Embed Size (px)

Citation preview

12.07.201

2 1

IntraFish – Seafood Investor Forum London 31 October 2014

2

The Seafood case: Evolution, not revolution

1) A decade of industry evolution masked by a single event with double impact, Chile…

2) Lower supply growth going forward

3) Potential Re-rating of company valuations

Source: Kontali, DNB Markets

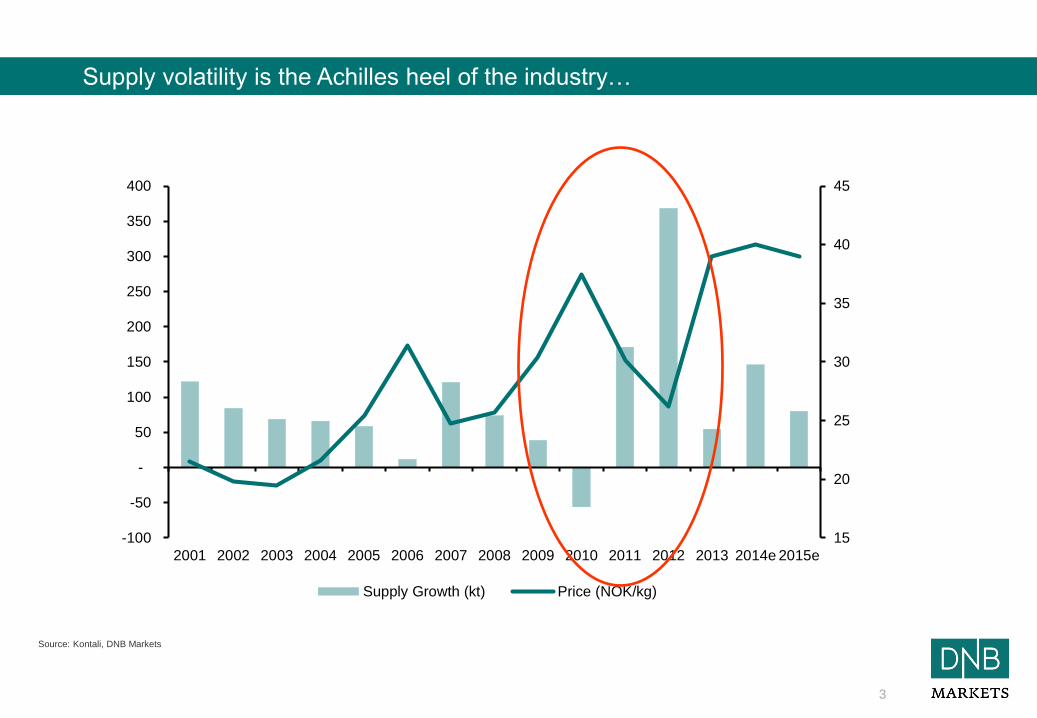

Supply volatility is the Achilles heel of the industry…

3

15

20

25

30

35

40

45

-100

-50

-

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014e 2015e

Supply Growth (kt) Price (NOK/kg)

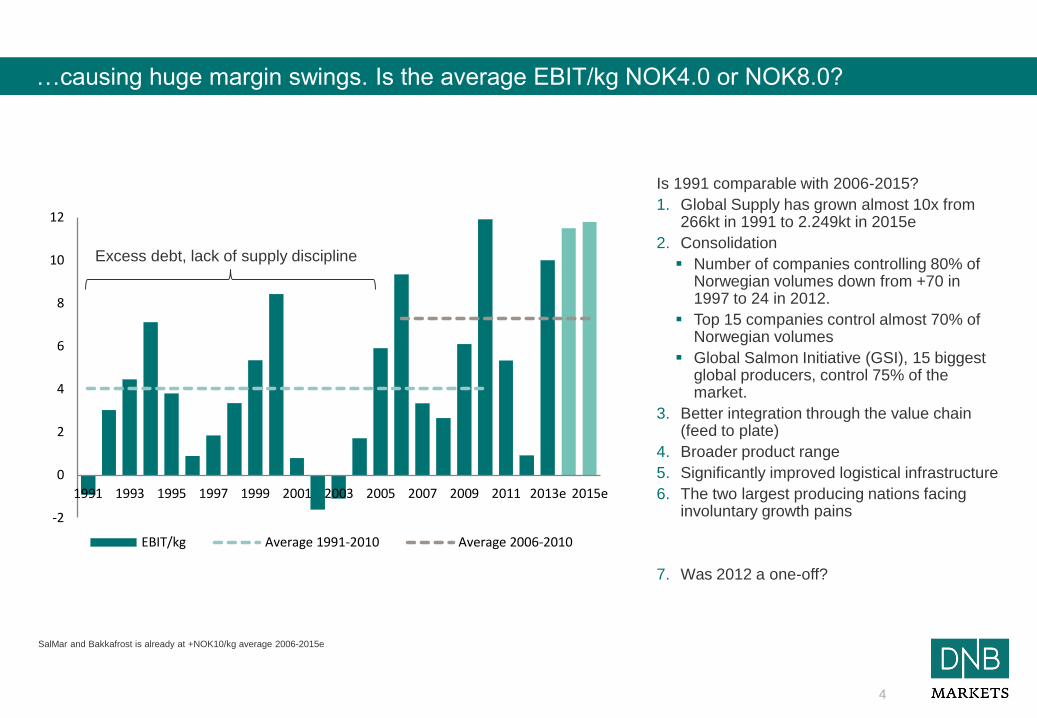

Is 1991 comparable with 2006-2015?

1. Global Supply has grown almost 10x from 266kt in 1991 to 2.249kt in 2015e

2. Consolidation

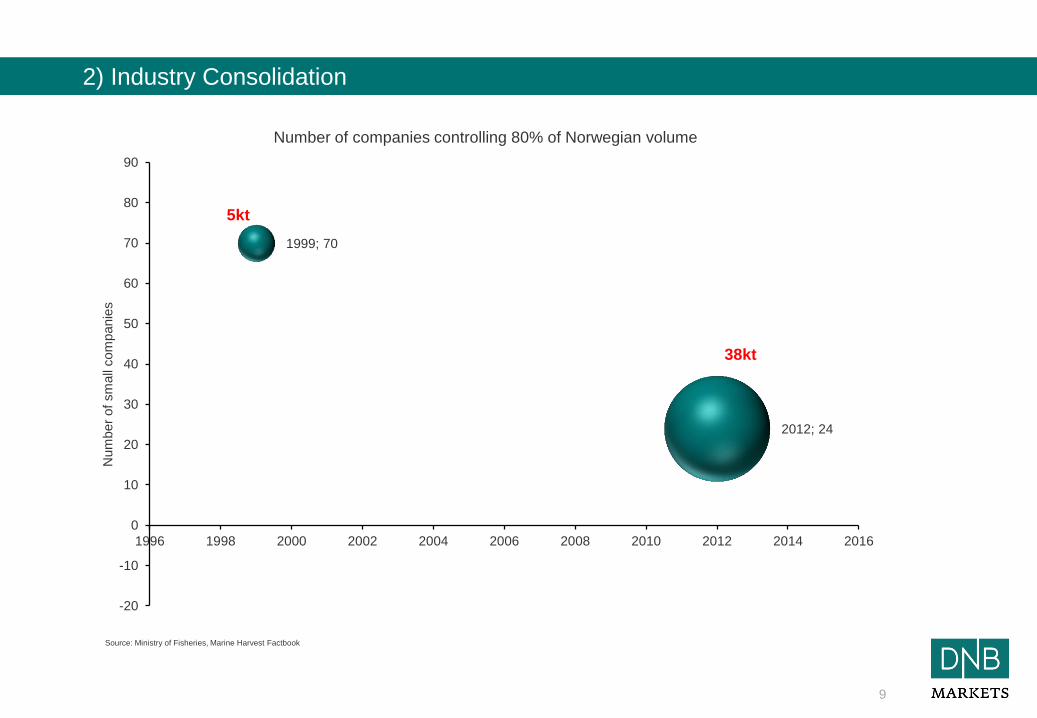

Number of companies controlling 80% of Norwegian volumes down from +70 in 1997 to 24 in 2012.

Top 15 companies control almost 70% of Norwegian volumes

Global Salmon Initiative (GSI), 15 biggest global producers, control 75% of the market.

3. Better integration through the value chain (feed to plate)

4. Broader product range

5. Significantly improved logistical infrastructure

6. The two largest producing nations facing involuntary growth pains

7. Was 2012 a one-off?

SalMar and Bakkafrost is already at +NOK10/kg average 2006-2015e

4

…causing huge margin swings. Is the average EBIT/kg NOK4.0 or NOK8.0?

