Embed Size (px)

Citation preview

International long-term Investment & financingDr. S H UZMAAsst. ProfessorSchool of ManagementNIT Rourkela

•Let us all be happy and live within our means, even if we have to borrow the money to do it with.

•Artemus Ward

The spread (the difference between the bid and the ask price of a security asset).

• The interest paid on syndicated loans is usually calculated by adding a spread to the London interbank offer rate (LIBOR) or another reference rate such as the US prime rate or the Singapore interbank offer rate (SIBOR).

• Determinants of the spread•Availability of funds•Creditworthiness of borrowers•Maturity •Fees

EQUITY FINANCING• The country in which shares should be issued• Euroequities: Share issues involving sales of new

shares outside the home country are called Euroequity issues.

• Investor protection and disclosure requirements• American Depository Receipts (ADRs): An ADR is

essentially a receipt issued by a depository bank in the United States that is backed by foreign shares that are deposited with a custodian bank in the country of issue of the original shares. ADRs are quoted and traded in U.S. dollars just like domestic U.S. shares.

International equity financing• Primary market functions: underwriting of new

equity issues• Secondary market functions: trading of

equities abroad• Reasons for listing on foreign stock

exchanges:• To improve the liquidity of existing shares• To boost political and commercial visibility in

foreign countries• To support a new equity issue• To broaden ownership

•Costs of foreign listing: One cost of foreign listing is greater disclosure requirements

•Selling shares in international markets:

•Private placements underwritten by institutions from the host country

•Selling Euro-equity issues•Selling a subsidiary’s shares to foreign

investors•Selling shares to a foreign firm to form an

alliance

BOND FINANCING

•The same two issues arise with bond financing as with equity financing, namely, (1) the country of issue and (2) the vehicle of issue.

•If a US company sells a US-dollar-denominated bond in Britain, the currency of issue is not that of the country of issue. In the former of these situations the bond is called a foreign bond; in the latter it is called a Eurobond.

Foreign bonds versus Eurobonds•A foreign bond is a bond sold in a foreign

country in the currency of the country of issue. The borrower is foreign to the country of issue, hence the name. For example, a Canadian firm or a Canadian provincial government might sell a bond in New York denominated in US dollars. Similarly, a Brazilian company might sell a euro-denominated bond in Germany.

•Eurobonds are placed (sold) in countries other than the country in whose currency the issue is denominated.

•Foreign bonds are issued by borrowers who are foreign to the country where the bonds are placed

•The bonds are denominated in the country’s currency

Nicknames of foreign bonds

•Yankee bonds (United States)•Samurai bonds (Japan)•Bulldogs (United Kingdom)•Matilda bonds (Australia)•Reasons for the emergence of the

Eurobond market:•Absence of regulatory interference•Less stringent disclosure requirements•Favourable tax status

Types of international bonds• Zero-coupon bonds (rendering profit at maturity when the bond

is redeemed for its full face value).• Multicurrency bonds (the issue and amount and interest

payments are agreed in different currency to that agreed for the repayments).

• Global bonds: introduced by the World Bank in 1989. Most of these bonds are dominated in the currency of where the company is based). The characteristics is that these bonds are highly liquid.

• Novel bonds: represent financial innovation in the bond market. Examples are reserve floaters (on which coupon rate falls and market interest rate rises), asset backed bond (are backed by a specific group of assets), catastrophe bonds (whose payment depends on materialization of a certain events) and indexed bonds (whose payments are tied to general price level or a particular commodity).

Selecting the currency of issue

iSi

Where i= is the underlying interest rate, S. = is the annual percentage of change of the exchange rate between 0 and n.

•If this condition is satisfied, the bond issue should be dominated in a foreign rather than the domestic currency.

•Eg. An Australian company should, choose a Swiss franc issue rather than an Australian dollar issue. If the bond were sold in any other country, it would be a Eurobond issue.

i S i

On the other hand, if the above equation, then the issuing firm should use domestic currency denomination. In the case of the Australian firm, if the bonds were sold in Australia, it would be a domestic bond issue rather than an international issue. If the bonds were sold outside Australia, it would be a Eurobond issue.

)()( aaddS

A foreign equity investment is preferred if:

Where d* and a* are dividend yield and the rate of capital appreciation associated with foreign equity investment. Which means that foreign equity investment may be preferred even when it offers lower dividend yield and rate of capital appreciation than domestic equity investment. This would be the case if the foreign currency appreciates by more than the sum of the dividend yield and capital apprciation rate differential.

