Embed Size (px)

Citation preview

P a g e | 1

INTERNSHIP REPORTOn

Six Week TrainingAt

SILK Bank Ltd.Karachi, Pakistan.

Submitted By:

Syed Ali AmeerInternee

B.Com, PIPFA Finalist, CA Intermediate

Submitted To:Saleem Ahmed Siddiqui

Branch ManagerSILK Bank Hyderi Branch (0022)

Submitted On:5th May, 2014

P a g e | 2

PREFACE

Internship is the integral and basic requirement of all the business study programs. Because it is the practical implication of the theoretical knowledge which we have taught in our business Subjects to gain further knowledge and experience about professional business activities. It Equips us with the necessary knowledge, skills and values of business culture which are basic Requirement of the business professional and which also helps new graduates to perform Professionally as they get first step in their practical professional life.

For this reason I was placed at Silk Bank Limited Hyderi Branch (0022) KarachiWhere I have done my six weeks internship. During my internship tenure I have gained a lot of Knowledge about Banking Operations under the supervision and guidance of my Internship Supervisors.

During my whole duration I was rotated in all the different Areas of the branch and was thoroughly briefed about the procedures of all the banking operations by the concerned staff. My internship report contains all the knowledge which I have learnt there.

P a g e | 3

ACKNOWLEDGEMENT

All praises are for Allah Almighty that has bestowed upon human being the crown of creation and has endowed him with knowledge and wisdom. After Allah, the last Prophet Mohammad (PBUH) Who brought for us revelation and unlimited knowledge and civilized the barbarian human being. I am very thank full to Allah Almighty who gave me the courage to complete this complex task and to my ever caring and loving parents whose prayers helped me to reach this stage of my life.

Besides, there are many people who supported me in formulation of this report and without the support of them I could never be able to complete this report successfully. In this respect I am very thank full to Mr. Saleem Ahmed Siddiqui (Branch Manager), Mr. Irfan Shaikh (Branch Operations Manager) and the qualified staff members ofHyderi Branch, who cooperated with me with their guidance at each step of my internship. They have provided me a lot of important information and knowledge about the banking operations in a very short period of time.

Last but not least, my very special thanks to Relationship ManagersMr. Mohsin Rafat (SRM) and Mr. Muhammad M. Azhar (RM) who provided me with his guidance and profitable knowledge as a Teacher whenever I need that. I am also paying Gratitude to Sales Executives (SE) whom gives me opportunity to Learn and enables me to work diligently as a Team Member.

P a g e | 4

Dedicated to:

My Ever Caring & LovingParents

And

Respectable Teachers

P a g e | 5

TABLE OF CONTENTS

PAGES

Executive Summary 06

Introduction of Organization 07

Banking History 07

Introduction of Silk Bank Limited 08

Vision, Mission & Core Values of Organization 09

Segments and Hierarchy of Branch (Organogram) 10

Key Functions of Designated Officers 11

Upward Hierarchy of Branch Banking 14

3rd Segment of Branch Banking 15

Scope of Banking 16

Wholesale Banking and its Classification 17

Statement of Compliance 21

Products of Silk Bank Limited 22

Required Documents for Accounts Opening 23

Accounts Dormancy Removal 24

Know your Customer (KYC) 25

Customer Risk Profiling (CRP) 26

Electronic Credit Information Bureau (ECIB) 29

High Value Transaction Record (HVTR) 29

Introduction to Banking Softwares 30

SWOT Analysis 31

Suggestions and Recommendations 32

Conclusion 33

P a g e | 6

EXECUTIVE SUMMARY

Silk Bank Limited is a private bank providing financial services to the customers under the leadership of Former Finance Minister Mr. Shaukat Tarin. Bank is engaged in Wholesale and Retail Banking. Currently bank continues to strengthen its presence in market by the help of expansion plan. By the end of 2013 Bank has 85 branches which include 10 Islamic Banking branches.

The Silk Bank Limited is growing very impressively and making profits which growing higher day by day with the slogan of “Yes We Can” making the wishes of people come true through the philosophy of transferring concepts to reality.

Bank’s product portfolio includes such type of innovative products according to the needs and preferences of the customers which are providing benefits to customers as well as adding profits to the bank. These products include Auto Finance, Business Value Account, Money Market Express, Munafa Rozana / Super Saver, Online Express, Ready Line, Salary Premium Account, Visa Debit Cards, Credit Cards, Online Banking and Islamic Banking Products.

Bank’s growth graph is showing upward, positive and continuous trends and its profit percentage is increasing every year. Last but not the least, this report almost includes each and every aspect about Silk Bank Limited which is very helpful for every reader.

P a g e | 7

INTRODUCTION

History of Banking:

The word “Bank” is derived from the Italian word “Bancus or Banque” which means bench, desk or counter. Because in ancient times, the benches were used by the Jews for the purpose of exchanging money. In ancient times the religious temples were used as the safest place for keeping money and gold by people of that time under the supervision of the priests. Goldsmiths then acted as the financial agents in exchange of gold and valuables which provided the basis of Modern banking. Today’s modern banking system is the ultimate and step by step achievement of the ancient banking system of accepting deposits from those who have surplus and lending to those who do not have it or have little.

Banking In Pakistan:

Prior to Independence British banks controlled the banking operation in Pakistan. After independence there were no resources so that Pakistanis could start their own banking system in a very short period of time. Then at that time it was decided that “Reserve Bank of India” will control the banking operations in Pakistan. But this was not good for the best interest of Pakistan because British Government at that time distributed the reserves of the “Reserve Bank of India” between India and Pakistan with the share of 70% India and 30% Pakistan. It was a very big loss for Pakistan at that time as being a new nation with new country having few resources for survival. Then “Quaid-e-Azam Muhammad Ali Jinnah” (The Governor General of Pakistan) at that time took a step ahead and inaugurated “The State Bank of Pakistan” on July 1st , 1948 which then took control of all the banking operations of Pakistan.

P a g e | 8

Introduction of SILK Bank Limited:

On September 15, 2001, under the supervision of the State Bank of Pakistan (SBP), the institution then known as the Prudential Bank was acquired by the management and associates of the Saudi Pak Industrial and Agricultural Investment Company (Pvt) Ltd (SAPICO).

On March 31, 2008, a Consortium comprising of IFC, Bank Muscat, Nomura International and Sinthos Capital led by senior bankers Mr. Shaukat Tarin and Mr. Sadeq Sayeed acquired 86.55% stake in Silk Bank for around $213 million or $0.47 per share (PKR 29.3 equivalent per share). Under the new leadership, the Bank will continue to focus on SME & Consumer financing resulting in efforts of increased profitability.

Consortium Partners:

On March 31, 2008, a Consortium comprising of IFC, Bank Muscat, Nomura International and Sinthos Capital led by senior banker Mr. Shaukat Tarin acquired the Bank. The Consortium Partners are following:

A member of the World Bank Group fosters sustainable economic growth in developing countries.

Largest bank of Oman with assets of over USD 15 billion, having significant presence in the Middle East.

It is a Japanese Investment Bank with network in over 30 countries and Total Assets ofUSD 221Billion. It recently acquired Lehman Brothers in Asia and Europe.

P a g e | 9

ETHICAL CODE OF PRACTICE

Vision

Benchmark of Excellence in Premier Banking.

Mission

To be the leader in premier banking trusted by customers for accessibility, service & innovation; be an employer of choice creating value for all stakeholder.

Values

Silkbank prides itself in being a conscientious and responsible corporate citizen with a commitment to the development of Pakistan. At Silkbank employees are encouraged to give back to society and we have made concerted efforts towards the development of healthcare, education and constructive, character building sports activities in the underdeveloped segments of our country.

