Embed Size (px)

Citation preview

INTERNATIONAL INSOLVENCY INSTITUTE

One Size Fits Some: Single Asset Real Estate Bankruptcy Cases

Kenneth N. Klee

From

The Kenneth N. Klee Collection

in

The International Insolvency Institute

Academic Forum Collection

http;//www, iiiglobal.org/component/jdozvnloads/viezucategor~/650.html

International Insolvency Institute

PMB 112

10332 Main Street

Fairfax, Virginia 22030-2410

USA

Email: [email protected]

OInternational Insolvency Institute 2011. All rights reserved.

Admin*1584723.1

ONE SIZE FITS SOME: SINGLE 1~SSE'T REALESTATE I3ANKRUPT~Y ~ASES~

Kenneth N. Kleej-~-

For several years tc debate has raged over whether .single asset real estate

ctcses should be singled ou"t for special treatment under the Bankru~itcy Code.

Under the current .~4 million debt ca1~, these cases involve apartment housesand sm~cll office buildings. But Goth Houses of Congress have ~iasser~ legzsla-tion that will re~ieal dhn, $4 million ca~i, potentially subjecting large officebuildings, sho~~iin~ centers, and ~ierhaps hotels to ex~iedited discriminatorytreatment in Chapter Y 1 reorganization cases. In this Article, Professor Kleeattempts to inform the debate by presenting empirical data gathered from anational questionnaire and cross-checking the data against the case files of abunlzru~tcy judge in the most active judicial district in tlae country. Tlaeresults are striking. Asset values rather than amounts ozuin~• stand out asreliable predictors of Milan confirmation. Sur~irisingly, 'value-to-loan ratiosare less reliable than asset values standing alone. The data shorn t12at va.lu-~~ble properties have u much greater ~irobaGility of confirming a f lan thanless valuable ~ro~ierties. The Article suggests that if Congress desires to dis-criminate against single asset real estate debtors, it should draw the line ata~i~iroximately .~7—~8.2 million in asset value rather than changing currentlaze to discriminate against all single asset real estate debtors.

INTROAUCTTON .................................................1286

~. WHY REUI2GANTZ~ S~ CASES AT ALI.? ........ . ......... 12$9

A. The History of Real Property ReorganizationCases...............................................1289

B. How Chapter 1 J. Functions for SAIZ~ Debtors .......1293C. Arguments For and Against Reorganization ......... 1296D. The Politics .........................................1302

IT. Z'I-IF. 2001 AMENDI~I~N'I' EXPLODES THE GE1T' ...............1303

A. The Rationale £or Congressional Action ...... , , ....1303

-~ O 2002, Kenneth N. Klee. All Rights Reserved.-~•f Professor of I.aw, University of Calitornza at Los Angeles (UCLA} School of Law.

The author gratefully appz~eciates and ack~~owledges comments of Professors Daniel J. Bus-sel, Caroline Gentile, Robert Goldstein, Lynn M. L.oPucki, 12ichard Sander, T~irk Stark, andElizabeth Warren, on previous drafts o£ this Article. The author gratefully appreciates andacknowledges valuable technical assistance by Joseph Doherty, Associate Director for Re-search, Empirical Research Group, UCLA School of T.,aw, azzd research assistance by JacobSimon, UCLA. School of I,aw, Class of 1998, Steven Cademartori, UCT..A School of Law,Class of 2000, and Arusi Loprinzi, UCLA School of Law, Class of 2003. The author is alsograceful for generous funding from the National Conference of Bankruptcy Judges ~ndow-mentfor Education and the Faculty Grants Program awarded by the Council on Researchof the Academic Senate at UCLA.

].285

1288 CORIVLI,L LAW .I-~EVIEU~ [Vol. 87:1285

aftei the order° for relief, unless "the debtor has filed a plan of reor-ganization that has a reasonable possibility of being con~rrried withina reasonable time,"10 or the debtor in possessionll has comrrzencedmonthly paynnents equivalent to interest'` to each secured cx-editor.13

If the X001 Axxzendment becomes law, however, mortgage holderscan prernat:urely flush out of the bankruptcy system some large realestate developers or owners that have liquidity problems before thelatter have a reasonable chance to reorganize.'` By threatening to doso, mortgage holders can control the Chapter 1 X process to their ben-efit. They can deczde 'whether to seize the property for potential up-side gain or leave it in Chapter 11 to serve their other purposes.l'Their benefit will come at the expense of property owners, generalunsecured creditors, and the public that subsidizes the cost of operat-ing the banlrruptcy system to achieve a public good.

.After testifying before Congress about the forerunner of the 2001Amendment, I recognized the desirability of gathering empirical datato determine whether large SA.RE debtors differed From small SAKEdebtors in their Chapter 11 experiences. X exazz~ix~ed the case law andgathered information in unreported cases to determine whetherSA12E debtors conf rmed Chapter 1 X plans. By analyzing plan confir-mation rates over the past t~cventy years, this Article tests the wisdorri of

ing text (discussing the uncertainty of an extension motion due to judicial hostility towardSAS debtors).

1~ 11 U.S.C. § 362(d} (3) (A).

I 1 Although the statute refers to a "debtor," it actually means a "debtor in possession"acting as the legal representative oP the bankruptcy estate. See icl. ~§ 323(a), 1107(a).lz Soane courts and comrnez~tators mistakenly characterize the statute as requiring the

payment of interest. Kather, the payments are "in an aznotu7t equal to interest." Sec i.d.§ 3G2(d) (3) (B). Unless the creditor is oversecured or ehe debtor is solvent, the statutefoz-bids the pay►nent of postpetition interest. See id. ~~ 502(b) (2), 506(b), 726(a) (5). Infact, if the crediCOr is oversecured, alChough postpetition interest witl accrue under~ 506(b), the statute might forbid the payment of postpetitioi~ interest prior to the conclu-sion of tl~e case as well. See Orix Credit Alliance, Iz~c. v. Delta Res., Inc. (X~z ~e Delta Res.,Inc.), 54 F.3d 722, 730 (11th Cir. 1995).

1 =; See '11 U.S.C. § 362(d) (3) (B).

i`~ See Ira ~e Klcernko, Inc., 181 B.R. 4'7, 4J (Bankr. S.D. Ohio 1J95) (noting that thepurpose of § 3G2(d) (3) is to "impose an expedited time frame for filing a [confirmable]plan" in SAKE cases); David B. Young, Automatic Stay Isseces: Selectecl Decent Develvjrmrn~s, in 2232'Cl l~NNUi11.. ~iURR13N't DL.VLLOPNII?NTS IN ~ANKRUPTC:Y AND REOIiGA~IIZ.~ITION ~, ~1 ~~I.Z

Commercial Law &Practice Course, Handbook Series No. A-820, 2001) ("11 U.S.C.362 (d) (3) ...seeks to place tl~e debtor ors a fast crack and to permit the rxioi•t~age lender

to foreclose unless the debtor acts swifCly.").

1 -"> `That is why mortgage holders financed the lobbying effort to press for this amezid-rnent. See generally 73~enlz~~te~itcy, at http://www.opensecrets.org/news/bankruptcy/in-dex.hmi (last visited Mar. 15, 2002) (indicating that during the 1999-2000 lobbying cycle,finance and credit card companies contributed ~9 million, and that during the same cycle,cornmerciai banks contributed X29 million, and credit unions coiatriUucc;d x$2.1 million—almost two and a half trines the amount spent by this industry dux'ing the 1996 presidentialcampaign}.

2002] ONE S17~ FITS SOMA J.28g

treating large and small SAIZ~ debtors alike in a manner diffea eastfrom all other Chapter 11 debtors,

Part I of this Article examines the history and policy behind SAREreorganization and asks a threshold question: Why should SAKE debtors have the opportunity to reorganize at all? Compelling policy rea-sons favor reorganization of SARE debtors, even though theories ofallocative efficiency might indicate otherwise. Part XI reviews the 2001Amendment's uniform procedure for all SAKE reorganizations bycharging the definition of SAKE to eliminate the $4 million cap andanalyzes the policies that the amendment implicates. Part III dis-cusses original data analyzing real estate cases to see how they fared ixzbankruptcy and finds that larger S.f1.RE debtors above the $4 millioncap have higher Chapter X 7 confirmation rates. In Part IV, this Articleargues that these findings do not justify Congress's proposal to repealfile SAKE ~4 million cap because Chapter 11 £unctions well for largerSAKE debtors. Congress acted on the basis o£ a hunch instead o£ do-ing its homework.

IWHY ~ORGANIZ~ SARE CASES AT L~.I.,L?

The question 'whether or under what conditions single asset realestate cases should be able to reorganize under the Bankruptcy Coderequires an evaluation of the costs and benefits of reorganization ascompared to foreclosure under state law. To place the evaluation ii1context, this Part begins with a brief history of real property reorgani-zations and describes how Chapter 11 reorganization cases work. Itexamines the arguments for and against allowing SA.R~ cases access toChapter 11 at all and focuses on the political motivations that led tothe adoption o£ the 200]. Anaendnnen.t rather than exclusion of SAKEdebtors from Chapter I1.

A. The Histo~c~y of Real Property Reorganization Gases

During the 1930s, the deteriorating economic climate in theUnited States led to massive defaults in the repayment of real propertymortgages.16 Eco~~~mic disaster threatened not only the debtors whoowed mortgage obligations, but also the financial institutions, particu-larly savings banks, that held the mortgages." As debtors defaulted,

lc See T-Iomer I~'. Caz•ey, Re«l Fro~ier~ty: Post De(~•ression a~n.cl Futzere,,J. Lrcwi. & PoL. Svc:.,Apr. 1943, ae 101, ].O1 ("Foreclosures reached staggering proportions [fl•om 1931 to 1~J35]and bankruptcies were occurring at an ever accelerating rate,").17 ,SCC ~LYfUS WICI{L.R, THIi ~AN[CING ~r1NICS OFD THF. Gx~nr• DeYxcsstoN 1G (1996) ("Real

estate lending, px-ixilarily nonfarnz, , ..was an important source of ttx~settled banking mar-kets during the Great De~~ression."); Milton EsbitC, Bcenit Portfolaos and Bccnk Tc~ilza~res During

tlae Great Detnession: CTticccgo, 46 J. Eco~v. HisT. 455, 45'7 (1986) ("[~']ully 95% of the bank

ecoubles in Chicago were predicated on real estate." (internal quotation marks omitted));

1290 CORNELL LAW REVIEW [Vol. 87:1285

~o~ tgage holders connmenced Foreclosure proceedings and financialinstitutions began to hold recoi d title to enormous amotYnts of realproperty.' Mazy of these financial institutions faced the Hobson'schoice of holding real estate that generated little income but carriedtax, maintenance, and insurance liabilities, or selliizg the real estateinto a thin nnarket with :few b~,tyers and distressed prices.l`' Yet inmany states, financial institutions could i~ot intervene to protect theirinterests by Foreclosing on mortgaged properties, because the stateshad imposed moratorium laws to suspend foreclosures.z~' As a result,the United States faced the prospect of numerous financial institutioninsolvencies.21 In addition, Congress saw a risk of undermining theU.S. economic system by allowing real property defaults to cause per-vasive dispossession of private ownership. Partially to ameliorate thissituation, Congress enacted Chapter XII of the Bankruptcy Act to per-mit individual and partnership debtors who owned real property theopportunity to reorganize.22 By ernacting Chapter XII, Congress cre-

Thomas S. Stone, Mortgage Moruto~zt~, 1 X Wis. L, ItLV. 203, 206 (1935) ("The wave of foreclo-sures ...was of little benefit to creditors."); Current Legislation, Emergency Mortgage I egisl~-tio~z, 8 Sr. JoHVS L,. REV. 204, 206 (1933) ("Savings banks and insurance companies withtheir millions in mortgages ...were caught in the deluge of foreclosure and in this time of~chaos, President Roosevelt declared the Banking Holiday.").

