Embed Size (px)

Citation preview

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 1

UNIT – 01

INTRODUCTION TO ESTIMATION

1.0 Introduction

An estimate is the anticipated or probable cost of work and is usually prepared before

the construction is taken up. It is indeed calculations or computations of various items

of an engineering work.

1.1 The following requirements are necessary for preparing an

estimate:

Drawings.

Detailed specifications

Standard schedule of rates of the current year

1. Drawings: Drawings like plan, elevation and sections of important points, (If the

drawings are not clear and without complete dimensions it becomes difficult to

estimate)

2. Specifications: Detailed specifications about workmanship& properties of materials

etc. There are two types of specifications:

a) General specification

b) Detailed specification.

a)General Specifications: This gives the nature, quality, class and work and materials

in general terms to be used in various parts of wok.

b) Detailed Specifications: These gives the detailed description of the various items of

work laying down the Quantities and qualities of materials, their proportions, the

method of preparation workmanship and execution of work.

3. Standard schedule of rates of the current year: For preparing the estimate the unit

rates of each item of work are required.

1. For arriving at the unit rates of each item.

2. The rates of various materials to be used in the construction.

3. The cost of transport materials.

4. The wages of labour, skilled or unskilled of masons, carpenters, Mazdoor, etc.

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 2

1.2 WHAT ARE THE PURPOSES OF ESTIMATION?

It gives an idea of the cost of the work, i.e whether the project could be taken or

not.

To get administration approvals in case of govt projects

It gives an idea of time required for the completion of the work.

It is required to invite the tenders and Quotations and to arrange contract

It is also required to control the expenditure during the execution of work.

Estimate decides whether the proposed plan matches the funds available or not.

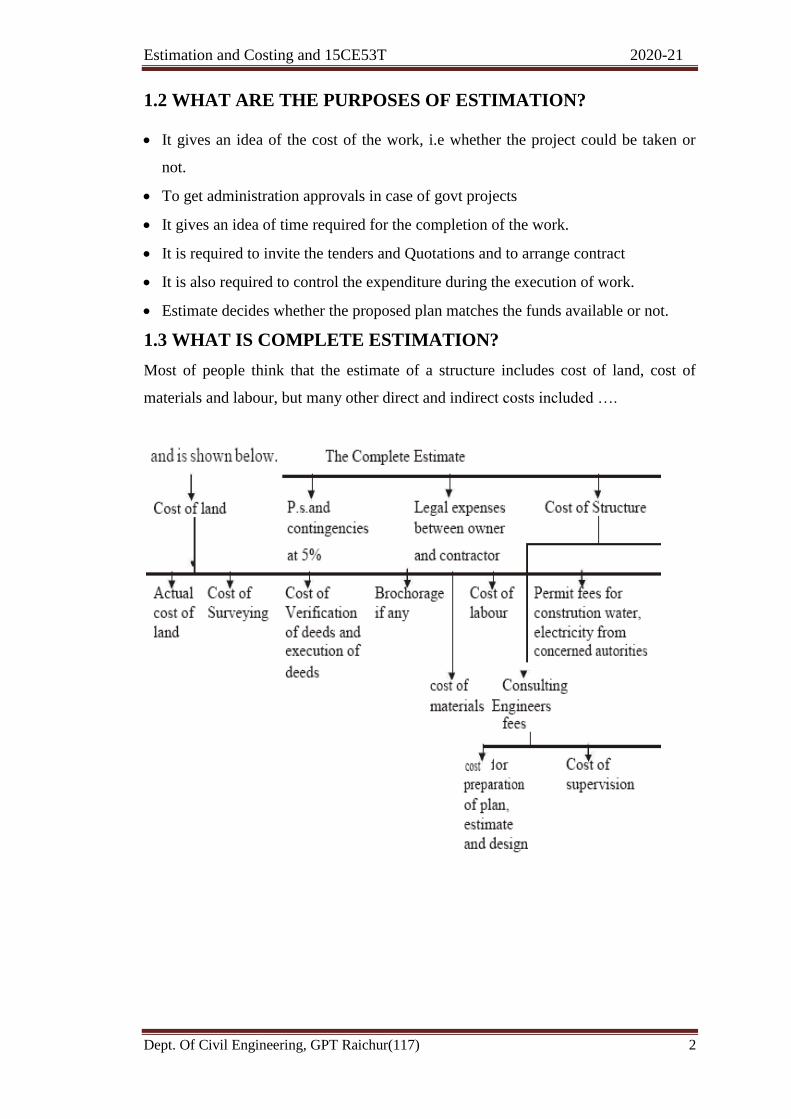

1.3 WHAT IS COMPLETE ESTIMATION?

Most of people think that the estimate of a structure includes cost of land, cost of

materials and labour, but many other direct and indirect costs included ….

