Embed Size (px)

Citation preview

CHAPTER – 1

1

INTRODUCTION

2

INTRODUCTION OF INVENTORY MANAGEMENT:

Inventories are the stock of products sold by a firm and the components that make

up the product while the trading firms buy finished products on wholesale and sell them

for profit, the manufacturing firms buy raw materials, process them, convert them into

finished goods and sell yourself them.

The firm should maintain sufficient stock of finished goods to see that sales are

made as and when demanded. Similarly stock of material should be maintained to have

uninterrupted production activities. Inventories form a link between purchase and sales of

a firm. As they represent assets, they require investment and thus involve commitment of

firm’s financial resources.

Definition of Inventory Management:

Inventory control may be defined as the “systematic control over the procurement,

storage & usage of materials so as to maintain an even flow of materials and avoiding at

the same time excessive investment in inventories”.

Material control covers 3 stages namely

1. Purchase of materials.

2. Storing of materials &

3. Issue of materials.

Inventory Management is the active control program which allows the

management of sales, purchases and payments.

Inventory management is a very high complexed process that involves many

variables such as purchase of raw materials, goods in process and storage of finished

goods.

3

Nature of Inventory:

Manufacturing firms have 3 types of Inventories. They are:

1. Raw Material.

2. Work in Progress &

3. Finished Goods.

Manufacturing firms should always maintain stock of raw materials because they

should be continuously supplied to production departments. If for any reason, there is

shortage of materials, the production activity has to be stopped.

As production is a continuous process, there will be work-in-progress i.e.,

materials which are in process not yet completely converted into finished goods. This

represents work-in-progress inventory. Similarly the firm should maintain stock of

finished goods to sell them whenever they are demanded. I case of trading concerns,

inventory comprises mostly finished goods.

Need For Holding Inventories:

The purpose of maintaining inventories is to uncouple various operations of the

firm i.e., each function should be made independent. If finished goods stock are

maintained, even if there is a delay in production activity, will go on; If work-in-progress

and raw materials stocks are maintained, the production activity will go on even if there

is delay in procuring raw materials.

A manufacturing firm requires supply of raw materials to enable uninterrupted

production. As there is a time gap between placing order for materials and actually

acquiring them, it is always necessary to maintain some quantity in stock.

4

If goods are not supplied when demanded, the firm may lose customers. But huge

inventories involve large financial resources not only to buy them, but even to maintain

them. Because of financial constraints, the should restrict the investment in inventories.

The question of managing materials arises only when the company holds

materials. Maintaining materials involves trying up of the company’s funds and

incurrence of storage and handling costs. If it is expensive to maintain materials, why do

companies hold material? There are 3 general motives for holding materials.

1. Transactions Motive.

2. Precautionary Motive &

3. Speculative Motive.

5

OBJECTIVES OF THE STUDY

The Present Study is based on Following Objectives:

1. To study the raw material being used.

2. To study the inventory management process.

3. To calculate Economic Order Quantity and Lead Time Consumption.

4. To calculate Reorder Level & Maximum Stock.

5. Activity Based Costing of Inventory.

6

SCOPE OF THE STUDY

The Scope and Period of Study is Restricted to the Followings:

1. The Scope is limited to the operations of “HETERO DRUGS LIMITED”.

2. The Information obtained from the Primary & Secondary Data was limited to

“HETERO DRUGS LIMITED”.

3. The key Information Performance Indicates was taken from 2009-13.

4. The Profit & Loss, the Balance Sheet was as on last 5 years.

5. Comparison Analysis was done in Comparison of Sister Units.

7

IMPORTANCE OF THE STUDY

1. Inventory Management helpful to study various factors.

2. It’s helpful to hold safety stock.

3. It’s helpful to purchase raw materials in reasonable prices.

4. It’s helpful to reduce wastage of raw materials.

5. It’s helpful to effective resource utilization.

6. Inventory Management helpful to measure standardization of stock.

7. Inventory Management helpful to issue of products effectively.

Sample Size:

The sample for the study was chosen by means of simple random sampling technique.

The sample covers all categories of employees from several departments of the company.

As the study was intended to measure the effectiveness of Inventory Management. It was

decided not to restrict the study to particular department (or) section. Hence the sample

covers the stock from various departments. The size of sample was fixed to 5 years.

8

LIMITATIONS OF THE STUDY:

The following are the various limitations faced during the entire study.

1. The study is confined to a period of last 5 years. As most of the data is from

secondary sources.

2. The Accuracy is limited. Any changes occurring in year are not annualized.

3. Non-Uniformity of data.

4. Data insufficiency.

5. Hypothetical Analysis.

9

RESEARCH METHODOLOGY

1. The material management mechanism is studied in details.

2. The various factors of inventory management are studied in details.

3. The technical analysis is respect to Economic Order Quantity; Activity Based

Costing techniques have been studied.

The data is collected from the “HETERO DRUGS LIMITED”, Bonthay pally Unit with the help of Primary & Secondary Data.

PRIMARY DATA:

1. Interaction with the Planning and Development department.

2. Interaction with the Finance department.

3. By approaching the experts of the concerned field.

SECONDARY DATA:

1. Material Management Manual of “HETERO DRUGS LIMITED”.

2. Accounting Manuals of “HETERO DRUGS LIMITED”.

3. Browsing various websites through internet.

4. Referring various journals & books.

10

CHAPTER -2

REVIEW OF LITERATURE

11

INTRODUCTION TO ACCOUNTING:

According to Smith & Ashburn, “Accounting is the science of recording and

classifying transactions and events, primarily of financial character and the art of making

significant summaries, analysis and interpretations of that transaction and events and

communicating the results to persons who must make decisions or form judgments”.

Accounting information is used by different people for different purposes.

Financial Accounting deals with preparation of Profit & Loss A/c and Balance Sheet,

catering to the requirement of owners, prospective investors, creditors and serves as a

basis for providing information to other udders.

Cost Accounting deals with classification, computation and analysis of costs on

different basis, providing useful information to managers, employees, government and

other users. Management Accounting, deals with processing of data generated.

1. Financial Accounting:

“Financial Accounting consists of classification, recording and analysis of

transactions in a subjective manner according to the nature of expenditure so as to enable

the presentation at periodic intervals of statement of profit or loss of the business and, on

a specified date, of its financial state of affairs”.

The day-to-day transactions are journalized, posted in the ledger and a Balance

Sheet is prepared. Without Financial Accounting it would have been difficult for any

enterprise to know the profit or loss made by it and its position as on a particular date.

12

2. Cost Accounting:

The ICMA (London) in its publication ‘Terminology of Cost Accounting’

defines Cost as “the amount of expenditure, actual or national, incurred on or attributable

to a given thing”. Costing as “the technique and process of ascertaining costs”. Cost

Accounting as “the process of accounting for cost from the point at which expenditure is

incurred or committed to the establishment of its ultimate relationship with cost centers

and cost units”.

3. Management Accounting:

Management Accounting is that branch of accounting that provides information to

management according to its needs. Management is definitely interested in the usual

figures of Profit/Loss, positions of assets and liabilities etc. However, it is more

concerned with information that helps it in its basic functions of planning, organizing and

control. Management has to set goals for the organization, evaluate various means by

which they can be achieved and select the best alter.

INTRODUCTION OF INVENTORY MANAGEMENT:

Inventories are the stock of products sold by a firm and the components that make

up the product while the trading firms buy finished products on wholesale and sell them

for profit, the manufacturing firms buy raw materials, process them, convert them into

finished goods and sell yourself them.

The firm should maintain sufficient stock of finished goods to see that sales are

made as and when demanded. Similarly stock of material should be maintained to have

uninterrupted production activities. Inventories form a link between purchase and sales of

a firm. As they represent assets, they require investment and thus involve commitment of

firm’s financial resources. Excessive inventories disrupt the production/sales activity.

Thus efficient and effective inventory management aims at maintaining just adequate

stocks which are neither excessive nor inadequate.

13

Definition of Inventory Management:

Inventory control may be defined as the “systematic control over the procurement,

storage & usage of materials so as to maintain an even flow of materials and avoiding at

the same time excessive investment in inventories”.

Material control covers 3 stages namely

1. Purchase of materials.

2. Storing of materials &

3. Issue of materials.

Inventory Management is the active control program which allows the

management of sales, purchases and payments.

Inventory management is a very high complexed process that involves many

variables such as purchase of raw materials, goods in process and storage of finished

goods.

Nature of Inventory:

Manufacturing firms have 3 types of Inventories. They are:

1. Raw Material.

2. Work in Progress &

3. Finished Goods.

Manufacturing firms should always maintain stock of raw materials because they

should be continuously supplied to production departments. If for any reason, there is

shortage of materials, the production activity has to be stopped.

14

As production is a continuous process, there will be work-in-progress i.e.,

materials which are in process not yet completely converted into finished goods. This

represents work-in-progress inventory. Similarly the firm should maintain stock of

finished goods to sell them whenever they are demanded. I case of trading concerns,

inventory comprises mostly finished goods.

Because of large size of inventories required to be maintained, considerable funds

are to be invested in them. As maintaining inventories have financial implications, their

efficient management becomes an essential part of financial management of a firm. The

decision regarding the levels of inventories to be maintained are not taken only by the

financial manager, but various others also are involved in it.

For example, sales manager desires to have huge stock of finished goods in order

to meet customers’ demands instantaneously. Production Manager wants to have

continuous supply of raw materials to see that production process runs smoothly without

any interruption; purchase manager wants to maintain sufficient stock of raw materials to

see that production department’s demands are met on time. Though inventory is more

directly related to production sales departments, financial manager has an active role to

play in efficient management of inventories because of financial implication.

1. Raw Materials:

Raw materials are those basic inputs are converted into finished products through

the manufacturing process. Raw materials are those units which have been purchased and

stored for future production. They are required to carry out production activities

uninterruptedly. The quantity of raw materials required will be determined by the rate of

the consumption and the time required for replacing the supplies. The factors like the

availability of raw materials and govt. regulations etc, too affect the stock of raw

materials. Raw material turn over ratio indicates the number of time material is replaced

during the year. To judge whether the ratio if a firm is satisfactory or not, it should be

compared over a period of the basis or trend analysis.

15

In general, a high material turnover is better than a low ration. Yet a very high

ratio is calls for a careful analysis. It is indicate of under investment in very low level of

inventory has serious implications. It is also likely that the firm may be following a

policy of replenishing it stock in too many small sizes. Similarly, very low inventory

turnover ratio is dangerous. It signified excessive material or ever investment. Carrying

excessive material involves the cost in terms of interest on funds of rental space and so

on. Similarly, a very low material turn over ratio is dangerous. It signified excessive

material or over investment. Carrying excessive inventory involves the cost in terms of

interest of funds of rental space and so on. Thus, a firm should have neither too low

material turnover. To avoid “stock out list” associated with a high ratio and the cost of

carrying the excessive material; there should be reasonable level for miss ratio. The firm

would be well advised to maintain a close watch on the trend of the ratio.

Raw Material Turnover Ratio can be calculated as follows:

Cost of raw material used

Raw Material Turnover Ratio = --------------------------------------------

Average Inventory

2. Work-in-Process:

Work-in-process is also called as stock in process. It refers to goods in the

intermediate stages of production. These are semi manufactured products. They represent

products that need more work before they become finished product for sale. The work in

process is that stage of stocks which are in between new materials and finished goods.

The raw materials enter the process of manufacturing but they are yet to attain the final

shape of finished goods. The quantum of work in process depends upon the time taken in

manufacturing process. The greater the time taken in manufacturing, the more will be the

amount of work-in-process.

16

3. Finished Goods:

The finished goods materials are those completely manufactured products which

are ready for sale. Stocks of raw materials and work-in-process facilitate production,

while stock of finished goods is required for smooth marketing operations. These are

goods, which are ready for consumers. The stock of finished goods provides a buffer

between production and market.

The purpose of maintaining material is to ensure proper supply of goods to the

customer. In some concerns the production is under taken on order basis. In these

concerns there will not be a need for finished goods inventory. The need for finished

goods stocks will be more when production is undertaken in general with out waiting for

specific orders. Thus, inventory serves as the link between the production and

consumption of goods.

The levels of 3 kinds of inventories for a firm depend on the nature of its

business. A manufacturing firm will have substantially high levels of 3 kinds of

materials, while a retail or wholesale firms will have a very high level of finished goods

in material and no raw material and work in process stock.

Within manufacturing firms there will be difference. Large heavy engineering

companies produce long production cycle products; therefore, they carry large materials.

On the other hand, materials of Consumer Product Company will not be large because of

short production cycle and fast turnover. A fourth kind of material, supplies is also

maintained by firms these materials do not directly enter production, but are necessary for

production process.

Usually, these supplies are small part of total material and do not involve

significant investment. Therefore, a sophisticated system of inventory control may not be

maintained for them.

17

Need For Holding Inventories:

The purpose of maintaining inventories is to uncouple various operations of the

firm i.e., each function should be made independent. If finished goods stock are

maintained, even if there is a delay in production activity, will go on; If work-in-progress

and raw materials stocks are maintained, the production activity will go on even if there

is delay in procuring raw materials. A manufacturing firm requires supply of raw

materials to enable uninterrupted production. As there is a time gap between placing

order for materials and actually acquiring them, it is always necessary to maintain some

quantity in stock.

If goods are not supplied when demanded, the firm may lose customers. But huge

inventories involve large financial resources not only to buy them, but even to maintain

them. Because of financial constraints, should restrict the investment in inventories. The

question of managing materials arises only when the company holds materials.