-2

0

2

4

6

8

10

12

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013e 2015e

EBIT/kg Average 1991-2010 Average 2006-2010

Excess debt, lack of supply discipline

Source: Kontali, DNB Markets

5

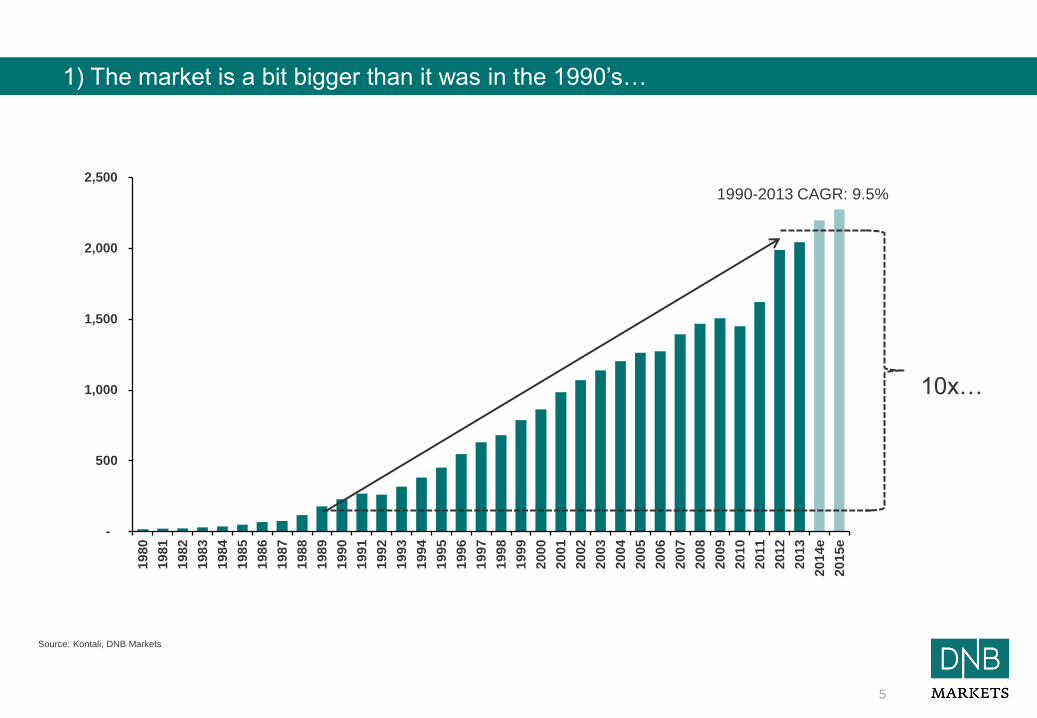

1) The market is a bit bigger than it was in the 1990’s…

-

500

1,000

1,500

2,000

2,500

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14e

20

15e

1990-2013 CAGR: 9.5%

10x…

6

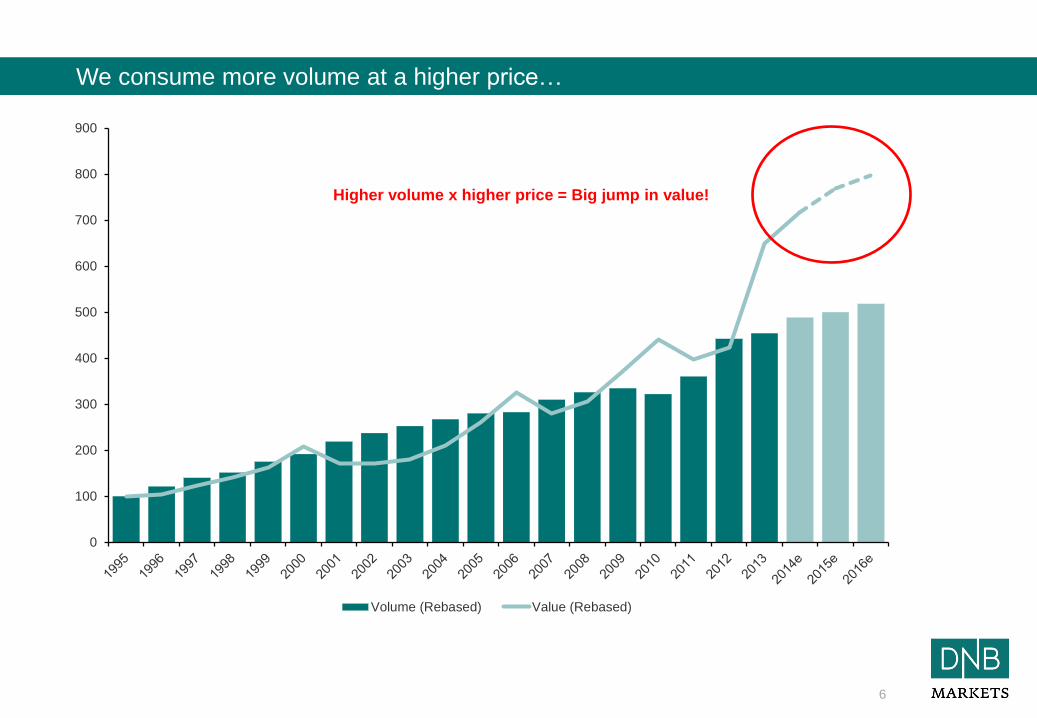

We consume more volume at a higher price…

Higher volume x higher price = Big jump in value!

0

100

200

300

400

500

600

700

800

900

Volume (Rebased) Value (Rebased)

Higher volume x higher price = Big jump in value!

7

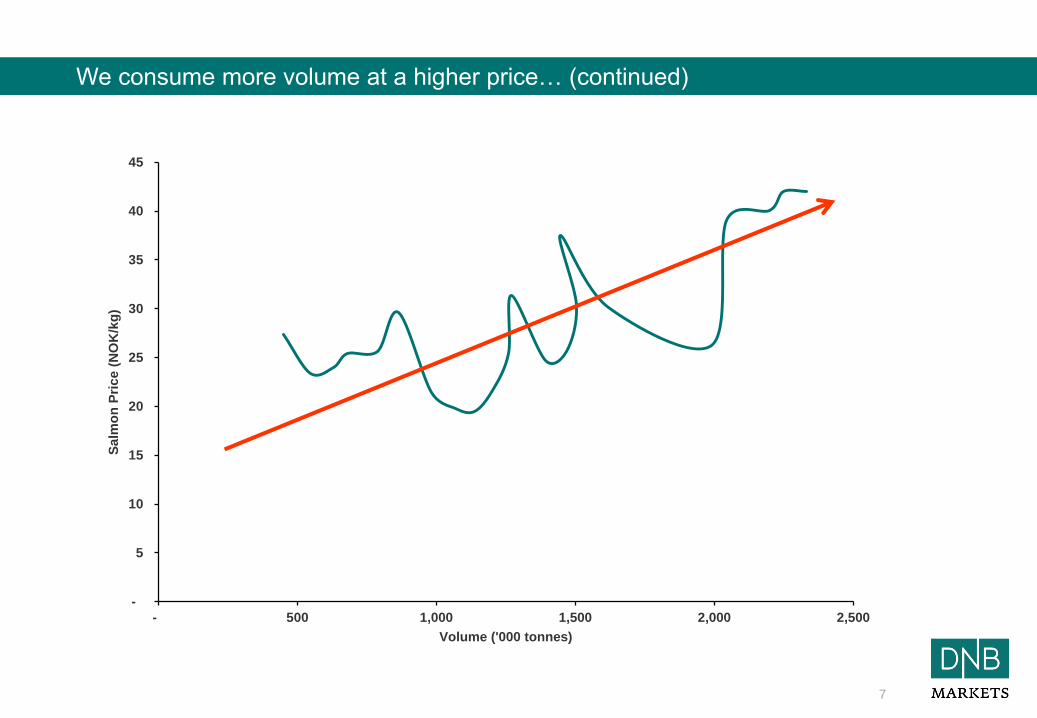

We consume more volume at a higher price (continued)…..

-

5

10

15

20

25

30

35

40

45

- 500 1,000 1,500 2,000 2,500

Salm

on

Pri

ce (

NO

K/k

g)

Volume ('000 tonnes)

We consume more volume at a higher price… (continued)

8

We are consuming more at a higher price (continued)…..

-

5

10

15

20

25

30

35

40

45

- 500 1,000 1,500 2,000 2,500

Salm

on

Pri

ce (

NO

K/k

g)

Volume ('000 tonnes)

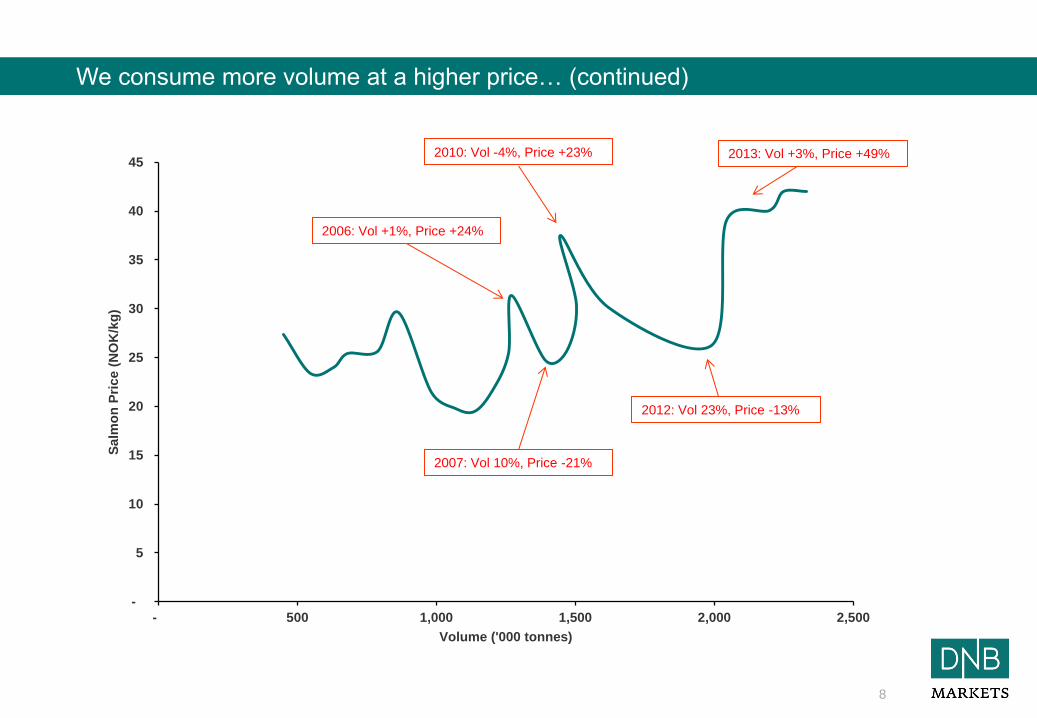

2010: Vol -4%, Price +23%

2006: Vol +1%, Price +24%

2012: Vol 23%, Price -13%

2013: Vol +3%, Price +49%

2007: Vol 10%, Price -21%

We consume more volume at a higher price… (continued)

