Embed Size (px)

Citation preview

Roberto Di Pietra1

� DEPARTMENT OF BUSINESS AND LAW

ROBERTO DI PIETRA

SIENA, NOVEMBER 4, 2013

International Financial

Accounting (IFA)

Part II - Entities and Financial Reporting Statements

Roberto Di Pietra2

FINANCIAL STATEMENT IFRS COMPLIANT

Part II – Financial Statement IFRS Compliant

� Nature and objectives of financial reporting

� Entities and financial reporting statements

Roberto Di Pietra3

NATURE AND OBJECTIVES OF FINANCIAL REPORTING

• Objectives of an accounting system

� The recording and control of business transactions

• This includes keeping a record of

• The amount of cash and cheques received,

for what and from whom

• The amount of cash and cheques paid, for

what and from whom

• Liabilities, expenses and good purchased

on credit

• Assets and goods sold on credit

Roberto Di Pietra4

NATURE AND OBJECTIVES OF FINANCIAL REPORTING

• Objectives of an accounting system

� The recording and control of business transactions

• The owners of a business

• Wish to safeguard their assets and to ensure that they are being utilized efficiently to produce wealth

• Employ accountants to put in place controls to protect business assets and to advice them on how to company is performing

• The control of assets of the accounting function

ensure that

• the correct amounts are paid to those entitled to them at the appropriate time

• the business’s debts are paid when due

• assets are safeguarded against fraud and misappropriation

Roberto Di Pietra5

NATURE AND OBJECTIVES OF FINANCIAL REPORTING

• Objectives of an accounting system

�Double-entry bookkeeping is regarded as the most

accurate method of bookkeeping

• The duplication is considered as a form of internal

check

�The Law states that companies must keep a proper

record of their transactions

• Final financial statements comprise a statement of profit

and loss showing the amount of profit or loss for the

period and a statement of the financial position showing

the financial position at the end of that period

• Stewardship function (the accountability of an

enterprise’s management for the resources entrusted to

them)

Roberto Di Pietra6

NATURE AND OBJECTIVES OF FINANCIAL REPORTING

• Objectives of an accounting system

�Financial statements are contained within an annual report which includes other reports which provide a vehicle for the management team to communicate directly with the stakeholders

�These other reports could provide information on

• The profitability of the business

• The level of activity and productivity

• The solvency and liquidity position

• The efficiency of credit control procedures

• The efficiency of inventory control procedures

• The effect of any loan on the business’s profitability and financial stability

Roberto Di Pietra7

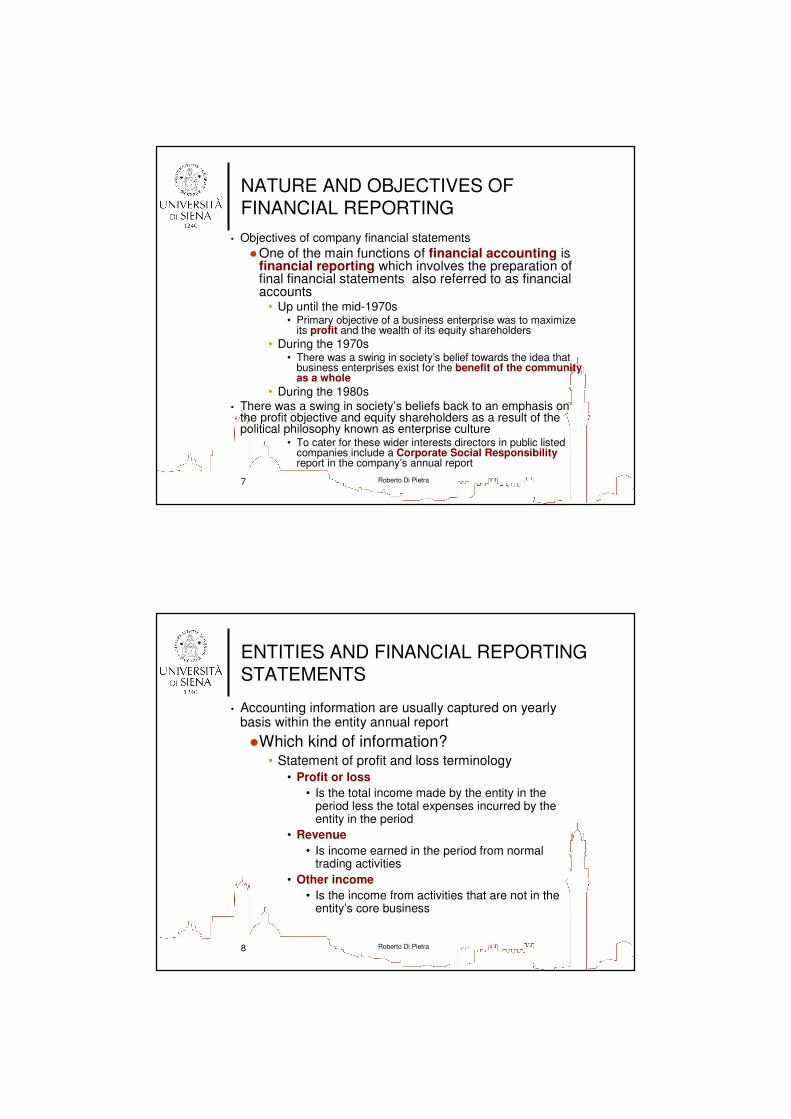

NATURE AND OBJECTIVES OF FINANCIAL REPORTING

• Objectives of company financial statements

�One of the main functions of financial accounting is financial reporting which involves the preparation of final financial statements also referred to as financial accounts

• Up until the mid-1970s• Primary objective of a business enterprise was to maximize

its profit and the wealth of its equity shareholders

• During the 1970s• There was a swing in society’s belief towards the idea that

business enterprises exist for the benefit of the community as a whole

• During the 1980s

• There was a swing in society’s beliefs back to an emphasis on the profit objective and equity shareholders as a result of the political philosophy known as enterprise culture

• To cater for these wider interests directors in public listed companies include a Corporate Social Responsibilityreport in the company’s annual report

Roberto Di Pietra8

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Accounting information are usually captured on yearly basis within the entity annual report

�Which kind of information?• Statement of profit and loss terminology

• Profit or loss

• Is the total income made by the entity in the period less the total expenses incurred by the entity in the period

