Embed Size (px)

Citation preview

InvestBulgaria Agencywww.investbg.government.bg

Business process outsourcing & system

support activities in Bulgaria:Opportunities for US companies, comparative analytical study

Draft for the Silicon Valley Conference

September 2004

InvestBulgaria Agencywww.investbg.government.bg

Summary

This presentation examines Bulgaria, Romania, Hungary, and Poland as alternative locations for software outsourcing, large scale support services operations and business process outsourcing

The analysis focuses on three key factor groups impacting performance:

Business environment stability and predictability

Productivity based on labor force cost and skill base

Infrastructure and partner support

The analysis uses latest data from the following official sources: Eurostat, IMF, World Bank, European Central Bank, EBRD, KPMG. Data used from individual government sources is indicated

The presentation also provides more specific info about Bulgaria and a review of the Bulgarian ICT sector

InvestBulgaria Agencywww.investbg.government.bg

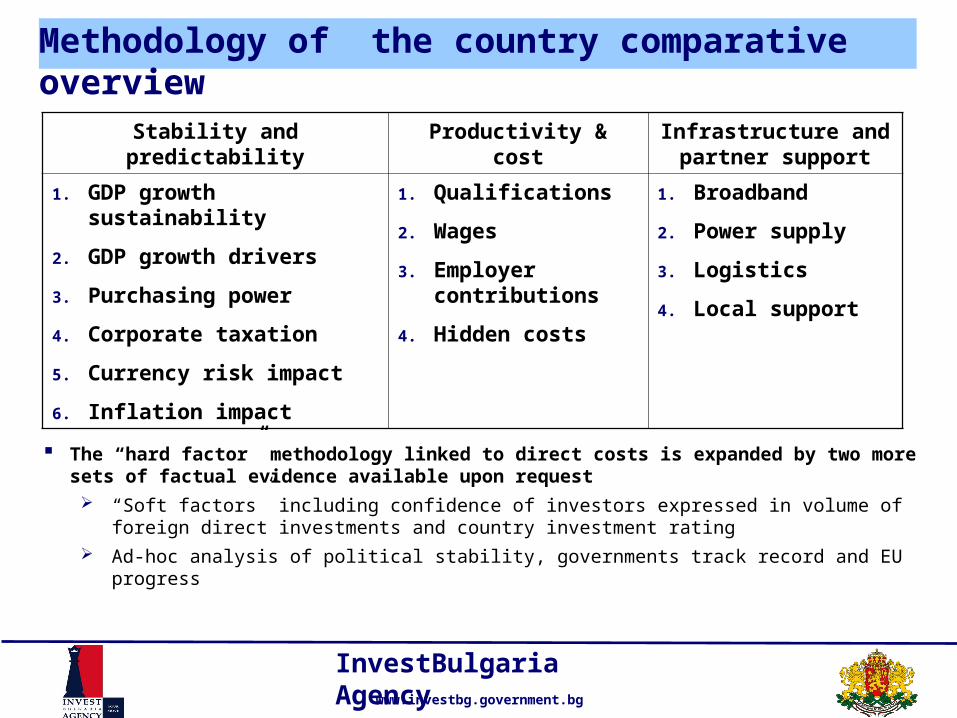

Methodology of the country comparative overview

Stability and predictability Productivity & cost Infrastructure and partner support

1. GDP growth sustainability

2. GDP growth drivers

3. Purchasing power

4. Corporate taxation

5. Currency risk impact

6. Inflation impact

1. Qualifications

2. Wages

3. Employer contributions

4. Hidden costs

1. Broadband

2. Power supply

3. Logistics

4. Local support

The “hard factor” methodology linked to direct costs is expanded by two more sets of factual evidence available upon request “Soft factors” including confidence of investors expressed in volume of foreign direct

investments and country investment rating Ad-hoc analysis of political stability, governments track record and EU progress

InvestBulgaria Agencywww.investbg.government.bg

1. GDP growth sustainability

Bulgaria

Romania

Poland

Hungary

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

1999 2000 2001 2002 2003 2004

Bulgaria leads in terms of average sustained GDP growth

Significance for a US investor's business: GDP growth is best indicator of near term visibility

4.2% 4.0% 3.8%

2.8%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Bulgaria Hungary Romania Poland

GDP growth 1999-2004E Average GDP growth 1999-2003

Source: EUROSTAT

InvestBulgaria Agencywww.investbg.government.bg

3. Purchasing power versus cost to employer

Bulgarian and Romanian population grew their purchasing power standards significantly more and faster than Poland over the past 5 years due to different economic models

At 2-3 times lower salary levels, Bulgarians and Romanians can now acquire more goods and services in their home economies than Polish

a US investor's employees in Bulgaria and Romania will continue to enjoy better life standards at lower nominal salaries over the medium run (5-10 years)

Growth of GDP per capita at purchasing power standards (1999 – 2004E)

Source: EUROSTAT

23.3%

21.1%

1.9%

15%

€535

€147

€177

€488

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Bulgaria Romania Poland Hungary

