Embed Size (px)

Citation preview

Intra Energy Corporation: African coal for African Growth May 2012 – Sydney Resources Round Up Graeme Robertson, Exec. Chairman

Sydney, Australia

For

per

sona

l use

onl

y

1

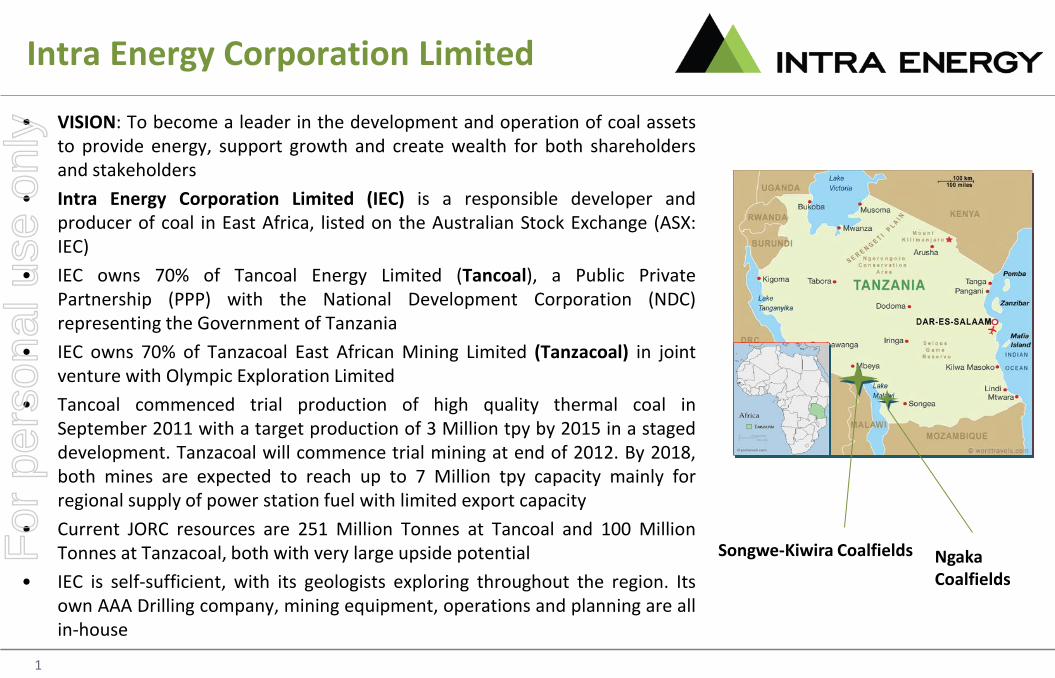

• VISION: To become a leader in the development and operation of coal assets to provide energy, support growth and create wealth for both shareholders and stakeholders

• Intra Energy Corporation Limited (IEC) is a responsible developer and producer of coal in East Africa, listed on the Australian Stock Exchange (ASX: IEC)

• IEC owns 70% of Tancoal Energy Limited (Tancoal), a Public Private Partnership (PPP) with the National Development Corporation (NDC) representing the Government of Tanzania

• IEC owns 70% of Tanzacoal East African Mining Limited (Tanzacoal) in joint venture with Olympic Exploration Limited

• Tancoal commenced trial production of high quality thermal coal in September 2011 with a target production of 3 Million tpy by 2015 in a staged development. Tanzacoal will commence trial mining at end of 2012. By 2018, both mines are expected to reach up to 7 Million tpy capacity mainly for regional supply of power station fuel with limited export capacity

• Current JORC resources are 251 Million Tonnes at Tancoal and 100 Million Tonnes at Tanzacoal, both with very large upside potential

• IEC is self-sufficient, with its geologists exploring throughout the region. Its own AAA Drilling company, mining equipment, operations and planning are all in-house

Intra Energy Corporation Limited

Songwe-Kiwira Coalfields Ngaka Coalfields

For

per

sona

l use

onl

y

2

• Population 45 million people, approximately 45% Christian, 35% Muslim

• Not a tribal society, identification more with birthplace

• Politically stable, multi-party democracy, 30% of Members of Parliament are female

• Free Press, English and Swahili speaking, British Common Law system

• Globally competitive tax and regulatory framework for investors but legislation and decision making process needs improvement

