Embed Size (px)

Citation preview

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 1/65

Kathmandu University School of Management

Kathmandu College of Management

Internship Report

Title of the project: A Study on the need of market segmentation and

targeting at Nepal Bank Limited

As part of the requirement for BBA/BBIS programme

Internship Programme Code: RIS 401

Internship Employer

Himalayan Bank Limited

Interns

Anup Basnet, KU Redg No: A009187-08

Sambeed Regmi, KU Redg No: A009233-08

June, 2012

1

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 2/65

SIGNATURE PAGE

I/We certify that I/we have read the document and, in my/our opinion, it is satisfactory in

scope and quality as a project in the partial fulfillment for the undergraduate course of

‘Internship’ held at the Kathmandu College of Management during the Fourth Year Second

Semester, 2011.

Date: June 2011

_______________________

Project Evaluator

Kathmandu University School of Management

2

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 3/65

DISCLAIMER

The authors are confident that the result presented in this report will be taken as guidance

for a more comprehensive study at the future date. The authors of the report are not

responsible or liable legally or by any other means against the results of the report. Any

consequent decision based on this report shall not make the authors responsible.

The views expressed in this report are as per the findings and research undertaken. These

do not reflect the single rule of thumb nor are these endorsed by the college.

3

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 4/65

DECLARATION

We, the undersigned declare that this project entitled is a result of our own study/research

carried out in the year 2011. It has not been submitted to any other university or any other

examinations.

Signature:

______________ _____________

Bhawana Khanal Sumira Shrestha

Batch 2007-11 Batch 2007-11

Kathmandu College of Management Kathmandu College of Management

Reg No: A008035-07 Reg No: A008077-07

ACKNOWLEDGEMENT

4

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 5/65

This report and project work would have not been successful without help of so many

people. We would like to express our sincere gratitude to all of those helping hands.

Foremost we would like to thank KUSOM and KCM for providing this opportunity to do

internship. We would also like to thank Mr. Bishnu Raj Adhikari, principle of KCM for

giving us moral support and boosting up our confidence all the time.

We are much indebted to our internship co-coordinator Mr. Lakpa Gelu Sherpa, who

guided us throughout the project and helped us to complete the project in time.

Also we extend heartfelt thanks to Nepal Bank Limited family for giving us this

opportunity to be a part of their family and guiding us throughout the internship. We would

also like to thank Mr. Biswo Raj Kandel branch manager and Mr. Gyanendra Bikram Karki

(deputy manager/work supervisor) of Dillibazar branch for believing in us and giving us

responsibilities.

We also express our heartfelt gratitude to all the members of NBL, Dillibazar for their

invaluable assistance, openness, cooperation, supporting us throughput the internship

period and helping us to learn so many things.

EXECUTIVE SUMMARY

5

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 6/65

Nepal Bank Limited is the oldest commercial bank of Nepal. Nepal Bank Limited was

inaugurated by His Majesty King Tribhuwan. It was established 1937 which marked the

beginning of an era of formal banking in Nepal. It is certified ‘A’ grade financial institution

by NRB. NBL is one of the pioneers in Nepalese banking history and it has a very wide

network of branches across Nepal.

This internship report is divided into four parts. The first part is related to the background

of the internship which is described in terms of the opportunities and experiences and the

reasons for choosing the specified bank which is NBL, in our case. We have presented our

goals and objectives for the internship so that we would have a map of how we are going to

achieve those objectives during the entire internship period. We were engaged in different

departments during the internship and performed various jobs such as helping customers in

account opening and closing and also filling up the forms for customers who had difficulty

in reading and writing; Scrutinizing various schemes and interest rates of deposit and loan

provided by the bank and informed customers who inquired about the schemes; Printing,

issuing and recording the issue of checkbooks and printed statements for customers;

Preparing debit vouchers for Tribhuwan University pension and recorded the pension

disbursement; Operated Newton software to solve customers’ inquiries, print checkbooks,

statements and open or close accounts and so on.

In the second part of this report, a brief introduction of banking industry in Nepal and

Nepal Bank Limited is given.

A major part of the report consists of the project undertaken during our internship.

Basically, our research was directed towards importance of market segmentation and

targeting for effective marketing of banking services. We prepared a questionnaire, and we

also analyzed secondary data available regarding the bank and we also conducted

interviews with bank’s customers to know more about the customer attitude, preferences,and their views regarding services provided by banks. We also conducted unstructured,

direct personal interviews and telephone interviews with the bank’s customers. The purpose

of our research was to help NBL identify profitable market segments and to target them

with appropriate marketing strategies. The existing and potential customers are divided into

four segments on the basis of gender, age, income and occupation. The segments were

6

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 7/65

identified by observing the actual customers in the bank, during our internship. In order to

study the profitable segments and position the services to reach these segments, we

conducted a survey focused on segmentation and targeting the market. The questions were

focused on the preference of various services and service attributes, by different segments.

The survey consisted of questions regarding the preferences of customers towards services

quality, appealing attributes of service schemes, preference of communication media for

receiving information about bank’s new services, time preference by customers of different

segments and new services preferred by various groups. The survey established that,

customers use all the services of banks and providing higher quality service along with

value addition will help in promoting the brand name as well as capturing larger market

share. Similarly, contribution to corporate social responsibility helps to cast positive image

on customers and build brand equity. Quality in delivery of core services is very important,

nevertheless, attributes like ambience, fast service and convenience should not be ignored

The major finding of the survey is that appropriate market segmenting and targeting is very

important for effective marketing of services and enhancing of brand equity. Market should

be segmented into appropriate target groups according to demographics or psychographics,

and then bank should target each segment by building appropriate marketing strategies.

NBL must design innovative services and customize the services to match the needs of

various segments. More and more people are switching to internet based services and

online banking. So, NBL must put more effort on increasing its ATMs, developing

interactive website, developing internet based services and putting up advertisement and

promotion materials on internet according to the preference of the target segment.

Similarly, NBL providing flexibility in its service hours and procedures according to the

need of people belonging to various occupation groups is important. Special accounts for

senior citizens and children help in differentiating the services. Corporate social

responsibility and higher interest rates have similar appeals amongst the customers.

Similarly, customizing the services for various segments helps generate maximum value

from the market.

Developing innovative marketing strategies backed by strong products and services

succeed in capturing customer value and large share of market. Therefore, NBL should

7

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 8/65

focus on effective segmentation and targeting by launching the right products, to the right

customers, at the right time.