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 3

1.4 WHAT ARE THE TYPES OF ESTIMATES?

Preliminary Estimate / Approximate/ Rough estimate

Plinth Area estimate

Cube rate estimate

Approximate quantity method estimate

Detailed estimate / Item rate estimate

Revised estimate

Supplementary estimate

Supplementary & revised estimate

Annual repair and maintenance estimate.

Preliminary Estimate / Approximate/ Rough estimate:

Preliminary estimate is made at the very beginning of a project when there is limited

information available ( means there is no drawing and specification not available), it

is prepared with reference to the cost of similar projects.

Plinth Area Estimate:

In this method plinth area should be calculated by taking the external dimensions of

the building at the plinth level. Other open places shouldn’t be counted (

ex:courtyard), thus plinth area is multiplied by plinth area rate to get the approximate

amount.

Plinth area estimate = plinth area X rate

= (floor area + wall area) X rate

Fig: 01

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 4

Cube Rate Estimate: Cube Rate Estimate of a building is obtained by

multiplying plinth area with the height of building. Height of building should be

considered from floor level to the top of the roof level.

Thus cubical content of the building ( LXBXD) is multiplied by Cubical rate

Cube rate estimate = cubical content X Rate

= ( L X B X D) X Rate

Fig: 02

Approximate quantity method estimate: In this method Approximate total

length of walls is found in running meter and total length is multiplied by rate per

running meter.

For this method drawing should be available.

Approximate quantity method estimate = Total length of the wall X Rate per meter

Detailed Estimate:

The preparation of detailed estimate consists of working out quantities of various

items of work and then determines the cost of each item. This is prepared in two

stages.