Core values

Customer Focus Integrity

Teamwork

Creativity

Meritocracy

P a g e | 10

Humility

Segments of Branch Banking

There are Only Two Segments of Hyderi Branch where I was on Training; following:

OPERATION & SALES OF DEPOSITS

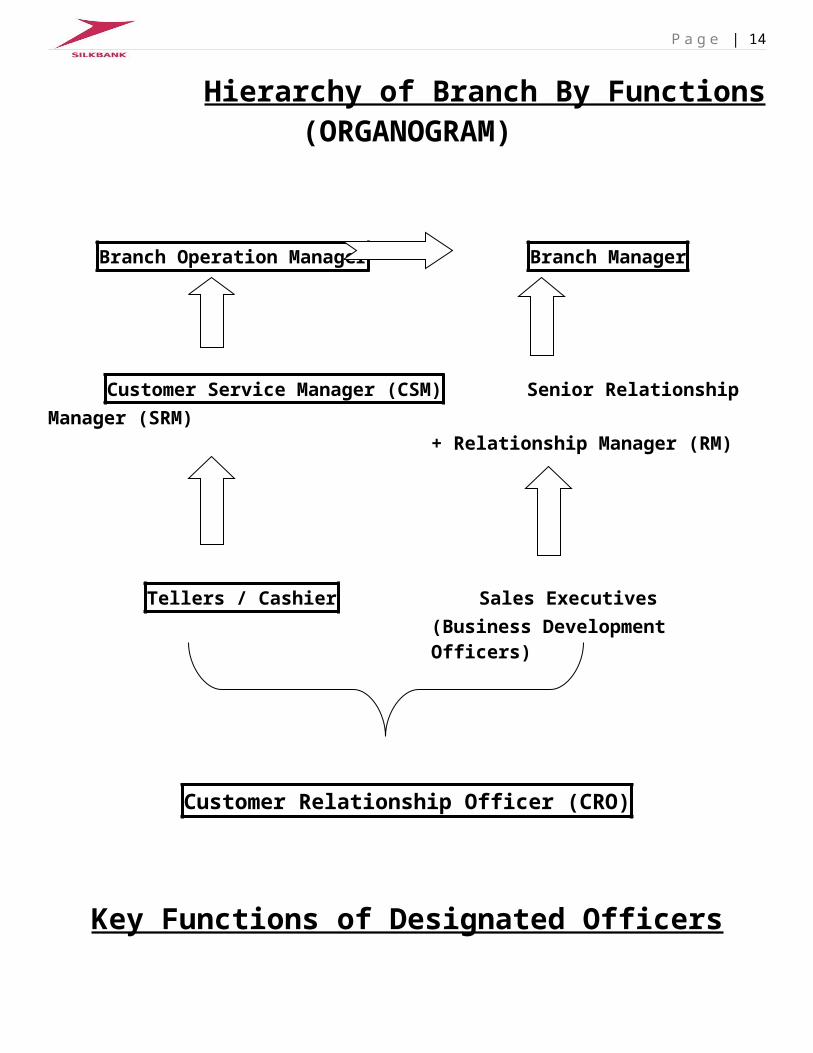

Hierarchy of Branch By Functions(ORGANOGRAM)

Branch Operation Manager Branch Manager

Customer Service Manager (CSM) Senior Relationship Manager (SRM)+ Relationship Manager (RM)

Tellers / Cashier Sales Executives (Business Development Officers)

P a g e | 11

Customer Relationship Officer (CRO)

Key Functions of Designated Officers

Branch Manager:

Maintain and rapidly increase Branch Portfolio. Entertain Corporate Clients and Highly Valuable Customers. Manage Human Capital of Branch. Report to Senior Coordinates such as Group Head, RGM, and AM etc. Supervise Branch Daily Operation. To administratively report to Head office and their respective departments such as TDR

Dept, ASD Dept, Insurance Division, Compliance Dept etc. Coordinate with Internal & External Auditors. Responsible for Guidance and Staff Motivation. Supervise Daily Accounts Opening Forms (AOF) and related matters. Daily Monitoring Branch Sales and in relation to Employees Performance. Perform other Key functions of Branch Banking in capacity of Branch Manager.

Branch Operation Manager:

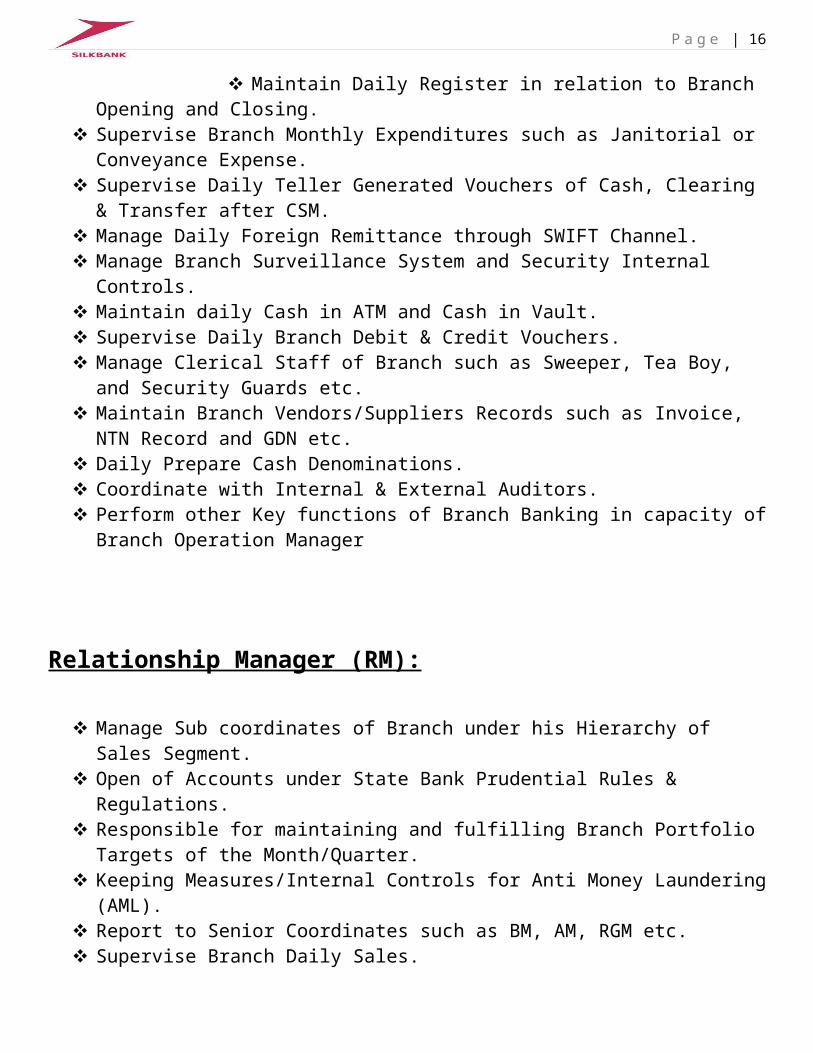

Responsible to deliver Efficient and Effective Service to the Highly Valuable Customers. Manage Sub coordinates of Branch under his Hierarchy of Operation Segment. Report to Senior Coordinates such as BM, Head Operations etc. Supervise Branch Daily Operation and Monitor Internal Control Assessment. Ensure the Minimization of Operational Risk at Branch. Control Supply of Money as per Branch Needs and Legal Regulations. Assists in Operating Lockers of Customers in Coordination with CSM. Maintain Daily Register in relation to Branch Opening and Closing. Supervise Branch Monthly Expenditures such as Janitorial or Conveyance Expense. Supervise Daily Teller Generated Vouchers of Cash, Clearing & Transfer after CSM. Manage Daily Foreign Remittance through SWIFT Channel. Manage Branch Surveillance System and Security Internal Controls. Maintain daily Cash in ATM and Cash in Vault. Supervise Daily Branch Debit & Credit Vouchers. Manage Clerical Staff of Branch such as Sweeper, Tea Boy, and Security Guards etc. Maintain Branch Vendors/Suppliers Records such as Invoice, NTN Record and GDN etc.

