by 10 to 20 percentage points.

Long and successful history

4

Chart 2: Dividend contribution has fallen since 1950s…..... Chart 3: ......as payouts declined

Source: Morgan Stanley, *Data is percentage share of 15-year

returns due to dividends. The share exceeds 100% when

equity prices have fallen over the 15 year period. May 2013

Source: Morgan Stanley, Data based on 10-year average

earnings and dividends, May 2013

20

40

60

80

100

18801890190019101920193019401950196019701980199020002010

US Payout Ratio, %

0

20

40

60

80

100

1890190019101920193019401950196019701980199020002010

Dividend Share as a % of Total Equity Return* in US

3 Recently there have been several examples of the stock market rewarding capital management initiatives. In

April, Woodside Petroleum in Australia announced an increase in dividends. The stock promptly leapt 12% over the next

two days, pressurising other companies to follow the same path.

-2

3

8

13

18

-5

5

15

25

35

1995 1998 2000 2002 2004 2006 2008 2010 2012

Earnings per share (LHS) Dividend per share (RHS)

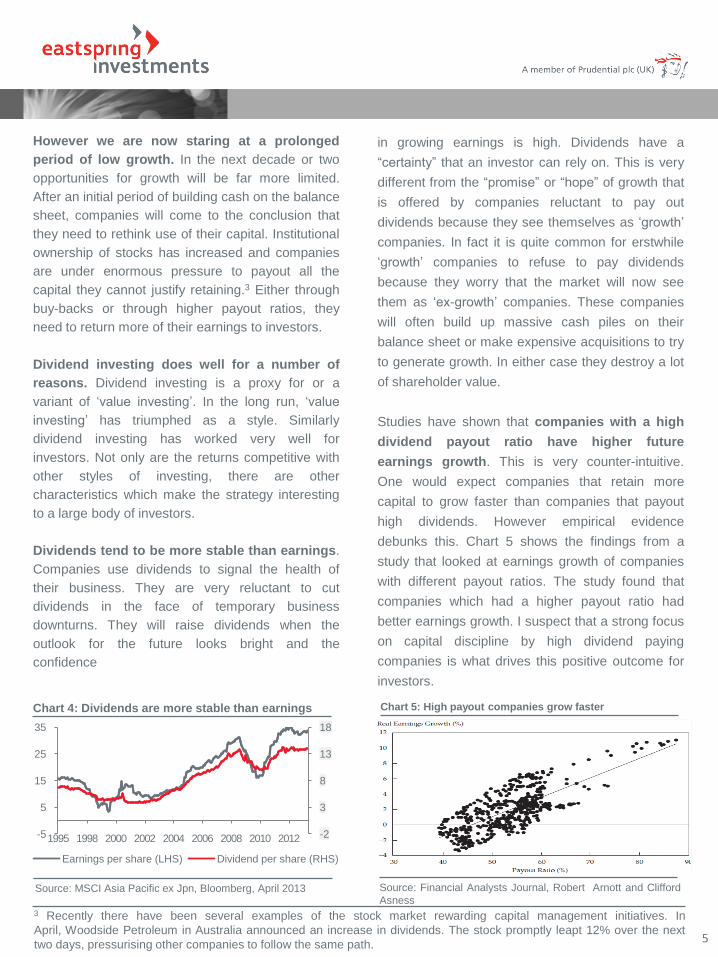

However we are now staring at a prolonged

period of low growth. In the next decade or two

opportunities for growth will be far more limited.

After an initial period of building cash on the balance

sheet, companies will come to the conclusion that

they need to rethink use of their capital. Institutional

ownership of stocks has increased and companies

are under enormous pressure to payout all the

capital they cannot justify retaining.3 Either through

buy-backs or through higher payout ratios, they

need to return more of their earnings to investors.

Dividend investing does well for a number of

reasons. Dividend investing is a proxy for or a

variant of „value investing‟. In the long run, „value

investing‟ has triumphed as a style. Similarly

dividend investing has worked very well for

investors. Not only are the returns competitive with

other styles of investing, there are other

characteristics which make the strategy interesting

to a large body of investors.

Dividends tend to be more stable than earnings.

Companies use dividends to signal the health of

their business. They are very reluctant to cut

dividends in the face of temporary business

downturns. They will raise dividends when the

outlook for the future looks bright and the

confidence

5

Chart 4: Dividends are more stable than earnings

Source: MSCI Asia Pacific ex Jpn, Bloomberg, April 2013

in growing earnings is high. Dividends have a

“certainty” that an investor can rely on. This is very

different from the “promise” or “hope” of growth that

is offered by companies reluctant to pay out

dividends because they see themselves as „growth‟

companies. In fact it is quite common for erstwhile

„growth‟ companies to refuse to pay dividends

because they worry that the market will now see

them as „ex-growth‟ companies. These companies

will often build up massive cash piles on their

balance sheet or make expensive acquisitions to try

to generate growth. In either case they destroy a lot

of shareholder value.

