Embed Size (px)

Citation preview

1

Introducing the Credit Card

2

5

8

11

13

15

18

19

– What a credit card is

– How a credit card works

– Fees associated with credit cards

– How to apply for a credit card

– How to avoid credit card debt

– How rewards programs work

– How to choose the right credit card for you

With the help of detailed explanations, simple exercises, and visual aids, you will soon be fully prepared to apply for and use a credit card.

Introducing the Credit Card

What is a credit card?

How does a credit card work?

Do credit cards have fees?

How can I apply for a credit card?

How can I avoid credit card debt?

How do rewards programs work?

Which credit card should I choose?

Glossary

This program was designed with high school students in mind. It goes over everything you need to know before you get your first credit card so you can manage it wisely.

» Ke

y To

pics

» T

able

of C

onte

nts

2

Introducing the Credit Card »

Wha

t is a

cre

dit

card

? By now, you have probably seen hundreds of credit cards in your life. They have changed the way people spend money online and in stores, and chances are you’ll get one when you’re on your own. Before you do that though, you need to know what a credit card is and how you should use it. This guide will help you out.

A credit card is a plastic card that represents a line of credit. A line of credit is an account with money that you can borrow repeatedly. In most cases, this is not going to be your money. It is going to come from a credit card issuer, like Chase or CitiBank. You will usually have more than one issuer for a single card. Your account will be assigned a certain limit based on the information from your application. Then you can swipe your card as needed to spend money out of it.

The money you spend on a credit card has to be paid back. If you do not make your payments by a certain day of the month, you will have to pay interest, and potentially a late fee. We’ll go over all of this in a little bit, but you have to understand one thing…

A credit card is not a source of free money.

This is not a scholarship, donation, gift, or anything along those lines. It’s something you can use when you need money, assuming you will pay it back.

Parts of a Credit Card

– Hologram: This is a 3D image, usually in gold, that verifies a real card from a counterfeit.

– Issuing Bank: This is the bank that sponsors the card. If there is no issuing bank, this part will have the card name or a blank spot.

– Card Number: This is a 16-19 digit number that represents the line of credit on the card. Every card number is unique, and it acts as the ID for the credit card. (Think about your driver’s license number for reference.)

– Issue Date: This is the date that the card was created. Not all credit cards have this.

– Expiration Date: This is the date that the card will no longer be valid. You must get a new card before this day, or you will not be able to access your account until a new card comes in.

3

Introducing the Credit Card

– Card Brand: This is similar to the issuing bank, but it represents the credit card company that manages the card. Examples include Visa, MasterCard, Discover, and American Express.

– Cardholder: This is the full name of the person or business that owns the card. If the card is for a specific person in a business, it may include both the first and last name of the person and the business name.

– Help Line: The customer service number for the card brand or the issuing bank, depending on the card.

– Magnetic Strip: This is a strip of information that a card machine reads to identify one card from another. (Think about a CD player reading the numbers on the back of a CD.)

– Signature Box: This is the area you are supposed to sign so no one else can use your credit card.

– Verification: This is a code that further identifies a credit card. It contains the last four digits of the card number, followed by three or four numbers. Those numbers make up the card verification value (CVV), which is also known as the CID for American Express, the CVV2 for Visa, and the CVC2 for MasterCard. You will probably only need this when you’re making payments by phone or online.

– Card Number: This is the reverse of the 16-19 digit number form the front of the card. Sometimes this is faded, but you will still be able to see the indentions for the numbers.

– Disclaimer: This is a note from the issuing bank or credit card company ensuring that you know the agreement associated with the card.

– Bank Address: This is the address someone should release the card to in the event that you lose it. It also acts as an address you can send mail inquiries to. Some banks will add an email address or website to this line for further contact information.

4

Introducing the Credit Card

Exercise 1

Choose the best answer.

1. What is a credit card?

A: A plastic card with a magnetic strip on the back

B: Something that represents a line of credit

C: A source of free money.

D: Both A and B

2. Which of these could be a credit card number?

A: 1122 2542 2565 215

B: 4670 1016 4923 7710

C: 5581 5820 4387 0956 1370

D: All of the above

3. How many digits are in a standard credit card number?

A: 16

B: 17

C: 18

D: 19

E: A credit card number can be 16 to 19 digits long.

