Embed Size (px)

Citation preview

Introduction to portfolio insurance

Introduction to portfolio insurance – p.1/41

Portfolio insurance• Maintain the portfolio value above a certain

predetermined level (floor) while allowing some upsidepotential.

• Performance may be compared to a stock marketindex, or may be guaranteed explicitly in terms of thisindex.

• Usually implementented via strategic allocationbetween the benchmark index, risk-free account and(possibly) option on the benchmark index.

Introduction to portfolio insurance – p.2/41

Portfolio insurance example (equity)

Example: Hawaii 3 fund marketed by BNP Paribas:

• At maturity, the value of the fund will be greater orequal to the largest of:

• 105% of the initial value. ⇐ less than the risk-freereturn over the holding period.

• 85% of the highest value attained by the Fundbetween 23/01/2007 and 3/07/2013 ⇐ floor can beadjusted throughout the life of the portfolio

• The portfolio protection is valid only at maturity.

Introduction to portfolio insurance – p.3/41

Portfolio insurance example (cont’d)

• Objective: benefit from the performance of a basket(DJ Euro STOXX 50, S&P 500 and Nikkei 225) whileensuring minimum annual performance of 0.7%.

• Danger of monetarization: to satisfy the insuranceconstraint, the exposure to risky asset may becomeand remain zero.

• Even if the Fund performance depends partially on theBasket, it can be different due to capital insurance.

• Strategy: The Fund will be actively managed usingportfolio insurance techniques.

Introduction to portfolio insurance – p.4/41

Portfolio insurance techniques

• Stop-loss (for someone who doesn’t know stochasticcalculus).

• Option-based portfolio insurance (OBPI).

• OBPI with option replication.

• Constant proportion portfolio insurance (CPPI).

Introduction to portfolio insurance – p.5/41

Stop-loss strategy

Introduction to portfolio insurance – p.6/41

Stop-loss strategy

• The simplest and the most intuitive strategy but its costis difficult to quantify in practice.

• The entire portfolio is initially invested into the riskyasset.

• As soon as the risky asset St drops below the floor Ft,the entire position is rebalanced into the risk-freeasset.

• If the market rebounds above the floor, the fund isreinvested into risky assets.

Introduction to portfolio insurance – p.7/41

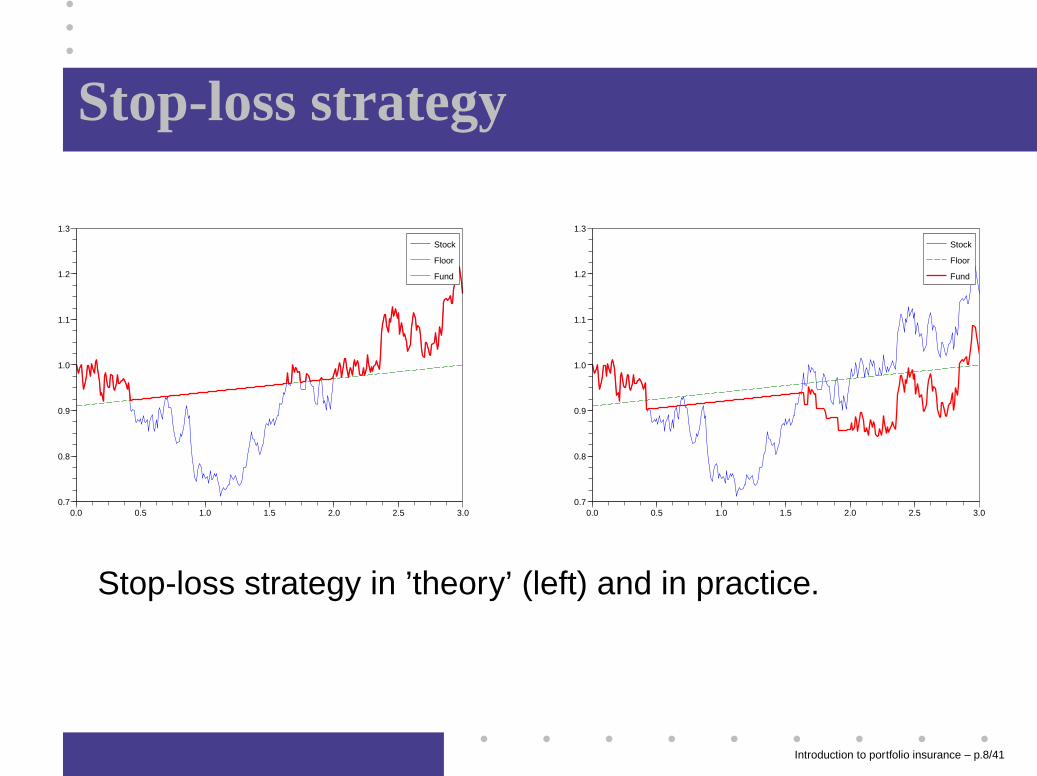

Stop-loss strategy

0.0 0.5 1.0 1.5 2.0 2.5 3.00.7

0.8

0.9

1.0

1.1

1.2

1.3

Stock

Floor

Fund

0.0 0.5 1.0 1.5 2.0 2.5 3.00.7

0.8

0.9

1.0

1.1

1.2

1.3

Stock

Floor

Fund

Stop-loss strategy in ’theory’ (left) and in practice.