1H See Carey, su~rra note 16, at 104 (" [P] roperty passed in great volume to the creditorclass during the intezval from J930 to 1937."). Contemporary litex-ature contains the fol-lowing hyperbole: "When one realizes that approximately 5U per cent of Che farm lands inCentral and Northern California are conCrolled by one institution—the Bank of America—tlie irony o£ these ̀ embittered' Farmers defending their ̀ homes' against strikers becomesapparent." CAREY MCWTLLIAMS~ FACTORIES IN "I'H~ FIELD: THE STORY OF MIGRATORY FARNfLABOC2 IN CALIFORNIA 233 ~I939~.

1~ See, e.g., Stone, su~ira note 17, at 206 {"[T]he past few years lave found banks andother lending i~ZStitutions loaded down with physical properties which they cannot oper-ate."); Arthur E. Sutherland, ,Jr., Foreclosure and Sale: Sonae Suggested Clcanges in tlae Nezu YorkP>•ocedure, 22 CoKNi:LL L.Q. 216, 217 (193) ("The gxeat lending institutions are reluctantto load themselves with foreclosed real estate ....").

Z~~ See, e.~:, Robert H. Skiiton, Mm~gage Moratoria Since 1933, 92 U. Pa. T.. 12rv. 53, 88(1943) ("The chief criticism that may be made of the New York moratorium is that it wastoo inclusive. Commercial properties , ..were protected against the consequences of de-fault in principal.") ; see ~ilso William L. Prosser, The Minnesota Mm•tgr~ge Moratorium, 7 S. CAL.I~. 12~v. 353, 355, 360–G3 (1934) (discussing Minnesota's executive and legislative responsesto the wave o£ foreclosures and forced sales); Stone, su~rrca note 17, at 219-20 (discussingthe Wisconsin Mortgage Moratorium Law of 1933); Current Legislatio~~, su~ircc note 17, at206-09 (discussing New York's nnortgage moratorium statutes).z1 See Raymond J. Mischler, After tlae Mortgage Moratorium—W{aat?, 19 Iowa L. RLV. 560,

561 (1934) ("Foreclosures and forced sales were reaching proportions that threatenedstate and national stability.").

z~ See Morris W. Macey & M. ~1~zlliam Macey, Jr,, 1'fae C/aa1~ter XII Cla•rysalis, 52 A,u.Bwrrxx. LJ. 121, 123 (1978) ("Chapter XII was ...developed principally to meet an emer-gency situation prevalent in Illinois and, to some exteizt, Massachusetts."). Congxess en-acted Chapter XII as part of the Chandler Act of 1938, Pub. L. No. 75-696, ch. XII, 52 Stat.840, 9X6-30 (repealed Uy Bankruptcy Reform Act of 1978, Pub. L. No. 95-598, § 401, 92Star. 2549, 2682), and at the same Cline it passed Cl~apeer X of the Bankruptcy Act tofacilitate corporate reorganization o£ different kinds cif businesses, including those owningreal property. See id. ch. X, 52 Stat. at 8$3-905 (repealed by Bankrupi:cy .lZeform Act of

2002] ONE SIZE FITS 5011 1291

ated a beneficial legal mechanism to prevent financial institutionsfrom either conducting massive resales of foreclosed real estate intodepressed markets or retaining concentrated ownership o£ real prop-erty on their balance sheets. Before the enactment of Chapter XII,SAKE debtors either renegotiated consensually with their mortgageholders or liquidated the property under the Bankruptcy Act of 1898or state mortgage foreclosure laws.

When Congress enacted the Bankruptcy Code in 1978, it contin-ued to permit SAKE debtors to reorganize under the same laws andrules as other kinds of Chapter 11 debtors. A property owner was eli-gible to £ile for relief under Chapter 1 ]. whether the owner was anindividual, partnership, ox corpoxation.23 The 1978 Bankruptcy Codegave all kinds of SAKE debtors a breathing spell to permit them torestructure their property and their mortgage.

In 1994, however, the law changed fundamentally f'or some SAKEproperty owners when Congress adopted special rules fox SAKE debt-ors with secured debts o£less than ~4 million ("small" SAKE debtors}.In those cases, Congress restricted small SAKE debtors to an expe-dited Chapter 11 procedure designed to confirm a plan quickly orforce the debtor to pay the mortgage holder. Debtors who could doneither faced losing their property to Foreclosure. To protect ~cnortgage lenders in SAKE cases having secured debts n~.ot greater than ~4million,24 the 1994 amendments added an additional procedure bywhich a real property mortgage holder could obtain relief fronn ~ 362of the Bankruptcy Code's automatic stay against lien £oreclosure.25

1978, § 401, 92 Stat, at 2682); see ce~so Charlestown Say. Bank v. Martin (,i~n re Colonial RealtyInv.), 516 F2d 154, 158 (1st Cir. 1975). The court stated:

The power to prevent secured parties from availing o£ their contractualremedies ... ,and to compel those creditors ... in possession at the tinneof filing co return tl~e debtoz's property is essential to preserve the possibil-iCy of a successful rearrangement of the debtor's affairs. LitCle hope of re-suscitation would remain for the debtor disembowelled just prior to filing.

Id.z~ Individuals (]zuman beings), partnerships, and corporations are eligible to be

Chapter 11 debtors. See 11 U.S.C. §§ 101(41), 109(b), (d) (2000); ToibU v. Radloff, 501U.S. 157, 166 (1991} (holding tl~ac an individual debtor not engaged in business was eligi-ble to file under Chapter 11). See generally infra note 30 (discussing the meaning of theterms "individual" and "corporation" in the Bankruptcy Code). Individual debtors withregular income and noncontingent, liquidated secured debts less than $871,550 and non-contingent, liquidated unsecured debts less than $290,525 may Zile Chapter 13 cases in-stead o£ Chapter 11 cases. See 11 U.S.C. ~ 109(e) (2000) (as amended effective April 1,2001). Geizerally, Chapter 13 cases are less expensive and more effective than Chaptex J1cases. Thus, an individual SARA debtor who is eligible might choose Co fle a ChapCer 13case instead of a ChapCer 11 case. This Article assumes that the debtor files for relief underChapter 11.Z4 For the Code's definition of °single asset real estate," see ,su1yra• note 6.2~ See Bankruptcy Reform Act oi' 1994, Pub. L. No. 103-394, § 2]8(b), 108 Stal. ~k106,

4128 (codified as amended at 11 U.S.L. ~ 362(4)(3) (2000)); see infra note 2G. Lenderswith secured loans of al least ~4 million did not receive tl~e be~zefits of these protections,

1292 CORNELL LAW REVIEW [Vol. 87:1285

Section 362 (d) (3) permits a S.ARE mortgage holder to get relief fromthe automatic stay to foreclose unless, within ninety days after the or-

der for relief; the debtor files a confirmable plan ox begins makingmonthly payments to the mortgage holder.26 Thus the amendmentsminimize the mortgage holder's out-of-pocket loss by shortening theChapter 11 process or forcing the debtor to "pay to play" by makingcash payments to the lez~.der. This shifts the risk of delay from ehesecured lender to the debtor. It also creates a barrier to entry thatdiscourages small real estate owners from filing for Chapter 11 re-lief.~' Mortgage holders and their lobbyists justified the provisionbased on an alleged "shared experience" that, in most real estatecases, debtors file solely to delay foreclosure.2~ They convinced Con-

although they could seek relief from the automatic stay under § 362(d) (i) or (2). See 11U.S.C. § 362(d) (1)—(2). Presurn.ably Congress adopted the ~$4 million cap in 1994 becauseis thought that different policy concerns governed larger cases.

2~ Section 362(d) (3) provides as follows:

[The court shall grant relief from the automatic stay of § 362(a)] (3) withrespect to a stay of an act against single asset real estate under subsection(a), Uy a creditor whose claim is secured by an interest in such real estate,unless, not later than the date that is 90 days after the entry of the ordex forrelief (or such later date as the court may determine for cause by orderentered within that 90-day period)---

(A} the debtor has fled a plan of reorganization that leas a reasonablepossibility of being confirmed within a reasonably time; or

(B) the debtor has commenced monehly payments to each creditor•whose claim is secured by such real estate (other than a claim se-cured by a judgment lien or by an unmatured statutory lien), whichpayments are in an amount equal to interest at a current fair marketrate on the value of the crediCor's interest in the Y•eal estate.

11 U.S.L. § 362(d)(3).

L7 One commentator believed that the 1994 amendments would cause the bankruptcycourts to experience ixlcreased efficiency because the amendments would "minimize filingswhere nn real proUability of confirmation exists." See Co•~nmercircl rend Creclit Isszaes in Ba~xk-r~u1~lcy: Hea~~ing• Before t{te Subcor~t~~t. on Courts f~' Adnain. Practice of the Senule Gorra7~r.. o~z tlaeJecdiriri~y, 102d Long. 89 {1991) [llereinafcer Co~nntc~rcial tend Credit Hearing] (statement ofMary Jane Flaherty). Althougi~ it is obvious Chat a debtor would prefer aninety-day delayto immediate foreclosure, as a nnatter of cost/benefit analysis, the foregoing speculauo~~sappear to Ue sound. Debtors that own small real estate projects will be less inclined to paya bankruptcy attorney's retainer, a Chapter 11 filing fee, the quarterly U.S, crtrscee's fees,and the other substantial incremental cows of filing for Chapter• 11 when the limitations of§ 362(d) (3) operate to compress and restrict their opportunity to reorganize. See 23 U.S.C.§ 1930(x) (3), (6) (Supp. V 1999). At the margin, they will walk away and allow lenders toforeclose or give lenders a deed to the property in lieu of foreclosure. Another commenta-tor has speculated that the 1994 amendment would discourage small real estate debtorsfrom filing for Chapter 11 relief, thereby resulting in earlier foreclosures under sCaCe law.Sne,John C. Murray, Tlae Lencle>•'s Guide to Single tlsset Deal Estate 14an.1trz~1~tcies, 31 I2~nL T'ao►~.~'itoa. & TR. J. 393, 448 (1996).

LH See, e.g., Co•~nntercial a~xcl Credit Heardng, su~ira note 27, at 88-89 (statement of MalyJane Flaherty) ("The problem with single asset cases is that there is usually no reasonableprospect cif reorg'anizaCion. The bankruptcy filing is simply used as a legal method to delayforeclosure. I.e~~ders typically receive relief from the stay, but only after subseantial delayand expense.").

2002] ONE S.I/~Fs' FIIS SOME X293

gress that these cases seldom result in confirmed plans but instead usethe resources of the federal courts for improper dilatory purposes.z`•'

In 2001, once again bowing to pressure from mortgage holdersand their lobbyists, each House of Congress introduced and passedbills repeaxing the $4 million cap and subjecting all SARE debtors tothe expedited procedures that since 1994 had applied only to smallSAIZ~ debtors.

B. How Chaptea l.1 Functions for SAlZE Debtors

Befog°e analyzing the 2001 Amendment, it is usefiil to understandho~v Chapter 11 functions for SAIZE debtors and to consider whetherSARE cases should reorganize at all. Coni;inuing the pattern of fed-eral reorganization relief that started during the Great Depression,the Bankruptcy Code allows almost any kind of SA12E debtor to initi-ate aChapter 11 reorganization case, whether the debtor is ~n individ-ual, partnership, or corporation.~30 After filing a Chapter I1 petition,the debtor ordinarily remains as a debtor in possession9~' with the

L`~ See id,; Bankrtc1~tcy Xeforrn: Hearing Before the Sacbcomm. an F,con. f~ C:orrtmerci~cl Laru of

tlaeHouse Comm. on t,1ce,Jucliciccry, 103d Cong. 532 (]994) (statement of Warren T.asko, ~xec-

utive Vice President, IVlox~tgage Bankers Association of America} ("~'he survey also confirms

that Cliaptez• 11 is tieing used by developers and owners of single asset real prape~•ty for

delay, not f'or legitimate reorganization of a business."). The subcommittee manager of

ehe bill in tl~e House of Repx•eseritatives described the 1994 amendments as "desigr~ecl to

curtail bankruptcy fraud and abuse ax-~d reduce the unnecessax-y costs and delays of~ the

bankruptcy process." 140 Co~rc. Rre. H10,'771 (daily ed. Oct. 4, 194) (stateinciit of Rep.