Studies have shown that companies with a high

dividend payout ratio have higher future

earnings growth. This is very counter-intuitive.

One would expect companies that retain more

capital to grow faster than companies that payout

high dividends. However empirical evidence

debunks this. Chart 5 shows the findings from a

study that looked at earnings growth of companies

with different payout ratios. The study found that

companies which had a higher payout ratio had

better earnings growth. I suspect that a strong focus

on capital discipline by high dividend paying

companies is what drives this positive outcome for

investors.

Chart 5: High payout companies grow faster

Source: Financial Analysts Journal, Robert Arnott and Clifford

Asness

4 One is reminded of Einstein‟s quote about compound interest being the eighth wonder of the world. Dividends have the

same wonderful quality of compounding.

3.9%4.8%

2.3%

3.1%

0%

2%

4%

6%

8%

MSCI World MSCI Asia Pacific ex Jpn

Price Return Dividend

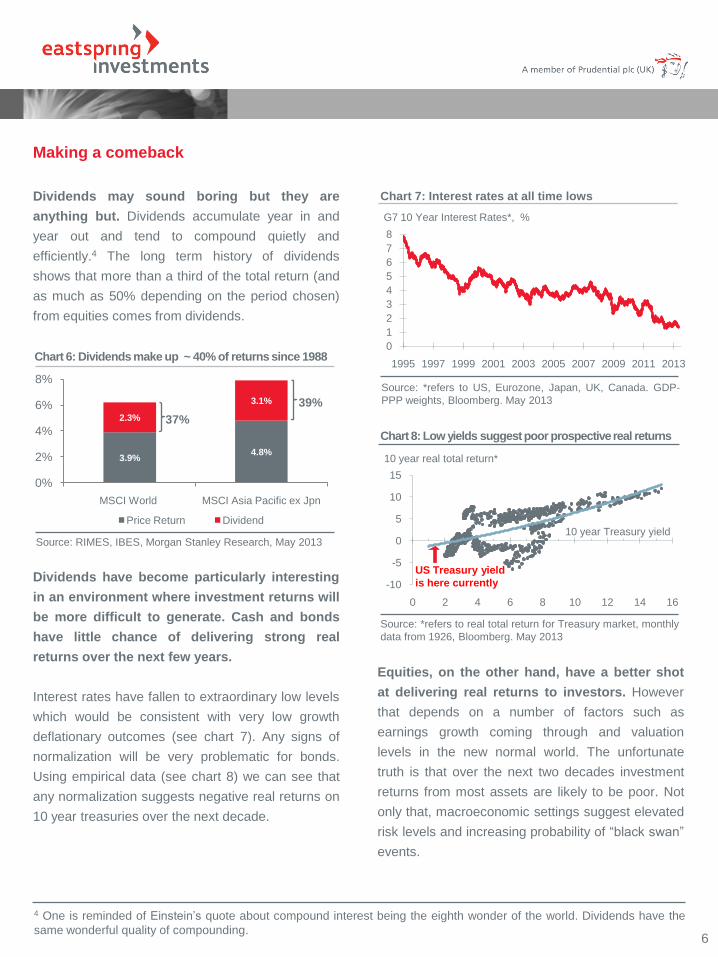

Dividends may sound boring but they are

anything but. Dividends accumulate year in and

year out and tend to compound quietly and

efficiently.4 The long term history of dividends

shows that more than a third of the total return (and

as much as 50% depending on the period chosen)

from equities comes from dividends.

Dividends have become particularly interesting

in an environment where investment returns will

be more difficult to generate. Cash and bonds

have little chance of delivering strong real

returns over the next few years.

Interest rates have fallen to extraordinary low levels

which would be consistent with very low growth

deflationary outcomes (see chart 7). Any signs of

normalization will be very problematic for bonds.

Using empirical data (see chart 8) we can see that

any normalization suggests negative real returns on

10 year treasuries over the next decade.

6

Chart 7: Interest rates at all time lows

Source: *refers to US, Eurozone, Japan, UK, Canada. GDP-

PPP weights, Bloomberg. May 2013

Making a comeback

Equities, on the other hand, have a better shot

at delivering real returns to investors. However

that depends on a number of factors such as

earnings growth coming through and valuation

levels in the new normal world. The unfortunate

truth is that over the next two decades investment

returns from most assets are likely to be poor. Not

only that, macroeconomic settings suggest elevated

risk levels and increasing probability of “black swan”

events.