Introduction to portfolio insurance – p.8/41

The loss is not stopped

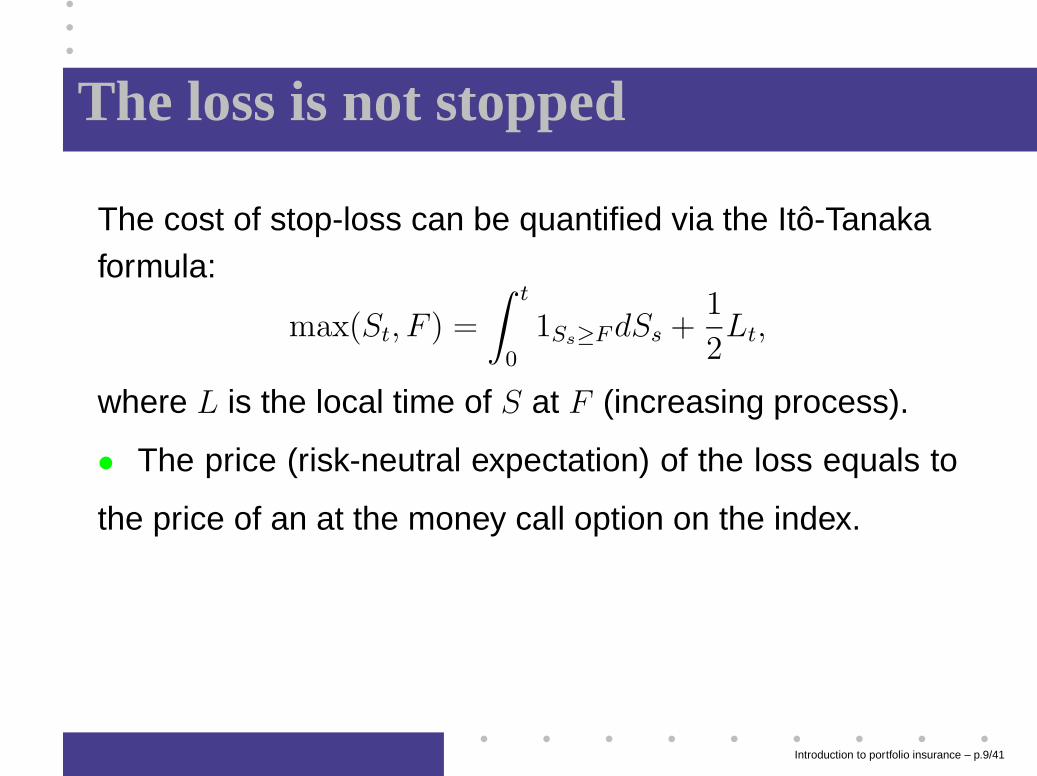

The cost of stop-loss can be quantified via the Itô-Tanakaformula:

max(St, F ) =

∫ t

0

1Ss≥F dSs +1

2Lt,

where L is the local time of S at F (increasing process).

• The price (risk-neutral expectation) of the loss equals to

the price of an at the money call option on the index.

Introduction to portfolio insurance – p.9/41

Option-based portfolio insurance

Introduction to portfolio insurance – p.10/41

Basic strategy with European guarantee• Let K be the floor (with KB(0, T ) < 1).

• Invest a fraction λ of the fund into the index S.

• Use the remainder to buy a Put on λS.

• The total cost is

f(λ) = λ + PλS(T,K)

increasing function with f(0) = KB(0, T ) < 1 andf(1) = 1 + PS(T,K) > 1.

⇒ There exists a unique λ∗ ∈ (0, 1), realizing theput-based strategy.

Introduction to portfolio insurance – p.11/41

Optimality of the put-based strategy

Let u(x) = x1−γ

1−γand let ST be the optimal unconstrained

portfolio:

E[u(ST )] = maxE[u(XT )] subject to X0 = 1.

Then the put-based strategy is the optimal strategy subject

to the floor constraint (El Karoui, Jeanblanc, Lacoste ’05).

Introduction to portfolio insurance – p.12/41

Equivalent strategy using calls

By put-call parity, the put-based strategy is equivalent to:

• Buy zero-coupon with notional K to lock in the capitalat maturity

• Use the remainder to buy a call on λ∗ST with strike K

(or anything else!).

• Often, at-the-money calls are used; fund’s performanceis then proportional to the risky asset performance:

VT = 1 + k(ST − 1)+, k =1 − B(0, T )

C(T )< 1.

k is called gearing or indexation.

