Embed Size (px)

Citation preview

www.dbsvickers.com

ed-JS / sa- AS

Think it, Get it: Services to Eclipse Products

Internet of things (IoT) will revolutionise businesses, like the Internet in the 1990s. Smart city programs will accelerate IoT adoption in Asia

Service (not hardware) companies will grab over 80% of IoT spending.

Lion’s share of IoT spending will come from businesses with consumers paying < 25%

IoT will help product companies to transform into service companies. The first wave of Information Technology (IT) in the 1960s and 70s automated the value chain of enterprises. The second wave which was the Internet in the 1990s led to global supply chains. The third wave of IoT is creating smart, connected products. For the very first time, vendors are able to track their products and maintain relationships with customers even after the sale. With IoT, product companies are in a position to launch new services and generate recurring revenue streams.

Smart cities to accelerate IoT adoption in Asia. We expect South Korea and Singapore to be among the global leaders in adopting IoT. Singapore is leveraging on its Smart Nation program to resolve challenges in the utilities, transport and healthcare space. China plans to build 202 smart cities to cope with rapid urbanisation. In fact, Asian enterprises are ahead of their US peers in IoT adoption. Consumer electronics players like Samsung and LG target for 90% of their products to be IoT-capable by 2017.

Where to focus in the IoT value chain? IoT services – akin to brain of IoT - will comprise over 80% of revenue. We expect businesses to account for over 75% of spending on IoT services in pursuit of launching new services and reaping savings. Telcos may see marginal benefits as most IoT data will traverse over Wi-Fi or Bluetooth. Bigger opportunities lie in providing industry specific solutions, cloud Infrastructure and security capabilities.

Stock picks. We like ST Engineering for its potential to secure contracts from Smart Nation project. Keppel DC REIT will benefit from demand for data centers. ZTE will benefit from smart cities in China. Kingdee will ride on adoption of cloud based ERP solutions while Wasion will benefit from growth of Smart Grid in China.

HSI: 22,640.04 STI : 2,998.35 Analysts Sachin Mittal +65 6682 3699 [email protected]

Regional Research Team Business models to shift with Internet of Things

Advanced

Tran

sactional

Product

Premium Product

Service

Platform

Basic

Relational

IoT Capability

Customer Relationship

Source: DBS Bank Key companies with exposure to IoT

Source: DBS Bank; DBS Vickers

DBS Group Research. Equity 2 Nov 2015

Regional Industry Focus

Internet of Things & Smart Cities

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price Performance (%)

30 Oct 15 US$m 3 mth 12 mth Rating

S$ ST Engineering 3.31 7,330 3.60 0.91 -10.78 BUY Keppel DC REIT 1.05 658 1.14 -3.69 nm BUY 800 Super 0.49 62 NR 1.03 2.08 NR Vicom 6.04 388 NR -1.61 3.03 NR HK$ Wasion 8.64 1,145 12.50 (18.80) 7.20 BUY Kingdee 3.37 1,266 3.80 (7.76) 26.88 BUY ZTE 18.96 11,926 24.00 6.48 22.62 BUY

Regional Industry Focus

Internet of Things & Smart Cities

Page 2

Analyst Sachin Mittal +65 6682 3699 [email protected] Tsz Wang TAM CFA +852 2971 1772 [email protected] Suvro SARKAR +65 6682 3720 [email protected] Patricia YEUNG +852 2863 8908 [email protected] Paul YONG CFA +65 6682 3712 [email protected] Ling Lee Keng +65 6682 3703 [email protected] Chris KO +852-2971 1707 [email protected]

Table of contents What is IoT 3 Monetization Model for IoT 4 Size of IoT Opportunity 6 Value Chain of IoT 8 IoT Adoption in Asia 10 IT Spending Breakdown 13 Singapore Smart Nation Project 14 China – Smart Cities 19 Companies Exposed to IoT 20 Appendix

Potential impact on various sectors 23

STOCK PROFILE 28

ST Engineering 29

Keppel DC Reit 32

800 Super Holdings 37

Vicom 39

Wasion Group Holdings 41

Kingdee 44

ZTE 47

Regional Industry Focus

Internet of Things & Smart Cities

Page 3

What is IoT? IoT is a network of things that are connected to each other and refers to an ecosystem comprising of things, connectivity and services including data analysis. 1) The thing (a sensor embedded in the product) has

some intelligence to sense changes around it.

2) Connectivity is also referred to as Machine-to-Machine (M2M) connectivity via cellular, Wi-Fi or Bluetooth etc.

3) The service is usually hosted in a remote location away from the thing. This can be a cloud infrastructure along with specific applications and data analytics. The service portion is likely to be the largest portion of the IoT pie on our estimate.

3 parts- Things, connectivity and Service

Source: Gartner (December 2014), DBS Bank Why IoT now? The growth in IoT-enabled devices has been fueled by the declining cost of sensors, connectivity and data processing power. Smart phone revolution has resulted in a big scale of production for these components, bring down the cost of components required for IoT. The software needed to analyze this data has improved gradually and companies are using it to boost operations and seek out new business models.

High smart phone volumes have driven down costs, paving the way for cheap IoT sensors

Source: DBS Bank According to an article published in Harvard Business Review (HBR) in Jan 2015, there have been 3 waves of IT so far. Wave 1 in 1960s and 70s – IT automated value chains such as order processing and billing Wave 2 in 1990s – Internet enabled connectivity made supply chains global and efficient Wave 3 Now – Embedded sensors resulting in smart, connected products for the very first time. Unlike the previous waves of IT transformation that boosted productivity, this wave will change the structure of industries. Smart, connected products will blur the boundaries within an industry and change the basic principles of product design. IoT will force vendors to standardise their products. For example, a patient’s home health monitor needs to talk to the hospital’s health informatics system which will require coordination on technological and product levels. Similarly, in the farming sector, when a tractor manufacturing company goes into smart, connected tractors, its product should be able to talk to irrigation systems, weather data systems and seed optimisation databases. This can be achieved through deep co-operation during product development. This is precisely the reason that Governments and big enterprise customers have an important role to play in standardising IoT protocols across the entire range of products in a sector.

Regional Industry Focus

Internet of Things & Smart Cities

Page 4

Monetization Model for IoT Business Models to shift under IoT

Source: DBS Bank Premium Product In this model, a vendor charges a premium price for the connected features of the product. An example is LIFX which produces remotely programmable LED light bulbs that can be controlled through a smart-phone app. These bulbs are sold at a premium due to this differentiation. Service Provider In this much desired model, a vendor converts what has been a traditional product into a service, builds a relationship with the customer even after the sale of the product and generates recurring revenue stream. For example, Volkswagen’s “Car-Net” service offers security features, maintenance assistance, and navigation tools to its customers for a subscription fee of US$17.99/month. With this, automatic crash notifications can be sent to chosen contacts when airbags come into use in the vehicle. A classic example of new service revenue for enterprises is Rolls-Royce who instead of selling aero engines, now contracts with many of its customers for "power-by-the-hour". Rolls-Royce is able to deliver this service due to remote monitoring and use of big data analytics on parameters such as pressure and temperate etc.

Another example of service revenue is smart thermostat manufacturer Nest (acquired by Google in 2014 for US$3.2 billion) who uses its Learning Thermostat — a home automation and energy management product — as a platform to offer energy management services to utility companies Nest charges utility companies US$30 to US$50 per thermostat annually for its service. Nest automatically reschedules usage of equipment with high electricity consumption such as air conditioners to avoid outages during the peak hours. By doing so, it has been able to reduce overall electricity requirement by as much as 50% in peak times. Platform provider In an ecosystem, the focus is not on selling a product or a service, but on providing a shared platform to other players in the ecosystem – hardware manufacturers, software developers, service providers. The platform provider ideally makes money from both end customers as well as other platform users. Platform users pay for listing and the platform provider also gets a share whenever a product is sold to the end customer on the platform. SmartThings sells its own products and services while creating a platform for other IoT companies to sell their services. SmartThings has a smartphone app that is used to control its hub and all of its connected devices. Various products that the company sells as part of the platform include locks, switches, environment sensors, alarms etc. SmartThings offers design guidelines to developers who want to make products for its platforms. SmartThings works with partners such as Belkin and Phillips, and on operating systems such as Android and iOS. According to popular technology review website - CNET, Over 1,000 devices and 8,000 applications have been made till August 2014 when the company was acquired by Samsung Electronics for approximately $200 million.

Advanced

Tran

sactional

Product

Premium Product

Service

Platform

Basic

Relational

IoT Capability

Customer Relationship

Regional Industry Focus

Internet of Things & Smart Cities

Page 5

Examples of new service launch by product companies with the help of IoT

Source: Companies, DBS Bank

Service Benefits to Customers and Vendors

Video analytics service by a telecom service provider

Businesses can gain insights into customer’s in-store behaviour without having to pay any upfront cost to buy the product. Singtel offers the cloud based Video-Analytics solution for the retail industry on a monthly subscription basis. The service leverages analytics to extract information such as age, gender and emotions from video images.

Instant Ink service by a printer manufacturer

Customers benefit from higher usage of the printer. HP Instant Ink program allows customers to subscribe to a monthly service that enables the customer to print a fixed number of pages through their printer. A sensor is installed in the printer to detect when the printer will run out of ink and HP will mail the customer with an ink cartridge before the printer runs out of Ink. The monthly charge is inclusive of the ink cartridge, shipping and recycling of ink cartridges.

