Embed Size (px)

Citation preview

INVESTED IN ADVISORS | FEBRUARY 2020 FINANCIAL-PLANNING.COM / @FINPLAN

The Next MoveThere comes a time when advisors must decide how much more to grow. Here’s how to make the tough choice.

AVOID THE FAFSA TRIPWIRE P. 34

001_FP0220 1 1/21/20 10:13 AM

002_FP0220_001 2 1/17/2020 2:23:25 PM

February 2020 Financial Planning 1Financial-Planning.com

February 2020 | VOL. 50 | NO. 2Contents

20The Next Move

There comes a time when advisors must decide how much more to grow. Here’s how to make the tough choice.BY MICHAEL KITCES

Columns9My Plan B for successionAn exit strategy doesn’t have to be set in stone. It can be as fluid and adaptable as other major life choices.

BY CAROLYN McCLANAHAN

12 The day I lost it over a FAANG stockThere’s a way to offer sound counsel to clients and also permit them the opportunity to take a profitable flier from time to time.

BY KIMBERLY FOSS

16 Are advisors overpaid?Our industry is one of the few that’s barely experienced pricing pressure — so far. Here’s how to assure you keep providing value.

BY ALLAN BOOMER

18 Building — then leaving — a support systemI created a meaningful study group. Here’s why I stepped away.

BY DAVE GRANT

001_FP0220 1 1/17/2020 2:57:55 PM

2 Financial Planning February 2020

Contents February 2020 | VOL. 50 | NO. 2

Upfront & more

4 Financial-Planning.com5 Editor’s View7 Retirement Advisor

Confidence Index39 CE Quiz

Source: Company data

Ladenburg IBDs generated $1.38 billionin 2018

$104.7M

$122.8M

$129.1M

$220.7M$803.5M

Investacorp, $104.7M

KMS Financial Services,$122.8M

Securities ServiceNetwork, $129.1M

Triad Advisors, $220.7M

Securities America,$803.5M

2926

In|Vest26‘A ton of inbound calls’ for BettermentSchwab-TD Ameritrade deal triggers advisor interest.

BY CHARLES PAIKERT

27Wealthfront takes on banks The digital firm has ambitious plans to out-maneuver the big brick-and-mortars.

BY TOBIAS SALINGER

28Should firms end forced arbitration for sexual harassment claims? Current employment contracts benefit companies and silence women, according to advisors and industry professionals.

BY CHARLES PAIKERT

IBD Intel29 Rivals lurking after Advisor Group’s Ladenburg deal?Competitors eye the 4,400 reps poised to operate in a new parent IBD network after the $1.3 billion acquisition.

BY TOBIAS SALINGER

Client31New tax law obliterates IRA trust planningThe Secure Act expands retirement savers’ options, but it has all but eliminated the stretch IRA for beneficiaries.

BY ED SLOTT

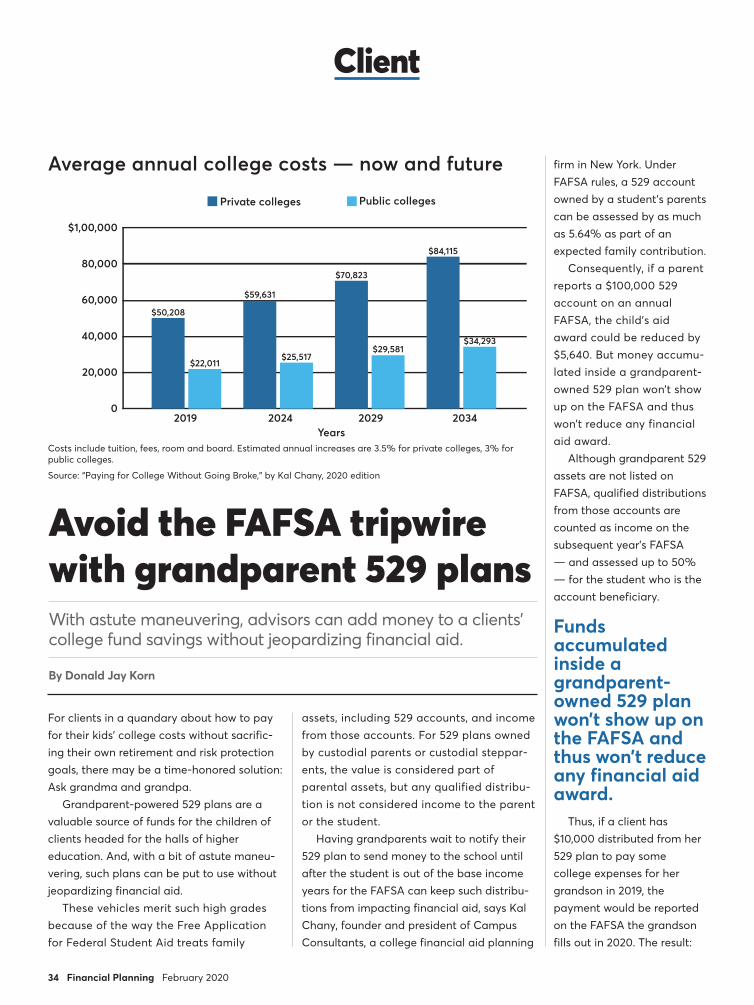

34Avoid the FAFSA tripwire with grandparent 529 plansWith astute maneuvering, advisors can add money to clients’ college fund savings without jeopardizing financial aid.

BY DONALD JAY KORN

Portfolio36 Breaking clients of their S&P 500 addictionThe tricky part is educating clients on how to recognize what constitutes underperfor-mance and overperformance.

BY CRAIG L. ISRAELSEN

Selfie40 A succession wake-up callI helped others plan for the unexpected, but it took a personal tragedy to put my own strategy in place.

BY WILLIAM MULLIN

Financial Planning Vol. 50/No. 2 (ISSN 0746-7915) is published monthly (12 times a year) by Arizent, One State Street Plaza, 27th Floor, New York, NY 10004-1505. Subscription price: $149 for one year in the U.S.; $229 for one year in all other countries. Periodical postage paid at New York, NY and U.S. additional mailing offices. POSTMASTER: Send address changes to Financial Planning, Arizent, One State Street Plaza, New York, NY 10004. For subscriptions, renewals, address changes and delivery service issues contact our Customer Service department at (212) 803-8500 or email: [email protected]. Financial Planning is a trademark used herein under license. Copying for other than personal use or internal use is prohibited without express written permission of the publisher. ©2020 Arizent and Financial Planning. All rights reserved.

LICENSING AND REUSE OF CONTENT:

Contact our official partner, Wright’s Media, about available usages, license and reprint fees, and award seal artwork at [email protected] or (877) 652-5295 for more information. Please note Wright’s Media is the only authorized company with which we’ve partnered for Arizent content.

CUSTOMER SERVICE [email protected] or (212) 803-8500

Financial-Planning.com

1 STATE STREET PLAZA, 27TH FLOOR

NEW YORK, NY 10004-1505 • (212) 803-8200

EDITOR-IN-CHIEF

Chelsea Emery

MANAGING EDITOR, OPERATIONS AND INNOVATION

Maddy Perkins

SENIOR EDITORS

Ann Marsh (West Coast Bureau Chief),

Charles Paikert, Tobias Salinger, Andrew Welsch

TECHNOLOGY EDITOR

Suleman Din

ASSOCIATE EDITORS

Sean Allocca, Jessica Mathews, Andrew Shilling

COLUMNISTS

Allan Boomer, Brent Brodeski, Kelli Cruz, Kimberly Foss,

Dave Grant, Carolyn McClanahan

CONTRIBUTING WRITERS

Ingrid Case, Kenneth Corbin, Alan J. Foxman, Craig L. Israelsen,

Michael Kitces, Donald Jay Korn, Joseph Lisanti, Allan S. Roth,

Ed Slott

COPY EDITORS

Fred Eliason, Dina Hampton, Rebecca Stropoli

GROUP EDITORIAL DIRECTOR,

FINANCIAL PLANNING AND EMPLOYEE BENEFITS GROUPS

Scott Wenger

EXECUTIVE DIRECTOR, CONTENT OPERATIONS

AND CREATIVE SERVICES

Michael Chu

SENIOR ART DIRECTOR

Nick Perkins

WEST COAST/SOUTHEAST SALES MANAGER

Frank Rose (212) 803-8872

NORTHEAST SALES MANAGER

Hilary Whidden (212) 803-8643

MIDWEST SALES MANAGER

Victoria Hamilton (212) 803-8594

SENIOR MARKETING MANAGER

Jamie Billington (212) 803-6099

CHIEF EXECUTIVE OFFICER...........................Gemma Postlethwaite

CHIEF FINANCIAL OFFICER ............................................Debra Mason

CHIEF STRATEGY OFFICER ............................................... Jeff Mancini

CHIEF CUSTOMER OFFICER ...........................................Dave Colford

CHIEF CONTENT OFFICER.................................................David Evans

VP, PEOPLE & CULTURE .......................................................... Lee Gavin

002_FP0220 2 1/17/2020 1:22:59 PM

Change your perspective.