Introduction to portfolio insurance – p.13/41

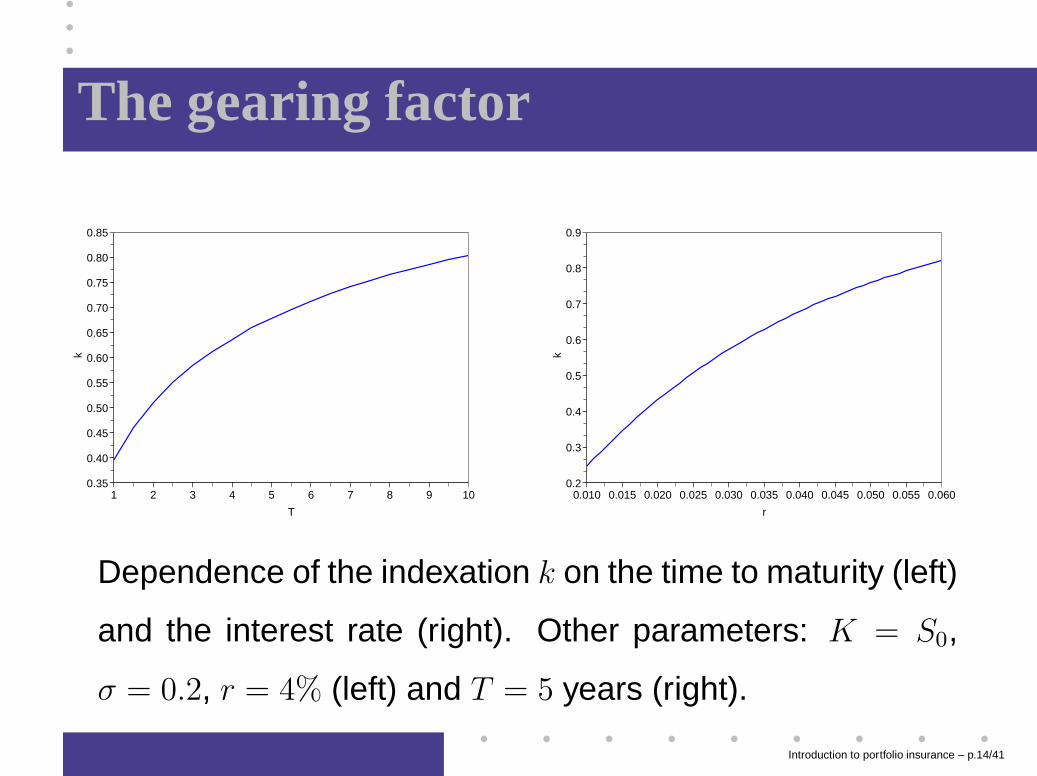

The gearing factor

1 2 3 4 5 6 7 8 9 100.35

0.40

0.45

0.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

T

k

0.010 0.015 0.020 0.025 0.030 0.035 0.040 0.045 0.050 0.055 0.0600.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

r

k

Dependence of the indexation k on the time to maturity (left)

and the interest rate (right). Other parameters: K = S0,

σ = 0.2, r = 4% (left) and T = 5 years (right).

Introduction to portfolio insurance – p.14/41

American capital guarantee• One cannot simply buy and hold an American put

because it is not self-financing.

• The correct strategy is dynamic trading in S andAmerican puts on S:

Vt = λtSt + P a(t, λtSt), λt = λ0 ∨ supu≤t

(

b(u)

Su

)

,

where b(t) is the exercise boundary and λ0 is chosenfrom the budget constraint.

• This self-financing strategy, satisfies Vt ≥ K, 0 ≤ t ≤ T

and is optimal for power utility in complete markets (EKJL).

Introduction to portfolio insurance – p.15/41

Replicating options

Danger of the OBPI approach: absence of liquid optionsfor long maturities (especially in the credit world)

• Counterparty risk if the option is boughtover-the-counter

• Marking-to-market difficult at intermediate dates

Common solution: replicate the option with a self-financing

portfolio containing ∆(St) stocks.

Introduction to portfolio insurance – p.16/41

OBPI with option replication

Advantages:

• No need to structure a long-dated option

• The portfolio is easy to mark to market and liquidate

Drawbacks:

• The replication is only approximate, especially inincomplete markets

• Transaction costs may be high

• Model-dependent

Introduction to portfolio insurance – p.17/41

Constant proportion portfolioinsurance

Introduction to portfolio insurance – p.18/41

The basic CPPI strategy

• Introduced by Black and Jones (87) and Perold (86).

• A fixed amount N is guaranteed at maturity T .

• At every t, a fraction is invested into risky asset St andthe remainder into zero-coupon bond with maturity T

and nominal N (denoted by Bt).

• If Vt > Bt, the risky asset exposure ismCt ≡ m(Vt − Bt), with m > 1.

• If Vt ≤ Bt, the entire portfolio is invested into thezero-coupon.

Introduction to portfolio insurance – p.19/41

Features and extensions

• Model-independent (for continuous processes).

• Maturity-independent, open-entry and open-exit.

• Greater upward potential than OBPI: while in OBPI theexposure is limited to the indexation k < 1, the CPPIexposure in bullish markets is only limited by themultiplier.

• Variable floor (ratchet) easily incorporated.

Introduction to portfolio insurance – p.20/41

Analysis of CPPI: Gaussian setting

Suppose that the interest rate r is constant and

dSt

St= µdt + σdWt.

Then the fund’s evolution is given by

dVt = m(Vt − Bt)dSt

St

+ (Vt − m(Vt − Bt))rdt.

Ct satisfies the Black-Scholes SDE:

dCt

Ct

= (mµ + (1 − m)r)dt + mσdWt.

Introduction to portfolio insurance – p.21/41

Analysis of CPPI: Gaussian setting

In the Black-Scholes model, CPPI strategy is equivalent to

• Buying a zero-coupon with nominal N to guarantee thecapital at maturity (superhedging the floor);

• Investing the remaining sum into a risky asset whichhas m times the excess return and m times thevolatility of S and is perfectly correlated with S.