Maintaining materials involves trying up of the company’s funds and incurrence of

storage and handling costs. If it is expensive to maintain materials, why do companies

hold material? There are 3 general motives for holding materials.

1. Transaction Motive:

Emphasizes the need to maintain materials to facilitate smooth production and

sales operations.

2. Precautionary Motive:

Necessities holding of materials to guard the risk of unpredictable changes in

demand and supply forces and other factors.

3. Speculative Motive:

Influences the decision to increase or reduce material levels to take advantage of

price fluctuation.

18

Objectives of Inventory Management:

Large size inventories are require to ensure continuous and uninterrupted

production and efficient sales activity; but at the same time maintaining huge inventories

also reduce the profitability of the firm because they involve some costs. One cost

involved is the carrying cost. The stock purchased should be stored. The large the goods

purchased bigger should be the store were house bigger the size, the higher the cost-rent,

insurance, store keeper’s salary etc.

Another cost is financing cost. Maintaining huge stocks require amounts to be

invested in them. These funds are to be maintained to be financed at a cost. Thus efficient

management involves meeting 2 conflicting needs:

1. Maintaining large stocks of inventories to achieve efficient and smooth

production and effective sales.

2. To ensure regular and uninterrupted supply of materials i.e., to make materials

available as and when they are needed.

3. To keep investments in stock at a reasonable level, so that there is no loss of

interest on capital.

4. To purchase the materials at a reasonable price without sacrificing the quantity of

such materials.

5. To avoid abnormal wastage by exercising direct control.

6. To avoids the risk of spoilage obsolescence of the materials by fixing the

maximum stock level; and

7. Restricting the inventories to the minimum to maximize the profitability.

Thus, inventory management decisions involve a trade off between profitability

and risk. The level of inventories maintained should neither be excessive nor inadequate.

19

Scope of Inventory Management:

Inventory management is a very simple concept - don't have too much stock

and don't have too little. Since there can be substantial costs involved in straying

above and below the optimal range, careful inventory management can make a

huge difference in the profitability of a business. Although the concept is simple,

the process of getting the right balance can be quite a complex and time

consuming task without the right technology. There are two fundamental questions

that must be answered, in order to manage the inventory of any physical item -

when to order and how much to order.

LSS will provide technical and economical expertise, at no charge, to assist

in determining probable valves to include in an inventory management program.

Methods to be used will include repair cost economics and the frequency of use

criteria of certain valve sizes, pressure, and type.

1. Usage of surplus inventory is cost effective.

2. Offers better control on deliveries.

3. Utilizes company assets.

4. Adds $ to the bottom line.

5. Avenue to sell un-needed equipment

6. No Cost until repair is performed.

7. Saves Valuable time and effort for the customer.

8. Ease accounting functions through reporting.

9. Vast types of equipment serviced.

10. Centralizing inventory for easier accessibility will lead to more complete

Surplus inventory utilization.

20

Functions of Inventory Management:

Inventory management is a highly complex process that involves many

variables. A business must coordinate receiving and stowing with outbound

shipments, always ensuring there is ample space for new stock and that all items

are accounted for. The flow of goods in and out of a business must be monitored

closely to identify market trends and to create strategic plans for the enterprise’s

future.

1. Flow of Goods:-

Not only must a business keep track of the goods coming in and going out,

it must also track the costs to procure, store, sell and ship these goods. The

company must also account for damage, loss, and labor costs associated with

handling the merchandise. Inventory management software allows an enterprise to

track all of these things, while detailing the precise location of goods to allow for

fast and efficient order picking.

2. Replenishment:-

Inventory Management Software The business can determine the

appropriate ordering times for inventory replenishment with inventory

management software. Software allows for controls to be set that determine stock

levels for reorder, ensuring the business always have enough products to meet

demand. The software even helps determine what an item’s reorder point should

be by taking in factors like lead time, seasonal changes and the time between

receiving and stowing. These settings can easily be altered when needed.

21

3. Additional Functionality:-

Some software packages carry other functions that allow the company to

extend operations beyond brick and mortar, addition E-commerce capabilities.

Further enhancements allow the business to consolidate shipments, and process

back orders, returns and substitutions.

4. Choosing the Right Software:-

Selecting the right software will depend on the scrutiny the company places

on core business functions. It is easy to become distracted by the bonus features

some software offers. A business must determine the core functions needed and

focus on acquiring software that fills those needs most efficiently. It is not safe to

assume a given software package has the basic functionality all businesses should

have. Always scrutinize the list of functions the software vendor provides and ask

questions to fully understand the depth of capability for each function.

5. Tailoring to Business Needs:-

Not all software is created alike and most packages were designed with

specific businesses in mind and then later marketed to a wider audience. For this

reason, it is vital that a company seek software that fits the core business model.

Manufacturers will seek to find software design specifically for that type of

business.

6. Customer Service:-

No company should purchase a software package without first speaking to

other clients who use the software. While contacts can be made through the

salesman, it is obvious that the salesman will only point to positive reviews. A

business can research forums online to connect with other users of a software and

collect user experiences before making a purchase decision. The research should

focus on customer satisfaction, responsiveness of the help desk and ease of use.

22

Advantage of Inventory Management:

Advantage of Inventory reconciliation Management for Accounting

Software. Inventory Reconciliation Management is indispensable for the

successful, efficient inventory reconciliation auditing of any organization.

Inventory Reconciliation is the ideal solutions to validate the data your business

depends upon.

Advantages of high level of stocks are many like it provides a buffer to the

companies against the high demands. If the prices of the products are expected to

increase in future then a high level of inventory

Can also give a capital gain to the companies. High level of stocks can also

eliminate the risk of fall of supply in the future. Shortages of goods in the market

in future can be handled by keeping high levels of inventory.

Disadvantage of Inventory Management:

On the other hand, the main disadvantage of keeping high levels of finished

products will increase the costs of the warehouse management. Secondly, if the

prices of the finished goods are expected to fall then the company can get the

capital loss. Poor inventory management can result in the loss of inventory like

obsolete inventory problems.

23

Factors Determining the Level of Inventories:

The level of inventory depends upon a number of factors:

1. Usage during the Period

2. Lead Time

3. Trade Discount

4. Production Cycle Period

5. Demand for the Product.

1. Usage during the Period:

The level of raw material inventory depends upon the quantity of raw materials

used daily. The more the usage, the more will be the stock required. Similarly the stock

of finished goods depends upon the anticipated daily sales of the firm.

2. Lead Time:

Lead time is the time period between placing an order for materials and actually

receiving delivery of these goods in case of raw materials. In case actually receiving

delivery of these goods in case of raw materials. In case of finished goods it refers to

production cycle period i.e., the time taken to convert raw materials and work-in-progress

into finished goods. If materials are to be purchased from a distant place, some times it

may take even a few months to get delivery of these goods after placing an order. In such

cases, huge stocks should be maintained to see that production activity is not stopped for

shortage of materials. Some times unforeseen factors like strikes, bands etc., may cause

further un-anticipated delay in procuring materials. Some safety stock should additionally

be maintained over and above the minimum level to meet such contingencies.

24

3. Trade Discount:

Another reason for acquiring huge raw materials is attractive bulk discounts the

firm can avail on bulk purchases and the expected savings in other costs. For example, if

the materials cost Rs.100/- per unit and if 5% discount is offered on purchase of 300 units

or more, by purchasing 300 units, the price will be reduced to Rs.95/- per unit. Similarly

if the transport costs are Rs.2000/- per truck, a truck load of materials may be purchased

and kept in stock.

4. Production Cycle Period:

Work-in-progress inventory depends upon the length of production process. The

longer the process, the higher would be the inventory. Most of the firms try to reduce the

production cycle period by improving the production techniques. Otherwise huge funds

blocked up in work-in-progress.

5. Demand for the Product:

Stocks of finished goods are determined to sell them on demand. If goods cannot

be supplied when they are on demand, the firm may lose the customer. Frequent delays in

supply of goods results in losing not only the existing customer but even the prospective

customers.

25

Purchase of Materials:

The work of purchasing materials should be handled, of the size of the concern

permits, by a separate purchasing department. Purchasing should be centralized i.e., all

purchases should done by purchasing department except for small purchases which may

be made departmental managers.

The most important function of the purchases department is “to buy and supply

the materials and stores required for various departments of right quality, in right

quantity, and at right time and at right price”. Whenever there is a need for stores a

Purchase Requisition Note is prepared by the storekeeper. It contains particulars

regarding quantity, the quality or material specifications and the by which the materials

are required.

A purchase order prepared by the purchase department and sent to the suppliers,

the purchase order is generally prepared in triplicate. The original copy is sent to the

vendor, the duplicate is sent to the accounting department. The fourth and fifth copies, if

made, are sent to the shopkeeper and the receiving department, respectively.

Inventory Management Techniques:

Efficient inventory management needs a systematic approach. We are using on

the following techniques:

1. Economic Order Quantity.

2. Safety Stock.

3. Re-order Point.

4. Maximum Stock Level.

26

5. ABC Analysis (or) Selective Inventory Control, and

1. Economic Order Quantity:

Economic Order Quantity is a very important dimension if inventory

management. It is that level of quantity which minimizes the total cost of inventory

including ordering costs and carrying costs. This model is based on the following

assumptions.

Usage of particular item of inventory over a period is with certainty and the usage

is even throughout the period.

The cost per is constant and the carrying cost per unit also constant.

There are only 2 costs associated with inventories the carrying costs and the

ordering costs.

There are 2 basic questions relating to inventory management:

What should be the size of the order?

At what level should the order be placed?

To answers the first question the economic order quantity model is helpful. If the

firm is buying raw materials, it has to be purchased on replenishment. This problem is

called order quantity problem and the task of the firm is to determine the optimum or

EOQ.

The determination of the appropriate quantity to be purchased in each lot to

replenish stock as a solution to the order quantity problem necessitate resolution of

conflicting goals buying in large quantities implies a higher inventory level which will

assure.

1. Smooth production / sales operations.

2. Lower ordering or set-up costs.

27

But it involves higher carrying costs. On the other hand small orders wick reduce

the carrying costs of inventory by reducing the average material level but the ordering

costs would increase as there is a likelihood of interruption the operations due to stock-

outs.

A firm should place neither too lame nor too small orders on the basis of trade off

between the benefits from the availability of inventory and the cost of carrying.

To take enough to avail the concessions in purchasing materials.

Ensuring that the materials of requisite specifications and quality have been

received in good condition.

Determining an optimum material level involves 2 types of costs:

A. Ordering Costs:

The term ordering cost is used in case of raw material and includes the entire

costs of acquiring raw materials. They include costs incurred in following activities;

purchase ordering, transporting, receiving and inspecting. Ordering costs increase the

number of orders; thus more frequently the material is acquired the firm’s ordering costs.

On the other hand, if the firm maintains large inventory levels, they will be few orders

placed and ordering costs will be few orders placed and ordering costs will be relatively

small. Thus, the ordering costs decrease with increasing size of inventory.

B. Carrying Costs:

Costs incurred for maintaining a given level of inventory are called carrying costs.

They include storage, taxes, insurance, deterioration, obsolescence incurred in recording

and providing special facial facilities such as fencing, lines etc.

28

Carrying costs vary with inventory size. The economic size of the inventory

would thus depend on trade-off between costs and ordering costs.

EOQ:

The optimum inventory size is commonly referred to as economic order quantity.

It is that order size at which annual total costs of ordering and holding are the minimum.

To find this the formula is:

EOQ = Squire (2AO/C)

Where,

A = Annual Total Requirement,

O = Ordering Costs,

C = Carrying Costs.

Assumptions of EOQ:

1. The forecasts usage / demand for a given period, usually one year, is known.

2. The usage / demand is even throughout the period.

3. Inventory orders can be replenished immediately (there is no delay in placing and

receiving orders).

4. There are 2 distinguishable costs associated with inventories; costs of ordering

and costs of carrying.

5. The cost per order is constant regardless of the size of order.

6. The cost of carrying is a fixed percentage of the average value of inventory.

2. Safety Stock:

It is not always possible to estimate the daily usage of materials or daily sales of

different products with certainty. Similarly the lead time, though can be estimated on the

basis of past experience, due to some unforeseen reason it may get delayed by a few days.

In such cases, if materials are not in stock, sales activity may be stopped or slowed down.

Therefore it is always essential that some safety stock is maintained as a buffer for such

29

contingencies. Thus, “safety stock” is the quantity of stock to be maintained over and

above the ordinary level, to be able to meet such unforeseen situations. The ordinary level

should be adjusted for safety stock.

Thus the formula to determine the re-order point when the safety stock is

maintained is as follows:

Re-order = (Lead Time * Average Usage) + Safety Stock

3. Re-order Point:

The problem, how much to order, is solved by determined the economic order

quantity, yet the answer should be sought to the second problem, when to order. This is a

problem of determining the re-order point under certainty, we should know:

Lead time.

Average usage, and

Economic order quantity.

Re-order Point = (Lead Time * Average Usage)

4. Maximum Stock Level:

The maximum level is the largest quantity of a particular material, which should

be kept in the store at any one time. The fixation of maximum level is necessary to avoid

unnecessary blocking of capital in materials, losses on account of deterioration and

obsolescence of materials, extra overheads and temptation to thefts.

30

The maximum level of material should be decided after taking into consideration

the following:

Storage space.

Availability of working capital.

Seasonal considerations.

Rate of consumptions materials and time necessary in obtaining the new

materials.

Rules framed by govt. for import or procurement.

Cost of storage, insurance, interest on capital invested in stock.