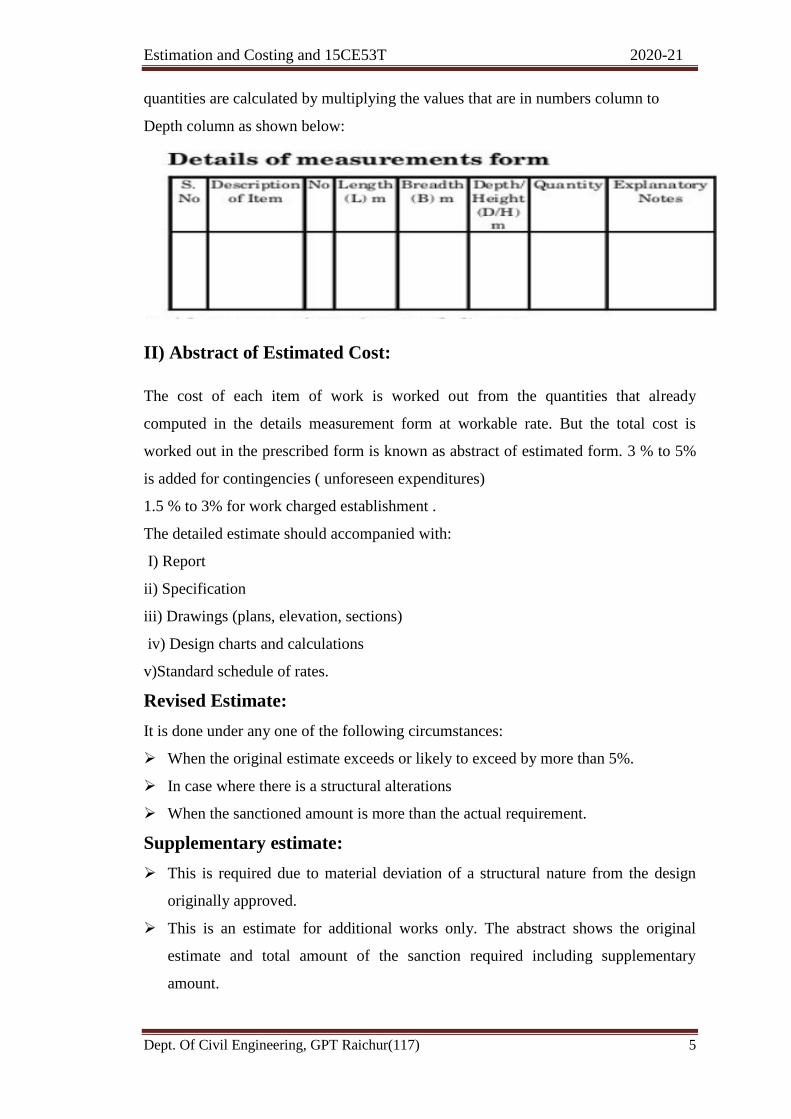

I) Details Of Measurements And Calculation Of Quantities:

The complete work is divided into various items of work such as earth work

concreting, brick work, R.C.C. Plastering etc., The details of measurements are taken

from drawings and entered in respective columns of prescribed preformed. The

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 5

quantities are calculated by multiplying the values that are in numbers column to

Depth column as shown below:

II) Abstract of Estimated Cost:

The cost of each item of work is worked out from the quantities that already

computed in the details measurement form at workable rate. But the total cost is

worked out in the prescribed form is known as abstract of estimated form. 3 % to 5%

is added for contingencies ( unforeseen expenditures)

1.5 % to 3% for work charged establishment .

The detailed estimate should accompanied with:

I) Report

ii) Specification

iii) Drawings (plans, elevation, sections)

iv) Design charts and calculations

v)Standard schedule of rates.

Revised Estimate:

It is done under any one of the following circumstances:

When the original estimate exceeds or likely to exceed by more than 5%.

In case where there is a structural alterations

When the sanctioned amount is more than the actual requirement.

Supplementary estimate:

This is required due to material deviation of a structural nature from the design

originally approved.

This is an estimate for additional works only. The abstract shows the original

estimate and total amount of the sanction required including supplementary

amount.

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 6

Supplementary estimate is required due to some new works or due to change of

design, so additions or revisions of drawings may be necessary.

Supplementary And Revised Estimate: It is prepared when the volume of

the work increased as well as additional works are incurred in the project. In such

cases additional works estimation being done and there is a need of revision of

originally sanctioned amount.

Annual repair and maintenance estimate:

It is prepared to maintain the structure or work in safe condition, it includes repair

works of buildings, Roads, Bridges and culverts.

