Embed Size (px)

DESCRIPTION

Introduction of Panel Members. Sarbanes-Oxley Section 404 Overview. Insert Worlds Image / Client Specific Image Here. Scott Henderson [email protected] August 5, 2005. The Birth of the Sarbanes-Oxley Act of 2002. - PowerPoint PPT Presentation

Citation preview

1

Introduction of Panel MembersSarbanes-Oxley

Section 404 Overview Insert

Worlds Image /

Client Specific Image

Here

Scott [email protected]

August 5, 2005

2

The Birth of the Sarbanes-Oxley Act of 2002

Corporate and accounting scandals involving a limited number of large, prominent companies have resulted in a significant loss of public trust in corporate accounting and reporting practices.

In response, the U.S. Congress enacted the Sarbanes-Oxley Act of 2002 to establish a higher corporate governance standard.

The primary objectives of Sarbanes-Oxley are to:

Prevent accounting and reporting problems from recurring

Rebuild public trust in corporate practices and reporting

Define a higher level of responsibility, accountability and financial reporting transparency

Provides penalties and fines for wrongdoings.

3

Sarbanes-Oxley Act – Quick Refresher

The Act was signed into law on July 30, 2002 and includes the following eleven titled sections:

Title I Creation of Public Company Accounting Oversight Board

Title II Auditor IndependenceTitle III Corporate Responsibility Title IV Enhanced Financial DisclosuresTitle V Analyst Conflicts of InterestTitle VI Commission Resources and AuthorityTitle VII Studies and ReportsTitle VIII Corporate and Criminal Fraud AccountabilityTitle IX White Collar Crime Penalty EnhancementsTitle X Corporate Tax ReturnsTitle XI Corporate Fraud and Accountability

4

Enhanced Financial Disclosures - Section 404

Kodak management must now assess internal controls annually. This requires:

Section 404(a)(1) - An internal control report to be prepared by Kodak management stating management’s responsibility for establishing and maintaining an adequate internal control structure and procedures for financial reporting.

Section 404(a)(2) - Management must assess effectiveness of internal control structure and procedures for financial reporting as of the end of the most recent fiscal year.

Both Kodak AND individual members of company management are subject to potentially significant criminal and civil penalties for noncompliance with this new legislation.

