Embed Size (px)

Citation preview

AnnuitiesWilliam A. Despo830 Third Avenue

New York, NY 10022(212) 430-8020(973) 491-3325

January 2013

The Evolving World of Annuities

Marketplace is changing• Sun Life Insurance stopped selling annuities.

• Hartford Insurance stopped selling annuities, and plans to diverse Woodbury Financial.

• Increase regulation by insurance regulators.

• FINRA regulating its brokers that have customers who sell securities to buy annuities.

• Litigation and class actions.

• Types of annuities constantly changing.

2

Senior Citizen Victims?

NY Times and WSJ have pointed to problems with the use of professional designations such as “Certified Retirement Financial Adviser,” “Certified Senior Advisor,” “Chartered Senior Financial Planner,” etc.

Titles seemed to be more a marketing tool. Titles used in marketing of unsuitable

annuities.

3

States React to Senior Abuse

Insurance commissioners across the country have examined the background and training of all those sell annuities.

States have developed training programs for producers.

Producers must meet minimum knowledge standards regards to the product as well as the law.

4

National Suitability Standard

NAIC calls for a national standard of suitability products for non-registered products.

NAIC drafted a model setting suitability standards for life and annuity products.

Focus on sales to persons over the age of 65.

Model Act called Senior Protection in Annuity Transactions Model Regulation.

5

FINRA Reacts

FINRA adopts rules to deal with variable annuities and annuities in an attempt to govern the conduct of the registered personnel.

Sanctions, fines, suspensions and bars. FINRA also serves as an arbitration forum

for customers who have claims involving annuities.

6

Typical Claims in a Senior Abuse Claim

Breach of fiduciary duty, suitability, negligence, fraud, consumer fraud, RICO

Class actions Mental capacity Reliance and control Enforceability of arbitration clauses

7

Overview to Annuities

Neil Hartzell, LeClairRyanOne international Place

Boston, MA(617) 502 8209

January 2013

9

What are they?

Contract between purchaser and life insurance company designed to meet retirement and other long term money management goals. Purchaser makes a lump sum payment or series of payments; in return insurer agrees to make periodic payments to purchaser; payments from insurer can begin immediately or at some future date.

Defined by Internal Revenue Code and regulated by individual states. Variable annuities (discussed below) are regulated by the Securities and Exchange Commission and overseen by the Financial Industry Regulatory Authority (FINRA; the largest non-governmental regulator for all securities firms doing business in the United States).

10

Benefits

Typically offer tax deferred growth of earnings and may include a death benefit; death benefits vary; typical death benefit payment can be amount paid for annuity (either the lump sum amount or the total of payments made by purchaser).

Withdrawals are taxed at ordinary income rates, not capital gains; once retired likely in lower income tax bracket.

Typically offer guaranteed rate of return; amount determined by agreement/contract with insurance company.

No maximum investment restriction unlike 401K and IRA Accounts.

11

Disadvantages

Early withdrawal may result in tax penalties and surrender charge (sometimes substantial) from the insurance company.

Not very liquid. If purchaser may need access to funds before payments begin, early withdrawal fees can be as high as 10% in first year (usually percentage of penalty reduces in following years).

Annuities can be sold on secondary market but such sale will likely incur transfer fees (most investors do not read contacts carefully and thus can claim to be unaware of such fees).

12

Disadvantages (cont.)

Common criticism is that fees for buying an annuity can be high (some brokers or financial planners like to recommend and sell annuities because commission fee is high).

Company will say that fee is not deducted from amount purchased.

(Example: Annuity purchased for $100,000; broker gets fee of $4,000. Amount showed on contract is $100,000, but commission fees is usually deducted from annuity over time in the form of yearly expenses.)

13

Disadvantages (cont.)

Subsumed in income/expense statement if annuity withdrawn early; most purchasers unaware that this is how commission is paid.

Trail commissions can add to costs (trail commissions paid for each year annuity remains in force).

Fees can sometime reduce annual yield by up to 2-3%.

14

Types of Annuities

15

Immediate or Life Annuity

Distributes savings with a tax deferred growth factor; return is part principal (not taxed) and part investment income (that is taxed)

Provides income for life of annuitant similar to a defined benefit or pension plan

16

Deferred Annuity

Accumulates savings with a view to eventual distribution either in manner of immediate annuity or as a lump sum payment.

Generally 3 types of deferred annuities: fixed, indexed and variable. There are different types within these 3 groups.