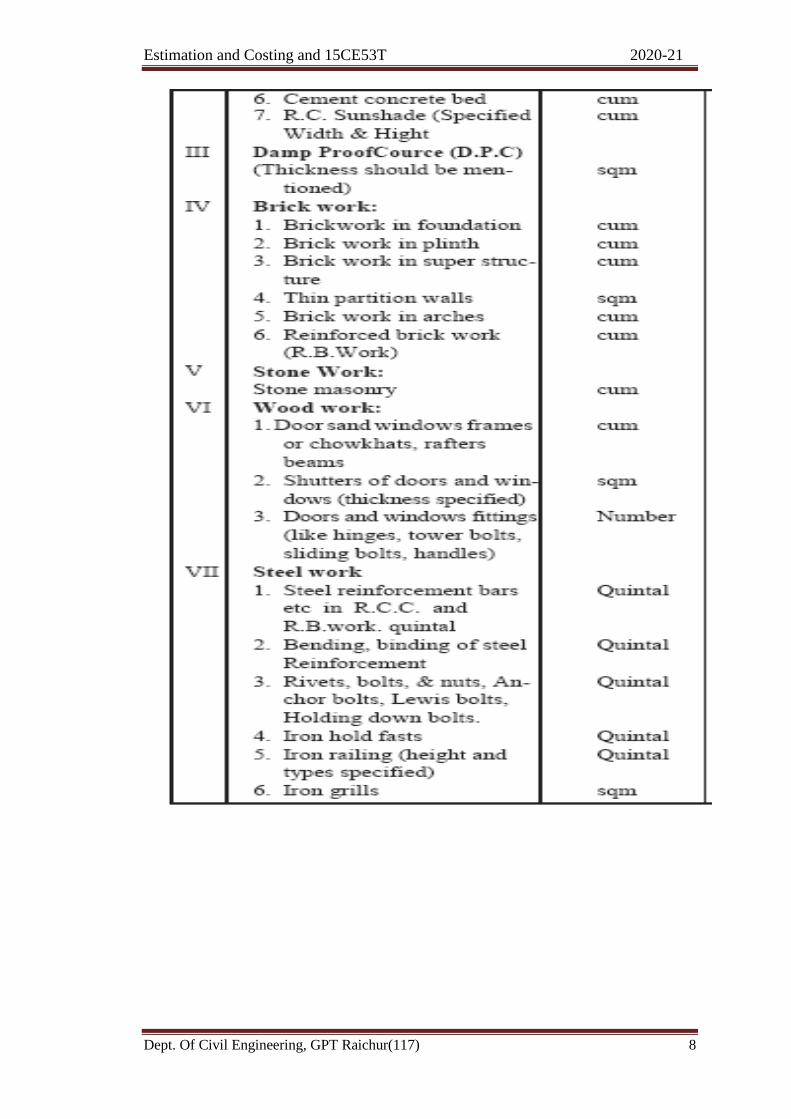

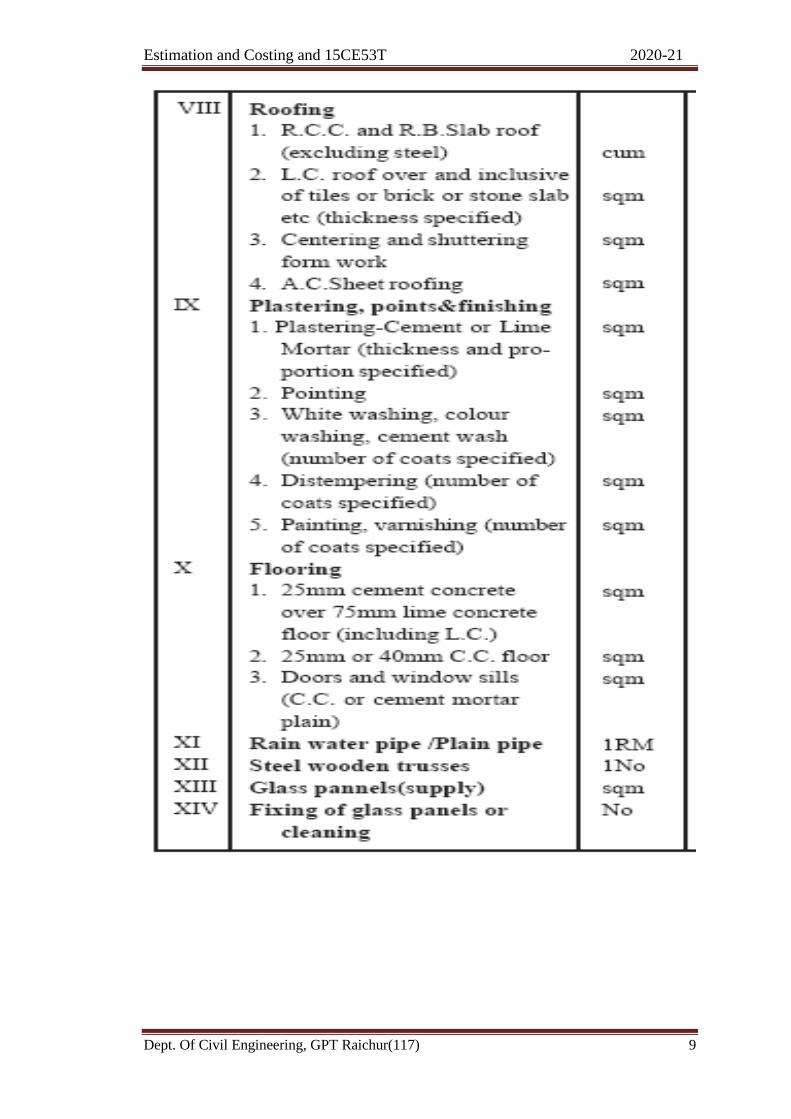

1.5 Units of measurements for different items of works:

The units of measurements are mainly categorized for their nature, shape and size and

for making payments to the contractor and also. The principle of units of

measurements normally consists the following:

Single units work like doors, windows, trusses etc., is expressed in numbers.