5

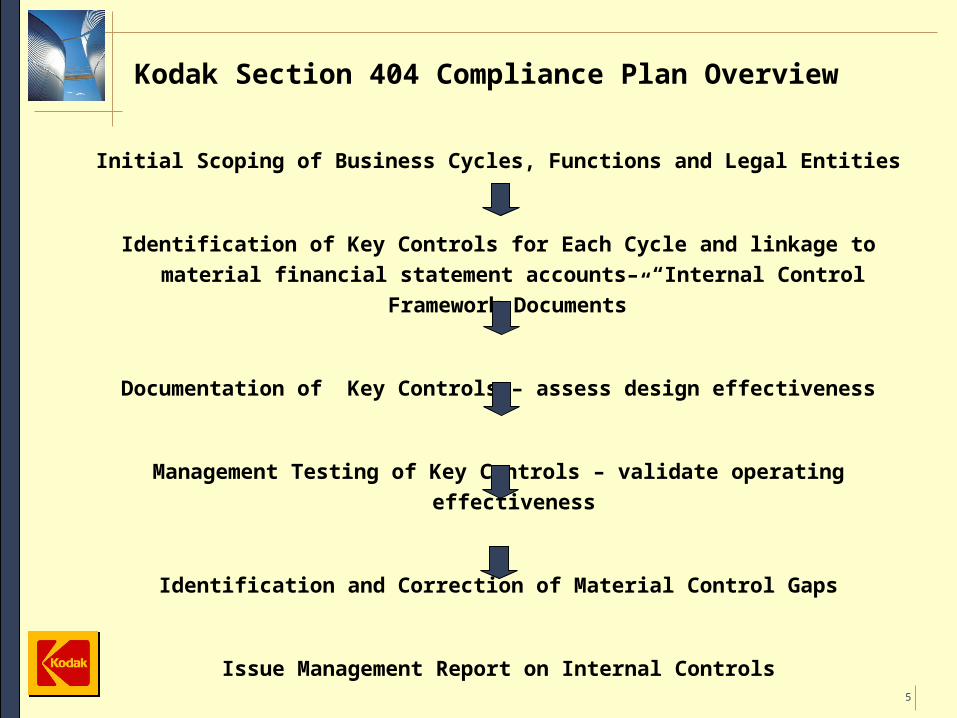

Kodak Section 404 Compliance Plan Overview

Initial Scoping of Business Cycles, Functions and Legal Entities

Identification of Key Controls for Each Cycle and linkage to material financial statement accounts– “Internal Control

Framework Documents”

Documentation of Key Controls – assess design effectiveness

Management Testing of Key Controls – validate operating effectiveness

Identification and Correction of Material Control Gaps

Issue Management Report on Internal Controls

6

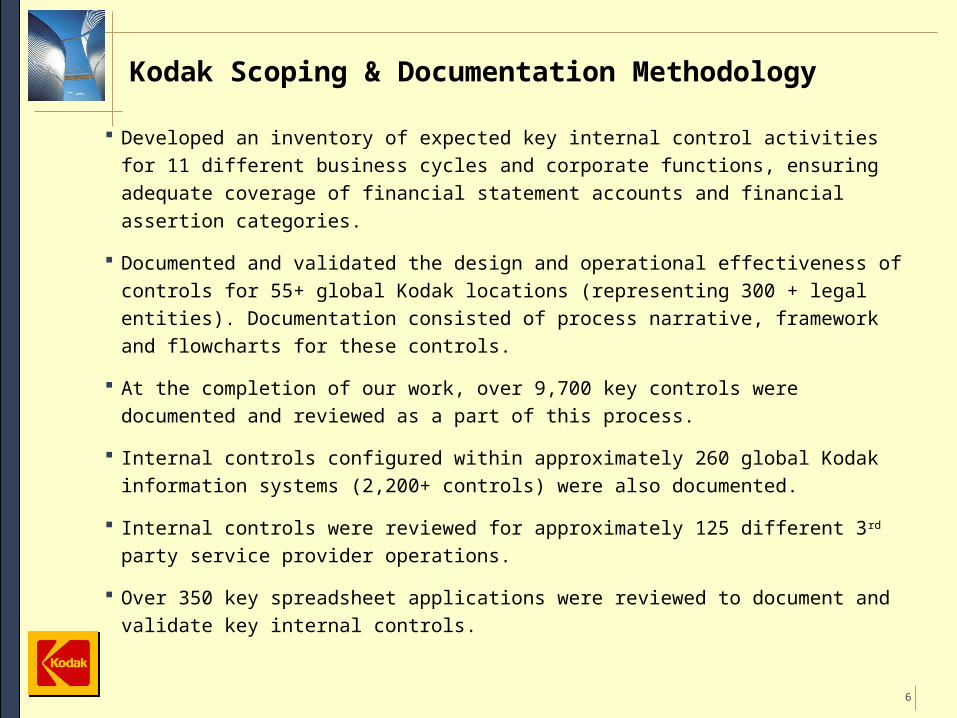

Kodak Scoping & Documentation Methodology

Developed an inventory of expected key internal control activities for 11 different business cycles and corporate functions, ensuring adequate coverage of financial statement accounts and financial assertion categories.

Documented and validated the design and operational effectiveness of controls for 55+ global Kodak locations (representing 300 + legal entities). Documentation consisted of process narrative, framework and flowcharts for these controls.

At the completion of our work, over 9,700 key controls were documented and reviewed as a part of this process.

Internal controls configured within approximately 260 global Kodak information systems (2,200+ controls) were also documented.

Internal controls were reviewed for approximately 125 different 3rd party service provider operations.

Over 350 key spreadsheet applications were reviewed to document and validate key internal controls.

