Embed Size (px)

Citation preview

Intervention Plan

Insurance

1

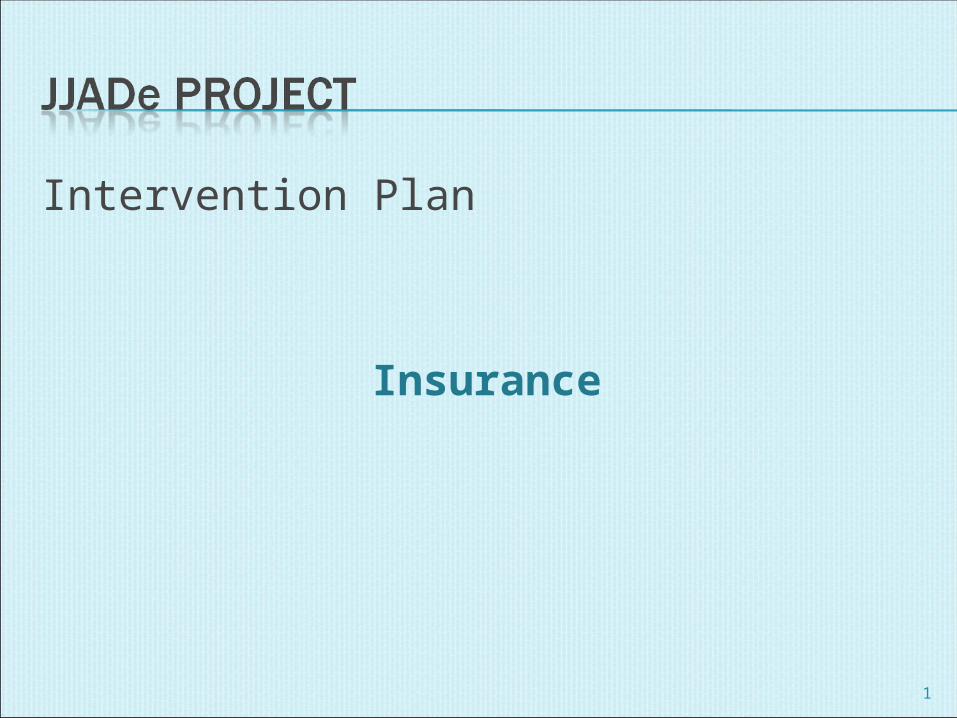

Market Condition: There is a demand for the retention of the skilled force in the jewelry industry.

Design Interventions and Business Models : Insurance for the Artisans. NGOs/Community Youth/Value Chain Members as the Service Agents for the Insurance Company for delivery of

this service.

Market Players with Incentives: Insurance Companies who have not realized the potential in the lower segment

for introducing their Insurance Products.

Constraints: the industry doesn’t have a retained skill force, as the artisans in time of contingencies tend to

shift from skilled to unskilled form of labor

Underlying Causes: There are very few social security schemes which exist for the informal sector, and the

ones that are there, have not been disseminated well. Also, there is no delivery mechanism for these schemes.