• Revenue

• Is income earned in the period from normal trading activities

• Other income

• Is the income from activities that are not in the entity’s core business

Roberto Di Pietra9

ENTITIES AND FINANCIAL REPORTING STATEMENTS

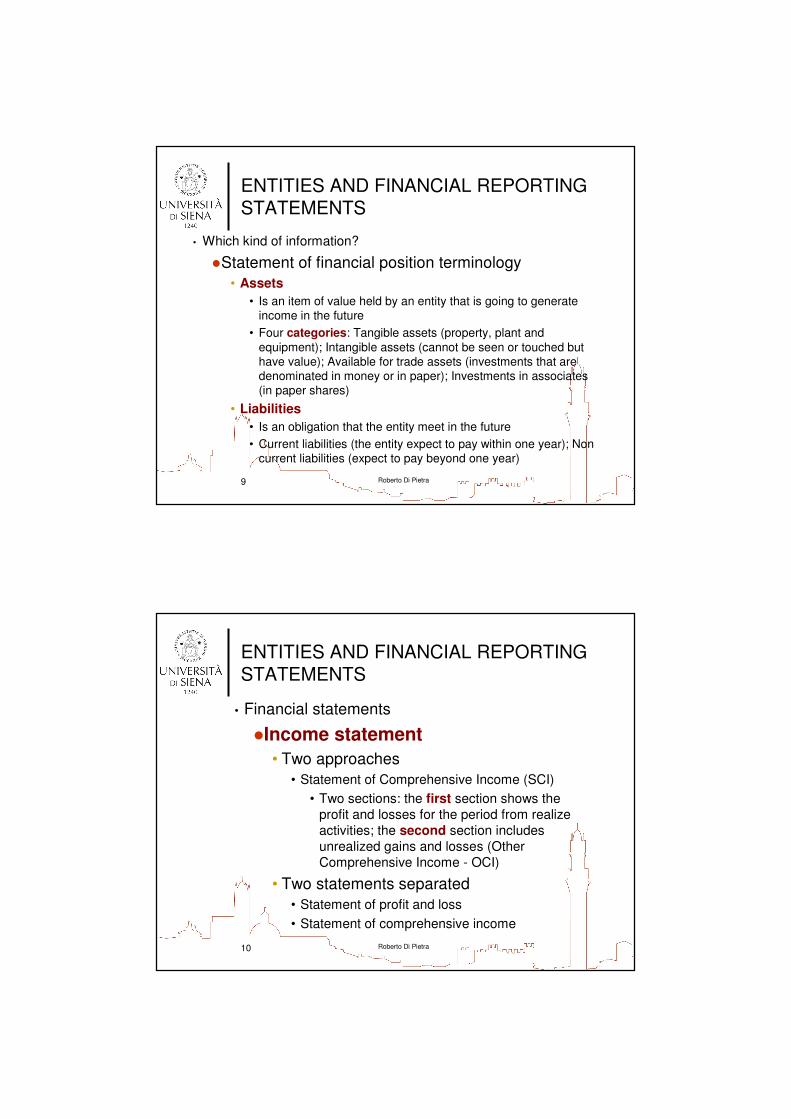

• Which kind of information?

�Statement of financial position terminology

• Assets

• Is an item of value held by an entity that is going to generate

income in the future

• Four categories: Tangible assets (property, plant and

equipment); Intangible assets (cannot be seen or touched but

have value); Available for trade assets (investments that are

denominated in money or in paper); Investments in associates

(in paper shares)

• Liabilities

• Is an obligation that the entity meet in the future

• Current liabilities (the entity expect to pay within one year); Non

current liabilities (expect to pay beyond one year)

Roberto Di Pietra10

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Financial statements

�Income statement

• Two approaches

• Statement of Comprehensive Income (SCI)

• Two sections: the first section shows the

profit and losses for the period from realize

activities; the second section includes

unrealized gains and losses (Other

Comprehensive Income - OCI)

• Two statements separated

• Statement of profit and loss

• Statement of comprehensive income

Roberto Di Pietra11

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Financial statements

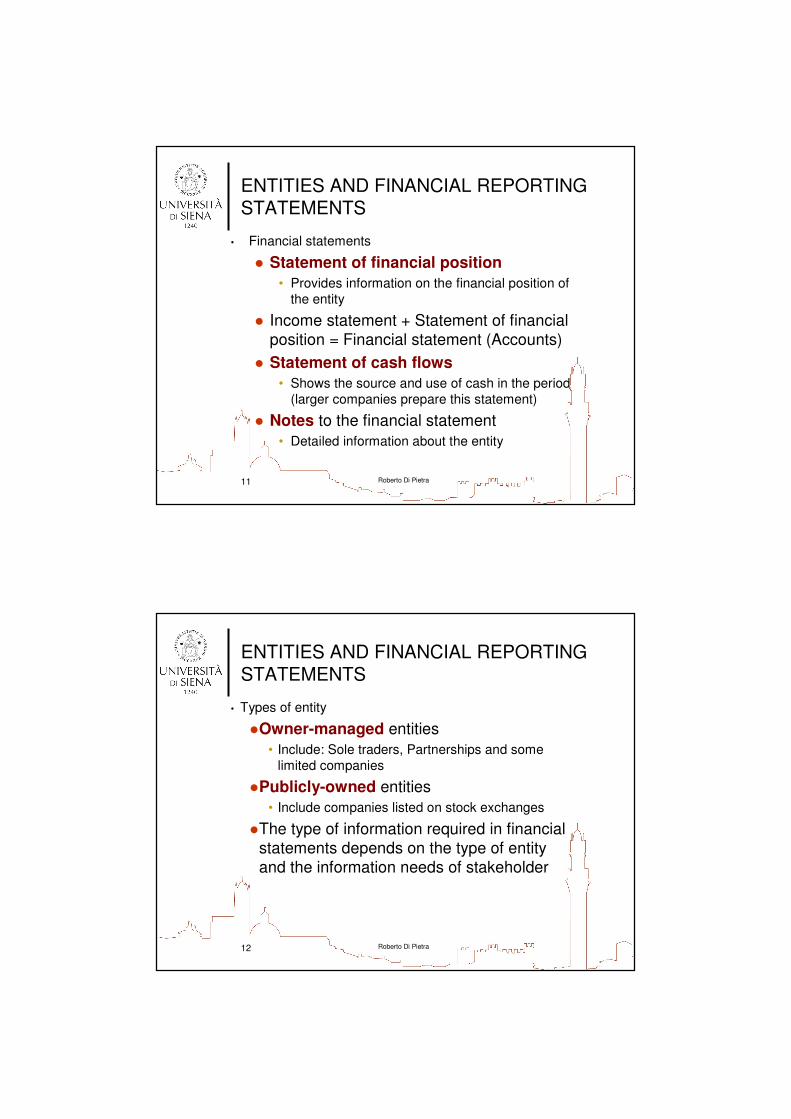

� Statement of financial position

• Provides information on the financial position of

the entity

� Income statement + Statement of financial

position = Financial statement (Accounts)

