Embed Size (px)

Citation preview

1

Inventory Cost Accounting Tips and Tricks

Nick Bergamo, Senior Manager Linda Pei, Senior Manager

2

Disclaimer

The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication of this information is not intended to create, and receipt does not constitute, a legal relationship, including, but not limited to, an accountant-client relationship. Although these materials may have been prepared by professionals, they should not be used as a substitute for professional services. If legal, accounting, or other professional advice is required, the services of a professional should be sought.

3

4

Presenters

Nick Bergamo Senior Manager [email protected] 949-221-4022 Linda Pei Senior Manager [email protected] 818-577-1885

Objectives

Session Objectives: • Understand the principles, procedures and

terminologies of inventory management and manufacturing cost accounting

• Understand the flow and accounting of inventory costs

• Understand various costing methodologies • Describe basic controls around product costing • Benefits and pitfalls of costing techniques

Agenda

• Overview – Inventory and Cost Accounting • Types of Inventory – Manufacturing • Product Cost Elements • Types of Cost Systems • Product Costing • Standard Costing • Inventory Controls

Overview: Inventory and Cost Accounting • Inventory is defined as (FASB ASC 330-10):

– Assets held for sale in the ordinary course of business (“FGs”),

– In the process of production for sale (“WIP”), or – To be consumed in the production of goods and services

to be available for sale (“RMs”). • Typically excludes long-term assets subject to

depreciation accounting (including fixed assets held for sale).

• The primary basis of accounting is cost.

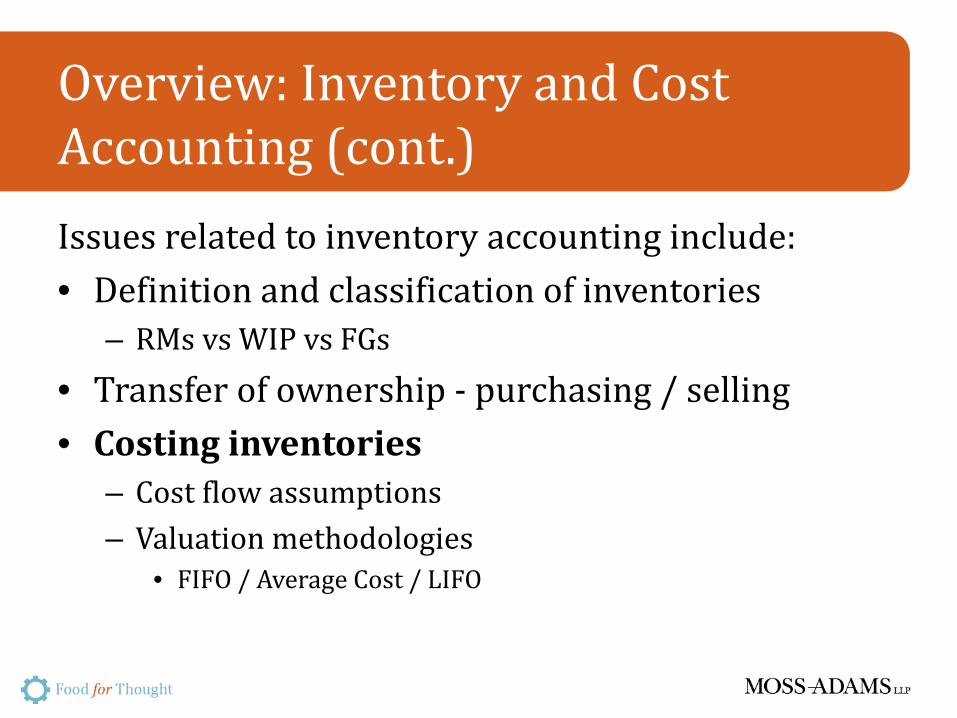

Overview: Inventory and Cost Accounting (cont.) Issues related to inventory accounting include: • Definition and classification of inventories

– RMs vs WIP vs FGs • Transfer of ownership - purchasing / selling • Costing inventories

– Cost flow assumptions – Valuation methodologies

• FIFO / Average Cost / LIFO

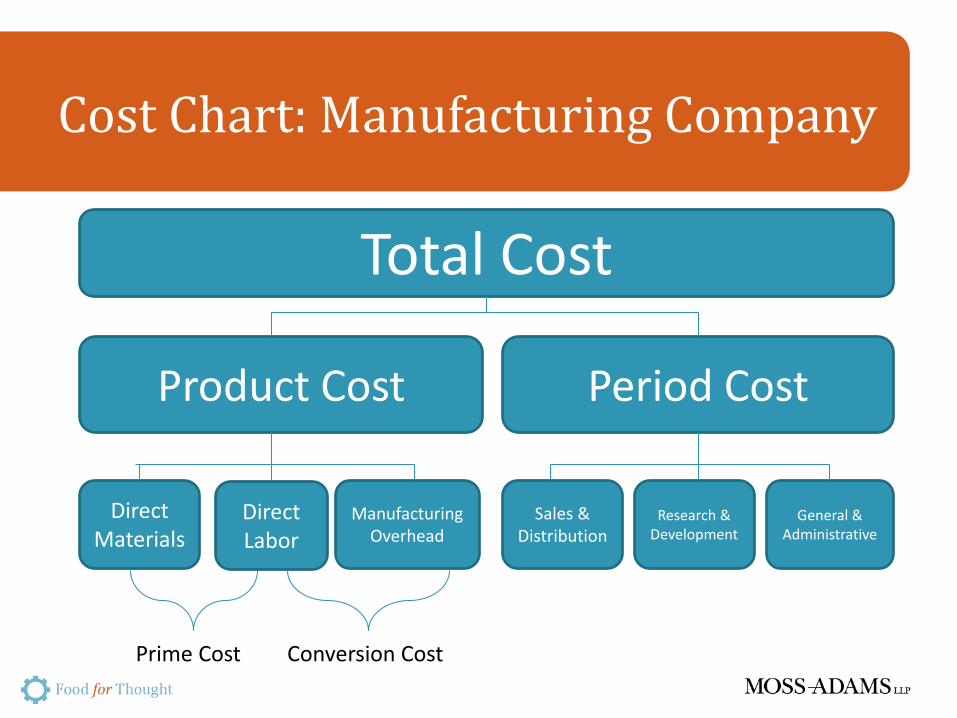

Cost Chart: Manufacturing Company

Total Cost

Product Cost Period Cost

Direct Materials

Direct Labor

Manufacturing Overhead

Sales & Distribution

Research & Development

General & Administrative

Prime Cost Conversion Cost

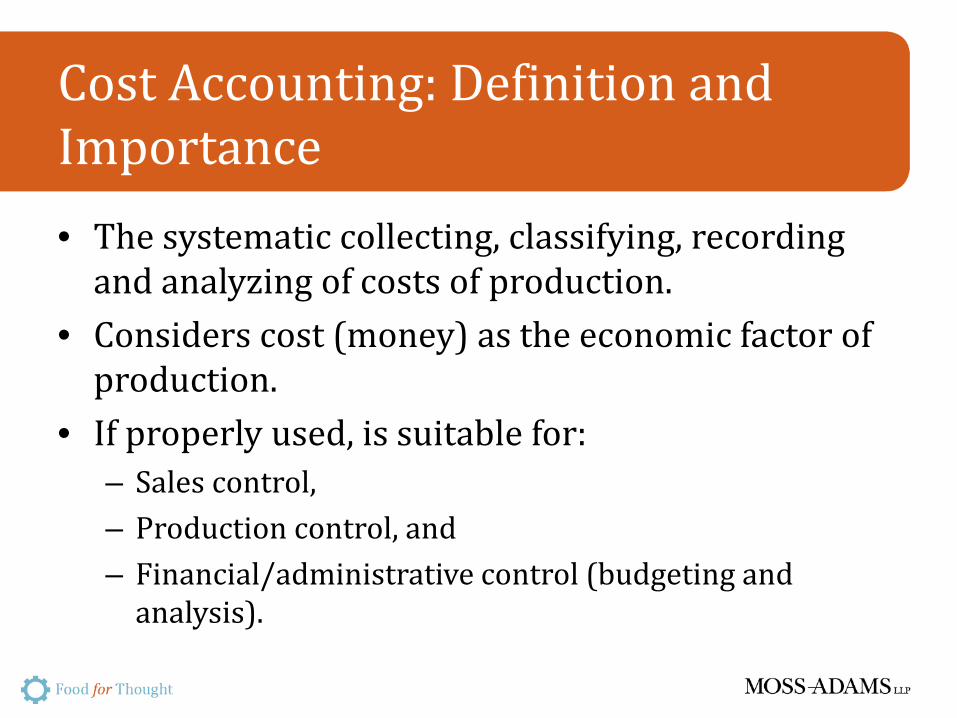

Cost Accounting: Definition and Importance • The systematic collecting, classifying, recording

and analyzing of costs of production. • Considers cost (money) as the economic factor of

production. • If properly used, is suitable for:

– Sales control, – Production control, and – Financial/administrative control (budgeting and

analysis).