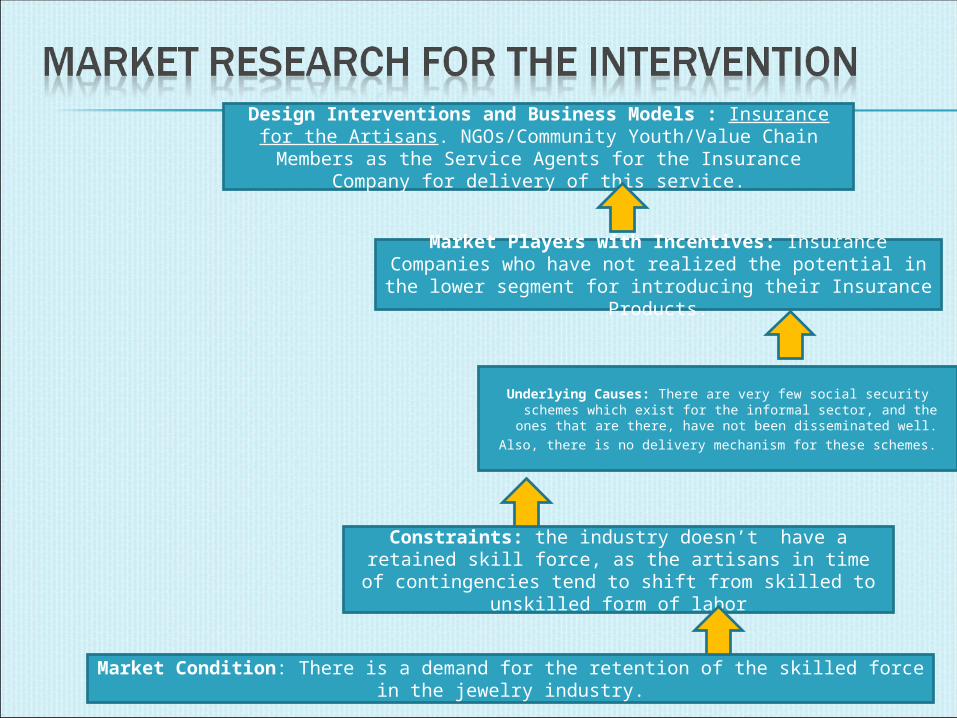

1. Stage of intervention: Pilot 2.a Rationale: Lack of Social Security Systems in the informal sector forces the skilled

artisans to shift to unskilled work in the time of contingencies. By providing Social Security measures like Insurance, it can be ensured that the Industry will have a retained workforce.

2.b. Market Research for the intervention: With the various discussions held at the community level, it was realized that, there are barely any social security measures for the informal sector, and even if there are, they have not been disseminated well.

A secondary research was done on the available social security schemes which are available and are specific to the Jewelry or handicrafts sector. Two of the schemes were identified, which gets subsidized if the artisan is in possession of the Artisan ID card.

Further secondary research was also conducted on various other schemes for the informal sector. The list of these schemes were circulated amongst the Consortium Partners, for perusal at their end.

3. Sustainable solution: Insurance companies perceiving the artisans community as a viable venture for themselves for the small ticket size Insurance product. Also, it has been made mandatory for the Insurance Companies to develop a certain percentage of product range for the people from the lower economic strata.

• Target business – Artisans and Enterprises• Business service solution or solutions – Artisans and Enterprises as a potential

business market for the Insurance companies to introduce their small ticket size insurance product.

• Service model/ provider: NGOs, Community Youth, Value Chain Players (like Brokers) as the service agents, who will get commission from the Insurance Companies and the clientele.