� Statement of cash flows

• Shows the source and use of cash in the period

(larger companies prepare this statement)

� Notes to the financial statement

• Detailed information about the entity

Roberto Di Pietra12

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Types of entity

�Owner-managed entities

• Include: Sole traders, Partnerships and some

limited companies

�Publicly-owned entities

• Include companies listed on stock exchanges

�The type of information required in financial

statements depends on the type of entity

and the information needs of stakeholder

Roberto Di Pietra13

ENTITIES AND FINANCIAL REPORTING STATEMENTS

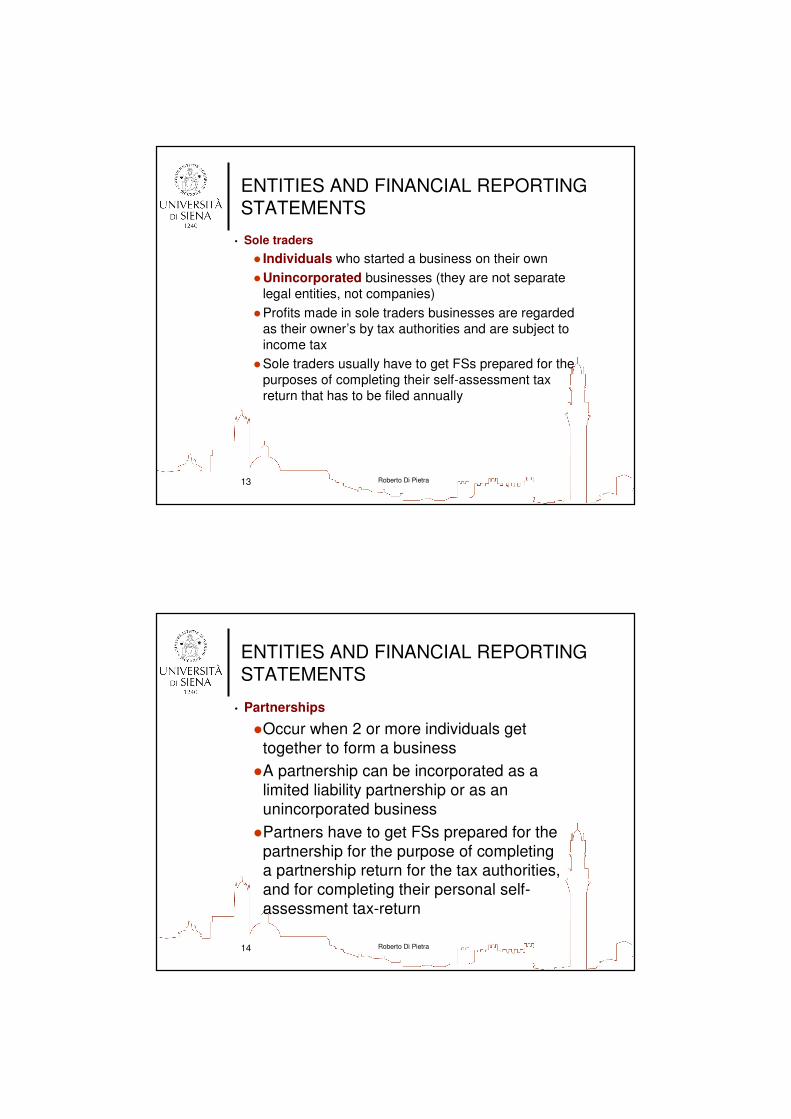

• Sole traders

� Individuals who started a business on their own

�Unincorporated businesses (they are not separate

legal entities, not companies)

�Profits made in sole traders businesses are regarded

as their owner’s by tax authorities and are subject to

income tax

�Sole traders usually have to get FSs prepared for the

purposes of completing their self-assessment tax

return that has to be filed annually

Roberto Di Pietra14

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Partnerships

�Occur when 2 or more individuals get

together to form a business

�A partnership can be incorporated as a

limited liability partnership or as an

unincorporated business

�Partners have to get FSs prepared for the

partnership for the purpose of completing a partnership return for the tax authorities,

and for completing their personal self-

assessment tax-return

Roberto Di Pietra15

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Companies

� Are incorporated by law as separate legal entities

� Can own assets and can take action in their own right

� Are regulated by legislation, the accounting profession and the stock exchange

� 2 most common forms

• Public limited companies

• Private limited companies

� When a company is formed its ownership is split in shares

� The share are sold on stock exchange to members of the public

� A company should prepare a Statement of Comprehensive Income and a Statement of Financial Position

Roberto Di Pietra16

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

� The components of FSs required by IAS1 are

� To report on profit and loss 2 options are available

• The first involves producing a single statement called Comprehensive Income Statement (Comprehensive Income on normal trading activities + Other Comprehensive Income)

• The second is to produce an Income Statement and a separate statement dealing with all non-owner changes in equity (Statement of Other Comprehensive Income)

� To report the net worth of the business, a Statement of Financial Position has to be prepared at the reporting date

� A Statement of Changes in Equity is required to show all owner changes in equity, such as dividend paid to owners, or new shares issues

� A Statement of Cash Flows is also required

Roberto Di Pietra17

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

�Purpose of FSs

• FSs are a structured presentation of the Financial

position and Financial Performance of an Entity

• The Financial position of an entity is shown at a point in

time and is presented as a “BS” under IAS 1

• The Financial performance of an entity is shown for a specific period of time (usually 1 financial year) or an interim period (such as half year). It is presented as an

“CIS” and “CFS” under IAS 1

� IAS 1 does not prescribe “Who” must prepare FSs

• The requirements to prepare FSs usually stems from a

country’s legislative environment and from individual

entities’ constitutions

Roberto Di Pietra18

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

�General purpose FSs are

• those intended to meet the needs who are not in a

position to demand reports that are tailored their

particular information needs

�IAS 1, § 9, states that

• The objective of general purpose FSs is to

provide information about the financial position,

financial performance and cash flows of an entity

that is useful to a wide range of users in making

economic decisions

Roberto Di Pietra19

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

�FSs show the results of management’s stewardship of the resources entrusted to do it