• Strategic infrastructure hub for trade to/from Malawi, Zambia, DR Congo, Burundi, Rwanda and Uganda – common borders

• Well-established mining services industry, third largest gold producer in Africa

• Largest city and port is Dar es Salaam

TANZANIA F

or p

erso

nal u

se o

nly

3

• Minerally and agriculturally wealthy, Tanzania and neighbouring nations are some of the poorest in the world

• Change is occurring with major gas discoveries offshore and exploration of the great lakes expected to yield oil and gas

• IMF forecasts GDP growth in 2012 at 6.4% noting that growth is restrained by severe electricity shortage

• Industrial production expensive with cement, textiles, cotton, breweries, coffee, tobacco and limestone industries suffering from expensive diesel generation and unreliable supply

• Installed capacity of electricity generation 1,190MW of which currently only 610MW is operational, from hydro, gas and diesel generation

• Rich in unexploited energy – coal, gas and geothermal – TANCOAL is, however, the first operating coal mine in the East African region. There are no base load coal-fired power stations in East Africa

• As Tancoal is a PPP, political risk of resource nationalisation is minimised

Tanzania, East Africa

Songea Main roads Railway

Tanga

For

per

sona

l use

onl

y

4

African Coal for African Growth Major coal producers in South Africa, Botswana and Mozambique are focused on coal for export to India and China. Most thermal coal outside South Africa is lower quality and requires coal preparation to reduce ash and upgrade heating value. Massive infrastructure costs are in excess of mining costs. Shareholders fund infrastructure rather than mining and compete for market shares with cheaper production from Indonesia. Intra Energy’s focus is on Central East African domestic and regional supply to support industrialisation and electricity generation critical to economic growth in a region which is growing at nearly the same rate as India and China. IEC has limited competition as the only coal producer in the region, is using existing infrastructure and has a high quality coal which in Tancoal does not require coal preparation with its loss in saleable coal.

Rwanda • 2010 GDP growth: 7.5% • 2012 GDP estimated growth: 7.9% • Electricity shortage reaching critical

Mozambique • 2010 GDP growth 7.2% • 2012 GDP estimated growth: 7.5% • FDI for coal mines and infrastructure

Kenya • 2010 GDP growth: 5.6% • 2012 GDP estimated growth 6.1% • Electricity shortage, election 2012

Tanzania • 2010 GDP growth 7.0% • 2012 GDP estimated growth: 6.4% • Electricity crisis

Source of GDP data: International Monetary Fund, World Economic Outlook Database and local sources

Malawi • 2010 GDP growth: 7.2% • 2012 GDP estimated growth 5.1% • Electricity crisis and political change

Zambia • 2010 GDP growth: 7.6% • 2012 GDP estimated growth 6.7% • Power shortage, reduction in copper

output Average GDP estimated for 2012 is 6.4% for East African Nations compared to 6.8% for India and 6.1% for Indonesia with China at 8.2% but declining

For

per

sona

l use

onl

y

5

Intra Energy Strategic Development

• Domestic supply to Tanzanian industrial market using coal for import substitution (Tanzania imported 230,000 tonnes thermal coal in 2010) and replacement of diesel and wood in industrial processes. Limited export regionally to Malawi by barge and Kenya by road. Depletion of forests for kiln-firing targeted for coal replacement in tune with Tanzanian environmental concerns. Trucking is the highest cost component but competitive with South Africa and Mozambique coal into Mombasa Port, Kenya and throughout Tanzania/Malawi. Potential for 500,000 tonnes by 2015.

• Power generation with first 150MW (120MW nett) power station currently being designed and sited adjacent to Tancoal area for operation in 2015 and with the Power Purchase Agreement (PPA) under negotiation. Transmission expansion will allow additional generation connection at Songea, the main town. Other projects include mine mouth 450MW power generation at Tanzacoal and an integrated stockpile and generation facility near Dar es Salaam as well as industrially-related generation in Tanzania, Malawi and neighbouring countries. All coal-fired generation is base load.

• Export coal utilizing a southern growth corridor to the Port of Mtwara north of the border with Mozambique. Target markets are not India or China but specific Indian Ocean countries, Kenya and potentially Somalia. Supply to be partly tied to power generation where IEC is the fuel supply partner.