P a g e | 12

Daily Prepare Cash Denominations. Coordinate with Internal & External Auditors. Perform other Key functions of Branch Banking in capacity of Branch Operation

Manager

Relationship Manager (RM):

Manage Sub coordinates of Branch under his Hierarchy of Sales Segment. Open of Accounts under State Bank Prudential Rules & Regulations. Responsible for maintaining and fulfilling Branch Portfolio Targets of the

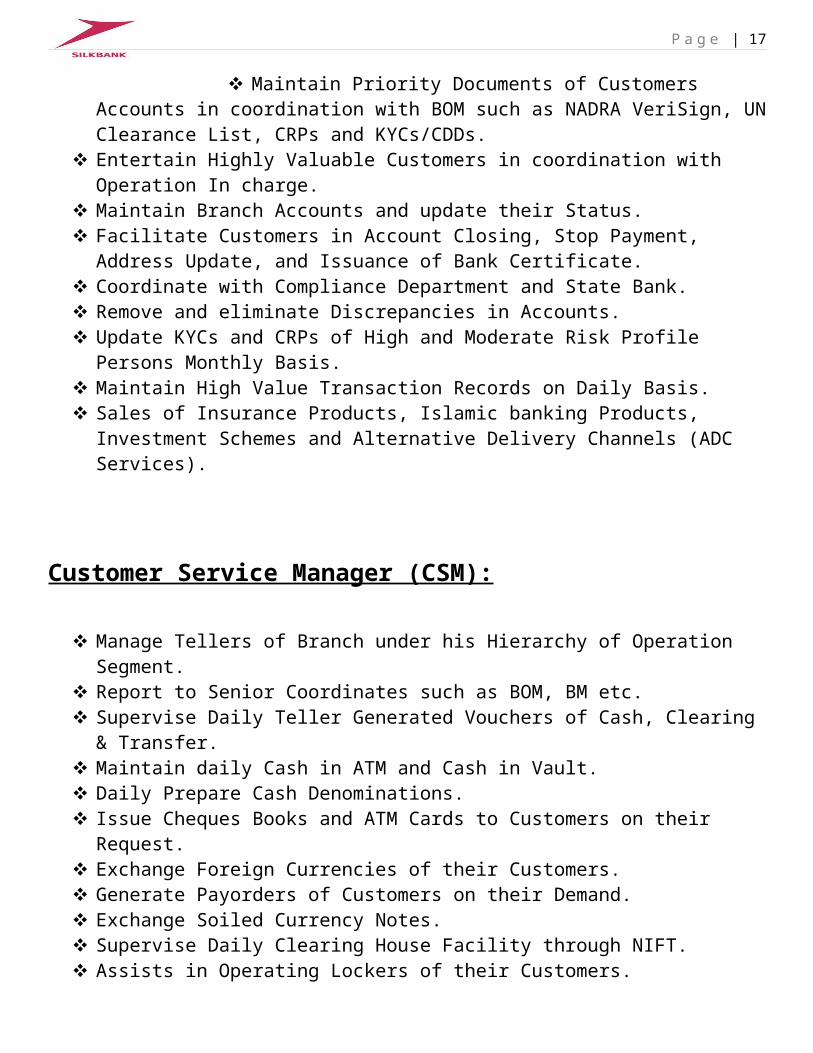

Month/Quarter. Keeping Measures/Internal Controls for Anti Money Laundering (AML). Report to Senior Coordinates such as BM, AM, RGM etc. Supervise Branch Daily Sales. Maintain Priority Documents of Customers Accounts in coordination with BOM such as

NADRA VeriSign, UN Clearance List, CRPs and KYCs/CDDs. Entertain Highly Valuable Customers in coordination with Operation In charge. Maintain Branch Accounts and update their Status. Facilitate Customers in Account Closing, Stop Payment, Address Update, and Issuance of

Bank Certificate. Coordinate with Compliance Department and State Bank. Remove and eliminate Discrepancies in Accounts. Update KYCs and CRPs of High and Moderate Risk Profile Persons Monthly Basis. Maintain High Value Transaction Records on Daily Basis. Sales of Insurance Products, Islamic banking Products, Investment Schemes and

Alternative Delivery Channels (ADC Services).

Customer Service Manager (CSM):

Manage Tellers of Branch under his Hierarchy of Operation Segment. Report to Senior Coordinates such as BOM, BM etc. Supervise Daily Teller Generated Vouchers of Cash, Clearing & Transfer. Maintain daily Cash in ATM and Cash in Vault. Daily Prepare Cash Denominations. Issue Cheques Books and ATM Cards to Customers on their Request. Exchange Foreign Currencies of their Customers. Generate Payorders of Customers on their Demand.

P a g e | 13

Exchange Soiled Currency Notes. Supervise Daily Clearing House Facility through NIFT. Assists in Operating Lockers of their Customers.

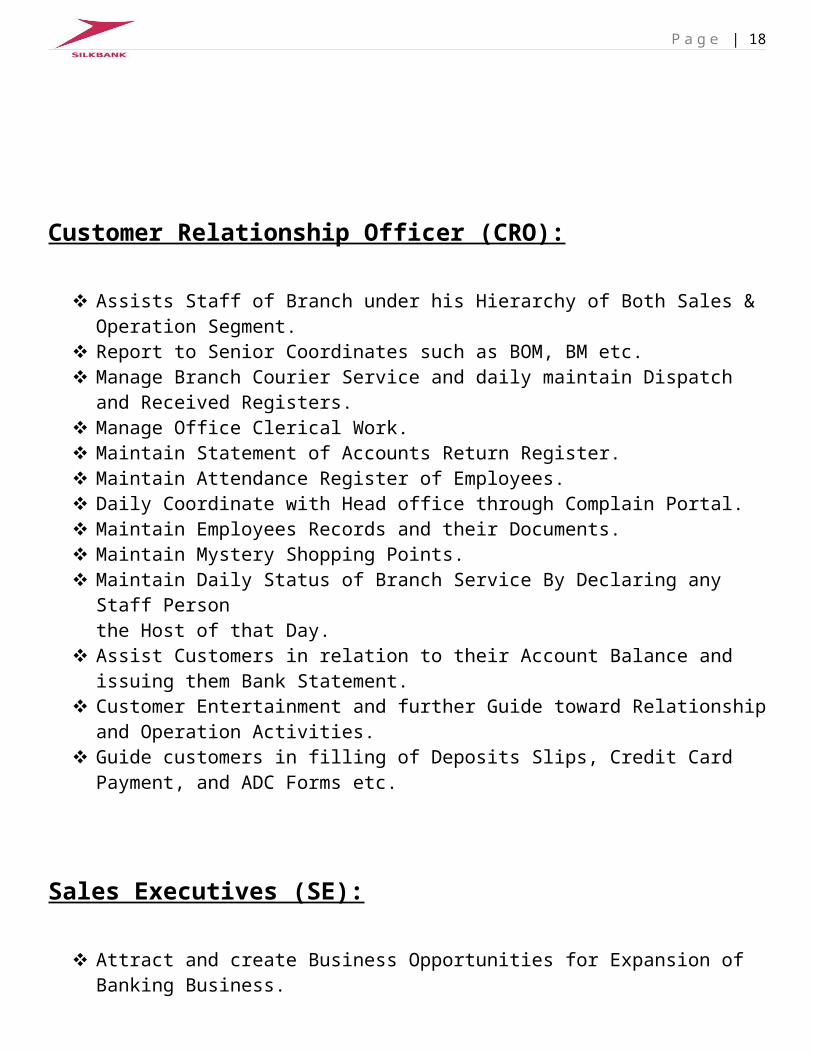

Customer Relationship Officer (CRO):

Assists Staff of Branch under his Hierarchy of Both Sales & Operation Segment. Report to Senior Coordinates such as BOM, BM etc. Manage Branch Courier Service and daily maintain Dispatch and Received Registers. Manage Office Clerical Work. Maintain Statement of Accounts Return Register. Maintain Attendance Register of Employees. Daily Coordinate with Head office through Complain Portal. Maintain Employees Records and their Documents. Maintain Mystery Shopping Points. Maintain Daily Status of Branch Service By Declaring any Staff Person

the Host of that Day. Assist Customers in relation to their Account Balance and issuing them Bank Statement. Customer Entertainment and further Guide toward Relationship and Operation Activities. Guide customers in filling of Deposits Slips, Credit Card Payment, and ADC Forms etc.

Sales Executives (SE):

Attract and create Business Opportunities for Expansion of Banking Business. Sales of Bank’s Products by Establishing Contacts and developing Relationships with

Valuable Customers. Bank Products such as Accounts, Insurance Products, Islamic Banking Products,

Investment Schemes and Alternative Delivery Channels (ADC Services). Filling and Complete AOF in accordance under State Bank Prudential Rules &

Regulations. Report to Senior Coordinates such as BM, SRM, and RM etc. Follow up Customers for fulfill the Required Documents and get Adequate Information

required in KYC. Assists in RM to Facilitate Customers in Account Closing, Dormancy Removal, Stop

Payment, Address/Contact Update and Issuance of Bank Certificate.