17

Types of Deferred Annuity: Fixed

Typically offer guaranteed rate of return over life of contract. Similar to bank CDs. Guaranteed rate may, however, only be the same for first 5 years. After that, may fluctuate, with a minimum base rate (e.g. no lower than 3%).

Typically allow some percentage of interest/principal to be withdrawn early (e.g. 10% per year) without penalty.

18

Types of Deferred Annuity: Equity Indexed

Is a type of fixed annuity Performance typically tied to a stock market index

(S&P 500, Dow Jones Industrial Average). Caps, spreads crediting methods and margins can

reduce returns• Disadvantage is they don't pay participating

market dividends• Advantage is purchaser can never earn

less than 0%, even if indexes are negative for the year

19

Types of Deferred Annuity: Variable Annuities

Insurance companies invest money in subaccounts

Functionally equivalent to mutual funds Primary use to allow investors to engage in

tax deferred investing for retirement accounts greater than amounts permitted by IRA or 401K plans

20

Types of Deferred Annuity: Variable Annuities (cont.) Many offer guaranteed rate of return even if underlying

accounts perform poorly. Such guarantees come with costs in form of fees and

expenses. Regulated by individual states as insurance products and

Securities and Exchange Commission as securities under federal laws.

Underlying investment can take many forms: can be in stocks, bonds, mutual funds or combinations some annuities come with automatic rebalancing feature as purchaser (the annuitant) ages or to reduce risk over market fluctuations.

21

Types of Deferred Annuity: Variable Annuities (cont.)

Many different types of performance guarantees: guaranteed minimum death benefits (several different forms, return of premium, roll-up of premium at a particular rate, maximum anniversary value); guaranteed living benefits.

Generally highest area for criticism as claims arise for being sold to wrong person who claim investments could have performed better elsewhere and these products typically have higher fees than other annuities. Commissions can range from 1-12%.; average is about 6%.

Fees reduce rate of return. Guaranty of no loss of principal is not really a benefit since

over long term US financial markets have generated positive returns.

22

Annuities and 401K and IRA Plans

23

Annuities/401K & IRA Plans

401K and IRA Plans are already tax deferred, so no additional tax benefits.

If death benefit on variable annuity funded with IRA or 401K funds exceeds account value at death of policy owner, beneficiary will be taxed on total amount of death benefit received forfeiting life insurance policy tax-free death benefit.

Can be appropriate if retiree needs lifetime income at retirement; particularly if annuity provides for guaranteed income, death benefit.

24

Annuities and Trusts

25

Charitable Remainder Trusts

Very complex area, intersection between state trust law, IRS regulations and FINRA regulations.

May be suitable in some circumstances. IRS letter ruling suggests a charitable remainder

trust may invest in annuities without compromising trust status.

Does annuity create the income needed by the trust beneficiaries? (This can depend on what annuity is invested in; dividends may be income, increase in value may not be income.)

26

Charitable Remainder Trusts (cont.)

Does trust need income or guaranteed income?

Are other investments more suitable (i.e. income producing real estate)?

Criticism over high commissions Evidence that broker considered other

investments What was explained to grantor of trust?

27

Insurance Company Default Risk

28

Insurance Company Default Risk

Many companies have gone out of business in recent years.

Insurance company defaults governed by state law.• What is insurance company rating when

annuity was sold?• What is state guaranty fund policy when insurer

goes out of business?• Caps on benefits?• Taken into account when annuity sold?

29

Claims/Damages in Annuity Cases

30

Claims/Damages: Theories

Typical claims involve suitability, failure to supervise, negligence, breach of fiduciary duty

Factors –• Age and financial circumstances of investor

• Sophistication of investor

• Forms/Disclosures signed, risks explained

• Evidence that financial goals reviewed

31

Claims/Damages: Theories (cont.)

Factors –• Documentation of recommendations

• Documentation if recommendations ignored

• Witnesses

• Alternative, better suited investments

• Credibility of claimant

• Credibility of broker

32

Claims/Damages: Damages

Proof that underlying amount paid into annuity (either lump sum or amounts paid in over time) would have performed better in another investment.

What is comparison? • Is it a high growth fund that may have

performed well over a specific period of time, but that which the investor (who was looking for a low-risk guaranteed return) would likely never have invested in?

33

Claims/Damages: Damages (cont.)

Comparisons between performance of mutual funds that tracked the same mix/type of underlying securities have been upheld by courts/arbitrators as appropriate comparisons.