TD Ameritrade Institutional, Division of TD Ameritrade, Inc. member FINRA/SIPC. TD is a trademark jointly owned by TD Ameritrade IP Company, INC. and the Toronto-DominionBank. © 2019 TD Ameritrade

003_FP0220 3 1/17/2020 2:23:26 PM

4 Financial Planning February 2020

What’s going on @financial-planning.com

Innovative growth strategiesFrom curating trips to Italy to designing their own software, a few planners found some creative ways to deepen existing client relationships and make new ones. These new approaches are as diverse as the people and firms charting them. Read more here: https://bit.ly/2QktxpI

WEB SPECIAL

Source: Company data, 2019

Number of RIA clients at custodians7.5K

7.0K

3.0K

750

CharlesSchwab

TD Ameritrade FidelityInvestments

BNY MellonPershing

TradePMR E-Trade RaymondJames

400 225 200

The race to zero commissionsNow that trading costs are plunging, trade frequency will likely go up and there will be more indexing and tax-loss harvesting. The shift could also be a boon for technology providers. Read more here: http://bit.ly/2Nq4P5i

GUIDE TO GROWTH

Feb. 17-20T3 Advisor ConferenceSan Diegohttps://bit.ly/2SMB7Lq

May 4-7FPA RetreatCedar Creek, Texashttp://bit.ly/2qoYPRq

May 6-9NAPFA Spring ConferenceDenverhttp://bit.ly/2NL84DU

June 3-5Morningstar Investment Conference Chicagohttp://bit.ly/2NrsK4m

EVENTS

www.financial-planning.com

004_FP0220 4 1/17/2020 9:19:32 AM

February 2020 Financial Planning 5Financial-Planning.com

Editor’s View

Financial Planning is sharply focused on what matters most to advisors — their clients, their practice, and managing their client’s portfolios.

Subscribe and listen: www.financial-planning.com/podcast

From AI to chatbots, hear what else is next for advisors.

001_FP 1 1/17/20 10:51 AM

Difficult choices have trade offs. But what’s the cost of delaying a decision?

Breakup

It was time to make the change. In December I ended my 13-year-relationship with a very proficient RIA and hired another that offered more in-depth financial advice — and lower fees.

The payoffs were immediate. My new planner ad-vised me on health care plan choices, cut my taxes by setting up a Simple IRA for my husband’s consult-ing firm and advised on switching our 529 plans to a different state.

Yet I had delayed making this long-desired switch for more than a year because of the emotional discomfort of ending what had otherwise been a long and beneficial partnership.

What decisions are you delaying? Is it time to reevaluate your fee struc-ture? Hire a tax expert for your firm? Create a succession plan? In some cases, having multiple solutions reduces the pressure, as columnist and advisor Carolyn McClanahan has found.

“I actually have Plan A and Plan B for the business,” writes McClanahan about her firm’s succession planning process (p. 9). “Plan A is to sell the busi-ness to my team for a bargain price — remember, I’m saving for my future so any extra money is gravy. Plan B is if, for some reason, I don’t have a team who wants to continue the practice.”

The 18 months it took me to switch planners cost my family thousands of dollars. How much will procrastination cost you? —Chelsea Emery

005_FP0220 5 1/17/2020 3:01:17 PM

GO FROM

Financial AdvisorTO

Retirement Hero

For its retirement plan recordkeeping customers, ADP agrees to act as a nondiscretionary recordkeeper performing ministerial functions at the direction of the plan sponsor and/or plan administrator. ADP, the ADP logo and Always Designing for People are trademarks of ADP, LLC. All other trademarks and service marks are the property of their respective owners. 99-5376-D-ADV03-0319 ADPBD20190225-0655 Copyright © 2019 ADP, LLC. All Rights Reserved.

You don’t need a cape to be your clients’ #RetirementHeroADP is transforming the way people save for retirement by providing your clients with access to the tools and resources they need to help their employees become retirement ready. Like our ADP mobile app, which makes it easy to enroll, manage, and track progress — anytime, anywhere.

DESIGN A RETIREMENT PLAN THAT UNLEASHES YOUR INNER SUPERHERO.

www.adp.com ■ 844-ADP-ELITE

99-5376-D-ADV03_v1_RH_Ad_Advisor_wmn-suit_7.875x10.5.indd 1 3/8/2019 12:43:10 AM006_FP0220 6 1/17/2020 2:23:26 PM

February 2020 Financial Planning 7Financial-Planning.com

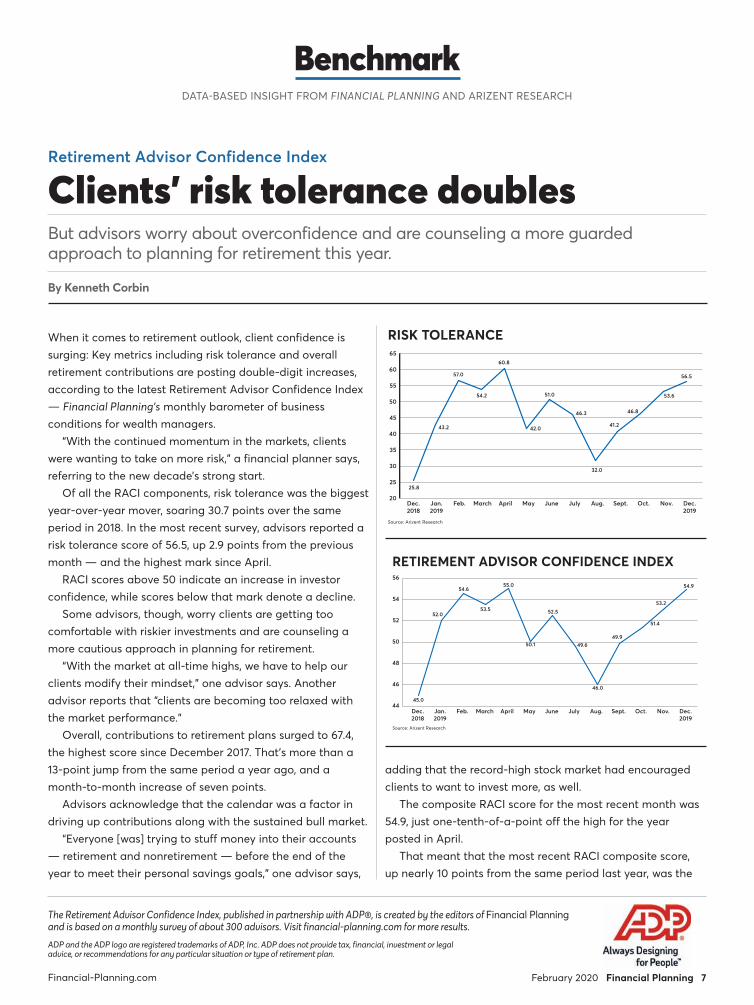

When it comes to retirement outlook, client confidence is surging: Key metrics including risk tolerance and overall retirement contributions are posting double-digit increases, according to the latest Retirement Advisor Confidence Index — Financial Planning’s monthly barometer of business conditions for wealth managers.

“With the continued momentum in the markets, clients were wanting to take on more risk,” a financial planner says, referring to the new decade’s strong start.

Of all the RACI components, risk tolerance was the biggest year-over-year mover, soaring 30.7 points over the same period in 2018. In the most recent survey, advisors reported a risk tolerance score of 56.5, up 2.9 points from the previous month — and the highest mark since April.

RACI scores above 50 indicate an increase in investor confidence, while scores below that mark denote a decline.

Some advisors, though, worry clients are getting too comfortable with riskier investments and are counseling a more cautious approach in planning for retirement.

“With the market at all-time highs, we have to help our clients modify their mindset,” one advisor says. Another advisor reports that “clients are becoming too relaxed with the market performance.”

Overall, contributions to retirement plans surged to 67.4, the highest score since December 2017. That’s more than a 13-point jump from the same period a year ago, and a month-to-month increase of seven points.

Advisors acknowledge that the calendar was a factor in driving up contributions along with the sustained bull market.

“Everyone [was] trying to stuff money into their accounts — retirement and nonretirement — before the end of the year to meet their personal savings goals,” one advisor says,

adding that the record-high stock market had encouraged clients to want to invest more, as well.

The composite RACI score for the most recent month was 54.9, just one-tenth-of-a-point off the high for the year posted in April.

That meant that the most recent RACI composite score, up nearly 10 points from the same period last year, was the

But advisors worry about overconfidence and are counseling a more guardedapproach to planning for retirement this year.