Works consists linear measurements involve length like cornice, fencing, hand

rail, bands of specified width etc., are expressed in running metres (RM)

Works consists areal surface measurements involve area like plastering, white

washing, partitions of specified thickness etc., are expressed in square meters (m2)

Works consists cubical contents which involve volume like earth work, cement

concrete, Masonry etc are expressed in Cubic metres

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 7

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 8

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 9

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 10

1.6 Deduction of openings in different items of work and

measurement as per BIS-2000

Plastering

Plaster work shall be classified according to the material used and each classification

shall be measured separately.

Rules for measurements:

Plastering on roofs, ceilings and walls shall be measured separately.

Removing plaster by scraping or otherwise shall be measured separately in square

metres.

Plastering at a height greater than 10 m above ground/datum level shall be

measured separately in stages of 5-m height except interior plastering in case of

building which shall be measured separately for each storey.

All plastering shall be measured in square metres unless otherwise described.

Rules for Deduction:

For jambs, soffits, sills, etc; for openings not exceeding 0.5 m2 each in area, for ends

of joists, beams, posts, girders, steps, etc, not exceeding 0.5 m2 each in area, and for

openings exceeding 0.5 m2 and not exceeding 3 m2 in each area, deductions and

additions shall be made in the following manner:

No deduction shall be made for ends of joists, beams, posts, etc, and openings not

exceeding 0.5 m2 each and no addition shall be made for reveals, jambs, soffits,

sills, etc, of these openings nor for finish to plaster around ends of joists, beams,

posts, etc.

Deductions for openings exceeding 0.5 m2 but not exceeding 3 m2 each shall be

made as follows and no addition shall be made for reveals,jambs, soffits, sills, etc,

of these openings:

1)When both faces of wall are plastered with same plaster, deduction shall be made

for one face only.

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 11

2)When two faces of wall are plastered with different types of plaster or if one face is

plastered and the other pointed, deduction shall be made from the plaster or pointing

on the side on which width of reveals is less than that on the other side but no

deduction shall be made on the other side. Where widths of reveals on both faces of

wall are equal, deduction of 50 percent of area of opening on each face shall be made

from areas of plaster and/or pointing as the case may be.

3)When only one face is plastered and the other face is not, full deduction shall be

made from plaster if width of reveal on plastered side is less than that on unplastered

side hut if widths of reveal on both sides are equal or width of reveal on plastered side

is more, no deduction shall be made.

4) When width of door frame is equal to thickness of wall or is projecting beyond

thickness of wall, full deduction for opening shall be made from each plastered face

of the wall.

In case of openings of area above 3 m2 each, deduction shall be made for opening on

each face but jambs., soffits and sills shall be measured.

1.7 BILL OF QUANTITIES: A bill of quantities (BOQ) is a document used in

tendering in the construction industry / supplies in which materials, parts, and labor

(and their costs) are itemized. It also (ideally) details the terms and conditions of the

construction or repair contract and itemizes all work to enable a contractor to price the

work for which he or she is bidding .The quantities may be measured in number,

length, area, volume, weight or time. Preparing a bill of quantities requires that the

design is complete and a specification has been prepared. The bill of quantities is

issued to tenderers for them to prepare a price for carrying out the works. The bill of

quantities assists tenderers in the calculation of construction costs for their tender,

and, as it means all tendering contractors will be pricing the same quantities (rather

than taking-off quantities from the drawings and specifications themselves), it also

provides a fair and accurate system for tendering.

1.8 SCHEDULE OF RATES:It is available in printed book format, it contains

list of various items of works, including material rate, labour wages and transportation

charges etc..provided by the PWD( Public Works Division)

Estimation and Costing and 15CE53T 2020-21

Dept. Of Civil Engineering, GPT Raichur(117) 12

1.9 LEAD STATEMENT: Lead statement: The distance between the source of

availability of material and construction site is known as "Lead” and is expected in

Km. The cost of conveyance of material depends on lead.

This statement will give the total cost of materials per unit item. It includes first cost,

conveyance loading, unloading stacking, charges etc.