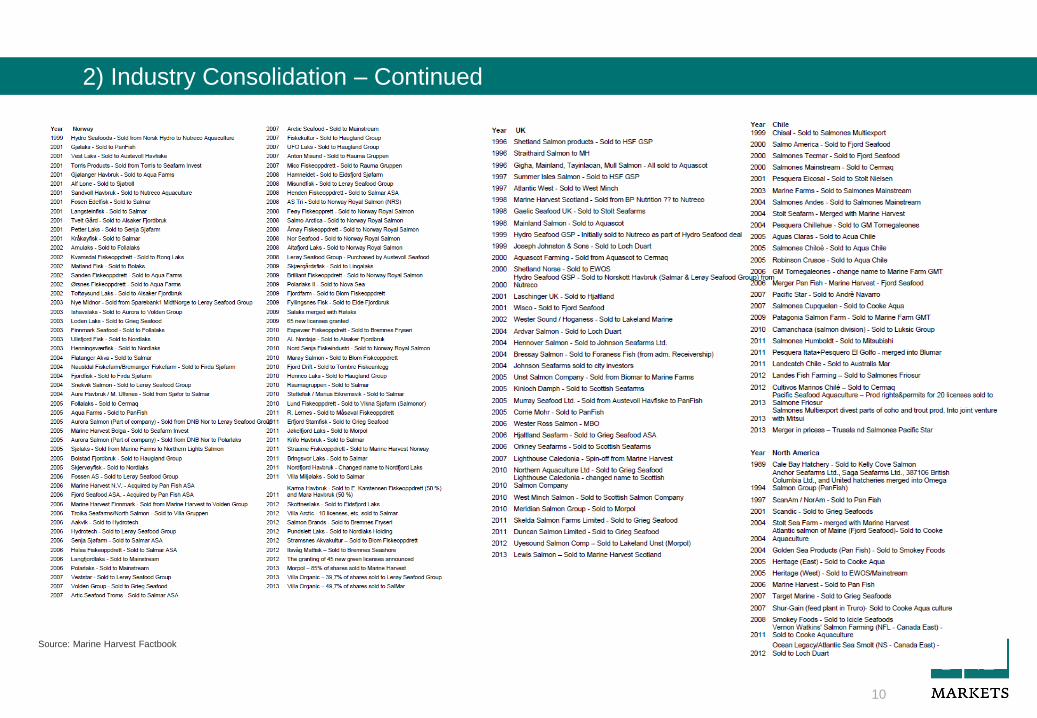

2) Industry Consolidation

9

Source: Ministry of Fisheries, Marine Harvest Factbook

1999; 70

2012; 24

-20

-10

0

10

20

30

40

50

60

70

80

90

1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Num

ber

of

sm

all

com

panie

s

Number of companies controlling 80% of Norwegian volume

5kt

38kt

Source: Marine Harvest Factbook

10

2) Industry Consolidation – Continued

11

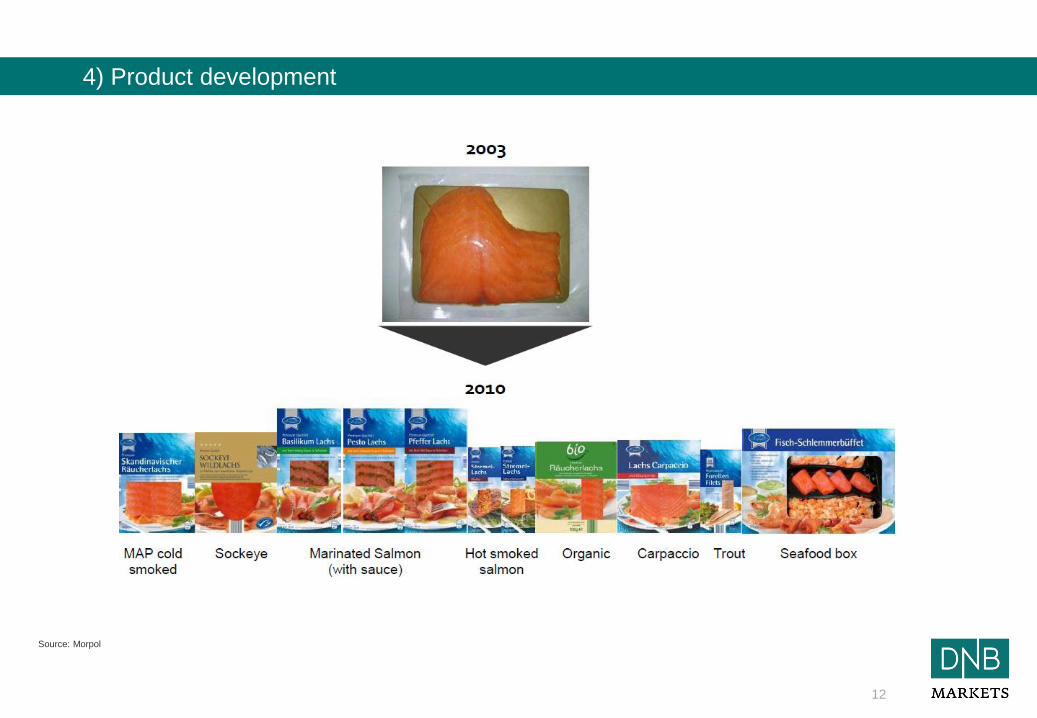

3) Companies are getting more integrated

Source: Morpol

12

4) Product development

Source: DNB Markets

13

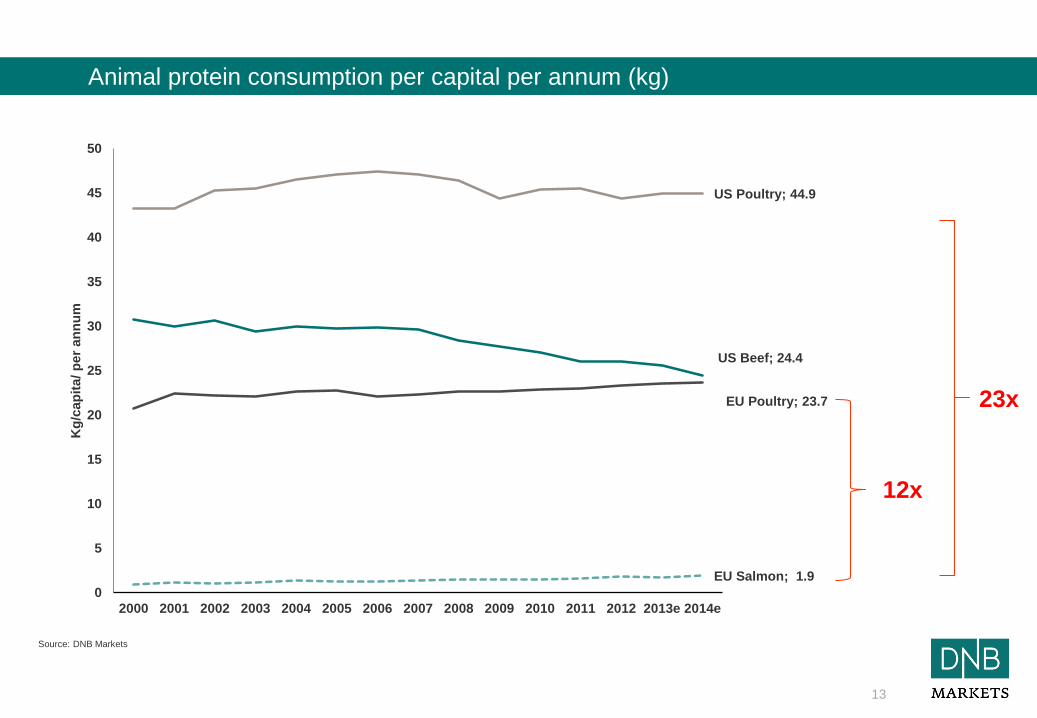

Animal protein consumption per capital per annum (kg)

US Beef; 24.4

US Poultry; 44.9

EU Poultry; 23.7

EU Salmon; 1.9

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013e 2014e

Kg

/cap

ita

/ p

er

an

nu

m

12x

23x

Improvement to the logistical infrastructure

Truck

Airfreight to US and Asia

Train

Fresh frozen

Modified Atmospheric Packaging (MAP)