Gro

wth

of

GD

P/C

apita

0

100

200

300

400

500

600

Ave

rga

ge

mo

nth

ly s

ala

ry,

en

d o

f 20

03

*

* As of Oct for Hungary

InvestBulgaria Agencywww.investbg.government.bg

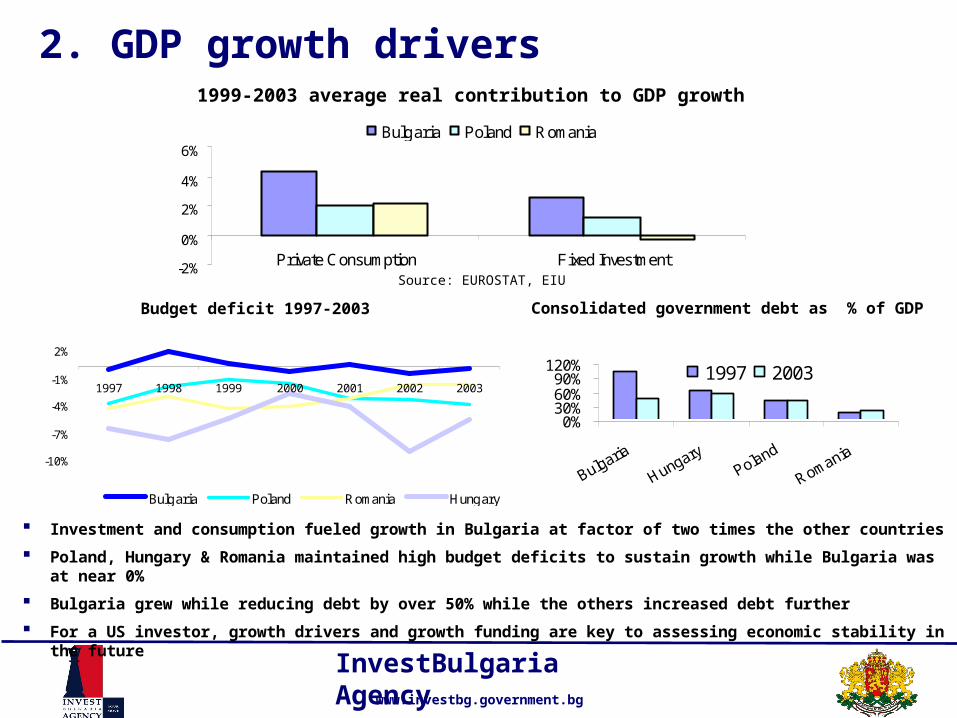

2. GDP growth drivers

-10%

-7%

-4%

-1%

2%

1997 1998 1999 2000 2001 2002 2003

Bulgaria Poland Romania Hungary

Investment and consumption fueled growth in Bulgaria at factor of two times the other countries

Poland, Hungary & Romania maintained high budget deficits to sustain growth while Bulgaria was at near 0%

Bulgaria grew while reducing debt by over 50% while the others increased debt further

For a US investor, growth drivers and growth funding are key to assessing economic stability in the future

Budget deficit 1997-2003 Consolidated government debt as % of GDP

1999-2003 average real contribution to GDP growth

-2%

0%

2%

4%

6%

Private Consumption Fixed Investment

Bulgaria Poland Romania

0%30%60%90%

120%

Bulgaria

HungaryPoland

Romania

1997 2003

Source: EUROSTAT, EIU

InvestBulgaria Agencywww.investbg.government.bg

4. Corporate taxation

Bulgaria has a lower corporate tax rate than Romania

Nominal tax levels are equally important with the government’s ability to keep stated tax policy

For a US investor, lower tax levels and tax policy predictability have direct impact on profitability

2004 and stated 2005 corporate tax rates

Source: KPMG, Government budgetary programs

16%

19.5%

25%

15% 15%

23%

19%

0%

5%

10%

15%

20%

25%

30%

Hungary Poland Bulgaria Romania

2004 2005 (gov. program)

InvestBulgaria Agencywww.investbg.government.bg

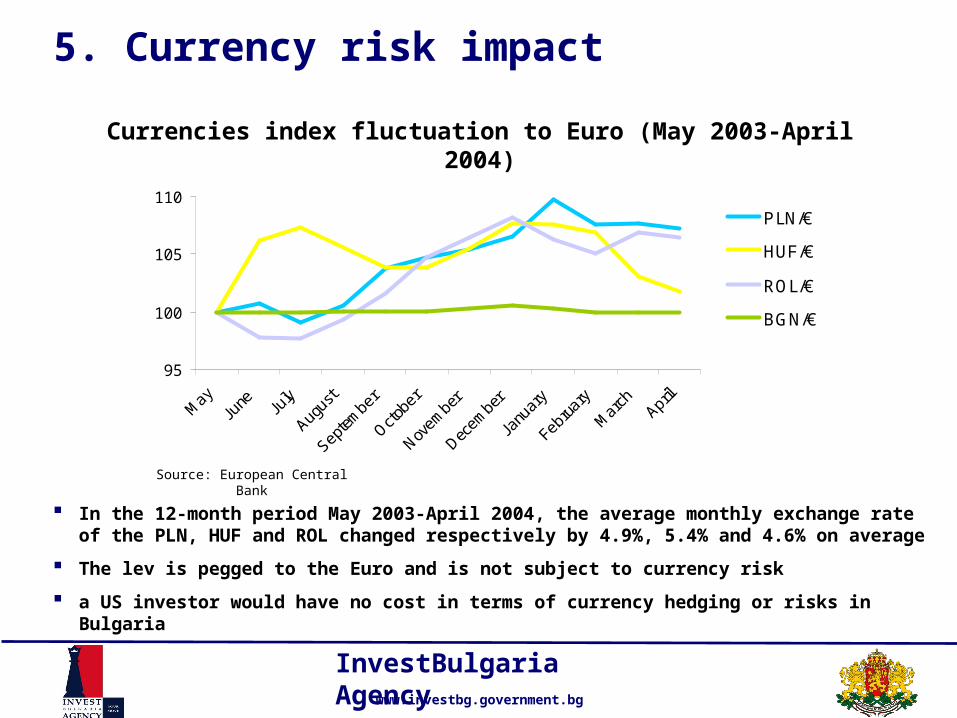

5. Currency risk impact

In the 12-month period May 2003-April 2004, the average monthly exchange rate of the PLN, HUF and ROL changed respectively by 4.9%, 5.4% and 4.6% on average

The lev is pegged to the Euro and is not subject to currency risk

a US investor would have no cost in terms of currency hedging or risks in Bulgaria

Currencies index fluctuation to Euro (May 2003-April 2004)

Source: European Central Bank

95

100

105

110

May

June Ju

ly

Augus

t

Septe

mber

Octob

er

Novem

ber

Decem

ber

Janu

ary

Febr

uary

Mar

chApr

il

PLN/€

HUF/€

ROL/€

BGN/€

InvestBulgaria Agencywww.investbg.government.bg

6. Inflation exposure

Inflation is significant source of risk exposure to real growth and profit expectations

Bulgarian, Polish and Hungarian economies have curbed inflation; inflation level remained high in Romania

a US investor would have significant exposure to lower stability and visibility in Romania

Inflation rates (2000 – 2003)

Source: Eurostat

0%

10%

20%

30%

40%

50%

Bulgaria Poland Hungary Romania

2000 2001 2002 2003

InvestBulgaria Agencywww.investbg.government.bg

7. Education

Levels of secondary and higher education in the three countries is comparable (no data for Romania)