• IAS 1 states that

• To meet this objective financial information should provide information about an entity’s

• Assets

• Liabilities

• Equity

• Income and Expenses (including Gains and Losses)

• Other changes in Equity

• Cash Flows

Roberto Di Pietra20

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

�The components of FSs• IAS 1 requires that a complete set of FSs include the

following:

• A Balance Sheet (BS): Statement of Financial Position

• A Statement of Comprehensive Income (SCI) (or a separate Income statement – IS): Statement of Financial Performance

• A Statement of Changes in Equity (SCE)

• A Cash Flow Statement (CFS): Statement of Cash Flow

• Notes (comprising a summary of significant accounting policies and other explanatory notes)

Roberto Di Pietra21

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

�The components of FSs

• Entities often present other information

• Financial ratios

• Narrative review of operations by management

or the directors

• In some jurisdictions, Entities are obliged

under corporations legislation to prepare a

Directors report (Management report) that

covers, among other matters, commentary on

the results of operations and financial position

of the entity

• Notes are defined in IAS 1, § 11 (read it)

Roberto Di Pietra22

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1 – Presentation of financial statements

�Management Commentary Project• Completed in December 2010

• The IASB has issued the IFRS practice statement Management Commentary (MC)

• The practice statement provides a broad, non-binding framework for the presentation of management commentary that relates to FSs prepared in accordance with IFRS

• The practice statement is not an IFRS

• Entities are not required to comply with the practice statement, unless specifically required by their jurisdiction

• MC is a narrative report that provides a context within which tointerpret the financial position, financial performance and cashflows of an entity

• MC also provides management with an opportunity to explain its objectives and its strategies for achieving those objectives

• MC encompasses reporting that jurisdictions may describe as Management’s Discussion and Analysis (MD&A), Operating and Financial Review (OFR), or Management’s Report (MR)

Roberto Di Pietra23

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations in the presentation of FSs

�Requirements provided by IAS 1• Are intended to ensure that the FSs of an

entity are a faithful presentation of its Financial position, Financial performance and Cash Flow

• Fair presentation and compliance with IFRSs

• Going concern

• Accrual basis of accounting

• Consistency and presentation

• Materiality and aggregation

• Offsetting

Roberto Di Pietra24

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Fair presentation and compliancewith IFRSs

• IAS 1, § 13 states that

• FSs shall present fairly the Financial position,

Financial performance and Cash flow of an

entity

• IAS 1, § 14 requires that

• An entity presenting FSs that are compliant

with IFRSs make an explicit and unreserved

statement of such compliance in the notes to

the FSs

Roberto Di Pietra25

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Fair presentation and compliance with IFRSs

• IAS 1, § 17 says that

• In extremely rare circumstances, management

must depart from IFRSs. This is allowed only if 2

conditions are met

• Management concludes that compliance with a

requirement in a standard or interpretation would be

so misleading that it would conflict with the objective

of FSs set out in the Framework

• The relevant regulatory framework requires, or

otherwise does not prohibit, such a department

Roberto Di Pietra26

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Fair presentation and compliance with IFRSs

• IAS 1, § 22 explains that

• An item of information would be in conflict with the objective of FSs if it did not represent faithfully the

transaction of other events and conditions that it

either purports to represent or could reasonably

expected to represent

• IAS 1, § 18-20 address

• the disclosure requirements when an entity makes

such a departure. In such circumstances, the entity

must disclose (§ 18)

Roberto Di Pietra27

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Going concern

� IAS 1, § 23 states that

• FSs shall be prepared on a going concern basis

unless management intends to either liquidate the

entity or cease trading, or has no realistic

alternative but to do so

• When management is aware of any material

uncertainties that cast doubt upon the entity’s

ability to continue as a going concern, those

uncertainties must be disclosed

• When FSs are not prepared on a going concern

basis, that fact must be disclosed

Roberto Di Pietra28

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Accrual basis of accounting

• FSs must be prepared using the accrual basis of

accounting

�Consistency of presentation

• IAS 1, § 27 requires that

• The presentation and classification of items in the

FSs shall be retained from one period to the next

• When such a change is made, the comparative

information must also be reclassified

• Financial institutions (such as Banks) frequently use

the presentation in order of liquidity

Roberto Di Pietra29

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Materiality and aggregation

• Omissions and misstatements of items are

material if they could, individually or collectively,

influence the economic decisions of users taken

on the basis of the FSs

• Materiality depends on the size and nature of the omission or misstatement judged in the surrounding circumstances. The size or nature of the item, or a combination of both, could be the determining factor

• IAS 1, § 29 states that

• Each material class of similar items must be presented separately in the FSs

• Items of a dissimilar nature or function must be presented separately unless they are immaterial

Roberto Di Pietra30

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Offsetting

• IAS 1, § 32 states that

• Assets and Liabilities, and Income and Expenses,

shall not be offset unless required by a standard

or interpretation

• IAS 32 Financial instruments: Disclosure and

Presentation defines a right of set-off in respect of

Financial assets and liabilities

• For items to be set off under IAS 32 (and IFRS 7)

there must be a legal right of set-off

• This means that there must be a legal agreement

documenting the right of the parties to set off

amounts owed to/from each other

Roberto Di Pietra31

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Offsetting

� IAS 1, § 34-35 go on

• To identify situations where offsetting would be appropriate. These include the following:

• Gains and losses on the disposal of non-current assets should be reported net, instead of separately reporting the gross proceeds as income and the cost of the asset disposed of as an expense

• Expenditure related to a provision recognised in accordance with IAS 37 may be offset against an amount reimbursed under a contractual arrangement with a third party

• Gains and losses arising from a group of similar transactions, such as foreign exchange gains and losses arising on financial instruments held for trading, should be reported net unless they are material

Roberto Di Pietra32

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Overall considerations: IAS 1 Requirements

�Comparative information

• IAS 1, § 36 requires

• The disclosure of comparative information in

respect of the previous period for all amount

reported in the FSs

• This extends to narrative information where the

comparative narrative information remains relevant

• IAS 1 requires that

• When the presentation or classification of items in

the FSs is amended, comparative amounts should

be reclassified

Roberto Di Pietra33

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Structure and content of FSs: general requirements