3

NGOs as Service Delivery Agents for the Insurance Companies

Community Youth as the Service Agents

Value Chain Members (e.g. Brokers) as the Service Agents

4

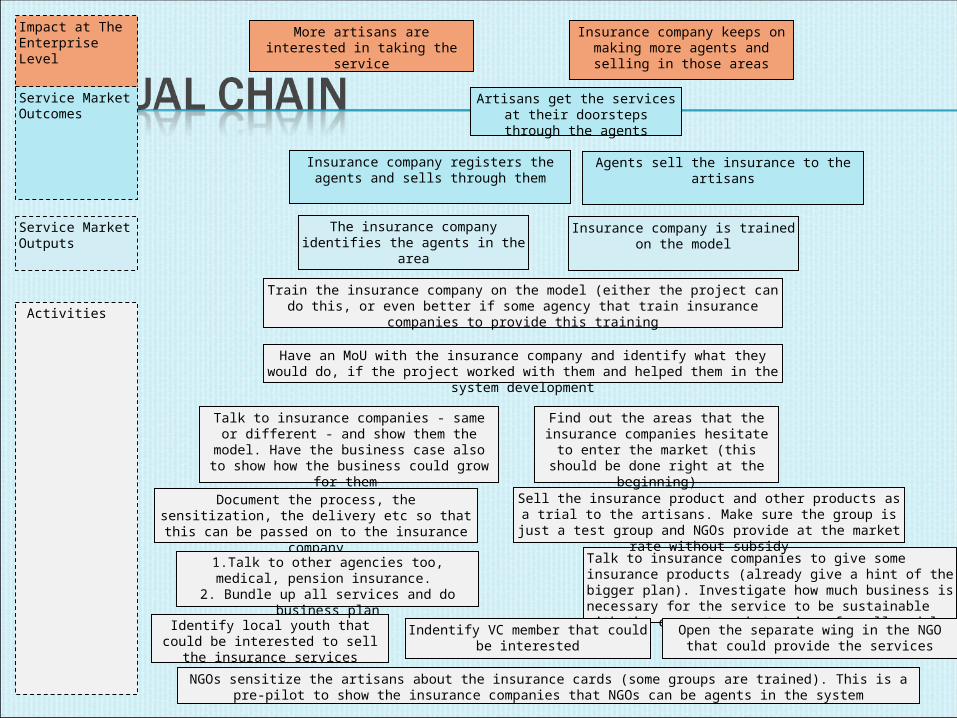

Impact at The Enterprise Level

NGOs sensitize the artisans about the insurance cards (some groups are trained). This is a pre-pilot to show the insurance companies that NGOs can be agents in the system

Have an MoU with the insurance company and identify what they would do, if the project worked with them and helped them in the system development

Insurance company is trained on the model

Activities

Service Market Outcomes

Service Market Outputs

Artisans get the services at their doorsteps through the agents

More artisans are interested in taking the service

Insurance company registers the agents and sells through them

Talk to insurance companies - same or different - and show them the model. Have the business

case also to show how the business could grow for them

Document the process, the sensitization, the delivery etc so that this can be passed on to the insurance

company

Identify local youth that could be interested to sell the insurance

services

1.Talk to other agencies too, medical, pension insurance.

2. Bundle up all services and do business plan

Talk to insurance companies to give some insurance products (already give a hint of the bigger plan). Investigate how much business is necessary for the service to be sustainable with the current market prices for all models

Sell the insurance product and other products as a trial to the artisans. Make sure the group is just a test group and NGOs

provide at the market rate without subsidy

The insurance company identifies the agents in the area

Find out the areas that the insurance companies hesitate to enter the market

(this should be done right at the beginning)

Train the insurance company on the model (either the project can do this, or even better if some agency that train insurance companies to provide this training

