Embed Size (px)

Citation preview

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS -INTRODUCTION

IPSAS OBJECTIVES

•Comparability with other international organisations and national

governments

•Enhanced governance and internal financial management

•Enhanced accountability, transparency and harmonization

• Improved consistency, quality and credibility of financial reports

WHY IPSAS?• Responding to a more connected world

• Allows comparisons between countries

• Public sector mainly used cash based accounting

• Primitive accounting mechanisms

• Need to distinguish between capital and revenue spending

• Encourages cross-border investment

• Introduction of International Financial Reporting Standards (IFRS)

• Recognition that IFRS is designed for the private sector

• Though UK and US public sector both using amended IFRS

• Need for standards that reflect the different needs of the public sector

• Standards amended

• IPSAs that have no IFRS equivalent

• Based on accrual accounting concepts though also Cash IPSAS

IPSAS GOALS

• Standards set out requirements on recognition, measurement and disclosure for

transactions and events

• Goals:

to have uniform standards for accounting at public sector organisations

around the world

To enable comparison of data across organisations

To improve financial accounting transparency

THREE SETS OF STANDARDS

• Cash-based accounting statements

• Encourages voluntary statements on an accrual basis

• Transitional arrangements

Cash basis IPSAS

• Convergent with IFRSs

• Adapted to public sector context where there is a significant issue

• Deals with public sector issues not dealt with by IFRSs

Accruals IPSAS

• Government Business Entities

• You need awareness of the issues arising in IFRS

• IFRS 9 affecting Financial Services including central banks

IFRS

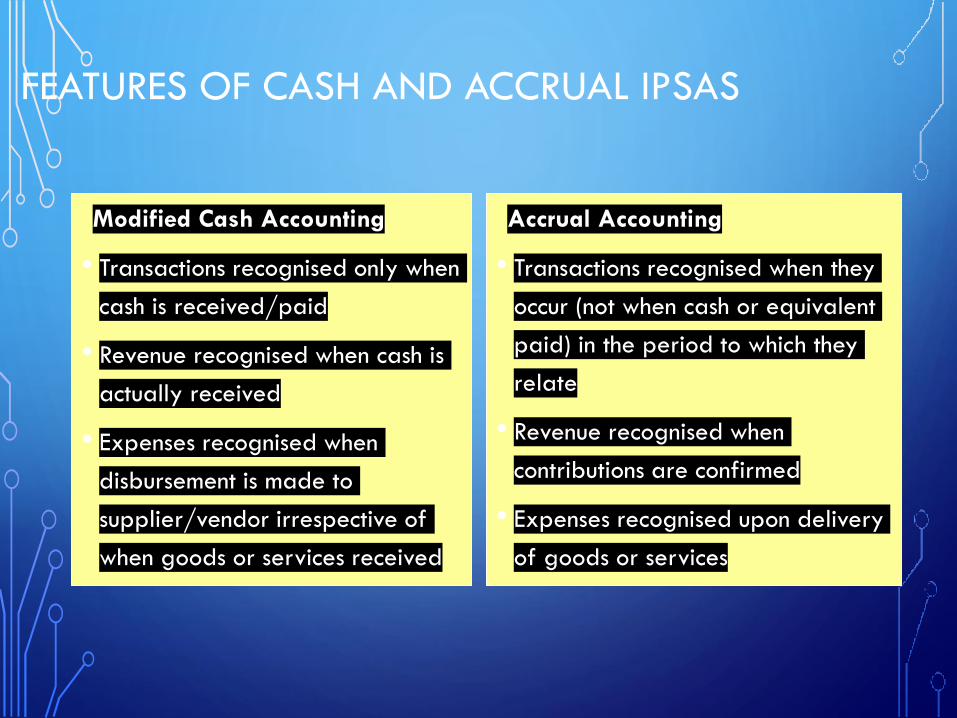

FEATURES OF CASH AND ACCRUAL IPSAS

Modified Cash Accounting

• Transactions recognised only when

cash is received/paid

• Revenue recognised when cash is

actually received

• Expenses recognised when

disbursement is made to

supplier/vendor irrespective of

when goods or services received

Accrual Accounting

• Transactions recognised when they

occur (not when cash or equivalent

paid) in the period to which they

relate

• Revenue recognised when

contributions are confirmed

• Expenses recognised upon delivery

of goods or services

ACCRUALS : A REFRESHER

•Definition “All income and charges relating to the financial

year…shall be taken into account without regard to the date of

receipt or payment”

•This means that expenditure is recorded as it is incurred and

income as soon as it is earned during an accounting period, even

if cash is not paid or received in that period

•Major differences in treatment of capital expenditure (on fixed

assets) and introducing debtors and creditors

WHY ACCRUALS ACCOUNTING?

