Embed Size (px)

Citation preview

International Financial Management: INBU 4200

Fall Semester 2004Lecture 6

International Banking and the International Money Markets

(Chapter 6)

International Banking

• International (global) banks can be distinguished from domestic banks by the:

– Services they offer– The deposits they attract– The loans they make

International Banks: Services

• Financing cross border trade (exports)– Letters of credit; bankers’ acceptances

• Offering foreign exchange services– Buying and selling foreign exchange for clients– Offering hedging contracts

• Offering interest rate and currency swap financing.

• Consulting services to global firms– Hedging strategies; international cash management.

• Underwriting eurobonds, foreign bonds, equity issues for global firms.

International Banking: Deposits

• May or may not be involved in accepting domestic deposits.– For example, China currently does not allow

foreign banks to engage in this activity (“retail banking”).

• Global banks participate in eurocurrency deposit market.– Accepting “offshore” deposits– Time deposits of currencies other than the

currency of the country in which the bank is operating.

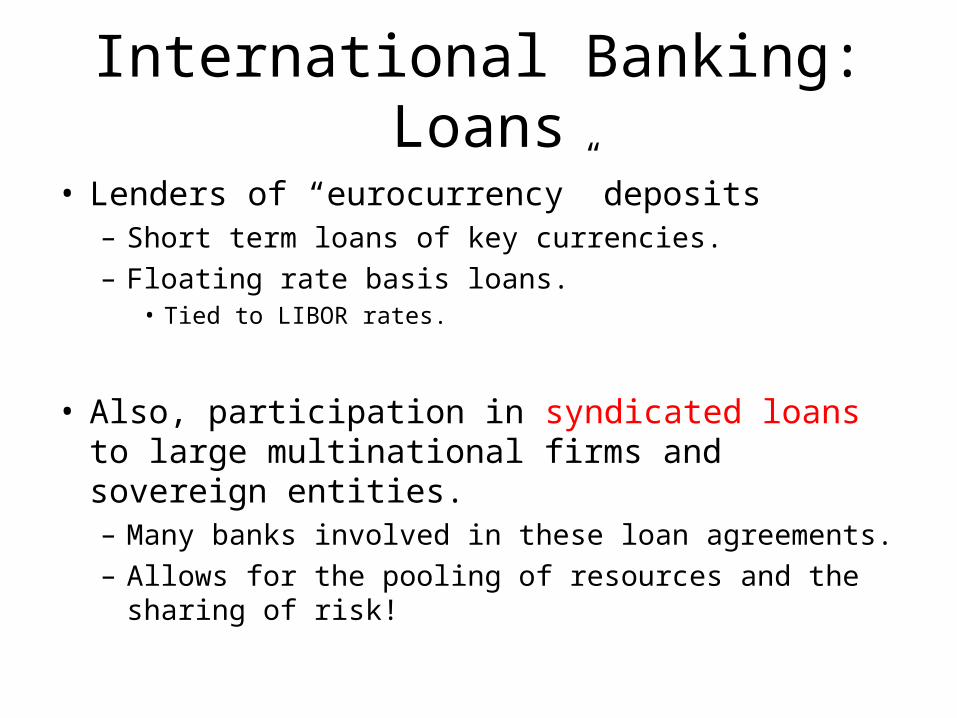

International Banking: Loans

• Lenders of “eurocurrency” deposits– Short term loans of key currencies.– Floating rate basis loans.

• Tied to LIBOR rates.

• Also, participation in syndicated loans to large multinational firms and sovereign entities.– Many banks involved in these loan agreements.– Allows for the pooling of resources and the sharing of

risk!