Benchmark

Clients’ risk tolerance doubles

By Kenneth Corbin

DATA-BASED INSIGHT FROM FINANCIAL PLANNING AND ARIZENT RESEARCH

The Retirement Advisor Confidence Index, published in partnership with ADP®, is created by the editors of Financial Planning and is based on a monthly survey of about 300 advisors. Visit financial-planning.com for more results.ADP and the ADP logo are registered trademarks of ADP, Inc. ADP does not provide tax, financial, investment or legal advice, or recommendations for any particular situation or type of retirement plan.

Retirement Advisor Confidence Index

Source: Arizent Research

RISK TOLERANCE

25.8

43.2

57.0

54.2

60.8

42.0

51.0

46.3

32.0

41.2

46.8

53.6

56.5

20

25

30

35

40

45

50

55

60

65

Sept.Dec.2018

Dec.2019

Jan.2019

Feb. March April May June July Aug. Oct. Nov.

Source: Arizent Research

RETIREMENT ADVISOR CONFIDENCE INDEX

44

46

48

50

52

54

56

Sept.Dec.2018

Dec.2019

Jan.2019

Feb. March April May June July Aug. Oct. Nov.

45.0

52.0

54.6

53.5

55.0

50.1

52.5

49.6

46.0

49.9

51.4

53.2

54.9

007_FP0220 7 1/17/2020 11:59:51 AM

8 Financial Planning February 2020

Financial Planning does not provide a certificate of completion. However, you will receive confirmation if you’ve passed the quiz. Please keep the confirmation for your records. Financial Planning reports results to the CFP Board weekly. The board may take an additional two weeks to post results.

Sign up for free and get started today. www.financial-planning.com/ce-quiz

Easily earn up to 12 hours of CE credit from the CFP Board and the Investments & Wealth Institute. Read the articles and answer the appropriate questions correctly to qualify for CE credit.

Earn CE credits with Financial Planning

001_FP0003 1 1/17/20 10:53 AM

second highest reported since January 2018. Among asset classes, equities posted the strongest yearly gains. That RACI survey component saw a score of 62.9 in the most recent period, off less than a point from the previous month. But it was more than 22 points ahead of last year.

One advisor reports “allocating more to equities due to rate conditions and generally positive longer-term outlook,”

and some advisors are wondering when the wave will crest.“As bonds have matured, more clients are looking at higher

dividend-paying stocks in solid businesses to replace fixed income,” one suggests. “At times like this you know you have to be close to the peak because stocks are being viewed as having less long-term risk than a 2% bond, which we know is not the case.” FP

Benchmark

Kenneth Corbin is a Financial Planning contributing writer in Boston and Washington. Follow him on Twitter at @kecorb.

Source: Arizent Research

DOLLAR AMOUNT OF ALL CONTRIBUTIONS RECEIVED FOR RETIREMENT PLANS

50

52

54

56

58

60

62

64

66

68

70

Sept.Dec.2018

Dec.2019

Jan.2019

Feb. March April May June July Aug. Oct. Nov.

54.1

63.9

58.6

63.0

64.1

55.2

59.058.3

54.6

60.2 60.7

60.4

67.4

AMOUNT OF CLIENT ASSETS USED TO PURCHASE EQUITY-BASED SECURITIES

Source: Arizent Research

40

45

50

55

60

65

70

Sept.Dec.2018

Dec.2019

Jan.2019

Feb. March April May June July Aug. Oct. Nov.

40.6

60.562.1

58.6

64.8

54.1

58.5

50.0

44.6

53.2

57.6

63.862.9

008_FP0220 8 1/17/2020 3:11:47 PM

February 2020 Financial Planning 9Financial-Planning.com

Rarely does life or business play out as intended. Many advisors avoid planning for succession until upheaval occurs.

Those who do plan in advance are often blindsided when their next generation bolts for greener pastures.

Because we cannot predict the future, my approach to succession planning is very Bud-dhist — plan for what you want and don’t be attached to the outcome.

How does this work? A succession plan is not only for retire-

ment — it is also something that is needed in the unfortunate events of premature death, serious illness or incapacity.

All advisors should have a plan for these potential events from day one of opening their business.

If you are a solo practitioner, the plan may be something as simple as a list of other advisors you trust to take care of your clients. If your firm has multiple advisors, a buy-sell

agreement and standardized processes to ease transition of client care may be enough.

From a personal standpoint, make sure you have enough disability and life insur-ance to provide for yourself and your family. This takes the onus off the need to get value from your practice if you experience an untoward event.

Just like some doctors live an unhealthy lifestyle, there are financial planners who fail to have their own financial plan.

The bigger challengePlanning for the day you no longer want to work is the bigger challenge.

A good succession plan takes years to put into place. You have to develop talent to replace you, let them fly with taking care of clients, reward them appropriately for their growth and finally let go of control.

A lot can happen during those years, and there are many reasons a succession plan

McClanahan

My Plan B for succession

By Carolyn McClanahan

An exit strategy doesn’t have to be set in stone. It can be as fluid and adaptable as other major life choices.

can fall apart. Control of this process is an illusion.

You may get to the point when you are supposed to leave and find out you aren’t ready to go. Your replace-ments may decide they want to move to another area of the country for family or the weather. Or after a number of years working with you, they may discover they don’t like how you run your business.

Selling your practice is also fraught with challenges. Most of us think our practice is more valuable than what other people want to pay for it.

Market valuations rise and fall, and finding a buyer who gels with your values may be tough. The transi-tion can take a lot of time to unfold.

Taking the first stepThe first step in a succession plan is making sure you develop the resiliency to pivot if plans don’t work out. The fact is that too many owners count on the value of their practice as their main savings for retirement.

This lack of liquid financial freedom can box them into a corner.

Just like we tell our clients, it is crucial to save

CLIENT MANAGEMENT

Just as some doctors live an unhealthy lifestyle, there are financial planners who fail to plan.

009_FP0220 9 1/17/2020 9:20:41 AM

10 Financial Planning February 2020

McClanahan

for the day we can no longer work, or no longer want to work. I have Plan A and Plan B for the day I give up my practice.

What are Plans A and B?Plan A includes saving enough for my needs and basic wants so these are fully funded by the day my disability insurance runs out.

This way, no matter what value I receive from my practice or when I have to quit for whatever reason, my husband and I will be OK.

Plan B provides for all the nice extras should I receive an actual return on my practice — with the additional funding, we’ll leave a legacy, give more to charity while we are alive and upgrade our travels and experiences.

The most important step in a succes-sion plan is making sure you have well-documented processes in place. Advisors keep too much institutional knowledge in their head.

By developing a culture of standard processes and good documentation of the client’s story, and codifying how work is done, you provide a bridge to train the next potential successor if the first one doesn’t work out, or if you make an unexpected premature exit from your practice.

Also, well-documented processes and organized workflow increase the attractiveness of your practice in a sale.

Happy employees are most likely to stick around.

Is your workplace enjoyable? Is the work a fun challenge, and do your employees know their career path? What are you doing, if anything, to foster their growth?

I travel a significant amount for speaking engagements and have a great team that supports this contribu-

tion to the profession. However, over the past couple of

years, we’ve had some road bumps and interpersonal challenges, mostly caused by a failure in leadership — that would be me!

An unhappy team memberA key team member of ours was

becoming unhappy. We have a healthy enough culture

that he told me about his concerns early, and he thankfully didn’t bolt for the door.

I’m a big believer in coaching, and have utilized coaches for myself for most of the past 12 years.

I pulled in a couple of coaches to help us and we are back on a good path. But the light bulb went off for me — my team would benefit greatly from individual work with a coach.

Duh. For 2020, we have set aside a very

nice budget for the team members to work on their growth and the issues that they want to address.

I’m excited to see what happens in this new year.

I preach to clients and other advisors that the best financial plan includes finding work you love and doing it as long as possible.

And the most important part is to make sure you thoroughly enjoy the rest of your time along the way, so there are no regrets if you don’t live a long life.

The people who are more likely to

die peacefully are those with the fewest regrets. This is the way I live and I’m frankly at peace if I die today. In the long term, my plan is to gradually cut back, and with that, I will cut my pay and responsibilities.

I estimate that I’ll work at least another 20 years, but who knows? That puts me into my 70s, and I’ll have plenty of savings.

My team is mostly equipped to take care of our clients and we have a buy-sell agreement in place.

My current role is quality control, taking care of client life emergencies and tax planning.

My team is smart and will hire someone to take those responsibilities if I’m out of action anytime soon.

Just like I have plan A and B for my personal life, I actually have plan A and plan B for the business.

Plan A is to sell the business to my team for a bargain price — remember, I’m saving for my future, so any extra money is gravy.

Plan B is if, for some reason, I don’t have a team who wants to continue the practice when I no longer can.