P a g e | 14

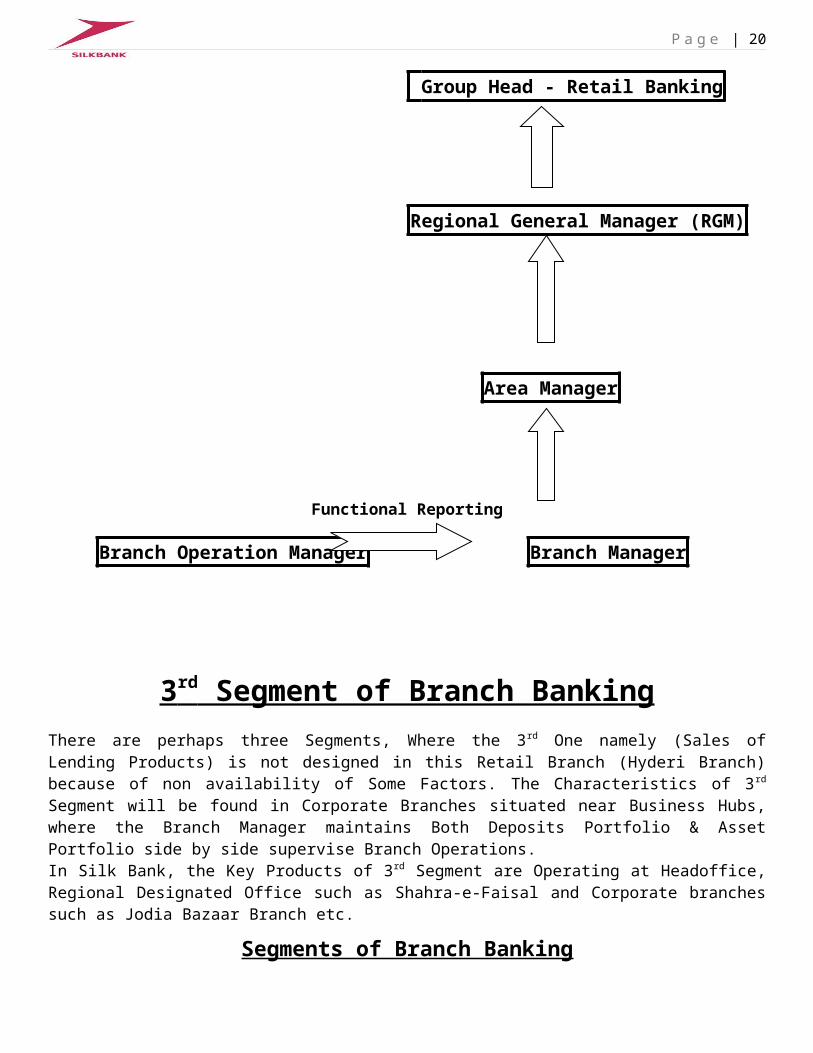

UPWARD HIERARCHY OF BRANCH BANKING

There are Two Types of Reporting; following:

Functional Reporting Administrative Reporting (Upward Reporting)

Managing Director/President (CEO)

Group Head - Operations

Group Head - Retail Banking

Regional General Manager (RGM)

Area Manager

P a g e | 15

Functional Reporting

Branch Operation Manager Branch Manager

3 rd Segment of Branch Banking There are perhaps three Segments, Where the 3rd One namely (Sales of Lending Products) is not designed in this Retail Branch (Hyderi Branch) because of non availability of Some Factors. The Characteristics of 3 rd Segment will be found in Corporate Branches situated near Business Hubs, where the Branch Manager maintains Both Deposits Portfolio & Asset Portfolio side by side supervise Branch Operations.In Silk Bank, the Key Products of 3rd Segment are Operating at Headoffice, Regional Designated Office such as Shahra-e-Faisal and Corporate branches such as Jodia Bazaar Branch etc.

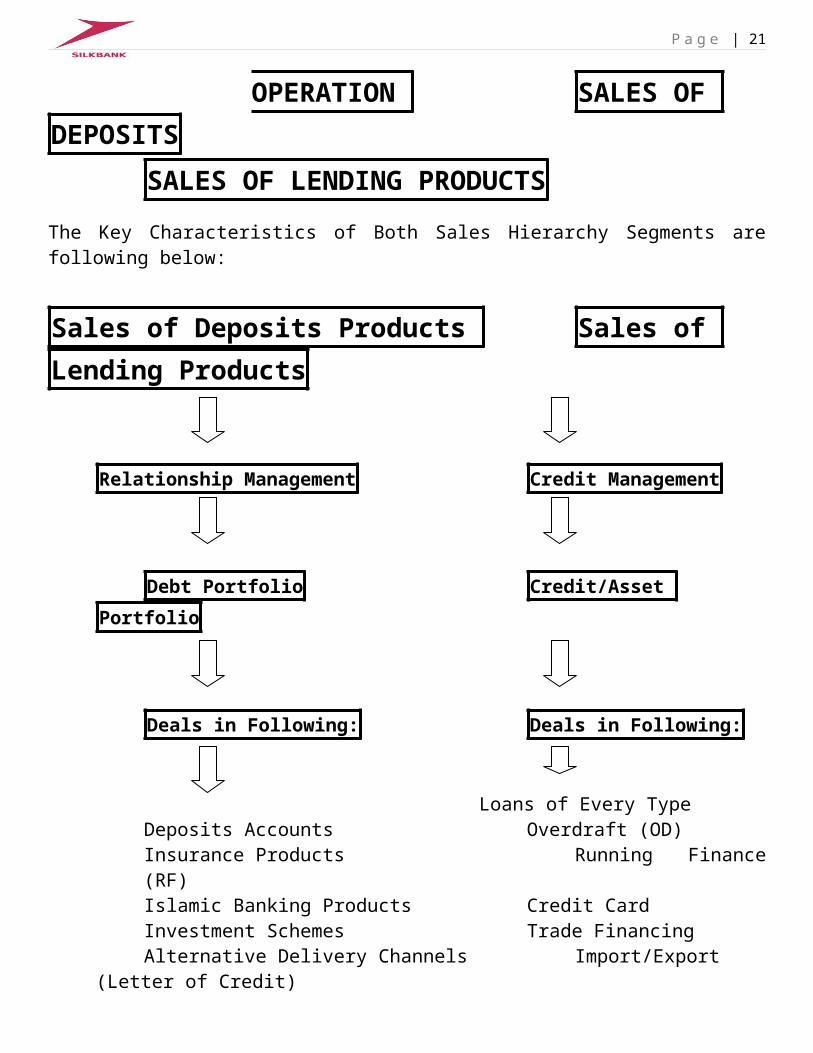

Segments of Branch Banking

OPERATION SALES OF DEPOSITS

SALES OF LENDING PRODUCTS

The Key Characteristics of Both Sales Hierarchy Segments are following below:

Sales of Deposits Products Sales of Lending Products

Relationship Management Credit Management

Debt Portfolio Credit/Asset Portfolio

Deals in Following: Deals in Following:

Loans of Every TypeDeposits Accounts Overdraft (OD)Insurance Products Running Finance (RF)

P a g e | 16

Islamic Banking Products Credit CardInvestment Schemes Trade FinancingAlternative Delivery Channels Import/Export (Letter of Credit)

