Embed Size (px)

Citation preview

159 Madison Avenue, Suite 10i New York, NY 10016

Phone: 646.526.8403

www.sirelinecapital.com [email protected]

SIRE LINE CAPITAL MANAGEMENT

HOW TO TURN $10,000 INTO $10,000,000:

INVEST LIKE WARREN BUFFETT

Disclaimer

2 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Disclaimer: All information in this report is provided for informational purposes

only and should not be deemed as an offer to sell or the solicitation of an offer to

buy. References to specific securities and issuers are for illustrative purposes only

and are not intended to be, and should not be interpreted as, recommendations to

purchase or sell such securities. Past performance is no guarantee of future

results. The opinions expressed herein are those of Sire Line Capital and are

subject to change without notice. Entities including, but not limited to, Sire Line

Capital, directors and employees may have a position in the securities mentioned

above and/or related securities. This presentation is not intended for public use or

distribution. Reproduction without written permission is prohibited.

Sire Line Capital Management

3 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Who are we? A registered investment adviser based in New York We provide investment management services to all types of investors The foundation of our investment philosophy was inspired by Warren Buffett

Why are we giving this presentation? To remove the mystery of investing in the stock market To show you why some money managers outperform others over the long term To help you better protect and grow your hard-earned assets

Sire Line Capital Management

4 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

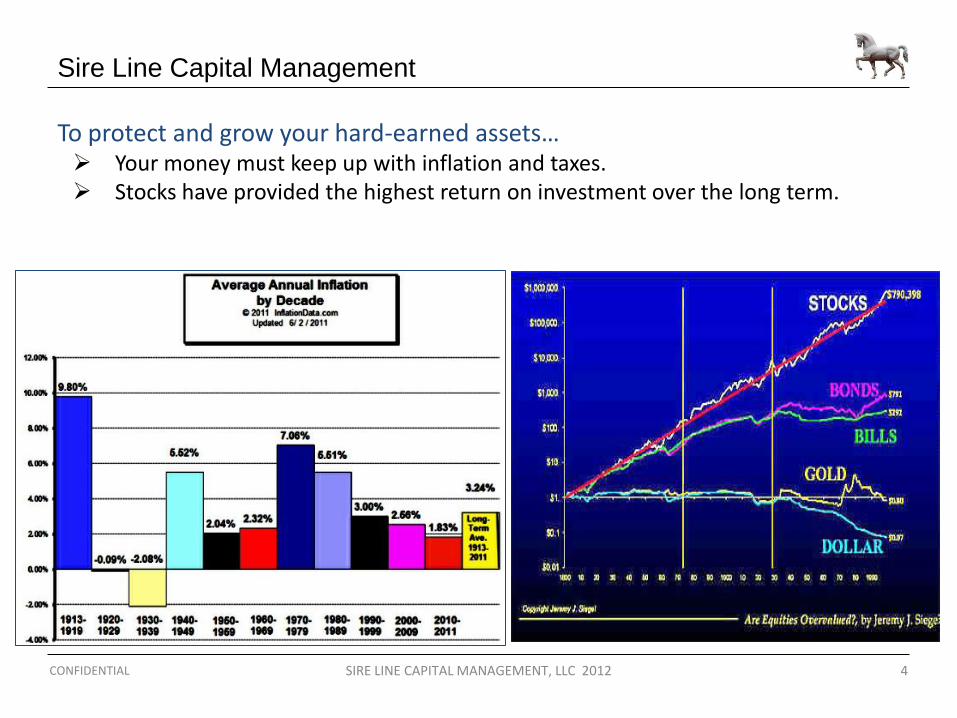

To protect and grow your hard-earned assets… Your money must keep up with inflation and taxes. Stocks have provided the highest return on investment over the long term.