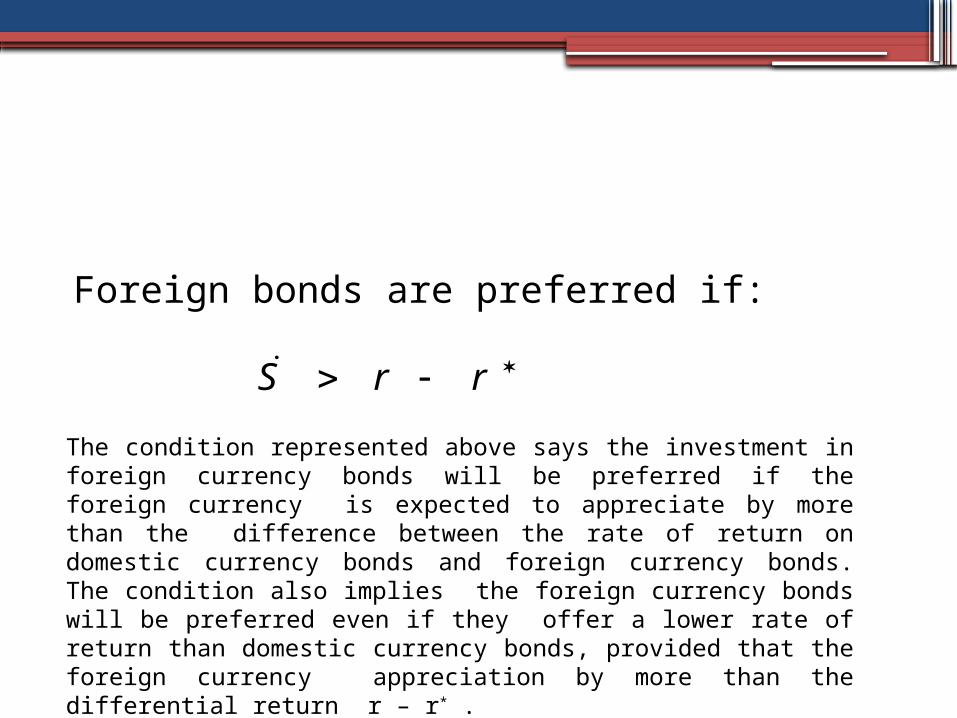

rrS

Foreign bonds are preferred if:

The condition represented above says the investment in foreign currency bonds will be preferred if the foreign currency is expected to appreciate by more than the difference between the rate of return on domestic currency bonds and foreign currency bonds. The condition also implies the foreign currency bonds will be preferred even if they offer a lower rate of return than domestic currency bonds, provided that the foreign currency appreciation by more than the differential return r – r* .

Borrowing with foreign-source income

•There may be less foreign exchange exposure and risk involved in foreign-currency borrowing than in domestic-currency borrowing when the borrower is receiving income in foreign exchange and is facing a long exposure in the foreign currency. That is, foreign-currency receivables can require a negative premium when borrowing in foreign exchange because exposure is reduced.

Tax considerations• Bond buyers who pay a lower tax rate on

capital gains than on interest income prefer a dollar of capital gain from foreign-currency appreciation to a dollar of interest income. This means that if, for example, the dollar-bond interest rate was equal to the yen-bond rate plus an expected appreciation of the yen, the yen bond would be preferred by lenders because it provide expected capital gain from an appreciation of the yen.

Other bond-financing considerations

• Issue cost• Issue size

•Multicurrency bonds•Not all Eurobonds are denominated in a

single currency. Rather, some Eurobonds are multicurrency bonds. Some multicurrency bonds give the lender the right to request repayment in one or two or more currencies.

BANK FINANCING, DIRECT LOANS•Parallel loans

A parallel loan involves an exchange of funds between firms in different countries, with the exchange reversed at a later date.

• a parallel loan involves an initial exchange of funds between firms in different countries, such that the transaction is reversed some time in the future.

Parallel loans and credit swaps

A parallel loan

• Rio Tint

o

• Toyota’s• subsidiary

• Loan

• Loan + interest

• Toyota

• Rio Tinto’s subsidiary

• Loan

• Loan + interest

• Australia• (AUD funds)

• Japan• (JPY funds)

Credit swaps:• A credit swap involves the exchange of

currencies between a bank and a firm rather than between two firms. It is an alternative method of obtaining debt capital for a foreign subsidiary without sending funds abroad.

• a credit swap makes it possible to acquire a loan for a foreign subsidiary without having to send funds abroad.

• It involves the exchange of currencies between a bank and a firm, not between two firms.

A credit swap

• BHP • NAB

• Deposit

• Deposit + interest

• BHP’s• subsidiary

• Correspondent bank

• Loan

• Loan + interest

• Australia• (AUD funds)

• Japan• (JPY funds)

GOVERNMENT AND DEVELOPMENTBANKLENDING• Government lending: governments of countries acting

as hosts to foreign direct investment may provide financing when they believe that the underlying projects will generate jobs, facilitate the transfer of technology and/or provide training for local workers

• It is not at all uncommon for financing to be provided by governments or development banks. Because government and development-bank financing is generally at favorable terms, many corporations consider these official sources of capital before considering the issue of stock, the sale of bonds, loans from commercial banks, or parallel loans from other corporations.