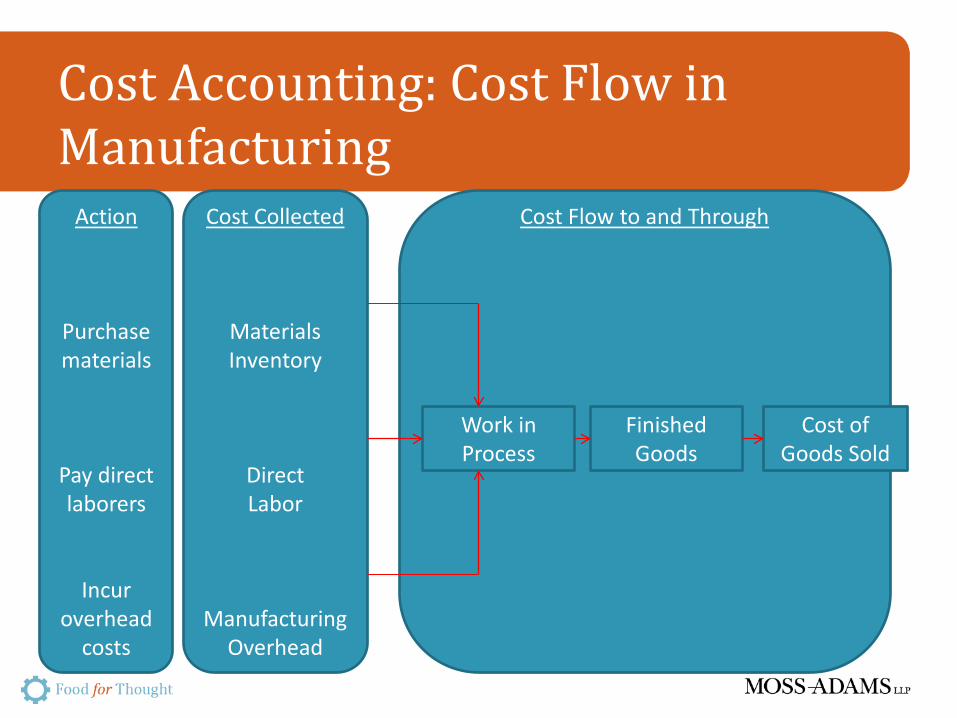

Cost Accounting: Cost Flow in Manufacturing

Action

Purchase materials

Pay direct laborers

Incur overhead

costs

Cost Collected

Materials Inventory

Direct Labor

Manufacturing Overhead

Cost Flow to and Through

Work in Process

Finished Goods

Cost of Goods Sold

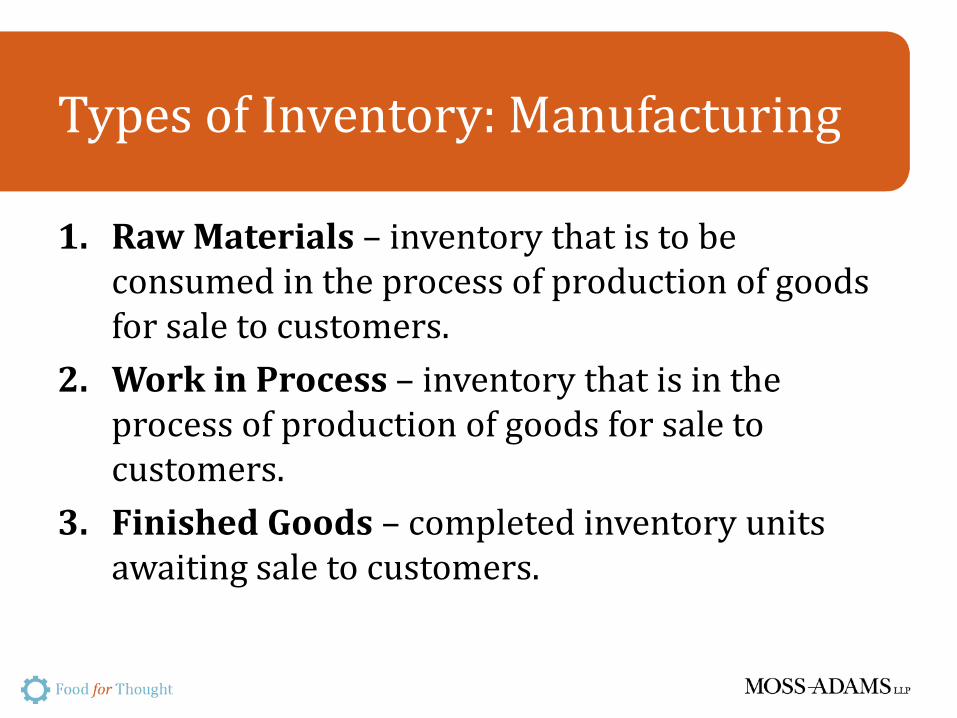

Types of Inventory: Manufacturing

1. Raw Materials – inventory that is to be consumed in the process of production of goods for sale to customers.

2. Work in Process – inventory that is in the process of production of goods for sale to customers.

3. Finished Goods – completed inventory units awaiting sale to customers.

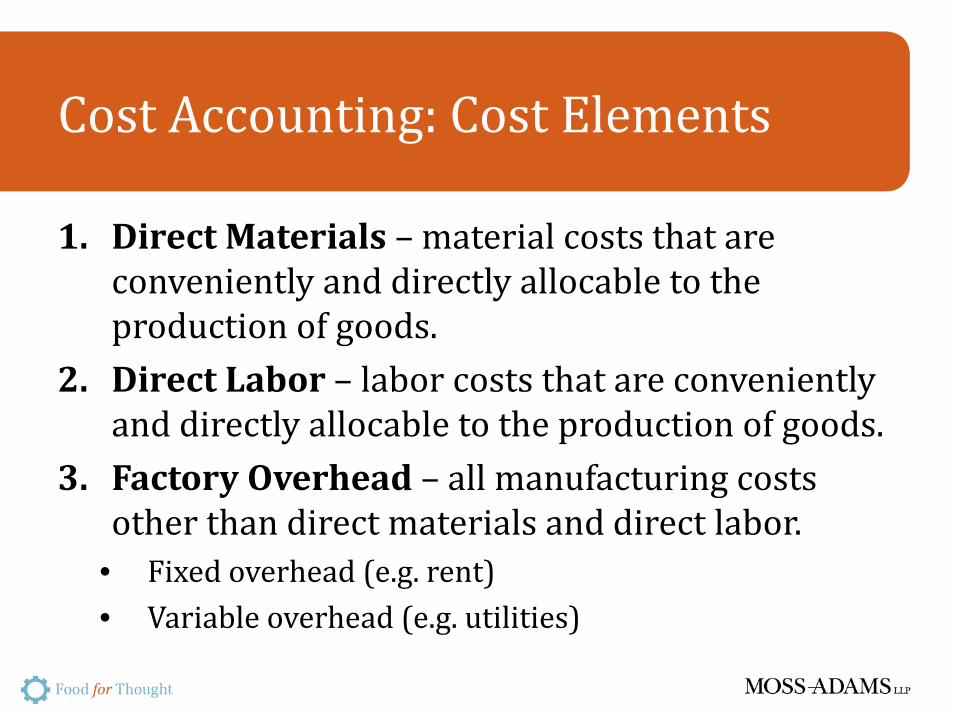

Cost Accounting: Cost Elements

1. Direct Materials – material costs that are conveniently and directly allocable to the production of goods.

2. Direct Labor – labor costs that are conveniently and directly allocable to the production of goods.

3. Factory Overhead – all manufacturing costs other than direct materials and direct labor.

• Fixed overhead (e.g. rent) • Variable overhead (e.g. utilities)