LIST OF TABLES

1. List of products of NBL………………………………………………….10

2. Comparison of interest rates and profitability……………………………21

8

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 9/65

9

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 10/65

LIST OF FIGURES

1. Factors considered by customers while transacting with bank………………….32

2. Importance given by customers to corporate social responsibility………………33

3. Preference of communication media by various age groups…………………….34

4. Preference of communication media on the basis of occupation………………..35

5. Preferred time of customers on the basis of occupation for doing banking

transactions………………………………………………………………………36

6. Preference of new service by different age groups……………………………...37

7. Preference of new services by different occupation segments………………….38

8. What customers liked about recently visited bank……………………………....39

10

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 11/65

LIST OF ACRONYMS

KCM: Kathmandu College of Management

BBA: Bachelor in Business Administration

NBL: Nepal Bank Limited

NRB: Nepal Rastriya Bank

KUSOM: Kathmandu University School of Management

ABBS: Any Branch Banking System

PEST: Political-legal, Economic, Socio-cultural, and Technology

SWOT: Strength, Weaknesses, Opportunities, Threats

BOD: Board of Directors

CSR: Corporate Social Responsibility

SLR: Statutory Liquidity Requirement

CRR: Cash Reserve Ratio

CEO: Chief Executive Officer

BOD: Board of Directors

HBL Himalayan Bank Limited

NIBL: Nepal Investment Bank Limited

RBB: Rastriya Banijya Bank

11

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 12/65

ATM: Automated Teller Machine

IT: Information technology

HRM: Human Resource Management

Declaration

Recommendation letter from employer

Recommendation letter from college supervisor

Acknowledgement

Executive summary

Table of contents

List of tables

List of figures

TABLE OF CONTENTS

Contents Page

Part one

INTRODUCTION

1. Background 1

2. Objectives of internship 2

3. Jobs performed in the internship 3

4. Jobs of intern’s supervisors 6

12

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 13/65

Part Two

INTRODUCTION OF COMPANY

1. Introduction of Nepal Bank Limited 8

a. Vision/Mission/Values and objectives 8

b. Organizational Strategies 9

c. Major Products/product lines 10

d. Organizational structure 14

2. Analysis of the organization’s general and competitive environment 15

Part Three

PRESENTATION OF THE PROJECT

A study on the need of market segmentation and targeting at Nepal Bank Limited

Section I: Introduction

1. Introduction of the project 22

2. Objectives 23

3. Scope and limitations 23

Section II: Conceptual Framework 25

1. Review of related literature

Section III: Methodology 28

1. Methodology/ procedures

Section IV: Presentation and Analysis 31

13

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 14/65

Section V: Conclusions 42

1. Project specific conclusion and suggestions

Part four

REFLECTION OF INTERNSHIP 43

References 45

Appendixes

14

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 15/65

15

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 16/65

PART ONE

INTRODUCTION

1.Background

This report is prepared in the partial fulfillment of the undergraduate program of

Kathmandu University School of Management. The students of Bachelors of Business

Administration (BBA) are required to undergo internship program for a period of eight

weeks, during the eighth semester.

The internship program provides students with an excellent opportunity to apply the

knowledge gained in the classroom lectures, into real work environment. It also builds up

confidence in the students so as to prepare them for the challenge of the corporate world.

Internship program helps students in developing practical approach and professionalism

toward work and improving business relations.

For our internship, we choose Nepal Bank Limited, Dillibazar. Nepal Bank Limited is one

of the pioneers in Nepali Banking Industry. It has the widest networking all over Nepal and

provides wide range of services. It has been providing banking services to all segments of

people and organizations. We chose NBL to accomplish our internship so that we could

learn the basics of banking and understand the challenges and opportunities faced by a

typical Nepali bank.

During the internship period we were placed in customer service desk, remittance

department, credit department, teller and administration. We gained knowledge and

experience about the functioning and organization of various departments and the role of

each department in the overall functioning of the bank. We also conducted a study on the

need of market segmentation and targeting at Nepal Bank Limited. This research was very

important to the bank and it was also an interesting subject matter for us because it was

related to theories we learnt in classroom lectures. We surveyed the customers of various

age groups, income groups to identify the profitable segments in the market and target them

appropriately.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 17/65

2. Objectives of Internship

Internship program for Bachelors of Business Management, Kathmandu University is

basically designed for students to gain practical knowledge and real life experience.

Internship Program provided the interns with an excellent opportunity to learn the work in

the field of interest. As fresh graduates, it is quite difficult to enter the job market without

experiences. The internship program’s main objective is to develop a very good platform to

develop our skills, confidence and prepare us for the challenge

Internship program provided interns with an opportunity to learn practical aspects of Nepali

Banking industry. Working in one of oldest banks of Nepal, Nepal Bank Limited, helped in

gaining knowledge about the basics of contemporary banking. Since we intend to work for

contributing to Nepali Banking Industry, we had to gain acquaintance with the industry, the

corporate culture and the nature of work.

Goals for internship

• To complete internship program, regarding it as an opportunity to get acquainted

with real work environment.

• To observe and learn the functioning, operations and management of banking

system.

• To get acquainted with the corporate culture in banks of Nepal and explore the

challenges and opportunities

• To explore the career opportunities, in Banking.

• To enhance decision making skills and ability to work in teams.

• To develop personality and build a professional attitude towards work.

• To develop interpersonal and communication skills.

• To increase personal relations with people in the industry.

• To make practical use of classroom learning in solving real world problems.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 18/65

3. Jobs performed in the internship

During our two months period of internship in Nepal Bank Limited we were placed in all

the departments of the branch. On the first day we were given a brief orientation of the

organization and we were introduced to the members of the bank. We had a brief meeting

with the branch manager Mr. Bishow Raj Kandel who explained us our duties and

responsibilities in the organization throughout our internship. We were given knowledge of

NBL culture, operations/functions.

We worked in the Customer Service Department, Teller, Remittance Department, Credit

Department and Administration Department. We also invested some of our time in

marketing the products of the bank.

Customer Service Department

The customer service department is the department where the customers make first contact

with the bank. The customer service department basically seeks to help customers with

their problems and queries. We started our work from customer services by performing the

following jobs:

• The supportive members of customer services briefed us about the functioning of

the customer services and the whole bank. They explained the tasks performed at the

help desk and acquainted us with the relationship between the tasks performed at thehelp desk and that of other departments.

• Helped customers in account opening and closing and also filling up the forms for

customers who had difficulty in reading and writing.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 19/65

• Prepare interest expense voucher, tax paid voucher, and voucher for service charge

taken.

• Scrutinized various schemes and interest rates of deposit and loan provided by the

bank and informed customers who inquired about the schemes.

• Printed, issued and recorded the issue of checkbooks and printed statements for

customers.

• Prepared debit vouchers for Tribhuwan University pension and recorded the

pension disbursement.

• Operated Newton software to solve customers’ inquiries, print checkbooks,

statements and open or close accounts.

• Helped in filing the vouchers and other records.

Teller

Teller is the place where the cash deposits are received and credited to respective accounts

and cash payments are made against checks and respective accounts are debited. I

performed the following jobs in this department:

• Observed the process of deposit and withdrawal process, ABBS transactions and

entering the transactions in the software.

• Identifying discrepancies (if any) in the checks.

• Checking the requirements for processing any transaction; like authorized

signature, endorsements and common seal.

• Observed the process of clearing.

Remittance Department

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 20/65

Remittance Department at Nepal Bank Limited is the department which sends and receives

money from various parts of the world and from those branches of NBL which does not

have ABBS facility.

• Helped customers in filling up receipts for sending and receiving remittances.

• Recording and preparing vouchers for remittance, drafts and out bills.

• Entered the OBC vouchers in OBC ledger, stamped the out bills and entered them

in excel sheet format prepared by the remittance department.

• Assisted in the clearing process.

•Support employees in maintaining other records

• Prepared voucher for commission charged in sending money to branches not having

ABBS facility

Credit Department

Credit department is that section of bank which provides various types of credit to

individuals and organizations to generate interest income to the bank. In the credit

department we performed the following jobs:

• Prepared vouchers for interest income received, closing and renewal of the loan

accounts

• Went through credit manual of NBL to get basic knowledge of various types of

credit provided by NBL and the detail guidelines to process credit to customers.