Indentify VC member that could be interested

Open the separate wing in the NGO that could provide the services

Insurance company keeps on making more agents and selling in

those areas

Agents sell the insurance to the artisans

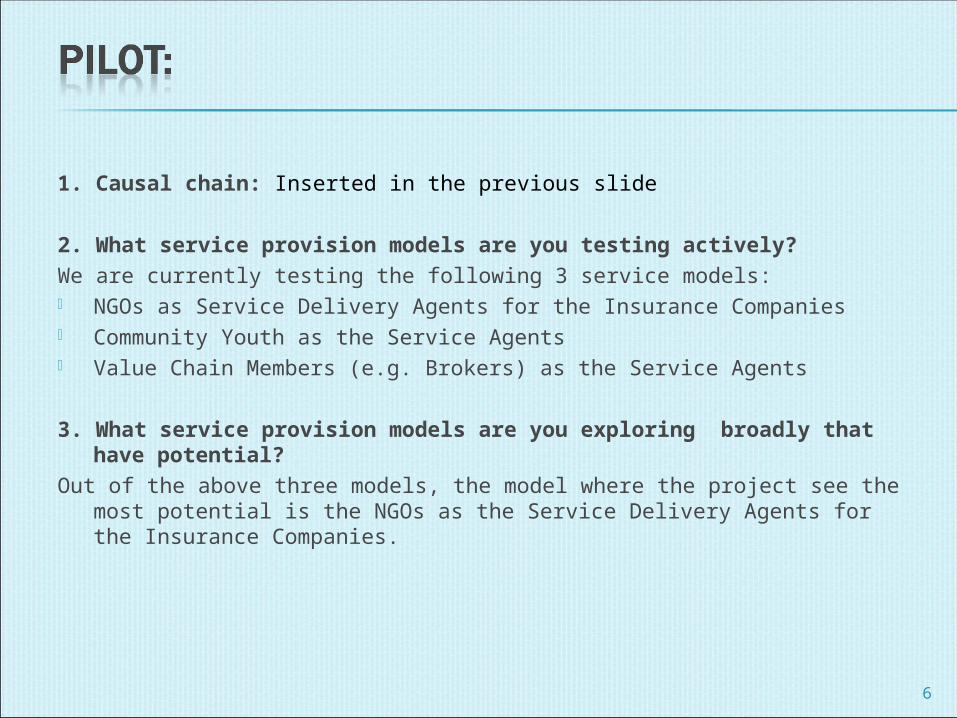

1. Causal chain: Inserted in the previous slide

2. What service provision models are you testing actively?We are currently testing the following 3 service models: NGOs as Service Delivery Agents for the Insurance Companies Community Youth as the Service Agents Value Chain Members (e.g. Brokers) as the Service Agents

3. What service provision models are you exploring broadly that have potential?

Out of the above three models, the model where the project see the most potential is the NGOs as the Service Delivery Agents for the Insurance Companies.

6

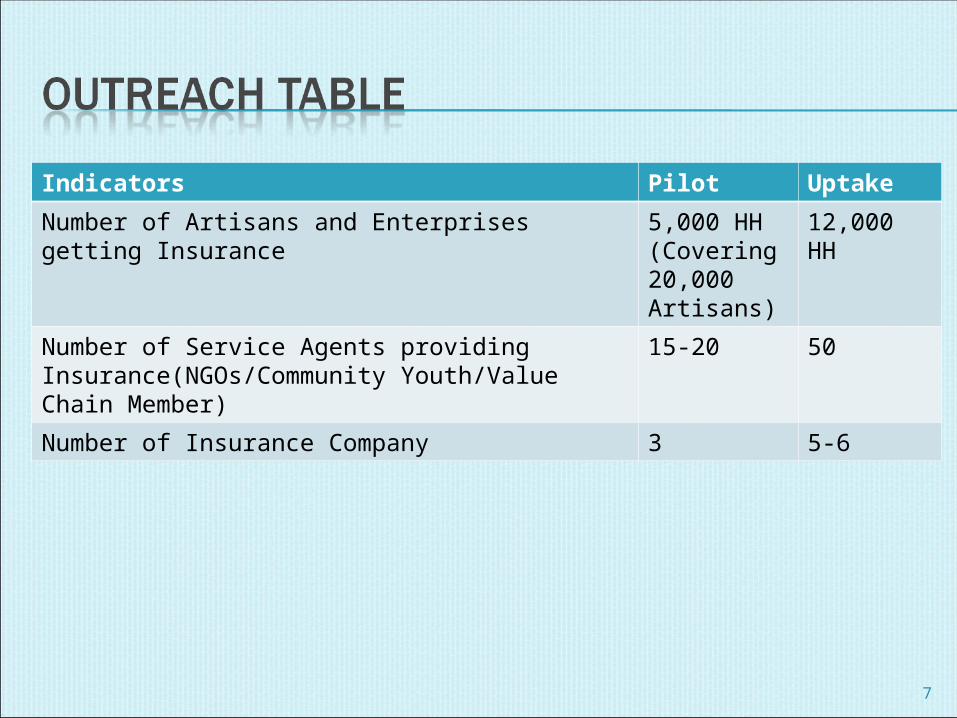

Indicators Pilot Uptake

Number of Artisans and Enterprises getting Insurance

5,000 HH (Covering 20,000 Artisans)

12,000 HH

Number of Service Agents providing Insurance(NGOs/Community Youth/Value Chain Member)

15-20 50

Number of Insurance Company 3 5-6

7

4. 4.a. Service delivery model : NGOs as the Service Delivery Agents for the Insurance Company

Biz model for each service delivery model (who pays in the short and long term)Initially, the cost of operations is borne by the project for the artisans. At this stage the artisans are only paying the subsidized premium for the insurance.In the long term, the clientele (artisans), will be paying to the service agents for the services being delivered to them. NGOs would be getting paid commission from the Insurance Company for catering to the clientele and increasing the area of operations.