Synar) .

''~> T'he Bankruptcy Code rises the Germ "individual" co mean a parCicular human be-

i~ag. .See Farm Fresh Poultry, Inc. v. Houton Co. (In rc~ Houton Co,), 43 B.K. 389, 391

(Bankr. N.D. Ala. 1984) ("The tez~An ̀ andi~~idual' is not i~~cluded in the definitions found in

11 U.S.C. § 101; however, it may be said to mean generally a single human being as distin-

guished from a social group or insCiCUtion.");David Swarthout, Noce, When Is ccn Indir~iclual

ci Co~~i~ratioya?—Wla~n, tlr.e Court 1l~Xisinter~rrets a Statute, 17zrct's Wlaeia!, 8 Ami. Ba,vita. T~sr. I..

Rev. 151, 152 ri.9 (2000) (citing '1"oiL~ v. Radloff, 501 U.S. 157, 160-61 (1991), for the

proposition that the Court's use of the term "individual" excludes "corporate clebCors and

only refers] to human beings."). The Bankruptcy Code's definition of "corpoz~acion"

pt•obably includes limited liability companies, limited liability partnerships, and business

tz•usts, but not true tz~usts. See ll U.S.C. § 101(9) (2000) (defining "corporation"); Sally S.

Neely, Part~aers/ai~s cencl Yrertners a~acl C,imitecl I iability Cona~anies cancl Members in X3cin~tr•ae~~tcy.•

Pr%o,rccls fir Refor~~rt, '71 Apt. Btwxx. L..]. 2~1, 286 (1997) (stating that a I.I.0 "appeals co be a

corporaeion" under tl~e Bai~krixptcy Code's definition of "corpoi•aeiozi");Thomas F. Blake-

rnore, I,irreilecl I ir~bi.lr.Gy Corn~~anies ca•~zcl dhn, BanJi~~u~~tey Code.• A 1 eclanieccl 1Zcroieru, Ayi. B~Nitit.

Insi•. J. (Am. Bankr. Tnst., Wash., D.C.), Jtizze 1994, at 12 (staeiz~g that "a I..I.0 would appear

to qualif}~ as a ̀ coz~poration' under [Bankrupecy] Code § 101(9)").

31 See 11 U.S.G. § 1101 {1) (2000) (defining "debtor in possession" t.o mean the debtor

except when a trusCee is serving in the case). It is rare f'or Chapter 11 t~~ustees to be ap-

pointed oz~ elected. See icl. § 110~(a) (2000) (speci£yin~ grounds foi• the appoiz~cmenc of~ a

Chaptea~ X1 trustee).

1294 COR.NELL LAW I~VIEW [Vol. 87:1285

power to operate its business,~2 sell assets,33 obtain credit,~~ and pro-pose aplan of reorganizatioi~..~~'

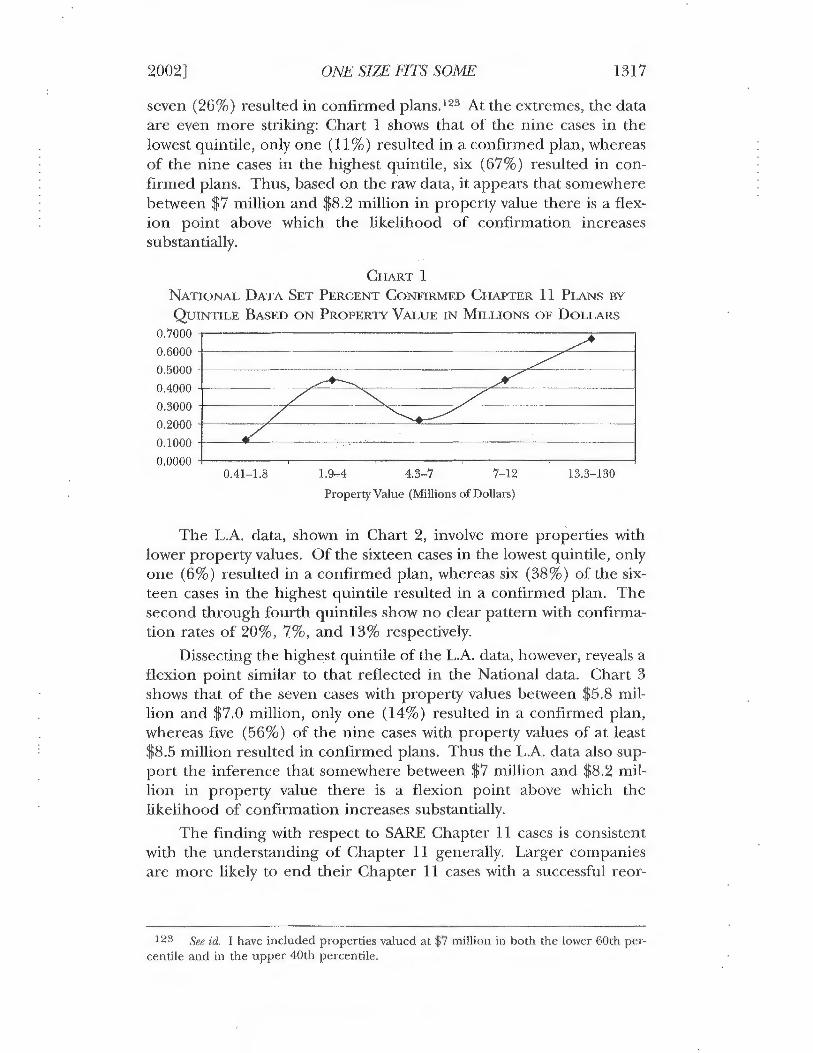

For at least the last sixty years, no.osC SARA debtors in bankruptcyhave had over-leveraged capital structures where a decline in rents (orinability to rent) produces a cash flow insufi'~cient to service their se-cured debts. Some debtors have obtained junior mortgages to createadditional short-term cash flow, but this strategy often adds more debtwithout solving the debtor's long-term liquidity crisis. Ultimately, theliquidity crisis escalates to the point where the mortgage holderthreatens to t'oreclose and the debtor walks away fa om the property,renegotiates with the rcnortgage holder out of court, ox files a ChapterX 1. petition. Tn these Chapter 1 T cases, the debtor's plan of reorgani-zation almost always proposes debt relief Debt relief tales manyforms, ranging from a simple extension of the xn~aturity date or anadjustment of the interest rate or of the debt amortization period, toforgiveness of indebtedness or the conversion of debt to either equityor a participating mortgage. Indeed, a principal purpose of bank-ruptcy is to give the debtor an opportunity to solve its liquidityproUlems.~~'

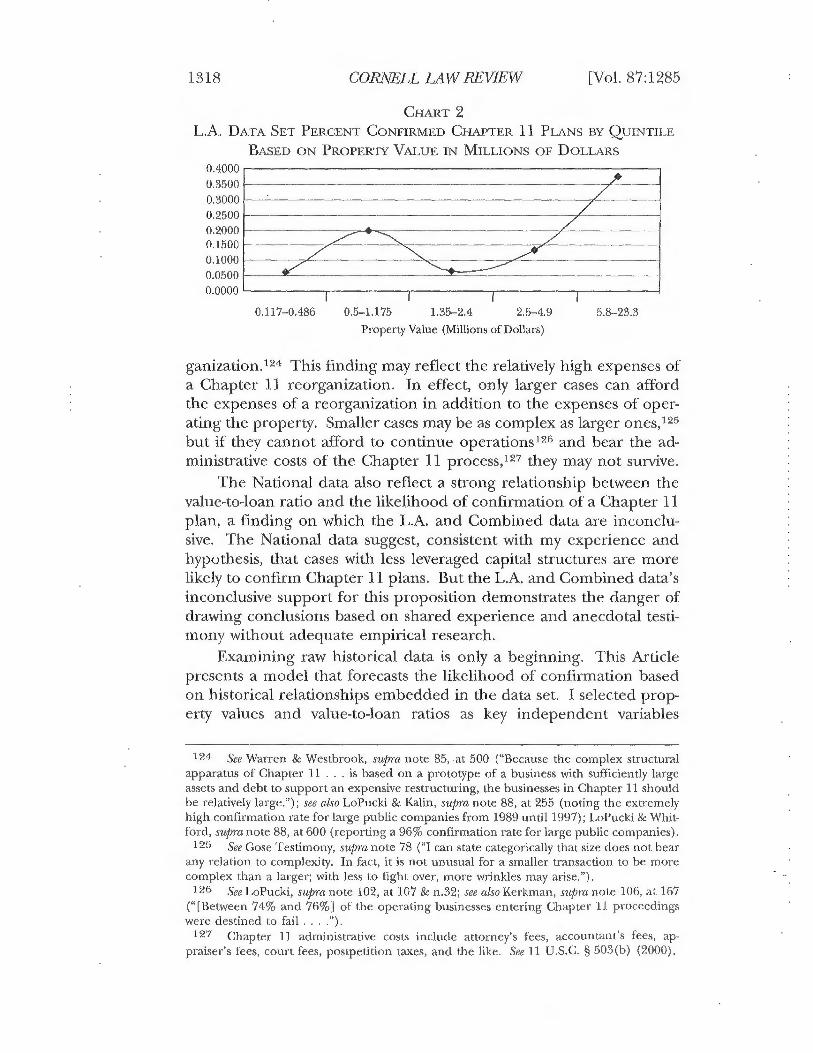

In some SAKE cases, the borrower needs to restructure both thesecured debt and the business operations. For example, a buildingmight requiie construction for completion, expansion, retrofitting,repair, or renovation. In this kind of SAKE case, the debtor in posses-sion first must obtain additional capital to finance the needed con-struction in order to prove that its reorganization plan is feasible. Ifthe value of the properey is less than the mortgage debt, the debtor inpossession probably will i~ot obtain additional financing on an un-secured basis or even with a junior lien for secuxity. Sometimes thedebtor in possession obtains debtor in possession financing securedby a senior lien on the properry.~'' Most lenders, howevei, will notprovide financing to a postpetition debtor in possession uzzless thedebtor in possession secures the new credit with a so-called "prixn~ing"

3L See id. §~ 1107(a), 1103.3 See id. § 363.

3`~ See id. § 364. '

ire See icl. § 1121(a) (giving the debtor the right to file a plan).~;~ See, e.g., H.R. Rr,r. No. 95-595, at 221 (1J77), i~ejrrintecl in 1978 U.S,C.C~,A.N. 59f3,

6X80 ("The purpose of [a] reorganization .. ,case is to formulate az~d have confirmed aplan of reorganization ... f'or the debtor."); Elizabeth Warren, 13anl~rtt/~Gcy Policyina/ring- inan Im1~eifect Warld, 92 MicFi. I,. Rrv. 336, 372 (1993) (characterizing Chapter 11 as "ct•eatingan opportunity for a business to survive its im~xiediate financial crisis"). I3tit see Kevin A.Kordana &uric A. Posner, A Positive'1'heory of Claa1iter 11, 74 N.Y,U. L. Rr~v. 161, 164 (1999)("tiVe assume el~at the puz•pase of Chapter ll is to mirz3zxiize the cost of credit.").