0

1

2

3

4

5

6

7

8

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

G7 10 Year Interest Rates*, %

Chart 8: Low yields suggestpoor prospectivereal returns

Source: *refers to real total return for Treasury market, monthly

data from 1926, Bloomberg. May 2013

-10

-5

0

5

10

15

0 2 4 6 8 10 12 14 16

10 year Treasury yield

10 year real total return*

US Treasury yield

is here currently

Chart 6: Dividends make up ~ 40% of returns since 1988

Source: RIMES, IBES, Morgan Stanley Research, May 2013

39%

37%

5 Buying any overpriced asset is unlikely to make for a rewarding investment. Dividend stocks are not immune to this

economic reality.7

It is hence no surprise that investors in the

recent past have migrated aggressively to

income strategies. Having exhausted the return

potential of government bonds, corporate

bonds, and high yield corporate bonds, they are

increasingly turning to dividend stocks. Even

investors who have historically invested in equities

for growth are showing a preference for the

"certainty of dividends" over the "promise of

growth".

We believe this trend is still in its early stages.

There is a risk that dividend stocks might become

overvalued at some stage in the next few years. We

are not there yet. Even if we do get to a “dividend

bubble” phase5, I believe that the interest in dividend

investing is likely to be enduring.

Ageing populations in the more developed Asian

economies and in China will further boost the

demand for income generating assets.

Irrespective of whether dividend stocks get cyclically

overpriced or not, structurally the interest in dividend

investing is likely to remain much higher than has

been in the last 50 years. The strategy will remain

relevant and may once again be the dominant way

investors invest in equities in the “new normal”

world.

Section II Investment Opportunities In Asia

20 years ago as a rookie investor when I went

around Asia interviewing company management, a

section of questions on my checklist would be

around dividends. What was the dividend strategy of

the company? Did they plan to progressively

increase dividends? How did the company balance

the need to retain capital for reinvestment versus

dividends? How high did they set the investment

hurdle rates for growth capital expenditure?

This was all classic investment theory I had learnt at

business school. The real world in Asia behaved

very differently. The responses varied from a hearty

laugh to a commiserative sigh. The suggestion from

both was that I was asking all the wrong

questions, that dividends didn‟t matter, and that I

didn‟t really understand investing in Asia.

Clearly Asia in the early 90’s did not have a

dividend culture. Corporate Asia was very growth

focused. Underdeveloped capital markets meant

that growth had to be funded heavily with retained

profits. However the lack of a dividend culture also

meant that in many instances there was a lack of

capital discipline. This was very visible in the boom

of the early to mid-90s when companies frequently

invested their surpluses on unrelated businesses

(typically a real estate development) or trophy

assets (golf courses).

Towards the end phase of that bull

market, companies were raising money in short-

term, un-hedged US$ debt and using this money to

invest for growth or their pet projects. This was a big

contributory factor to the Asian financial crisis of

1998.

The Asian crisis of 1998 made a deep and lasting

impression on corporate Asia, changing behavior

quite dramatically. Companies responded in three

stages.

In the first stage, the banking sector and the

corporate sector repaired balance sheets.

Companies reduced their debt levels. Currency

exposures were reined in. Tenure of borrowing was

extended. Balance sheet strength was rebuilt.

Growing and Consolidating

8

Chart 9: Corporate Asia has repaired its balance sheet

Source: MSCI Asia ex Jpn,Datastream, UBS

estimates, December 2012

0%

20%

40%

60%

80%

1988199019921994199619982000200220042006200820102012

Net Debt to Equity Ratio, %

6 Taiwan tax rules encourage companies to aggressively pay out dividends. However, most companies in Taiwan have

highly cyclical businesses and hence dividends tend to be of a “constant payout” nature rather than “progressive”. The

dividends mimic the cyclicality of underlying earnings.