• Increasing realisation of the limitations of cash accounting,

especially in relation to capital

• Increasing dissatisfaction in the financial and management

information available through cash accounting

•Accruals accounting demands greater accountability

•Accruals accounting is already applied elsewhere : in private

sector, rest of public sector, and overseas

•Severe limitations of cash-based information in relation to

decision-making

•The need to make comparisons over time

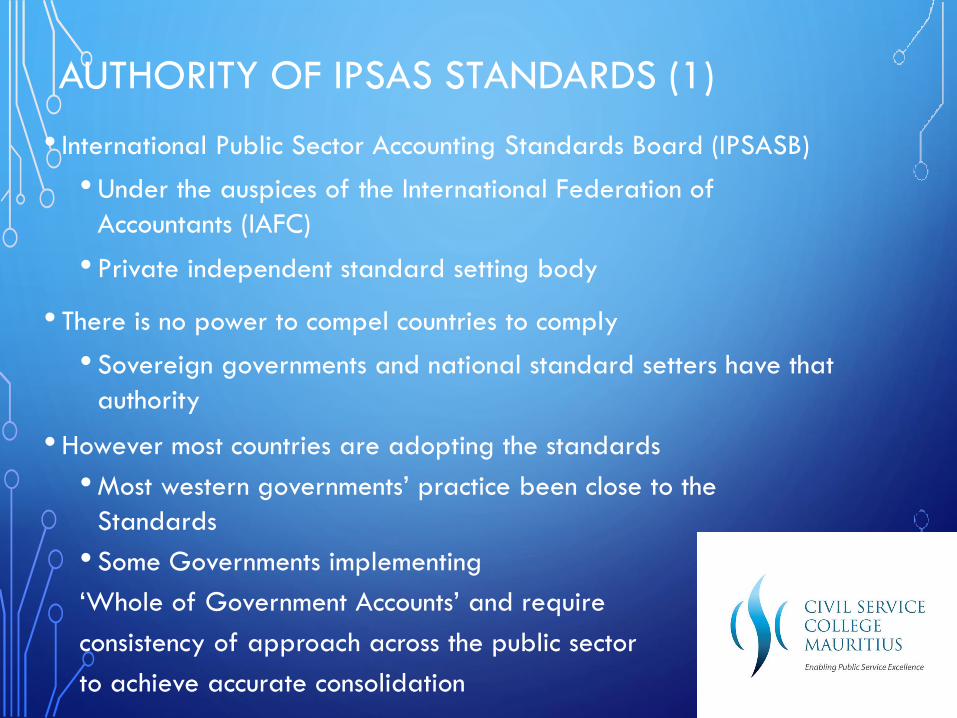

AUTHORITY OF IPSAS STANDARDS (1)

• International Public Sector Accounting Standards Board (IPSASB)

•Under the auspices of the International Federation of

Accountants (IAFC)