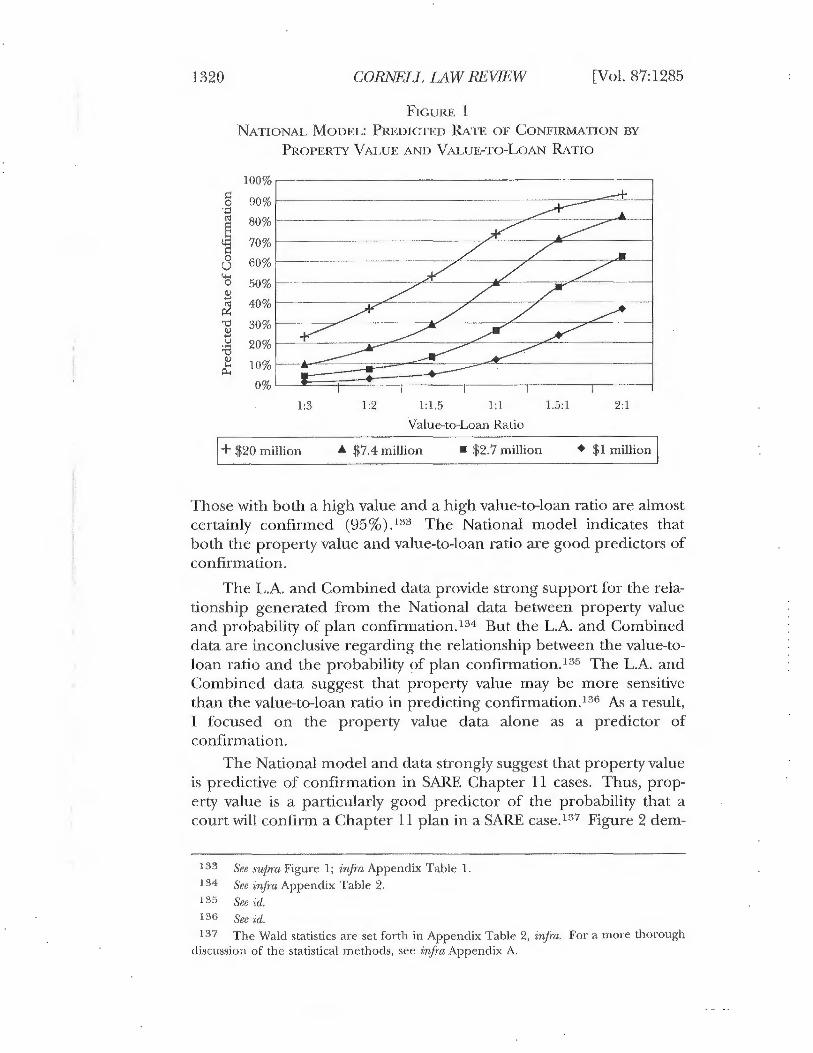

37 See 11 U.S.C. § 3f4 (giving the debtor in possession the ability to obeain postpeci-tioA~ financing).

2002] ONE SIZE FITS SOME 1295

lien. with priority ahead of the prepetitioai rnortgages.3s The law per-mits this to be done only if the court determines that there is ade-

quate protection of the prepetitio~~. mortgage holder's interest in the

real properry.39 Although a value cushion is a common form of ade-

quate protection,`~0 where the amount of prepetition mortgage debtexceeds the value of the property, this method of protection is un-available. Tn some S1~RE cases, however, the value added by new con-seruction will provide a sufficient cushion to cover new postpetitionfinancing and aclequaeely protect the prepetition z~ortgage holder'sinterest in properry.41 Even if the debtor in possession cannot obtaindebtor-in-possession financing, it may be possible for existing ox ne~vequity owners to infuse equity capital under a reorganization play.Unless the prepetition mortgage holder votes to accept the plan, how-ever, the equity owners may infuse equity only if the debtor uses amarket process to determine the value of the new equity.42

While the debtor in possession attempts to obtain debtor-in-pos-session £znancing or new equity, the law automatically stays the se-

cured lender from pursuing its foreclosure rights.43 Although it ispossible fox the debtor to nnake periodic cash payr~.ents to the lender

as a form of adequate protection,44 not all courts require current pay-

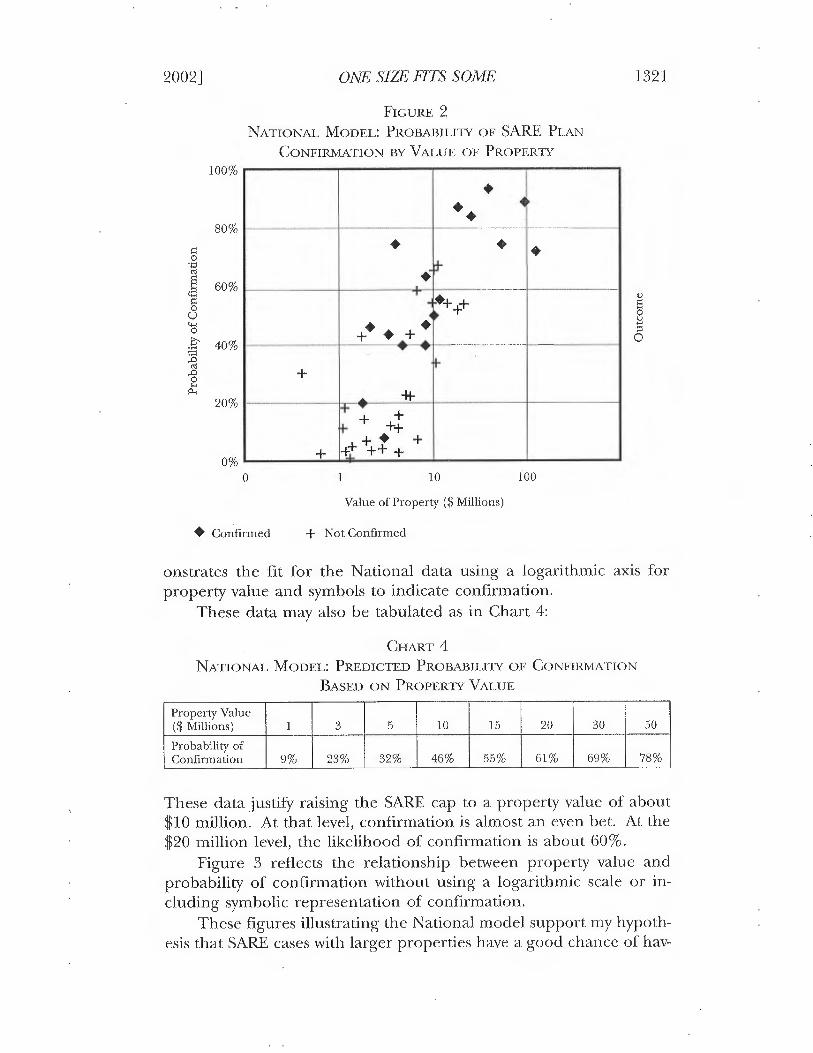

inent of postpetition i~ terest on prepetition tnortgages.4' Under thereorganization plan, unless the debtor is solvent, the undersecuredlender's clam will include principal and prepetition interest, b~xt n.otpostpetition interest.~6 Fox example, assume that a debtor owes amortgage holder. ~1 million under a note bearing annual interest at1Q% and secured by peal property worth $800,000. I£ the court con-firms the reorganization plan and it is effective one year after the

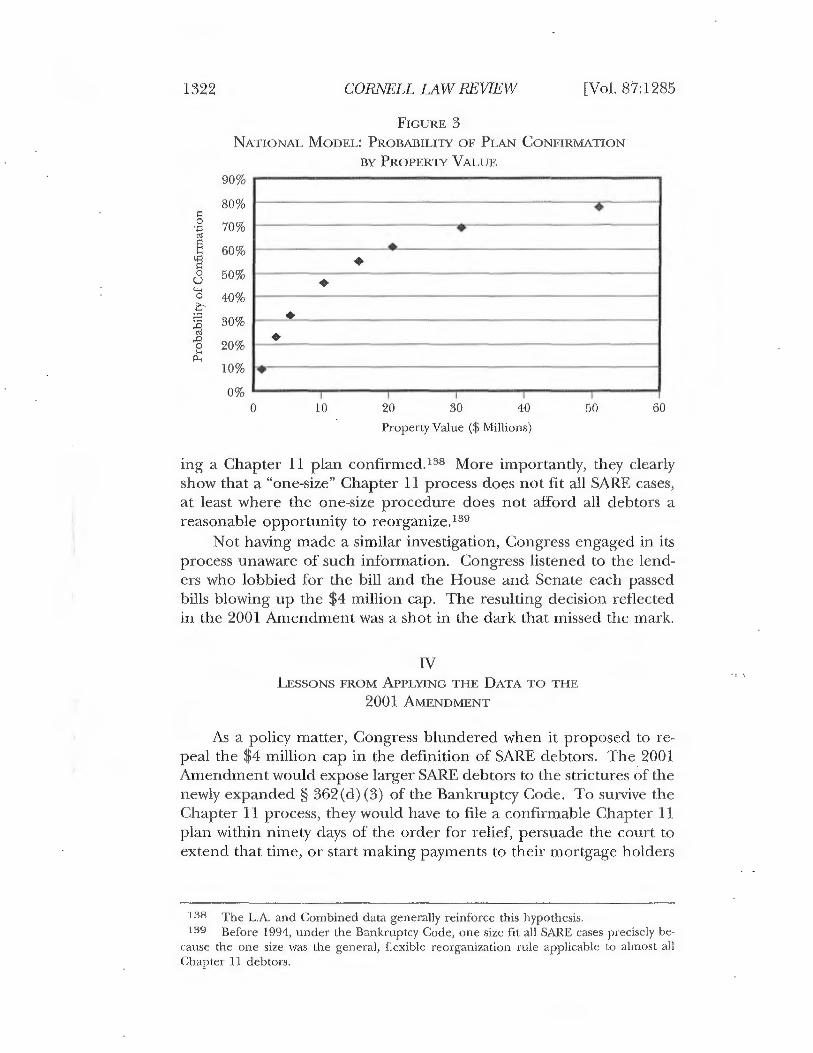

~8 See •r'd,. § 364(4).=;~ See id. ~ 361; id. § 364(cl) (1) (B).~~> See, e.g., Piscole v. Mellor (In 7•e Mellor), 734 ~'.2d 1396, 1400 (9th Cir. 1984); Mc-

Combs Props. VI, Ltd. v. First Tex. Say. Assn (In re McCombs Props. VI, Ltd.), 88 B.R. 261,266 (Bankr. C.D. Cal, 1988).

`11 See, e.g•., In reLedgemere Land Corp., 125 B.R. 58, 63 (Bankr. D. Mass. 1991).4~ See Bank of Am. Nat'1 Truse & Say. Assn v. 203 N. LaSalle St. P'ship, 526 U.S. 434,

445-58 (1999) (holding that if the new value principle exisCs under the Bankruptcy Code,it requires the equity co be exposed to a za~arket value such as through an auction oz~ thetermi~iation of the debtors plan exclusivity).43 See 11 U.S.C. § 362(a) (2000).44 See icl,. § 361(1) .'~~ See, e.g•., Orix Credit Alliance v. Delta Res., Inc. (In re Delta Res., Inc.), 54 I'.3d 722,

729 (lJth Cir. 1995) (noting that if the mortgage holder is oversecuzed, some courts per-mit postpetition interest Co accrue, but do not permit its payment until the conclusion ofthe case}, If the morCgage holder is undersecured, it might not have the right Co paymento£ postpetrtion interest as long as the value of the real property is not declining. See, e.g.,United Say. llss'n v. Tiznbcrs of Inwood Forest Assocs., Ltd., 484 U.S. 365, 382 (1988)(holding that the undersecured creditor is not entitled to adequaCe protection for thedelay in its foreclosure rights attributable to the autoixzatic stay).n~ See 11 U.S,C. §§ 502(b) (2), 726(a) (5) (2000).