Must factor in costs/commissions for comparison funds in damage calculations.

Punitive damages under FINRA rules, state law or state law applicable Elder Abuse Act.

34

Claims/Damages: Damages (cont.)

Attorneys fees under FINRA, state law, any applicable contracts, or state law applicable Elder Abuse Act.

Did monthly distributions reduce principal amount or were they just based on income generated by underlying investments (i.e. dividends)?

Claims can include withdrawal amounts if plaintiff proves annuity was unsuitable in the first place?

35

Know-Your-Customer and Suitability Rules

Changes to the New FINRA

Richard A. McGuirk70 Linden Oaks, Suite 210

Rochester, NY 14625(585) 270-2105

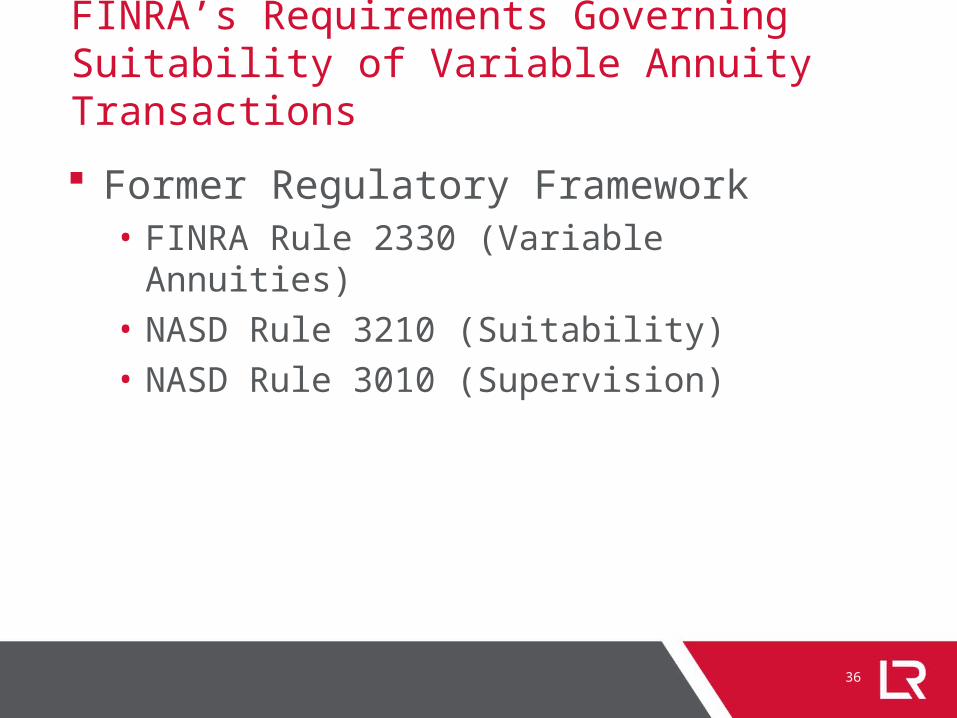

FINRA’s Requirements Governing Suitability of Variable Annuity Transactions

Former Regulatory Framework• FINRA Rule 2330 (Variable Annuities)

• NASD Rule 3210 (Suitability)

• NASD Rule 3010 (Supervision)