4. What happens after the expiration date on a credit card?

A: The card no longer works

B: The cardholder has to get a new card

C: The card blows up

D: Both A and B

5. How many numbers are in a CVV code?

A: 1

B: 2

C: 3

D: 4

E: 3 or 4

5

Introducing the Credit Card »

How

doe

s a c

red

it ca

rd w

ork?

Credit Card Processing

A credit card works a lot like a CD (you know, that thing people used before iPods came out). When you put a CD into a CD player, the reader in the machine analyzes codes on the back of the CD. In the end, you hear music, voices, or other sounds. With a credit card, the magnetic strip on the back of the card contains coded information about the card itself. When you swipe your card at a register, the card reader picks up on that information to identify the card.

In some cases, you don’t actually have to swipe your card to use it. You may use your credit card number, expiration date, and CVV code to identify the card. Some websites and businesses will also ask for the zip code for the billing address, which is something that is not visible on the outside of the card. They do this to prevent someone else from stealing and using your credit card.

We could make a whole book about credit card processing, but we’ll try to keep this simple. When you swipe a credit card, your account information is passed through several companies in a matter of seconds. The basic steps of the process are as follows:

Step 1 – AuthorizationThis is the only step that happens while you are at the register. The merchant you make a purchase through will send your credit card information to an acquirer, which is the messenger between the merchant and the credit card company. The acquirer sends the request to an issuer or a set of issuers, which would be the credit card company and/or the issuing bank. If the issuer says you have enough money in your account, it will give the acquirer permission to run the card. Then the acquirer will give approval to the merchant.

Long story short, someone asks if your card is good to go, and then someone else answers yes or no. Step 2 – BatchingAt the end of the night, a merchant will gather all of the transactions from the day and put them into a “batch.” This batch is re-sent to the acquirer, who then passes the information through to the issuers. This is all done so the merchant can get money from the credit card companies and banks.

6

Introducing the Credit Card

Step 3 – ClearingOnce the issuers assess the batches, they will take out whatever their fees are and send the rest of the money to the acquirer. This step is called “clearing” because the issuers have to clear the funds to send out. Most of these funds will ultimately go to the merchant.

Step 4 – Funding This is the last step of the process, where the merchant finally gets its money. The acquirer will take out a small portion of the money to cover its expenses, and then it will send all the rest to the merchant. At this time, your credit card is officially charged for the purchase, and you should see the money clear your account.

Credit Card Payments

When processing is complete, you will get a charge on your credit card account that you have to pay back. This will probably be removed from your balance right away, but it may not show up on your credit card statement until several days later. This is the “bill” for your credit card, which highlights all of your transactions and payments for the month.

Most credit card companies will offer several ways to make payments. You could:

– Pay online

– Pay over the phone

– Pay through the mail

– Pay at a store or bank

– Pay with another card (through a balance transfer)

– Pay through an auto-debit (where the company takes money directly from your bank account or pay check)

You will at least need to make a minimum payment for every month that you have a balance on your card. If you do not owe any money, you obviously won’t have to pay anything. If you fail to make your payments on time or you simply cannot make your payments all at once, you will have to pay several extra fees beyond the minimum payment. Your minimum monthly payment will vary in value based on your credit card, but it is usually 2% of the balance or $15 (whichever is higher).

7

Introducing the Credit Card

Exercise 2

Choose the best answer.

1. True or false: You have to swipe a credit card to use it.

A: True

B: False

2. Which parties participate in credit card processing?

A: The issuer, the director, and the buyer

B: The acquirer, the analyst, and the accountant

C: The merchant, the acquirer, and the issuer

D: The authorizer, the batcher, and the lender

3. What are the steps of credit card processing?

A: Authorization, batching, sorting, and funding

B: Batching, acquiring, issuing, and lending

C: Clearing, funding, batching, and selection

D: Authorization, batching, clearing, and funding

4. Which of the following is not a way to pay off a credit card?

A: At a store or bank

B: With another credit card

C: On the phone

D: All of these will work as credit card payment options

5. What is the approximate minimum payment for a card with a $1,000 balance?

A: $15

B: $20

C: $100

D: $200

8

Introducing the Credit Card »

Do

cred

it ca

rds h

ave

fees

? You can’t understand how a credit card works without learning about the fees associated with it. Some credit cards have more fees than others, but they all have some sort of carrying costs. The most common credit card fees include:

– Annual Fee: This is money that you have to pay every year for using a credit card. It could be $0, or it could be $250+. It just depends on the card you get.