Introduction to portfolio insurance – p.22/41

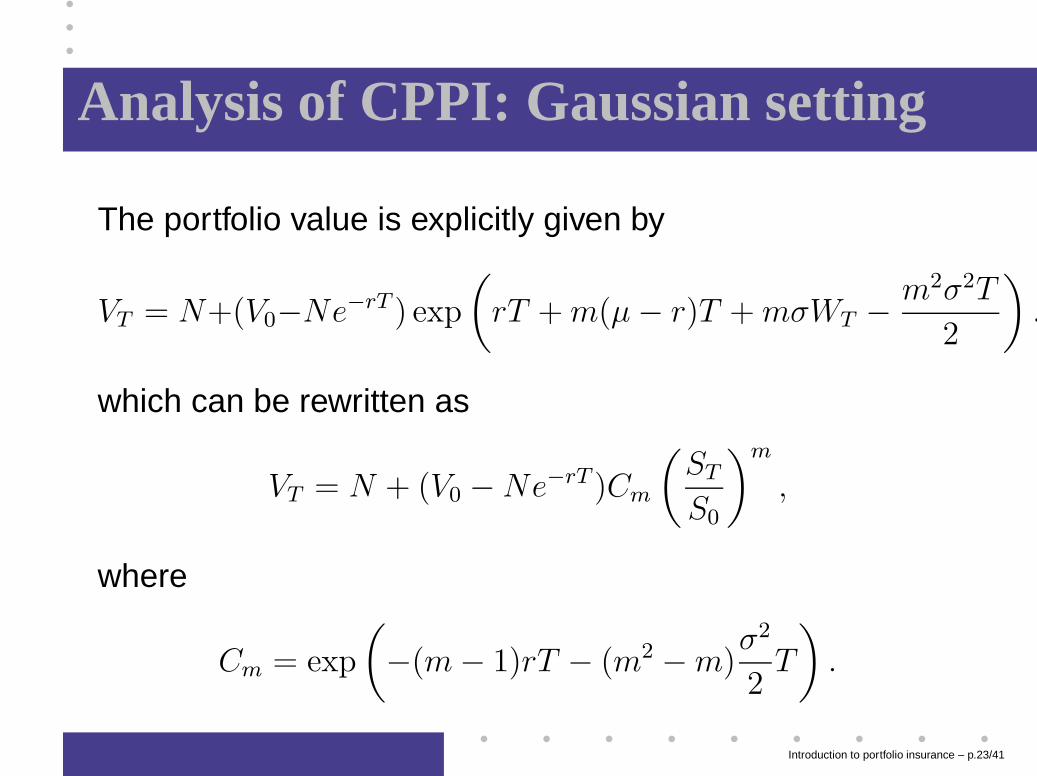

Analysis of CPPI: Gaussian setting

The portfolio value is explicitly given by

VT = N+(V0−Ne−rT ) exp

(

rT + m(µ − r)T + mσWT − m2σ2T

2

)

.

which can be rewritten as

VT = N + (V0 − Ne−rT )Cm

(

ST

S0

)m

,

where

Cm = exp

(

−(m − 1)rT − (m2 − m)σ2

2T

)

.

Introduction to portfolio insurance – p.23/41

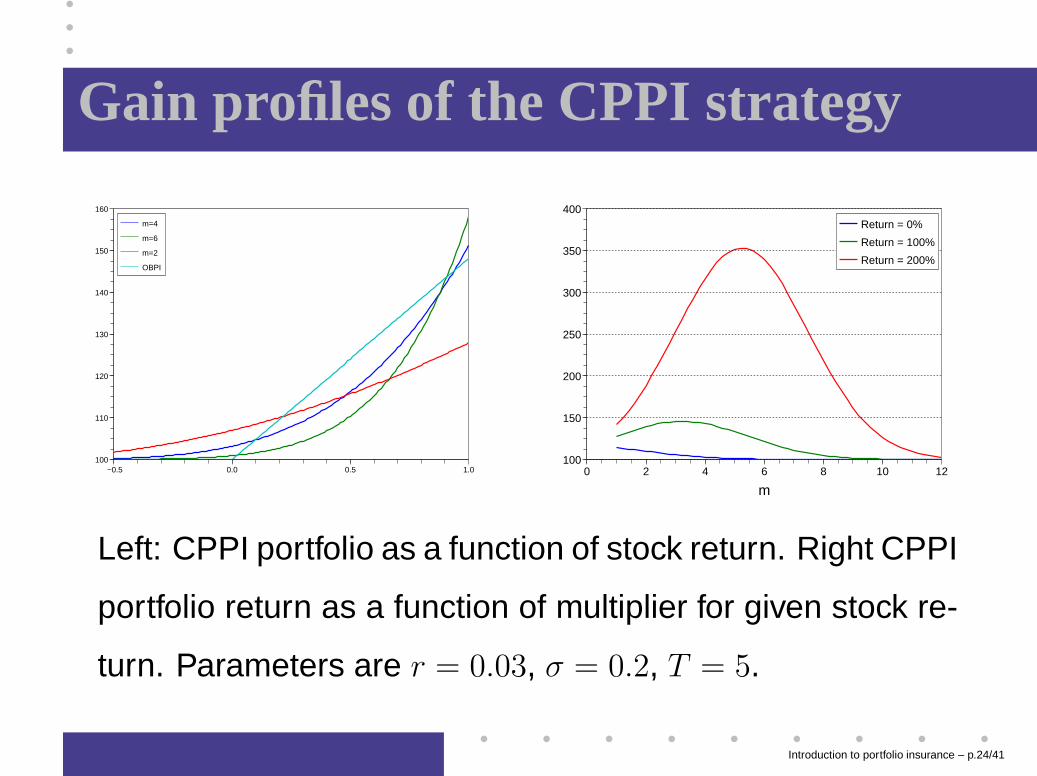

Gain profiles of the CPPI strategy

−0.5 0.0 0.5 1.0100

110

120

130

140

150

160

m=4

m=6

m=2

OBPI

0 2 4 6 8 10 12100

150

200

250

300

350

400

m

Return = 0%

Return = 100%

Return = 200%

Left: CPPI portfolio as a function of stock return. Right CPPI

portfolio return as a function of multiplier for given stock re-

turn. Parameters are r = 0.03, σ = 0.2, T = 5.