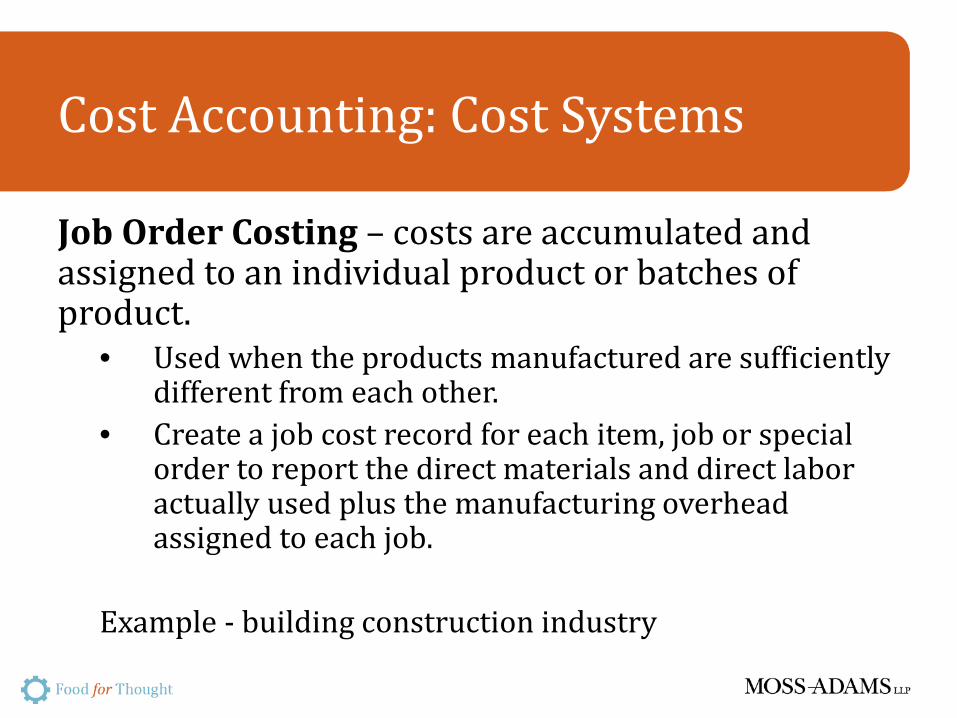

Cost Accounting: Cost Systems

Job Order Costing – costs are accumulated and assigned to an individual product or batches of product.

• Used when the products manufactured are sufficiently different from each other.

• Create a job cost record for each item, job or special order to report the direct materials and direct labor actually used plus the manufacturing overhead assigned to each job.

Example - building construction industry

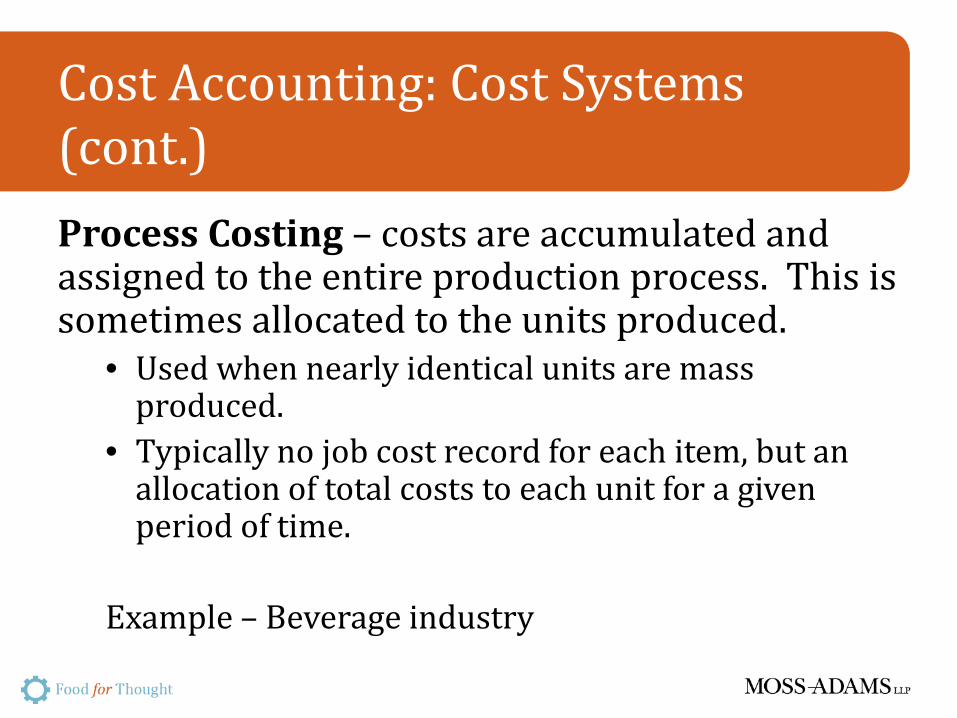

Cost Accounting: Cost Systems (cont.) Process Costing – costs are accumulated and assigned to the entire production process. This is sometimes allocated to the units produced.

• Used when nearly identical units are mass produced.

• Typically no job cost record for each item, but an allocation of total costs to each unit for a given period of time.

Example – Beverage industry

Cost Accounting: Cost Systems (cont.) Operational Cost Accounting – costing method where neither process nor job-lot costing applies.

Example – Assembly industries

Polling Question #1

What cost system does your company currently employ? a. Job order costing. b. Process costing - actual. c. Process costing - standard. d. Other.

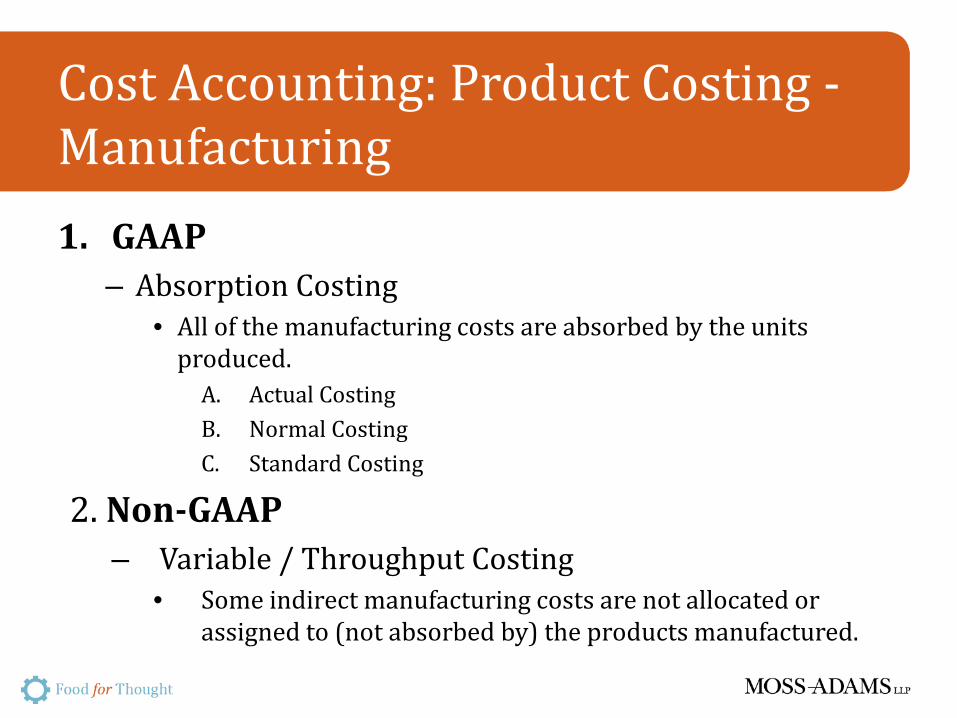

Cost Accounting: Product Costing - Manufacturing 1. GAAP

– Absorption Costing • All of the manufacturing costs are absorbed by the units

produced. A. Actual Costing B. Normal Costing C. Standard Costing

2. Non-GAAP – Variable / Throughput Costing

• Some indirect manufacturing costs are not allocated or assigned to (not absorbed by) the products manufactured.