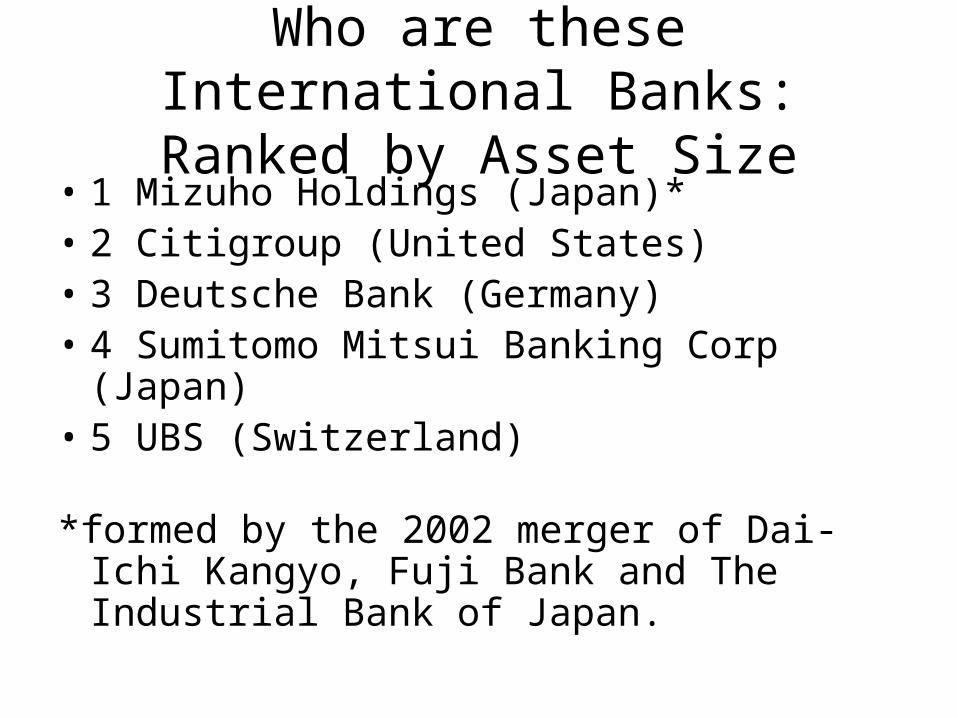

Who are these International Banks: Ranked by Asset Size

• 1 Mizuho Holdings (Japan)*• 2 Citigroup (United States)• 3 Deutsche Bank (Germany)• 4 Sumitomo Mitsui Banking Corp (Japan)• 5 UBS (Switzerland)

*formed by the 2002 merger of Dai-Ichi Kangyo, Fuji Bank and The Industrial Bank of Japan.

Who are these International Banks: Ranked by Asset Size

• 6 BNP (France)• 7 JP Morgan Chase (United States)• 8 HSBC (United Kingdom)• 9 Bayerische Hypo-und Vereinsbank- (Germany)• 10 Bank of America (United States)• 11 ING (Netherlands)• 12 Credit Suisse (Switzerland)• 13 Bank of Tokyo – Mitsubishi (Japan)• 14 ABN AMRO (Netherlands)

Who are these International Banks: Ranked by Asset Size

• 15 Industrial & Commercial Bank of China (China)

• 16 Royal Bank of Scotland (United Kingdom)• 17 Barclays Bank (United Kingdom)• 18 Crédit Agricole (France)• 19 Norinchukin Bank (Japan)• 20 Morgan Stanley Dean Witter (United States)• 21 Société Générale (France)

Who are these International Banks: Ranked by Asset Size

• Of the largest 50 commercial banks:

• 9 are American

• 6 are Japanese and United Kingdom

• 5 are French and German

• 4 are Chinese

• 3 are Dutch

Why do Banks Establish International Operations?

• Low Marginal Costs in doing so– Apply home knowledge to foreign market

• Knowledge Advantage– Overseas operations can utilize the parent’s

knowledge to compete in foreign market

• Home Information Source– Providing local (foreign) firms with information about

parent’s home market

• Prestige– Global banks can attract clients abroad

Why do Banks Establish International Operations?

• Regulation Advantage– Global banks may not face the same regulations as

domestic banks (e.g., reserve requirements on eurocurrency deposits).

• Wholesale and Retail Defensive Strategy– Following corporate clients overseas– Providing retail customer overseas services

• Circumventing Government Restrictions– Wanting to do business in RMB (Yuan).

• They have to have a license permitting them to operate in China and with the RMB.

Why do Banks Establish International Operations?

• Growth– Home market may be saturated

• Risk Reduction– Greater stability of consolidated earnings.

Example of Global Bank: Citigroup

• Financial services firm combining banking, insurance, and investments under one global organization.– “Universal or full service bank”

• Currently located in over 100 countries– Began international operations in 1912!