– Application Fee: This is a fee you may have to pay to apply for a card. This is mostly for cards with extensive rewards programs, and it is used to cover the time and money spent checking your credit.

– APR: This is the annual percentage rate, or the amount of interest that is charged on a balance over the course of a year. If you pay back your balance within a certain time frame (usually 25-30 days), you can avoid this charge. Since this is an annual rate, it represents the interest paid in all the months combined. To calculate the interest for an individual time frame, simply divide your rate by the number of days or months in question. (A monthly percentage rate would be approximately 1/12 of the APR)

– Balance transfer Fee: This is a fee you pay if you move the balance of your card to another card. Most people will do this to combine the debt from several cards into one, thereby having fewer bills to pay. In most cases, this is 1-3% of the balance.

– Cash Advance Fee: This is a fee that you have to pay when you withdraw money from the card at an ATM. It is usually around 2% of the money withdrawn.

– Decline Fee: This fee is charged to your account when you try to make a payment on something you do not have the money for. It is similar to the return check fee a bank may charge if a check bounces on your account. It can be as much as $35, but some credit cards will not ask for this.

– Foreign Transaction Fee: This fee shows up when you buy something overseas. It is used to cover the cost of transferring your money into foreign currency. Not all credit cards have this.

– Late Fee: This is a fee charged to you in the event that you do not make your payments on time. It is usually $10-$25, and it will be considered part of your minimum credit card payment.

– Over-the-limit Fee: This is a charge for times when you go over your maximum credit card limit. If your account has only been approved for $750, a balance of $800 would lead to an over-the-limit fee. This will vary in value by credit card, but most of the time it is around $30.

Note that not all cards carry all of these fees. In fact, some cards have absolutely no fees at all. You may also see “other fees” or “miscellaneous fees” on your credit card statements. These are terms used to cover any extra costs associated with the card. They could be anything from payment for customer support to charges for identity theft insurance. You will have to ask your credit card provider for more information about the fees on your account.

For example:

Let’s pretend that you have a credit card with a $1,500 balance on it. Your card gives you up to 25 days to make a payment without any penalties or fees. It is now 34 days since the bill was due.

9

Introducing the Credit Card

The card has an APR of 13%, as well as a $10 late fee and a 2% minimum payment plus interest.

Interest:

.13/12 months = .01083% interest for the month

.01083 x $1,500 = $16.25

Minimum Payment:

.02 x $1,500 = $30

For this card, the minimum payment will be 2% of the balance + the interest + the late fee.

$30 + $16.25 + $10 = $56.25

You would at least need to pay $56.25 to keep your account in good standing.

10

Introducing the Credit Card

Choose the best answer.

1. What does APR stand for?

A: Annual purchase rate

B: Annual percentage rate

C: Approximate payment rotation

D: Authorization processing rate

2. Which fees do all credit cards have?

A: Annual fees

B: Over-the-limit fees

C: Foreign transaction fees.

D: Some credit cards have no fees at all.

3. When do you have to pay a cash advance fee?

A: When you move a balance from one card to another

B: When you do not make your payments on time

C: When you spend more than your limit on a card

D: When you withdraw money from an ATM

4. If a card has a $2,400 balance and a minimum payment of 4%, what would you need to pay to

keep your card in good standing? Assume that there are no other fees involved.

A: $40

B: $24

C: $96

D: $240

5. What would be the approximate one-month interest be for a $5,000 credit card balance with a

12% APR?

A: $120

B: $600

C: $500

D: $50

Exercise 3

11

Introducing the Credit Card »

How

can

I ap

ply

for a

cre

dit

card

?

Parts of a Credit Card Application

Applying for a credit card is surprisingly simple, especially if you don’t have to pay an application fee. All you have to do is fill out a form and hope that you get approved. You must be 18 or older to apply for any type of credit card, and you must have a job. This shows that you will have the income to pay for the card after making a purchase with it.

You can either complete an application online, through the mail, or in a store, depending the card you want to get. Online applications can be approved in seconds, but mail-in ones may not be approved for 7-10 business days. This is why most people apply for cards online nowadays. It’s just easier to do in the long run.

Every credit card application is a little different, but the overall information is the same. Here are some common components of a credit card application:

– Card Features: Most credit cards will include a statement at the beginning of an application that explains what the card is and what fees/rewards are associated with this. You do not have to fill anything out in this section, but you should look over it.