Introduction to portfolio insurance – p.24/41

Optimality of CPPI

The CPPI strategy can be shown to be optimal in thecontext of long-term risk-sensitive portfolio optimization(Grossman and Vila ’92, Sekine ’08):

supπ∈A

lim supT→∞

1

γTlog E (Xx,π

T )γ (RS)

• The optimal strategy π and the value function do notdepend on the initial value x > 0.

• In the Black-Scholes setting, the Merton strategyπ∗ ≡ µ−r

σ2(1−γ)is optimal.

Introduction to portfolio insurance – p.25/41

Optimality of CPPI

For the problem (RS) under the constraint Xx,πt ≥ Kt for all

t, an optimal strategy is described by

• Superhedge the floor process with any portfolio K̄

satisfying K̄0 < x.

• Invest x − K̄0 into the unconstrained optimal portfolio.

In the Black-Scholes model ⇒ classical CPPI withmultiplier given by the Merton portfolio π∗.

• Extension by Grossman and Zhou ’93 and Cvitanic andKaratzas ’96: the CPPI strategy with stochastic floor isoptimal for (RS) in case of drawdown constraints.

Introduction to portfolio insurance – p.26/41

Optimality of CPPI: critique

• Merton’s multiplier may be too low: it results from theunconstrained problem which takes into account bothgains and losses, and under the floor constraintinvestors accept greater risks to maximize gains.

• In models with jumps, the positivity constraint oftenimplies 0 ≤ π ≤ 1, which is not sufficient for CPPI ⇒one may want to authorise some gap risk ⇒optimisation under VaR constraint.

• Market practice is to use basic CPPI with m fixed asfunction of the VaR constraint.

Introduction to portfolio insurance – p.27/41

Some explicit computations forCPPI with jumps

Introduction to portfolio insurance – p.28/41

Introducing jumps

Suppose that S and B may be written as

dSt

St−= dZt and

dBt

Bt= dRt,

where Z is a semimartingale with ∆Z > −1 and R is acontinuous semimartingale.This implies

Bt = B0 exp

(

Rt −1

2[R]t

)

> 0.

Example: Rt = rt and Z is a Lévy process.

Introduction to portfolio insurance – p.29/41

Stochastic differential equation

Let τ = inf{t : Vt ≤ Bt}. Then, up to time τ ,

dVt = m(Vt− − Bt−)dSt

St−

+ {Vt− − m(Vt− − Bt−)}dBt

Bt−

,

which can be rewritten as

dCt

Ct−

= mdZt + (1 − m)dRt.

where Ct = Vt − Bt is the cushion.

Introduction to portfolio insurance – p.30/41

Solution via change of numeraire

Writing C∗t = Ct

Btand applying Itô formula,

dC∗t

C∗t−

= m(dZt − d[Z,R]t − dRt + d[R]t) := mdLt,

which can be written as

C∗t = C∗

0E(mL)t,

where E denotes the stochastic exponential:

E(X)t = X0eXt−

1

2[X]ct

∏

s≤t,∆Xs 6=0

(1 + ∆Xs)e−∆Xs .

Introduction to portfolio insurance – p.31/41

Solution via change of numeraire

After time τ , the process C∗ remains constant. Therefore,the portfolio value can be written explicitly as

C∗t = C∗

0E(mL)t∧τ ,

or again as

Vt

Bt= 1 +

(

V0

B0− 1

)

E(mL)t∧τ .

Introduction to portfolio insurance – p.32/41

Probability of loss

Proposition Let L = Lc + Lj, with Lc continuous and Lj

independent Lévy process with Lévy measure ν. Then

P [∃t ∈ [0, T ] : Vt ≤ Bt] = 1 − exp

(

−T

∫ −1/m

−∞

ν(dx)

)

.

• In Lévy models, the basic CPPI has constant lossprobability per unit time.

Introduction to portfolio insurance – p.33/41

Probability of loss

Proof: Vt ≤ Bt ⇐⇒ C∗t ≤ 0 ⇐⇒

C∗t = C∗

0E(mL)t ≤ 0.

But since

∆E(X)t = E(X)t−(1 + ∆Xt),

this is equivalent to ∆Ljt ≤ −1/m.

For a Lévy process Lj, the number of such jumps in the

interval [0, T ] is a Poisson random variable with intensity

T∫ −1/m

−∞ν(dx).