• Go to home page and view countries and product lines– http://www.citigroup.com/citigroup/homepage/

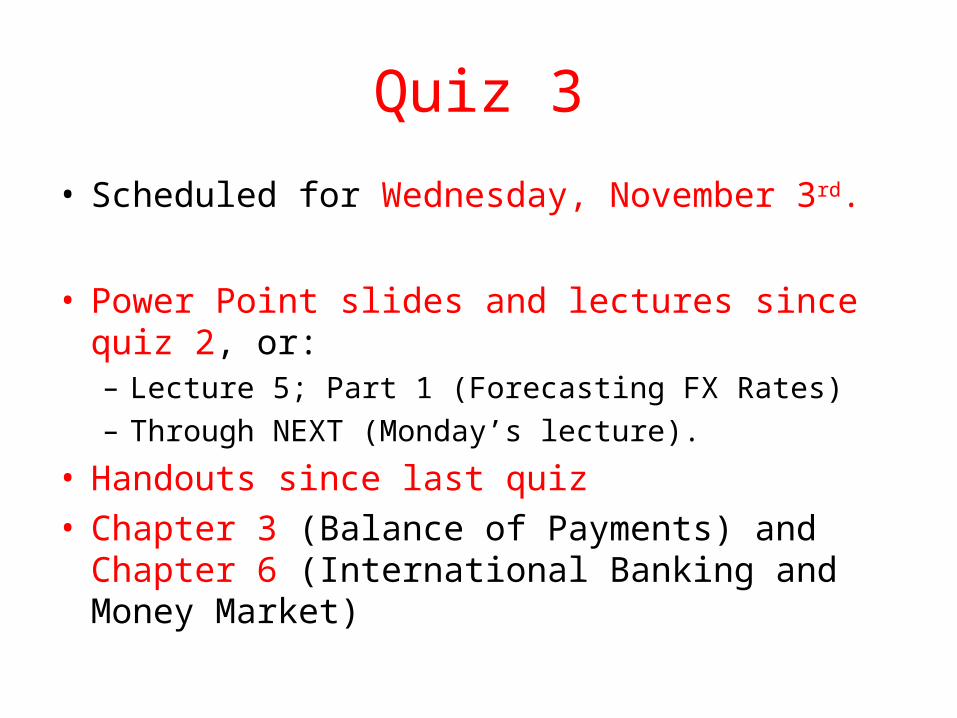

Quiz 3

• Scheduled for Wednesday, November 3rd.

• Power Point slides and lectures since quiz 2, or:– Lecture 5; Part 1 (Forecasting FX Rates) – Through NEXT (Monday’s lecture).

• Handouts since last quiz• Chapter 3 (Balance of Payments) and Chapter 6

(International Banking and Money Market)

Services Offered by International Banks

• The particular services offered by global banks are a function of:– The regulatory environment.

• What will governments allow?• Developing countries still somewhat restrictive

regarding foreign banks.

– The type of banking office established.

Types of International Banking Offices

• Correspondent Bank– No physical presence overseas– Correspondent relationships with banks in foreign

markets• Results in “correspondent” balances held at correspondent

banks.

– Allows banks to service core clients with little cost.• Reciprocal deposit accounts for clients.• Facilities foreign exchange conversion for clients• Facilities trade financing (clearing bankers acceptances) for

clients.

Types of International Banking Offices

• Representative Office– Small service facility staffed by parent bank

personnel– Cannot make loans or accept deposits– Useful strategy if bank has many important

clients in foreign country– Office it there to assist core clients with

• Country and economic information• Introductions to government/business contacts• Credit evaluations of local firms

Types of International Banking Offices

• Foreign Branch Office– Most popular form of U.S. bank expansion abroad.– Legally part of the parent bank– Subject to regulations at home and in foreign market.– Branch lending limits are based on parent capital (not

branch office)• Thus, can provide larger loans to overseas clients.

– Allows for fast global clearing of checks within the bank

• Branch to Branch and to parent.

Types of International Banking Offices

• Subsidiary Bank– Locally incorporated (in foreign country) bank.

• Either wholly owned by parent, or joint venture• Non-controlling subsidiary (i.e., arising out of a joint venture)

is referred to as an “affiliate bank.”

– Operate under the banking laws of the country in which they are incorporated.

– Arrangement was particularly desirable before the abolition of U.S. Glass Steagell Act.