7

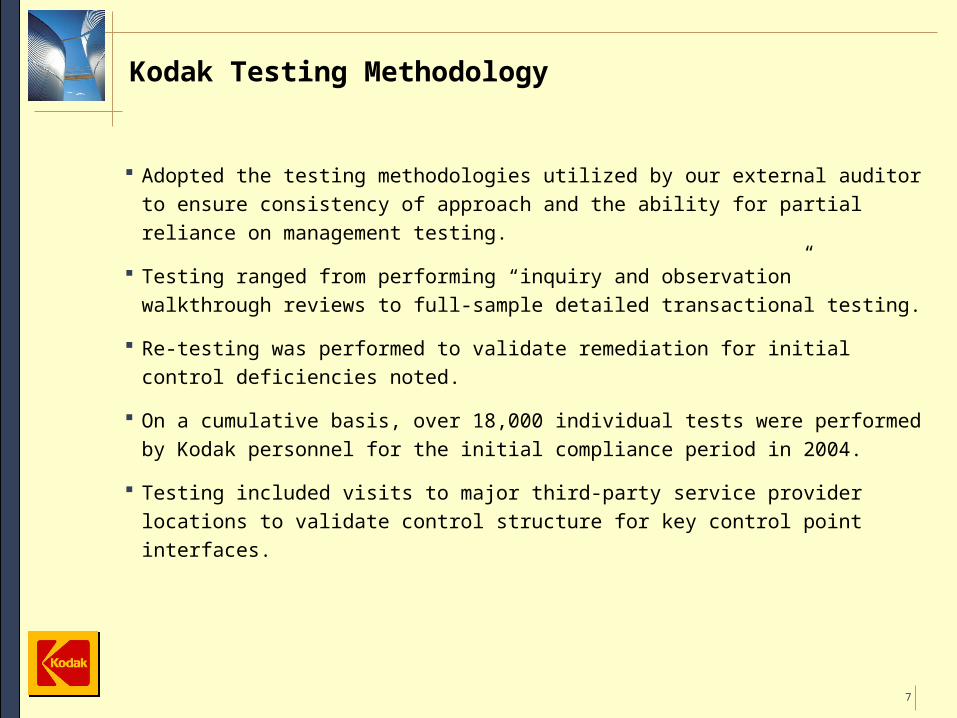

Kodak Testing Methodology

Adopted the testing methodologies utilized by our external auditor to ensure consistency of approach and the ability for partial reliance on management testing.

Testing ranged from performing “inquiry and observation” walkthrough reviews to full-sample detailed transactional testing.

Re-testing was performed to validate remediation for initial control deficiencies noted.

On a cumulative basis, over 18,000 individual tests were performed by Kodak personnel for the initial compliance period in 2004.

Testing included visits to major third-party service provider locations to validate control structure for key control point interfaces.