Bulgaria has a larger proportion of students enrolled in the key 3 fields

4,641

3,5062,938 2,736

0

1,000

2,000

3,000

4,000

5,000

Poland Hungary Bulgaria Romania

Net enrollment rates

in secondary education

Source: Global Education Digest, European Center for Higher Education (UNESCO), Academic year 2002/2003

14 15

2022

0

5

10

15

20

25

Bulgaria Hungary Romania Poland

Number of higher education

students per 100,000 inhabitants

High education - students /

teaching staff ratio

42 19 2

52

53

56

37

36

32

36 7

13

7

1

3

0% 20% 40% 60% 80% 100%

OECD Average

Hungary

Poland

Bulgaria Social sciences, business & law

Engineering, manufacturing &construction Computing

Other subjects

92% 91%

86%

80%

70%

75%

80%

85%

90%

95%

Hungary Poland Bulgaria Romania

Source: Global Education Digest - UNESCO, National Statistics Institute (academic year 2001/2002)

Source: OECD statistics (academic year 2001/2002)

InvestBulgaria Agencywww.investbg.government.bg

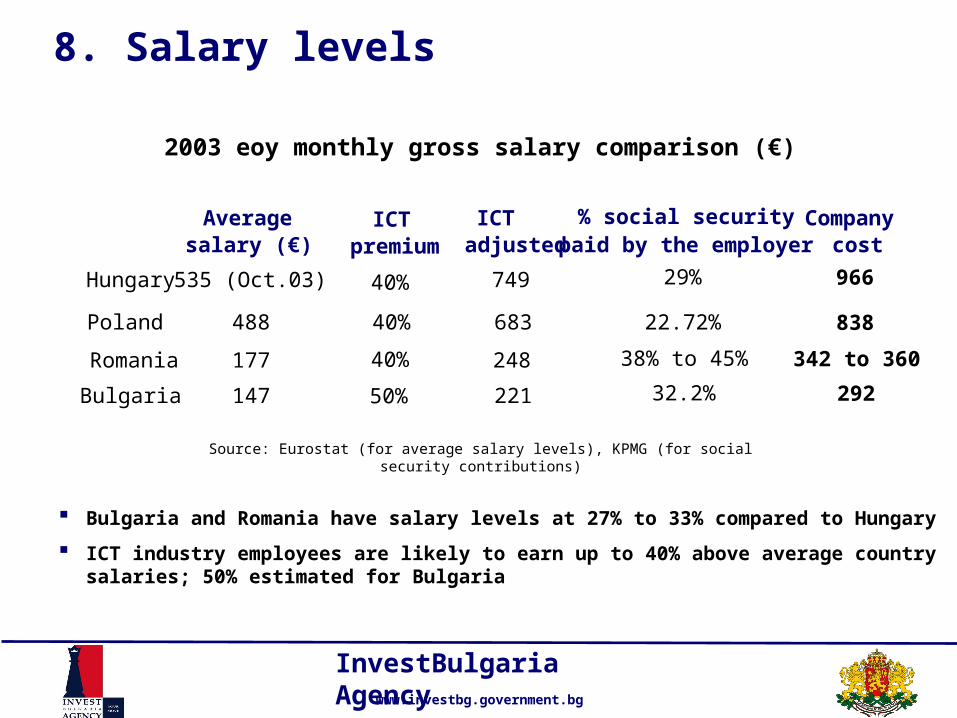

8. Salary levels

Bulgaria and Romania have salary levels at 27% to 33% compared to Hungary

ICT industry employees are likely to earn up to 40% above average country salaries; 50% estimated for Bulgaria

2003 eoy monthly gross salary comparison (€)

Source: Eurostat (for average salary levels), KPMG (for social security contributions)

683

248

221

Average ICT ICT salary (€) premium adjusted

Poland 488 40%

Romania 177

Bulgaria 147

Hungary 535 (Oct.03) 749

32.2%

% social securitypaid by the employer

29%

Company cost

22.72%

38% to 45%

292

966

838

342 to 360

40%

40%

50%

InvestBulgaria Agencywww.investbg.government.bg

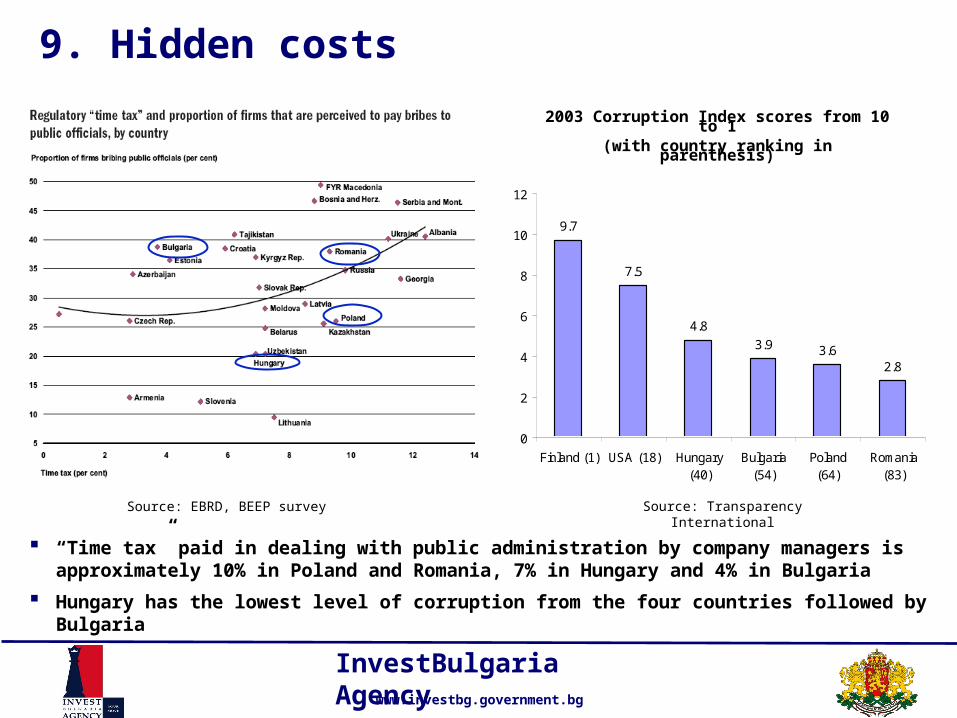

9. Hidden costs

“Time tax” paid in dealing with public administration by company managers is approximately 10% in Poland and Romania, 7% in Hungary and 4% in Bulgaria