I most likely will let the client base naturally downsize and refer remaining clients to advisors I trust.

A healthy sense of detachmentA sale wouldn’t be out of the question, but what I’ll have left at the end probably won’t be worth the effort. Most of all, I have a healthy sense of detachment.

I’ll do my best to make sure our clients are well cared for and the team finds fulfillment in their work so they’ll want to carry it on when I’m gone.

If it doesn’t work out as I planned, I did my best and had a joyful life along the way. FP

Carolyn McClanahan, a CFP and M.D., is a Financial Planning columnist and director of financial planning at Life Planning Partners in Jacksonville, Florida. Follow her on Twitter at @CarolynMcC.

The best financial plan includes finding work you love and doing it as long as possible.

010_FP0220 10 1/17/2020 9:20:42 AM

Last Modified

Art Director

Copy Writer

Proj Mgr

Acct Svc

Prod Mgr

Art Buyer

Copy Edit

Mac

100

None

None

Trim

Live

Folded Size

Finishing

Colors Spec’d

ETAS January Print Ad

8.125” x 10.75”

None

Job Description

Bleed

Special Instr.

Publications Financial Planning

Job # Document Name ETF-A-19-11207542-357_ETAS-Print.inddETF-A-19-11207542 Version #357

jbass

TBD

rwaller

shennagin

rwaller

TBD

TBD

nminieri

Colors In-UseLinked GraphicsETRADE_Star_Rball_4c.ai ETRADE_DGM_Logo_With_K_Advisor_Ser-vices_K-4C.eps

Cyan Magenta Yellow Black

CONT

ENT

7.875” x 10.5”

7” x 10”

None

None

4C

BY SIGNING YOUR INITIALS ABOVE, YOU ARE STATING THAT YOU HAVE READ AND APPROVED THIS WORK.

1-6-

2020

4:0

9 PM

ACCT SERVICE PROD COPY EDIT

COPYWRITER ADCD/ACD

User Printer Output Date

1-6-2020 4:09 PM

BOSMLW-NMXWJ040 9FL-YELLOW-COLOR 1-6-2020 4:09 PMMech Scale

Print Scale

Stock

Mechd By: nminieri RTVd By: nminieri

1

RELE

ASED

TO

VEND

OR

Vend

or: Fi

nanc

ial Pl

annin

g

Relea

se Da

te: 1.

6.20

And we’re dedicated to offering you the best experience you can get. Our Relationship Managers take the time to learn your business inside and out, meaning you can spend more time doing your work and less time dealing with the back of the house. Plus, they work tirelessly to find customized solutions for your business, helping you achieve your full potential on your own terms.

To learn more, call 800-955-7808 or visit etrade.com/advisorservices.

© 2020 E*TRADE Savings Bank, doing business as “E*TRADE Advisor Services.” Member FDIC. All rights reserved. Investment Products: Not FDIC Insured — No Bank Guarantee — May Lose Value. E*TRADE, E*TRADE Advisor Services, and Liberty are registered trademarks or trademarks of E*TRADE Financial Corporation. All other trademarks mentioned herein are the property of their respective owners. Product and service offerings are subject to change without notice. E*TRADE Savings Bank and its affiliates (“E*TRADE”) do not warrant these products, services and publications against different interpretations or subsequent changes of laws, regulations and rulings. E*TRADE does not provide legal, accounting, or tax advice. Always consult your own legal, accounting, and tax advisors.

WE’RE ASDEDICATED TOYOU AS YOU ARE TO YOUR BUSINESS.

011_FP0220 11 1/17/2020 2:23:26 PM

12 Financial Planning February 2020

Not long ago, I was having a difficult conversation with a client. This woman would not listen to reason, and despite my best efforts, I was about to lose it.

“How many times have you heard me say it?” I told her. “You made a good investment; the stock has had a good run. But now, because of that, you’re overweighted. You need to take some gains off the table and reallocate that money so you can stay within the guidelines we’ve set up for you. And it’s in your retirement account, so you don’t even have to worry about the capital gains. What’s the problem? Which part of this do you not understand?”

I was really laying it on thick. And I was right! We had clearly established our ground rules for asset allocation. But the client had wanted to make a play on one of the FAANG stocks; it seemed very important to her.

Reluctantly, I helped her make the buy in her IRA. We had set a firm limit of no more than 10% allocated to any individual stock, and she understood that. But with the big rise in price she experienced, the stock’s value was now way outside the boundaries for any individual holding. It was time to sell. Why was she refusing my advice?

Possibly because, in this case, the client was me.

‘Why would you sell a winner?’I sat there, staring at my screen, knowing I needed to hit the sell button … and I couldn’t do it. As I continued to broil in my own indecision, the tapes of previous client conversations started playing over in my mind: “But the price is still going up!” “Why would you sell a winner?” “I read all the

The day I lost it over a FAANG stock

By Kimberly Foss

There’s a way to offer sound counsel to clients and also permit them the opportunity to take a profitable flier from time to time.

material on the stock, including an article in Forbes that says it could go even higher!”

I had heard it all before from the other side of the desk, but now that I was my own client, I was finding it much harder to follow my own advice.

Fast-forward: I did ultimately sell that position, and I did reallocate the money. To sweeten the irony, the next day my darling stock experienced a major sell-off. I simultane-ously got to cash out close to the top (at the time) and dodge a bullet.

But I’ll never forget how hard it was to pull that trigger. I remind myself of that every time I sit down with a client who is eager to cash in on a major payday with one of the FAANG stocks. With all the hype and glamour that come alongside these five technology giants — Face-book, Apple, Amazon, Netflix and Google — it’s not hard to see how even the most savvy clients can become dazzled.

A profitable flier How do we manage to offer sound counsel to our clients

This woman would not listen to reason, and despite my best efforts, I was about to lose it.

FossIN PRACTICE

012_FP0220 12 1/17/2020 9:21:38 AM

t h i n g s p e o p l e s a y t o t h e i r f i n a n c i a l a d v i s o r s

“i need to play

catch up,

but i can’t afford

to trip up.”

The security of lifetime income meets real market opportunities.A Lifetime Check is protected income for life, and that can help almost any retirement plan stay on track.

But with Jackson’s variable annuities, you can do even more. That’s because we believe in giving fi nancial

advisors more investment choices and the ability to take advantage of market opportunities when they occur,

which means you can help keep your clients’ retirement plans rolling along smoothly.

Find the annuity to help your clients pursue fi nancial freedom at www.Jackson.com/LifetimeIncome

Before investing, investors should carefully consider the investment objectives, risks, charges and expenses of the variable insurance product, including its underlying investment options. The current prospectus (or for the variable insurance products the contract prospectus and underlying fund prospectuses, which are contained in the same document) provides this and other important information. Please contact your representative or the Company to obtain the prospectus(es). Please read the prospectus(es) carefully before investing or sending money.

Variable annuities are long-term, tax-deferred investments designed for retirement that involve investment risk and may lose value. Earnings are taxable as ordinary income when distributed and may be subject to a 10% additional tax if withdrawn before age 59½. Add-on benefi ts are available for an extra charge in addition to the ongoing fees and expenses of the variable annuity and may be subject to conditions and limitations.Guarantees are backed by the claims-paying ability of Jackson National Life Insurance Company® or Jackson National Life Insurance Company of New York® and do not apply to the investment performance of the separate account or its underlying investments.Annuities are issued by Jackson National Life Insurance Company (Home Offi ce: Lansing, Michigan) and in New York by Jackson Life Insurance Company of New York (Home Offi ce: Purchase, New York). Variable annuities are distributed by Jackson National Life Distributors LLC. These products have limitations and restrictions. Contact the Company for more information. Jackson is the marketing name for Jackson National Life Insurance Company and Jackson National Life Insurance Company of New York.

Not FDIC/NCUA insured • May lose value • Not bank/CU guaranteed • Not a deposit • Not insured by any federal agency

CNC22663B 08/19

CNC22663B_0819_JFP.indd 1 8/1/19 2:44 PM

013_FP0220 13 1/17/2020 2:23:27 PM

14 Financial Planning February 2020

Foss

while also permitting them the oppor-tunity to take a profitable flyer from time to time? I believe, as with most things in life, that the answer lies in a thorough knowledge of the client. A sense of proportion and discipline is also invaluable.

Part of that essential client knowl-edge is understanding the magnetic pull of the big score. Like all human beings, our clients experience greed — the temptation to let all the chips ride just one more time.

I certainly felt that pull as I looked at the gain in my IRA account. Because I know how it feels, I can explain to my clients that no emotion — especially that lust for the big win — is a valid basis for making long-term financial decisions. I remind them that we have to focus on what we can control: allocation, expenses, discipline and structure.

Research has shown that individuals don’t pick stocks any better than choosing them by throwing darts at a

dartboard. So I don’t try.