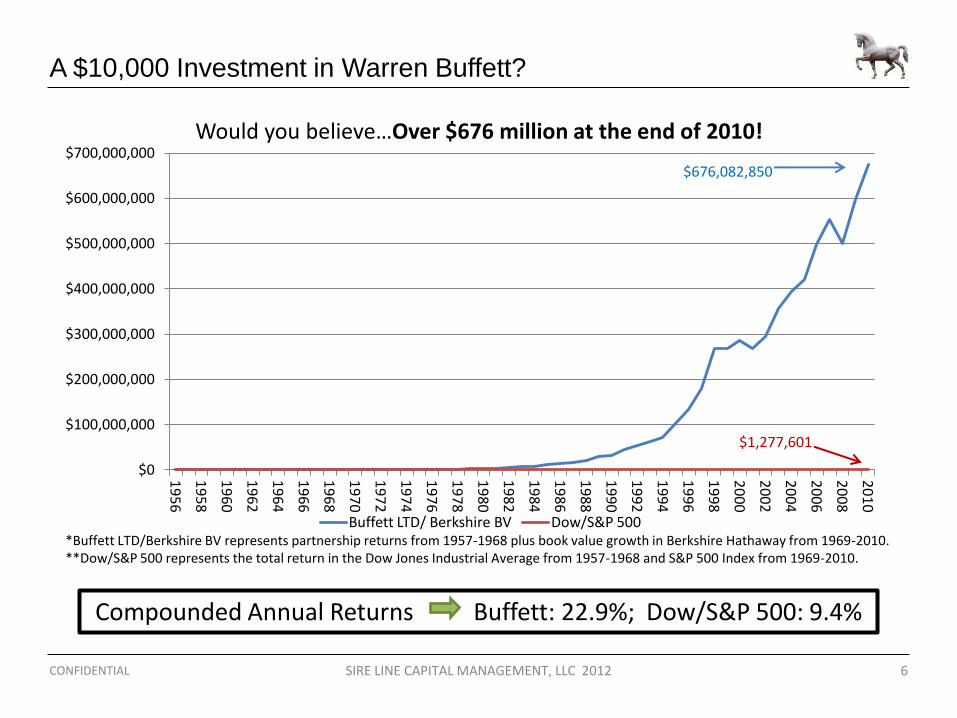

A $10,000 Investment in Warren Buffett?

5 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

*Question:

If you had invested $10,000 in the Buffett Partnership in 1956 and rolled it over into Berkshire Hathaway stock in 1969, how much would you have had at the end of 2010?

Warren Buffett: Professional Money Manager? 1956 ― 1969: Buffett Partnerships (an early hedge fund) 1965 ― Today: Chairman & CEO of Berkshire Hathaway

A $10,000 Investment in Warren Buffett?

6 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Would you believe…Over $676 million at the end of 2010!

Compounded Annual Returns Buffett: 22.9%; Dow/S&P 500: 9.4%

*Buffett LTD/Berkshire BV represents partnership returns from 1957-1968 plus book value growth in Berkshire Hathaway from 1969-2010. **Dow/S&P 500 represents the total return in the Dow Jones Industrial Average from 1957-1968 and S&P 500 Index from 1969-2010.

$676,082,850

$1,277,601

$0

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

Buffett LTD/ Berkshire BV Dow/S&P 500

A $10,000 Investment in Warren Buffett?

7 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

How did he do it? By…

investing in high-tech, high-growth stocks? No.

investing in newly created public companies? No.

day-trading? No.

trading on inside information? No.

predicting the future better than others? No.

Warren Buffett Tenets

8 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Only invest in high-quality businesses that:

1) Are simple to understand

2) Have favorable long-term economic characteristics

3) Are managed by honest and able managers

4) Can be purchased at a significant discount to intrinsic value

9 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Buffett’s Most Recent Investment:

An Example:

An Example:

10 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

I. Simple to understand?

They provide IT support services for corporations

Over 100 years old

Significant global presence, operating in more than 170 countries

Nearly 60% of its operating income is annuity-like/recurring.

5 operating segments:

Segments: Main Products/Services: % of Income Margins

Software Middleware and operating systems software 44% 35%

Global Technology Services IT outsourcing services 27% 15%

Global Business Services Analytics, Strategy, Consulting 13% 15%

Global Financing Client financing 9% 48%

Systems and Technology Enterprise server and storage systems 7% 8%

11 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

II. Consistent operating history/favorable long-term prospects? Buffett: “It is a big deal for a large company to change auditors, law firms or IT

support.”

Strengths in R&D: IBM has been awarded more U.S. patents every year than any other company for 18 consecutive years (5,896 in 2010 alone)

5 year CAGR: Sales/share = 8.4%, EPS = 16.6%

Free cash flow margins = 15%

5-yr avg. return on invested capital = 27%; ROE = 70%

An Example:

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Sales per share

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Diluted EPS

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

2001 2006 2011

ROIC ROIC-tangible ROE

Return on Capital

12 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

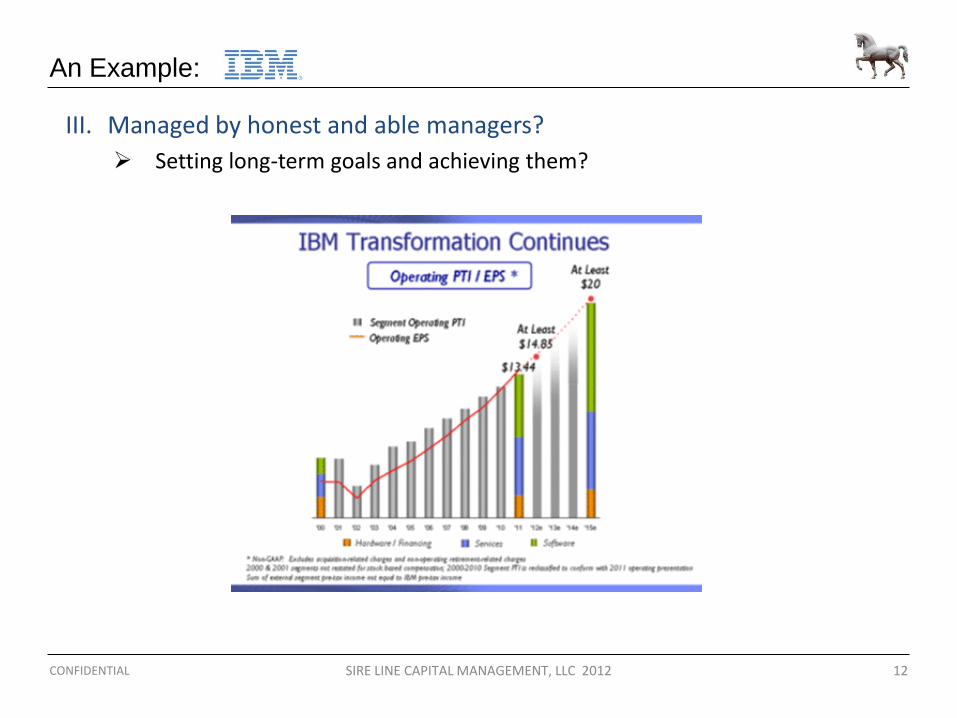

III. Managed by honest and able managers?

Setting long-term goals and achieving them?

An Example:

13 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

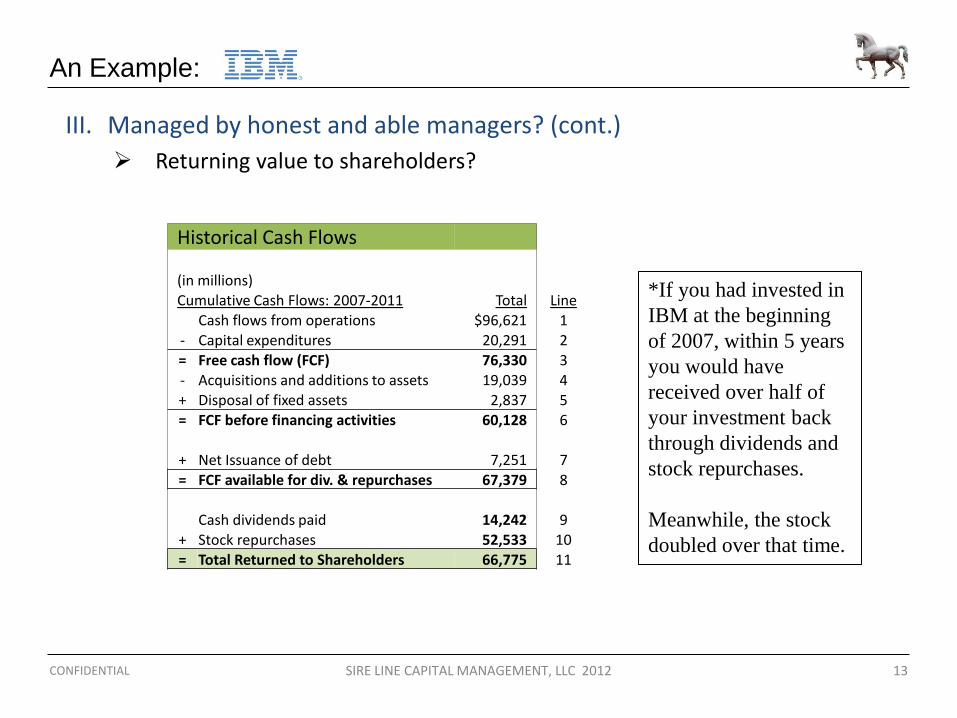

III. Managed by honest and able managers? (cont.)

Returning value to shareholders?