Pay by flight hours service by a jet engine supplier

Customers benefit from lower downtime and don’t have to pay any upfront cost to buy the equipment. Rolls Royce introduced “TotalCare”, a suite of predictive maintenance and repair services for its jet engines. Customer pays Rolls Royce based on the number of flight hours the engine is used for and Rolls Royce takes the responsibility to maintain and improve the durability of its engines.

Remote monitoring service by a turbine manufacturer

Customers enjoy greater flexibility with access to services provided by experts while saving downtime and maintenance costs. General Electric (GE) has opened facilities around the world to provide real-time monitoring and diagnostic services for its global base of gas turbines and compressors. A combination of sensors and control devices capture data about the performance of the equipment which is transmitted to these facilities where maintenance and repair needs are monitored and scheduled.

Mobility as a Service by an auto maker

Addresses customer’s logistics problems and provides them with easier access to the vendor’s offering. Daimler AG, the German multinational car manufacturer launched Car2Go, a car sharing program which allows customers to locate and use vehicles provided by Daimler for their journeys. The customer is charged per minute for the use of the vehicle while all fuel and maintenance charges are borne by the vendor.

Regional Industry Focus

Internet of Things & Smart Cities

Page 6

IoT Market Opportunity

Gartner forecasts installed base of 25 billion connected things in 2020 compared to 4.9 billion in 2015, representing 33% CAGR. This excludes smartphones and PCs, but includes dedicated objects, such as vending machines, jet engines, connected soap dispensers etc. In terms of annual shipments, Gartner forecasts 1.6 billion connected things in 2015, rising to 8.3 billion in just five years in 2020. The highest volume shipments are expected to come from connected LED interior light bulbs followed by smart TVs and automotive infotainment systems. By 2020, over 80% of IoT supplier revenue will be from services The incremental cost of hardware and software is relatively small while the services opportunity (including data analytics) is much larger. Gartner forecasts IoT will support total services spending of US$69.5 billion in 2015 rising to US$263 billion by 2020 at 23% CAGR.

IoT connectivity opportunity (part of service revenue) will be relatively small At US$32 billion in 2020, the opportunity for IoT connectivity services is just 12.3% of total IoT service opportunity. As the revenue base of telecom service providers’ fixed and mobile revenue is large, it will translate to <3% of their total revenue according to Gartner. Very few IoT connections may go through the SIM-based cellular networks and most of the devices will be connected over free networks such as Wi-Fi and Bluetooth, ZigBee etc provided by IT companies and engineering teams of customer organizations. Telcos are expected to charge only US$1-3 for each cellular connection, which is much lower than smart phone connections. Connected cars, smart electric meters, remote patient monitoring and outdoor security cameras will be top applications for telcos.

Gartner IoT related service revenue forecast

Source: Gartner (Dec 2014)

Regional Industry Focus

Internet of Things & Smart Cities

Page 7

IoT solutions opportunity (part of service revenue) will be significant At a size of US$231 billion in 2020, the IoT solutions opportunity will be much bigger than connectivity. However, this will require IoT players to provide (i) industry specific solutions to enterprises helping them either launch a new service or reduce cost. (ii) Services such as security, health monitoring services etc to consumers and charge a monthly fee. Enterprises to account for over 75% of spending on IoT services Gartner forecasts consumer services to account for 24.7% of IoT service revenue in 2020 with enterprises accounting for the bulk. Enterprises will be big adopters of IoT so that they (1) sell new services to their customers (both enterprises and consumers) (2) lower their costs by reducing downtime of their equipments and supply chain costs. IoT adopters to reap 6-7x more benefits than IoT suppliers. Gartner forecasts that IoT will produce close to US$1.9 trillion of economic value-add in 2020. Economic value-add for a sector is essentially the sales in that sector minus inputs and supplies from other industries.

For example, manufacturing sales minus the cost of raw materials and energy will be the economic value- add for the manufacturing sector. IoT will also facilitate new business models, such as usage-based insurance calculated based on real-time driving data. The banking and securities industry will continue to innovate around mobile and micro-payment technology. IoT will also support a large range of health and fitness devices and services, combined with medical advances, leading to significant benefit to the healthcare sector. Emerging connected sensor technology will lead to value creation in diverse areas such as utilities, transportation and agriculture. Most industries will also benefit from the generic technologies, in that their facilities will operate more efficiently through the use of smart building technology such as connected LEDs and heating, ventilation and air-conditioning (HVAC) systems. McKinsey Global Institute has even higher projections. McKinsey predicted in 2013 that IoT would improve global productivity by between US$2.7 trillion and US$6.2 trillion annually between 2013 and 2025. McKinsey believes 80% to 100% of all manufacturers will be using IoT applications in 10 years.

Economic Value-Add by Industry Sectors in 2020

Source: Gartner (Dec 2014)

Regional Industry Focus

Internet of Things & Smart Cities

Page 8

IoT Value Chain

Source: Arthur D Little Smart Module – Smart modules combine the radio, sensor and microcontroller, integrate it with storage, and make it “insertable” into a device. Radio/communications chips provide the underlying connectivity, sensors provide much of the data gathering, micro-controllers provide the processing of that data. Intel and Qualcomm are leading chip makers for microcontrollers and radios respectively. Leading sensor manufacturers are companies such as InvenSense, STMicroelectronics, Bosch, NXP, Freescale etc. Smart Object – The smart object is the product – a refrigerator, a vending machine, a car, etc. – that its manufacturer has designed to be able to connect to others via its smart module and a network. Network Operator - The network operator enables and manages fixed or wireless communication with a smart object using cellular or non-cellular technologies such as Wi-Fi, or smart objects can be connected with each other via Bluetooth, ZigBee etc without the operator. Service enabler or Platform provider – The platform provides the underlying management and billing capabilities to IoT (such as Android OS to mobile). It also manages the multitude of partners that offer third party applications that run on the platform (e.g. for vehicle tracking), in a way that is similar to how an app store is managed. Apple, Google, Intel, Qualcomm, IBM, Amazon, HP, SAP etc are vying to be platform providers as this part captures the maximum value in the value chain.

IoT platform at the centre of the value chain There are multiple players trying to promote their platforms to attract more developers to come out with new innovative solutions. 1) Smart Home - Apple’s HomeKit, Google’s Brillo,

GE Wink, Smarthings etc.

2) Smart Healthcare - Apple’s HomeKit, Google Fit, Samsung SAMI, Human API etc.

3) Smart Car - Apple’s Carplay, Google’s Android Auto, Microsoft’s Windows in the Car, Ford’s Applink etc.

Sectors like utilities (smart metering), industrial applications and smart cities present attractive business opportunities despite the lack of standardised IoT platforms. These applications focus mostly on solving well-understood needs for known customers. As such, a universal platform supporting innovative services is not essential to provide smart city services as long as various government agencies in a city/country use a single platform. System Integrator –The smart object has to be integrated with the platform and its relevant applications. In most cases today, this integration is cloud-based, meaning that a chosen application platform will support the integration through standardised application programming interfaces (APIs) as a consequence. All large system integrators, such as Ericsson and IBM, are entering this territory, which used to be dominated by smaller regional players.

Regional Industry Focus

Internet of Things & Smart Cities

Page 9

Service Providers – They brings together the hardware, the connectivity and the platform to provide end-to-end solutions to different verticals. Most importantly,

they take care of bundling the solutions, setting the tariffs, billing and customer care.

Some of the popular categories by Shipments in 2020

Source: Gartner (Dec 2014) Connected LED lights, smart TVs, auto infotainment, smart meters and thermostats will be top IoT products. Gartner forecasts that the highest volume will come from connected LED interior light bulbs for business applications in 2020 followed by smart TVs and automotive infotainment with increased availability of online on-demand content.

Smaller-volume consumer items such as networked thermostats, which enable analytics-based advice for energy-saving programs as well as remote controls would also be highly in demand.

Regional Industry Focus

Internet of Things & Smart Cities

Page 10

South Korea and Singapore are expected to be among Top 5 global markets to adopt IoT

*Bubble size represents 2020 GDP size Source: AT Kearney IoT Spending in Asia Pacific Frost & Sullivan estimates that total spending on IoT in the Asia Pacific was US$10 billion in 2014, which will grow at a CAGR of 34.1% to reach US$59 billion by 2020. Asia Pacific is characterised by a large presence of manufacturing economies which is expected to drive spending on IoT applications in telematics and supply chain visibility. IoT spending in the manufacturing industry is expected to be one of the fastest growing markets in Asia Pacific, growing at a rapid CAGR of 52.7% between 2014 and 2020. Adoption of IoT is not without its challenges, as there are several hurdles that could prevent it from achieving rapid growth. Security and information privacy are some of the largest hurdles to the adoption of IoT. With smart and connected devices embedded in business processes and tied to critical functions, the ability to negatively affect enterprises and individuals is increased significantly.

IoT Adoption in Asia Pacific Gartner’s survey found APAC companies more aggressive in IoT adoption. According to a Gartner Survey, APAC respondents generally expect IoT to have a greater long-term impact on their organisations than respondents in other regions. We believe this attitude is partly because some Asian organisations tend to conduct very long-term strategic planning and partly because some of the respondents may come from smaller and more agile organisations. North America lags in terms of IoT impact. This may partly be a consequence of some respondents coming from larger and less agile organisations. Forrester survey puts Asia Pacific ahead in IoT adoption. Below are the findings of a recent global study done by Forrester Consulting on IoT implementation in various enterprises. In Asia Pacific, 58% of enterprises are either implementing or planning to implement IoT over the next 24-months versus only 45% globally.