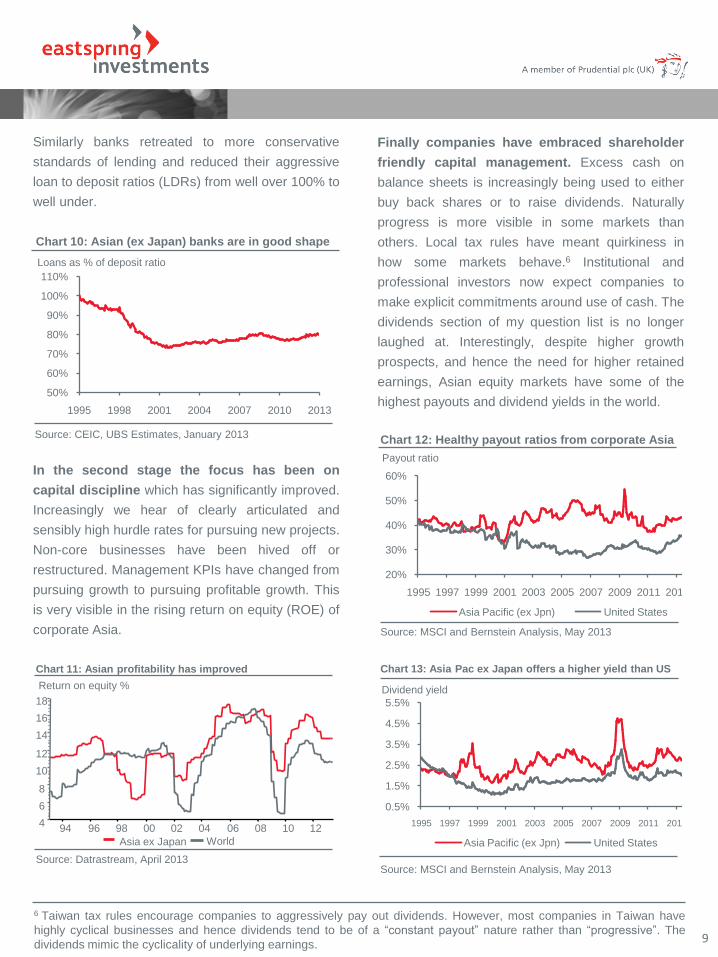

Similarly banks retreated to more conservative

standards of lending and reduced their aggressive

loan to deposit ratios (LDRs) from well over 100% to

well under.

9

Finally companies have embraced shareholder

friendly capital management. Excess cash on

balance sheets is increasingly being used to either

buy back shares or to raise dividends. Naturally

progress is more visible in some markets than

others. Local tax rules have meant quirkiness in

how some markets behave.6 Institutional and

professional investors now expect companies to

make explicit commitments around use of cash. The

dividends section of my question list is no longer

laughed at. Interestingly, despite higher growth

prospects, and hence the need for higher retained

earnings, Asian equity markets have some of the

highest payouts and dividend yields in the world.

In the second stage the focus has been on

capital discipline which has significantly improved.

Increasingly we hear of clearly articulated and

sensibly high hurdle rates for pursuing new projects.

Non-core businesses have been hived off or

restructured. Management KPIs have changed from

pursuing growth to pursuing profitable growth. This

is very visible in the rising return on equity (ROE) of

corporate Asia.

Chart 12: Healthy payout ratios from corporate Asia

Source: MSCI and Bernstein Analysis, May 2013

20%

30%

40%

50%

60%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Payout ratio

Asia Pacific (ex Jpn) United States

Chart 11: Asian profitability has improved

Source: Datrastream, April 2013

Return on equity %

Asia ex Japan World

94 96 98 00 02 04 06 08 10 124

6

8

10

12

14

16

18

Chart 13: Asia Pac ex Japan offers a higher yield than US

Source: MSCI and Bernstein Analysis, May 2013

0.5%

1.5%

2.5%

3.5%

4.5%

5.5%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Dividend yield

Asia Pacific (ex Jpn) United States

Chart 10: Asian (ex Japan) banks are in good shape

Source: CEIC, UBS Estimates, January 2013

50%

60%

70%

80%

90%

100%

110%

1995 1998 2001 2004 2007 2010 2013

Loans as % of deposit ratio

50%

60%

70%

80%

90%

100%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Fraction of companies that pay a dividend vs regional universe

Asia Pacific (ex Jpn) United States

Thanks to the change in corporate behavior

towards dividends, Asia now has a wide and

deep pool of dividend paying listed companies.

The Asia ex-Japan listed universe has

approximately 1,250 companies with a market

capitalization of over $1 billion. Of these, about 850

trade more than US$ 3 million per day on average.

This constitutes our broadest definition of the

investible universe. Our narrowed down list consists

of about 320 companies that have a dividend yield

of over 3%.

Within this list there are about 120 companies that

have delivered an annualized growth rate of 10% in

dividends over the last 5 years. This is our focus list.

10

Companies in Asia-Pacific have a higher propensity to pay dividends

At Eastspring Investments we run a large and

very successful dividend strategy.