Hungary has the lowest level of corruption from the four countries followed by Bulgaria

Source: EBRD, BEEP survey

9.7

7.5

4.8

3.9 3.62.8

0

2

4

6

8

10

12

Finland (1) USA (18) Hungary(40)

Bulgaria(54)

Poland(64)

Romania(83)

2003 Corruption Index scores from 10 to 1(with country ranking in parenthesis)

Source: Transparency International

InvestBulgaria Agencywww.investbg.government.bg

10. Infrastructure

Budapest, Warsaw and Sofia are classified in the upper access group; Bucharest is in the medium class group

No major power outages occurred in the four cities in 2003

Key infrastructure parameters

*Source: ITU survey December 2003

ITU Digital Access Index 2002*

Power outages 2003

Flight time to Munich

Budapest 0.63 No 1.15 h

Warsaw 0.59 No 1.35 h

Sofia 0.53 No 2.0 h

Bucharest 0.48 No 1.54 h

InvestBulgaria Agencywww.investbg.government.bg

11. Local support

IBA is presently assisting foreign investors involved in expansions including over 2,000 technology and support jobs

Site development support, staff recruitment and training are included in the assistance programs of the Bulgarian Government as part of its ICT priority strategy

Support to ICT companies in Bulgaria by IBA in 2004

Investor (country)

Status pre IBA support Project Current status

American Standard (USA)

Manufacturing site with 4,000 employees

Expansion of European IT support

25 jobs to be created in June

Business Park Sofia (Germany) – City Call (Belgium)

400-500 seats contact center

Expansion to 2,000 seats

Office construction in progress

SAP Labs (Germany)

180 software development team

Developer and tester recruitment

Recruitment in progress

TaxBack (Ireland)

Service hub supporting 18 offices worldwide

Expansion of office space and people

Negotiations with schools

InvestBulgaria Agencywww.investbg.government.bg

IBA’s project pipeline in ICT services

Company description Timing of inquiry Project description Technology/Service

Global mobile communications leader

Apr-04 R&D Telecom networking

Global networking leader Mar-04 National research network Broadband

Top 3 global IT solutions provider

Oct-03 Software development Systems Integration

Top 3 EU mobile network solutions provider

Apr-04 Offshore demand center Systems services

Top 3 EU electrical engineering and electronics solutions provider

Nov-04 Software development Medical

Ongoing discussion on potential projects in Bulgaria

Strictly confidential

InvestBulgaria Agencywww.investbg.government.bg

Bulgaria: country specific information

Foreign direct investment development

Technical and language education

Operational cost

InvestBulgaria Agencywww.investbg.government.bg

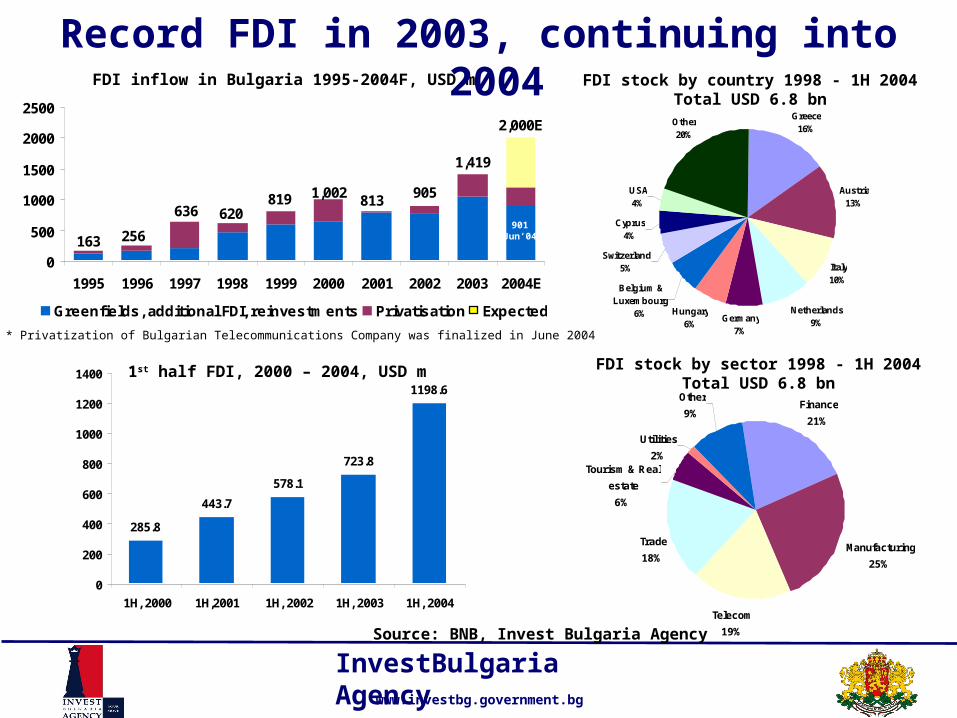

163 256

636 620819 8131,002 905

1,419

2,000E

0

500

1000

1500

2000

2500

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004E

Greenfields, additional FDI, reinvestments Privatisation Expected

FDI inflow in Bulgaria 1995-2004F, USD m

Record FDI in 2003, continuing into 2004FDI stock by country 1998 - 1H 2004

Total USD 6.8 bn

FDI stock by sector 1998 - 1H 2004Total USD 6.8 bn

Source: BNB, Invest Bulgaria Agency

1st half FDI, 2000 – 2004, USD m

285.8

443.7

578.1

723.8

1198.6

0

200

400

600

800

1000

1200

1400

1H, 2000 1H,2001 1H, 2002 1H, 2003 1H, 2004

Greece16%

Austria13%

Italy10%

Netherlands9%Germany

7%

Belgium & Luxembourg

6%

Switzerland5%

Cyprus4%

USA4%

Other20%

Hungary6%

Finance

21%

Manufacturing

25%

Telecom

19%

Utilities

2%

Other

9%

Trade

18%

Tourism & Real

estate

6%

901Jun‘04

* Privatization of Bulgarian Telecommunications Company was finalized in June 2004