New technology to increase freshness of product

Retailers now receive desired quantity and quality with greater certainty

14

5) Logistical improvements

15

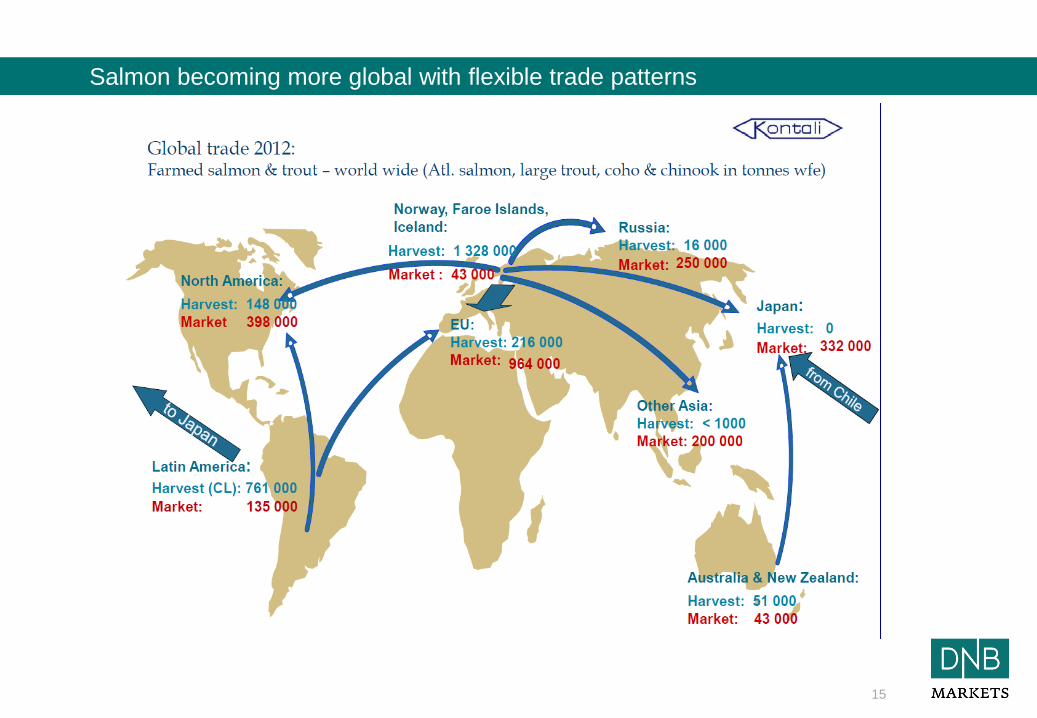

Salmon becoming more global with flexible trade patterns

Source: Ministry of fisheries, DNB Markets

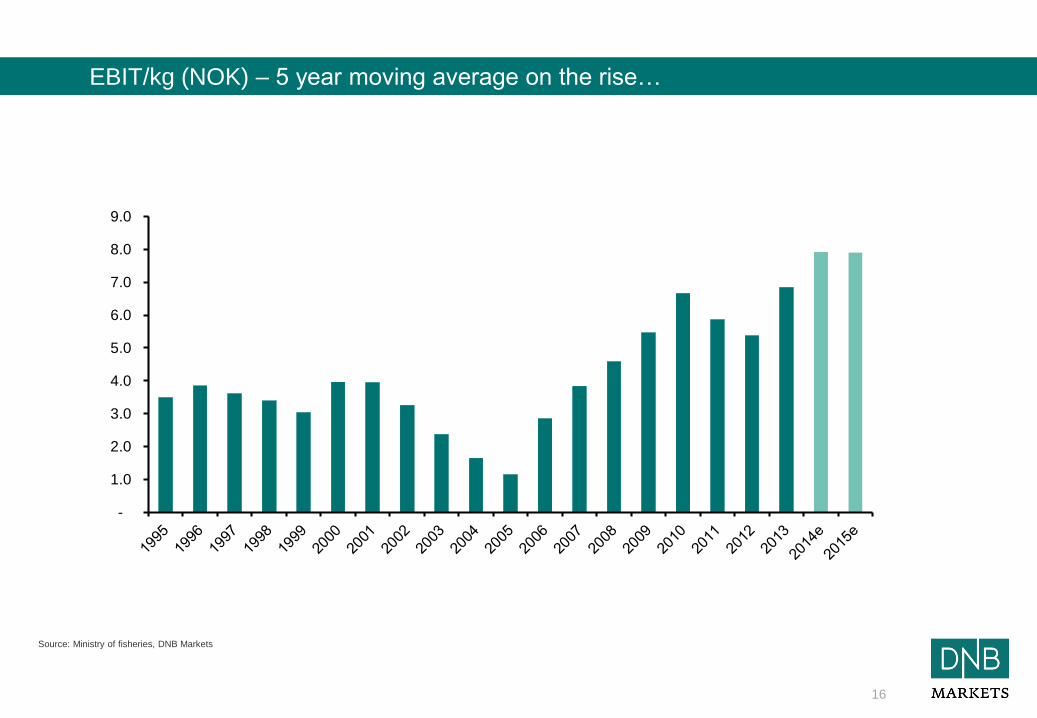

EBIT/kg (NOK) – 5 year moving average on the rise…

16

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

*SalMar and Bakkafrost is already at +NOK10/kg average 2006-2015e

17

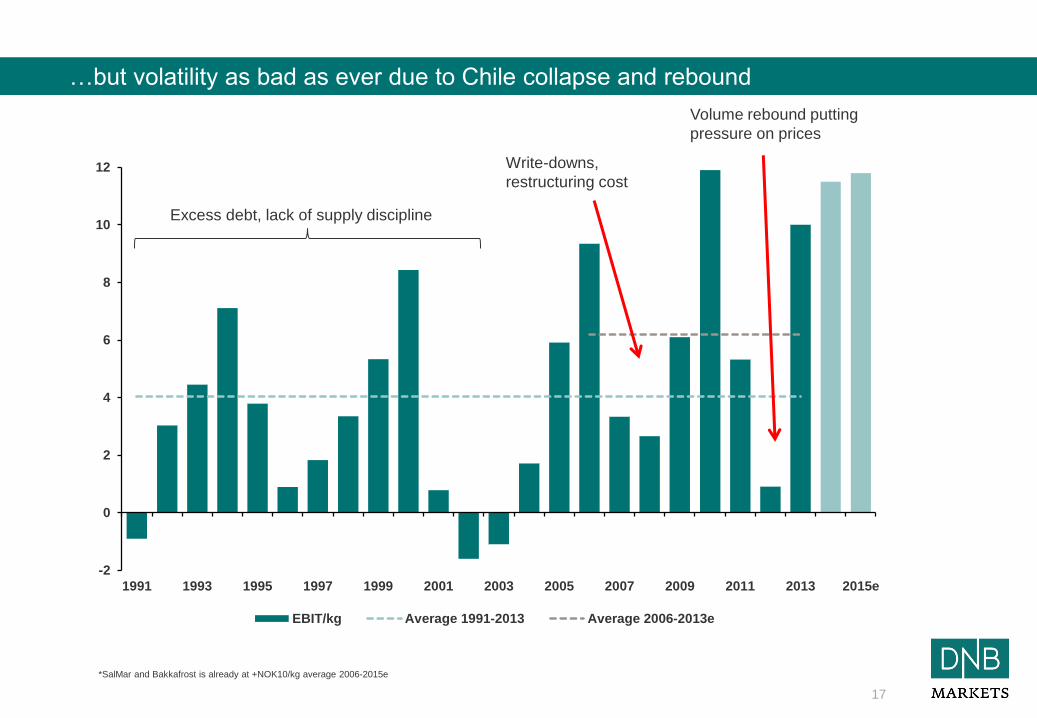

…but volatility as bad as ever due to Chile collapse and rebound

-2

0

2

4

6

8

10

12

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015e

EBIT/kg Average 1991-2013 Average 2006-2013e

Write-downs,

restructuring cost

Volume rebound putting

pressure on prices

Excess debt, lack of supply discipline

18

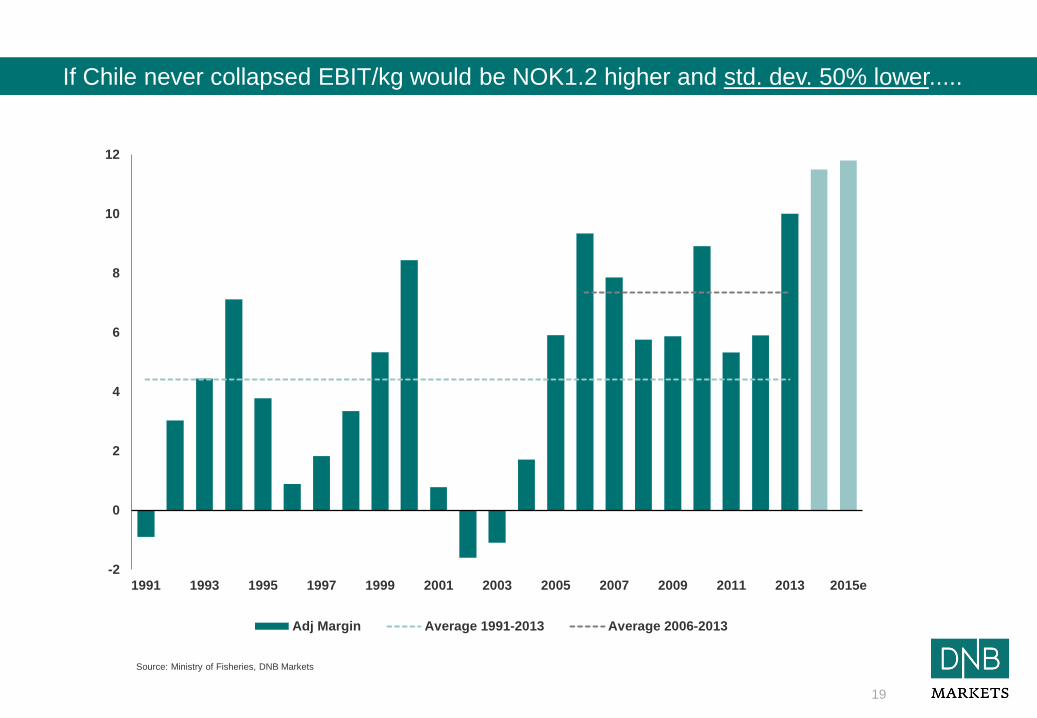

What if Chile never collapsed……

Source: Ministry of Fisheries, DNB Markets

If Chile never collapsed EBIT/kg would be NOK1.2 higher and std. dev. 50% lower.....

19

-2

0

2

4

6

8

10

12

1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015e

Adj Margin Average 1991-2013 Average 2006-2013

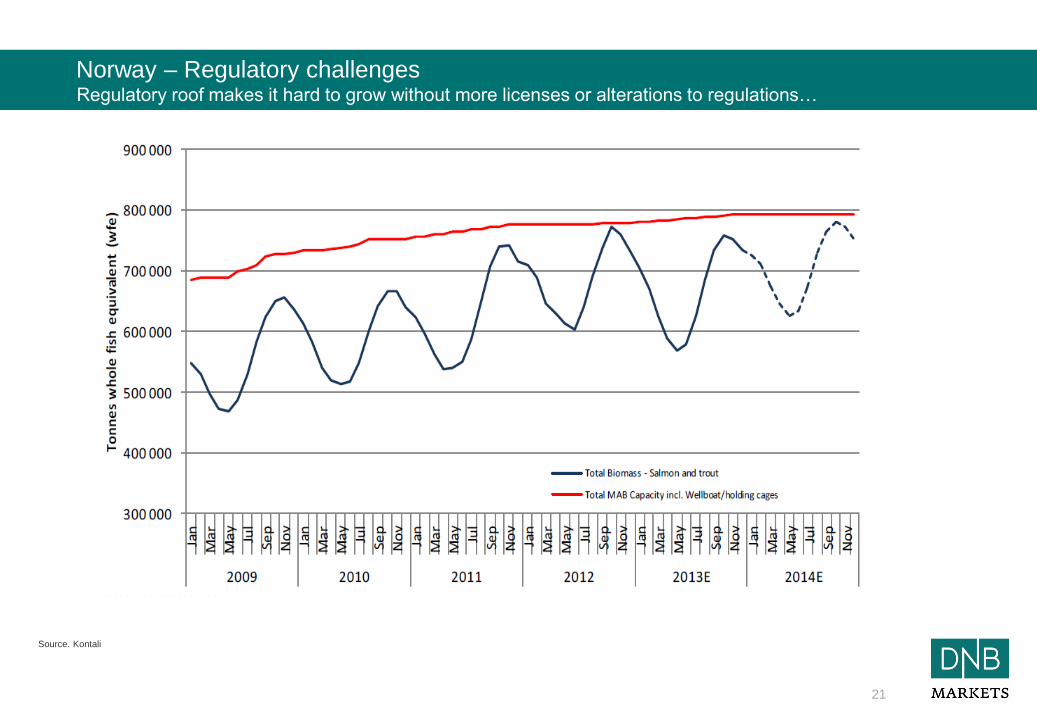

No rolling MAB in Norway

Growth in Norway will be accompanies by very strict demands to

biological sustainability

20

Latest Seafood Sector update titled – Few clouds in the sky

Source. Kontali

Norway – Regulatory challenges Regulatory roof makes it hard to grow without more licenses or alterations to regulations…

21

22

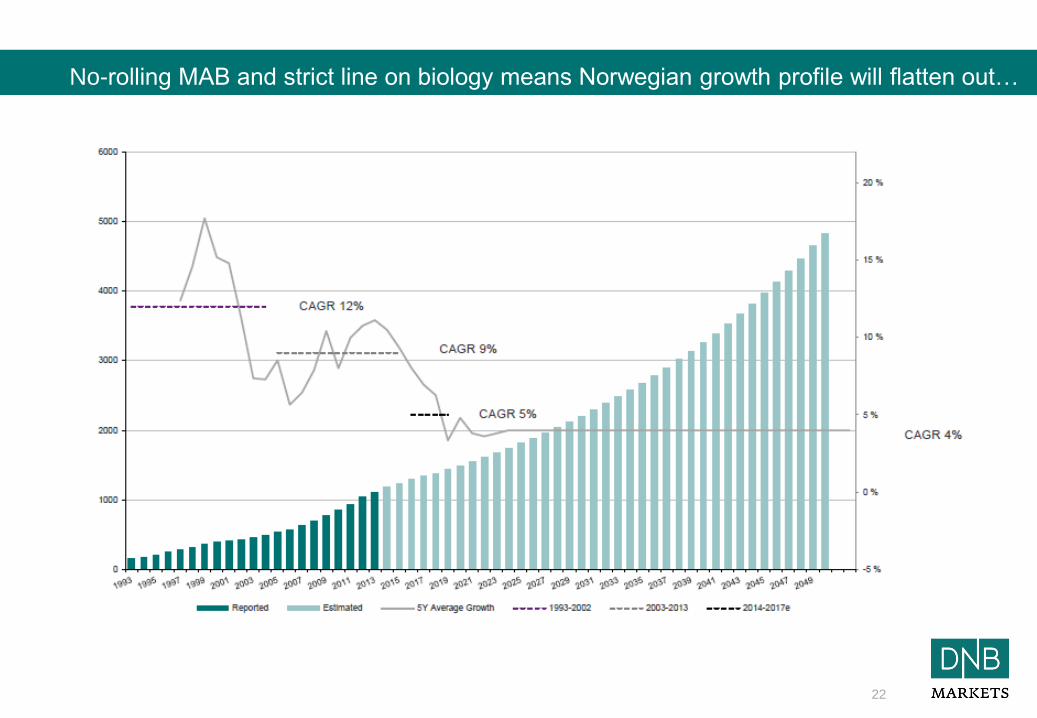

No-rolling MAB and strict line on biology means Norwegian growth profile will flatten out…

