Embed Size (px)

Citation preview

International Finance

AgendaBalance of paymentParity conditions in International FinanceThe foreign exchange marketFutures and option marketsSwaps and interest derivativesMeasuring and managing translation and transaction exposureMeasuring and managing economic exposure

AgendaBalance of paymentParity conditions in International FinanceThe foreign exchange marketFutures and option marketsSwaps and interest derivativesMeasuring and managing translation and transaction exposureMeasuring and managing economic exposure

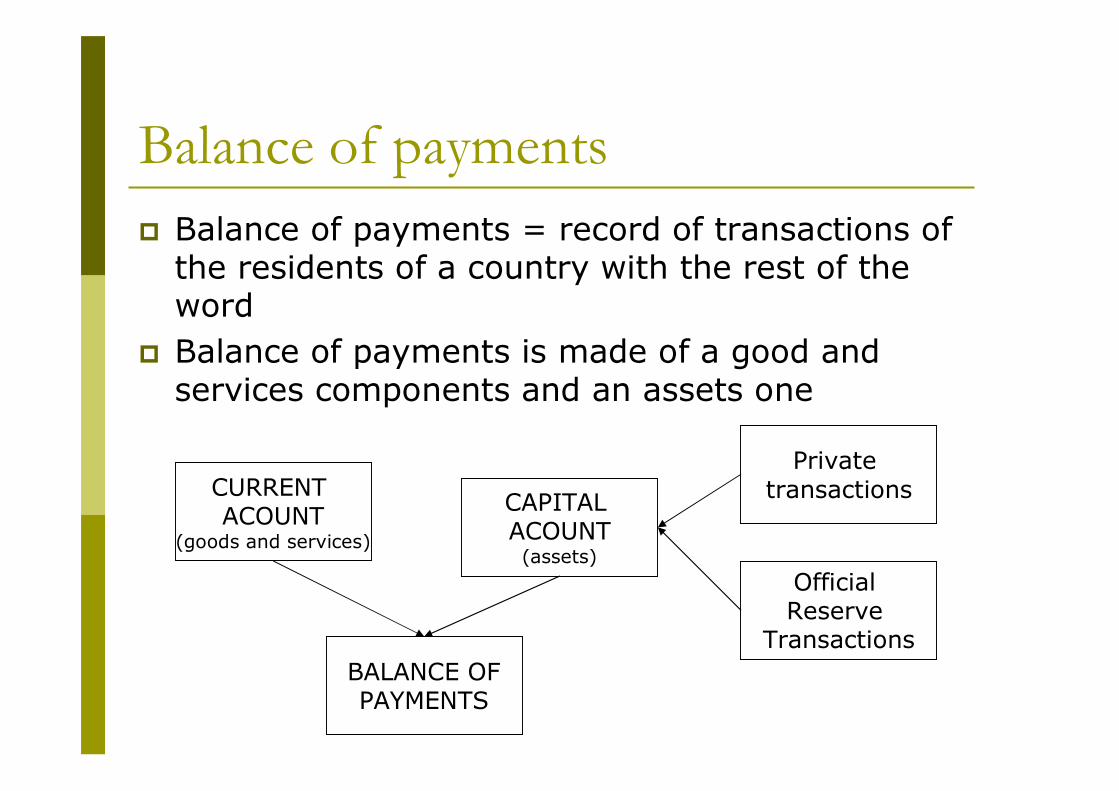

Balance of paymentsBalance of payments = record of transactions of the residents of a country with the rest of the wordBalance of payments is made of a good and services components and an assets one

CURRENT ACOUNT

(goods and services)

CAPITAL ACOUNT

(assets)