InvestBulgaria Agencywww.investbg.government.bg

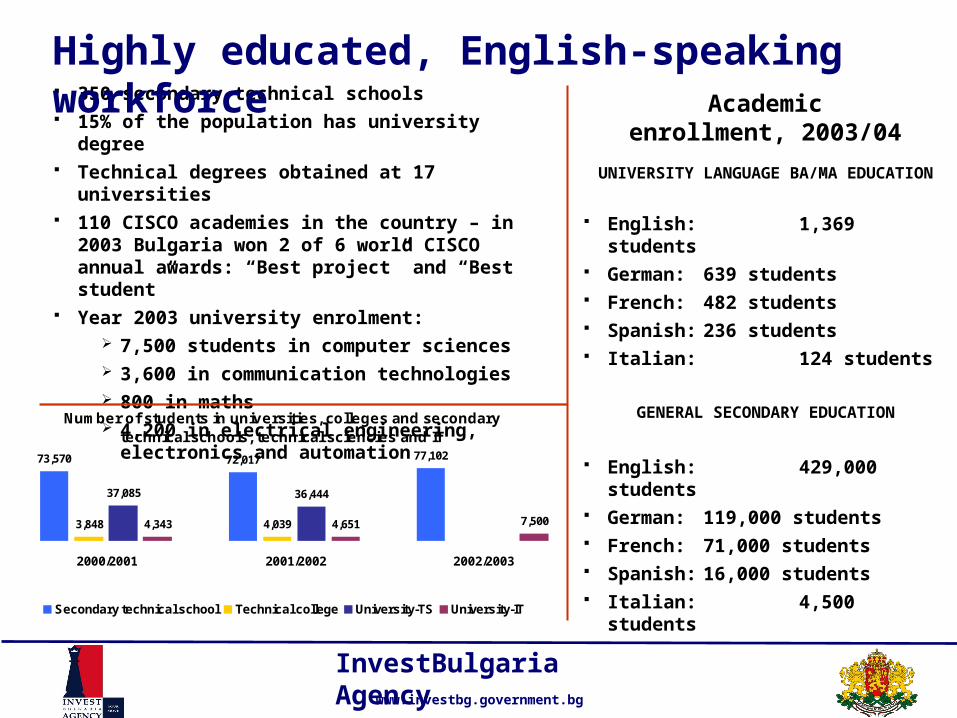

Number of students in universities, colleges and secondary technical schools, technical sciencies and IT

73,570 72,017 77,102

3,848 4,039

37,085 36,444

4,343 4,651 7,500

2000/2001 2001/2002 2002/2003

Secondary technical school Technical college University-TS University-IT

350 secondary technical schools 15% of the population has university degree Technical degrees obtained at 17 universities 110 CISCO academies in the country – in 2003

Bulgaria won 2 of 6 world CISCO annual awards: “Best project” and “Best student”

Year 2003 university enrolment: 7,500 students in computer sciences 3,600 in communication technologies 800 in maths 4,200 in electrical engineering, electronics and

automation

Highly educated, English-speaking workforce

UNIVERSITY LANGUAGE BA/MA EDUCATION

English: 1,369 students German: 639 students French: 482 students Spanish: 236 students Italian: 124 students

GENERAL SECONDARY EDUCATION

English: 429,000 students German: 119,000 students French: 71,000 students Spanish: 16,000 students Italian: 4,500 students

Academic enrollment, 2003/04

InvestBulgaria Agencywww.investbg.government.bg

Bulgaria - most competitive cost base in Europe

Property

cost

/per sq. m/

Tax

Office rent, class A, Sofia

Office purchase price, Sofia centre

Industrial property rent prices, large cities

Industrial construction works cost

Office building

€ 9 to 17

€ 700 to 1,400

€ 3 to 5

€ 250-300

€ 350-500

Corporate tax rate 19.5% (15% in 2005) 0% in areas of high unemployment for manufacturing activities

VAT exemption for equipment imports for investments over € 5 million

Personal income tax 29% highest bracket (monthly income over € 300)

0% capital gains tax

InvestBulgaria Agencywww.investbg.government.bg

Bulgaria: competitive ICT industry

Stable legal framework

Rapidly developing infrastructure

High value added software industry

Contact centers booming

InvestBulgaria Agencywww.investbg.government.bg

ICT industry: Legal and regulatory framework

IPR protection in place

Law on copyright and related rights (1993- last amnd. 2003)

Patent Act (amnd. 2003)

A new law on telecommunications provides for the full liberalization of the telecom market by 2005

Law on Electronic Document and Electronic Signature (2001-2002) – secure conduct of e-commerce

Law on the Protection of Personal Data (2002) – human rights protection in line with the EU norms

Classified Information Safeguarding Act (2002-2003)

Convention on Cyber Crime of the Council of Europe ratified

InvestBulgaria Agencywww.investbg.government.bg

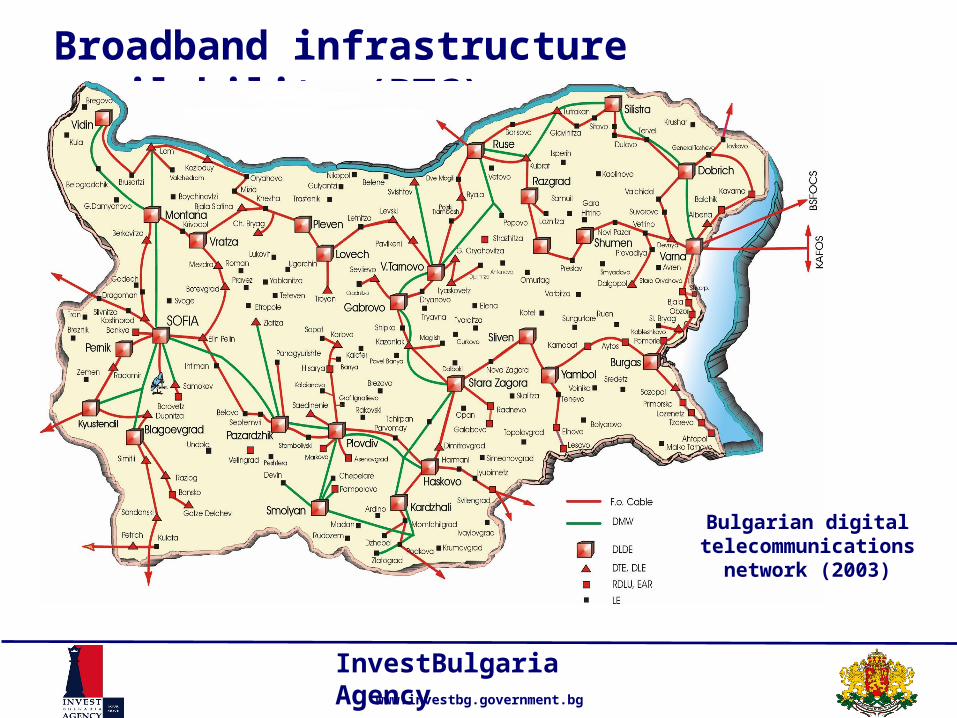

Broadband infrastructure availability (BTC)