�The FSs must be identified clearly and distinguished from other information in the same published document

• IAS 1, § 46-50, Other general requirements are:

• Each component of the FSs must be identified clearly

• Disclosure must be made of

• The name of the reporting entity and any change in that name from the preceding reporting date

• Whether the FSs cover the individual entity or a group of entities

• The SFP date or the period covered by FSs

• The presentation currency (as defined in IAS 21: Effects of Changes in Foreign Exchange Rates)

• The level of rounding used in presenting amounts in the FS

Roberto Di Pietra34

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Structure and content of FSs: general requirements

�The FSs must be identified clearly and distinguished from other information in the same

published document

• IAS 1, § 46-50, Other general requirements are:

• FSs must be presented at least annually

• If an entity’s SFP date changes and FSs are

presented for a period longer or shorter than one

year, the entity must disclose, in addition to the

period covered by the FSs:

• The reason for using a longer or shorter period

• The fact that comparative amounts for the SCI,

SCE, SCF and related notes are not entirely

comparable

Roberto Di Pietra35

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• The Objective of a SFP (BS)

� The view on the financial position proposed with a SFP has some limitations that arise from

• The optional measurement of certain assets at historical cost or depreciated historical costrather than at a current value

• The mandatory omission of intangible self-generated Assets from the SFP as result of the recognition and measurement requirements of IAS 38

• Financial engineering that frequently lead to off-SFP rights obligations

� Because of these limitations the SFP should be read in conjunction with the Note to the FSs

Roberto Di Pietra36

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� Assets and Liabilities are classified in a manner that facilitates the evaluation of an entity’s financial structure and its liquidity, solvency and financial flexibility

� Assets and Liabilities are classified according:

1) To their function in the operations of the entity concerned

2) To their liquidity and financial flexibility

Roberto Di Pietra37

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� IAS 1, § 51

� Requires to classify Assets and Liabilities as current or non-current on the face of

its SFP

• Except when a presentation based on liquidity

is considered to provide more relevant and

reliable information

• When this exception arises all assets and

liabilities are required to be presented in order

of liquidity

Roberto Di Pietra38

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� The main classification is considered to be more relevant when an entity has a

clearly identifiable operating cycle

• On this basis it is possible to distinct between

Assets and Liabilities that are expected to

circulate within the entity’s operating cycle and

those used in the entity’s long-term operations

• The typical cycle operates from cash,

purchase of inventory and finally back to cash

through collection of the receivables

Roberto Di Pietra39

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� The average time of the operating varies with the

nature of the operations making up the cycle and

may extend beyond 12 months

• Industries with very long operating cycles may exist

• e.g. we could include real estate development and construction, agriculture (plantation development) and property development

• IAS 1, § 54

• Explains that for financial institutions a presentation base broadly on order of liquidity is usually considered to be more relevant than a current/non-current presentation

• Such entities do not supply goods or services within a clearly identifiable operating cycle

Roberto Di Pietra40

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� IAS 1, § 57 mandate the classification of Assets and Liabilities as current or non-current as follows

• An Asset shall be presented as current when it satisfies “any” of the following criteria:

• a) it is expected to be realised in (or is intended for sale or consumption in) the entity’s normal operating cycle;

• b) it is held primarily for the purpose of being traded;• c) it is expected to be realised within 12 months after

the balance sheet date; or• d) it is cash or a cash equivalent (as defined in IAS 7)

unless it is restricted from being exchanged or used to settle a Liability for at least 12 months after the balance date

• All other Assets shall be considered as non-current

Roberto Di Pietra41

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� IAS 1, § 60 mandate the classification of assets and liabilities as current or non-current as follows:

• A Liability shall be classified as current when it satisfies “any” of the following criteria:

• a) it is expected to be settled in the entity’s normal operating cycle;

• b) it is held primarily for the purpose of being traded;

• c) it is due to be settled within 12 months after the balance date; or

• d) the entity does not have an unconditional right to defer settlement of the liability for at least 12 months after the balance date

� All other Liabilities shall be classified as non-current

Roberto Di Pietra42

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� Current Assets may include inventories

and receivables that are expected to be sold, consumed or realised as part of the

normal operating cycle beyond 12 months

� Current Liabilities may include payables

that are expected to be settled after more

than 12 months after SFP date

Roberto Di Pietra43

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Statement of Financial Position classification

� The criteria for classifying Liabilities as current or non-current are based solely on the conditions existing at the SFP date

� IAS 1, § 61• Clarifies that financial liabilities that are due to be settled within

12 months after the SFP date are classified as current Liabilities

� IAS 1, § 64• Explains that if an entity expects and has the discretion to

refinance or roll over an obligation for at least 12 months after the SFP date an existing loan facility, the obligation is classified as non-current

� IAS 1, § 65• Explains that if an entity breaches an undertaking under a long-

term loan agreement on or before SFP date with the effect that the loan is repayable, the loan is classified as current

Roberto Di Pietra44

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the

face of the SFP

� IAS 1 does not prescribe a standard SFP format that must be adopted

� IAS 1, § 68 prescribes

� A list of items that are considered to

be sufficiently different in nature or function to warrant presentation on the face of the SFP as separate line items

Roberto Di Pietra45

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SFP

� Items required to be included in the SFP:

1) Property, plant and equipment

2) Investment property

3) Intangible assets

4) Financial assets (excluding amounts under (e), (h) and (i)

5) Investments accounted for using the equity method

6) biological assets

7) inventories

8) trade and other receivables

9) cash and cash equivalents

…

Roberto Di Pietra46

ENTITIES AND FINANCIAL REPORTING STATEMENTS

10) the total assets classified as assets for sale and assets included in disposal groups …

11) trade and other payables

12) provisions

13) financial liabilities (excluding amounts shown under (i) and (k)

14) liabilities and assets for current tax (as defined in IAS 12)

15) deferred tax liabilities and deferred tax assets (as defined in IAS 12)

16) minority interest, presented within equity

17) issued capital and reserves attributable to equity holders of the parent

Roberto Di Pietra47

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SFP

� IAS 1, § 69• Requires additional line items, headings and

subtotals to be presented on the SFP when their inclusion is relevant to an understanding of the entity’s financial position