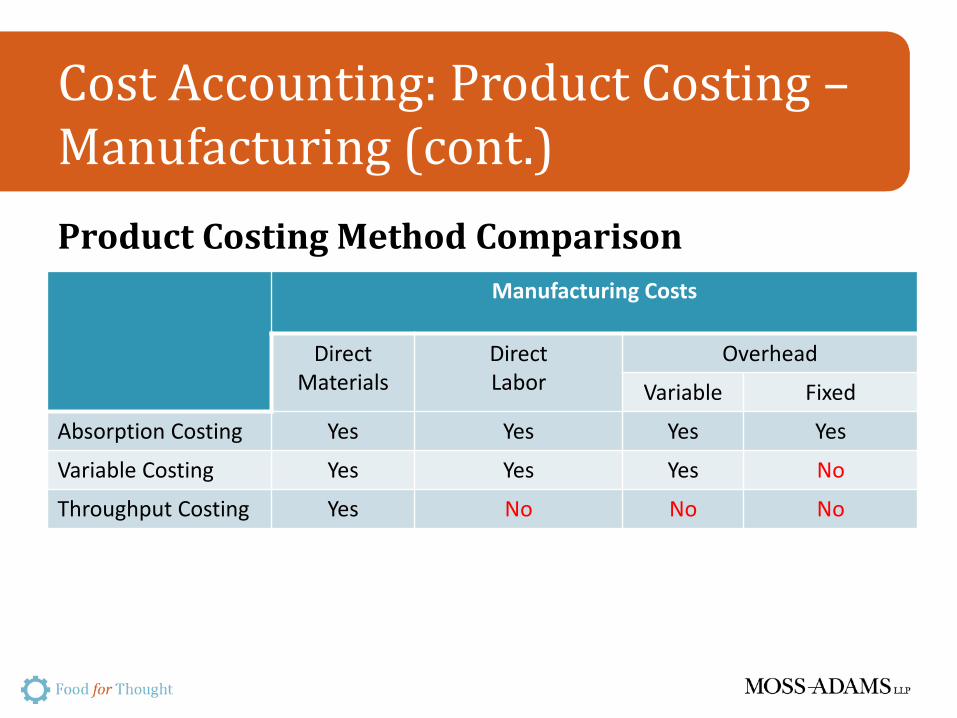

Cost Accounting: Product Costing – Manufacturing (cont.) Product Costing Method Comparison

Manufacturing Costs

Direct Materials

Direct Labor

Overhead

Variable Fixed

Absorption Costing Yes Yes Yes Yes

Variable Costing Yes Yes Yes No

Throughput Costing Yes No No No

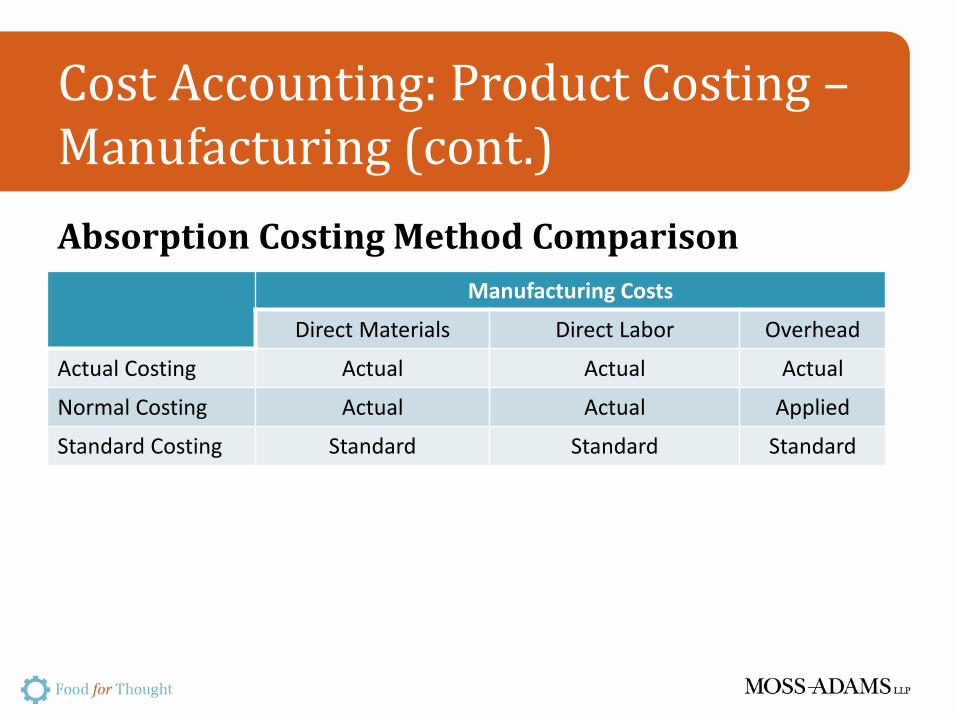

Cost Accounting: Product Costing – Manufacturing (cont.) Absorption Costing Method Comparison

Manufacturing Costs

Direct Materials Direct Labor Overhead

Actual Costing Actual Actual Actual

Normal Costing Actual Actual Applied

Standard Costing Standard Standard Standard

Cost Accounting: Standard Costing

Standard Costing • Pre-determined costs are assigned as product cost • Acceptable as long as adjusted at regular intervals

for changes in fact patterns

Cost Accounting: Standard Costing (cont.) Material Cost Standards 1. Price Standard – the price that should be paid

for a unit of material 2. Quantity Standard – the amount of material that

should be consumed in the manufacturing of one unit of product

Cost Accounting: Standard Costing (cont.)

Material Variance Price Variance

(Actual Rate – Standard Price) x Quantity Purchased

Purchase Variance (PO Price –

Standard Price) x Quantity Purchased

Invoice Price Variance

(Invoice Price –PO Price) x Quantity

Purchased

Usage Variance

(Actual Qty. Used – Standard Qty.) x Standard Price

Purchasing Production

Cost Accounting: Standard Costing (cont.) Labor Cost Standards 1. Rate Standards – the cost of labor that is applied

to manufacture one unit of product 2. Quantity Standard – the amount of time

required to make one unit of product

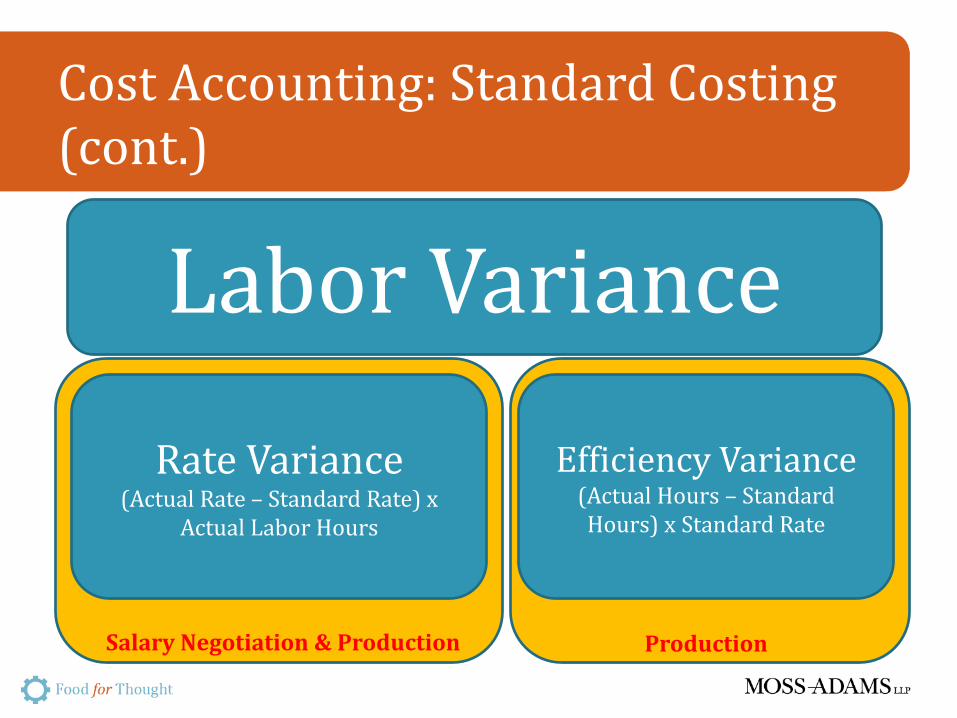

Cost Accounting: Standard Costing (cont.)