Historical Cash Flows

(in millions) Cumulative Cash Flows: 2007-2011 Total Line

Cash flows from operations $96,621 1

- Capital expenditures 20,291 2 = Free cash flow (FCF) 76,330 3 - Acquisitions and additions to assets 19,039 4 + Disposal of fixed assets 2,837 5 = FCF before financing activities 60,128 6 + Net Issuance of debt 7,251 7

= FCF available for div. & repurchases 67,379 8 Cash dividends paid 14,242 9 + Stock repurchases 52,533 10 = Total Returned to Shareholders 66,775 11

An Example:

*If you had invested in

IBM at the beginning

of 2007, within 5 years

you would have

received over half of

your investment back

through dividends and

stock repurchases.

Meanwhile, the stock

doubled over that time.

14 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

IV. Trading at a significant discount to intrinsic value? Buffett looks for companies whose business economics…

…have performed better than their stock prices.

An Example:

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Sales per share

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Diluted EPS

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

P/E Ratio

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

EV / EBITDA

15 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

IV. Trading at a significant discount to intrinsic value? (cont.)

Traditional measures of value suggest…

Traditional Valuation (in millions, except per share)

As of 3/31/2011*

Stock price $163.00 x Shares outstanding 1,287 = Market value of equity $209,846 + Total debt $28,624

- Cash $11,651 = Enterprise value (EV) $226,819

Income Statement: FY2010 EPS $11.52 FY2010 EBITDA $22,981 FY2010 SALES $99,870

Valuation Multiples: P/E 14.2 x EV/SALES 2.3 x EV/EBITDA 9.9 x

“The stock market is filled with

individuals who know the price of

everything, but the value of nothing.”

-Philip Fisher But…What is the VALUE of IBM?

An Example:

*Buffett started buying in early 2011.

16 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

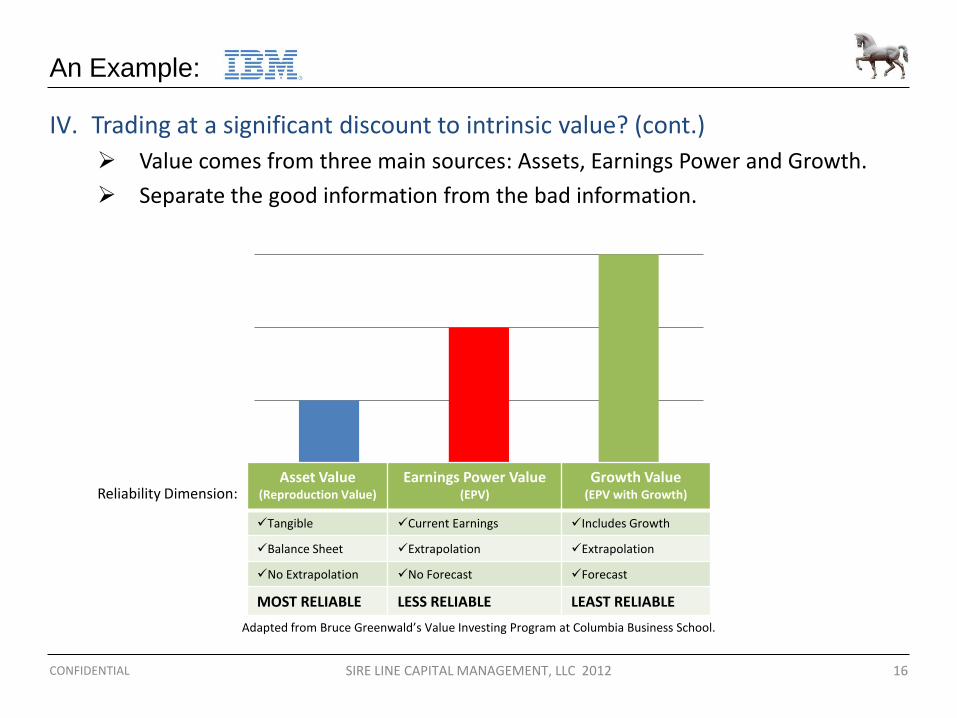

IV. Trading at a significant discount to intrinsic value? (cont.)

Value comes from three main sources: Assets, Earnings Power and Growth.

Separate the good information from the bad information.