The 10% rule All that said, making a pure play in one of the FAANG stocks with a preset portion of portfolio assets can make sense for certain clients. But this is where a sense of proportion becomes important. When I determine that a particular client fits that profile, the first thing I do is set a limit of 10% not to be exceeded in any one individual stock.

Why 10%? This relatively low percentage of assets protects the client from most of the consequences of lousy market timing — which is unpredict-able — while still affording enough skin in the game to make the experience

meaningful.Next, we set a firm upside target, at

which point we agree in advance to take profits and reallocate according to the client’s asset allocation plan. The idea here is to allow the client a bit of room for the stock to run — without violating the investment integrity of the allocation we’ve put in place.

Let me be clear: I’ve been a fan of Google and Amazon, and even Apple, since the early days; I’ve even bought them in my son’s 529 account and, as I mentioned, in my own IRA. (Personally, I’m less enamored of Facebook and Netflix).

But even though my son has a lot of years available to recover financially if one of his FAANG holdings goes bust, I’m still not going to violate the guidelines that we’ve put in place. As a wealth advisor to my clients and myself, how can I expect my clients to follow my advice if I don’t walk the talk myself?

Hogs get slaughteredAnd so, this brings us back to where we started. The ancient proverb, “Physi-cian, heal thyself,” seems very appli-cable here. Before we start lecturing our clients on the pitfalls of being over-enticed by the big tech stocks, we need to take stock of our own tenden-cies.

The advice we give to our clients has real-world ramifications, and no stock will go up forever. It may be fine to occassionally let that occasional client take a flier on Apple or Amazon or the next stock market sensation. But set your limits, both going in and coming out.

And remember: Pigs profit, but hogs get slaughtered. Especially if the client is you. FP

Kimberly Foss, CFP, CPWA, is a Financial Planning columnist and the founder and president of Empyrion Wealth Management in Roseville, California, and New York. Follow her on Twitter at @KimberlyFossCFP.

I sat there, staring at my screen, knowing I needed to hit the sell button … and I couldn’t do it.

With all the hype that swirls around FAANG stocks, even the most savvy clients can become overly optimistic about the potential for future gains.B

LOO

MB

ERG

NEW

S

014_FP0220 14 1/17/2020 9:21:41 AM

Reason #5 of 76

Advisor Advantage Powered with Cambridge

Fee only or fee focused solutions for independence. Offering intelligent flexibility to the independent financial professional for their business.

877-688-2369 | joincambridge.com ®A Financial Solutions Firm

Securities offered through Cambridge Investment Research, Inc., a broker-dealer, member FINRA/SIPC, and investment advisory services offered through Cambridge Investment Research Advisors, Inc., a Registered Investment Adviser. Both are wholly-owned subsidiaries of Cambridge Investment Group, Inc.

Advisor Advantage is an inclusive approach to delivering service and support, including:

An extensive product menu and custodian choices

Sophisticated and integrated technology options

Multiple strategies for advisor growth

A smart approach to service and support customizable to your business model

Your choice for dual registration or no FINRA registration

Contact us to speak to a truly independent firm and learn more about the 76 ways we can support you and your business. Your choice is our business.

015_FP0220 15 1/17/2020 2:23:27 PM

16 Financial Planning February 2020

I offended an entire table of fellow financial advisors while attending a conference last year when I made this statement: “Everyone at this table makes too much money relative to what we do.”

I went on to explain that in no other profession do service providers have the luxury of basing their prices on what their clients can afford to pay.

Imagine a lawyer with one hourly rate for one group of clients and a higher rate for another group. Or a doctor who charges a higher copay to his patients who make more money.

‘Good old days’I passed my first securities exam in 2000. At the time, financial advisors were charg-ing an average fee of 1% to their clients for investment advice. Now, 20 years later, many advisors are still charging similar fees.

A 2018 study by RIA in a Box, which

surveyed 1,500 firms, found the average advisory fee charged to clients was 0.95%.

Since 2000, there has generally been tremendous fee compression in the financial services sector.

I remember hearing stories from older advisors of the good old days, when equity trades cost 12 cents a share — a 1,000-share order would cost $120 (not to mention the minimum ticket charge for small orders).

The great raceBy 2000, that 1,000-share order cost

$19.95. At the beginning of 2019, the cost was $4.95, and today it’s $0.

In the managed money world, there are now more assets under management in low-cost equity ETFs than higher-cost equity mutual funds.

When it comes to pricing, race to the bottom is not just occurring within the financial services industry.

Boomer

Are advisors overpaid?

By Allan Boomer

Our industry is one of the few that’s barely experienced pricing pressure ... so far. Here’s how to assure you keep providing value.

Amazon is pushing prices lower and, in the process, forcing traditional retailers out of business.

Planet Fitness charges a fraction of the fees charged by Bally 20 years ago — I could go on.

As a financial advisor, I always relished the fact that clients will pay a premium for good advice. But how much of a premium will they pay and for how long?

Robo specterWe all know that robo

advisors are really robo investors and that there is no replacement for financial planners.

However, as robo advisors push fees for investment advice lower, they are causing clients generally to devalue investment advice.

That’s because even if clients avoid using those digital platforms, the knowledge that there are less-expensive options makes part of what we do seem less valuable.

Despite the impact of fee breakpoints for larger clients, there are some clients who are paying two times to three times what other clients are paying for very similar financial advice

CLIENT MANAGEMENT

We all know that robo advisors are really robo investors and that there is no replacement for financial planners.

016_FP0220 16 1/17/2020 9:22:47 AM

February 2020 Financial Planning 17Financial-Planning.com

and services. When you look at our compensa-

tion per hour, there is huge variability in the rates that are charged to our well-heeled clients when compared with the rates for clients who can barely meet our minimums.

In other words, our wealthier clients are supplementing our less-wealthy clients.

Ironically, our lower-wealth clients sometimes take up way more of our time than our wealthier clients — which further exacerbates this pricing inequity. As long as clients value what we do for them, none of this matters. So our job is to make sure we are delivering value.

Let’s assume the average price in the marketplace for a solid comprehen-sive financial plan is $10,000.

This makes a lot of sense for the $1 million client who is paying a fee that equates to 1%. It may even make sense for the $2 million client to pay $15,000 to $20,000 for a similar service.

But once you get above $5 million, it

becomes a head-scratcher. Why should this client pay $25,000 to $50,000 for a financial plan? And why should any client pay more than $100,000 a year?

New wave plannersThey do it today because it has

always worked that way. How long will this continue? And will their children who inherit their wealth be willing to work under this same fee arrangement?

There is a wave of planners com-pletely turning the fee model on its head by charging flat fees. They would take a $10 million client and charge a flat of $10,000 or $20,000 and then use a robo-type process to manage all or part of the investment portfolio.

This implies that the greatest fee compression will occur in financial planning at the ultrahigh-net-worth end of the market.

It’s one of the reasons that family offices exist — wealthy families added up all the money they were paying to advisors and decided to do things differently. They saw it would be cheap-er to hire their own staff, rent or buy their own offices and pay for their own technology.

7 ways to boost valueThere is an old adage that says

“price is what you pay, value is what you get.”

The answer is not to lower your fees or to pivot to a flat-fee model. We have to explore ways to deliver more value.

1. Watch your service levels and service standards. My firm recently instituted a series of service standards for routine requests like responding to emails, returning phone calls or completing client research requests.

Each of these service items has a “standard” response time and an

“excellent” response time. To maintain these standards we had to invest in more staff and train them to focus on delivering these standards.

2. Give your clients more technol-ogy. Not every client will use the online portals, apps and calculators we have access to, but the ones who do will find them tremendously valuable.

3. Develop a calendar. My firm recently implemented a financial planning calendar to ensure we are consistently and regularly discussing financial planning topics with every client each month or quarter, as opposed to the lazier way of conduct-ing financial planning on demand.

4. Maintain better communication. Send your clients articles from time to time — and not just on financial topics. Perhaps suggest a biography to read or a restaurant to consider. Remember that part of what the clients are paying for is a relationship with someone who understands them beyond their money.

5. Create experiences. My firm will be rolling out targeted client dinners this year with groups of clients with similar interests and backgrounds.

We are also researching games and activities for their children to learn about financial stewardship.

6. Take better notes. The CRM we implemented a few years ago helps us remember the personal details of a client’s life better than before.

7. Focus on life goals, not just financial goals. It’s as important for us to understand “why” they want to achieve certain goals as it is for us to understand “what” they want to achieve. If you can make your client’s actual life meaningfully better (as opposed to just their financial life), you have landed a client for life. FP

Allan Boomer, a Financial Planning columnist, is managing partner and chief investment officer of Momentum Advisors in New York. He co-hosts a weekly radio show on SiriusXM Ch. 126 that focuses on wealth building and entrepreneurship. Follow him on Twitter @MomentumAdvice.