1296 CO.RNLLL I AW KL''VIEW [Vol. 87: J 2~5

bankruptcy filing, the mortgage holder will receive considerationworth X800,000 on the effective date of the plan but will forgoX100,000 in postpetition interest. Thus, bankruptcy may reduce theundersecured mortgage lender's recovery on a present value basiscompared to what the lender would have received by pursuzng il:s statelaw rights.

G. Arguments For and Against Reorganization

We now discuss the fundannental question: Why should Coa~gresspernnit SERE cases to reorganize under Chapter 11?47 Some corxznnen-taeors have contended, or have adopted theoretical positions thatshould lead them to contend, that the Chapter 11 process in SAKEcases is inefficient compared to Che alternative of mandatory promptauctions.4~ A.ilocative efficiency, they argue, requires swift and ii~ex-pensive foreclosure i~z accordance with state law.``' These comnnenta-tors contend that permitting the borrower to file a Chapter 11petition inefficiently delays foreclosure, thereby imposing increasedcosts on secured creditors.5~' Secured creditors in turn pass theselosses on to all Uorro~vers in the form of higher interest rates.

Other commentators argue that bankruptcy law should permit in-terference with state law only if it solves a "common pool problem."~~In their view, bankruptcy la~v is necessary to prevent one creditor fromacting in its own. sel£ interest to the detriment o£ creditors as awhole.5~ For example, the law properly prevents a creditor with a se-curity interest. in valuable machinery of an insolve~~t manufacturingcompany from foreclosi~zg on its security interest and causing the liq-uidation o£ the debtor to the detriment o£ all other creditors. Thesecommentators argue that almost all SARE cases are two-party disputes

~7 See, e.g., Xoung, s24frra note 14, at 59 ("It is at least arguable that single asset realestate debtors do not belong in a reorganization proceeding at all."),48 See, e.g•., Douglas G. Baird &Edward R. Morrison, Banlzru~itcy llecision Making> 17 J.~..

~co;v. & Oxc. 356, 371 (2001).4J See Alex M. Johnson, Jr., Critiquing the Foreclosure Process: An Eco~aomic Af~1~roaclt Based

on tlae Ptcrrcdignaatic Norms of ]3ankru,~tcy, 79 Vw. L. REV. 959, 989 {1993). Johnson explains:

Tl~e ability of a lender to foreclose on a mortgage in an inexpensive andexpeditious manner is a key element of Che ex ante bargain struck betweencreditor aid debtor, a bargain that, allows the debtor to obtain a loan at avery attractive interest rate, at leasC compared with other forms of debt suchas personal Ioans.

Id.'~> Taken to its extreme, this argument supports prompt, strict foreclosure with no

right of redemption as Che anost efficient system. See, e.g., James Geoffrey Durham, In De-fense of SErict Foreclosure: A Legal and Econontir, Analysis of Mortgage Foreclosure, 36 S.C. L. Rev.461, 462 (1985) (concluding that "strict Foreclosure ... is the most efficient anethod of

foreclosure, a~1d is ec~uitahle and fair in almost every situation").51 See, e.g•., THOn~s H. JACicso~v, Txc Locrc A~i~ L~MtTS or BnNxizurrcy Lnw 19, 194-95

(1986).5z See id.

2002] ONF SIZE FITS SOME 1297

that involve only a debtor and a mortgage holder; therefore, there isno common pool problem, and there should Ue no bankruptcy case.~~Permitting a SAKE debtor to file for bankruptcy confers no benefitson a pool of other claimants, there being none, they argue, and it onlyimposes unjustified costs and delays on mortgage holders, resulting inhigher interest rates, fewer mortgage loan approvals,54 and the "with-holding from the marketplace property capable of producingvalue."~5 "The time spent in the Bankruptcy Court is wasteful andwithout any public benefit."'~ Therefore, proponents of this argu-ment support amending the Bankruptcy Code to bar SAKE cases fromreorganizing under Chapter 11.5

Contrary to the claim that the coxx~nnon pool problem is the soleor primary basis for evaluating the desirability of allowing SAKE debt-ors access to Chapter 11, three principal arguments, developed below,powerfully favor giving access to Chapter 11 so that SAKE debtorshave an opportunity to reorganize. First, Chapter 11 smoothes outmarket inefficiencies, particularly during massive real estate down-turns. Second, federal public policy supports giving property owners achance to save their investments. Third, macroeconomic and socialpolicies favor reorganization of SAKE debtors.

First, during broad-based financial crises, allowing debtors torestructure debts in Chapter 11 smoothes economic turbulence andprecludes tk~e downward spiral in real estate prices that can resultwhen mortgage holders simultaneously dump massive amou~~ts offoreclosed properties on the market. In addition, Chapter 11 func-tions in SAKE cases to snnooth out market inefficiencies caused by

5~ See, e.g•., Daniel ~. Draper, Stays of Mortgage Foreclosure—A Fra~iosal fns• Reform, 93BANI{ING I.J. 133, 13.5-3G (1976). Draper writes:

Although, in many cases, the insolvent debtor can adjust its fi~~ancial situation and eventually satisfy creditors, in our experience that is rarely, if ever,the case £or asingle-project real estate corporation. The presumption that"time will ]zeal" is simply not valid where the debCOr has virtually nothing toreorganize except a single mortgaged projecC .... Stays against securedcreditors of single-project corpor~itions z-arely increase the probability of re-organization and consequently cannot further airy policy aimed at enhanc-ing all opportunities for success by the debtor.

Yd.; Commercial and Public Sector Issues in Bankru~itcy: Hearing Before dhe Sul~comm. on Fcon. f~Commercial I azu of tlae House Comna. on t1ae,Judiciary, J 02d Cong. 250 (1992) (statement ofMichael F. Brown) ("When financial problems arise ...virtually the only creditor is themortgage bolder. Generally there is little or no trade debt or other associated debt.").54 Sec Commercial and Credit Heareng, su~~ra note 27, at 183 (J 991) (statement of James

W. Nelson) ("Tlie results of lenders' potential losses from single-asset foreclosure delaysare higher mo~•tgage interest rates to connpensate for loss, [and] a disincentive. for institu-tional Lenders to continue to invesC in commercial mortgages ....").55 Draper, sulrrce note 53, at 138.5e Icl, at 112.57 See e.g•., I NAT'L BANICI2. REVIEW COMi~I'N, $ANICI2UPTCY: THE NEXT TWENTY }(EARS

661 n.1678 (7.997) (citia~g authorities), available at littp://goviza£o.libz•azy,unr.edu/nbrc/reporttitlepg.html,

1298 CORNELL LAW REVIEW [Vol. 87:1285

state foreclosure systems.~~ Specifically, some state law foreclosure sys-tems are flawed because they permit lenders to seize property andconduct foreclosure sales without sufficient notice, resulting in artifi-cially depressed prices.5~ Although the Depression is long gone, "themodern nnortgage market is subjece to deficiencies that create similarmarket declines."60 These evils exist "[n]ot ...only in. time of emer-gency."6r Thus, many foreclosures result in nonconsensual sales at be-low market price. By contrast, Chapter 11 gives the property ownerthe opportunity to sell the property over a reasonable period of time.When debtors sell properties with their lenders' cooperation, the re-sulti~g orderly sales can increase value for the lenders and other cred-itors. Alternatively, Chapter 11 permits the property owner torestructure the mortgage through a consensual valuation under aplan supported by the mortgage holder or through a "market-tested"valuation in a contested plan con£irmation.62

Several commentators have endorsed these arguments. Based onhis previous writing,63 Judge Bu££ord testified that real estate reorgani-zation had its roots in the Depression and that Congress enacted it toprevent banks fronn owning most of the real estate in the nation.~4

58 See, e.g., Lynn M. LoPucki, Strange Visions in a Strange World; A Kelly to ProfessorsBruclley and Rosenxzueig, 91 Mtei-i, I... REV. 79, 100 (1992).

r'~ See Arthur ,J. I-Iughes, Reorga~tixution Under the Amendecl Banlzrulitcy ~lct, 13 No•i•ar,DAME I..Aw. 112, 114 (1937). Hughes writes:

Market values did not properly approximate the real values of Che proper-ties. The scarcity of purchasers generally enabled a few buyers to acquireproperties at ...far below the cost o£ the propexties .... To be forced tosell in such a inarkeC, was certain to result in a complete loss to the debtorand a substantial loss to the creditors.

Id.; see also Armstrong v. Csurilla, 817 P.2d 1221, 1223 (N.M. 1991) ("When property suU-ject to a mortgage or other Lien is sold in foreclosure proceedings, the buyer is usually themortgagee or other lien creditor and the price for which the property is ̀ bought in' issometimes significantly less than the property's fair market value."); cf. BFP v. ResolutionTrust Gorp., 511 U.S. 531, 539 (1994) (noting that property sold under the strictures offoreclosure is simply worth less than fair market value).

~o Robert M. Washburn, '1'Ite Judicial and I egislative Res~ionse to Price Inadequ~iey in Nlort-gag~e Far•eclosure Sales, 53 S. CnL. L. I2BV. 843, 851-52 & n.48 (1980) (citing Nat'l Bank v.Equity Investors, 506 P.2d 20, 43-44 (Wash. 19'73) (en banc)); see also Arthur ~. Wilmarth,Jr., The Lx~unsion of Stale Banit Pozue~s, the Federal Xes~ionse, and the Case for Pt~eserving tlae. DualBanking System, 5H FORDHAM L, Rcv. 1133, 1244 (1990) ("[During the late 1980s,] bankfailures in Texas have Ueen caused primarily by an excessive concentration of bank assetsin commercial loans related to real estate and energy ventures.").

61 D J. Farage, Mortgage Def ciency J~urlgment Acts an,cl '1'laeir Constitutionality, 41 Dic:tc, L.REV. 67, 67 (1937) ("[E]mergencies do expose Co the spotlight certain economic malprac-tices, which, in more prosperous times, flourish unheeded.").62 See Bank of Ain. Nac'1 Trust & Say. Assn. v. 203 N. LaSalle 5t. I.td. P'ship, 526 U.S.

439: (1999).63 See Samuel L. Bufford, What Is Right About Banl~rie~itcy Lazu and Wrong ALout Its C~ztics,

72 WnsH. U. L.Q. 829, 836-38 (1994) (arguing that bankruptc}~ law "prevents secured cred-itors from collectively starling a downward spiz'al of foreclosures and bank failures thatcould result in the failure of the entire economy").

6`~ S82 I NAT'I. BANICIt. RtiVIL'W COtv1M'v, szc1~rca note 57, at 680.

2002 ] O1VE SIZE FITS SOME 1299

For~xaer FDIC Chairman William Seidman testified before the HouseBanking Committee in 1990 that when bank .regulators force quick

sales v£ real estate owned after foreclosure, property values declineprecipitously.~~ Thus, when it considered the Bankruptcy Reform. Actof 2001, Congress was aware that orderly liquidations leave society bet-ter off.

Second, Chapter J l also implements zrnportant federal policiesprotecting ownership investments in real estate. Contrary to the asser-

tion that SAKE cases are two-party disputes, many cases involve the

interests of numerous owners who have invested in the real estate pro-

ject.6~ As a normative anatter, Chapter lJ protects general partners or

guarantors who rxiight be liable £or foreclosure deficiencies from the

risk of an unfair6'' or inefficient state foreclosure process. Asa conse-

quence, partners and guarantors can make efficient decisions ex ante

whether to invest in real estate projects.~~ Moreover, rr~inimizing £ore-

closure deficiencies has a beneficial second-order effect. The efficien-

cies of Chapter 11 reduce the tax recapture liability of partners in a

e~ See, e.g., 5cuart D. Root, F3ank Ca~iital, Asset Liquidation, and the Credit Crunch, 1993

CoLV~~. Bus. L. REV. 169, 182-83 (citing Federal Home I oan .Bank Board 1988 lleals: Hearings

Before tTte Ilo2ese Conan. on 13aniting, Fin. ~' Urban Affairs, 101st Gong. 28 (1990) (testimony of

William Seidman, Chairman, FDIC)) ("Congress ...seemingly ignored ...estimate [s] that

assets lose up to twenty percent of value when trey are taken over by the government for

disposition. A liquidation program involving hundreds of billions of dollars in assets is

thus bound to have. an adverse impact on values of assets held by institutions." (footnotes

omitted) ).