Reliability Dimension: Asset Value

(Reproduction Value)

Earnings Power Value (EPV)

Growth Value (EPV with Growth)

Tangible Current Earnings Includes Growth

Balance Sheet Extrapolation Extrapolation

No Extrapolation No Forecast Forecast

MOST RELIABLE LESS RELIABLE LEAST RELIABLE

Adapted from Bruce Greenwald’s Value Investing Program at Columbia Business School.

An Example:

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

REPLACEMENT VALUE EARNINGS POWER VALUE - NG EARNINGS POWER VALUE - G

17 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Equity Valuation of IBM at the end of 2010: Asset Value = $98.9 billion

Earnings power value = $215 billion. Growth does add value!

Total intrinsic value likely between $320 billion ― $360 billion.

Reliability Dimension: Asset Value

(Reproduction Value)

Earnings Power Value (EPV)

Growth Value (EPV with Growth)

Tangible Current Earnings Includes Growth

Balance Sheet Extrapolation Extrapolation

No Extrapolation No Forecast Forecast

MOST RELIABLE LESS RELIABLE LEAST RELIABLE

Adapted from Bruce Greenwald’s Value Investing Program at Columbia Business School.

An Example:

$ in

Mill

ion

s

Buffett paid this amount…

…but paid nothing for future growth.

18 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

IV. Trading at a significant discount to intrinsic value? (cont.) From 1999 through 2002, the stock was overvalued.

In 2008-2009, the stock was trading close to reproduction value.

Today (January 31, 2012), IBM’s stock remains undervalued (paying nothing for future growth).

An Example:

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

$350,000

$400,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ in

mill

ion

s

EARNINGS POWER VALUE - G EARNINGS POWER VALUE - NG REPLACEMENT VALUE HIGH MARKET VALUE LOW MARKET VALUE CURRENT MARKET VALUE

19 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

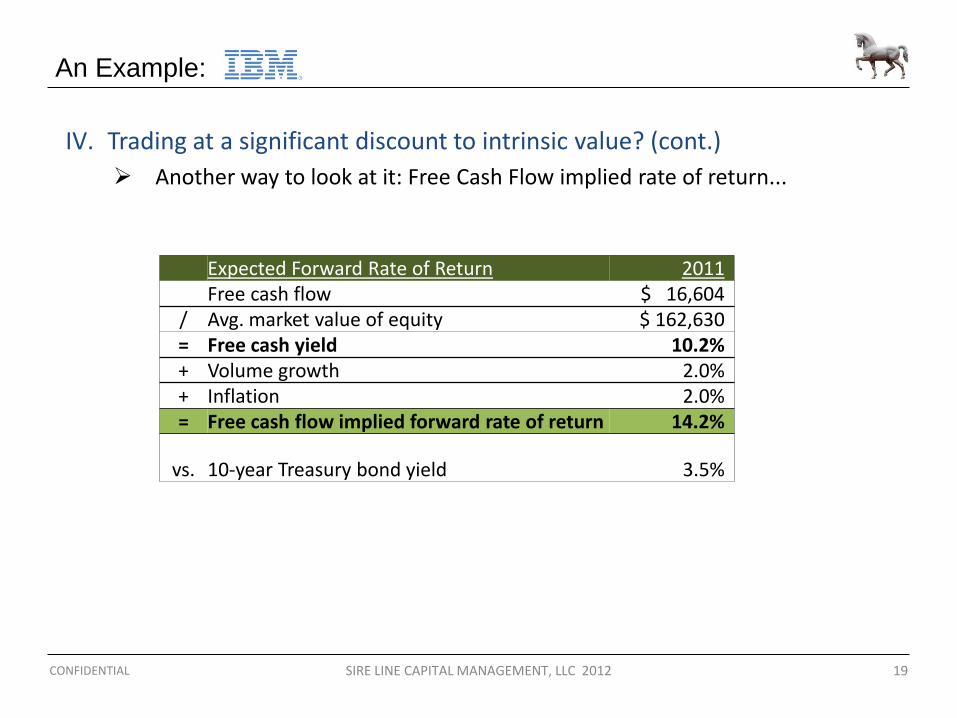

IV. Trading at a significant discount to intrinsic value? (cont.)

Another way to look at it: Free Cash Flow implied rate of return...

An Example:

Expected Forward Rate of Return 2011 Free cash flow $ 16,604

/ Avg. market value of equity $ 162,630 = Free cash yield 10.2% + Volume growth 2.0% + Inflation 2.0% = Free cash flow implied forward rate of return 14.2%

vs. 10-year Treasury bond yield 3.5%

An Example:

20 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Does IBM pass all of Warren Buffett’s tenets?