Bulgarian digital telecommunications

network (2003)

InvestBulgaria Agencywww.investbg.government.bg

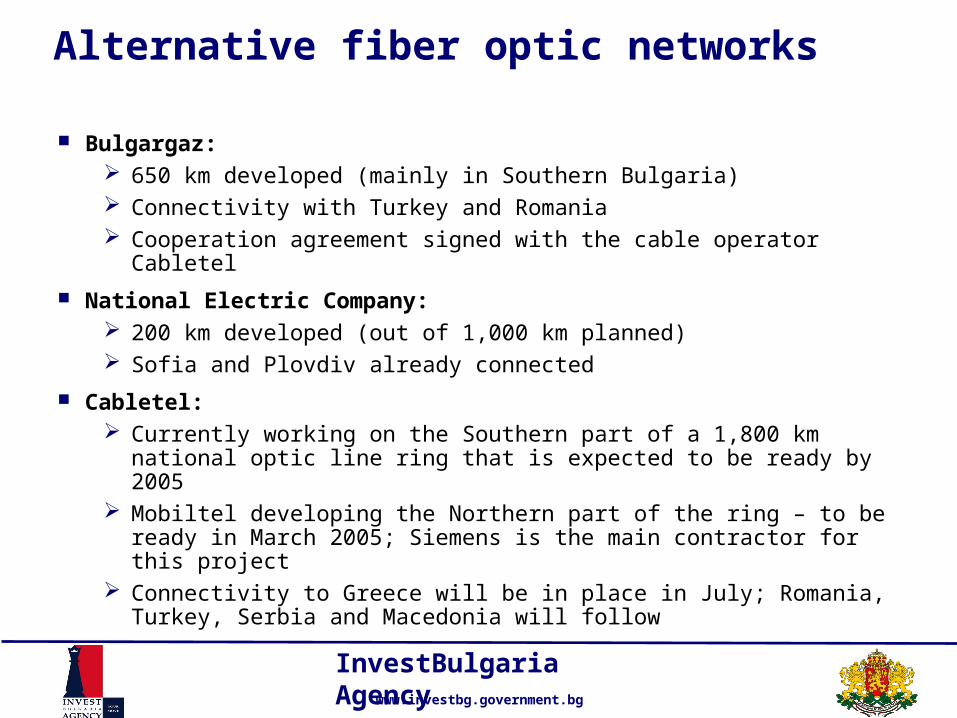

Bulgargaz: 650 km developed (mainly in Southern Bulgaria) Connectivity with Turkey and Romania Cooperation agreement signed with the cable operator Cabletel

National Electric Company: 200 km developed (out of 1,000 km planned) Sofia and Plovdiv already connected

Cabletel: Currently working on the Southern part of a 1,800 km national optic line

ring that is expected to be ready by 2005 Mobiltel developing the Northern part of the ring – to be ready in March

2005; Siemens is the main contractor for this project Connectivity to Greece will be in place in July; Romania, Turkey, Serbia

and Macedonia will follow

Alternative fiber optic networks

InvestBulgaria Agencywww.investbg.government.bg

Source: Bulgarian Telecommunications Company

Fixed lines cover 85% of the households; 80% digitalization by 2008Full telecom liberalization by Jan 2005Telecom privatization complete in 2004; investor committed a full network upgrade

€ 1.2 billion buoyant telecom market

DIGITALIZATION ('000 of lines)

779

2,575 2,536 2,4802,333

2,078

346 433573

258

0

500

1,000

1,500

2,000

2,500

3,000

1999 2000 2001 2002 2003

Digital lines Analogue lines

OPTICAL TRANSMISSION NETWORK (km)

3,000

2,617

2,1882,114

1,8401,799

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1997 1998 1999 2000 2002 2003 E

InvestBulgaria Agencywww.investbg.government.bg

• Bulgaria is the leader in the field of outsourcing among the countries in East Europe ← Latest research of CIO and Meta Group

• Bulgarian software companies develop the expert specification together with the client, provide smart solutions and meet the deadlines within the initial budget

• Bulgarian software developers have a wide expertise in:

• Key markets of the Bulgarian software industry – the US, Canada, Germany, France, UK, the Netherlands, Austria, Italy, Japan, China

• ESI Centre in Bulgaria since 2003

Bulgarian software industry review

Sophisticated information systems Industry knowledge and solutionsNetwork security services & solutionsE-business and wireless applicationsGeographic Information SystemsRapid Prototyping Systems

Gaming solutionsWeb designComplex B2B solutionsEmbedded softwareCAD/CAMMultimedia