Regional Industry Focus

Internet of Things & Smart Cities

Page 11

Expected Long-Term Impact of IoT by Region

Source: Gartner (Feb 2015) IDC survey also puts Asia Pacific as a leader in IoT adoption. Market research firm IDC shared the results of its survey of 2350 IT and business decision makers in (mostly) large and medium-size enterprises worldwide in 2015. According to the survey results, enterprises in Asia Pacific are leaders in IoT adoption. B2B is considered by survey participants as the

area where IoT will grow, a reversal from last year where a majority of survey participants thought that consumer IoT is where the action will be.

Shift in the location of processing the data: More

survey participants this year will process the data generated by IoT sensors at the ”edge” rather

than in the data center, a reversal from last year’s survey.

Top drivers for creating an IoT strategy: Increased

productivity (14.2%), time to market (11.8%), and process automation (10.1%). Top challenges for the IoT: Security, upfront costs, ongoing costs.

IoT is anyone’s game in 2016: Hardware and

networking vendors have lost ground in their perception as “leaders,” while software vendors, analytics vendors, and device/component vendors have gained in terms of market awareness/ perception.

IDC survey on IoT

Source: IDC

Regional Industry Focus

Internet of Things & Smart Cities

Page 12

Short- and Long-Term Impact by Industry – Impact will be higher on Utilities, Transportation, Retail and Manufacturing sectors over the next 3 years

Source: Gartner (February 2015) According to Gartner’s survey, respondents expect the utility sector, followed by transportation, services, manufacturing and retail to be impacted the most by IoT in the short term (<3 years). In the long term (>5 years), they expect the highest impact to remain on utilities, followed by retail and manufacturing.

Surprisingly, respondents do not see much potential in transport and services in the long term despite good short term potential. This could be explained by the fact that these industries have already invested in tracing and telemetry services.

Regional Industry Focus

Internet of Things & Smart Cities

Page 13

IT Spending Breakdown IT spending by Sector, worldwide, 2013-2019

Spending (Billions of Dollars)

2013

2014

2015

2016

2017

2018

2019

CAGR (%) 2014-2019

Data Center Systems 164 168 169 172 174 176 177 1.1

Software 297 314 312 332 353 375 400 4.9

Devices 677 694 658 659 665 673 681 -0.4

IT Services 937 955 919 955 996 1,039 1,087 2.6

Communications Services 1,605 1,606 1,495 1,499 1,527 1,551 1,572 -0.4

Overall IT 3,680 3,736 3,555 3,616 3,714 3,815 3,917 1.0

Growth (%)

Data Center Systems - 2.6 0.9 1.5 1.2 1.2 0.8 -

Software - 5.7 -0.7 6.2 6.4 6.4 6.5 -

Devices - 2.5 -5.1 0.1 1.0 1.1 1.2 -

IT Services - 1.9 -3.7 3.9 4.2 4.4 4.6 -

Communications Services - 0.1 -6.9 0.2 1.9 1.6 1.3 -

Overall IT Growth - 1.5 -4.9 1.7 2.7 2.7 2.7 -

Source: Gartner (Oct 2015) Enterprise software is the fastest growing segment. Gartner expects key applications such as digital commence, marketing and sales software to be the key drivers. We believe that cloud services and data analytics are two key reasons for enterprises to spend more. Traditional on-premise application providers are being disrupted by cloud service providers. Meanwhile, increasing unstructured data and rising adoption of big data analytics is another key driver. IT services is the second fastest growing segment. Many of the developed markets are shifting toward next-gen social, mobility, analytics and cloud (SMAC) solutions. IT outsourcing demand especially in Europe is expected to increase over the next several years in order to cut costs. Moderate growth in data centre systems. The stagnating servers and storage market due to disruptive technologies, such as cloud computing and software defined storage, will lead to moderate growth in data center systems.

Network refreshes will fuel demand for network equipment. We believe that network equipment companies are better prepared to handle transition to cloud. Devices sales are likely to decline. PC and tablet market continues to weaken with spending declining by 9.6% in 2015. On the mobile phones, Apple’s high end phones continue to do well while Android growth is slowing due to lower replacement activity from higher life of smartphones. Communication services sales may decline as well. The abolition of roaming charges in the EU (due to regulation) and the elimination of roaming charges in parts of North America (due to competition) are key concerns. This could be partially offset by communication providers seeking additional revenue from IoT connectivity and value based pricing.

Regional Industry Focus

Internet of Things & Smart Cities

Page 14

Singapore’s Smart Nation Project Singapore’s Smart Nation Programme will harness IT, networks and data to raise standards of living, productivity and responsiveness to people’s needs and aspirations. Smart Nation will rely on IoT and big data. Singapore’s small size will help in standardisation. Many would consider Singapore’s small size a disadvantage in some areas but it gives Singapore an edge in the implementation of the Smart Nation. Most smart city projects around the world are led by their pro-active mayors or governors who may have little control over national policies. These projects may be constrained by certain laws that affect the whole nation. For example, Federal and State legislation may not allow for the smooth transition of some American cities into becoming smart cities. As such, many smart city projects are going for piecemeal solutions only such as street lighting or waste management. In Singapore, the fact that this program is led by the national government means that legislations can be amended and various public agencies are strongly motivated to make it a success. This enables Singapore to lead the standardisation efforts for Smart City. An Internet of Things (IoT) Standards Outline in support of Singapore's Smart Nation initiative has been laid out and announced in Aug 2015 The IoT Standards Outline focuses on three types of standards, namely sensor network standards, IoT foundational standards and domain-specific standards. Standards will play a critical role to create an environment where government agencies, planners, developers, manufacturers come together to develop new technologies and smart solutions efficiently. Smart Nation Infrastructure HetNet is a key component of Smart Nation. The government is keen to promote Heterogeneous Network (HetNet) technology for Smart Nation. HetNet network services will be maintained by switching between different types of networks such as Wi-Fi and 4G and 3G. It is meant to mitigate capacity crunch, optimise overall network capacity to improve quality of service, facilitate intra-operator roaming that would improve network resiliency.

Smart Nation Infrastructure

Source: DBS Bank

Singapore’s unique focus on HetNet. We see at least two key reasons for this. Firstly, Singapore often sees extremely high data usage in certain pockets of the city such as in MRT stations and popular shopping malls. HetNet deploying Wi-Fi for small cells and 4G for macro cells is a relatively more economical solution than only deploying 4G due to cheaper cost of Wi-Fi equipment. Also, Wi-Fi uses an unlicensed spectrum of around 2.4 GHz band, thus making it more spectrum efficient. HetNet will be able to provide better user experience. Secondly, HetNet could also be a better solution than public Wi-Fi networks alone in the monitoring of various services especially when people are mobile. For example, when one leaves home to catch public transport, everything can be monitored by operators using HetNet.

All Singapore telcos are trialling HetNet in Jurong. In fact, we do not think there is a business case for the fourth telco without deploying HetNet as the new entrant will only be able to secure 5-15% market share at best in the long term. A conventional mobile network may require up to S$1bn for a nationwide network while a HetNet may only need one-third of the capex based on our understanding. The new telco could quickly achieve nationwide 4G coverage using 900MHz spectrum on a small user base initially. As and when the number of users rise in a given macro cell, it may deploy more small cells of Wi-Fi or LTE in a cost efficient manner.

Regional Industry Focus

Internet of Things & Smart Cities

Page 15

Besides, there are other parts as shown below (i) New Fiber network called IP Core to add network resilience and secure public data during transmission; (ii) Above

the Ground (AG) boxes for powering and connecting to sensors in public spaces; and (iii) Data centre for the collection of public data.

Smart Nation Services

Source: DBS Bank

There are currently 5 main areas of focus. These are Smart Health-Assist, Smart Logistics/Mobility, Smart HDB Town Framework and Smart Tech Challenges. The government's annual projected healthcare spending is expected to reach S$12 billion by 2020, up from an estimated S$8bn in 2015. Smart Health-Assist The Challenge - Limited Healthcare Infrastructure. Hospitals are already operating at close to full capacity in Singapore. Along with medical tourists coming for

better treatment, Singapore is also facing a rapidly ageing population which will squeeze Singapore’s healthcare capacity. It is estimated that by 2030, there will be 900,000 elderly citizens in Singapore which represents a 1 in 5 ratio, increasing the emphasis of the importance of Singapore’s healthcare system. The Pioneer Generation Package is for 450,000 Singaporeans. In contrast, there are c.1m Singaporeans between the ages of 45 and 64, who will reach retirement age in 10 to 20 years.

The challenge of Ageing population in Singapore

Source: Smart Nation-Forbes

Regional Industry Focus

Internet of Things & Smart Cities

Page 16

Singapore would use telehealth to tackle its own healthcare challenges. National University Hospital is undertaking a trial to see if remote healthcare is viable. In this trial, patients are monitored at home with smart devices so that arlier intervention can be provided if need be in order to reduce the number of visits to hospital. From the perspective of the consumer/patient, they will be able to manage their medical conditions especially chronic diseases such as cardiovascular, diabetes, respiratory diseases whilst in the comfort of their own homes. Any deterioration of a patient’s health can be detected faster than if the patient was left to their own devices to visit a medical professional. Another use for the sensors would be the development of Smart Elderly Alert Systems for the monitoring of elderly relatives to keep them safe. Sensors placed in the flat can help to monitor the movements of the elderly, and caregivers will be alerted should irregular movements be detected. This in turn would reduce traffic in hospitals’ emergency departments or inpatient admissions by early intervention by the healthcare provider. This would also mean that healthcare staff can be more efficiently allocated. There are 3 key areas (not including infrastructure) that still require development, namely next generation sensors, decision support systems and big data analytics. Development of Next Generation Sensors. Currently, most commercially available healthcare sensors are often intrusive and cumbersome when a patient needs constant monitoring. Sensors are also not refined and may set off false alarms. This opens an opportunity to develop solutions to these problems, for example, heart rate and blood pressure monitors that come in stick-on patches, digital wrist watches or sensors embedded in items such as pillows. Decision Support Systems. Decision Support Systems (DSS) are meant to help healthcare professionals diagnose and recommend the right treatments and care plans for patients. This increases the consistency of treatments of evidence-cased care and the monitoring of key clinical and service outcomes. For example, if a medical professional comes across a rare case that he or she has not seen before, they are able to access a database of all the past medical cases to ensure that their diagnosis is correct.