The answer is not to lower fees or pivot to a flat-fee model. We have to explore ways to deliver more value.

My firm is researching games for clients’ children to learn about financial stewardship.B

LOO

MB

ERG

NEW

S

017_FP0220 17 1/17/2020 9:22:49 AM

18 Financial Planning February 2020

I recently left the study group I created five years ago. There hadn’t been a falling out and there wasn’t anything wrong with the group. It just no longer supplied the support structure I needed.

I’ve since moved to quarterly one-on-one conversations with select advisors. It suits me much better.

Here’s how I got from there to here.

Look for differences, tooPeople have asked me over the years how my study group came into being. The reality is I called each advisor and asked them if they’d like to join me. It was that easy.

Beforehand, I had researched each potential member to understand where they were in starting or running their firm, their fee model and their geographical location.

I was looking for similarities but also some differences. All of the planners ran their own practices, but some were fee-only and others

were fee-based. Some had a stable AUM on which to build their business, while others were starting from scratch.

But everyone wanted to be a great advisor and wanted to learn from others. We developed a set of engagement standards, which helped us understand appropriate behaviors and what was expected.

Over five years, we got to know each other really well — sharing our professional and personal highs and lows. We met every two weeks via video conference and then tried to meet in person each year.

It worked well for the first few years, but then professional and personal lives evolved. Some of us (me included) wouldn’t be able to make a call for four to six weeks. Then, as babies and toddlers entered our respective family mixes, the in-person retreats became increasingly difficult to schedule.

Gradually, I felt my close relationships in the group start to weaken. I started to talk

Building — then leaving — a support system

By Dave Grant

I created a meaningful study group. Here’s why I stepped away.

to advisors outside of the group. Eventually, I found myself gaining more value from these one-on-one conversations. At that point, it became appropri-ate for me to step away from the group.

Dead-end conversationsAdvisors’ collaborative needs evolve over time. If you’re starting your own firm, give and take with other advisors helps you make sure you’re doing everything correctly and haven’t missed any tricks. If you’re transitioning to a new service model, like managing money, it’s helpful to have another advisor on the custodial platform to use as a sounding board as you get familiar with the system.

But, in my old group, we’d passed the startup phase and had defined client types. We weren’t looking to grow a megafirm and were starting to make some good income.

With some of the initial goals achieved, conversa-tions began to run dry.

After six years at my firm, I have a good idea of the hours I want to work, the revenue I need to support my family and the ideal clients I want to work with. It’s in a

At some point, a group approach may stop working and one-on-one conversations seem to work better.

GrantNEW GENERATION

018_FP0220 18 1/17/2020 2:33:35 PM

February 2020 Financial Planning 19Financial-Planning.com

comfortable growth stage. I don’t have talking points every couple of weeks.

But I also came to realize that my temperament was a factor in outgrow-ing my group. I’m a listener more than a talker. There were times on a video call or at a meeting that I didn’t say much.

Conversation was flowing and it was fun to see people hashing things out. Conversely, there were other topics, like digital content marketing, where I had a lot of ideas and domi-nated the conversation.

But, on the whole, I came to realize that a group setting just doesn’t suit my personality. I’m at home when I can engage in a one-on-one conversation that doesn’t have a time limit.

Once I recognized this, I set up quarterly calls with select advisors and it has suited me much better. It’s known ahead of time that our calls are likely to last over an hour as we canvass personal and professional updates, but may also stumble on a professional topic on which we take a deep dive. For local advisors, we clear two hours for lunch to enjoy each other’s company and share ideas.

A new approachIn transitioning out of my group, I took a different approach in finding one-on-one relationships. As I wasn’t specifically looking for opinions or guidance in my business from these relationships, I sought out more diversity among those who were already friends.

I now have a group of three advisors I talk to regularly and one online group of four advisors who discuss practice management issues of lifestyle prac-tices. My one-on-one relationships are

long-term friendships in the industry before we become business confidants. One owns a much larger RIA than mine in California, another is transitioning to his own firm in the suburbs of Chicago, and yet another runs a practice alongside another business.

We are different, but the one thing that is important to all of us is that we value the one-on-one nature of our relationship. We discuss each other’s business, knowing that the other might not have gone through it before — or will even go through it in their career — but we seek a fresh set of eyes.

The strong friendships set these relationships apart from other profes-sional relationships. We can challenge each other on topics or opinions without the risk of a group dynamic making it uncomfortable.

Do you need a support system?Do you have a support system in place? If not, consider finding some advisors you admire and ask them if they’d be willing to talk with you on a frequent basis. Many will be flattered, and say yes.

But what if things are more advanced than that? What if you are in a group setting when, in reality, you excel in the one-on-one environment or vice versa?

This is where you need to understand where you feel comfortable in relational communications and what support you need for the next phase of your career.

Don’t feel bashful about walking away from a group or relationship — there’s a chance, after all, that others are thinking the same as you and just need someone to take the initiative.

Design the system that suits you the best, and then you’ll be able to give your best to those with whom you interact. FP

If you lack a support system, find some advisors you admire and ask if they’d be willing to talk with you on a frequent basis.

Dave Grant, a Financial Planning columnist, is founder of the planning firm Retirement Matters in Cary, Illinois. He is also the founder of NAPFA Genesis, a networking group for young fee-only planners. Follow him on Twitter at @davegrant82.

For some personalities, a one-on-one conversation just seems to work better.ABO

DE

STO

CK

019_FP0220 19 1/17/2020 2:33:43 PM

February 2020 Financial Planning 21Financial-Planning.com20 Financial Planning February 2020

By Michael Kitces

As the advisory industry has grown less transactional and more relationship-based, the total number of clients any one advisor can handle has decreased dramatically.

Advisors now straddle a capacity crossroads: Should they con-sciously decide to stop growing — or hire additional staff to increase the firm’s scope? It’s a decision that will reverberate throughout their practices, careers and personal lives.

The problem has become especially acute in the past decade or so. In the early days of the profession, advisors rarely had to consider their capacity to take on business, because the business itself was more transactional. The focus was on finding new opportunities.

Clients, meanwhile, were simply people whom the advisor had once sold a product to and had minimal ongoing service needs. That’s why brokers or insurance agents often had hundreds of clients — many of whom the advisor might not have actually met with in one, three or even five-plus years.

Today, however, there are only so many hours in the week to take

The Next Move

There comes a time when advisors must decide how much more to grow. Here’s how to make the tough choice.

Financial-Planning.com22 Financial Planning February 2020

all the meetings and perform all of the service work. That often leaves advisors with room for no more than 75 to 100 clients.

The most straightforward way to navigate the capacity crossroads is simply to hire more staff. This often entails hiring an administrative assistant to handle more of the servicing work, then adding a para-planner to help with the planning support, and eventually a servicing advisor to manage at least a portion of client relationships.

Adding staff, however, means the advisor now has to manage a team. This results in a material burden of

additional work — in the name of generating what is often remarkably little additional income.

Early clients generate substantial income for the advisor-owner doing the work, but the owner only generates the profit margin remaining after other advisors start doing the work.

Enter small giantsThe fact is that some advisors don’t want to hire and manage people. This has led to a dichotomy in the industry between so-called lifestyle firms that choose not to hire and remain founder-centric, and enterprise firms that grow beyond the founder.

But many firms don’t clearly fit either definition. Some focus on being high-income solo advisors and others on rapid growth and scaling to become a large enterprise.

Then there is a substantial subset of advisory firms that do eventually grow beyond their founders, adding associ-ate advisors, service advisors and sometimes even partners, in a desire to serve more clients. The crucial differ-ence is they don’t have the mentality of being enterprise builders by any classic definition.

Rather than grow for growth’s sake — maybe with the goal of a sale and liquidity event for the founders — these firms are simply trying to get better at delivering whatever unique service they have created. This is where “small giants” come in.

In 2006, Bo Burlingham, the former executive editor of Inc., published “Small Giants.” The subject of his book is companies that “choose to be great instead of big.” These companies are purpose driven. They aim to be the best at whatever they do, rather than make decisions solely to maximize growth.

Part of what make small giants successful is their holistic focus. Their goals are being better and prioritizing service — not only to clients but also to employees, vendors and suppliers, and communities.

In turn, this focus encourages higher-quality relationships, reinforcing these stakeholders’ attraction to the business in the first place.

Together, it creates what Burlingham calls the “mojo” of small giants: the

Lifestyle firms are those in which advisors are paid first and foremost for advisory work. Notably, lifestyle firms are rarely sold.

business equivalent of a leader’s charisma, which makes people want to connect with the company.