� IAS 1, § 72• Explains that the judgement on whether additional

items should be separately presented is based on an assessment of

a) the nature and liquidity of assets

b) the function of assets within the entity

c) the amounts, nature and timing of liabilities

Roberto Di Pietra48

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SFP or Notes

� IAS 1, § 74

• Requires sub-classifications of the line items

to be presented either on the face of the SFP or

Notes in a manner appropriate to the entity’s

operations

• In some cases the sub-classifications are

governed by a specific IFRS

• IAS 2 requires the total carrying amount of inventories to be broken down into classifications appropriate to the entity (merchandise, production supplies,

materials, work in progress and finished goods)

Roberto Di Pietra49

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Objective of the Statement of Comprehensive Income

� The Statement of Comprehensive Income (SCI) is the primary source for information about an entity’s financial performance

� IAS 1, § 81 requires all items of income and expense recognised in a period to be included in a single statement of comprehensive income or in 2 separate statements, comprising a separate Income Statement reporting components with profit or loss and reporting other components of comprehensive income

� The SCI summarises the elements used to measure profit or loss for the period + gains and losses recognised directly in equity during the period

Roberto Di Pietra50

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Objective – The SCI

� Is the most common measure of an entity’s performance

� Is used to determine other summary indicators (EPS, rates of return on total assets or equity)

� Can be used to assist to predict an entity’s future performance and future cash flows

• This the case if there is appropriate disclosure of unusual items of income and expense that will assist a user in judging the quality of an entity’s performance

• The ability to identify likely non-recurring items of income or expense is of particular significance in making this judgement

Roberto Di Pietra51

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on

the face of the SCI

� IAS 1

• Does not prescribe a standard SCI format that must be adopted

• It prescribes line items that are

considered to be of sufficient

importance to the reporting of the

performance of an entity to warrant their presentation on the face of the

SCI

Roberto Di Pietra52

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SCI

� IAS 1, § 82 requires the following items

1) revenue

2) finance costs

3) share of profit or loss of associates and joint ventures accounted for using the equity method

4) tax expense

5) a single amount comprising the total of (i) the post-tax profit or loss of discontinued operations and (ii) the post-tax gain or loss recognised on the measurement to fair value less costs to sell or on the disposal of the assets or disposal group(s) constituting the discontinued operation

6) profit or loss

Roberto Di Pietra53

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SCI

� The components of OCI referred to in item g) include

• Changes in the FV of available-for-sale investments directly in equity in accordance with IAS 39

• Cash flow hedges deferred in equity in accordance with IAS 39

• Asset revaluation gains recognised in accordance with IAS 16

• Foreign currency gains and losses on translation of the FSs of net investments in foreign operations recognised directly in equity in accordance with IAS 21

• Actuarial gains and losses deferred in equity in accordance with IAS 19

Roberto Di Pietra54

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SCI

� IAS 1, § 83 requires disclosure of the following

items as allocations of profit or loss for the

period in the SCI

• a) profit or loss for the period attributable to:

• i) non-controlling interests

• ii) owners of the parent

• b) total comprehensive income for the

period attributable to:

• i) non-controlling interests

• ii) owners of the parent

Roberto Di Pietra55

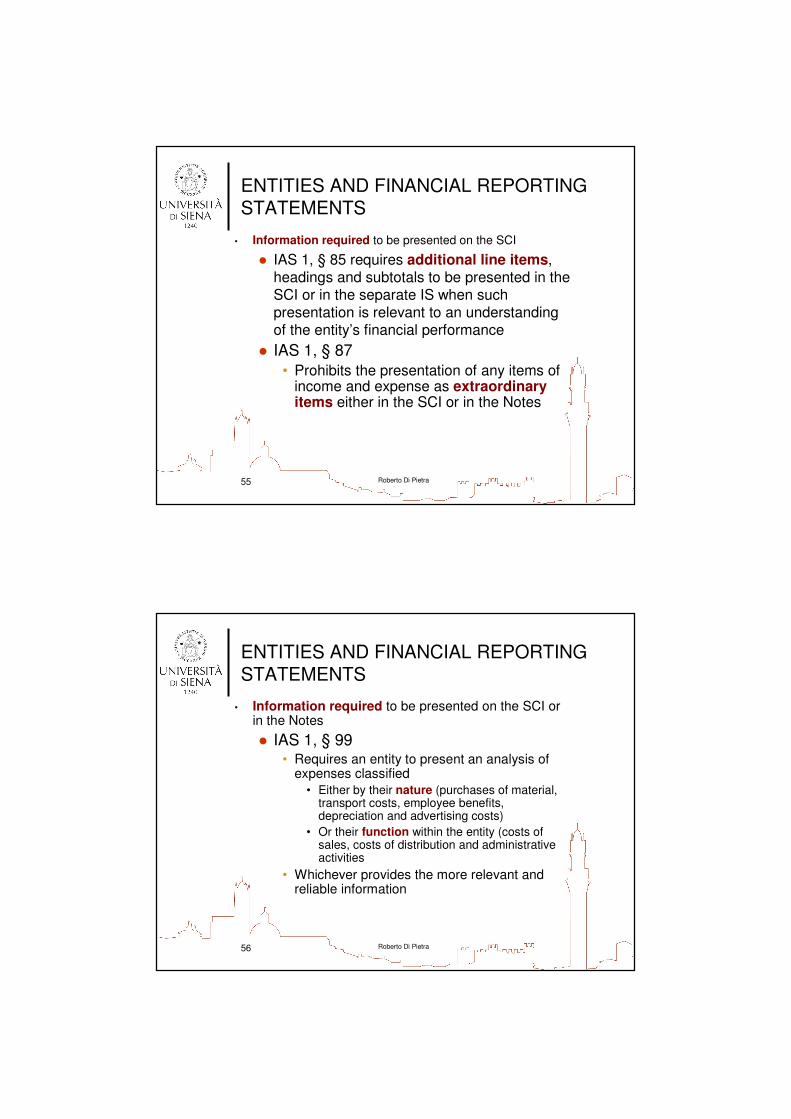

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SCI

� IAS 1, § 85 requires additional line items, headings and subtotals to be presented in the SCI or in the separate IS when such presentation is relevant to an understanding of the entity’s financial performance

� IAS 1, § 87

• Prohibits the presentation of any items of income and expense as extraordinary items either in the SCI or in the Notes

Roberto Di Pietra56

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be presented on the SCI or in the Notes

� IAS 1, § 99• Requires an entity to present an analysis of

expenses classified

• Either by their nature (purchases of material, transport costs, employee benefits, depreciation and advertising costs)