Introduction to portfolio insurance – p.34/41

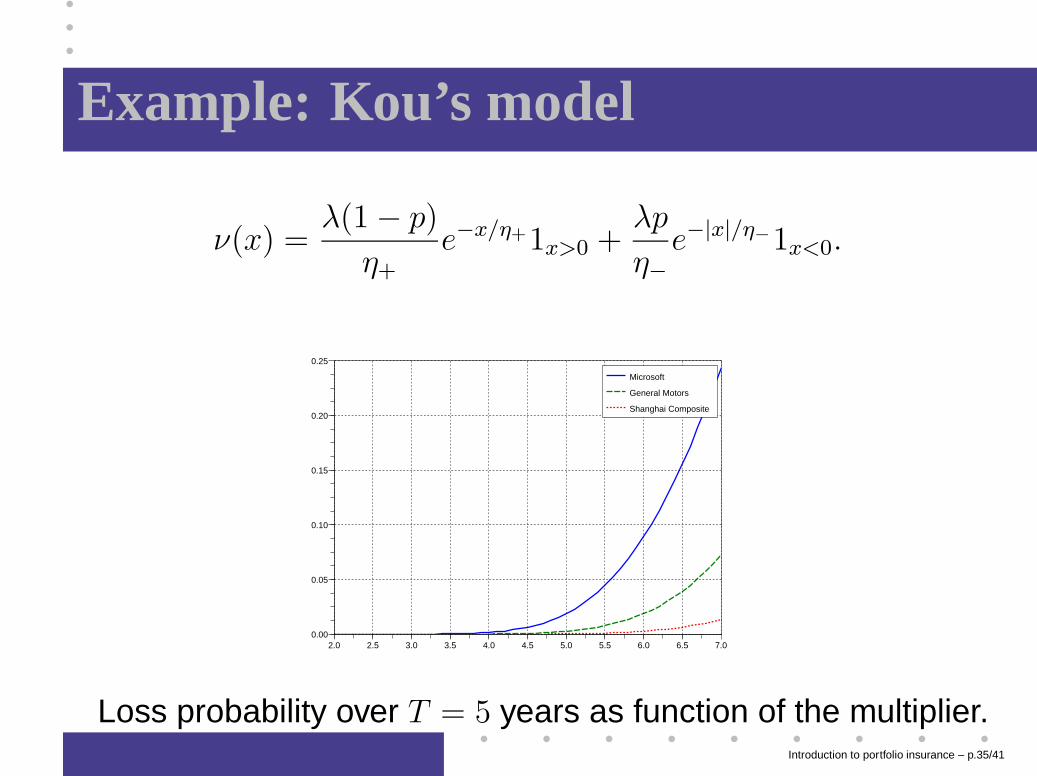

Example: Kou’s model

ν(x) =λ(1 − p)

η+e−x/η+1x>0 +

λp

η−e−|x|/η

−1x<0.

2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 6.0 6.5 7.00.00

0.05

0.10

0.15

0.20

0.25

Microsoft

General Motors

Shanghai Composite

Loss probability over T = 5 years as function of the multiplier.Introduction to portfolio insurance – p.35/41

Stochastic volatility and variablemultiplier strategies

Introduction to portfolio insurance – p.36/41

Stochastic volatility via time change

The traditional stochastic volatility model dSt

St= σtdWt can

be equivalently written as

St = X(vt) where vt =

∫ t

0

σ2sds and

dX(t)

X(t)= dWt.

Similarly, Carr et al.(2003) construct stochastic volatilitymodels with jumps from a jump-diffusion model:

St = E(L)vt , vt =

∫ t

0

σ2sds, L is a jump-diffusion.

• The stochastic volatility determines the intensity of jumps

Introduction to portfolio insurance – p.37/41

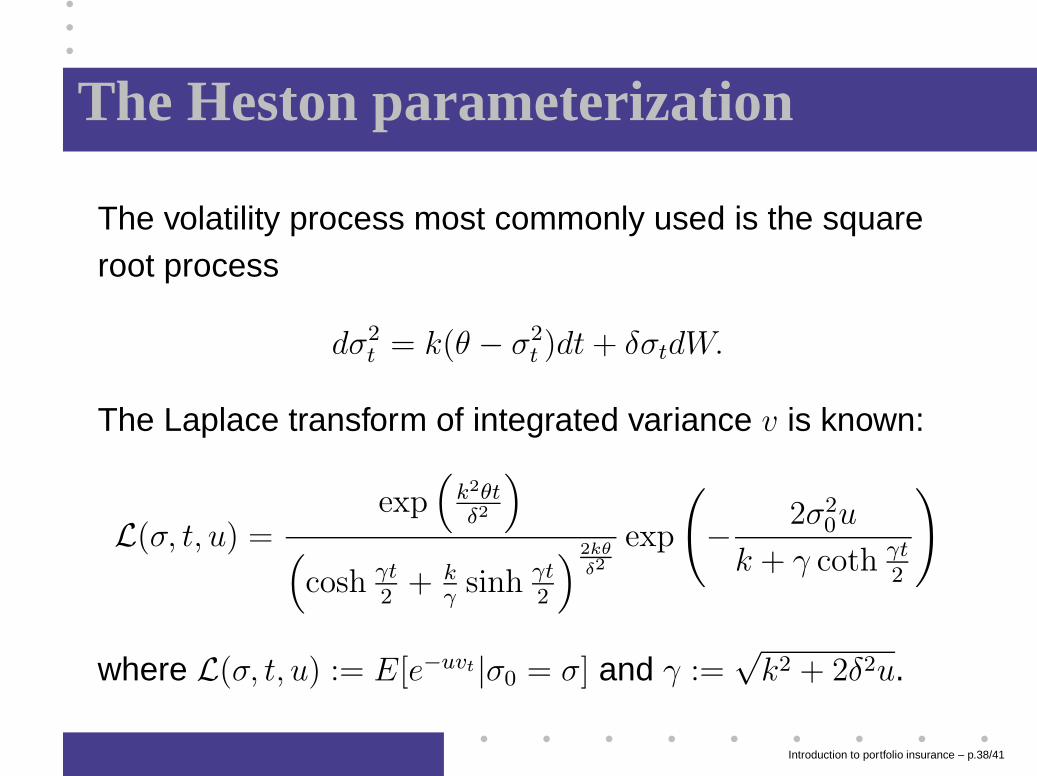

The Heston parameterization

The volatility process most commonly used is the squareroot process

dσ2t = k(θ − σ2

t )dt + δσtdW.