Stage 1 - Current

Stage 2 - 2012 - 2020

Stage 3 - 2016 onwards For

per

sona

l use

onl

y

6

Production • Tancoal JORC Resource 251 Million tonnes (Measured: 139mt; Indicated: 66mt; Inferred: 46mt) mainly to measured

status, Tanzacoal JORC resource 100 Million tonnes (Measured: 0mt; Indicated: 75mt; Inferred: 35mt), both open-ended with large upside potential

• Thermal coal is mined, crushed and stockpiled for quality product without expensive preparation/washing – sold on Raw basis

• Tancoal product is hauled to local stockpiles for trucking directly to consumers or barging across Lake Nyasa to Malawi and a northern stockpile area

• Tancoal quality on air-dried basis – CV 6,500Kcal/kg, Ash 18%, Inherent Moisture 3.0%, Volatile Matter 25% and Total Sulphur 0.5%. Tanzacoal is higher Ash and lower CV product

• Total IEC expenditure (including AAA Drilling below) USD 13M on operations for production capacity up to 35,000 tpm, USD 10M for acquisition of Tanzacoal properties and USD 10M in bank.

Sales • Tancoal sold 4,800mt in March 2012 to cement, gypsum and brewery companies • Sales will see gradual increases as the availability of reliable coal supply becomes apparent as this option had never

existed previously • Currently building trucking capacity and assessing infrastructure improvements – there is virtually no public road bulk

haulage in Tanzania (there has not been any coal mining!) • Tancoal is exporting approximately 1,100tpm to Malawi with trial supply by road to Kenya

Operations – First Modern Coal Mine in Tanzania

For

per

sona

l use

onl

y

7

AAA Drilling • IEC has established its own exploration drilling operation in Tanzania. AAA Drilling operates two new Atlas Copco rigs

and down hole logging equipment and is drilling for IEC’s African subsidiaries as well as undertaking external work for minerals, unconventional gas (CBM) and geothermal for profit enhancement

Exploration • Currently working to increase JORC resources and mine planning for Tancoal and mapping in Tanzacoal • IEC Exploration team currently also investigating coal deposits in neighbouring countries for development potential

Operations – First Modern Coal Mine in Tanzania - continued

Tancoal coal pit; setting up drill rig

For

per

sona

l use

onl

y

8

Tancoal Energy - Supply Chain

Clockwise from above: Tancoal coal pit; first shipment of coal from Ndumbi port; loading of barges at Tancoal; weighbridge in operation

For

per

sona

l use

onl

y

9

• Tancoal employs from the local community with training schemes in place to transfer technology and basic skills to support the mining operations

• Schools are being rebuilt and from secondary level the top five local students are selected monthly for special training in environmental, medical and mechanical skills

• “Mbalawala Women’s Group” was established after consultation with local women and in partnership with community leaders. The project aims to establish a number of activities so that the women learn new skills and will have an opportunity to run each activity as a business (for example briquette making). It also enables IEC to work with local women to improve their skills, health, independence and social equality

• Infrastructure is being upgraded with the construction and rebuilding of bridges, roads and port facilities

• Community involvement in vegetable production from pit backfill areas to be used for supply and catering to Tancoal personnel

Community Development Program F

or p

erso

nal u

se o

nly

10

Recent Achievements

Dec 2010 Mar 2011 Sep 2011

IEC increased its stake in Tancoal to 70%

(acquired minority interest)

Mining License Granted

Funding of IEC by Aspac Mining Ltd

Jun 2011

Commenced mine development planning,

purchasing mine equipment and upgrading

infrastructure -US$13 million

Mbalawala Environmental Approval granted

Signed port facilities

agreement with TPA

Commenced coal mining

Commencement of trial coal supply

Mar 2012

Commencement of coal supply on term

contracts/exports to Malawi and Kenya regional markets

Signed MOU with Tanesco for

150MW (120MW nett) power

station development

May/June 2012

Tanzacoal joint venture formed (70%

IEC) with 100M tonnes JORC

Mbalawala Ground Breaking Ceremony and

first overburden removal

For

per

sona

l use

onl

y

11

Vice-President visits Tancoal Mine F

or p

erso

nal u

se o

nly

12

IEC’s immediate focus for 2012 is to expand coal sales and hence production as well as drilling and geological work to increase JORC qualified resources for Tancoal; explore for new commercial coal deposits in neighbouring nations and pursue a staged power generation development opportunity