Big Data Analytics. The data collected by the sensors will be stored in national health data bases which would allow medical professionals to gather new insights into disease patterns and contribute to further medical research. In Chicago, there is a group called the Health Data Liberation Meetup Group that is devoted to helping providers, insurers, and institutions to adopt open data practices in the field of healthcare. Smart Transport The Challenge is Limited Space for Roads. With a population of 5.4 million and approximately one million cars on the roads, the number of vehicles that Singapore can have is severely limited. At the same time, roads take up 12% of land space suggesting that we cannot increase its operating capacity. In response to this, the LTA has come up with ideas that make use of ICT solutions. Challenge in Transport Sector in Singapore

Source: Smart Nation-Forbes Smart Traffic Congestion Management. The government plans to replace the current ERP system with one that uses satellite position technology by 2020. This would get rid of those structures that are a negative externality to many people’s eyes and clear up space for other things. Using Global Positioning System (GPS), motorists may have to pay based on the distance travelled in a congested zone rather than paying a flat fee. It could also replace a whole range of things from replacing parking coupons to paying for tolls at checkpoints. It would also allow motorists to obtain real-time traffic information on an interactive computer installed in vehicles, in place of the existing in-vehicle unit. The system should ideally be able to

Regional Industry Focus

Internet of Things & Smart Cities

Page 17

learn a motorist’s regular route and calculate how much he could expect to pay that day. It should also be able to suggest alternative routes with different prices and journey times. There is a possibility that motorists could pay ERP charges at the end of a month, after the distance clocked has been compiled. A range of payment options will be available, from upfront payment through Contactless e-Purse Application (CEPAS)-compliant stored value cards to backend payment using credit and debit cards, a virtual payment account and GIRO. Monthly subscription fees for all transportation needs? Whether you travel by bus, train or cab, the Mobility-as-a-Service (MaaS) mobile app may allow you to pay a one-off, monthly subscription fee to get around Singapore. Adding the fact that you will be able to get the app to plan a trip for you — all you need to do is enter your starting point and destination — and MaaS could just be the next efficient, one-stop platform for our transportation needs. Details are scant, but according to IDA, this integrated model will allow commuters to get around at a lower cost. Another huge advantage is its efficiency; there is no risk that one’s ez-link card is running out of money, or having to rush to top up the card when one is running late for work. Autonomous Vehicles in Sentosa. In April 2015, IDA revealed that it will be working with the Sentosa Development Corporation. Driverless cars will ferry visitors around the island, drones will roam to check for litter, and self-driving lawnmowers will maintain the landscape. Ministry of Transport, Sentosa Development Corporation and ST Engineering have signed MOUs to conduct tests for a fleet of “on-demand self-driving shuttles”, which will complement the island’s existing bus, tram and monorail network. These driverless shuttles will allow guests to travel around the island by calling for them via smartphones or information kiosks. The public trials for this will take place after 2018, once an engineering study determining the technical requirements for seamless navigation is completed Smart Logistics Two key challenges today. Present day track and trace technologies are often used by large organisations for premium cargo but many of them lack near time information. Also verifications are also very disjointed

with the change of custody across different service providers with as many as 25 parties required to process one export shipment, with each using different standards. Smart logistics will be a centralised platform. This platform will allow different players - cargo owners, freight forwarders and ground handlers - to leverage upon sensory networks in airports and seaports to track and manage their cargo in near real time. The government will fund the building of the infrastructure and allow small players to access it at an affordable price. According to IDA, smaller players in particular, will benefit from this more affordable system that will enable timely response to unforeseen events, automate labor intensive processes and reduce inventory. TradeNet, the e-government platform for the local trade and logistics industry launched 25 years ago, will be undergoing a facelift. There is a plan to combine the backend systems of TradeNet, TradeXchange and Customs into one system, tentatively to be named National Trade Infrastructure, once the current contract expires in 2017. The government hopes that this keystone project will boost Singapore's productivity and competitiveness through a digitalised, integrated supply chain. A tender for this project had been called and bids are now being evaluated. Ningbo City in China, for example, has developed a Smart Logistics Center to streamline the port’s entire supply chain and allows 5,000 logistics companies in Ningbo to share data. Using this cloud platform, logistics companies and their clients can work together to respond to changing demands to better decide what to produce and when and where to ship it. Every shipping vehicle has a GPS tracker now and the idling of trucks has decreased significantly by up to 80% in some cases. Smart HDB Town Framework The Smart HDB Town Framework maps out the introduction of smart technologies in HDB towns and estates by focusing on four key areas: Smart Planning, Smart Environment, Smart Estate and Smart Living Smart Planning. It refers to the use of computer simulations and data analytics to enable HDB to effectively plan and design its estates. For example, when assessing the effectiveness of various initiatives (e.g. LED lighting, solar energy, vertical greenery, rainwater harvesting, recycling, pneumatic waste collection), and making a decision on the best

Regional Industry Focus

Internet of Things & Smart Cities

Page 18

combination to achieve sustainability goals in a cost effective way. Each car park will also have an intelligent parking demand monitoring system that will automatically increase the number of available lots during non-peak hours for visitors, as residents with season parking tickets are out, and reduce the number of available lots for short-term parking visitors in the evening, to ensure sufficient lots are reserved for residents with season parking tickets returning home. Smart Environment. Estates will be linked with a network of sensors to create a Smart Environment. These sensors will capture real-time information on environmental factors such as temperature and humidity. Innovative solutions can then be found to create a more pleasant environment for residents. For example, fans in common areas can be triggered when certain thresholds of temperature and humidity are reached. The fan speed can be regulated to improve the thermal comfort level for residents, while reducing energy consumption. Smart Estate. Data will be analysed by Smart technologies to optimise maintenance cycles and pre-empt problems. This will allow us to better understand the usage patterns of common amenities so as to easily check and identify problems to resolve them. For example, lighting fitted with sensors can help HDB to understand human traffic patterns and optimise the provision of lighting. The lighting in common areas with little or no human traffic detected could be reduced to 30%, hence reducing energy usage. Another example would be the installation of a Smart Pneumatic Waste Conveyance System. Waste disposal patterns and volumes can be monitored which will allow effective waste collection frequencies. This can help to optimise the deployment of resources needed for waste collection. Smart Living. The Smart Nation plans include using smart technology in housing estates. HDB estates are the first to try using these smart technologies to see if individuals can adapt these for day to day living. Residents will be able to tap on Smart home applications developed by commercial companies that can enhance energy savings, and enable them to access services like healthcare, in the comfort of their homes. Seventeen companies are participating in the trials, including the likes of Samsung, LG Electronics and StarHub. For example, HDB, together with the Energy Market Authority (EMA) and Panasonic, are exploring a suite of different energy choices and solutions for households. Residents can also monitor their energy consumption patterns, and manage their home appliances anywhere, in real time.

Smart Tech Challenges The Smart Nation Tech Challenge is meant to encourage individuals and businesses to join the government and use new technologies to solve problems that we face in an urban environment. The Smart Nation Tech Challenges are very much a government-led initiative. Other smart cities such as Amsterdam and New York have citizen-led initiatives that allow anyone to convert an idea into a feasible project. Although there is no clear direction, there is a lot of citizen engagement Video Analytics Smart Nation Tech challenge. Video analytics is the analysing of video streams and footages taken by surveillance systems and translating these into data that the government or another type of organisation could use. It could potentially boost public safety and improve resource utilisation when video analytics software senses that something is amiss, or improve services in areas such as transportation, healthcare, retail and security through relevant data gained. The challenge is thus to build up industry technical capabilities in video analytics (i.e. accuracy and availability of algorithms) and to create solutions to video analytic problems so as to generate greater value from cameras. The evaluation, validation and announcement of winners for the challenge is expected to be announced in January 2016. There are three main benefits to the advancement of video analytics technology, namely public safety, manpower utilisation and situational awareness.