Our equity income strategies invests across Asia

Pacific ex Japan, focusing on total returns from

companies that pay out a reasonable dividend.

Dividend sustainability, dividend growth, a strong

minority shareholder orientation and good valuation

are all essential criteria before we buy a company.

The strategies hold about 60 to 70 names – these

are the companies which we have bought after

conducting in-depth research and analysis. We find

that increasingly it is possible to construct a well

diversified, yield oriented equity strategy in Asia.

This would not have been easy 20 years ago.

Source: MSCI and Bernstein Analysis, May 2013

Chart 14: Companies in Asia Pacific have a higher

propensity to pay dividends

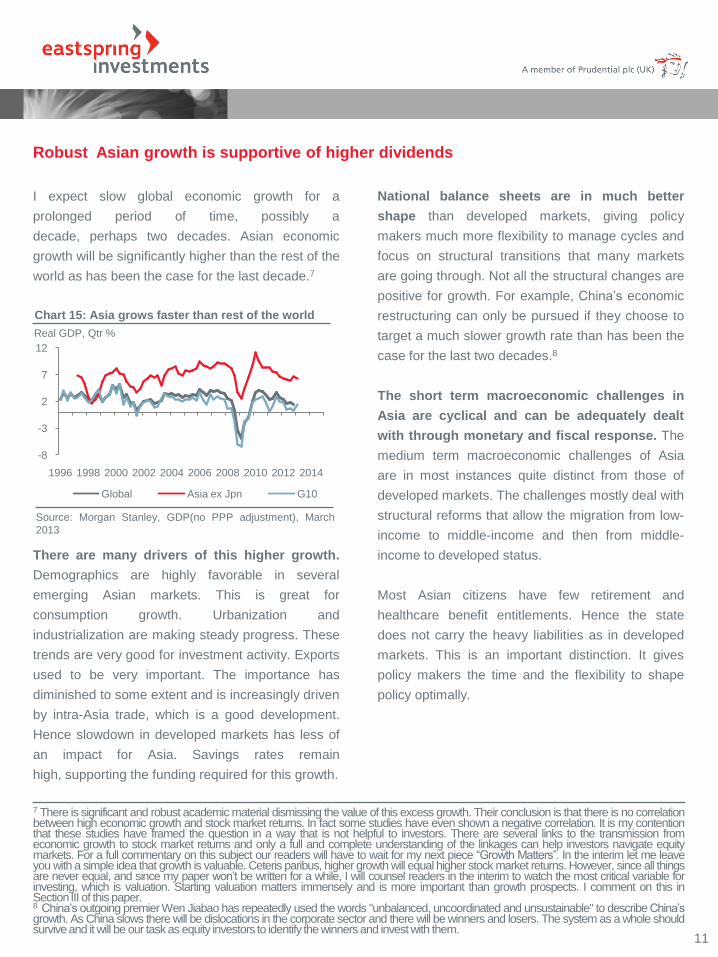

I expect slow global economic growth for a

prolonged period of time, possibly a

decade, perhaps two decades. Asian economic

growth will be significantly higher than the rest of the

world as has been the case for the last decade.7

11

Robust Asian growth is supportive of higher dividends

7 There is significant and robust academic material dismissing the value of this excess growth. Their conclusion is that there is no correlationbetween high economic growth and stock market returns. In fact some studies have even shown a negative correlation. It is my contentionthat these studies have framed the question in a way that is not helpful to investors. There are several links to the transmission fromeconomic growth to stock market returns and only a full and complete understanding of the linkages can help investors navigate equitymarkets. For a full commentary on this subject our readers will have to wait for my next piece “Growth Matters”. In the interim let me leaveyou with a simple idea that growth is valuable. Ceteris paribus, higher growth will equal higher stock market returns. However, since all thingsare never equal, and since my paper won‟t be written for a while, I will counsel readers in the interim to watch the most critical variable forinvesting, which is valuation. Starting valuation matters immensely and is more important than growth prospects. I comment on this inSectionIII of this paper.8 China‟s outgoing premier Wen Jiabao has repeatedly used the words "unbalanced, uncoordinated and unsustainable" to describe China‟sgrowth. As China slows there will be dislocations in the corporate sector and there will be winners and losers. The system as a whole shouldsurviveand it will be our task as equity investors to identify the winners and invest with them.

There are many drivers of this higher growth.

Demographics are highly favorable in several

emerging Asian markets. This is great for

consumption growth. Urbanization and

industrialization are making steady progress. These

trends are very good for investment activity. Exports

used to be very important. The importance has

diminished to some extent and is increasingly driven

by intra-Asia trade, which is a good development.