BALANCE OFPAYMENTS

Private transactions

Official Reserve

Transactions

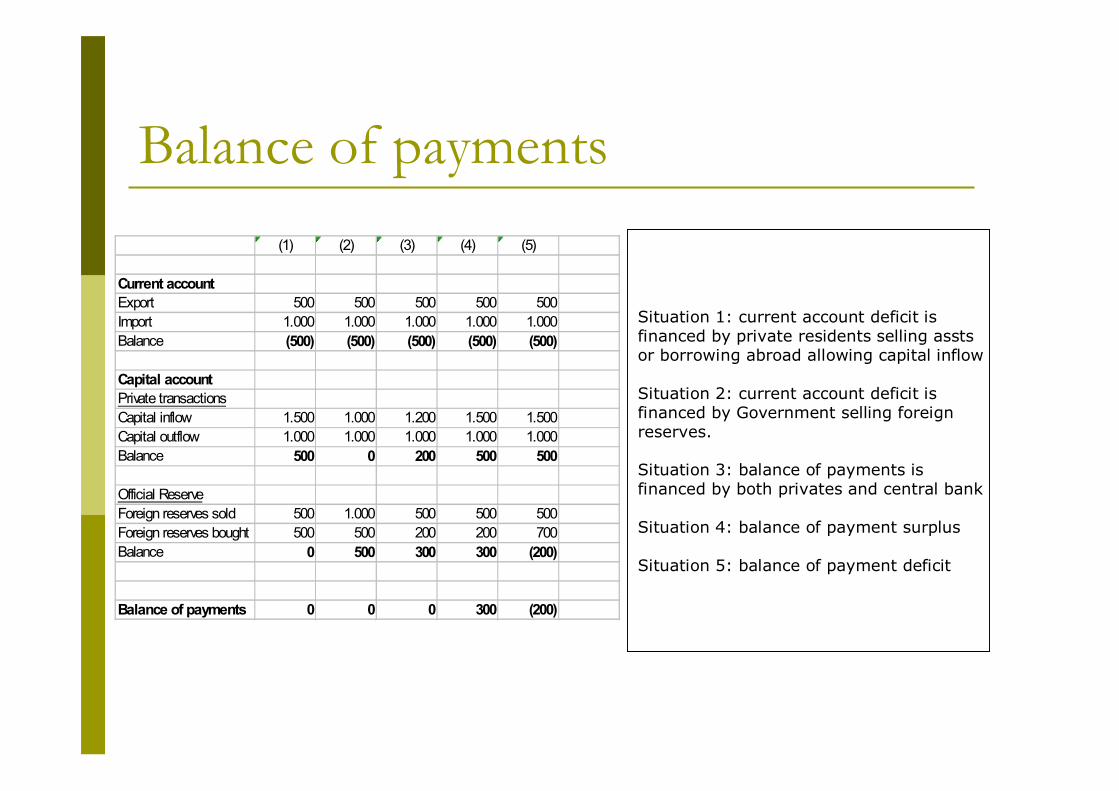

Balance of payments

(1) (2) (3) (4) (5)

Current accountExport 500 500 500 500 500Import 1.000 1.000 1.000 1.000 1.000Balance (500) (500) (500) (500) (500)

Capital accountPrivate transactionsCapital inflow 1.500 1.000 1.200 1.500 1.500Capital outflow 1.000 1.000 1.000 1.000 1.000Balance 500 0 200 500 500

Official ReserveForeign reserves sold 500 1.000 500 500 500Foreign reserves bought 500 500 200 200 700Balance 0 500 300 300 (200)

Balance of payments 0 0 0 300 (200)

Situation 1: current account deficit is financed by private residents selling assts or borrowing abroad allowing capital inflow

Situation 2: current account deficit is financed by Government selling foreignreserves.