• Entered transactions like renewal of loan, new loan and closing of loan accounts in

the Newton software.

• Helped in loan sanction process.

Administration Department

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 21/65

Administration department is responsible for the recording of all the transactions daily,

correspondence, inventory management and other administration activities. We performed

the following jobs in administration department:

• Observed how salary sheets are prepared, passed and recorded. Similarly, studied

how all other expenses and revenue accounts are recorded, rechecked and passed.

• Studied the procedure for tax preparation to report to head office and Nepal Rastra

Bank

• Learnt the formal procedures of correspondence and communication with the head

office and other branches.

• Learned the basic functions of administration department such as writing off

depreciation, preparing salary of employees, maintaining books of assets, preparing

budget and so on.

4. Role of Intern’s Supervisors

At NBL, the deputy manager, Gyanendra Bikram Karki, is the operation head of the branch

office. He supervises all the work in the office except credit He verifies the transactions of

the bank and approves important decisions as. He is also the work supervisor of the interns.

He is responsible for assigning work and duties to the interns and evaluating performance.

Customer Service Department

At the customer service desk, the department heads had the following responsibilities:

• Catering to the clients’ needs, serving their problems, and responding to their queries.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 22/65

• Printing statements, issuing checks, opening accounts, filing and recording and carrying

out various other transactions.

• Disbursement of pensions and providing ATM cards.

Remittance Department

At the remittance department, the department heads had the following responsibilities:

• Transferring money to various other branches of NBL and receiving money from abroad

as well as from other branches of NBL.

• Clearing function

Teller

At the teller, the department heads had the following responsibilities:

• Receiving deposits and making cash payments to customers.

• Payment of salary, pension and preparing pension lists.

• Fund management.

Administration

At the administration department, the department heads had the following responsibilities:

• Passing salary accounts and all other expenses and revenue accounts.

• Maintaining accounts of assets, managing inventory.

• Preparing estimated budget to report to the head office

• Preparing quarterly reports and sending it to NRB.

• Financial statements and tax reporting.

Credit Department

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 23/65

At the credit department, the department heads had the following responsibilities:

• Loan appraisal.

• Opening, renewal and closing of loan accounts.

• Evaluation and assessment of collateral.

• Dealing with clients and maintain valuable customer relationship.

PART TWO

INTRODUCTION OF INDUSTRY AND COMPANY

Commercial Bank Act 1974 defines a commercial bank: ' A commercial bank means bank

which deals in exchanging currency, accepting deposit, giving loans and doing commercial

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 24/65

transactions.' Prior to the establishment of Nepal Bank Limited, people relied on

borrowings from the corrupt moneylenders, who charged very high interest rates and added

other dues. With the cooperation of Imperial Bank of India, Nepal Bank Limited came into

existence under the Nepal Bank Act 1937. Nepal Bank played a dual role of commercial

bank and the central bank until the establishment of Nepal Rastra Bank on 26th April, 1956

it carried all the functions of a central bank.

Among various service sector banking is the most growing sector in case of Nepal. There

are 31 commercial banks, but only a small percent of people are covered by banking

services. There is very high competition because most of the banks and financial

institutions are concentrated in urban sectors only. There are lots of untapped areas where

banks can excel it and at the same time attract more and more people to the banking

services.

1. Introduction of Nepal Bank Limited

Nepal Bank Limited is one of the oldest commercial bank in Nepal. Nepal Bank Limited

was established in 1937. NBL was inaugurated by His Majesty King Tribhuwan. The age of

formal commercial bank, in Nepal started with the establishment of Nepal Bank Limited.

The bank is also one of the largest in Nepal with 110 branches in the 55 districts of the

country.a. Vision, Mission, Values and Objectives of Nepal Bank Limited

Vision:

To remain the leading financial institution of the country

Mission:

Nepal Bank Limited seeks to provide an environment within which the bank can bring

unique financial value and services to all customers. It will be a sound institution where

depositors continue to have faith in the security of their funds and receive reasonable

returns; borrowers are assured of appropriate credit facilities at reasonable prices; other

service- seekers receive prompt and attentive service at reasonable cost; employees are paid

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 25/65

adequate compensation with professional career growth opportunities and stockholders

receive satisfactory return for their investment. (Bank overview: Nepal Bank Limited)

Values:

• Respect, service and safety for the customers we serve

• Respect, reward and opportunity for the people with whom we work

• Respect, cooperation and support for the economic community of Nepal

Objectives:

Nepal Bank Limited has the following objectives:

• Maintaining leading share of banking sector with a significant presence in all major

geographical areas in the country.

• Providing competitive and customer oriented banking services to all customers

through competent and professional staff.

• Reclaiming leadership within the national financial community.

b. Organizational Strategies

The organizational strategies for NBL are as follows:

• To improve the human resource of the bank to provide greater customer satisfaction

• To expand the market share and increase the customer base of the bank

• To bring in new products and programs that meet customer needs

• To maintain strategy of stabilization

c. Major products of NBL

NBL is one of banks, in Nepal, having largest deposit base. It renders its services to a very

large number of customers all over Nepal, by maintaining its competitive position, despite

the fierce competition. The products and services offered by NBL has been continuously

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 26/65

upgraded and improved according to the needs of the customers and changes in the banking

environment. The Products of NBL are basically the services designed and provided to

customers in terms of deposit schemes, credit facilities and other services of the bank.

Since NBL is one of oldest commercial bank of Nepal, it has providing banking services to

a large number of customers. NBL has designed its schemes and services in such a way that

it is assessable and suitable for everyone. The products and services of the bank target all

the age groups from senior citizens to youngsters. NBL has competitive interest rates for

women, senior citizens and E-banking and ATM facilities to young and busy people.

Similarly, it has credit facilities for entrepreneurs, businesses and consumption purposes. It

provides services that meet the needs of modern bank in order to compete in the market and

retain its customers. It has ABBS facility within Kathmandu Valley and various parts of

Nepal. It has recently started mobile banking and E- banking facilities to its customers. The

list of products and services provided by NBL is presented below:

Table 1: List of products of NBL

Deposits:

• NBL General Savings

•

Women Special Savings

• Senior Citizen Special Savings

• Employee Saving Account

• NBL fixed Deposit Account

• Current Deposit and call deposit

account

• Special Savings Account

Loans:

• Gold- Silver Loans

•

Export Loans

• Post-shipment and pre-shipment loans

• Hypothecation Loan

• Trust Receipt Loan

• Overdraft loan

• Housing Loan, Personal Loan

• Term Loan

• Industrial and working capital Loan

Other services provided by NBL are listed below:

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 27/65

SMS Banking:

Remittance:

NBL Remit service is based on online data transfer system and it is instant enough,

efficient and very much secure. For the authentication purpose, secret key is generated on

the system, which is required by the customer while being paid. Remittance facility is

available both for instant cash payment and credit to the beneficiary personal account.

Manager’s Check: It is a check drawn by Nepal bank on itself, which is used for payments

on behalf of Nepal bank.