Labor Variance

Rate Variance (Actual Rate – Standard Rate) x

Actual Labor Hours

Efficiency Variance (Actual Hours – Standard Hours) x Standard Rate

Salary Negotiation & Production Production

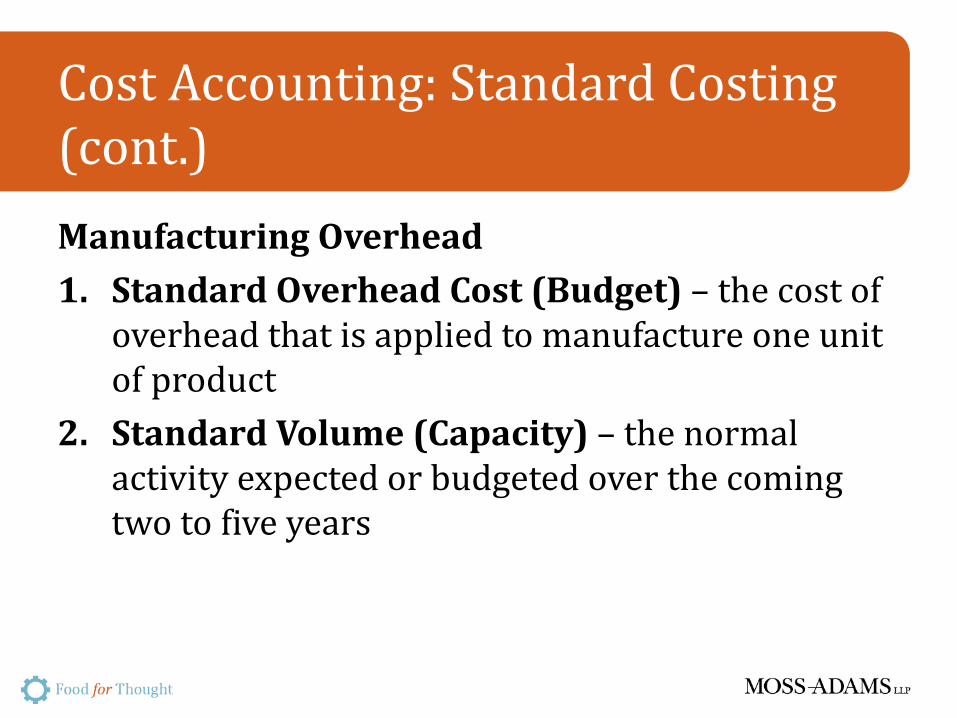

Cost Accounting: Standard Costing (cont.) Manufacturing Overhead 1. Standard Overhead Cost (Budget) – the cost of

overhead that is applied to manufacture one unit of product

2. Standard Volume (Capacity) – the normal activity expected or budgeted over the coming two to five years

Cost Accounting: Standard Costing (cont.)

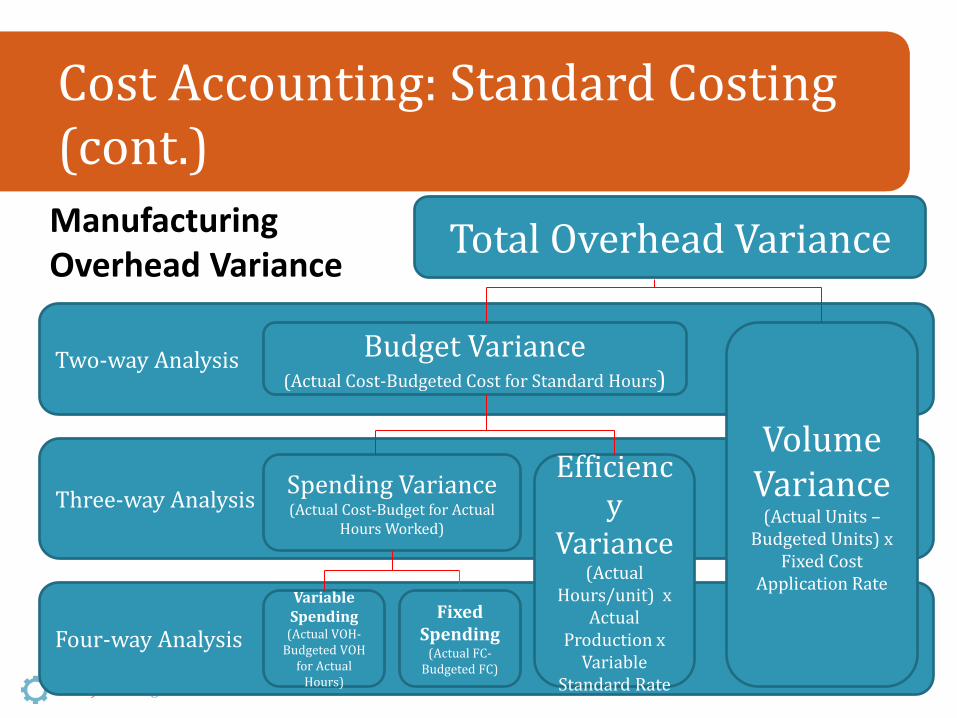

Total Overhead Variance Manufacturing Overhead Variance

Two-way Analysis

Three-way Analysis

Four-way Analysis

Budget Variance (Actual Cost-Budgeted Cost for Standard Hours)

Spending Variance (Actual Cost-Budget for Actual

Hours Worked)

Variable Spending

(Actual VOH-Budgeted VOH

for Actual Hours)

Fixed Spending

(Actual FC-Budgeted FC)

Efficiency

Variance (Actual

Hours/unit) x Actual

Production x Variable

Standard Rate

Volume Variance

(Actual Units – Budgeted Units) x

Fixed Cost Application Rate

Polling Question #2

Does your company currently utilize the services of a third party manufacturer? a. Yes, we have an established relationship with our

manufacturing partner. b. Yes, but the relationship is somewhat new. c. No, manufacturing occurs in-house. d. No, we do not manufacture any products.

Scenario of Actual Costing

ABC, LLC is a beverage company founded in January 2000 with five Stock Keeping Units (SKUs). The Company has steady and stable production volumes from month to month and little to no variability in material, labor and overhead costs.

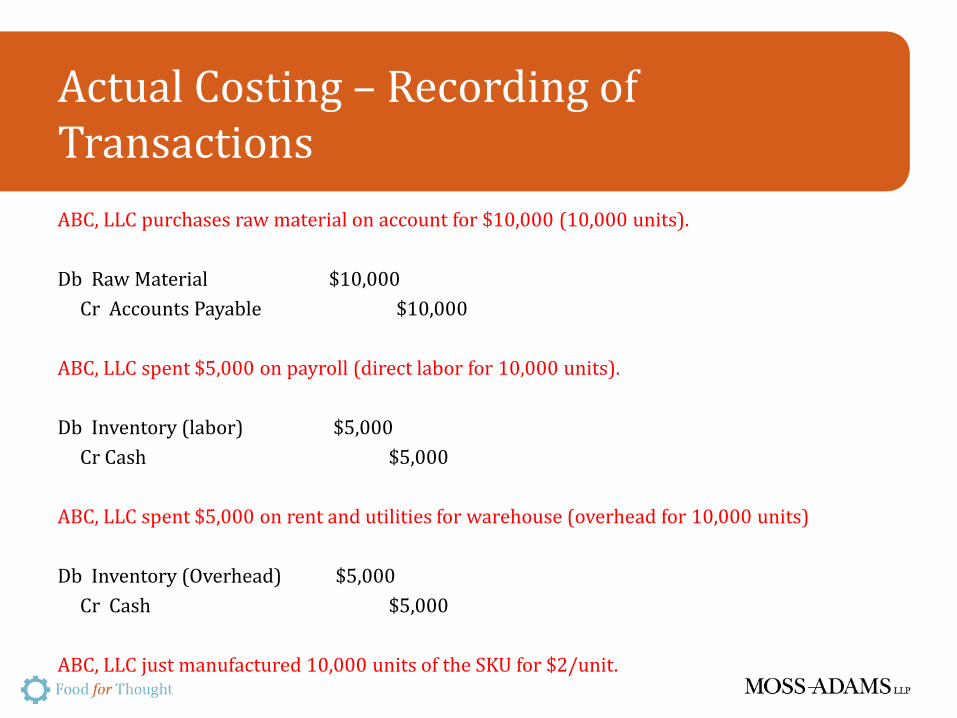

Actual Costing – Recording of Transactions ABC, LLC purchases raw material on account for $10,000 (10,000 units). Db Raw Material $10,000 Cr Accounts Payable $10,000 ABC, LLC spent $5,000 on payroll (direct labor for 10,000 units). Db Inventory (labor) $5,000 Cr Cash $5,000 ABC, LLC spent $5,000 on rent and utilities for warehouse (overhead for 10,000 units) Db Inventory (Overhead) $5,000 Cr Cash $5,000 ABC, LLC just manufactured 10,000 units of the SKU for $2/unit.