• Or their function within the entity (costs of sales, costs of distribution and administrative activities

• Whichever provides the more relevant and reliable information

Roberto Di Pietra57

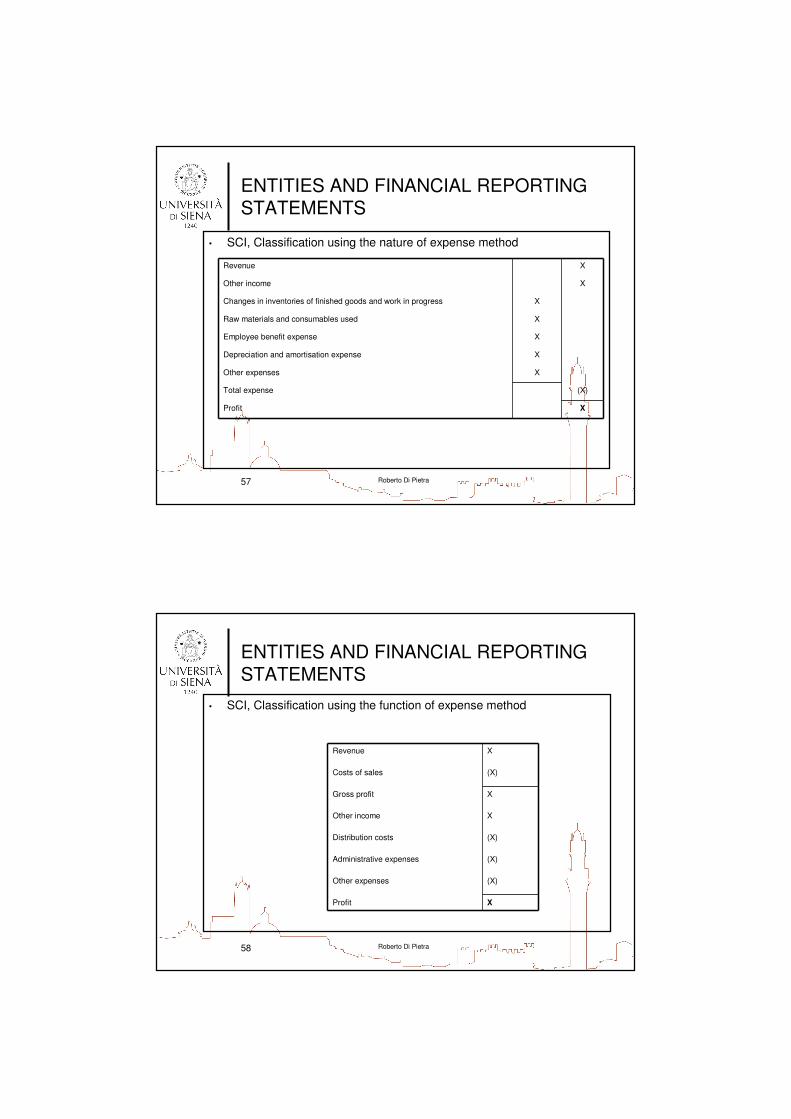

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• SCI, Classification using the nature of expense method

Revenue X

Other income X

Changes in inventories of finished goods and work in progress X

Raw materials and consumables used X

Employee benefit expense X

Depreciation and amortisation expense X

Other expenses X

Total expense (X)

Profit X

Roberto Di Pietra58

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• SCI, Classification using the function of expense method

Revenue X

Costs of sales (X)

Gross profit X

Other income X

Distribution costs (X)

Administrative expenses (X)

Other expenses (X)

Profit X

Roberto Di Pietra59

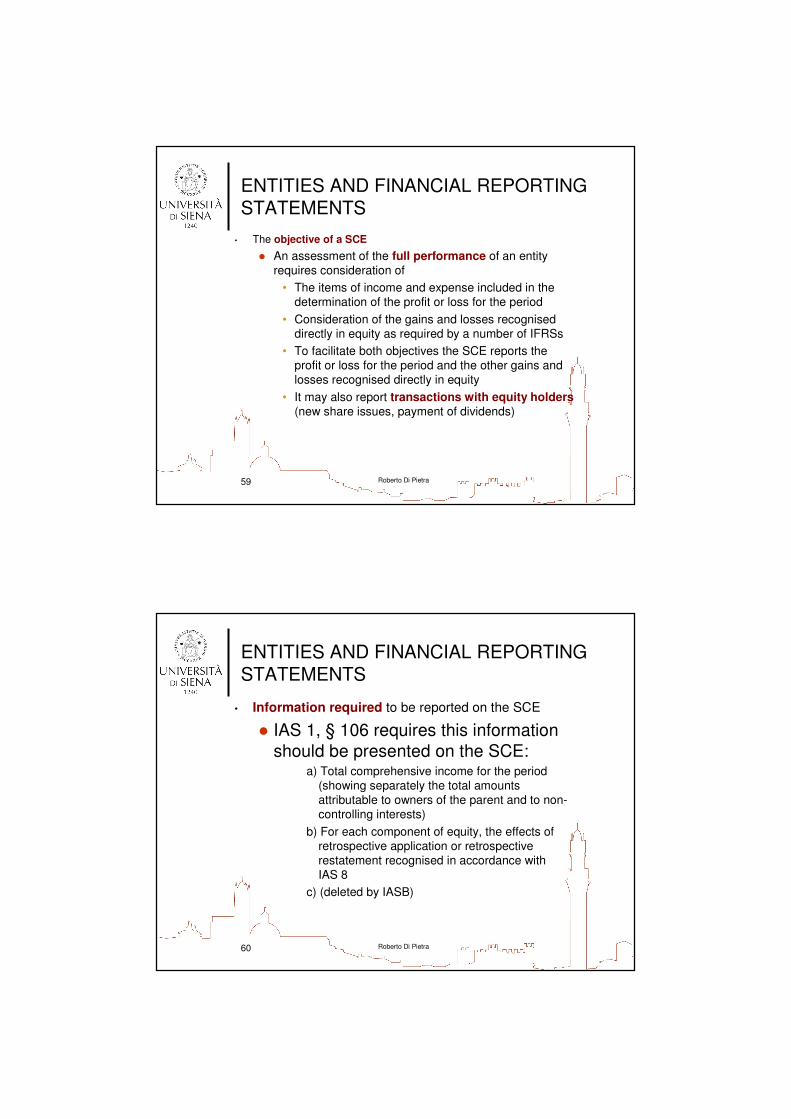

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• The objective of a SCE

� An assessment of the full performance of an entity

requires consideration of

• The items of income and expense included in the

determination of the profit or loss for the period

• Consideration of the gains and losses recognised

directly in equity as required by a number of IFRSs

• To facilitate both objectives the SCE reports the

profit or loss for the period and the other gains and

losses recognised directly in equity

• It may also report transactions with equity holders(new share issues, payment of dividends)