• Private independent standard setting body

• There is no power to compel countries to comply

• Sovereign governments and national standard setters have that

authority

•However most countries are adopting the standards

•Most western governments’ practice been close to the

Standards

• Some Governments implementing

‘Whole of Government Accounts’ and require

consistency of approach across the public sector

to achieve accurate consolidation

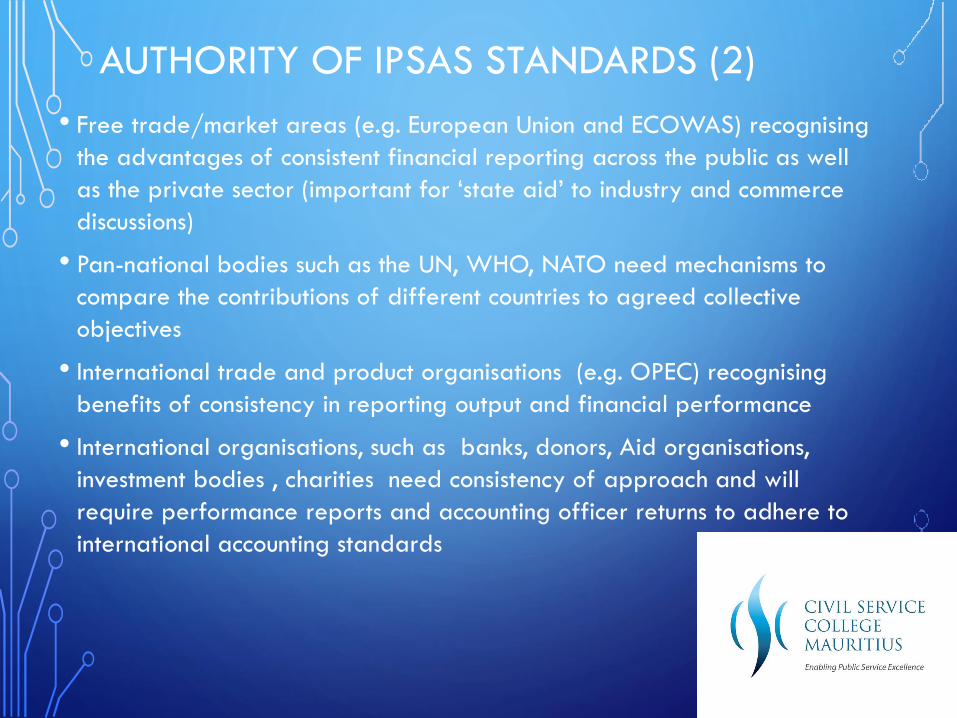

AUTHORITY OF IPSAS STANDARDS (2)

• Free trade/market areas (e.g. European Union and ECOWAS) recognising

the advantages of consistent financial reporting across the public as well

as the private sector (important for ‘state aid’ to industry and commerce

discussions)