Source: Aquacbench, DNB Markets

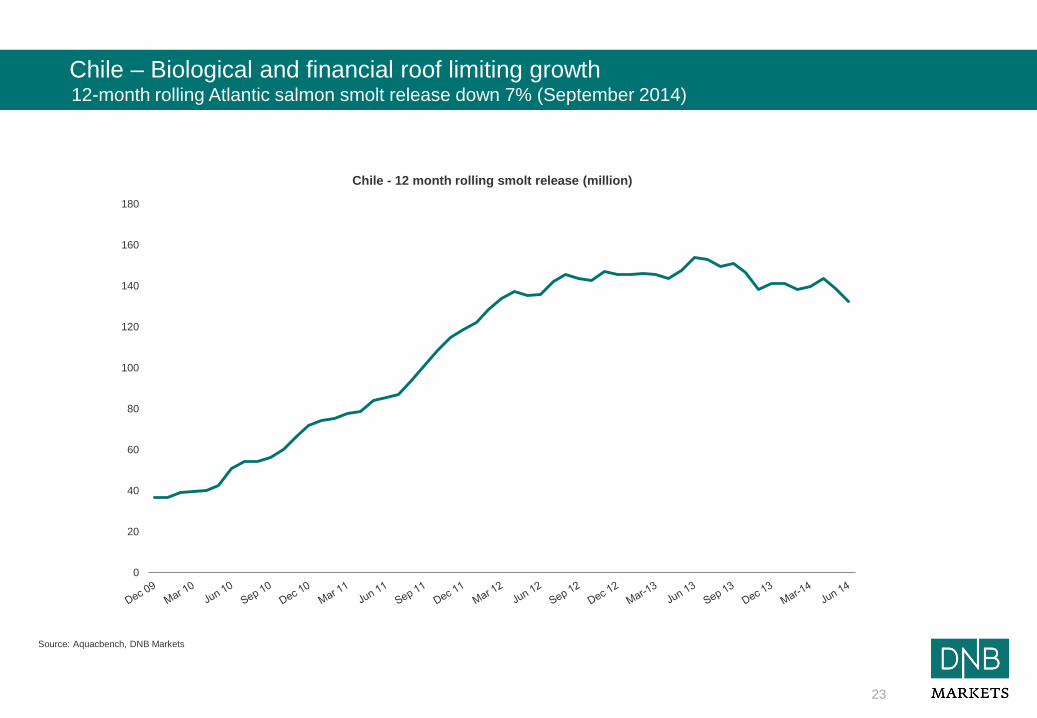

Chile – Biological and financial roof limiting growth 12-month rolling Atlantic salmon smolt release down 7% (September 2014)

23

0

20

40

60

80

100

120

140

160

180

Chile - 12 month rolling smolt release (million)

24

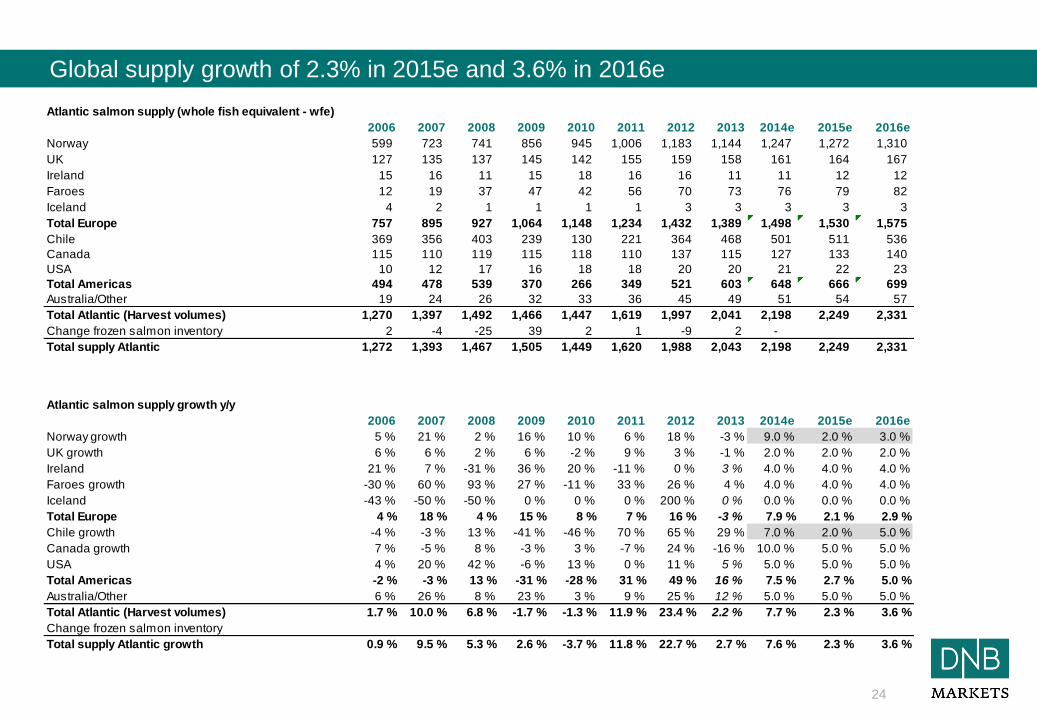

Global supply growth of 2.3% in 2015e and 3.6% in 2016e

Atlantic salmon supply (whole fish equivalent - wfe)

2006 2007 2008 2009 2010 2011 2012 2013 2014e 2015e 2016e

Norway 599 723 741 856 945 1,006 1,183 1,144 1,247 1,272 1,310

UK 127 135 137 145 142 155 159 158 161 164 167

Ireland 15 16 11 15 18 16 16 11 11 12 12

Faroes 12 19 37 47 42 56 70 73 76 79 82

Iceland 4 2 1 1 1 1 3 3 3 3 3

Total Europe 757 895 927 1,064 1,148 1,234 1,432 1,389 1,498 1,530 1,575

Chile 369 356 403 239 130 221 364 468 501 511 536

Canada 115 110 119 115 118 110 137 115 127 133 140

USA 10 12 17 16 18 18 20 20 21 22 23

Total Americas 494 478 539 370 266 349 521 603 648 666 699

Australia/Other 19 24 26 32 33 36 45 49 51 54 57

Total Atlantic (Harvest volumes) 1,270 1,397 1,492 1,466 1,447 1,619 1,997 2,041 2,198 2,249 2,331

Change frozen salmon inventory 2 -4 -25 39 2 1 -9 2 -

Total supply Atlantic 1,272 1,393 1,467 1,505 1,449 1,620 1,988 2,043 2,198 2,249 2,331

Atlantic salmon supply growth y/y

2006 2007 2008 2009 2010 2011 2012 2013 2014e 2015e 2016e

Norway growth 5 % 21 % 2 % 16 % 10 % 6 % 18 % -3 % 9.0 % 2.0 % 3.0 %

UK growth 6 % 6 % 2 % 6 % -2 % 9 % 3 % -1 % 2.0 % 2.0 % 2.0 %

Ireland 21 % 7 % -31 % 36 % 20 % -11 % 0 % 3 % 4.0 % 4.0 % 4.0 %

Faroes growth -30 % 60 % 93 % 27 % -11 % 33 % 26 % 4 % 4.0 % 4.0 % 4.0 %

Iceland -43 % -50 % -50 % 0 % 0 % 0 % 200 % 0 % 0.0 % 0.0 % 0.0 %

Total Europe 4 % 18 % 4 % 15 % 8 % 7 % 16 % -3 % 7.9 % 2.1 % 2.9 %

Chile growth -4 % -3 % 13 % -41 % -46 % 70 % 65 % 29 % 7.0 % 2.0 % 5.0 %

Canada growth 7 % -5 % 8 % -3 % 3 % -7 % 24 % -16 % 10.0 % 5.0 % 5.0 %

USA 4 % 20 % 42 % -6 % 13 % 0 % 11 % 5 % 5.0 % 5.0 % 5.0 %

Total Americas -2 % -3 % 13 % -31 % -28 % 31 % 49 % 16 % 7.5 % 2.7 % 5.0 %

Australia/Other 6 % 26 % 8 % 23 % 3 % 9 % 25 % 12 % 5.0 % 5.0 % 5.0 %

Total Atlantic (Harvest volumes) 1.7 % 10.0 % 6.8 % -1.7 % -1.3 % 11.9 % 23.4 % 2.2 % 7.7 % 2.3 % 3.6 %

Change frozen salmon inventory

Total supply Atlantic growth 0.9 % 9.5 % 5.3 % 2.6 % -3.7 % 11.8 % 22.7 % 2.7 % 7.6 % 2.3 % 3.6 %

Analysts: Alexander Aukner (+47 24 16 90 79; [email protected] )