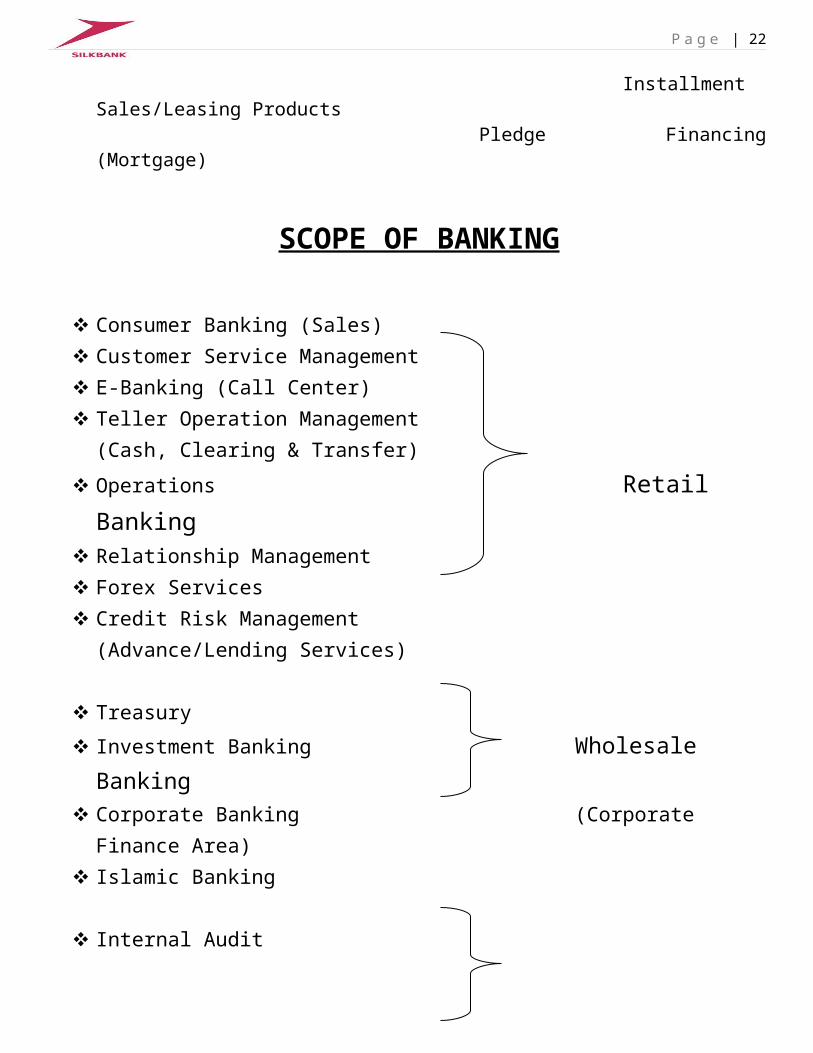

Installment Sales/Leasing ProductsPledge Financing (Mortgage)

SCOPE OF BANKING

Consumer Banking (Sales) Customer Service Management E-Banking (Call Center) Teller Operation Management

(Cash, Clearing & Transfer)

Operations Retail Banking Relationship Management Forex Services Credit Risk Management

(Advance/Lending Services)

Treasury

Investment Banking Wholesale Banking Corporate Banking (Corporate Finance Area) Islamic Banking

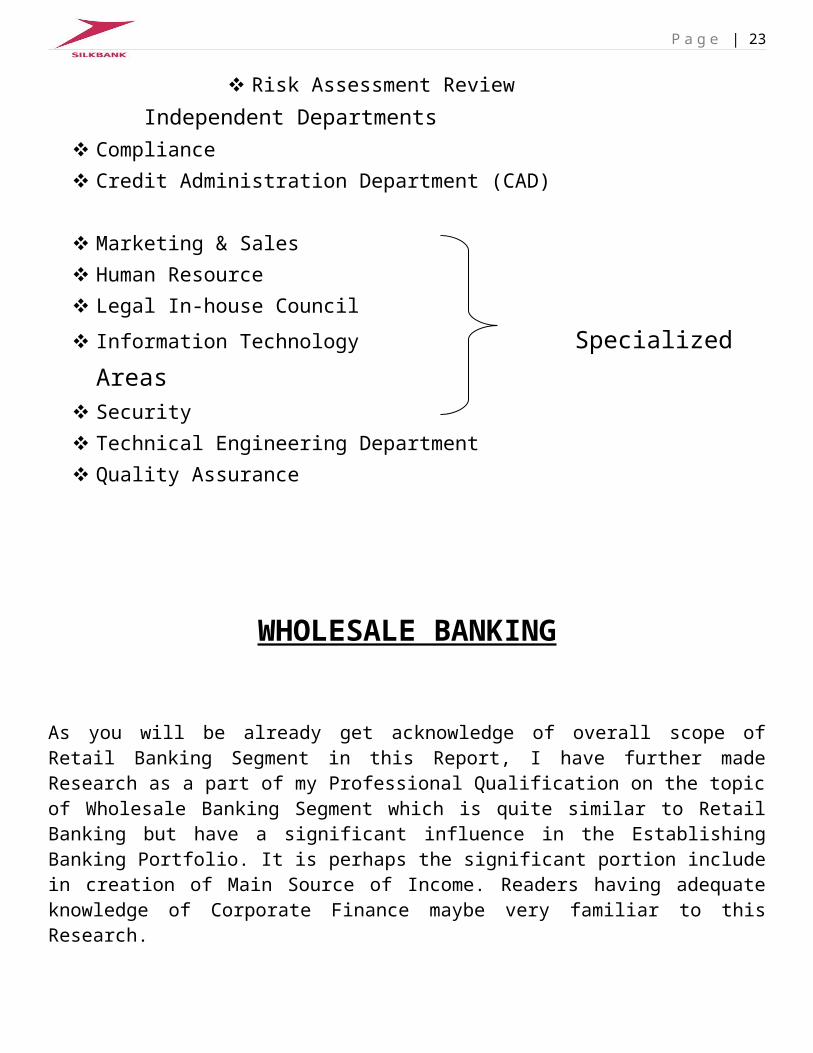

Internal Audit Risk Assessment Review Independent Departments Compliance Credit Administration Department (CAD)

Marketing & Sales Human Resource Legal In-house Council

Information Technology Specialized Areas Security

P a g e | 17

Technical Engineering Department Quality Assurance

WHOLESALE BANKING

As you will be already get acknowledge of overall scope of Retail Banking Segment in this Report, I have further made Research as a part of my Professional Qualification on the topic of Wholesale Banking Segment which is quite similar to Retail Banking but have a significant influence in the Establishing Banking Portfolio. It is perhaps the significant portion include in creation of Main Source of Income. Readers having adequate knowledge of Corporate Finance maybe very familiar to this Research.

DEFINATION:

Wholesale banking also Known as Merchant Banking is the provision of servicesBy banks to organizations such as Mortgage Brokers, large corporate clients, mid-sized companies, real estate developers and investors, international trade finance businesses, institutional customers (such as pension funds and government entities/agencies),and services offered to other banks or other financial institutions.

Wholesale finance means financial services, which are conducted between financial services companies and institutions such as banks, insurers, fund managers, and stockbrokers.

In short, this type of banking will provide services to other banks or large corporations.Some retail banking covers business transactions but not in the same scale as wholesale banking. Think of it like the discount superstore that deals in such large amounts that they can offer special prices or reduced fees, on a per dollar basis.

Following are the Branches of Wholesale Banking Segment:

Corporate Banking Investment Banking

P a g e | 18

Treasury

Corporate Banking:

Corporate Banking is defined as those Products and Services that relateto the Lending Activities between a Bank and its clients.It is different to Retail Banking activities for Individual Accounts, where a Bank deals with Corporate Clients such as Corporations, Listed Companies etc.A Bank maintains specific Divisions or Department for corporate bankingwhich is responsible for handling the needs of corporate clients.

The Main function of Corporate Banking is lying in Category ofWorking Capital Management, Where it provides a highly sophisticatedstructured finance to its corporate clients which may be secured or unsecured.All those facilities related to managing Working Capital(Current Assets – Current Liabilities) such as managing Receivables, Invoice Discounting, Factoring, Cash Management, Trade Finance, overdraft etc.