• Tanzania lacks base load power and sufficient electricity generating and transmission capacity (1,150MW installed, 600MW operating), restricting industrialisation, development and the basic rights of the people to access electricity. Historically, generation has been sourced from hydro and natural gas with private businesses based on generation from diesel gensets

• There is no coal-fired generation in Tanzania and its neighbouring countries as Tancoal is the first time that coal has been produced reliably in quantity in the region

• Coal can not only generate sufficient base load electricity to meet the industrial growth needs and electrification of Tanzania, utilising Tancoal and Tanzacoal as coal suppliers into mine mouth generation, but also create revenue from the export of electricity to neighbouring countries. Coal provides the cheapest source of power – approximately ¼ of the cost of diesel generation

• IEC has completed a MOU with the Tanzania Electric Supply Company to enter into PPA negotiations for the development of a 150MW (120MW nett) mine mouth power station and is in discussions for the development of 450MW (3 stages, 150MW each) power stations at Tanzacoal and a number of 75MW units in strategic locations. A 150MW (120MW nett) coal-fired power station will consume approximately 400,000mt coal per year

2012 Focus F

or p

erso

nal u

se o

nly

13

Mr Graeme Robertson - Executive Chairman BA, FAICD, MAIE • Joined the board in November 2010, appointed Executive Chairman in January 2011 • Over 30 years experience in the coal, infrastructure and power development industries. CEO and Managing Director of New Hope

Corporation 1983 - 2005 • During this period he pioneered the development of major international companies including as President Director of Adaro Indonesia,

the largest single open cut coal mine in the Southern Hemisphere, President Director of Indonesia Bulk Terminal, a 12 mtpa capacity bulk coal port and an advisor to the development of the 1,230MW Paiton Power station, the first IPP in Indonesia

• His career has spanned both public and private energy related developments including directorships with the Port of Brisbane Authority and Washington H. Soul Pattinson & Co Ltd, one of Australia's oldest listed companies. He is currently Chairman of NuEnergy Gas Limited (ASX:NGY)

• Recipient of the Asia 500 Award in 2000 and the Coaltrans Lifetime Achievement Award in 2010 for his contribution to the coal industry

Mr David Mason – Executive Director, Exploration and Business Development MBA, BSc (Hons) • Joined the board in January 2011 • Over 30 years exploration, drilling and mining experience throughout Australasia • Previously a Director of Overseas & General Limited (ASX:OGL), a coal producer in Indonesia and Operations Director of Haddington

Resources (now Altura Mining, ASX:AJM) a diversified resource company, which acquired the resource investment and mining service companies of Minvest International, a group he co-founded and managed

• Former GM of the Minvest Group, and assisted in the development of the Adaro Indonesia coal mine, the MHU coal mine, a suite of exploration assets and mining service companies

Appendix

IEC Board of Directors F

or p

erso

nal u

se o

nly

14

Appendix

IEC Board of Directors – cont.

Mr Jonathan Warrand – Executive Director and Chief Financial Officer MBA (Exec), CA, FFinsia, Assoc. IPAA, BCom • Joined the board in January 2011 • Managing Director of Intrasia Capital Pty Limited, a proprietary investment firm in Sydney and through its related operations has

offices in Singapore and Mauritius • He has over twenty three years of corporate advisory across various sectors including soft and hard commodities, financial services

and real estate and has experience in equity and debt capital markets, strategic planning, capital management and corporate advisory

Mr Clive Hartz – Non-Executive Director and Deputy Chairman • Clive is Chairman and Chief Executive Officer of a private diverse investment group that he established in 1976. The group’s interests

span property, exploration, mining and construction and have included the development of retirement villages, offices, showrooms, industrial and residential buildings, subdivisions and shopping centres. Clive has held a number of public positions and was a director of Archangel Diamond Corporation, a Canadian listed company which made the first major diamond discovery in Russia by a western group. Clive was a key participant the resurrection of Skywest Airline in Western Australia. He is currently the President and Chairman of IGC Resources Inc., a Canadian listed resources company. Clive was a founding director of Intra Energy Corporation Limited.