Maximum Stock Level is ascertained by the following:

Maximum Stock Level = Reorder Level + EOQ

5. ABC Analysis (or) Selective Inventory Control:

Usually a firm to maintain several types of materials. It is not desirable to keep

the same degree of control on all the items. The firm should pay maximize attention to

those items whose value is the highest. The firm should, therefore, classify materials to

identify which items should receive the most effort in controlling. The firm should be

selective in its approach to control investment various type of materials. This analytical

approach is called ABC analysis and tends to measure the significance of each item of

material in terms of its value.

The high value it ms are classified as ‘A items’ and would be under the tightest

control. ‘C items’ represent relatively least value and would be under simple control. ‘B

items’ fall in between these 2 categories and require reasonable attention of management.

31

The ABC analysis concentrates on important items and is also known as control by

importance and exception. As items are classified in the importance of their relative

value, this approach is also known as “Proportional Value Analysis”.

The following steps are involved in implementing the ABC analysis:

Classify the items of materials, determining the expected use in units and price

per unit for each item.

Determining the total value of each item by multiplying the expected units by its

unit’s price.

Rank the items in accordance with the total value, giving first rank to item with

highest total value and so on.

Compute the ratios (%) of number of units of each item to total units of all items.

And the ratio of the total value of each item to total value of all items.

Combine items on the basis of their relative value to 3 categories, A, B and C.

32

CHAPTER-III

INDUSTRY PROFILE

33

INDUSTRY PROFILE

Indian bulk drug industry

The independent bulk drug manufacturers in India are currently caught between

the devil and the deep sea, as the option left with them is only the regulated markets or an

earlier closure without suffering huge loss.

The bulk drug units without a formulation activity on their own have been under

tremendous pressure of price war in the domestic market, which has forced them to get

34

into either exports where the global quality standards are to be met or quitting the

business once for all.

The industry sources are -- by large - of the opinion that competing in the

domestic market has become next to impossible as the market is currently flooded with

discounted sales and instant price cuts. The abundant supply, low demand from domestic

formulation companies for the local made drugs and dumping of imported drugs have

together contributed to this chaotic market situation and the result is uncertainty in the

industry, say industry sources.

The production of pharmaceuticals in India increased by 13.68 per cent during the

year 1997-98 against the previous year, the production value of bulk drugs during the

year was only Rs 2,623 crore and that of pharmaceutical formulations was Rs 12,068

crore. However, the exports of Pharmaceuticals during the year 1997-98 was Rs 49780

million, which continued to grow especially in the bulk drug segment in the following

years as the domestic market proved to be uncomfortable for the manufacturers. The

ruling prices of many of the bulk drugs in the domestic market have been on a declining

trend and even touched far below the notified price. From a meager Rs 46 crore worth of

pharmaceuticals, drugs and fine chemicals exports in 1980-81, pharmaceutical exports

has risen to approximately Rs. 6152 crore in 1998-99, with an average growth of 11.91

per cent annually.

Following the de-licensing of the pharmaceutical industry, industrial licensing for

most of the drugs and pharmaceutical products has been done away with; manufacturers

are free to produce any drug duly approved by the Drug Control Authority.

Technologically strong and totally self reliant, the pharmaceutical industry in India has

low costs of production, low R&D costs, innovative scientific manpower, strength of

national laboratories and an increasing balance of trade.

Though domestic pharmaceutical industry output is expected to exceed Rs 260

billion in the financial year 2002, the bulk drugs will account for only Rs 54 billion ie. 21

per cent and formulations the remaining Rs 210 billion with 79 per cent. Reflected in the

35

import export volume during the financial year 2001, there is a conscious move among

the bulk drug manufacturers from the domestic sales to foreign supply. However, during

the year, the imports were Rs 20 billion as against the exports of Rs. 87 billion.

The Indian Pharmaceutical sector is highly fragmented with more than 20,000

registered units. It has increased drastically in the last two decades. The leading 250

pharmaceutical companies control 70 per cent of the market with the market leader

having nearly 7 per cent of the market share. It is an extremely fragmented market with

severe price competition and government price control.

As a result, over 60 per cent of India’s bulk drug production is exported and only

40 per cent is currently sold in the local market to formulators. However, many of the

major formulation companies use their in house production of bulk drugs, where they

themselves have excess capacity.

The industry alleges that though the import of bulk drugs through official channel

have slowed down in the past 2-3 years, the dumping and smuggling of drugs are rampant

at present. This also has caused huge price discounts in the domestic market.

During the last decade the production of bulk drugs has grown from Rs. 240 crore

in 1980-81 to Rs. 1320 crore in 1993-94. Since 1986, the Drug Industry has grown

significantly, as mentioned earlier, in terms of production of bulk drugs and formulations.

In many cases manufacture of bulk drugs has also been established from the desired basic

stage. It is estimated that in case of bulk drug production the contribution of small-scale

sector is approximately 30 per cent of the total production in the country.

It may also be mentioned that the pharmaceutical sector has been able to carve a

special niche for itself in the international market as a dependable exporter of bulk drugs.

However, a number of small bulk drug units who were dependent only on the local

formulation sector are in fixes they are neither in a position to survive in the market with

present local prices nor capable of reaching out to the export market.

36

Thus, the industry sources predicts, at least 70 per cent to 80 per cent of the

independent bulk drug manufacturing units would face extinction from the sector in the

near future as the domestic market does not show any positive signals yet.

Pharmaceuticals are medicinally effective chemicals, which are converted to dosage

forms suitable for patients to imbibe. In it basic chemical form, pharmaceuticals are

called bulk drugs and the final dosage forms are knows as formulations. Usage of

pharmaceuticals is governed by the underlying medical science. The four primary

medical sciences are as under:

Allopathy or modern medicine has gained global popularity.

Ayurveda, an ancient Indian science, mainly herbal remedies.

Unani having Chinese Origin is South East Asia.

Homeopathy, founded by a German Physician, was fairly popular in the

early 20th century.

INDUSTRY SECNARIO:

World-over, the Pharmaceuticals industry is focused on Allopathy, the most

modern medical science. Other modes of medical treatment such Homeopathy,

Ayurveda and Unani are more prevalent in third world countries.

The exports from the Indian pharmaceutical industry to the well regulated market

in United States of America is increasing rapidly, by recording the highest growth in the

current financial year when compared to the recent past.

The Indian pharma exports to US have already recorded a favorable momentum

right from the year 2002, increasing from USD million 489.08 in April 02-March 03 to

USD million 680.50 in April 2005 – March 2006.

From being an import dependent industry in the past 1950,s Indian pharmaceutical

industry has achieved self-sufficiency and gained global recognition as a producer of low

37

cost high quality bulk drug and formulations. Leading Indian companies have developed

infrastructure in over 60 countries including developed markets like USA and EUROPE.

In the last few years several pharmaceutical companies have demonstrated that they

posses the ability to engage in commercially viable research and development activities

and become significant players in the international market.

MAJOR PLAYERS IN PHARMA

Ranbaxy Laboratories

(Sri S T Kalairaj, Chairman)

Ranbaxy is the leader in the Indian pharmaceutical market, taking in $1.174

billion in revenues for a net profit of $160 million in 2004. It was the first Indian

pharmaceutical to have a proprietary drug (extended-release ciprofloxacin, marketed by

Bayer) approved by the U.S. FDA, and the U.S. market accounts for 36% of its sales.

78% of Ranbaxy’s sales are from overseas markets; its offices in 44 countries manage

manufacturing in 7 countries and distribution in over 100.

IMS Health estimated that Ranbaxy is among the top 100 pharmaceuticals in the

world and that it is the 15th fastest growing company. By 2012, Ranbaxy hopes to be one

of the top 5 generics producers in the world, and it consolidated its position with the

purchase of French firm RGP Aventis in 2003. Ranbaxy also has higher aspirations,

however, “to build a proprietary prescription business in the advanced markets.” To this

end, it keeps a dedicated research facility in Gurgaon staffed with over 1100 scientists.

They currently have two molecules in Phase II trials and 3-5 in pre-clinical testing. It

spent $75 million in R&D in 2004, a 43% increase over its 2003 expenditure.

Dr. Reddy's Laboratories

(Dr.K. Anji Reddy, Chairman)

38

Founded in 1984 with $160,000, Dr. Reddy’s was the first Asia-Pacific

pharmaceutical outside of Japan and the sixth Indian company to be listed on the New

York Stock Exchange. It earned $446 million in fiscal year 2005, deriving 66% of this

income from the foreign market. In order to strengthen its global position, Dr. Reddy

acquired UK-based BMS Laboratories and subsidiary Meridian Healthcare.

Although 58% of Dr. Reddy’s revenues come from generic drugs, the company

was committed to WTO-compliance long before the 2005 bill took effect, and most of

these products were already off patent. Dr. Reddy has long been a research-oriented firm,

preceding many of its peers in setting up a New Drug Development Research (NDDR) in

1993 and out-licensing its first compound just four years later. Dr. Reddy’s has since

outlicensed two more molecules and currently has three others in clinical trials.

Although Dr. Reddy’s is publicly-traded, the Reddy family (including

founder/chairman K. Anji Reddy, son-in-law/CEO GV Prasad and son/COO Satish

Reddy) holds a hefty 26% share in the company.

Nicholas Piramal

(Asish Mishra, Chairman)

Now a company grossing $350 million per year, Nicholas Piramal started its

existence with the 1988 acquisition of Nicholas Laboratories and grew through a series of

mergers, acquisitions and alliances. The company has formed a name for itself in the field

of custom manufacturing. It cites its 1700-person global sales force as another core

strength; with its acquisition of Rhodia’s inhalation anesthetics business, Nicholas

Piramal gained a sales and marketing network spanning 90 countries.

Nicholas Piramal is well-poised for the challenge of surviving in the aftermath of product

patent protection. The company has respected intellectual property rights since its

inception and refused to "support generic companies seeking first-to-file or early-to-

market strategies." Instead, it decided to make its own intellectual property and opened a

39

research facility last November in Mumbai with hopes of launching its first drug in 2010

at a cost of $100,000.24.

Chapter-IV

COMPANY PROFIL

40

COMPANY PROFILE

Mr. Dr. B. PARTHA SARADHI REDDY

Managing Director, Hetero Drugs Ltd.

Hyderabad: Hyderabad-based Pharma Company Hetero Drugs Ltd, A relatively

young company in the Indian Pharmaceutical Industry is making rapid strides both

nationally and internationally. Involved in the manufacture of active pharmaceutical

ingredients and finished dosage forms, Hetero is one of the very few companies which

41

have been able to carve a niche in the market given the present Scenario where it requires

intellectual strength, core competencies and the right vision for the future.

Address: H.No. 8-3-166/7/1, Erragadda, Hyderabad, Andhra Pradesh 500 018, India

Phone: +91-(40)-23704923 Fax: +91-(40)-23704926

Today, it’s a name which epitomizes hard work, experience and success. A

relatively young company that is making its presence felt and making rapid progress

nationally and internationally.

42

Involved in the manufacturing of active pharmaceutical ingredients and finished

dosage forms, Hetero is one of its kinds of the very few companies which have been able

to carve a niche in the pharmaceutical industry given the present scenario where it

requires a right blend of intellectual strength, core competencies and a precise foresight

for the future.

Hetero has come a long way since its inception in the year 1993 to be recognized

as a strong player in the field of pharmaceuticals, as a result of its combined strength in

research, manufacture and marketing.

Established in the year 1993, with the motto to be the best in the API

manufacturing, Hetero today embodies the vision of a top notch player in developing and

commercializing products catering to a variety of therapeutic categories, integrating into

a leading finished dosage manufacturer.

43

True to the Statement, "Where the Future Started Yesterday", with a foresight on the

current trends in the Pharmaceutical Market, Hetero has grown from strength to strength,

combining its Research Strengths, Manufacturing Capabilities, and Human Resources

and well established quality management system.

With full-fledged marketing capabilities, the company has been able to market its

products in over 100 countries in Asia, Middle-east, Eastern Europe and Latin America.

With its compliance to the most stringent regulatory requirements, Hetero has today

gained foothold to market several of its APIs in the United States, Canada and Europe.

With all six manufacturing facilities being supported by excellent infrastructure and

compliance to the GMP requirements, Hetero has crossed numerous milestones in a

comparatively short period since its inception.

Hetero Drugs Ltd has been chosen by the Clinton Research Foundation as one of

the four Indian pharmaceutical companies that would supply HIV/AIDS drugs to four

African and nine Caribbean nations. HDL range of three drug combinations, namely

'Nevirapine', 'Lamivudine', 'Stavudine', were available at a price that AIDS patients in

India could afford

The spirit and brain behind the success story of Hetero is its founder Dr.BPS Reddy, a

Scientist who started the company drawing immense strength from the vast and rich

experience he gained during his earlier stint at the Laboratory where he was instrumental

in developing and commercializing processes for several APIs.

44

The Company was started by him with a vision to be recognized as an aggressive

company that combines its strength of R&D and manufacturing with definite advantages

in terms of cost and chemistry with a strong emphasis on Quality of the products.

The untiring efforts of the Chairman saw Hetero develop processes for several

products at relatively low cost, thus making it possible for several life saving drugs to be

available at affordable prices, meeting all the Regulatory and Quality norms.

With the organization having reached a point where it is identified among the

widely recognized companies, the Chairman is now focusing on giving new dimensions

to the company in terms of exploring possibilities of further growth, exploring new

horizons in the field of Pharmaceutical development and evolving strategies to take the

company to greater heights.