– Personal Information: This will include your name, address, phone number, email address (sometimes), date of birth, and your social security number. For some applications, you only need to include the last four digits of your social security number, or you may not need to include anything at all. You may also need to provide a previous address if you have lived in your current home for less than three years. If you are a college student, the card company may further request the address of your “permanent residence,” since you will only live at school for part of the year.

– Financial Information: This will include information about your job and your annual income. A credit card company will want to know where you work, how long you have been there, and how much you make before taxes.

– Additional User Information: This is for people who want to get secondary cards for their accounts. If you want to give someone else the chance to use your credit card, you will need to provide his or her name, address, and phone number.

– Terms and Disclaimers: This is a long list of terms that you will agree to if you decide to complete the application. In mail-in applications, this will usually be at the back. In online applications, it may be accessible through a link somewhere on the page. It could also be in a scroll-down list, right before you virtually sign your application.

Again, this format may be different for a credit card you apply for, but it represents the general information you will read and provide on the application. See the sample credit card application at the end of this document for more information.

12

Introducing the Credit Card

Choose the best answer.

1. How old do you have to be to apply for a credit card?

A: 21

B: 18

C: 16

D: 13

2. Do you have to provide your social security number to apply for a credit card?

A: Yes

B: No

C: It depends on the credit card.

3. Complete the sample application at the end of this document.

Exercise 4

13

Introducing the Credit Card »

How

can

I av

oid

cre

dit

card

deb

t?

Causes of Credit Card Debt

A lot of high school graduates avoid getting a credit card because they don’t want to be in debt. Having a credit card doesn’t mean that you’re going to ruin your credit and owe a bunch of money to someone. In fact, credit cards can actually improve your credit score. You just have to know how to manage them correctly.

There are two causes of credit card debt: bad spending and bad payments. Either you will spend more money than you can logically pay back, or you will fail to pay on a balance you owe. Both of these problems are avoidable, but don’t be surprised if you fall into one or both of them at first. It’s easy to get caught up in the excitement of spending before you realize what kind of situation you’ve put yourself in.

How to Avoid Credit Card Debt

Avoiding credit card debt is a simple process. Once you find a system that works for you, all you have to do is repeat the process. Here are some tips to help you manage your credit card:

– Don’t buy anything you don’t already have the money for. If you can pay your credit card back immediately, you will still get the credit for it without worrying about debt.

– Always keep track of your balance. Know what you have spent, what you can spend, and what you need to spend in the future. This will help you avoid overdraft fees, embarrassing declines, and most importantly…credit card debt.

– Avoid high interest rates or high annual fees. If it costs you $75 to have a credit card that you rarely use, it isn’t worth the money. Look for a card with minimal fees that match your spending habits.

– Reserve your card for emergencies. This won’t help your credit much, but it will help you avoid debt. You might want to train yourself not to use the card until you feel capable to do so responsibly.

– Watch your account for suspicious activity. This will protect you against identity theft. If you notice anything on your account that you did not authorize, contact your credit card company right away.

As you can see, you don’t have to bypass credit cards completely to avoid the debt associated with them. If you manage your money the way you are supposed to, you can build your credit and have funds left over for backup. There is no sense in having a credit card if you can’t see any practical use for it. Keep that in mind before you apply.

14

Introducing the Credit Card

Choose the best answer.

1. True or false: You cannot have a credit card without getting credit card debt.

A: True

B: False

2. What are the causes of credit card debt?

A: Bad spending

B: Bad payments

C: Bad shoes

D: Both A and B

Exercise 5

15

Introducing the Credit Card »

How

do

rew

ard

s pro

gram

s wor

k?

Different Types of Rewards

Rewards, rewards, rewards. They sound so enticing from afar. Many credit card companies will try to lure in applicants with rewards programs because that gives them more of a reason to use their cards. You may find great success with these rewards, but you cannot be fooled by them. In many cases, they aren’t all they’re made out to be.

Some cards offer one specific kind of reward, and others offer a variety of rewards throughout the year. Common reward offers include:

– Cash Back: This is money that you get back after buying certain things on your card. It will usually be 1-5% of the purchase price, and it can be used on new purchases once you pay off your balance.

– Gas Rewards: These will give you money back for purchases you make at a gas station.

– Air Miles: These are usually tracked as points that you can cash in for airline tickets in the future. Each ticket will hold a certain point value (usually in the hundreds), so you have to rack up a lot of them to be able to get a free plane ticket.