36

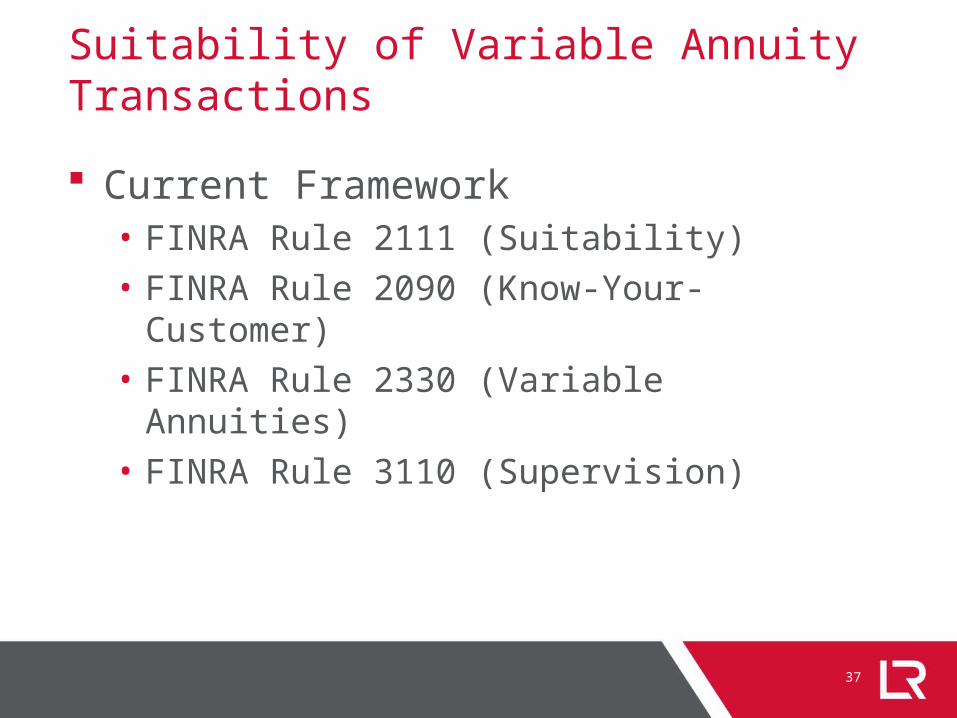

Suitability of Variable Annuity Transactions

Current Framework• FINRA Rule 2111 (Suitability)

• FINRA Rule 2090 (Know-Your-Customer)

• FINRA Rule 2330 (Variable Annuities)

• FINRA Rule 3110 (Supervision)

37

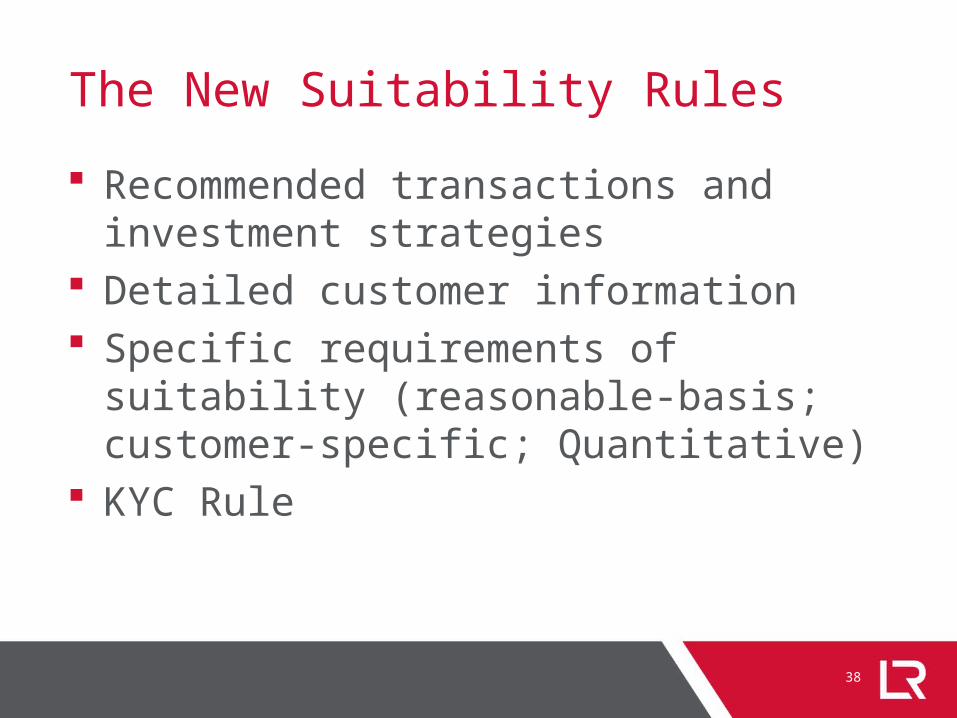

The New Suitability Rules

Recommended transactions and investment strategies

Detailed customer information Specific requirements of suitability

(reasonable-basis; customer-specific; Quantitative)