Situation 3: balance of payments isfinanced by both privates and central bank

Situation 4: balance of payment surplus

Situation 5: balance of payment deficit

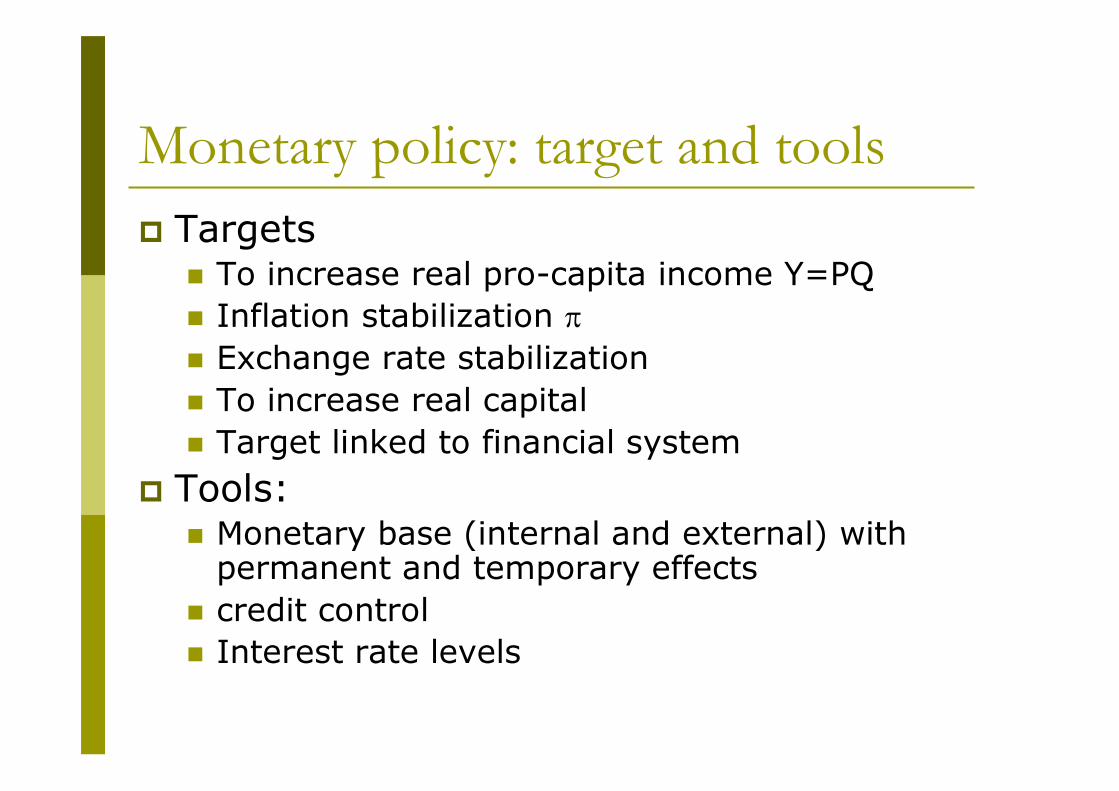

Monetary policy: target and toolsTargets

To increase real pro-capita income Y=PQInflation stabilization Exchange rate stabilizationTo increase real capital Target linked to financial system

Tools:Monetary base (internal and external) with permanent and temporary effectscredit controlInterest rate levels