For

per

sona

l use

onl

y

15

IEC Board of Directors – cont.

Mr Bill Paterson – Non-Executive Director BE (Civil) (Hons) • Joined the Board in March 2012 • Bill graduated in 1964 from Auckland University with an honours degree in civil engineering. From 1973, for 27 years, he made major

contributions as a director to the growth and success of one of Australia's premier engineering consultancies. That business in 2002 became a listed engineering services provider, now known as Worley Parsons Ltd.

• Bill has extensive experience and continuing involvement in the planning, design and implementation of a wide range of civil, infrastructure and building projects in the commercial, industrial and energy related sectors.

Dr Francis Lung – Non-Executive Director PhD, LLB • Joined in the Board in July 2011 • Dr Francis Lung is highly credentialed with a PHD in engineering (University of Leeds) and a Bachelor of Laws (University of London).

He has received awards for his scientific research in engineering and held senior positions within the infrastructure and utility industries over the past 22 years at companies such as Duke Energy, Royal Dutch Shell and Hong Kong Mass Transit Railway.

• Dr Lung is currently the Managing Director of the China Urban Infrastructure Fund which is a multi million dollar private equity fund investing in infrastructure projects in China. He is also the Chairman of a software company, and the Deputy Chairman & CEO of Hydrotech International, an ASX listed waterproofing technology company.

For

per

sona

l use

onl

y

16

Appendix

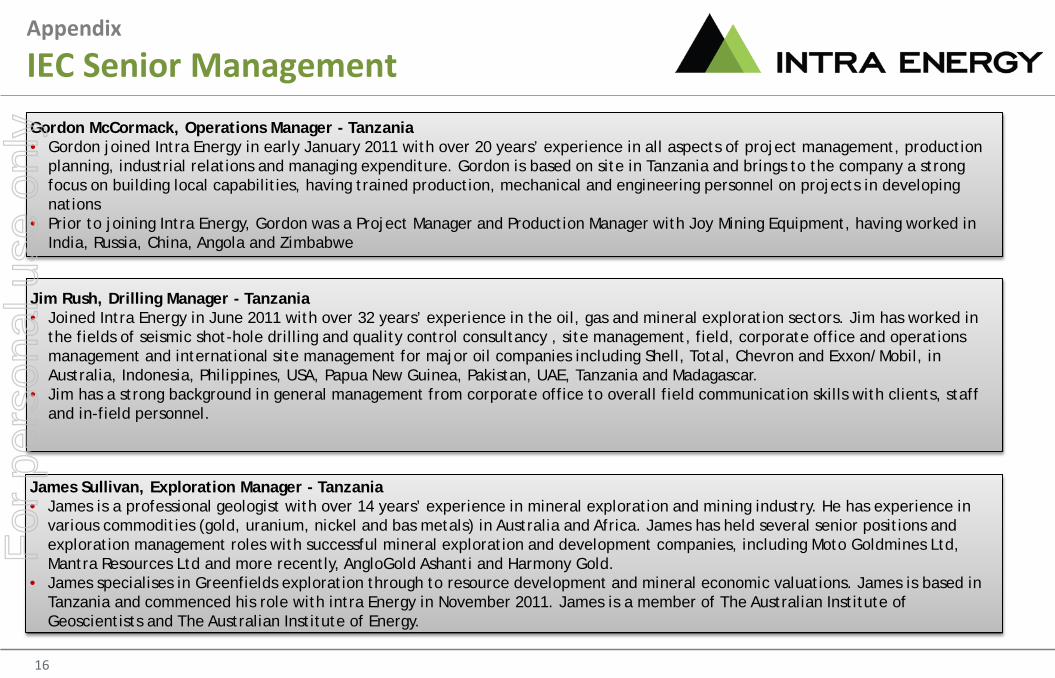

IEC Senior Management

Jim Rush, Drilling Manager - Tanzania • Joined Intra Energy in June 2011 with over 32 years’ experience in the oil, gas and mineral exploration sectors. Jim has worked in

the fields of seismic shot-hole drilling and quality control consultancy , site management, field, corporate office and operations management and international site management for major oil companies including Shell, Total, Chevron and Exxon/Mobil, in Australia, Indonesia, Philippines, USA, Papua New Guinea, Pakistan, UAE, Tanzania and Madagascar.