InvestBulgaria Agencywww.investbg.government.bg

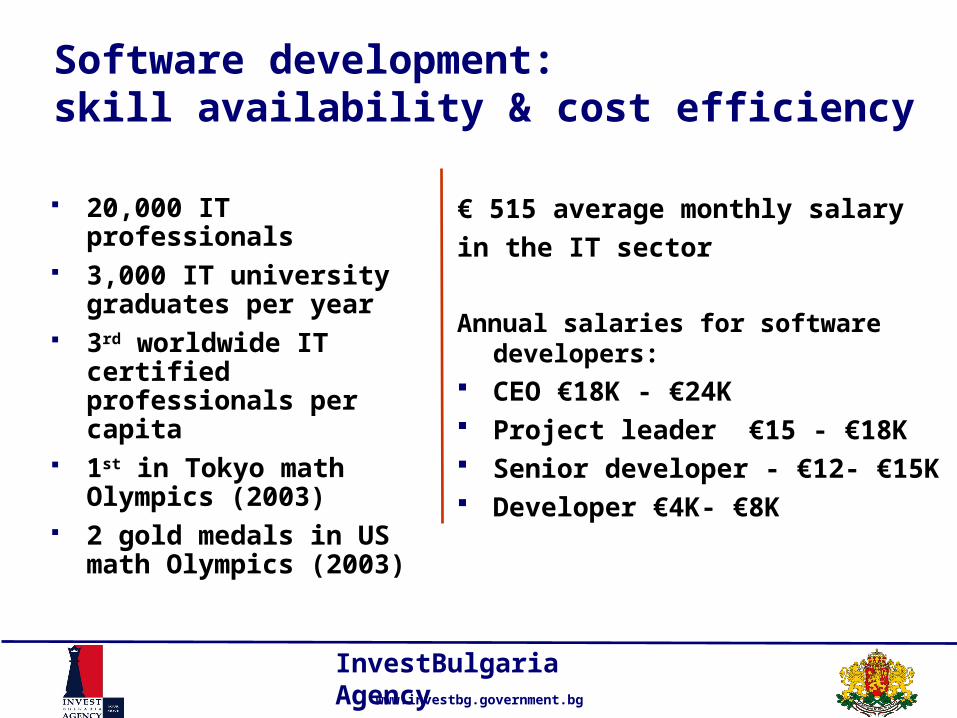

20,000 IT professionals 3,000 IT university

graduates per year 3rd worldwide IT certified

professionals per capita 1st in Tokyo math Olympics

(2003) 2 gold medals in US math

Olympics (2003)

Software development:skill availability & cost efficiency

€ 515 average monthly salary

in the IT sector

Annual salaries for software developers: CEO €18K - €24K Project leader €15 - €18K Senior developer - €12- €15K Developer €4K- €8K

InvestBulgaria Agencywww.investbg.government.bg

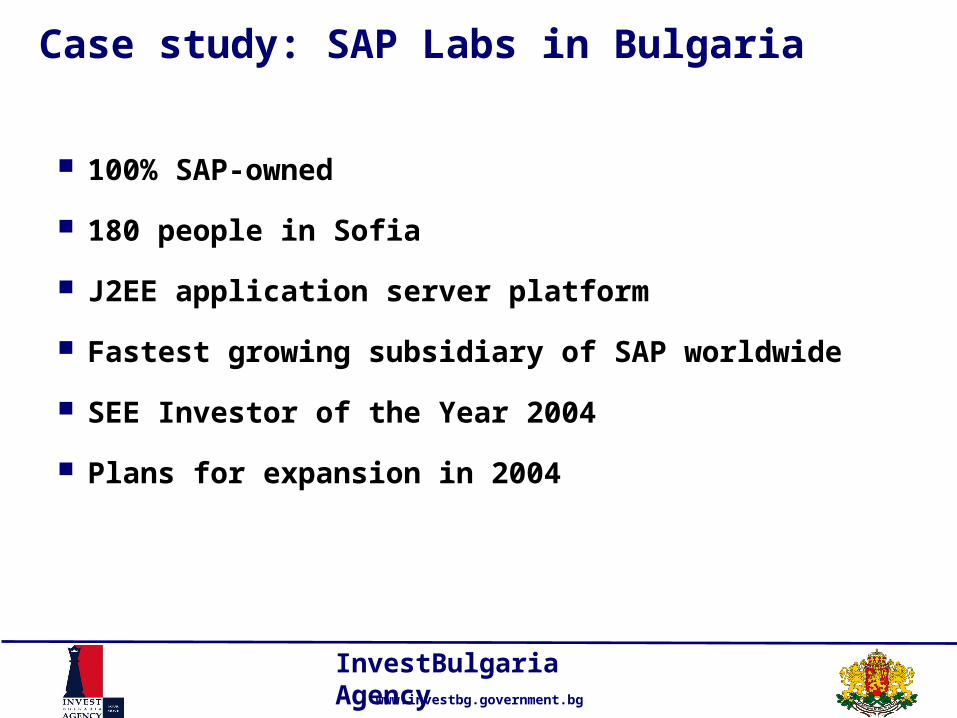

Case study: SAP Labs in Bulgaria

100% SAP-owned

180 people in Sofia

J2EE application server platform

Fastest growing subsidiary of SAP worldwide

SEE Investor of the Year 2004

Plans for expansion in 2004

InvestBulgaria Agencywww.investbg.government.bg

Case study: Tumbleweed – US leading provider of secure Internet messaging software in Bulgaria

Tumbleweed Communications Bulgaria:

Since 2002: leading provider of enterprise solutions in the areas of anti-spam, anti-virus, e-mail filtering, and e-mail encryption

more than 600 enterprise customers

Currently employs approximately 60 people

After selling operations in Bangalore, India announced expansion of existing business operations in Sofia, Bulgaria by 50% by the end of 2004

Will employ 90 people by the end of 2004

““Over the past several years, we have proven that Bulgaria is a competitive, productive place to do Over the past several years, we have proven that Bulgaria is a competitive, productive place to do business with a lot of talented and well-trained people. As we look to expand here in Sofia, we plan to business with a lot of talented and well-trained people. As we look to expand here in Sofia, we plan to

continue hiring the best and the brightest people that Bulgaria has to offer.” continue hiring the best and the brightest people that Bulgaria has to offer.”

Eric Dumas, Director of Tumbleweed Communications Bulgaria Eric Dumas, Director of Tumbleweed Communications Bulgaria

InvestBulgaria Agencywww.investbg.government.bg

Bulgaria: a highly competitive locationfor contact center business

11 contact centers in Bulgaria – mainly marketing and technical support

Main foreign companies having a contact center in Bulgaria: American Standard, Hewlett Packard, City Call - Belgium, Tax Back - Ireland

Countries serviced from Bulgaria - USA, Canada, Australia, New Zealand, Japan, Ireland, UK, the Netherlands, Belgium, Germany, Italy

Languages to be actively supported from Bulgaria – English, German, French, Spanish, Italian, Russian

Average company cost: EUR 300-470 for contact agents EUR 550-650 for supervisors

InvestBulgaria Agencywww.investbg.government.bg

Case study: City Call, Belgium → IMRO, Bulgaria

Initial investment of € 500,000

– Survey made Sep - Nov 2002

– Bulgarian company set in Dec 2002

– Operation stared in April 2003

– 300 phone operators employed June 2003 Office in Business Park Sofia; 2 MB line provided by BTC Net Contact center activities – marketing + help desk Languages used: French and Dutch - customers from Belgium & France

are served Salary ratio 6:1 compared to company similar facility in Belgium Established local partnerships with the French language programs of the

major Sofia universities and colleges € 5 million will be invested & 2,000 jobs will be created in 2004-2005

InvestBulgaria Agencywww.investbg.government.bg

Case study: Taxback - Irish tax refund service support center

Taxback: call and service center in Varna, Bulgaria2001: 150 employees

2003: 265 employees

24 Hour Tax Advice in 6 different languages

Bulgarian Taxback people developing/training new business operations of Taxback in Russia and Spain

Taxback globally:18 offices worldwide

Income tax refunds for all nationalities that have worked in the USA, Canada, the UK, Australia, New Zealand, Germany, Ireland, the Netherlands and Japan to customers all over the world

120,000 tax returns per annum

Skilled labor force (oriented towards excellence of service) was the key Skilled labor force (oriented towards excellence of service) was the key factor for Taxback to establish the Bulgarian office.factor for Taxback to establish the Bulgarian office.