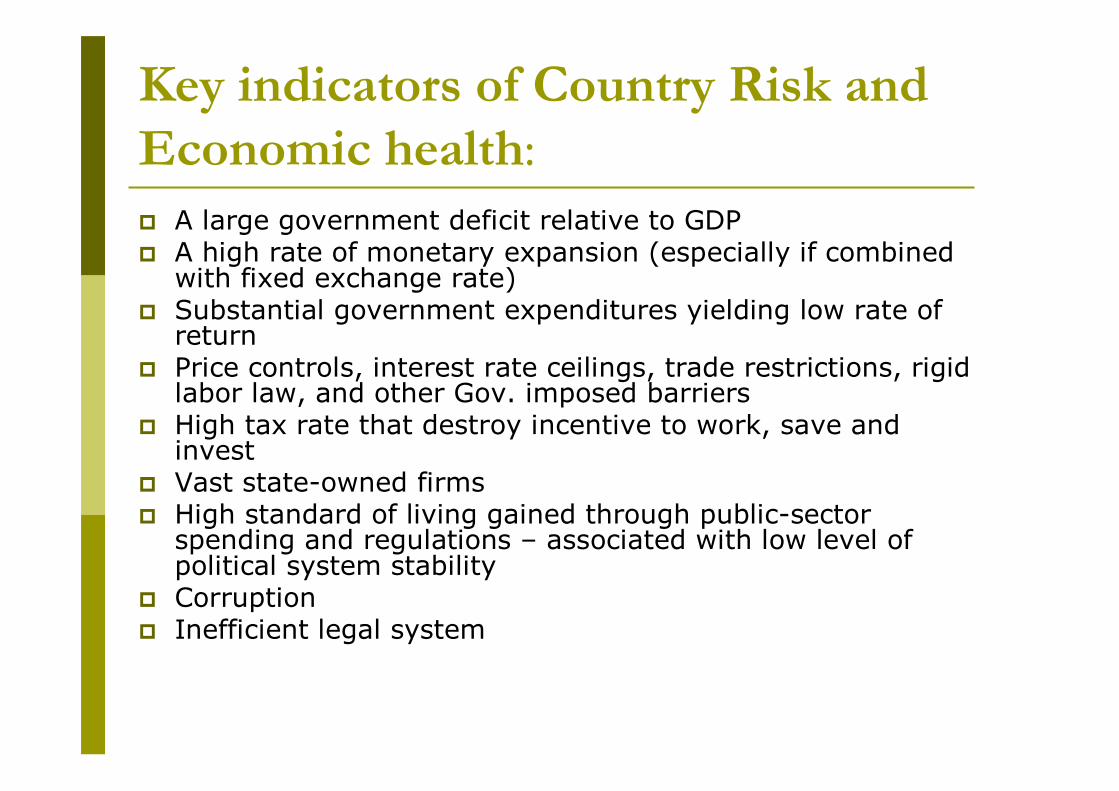

Key indicators of Country Risk and Economic health:

A large government deficit relative to GDPA high rate of monetary expansion (especially if combined with fixed exchange rate)Substantial government expenditures yielding low rate of returnPrice controls, interest rate ceilings, trade restrictions, rigid labor law, and other Gov. imposed barriersHigh tax rate that destroy incentive to work, save and investVast state-owned firmsHigh standard of living gained through public-sector spending and regulations – associated with low level of political system stabilityCorruptionInefficient legal system

Parity conditions in International Finance

..