ABBS: Customers can withdraw or deposit money from any branch of NBL, without

having to bear extra charges, across Nepal having the facility of anywhere branch banking

services.

Clearing: NBL provides the facility of clearing check on behalf of its customer it accepts

check of other banks.

NBL has recently launched SMS Banking services. SMS banking provides the following

services:

• Secure transaction with PIN code

• Instant Balance Information

• Last three transactions with current Balance

• PIN code changing facility

• Latest Exchange rate of Foreign currency

•

Account Stop Facility

• Check Book print request

• Account statement print request

• New Product information of bank

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 28/65

ATM Card: NBL provides ATM cards to its customers. The ATMs are placed at main

points in Kathmandu and other cities and customers can also use the card in India in the

ATMs of Punjab Bank Limited. Transactions from ATM of NBL, is free of cost. Similarly,

Point of sale transactions and issuance of new card doesn’t incur any cost to customers.

E-Banking: Nepal Bank Limited provides the customers with E- Banking services so as to

enhance its services along with the rapid changes in technology

Bank Draft: NBL also has the facility of bank draft for transfer of money. However, the

uses of bank draft have decreased considerably due to E- remittance services and electronic

payment systems.

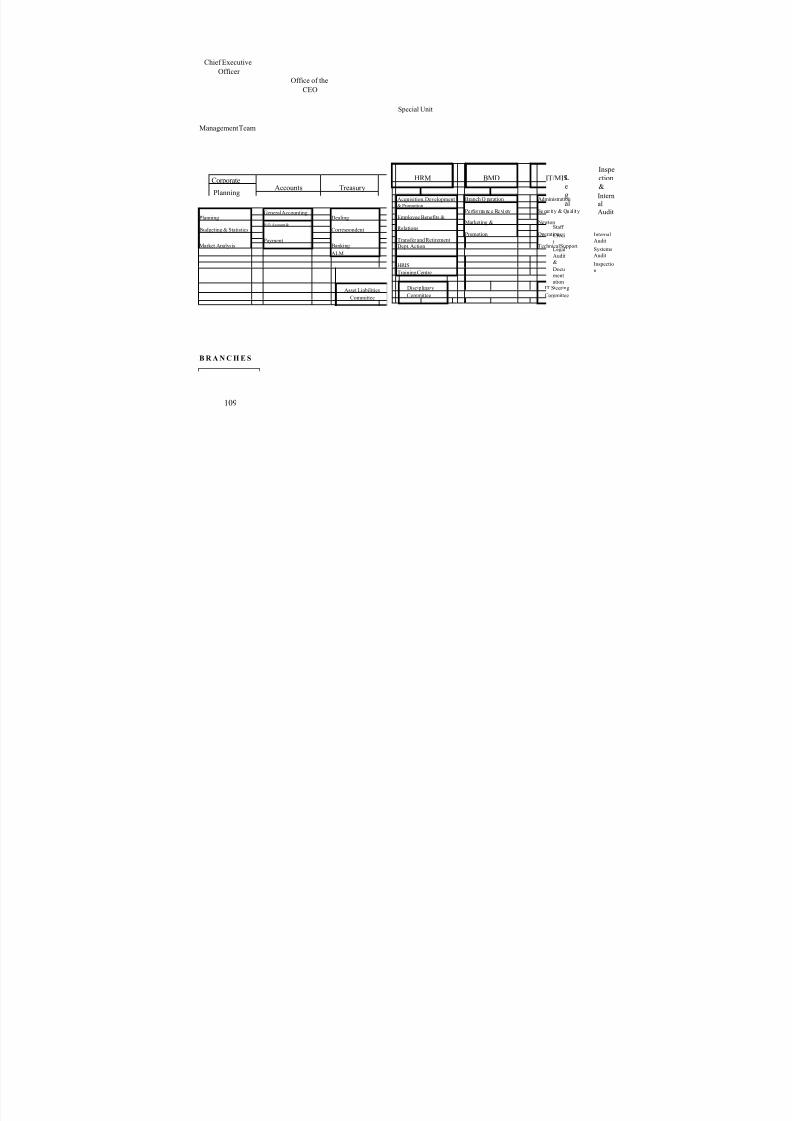

d. Organizational structure of the company

NBL has centralized organization structure. Organization’s strategies, policies, procedures,

interest rates, and all other major decision are made by head-office and all the branches

work in accordance to the circulation given by head-office. Branch have very less say

regarding decision making. NBL has centralized structure with management committee on

the top of the hierarchy. Below the management committee lays the Chief Executive

Officer and Management team. Below in the hierarchy are the various departments such as

corporate planning, accounts, treasury, central finance, credit, HRM, IT, legal, inspection

and internal audit. Corporate planning department is responsible for planning, budgeting,

and statistics, and market analysis. Similarly, account department performs the general

accounting, head office account and payment functions. Likewise treasury department does

the asset-liability management and other banking jobs. Central finance department handles

the trade finance, guarantee, remittance, agency, and back office. Likewise, credit

department deals with risk management, relationship management, and credit management.Human Resource Management department manages the acquisition, development, and

promotion of employees, manages employee benefits and relation, transfer and retirement,

human resource management system, and training centers. Similarly, BMD department

supervises the operation of various branches, review performance, and marketing and

promotion. IT department ensures that the technical support is always standing by in case if

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 29/65

any problem occurs in the bank software, checks security and quality, observe day to day

operation, and administration. MSD department carries the task of asset management,

procurement, developing PR, and dispatch. Legal department handles issues related to staff,

credit, and legal audit and documentation. And finally Inspection and internal audit

department carries the function of internal audit, system audit and, inspection. There are

various committees to further supervise the departments such as asset-liability committee

for treasury department, credit committee for credit department, disciplinary committee for

Human Resource Department, and IT steering committee for IT department. All the

departments further assist branches but especially branch management department is

responsible for direct supervision of branches. Organization structure of Nepal Bank

Limited is presented in Annex-2.

NBL, Dillibazar organizational structure is based on hierarchy. There is one branch

manager, one deputy manager, one assistant manager, and other employees of various

levels. There are various departments such as Customer service, Remittance, teller,

administration, and credit.

2. Organization’s general and competitive environment

Environment Analysis

Organizations’ environment is the surrounding and context in which businesses operate.

Environment plays a major role in defining the success and profitability of and

organization. Businesses are highly affected and influenced by the environment in which

they operate. Banking industry is also very much affected and influenced by the external

environment, so banks need to study and analyze the external environment continuously.

PEST analysis is one of the methods to analyze the environmental forces. It considers 4

major environmental forces affecting the industry. They are:

• Political-legal environment,

• Economic environment,

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 30/65

• socio-cultural environment and

• Technological environment.

Political- legal environment

Instability in the political system in Nepal poses huge challenge to banking industry.

Political system changes often and rules and regulations keep changing accordingly.