8

Kodak Testing Results

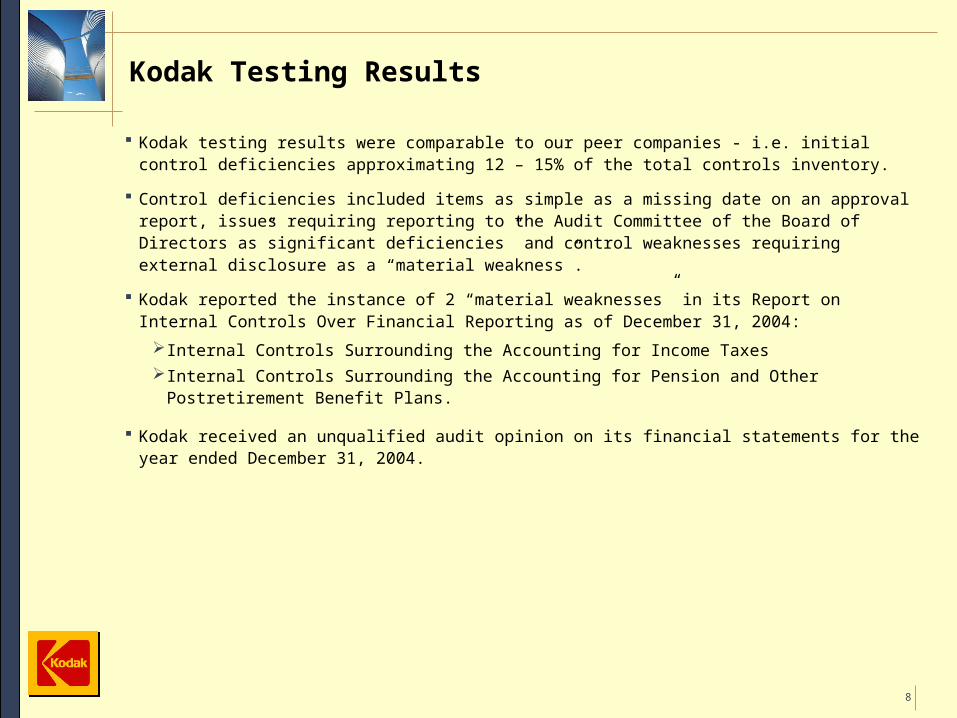

Kodak testing results were comparable to our peer companies - i.e. initial control deficiencies approximating 12 – 15% of the total controls inventory.

Control deficiencies included items as simple as a missing date on an approval report, issues requiring reporting to the Audit Committee of the Board of Directors as”significant deficiencies” and control weaknesses requiring external disclosure as a “material weakness”.

Kodak reported the instance of 2 “material weaknesses” in its Report on Internal Controls Over Financial Reporting as of December 31, 2004:

Internal Controls Surrounding the Accounting for Income TaxesInternal Controls Surrounding the Accounting for Pension and Other Postretirement

Benefit Plans.

Kodak received an unqualified audit opinion on its financial statements for the year ended December 31, 2004.

9

Kodak Costs of Compliance

External audit fees related to Kodak Section 404 internal controls activities - $7.1 million.

Comparable costs were incurred for internal resources dedicated to Section 404 compliance activities.

The average cost of Section 404 compliance incurred by most multi-national corporations was $1 million for each $1 billion of revenues.

Full-time equivalent Kodak resources dedicated to 2004 Section 404 internal control compliance activities – 45+. Additional co-source external resources were engaged to assist with compliance activities.

Estimated Kodak resource hours expended on 2004 Section 404 internal control compliance activities – 55,000+.

10

Key Benefits Gained From Sarbanes-Oxley in 2004

Strengthened global internal control environment. Reinforced the notion with all business constituents that “good controls mean good business”.

Helped Kodak identify and strengthen existing entity-wide governance and internal controls improvement opportunities.

Facilitated the identification of operational best practices and efficiency opportunities:

Standardized business processes and controlsWorking to streamline our legal entity structure

Compliance with Sarbanes–Oxley in 2004 has positioned us well to comply with comparable legislation currently being enacted elsewhere around the globe.

11

Sarbanes-Oxley – Opportunities for Improvement

Year 1 was a learning opportunity for all parties involved in terms of expectations, approach and results.

More focus on risk-based approach vs. simply “executing the audit program”. Implementation of “COSO II” and its risk based approach will help.

Section 302 – the “forgotten” section of Sarbanes-Oxley. Need continued focus on top-level “tone at the top”, governance and

corporate culture issues and controls. Public perception and understanding of the implications of Sarbanes-

Oxley is not there yet – impacts on shareholder value vs. benefits gained.

12

Sarbanes–Oxley Compliance Actions in 2005

Creation of a dedicated Global Internal Controls organization charged with coordination of ongoing Sarbanes-Oxley compliance by 1,100 global business process control owners.

Remediation of identified 2004 material weaknesses by 9/30/05. Acquisition and implementation of a Sarbanes-Oxley compliance and

reporting software package. Initial year Sarbanes-Oxley compliance work for $2 billion of acquisitions

completed in 2005. Operationalization and simplification of the 2004 compliance approach.

Implementation of the PCAOB guidance in May 2005.