Other sources of financing

•Lending by international organisations: a number of development institutions grant developing countries loans to finance infrastructure projects.

•While these loans are granted to the host governments, the companies operating there are financed indirectly.

•International Development Agency (IDA)•International Finance Corporation (IFC).

OTHER FACTORS AFFECTING THEFINANCING OF SUBSIDIARIES• Generally, the more financing is denominated in

local currency of income, the lower the danger from changing exchange rates. This supports the use of debt. Reinforcing the tendency toward using debt is the greater political sensitivity with regard to repatriating income on equity than with regard to receiving interest on debts.

• Certain governments require that a minimum equity/debt ratio be maintained, while some banks also set standards to maintain the quality of debt.

FINANCIAL STRUCTURE• Subsidiary or parent determination of financial structure

If the success or failure of an overseas subsidiary has little or no effect on the ability of the parent or other subsidiaries to raise capital, decisions on financial structure can be left to subsidiaries. A subsidiary can then weigh the various economic and political pros and cons of different sources of funds and adopt a financial structure that is appropriate for its own local circumstances.

• Capital structure in different countriesFinancial structure varies from country to country. Possible reasons for the variations can be found in explanations of capital structure commonly advanced in a domestic context. These explanations hinge on the tax deductibility of interest payments but not dividends, and on bankruptcy and agency costs.

Summing Up• If capital markets are internationally integrated, the cost of

capital should be the same wherever the capital is raised.• If capital markets are segmented, it pays to raise equity in

the country in which the firm can sell its shares for the highest price. It may also pay to consider selling equity simultaneously in several countries; such shares are called Euroequities.

• Low issuance costs may make some markets better than others for selling shares. Generally, the costs of selling shares are lowest in big financial markets such as New York.

• Firms must decide on the best vehicle for issuing equity and raising other forms of capital. In particular they must determine whether capital should be raised by the parent company or a financing subsidiary.

• A foreign bond is a bond sold in a foreign country and in the currency of that country. A Eurobond is a bond in a currency other than that of the country in which it is sold.

• Firms must decide on the currency of issue of bonds. All foreign-pay bonds are by definition in a foreign currency for the firm, and many Eurobonds are also in a foreign currency for the firm.

• Large gains or losses are possible from denominating bonds in currencies that are not part of a firm’s income. For this reason a risk premium may be demanded before speculating by issuing foreign-currency-denominated bonds.

• When a firm has foreign-currency income, foreign-currency borrowing reduces exchange-rate exposure. Therefore, a firm may be prepared to pay higher interest on a foreign-currency-denominated bond than on a bond denominated in domestic currency.

• When bond buyers face lower tax rates on foreign exchange gains than on interest income, it may pay to issue strong-currency bonds. These will have relatively low interest rates because they offer bond buyers part of their return as capital gain.

• Bond issuers should consider costs and sizes of bond issues when determining the country of issue.

• Bonds denominated in two or more different currencies, called multicurrency or currency-cocktail bonds, will appeal to lenders if there are costs associated with forming portfolios of bonds denominated in single currencies.

• A substantial proportion of financing of overseas subsidiaries is provided from within multinational corporations.

• Parallel loans are made between firms. They are particularly useful when there are foreign exchange controls.

• Credit swaps are made between banks and firms. They are also a way of avoiding foreign exchange controls.

• Political risk can be reduced by borrowing in countries in which investment occurs; this tends to increase debt/equity ratios of subsidiaries.

• Because parent companies tend to honor subsidiaries’ debts whether legally obligated to do so or not, a parent company should monitor subsidiaries’ debt/equity ratios as well as its own global debt/equity ratio. Nevertheless, parent companies should allow variations in debt/equity ratios between subsidiaries to take advantage of local situations.

• If a country has a high debt/equity ratio, this can be because of high tax shields on debt, or low bankruptcy or agency costs.

• The links between banks and corporations in Japan, Germany, and some other countries may explain the high debt/equity ratios in these countries. However, it does appear in general from the within-country variations in financial structure that industry- and firm-specific influences on financial structure are more important than country effects.

Reference

•Maurice D. Levi (2005) International Finance, 4th Edition, Routledge

![Development of microcontroller based over-current …ethesis.nitrkl.ac.in/6129/1/110EE0228-6.pdf[2] Department of Electrical Engineering, NIT Rourkela, Odisha, India - 769008 Certificate](https://img.pdfslide.us/doc/110x75/5aa7ce5f7f8b9ab8228cbc14/development-of-microcontroller-based-over-current-2-department-of-electrical.jpg)

![NATIONAL INSTITUTE OF TECHNOLOGY ROURKELA...Page - 2 of 12 NIT Rourkela - EPTP Admission Notice [2020-21] Sl. No. Name of the Department Code Specialization for Part-Time M. Tech](https://img.pdfslide.us/doc/110x75/60ced0515d5db159974d30d5/national-institute-of-technology-rourkela-page-2-of-12-nit-rourkela-eptp.jpg)