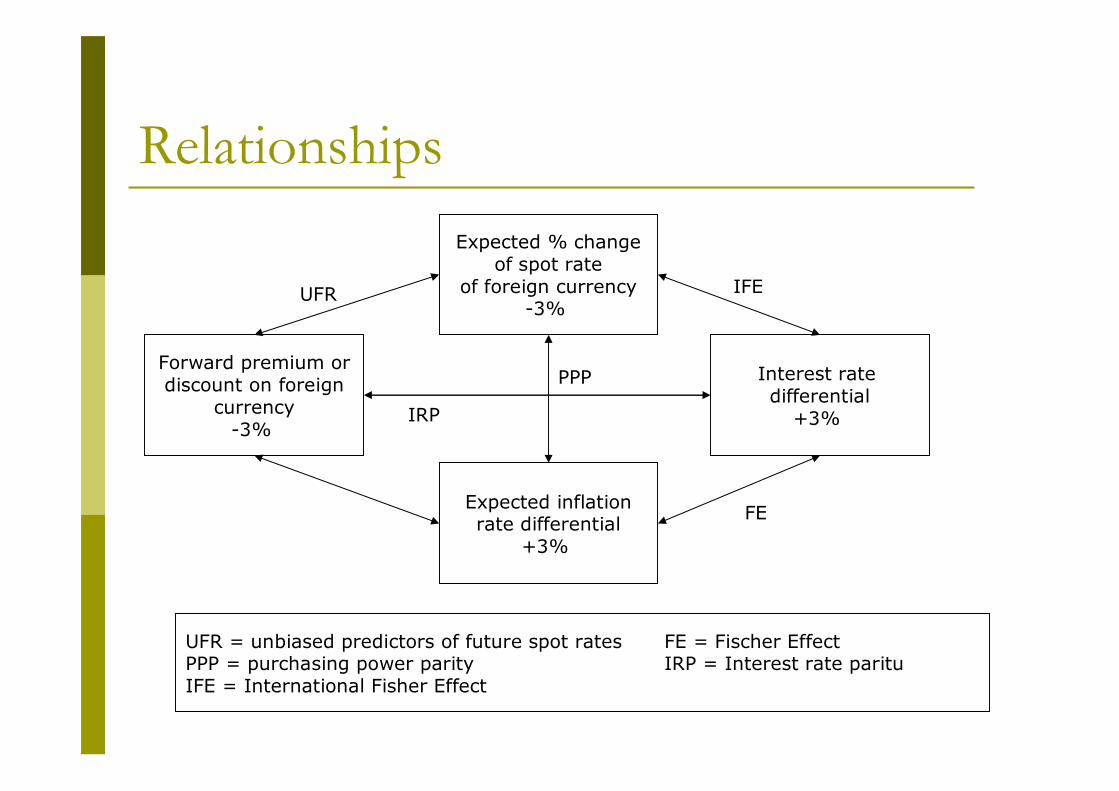

RelationshipsExpected % change

of spot rateof foreign currency

-3%

Interest rate differential

+3%

Expected inflationrate differential

+3%

Forward premium ordiscount on foreign

currency-3%

IFE

FE

IRP

UFR

PPP

UFR = unbiased predictors of future spot rates FE = Fischer EffectPPP = purchasing power parity IRP = Interest rate parituIFE = International Fisher Effect