How will the service be developed by ACCESS?ACCESS has done market analysis both in terms of need and demand for this particular service. ACCESS has also identified the Service Providers to fill in the gap for the demand and supply. ACCESS is also initiating dialogues with various Insurance Companies, and illustrate them the potential even in the low ticket size Insurance product, since at a certain level, its even mandatory for the Insurance Companies to cater to some number from social sector as well.

How will providers be strengthened by ACCESS?ACCESS would be providing assistance in identification of Service Providers to the Insurance Companies. ACCESS would also facilitate linkages between NGOs and Insurance Companies, for developing the appropriate product for the target community.

How will demand be stimulated by ACCESS?ACCESS would be identifying various Insurance companies and demonstrate them the potential market in the community. At the level of community, the demand would be stimulated through the service agents(NGOs), facilitated by ACCESS.

8

What kind of subsidies be offered at this phase by ACCESS?The cost of market analysis and need assessment would be borne by ACCESS. Moreover, the HR cost of NGOs for entering the artisans inhabited areas, their sensitization and capacity building etc. would be subsidized by ACCESS. Also the delivery of service is being borne by the project at this stage of the project.

What level of outreach you will target?Population covered for which the Insurance coverage would be provided would be 20,000 in the pilot stage.

How will you know whether to go forward with strategy or to end it?If the number of Insurance companies start introducing their new Insurance products or the existing company introduce more products or the Insurance companies increase the number of agents, would indicate that the strategy should be taken forward.

RA plan for this: What indicator will decide the above IRAP uploaded

http://value.worktodos.com/index.cfm?page=files&fId=78775

9

Impact at The Enterprise Level

Identify training providers or others that the insurance companies seek help in marketing or follow the rules (Government etc)

More agents are being formed

Activities

Service Market Outcomes

Service Market Outputs

Efficiency increase of the artisans

Develop the training module with such companies (by showing them work on the ground)

Promote the product of such training companies

Training providers/consultants know how to deliver products to insurance companies

Insurance companies are taking the training from such consultants for their staff

Agents income increase, more agents, insurane companies income increase

Consultants are promoting the products to more insurance companies

More artisans get the insurance product

Impact at Poverty Level

Improved Working Conditions and Increase in Income

Market uptake causal chain – inserted in the previous slide

Who will continuously stimulate demand and how?The demand would be stimulated by the Service Agents at the level of the community, and the at the level of Service Providers, the demand would be stimulated by the Consultants. These consultants for their own sustenance would continuously try to identify new Insurance Companies for delivering their services as well.

What is target outreach? The target would be the artisans and enterprises from the whole

Jewelers community, in need of small ticket size Insurance product.

What elements of the program are still in hand of the project at this point?at this point, the project is still initiating and negotiating with the Insurance Companies to demonstrating them the potential in introducing their Insurance Products. 11

What indicators tell you that the program is going well? Increase in number of Insurance companies with low ticket

size insurance product Increase in number of Service Agents(NGOs/Community

Youth/Value chain players) providing Insurance Increase in number of Insurance Products by the Insurance

Companies

What is the frequency of review of these decisions or this initial piece?Informally these decisions are reviewed on weekly basis, and formally on a monthly basis when the pace and the direction of the intervention is mapped.

12

Who does what in the team?Project Director – Developing the Result Assessment Plans for the Intervention is

largely developed by the Project Director. The dialogues with Insurance Companies are also initiated by the Project Director. Any strategy level changes are largely guided by the Project Director.

Program Coordinators- the Program Coordinators assist the Project Director in doing Market Research and Gap Analysis for the need and the demand for the Intervention. Operations on the daily basis are handled at the level of the Program Coordinators.

Program Coordinators also work in collaboration with each other under the supervision of the Program Director on the IRAPs.

Program Coordinators also maintain the liaising with the Consortium on a daily basis.

Entry stage activities: Market research on the need of Insurance and the Gap analysis in term of the incentivized Service Providers for the Insurance, was the entry point.

Exit stage activity:Once the insurance Companies start seeing the community as a potential market for themselves, and there is a continuous felt need of Insurance from the community as well, would be the exit point.

How do you coordinate this with other activities?The activities under this particular intervention is done in coordination with other interventions, since many of the activities are intertwined or prerequisite for the other. E.g Artisan ID Card is a pre requisite for Insurance.

13