Ultimately, Burlingham finds the defining characteristics of small giants are their mission-driven purpose; service leadership; intimate, employee-first culture; relationship-centric approach to customers, suppliers and vendors; deep roots in their communities; and focus on not necessarily maximizing profits, but being certain to protect their gross margins to remain stable without compromising company values.

This model goes beyond the lifestyle firm that reaches its capacity and stops growing. But it isn’t the same as a classic enterprise that pursues growth and maximizes shareholder value — with whatever outside capital and potential loss of control that may entail.

Similar upsidesHere is the conventional view of business: It’s a grow-or-die world, and owners should always want to keep growing and maximizing profits.

Yet the connection between advisory firm growth and its anticipated benefits is not so straightforward.

There are virtually no economies of scale to be found in the operation of an advisory firm as it grows from $50 mil-

The not-so-sweet smell of successA quantum leap in the size of an advisory practice may bring only a small step upward in pay for the founder. Here’s a hypothetical example:

Celia started her advisory practice with the goal of earning a good, healthy income. After her first year in business she was happily advising 25 clients, with an annual gross revenue of $50,000 and a net revenue of $35,000.

She loved spending time with clients, having lengthy discussions about their lives and goals, and creating thoughtful, detailed plans for them. She did such a good job they began referring several of their friends.

She didn’t want to refuse her clients’ referrals, but without a clear vision of what she wanted to grow toward — or who her ideal target client was — the firm quickly mushroomed to more than 100 clients.

With an increase of gross revenue to $250,000 across those 100 clients, Celia had to hire an assistant at $40,000 per year and a paraplanner at $55,000 per year. Now that she had employees and a much larger client base, she needed a larger office space and faced other new overhead expenses, including insurance, payroll services and taxes, and new office equipment.

Once Celia’s employees and overhead expenses were paid, her net revenue was only $105,000.

Despite the fact that she quadrupled her client base, adding more than $200,000 of additional revenue, her net take-home income rose to only $70,000. Celia was stressed out and unhappy. And because she had so many more clients, she couldn’t spend the focused time on plans that she once enjoyed so much.

There was little opportunity to catch up with her favorite clients over lunch or drinks, and she resented having to maintain a strict meeting schedule to ensure she could give all her clients at least some attention.

The business was growing, but Celia wasn’t happy. —Michael Kitces

COMMUNITYSmall giants understand the value ofestablishing deep roots in theircommunity.

CULTURESmall giants foster a culture of intimacyby putting employees first, caring for them in the totality of their lives.

PURPOSESmall giants have a vision, a powerfulmission statement and core valuesthat can be brought to life.

CUSTOMERSSmall giants cultivate meaningfulrelationships with customers,suppliers and all stakeholders.

LEADERSHIPSmall giants are made up of servantleaders who believe in leading byvalues.

FINANCESmall giants believe in protecting theirgross margins without compromisingcompany values.

6 key traits of a small giant business

Source: www.smallgiants.org

022_FP0220 22 1/17/2020 9:51:13 AM

February 2020 Financial Planning 23Financial-Planning.com

But many firms don’t clearly fit either definition. Some focus on being high-income solo advisors and others on rapid growth and scaling to become a large enterprise.

Then there is a substantial subset of advisory firms that do eventually grow beyond their founders, adding associ-ate advisors, service advisors and sometimes even partners, in a desire to serve more clients. The crucial differ-ence is they don’t have the mentality of being enterprise builders by any classic definition.

Rather than grow for growth’s sake — maybe with the goal of a sale and liquidity event for the founders — these firms are simply trying to get better at delivering whatever unique service they have created. This is where “small giants” come in.

In 2006, Bo Burlingham, the former executive editor of Inc., published “Small Giants.” The subject of his book is companies that “choose to be great instead of big.” These companies are purpose driven. They aim to be the best at whatever they do, rather than make decisions solely to maximize growth.

Part of what make small giants successful is their holistic focus. Their goals are being better and prioritizing service — not only to clients but also to employees, vendors and suppliers, and communities.

In turn, this focus encourages higher-quality relationships, reinforcing these stakeholders’ attraction to the business in the first place.

Together, it creates what Burlingham calls the “mojo” of small giants: the

Lifestyle firms are those in which advisors are paid first and foremost for advisory work. Notably, lifestyle firms are rarely sold.

business equivalent of a leader’s charisma, which makes people want to connect with the company.

Ultimately, Burlingham finds the defining characteristics of small giants are their mission-driven purpose; service leadership; intimate, employee-first culture; relationship-centric approach to customers, suppliers and vendors; deep roots in their communities; and focus on not necessarily maximizing profits, but being certain to protect their gross margins to remain stable without compromising company values.

This model goes beyond the lifestyle firm that reaches its capacity and stops growing. But it isn’t the same as a classic enterprise that pursues growth and maximizes shareholder value — with whatever outside capital and potential loss of control that may entail.

Similar upsidesHere is the conventional view of business: It’s a grow-or-die world, and owners should always want to keep growing and maximizing profits.

Yet the connection between advisory firm growth and its anticipated benefits is not so straightforward.

There are virtually no economies of scale to be found in the operation of an advisory firm as it grows from $50 mil-

lion to $250 million to $1 billion to $3 bil-lion. That’s because overhead expense ratios and profit margins remain remarkably steady.

I maintain that there’s no discern-ible growth-leads-to-efficiencies link to be found among 99%-plus of all advisory firms.

Another drag: Growth often necessitates introducing new partners to the business who have a stake in what is being built, otherwise they’ll walk away with their clients and revenue. This results in a dilutive effect to equity and profits.

At the same time, actual take-home income growth ends up being far slower than revenue growth as advisory firms expand past their founder’s capacity.

Consider this: For the first 100 clients, the advisor earns virtually all the net revenue, minus just a small allocation for overhead expenses.

Those expenses can be as high as 70 to 80 cents on the dollar. Yet the

advisor earns just the profit margin, which may be no more than 20 to 30 cents on the dollar beyond that point.

This is even more common for firms reinvesting heavily to produce growth, such that they can’t even enjoy 20% to 30% profit margins because of all the additional capacity hiring they must do. (On the other hand, the growing availability of technology has made solo advisory firms more efficient and profitable than ever.)

Top-performing solo advisory firms can actually generate the same take-home pay as the average partner at a $1-billion-plus AUM super-ensem-ble advisory firm, according to industry studies. And some high-producing solo advisors can be even more profitable.

Of course, advisory firm founders who build larger ensembles do build the value of their equity, in addition to the income stream. Yet owing to the necessary burden of reinvestment of profits to fuel that growth, owners of growing ensemble firms typically take home even less in income for years or decades — such that the value of the equity may not materially enrich the founder. It instead merely makes up for

A small giant is preferable for those who want a good income but also hope their business delivers a better solution.

COMMUNITYSmall giants understand the value ofestablishing deep roots in theircommunity.

CULTURESmall giants foster a culture of intimacyby putting employees first, caring for them in the totality of their lives.

PURPOSESmall giants have a vision, a powerfulmission statement and core valuesthat can be brought to life.

CUSTOMERSSmall giants cultivate meaningfulrelationships with customers,suppliers and all stakeholders.

LEADERSHIPSmall giants are made up of servantleaders who believe in leading byvalues.

FINANCESmall giants believe in protecting theirgross margins without compromisingcompany values.

6 key traits of a small giant business

Source: www.smallgiants.org

023_FP0220 23 1/17/2020 9:51:15 AM

24 Financial Planning February 2020

the foregone profits along the way, except for perhaps a small subset of the very largest enterprise advisory firms.

Given that the challenges facing small giant practices and enterprise advisory firms can be remarkably similar, what’s the best path for the owner of an advisory firm to take at the capacity crossroads?

A lifestyle firm becomes preferred for those who work to live, rather than live to work. This includes advisors who not only want to balance the demands of the business against their nonbusiness goals and desires, but also specifically want to remain primarily client-facing and to avoid the burdens of managing a substantial number of people.

Lifestyle firms are simply those in which advisors are first and foremost paid for the advisory work they do. Notably, lifestyle firms are rarely sold. Instead the most profitable path for them is simply to remain in the business and realize an income as long as they can, which is more remunerative than selling the firm anyhow.

A small giant is preferable for those who don’t only want to make a good

income, but feel a fundamental drive to have their business deliver a better solution. These individuals recognize that such a path will inevitably mean the advisory business must grow beyond its founder, and the founder will ultimately wear the hats of advisor and firm owner managing a growing team.

Small giants tend to pursue internal succession plans and/or heavily utilize employee stock ownership plans, recognizing that when a unique purpose-driven business is built, it’s extremely difficult to find external buyers who will honor the business’ original vision and purpose. Internally developed talent, steeped in the culture of the firm and able to carry the legacy and vision of the business forward, is infinitely preferable.

An enterprise, meanwhile, is the preference for those who feel driven to transform from an advisor to an advisory firm business owner.