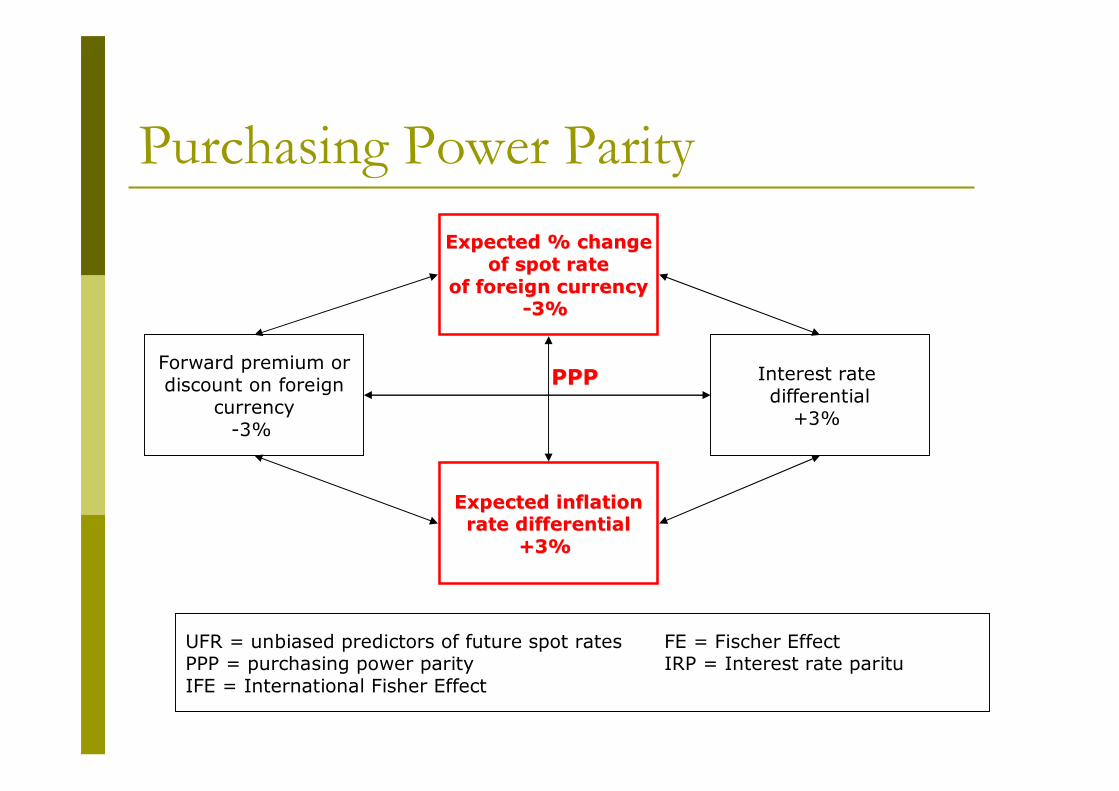

Purchasing Power ParityExpected % changeExpected % change

of spot rateof spot rateof foreign currencyof foreign currency

--3% 3%

Interest rate differential

+3%

Expected inflationExpected inflationrate differentialrate differential

+3% +3%

Forward premium ordiscount on foreign

currency-3%

PPPPPP

UFR = unbiased predictors of future spot rates FE = Fischer EffectPPP = purchasing power parity IRP = Interest rate parituIFE = International Fisher Effect

Purchasing Power Parityet = e0 x (1+ih)t/(1+if)t; et is the PPP rate.For example:

US inflation rate 5%; Switz. inflation rate 3%Spot rate = SFr 1 = $ 0,75et = e0 x (1+ih/1+if)t = 0,75 x (1,05/1,03)3

e3 = 0,7945; it’s the best prediction for the Franc spot rate in 3 years

PPP is also expressed as follow: (et – e0) /e0 = ih – if => exchange rate change should equal the inflation differential.

PPP says that currencies with high rates of inflation should devaluate relative to currencies with lower rates of inflation