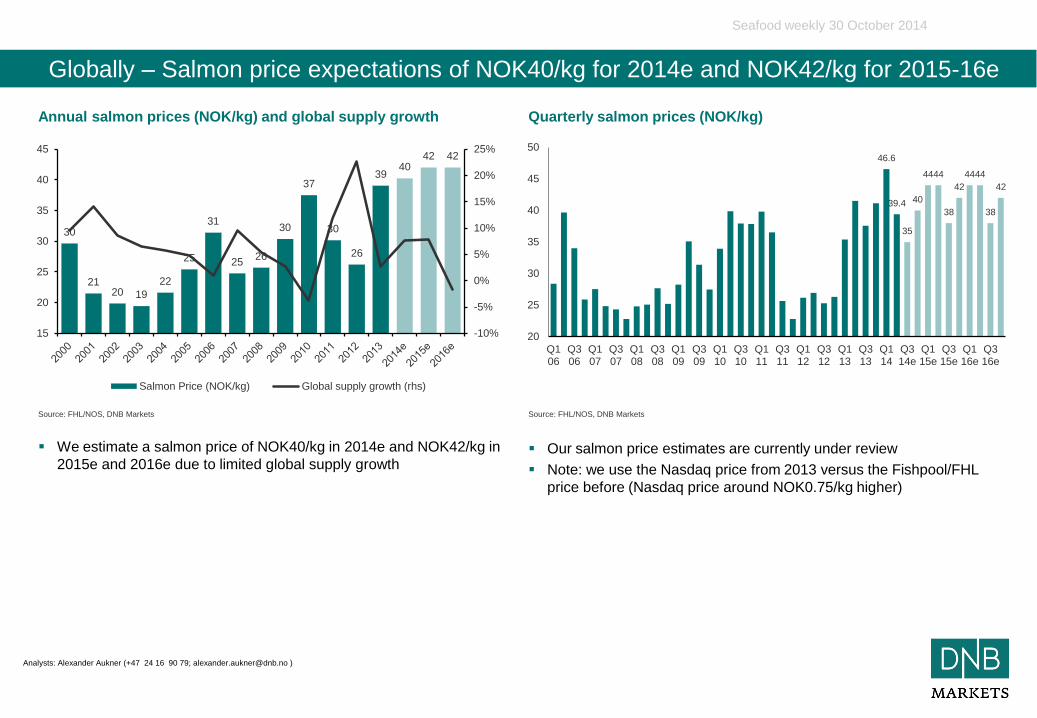

Seafood weekly 30 October 2014

We estimate a salmon price of NOK40/kg in 2014e and NOK42/kg in

2015e and 2016e due to limited global supply growth

Globally – Salmon price expectations of NOK40/kg for 2014e and NOK42/kg for 2015-16e

Our salmon price estimates are currently under review

Note: we use the Nasdaq price from 2013 versus the Fishpool/FHL

price before (Nasdaq price around NOK0.75/kg higher)

Source: FHL/NOS, DNB Markets Source: FHL/NOS, DNB Markets

Annual salmon prices (NOK/kg) and global supply growth Quarterly salmon prices (NOK/kg)

30

21 20 19

22

25

31

25 26

30

37

30

26

39 40

42 42

-10%

-5%

0%

5%

10%

15%

20%

25%

15

20

25

30

35

40

45

Salmon Price (NOK/kg) Global supply growth (rhs)

46.6

39.4

35

40

44 44

38

42

44 44

38

42

20

25

30

35

40

45

50

Q106

Q306

Q107

Q307

Q108

Q308

Q109

Q309

Q110

Q310

Q111

Q311

Q112

Q312

Q113

Q313

Q114

Q314e

Q115e

Q315e

Q116e

Q316e

Extract from the consultation note - the draft regulations on capacity increases in salmon and trout farming in 2015

The report "Value creation based on productive seas in 2050" envisions the future of Norwegian marine industries. On the

condition that we manage to solve environmental problems in the aquaculture industry and that there is political will to prioritize

aquaculture industry has a far greater growth potential than is being utilized today. To realize the potential of reporting in 2050

there must be growth and development in salmon farming. The growth of salmon farming should probably be somewhere

between three and five percent on average per year for the industry to be able to produce five million tonnes in 2050

The government will publish a white paper on predictable and sustainable growth of aquaculture in the spring of 2015. The effect

of growth policies in the message we will probably only be able to begin to see in 2017, while the increase in capacity now take

effect as early as 2015. The "strictness" that we present today, will be taken with us in the work on the white paper.

26

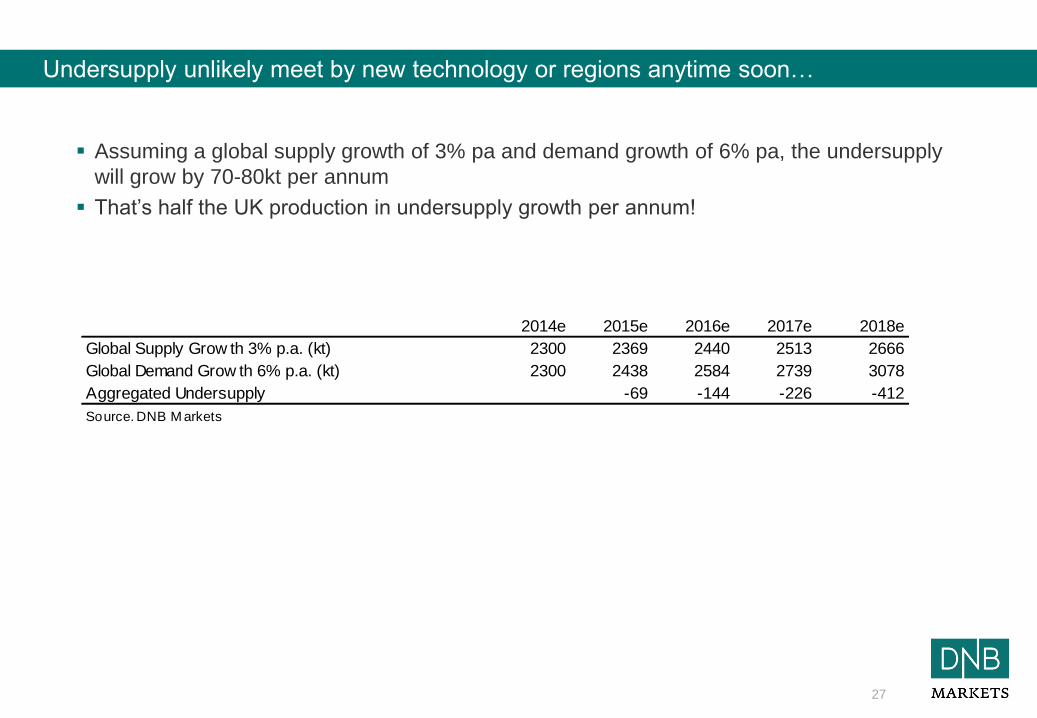

And what about the growth profile post 2017….?

…seems 3-5% annual growth is the number to look for, but growth

may be even lower until sea-lice problems are resolved

Assuming a global supply growth of 3% pa and demand growth of 6% pa, the undersupply

will grow by 70-80kt per annum

That’s half the UK production in undersupply growth per annum!

27

Undersupply unlikely meet by new technology or regions anytime soon…

2014e 2015e 2016e 2017e 2018e

Global Supply Grow th 3% p.a. (kt) 2300 2369 2440 2513 2666

Global Demand Grow th 6% p.a. (kt) 2300 2438 2584 2739 3078

Aggregated Undersupply -69 -144 -226 -412

Source. DNB M arkets

Solid balance sheets and attractive valuations mean we

remain positive to the sector

29

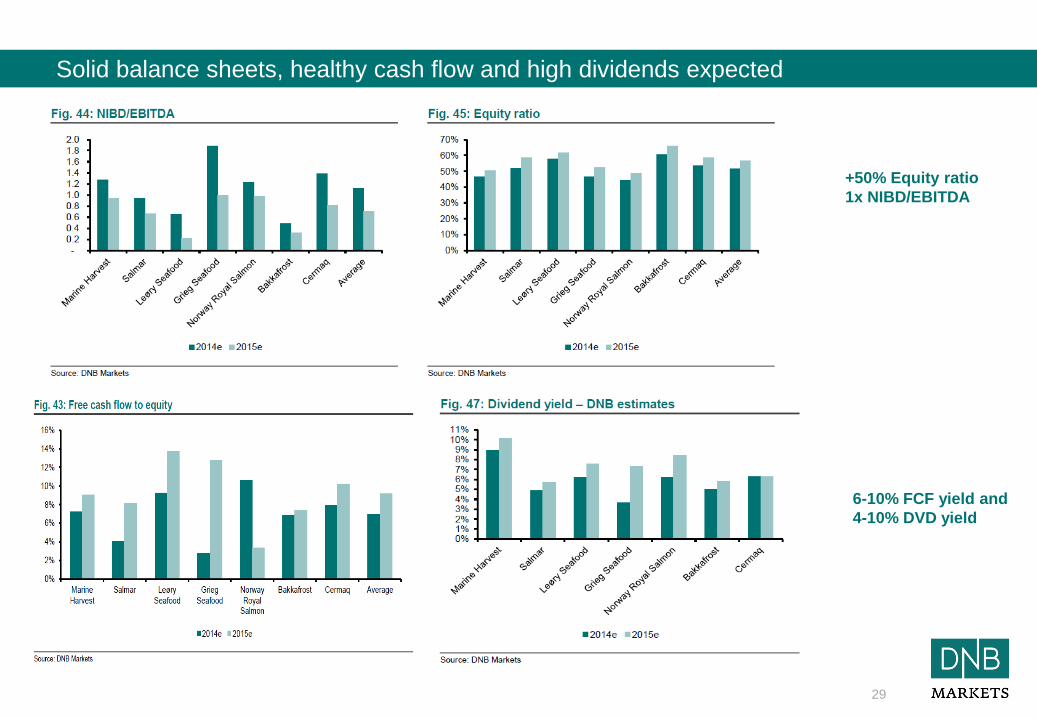

Solid balance sheets, healthy cash flow and high dividends expected

+50% Equity ratio

1x NIBD/EBITDA

6-10% FCF yield and

4-10% DVD yield

30

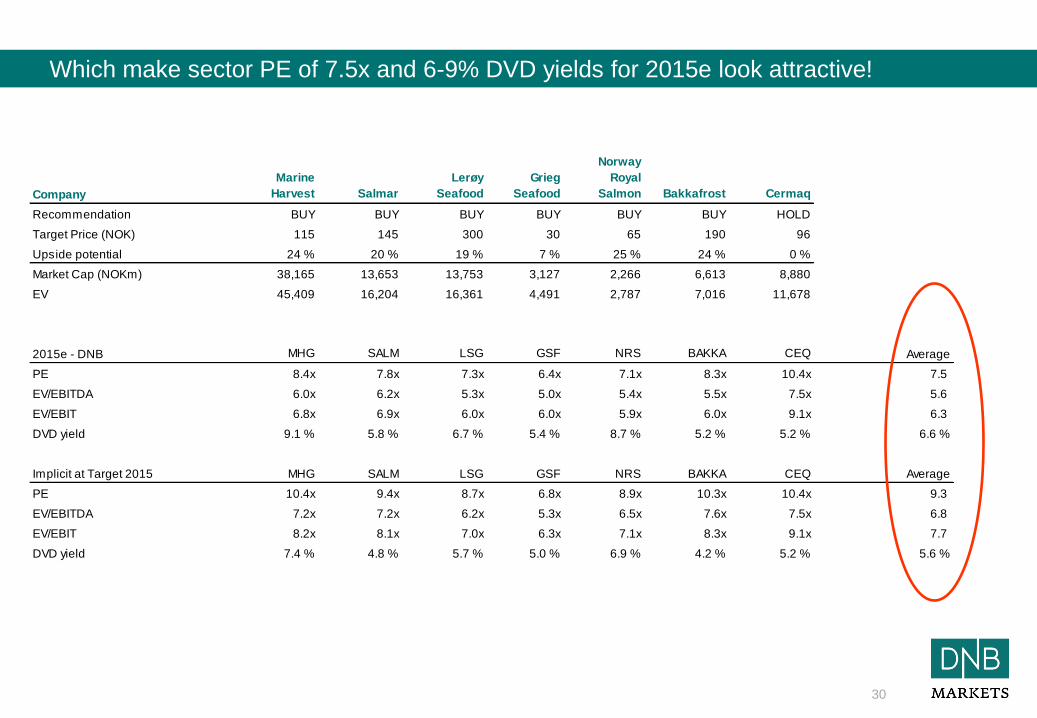

Which make sector PE of 7.5x and 6-9% DVD yields for 2015e look attractive!