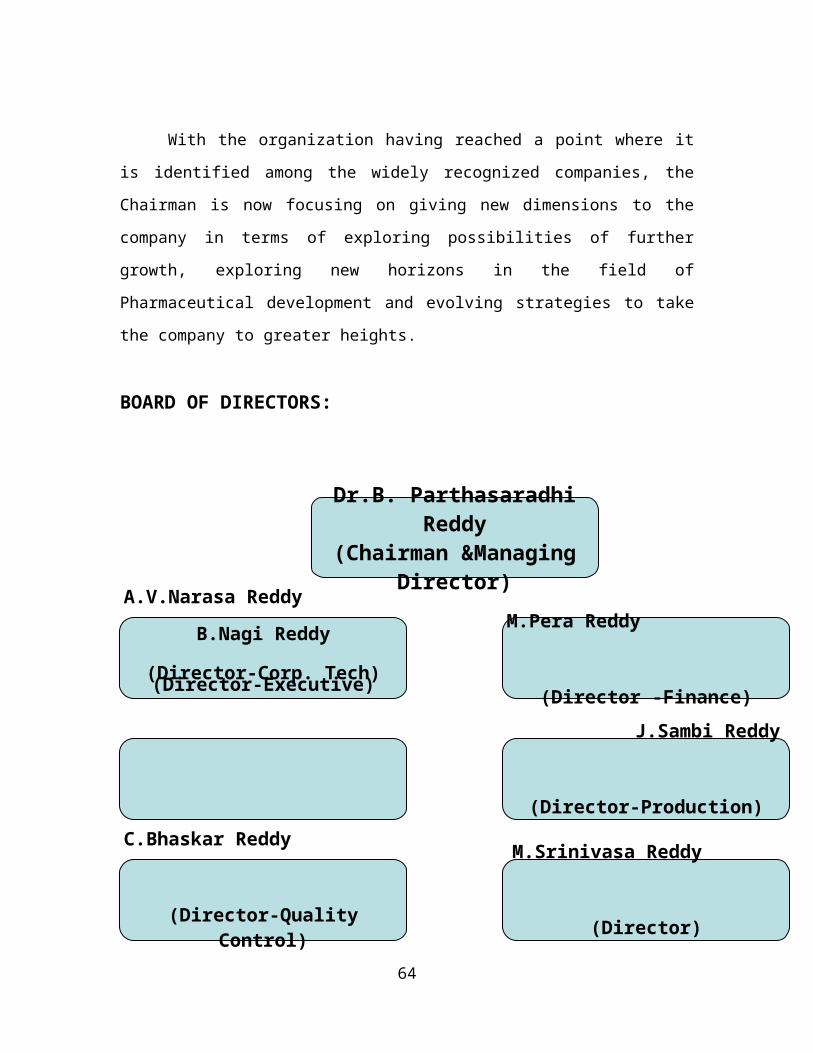

BOARD OF DIRECTORS:

45

46

Dr.B. Parthasaradhi Reddy(Chairman &Managing

Director)

B.Nagi Reddy

(Director-Executive)

M.Pera Reddy

(Director -Finance)

A.V.Narasa Reddy

(Director-Corp. Tech)

J.Sambi Reddy

(Director-Production)

C.Bhaskar Reddy

(Director-Quality Control)

M.Srinivasa Reddy

(Director)

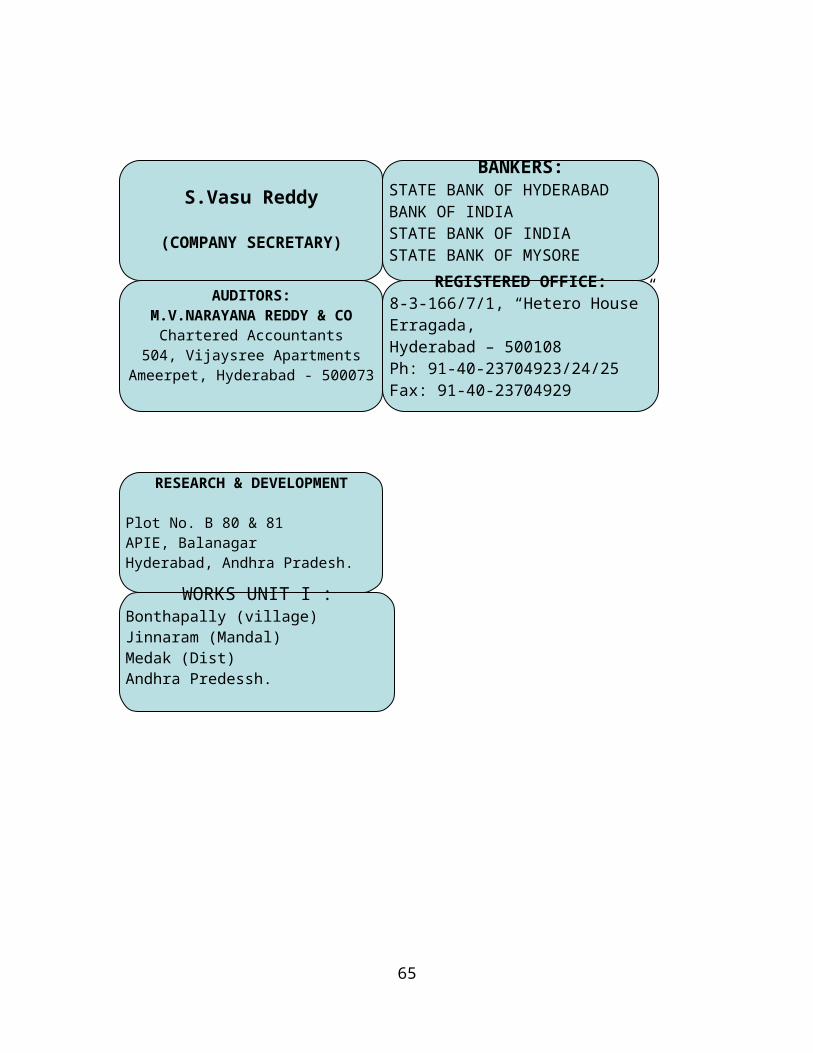

S.Vasu Reddy

(COMPANY SECRETARY)

BANKERS:STATE BANK OF HYDERABADBANK OF INDIASTATE BANK OF INDIASTATE BANK OF MYSORE

AUDITORS:M.V.NARAYANA REDDY & CO

Chartered Accountants504, Vijaysree Apartments

Ameerpet, Hyderabad - 500073

REGISTERED OFFICE:8-3-166/7/1, “Hetero House”Erragada,Hyderabad – 500108Ph: 91-40-23704923/24/25Fax: 91-40-23704929

Hetero Group

HETERO DRUGS LIMITED

HETERO LABS

HETERO RESEARCH FOUNDATION

SYMED LABS

GENX PHARMA

HETERO HEALTH CAR

MILESTONES / AWARDS

47

RESEARCH & DEVELOPMENT

Plot No. B 80 & 81APIE, BalanagarHyderabad, Andhra Pradesh.

WORKS UNIT I :Bonthapally (village)Jinnaram (Mandal)Medak (Dist)Andhra Predessh.

UNIT II :Plot No. 16, CIE Gandhinagar Jeedimetla,Hyderabad

UNIT III :22-110-IDAJeedimetla,Hyderabad

The Company has been Scaling New Heights on a continual basis. These achievements

have been the result of concerted efforts on the part of different functions within the

organization to achieve the organizational goal of being a leader.

In its path to success, Hetero has seen many a milestone being crossed and achieved

many awards on various fronts. Awards for exemplary work in R&D and marketing are

just a few to name.

A track of few events that saw Hetero reaching its Zenith of glory is:

National Award for “Best Efforts in Research and Development” from the

Department of Scientific and Industrial Research, Ministry of Science and

Technology, Government of India, in the year 1996.

Highest Exporter award (for the year 1999) against stiff competition from

internationally recognized domestic competitors.

Approval of the API facilities by USFDA for compliance to CGMP norms

Approval of the finished dosage facilities by whom for the supply of anti-

retroviral drugs.

48

Vision & Values

Hetero visualizes itself as an aggressive player in the global pharmaceutical scenario,

supplying generics developed, combining intellectual property, research strengths and

strong human resource inputs.

The company values the concepts of having social responsibilities in the course of its

assent to greater heights. It strongly believes in focusing on customer requirements and

delivering the products at the right pace.

Hetero considers its human resources as the core of all its capabilities and believes in

tapping and honing the talents of its members to reach the zenith of success.

It believes in continuous evaluation and improvement in all the factors that contribute in

transforming the organization into a global force to reckon with.

Hetero takes due cognizance to the fact that the processes that it develops should be all

eco-friendly and should not result in any consequence that harms the ecological harmony.

MISSION

49

Hetero’s Mission is to be a globally acclaimed Pharmaceutical Company, Meeting the

requirements of Healthcare imbibing the philosophy of both commercial and social

concerns, driven by research and manufacturing capabilities.

APIs

Hetero API Facilities are designed to meet the best of global standards for an API

Facility.

This state- of- the- art facilities caters to the growing demand of manufacturing a large

spectrum of APIS.

Hetero's production muscle stems from its endeavors to install plant, equipment, systems

and personnel that portray the best in the Indian pharmaceutical industry. Professional

teams equipped with cutting-edge technology come together in developing,

commercializing and delivering latest Intermediate and Active Pharmaceutical

Ingredients across the globe.

50

Hetero's state-of-the-art plant, which conforms to stringent CGMP guidelines, facilitates

pilot and large scale production. This has enabled it to deliver a wide range of APIs of

international standard and intermediate chemicals for diverse healthcare applications.

RESEARCH AND DEVELOPMENT

Hetero’s emphasis has always been on Research and Development. The emphasis was to

ensure that the processes being adopted for the products are cost effective, safe to handle

and with optimum advantage in terms of yield and quality.

Having laid solid foundation towards the end Hetero’s R&D approach has also taken

cognizance of the present scenario where stringent patent regime is under

implementation. Hetero’s teams of scientists have been and are involved in developing

non-infringing processes for its products. With its ability to explore new heights and

achieve the best, Hetero has been able to file patents for several of its processes.

From an organization, which was concentrating on developing processes for API’s

Hetero, has now a full-fledged R&D Facility for formulation development.

51

STRENGHTS:

Strong emphasis on Research and Development.

Ability to develop processes for a large range of therapeutic Categories.

Ability to orient and adapt to the changing facets of Industry, particularly in terms

of Regulations, Intellectual property and Manufacturing Capabilities.

Cohesive team of Skilled Professionals in all Wings related to Research,

Manufacture and Marketing.

Strong Customer base and market Presence.

A Strong Commitment towards the society to provide timely support by providing

life Saving drugs at relatively low costs, Short Span of time.