~E' Some cases also involve unsecured creditors, such as vendors, property managers,and tenants.

e'~ Although law-and-econonnics scholarship generally has steered clear of distribu-

tioiial issues, recently economic a~~alysis in the literature has attacked the propriety of mak-

ing fairness-based assessments. See, e.g., Louis I~aplow Sc Steven Shaven, Fairness Versus

Welfare, 114 HnKV. L. REV. 961, 1011 (2007.) (criticizing fairness-based assessments on theground eliat they depend "exclusively on the effects of legal rules on individuals' well-

being" and, as a consequence, "can make individuals worse off, that is, reduce social wel-

fare"). In tt►is Article, by "unfair," I refer to a state foreclosure statute that provides insuffi-

cient notice or auction procedures to produce a #air market price. See sources cited supra

note 59 and accompanying text. Some commentaeors might argue that the state foreclo-

sure system is part of the property owner's bargain when it obCains tl~e mortgage. Others

might reply that the property owners righC co file for Chapter 11 relief was a risk the

mortgage holder took when it made the loan.

~~~ Congress changed the risk/reward ratio for real estate investments in 1986 when ie

withdrew tax incentives to invest in real estate and c;nacted passive activity loss rules. See

Daniel S. Goldberg, Tax Sztbsidies: One-Time vs. Periodic: An Economic Analysis of tlae Tax Policy

Alter7aatives, 49 Tnx L. Rz~:v. 365, 3~0 (1994), But Chaptez- 11 iennains az~ important ~~art of

the risk/reward ratio by protecting owners fi~om immediate loss of their investments in the

event their }~usiness faces a liquidity crisis. See, e.g., Warren, su~iru note 36, at 357-58(describing Che policies o£ Chapter 71 as encouraging risk-taking behavior); LoYucki, su1rra

note 58, aC 100 (asserting that Chapter ll offers "the owners, and more importantly thecreditors, an alternative to putting ehe debtoz's assets ozi the auction block" when thedebtor faces a liquidity crisis).

1300 CORNELL LAW I~VIEW [Vol. 87:1285

debtor real esi:ate partnership, thus preventing governments fromreaping a windfall due to artificially low foreclosure prices.'`'

Third, macroecononnic and social policies also favor reorganiza-tion of SARE debtors. Granting SAKE debtors meaningful access toChapter 11 x~.ot only makes good economic sense, Uut it is also goodsocial policy. Generally, nnortgage lenders are the successful Uiddersat foreclosure sales.'70 Chapter 11 prevents undue concentration ofreal estate ownership into the hands of large financial institutions dur-ing economic downturns by facilitating reorganization and thedebtor's retention of ownership.'71 Moreover, some com.rnentatorscontend that Chapter 11 allows the bankruptcy court to consider equi-table, community, and other factors in ruling on a nnortgage holder'srelief from a stay motion.'72 For example, a court might consider that

~`~ Federal and state governments impose taxes on depreciation recapture and capital

gains arising from loan foreclosures whether ox not the loan is recourse. See, e.g., 26 U.S.C.§§ 1231, 1245, 1250 (1994 & Supp. V 1999)., The concept of a nonrecourse loan in bank-ruptcy is described Uy tl~e Supreme Court in Joltnsan v. Home Stale Bank, 507 U.S. 78, 86{1991) (defining nonrecourse loans as "agreements where the creditor's only rSghts areagainst property of the debeor, and not againsC tkie debtor personally" (citation omitted)).Taxpayers who dispose of property subject to nonrecourse debt in excess of basis typically

must pay tax on an amount of gain equal to the excess. See Comm'r v. Tufts, X61 U.S. 300,317 (1983). For a thorough description of hQw real property foreclosures create taxablegains, see Interlaotel Co. v. Commissioner, 81 "Z'.C.M, (CCH) 1809: (T. C, 2001), See also GregoryM. Stein, Tlae Sco1~e of the Borrower's Liability in a Nonrecourse RealTstate I oan, 55 Wnsx. & T..r~L. REV. 120'7, 1220 (1998) (discussing the tax benefits to limited partners when their part

nerships borrow on a noni-ecourse basis xather than on a recourse basis).

70 Basil H. Mattingly, The Shift from Poruer to Process: A Functional Afr~ri-oaeh to ForeclosureI azu, $0 Mtut~,. L. Rev. 77, 101 (J.996) (seati~~g that lenders rely nn foreclosure "to controltheir collateral, to cixe the borrower out of the title picture" Uecause they "gez~,erally antici-pate being the purchaser at foreclosure sales"). "`Typically, leaders are the successful bid-ders at foreclosure sales. After buying the property the lenders take the property into theirportfolios.... [TJhey [then] hire real estate agents to locate prospective purchasers."' Id.ac 101 n.104 (quoting Maury B, Poscover, A Commercially Reaso~zable Sale Under Article 9:Com~rnercial, h'e~rsonable, and .Fair to All Involved, 28 LoY. L.A. L. REV. 235, 2A6 (1994)).

'71 I'or example, during the 1980s, government regulators seized several savings andloan associations and forced most of them to simultaneously market and sell the real estatethey owned. As a result, the market was flooded with real estate inventory and prices plum-meted. See Goldberg, su[rra note 68, at 341 ("[P]rices declined further and the marketbecame flooded with available real estate.").

72 See, e.g~,, Ray~x~ond T. Nimz~er, Real Estate Creditors and the Automatic Stay: A Stiedy inBelaavioral Economics, 1983 Ariz. ST. LJ. 281, 281 (1983). Niminer writes:

A secuxed creditor ~vho can remove the stay may gain a substantial eco-nomic bex~efit. Depending on the relationship between the secured collat-eral and the debtor's overall estate, denial or delay of foreclosure m:ay bevital to ultimate completion of a plan £or relief .... [rconon~ic and fina~~-cial] Factors a~•e not the only considerations that courts apply.... The res~rltis a general balancing of equitable factors ...that is significantly morecomplex than the pure economic evaluation often suggested in theliterature.

Id.; ,see ~clso Karen Gross, faking Community Interests into Account in Bankru~~try: An Essay, 72WASH, U. L.Q, 1031 (7.994) (arguing that courts should take cozx~mixnity interests into ac-count in bankruptcy).

2002] O1VE SIZE 1{ITS SOME 130].

"[m]any foreclosures occur in inner-city neighborhoods occupied bylow-income groups ... fac[ing) unemployment in an economic down-turn ... [and] are thus more likely to default on their mortgage loansand less able to avoid foreclosure."73

It appears that these three argurr~ents won out over law-and-eco-nomics arguments to the contrary. For reasons that were not appar-ent in congressional debates concerning the 2001 Amendment,neither Congress x~or the nnortgage holders embraced arguments toexclude SARA debtors from Chapter 11.74 Perhaps they ~cvere awarethat within the realnn o£ econoxxxics (in opposition to the efficiencyarguments identified at the beginning of this subpart}, some com-m;entators believe that Chapter 11 reorganization promotes allocativeefficiency as compared with foreclosure under state law.'75 Or perhapsthey accepted the above three arguments ix~ response to the efficiencyand common pool problems. State law foreclosure is more efficientthan Chapter 11 under most market conditions. When real estatemarkets are turbulent, however, ouz experience with the Depressionteaches us that state law foreclosure imperils both borrowers and lencl-ers. Moreover, we should not forget that politicians are responsiblefor legislation. Many politicians consider issues of fairness and equitythat generally fall outside the realm of allocative efficiency.76 As iden-tified above, these concerns could well support a political decision toallow SARA debtors access to Chapter Y 1. As discussed below, that iswhat the politicians did.

7~ Washburn, ,su1ira note G0, at 853.7~ Some witnesses made arguments based on efFciency to urge re}~eal of the °~4 mi!-

lion cap, but not to support an outright ban on SAKE deUtors' access to Chapter 11. SeeBankru~itcy Amendments of 1997; and Bankruptcy Law ̀L'eclanical Corrections Act. of 1997: Hete~zng

on H.R. 764 and H.R. 120 Before tlae Subconzna. on Commercial f~' Admin, I aru of tlae Hoarse Conam.

on the Jicdiciary, 105th Long. 106-09 (1997) [hereinafter Banl~rzc~itcy tlmendments Hearing](statement of Donald R. Ennis) (asserting that repeal of the ~4 million cap is necessary "topermit the efficient operation of Che single asset provisions and ehe fulfillment of theirpurpose") .75 contrary to the argument that allocative efficiency requires strict Foreclosure with-

out redemption, econonnic data demonstrate that mortgagor protection laws "may indeedpromote economic efficiency." Michael H. Schill, An economic flnalysis of Mmtgagar Proteo-Lion. L~~rur, 77 V~. L. 12~v. 489, 497 (1991). According to Schill, "[V]iewer] from an ex anteperspective, inoz-tgagor protections may promote, rather than impede, economic efficiencyby functioning as a lbrin o~ insurance against the adverse effects of default and foreclo-sure." Icl. at 538. This Article does not attempt to resolve which commentators are correct,whether state law foreclosure systems are pre£eraUle to Chapter X1, or which group has theburden of proof in evaluating comparative economic efficiencies. Rather, zt is based onthe assumption that Congress has adopted Chapter 11 as a federal alternative to state lawforeclosu~~e.7f See &plow 8c Shaven, s~i~rra note &7, at 10].1 (argttin~ that economic analysis should

give no weight to i~otioi~s of fairness).

1302 CORNELL LAW REVIEW [Vol. 87:1285

D. The Politics

Those interest groups that pushed for special treatment of ~SAREdebtors could have instead called for their exclusion. Since argu-ments for the complete exclusion of two-party disputes were made atthe time of both the 1994 and 2001 amendments, why did the lendingindustry not push £or an outright exclusion of SARA cases from bar~lc-ruptcy? Perhaps their lobbyists counseled against trying to overturn afederal policy that is over sixty years old. Alternatively, it is possiblethat mortgage holders wanted their borrowers, in some cases, to haveaccess to Chapter 11.

In cases in which tine to the property is clouded or the propertycontains toxic waste, for example, mortgage holders prefer to use thebankruptcy court to their o~vn advantage.77 Chapter 11 £ally con-strains the property owner's activities, and the property may be cle-aned while the mortgage holder avoids any liability arising out ofownership resulting from foreclosure, By permitting property ownersto reorganize under Chapter 11, mortgage holders get the best ofboth worlds.

However, the lenders' attraction to Chapter 11 is narrow: Theywant all of the benefits of bankrupi:cy and also control over the pro-cess. For example, they do not want the debtor to be able to restruc-ture secured debt without the lender's co~~.sent. Moreover, lendersare not content to receive these benefits in small SARL, cases; theywant them in all SARE cases.'78 Thus, they influenced the National

Bankruptcy Review Commission to make a recommendation to Co~~-