Political systems have direct affect on the growth and development of the society. Political

system shapes the economy of any country. Banking is the backbone of economy, so it is

highly regulated. The government plays a major role in designing the banking industry. In

Nepal, banks and financial institutions are regulated by Nepal Rastra Bank. Since the

central bank is also the banker to the government, NBL is influenced by the politicalenvironment to a great extent. Similarly legal environment also affects the banking

industry. NBL should work according to the directives and circulations send by Central

Bank. The central bank determines the interest rates, SLR, CRR and other requirements

that have to be compulsorily fulfilled by the financial institutions. The legal environment

not only consists of the regulator but also the industry. Commercial banks operate within a

highly dynamic and competitive environment where the banks have to draw fine line

between ethics and profitability. Banks operate in a highly litigious environment. So,

commercial banks must be very careful in matters, in which it stands accountable and

liable. NBL lies strictly within the regulation of NRB, so, it has to comply with the

regulations posed by NRB because it has a huge amount of money and assets of public,

government and owners. Legal environment is also very much dynamic since it keeps on

changing and bank has to maintain compliance with the new rules and regulation no matter

what

Economic environment

Economic environment is one of the important external factors, influencing the industry

and the firm itself. Economic environment includes the general macro-economic factors

such as interest rates, inflation level, unemployment level, growth in economy and so on.

Since bank is the backbone of economy, economic environment has direct impact on the

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 31/65

behavior of customers of bank. When, economy is in growing trend, economic activities

boom. People and businesses will have surplus money and the deposit of bank will

increase. Similarly, investment activities increase and bank will be able to lend out more

money to borrowers and investors and realize higher profits. More people will demand

money in the form of credit for business and consumption purposes. Thus, bank will

generate more revenue. Unemployment level also affects the banking industry. Rise in

inflation rate will discourage people to keep money in the bank, as value of money starts

decreasing.

Socio-cultural environment

Society and culture shapes the attitude and behavior of people. Bank operates in a society

and society has a major role in determining the profitability and growth of the bank. The

attitude of the members of the society is important for a bank’s success. So, positioning the

bank in terms of its value proposition is important. Moreover, customers nowadays are

more educated and better aware about the banking system mainly due to education and

having access to information. Socio-cultural forces include the lifestyle, demographics,

psychographics and behavioral aspects of the people.Change in lifestyle have entailed a

major impact on the banking sector. Nepal Bank has faced the need to continuously

upgrade its service quality and value addition for retaining its brand image in the society.Similarly, NBL was faced the challenge of technological innovation and advancement.

Besides, banking in the past was considered to be a place for rich people only. But

nowadays, banking is not confined to rich people and business people only. People from all

levels of the society, backgrounds, income levels and occupational status are coming under

the banking service. Banking is equally important for students, businesses, housewives, and

all other people. Banking habit of people is changing continuously and in a better way.

Bank has become a inevitable element for the development of people and society. Nepal

bank is very much aware about such changes in the socio-cultural environment and is

constantly updating and upgrading its products and services accordingly.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 32/65

Technological environment

Technological environment is the most dynamic and challenging environment for banks.

Changes in technology have made the banking operation much easier, systematic and

standard. Nevertheless technology provides businesses with competitive advantage,

innovation and cost leadership, it poses immense threat of competition and imitation by

competitors. Technology poses threats because every new technology becomes obsolete

when new and improved version comes in the market. When competitors easily imitate the

technology the pioneer will face strong competition to overcome the huge investment in

research and development of the technology. Technological environment has affected the

banking industry to a great extent. The major change that has been seen in Nepal Bank

Limited is that few years back, the bank was not computerized. But now it has been

computerized, out of necessity as well as due to competition given by other commercial

banks. The bank has become more efficient due to the presence of computerized system

and software. The transactions are operated through the server and it has increased the

customer satisfaction as well as employee performance. NBL has been able to provide the

facility of any branch banking system due to the technological change; otherwise it would

have been impossible to provide the facility of ABBS. Another major example of

technological change is the presence of instant ATM cards to customers for withdrawing

money.

Porter’s Analysis

An industry is comprised of a number of firms producing similar product or providing

similar services. Industry Analysis considers identifying and examining important

stakeholder groups in a corporation’s task environment. According to Michael Porter there

are five factors that determine the competitive position of a firm/industry and its ability to

generate revenue.

• Threats of new entrants

• Rivalry among existing firms

• bargaining power of buyers

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 33/65

• Bargaining power of suppliers

• Availability of substitute products

Threat of New Entrants:

Threat of new entrants is one of the forces defined by Porter as “Forces driving industry

profit”. New entrants to an industry are threats to existing firms because they enter the

industry with new strategies, resources and capacity.

Banking Industry in Nepal had high intensity of threat of new entrants. Banking industry

highly regulated in Nepal. However the number of banks and financial institutions seems to

be increasing every year. The number of commercial banks in Nepal is thirty one. New

commercial banks bring with them required capital investment, as per the regulation of

NRB. In addition, they bring new technology and better resources. In order to capture

market share and accumulate large deposits they practice market penetration strategy; that

is, they offer higher interest rates for deposits and lower interest rates for loans. NBL is

constantly facing the threat of new entrants in the industry and it had to increase its interest

rate and introduce new schemes to align with market competition. NBL has been trying to

keep up with the fierce competition.

Rivalry among Existing Firms:

Competition is aggressive in every profitable industry. Similarly, there is intense

competition among the banks. Commercial banks face competition, not only from other

commercial banks, but also from finance companies, development banks and co-operatives.

The rivalry among the firms in this industry is high. The banks are competing to increase

their profitability. The following factors can be observed in Nepali banking industry, which

leads to intense rivalry among the firms, according to Porter.

• Number of competitors: The number of competitors in Nepalese banking industry

is very large for economy like Nepal. There are 31 commercial banks till date.

Competitive move by one bank leads to similar actions and sometimes counter efforts

by other banks.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 34/65

• Product or service characteristics: The products and services provided by all the

commercial banks are almost the same. For example: ATM, evening counter, call

deposit accounts, lockers, documents for import, export and so on. Customers.

Moreover most of banks are located in similar locations.

• Height of Exit Barriers: Banks have a greater height of exit barriers. Banking

sector is highly regulated and banks cannot voluntarily leave the industry because they

have publics and governments money at stake.

Bargaining Power of buyers

For banks, buyers are the people who take loans or borrow from bank. Nowadays due to

competition bargaining power of buyers is higher than before. They demand lower interest

rate and flexible paying terms. To cater to the customer needs NBL has been providing

various kinds of loans.

Bargaining power of Suppliers

For banks, suppliers are the depositors. There is huge pressure on the bank to increase

interest rate as new banks are proving interest on general savings as high as 11%.

Depositors are very well-informed and educated this day, so their bargaining power is also

high.

Availability of substitute products

Substitute products are those products which are not alike but fulfill the same purpose.

Even finance companies and co-operative are providing services like commercial banks.

Customers nowadays have so many options on where to deposit their money or make

investment. Similar is the case while borrowing. The services provided by banks are highly

substituted.

SWOT ANALYSIS

An organization’s performance is highly determined by the environment in which it

operates. In order to survive and compete in hypercompetitive environment, Businesses

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 35/65

need to scan the external as well as internal environment. SWOT is one of the very

important analyses; any organization has to go through in order to analyze the Strengths,

Weaknesses, Opportunities and Threats. SWOT is an effective way to identify and analyze

strategic factors. The SWOT analysis of NBL is presented below:

Strengths of NBL

• NBL is a pioneer in Nepali Banking Industry and it has been providing banking services

in Nepal since its establishment in 1937 A.D. Therefore, NBL has a distinct recognition

in banking sector.

• NBL provides banking services even in remote areas and benefits from such

networking.