Hence slowdown in developed markets has less of

an impact for Asia. Savings rates remain

high, supporting the funding required for this growth.

National balance sheets are in much better

shape than developed markets, giving policy

makers much more flexibility to manage cycles and

focus on structural transitions that many markets

are going through. Not all the structural changes are

positive for growth. For example, China‟s economic

restructuring can only be pursued if they choose to

target a much slower growth rate than has been the

case for the last two decades.8

The short term macroeconomic challenges in

Asia are cyclical and can be adequately dealt

with through monetary and fiscal response. The

medium term macroeconomic challenges of Asia

are in most instances quite distinct from those of

developed markets. The challenges mostly deal with

structural reforms that allow the migration from low-

income to middle-income and then from middle-

income to developed status.

Most Asian citizens have few retirement and

healthcare benefit entitlements. Hence the state

does not carry the heavy liabilities as in developed

markets. This is an important distinction. It gives

policy makers the time and the flexibility to shape

policy optimally.

-8

-3

2

7

12

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014

Global Asia ex Jpn G10

Real GDP, Qtr %

Source: Morgan Stanley, GDP(no PPP adjustment), March

2013

Chart 15: Asia grows faster than rest of the world

0

20

40

60

80

100

120

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Sovereign Debt as a % of GDP*

G7 Advanced economies Emerging and developing economies

0%

20%

40%

60%

80%

2007 2008 2009 2010 2011 2012

Share of Industry Smartphone Profits

Apple Samsung

8.3

10.9

12.6

15.0

16.2

16.9

17.7

17.5

19.5

23.4

32.9

3425

21 20 20 21 21 19 19 17

9 0

10

20

30

40

500

5

10

15

20

25

30

35

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

US$ bn

Brand Value (LHS) Brand Rank (RHS)

12

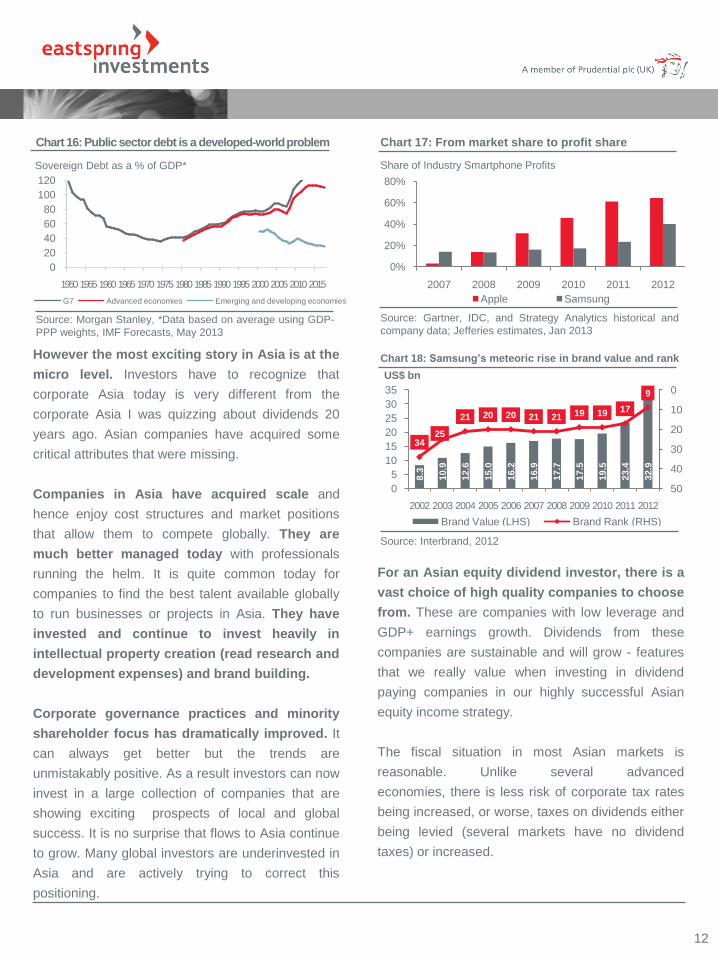

Chart 16: Public sectordebt is a developed-worldproblem

However the most exciting story in Asia is at the

micro level. Investors have to recognize that

corporate Asia today is very different from the

corporate Asia I was quizzing about dividends 20

years ago. Asian companies have acquired some

critical attributes that were missing.

Companies in Asia have acquired scale and

hence enjoy cost structures and market positions

that allow them to compete globally. They are

much better managed today with professionals

running the helm. It is quite common today for

companies to find the best talent available globally

to run businesses or projects in Asia. They have

invested and continue to invest heavily in

intellectual property creation (read research and

development expenses) and brand building.