CEQ – Bid from

Mitsubishi Corp.

Company

Marine

Harvest Salmar

Lerøy

Seafood

Grieg

Seafood

Norway

Royal

Salmon Bakkafrost Cermaq

Recommendation BUY BUY BUY BUY BUY BUY HOLD

Target Price (NOK) 115 145 300 30 65 190 96

Upside potential 24 % 20 % 19 % 7 % 25 % 24 % 0 %

Market Cap (NOKm) 38,165 13,653 13,753 3,127 2,266 6,613 8,880

EV 45,409 16,204 16,361 4,491 2,787 7,016 11,678

2015e - DNB MHG SALM LSG GSF NRS BAKKA CEQ Average

PE 8.4x 7.8x 7.3x 6.4x 7.1x 8.3x 10.4x 7.5

EV/EBITDA 6.0x 6.2x 5.3x 5.0x 5.4x 5.5x 7.5x 5.6

EV/EBIT 6.8x 6.9x 6.0x 6.0x 5.9x 6.0x 9.1x 6.3

DVD yield 9.1 % 5.8 % 6.7 % 5.4 % 8.7 % 5.2 % 5.2 % 6.6 %

Implicit at Target 2015 MHG SALM LSG GSF NRS BAKKA CEQ Average

PE 10.4x 9.4x 8.7x 6.8x 8.9x 10.3x 10.4x 9.3

EV/EBITDA 7.2x 7.2x 6.2x 5.3x 6.5x 7.6x 7.5x 6.8

EV/EBIT 8.2x 8.1x 7.0x 6.3x 7.1x 8.3x 9.1x 7.7

DVD yield 7.4 % 4.8 % 5.7 % 5.0 % 6.9 % 4.2 % 5.2 % 5.6 %

31

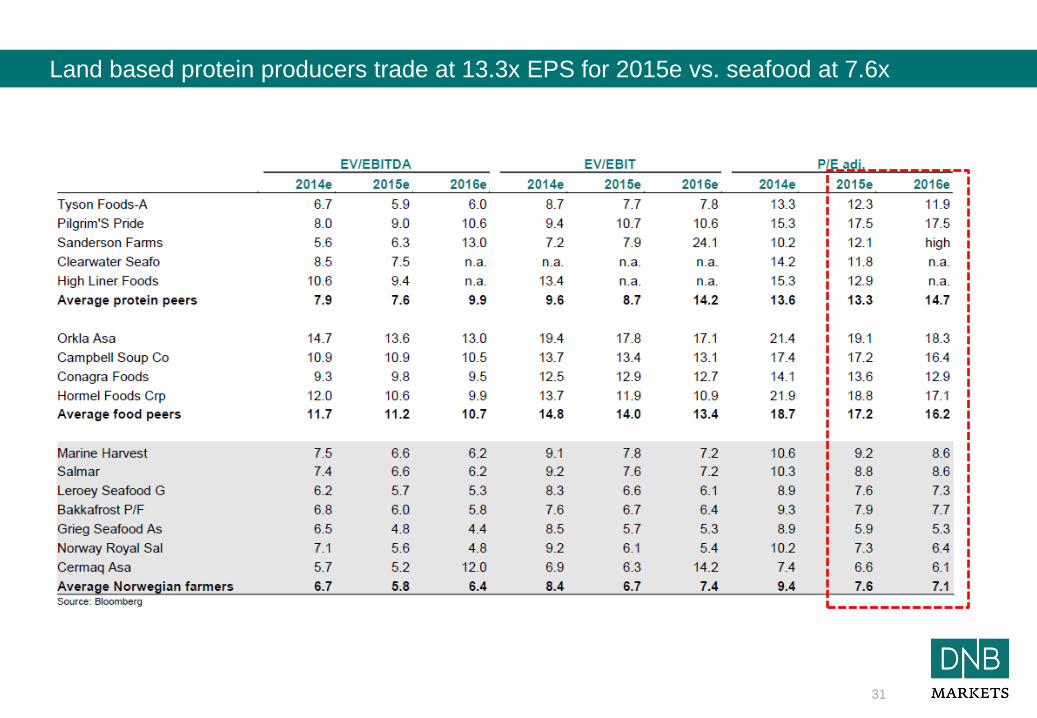

Land based protein producers trade at 13.3x EPS for 2015e vs. seafood at 7.6x

32

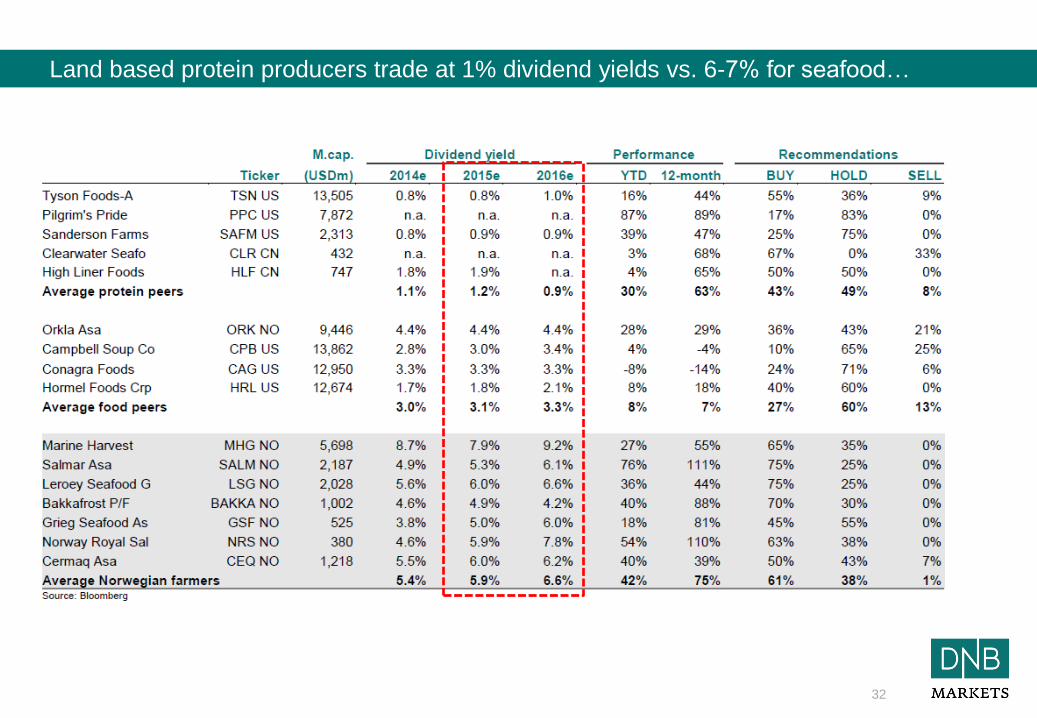

Land based protein producers trade at 1% dividend yields vs. 6-7% for seafood…

33

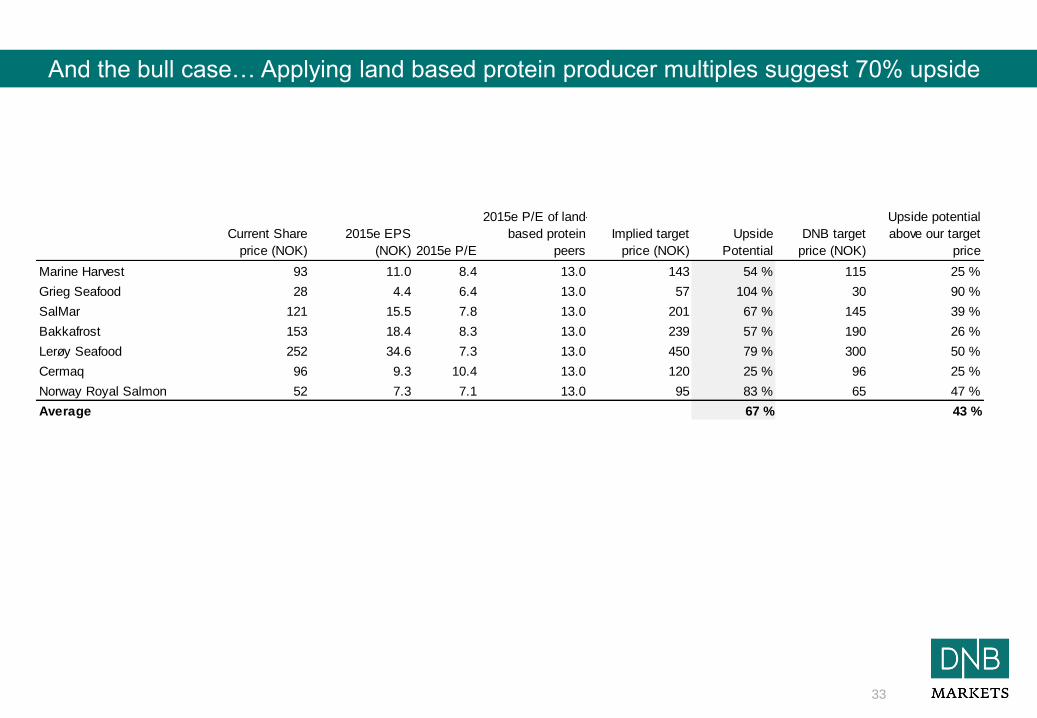

And the bull case… Applying land based protein producer multiples suggest 70% upside

Current Share

price (NOK)

2015e EPS

(NOK) 2015e P/E

2015e P/E of land-

based protein

peers

Implied target

price (NOK)

Upside

Potential

DNB target

price (NOK)