– Travel Rewards: These are similar to air miles, but they cover hotel fees, cruises, and more. You might be able to use your points on package deals through your credit card company, or you could cash them in for a specific hotel, rental car, airplane, etc.

In addition to these rewards, some cards offer discounts for travel accommodations, online purchases, and more. Simply put, you could save money on the things you need most just by paying with your credit card. Of course, you will have to make sure the card’s carrying costs do not exceed its rewards. If you manage your money correctly though, a rewards program may work in your favor.

Calculating Rewards

Since every card’s rewards program is a little different, it is hard to set up a definitive formula to help you calculate the rewards you can get. Instead of doing that, we’ll show you what the rewards might look like on the Capital One Cash Rewards card.

Capital One Cash Rewards Card Features– 1% cash back on all purchases

– 50% bonus on the cash back you earn every year

– 0% intro APR for the first year (the time frame will vary)

– 19.8% APR after the intro period

– $39 annual fee

16

Introducing the Credit Card

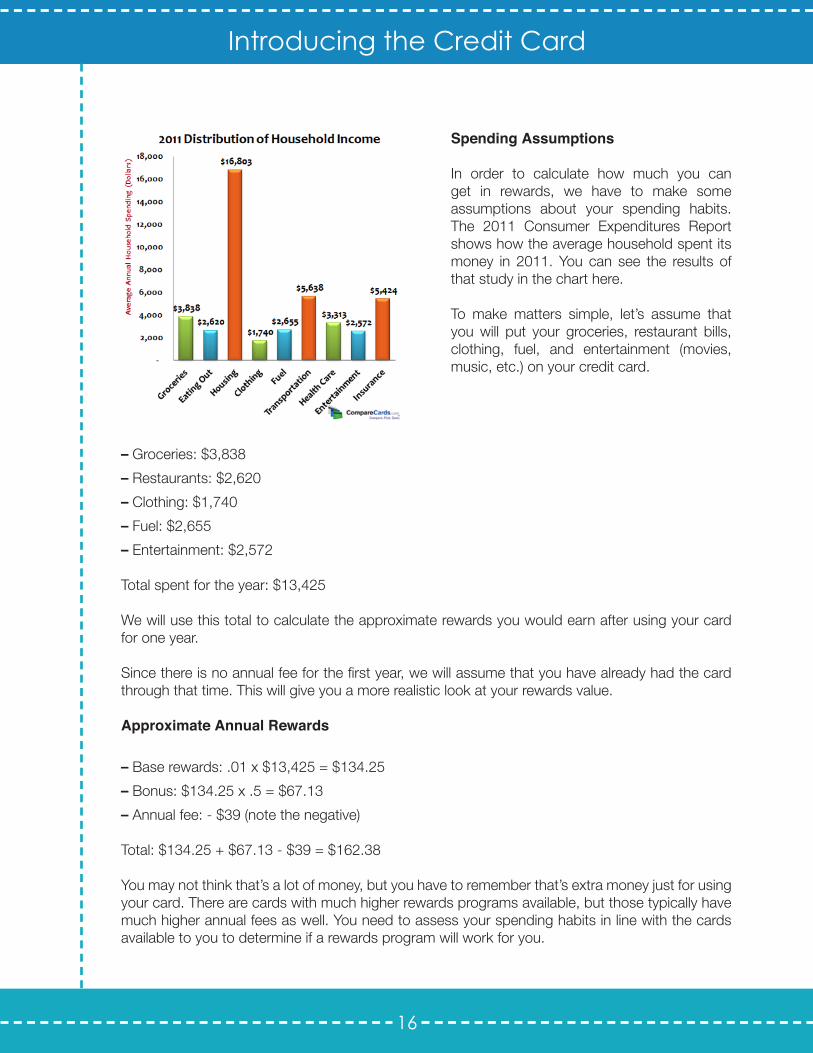

Spending Assumptions

In order to calculate how much you can get in rewards, we have to make some assumptions about your spending habits. The 2011 Consumer Expenditures Report shows how the average household spent its money in 2011. You can see the results of that study in the chart here.

To make matters simple, let’s assume that you will put your groceries, restaurant bills, clothing, fuel, and entertainment (movies, music, etc.) on your credit card.