InvestBulgaria Agencywww.investbg.government.bg

Why Bulgaria: conclusions

Best investment credibility in the region

Success story quotes

National commitment for encouraging foreign investment

InvestBulgaria Agencywww.investbg.government.bg

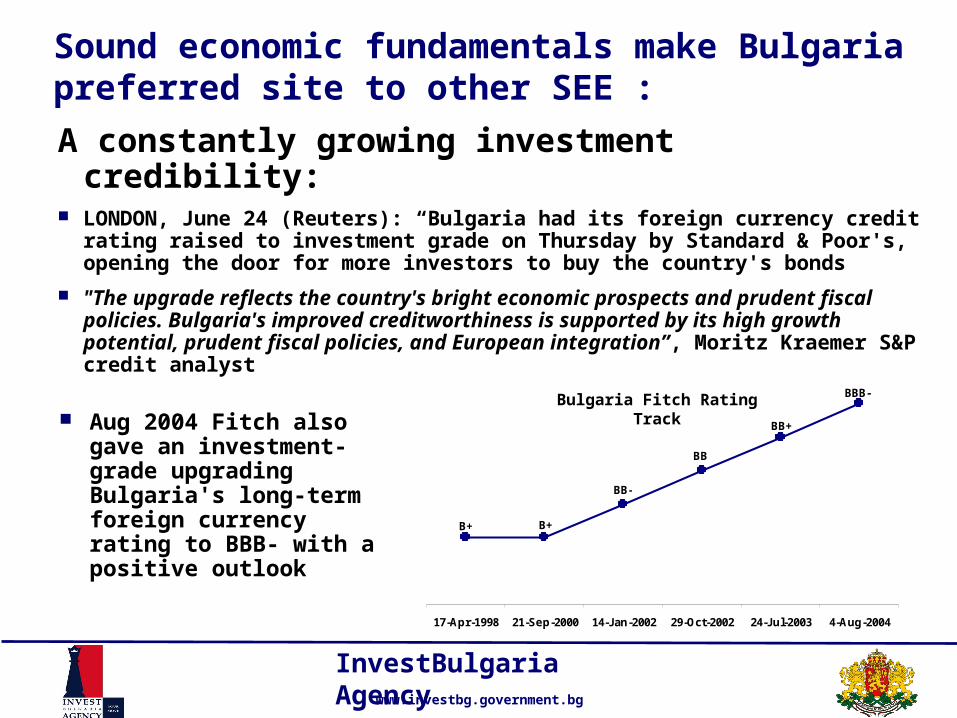

Sound economic fundamentals make Bulgaria preferred site to other SEE :

A constantly growing investment credibility: LONDON, June 24 (Reuters): “Bulgaria had its foreign currency credit

rating raised to investment grade on Thursday by Standard & Poor's, opening the door for more investors to buy the country's bonds

"The upgrade reflects the country's bright economic prospects and prudent fiscal policies. Bulgaria's improved creditworthiness is supported by its high growth potential, prudent fiscal policies, and European integration”, Moritz Kraemer S&P credit analyst

BBB-

BB+

BB

BB-

B+B+

17-Apr-1998 21-Sep-2000 14-Jan-2002 29-Oct-2002 24-Jul-2003 4-Aug-2004

Bulgaria Fitch Rating Track Aug 2004 Fitch also gave

an investment-grade upgrading Bulgaria's long-term foreign currency rating to BBB- with a positive outlook

InvestBulgaria Agencywww.investbg.government.bg

The testimonials: “Forget India – Let’s Go to Bulgaria”, Business Week, March 2004:

“It was access to nearby talent that convinced SAP to set up its Bulgarian outpost…” BW, March

“Scattered around the capital are hundreds of small software companies doing projects for an impressive list of the biggest customers in the world, including Boeing, BMW, General Motors, Siemens, Nortel…” BW, March

“Other giants, such as SAP and Computer Sciences, have local labs in Sofia…”

“There is an exceptionally high level of talent in Eastern Europe”, Kasper Rorsted, Managing Director for EMEA at Hewlett-Packard Co.

“The combination of existing and proven local expertise, the excellent academic facilities and the strength of the Bulgarian economy, made Sofia an ideal choice for further investment in our global mixed-signal engineering capabilities.” Nelly Pergoot, Managing Director, AMI Semiconductor Bulgaria

Bulgaria delivers cutting edge solutions in ICT from a proprietary platform

InvestBulgaria Agencywww.investbg.government.bg

Administrative business-friendly environment

Wide public support for the National strategy for encourage-ment of investment created by Ministry of Economy

Ministry of Economy responsible for investment policy making InvestBulgaria Agency, part of the Ministry of Economy, assists

investors set up business in Bulgaria through:

Informational services and individual administrative services

Consulting

Marketing research

Sector analyses

Business contacts

Linkages with the central and local government institutions facilitating investment projects implementation

Investment marketing

InvestBulgaria Agencywww.investbg.government.bg

New Law on investment promotion – Aug 2004 Equal treatment of Bulgarian and foreign investors Preferential treatment for manufacturing or service providing

investment projects, creating employment – implementation required within 3 years

3 classes investments according to project value: 1st class - over € 50 mln 2nd class – between € 25 - 50 mln 3rd class - between € 5 - 25 mln

All classes benefit from speeded-up administrative service as well as information service

Individual administrative services for 2nd and 1st class investors Infrastructure support to the borders of the investment project

site together with facilitated land acquisition for 1st class investors