• Pan-national bodies such as the UN, WHO, NATO need mechanisms to

compare the contributions of different countries to agreed collective

objectives

• International trade and product organisations (e.g. OPEC) recognising

benefits of consistency in reporting output and financial performance

• International organisations, such as banks, donors, Aid organisations,

investment bodies , charities need consistency of approach and will

require performance reports and accounting officer returns to adhere to

international accounting standards

COMPLIANCE

•Requires adherence to all applicable standards

•Compliance certified on organisation's general- purpose

financial statements

•Auditors must determine that accounting and reporting

are in accordance with all relevant standards

•The majority of the standards are accrual based

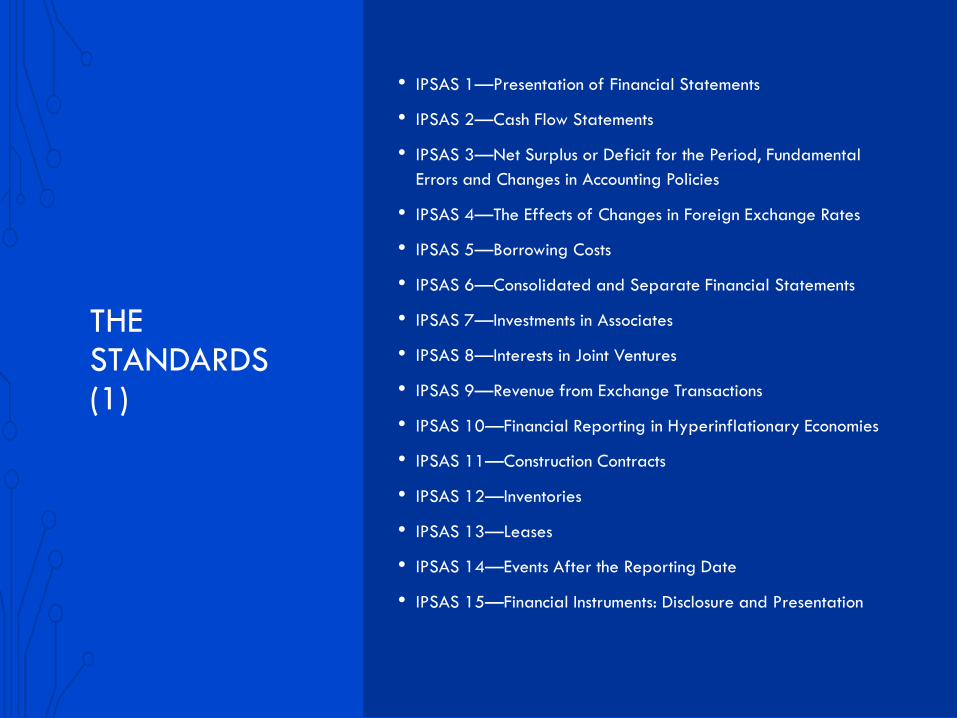

THE STANDARDS (1)

• IPSAS 1—Presentation of Financial Statements

• IPSAS 2—Cash Flow Statements

• IPSAS 3—Net Surplus or Deficit for the Period, Fundamental

Errors and Changes in Accounting Policies

• IPSAS 4—The Effects of Changes in Foreign Exchange Rates

• IPSAS 5—Borrowing Costs

• IPSAS 6—Consolidated and Separate Financial Statements

• IPSAS 7—Investments in Associates

• IPSAS 8—Interests in Joint Ventures

• IPSAS 9—Revenue from Exchange Transactions

• IPSAS 10—Financial Reporting in Hyperinflationary Economies

• IPSAS 11—Construction Contracts

• IPSAS 12—Inventories

• IPSAS 13—Leases

• IPSAS 14—Events After the Reporting Date

• IPSAS 15—Financial Instruments: Disclosure and Presentation

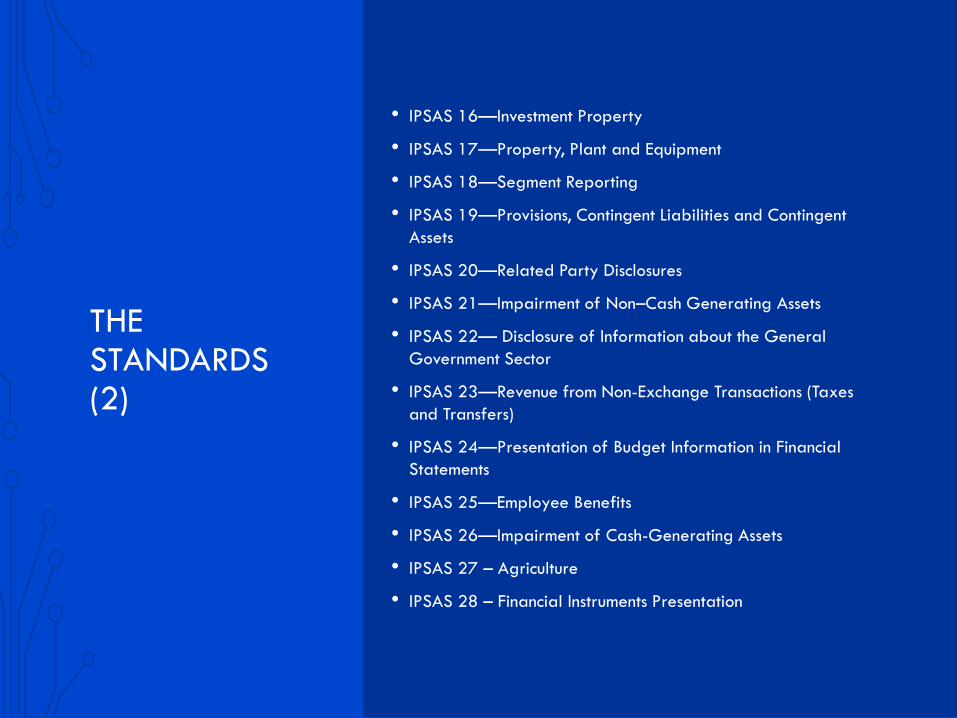

THE STANDARDS (2)

• IPSAS 16—Investment Property

• IPSAS 17—Property, Plant and Equipment

• IPSAS 18—Segment Reporting

• IPSAS 19—Provisions, Contingent Liabilities and Contingent

Assets

• IPSAS 20—Related Party Disclosures

• IPSAS 21—Impairment of Non–Cash Generating Assets

• IPSAS 22— Disclosure of Information about the General

Government Sector

• IPSAS 23—Revenue from Non-Exchange Transactions (Taxes

and Transfers)