52

CHAPTER – 4

DATA ANALYSIS

AND

INTERPRETATION

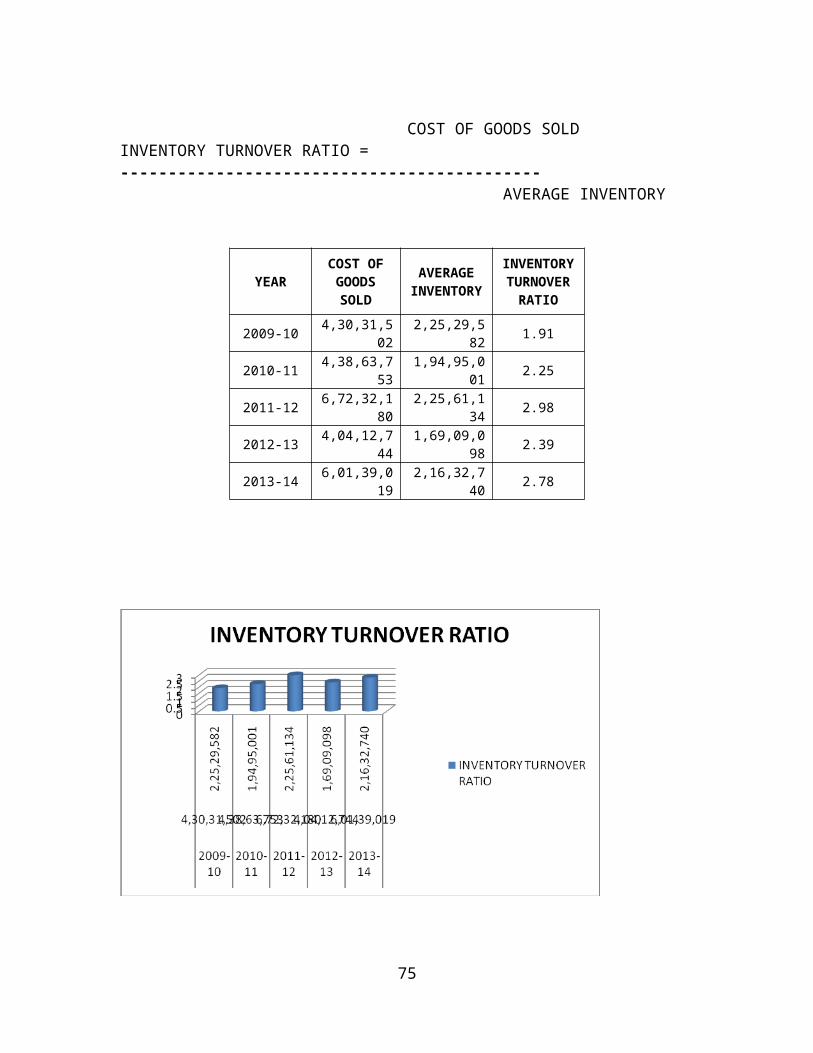

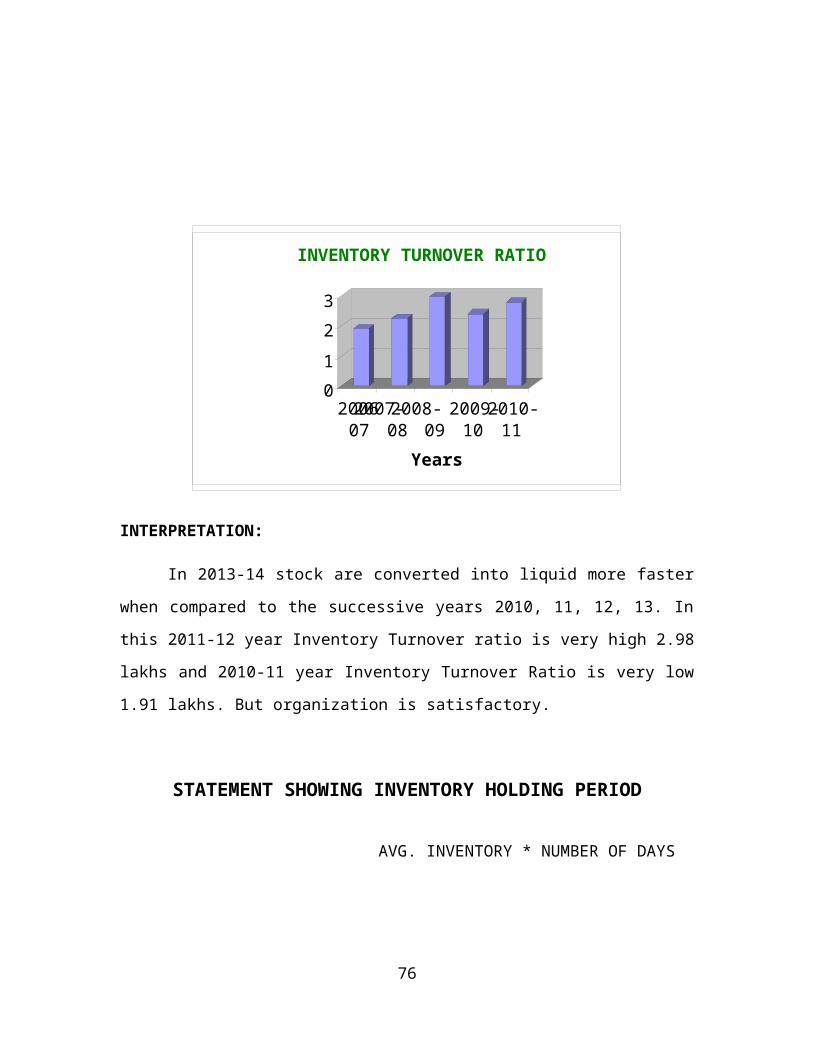

STATEMENT SHOWING INVENTORY TURNOVER RATIO

COST OF GOODS SOLD

53

INVENTORY TURNOVER RATIO = -------------------------------------------- AVERAGE INVENTORY

YEARCOST OF GOODS SOLD

AVERAGE INVENTORY

INVENTORY TURNOVER

RATIO

2009-10 4,30,31,502 2,25,29,582 1.91

2010-11 4,38,63,753 1,94,95,001 2.25

2011-12 6,72,32,180 2,25,61,134 2.98

2012-13 4,04,12,744 1,69,09,098 2.39

2013-14 6,01,39,019 2,16,32,740 2.78

54

INTERPRETATION:

In 2013-14 stock are converted into liquid more faster when compared to the

successive years 2010, 11, 12, 13. In this 2011-12 year Inventory Turnover ratio is very

high 2.98 lakhs and 2010-11 year Inventory Turnover Ratio is very low 1.91 lakhs. But

organization is satisfactory.

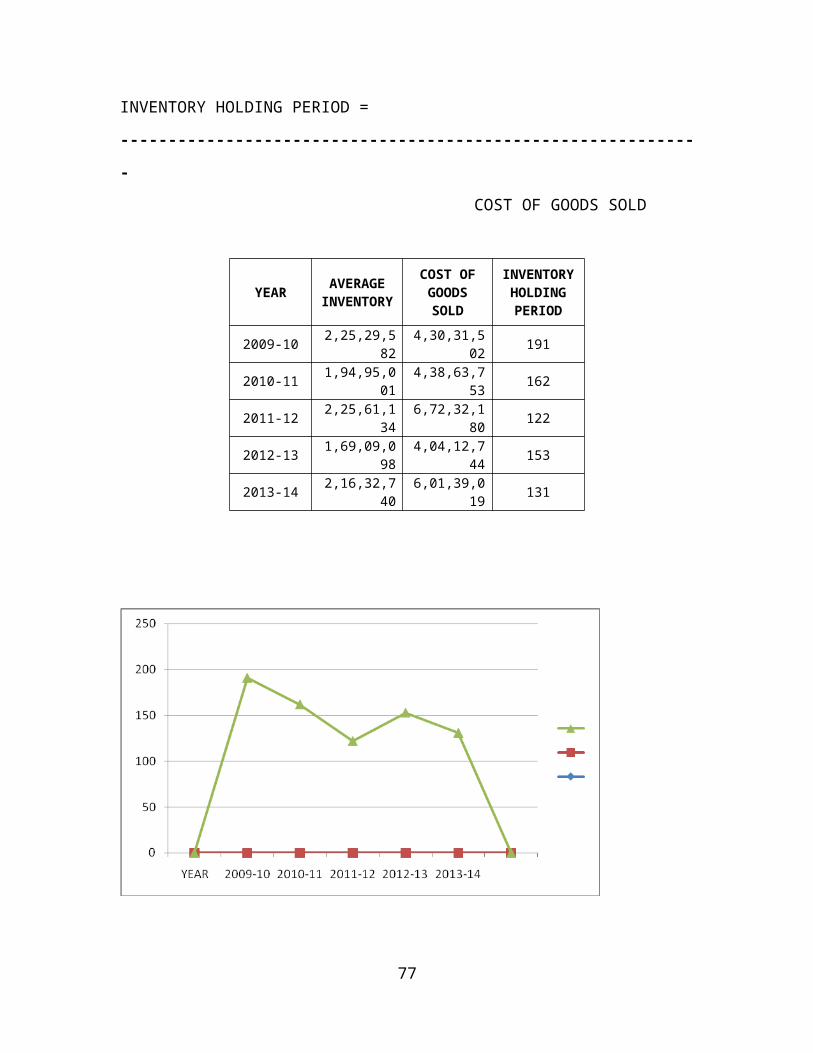

STATEMENT SHOWING INVENTORY HOLDING PERIOD

AVG. INVENTORY * NUMBER OF DAYS

INVENTORY HOLDING PERIOD = -------------------------------------------------------------

COST OF GOODS SOLD

YEARAVERAGE

INVENTORY

COST OF GOODS SOLD

INVENTORY HOLDING PERIOD

2009-10 2,25,29,582 4,30,31,502 191

2010-11 1,94,95,001 4,38,63,753 162

2011-12 2,25,61,134 6,72,32,180 122

2012-13 1,69,09,098 4,04,12,744 153

2013-14 2,16,32,740 6,01,39,019 131

55

0

1

2

3

200607

2007-08

2008-09

2009-10

2010-11

Years

INVENTORY TURNOVER RATIO

INTERPRETATION:

In 2012-13 the Inventory Conversion Period is less when compared to its

successive year 2011-12. In 2011-12 the inventory conversion period has tremendously

increased due to the problems in clearing stock. In 2006-07 holding period has decreased

to 162 days when compared to its 2009-10 holding period. Compared to 2010-11 holding

period 2010-11 holding period decreased to 122 days.

ECONOMIC ORDER QUANTITY

Suppose the ordering cost per order ‘O’ is fixed. Total order costs will be number of

orders during the year multiply by ordering cost per order. If ‘A’ represents the total

annual requirements and ‘Q’ represents the order size, the number of orders will the

‘A/Q’ and the total order costs will be

56

AO

Total Ordering Cost = --------- -------------- (1)

Q

Where,

A = Annual Requirements,

O = Ordering Costs,

Q = Order Size,

C = Carrying Costs per Unit.

Let us further assume that Carrying Costs per unit ‘C’ is constant. The total carrying costs

will be the product of the average material units and the carrying costs per unit. If ‘Q’ is

the order size and the usage is assumed to be steady, the average material will be

Q

Average Material = --------- -------------- (2)

2

QC

Average Material = --------- -------------- (3)

2

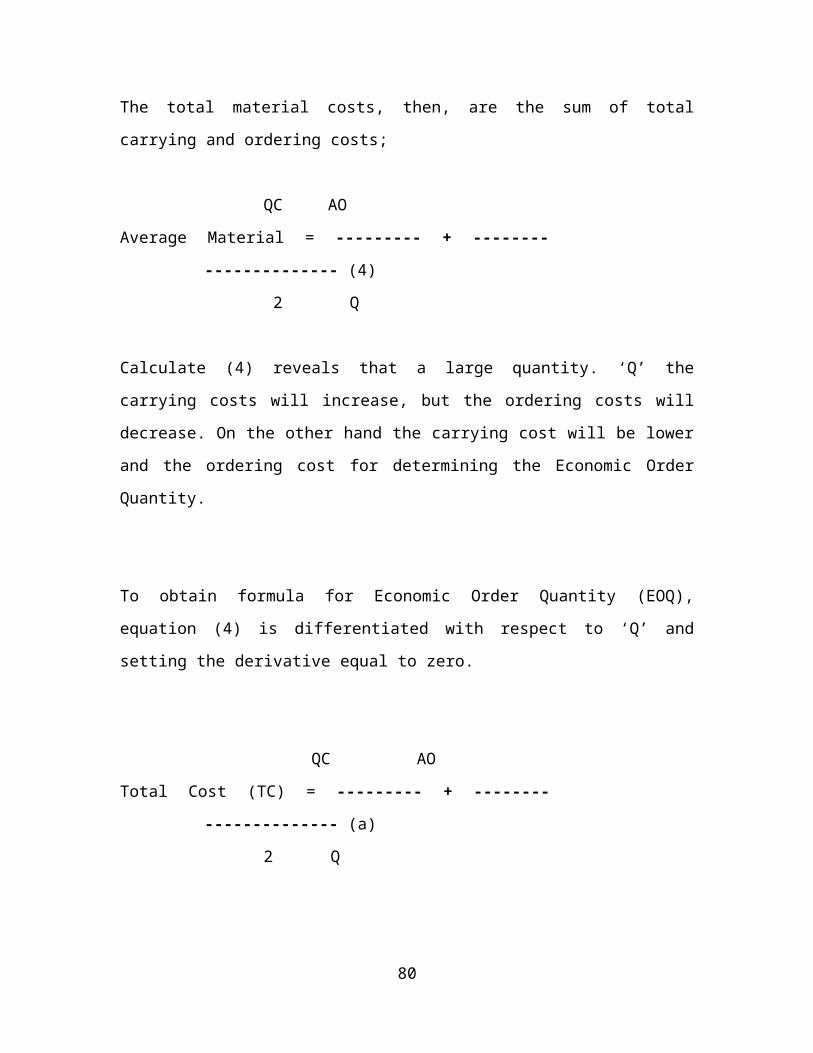

The total material costs, then, are the sum of total carrying and ordering costs;

QC AO

Average Material = --------- + -------- -------------- (4)

2 Q

57

Calculate (4) reveals that a large quantity. ‘Q’ the carrying costs will increase, but the

ordering costs will decrease. On the other hand the carrying cost will be lower and the

ordering cost for determining the Economic Order Quantity.

To obtain formula for Economic Order Quantity (EOQ), equation (4) is differentiated

with respect to ‘Q’ and setting the derivative equal to zero.