KYC Rule

38

39

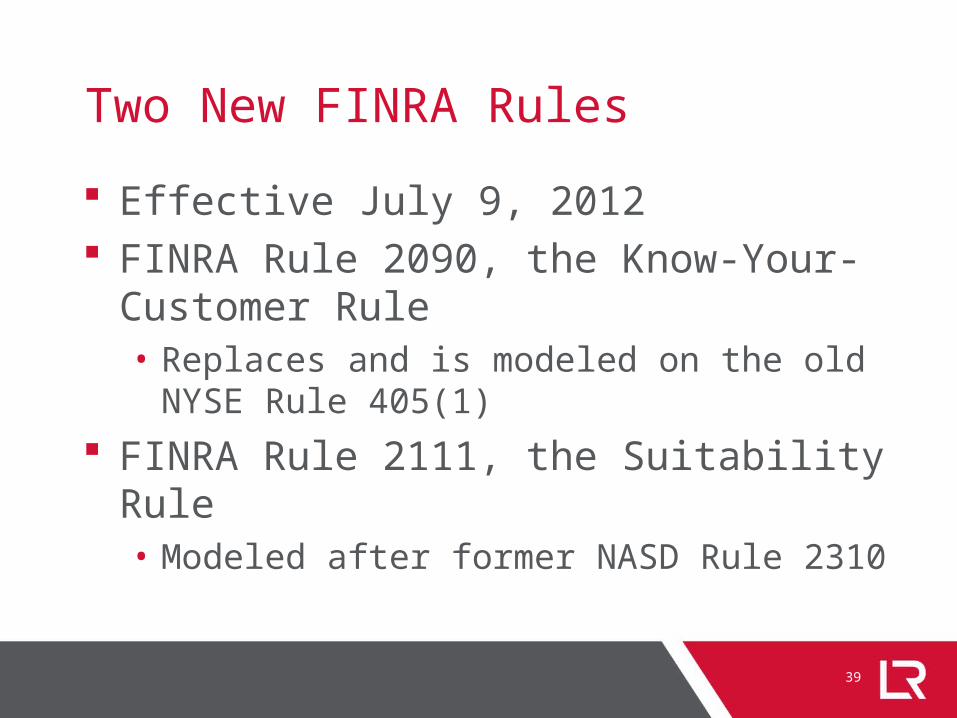

Two New FINRA Rules

Effective July 9, 2012 FINRA Rule 2090, the Know-Your-

Customer Rule • Replaces and is modeled on the old NYSE

Rule 405(1)

FINRA Rule 2111, the Suitability Rule • Modeled after former NASD Rule 2310

40

Know-Your-Customer Rule

Requires firms to use “reasonable diligence” in opening and maintaining accounts and to know the “essential facts” concerning the customer

Unlike the former NYSE Rule 405, the new rule does not specifically address orders, supervision or account opening

41

Essential Facts

Required to –• Effectively service the customer’s account• Act in accordance with any special handling

instructions for the account• Understand the authority of each person acting

on behalf of the customer• Comply with applicable laws, regulations and

rules

42

Suitability Rule

Modeled after former NASD Rule 2310 Requires the firm to “have a reasonable

basis to believe that a recommended transaction or investment strategy involving a security or securities is suitable for the customer, based on the information obtained through the reasonable diligence of the [firm] to ascertain the customer’s investment profile.”

43

Suitability Rule (cont.)

A “customer’s investment profile includes, but is not limited to the customer’s age, other investments, financial situation and needs, tax status, investment objectives, investment experience, investment time horizon, liquidity needs, risk tolerance, and any other information the customer may disclose to the [firm] in connection with such recommendation.”

44

Suitability Rule (cont.)

New rule broadens the explicit list of customer-specific factors that firms must attempt to obtain and analyze, including the customer’s age, investment experience, time horizon, liquidity needs, and risk tolerance.

45

Role of a “Recommendation”

The rule continues to use a “recommendation” as the triggering event for application of the rule and continues to apply a flexible “facts and circumstances” approach to determining what communications constitute such a “recommendation.”

46

Role of a “Recommendation” (cont.)

Whether a “recommendation” has occurred is an objective rather than subjective determination.

“An important factor in this regard is whether – given its content, context and manner of presentation – a particular communication from a [firm] to a customer reasonably would be viewed as a suggestion that the customer take action or refrain from taking action regarding a security or investment strategy.” Source: FINRA Regulatory Notice 11-02, “Know Your Customer and Suitability,” January 2011.

47

Suitability Rule Applies to “Strategies”

The term “strategy” “should be interpreted broadly … Among other things, the term ‘strategy’ would capture a broker’s explicit recommendation to hold a security or securities.”

Source: FINRA Regulatory Notice 11-02.

48

“Recommendation” Suitability

Reasonable-basis suitability Customer-specific suitability Quantitative suitability

49

Reasonable-basis Suitability

Firm must have a reasonable basis to believe that the recommendation is suitable for at least some investors.