Products & Services:

Cash Management Cash Mobile Facility Overdraft Facility Bill & Receivable Discounting Corporate Leasing Sale & Lease Back Option Trade Finance Pledge Finance (Mortgage) Running Finance (RF) Term Loans (Short/Long) Corporate Fund Transfers / Remittances Corporate Transactional Convenience via Online Banking Import & Export Financing

P a g e | 19

Import & Export Bills for Collection Letters of Credit & Guarantee on Shipment Insurance in Transit

Investment Banking:

Investment banking includes the development, marketing and trading of a large range of securities and other financial instruments on the world’s financial markets. These include equities, which are stocks or shares, commodities, fixed income or bonds, and currencies. All of these, which are known as ‘asset classes’, can be traded directly or by using derivative instruments such as futures, options and swaps. . These instruments can help clients manage their risks and also provide investment opportunities.Contrary to common misconceptions, investment banking does not only encompass capital market activities. It also includes research into macro-economic trends and effects, and detailed analyses of the performance and factors affecting specific industry sectors and individual companies. In addition, investment banking traditionally includes the research and advisory services that banks offer to its clients for their major transactions such as mergers & acquisitions and initial or secondary offerings of their shares. An investment bank may also assist companies involved in mergers and acquisitions, and provide ancillary services such as market making, trading of derivatives, fixed income instruments, foreign exchange, commodities, and equity securities.

Products & Services:

Equity and Advisory Products:

Wealth management, innovative capital raising techniques, underwriting, placement of IPO’s, restructurings, public and private equity placements and mergers & acquisitions, Divestitures, Capital Rationing, Valuations, raising various forms of equity and quasi-equity structured a convertible debt note

Debt Capital Markets (DCM): Syndications, securitizations, privately placed and listed TFCs, term finance facilities, commercial papers, Corporate Bonds, Sukuk Bond

Project Structured Finance: Project financing involves financing of long-term infrastructure and industrial projects. These are non-recourse or limited recourse financings where project debt and equity used to

P a g e | 20

finance the project are paid back from the cash flows generated by the project. Such as Carbon Finance, Green Emission etc.

Treasury Management:

It is define as Management of an enterprise's holdings, with the ultimate goal of maximizing the firm's liquidity and mitigating its operational, financial and reputational risk.Treasury Management includes a firm's collections, disbursements, concentration, investment and funding activities. In larger firms, it may also include trading in bonds, currencies, financial derivatives and the associated financial risk management.

Treasury Department of a Bank may have following Segments:Money Market Deskwhich is devoted to buying and selling interest bearing Government Debt Securities and minimizing Interest Rate Risk on them.Foreign Exchange DeskWhich deal in Forex Services: buys and sells currencies at Spot Rates and responsible forHedging Currency Rate Risk.

Products & Services:

Ijarah Sukuk Bonds Treasury Bills (T-Bills) Pakistan Investment Bonds (PIBS) Forward Sale & Purchase, Foreign Currency Bill Purchase, Commercial Papers, Mutual Funds distribution, Term Finance Certificates Disbursements, Liquidity & Investment Solutions for covering their currency

exposures & risks

P a g e | 21

STATEMENT OF COMPLIANCEA Statement which possess the Compliance Responsibility over Bank to follow such Rules & Regulations which maybe Local or International having Legal Jurisdictions. The Bank is liable to compliance with them according to their Priority Standard as where Jurisdictions of Law prevail in such Business Activities conduct by Bank. Following are the Legal Laws, Standards, Guidelines, Circulars, Rules & Regulations, Statutory Notifications and related Rules of Autonomous Bodies:

Banking companies Ordinance 1962 implement by SBP State Bank Prudential Rules State Bank Notifications/Circulars/Guidelines Companies Ordinance 1984 implement by SECP SECP Notifications/Circulars/Guidelines IFRS and IAS Standards for Accounting Framework issued by IASB ISA Standards for Audit Framework issued by IFAC Islamic Finance Accounting Standards (IFAS) issued by ICAP AAOIFI Standards BASEL Accord Standards issued by Basel Banking Committee, Switzerland Ministry of Finance Statutory Orders (SRO’s/Circulars) Anti Money Laundering Act 2010 Negotiable Instruments Act 1881 Electronic Fund Transfer Act 2007 Financial Institution (Recovery of Finances) Ordinance 2001 Offences in respect of Banks (Special Courts) Ordinance 1984 State Bank of Pakistan Act 1956 Modarba Companies Ordinance 1980 Leasing Companies Rules 2000 Microfinance Institutions Ordinance 2001 Insurance Ordinance 2000 Non-Banking Finance Companies Rules 2003 Stock Exchange Regulatory Framework Board of Investment Rules FBR Taxation Laws & Rules Chamber of Commerce Industries (KCCI, LCCI)

P a g e | 22

Auditor General Pakistan (AGP) FIA, NAB and other Law Enforcement Agencies United Nations (UN) and other International Bodies

Products of SILK Bank Limited

There are following Products:

All-In-One Account

Basic Banking Account (BBA)

Business Value Account

IPS Account

PLS Account DEPOSITS

Salary Premium Account PRODUCTS

Munafa Rozana / Super Saver

Money Market Express

Online Express

Auto Finance

Home Finance LENDING

Personal Loan PRODUCTS

Ready Line

Credit Cards

Visa Debit Cards

E- Statement ALTERNATIVE

SMS Alerts DELIVERY CHANNELS

P a g e | 23

Internet Banking

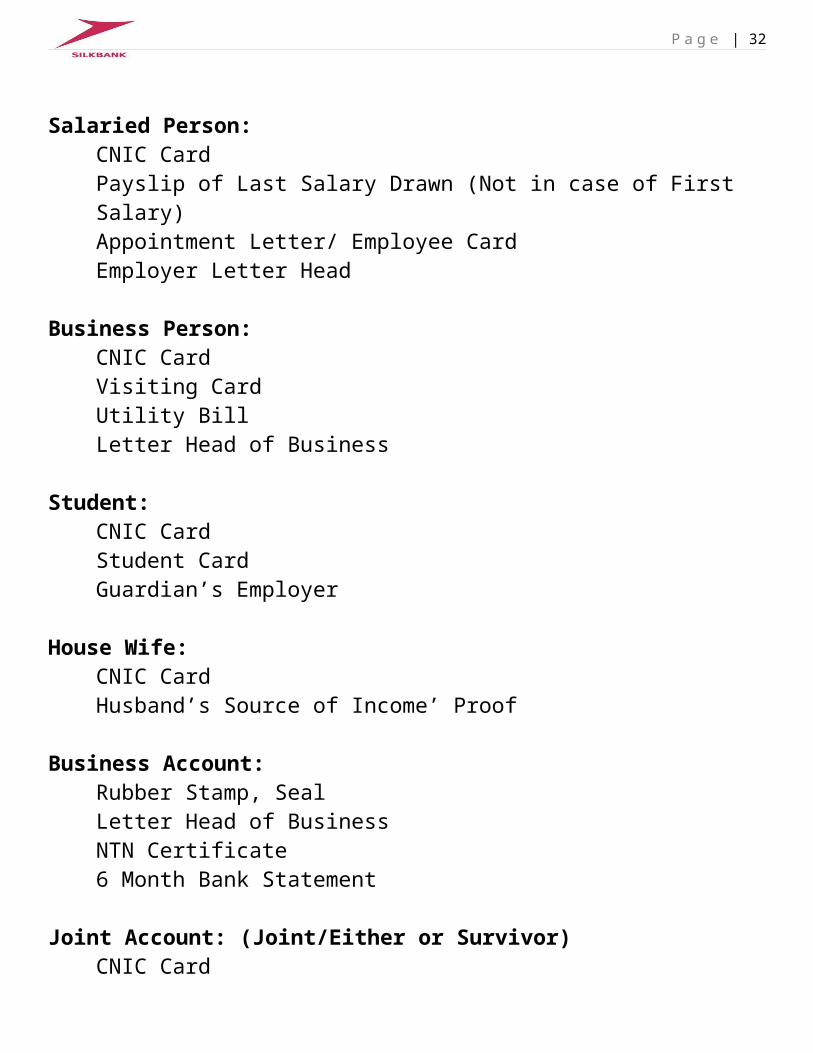

Required Documents forAccounts Opening of Following Categories

Salaried Person:CNIC CardPayslip of Last Salary Drawn (Not in case of First Salary) Appointment Letter/ Employee CardEmployer Letter Head

Business Person:CNIC CardVisiting CardUtility BillLetter Head of Business

Student:CNIC CardStudent CardGuardian’s Employer

House Wife:CNIC CardHusband’s Source of Income’ Proof

Business Account:Rubber Stamp, SealLetter Head of BusinessNTN Certificate6 Month Bank Statement