Regional Industry Focus

Internet of Things & Smart Cities

Page 19

China – Smart Cities IoT is one of priority projects of China’s 12th Five-Year Development Plan (2011- 2015). In February 2012, China’s Ministry of Industry and Information Technology (MIIT) released the national 12th five year plan which put forward the objectives, investments and roadmap for China’s IoT market. According to China’s R&D Center for Internet of Things (CIT-China), the Chinese government is expected to invest c. RMB 3.8t (US$ 610b) in developing a M2M ecosystem within the decade ending 2020. China’s central government has selected over 200 cities to pilot smart city projects. These cities include Beijing, Shanghai, Guangzhou and Hangzhou beside others. Over 90% of China’s provinces and municipalities have listed IoT as a pillar industry in their development plans, For example In Zhenjiang, Jiangsu province, high-speed 4G networks have become standard in buses, trains and the city’s app broadcasts bus arrival times. Zhenjiang states that over 500,000 commuters now utilize these features daily saving 6,700 tons of carbon dioxide and US$ 2.7m in fuel costs annually by more closely tracking real-time bus routes. China Smart City Technology market to boom

Source: Navigant Research

Tai Lake in Wuxi City is using IoT technologies to monitor and predict the Cyanobacteria outbreak and protect the water supply to the city. China Smart City Industry Alliance, an association sponsored by MIIT predicts that smart city related industries will grow at a compound annual growth rate of 18% over the next 15 years from 2014 and IDC predicts that urban construction investments associated with smart cities in China will reach RMB 2t (over US$ 300b) over the decade ending 2025. In smart city initiatives rolling out smart grids, establishing smart traffic management systems, video analytics and surveillance and smart governments are key areas of focus. Big spending on smart meters and grids. China’s biggest power distributer, China State Grid Corp., has spent about RMB 400b (US$ 6b) last two years on its electricity networks and plans to invest over RMB 420b (US$ 6.8b) in 2015. Growing electricity demand due to urbanization, the nation’s pledge to generate 20% of its energy requirements by 2020 from renewable sources and increasing demand for electric vehicles is expected to drive demand for smart grids. McKinsey estimates that China’s urban population will grow to 840m by 2020 and over 5m electric vehicles to be on the roads by 2020. By 2013 China had deployed over 250m smart meters. A recent report by the WorldWatch institute states that the Chinese government is planning to have smart meters installed in 95% of China’s households by 2017. As such, over 435m smart meters are expected to be deployed by 2017.

Regional Industry Focus

Internet of Things & Smart Cities

Page 20

Companies Exposed to IoT 1. ST Engineering is likely to secure a couple of

billion dollars worth of Smart Nation projects over the next 3-5 years in our view.

The company has already secured 7 out of 15 pilot projects in Jurong Lake district for the Smart Nation project. 1) Smart Traffic management system 2) Location information in urban environment 3) Estate energy management system 4) Smart Outdoor lighting 5) Smoke Detection 6) Smart Walk 7) Smart Phone as sensor Smart Traffic management system could be worth S$1bn –S$2bn on our estimate. This system would get rid of those structures that are a negative externality in many people’s eyes, and clear up space for other things. Using Global Positioning system (GPS), which is ubiquitous, motorists could end up paying based on the distance travelled in a congested zone rather than paying a flat fee. The new system could also obtain real-time traffic information on an interactive computer installed in vehicles, in place of the existing in-vehicle unit. There are over 1 million vehicles in Singapore and about 100K of them are replaced each year. If the new in-vehicle were to cost S$100-200 per vehicle, we estimate this could translate to S$1bn-2bn worth of sales initially, followed by S$100m worth of sales each year. While Singapore government has not disclosed its budget for Smart Nation, we think these seven projects could be worth couple of billion dollars over the next 3-5 years. ST Electronics offers various enterprise solutions. ST Electronics offers solutions like waste management, Smart Grid, Automated Metering Infrastructure (AMI), Smart Building, Smart Lighting, elder care, emergency response system etc which demonstrates the software capabilities of ST Electronics.

2. Keppel DC REIT offers investors exposure into the highly specialised and resilient data centre market.

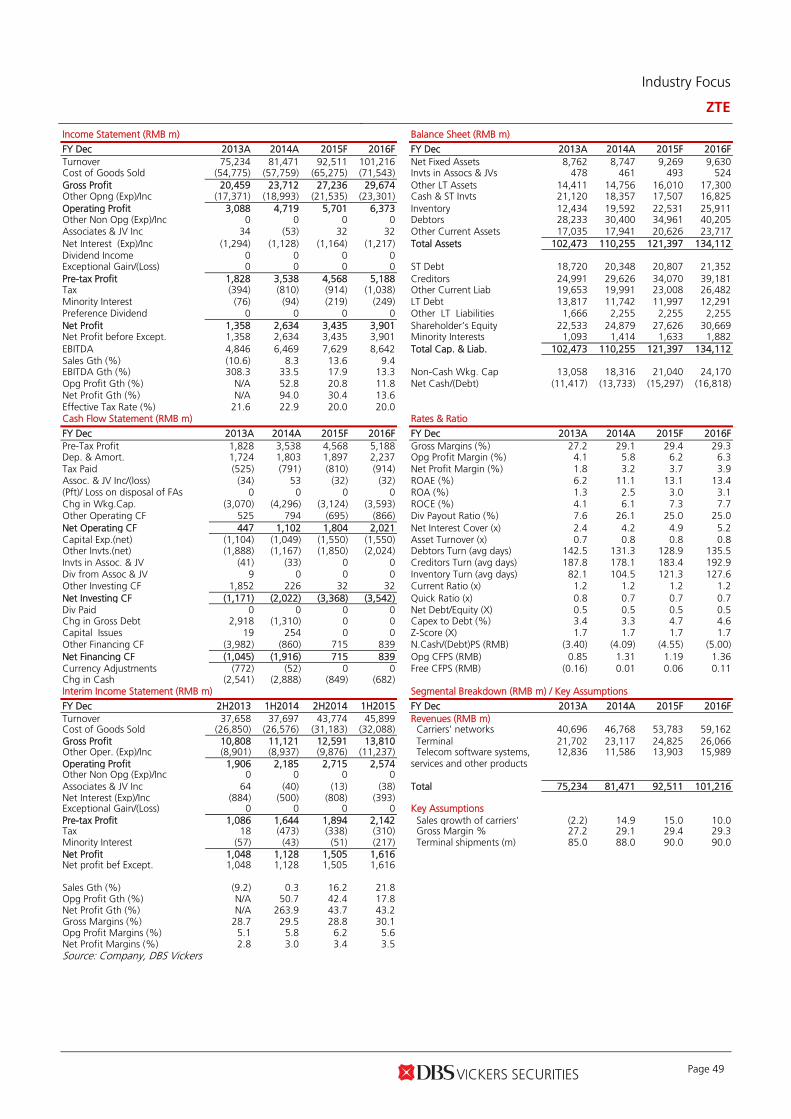

With close to 70% of NPI derived from co-location leases, the Trust is poised to ride on rising global usage of data and demand for data centres. Earnings are further supported by its master leased properties (30% of NPI) which have average annual escalations of 2-4%. Visible earnings growth profile underpinned by acquisition potential. With foreign sourced distributions fully hedged until 1H17, and 90% of borrowings hedged into fixed rate debt, Keppel DC REIT stands out for its stable and highly visible earnings profile. Earnings catalyst will come from the acquisition of T27, which we believe could occur in 1H16. While an acquisition of >S$250m is expected to trigger an equity fund raising exercise, we believe the acquisition will be accretive to earnings given that the stock is trading at a low implied cap rate of 6.3%. Imputed S$250m of acquisitions into FY16 numbers. We have assumed S$250m of acquisitions in FY16 to account for the purchase of T27; we have assumed the equity fundraising will bring gearing down to 30%, which is the Manager’s long-term target level 3. ZTE will benefit from Chinese telco’s 4G capex in

2015, capacity expansion in 2016 and growth in enterprise and government solutions in the long term.

Rising participation from government and enterprise businesses is supportive of margins. ZTE’s service/software revenue increased 36.1% y-o-y in 1H15 (16% of sales) on smart city project wins. ZTE is well positioned with its total solution capabilities (hardware, software, wireless transmission, integration operation, etc). ZTE has signed contracts with government agencies and enterprises in more than 140 cities in 40 countries (~100 in China), which should help support growth in 2H15 and beyond. The company is already working with Tencent on a number of smart city projects whereby ZTE focuses on systems and infrastructure, and Tencent on terminal services to customers. ZTE estimates that the Smart City market is worth c.RMB100 billion (~US$16 billion).

Regional Industry Focus

Internet of Things & Smart Cities

Page 21

Networking equipment business is near term driver. Networking equipment sales grew 30.6% y-o-y in 1H15 (62% of sales) on strong growth in 4G base stations. With tower sharing in the process, we see a shift in spending by telcos from infrastructure (tower construction) to base stations and optical broadband networks. While 4G capex is likely to see some decline in China in FY16F, we expect ZTE to register stable networking equipment business < in FY16F from growth in overseas business (~40% of networking equipment business). Handset business is undergoing restructuring. Handset revenues decreased 4.3% y-o-y (22% of sales) on weaker end-demand, especially in China. ZTE is shifting its focus to the high-end market and the overseas market, while restructuring its domestic business. While domestic handset business is declining, the overseas market delivered strong growth in 1H15, as ZTE is now the fourth largest smartphone brand in the US and the second largest in the US prepaid market. Almost half of total sales are ex-China. International operating revenue rose 16.8% y-o-y to RMB21.5bn in 1H15 (47% of sales). This was on the back of its strategy of focusing on populous nations and mainstream global carriers. Higher R&D spending to enter higher-margin sectors. With R&D spending-to-total revenue increasing to 12% in FY15 from 9.5% previously, ZTE is able to enter several high margin industries including video conferencing solutions and high-end core routers in the enterprise sector. According to management, ZTE's self-developed chips and operating systems differentiates the company from its peers and it has provided network services to various local governments and enterprise in China. ZTE offers various enterprise solutions like Smart Grid, Smart Traffic management systems etc. For example, the Yinchuan smart government system by ZTE enables one-stop approval of 432 business processes of government departments. It shortens the approval period by 78% and reduces the enterprise registration period from five days to one day.