• IPSAS 24—Presentation of Budget Information in Financial

Statements

• IPSAS 25—Employee Benefits

• IPSAS 26—Impairment of Cash-Generating Assets

• IPSAS 27 – Agriculture

• IPSAS 28 – Financial Instruments Presentation

THE STANDARDS (3)

• IPSAS 29 – Financial Instruments Recognition and

Measurement

• IPSAS 30 - Financial Instruments Disclosure

• IPSAS 31 – Intangible Assets

• IPSAS 32 – Service Concession Arrangements Grantor

• IPSAS 33 – First Time Adoption of Accrual Basis IPSAS

• IPSAS 34 – Separate Financial Statements

• IPSAS 35 – Consolidated Financial Statements

• IPSAS 36 – Investments in Associates and Joint Ventures

• IPSAS 37 – Joint Arrangements

• IPSAS 38 – Disclosure of Interests in Other Entities

• The above are new and will replace IPSAS 6, 7 and 8

• Cash Basis IPSAS—Financial Reporting Under the Cash

Basis of Accounting

APPLICATION

• General purpose financial statements

• All public sector entities

National

Regional (e.g. state, provincial or territorial)

Local government (e.g. city towns)

And their departments, agencies, boards,

commissions

• Do not apply to Government Business Entities

Is an entity with the power to contract in its

own name

Financial and operational authority to carry

on a business

Sells goods and services at a profit or full

cost recovery

Is not reliant on continuing government

funding to be a going concern

Is controlled by a public sector entity

SOME PRACTICAL POINTS

•How does the World Bank and other donors determine which

projects to support across over 100 countries (with different

currencies, languages, religions, culture and relative need)? How is

success measured?

•How does the UN or NATO determine relative contributions of

nation states to international initiatives (the cost of maintaining

troops and equipment in a foreign country, where several currencies

and accounting practices may be involved)?

•How does a free trade area decide if the State Aid regulations

have been breached and by how much?

•How does a free trade area fix trade limits for non-participating

countries and how is it monitored?

Values and measuring systems vary across the world,

making comparisons difficult

INTERNATIONAL PUBLIC SECTOR ACCOUNTING STANDARDS

FINANCIAL STATEMENTS GENERAL

FINANCIAL STATEMENTS

The components of financial statements are:

•A statement of financial position (balance sheet)

•A statement of financial performance (revenue account)

•A statement of changes in net assets/equity

•A cash flow statement

•When the entity makes publicly available its budget, a

comparison of budget and actual amounts

•Notes, comprising a summary of significant

accounting policies and other explanatory notes

The principal requirements are set out in IPSAS 1

WHAT ARE FINANCIAL STATEMENTS FOR?

• Reporting performance to shareholders and stakeholders

• Providing information about the sources, allocation and uses of

financial resources

• Providing information about how the entity financed its activities and

met its cash requirements

• Providing information that is useful in evaluating the entity’s ability to

finance its activities and to meet its liabilities and commitments

• Providing information about the financial condition of the entity and

changes within it

• Providing aggregate information useful in evaluating the entity’s

performance in terms of service costs, efficiency

and accomplishments

• Providing information for potential investors

FINANCIAL STATEMENTS

• Financial reporting may also provide users with information:

• Indicating whether resources were obtained and used in accordance with

the legally adopted budget

• Financial statements can also have a predictive or prospective role, providing

information useful in:

• Predicting the level of resources required for continued operations

• The resources that may be generated by continued operations

• The associated risks and uncertainties

• Indicating whether resources were obtained and used in accordance with

legal and contractual requirements, including financial limits established by

appropriate legislative authorities

FINANCIAL STATEMENTS IN THE PUBLIC SECTOR

There are additional reasons for public service organisations to report:

• Accountability to the public

• Stewardship

• Corporate governance

• Reporting on the financial mandate

• Reporting on performance

• Reporting on the financial health of the Government and the nation

• Part of the basis for financial planning in future

• Promoting debate and discussion on the level of

public expenditure

• Basis for scrutiny and audit

FINANCIAL STATEMENTS

Financial statements provide

information about an entity’s:

• Assets

• Liabilities

• Net assets/equity

• Revenue

• Expenses

•Other changes in net assets/equity

• Cash flows

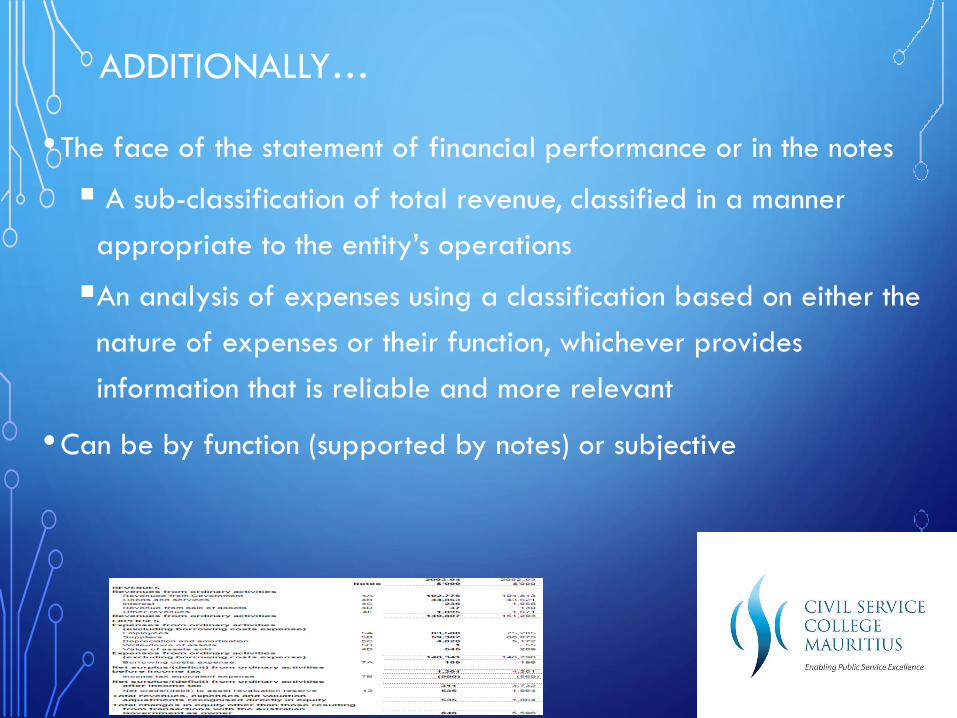

ADDITIONALLY…

•The face of the statement of financial performance or in the notes

A sub-classification of total revenue, classified in a manner

appropriate to the entity’s operations

An analysis of expenses using a classification based on either the

nature of expenses or their function, whichever provides

information that is reliable and more relevant

•Can be by function (supported by notes) or subjective

GENERAL

• ‘Going concern’ basis other than when

being liquidated or ceasing operation

• Consistency in presentation unless:

• Significant change in operations

demands changes

• Financial statements have been

reviewed

• Changes in an IPSAS

• Materiality and Aggregation

• Each material class presented

separately

• Offsetting – assets and liabilities and

revenue and expenses not to be offset

(unless so specified by IPSAS)

• Include comparative information for

previous year

• Reporting period at least annually and

QUALITIES• Understandable with reasonable knowledge

• Relevant and material

• Reliable

Faithful representation – substance over legal form

Neutral in presentation

Prudence – conservative but not excessively so (for instance excessive

provisions or reserves)

Completeness

• Or “the truth the whole truth and nothing but the truth”!

• Comparability and consistency

Between entities

Over time

TRUE AND FAIR VIEW

• ‘True and Fair View’ concept has been at the heart of UK accounting

practice for over 40 years

• The Financial Statements should show a ‘true and fair view’ of the financial

position of the entity

• This is checked and affirmed by the External Auditor

• BUT never defined in UK law

• Gaining in international importance in recent years (Austria, Finland,

Sweden….12 states of the EU)

• Adopted by the European Union (4th Directive on company law)

• Ambiguous and not easily exported across the world

• May be inappropriate for IFRS

• Concept of fair value

FAIR PRESENTATION

The Standard clarifies that fair presentation requires

the faithful representation of the effects of transactions,

other events and conditions in accordance with the

definitions and recognition criteria for assets, liabilities,

revenue and expenses set out in the IPSASs.