Firm’s reasonable diligence must “provide the firm … with an understanding of the potential risks and rewards associated with the recommended security or strategy.”

Source: FINRA Regulatory Notice 11-02.

50

Reasonable-basis Suitability (cont.)

It is not sufficient protection under this requirement that a firm’s “product committee” conduct the required diligence.

Broker or associated person involved in the recommendation to the customer must still comply with the reasonable-basis obligation.

Broker “can rely on a firm’s fair and balanced explanation of the potential risks and rewards of a product. However, if the associated person remains uncertain about the potential risks and rewards of a product or has reason to believe that the firm failed to address a particular issue … then the associated person would need to engage in further inquiry before recommending the product.”

Source: FINRA Regulatory Notice 11-25, “Know Your Customer and Suitability,” May 2011.

Reasonable-basis Suitability (cont.)

Reasonable basis• Lack of training is now a suitability violation!

51

52

Customer-specific Suitability

Firm must have a “reasonable basis to believe that the recommendation is suitable for a particular customer based on that customer’s investment profile.”

Source: FINRA Regulatory Notice 11-02.

53

Quantitative Suitability

Broker who has actual or de facto control over a customer account must “have a reasonable basis for believing that a series of recommended transactions, even if suitable when viewed in isolation, are not excessive and unsuitable for the customer when taken together in light of the customer’s investment profile.

54

Quantitative Suitability (cont.)

A broker has actual control, for example, where he has discretionary trading authority.

A broker would have de facto control over an account if the customer routinely follows the broker’s advice because the customer is unable to evaluate the broker’s recommendation and exercise independent judgment.

Source: FINRA Regulatory Notice 12-25, “Suitability”, May 2012 (copy attached).

55

Quantitative Suitability (cont.)

Thus, the new rule “makes clear that a broker must have a firm understanding of both the product and the customer. It also makes clear that the lack of such an understanding itself violates the suitability rule.”

Source: FINRA Regulatory Notice 11-02.

56

Customer’s Best Interest

In certain guidance, for example in FINRA Regulatory Notice 11-02, cases standing for the proposition that a broker’s recommendations must be consistent with his customer’s best interests.

Effectively, that means that the broker should not put his own interests in front of the customers.

57

Customer’s Best Interest (cont.)

In FINRA Regulatory Notice 12-25, FINRA provided a list of examples in which FINRA and the SEC found brokers in violation of the suitability rule by placing their interests ahead of a customer’s.

58

Customer’s Best Interest (cont.)

Violation examples –• Motivation for recommending one product over

another was to receive larger commissions.• Mutual fund recommendations were made to

maximize commissions rather than establish an appropriate portfolio.

• Broker who recommended new issues being pushed by his firm so that he could keep his job.

See FINRA Regulatory Notice 12-25 (and cases cited therein).

FINRA Rule 2821: Heightens Suitability Standard for Deferred Annuities Enhance broker-dealers compliance

supervisory systems Rule 2821 applies to both purchases and

sales of deferred variable annuities.• Exceptions: tax qualified, employer-sponsored

retirement or benefit plan

59

FINRA Rule 2821

Registered representative must have a reasonable basis to believe that the customer has been informed, in general terms, of the material features of a deferred variable annuity. Features include potential surrender period and surrender charges, potential tax penalty, mortality expenses, charges for and features of enhanced riders, insurance and investment components, and market risk.

60

FINRA Rule 2821 (cont.)

May not ignore product-specific features. Informed is more than deliver of written

material. Registered representative must have a

reasonable belief that the customer will benefit.

61

FINRA Rule 2821 (cont.)

Requires registered representative to make reasonable efforts to obtain and consider various other types of customer-specific information.

• Customer age, annual income, financial situation and needs, investment experience, investment objectives, intended use of the investment, time horizon, other assets, liquidity needs, liquid net worth, risk tolerance, tax status and other information that reasonable registered representative would consider in making recommendations.

62

EQUITY INDEX ANNUITIES

WILLIAM A. DESPO

63

Equity Index Annuity (EIA)

EIA are financial instruments in which the insurance company guarantees a stated interest rate with some protection from loss of principal, and provides an opportunity to earn additional interest based on the performance of a securities market index.

64

Regulation of Equity Index Annuities

Prior to the adoption of the Dodd Frank Wall Street Reform and Consumer Protection Act of 2010 –• Uncertainty existed as whether an EIA was a

security or an insurance product.