77 Lenders may realize another subtle benefit of Chapter 1 X. Mortgage holders whodo not want to foreclose on defaulted real properties may use the aucornatic stay of borrow-ers' Gllapter 11 filings to accomplish that objective, even if the mortgage holders' ~overn-menC regulaCOrs would pre#'er immediate Foreclosure. During a borrowers Chapter llcase, the automatic stay legally prevents foreclosure unless the lender obtains relief fi-omthe stay. Lenders who do not want real estate assets on their books can fail to seek relieffrom the automatic stay or delay the process. See Sutherland, su1~ra note l9, at 217 ("T'hemortgagee has ordinarily used every resource to encourage the debtor to keep up kzis inter-est and taxes, and comes to foreclosure only when the case is hopeless. The great lendinginstitutions are reluctant to load themselves with foreclosed real estate ....").

~~ See, e.g•,, Bankraa~~tcy Amendments Hearr'ng, sZC1rra note 74, at 118, 12J —22 (statement ofJill M. Sturtevant, Assistant General Counsel, Bank of America) ("[T'he A~ne~-ican BankersAssociation] scro~igly supports the ...provision ... strik[ing] the ~p~! million debt cap .. .contained in the definition [of] ̀sixigle asset real estate."' (emphasis omitted)); Oversight ofthe National 13r~nliru1~tcy Reuieru Commission l~~ort: I-Iea~zng Before the Subcomm. on Acl~nin. Over=siglct f~ tlae Co2crls of the S. Comm. on 1.heJudiciary, 105th Cong. (1997) {statement of John A.Gose) [hereinafter Gose Testimony] ("No rational correlation exists between Che size of asingle asset real estate bankruptcy ai~.d the complexity of that transaction. A cap, whichpresently exists in the Bazxkruptcy Code, is purely arbitrary."), at 1997 WL 65J242.

2002] ONL SI7,E FITS 5'OME 1303

gress to amend the law,7`' and they financed lobbyists to shepherd thatamendment into la~v.~0

It is not surprising, therefore, that in passing the 2001 .Amend-ment, Congress nominally retained access to Chapter 11 for SARAdebtors while sharply reducing the meaningfulz7ess of that access.The result is a proposed law that pernnits debtors access to Chapter X 1,but under such tight time restrictions that, after ninety days, thedebtor's Functional ability to remain in Chapter 11 usually will be atthe complete discretion of the mortgage holder. Moreover, unlikecuxrent law, the restrictive procedures of the 2001 Amendment wouldapply to single asset real property projects of all sizes without regard tothe dollar arx~ount of the mortgage. With this background, we areprepared to examine closely the 2001 Amendment as a prelude todetermining whether Congress made the right choice in elixx~inatingthe cap.

IITHE ̀~OO~ AMENDMENT EXPLODES TE-IE CAP

A. The Rationale for Congressional Action

The Bankruptcy Reform Act of 2001 paroposes to abolish the ~4million cap in the definition of SERE based a~1 argunnents made atcongressional hearings that aone-size reorganization procedure couldfit all SAKE Uanlcruptcy cases.~l Tt is the author's experience that lab-

7~ At the instigation of the author, a majority oP the bankruptcy commissioners alsosupported an alternative recommendation that would have raised the SAKE cap but noteliminated it. See ]. NnT~L BANICR. RLVCL:W COMNi., supra note 57, at 684.~~ See, e.g., Bc~nl~ru~itey I~nforrrc Art of 1999 (Part I!): Hearing on H.li. 833 Befvre t7ae SzeL-

com.na. on. Commercial ~' tl~lmi~a. I.aru of the House Go•~n~n, on the Ji~dicira~y, 106th Cong. 5-14(199J) (statement of George J. Wallace, nn behalf of the Consumer Bankruptcy RefozmCoalition); Bct~alzrtt~itey Reform Act of 1998 Part I• Hewing on H.R. 3150 Before the S2tbcomm. onGom~nercial E~' Adntin. Lazu of tlae House Comm.. on tlae Judiciary, 105th Cong. 25-28, 38-40(x998) (statement of Lloyd N. Cutler, on behalf of the Bankruptcy Issues Council); Ba~alz-rta~tcy Reforrn Act of 1998; Res~~onsiGle Borrower Protection Act; and Consume• Lenders tend Barroru-e~s Barak-ria1~Gcy Acco•tcntraLiliGy Art of 1998 Pccrt II: Her~•~ting• on H.R. 3150, H.R. 2500, and H.R.3146 13e%ore the S2cbconi~na. on Co~~tnaer•cia.l f~' Adnti~z. Lazu of th.e House Comm. on tlae Judiciary,105th Cong. 56-63 (1998) (statement of George J. Wallace, on behalf o£ e11e AmericanFinancial Services Association).

~1 See sources cited sic1~ra note 78 and accompanying Cext. One congressman charac-terized the repeal of the ~4 million cap as necessary to cure an "injustice" stemming "froma last minute decision that was made in the 103rd Congress, which placed an arbitrary f~4million ceiling on ehe single asset provisions of the bankruptcy reform bill. The effect hasbeen to render investors helpless in foz'eclosure on single assets valued at over• $~4 millioa~."See 145 Cotvc~. Rrc.. H2713 (daily ed. May 5, 1999) (statement of Rep. I{nollenberg). Inex-plicably, in the pending Bankruptcy Reform Act of 2001, Congress adopted exactl~~ theopposite x-ation~ile in expanding the deUt threshold fi•oxn $2 million to ~3 million in thede£'inition of sn~.all business debtors for the purpose oi' segregating small businesses fromlarger businesses. Sec, Bankruptcy Re£orm Act of 2001, H.Tt. 333, 107th Cong. §X32 (a)(2001) (pz•oposing to amend the definition of "stxxal] business debtor" in § 101(51)(D) ofthe BankrupCcy Code to cover busi~~c:sses that have "aggregate nonco~iCingene, liquidated

].304 CORNET L LAW REVIEW [Vol. 8'7:1285

byists fox lenders convinced Congress that a real estate case is a realestate case is a real estate case, whether it is an apartment house or theWaldorf Astoria Hote1.~2 Some witnesses told Congress that it shouldrepeal the ~$4 nnillion cap because large properties have the samennaintenance, tax, and recapitalization probler~as as small properties.8~They also stated that repeal of the ~$4 million cap was necessary "topermit the efficient operation of the single asset provisions and thefulfillment of their purpose."84 Other witnesses and comnnexztatorstook the position that some form: of a cap ~evas appropriate, but had nohard data to support their claiz~s.~' .Although a few witnesses sug-gestecl banning SARE cases from Chapter 11 altogether, others saidChapter 11 played an important role in SAKE cases.

Some witnesses unsuccessfully argued in support of retaining the~$4 million cap and treating large SAKE debtors the same as otherChapter 11 debtors.~~ They argued that separate treatment of allS1~RE debtors from other debtors would induce lenders to force bor-ro~vers to incur transaction costs to form new single asset entities inorder to finance each pxoperty, even. if the same real party in interesto~rned the properties. Thus, if a manufacturer seeks financing forconstruction of a $~50 xrnillion plant, a rational lender will require themanufacturer to form a single asset cox~apany to hold title to the realestate and become the borrower. The lender may force the rnanufac-tu~ ex to guarantee the debt. As a result, the manufacturer will notavoid liability on the loan, and will incur the transaction costs of form-ing the single asset company and maintaining separate tax, account-ing, and legal records. Moreover, in the event of insolvency of several

secured and tYnsecured debts .. , in an amount not more than $3,000,000"), avc~ilaGle cathttp://thomas.loc.gov; Bankruptcy Reform Act of 2001, S. 420, 107th Cong. § 432{a)(2001) (same), «v~eilt~l~le at http://thomas.loc.gov.

~z See In re Penn Gent. Transp. Co., 354 F. Supp. fill (E.D. Pa. 1972). After the 2001Amendment, if the ground leased was real propez•ty held by a SA.RF, debtor, Y1 U.S.C.§ 3G2(d)(3) would apply.

~~ See sources cited su1yrri note 78.~4 Ba~zkrzcptcy ~lmend~~nents Hearin; su~ira note 7~, at 107 (statement of Donald R.

Ennis).

Kra Sen., e.g., tid, at 46 (statement of Kenneth N: I~lee, Chairman, Committee on Legisla-

tion, National Bankruptcy Conference) ("I would have to think a $~10 million limit would

brixzg in the lion's share of the projects ...."); Lawrence Ponoi•off, Ilae Dacbious Role ofPrecedent an the west fm• Fi•>st Principles in the Reform of the Bcrnkru~itcy Cocle: Some Lessons from

the Civil I,rczu rind Rerelist '1'ra~litions, ~4 ANi. B.aNicK. L J. 173, 195 (2000) ("'Wisely, until now,ehe definition of ̀single asset real estate' has been limited to debtors with below a certainmaximum level of secured debt ...."). Aftez• tlae congressional hearings, Professors War-ren and Westbrook analyzed hard data and concluded that the ~4 million cap alreadycovers 72% of the SAKE cases and raising die cap co X15 million would capture 9~% of thecases. See ElizaUeth Warren &Jay Lawrence Westbrook, Tinancit~l Characteristics of B2uiyaessesin B~r~zk•~z~~~tcy, ~I3 ANT, Br1NKR. L, J. X99, 542-43 (1999).H~ See, e.g., Brcnli-rec1~tcy Amendments Flearing, szc~na note 74, ac 37, 46 (statement aa~d

eestimony of Kenneth N. Klee, Chairman, Committee on Legislatio~~, National Ba~~kruptcyConference).

2002] OIVE SIZE FITS SOME 1305

related piojects, instead of the manufacturer filing for bankruptcy forone company that owns several properties, the manufacturer will file aseparate bankruptcy petition for each company that holds a troubledproject, thereby paying multiple filing fees and inc~.irring the costs ofmultiple bankruptcy administrations.H7

In this light, it is reasonable to question ~vhy Congress abandonedthe line it drew in 1994. Was the change occasioned by lobbying ~res-sure from secured lenders, or did circunnstances change after 1994?ti11as Congress wrong in enacting the cap in the first place in 1994?Certainly the shared experience that led Congress to adopt the $4million cap in 1994 suggested that the group of larger SARE cases hadmore complex debt structures, greater capacity to service Chapter 11administrative expenses, aizd a greater likelihood of confirming aplan.$$ That is why Congress enacted special rules only for smallerSARA debtors. Anecdotal testimony led Congress to believe thatsmaller deUtors, for the most part, had simple debt structures, littlecapacity to service Chapter 11 administrative expenses, and no reason-able likelihood of con£irnning a plan. For the small SAKE debtors, itmade sense for Congress to pretermit the Chapter 11 process.

The sanne was not true, however, fox larger SAKE debtors in 1994,and it remains untrue in 2002. If there is a reasonable likelihood that,as a group, Iarge SAKE debtors will be able to confirm Chapter 11plans, what ratioi~.ale justifies subjecting these debtors to the stricturesof § 362 (d} (3) of the Bankruptcy Code? Indeed, if the data show thatmost large SAKE cases have a reasonable possibility of confirming aChapter 11 plan, it makes more sense for Congress to raise the ~4million cap to a specific dollar sum than to abandon it altogether.Perhaps Congress believed that if the cap Functioned well for snnallSARE debtors, it should extend it to all SAR.E debtors.

87 This strategic behavior certainly is one downside of the pending Bankruptcy Re-form Act of 2001, which allows lenders to opt nut of the regular Chapter 11 rules by requir-

ing borrowers to connpartmentalize real property assets. Another theoretical by-product of

the proposed Acc is that it should reduce monitoring by unsecured creditors. Unsecuredcreditors wi11 not likely pay atte~~tion to SAT2E cases if secured lenders will dominate and

quickly foreclose or receive assets as interest payments. In the author's experience, how-

ever, unsecured creditors seldom rno~~itoxed SARE cases even befo~•e the Act was proposed,

becarxse they had little at stake individually.

$H See, e.g., Lynn M. Lol'ucki & Sax•a D. Kalin, llaeTailure of Pxiblic Conz~~u~ay 13ank~-xc~~tcies

in Delazacere and Neu Yarh: Em~iirical Evidence of re `Rcice to tlae Bottom'; 54 V~a~n. L. RLV. 231,

256 (2001) (showing an extremely high confirmation rate for large public companies fi-om