Corporate governance practices and minority

shareholder focus has dramatically improved. It

can always get better but the trends are

unmistakably positive. As a result investors can now

invest in a large collection of companies that are

showing exciting prospects of local and global

success. It is no surprise that flows to Asia continue

to grow. Many global investors are underinvested in

Asia and are actively trying to correct this

positioning.

Chart 17: From market share to profit share

Source: Gartner, IDC, and Strategy Analytics historical and

company data; Jefferies estimates, Jan 2013

Chart 18: Samsung’s meteoric rise in brand value and rank

Source: Interbrand, 2012

For an Asian equity dividend investor, there is a

vast choice of high quality companies to choose

from. These are companies with low leverage and

GDP+ earnings growth. Dividends from these

companies are sustainable and will grow - features

that we really value when investing in dividend

paying companies in our highly successful Asian

equity income strategy.

The fiscal situation in most Asian markets is

reasonable. Unlike several advanced

economies, there is less risk of corporate tax rates

being increased, or worse, taxes on dividends either

being levied (several markets have no dividend

taxes) or increased.

Source: Morgan Stanley, *Data based on average using GDP-

PPP weights, IMF Forecasts, May 2013

Sovereign Debt as a % of GDP*

-30%

-10%

10%

30%

50%

0.5 1.0 1.5 2.0 2.5 3.0

Historical P/B

P/B on 10 June 2013 is 1.55x

Implied 3 year return = 11%

Section III Valuations and Risks

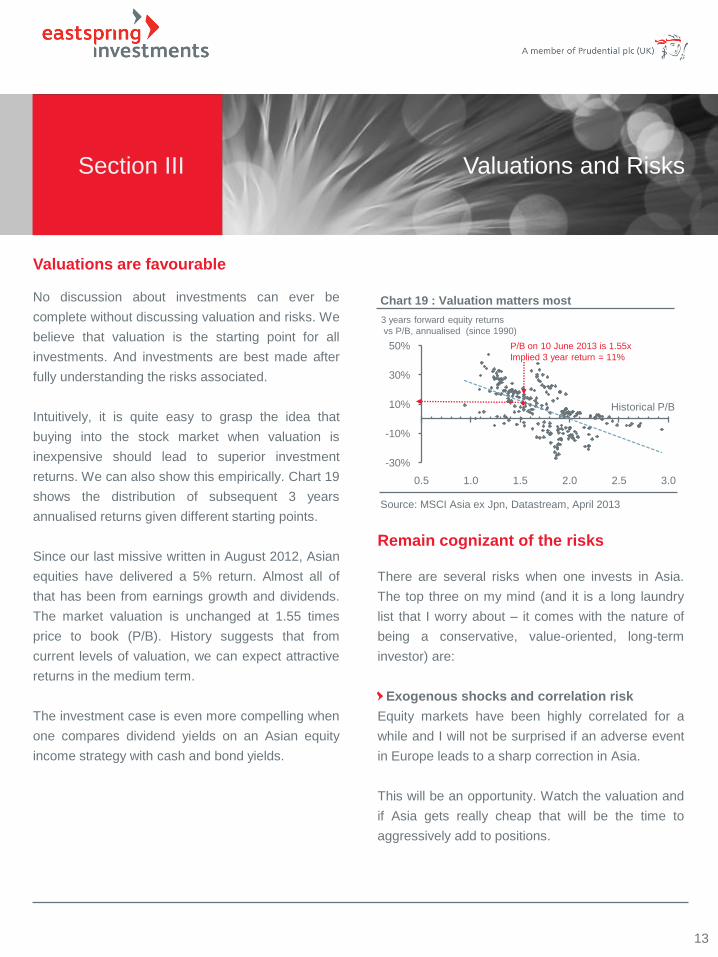

No discussion about investments can ever be

complete without discussing valuation and risks. We

believe that valuation is the starting point for all

investments. And investments are best made after

fully understanding the risks associated.

Intuitively, it is quite easy to grasp the idea that

buying into the stock market when valuation is

inexpensive should lead to superior investment

returns. We can also show this empirically. Chart 19

shows the distribution of subsequent 3 years

annualised returns given different starting points.

Since our last missive written in August 2012, Asian

equities have delivered a 5% return. Almost all of

that has been from earnings growth and dividends.

The market valuation is unchanged at 1.55 times

price to book (P/B). History suggests that from

current levels of valuation, we can expect attractive

returns in the medium term.

The investment case is even more compelling when

one compares dividend yields on an Asian equity

income strategy with cash and bond yields.