4. Wasion will benefit from State Grid’s plan to automate distribution and use automated meter reading and analytics

Wasion is a leading energy measurement system and service supplier in China. It has three main segments - Advanced Metering Infrastructure (AMI) for automated meter reading and analytics, Advanced Distribution Operations (ADO) for smart distribution and Smart Meters (SM) Higher margin businesses registering strong growth. AMI revenue grew 14.9% y-o-y in 1H15, (51.8% of sales), ADO revenue grew 70.6% (12.2% of sales) while Smart Meter (SM) revenue 9.0% (36.0% of sales). Wasion is in a transition phase, moving from the lower-margin SM business to higher-margin AMI and ADO businesses. Benefits from State Grid’s investment plan. State Grid will construct 50 new ADO substations. Distribution automation at cities will increase from 30% to 50%. Investments in the construction and upgrade of the smart grid will amount to >RMB80bn. As such, ADO sales are expected to more than double in FY15. Smart meter business remains solid. We estimate that the penetration rate of smart meters would reach 76% by 2015, compared with 80% as stated in the 12th Five Year Plan. Thus, installation will be accelerated. We expect State Grid’s tender size to remain stable at 80-90m units in 2015, compared with 91.7m units in 2014. Strong growth in international markets. Wasion has won a US$12.3m AMI contract in Tanzania, RMB68m and RMB10m AMI contracts in Mexico and Brazil respectively through its strategic partnership with Siemens. Overseas business comprised only 4% of sales in 2014, and is likely to rise to 9% of sales in 2015 on our estimate.

Regional Industry Focus

Internet of Things & Smart Cities

Page 22

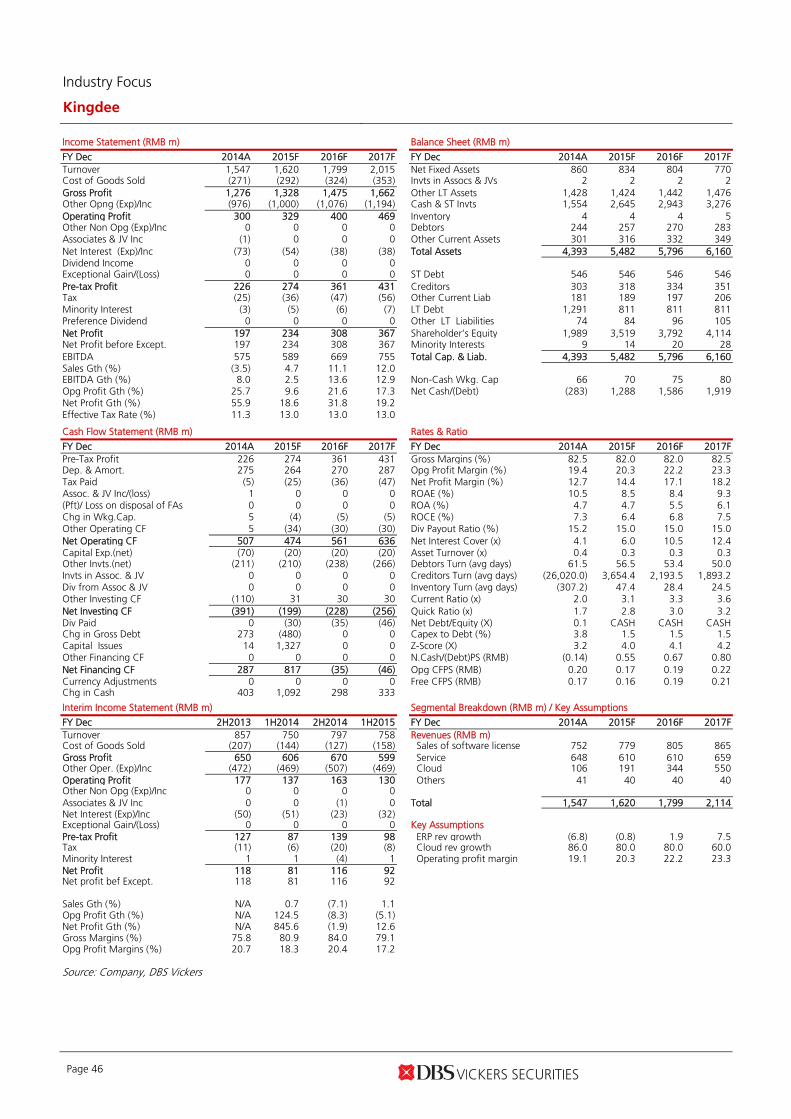

5. Kingdee will benefit from double-digit growth of Enterprise Resource Planning (ERP) solutions in China

Continued upside for business software in China. Enterprise Resource Planning (ERP) market in China is projected to grow to USD1.6b in 2018 at a five-year CAGR of 11%, according to Gartner. As the SME market is extremely underpenetrated and as inflation and higher labor costs are pushing Chinese SMEs to enhance their operating efficiencies, SME software market in China will continue to see solid growth. This is also supported by more ERP applications for e-commerce activities in China. Kingdee is the second largest Chinese provider of ERP software in China with a focus on SMEs. JD.com invested HK$1.3bn for a 10% stake in Kingdee at a purchase price of HK$4.6 per share on 26 May 2015. JD.com aims to promote Kingdee’s ERP products to its suppliers, which are integrated with JD.com’s supply chain system for overall inventory and logistics management Accelerating cloud and mobile applications on top of its traditional ERP products. Cloud segment remains in an investment phase and did not reach break-even till 1H15. Kingdee has been building the cloud business scale and expects it to account for 20-30% of total revenue by FY17 versus 11% in 1H15. Expect ERP revenue to resume growth as sales channel restructuring was almost completed in 1H15. Going forward, revenue growth along with operating leverage to flow through, resulting in margin expansion over the next two to three years.

Regional Industry Focus

Internet of Things & Smart Cities

Page 23

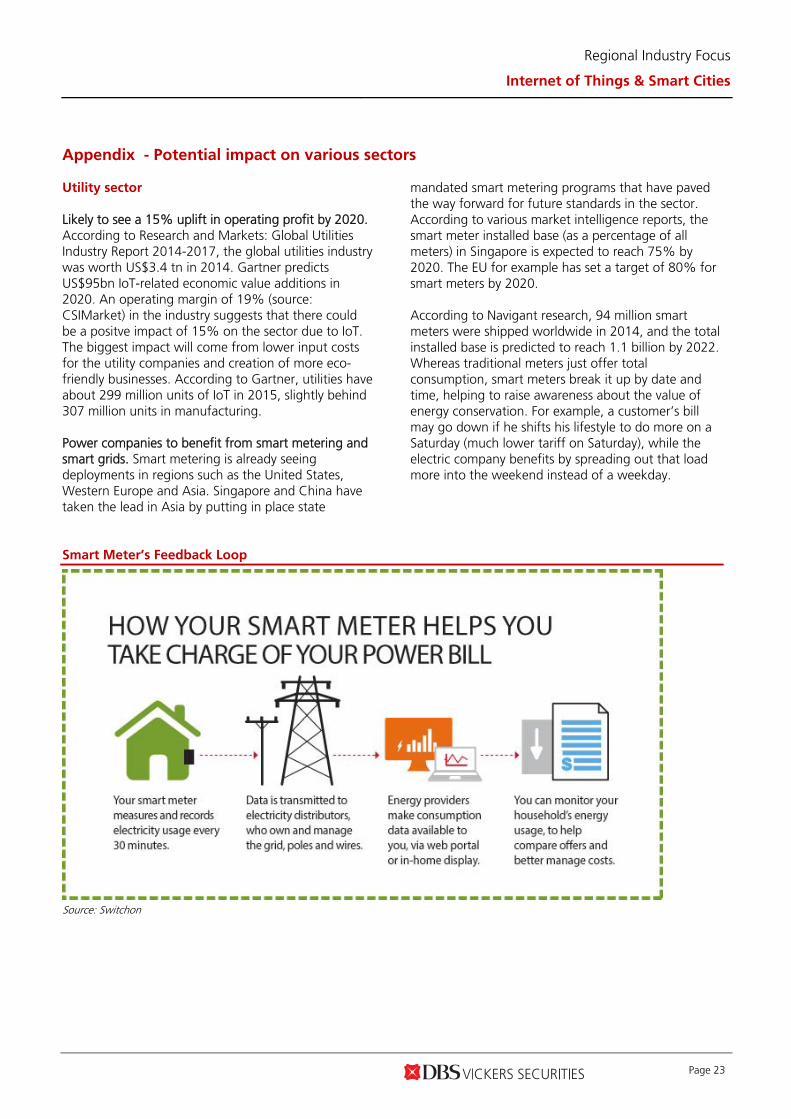

Appendix - Potential impact on various sectors Utility sector Likely to see a 15% uplift in operating profit by 2020. According to Research and Markets: Global Utilities Industry Report 2014-2017, the global utilities industry was worth US$3.4 tn in 2014. Gartner predicts US$95bn IoT-related economic value additions in 2020. An operating margin of 19% (source: CSIMarket) in the industry suggests that there could be a positve impact of 15% on the sector due to IoT. The biggest impact will come from lower input costs for the utility companies and creation of more eco-friendly businesses. According to Gartner, utilities have about 299 million units of IoT in 2015, slightly behind 307 million units in manufacturing. Power companies to benefit from smart metering and smart grids. Smart metering is already seeing deployments in regions such as the United States, Western Europe and Asia. Singapore and China have taken the lead in Asia by putting in place state

mandated smart metering programs that have paved the way forward for future standards in the sector. According to various market intelligence reports, the smart meter installed base (as a percentage of all meters) in Singapore is expected to reach 75% by 2020. The EU for example has set a target of 80% for smart meters by 2020. According to Navigant research, 94 million smart meters were shipped worldwide in 2014, and the total installed base is predicted to reach 1.1 billion by 2022. Whereas traditional meters just offer total consumption, smart meters break it up by date and time, helping to raise awareness about the value of energy conservation. For example, a customer’s bill may go down if he shifts his lifestyle to do more on a Saturday (much lower tariff on Saturday), while the electric company benefits by spreading out that load more into the weekend instead of a weekday.