Actual Costing – Recording of Transactions

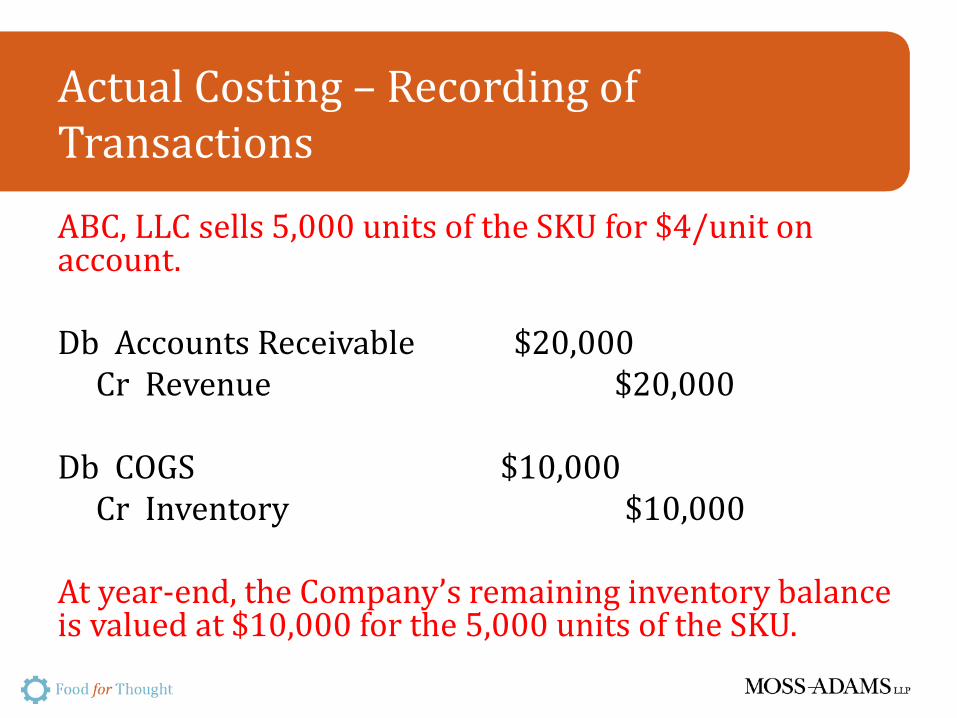

ABC, LLC sells 5,000 units of the SKU for $4/unit on account. Db Accounts Receivable $20,000 Cr Revenue $20,000 Db COGS $10,000 Cr Inventory $10,000 At year-end, the Company’s remaining inventory balance is valued at $10,000 for the 5,000 units of the SKU.

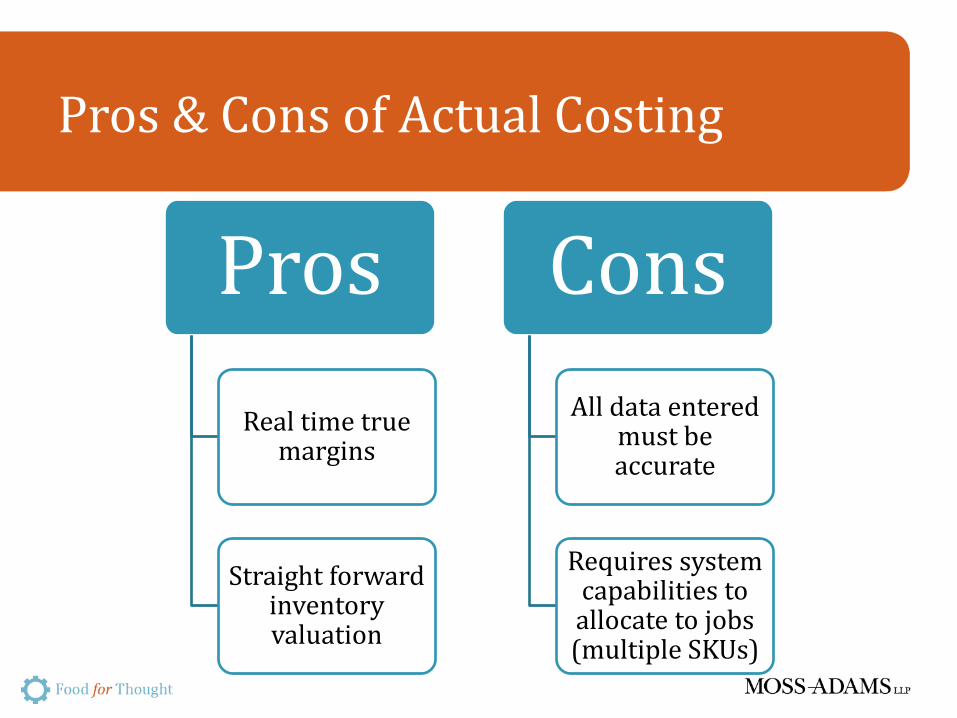

Pros & Cons of Actual Costing

Pros Real time true

margins

Straight forward inventory valuation

Cons All data entered

must be accurate

Requires system capabilities to allocate to jobs (multiple SKUs)

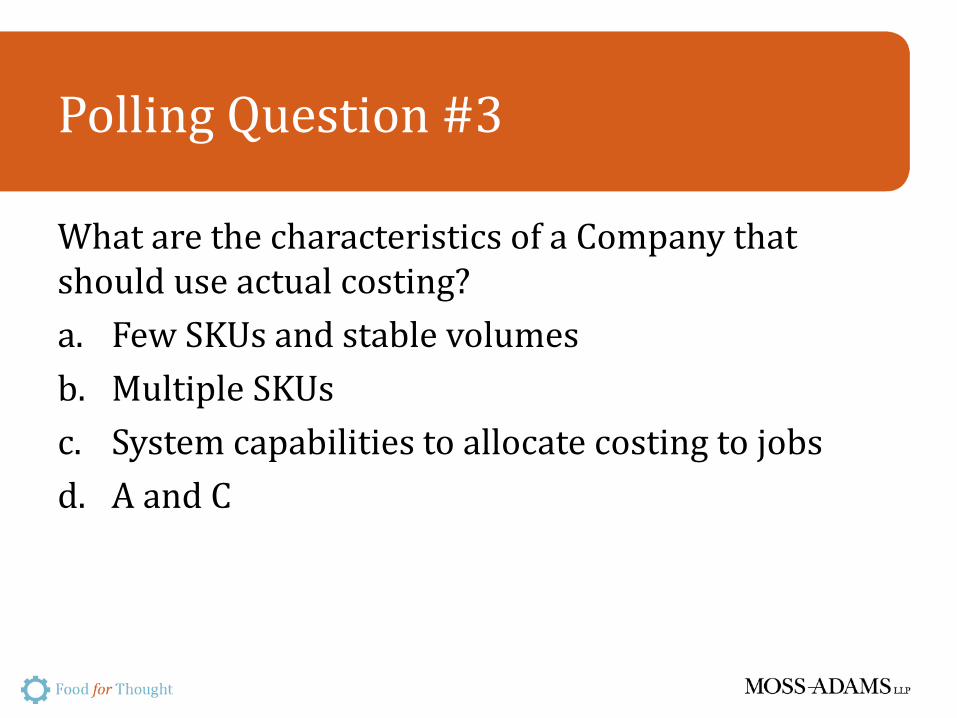

Polling Question #3

What are the characteristics of a Company that should use actual costing? a. Few SKUs and stable volumes b. Multiple SKUs c. System capabilities to allocate costing to jobs d. A and C

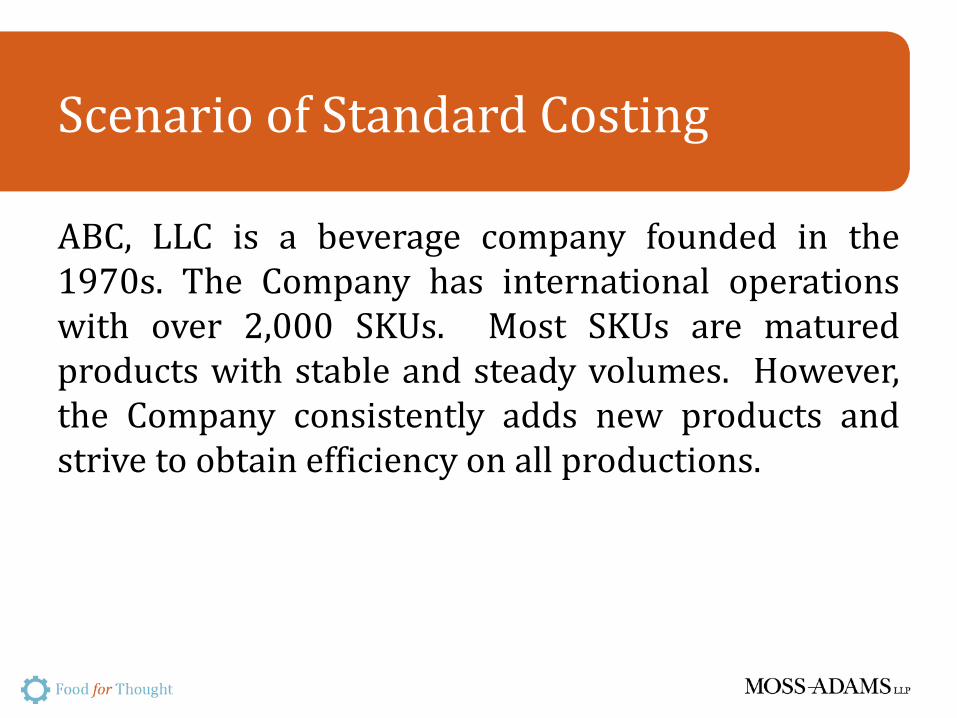

Scenario of Standard Costing

ABC, LLC is a beverage company founded in the 1970s. The Company has international operations with over 2,000 SKUs. Most SKUs are matured products with stable and steady volumes. However, the Company consistently adds new products and strive to obtain efficiency on all productions.