• Jim has a strong background in general management from corporate office to overall field communication skills with clients, staff and in-field personnel.

James Sullivan, Exploration Manager - Tanzania • James is a professional geologist with over 14 years’ experience in mineral exploration and mining industry. He has experience in

various commodities (gold, uranium, nickel and bas metals) in Australia and Africa. James has held several senior positions and exploration management roles with successful mineral exploration and development companies, including Moto Goldmines Ltd, Mantra Resources Ltd and more recently, AngloGold Ashanti and Harmony Gold.

• James specialises in Greenfields exploration through to resource development and mineral economic valuations. James is based in Tanzania and commenced his role with intra Energy in November 2011. James is a member of The Australian Institute of Geoscientists and The Australian Institute of Energy.

Gordon McCormack, Operations Manager - Tanzania • Gordon joined Intra Energy in early January 2011 with over 20 years’ experience in all aspects of project management, production

planning, industrial relations and managing expenditure. Gordon is based on site in Tanzania and brings to the company a strong focus on building local capabilities, having trained production, mechanical and engineering personnel on projects in developing nations

• Prior to joining Intra Energy, Gordon was a Project Manager and Production Manager with Joy Mining Equipment, having worked in India, Russia, China, Angola and Zimbabwe

For

per

sona

l use

onl

y

17

• Issued Capital (Ordinary Shares– ASX:IEC) 242.7m • Market Cap at $0.30 (as at 4 May 2012) $72.8m • Number of Shareholders 1159

• Top 20 Shareholders hold 57.6% • Top 5 Shareholders hold 46.7%

– Aspac Mining Limited (G Robertson & Associates) 23.4% – Mara Superannuation Pty Ltd (C Hartz & Associates) 8.7% – Lujeta Pty Ltd 6.3% – RBC Dexia Investor Services 5.8% – Peter Tsegas 2.5%

• Unlisted options 13.1m

Shareholder Overview F

or p

erso

nal u

se o

nly

18

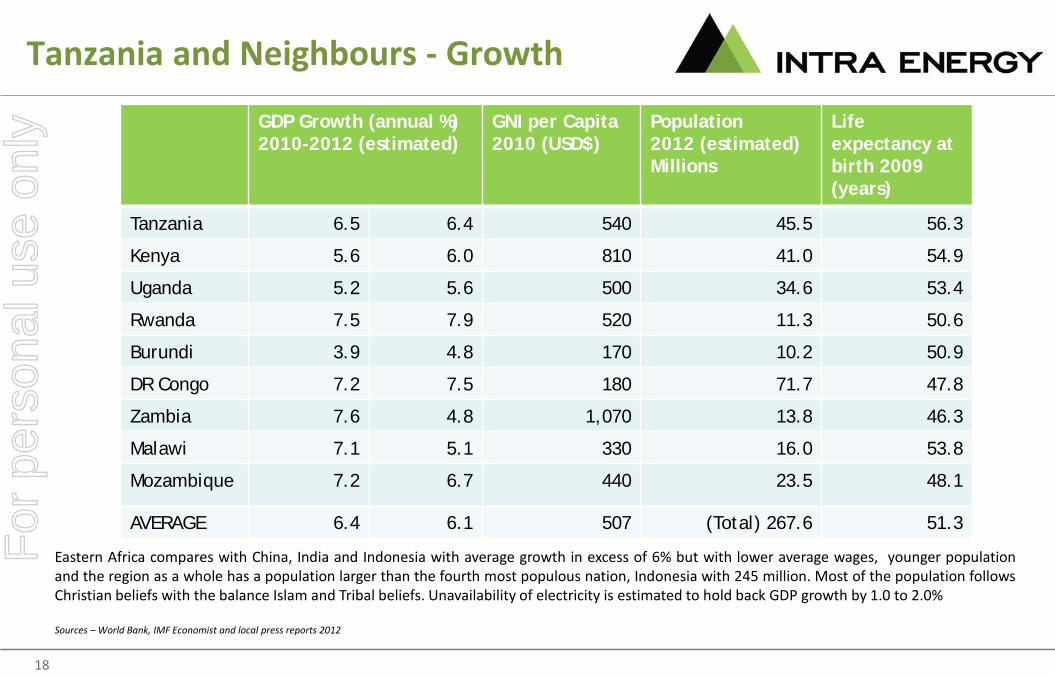

GDP Growth (annual %) 2010-2012 (estimated)