• NBL is a semi – government undertaking, thus less risky for depositors. NBL has public

faith and trust.

• NBL has experienced top- management. The Board of Directors is a five-member

committee, appointed by NRB. They provide good governance and support to the bank.

• NBL offers a wide range of products and services to compete with other banks and

improve its services with technological changes.

Weaknesses of NBL

• NBL is one of the banks with largest deposit base. Despite having huge capital,

NBL has not been able to exploit the opportunities.

• Centralized decision making in the organizational structure causes delay in decision

making.

• Least effort put into innovating new product and services according to the need of

customers.

• NBL has been quite slow in adapting to technological changes in the banking

industry, in comparison to other commercial banks.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 36/65

• Few opportunities provided to employees for development of their professionalism,

organizational orientation and career.

Opportunities for NBL

• NBL has the capacity to acquire latest banking technologies to position its premium

services and attract target new segments in the market.

• NBL can upgrade its non- computerized branches to computerized branches, in

order to enhance its networking efficiency and performance.

• It can improve its information system and upgrade the software to make the

operations more efficient, reduce down time and enhance networking.

• NBL has a huge deposit base compared to other commercial banks, despite of the

fierce competition in the banking industry. Thus, it has opportunities for investing in big

projects like hydropower, drinking water and national priority sectors.

•Since, NBL has a wide network; it can invest in small and medium projects in

remote parts of Nepal and serve niche markets like micro credit, alternative energy

sources like solar power.

Threats for NBL

• NBL faces the pressure of operating in a highly regulated sector.

• Establishment of several new commercial banks has lead to hyper competition in

the industry.

• Marketing penetration strategies undertaken by new banks and financial institutions

has reduced the spread of NBL.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 37/65

• Customers are aware and well informed about the infrastructures, interest rates and

value added services so NBL is obliged to provide high quality, customized servicesto

customers.

• Financial institutions like finance companies, cooperatives and development banks

providing more customized services, in competitive rates.

• Political, social and economic instability in the country is major threat to the

economy as well as banking sector.

Competitive Analysis

The organization’s competitive position in the market is determined by analyzing the rates

of deposits and loans as well as other services provided by the competitor banks. For

comparing the rates of loans, deposits and overalls profitability of NBL with other

competitive banks, we selected the following banks:

• Nepal Bank limited (NBL)

• Himalayan Bank Limited(HBL)

• Nepal Investment Bank Limited (NIBL)

• Rastriya Banijya Bank (RBB)

Table 2: Comparison of interest rates and profitability

Criteria NBL HBL NIBL RBB

Normal Savings 3.5% 5% 4.5% 3%

Fixed Deposit (1

year)

8% 9.5% 7.5% 7%

Term-loan 13-16.5% 16-17% 16% 13-14%

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 38/65

Overdraft 13-15% 15-17% 17% 13.5-14%

Net Profit 894,254,182 508,798,193 1,265,949,588 4,735,756,000

From the above data we can observe the following tendencies:

HBL provides the highest rate of interest rates in normal saving accounts and fixed deposit.

It makes up for its expensive deposit schemes by charging higher interest on loans, than

other banks. Though the interest rate on deposit and loans seems to vary according to the

banks, the spread is almost similar.

RBB has the highest net profit. HBL provides highest rate in fixed deposit accounts in

order to attract more amount of fixed deposit. HBL and NIBL have similar rates for loans,while NBL and RBB provide flexible interest rates on loans.

PART THREE

PRESENTATION OF MAJOR PROJECT

A study on the need of market segmentation and targeting at NepalBank Limited

Section I. Introduction

1. Introduction of the project

Nepal Bank Limited has been providing modern banking services in Nepali banking

industry for 74 years. It is one of the pioneers in Nepalese banking industry. Few decades

back, there were few banks and competition was very low. Most banks were concentrated

within Kathmandu valley and NBL was the bank which initiated branching outside the

valley and introduced banking to all segments of people all over Nepal. Since its

establishment, it accumulated huge deposits and retained its top position for a very long

time. However, due to rapid growth in the number of commercial banks, during the past

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 39/65

few years, NBL faced difficulty in retaining its customers. Moreover, it was unable to

attract new customers in comparison to the past. New commercial banks entered the

market with innovative products and services, advance technology, outstanding marketing

campaigns. They practiced market penetration pricing strategy by offering higher interest

rates on deposits and lower rates on loans in comparison to the prevailing market rates.

Since the switching cost for customers lowered, NBL lost many of its clients to

competitors. Nevertheless, NBL put least emphasis on marketing and promotions while

other banks continuously adapted to the latest marketing trends in order to reach to the

customers.

In this age of information, customers are bombarded with information. So, businesses put

their best efforts to reach their customers through marketing. Marketing is very important

to survive, compete and maintain valuable relationships with customers. The basic rule of

marketing is to segment the market and identify profitable segments to cater to the needs of

various segments, by innovating new services. Banking industry is a service industry and it

has huge potential to come up with innovative and creative services to stay ahead of the

competition and delight customers with value addition. For this, the most important thing

for a bank is to know “who are its customers?” and “what are their needs?” The bank needs

to segment the market into various segments and develop new products and services

according to the need and interest of the segments. The bank should identify profitable

segments and niches which are not served and focus on such segments to generate higher

profits. The bank should design its products and services through customer driven

marketing strategy. This project is a small effort to study the need of market segmentation

and targeting at Nepal Bank Limited.

2. Objectives of the project

The objectives of the project are as follows:

• To study the need of market segmentation in NBL, for marketing its services

effectively.

• To determine which customer segments exist in the customer base of NBL.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 40/65

• To determine the demographic, socio-economic and behavioral characteristics of

existing and potential customers in the banking industry.

• To identify the market segments with unmet needs that products and services of

NBL could meet.

• To identify how NBL should position its services to reach target segments.

• To find out the suitable means of communication for different target segments

• To find out which new services should be developed to generate higher profits from

potentially profitable target segments.

3. Scope and limitations of project

Scope

Scope of the project is to study the need of targeting and segmentation at NBL. Analysis of

segmentation and targeting is quite important in today’s context to build strategies and

develop new product and services according to the needs of various customer segments in

the market. This project’s study will be helpful for the bank to identity various segments,

their characteristics, their preferences of existing as well as new services, their preferred

means of communications to receive bank’s information, preferred time for visiting the

bank and their attitudes towards social welfare activities of the bank.

Limitations

The major limitations of the project undertaken are as follows:

• The findings and conclusions are made on our own analysis of primary and secondary

data.

• The research was carried out on small scale and we had limited access to information

and resources, therefore the result may not be relevant if generalized on a large scale.

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 41/65

• We had limited time to conduct the research in-depth.

• The customers were unwilling to invest more time and hesitant to provide more

information.

• In certain circumstances we had to make simplified assumptions to the complex

situation in absence of reliable and relevant information.

SECTION II: CONCEPTUAL FRAMEWORK

1. Review of related literature

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 42/65

This section portrays knowledge, understanding and definition about the subject matter

derived by reviewing the concepts from text books, related articles, theories and other

reliable sources of references.