• U.S. banks incorporated overseas so as to engage in investment banking activities.

Types of International Banking Offices

• Offshore Banking Centers– Organized branches or subsidiaries in recognized offshore

countries. Location critical here:• Offshore country: A country whose government allows the banking

system to engage in “external” banking activity.– Accepting deposits and making loans in currencies other than the home

currency of the offshore country.– IMF recognizes the following as offshore countries:

• Bahamas, Bahrain, the Cayman Islands, Hong Kong, the Netherlands Antilles, Panama, and Singapore.

– Characterized by:• Minimal host country regulations, low taxes, favorable time zone

location, and banking secrecy laws

– Visit: http://www.offshore-manual.com/taxhavens/Bahamas.html

U.S. Bank Involvement in Offshore Banking

• Started in 1960s so that U.S. banks could participate in the growing Eurodollar market, without having to set up operations in Europe. – U.S. banks were not able to do this out of the United

States.

• U.S. bank establishing “offshore” enterprises through a subsidiary structures.

• Why is this still attractive for U.S. banks?– Minimal banking regulations (no FDIC, low/no reserve

requirements) and low taxes.

The International Money Market

• The core of the international money market is the eurocurrency market.– A time deposit in a particular currency with is

other than the national currency of the country in which it is deposited.

– For Example, a U.S. dollar time deposit in banks in London, Hong Kong or Singapore.

• Banks accepting deposits can be host (offshore) banks, or foreign banks (including U.S. banks).

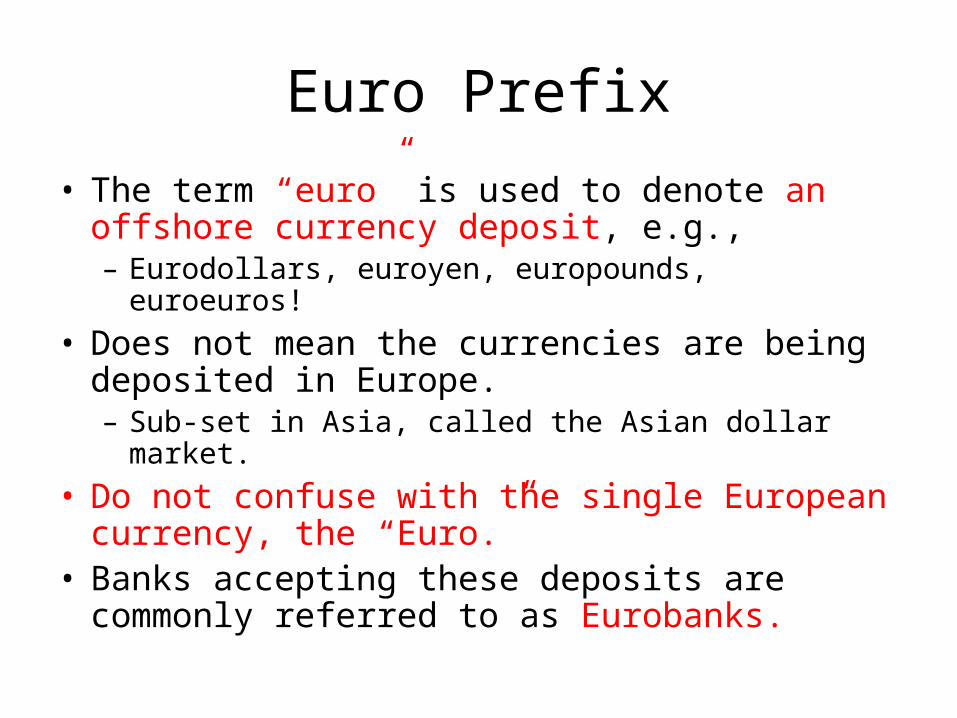

Euro Prefix

• The term “euro” is used to denote an offshore currency deposit, e.g.,– Eurodollars, euroyen, europounds, euroeuros!

• Does not mean the currencies are being deposited in Europe.– Sub-set in Asia, called the Asian dollar market.

• Do not confuse with the single European currency, the “Euro.”

• Banks accepting these deposits are commonly referred to as Eurobanks.

Eurocurrency Market

• The eurocurrency market is a external market that runs alongside a country’s domestic banking market.