Smart Meter’s Feedback Loop

Source: Switchon

Regional Industry Focus

Internet of Things & Smart Cities

Page 24

Most importantly, the data generated will used by utility companies for automated billing and optimisation of electricity generation and distribution. In addition, governments are promoting the use of renewable energy, whose generation capacity varies according to weather patterns. Utility companies can develop better predictive models using the newly available sensory data to manage loads as well as implement dynamic grid operations to support the changes in generation and usage. IoT technology is also useful in testing and implementing new technologies. For example, techniques such as distributed energy generation where households generate energy which is then distributed to their neighbours through a smart grid can be adopted. In 2013, SP PowerAssets, a subsidiary of Singapore Power which owns the electricity transmission and distribution networks of Singapore, started rolling out a smart grid platform in Singapore with the participation of Smart-meter specialist, Silver Spring Networks. Water is another area of interest. This includes areas such as smart metering (for water) to tele-managed irrigation networks and use of optimised routes for efficient garbage collections. Smart meters for water, similar to electricity, can be used to control and reduce water usage and wastage. Smart water meters are

also an integral part of smart water systems which uses real time data to better monitor water usage and detect any problems such as leakage. In Singapore, Sembcorp Industries has already joined hands with Singapore Economic Development Board, to carry out applied research and development in areas such as smart water systems and carbon capture. The venture will also be investing up to S$8m to support the commercialisation of the projects. If the projects are successful, these initiatives could be deployed in Sembcorp's global operations. The use of sensory data can optimise the use of water in irrigation activities. For example, Barcelona is already testing a tele-managed irrigation system to reduce water usage, where plants are watered depending on the moisture level of the soil. This is important for areas with limited water supply and can reduce costs relating to transporting and distributing water. The Barcelona city council estimates a savings of US$555,000, representing a 25% cut in water usage. Waste management companies to benefit from lower manpower needs. Singapore, for example, is implementing Pneumatic Waste Collection System (PWCS).

Waste management with IoT

Source: FarSite Communications

Regional Industry Focus

Internet of Things & Smart Cities

Page 25

When residents throw rubbish down their chutes, it goes to a refuse chamber on the ground floor. A sensor will be triggered when the container in the refuse chamber is full. The waste is then transported by exhaust air, through underground pipes. It travels at speeds of between 50 and 80 kilometres per hour to a centralised bin, where the rubbish is stored in sealed containers. When full, trucks will transport them to incineration plants. As for the exhaust air, it is passed through dust and odour filters. The clean air is then discharged into the atmosphere. With the process being automated, overall manpower needs are expected to be 70% lower. The Housing and Development Board (HDB) is test-bedding the system at Yuhua to determine its feasibility for existing buildings. It is also assessing residents' receptiveness, as major retrofitting works are required to install the system in existing estates. The system will be implemented in the upcoming housing estates of Tampines North (a tender was recently called in June 2015 for the design, building, operation, and maintenance of a district level PWCS here), Bidadari and Punggol Northshore. Transportation sector Likely to see 21% upside in operating profit from IoT. Gartner projects IoT to have c. US$114bn impact on the transportation segment. According to Research and Markets’s Global Transportation Services Industry 2012-2017 forecast, the size of the global transportation industry will be US$ 2.7tn by 2017. Based on operating margins of 20% in 2Q15 (source: CSIMarket), the overall impact of IoT will be around 21% at operating profit level. Cargo Owners and Freight forwarders to see lower inventory and insurance costs. These players will be able to intervene pro-actively to manage deliveries in the case of a delay or any exceptional event, using real time tracking. They will also be able to prevent loss of inventory from environmental damage by monitoring and managing temperature, humidity, exposure to light etc especially for the commodities. Routes can

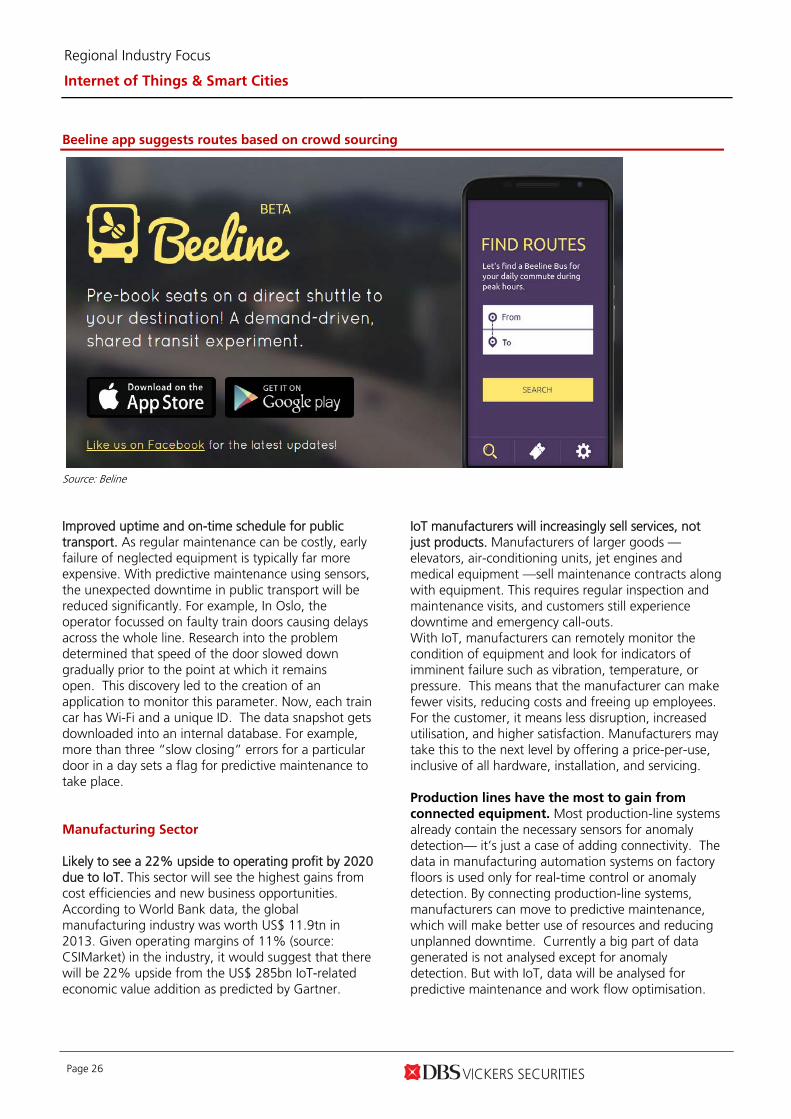

also be optimized. Through active monitoring, excess inventory along the supply chain can be minimised, which will add to profits. In addition, the data can be used to improve and optimise the logistics processes which can be lead to cost savings and reduce delays. As such, the cost of insurance for such shipments should reduce with a lower risk of shipment failure. Ground Handlers to benefit from optimisation of equipment use. By creating a tag association between cargo and ground handling equipment, ground handlers will be able to provide a full suite of real time track-and-trace capability to customers with such demands. Also, the tagging of equipment such as pallet dollies and tractors will reduce reliance on ground handlers to track equipments, translating to their optimal use. Companies such as Kerry Logistics have already stated to introduce higher levels of automation to its processes. The company introduced six fully automated and programmed robotic butlers at its PC3 flagship facility in Hong Kong to meet the ever-growing consumer demand in online shopping. Kerry Logistics is one of the first 3PLs in Asia to adopt robotic butlers in its operations to enhance fulfillment efficiency and accuracy. Usage of automation can have much bigger impact on e-commerce logistics than standard logistics services as e-commerce operations tend to be dominated by high volumes of small and irregular orders. The in-house system uses barcodes to track every item, enabling Kerry Logistics to increase service efficiency and accuracy. Increased flexibility of public transport. Another facet would be through understanding crowd behavior and patterns. The data collected by sensors in trains, busses, airplanes and transportation hubs can be used to predict the demand for transport services, which can be used to dynamically adjust availability of services. For example, Singapore launched Beeline app in April 2015, whereby bus routes are crowd sourced. People can input suggested routes at various times in the app which can be aggregated to start shuttle services.

Regional Industry Focus

Internet of Things & Smart Cities

Page 26

Beeline app suggests routes based on crowd sourcing

Source: Beline Improved uptime and on-time schedule for public transport. As regular maintenance can be costly, early failure of neglected equipment is typically far more expensive. With predictive maintenance using sensors, the unexpected downtime in public transport will be reduced significantly. For example, In Oslo, the operator focussed on faulty train doors causing delays across the whole line. Research into the problem determined that speed of the door slowed down gradually prior to the point at which it remains open. This discovery led to the creation of an application to monitor this parameter. Now, each train car has Wi-Fi and a unique ID. The data snapshot gets downloaded into an internal database. For example, more than three “slow closing” errors for a particular door in a day sets a flag for predictive maintenance to take place. Manufacturing Sector Likely to see a 22% upside to operating profit by 2020 due to IoT. This sector will see the highest gains from cost efficiencies and new business opportunities. According to World Bank data, the global manufacturing industry was worth US$ 11.9tn in 2013. Given operating margins of 11% (source: CSIMarket) in the industry, it would suggest that there will be 22% upside from the US$ 285bn IoT-related economic value addition as predicted by Gartner.