For enterprise builders, it’s likely that the founder will eventually move away from client relationships alto-gether. Instead, they immerse them-selves in the growth and development of their people and culture, and they build and maximize the shareholder value of the business by whatever path it takes.

This may take the form of organic or inorganic growth — self-funded or strategically taking outside investor capital. Often, there is an eventual goal of a liquidity event that may take the form of a sale to a larger firm, an acquisition by a strategic partner or private equity firm, or an IPO in the public markets. The key point is simply to recognize that the decision to keep growing past the capacity crossroads doesn’t have to be an all-in or all-out.

There is a middle ground: the small giant, the purpose-driven business that may grow along the way, but isn’t necessarily motivated by pure profit as much as a desire to blend financial and nonfinancial goals in delivering the business’ purpose-driven value.

The unhappiest advisory firm owners tend to be accidental business owners who find themselves develop-ing their business down an undesired path. They may make more money, but they become far less happy as they’re forced to take on roles to support a business they never envisioned.

By setting a vision that aligns to your goals and values, arriving at the capacity crossroads becomes not a moment to fear, but rather just a stop on your journey toward becoming something greater. FP

An enterprise is the preference for those who truly feel driven and motivated to transform from an advisor to an advisory firm owner.

Michael Kitces, CFP, a Financial Planning contributing writer, is a partner and director of wealth management at Pinnacle Advisory Group in Columbia, Maryland; co-founder of the XY Planning Network and AdvicePay; and publisher of the planning blog Nerd’s Eye View. Follow him onTwitter at @MichaelKitces.

$1,400,000

$1,000,000

$1,200,000

$800,000

$600,000

$400,000

$200,000

$0

Enterprises

Scal

e

Gro

w

Capacitycrossroads

Ref

ine

Laun

ch

Small giants

Lifestyle

Ann

ual r

even

ue

Years in business

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15

Possible pathways to take

Source: Michael Kitces

024_FP0220 24 1/17/2020 9:51:16 AM

Start here and sign up for free. www.financial-planning.com 212-803-8500

Ideas that advance your thinking and your career. Financial Planning delivers the essential analysis and insight that independent advisors need to make informed decisions about their businesses and the clients they serve.

001_FP0004 1 1/17/20 10:53 AM025_FP0220 25 1/17/2020 2:23:28 PM

Financial-Planning.com26 Financial Planning February 2020

IAN

TU

TTLE

IAN

TU

TTLE

ALSO IN IN|VEST: WEALTHFRONT’S BANKING ROADMAP P. 26 | SHOULD FIRMS END FORCED ARBITRATION FOR SEXUAL HARASSMENT CLAIMS? P. 27

Schwab’s planned $26 billion takeover of TD Ameritrade may be a boon for a surprising type of financial services firm — a challenger custodian that is also a robo advisor.

That’s the claim of Betterment CEO Jon Stein, who took aim at some of his favorite targets — including Charles Schwab, big banks and his independent robo nemesis Wealthfront’s Andy Rachleff — as a speaker at Financial Planning’s In|Vest West conference in December in San Francisco.

In the face of Schwab’s pending acquisition, Stein said his firm had been

presented with a major opportunity to recruit former TD Ameritrade advisors who aren’t happy switching to Schwab and are looking for other options.

While small advisory firms are Betterment’s primary target market, firms with significantly more assets were also approaching the robo advisor for custodial services. “The bigger firms want to talk,” Stein said. “We’re introducing models that we will be rolling out for them.”

Stein also took aim at banks, whose products, he claimed, “hurt America.”

Betterment, the leading independent

‘A ton of inbound calls’ for Betterment

By Charles Paikert

Schwab-TD Ameritrade deal triggers advisor interest.

robo advisor, which manages $20 billion in client assets, is “shifting resources hard” to the sector, Stein said, adding that banking represents one of the firm’s biggest opportunities.

Betterment recently introduced high-yield cash reserves, which attracted around $1 billion in deposits within a few weeks, according to Stein. The company also offers checking and savings products.

Nonetheless, the New York-based robo advisor’s banking efforts were still in the early days, he cautioned, adding that he couldn’t predict what that business would look like in five years.

Talking to millennialsAnd Stein couldn’t resist taking a shot at Rachleff, who raised eyebrows at an In|Vest West keynote session when he said his millennial customers came to Wealthfront so they wouldn’t have to talk to people.

The difference between Betterment and other robo advisors, Stein said, is that “we believe humans will always be part of financial services. Most of us still like talking to people. We’re not going to use technology to replace us.”

Betterment is also keeping a close eye on subscription pricing, Stein said. “The need to do [subscription pricing] to replicate services like Netflix is over-rated,” he said. “That’s not why we should do it. But doing it to be aligned with the customer is useful.”

Betterment, which is looking to go public “in the next few years,” will also continue building out its 401(k) and B2B Betterment for Advisors businesses, Stein said. “Our growth plan is to push as much value as we can into our products,” he said. FP

In a dig at Wealthfront, Jon Stein declared, “We believe humans will always be part of financial services.”

Tobias Salinger is a senior editor of Financial Planning. Follow him on Twitter at @TobySalFP.

Wealthfront takes on banks The digital firm has ambitious plans to outmaneuver the big brick-and-mortars.

By Tobias Salinger

As fintechs advance aggressively upon traditional banking services, Wealth-front CEO Andy Rachleff has a quick answer when asked what his digital investing firm can do that traditional banks can’t.

“First and foremost, we can be fairer to our customers,” Rachleff said during an interview at Financial Planning’s In|Vest West conference. “Everyone hates their cable guy and everyone hates their banks.”

‘Self-driving money’Only a few days after the Palo Alto, California-based firm’s December announcement that it would expand from robo advice, its core service, into mortgages, Rachleff laid out an ambitious roadmap he described as “self-driving money.”

By the end of March, Wealthfront

Charles Paikert is a senior editor of Financial Planning. Follow him on Twitter at @paikert.

Wealthfront CEO Andy Rachleff tells American Banker Editor at Large Penny Crosman the firm will use machine learning to figure out what clients spend.

026_FP0220 26 1/17/2020 2:37:11 PM

February 2020 Financial Planning 27Financial-Planning.com

IAN

TU

TTLE

ALSO IN IN|VEST: WEALTHFRONT’S BANKING ROADMAP P. 26 | SHOULD FIRMS END FORCED ARBITRATION FOR SEXUAL HARASSMENT CLAIMS? P. 27

robo advisor, which manages $20 billion in client assets, is “shifting resources hard” to the sector, Stein said, adding that banking represents one of the firm’s biggest opportunities.

Betterment recently introduced high-yield cash reserves, which attracted around $1 billion in deposits within a few weeks, according to Stein. The company also offers checking and savings products.

Nonetheless, the New York-based robo advisor’s banking efforts were still in the early days, he cautioned, adding that he couldn’t predict what that business would look like in five years.

Talking to millennialsAnd Stein couldn’t resist taking a shot at Rachleff, who raised eyebrows at an In|Vest West keynote session when he said his millennial customers came to Wealthfront so they wouldn’t have to talk to people.

The difference between Betterment and other robo advisors, Stein said, is that “we believe humans will always be part of financial services. Most of us still like talking to people. We’re not going to use technology to replace us.”

Betterment is also keeping a close eye on subscription pricing, Stein said. “The need to do [subscription pricing] to replicate services like Netflix is over-rated,” he said. “That’s not why we should do it. But doing it to be aligned with the customer is useful.”

Betterment, which is looking to go public “in the next few years,” will also continue building out its 401(k) and B2B Betterment for Advisors businesses, Stein said. “Our growth plan is to push as much value as we can into our products,” he said. FP

Tobias Salinger is a senior editor of Financial Planning. Follow him on Twitter at @TobySalFP.

Wealthfront takes on banks The digital firm has ambitious plans to outmaneuver the big brick-and-mortars.

By Tobias Salinger

As fintechs advance aggressively upon traditional banking services, Wealth-front CEO Andy Rachleff has a quick answer when asked what his digital investing firm can do that traditional banks can’t.

“First and foremost, we can be fairer to our customers,” Rachleff said during an interview at Financial Planning’s In|Vest West conference. “Everyone hates their cable guy and everyone hates their banks.”

‘Self-driving money’Only a few days after the Palo Alto, California-based firm’s December announcement that it would expand from robo advice, its core service, into mortgages, Rachleff laid out an ambitious roadmap he described as “self-driving money.”

By the end of March, Wealthfront

aims to have launched a debit card, automated bill pay and direct deposit. Later in the year, the company antici-pates being able to offer other auto-mated features such as rerouting of leftover money into clients’ investment portfolios.

Figuring out what clients spend and save every month requires machine deep learning, Rachleff said. “We use that to figure out what you spend. And then we use optimization techniques to make sure you have the right amount,” he said.