Previously, fair presentation was not defined.

FAIR VALUE

•Not easy to define

•Originally, public service organisations used historical cost

•Fair value introduces the concept of regular revaluations

•Harder on plant and equipment

•Market value often used as best reflection of fair value

•But which market?

THE MAJOR ISSUES

• The major areas that will affect many organisations include:

•Accruals

•Asset and capital accounting

• Treatment of PPPs

• Leasing

• Financial Instruments

• Pensions

•Others may have major impacts on your organisation but the

above are the main ones

• Identify:

• potential impacts on your accounts

•Actions to implement compliant

accounting treatments

ACCRUALS

•Considerable transactional task

•Changes the nature of budgetary control (controlling the cash

works much less well)

•Needs to be understood by managers not just finance

•The use of P2P system functionality can help considerably

•The heart of the standards

ASSET & CAPITAL ACCOUNTING

•Capitalisation of expenditure on assets with a life of over

a year

•Application of depreciation and amortisation

•Difficult for many managers to understand

• Impact of impairment on the accounts

• if you think managers find depreciation difficult!

•Decisions on accounting treatment

•Depreciated historic cost

•Revalued (but sill depreciated)

•More assets being brought into capitalisation

PPP AND LEASING

• Many PPPs involve the provision of assets to the public sector by the

private sector

• The majority of these assets are likely to form part of the public

sector organisation’s assets

• Under Service Concession Grantor standard fixed asset and

depreciation recognised

• Effect of changes has to be understood

• Complicated accounting rules

• Leasing standards changing

• All leases – operational and finance leases need to be treated as

assets of the lessor

• Previously only Finance Leases had to

be recognised as assets

• Cause of major fallout with the USA

FINANCIAL INSTRUMENTS

•Very complex area

• Introduces the need to account

for a range of instruments or

account differently:

•Concessionary loans

•Financial Guarantees

•The concept of Effective Interest

Rate applied to public sector

bonds

•Even more complex and

demanding in the private sector

•Reaction to the banking crisis

PENSIONS

•Governments usually have huge

occupational pension liabilities

•Under cash accounting they do not

appear in the accounts

•With IPSAS, pension liabilities and

assets appear in the accounts

• If unfunded or if there is a

shortfall it can make the balance

sheet appear very unhealthy

• The accounting arrangements are

complex and can require system

changes and actuarial input

RATIOS THAT CAN BE APPLIED

• Profitability Ratio – Profit after Tax/Capital and Reserves

• Debtor Days – Trade Debtors/Sales

• Creditor Days – Trade Creditors/Purchases

• Current Ratio – Current Assets/Current Liabilities

• Acid Test – Current Assets – Stock/Current Liabilities

• Rate of Return on Capital Employed (ROCE)

• How do these apply to

public sector organisations?

SUITABILITY FOR DEVELOPING COUNTRIES (1)

• Does government accounting

reform assist development?

Accounting reform expensive

The benefits are indirect

compared to capital

infrastructure investment

• But institutional rather than

bureaucratic infrastructure

Better management of

resources?

More accountability?

Track money against

results

Pressure from donors

SUITABILITY FOR DEVELOPING COUNTRIES (2)

• Increasing demands for open Government and access to information

• Greater demand for meaningful information

• Willingness to implement so financial and technical assistance is available from other countries

In democracies

• Still pressure for information from international media

• Pressure from free-trade partners or trade/product organisations

• Pressure from donors

• Improved information of value in Government decision-making

In non-democratic countries

DEVELOPING COUNTRIES

•For the public sector, the shift towards sovereign debt

being financed through bond issues will have an impact

•Private sector lenders will expect understandable

(compliant) accounts

•Capital markets will need to be developed further

•Credit ratings will be closely scrutinised

CONCLUDING REMARKS

• International Accounting Standards being

widely adopted across the world

• Stimulus is from the accounting profession

rather than Governments

• Clear need for commercial organisations to

report performance on a consistent and

reliable basis in a world market

• Differences between private sector and

public sector financial reporting are much

fewer than originally believed

• Move from cash accounting has financial

reporting and planning benefits

• Greater accountability and stewardship is

expected across the world

• This may be a club it is wise to be a

member of

• It doesn’t feel like a movement to impose

standards from the developed world on the

developing world……but