Upside potential

above our target

price

Marine Harvest 93 11.0 8.4 13.0 143 54 % 115 25 %

Grieg Seafood 28 4.4 6.4 13.0 57 104 % 30 90 %

SalMar 121 15.5 7.8 13.0 201 67 % 145 39 %

Bakkafrost 153 18.4 8.3 13.0 239 57 % 190 26 %

Lerøy Seafood 252 34.6 7.3 13.0 450 79 % 300 50 %

Cermaq 96 9.3 10.4 13.0 120 25 % 96 25 %

Norway Royal Salmon 52 7.3 7.1 13.0 95 83 % 65 47 %

Average 67 % 43 %

34

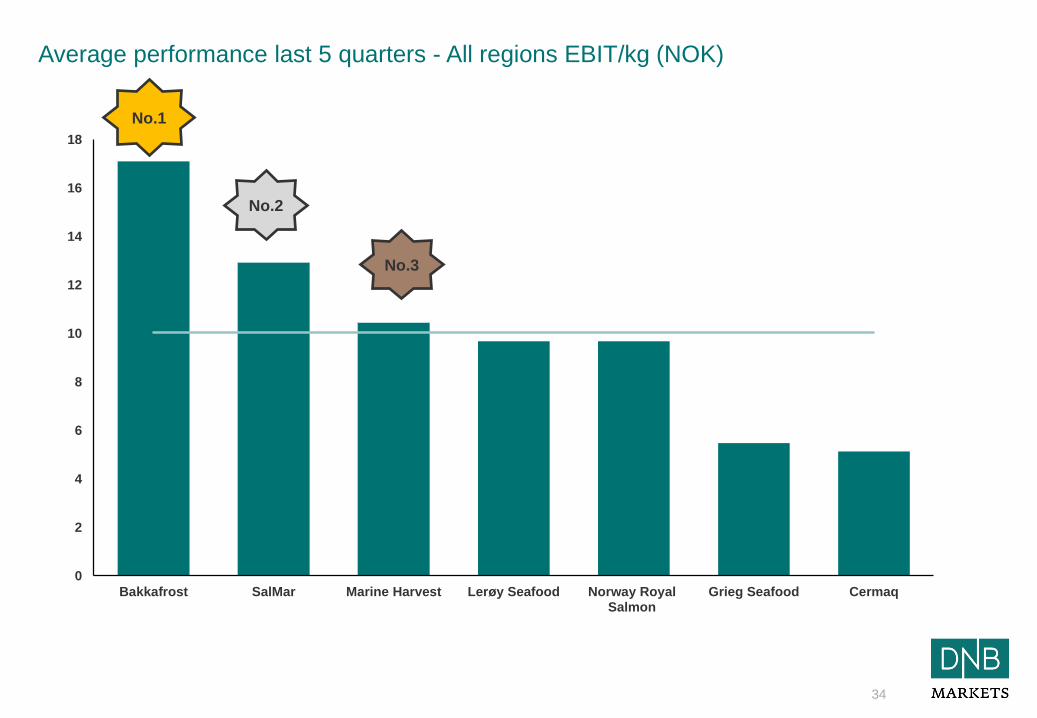

Average performance last 5 quarters - All regions EBIT/kg (NOK)

0

2

4

6

8

10

12

14

16

18

Bakkafrost SalMar Marine Harvest Lerøy Seafood Norway RoyalSalmon

Grieg Seafood Cermaq

No.1

No.2

No.3

35

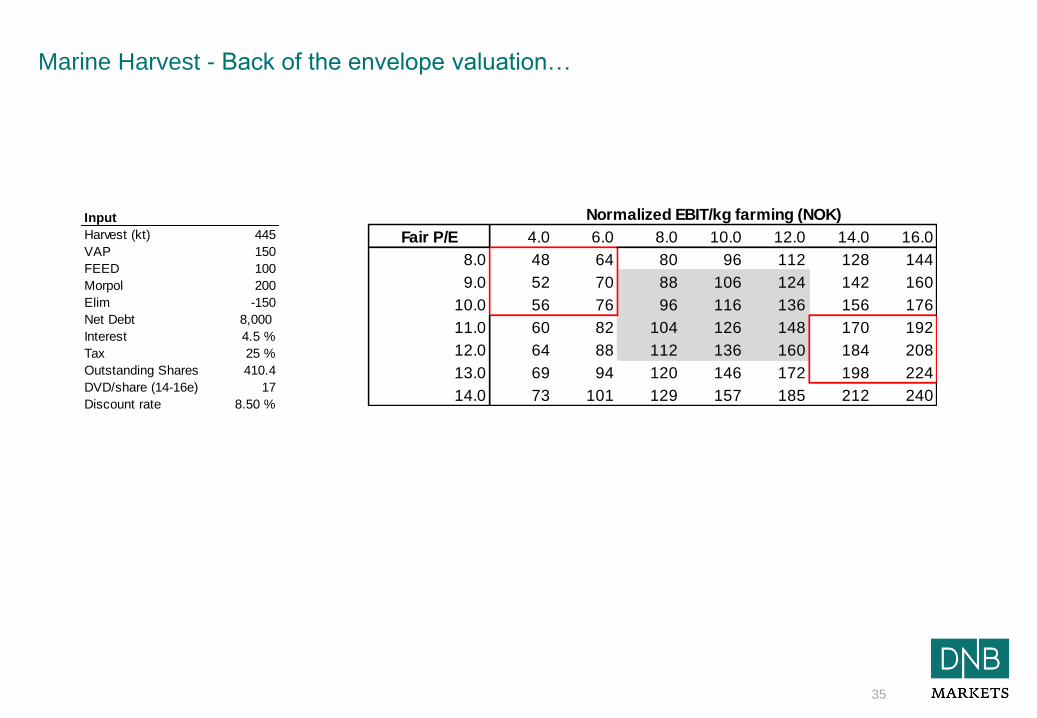

Marine Harvest - Back of the envelope valuation…

Fair P/E 4.0 6.0 8.0 10.0 12.0 14.0 16.0

8.0 48 64 80 96 112 128 144

9.0 52 70 88 106 124 142 160

10.0 56 76 96 116 136 156 176

11.0 60 82 104 126 148 170 192

12.0 64 88 112 136 160 184 208

13.0 69 94 120 146 172 198 224

14.0 73 101 129 157 185 212 240

Normalized EBIT/kg farming (NOK)Input

Harvest (kt) 445

VAP 150

FEED 100

Morpol 200

Elim -150

Net Debt 8,000

Interest 4.5 %

Tax 25 %

Outstanding Shares 410.4

DVD/share (14-16e) 17

Discount rate 8.50 %

Morning Presentation

36

Disclaimer

IMPORTANT/DISCLAIMER

This note (the “Note”) must be seen as marketing material and not as an investment recommendation within the meaning of the Norwegian Securities Trading Act of 2007 paragraph 3-10 and the

Norwegian Securities Trading Regulation 2007/06/29 no. 876. The Note has been prepared by DNB Markets, a division of DNB Bank ASA, a Norwegian bank organized under the laws of the

Kingdom of Norway (the “Bank”), for information purposes only. The Note shall not be used for any unlawful or unauthorized purposes. The Bank, its affiliates, and any third-party providers, as well

as their directors, officers, shareholders, employees or agents (individually, each a “DNB Party”; collectively, “DNB Parties”) do not guarantee the accuracy, completeness, timeliness or availability of

the Note. DNB Parties are not responsible for any errors or omissions, regardless of the cause, nor for the results obtained from the use of the Note, nor for the security or maintenance of any data

input by the user. The Note is provided on an “as is” basis. DNB PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY

WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE NOTE’S

FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE NOTE WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall DNB Parties be liable to any

party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost

profits and opportunity costs) in connection with any use of the Note, even if advised of the possibility of such damages. Any opinions expressed herein reflect the Bank’s judgment at the time the

Note was prepared and DNB Parties assume no obligation to update the Note in any form or format. The Note should not be relied on and is not a substitute for the skill, judgment and experience of

the user, its management, employees, advisors and/or clients when making investment and other business decisions. No DNB Party is acting as fiduciary or investment advisor in connection with the

dissemination of the Note. While the Note is based on information obtained from public sources that the Bank believes to be reliable, no DNB Party has performed an audit of, nor accepts any duty of

due diligence or independent verification of, any information it receives. Confidentiality rules and internal rules restrict the exchange of information between different parts of the Bank and this may

prevent employees of DNB Markets who are preparing the Note from utilizing or being aware of information available in DNB Markets/the Bank which may be relevant to the recipients of the Note.

Please contact DNB Markets at + 47 22 94 89 98 for further information and inquiries regarding this Note, such as ownership positions and publicly available/commonly known corporate advisory

performed by DNB Markets etc, in relation to the Norwegian Securities Trading Act 2007/06/29 no. 75 and the Norwegian Securities Trading Regulation 2007/06/29 no. 876.

The Note is not an offer to buy or sell any security or other financial instrument or to participate in any investment strategy. Distribution of material like the Note is in certain jurisdictions restricted by

law. Persons in possession of the Note should seek further guidance regarding such restrictions before distributing the Note.

The Note is for clients only, and not for publication, and has been prepared for information purposes only by DNB Markets - a division of DNB Bank ASA registered in Norway with registration number

NO 984 851 006 (the Register of Business Enterprises) under supervision of the Financial Supervisory Authority of Norway (Finanstilsynet), Monetary Authority of Singapore, the Chilean

Superintendent of Banks, and on a limited basis by the Financial Services Authority of UK. Information about DNB Markets can be found at dnb.no.

Additional information for clients in Singapore

The Note has been distributed by the Singapore branch of DNB Bank ASA. It is intended for general circulation and does not take into account the specific investment objectives, financial situation or

particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of any product referred to in the Note, taking into account your specific financial

objectives, financial situation or particular needs before making a commitment to purchase any such product.

Recipients of the Note should note that, by virtue of their status as “accredited investors” or “expert investors”, the Singapore branch of DNB Bank ASA will be exempt from complying with certain

compliance requirements under the Financial Advisers Act, Chapter 110 of Singapore (the “FAA”), the Financial Advisers Regulations and associated regulations there under. In particular, it will be

exempt from: - Section 27 of the FAA (which requires that there must be a reasonable basis for recommendations when making recommendations on investments).

Please contact the Singapore branch of DNB Bank ASA at +65 6212 0753 in respect of any matters arising from, or in connection with, the Note.

We, the DNB group, our associates, officers and/or employees may have interests in any products referred to in the Note by acting in various roles including as distributor, holder of principal

positions, adviser or lender. We, the DNB group, our associates, officers and/or employees may receive fees, brokerage or commissions for acting in those capacities. In addition, we, the DNB group,

our associates, officers and/or employees may buy or sell products as principal or agent and may effect transactions which are not consistent with the information set out in the Note.

Additional Information, including for Recipients in the In the United States:

The Note does not constitute an offer to sell or buy a security and does not include information, opinions, or recommendations with respect to securities of an issuer or an analysis of a

security or an issuer; rather, it is a “market letter,” as the term is defined in NASD Rule 2211.