IoT manufacturers will increasingly sell services, not just products. Manufacturers of larger goods —elevators, air-conditioning units, jet engines and medical equipment —sell maintenance contracts along with equipment. This requires regular inspection and maintenance visits, and customers still experience downtime and emergency call-outs. With IoT, manufacturers can remotely monitor the condition of equipment and look for indicators of imminent failure such as vibration, temperature, or pressure. This means that the manufacturer can make fewer visits, reducing costs and freeing up employees. For the customer, it means less disruption, increased utilisation, and higher satisfaction. Manufacturers may take this to the next level by offering a price-per-use, inclusive of all hardware, installation, and servicing. Production lines have the most to gain from connected equipment. Most production-line systems already contain the necessary sensors for anomaly detection— it’s just a case of adding connectivity. The data in manufacturing automation systems on factory floors is used only for real-time control or anomaly detection. By connecting production-line systems, manufacturers can move to predictive maintenance, which will make better use of resources and reducing unplanned downtime. Currently a big part of data generated is not analysed except for anomaly detection. But with IoT, data will be analysed for predictive maintenance and work flow optimisation.

Regional Industry Focus

Internet of Things & Smart Cities

Page 27

Healthcare Sector Likely to see a 9% upside to operating profit by 2020 due to IoT. According to Gartner, the biggest impact on healthcare industry from IoT comes from new market opportunities and lower input costs. The overall benefit for the healthcare segment, in terms of economic value, by adopting IoT is expected to be about US$ 285bn, according to Gartner. The global healthcare industry is expected to see revenues of about US$ 13.7b by 2020 according to estimates by Bain & Company. Given industry operating margins of about 23% in 2Q15 (source: CSIMarket), the overall benefit to the operational profit of the industry is likely to be around 9%. Remote patient monitoring will reduce staff costs and help to divert resources towards serious ailments. More than 70% of healthcare spending goes towards treating chronic ailments, such as diabetes, hypertension, chronic pulmonary diseases and cardiac conditions. Costs can be optimised if we can keep patients out of hospitals, in their homes and still provide a comparable level of care by using mobile applications like telehealth (for example, sensor-led continuous monitoring, rather than a nurse checking on patients frequently). A Singapore based company, Silverline is already using IoT tech to provide remote monitoring to the elderly. It claims to have established the world’s first mobile and

smart home assisted living ecosystem, which helps the elderly to lead a more wholesome and healthy life by empowering them through technology. They have a range of devices and customised smart phone apps for elderly and caregivers to monitor and track activity. Growing popularity of wearables to provide relevant data to healthcare providers. The availability of data from various wearables means that this information can now be sent to hospitals and ambulatory health records, and combined to create "complete" patient data that includes data for both within and out of a hospital setting. The old-style, hospital- or physician-focused data, without the accompanying data from wearables provides only a snapshot of the patient's condition at that particular time Hospitals and healthcare providers to benefit from less downtime and more efficient allocation of resources. For example, IoT technology can monitor and predict when important equipment of the hospital will need maintenance, allowing the hospital to avoid rescheduling patient and doctor appointments and increase utilisation of the asset. Similarly, hospitals can manage their pharmaceutical and equipment inventories more efficiently, which are generally overstocked. Hospitals will be able to incorporate a higher level of automation to their electronic health records systems through the use of lower cost sensors, which will cut labour requirements as well.

Regional Industry Focus

Internet of Things & Smart Cities

Page 28

STOCK PROFILES

www.dbsvickers.com ed: TH / sa: AS

BUY Last Traded Price: S$3.31 (STI : 2,998.35) Price Target : S$3.60 (9% upside) (Prev S$3.40) Reason for Report : Smart Nation initiatives Potential Catalyst: Better earnings execution, strong order wins, M&A Where we differ: More conservative on FY16/17 earnings Analyst Suvro SARKAR +65 6682 3720 [email protected]

Price Relative

Forecasts and Valuation FY Dec (S$ m) 2014A 2015F 2016F 2017F Revenue 6,539 6,345 6,194 6,155 EBITDA 835 852 861 883 Pre-tax Profit 651 660 666 686 Net Profit 532 531 536 545 Net Pft (Pre Ex.) 532 531 536 545 EPS (S cts) 17.1 17.0 17.2 17.5 EPS Pre Ex. (S cts) 17.1 17.0 17.2 17.5 EPS Gth (%) (9) 0 1 2 EPS Gth Pre Ex (%) (9) 0 1 2 Diluted EPS (S cts) 17.1 17.0 17.2 17.5 Net DPS (S cts) 15.0 15.0 15.0 15.0 BV Per Share (S cts) 68.4 70.4 72.6 75.1 PE (X) 19.4 19.4 19.2 18.9 PE Pre Ex. (X) 19.4 19.4 19.2 18.9 P/Cash Flow (X) 16.5 15.1 14.9 14.8 EV/EBITDA (X) 11.8 11.6 11.4 11.1 Net Div Yield (%) 4.5 4.5 4.5 4.5 P/Book Value (X) 4.8 4.7 4.6 4.4 Net Debt/Equity (X) CASH CASH CASH CASH ROAE (%) 25.0 24.6 24.0 23.7 Earnings Rev (%): - - - Consensus EPS (S cts): 17.2 18.2 19.4 Other Broker Recs: B: 8 S: 1 H: 4 ICB Industry : Industrials ICB Sector: Aerospace & Defense Principal Business: An integrated engineering group providing solutions and services in aerospace, electronics, land systems and marine sectors.

Source of all data: Company, DBS Bank, Bloomberg Finance L.P

At A Glance Issued Capital (m shrs) 3,103 Mkt. Cap (S$m/US$m) 10,273 / 7,330 Major Shareholders Temasek Holdings Private Ltd (%) 51.3 Aberdeen (%) 6.9 Capital Group Companies Inc (%) 5.0 Free Float (%) 36.8 3m Avg. Daily Val (US$m) 7.4

DBS Group Research . Equity 2 Nov 2015

Singapore Industry Focus

ST Engineering Bloomberg: STE SP | Reuters: STEG.SI Refer to important disclosures at the end of this report

Towards a smarter future ST Electronics should be one of the key local beneficiaries

of Singapore’s Smart Nation initiative

Working on pilot projects already

Significant contract wins in this space likely over FY16/17

Maintain BUY, TP raised to S$3.60 as we roll over to FY16

On track to secure orders. Singapore is poised to be among the global leaders in adoption of Internet of Things and big data as it pushes its Smart Nation program to resolve challenges in the utilities, transport and healthcare space through technology. Given the government’s proactive approach, we believe ST Engineering’s electronics division is well positioned to secure Smart Nation projects worth more than S$1bn in the near future. ST Electronics has already secured 7 out of 15 pilot projects in Jurong Lake district for the Smart Nation project, including 1) Smart Traffic Management System, 2) Location Information in Urban Environment, 3) Estate Energy Management System, 4) Smart Outdoor Lighting, 5) Smoke Detection, 6) Smart Walk and 7) Smart Phone as Sensor.

Strong competence in Smart City building blocks. ST Electronics has long track record in providing both hardware as well as system integration solutions as part of its Smart City capability build up. It has deployed or piloted sensor networks and smart utilities in cities like Paris, California, Texas, Sao Paulo, Auckland, Eliat (Israel) and Singapore already. It has also implemented intelligent traffic solutions in various Chinese cities like Beijing, Chengdu and Wuhan. ST Electronics also offers solutions like Smart Waste Management, Smart Water Management, Security Management Systems, Smart Healthcare Systems among others.

Stocks holds its allure. We believe the strength in the Electronics division will help to offset weakness in Marine division over the next 2 years and allow STE to report steady earnings and dividends. Maintain BUY on the counter, underpinned by healthy orderbook of S$12.4bn, strong balance sheet and dividend yield of 4.5%. Stronger earnings in 2H15 should provide catalysts in the near term. TP raised to S$3.60 as we roll over to FY16 valuation metrics.

90

110

130

150

170

190

210

2.2

2.7

3.2

3.7

4.2

4.7

Oct-11 Oct-12 Oct-13 Oct-14 Oct-15

Relative IndexS$

ST Engineering (LHS) Relative STI INDEX (RHS)

Page 30

Industry Focus

ST Engineering

INVESTMENT THESIS

Profile Rationale

ST Engineering (STE) is an integrated engineering group in the aerospace, electronics, land systems and marine sectors. The company has over the years diversified its businesses and geographies.

Orderbook at decent levels. Orderbook inched up to S$12.4bn at end-2Q15 from S$12.2bn as of end-1Q15 and covers close to two years of revenue and secures visibility, going forward. New contract wins announced YTD in FY15 have been somewhat slower compared to previous years owing to lack of major shipbuilding orders. 2H15 should be better than 1H15. For Aerospace sector, both revenue and PBT for 2H15 are expected to be comparable to that in 1H15. For Electronics, both revenue and PBT for 2H15 are expected to be higher than that in 1H15. For Land Systems, revenue is expected to be higher, while PBT for 2H15 is expected to be comparable to that in 1H15. For Marine, both revenue and PBT for 2H15 are expected to be lower than that in 1H15. Expanding capabilities in aerospace but impact is longer term in nature. Enhancing passenger-to-freighter conversion solutions via partnerships with Airbus in Europe. Expanding suite of cabin interior service solutions including VIP completions and reconfiguration business in the US; recent order wins in widebody VIP completion projects have inspired more confidence in the long-term outlook for these businesses.