• The market is two tiered:– Wholesale (interbank) market where global banks trade among

themselves.• Interbank Offer Rate: The rate charged by banks with excess

currency deposits to lend to other banks. (lending/borrowing rate)• Interbank Bid Rate: The rate at which a bank will accept deposits

from another bank. (deposit rate)• Offer rates higher than bid rates by about 1/8%• Major rates come out of London, thus London Interbank Offer and

Bid rates are important to the market.

– Retail market: where global banks accept deposits from clients and make loans to clients.

Interbank LIBOR Rates (London)

• LIBOR Rates (lending/borrowing), Overnight rates June 14 2004 Oct 22, 2004

US$ Libor 1.05875% 1.79875%Euro Libor 2.04625% 2.06563%£ Libor 4.50000% 4.81313%Yen Libor 0.03125% 0.03375%

LIBOR rates provided by the British Bankers Association and are “fixed” every day at 11:00 a.m. (London time). 8 banks are used in the fix.

• Source: The FT– http://www.marketprices.ft.com/markets/currencies/money

Importance of LIBOR Rates

• Used to calculate forward rates on currencies.– Forward rate offsets the LIBOR differential.

• Used by global banks in “scaling” lending rates to corporate and sovereign entity borrowers:

Lending rate = LIBOR + X (basis points)

Where X basis points is the lender’s estimation of the unique risk associated with a particular borrower.

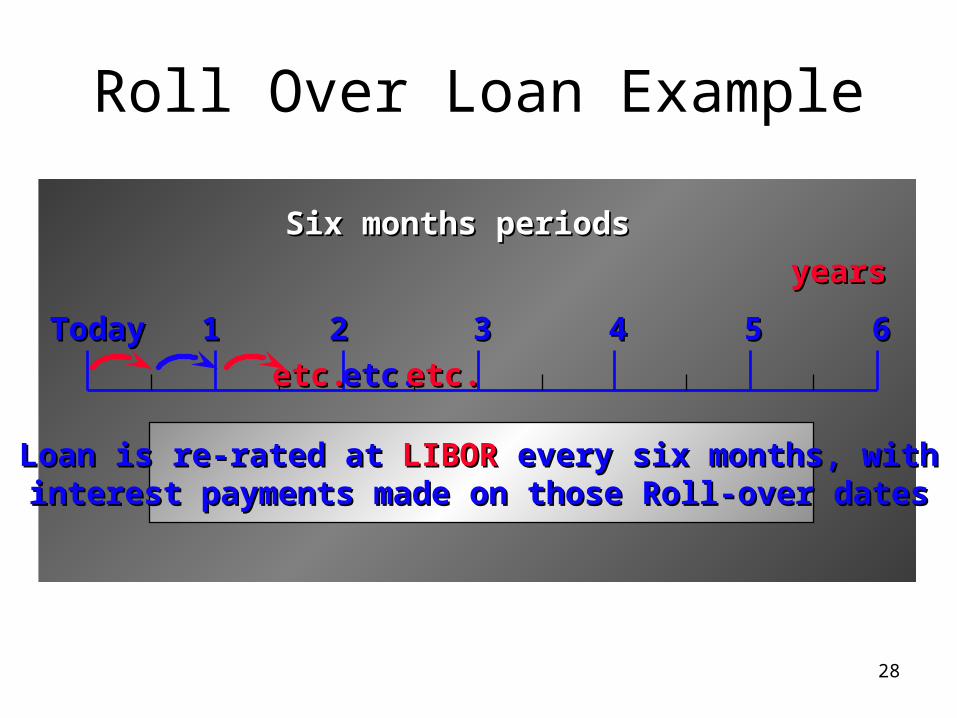

Libor Loans

• Libor loans are generally negotiated on a “roll-over” basis:– Every three to six months the loan is rolled

over at the new LIBOR rate• Thus these are floating rate loans.

– Avoids Eurobanks paying more for their deposits than the returns on their loans.

• Maintains a positive margin on euro-loans for these global banks.

28

Roll Over Loan Example

11 22 33 44 55 66TodayToday

Loan is re-rated at Loan is re-rated at LIBORLIBOR every six months, with every six months, withinterest payments made on those Roll-over datesinterest payments made on those Roll-over dates

Six months periodsSix months periods

yearsyears

etc.etc. etc.etc. etc.etc.