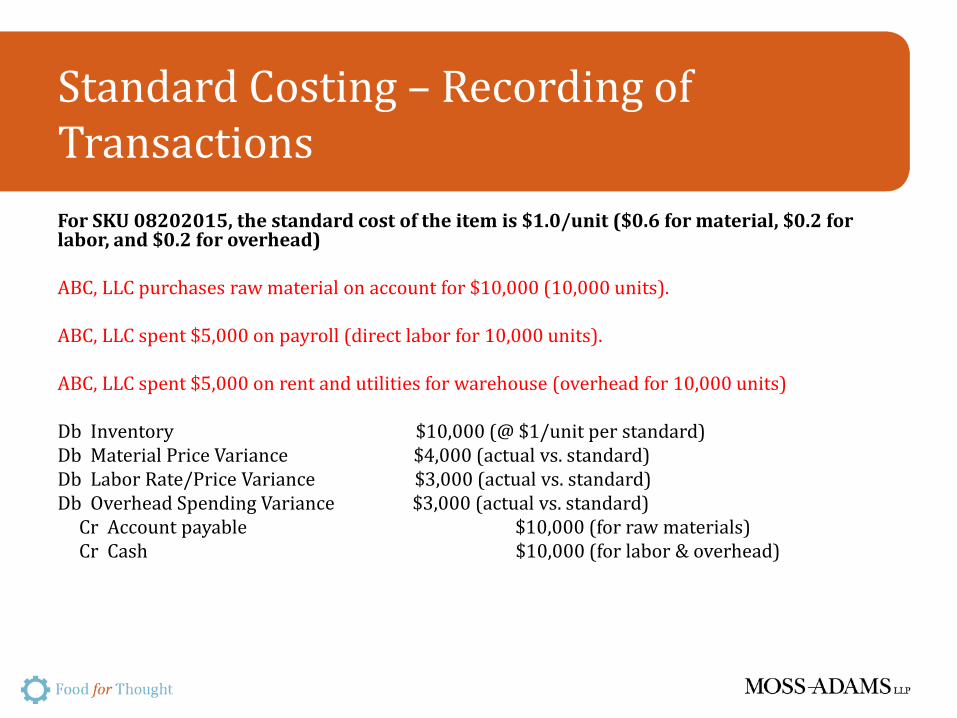

Standard Costing – Recording of Transactions For SKU 08202015, the standard cost of the item is $1.0/unit ($0.6 for material, $0.2 for labor, and $0.2 for overhead) ABC, LLC purchases raw material on account for $10,000 (10,000 units). ABC, LLC spent $5,000 on payroll (direct labor for 10,000 units). ABC, LLC spent $5,000 on rent and utilities for warehouse (overhead for 10,000 units) Db Inventory $10,000 (@ $1/unit per standard) Db Material Price Variance $4,000 (actual vs. standard) Db Labor Rate/Price Variance $3,000 (actual vs. standard) Db Overhead Spending Variance $3,000 (actual vs. standard) Cr Account payable $10,000 (for raw materials) Cr Cash $10,000 (for labor & overhead)

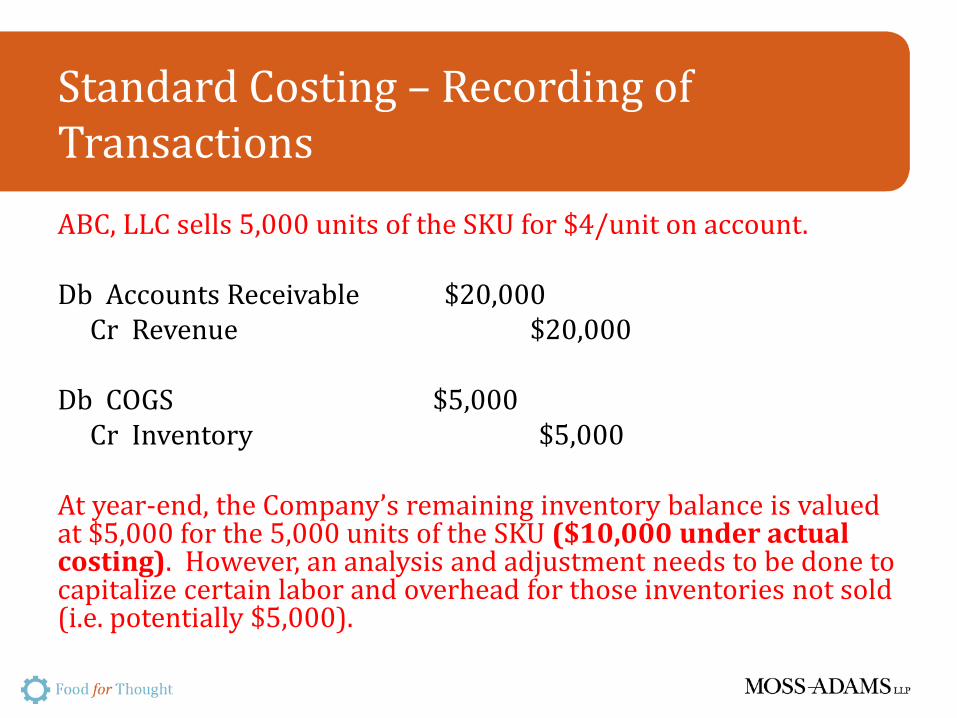

Standard Costing – Recording of Transactions ABC, LLC sells 5,000 units of the SKU for $4/unit on account. Db Accounts Receivable $20,000 Cr Revenue $20,000 Db COGS $5,000 Cr Inventory $5,000 At year-end, the Company’s remaining inventory balance is valued at $5,000 for the 5,000 units of the SKU ($10,000 under actual costing). However, an analysis and adjustment needs to be done to capitalize certain labor and overhead for those inventories not sold (i.e. potentially $5,000).

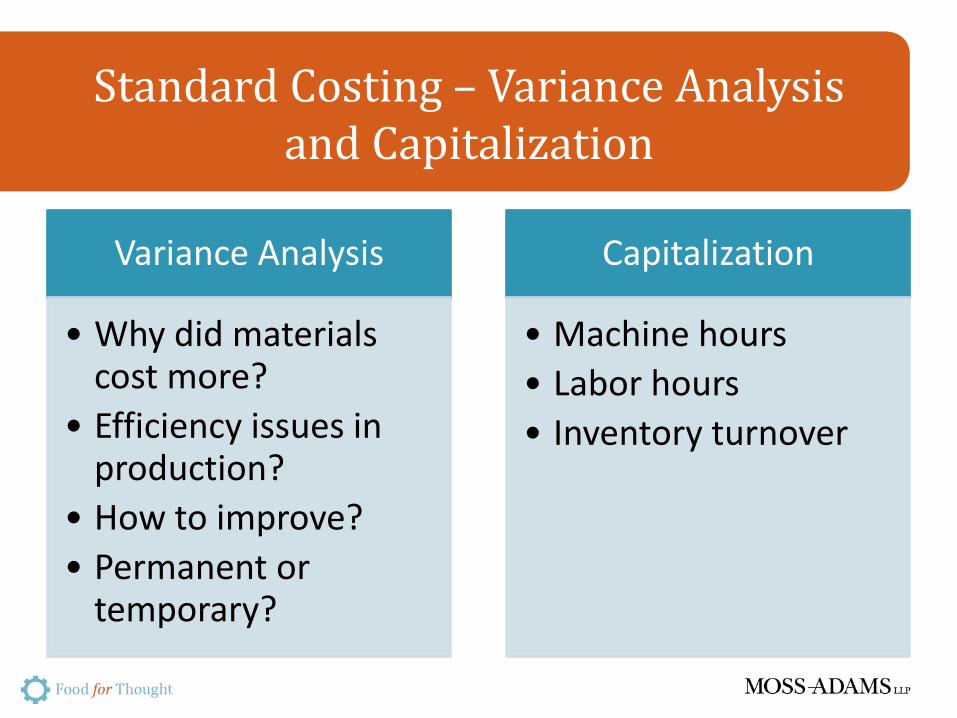

Standard Costing – Variance Analysis and Capitalization

Variance Analysis

• Why did materials cost more?