Joint Account: (Joint/Either or Survivor)CNIC Card

P a g e | 24

Proof of Both Source of IncomeUtility Bill

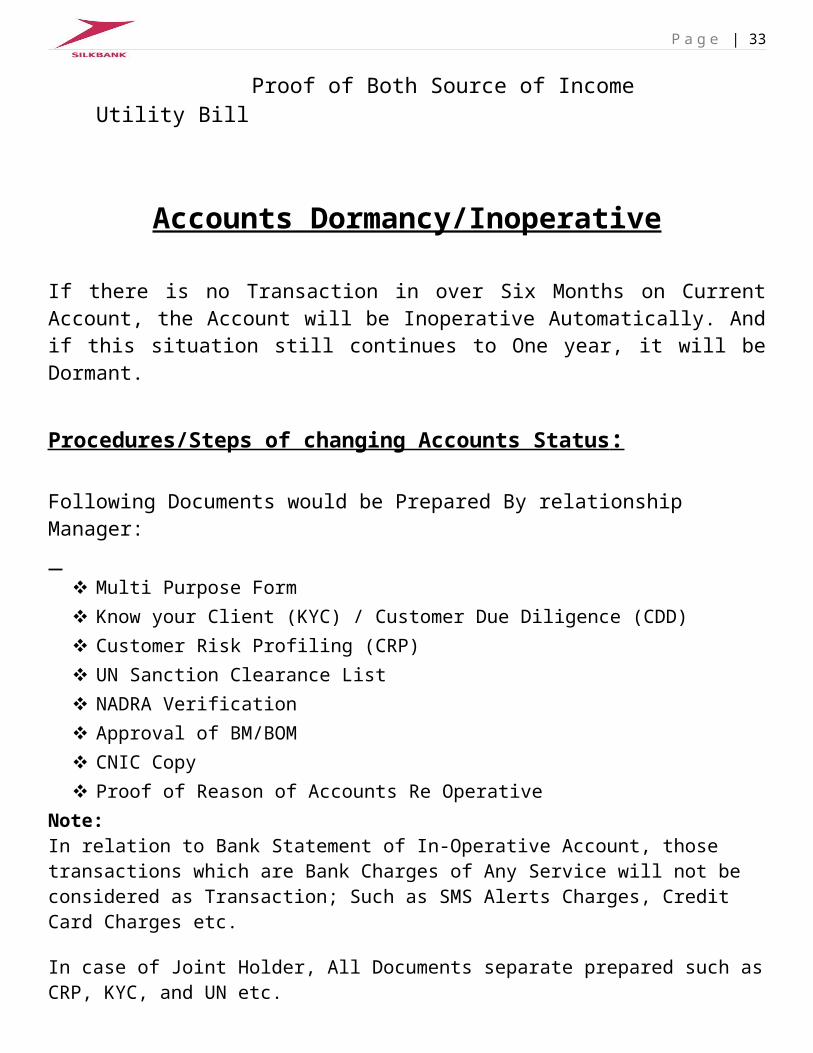

Accounts Dormancy/Inoperative

If there is no Transaction in over Six Months on Current Account, the Account will be Inoperative Automatically. And if this situation still continues to One year, it will be Dormant.

Procedures/Steps of changing Accounts Status :

Following Documents would be Prepared By relationship Manager:

Multi Purpose Form Know your Client (KYC) / Customer Due Diligence (CDD) Customer Risk Profiling (CRP) UN Sanction Clearance List NADRA Verification Approval of BM/BOM CNIC Copy Proof of Reason of Accounts Re Operative

Note:In relation to Bank Statement of In-Operative Account, those transactions which are Bank Charges of Any Service will not be considered as Transaction; Such as SMS Alerts Charges, Credit Card Charges etc.

In case of Joint Holder, All Documents separate prepared such as CRP, KYC, and UN etc.

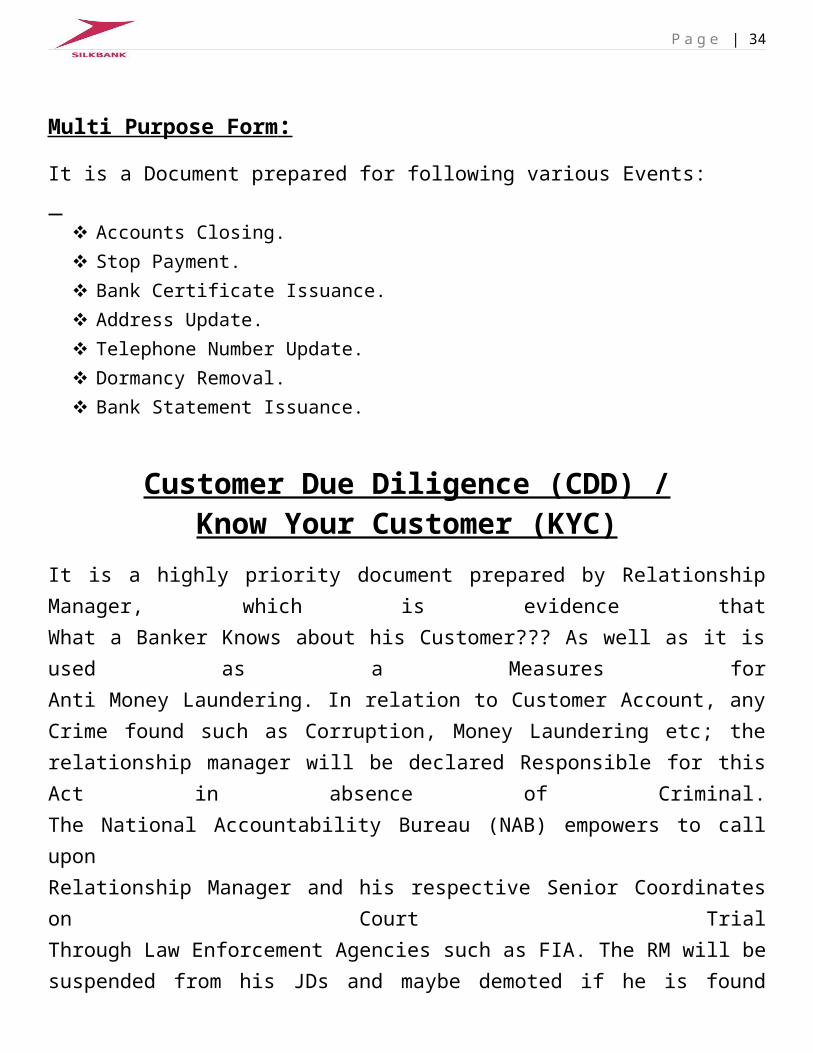

Multi Purpose Form :

It is a Document prepared for following various Events:

Accounts Closing. Stop Payment. Bank Certificate Issuance. Address Update.

P a g e | 25

Telephone Number Update. Dormancy Removal. Bank Statement Issuance.

Customer Due Diligence (CDD) /Know Your Customer (KYC)

It is a highly priority document prepared by Relationship Manager, which is evidence thatWhat a Banker Knows about his Customer??? As well as it is used as a Measures forAnti Money Laundering. In relation to Customer Account, any Crime found such as Corruption, Money Laundering etc; the relationship manager will be declared Responsible for this Act in absence of Criminal.The National Accountability Bureau (NAB) empowers to call uponRelationship Manager and his respective Senior Coordinates on Court TrialThrough Law Enforcement Agencies such as FIA. The RM will be suspended from his JDs and maybe demoted if he is found Guilty.The Definition of KYC is determined below:

According to State Bank Regulation; KYC in broader terms includes;

(a) Identifying the customer and verifying the customer’s identity on the basis of documents, data or information obtained from customer and/or from reliable and independent sources;

(b) Identifying, where there is a beneficial owner who is not the customer, the beneficial owner and taking adequate measures, to verify his identity so that the bank/DFI is satisfied that it knows who the beneficial owner is, including, in the case of a legal person, trust or similar legal arrangement, measures to understand the ownership and control structure of the person, trust or arrangement;

(c) Understanding and, as appropriate, obtaining information on the purpose and intended nature of the business relationship; and

(d) Monitoring of accounts/transactions on ongoing basis to ensure that the transactions being conducted are consistent with the banks/DFIs knowledge of the customer, their business and risk profile, including, where necessary, the source of funds and, updating records and data/ information to take prompt action when there is material departure from

P a g e | 26

usual and expected activity through regular matching with information already available with bank/DFI.