QC AO

Total Cost (TC) = --------- + -------- -------------- (a)

2 Q

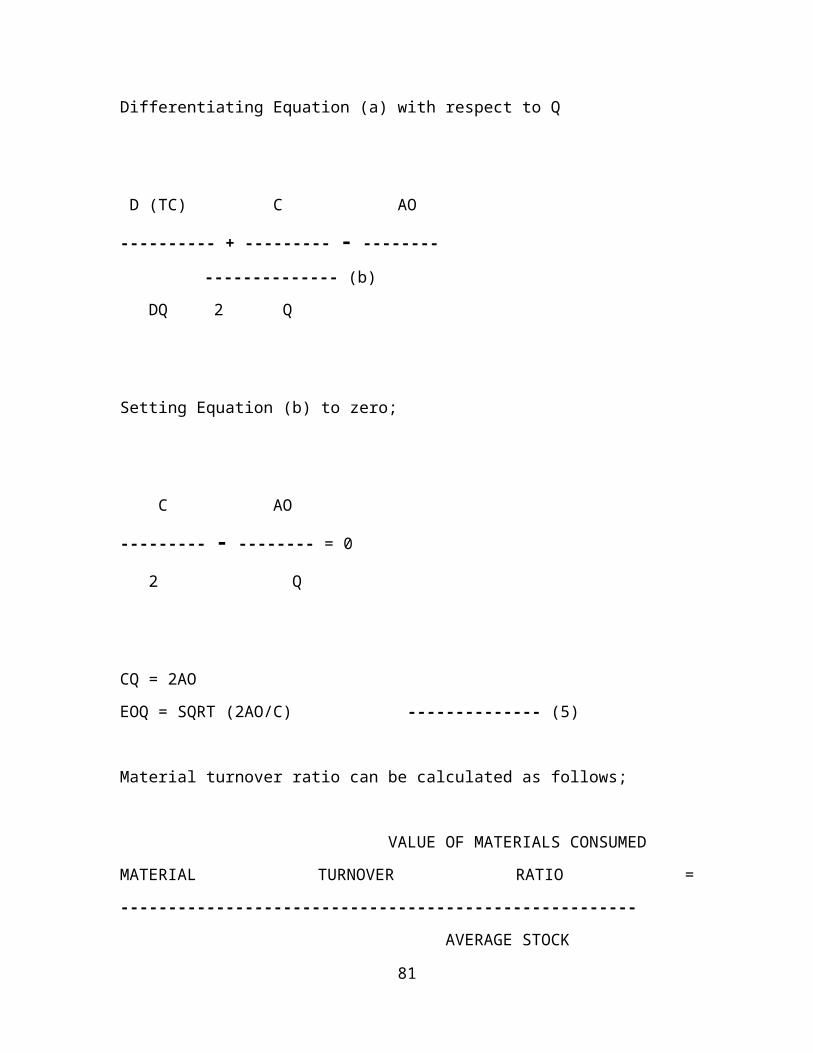

Differentiating Equation (a) with respect to Q

D (TC) C AO

---------- + --------- - -------- -------------- (b)

DQ 2 Q

Setting Equation (b) to zero;

C AO

--------- - -------- = 0

2 Q

58

CQ = 2AO

EOQ = SQRT (2AO/C) -------------- (5)

Material turnover ratio can be calculated as follows;

VALUE OF MATERIALS CONSUMED

MATERIAL TURNOVER RATIO = ------------------------------------------------------

AVERAGE STOCK

Where,

Maximum Level + Minimum Level

Average Stock = ---------------------------------------------------

2

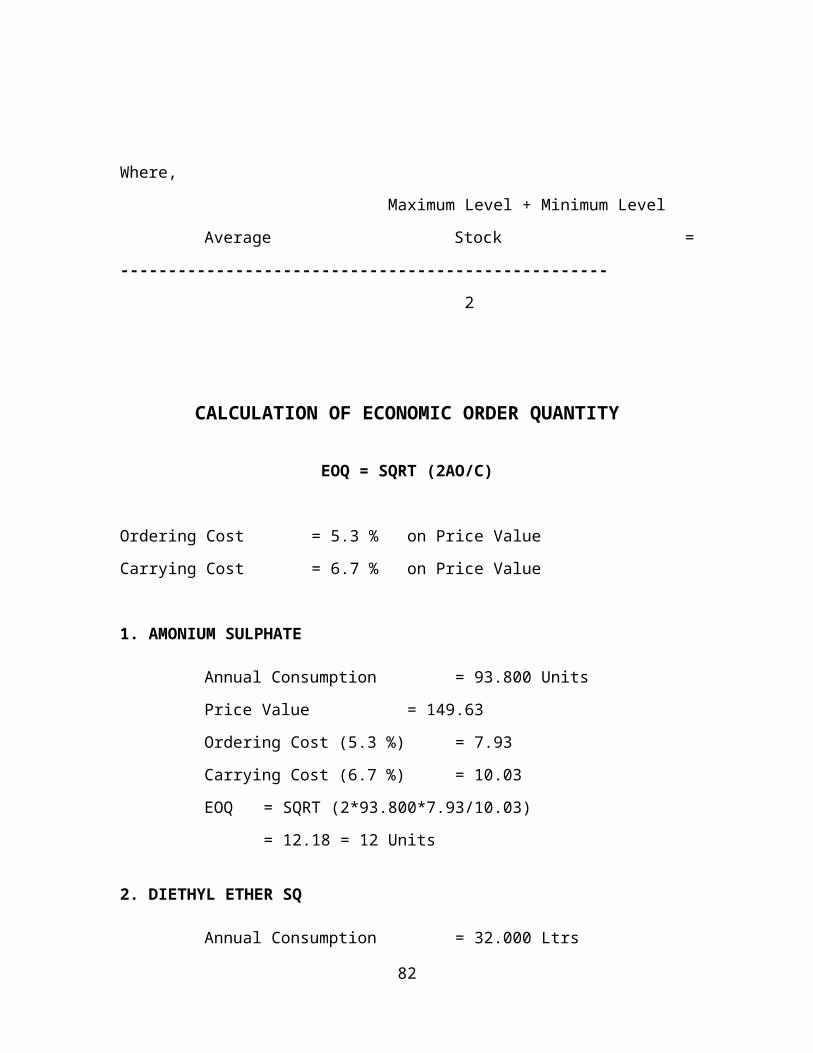

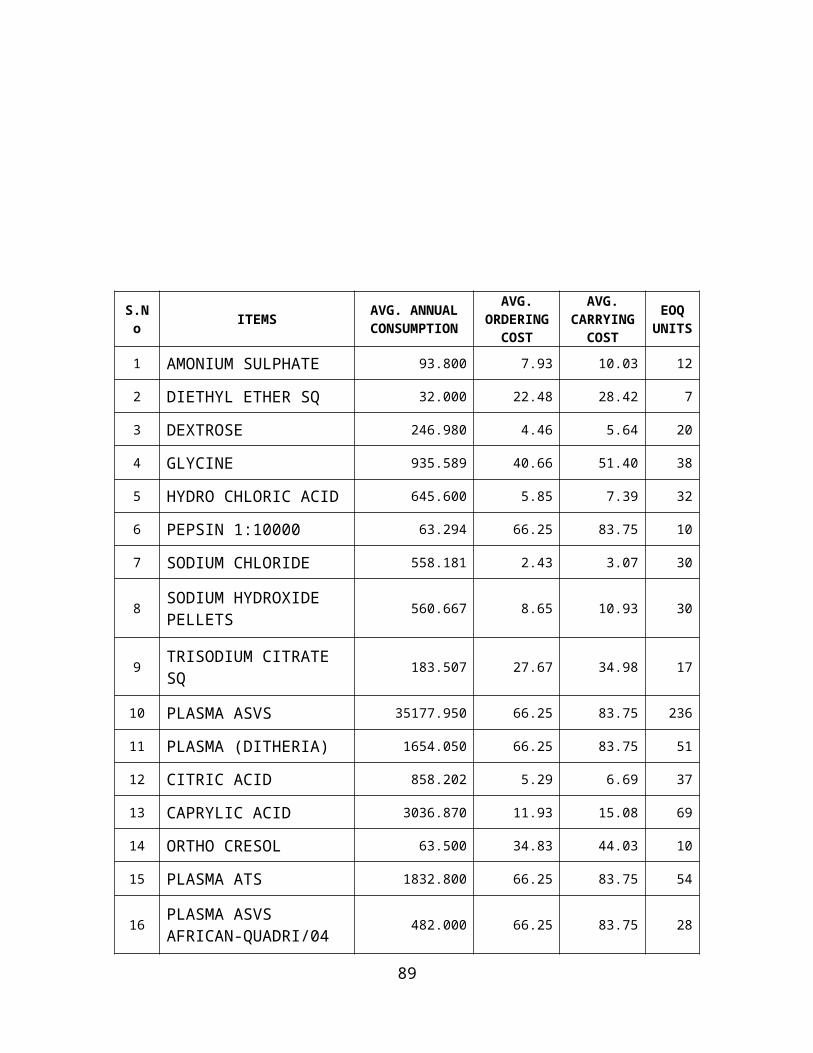

CALCULATION OF ECONOMIC ORDER QUANTITY

EOQ = SQRT (2AO/C)

Ordering Cost = 5.3 % on Price Value

Carrying Cost = 6.7 % on Price Value

1. AMONIUM SULPHATE

Annual Consumption = 93.800 Units

Price Value = 149.63

Ordering Cost (5.3 %) = 7.93

Carrying Cost (6.7 %) = 10.03

EOQ = SQRT (2*93.800*7.93/10.03)

= 12.18 = 12 Units

59

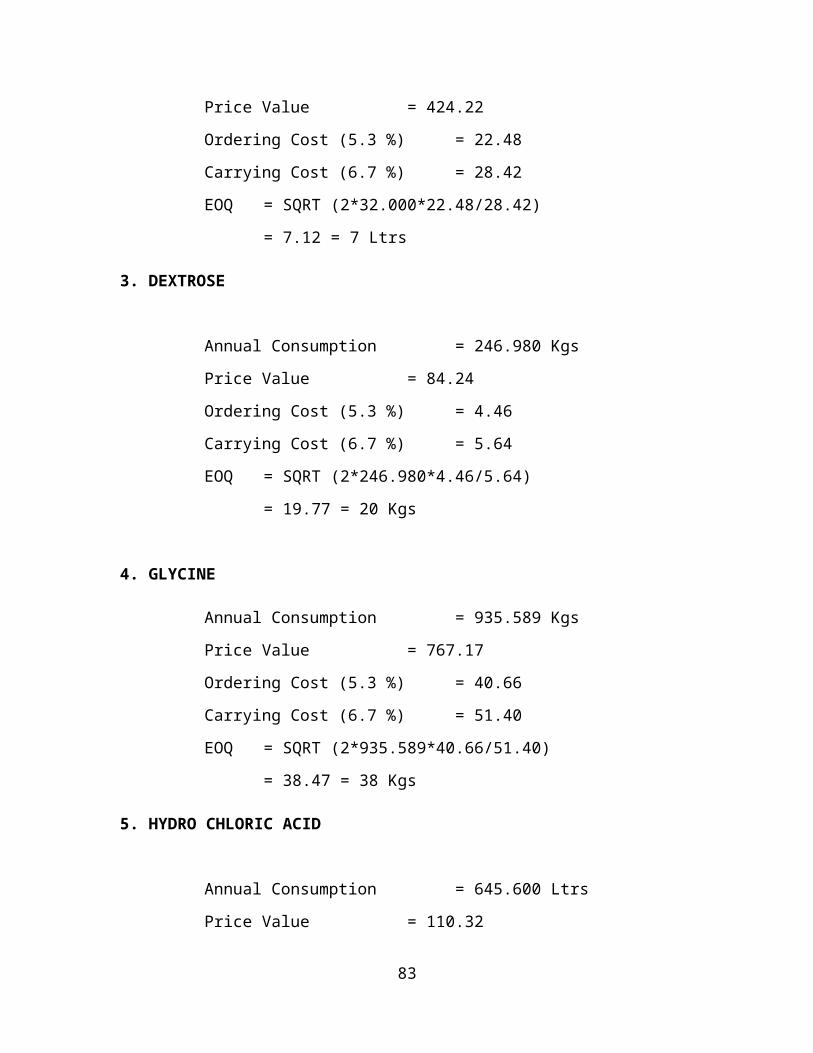

2. DIETHYL ETHER SQ

Annual Consumption = 32.000 Ltrs

Price Value = 424.22

Ordering Cost (5.3 %) = 22.48

Carrying Cost (6.7 %) = 28.42

EOQ = SQRT (2*32.000*22.48/28.42)

= 7.12 = 7 Ltrs

3. DEXTROSE

Annual Consumption = 246.980 Kgs

Price Value = 84.24

Ordering Cost (5.3 %) = 4.46

Carrying Cost (6.7 %) = 5.64

EOQ = SQRT (2*246.980*4.46/5.64)

= 19.77 = 20 Kgs

4. GLYCINE

Annual Consumption = 935.589 Kgs

Price Value = 767.17

Ordering Cost (5.3 %) = 40.66

Carrying Cost (6.7 %) = 51.40

EOQ = SQRT (2*935.589*40.66/51.40)

= 38.47 = 38 Kgs

5. HYDRO CHLORIC ACID

Annual Consumption = 645.600 Ltrs

Price Value = 110.32

Ordering Cost (5.3 %) = 5.85

Carrying Cost (6.7 %) = 7.39

EOQ = SQRT (2*645.600*5.85/7.39)

60

= 31.96 = 32 Ltrs

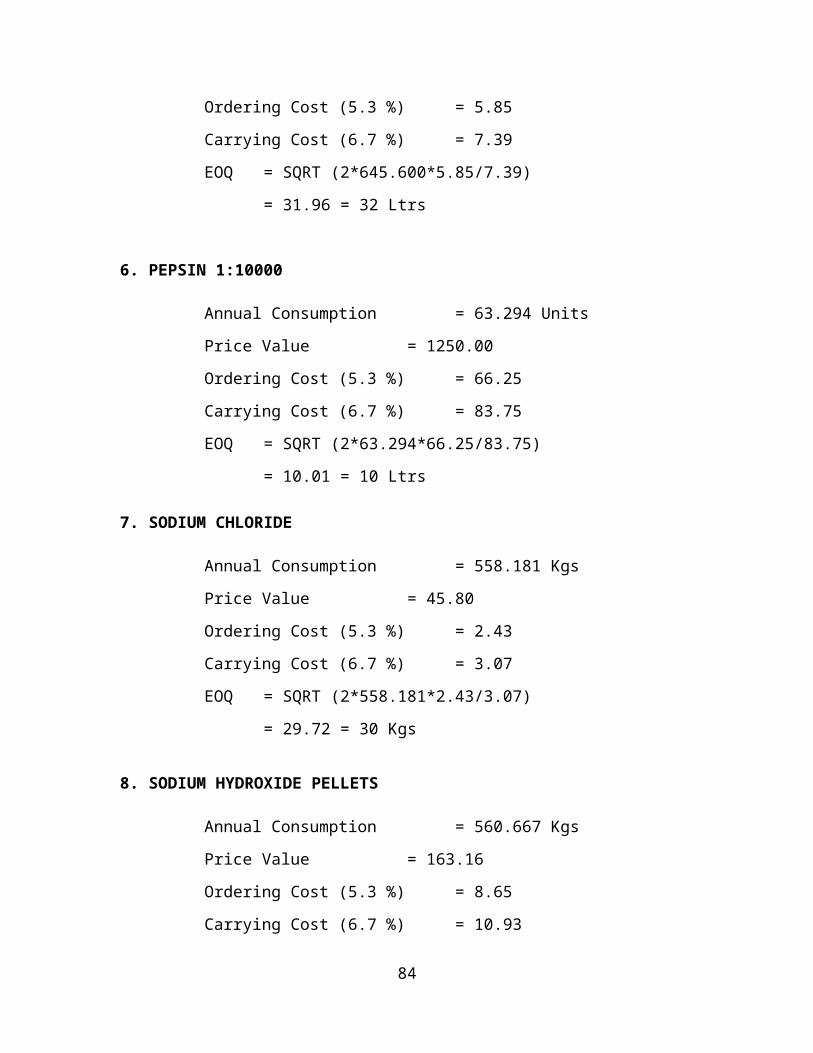

6. PEPSIN 1:10000

Annual Consumption = 63.294 Units

Price Value = 1250.00

Ordering Cost (5.3 %) = 66.25

Carrying Cost (6.7 %) = 83.75

EOQ = SQRT (2*63.294*66.25/83.75)