• FINRA Notice to Members 05-50 express concern about the marketing and supervision of sales of unregistered EIAs.

• In 2007 SEC Rule 151A declared that EIA were securities.

65

Regulation of EIAs (cont.)

National Association of Insurance Commissions issues Model Suitability Rule for EIAs

The Model Rule defines “Suitability information” to include, but not limited to, age, annual income, financial situation and needs, financial experience, financial objectives, intended use of the annuity, financial time horizon, and risk tolerance.

66

Regulation of EIAs (cont.)

Model Rule created duties for the insurers and insurance producers when recommending an EIA.• Reasonable basis exists when the

recommendation is suitable for the customer.

• A reasonable basis exists when it is believed that the customer was reasonably informed of the product, including surrender charge, and the customer will benefit from the product.

• Follows FINRA Rule 2821.

67

Regulation of EIAs (cont.) Dodd Frank Act exempts EIAs as securities

provided one of the conditions are satisfied:• A State adopts the model suitability rule by June

16, 2013;• EIA is XX by a company that is domiciled in a state

that adopts the model suitability rule by June 16, 2013; or

• EIA is XX by a company that adopts and implements practices on a nationwide basis that meets or exceeds the model suitability law requirements.

68

Regulation of EIAs (cont.)

State Regulation of EIAs• As of July 2012, 47 States have adopted some

form of the Model Suitability Rule.

• In North Carolina, “The Suitability in Annuity Transaction Act” became effective January 1, 2008. The purpose of the Act is to set standards for annuity-related recommendations made to consumers by insurance agents and companies.

69

Regulation of EIAs (cont.)

• The Act requires insurance companies and agents to assess the financial objectives of the consumer before recommending the purchase or exchange of an annuity. It requires the company or agent to make reasonable efforts to obtain information about a customers circumstances.

70

Regulation of EIAs (cont.)

• Insurance companies and agents must have reasonable grounds for believing that their annuity recommendations are suitable based on the information collected from the consumer. If a consumer elects not to provide the information, provides false information, purchases something that the agent or insurance company did not recommend, then agents and insurance companies have no obligations under the Act.

71

Regulation of EIAs (cont.)

• Violation of the Suitability in Annuity Transactions Act is considered an unfair and deceptive trade practice. Violators are subject to penalties and treble damages.

72

Defense Comments to Annuity Claims

The Senior Citizen (65 years and older)• Class Actions

– Yokoyama v. Midland Life Insurance Co., 243 F.D.R. 400 (D. Haw. 2007). Class action alleged that defendant deceptively marketed equity index annuities to senior citizens by way of false written material, failed to have sufficient procedures to ensure suitability of the annuity sales. Class action certification denied. Suitability is an subject to an individual assessment and cannot be done on a class wide basis. Individual questions predominate the class and the predominance requirement in Rule 23.

73

Defense Comments to Annuity Claims (cont.)

– Negrete v. Alliance Life Insurance Co. of North America, 23 F.R.D. 482 (C.D. Cal. 2006). Plaintiff claimed that Alliance engaged in a misleading marketing scheme to sell to senior citizens indexed annuities, which were not suitable. Violations of RICO and California’s “elder abuse” statue and consumer abuse law. The court certified the class action.

– DeCesar v. Lincoln Benefit Life Co., 852 A.2d 474 (R.I. 2004). Plaintiffs alleged that defendant breached the annuity contract by unilaterally changing the participation rate. The equity index policy specified a 80-percent participation rate but Lincoln revised the rate to 70 percent. Class certified.

74

Defense Comments to Annuity Claims (cont.)

FINRA enforcement actions• United Planners Financial Services of America

– September 24, 2012 – Fined $200,000 over variable annuity sales for failure to properly supervise and detect unsuitable sale of variable annuities

– April 14, 2009 – Fined $1.75 million for 250 unsuitable variable annuity sales.

75

– December 6, 2012 – Investment News reported that FINRA is investigating sales of variable annuities issued by Sun Life Financial, Inc. The annuities contained subaccounts invested in hedge funds. In 2010, the hedge funds were forced to closed due to, among other things, naked options trading in the S&P 500. Arbitration cases have been filed against the brokers who sold the annuities to customers, including SagePoint Financial, Geneos Wealth Management, Inc., Lincoln Financial Network, FSC Securities Corp., and National Planning Corp.

76

Defense Comments to Annuity Claims (cont.)