Valuations are favourable

13

Chart 19 : Valuation matters most

Source: MSCI Asia ex Jpn, Datastream, April 2013

Remain cognizant of the risks

There are several risks when one invests in Asia.

The top three on my mind (and it is a long laundry

list that I worry about – it comes with the nature of

being a conservative, value-oriented, long-term

investor) are:

Exogenous shocks and correlation risk

Equity markets have been highly correlated for a

while and I will not be surprised if an adverse event

in Europe leads to a sharp correction in Asia.

This will be an opportunity. Watch the valuation and

if Asia gets really cheap that will be the time to

aggressively add to positions.

3 years forward equity returns

vs P/B, annualised (since 1990)

14

China

China needs to transition from an aggressively

investment led economy to one that is more

balanced, more driven by market forces, and more

internally consistent.

This transition is neither easy nor risk-free and will

inevitably mean that China‟s economic growth rate

will slow meaningfully.

The macroeconomic challenges get all the attention

but the real challenge for equity investors like us is

to find the listed companies that can survive or even

thrive in this transition phase and beyond.

There are quite a few companies and some of them

even pay decent dividends. It is these investment

opportunities that we are most focused on.

Politics and Policy missteps

The potential of Asia is immense. However there

are very real challenges in policy making and

execution.

Over the last 6-8 years under the Congress led

government, India has been the poster child of how

not to run an economy.

There has been a lack of leadership and a lack of

progress. Important reforms have stalled and

investment activity has come to a grind.

Reversing this will not be easy and is a reminder of

how growth potential can be frittered away by poor

policy making.

Many Asian economies are young democracies and

are still learning how to deliver high quality

governance and long-range policy making even as

they have to go to polls every 5 years.

The good news is that the average voter seems to

have a strong intuitive sense for what is best for him

and votes accordingly. The pace of progress varies

but the direction does not.

Conclusion

Globally, dividend investing is back and here to

stay.

Asia has joined the Dividend Club. Dividend

investing is new to Asia but is catching on rapidly. A

dividend culture has been taking root and

consolidating. And local investors are increasingly

drawn to dividend investing.

For the global dividend investor, an Asian Dividend

strategy broadens the universe from which to

harvest dividends. It diversifies the portfolio and

introduces some exciting new investment

opportunities to the portfolio.

15

Eastspring Investments has a long and successful

track record of managing an Asian Equity Income

strategy.

Our investors have benefitted immensely from

investing in the Asian dividend story. We remain

optimistic that this will continue to be the case over

the next two decades.

16

Disclaimer

Eastspring Investments (Singapore) Limited, UEN: 199407631H

This document is intended for general circulation and for information purposes only. It may not be

published, circulated, reproduced or distributed in whole or part to any other person without prior consent. This

information is not an offer or solicitation by anyone in any jurisdiction in which such offer or solicitation is not

lawful or in which the person making such offer or solicitation is not qualified to do so or to anyone to whom it is

unlawful to make such an offer or solicitation. It should not be construed as an offer, solicitation of an offer, or a

recommendation to transact in any securities mentioned herein. The information does not take into account the

specific investment objectives, financial situation or particular needs of any person. Advice should be sought

from a financial adviser regarding the suitability of the investment product before making a commitment to

purchase the investment product. Past performance is not necessarily indicative of future performance. Any

prediction, projection, or forecast on the economy, securities markets or the economic trends of the markets is

not necessarily indicative of the future performance of Eastspring Investments (Singapore) Limited or any funds

managed by Eastspring Investments (Singapore) Limited. The value and any income accruing to the

investments, if any, may fall or rise. An investment is subject to investment risks, including the possible loss of

the principal amount invested. Whilst we have taken all reasonable care to ensure that the information contained

in this document is not untrue or misleading at the time of publication, we cannot guarantee its accuracy or

completeness. Any opinion or estimate contained in this document is subject to change without notice.

Eastspring Investments (Singapore) Limited is an ultimately wholly-owned subsidiary of Prudential plc of the

United Kingdom. Eastspring Investments (Singapore) Limited and Prudential plc are not affiliated in any manner

with Prudential Financial, Inc., a company whose principal place of business is in the United States of America.

MM704/270613

![On Steady Dividend Payment under Functional Mean Reversion ... · motivation for investing in stocks [11] so firms’ failure to maintain steady and high dividend payments is a discouragement](https://img.pdfslide.us/doc/110x75/5e8bc57b9020b54f4a55f261/on-steady-dividend-payment-under-functional-mean-reversion-motivation-for-investing.jpg)