Roberto Di Pietra60

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Information required to be reported on the SCE

� IAS 1, § 106 requires this information

should be presented on the SCE:a) Total comprehensive income for the period

(showing separately the total amounts

attributable to owners of the parent and to non-

controlling interests)

b) For each component of equity, the effects of

retrospective application or retrospective

restatement recognised in accordance with

IAS 8

c) (deleted by IASB)

Roberto Di Pietra61

ENTITIES AND FINANCIAL REPORTING STATEMENTS

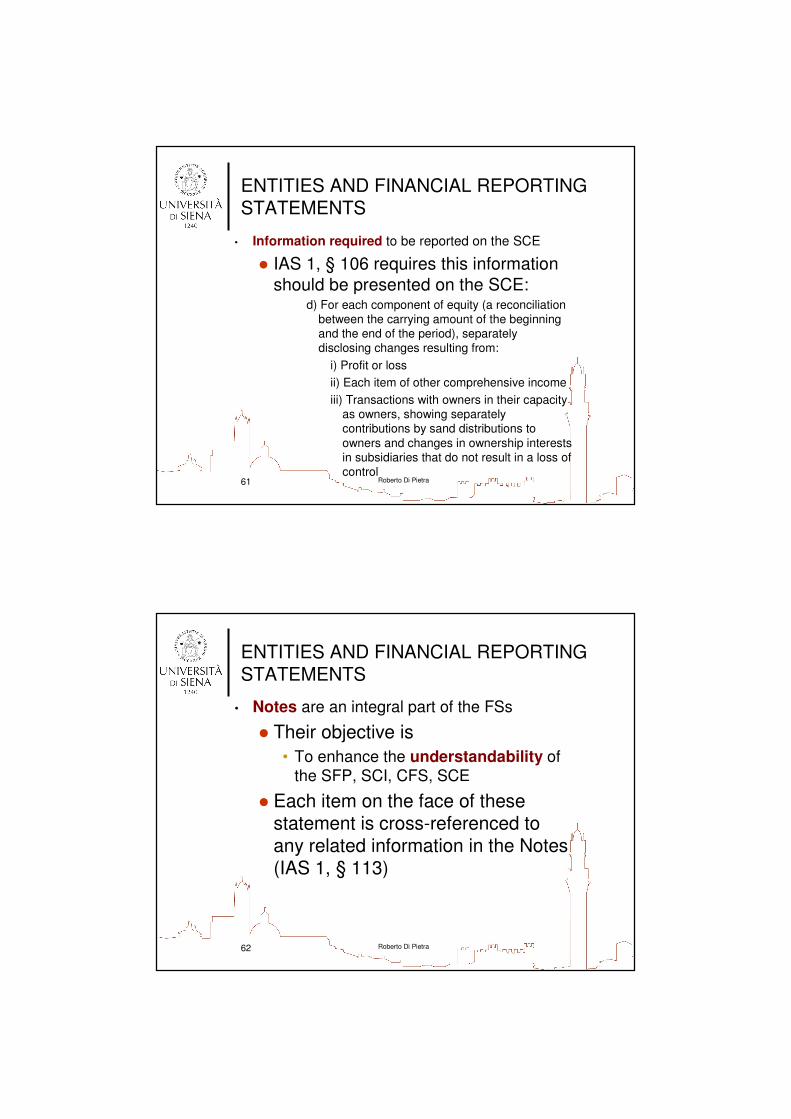

• Information required to be reported on the SCE

� IAS 1, § 106 requires this information

should be presented on the SCE:d) For each component of equity (a reconciliation

between the carrying amount of the beginning

and the end of the period), separately

disclosing changes resulting from:

i) Profit or loss

ii) Each item of other comprehensive income

iii) Transactions with owners in their capacity

as owners, showing separately

contributions by sand distributions to

owners and changes in ownership interests

in subsidiaries that do not result in a loss of

control

Roberto Di Pietra62

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Notes are an integral part of the FSs

� Their objective is

• To enhance the understandability of

the SFP, SCI, CFS, SCE

� Each item on the face of these statement is cross-referenced to any related information in the Notes (IAS 1, § 113)

Roberto Di Pietra63

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1, from 113 to 125 require that the Notes

disclose:

� A statement of compliance with IFRSs

• The basis of the FS’ preparation, including the measurement basis (historical cost, net

realisable value, fair value or recoverable amount)

• Other accounting policies used that are relevant to an understanding of the FSs

• Information about the key assumptions concerning the future, and other key sources

of estimation uncertainty at the SFP data

…

Roberto Di Pietra64

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• The summary of accounting policies is normally presented as the first note to the FSs and ordinarily begins with the required statement of compliance with IFRSs

� The disclosure of accounting policies is particularly relevant to an understanding of the FSs where options exist in FRSs

• The use of the entity method or proportionate consolidation for the recognition of an interest in a jointly controlled entity

• The extending of all borrowings costs or the capitalisation of that portion of borrowing costs applicable to qualifying assets

• The option to revalue property, plant and equipment as an alternative to using historical costs

Roberto Di Pietra65

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• Other disclosures are normally presented in the following

order (IAS 1, § 138)

� Supporting information for items presented on the

face of the BS, IS, SCE and CFS, in the order in

which each statement and each line is presented

� Other disclosures that do not appear on the face

of the BS, IS, CFS and SCE including

• Contingent liabilities

• Unrecognised contractual commitments,

including commitments under operating lease

• Non-financial disclosures, such as an entity’s

risk management objectives and policies

Roberto Di Pietra66

ENTITIES AND FINANCIAL REPORTING STATEMENTS

• IAS 1, § 125 requires the following note disclosures in

regard to dividends of an entity

(a) the amount of dividends proposed or

declared before the FSs were authorised for issue but not recognised as a

distribution to equity holders during the

period, and the related amount per share

(b) the amount of any cumulative preference

dividends not recognised