Simple to understand?

Have favorable long-term economic characteristics?

Managed by honest and able managers?

Can it be purchased at a significant discount to intrinsic value?

Conclusion: 1. Buffett bought IBM for roughly 60% of its true underlying value! 2. Free cash flow-based implied forward rate of return = 14%!!

What about other Stocks?:

21 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

More Examples…

22 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

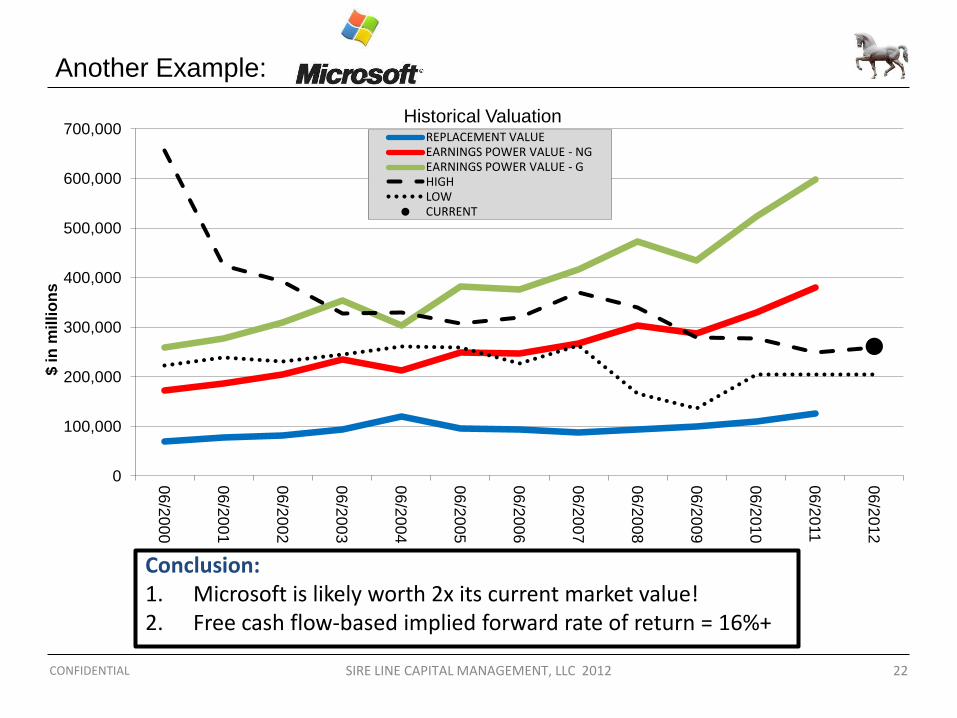

Conclusion: 1. Microsoft is likely worth 2x its current market value! 2. Free cash flow-based implied forward rate of return = 16%+

Another Example:

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

06

/20

00

06

/20

01

06

/20

02

06

/20

03

06

/20

04

06

/20

05

06

/20

06

06

/20

07

06

/20

08

06

/20

09

06

/20

10

06

/20

11

06

/20

12

$ in

mil

lio

ns

Historical Valuation REPLACEMENT VALUE EARNINGS POWER VALUE - NG EARNINGS POWER VALUE - G HIGH LOW CURRENT

23 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

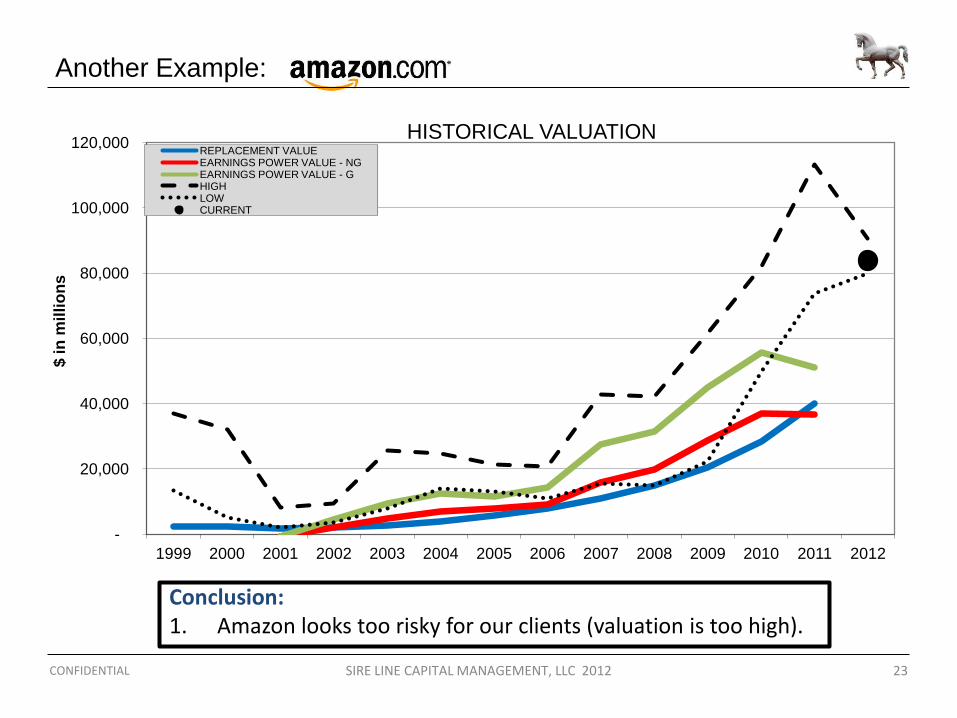

Conclusion: 1. Amazon looks too risky for our clients (valuation is too high).

Another Example:

-

20,000

40,000

60,000

80,000

100,000

120,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ in

mil

lio

ns

HISTORICAL VALUATION REPLACEMENT VALUE EARNINGS POWER VALUE - NG EARNINGS POWER VALUE - G HIGH LOW CURRENT

24 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Conclusion:

1. You can buy Apple Inc. today for roughly 60% of its intrinsic value!

2. Free cash flow-based implied forward rate of return = 13%+

Another Example:

-

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

09

/19

99

09

/20

00

09

/20

01

09

/20

02

09

/20

03

09

/20

04

09

/20

05

09

/20

06

09

/20

07

09

/20

08

09

/20

09

09

/20

10

09

/20

11

09

/20

12

$ in

mil

lio

ns

APPLE HISTORICAL VALUATION

REPLACEMENT VALUE EARNINGS POWER VALUE - NG EARNINGS POWER VALUE - G HIGH LOW CURRENT

25 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Conclusion:

1. JNJ is trading at half of its underlying value!

2. Free cash flow-based implied forward rate of return = 14%+

Another Example:

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

$ in

mil

lio

ns

Historical Valuation REPLACEMENT VALUE

EARNINGS POWER VALUE - NG

EARNINGS POWER VALUE - G

HIGH

LOW

CURRENT

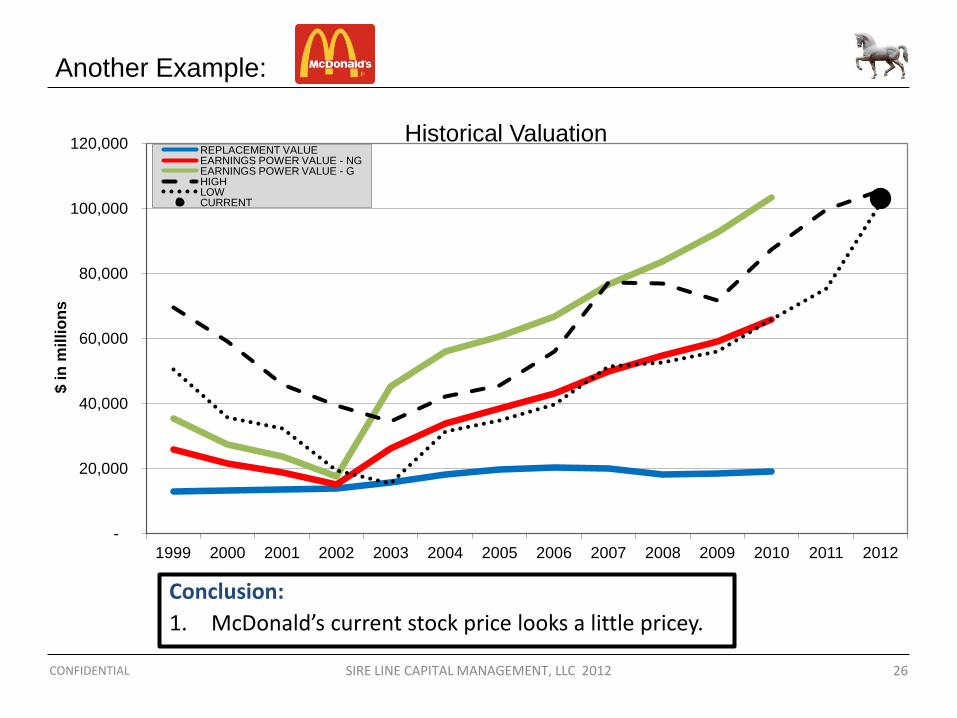

26 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Conclusion:

1. McDonald’s current stock price looks a little pricey.

Another Example:

-

20,000

40,000

60,000

80,000

100,000

120,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

$ in

mil

lio

ns

Historical Valuation REPLACEMENT VALUE EARNINGS POWER VALUE - NG EARNINGS POWER VALUE - G HIGH LOW CURRENT

27 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Conclusion: 1. You can buy Google today and get all of the growth for FREE! 2. Free cash flow-based implied forward rate of return = 13%+

Another Example:

$0

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

2004 2005 2006 2007 2008 2009 2010 2011 2012

$ in

mil

lio

ns

Historical Valuation REPLACEMENT VALUE EARNINGS POWER VALUE - NG EARNINGS POWER VALUE - G HIGH LOW CURRENT

Professional Money Managers

28 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

You should be asking me…

If Buffett’s investment philosophy is so simple, why don’t more professional money managers invest the same way he does?

Answer?

Why do people still smoke cigarettes?

Why do so many people live beyond their means?

Why do millions of people play the lottery?

*When we have an emotional connection to something (i.e. money), we do not always make the best decisions.

29 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

How do you know if the overall stock market is overvalued or undervalued?

Systematic Risk?

Expected Returns – The Equity Markets

30 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Are equity markets overvalued or undervalued?

Slightly overvalued when measured against GDP

Significantly undervalued when measured against bonds.

-30.0%

-10.0%

10.0%

30.0%

50.0%

70.0%

90.0%

3/1

3/2

000

9

4/1

4/1

0

7/1

4/1

0

10

/6/1

0

12

/29

/10

3/2

3/1

1

6/1

5/1

1

9/7

/11

11

/30

/11

potential Upside Potential Downside

Bonds vs. Stocks: Implied Forward Returns for the Equity Markets

0%

20%

40%

60%

80%

100%

120%

140%

160%

4Q

70

4Q

75

4Q

80

4Q

85

4Q

90

4Q

95

4Q

00

4Q

05

4Q

10

WILSHIRE 5000 AS A % OF GDP LONG-TERM AVG.

Total Market Value as a % of GDP

Expected Returns – The S&P 500 Index

31 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Long-term returns for the general market will likely be 7%-10% from here. Assumptions:

5% earnings growth for the S&P 500 Index.

A range (10x-25x) of price/earnings multiples for the S&P 500 ten years out (smaller colored lines). Results:

The thick black line is the actual 10-year rolling average forward return for the S&P 500.

In 1999, the average forward 10-year return for the market was negative.

Looking forward from 2011, average annual returns could be as high as 13% (assuming an end P/E multiple of 25), or as low as 3% (assuming an end P/E multiple of 10).

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

19

50

19

52

19

54

19

56

19

58

19

60

19

62

19

64

19

66

19

68

19

70

19

72

19

74

19

76

19

78

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

10

-ye

ar

retu

rns

10X 15X 20X 25X ACTUAL RETURN

32 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

Is the overall stock market overvalued or undervalued?

Slightly overvalued relative to GDP.

Undervalued vs. bonds.

Expected 10-year forward rate of return = 7% — 10% per year.

Systematic Risk?

33 CONFIDENTIAL SIRE LINE CAPITAL MANAGEMENT, LLC 2012

How to Turn $10,000 into $10,000,000 ?

Starting Value = $10,000 Rates of Return Buffett

Length of Time 5% 10% 13.7% 22.87% 10 years $16,289 $25,937 $35,950 $78,426 20 years $26,533 $67,275 $129,238 $615,060 30 years $43,219 $174,494 $464,604 $4,823,650 40 years $70,400 $452,593 $1,670,235 $37,829,825 54 years $139,387 $1,718,719 $10,017,279 $676,201,838

A 13.7% rate of return is what you need to turn $10,000 into $10,000,000.

Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily understandable business whose earnings are virtually certain to be materially higher five, ten and twenty years from now.”

— Warren Buffett

159 Madison Avenue, Suite 10i New York, NY 10016

Phone: 646.526.8403

www.sirelinecapital.com [email protected]

SIRE LINE CAPITAL MANAGEMENT

HOW TO TURN $10,000 INTO $10,000,000:

INVEST LIKE WARREN BUFFETT