Market is composed of various customer groups having distinctive needs, preferences, and

characteristics. Market is no more a place where the same products and services can satisfy

all the customers. Due to such heterogeneity in the markets, companies have accepted the

fact that, it is impossible to please all the customers with same products and services. So,

companies focus on developing customer driven marketing strategies to reach the

profitable segments in the market by designing appropriate marketing strategies.While

building customer driven marketing strategy, marketers plan the marketing mix. Marketing

mix is one of the modern concepts in marketing. Service marketing mix consists of

marketing elements like product elements, place and time, price, promotion and education,

process, physical environment, people, productivity and quality. These elements are

controllable in nature and defined by the marketers. Similarly, marketers have to emphasize

customer driven marketing strategy. It consists of decisions like how to divide the market

into significant customer groups, selecting the customer groups to be served, designing and

creating products and services that best serve the target customers and positioning the

products and services. Marketing is a process by which companies create value for

customers and build strong relationship with the customers to capture value from

customers. However, it is important for marketers to understand and develop suitable

marketing strategies for various customer segments with differing characteristics and

needs. The initial step in designing customer driven marketing strategy is to segment the

market. Market segmentation is the process of dividing the market into smaller groups with

distinct needs, characteristics and behavior. These consumer groups may require separate

products or marketing mixes. (Philip & Gary, Designing a Customer-Driven Marketing

Strategy, 2008)

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 43/65

Banking industry is one of the most competitive industries in Nepalese economy. It is a

smaller market with many firms competing with each other to capture more market and

claim more customers. So, marketers of banking products and services have to understand

that they cannot appeal to all the customers in the same way because customers vary in

demographic, psychographic, geographic, and behavioral attributes. In order to market

banking services effectively, it is important to identify market segments, select one or more

segments, developing services and marketing programs customized for each segment.

A market is made up of various different customer groups with different characteristics.

The heterogeneity in the customers makes it very difficult for the marketers of banking

services to market their service effectively. Therefore marketers segment the consumer

markets into various different segments. A market segment is made up of a group of buyers

having common characteristics, needs preferences and status. The purchasing behavior and

consumption patterns of each segment differ from the others. Effective segmentation helps

in identifying various customers and prospects into segments so that the relevant

characteristics within each segment and the dissimilarity between segments can be

measured. After segmenting the market the marketers select target segments to market their

products and services effectively. Marketing the products and services to the target

segments with appropriate marketing strategies helps in effectively reaching the profitable

customers. (Christoper & Jochen, 2004)

Markets can be divided into various segments with various attributes. The most common

basis for segmentation could be demographic, geographic, psychographic and lifestyle,

media and price segmentation. Demographic segmentation helps in segmenting the market

according to various demographic variables like age, gender, income, education level and

so on. It is very important because the characteristics and behavior of various demographic

groups tend to vary. Similarly, geographic segmentation divides the market or consumers

into various geographic regions. Such segmentation is useful for businesses operating in

different parts of the country or world. The values, culture, preferences and needs of

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 44/65

consumers vary according to the geographic area. Another important segmentation factor is

psychographic and lifestyle segmentation. Psychographic and lifestyle segmentation is

based on consumer attitudes, behaviors, emotions and interests. It focuses on values and

beliefs of the consumers. In order to locate such segments, qualitative segmentation

becomes very important. Similarly, media segmentation is based on the difference in media

to reach different customers while price segmentation segments the market according to the

price attributes of products and services. (market segmantation)

Marketing banking services poses a challenge amongst the marketers because unlike

consumer products and commodities, services have mostly intangible aspects. The service

quality is difficult to evaluate and the service cannot usually be experienced beforehand. So

it is difficult for marketers to determine what services to provide and what level of services

to provide to various customers. Thus the need for segmenting the customer market is

important for banks to identify profitable segments in the market and develop appropriate

products, services and strategies to market the services effectively.

Customers of service industry like banks differ in various attributes and are widely

scattered. So, bank must evaluate a segments size, growth and profitability and design

services by targeting those customers. Market segmentation provides better results than

simply offering same service to all the segments. Not catering to the real needs of various

customer groups can result in customer switching to other banks and loss of brand value.

Customers feel that they have least options to choose from and their needs being ignored.

Moreover segmenting the market helps the bank in finding out the profitable segments and

their unmet needs. In order to create value for targeted customers, bank should further

differentiate the services and position the services so that it occupies distinctive and

advantageous position in target customers’ minds, in comparison to competitors’ services.

The bank can develop new services, upgrade old ones or bring changes to the existing

services so as to provide superior value to the customers and delight them. Bank can also

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 45/65

add value proposition to its products and services and communicate the value proposition

in the market.

SECTION III: METHODOLOGY

Research methodology is the well formulated plan for carrying out the research. This

research was carried out by following the steps and procedures prescribed in marketing

research text book.

1. Problem Definition

Management decision problem

Is it necessary to segment customers in banking services?

Marketing research objective

To study the need of market segmentation and targeting for Nepal Bank Limited.

2. Research design formulation

This research was conducted as exploratory research to get insight about the need of market

segmentation and targeting in NBL to market its services effectively. For this research, we

needed information about the potential and existing customers. We also needed the

information about the current marketing plan of the bank and efforts made on promotion of

products and services. Similarly, we required the list of products and services currently

offered by the bank and products and services to be launched in near future. The most

important information was to discover whether market segmentation and targeting is

important to market banking services effectively.

Nature of the data

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 46/65

The data collected from various sources can be categorized into two parts.

Primary Data

• unstructured interviews with customers of bank

• unstructured interview with top-level employees of NBL

• Questionnaire survey

Secondary Data

• Information from website of the bank

• Published articles and journals

• Internet articles related to segmentation and targeting

• Annual reports of competitive banks

Secondary Data Analysis

To gain a brief insight about our project we referred to the website of NBL (nbl.com.np).

We obtained information regarding

• Deposit ( current ,saving, fixed)

• Loan/ Advances( consumer, corporate)

• Remittance

• Other services (Safe deposit vaults, ABBS, Internet Banking, ATM)

3. Methods of collecting data

Questionnaire Survey

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 47/65

We designed a questionnaire to collect primary data. This questionnaire consisted of open

ended, multiple choice, and dichotomous questions. The questionnaire was made up of

twelve questions which briefed about the most obvious customer segments of the bank.

Rest of the questions was directed towards the needs, preferences and behavior of various

customer groups. The questionnaire had questions regarding factors considered by

customers while banking, the services mostly used by the respondents, time preferred by

the customers to visit the bank, preference of communication media, and importance of

social responsibility of bank. The results from the survey helped us to understand the

attitude, preferences, and attributes that are regarded valuable by different segments of the

customers. Questionnaire survey is presented in Annex-2.

Interview

Direct communication and interaction with the customers of NBL during our internship

help us to discover real problems, preferences, and needs of the customers. We interviewed

20 customers of the bank so that we could come up with appropriate questionnaire. The

customers were from various age groups. After the questionnaire was formulated, we

interviewed 8 customers of the bank for any required additions and amendments in the

questionnaire. We also contacted customers over the telephone to get required information

about the aspects of the bank’s services which customer value.

Information from websites

We collected information regarding various services provided by NBL and other

competitive banks like Himalayan Bank Limited, Nepal Investment Bank Limited and

Rastriya Banijya Bank to compare the interest rates offered by these banks. We also

reviewed articles related to segmentation and target in the internet so that we could learn

about different types of segments in the banking service industry.