The Laplace transform of integrated variance v is known:

L(σ, t, u) =exp

(

k2θtδ2

)

(

cosh γt2

+ kγ

sinh γt2

)2kθ

δ2

exp

(

− 2σ20u

k + γ coth γt2

)

where L(σ, t, u) := E[e−uvt|σ0 = σ] and γ :=√

k2 + 2δ2u.

Introduction to portfolio insurance – p.38/41

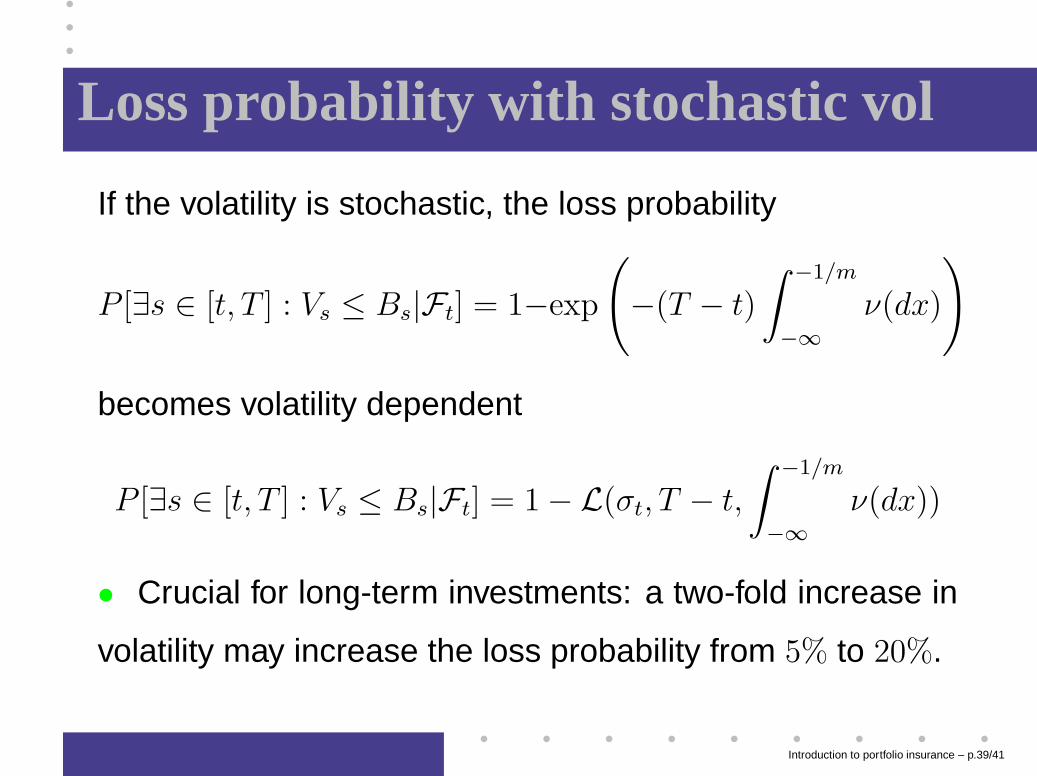

Loss probability with stochastic vol

If the volatility is stochastic, the loss probability

P [∃s ∈ [t, T ] : Vs ≤ Bs|Ft] = 1−exp

(

−(T − t)

∫ −1/m

−∞

ν(dx)

)

becomes volatility dependent

P [∃s ∈ [t, T ] : Vs ≤ Bs|Ft] = 1 − L(σt, T − t,

∫ −1/m

−∞

ν(dx))

• Crucial for long-term investments: a two-fold increase in

volatility may increase the loss probability from 5% to 20%.