= 10.01 = 10 Ltrs

7. SODIUM CHLORIDE

Annual Consumption = 558.181 Kgs

Price Value = 45.80

Ordering Cost (5.3 %) = 2.43

Carrying Cost (6.7 %) = 3.07

EOQ = SQRT (2*558.181*2.43/3.07)

= 29.72 = 30 Kgs

8. SODIUM HYDROXIDE PELLETS

Annual Consumption = 560.667 Kgs

Price Value = 163.16

Ordering Cost (5.3 %) = 8.65

Carrying Cost (6.7 %) = 10.93

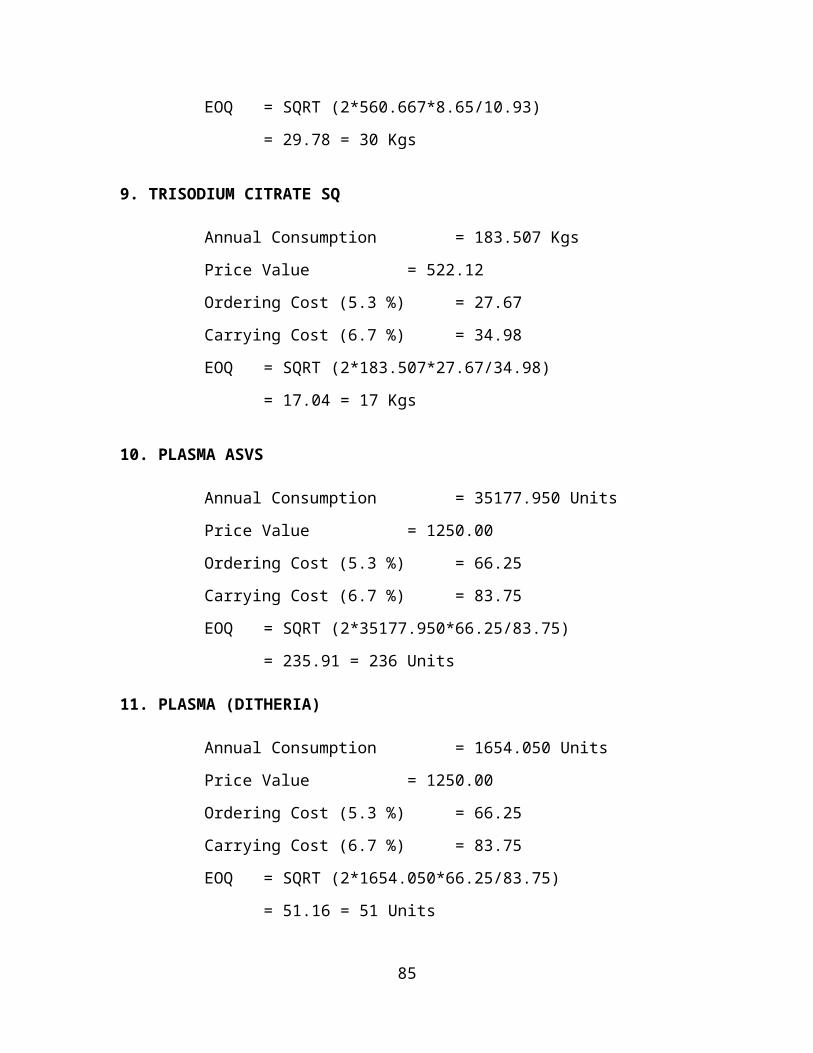

EOQ = SQRT (2*560.667*8.65/10.93)

= 29.78 = 30 Kgs

9. TRISODIUM CITRATE SQ

Annual Consumption = 183.507 Kgs

Price Value = 522.12

Ordering Cost (5.3 %) = 27.67

Carrying Cost (6.7 %) = 34.98

61

EOQ = SQRT (2*183.507*27.67/34.98)

= 17.04 = 17 Kgs

10. PLASMA ASVS

Annual Consumption = 35177.950 Units

Price Value = 1250.00

Ordering Cost (5.3 %) = 66.25

Carrying Cost (6.7 %) = 83.75

EOQ = SQRT (2*35177.950*66.25/83.75)

= 235.91 = 236 Units

11. PLASMA (DITHERIA)

Annual Consumption = 1654.050 Units

Price Value = 1250.00

Ordering Cost (5.3 %) = 66.25

Carrying Cost (6.7 %) = 83.75

EOQ = SQRT (2*1654.050*66.25/83.75)

= 51.16 = 51 Units

12. CITRIC ACID

Annual Consumption = 858.202 Kgs

Price Value = 99.84

Ordering Cost (5.3 %) = 5.29

Carrying Cost (6.7 %) = 6.69

EOQ = SQRT (2*858.202*5.29/6.69)

= 36.85 = 37 Kgs

13. CAPRYLIC ACID

Annual Consumption = 3036.870 Kgs

Price Value = 225.01

Ordering Cost (5.3 %) = 11.93

Carrying Cost (6.7 %) = 15.08

62

EOQ = SQRT (2*3036.870*11.93/15.08)

= 69.32 = 69 Kgs

14. ORTHO CRESOL

Annual Consumption = 63.500 Ltrs

Price Value = 657.23

Ordering Cost (5.3 %) = 34.83

Carrying Cost (6.7 %) = 44.03

EOQ = SQRT (2*63.500*34.83/44.03)

= 10.02 = 10 Ltrs

15. PLASMA ATS

Annual Consumption = 1832.800 Units

Price Value = 1250.00

Ordering Cost (5.3 %) = 66.25

Carrying Cost (6.7 %) = 83.75

EOQ = SQRT (2*1832.800*66.25/83.75)

= 53.85 = 54 Units

16. PLASMA ASVS AFRICAN-QUADRI/04

Annual Consumption = 482.000 Units

Price Value = 1250.00

Ordering Cost (5.3 %) = 66.25

Carrying Cost (6.7 %) = 83.75

EOQ = SQRT (2*482.000*66.25/83.75)

= 27.61 = 28 Units

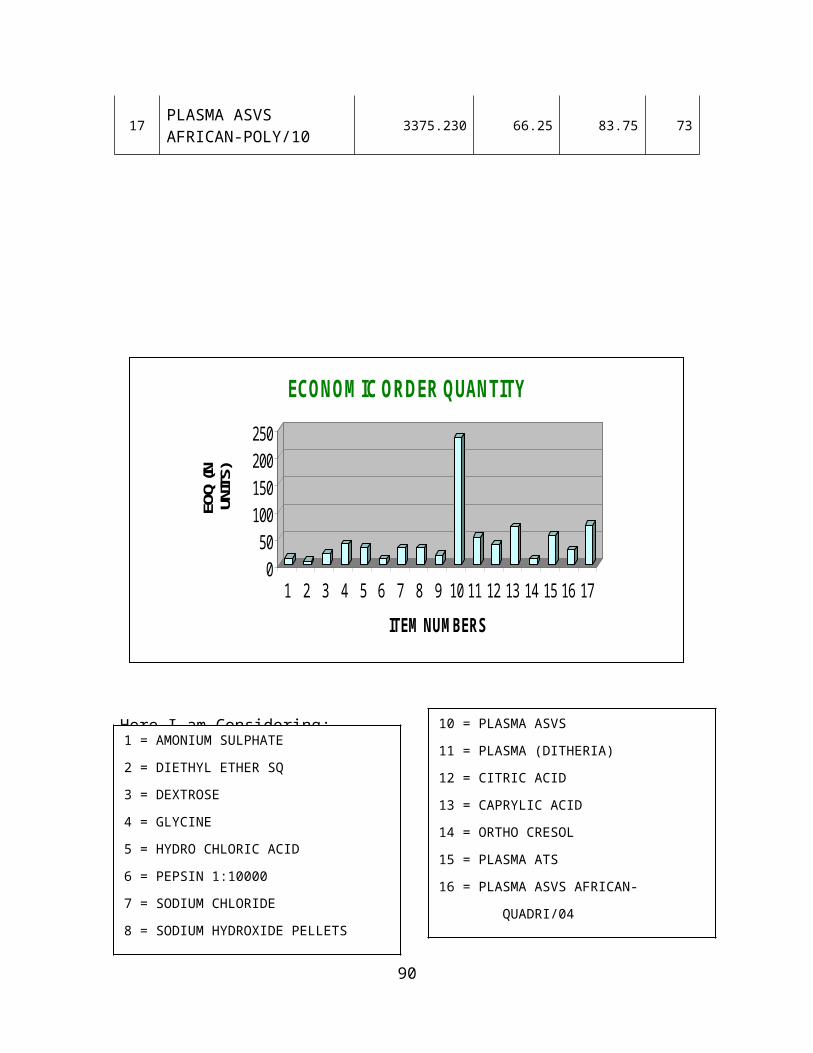

17. PLASMA ASVS AFRICAN-POLY/10

Annual Consumption = 3375.230 Units

Price Value = 1250.00

Ordering Cost (5.3 %) = 66.25

Carrying Cost (6.7 %) = 83.75

63

EOQ = SQRT (2*3375.230*66.25/83.75)

= 73.07 = 73 Units

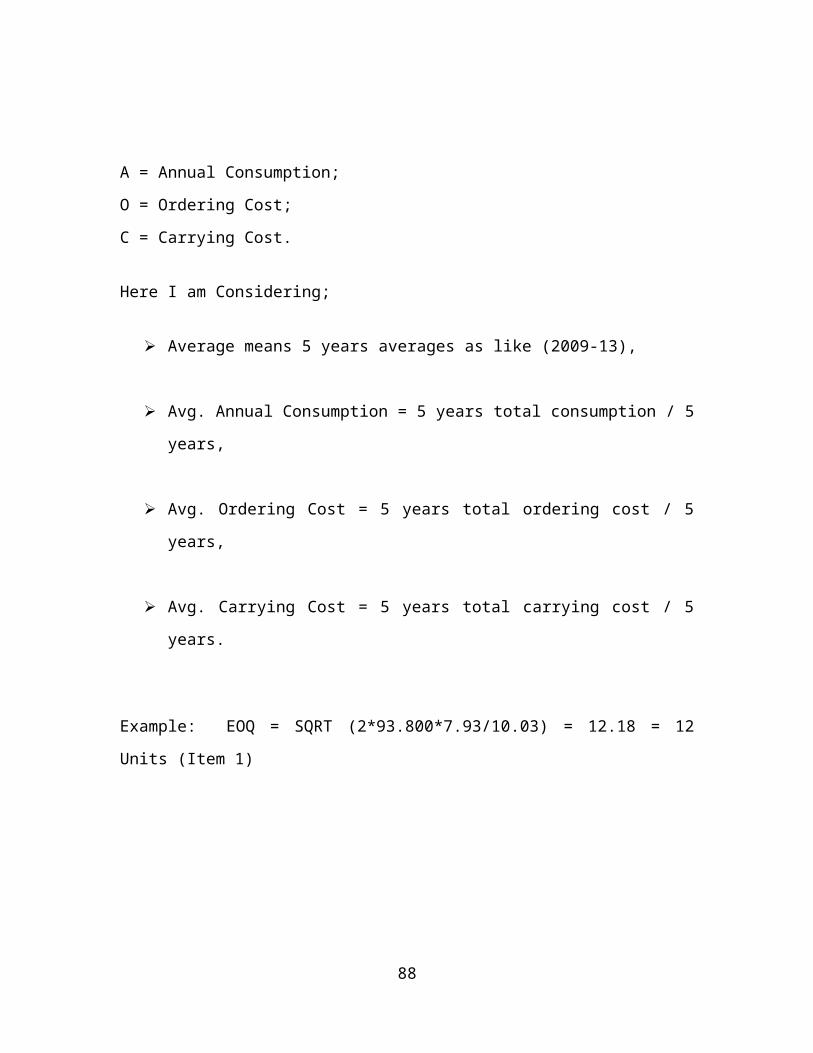

STATEMENT SHOWING ECONOMIC ORDER QUANTITY

EOQ SQRT (2AO/C)

A = Annual Consumption;

O = Ordering Cost;

C = Carrying Cost.

Here I am Considering;

Average means 5 years averages as like (2009-13),

Avg. Annual Consumption = 5 years total consumption / 5 years,

Avg. Ordering Cost = 5 years total ordering cost / 5 years,

Avg. Carrying Cost = 5 years total carrying cost / 5 years.