Mental capacity of a senior citizen• Capacity issues relate to a number of legal

issues– Capacity to enter into a contract

– Breach of fiduciary duty

– Negligence

– Fraud

– Consumer protection

77

Defense Comments to Annuity Claims (cont.)

Mental capacity can be defined as an individual’s impairment by reason of mental illness or mental deficiency to the extent that he lacks sufficient capacity to govern himself and manage his affairs.

Defense must obtain all medical records of the senior citizen, including a detailed diagnosis, how the condition was determined, and a careful review of all mental examination tests, including the Mini Mental State Examination Test. The MMSE is a short questionnaire of 10 to 30 questions that is used to screen for cognitive impairment and estimate the definition of impairment. It is typically given by a someone other than a doctor.

78

Defense Comments to Annuity Claims (cont.)

Important factors • Retain a qualified medical expert to review the medical

records. • Independently investigate the background of the senior

citizen. If able, speak with the person’s accountant, banker, neighbors, and friends.

• Examine tax returns and investment accounts.

79

Defense Comments to Annuity Claims (cont.)

Consider the senior citizen’s –• Ability to formulate reasonable decisions concerning

financial transactions (i.e., can he/she utilize a checking account and issue checks?)

• Knowledge of assets he/she owns• Ability to perform own personal care in an acceptable

manner such as personal hygiene• Orientation to time and place• Impairment of ability to remember current events

80

Defense Comments to Annuity Claims (cont.)

Fact Pattern Case Study

Eleanor Smith was a small business owner who retired in 2008. She was a high school graduate and took several courses at the local community college. Her work experience is basically on the job training. She was a sales person in the clothing industry, eventually starting her own sales company in 1960. Her company highest sales volume was $1.5 million, and never had more than4 employees. In 2008 she sold her company for $455,000.

In 2008 Ms. Smith rolled over her company retirement plan into an individual IRA at Foremost Broker, Inc., a FINRA member. The broker, Joe Quick, recommended an equity index annuity. She purchased the annuity for $2,100,000 for her IRA. The annuity had a surrender charge of $235,000 during the first 4 years and then reduces for the next 8 years to no surrender charge. The annuity was issued by New Insurance Company, Inc. Joe Quick left the securities industry after the Ms. Smith purchased the annuity.

Fact Pattern Case Study (cont.)

Innocent Larry was assigned Ms. Smith’s account by Foremost Broker in 2008. In 2009 Innocent Larry joins Honest Financial Services, Inc. and solicited Ms. Smith. She agreed to transfer her stock accounts from other brokers to Innocent Larry, and also gives him discretionary control to trade one of her accounts. At the same time Ms. Smith approaches Innocent Larry with concern about her annuity and New Annuity Insurance Company. She had read that the financial industry was in stress due to the financial meltdown of the industry. Innocent Larry says that he will look into New Annuity Insurance Company. Ms. Smith is also upset that the company had reduced the participation rate. Innocent Larry reports back that the insurance company has been downgraded from an A rating to junk status by Best Rating.

Fact Pattern Case Study (cont.)

Ms. Smith is extremely concerned about the safely of her money and directs Innocent Larry to look into other annuity companies and annuities. Innocent Larry reports that he believes that Major Insurance Company, one of the oldest and largest insurance companies in the industry, represents an A rated company with strong balance sheet. The annuity recommended by Innocent Larry offered by Major Insurance Company offers a better participation rate than New Insurance Company. However, there is a surrender charge of $190,000 over the first 3 years, reducing thereafter to the point there is no surrender charge after year 8.

Ms. Smith worried about safety of her annuity and decides to surrender her New Insurance Company annuity, and incurred a $235,000 surrender charge. She then buys a $1,800,000 annuity from Major Insurance Company.

Six months later, Innocent Larry receives a notice from Trust Company, Ms. Smith’s power of attorney, questioning the exchange of annuities, and claiming that he and Honest Financial Services acted improperly in exchanging the annuities. Trust Company alleges that Ms. Smith suffers from dementia, and did not have the mental capacity to approve the subject transactions.

Fact Pattern Case Study (cont.)

85

Thank You

Financial Services Litigation and Regulation Team

William Despo, LeClairRyan (973) 491-3325 [email protected] Hartzell, LeClairRyan (617) 502-8209 [email protected] Reimer, LeClairRyan (617) 502-8215 [email protected] Hutchison, LeClairRyan (617) 502-8210 [email protected] McGuirk, LeClairRyan (585) 270-2105 [email protected]