– Groceries: $3,838

– Restaurants: $2,620

– Clothing: $1,740

– Fuel: $2,655

– Entertainment: $2,572

Total spent for the year: $13,425

We will use this total to calculate the approximate rewards you would earn after using your card for one year. Since there is no annual fee for the first year, we will assume that you have already had the card through that time. This will give you a more realistic look at your rewards value.

Approximate Annual Rewards

– Base rewards: .01 x $13,425 = $134.25

– Bonus: $134.25 x .5 = $67.13

– Annual fee: - $39 (note the negative)

Total: $134.25 + $67.13 - $39 = $162.38

You may not think that’s a lot of money, but you have to remember that’s extra money just for using your card. There are cards with much higher rewards programs available, but those typically have much higher annual fees as well. You need to assess your spending habits in line with the cards available to you to determine if a rewards program will work for you.

17

Introducing the Credit Card

Choose the best answer.

1. What would the approximate annual rewards be for the first year in the Capital One Cash Rewards example above?

A: $134.25

B: $162.38

C: $201.38

D: $324.76

2. What can travel rewards be used for?

A: Hotel rooms

B: Airline tickets

C: Cruises

D: Vacation packages

E: All of the above

3. What would happen to the rewards from the sample if you also put your insurance payments on the card?

A: It would go up because the total spent would go up.

B: It would go down because the total spent would go up.

C: It would go up because the total spent would go down.

D: It would go down because the total spent would go down.

Exercise 6

18

Introducing the Credit Card »

Whi

ch c

red

it ca

rd sh

ould

I ch

oose

? Choosing the right credit card can be quite a challenge because there are so many of them available on the market. Rather than freaking out and calling mom for help, you simply need to compare your options. Here are some key factors to keep in mind:

– Annual Fee: The higher the annual fee, the harder it will be to avoid credit card debt. Make sure that your annual fee is something that you can afford consistently, even if that means giving up some rewards.

– Credit Level Requirements: What kind of credit do you need to apply for the card? If you know you have “fair” credit, there is no sense in applying for a card that requires an “excellent” score. If you do this too much, you may be declined because too many people have looked at your credit history.

– APR: Know what sort of fees you will encounter if you can’t pay off your balance in full. You may assume that you’ll always pay that back, but you don’t know what will happen in the future.

– Intro Rates vs. Long Term Rates: Make sure you understand what your actual rates are going to be for the card, not just the introductory ones. 0% APR is great, but not if it is followed by a 29% APR. Figure out what the intro period is for each card before falsely getting your hopes up.

– Rewards: Consider whether or not you can logically benefit from a card’s rewards program. If the numbers don’t add up, look for a card with the lowest carrying costs possible.

– Reliability: The final piece of the puzzle comes from the trust you instill in the credit card company. If you think they will take care of you in times of need, you should feel confident getting one of their cards.

Credit card companies will come at you from all angles when you turn 18. They know that once they get you to set up an account, chances are you’ll keep it for a long time. At this point, you are considered a “new card customer,” and as a result, you may feel somewhat loyal to the first credit card company you work with. “Hey, they gave me a shot. Now I owe them something.” Don’t get caught up in this. Take the time to find the right card from the start, and don’t be afraid to change if a better offer comes along. It’s not impossible to switch credit card companies even after you’ve been with one for a while. You just have to find a way to make that happen.

As much as it sucks to read this, you are the only one who can figure out what the right card is for you. Compare all the rates, rewards, and requirements carefully, and you’ll find exactly what you’re looking for.

19

Introducing the Credit Card

acquirer: The messenger between a merchant and a credit card issuer.

batch: A set of credit card transactions from a day.

card verification value: A three to four digit code on the back of a credit card that acts as additional identification.

card brand or processor: The credit card company that provides the credit card, such as Visa or American Express.

credit card: A plastic card with a magnetic strip on the back that represents a line of credit.

credit card number: The 16-19 digit number on the front of a credit card that identifies it individually.

credit card statement: A detailed list of transactions, fees, payments, and balance figures for a credit card.

expiration date: The date in which a credit card is no longer valid.

hologram: A three dimensional mark on a credit card that verifies it is real.

issuer: The bank or credit card company that issues the credit card.

line of credit: An account offered in exchange for trust that a card user will pay back its balance.

merchant: A store or service provider that accepts a credit card payment.

rewards: Special offers available for spending money on certain credit cards.

signature box: A box on the back of every credit card where a user is supposed to sign.

» G

loss

ary