Introduction to portfolio insurance – p.39/41

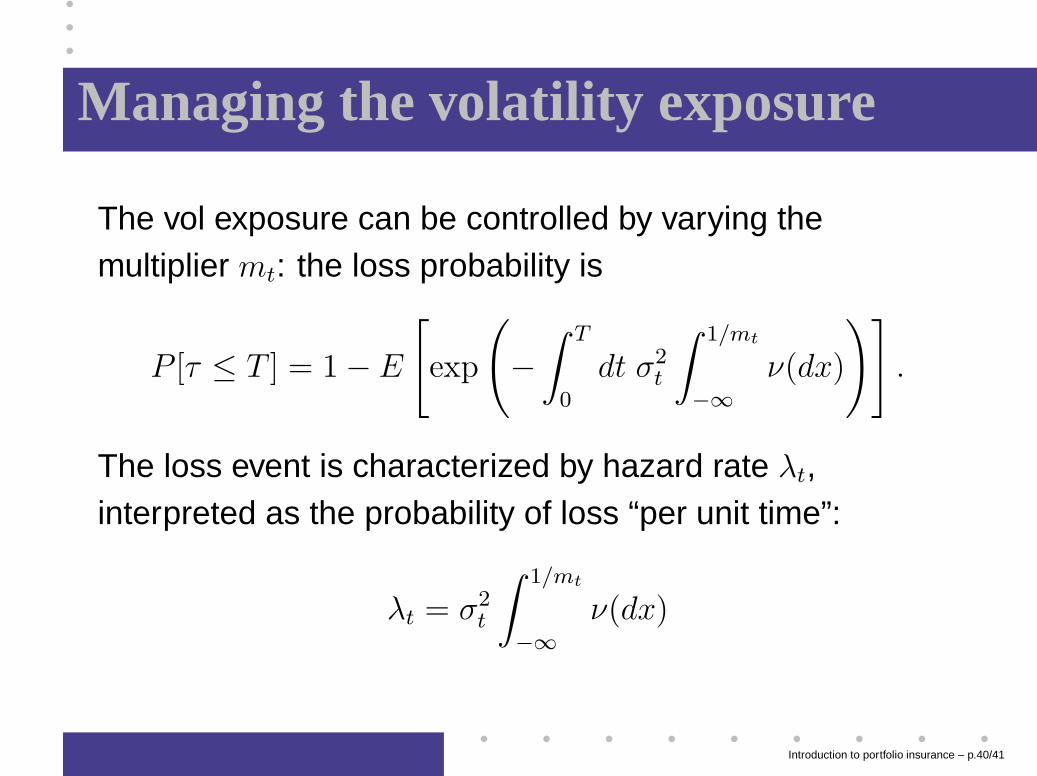

Managing the volatility exposure

The vol exposure can be controlled by varying themultiplier mt: the loss probability is

P [τ ≤ T ] = 1 − E

[

exp

(

−∫ T

0

dt σ2t

∫ 1/mt

−∞

ν(dx)

)]

.

The loss event is characterized by hazard rate λt,interpreted as the probability of loss “per unit time”:

λt = σ2t

∫ 1/mt

−∞

ν(dx)

Introduction to portfolio insurance – p.40/41

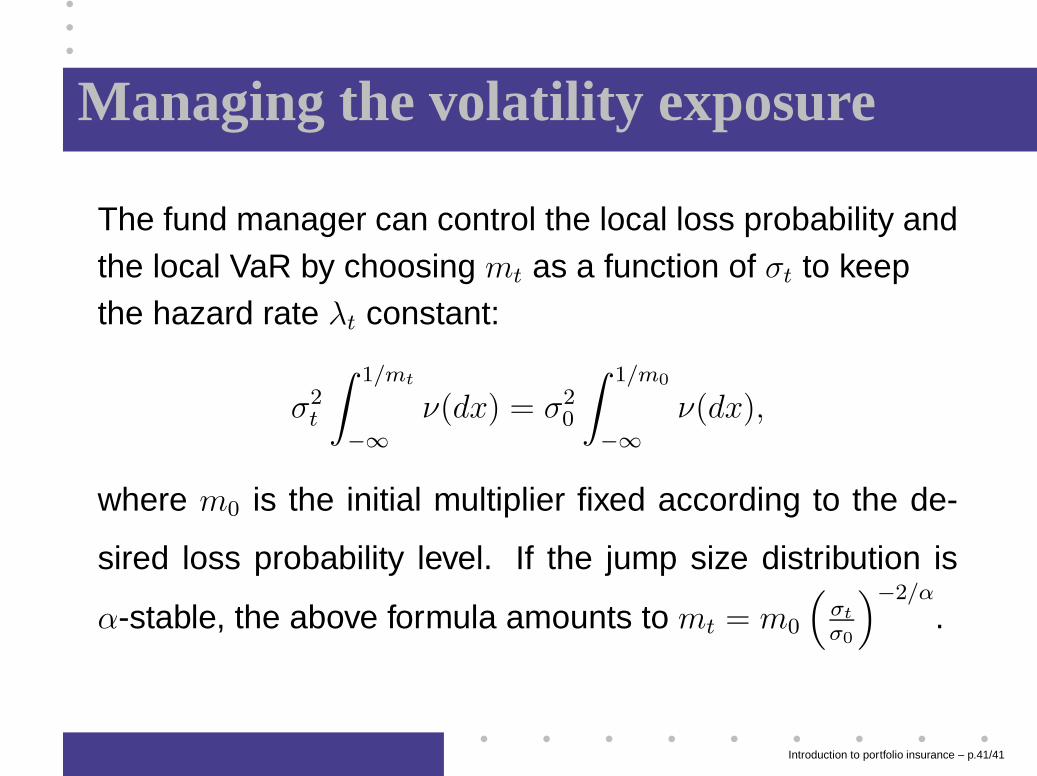

Managing the volatility exposure

The fund manager can control the local loss probability andthe local VaR by choosing mt as a function of σt to keepthe hazard rate λt constant:

σ2t

∫ 1/mt

−∞

ν(dx) = σ20

∫ 1/m0

−∞

ν(dx),

where m0 is the initial multiplier fixed according to the de-

sired loss probability level. If the jump size distribution is

α-stable, the above formula amounts to mt = m0

(

σt

σ0

)−2/α

.

Introduction to portfolio insurance – p.41/41

![NATIONAL HOSPITAL INSURANCE FUND ACT Hospital Insurance Fund Act.pdf · LAWS OF KENYA NATIONAL HOSPITAL INSURANCE FUND ACT CHAPTER 255 Revised Edition 2012 [1998] Published by the](https://img.pdfslide.us/doc/110x75/5e12f81a5e1d572ccb627d42/national-hospital-insurance-fund-act-hospital-insurance-fund-actpdf-laws-of-kenya.jpg)