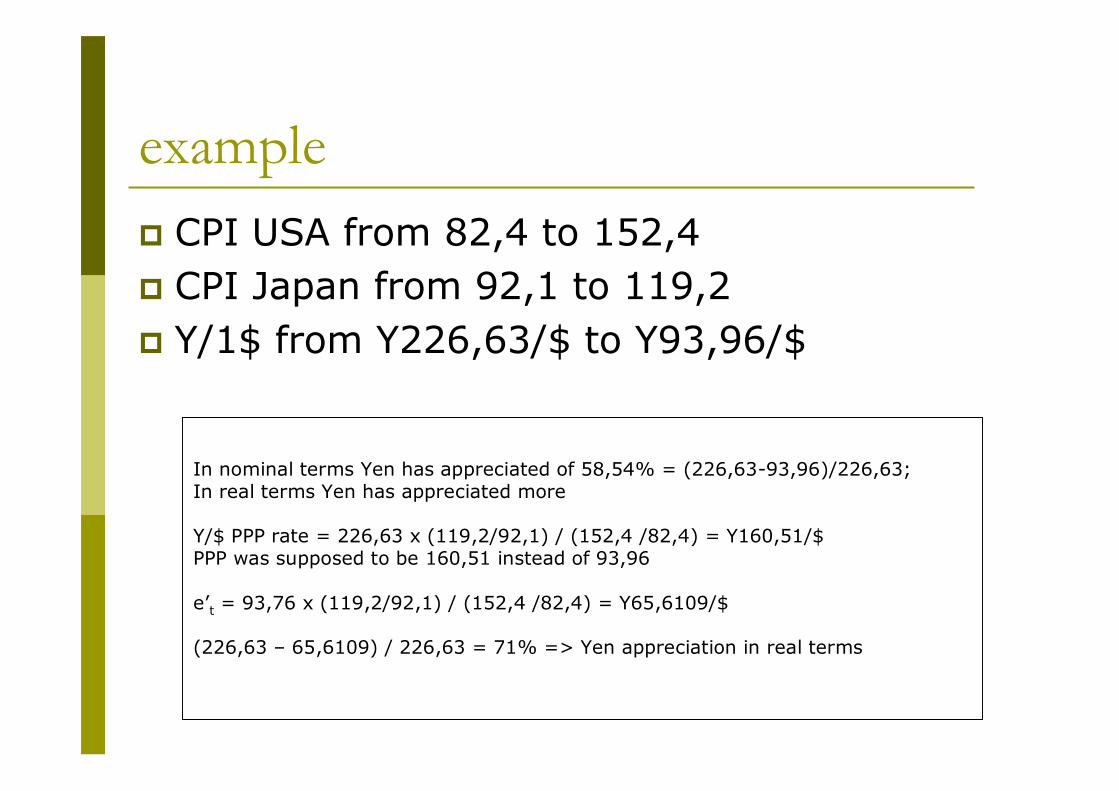

Real exchange rate Changes in nominal exchange rate may be of little significance in determining true effects of currency changes on firs and nations. Rather focus on real purchasing power of one currency relative to another Real exchange rate is nominal exchange rate adjusted for relative purchasing power of each currency since some based period.Real exchange rate at time t e’t relative to base period (specified as time 0) is defined as e’t=etPf/Ph

exampleCPI USA from 82,4 to 152,4CPI Japan from 92,1 to 119,2Y/1$ from Y226,63/$ to Y93,96/$

In nominal terms Yen has appreciated of 58,54% = (226,63-93,96)/226,63;In real terms Yen has appreciated more

Y/$ PPP rate = 226,63 x (119,2/92,1) / (152,4 /82,4) = Y160,51/$PPP was supposed to be 160,51 instead of 93,96