GNI per Capita 2010 (USD$)

Population 2012 (estimated) Millions

Life expectancy at birth 2009 (years)

Tanzania 6.5 6.4 540 45.5 56.3

Kenya 5.6 6.0 810 41.0 54.9

Uganda 5.2 5.6 500 34.6 53.4

Rwanda 7.5 7.9 520 11.3 50.6

Burundi 3.9 4.8 170 10.2 50.9

DR Congo 7.2 7.5 180 71.7 47.8

Zambia 7.6 4.8 1,070 13.8 46.3

Malawi 7.1 5.1 330 16.0 53.8

Mozambique 7.2 6.7 440 23.5 48.1

AVERAGE 6.4 6.1 507 (Total) 267.6 51.3

Tanzania and Neighbours - Growth

Eastern Africa compares with China, India and Indonesia with average growth in excess of 6% but with lower average wages, younger population and the region as a whole has a population larger than the fourth most populous nation, Indonesia with 245 million. Most of the population follows Christian beliefs with the balance Islam and Tribal beliefs. Unavailability of electricity is estimated to hold back GDP growth by 1.0 to 2.0% Sources – World Bank, IMF Economist and local press reports 2012

For

per

sona

l use

onl

y

19

Disclaimer

All statements in this presentation, other than statements of historical facts, that address future production, reserve or resource potential, exploration drilling, exploitation activities and events or developments that Intra Energy Corporation Limited (the “Company”) expects to occur, are forward-looking statements. Although the Company believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements are not guarantees of future performance and actual results or developments may differ materially from those in the forward-looking statements. Factors that could cause actual results to differ materially from those in forward looking statements include market prices, exploitation and exploration successes, and continued availability of capital and financing and general economic, market or business conditions. Investors are cautioned that any such statements are not guarantees of future performance and actual results or developments may differ materially from those projected in the forward-looking statements. The Company does not assume any obligation to update or revise its forward-looking statements, whether as a result of new information, future events or otherwise. To the extent permitted by law, Intra Energy Corporation Limited accepts no responsibility or liability for any losses or damages of any kind arising out of the use of any information contained in this presentation. The information in this presentation relates to Exploration Results, Mineral Resources or Ore Reserves based on the Mbalawala Mine Bankable Feasibility Study with related infrastructure feasibility options as at 31 August 2010, the Mbalawala Coal Mine Bankable Feasibility Study as at 13 August 2010 and the Resource Model Assessment and Review, Ngaka Project Area as at 20 July 2010, and have been reviewed by Mr D. Mason MBA, BSc (Hons). Mr Mason has sufficient experience, as to qualify as a Competent Person as defined in the 2004 edition of the “Australian Code for Reporting of Mineral Resources and Ore reserves”. Mr Mason consents to the inclusion in the report of the matters based on his information in the form and context in which it appears. The Songwe-Kiwira resource statement has been compiled by Phillip Sides, a qualified senior geologist employed by JB Mining Services Pty Ltd (JBMS), with over 25 years’ experience in the exploration and evaluation of coal resources. The author is a Member of the Australian Institute of Geoscientists and as such qualifies as a Competent Person as defined by the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (The JORC Code) 2004 Edition”. This report has been prepared using the guidelines for the estimation of black coal resources and reserves as contained in The JORC Code. Neither the author nor JB Mining Services Pty Ltd has any material interest or entitlement, direct or indirect, in the securities of Intra Energy Corporation Limited. Mr David Mason, Executive Director – Exploration and Business Development of Intra Energy Corporation Limited, originally requested this resource evaluation. All fees for the preparation of this report are charged on a time and materials basis. Initial evaluation, computer modelling of seam structure and coal quality and initial coal tonnage estimates were undertaken by Greg Jones, Senior Consultant/Director of JB Mining Services prior to handing over responsibility of the Resource evaluation to Phillip Sides.

For

per

sona

l use

onl

y