Customer Risk Profiling (CRP)

It is another Highly Prioritized Document which is in short Digital Record of KYC.Relationship Manager responsible to comply State Bank Circular No. 3 (2012) in relation to Guideline which states to profiles every new customer using their own judgment and information obtained through CDD/KYC process. A Template of Customer Risk Profiling (CRP) is provided at ‘Annexure-I’ of State Bank Guideline for guidance of Bank/DFIs in order to develop their own CRP formats considering their business activities, customer base and internal procedures etc.

Scope of CRP and KYC:

Bank is a part of a System to Detect and Prevent Money Laundering on any transaction value proceeds by any illegal means which shows Black into White Circumstances.

Following Business are considered as High Risk Profile Persons:

Any Private Limited Company Airline Industry Brokerage Firm Political Exposed Persons (PEPs) Jewelry Business Construction Company NGO’s Trust

CRP Enables to evaluate Risk of Bankruptcy by updating it simultaneously. It is an integral Part to defaulters Awareness as well as Anti Money Laundering.

Money Laundering:

Any Proceeds inward or outward relates to any act fromLow Standard Acts i.e. Kidnapping, Harassment to High Standard Acts i.e.Copyright Infringements, Tax Evasion etc mention in

P a g e | 27

Pakistan Penal Code 1860 - Second Schedule of AML Act 2010 is considered is Money Laundering.

P a g e | 28

P a g e | 29

Electronic Credit Information Bureau (E-CIB)

It is a Banking Surveillance Department of State Bank authorize to initiate an Information relates to Bank Customer, which is requested by Banker to access details.

A CIB is an organization that collects and collates credit dataon borrowers from its member financial institutions.The financial data is then aggregated in system and the resulting information (in the form of credit reports) is made available on request to contributing member financial institutions for the purposes of credit assessment, credit scoring and credit Risk Management. The major purpose of this database is to enable the financial institutions to know the credit history of their prospective customers thus enabling them to make a more prudent decision.

High Value Transaction Record (HVTR)

It is a Log file maintain daily by Relationship Manager By requesting it from BOM for issuance and giving Remarks/Comments on Each Transaction which is aboveRs. 100,000.The Proceeds will be monitor daily, Whenever the Account Holder of a Branch proceeds a transaction through (Cash, Clearing or Transfer) or through ATM/Credit Card mode, which is either Inward or Outward.

It includes all type of Risk Profile Persons (High, Medium and Low).

P a g e | 30

INTRODUCTION TO BANKING SOFTWARES

There are following Banking Softwares design for Retail Banking where Employees need Training time to time to get familiar with their Functions.

T-24 Temenos Software :

It is a Banking Software design for Retail Banking. Which Acquired By SILK Bank and implement through 3rd Part Vendor (Business Solution Consultancy Company).

This Software records Branch Banking’s Business Transactions through Assigned User ID Portals. Each User has assigned Separate Options and Functions to Access Information as per their Job Descriptions (JDs) Requirement.

This software has an ability to capture and process Events occurred in Branch Operation and Sales as a part of Banking; Such as Accounts Opening, Bank Statement Printout etc.

Rosetta Software:

It is a Banking Software use for Several Functions of Sales; including Scanning Documents with full information. It is usually used for scanning AOF Documents for Bank Digital Records.

P a g e | 31

SWOT Analysis

Strengths: Very Attractive Brand Name. Continuous and Phenomenal growth in profitability as its age is increasing. Surprise Testing of Branch Operation on Monthly Basis i.e. Mystery Shopping Workforce is very energetic because most of the workforce consists of the young employees. Branch location is very ideal due to situated Business Hub i.e. Hyderi Market. Training Schedule of employees is better than other banks. Computerized MCQs Test on Weekly Basis of Employees. Effective Banking Software Implementation i.e. T- 24 Temenos

Weaknesses: Small Age of Bank. Work overload on Employees. Ineffective Surveillance System. Small Network of Branch Banking as compare to other Banks. Customer Dissatisfaction regarding Investment Products and Insurance Policies.

Opportunities: Increasing demand of consumer banking. Increasing branch network in Pakistan. Increasing branch network at International level. Growing Islamic Banking branch network. Increased Rate of interest.

Threats: Adverse Law & Order Situations. Instable Rate of Inflation. Fluctuation of Interest Rate Risk of Default/Bankruptcy. Impairment of Customers Confidence over Bank Stability. Terrorism.

P a g e | 32

Global Economic Crisis. Government Instability. Trend of Banks Merging.

SUGGESTIONS & RECOMMENDATIONS

During my internship I found some of the faults and lack of some of the facilities in Bank’sOperations. Here are some of the suggestions which I recommend to the Silk Bank Limited.

The advertising of Bank and Bank’s Products is not so much good and exposed to people. So, Bank should hire some of the skilled Marketers who can design creative and attractive advertisements and advertising campaigns by using all possible means of Communication including Social Networking Websites to make every person aware of the bank’s updates about old and new products and services.

Training sessions of bank employees of all over the country are conducted by bank at Head Office Karachi which is very expensive for the bank to bear the accommodation and meal charges of the employees. So bank should expand and establish some more training centers in other cities of the country in order to reduce these expenses.

Bank is somewhat slow in launching new products. So bank should review its policies of launching new products in short and reasonable time.

Foreign branch network should be increased in order to capture profits from all over the world.

Bank should motivate Sales Team because they are the main Source of Income, so encourage them by giving Reasonable Incentives and Bonus.

There should be a communication link between executives and top level management.

Employees should not be overloaded with work, this helps in relaxation of employees and will increase job satisfaction of employees which is in best interest of the bank.

P a g e | 33

CONCLUSION

The “bank” is actually an institution which accepts or collects the money or deposits from those who have surplus of it and lend it to those who have in need of it or have capital in deficit, it actually acts as a financial intermediary which connects persons with surplus money to those who have shortage of money. In this process banks earn profit or commission for connecting these people.

The history of banking in Pakistan is very interesting because at the time of independence there was no bank in Pakistan which could perform the banking operations for this area of the world. Till the end of June,1948 the financial operations of Pakistan was governed by the “Reserve bank of India” but that casted a loss to Pakistan in a sense that British Government distributed the 70% of reserves to India and Pakistan got just 30%. After this Quaid-e-Azam laid down the foundation of “The State Bank of Pakistan” in July 1st, 1948.

In Pakistan there are a number of commercial banks which are accepting deposits and advancing loans to customers with a lot of other facilities of providing financial services and products to customers like car financing, home loans, debit and credit cards, agricultural loans and a lot of other products.

Silk Bank is one of the most important, emerging and profitable bank in Pakistan which is Under the Leadership of Mr. Shaukat Tarin. In its few years of age it showed a remarkable performance and improvement with huge profits which is becoming high and high. But do not forget about the “Global Economic Crisis 2008” which affected all the banks including all the businesses.

Bank has great strengths which its competitors do not have as it has a very attractive brand name with a slogan of “Yes We Can” which is somewhat emotional touchy for the persons who seeks for care. The HR of the bank are very trained, professional and skilled which is contributing towards the profits of the bank and bank in this way going towards attaining continuous profits. The workforce of the bank is very young and energetic and working is being done on standard basis. Pakistan government is supporting the bank because it is the foreign investment bank which is acting as FDI for Pakistan.

P a g e | 34

The graph of the bank’s performance is going in upward position which is a very good sign for the bank. It was possible for the bank because the bank has given a lot of importance and attention to its customers and made the product portfolio according to the needs and wants of the customers. Because bank is using the continuous process of assessing the needs and preferences of the customers which is very helpful in making new products and for providing the desired services to the customers. Bank has great strengths which its competitors do not have as it has a very attractive brand name with a slogan of “Yes We Can” which is somewhat emotional touchy for the persons who seeks for care

Last but not the least; Silk Bank has all the capabilities for coping with the changing business environment, bad economic conditions and political condition of the bank.

***** THE END *****