Example: EOQ = SQRT (2*93.800*7.93/10.03) = 12.18 = 12 Units (Item 1)

64

S.No ITEMSAVG. ANNUAL

CONSUMPTION

AVG. ORDERING

COST

AVG. CARRYING

COST

EOQ UNITS

1 AMONIUM SULPHATE 93.800 7.93 10.03 12

2 DIETHYL ETHER SQ 32.000 22.48 28.42 7

3 DEXTROSE 246.980 4.46 5.64 20

4 GLYCINE 935.589 40.66 51.40 38

5 HYDRO CHLORIC ACID 645.600 5.85 7.39 32

6 PEPSIN 1:10000 63.294 66.25 83.75 10

7 SODIUM CHLORIDE 558.181 2.43 3.07 30

8SODIUM HYDROXIDE PELLETS

560.667 8.65 10.93 30

9TRISODIUM CITRATE SQ

183.507 27.67 34.98 17

10 PLASMA ASVS 35177.950 66.25 83.75 236

11 PLASMA (DITHERIA) 1654.050 66.25 83.75 51

12 CITRIC ACID 858.202 5.29 6.69 37

13 CAPRYLIC ACID 3036.870 11.93 15.08 69

14 ORTHO CRESOL 63.500 34.83 44.03 10

15 PLASMA ATS 1832.800 66.25 83.75 54

16PLASMA ASVS AFRICAN-QUADRI/04

482.000 66.25 83.75 28

17PLASMA ASVS AFRICAN-POLY/10

3375.230 66.25 83.75 73

65

050

100150200250

EOQ

(IN

UNIT

S)

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

ITEM NUMBERS

ECONOMIC ORDER QUANTITY

Here I am Considering;

INTERPRETATION:

66

1 = AMONIUM SULPHATE

2 = DIETHYL ETHER SQ

3 = DEXTROSE

4 = GLYCINE

5 = HYDRO CHLORIC ACID

6 = PEPSIN 1:10000

7 = SODIUM CHLORIDE

8 = SODIUM HYDROXIDE PELLETS

9 = TRISODIUM CITRATE SQ

10 = PLASMA ASVS

11 = PLASMA (DITHERIA)

12 = CITRIC ACID

13 = CAPRYLIC ACID

14 = ORTHO CRESOL

15 = PLASMA ATS

16 = PLASMA ASVS AFRICAN-

QUADRI/04

17 = PLASMA ASVS AFRICAN-

POLY/10

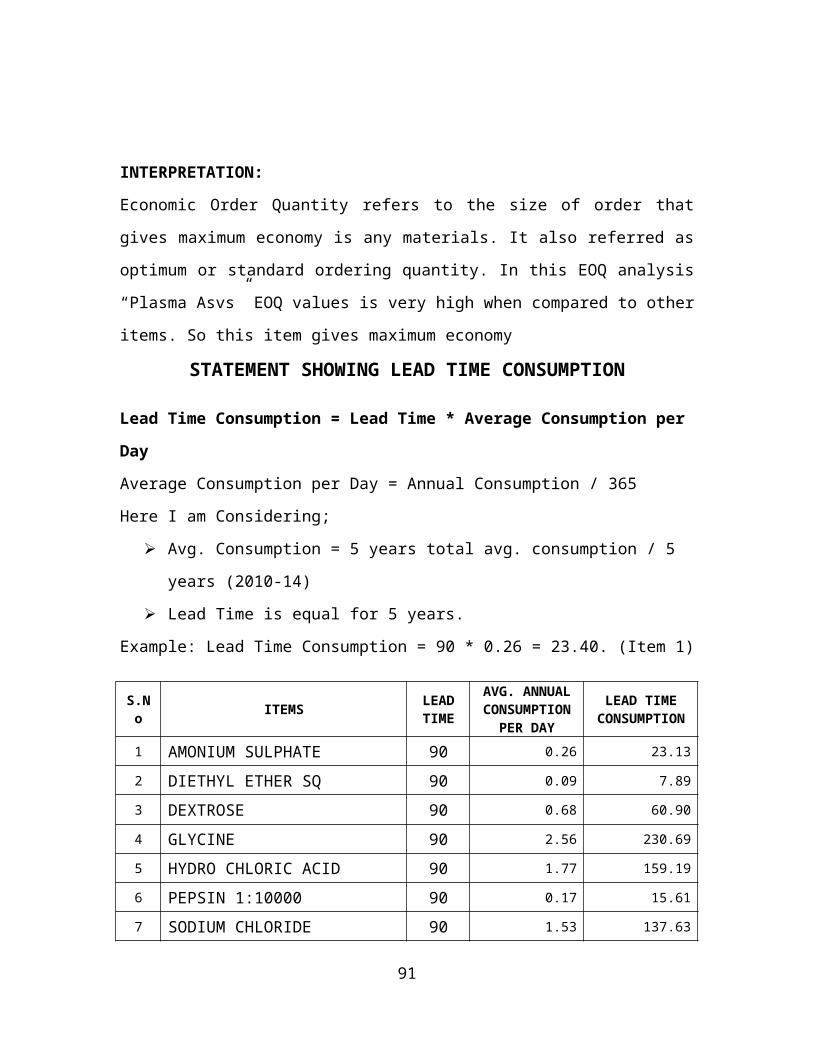

Economic Order Quantity refers to the size of order that gives maximum economy is any

materials. It also referred as optimum or standard ordering quantity. In this EOQ analysis

“Plasma Asvs” EOQ values is very high when compared to other items. So this item

gives maximum economy

STATEMENT SHOWING LEAD TIME CONSUMPTION

Lead Time Consumption = Lead Time * Average Consumption per Day

Average Consumption per Day = Annual Consumption / 365

Here I am Considering;

Avg. Consumption = 5 years total avg. consumption / 5 years (2010-14)

Lead Time is equal for 5 years.

Example: Lead Time Consumption = 90 * 0.26 = 23.40. (Item 1)

S.No

ITEMSLEAD TIME

AVG. ANNUAL CONSUMPTION

PER DAY

LEAD TIME CONSUMPTION

1 AMONIUM SULPHATE 90 0.26 23.13

2 DIETHYL ETHER SQ 90 0.09 7.89

3 DEXTROSE 90 0.68 60.90

4 GLYCINE 90 2.56 230.69

5 HYDRO CHLORIC ACID 90 1.77 159.19

6 PEPSIN 1:10000 90 0.17 15.61

7 SODIUM CHLORIDE 90 1.53 137.63

8SODIUM HYDROXIDE PELLETS

90 1.54 138.25

9 TRISODIUM CITRATE SQ 90 0.50 45.25

10 PLASMA ASVS 90 96.38 8674.02

11 PLASMA (DITHERIA) 90 4.53 407.85

12 CITRIC ACID 90 2.35 211.61

13 CAPRYLIC ACID 90 8.32 748.82

14 ORTHO CRESOL 90 0.17 15.66

15 PLASMA ATS 90 5.02 451.92

16 PLASMA ASVS AFRICAN- 90 1.32 118.85

67

QUADRI/04

17PLASMA ASVS AFRICAN-POLY/10

90 9.25 832.25

0.002000.004000.006000.008000.00

10000.00

Quan

tity

of

units

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Item Numbers

LEAD TIME CONSUMPTION

Here I am Considering;

INTERPRETATION:

Lead time is the period between placing an order for materials and actually receiving

delivery of these goods in case of raw materials. In this analysis lead time is 90 days. And

68

1 = AMONIUM SULPHATE

2 = DIETHYL ETHER SQ

3 = DEXTROSE

4 = GLYCINE

5 = HYDRO CHLORIC ACID

6 = PEPSIN 1:10000

7 = SODIUM CHLORIDE

8 = SODIUM HYDROXIDE PELLETS

9 = TRISODIUM CITRATE SQ

10 = PLASMA ASVS

11 = PLASMA (DITHERIA)

12 = CITRIC ACID

13 = CAPRYLIC ACID

14 = ORTHO CRESOL

15 = PLASMA ATS

16 = PLASMA ASVS AFRICAN-

QUADRI/04

17 = PLASMA ASVS AFRICAN-

POLY/10

“DIETHYL ETHER SQ” Items average annual consumption per day in 0.09, lead time

consumption is 7.89. It’s very low when compared to other items so tits better to produce

mote items.

STOCKABLE ITEMS PLANING SHEET OF THE COMPANY

Here I am Considering to 17 Particular Items;

Annual Avg. 5 years Consumption (2009-10 to 2013-14)

Avg. 5 years Unit Price as like (2009-10 to 2013-14)

Avg. 5 years Safety Stock.

S.NoMATERIAL

CODEITEMS

AVG. ANNUAL CONSUMPTION

UNIT PRICE

SAFETY STOCK

1 110001 AMONIUM SULPHATE 93.800 149.63 23.45

2 110002 DIETHYL ETHER SQ 32.000 424.22 8.00

3 110003 DEXTROSE 246.980 84.24 61.75

4 110006 GLYCINE 935.589 767.17 233.90

5 110007HYDRO CHLORIC ACID

645.600 110.32 161.40

6 110009 PEPSIN 1:10000 63.294 1250.00 15.82

7 110011 SODIUM CHLORIDE 558.181 45.80 139.55

8 110012SODIUM HYDROXIDE PELLETS

560.667 163.16 140.17

9 110014TRISODIUM CITRATE SQ

183.507 522.12 45.88

10 110016 PLASMA ASVS 35177.950 1250.00 8794.49

11 110017 PLASMA (DITHERIA) 1654.050 1250.00 413.51

12 110025 CITRIC ACID 858.202 99.84 214.55

13 110026 CAPRYLIC ACID 3036.870 225.01 759.22

14 110037 ORTHO CRESOL 63.500 657.23 15.88

15 110073 PLASMA ATS 1832.800 1250.00 458.20

16 110075PLASMA ASVS AFRICAN-QUADRI/04

482.000 1250.00 120.50

17 110076PLASMA ASVS AFRICAN-POLY/10

3375.230 1250.00 843.81

69

STATEMENT SHOWING RE-ORDER LEVEL

RE-ORDER LEVEL = SAFETY STOCK + LEAD TIME CONSUMPTION

Avg. Annual Safety Stock for 5 years (2010-14)

Avg. Lead Time Consumption for 5 years.

Example: 23.45 + 23.13 = 46.58. (Item 1)

S.No

ITEMS SAFETY STOCK

LEAD TIME CONSUMPTION

RE-ORDER LEVEL

1 AMONIUM SULPHATE 23.45 23.13 46.58

2 DIETHYL ETHER SQ 8.00 7.89 15.89

3 DEXTROSE 61.75 60.90 122.65

4 GLYCINE 233.90 230.69 464.59

5 HYDRO CHLORIC ACID 161.40 159.19 320.59

6 PEPSIN 1:10000 15.82 15.61 31.43

7 SODIUM CHLORIDE 139.55 137.63 277.18

8 SODIUM HYDROXIDE PELLETS 140.17 138.25 278.42

9 TRISODIUM CITRATE SQ 45.88 45.25 91.13

10 PLASMA ASVS 8794.49 8674.02 17468.51

11 PLASMA (DITHERIA) 413.51 407.85 821.36

12 CITRIC ACID 214.55 211.61 426.16

13 CAPRYLIC ACID 759.22 748.82 1508.04

14 ORTHO CRESOL 15.88 15.66 31.54

15 PLASMA ATS 458.20 451.92 910.12

16PLASMA ASVS AFRICAN-QUADRI/04 120.50 118.85 239.35

17PLASMA ASVS AFRICAN-POLY/10 843.81 832.25 1676.06

70

0.00

5000.00

10000.00

15000.00

20000.00

Quan

tity

in

units

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17

Item Numbers

RE-ORDER LEVEL

Here I am Considering;

INTERPRETATION:

Re-order point includes lead time and average usage. Re-order level means combing of

safety stock and lead time consumption should be average. Combining of this high safety

71

1 = AMONIUM SULPHATE

2 = DIETHYL ETHER SQ

3 = DEXTROSE

4 = GLYCINE

5 = HYDRO CHLORIC ACID

6 = PEPSIN 1:10000

7 = SODIUM CHLORIDE

8 = SODIUM HYDROXIDE PELLETS

9 = TRISODIUM CITRATE SQ

10 = PLASMA ASVS

11 = PLASMA (DITHERIA)

12 = CITRIC ACID

13 = CAPRYLIC ACID

14 = ORTHO CRESOL

15 = PLASMA ATS

16 = PLASMA ASVS AFRICAN-

QUADRI/04

17 = PLASMA ASVS AFRICAN-

POLY/10

stock and average lead time consumption is the best re-order level. In this analysis

“Plasma Asvs” re-order level is better when compared to other items.

STATEMENT SHOWING MAXIMUM STOCK LEVEL

MAXIMUM STOCK LEVEL = RE-ORDER LEVEL + EOQ

Example: Maximum Stock Level = 46.58 + 12 = 58.58 (Item 1)

S.No ITEMSRE-ORDER

LEVELEOQ

UNITS

MAXIMUM STOCK LEVEL

1 AMONIUM SULPHATE 46.58 12 58.58

2 DIETHYL ETHER SQ 15.89 7 22.89

3 DEXTROSE 122.65 20 142.65

4 GLYCINE 464.59 38 502.59

5 HYDRO CHLORIC ACID 320.59 32 352.59

6 PEPSIN 1:10000 31.43 10 41.43

7 SODIUM CHLORIDE 277.18 30 307.18

8 SODIUM HYDROXIDE PELLETS 278.42 30 308.42

9 TRISODIUM CITRATE SQ 91.13 17 108.13

10 PLASMA ASVS 17468.51 236 17704.51

11 PLASMA (DITHERIA) 821.36 51 872.36

12 CITRIC ACID 426.16 37 463.16

13 CAPRYLIC ACID 1508.04 69 1577.04