4. Sampling process and sample size

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 48/65

For collection of data for our research, we used sampling method. We used simple random

sampling and the sample size was 150. The sample we selected consisted of random people

in the market. Some of them were existing customers of NBL. This method was

appropriate for us not only because it was economical and least time consuming, but it also

provided us unbiased and accurate data for our research. The sample for our study was

quite representative of the population because it consisted of people from all age groups,

we had pre determined, Similarly, there were respondents from various occupations,

students, homemakers and unemployed. The respondents also had varied income scale.

5. Data preparation and analysis

The data we collected from the survey was processed through Excel. Further, it was

analyzed and interpreted using statistical tools like frequency distribution, methods of

central tendency and statistical diagrams. The questionnaire forms were inspected and

edited and the data was processed in Excel for further analysis.

Section IV: Presentation and analysis of the project

1. Analytical presentation of the project

Our project was to determine the need of market segmentation and targeting for Nepal

Bank Limited, to market the services more effectively to the target customers. Market

segmentation is important to services organization like banks due to the large number of

existing and potential customers, the existing and potential customers are divided into four

segments on the basis of gender, age, income and occupation. The segments were identified

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 49/65

by observing the actual customers in the bank, during our internship. However, there are

other segments in the market for banking services, which we have not considered for this

study.

In order to study the profitable segments and position the services to reach these segments,

we conducted a survey focused on segmentation and targeting the market. The survey

consisted of questionnaire and unstructured interview with the customers of bank. The

questions were focused on the preference of various services and service attributes, by

different segments. The questions provided an insight towards the most profitable segment

and segment with greater potential to increase the bank’s customer base and profitability.

We asked questions regarding the services they currently used most, new services they

would be interested in, appeal of corporate social responsibility, their preference of time for

visiting the bank, preference of communication media to receive information about the

banking services and so on.

Presently in NBL there are few products and services targeted towards some segments in

the market. NBL has deposit schemes like Women Special Savings which provides higher

interest than normal savings; Senior Citizen Special Savings is meant for senior citizens

who are mostly retired and look for reliable and trustworthy institution for placing their

savings and income. NBL has not reached most profitable segments in the market. It has

two deposit schemes that are targeted to actual segments in the market. The bank offers the

same products or schemes and services of all the customers. Similarly it tries to reach all

the customer groups with the same message through the same media.

a. Service attributes valued by customers

Fig 1: Factors considered by customers while transacting with bank

Banking industry is a very competitive industry in Nepal. Commercial banks are struggling

to retain their market position and attract new customers as they are competing not only

with the players of the same industry but also from other financial institutions like

8/2/2019 Internship Report Final Himalayan

http://slidepdf.com/reader/full/internship-report-final-himalayan 50/65

development banks, finance companies and co operatives. So, it is very important for bank

to differentiate itself from the competitors and add value to its services.

In the survey conducted, the respondents were asked what factors they paid more

importance to, while transacting with a bank. The survey result showed that 31% of the

respondents gave more importance to convenience. Convenience refers to the location of

the bank, the flexibility in providing services and time of delivering the services. Similarly,

28% of the respondents think that quality of customer services is an important attribute in

banks. 24% of the respondents emphasize trust factor, considering the incidents that has

been taking place in a few banks recently. Finally, 17% of the respondents think that they

consider networking of a bank, while transacting with it.

From the survey, we can see that customers put more emphasis in convenience of a bank, in

providing services to the customers.

b. Importance of Corporate social responsibility versus interest rates

Fig 2: Importance given by customers to corporate social responsibility

In our survey we had given various options for customer to choose their saving account.

There were three options which contribute something to the environment, old age homes,

underprivileged children and one that provide slightly higher interest than other accounts.

Our survey result shows that CSR increases the appeal of deposit schemes; however bank

cannot ignore the interest factor, which has a major influence on decision making by

customers.

Nowadays customers are becoming more responsible and aware about the social issues and

they want institutions like banks to contribute something to the society. Therefore what

bank can do is coming up with schemes that actually make a positive impact in the society

so that customer get positive image about the bank. The survey results showed that

customers value corporate social responsibility of banks to a great extent. Results showed

that customers would be happy to contribute to the old age homes, underprivileged children

and environment. Higher interest rates on savings accounts and other accounts would

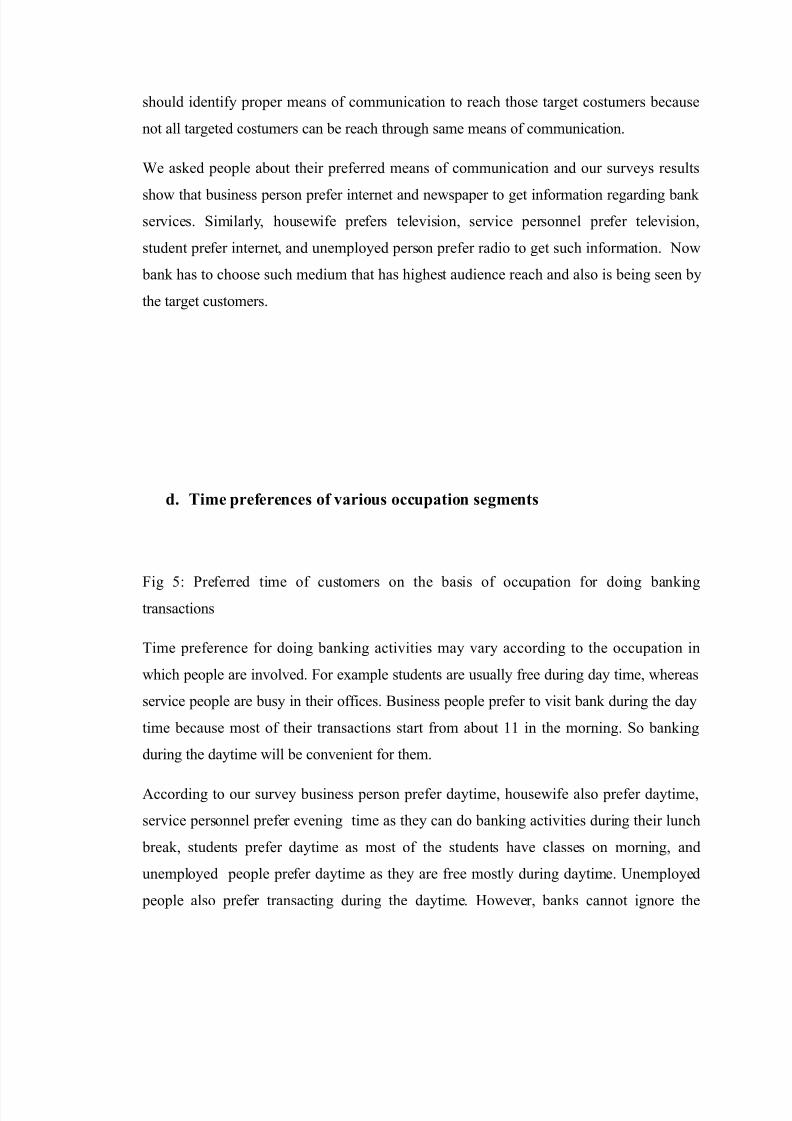

8/2/2019 Internship Report Final Himalayan