1989 until 1997); I ynn M. LoPucki 8c William G. ~1rl~itford, Patterns 7n the Bu~alti~~~~tcy Reor

ganiz~itio~. of~7 a~r~re, Publicly Held Com~~anies, 78 CoRNr~.i. L.. Rev. 597, 600 (1993) (reporting a96% confirmation i°ate for large, public companies).

130G CORNET L LAW REVIEW [Vol. 87:1285

B. Predicted effects of Blowing Up the Cap

Whether or not Congress justifiaUly proposed to explode the ~4million cap, if the proposal becomes law, parties in SARE cases willhave to adapt to those changes. The new reality for large BARE debt-ors will be that they will be subject to lenders' threats to bring, andactually file, motions for relief fronn the automatic stay under§ 362(d) (3). How will this change in leverage affect the way ChapterX 1 functions for large SAKE debtors? Certainly it will be unreasonablefor many large SAKE debi:ors to file a plan ~vithin ninety days after theorder for relief To be sure, the court can extexa.d this time for"cause,"H' but why should the large SAKE debtor have to bear the cost,burden, and uncertainty o1' bringing such a xnotiorz? The cost ofbringing a motion is inevitable and not recoupable. The burden ofproving the "cause" for an extension is on the large SAKE debtor,unlike all the other large debtors who have a minimum 120-day exclu-sivity period within which to file a plan and do not face automaticforeclosure if they fail to File ~cvithin that period. The uncertaintyabout whether the judge will grant the extension motion is obvious.Many judges have displayed open hostility toward SA12E debtors.~0

Of course, the debtor has the theoretical option of commencingpayments to the mortgage holder. But many SARE debtors are illiq-uid.J1 The ,BARE debtor might be cash poor because the debtor hasnot completed the real estate project, because the debtor needsmoney £or repairs, maintenance, or renovation, or because a downnnarket has created large vacancy rates. Moreover, in most SA12Ecases, the mortgage holder has a lien on the rents.'z Under current

~`~ See sources cited su~rtr note 9.`~~ Generally, judicial hostility is evldene when a judge cl~aY•acterizes tl~e SARA deUtor

as having •filed its bankruptcy petition "in bacl faith." See, e.g., Pac. Firse Bank ex rel. R.T.Capital Corp. v. Boulders on the River, Inc. (In re Boulders on die River, Inc.), 164 B.R. 99,103 (B.A,P. 9th Cir. 1994) ("Bad faith exists if' these is no realistic possibility of reorganiza-tion and the debeor seeks merely to delay or fi•ustraCe efforts n£ secured creditors.");United Say. Assn v. Timbers of Inwood Forest Assocs., Ltd. (In. re Timbers of Inwood ForestAssocs., L.td.), 808 r.2d 363, 384 (5th Cir. 198'7) ("To the extent Chat chi debtor in bank-ruptcy can prevent tl~e secured creditor f►•om enforcing aes rights against collateral whilethe debtor benefits from. the creditor's money, the debtor and 11is unsecured creditorsreceive a windfall at the expense of the secured creditor."), ~ff'd, 484 U.S. 365 (l98$).Courts often dismiss debtors' Chapter 11 petitions when they are filed in "bad faieh." See,e.g., Albany Partners, Ltd. v. Westbrook (In ye Albany Partners, Ltd.), 749 F.2d G70, 676(11th Cix. 1984) (a£firnzing a lower court's annulment of a stay); Singer Furniture Acquisi-tion Corp. v. SSMC: Tnc. N.V., 254 B.R. 46, 60 (M.D. Fla. 2000); .ree ~elsu Xra re Pac. Rin-~ Invs.,LLP, 243 B.R. 768, 7'73 (D. Colc>. 2000) (rejecting "the argument that the ability to reor-ganize precludes dismissal for bad faith."),

~1 See LoPucki, su~rr~a note 58, at 100; sow~ces cited sz~~nrc note 36.`~~ In some SAI2F, cases, the mortgage holciea• has an "absolute assig~lment" of Che rents

whereby the mortgage holder• owns the i•ent~s until the inortg~age is paid. See, e.g:, Great W.

Life Assurance Co. v. Rothman (1'n. re Ventura-T.ouise Props.), 490 F.2d 1141, 1143-4~ (9th

Cir. J.974) ("[A]n ag~•eemcnt can provide for an absolute assignment of'rents upon default.

2002] ONE SIZE FfTS SOML X307

law, mortgage holders have persuaded some courts that rents are ad-ditional collateral that the la~v must proi;ect separately, and that theyare unavailable to protect a mortgage holder's lien on a real propertyproject.~3 One bene~iciar provision of the proposed Bankruptcy Re-form Act of 200]. makes cents available to satisfy the deUtor's paymei~eobligation under § 362(d) (3) of the Bankruptcy Code.J4 But in manycases, the net rents will be insufficient to service the debtor's payment

`It has been held that such a provision, rather than pledging the rents as additional secur-ity, operates co transfer to the mortgagee, the nnortgagor's right to tUe rentals upon thehappening of a specified condition."' (quoting Kinnison v. Guar. Liquidating Corp., 115P.2d 450, 453 (Cal. 7941)). Although beyond tl~.e scope of phis Article, discussion of rentshas created a large body of literature, Not less than sixty-four law review articles containthe word "rents" in their titles. Of these, no fewer Chan seventeen also mention 1'n re 'Ven-t2aru-Ionise. See, e.g., David Gray Carlson, Rents in B~cnkrufitcy, 46 S.C. L. Rev. 1075, 1Y04(1995) (discussing In re Ventura-I ozcise for the proposition that judges routinely authorizeforfeitures upon default and allow secuz•ed parties Co collect rent}; Julia Patterson For-rester, AUniform and More ,Rational A~~irouch to .Rents as Secaerity fvr the Mortga~~e Loan, 46RuTC~RS L. Rev. 349, 379-82 (1993) (discLissing the trend in the treatment of absoluteassignment of rents cases); Patrick A. Randolph, Jr„ 4Vlae~a Should Bunkr~c~itcy Courts RecognizeLenders' Rents Interests? 23 U.C. DAV~s L. Rev. 533, 841-45 (1990) (discussing the condi-tional present assignmez~t theory as adopted in In re CTentaa•ra-Louise); John C. Siemers, TheMortgagee s I ien Against Rents, 25 ~'~~:x. 'TEC;x L. Rcv. 873, 892 n.70 (1994) (acknowledging 1'nre ~/entura I o2iise in a footnote); Joanne N. Davies, Note, FNMA v. Bugna: California Assign-ment of Rents Provision anti tlee Im~iact of the Bankru~tey Reform Act of 1994, 31 Lov. L.A. L. REV.1453, 1466 (1998) (discussing the "contradictory and confusing" case law surrounding theprotection of a lender's security interest in postpetition rents); Sandra Elzerman, Cotn-ment, Inte~~ests i•~t Collrcterully Assigned Rents and Profits Under the I3unitru~itcy Code, 22 Hous. I..Rev. 1251, 1265 n.101 (1985) (acknowledging In re Ventura-Louise in a footnote).

~3 See, e.~., In •re 499 W. Warren St. Assocs., Ltd. P'sliip, 142 B.R. 53, 56 (Bazikr.N.D.N.Y. 1J92) (stating that "a secured cz•editor holding both a mortgage securing a debton a parcel o#'real property, and a perfected security interest in rents derived therefrom,holds two distinct interests," and cliscussin~ cases laying out the contours of this approach);see also ,Jol1n Hancock Mut, Life Ins. Co. v. Madera Farms P'ship (In re Madera FarmsP'ship), G6 B.R. 100, 103 (B.A.P. 9th Cir, 1986) ("It is clear that Che rents are additionalcollateral."); In re Landing Assocs., Ltd., 122 B.R. 288, 296 (Bankr. W.D. Tex. 1990) (con-siclering• the value of the mortgage securing a debt nn a parcel of land as separate from thesecurity interest in the rents derived from it); Mortgage Guara~~tee Co. v. Sampsell, ].24F.2c1 353, 356 (Cal. Ct, App. 1942) ("There can be xzo question but that the assignment ofrentals in the deed of trList constituted additional primary security with the real propertydescribed in the deed of trust and the personal property described in the chattel mortgage." (citation omitted)).

J4 See Bankruptcy Refoa-m Act of 2001, H.R. 333, 10'7th Gong., ~ 444(2) (2001); Bank-ruptcy Ref~rin Act of 2001, S. X120, 107th Cong., ~ ~~14(2) (2001). Section 444(2) wouldamend 11 U.S.C. § 362(d)(3)(B) to preclude relief from the stay antler § 362(d)(3) if:

(B) file det~to7- leas commenced inonCl~ly payments that—

(i) may, in the deUtor's sole discretion, z~otrvithstanding section3G3(c) (2), be made from rents or other income gexierated before orafter the commencemei~l of the case by or fi-om the property to eachcreditor whose clai►n is secured by such real estate (other than a claimsecured by a judginenc lien or by an unmatured statutory lien); and(ii) are in an amount equal to interest aC the then applicablenondeiault contract race of interest nn the value of the creditor's inter-est in the real estate; ... .

H,R. 333, ~ 44~(2)> S. 420, § ~k44(2).

1308 CO.R.NELI. LAW REVIEW [Vol. 87:1285

obligation in full. Thtxs, in many SAR.E cases, the debtor's option tocomnnence making payments will be unrealistic.

If the debtor cannot file a confirmable plan within the fast trackof ~ 362 (d) (3), commence making payments to the mortgage holder,or persuade the court to grant an extension of time, then the moregage holder is effectively in complete control of the Chapter 11 pro-cess. If the property has a feature, for exaxxiple eanviroaiznental waste,such that the mortgage holder might benerit by leaving the propertyin Chapter 11, the mortgage holder can grant an extension o£ tinne orfail to foreclose following relief from the stay. Alternatively, if the bor-rower faces tax problems in the event of Foreclosure, the lender canthreaten foreclosure to extract a contribution o:f new equity into theproject Co reinstate the loan and restore it to a performing asset onthe lender's books. On the other hand, if the property has potentialupside and the mortgage holder desires to capture this upside for itsown benefit, then the mortgage holder gets relief from the automaticstay and the right to foreclose on the properey. In essence, the Chap-ter 11 case is over. Although this might be good news for the mortgage holder, it is bad news for the property owner who loses theopportunity to reorganize.

IIIDaT~. rRO~ SARE C~.rT~:n 1 X C~sEs

A. Methodology

Talk is cheap. It is easy to criticize Congress for failing to developdata concerning the operaCion of SAKE cases before it proposed sig-nificant changes, but it is much harder to develop those data than tocriticize Congress for failing to do so. This is especially true .Cor schol-a~ s and others who work with linnited access to the underlying dataand limited means to Fund the needed research. Given the impor-tance of bankruptcy law and the constitutional requirement that anyfederal bankruptcy law be unifornn,J5 it is astounding that Congresshas not developed better bankruptcy data on which to base its legisla-tive decisions. For example, there is no national database of bankruptcy court records; bankruptcy courts compile and store theirrecords locally. Furthermore, the Administrative Office of the U.S.Courts does not collect separately-recorded data nn SAKE cases. Thismeans that the resources necessary to draw a national sample of S,AR.Ecases would be beyond the reach of a single researcher.

Faced with the prospect o£ cursing the darkness or lighting a verysmall candle, however, X decided to study what I could. I drew twosamples of data: The first was a national sample of all reported Sl~TtE

~r> ,See U.S. CovsT. art. I, ~ 8, cl. 4.

2002] o~ srzr; rxTS sow 1309

decisions augmented by data ox~ unreported SURE cases sent to me bylawyers in response to a questionnaire. The second extracted SARAdata from the files of all Chapter 11 cases administered by a singlebankruptcy judge in Los Angeles. I refer to the first sample as the"National" data set and the second sample as the "L.A." data set. I alsocombined the National and L.A. data sets into a "Combined" data set.