• Efficiency issues in production?

• How to improve? • Permanent or

temporary?

Capitalization

• Machine hours • Labor hours • Inventory turnover

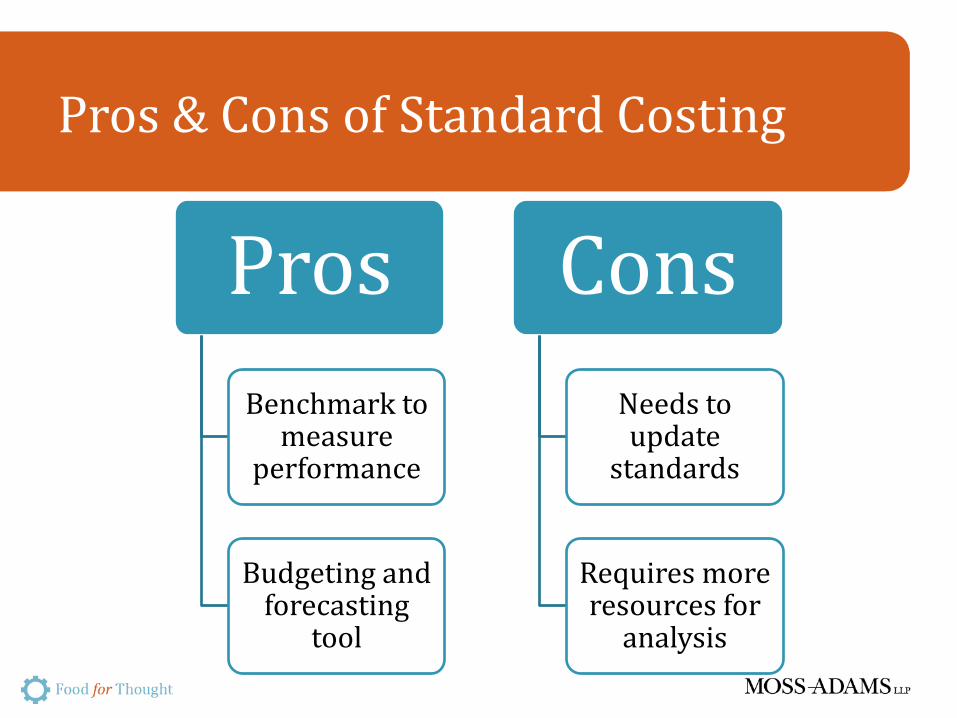

Pros & Cons of Standard Costing

Pros Benchmark to

measure performance

Budgeting and forecasting

tool

Cons Needs to update

standards

Requires more resources for

analysis

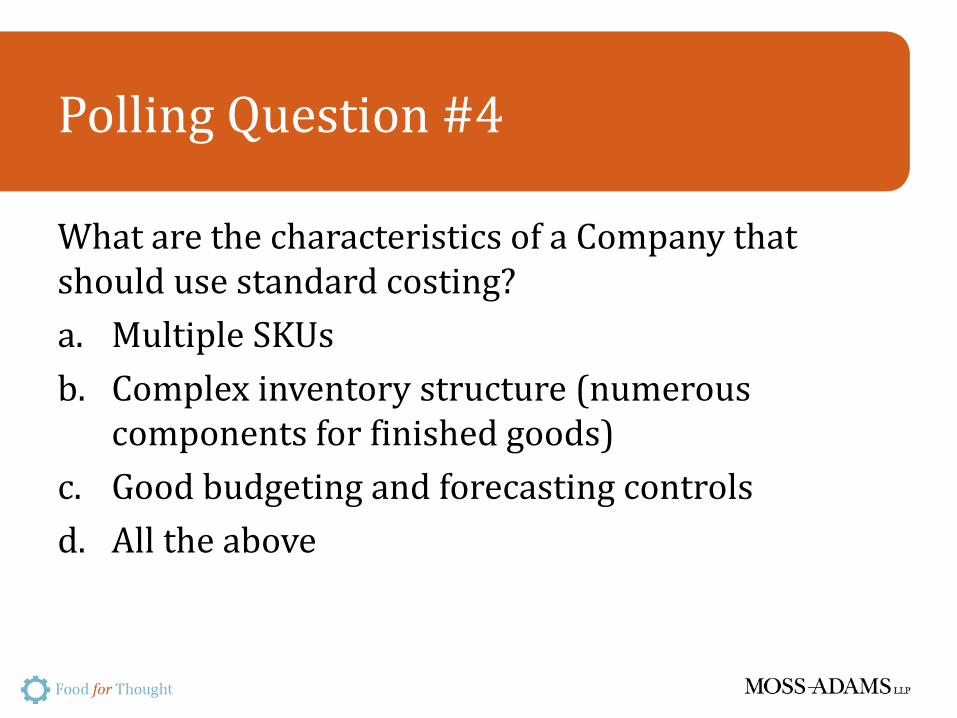

Polling Question #4

What are the characteristics of a Company that should use standard costing? a. Multiple SKUs b. Complex inventory structure (numerous

components for finished goods) c. Good budgeting and forecasting controls d. All the above

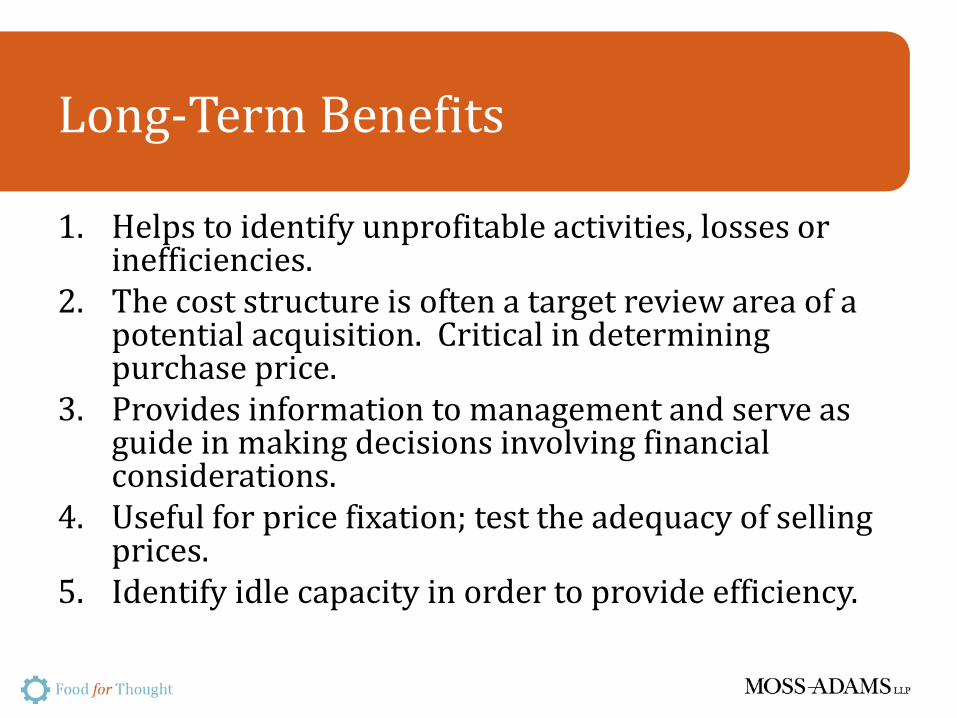

Long-Term Benefits

1. Helps to identify unprofitable activities, losses or inefficiencies.

2. The cost structure is often a target review area of a potential acquisition. Critical in determining purchase price.

3. Provides information to management and serve as guide in making decisions involving financial considerations.

4. Useful for price fixation; test the adequacy of selling prices.

5. Identify idle capacity in order to provide efficiency.

Inventory Controls

Sample Inventory Controls • Standard Cost Review • Variances, Inventory Revaluation, and Absorption

Costing Review and Allocation • Inventory Cut-off Controls • Inventory Count, Confirmation and Enterprise Unified

Process (EUP) Estimation • Inventory Reserves Calculation • Inventory Reconciliation • Inventory Roles Segregation of Duties

Questions?

Nick Bergamo Senior Manager [email protected] 949-221-4022 Linda Pei Senior Manager [email protected] 818-577-1885