e’t = 93,76 x (119,2/92,1) / (152,4 /82,4) = Y65,6109/$

(226,63 – 65,6109) / 226,63 = 71% => Yen appreciation in real terms

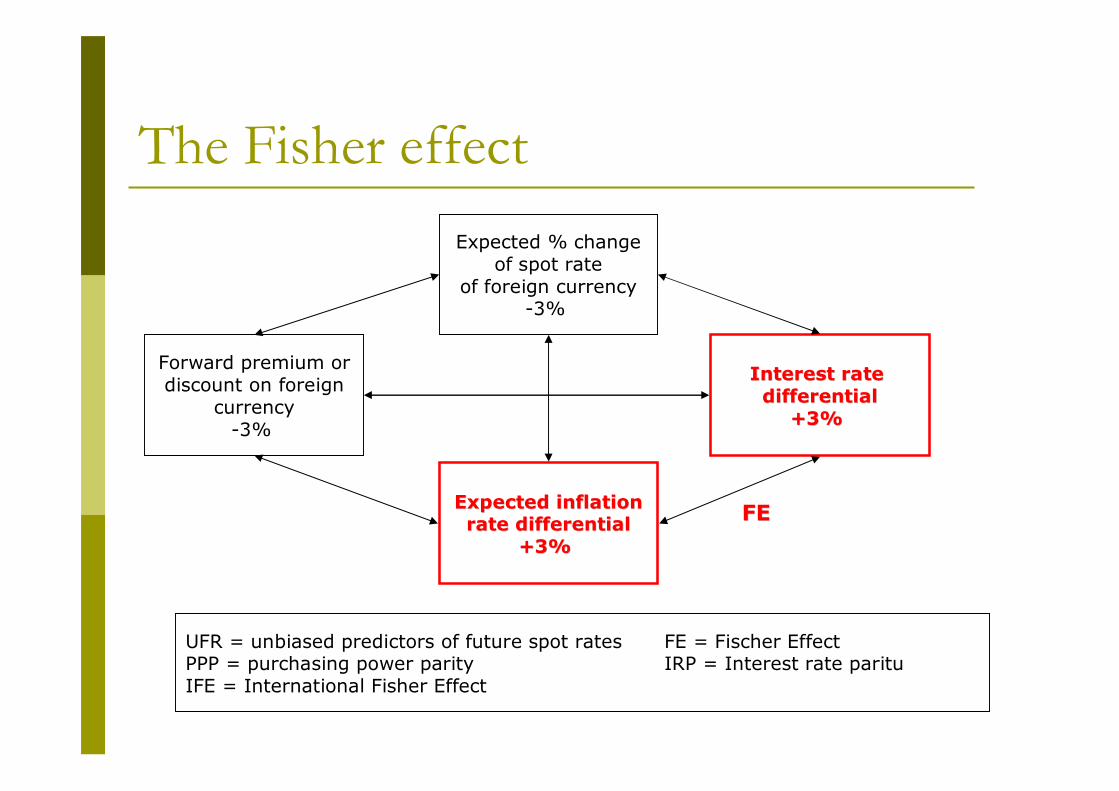

The Fisher effectExpected % change

of spot rateof foreign currency

-3%

Interest rate Interest rate differentialdifferential

+3% +3%

Expected inflationExpected inflationrate differentialrate differential

+3% +3%

Forward premium ordiscount on foreign

currency-3%

FEFE

UFR = unbiased predictors of future spot rates FE = Fischer EffectPPP = purchasing power parity IRP = Interest rate parituIFE = International Fisher Effect

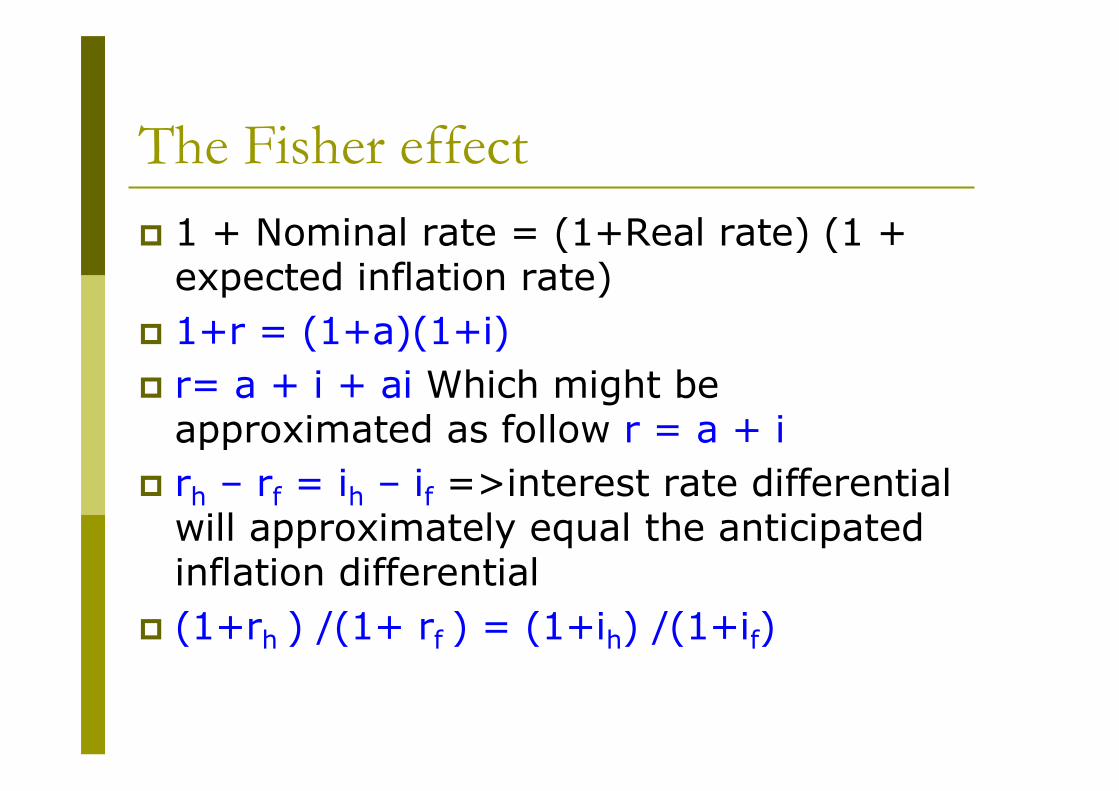

The Fisher effect1 + Nominal rate = (1+Real rate) (1 + expected inflation rate)1+r = (1+a)(1+i)r= a + i + ai Which might be approximated as follow r = a + irh – rf = ih – if =>interest rate differential will approximately equal the anticipated inflation differential (1+rh ) /(1+ rf ) = (1+ih) /(1+if)

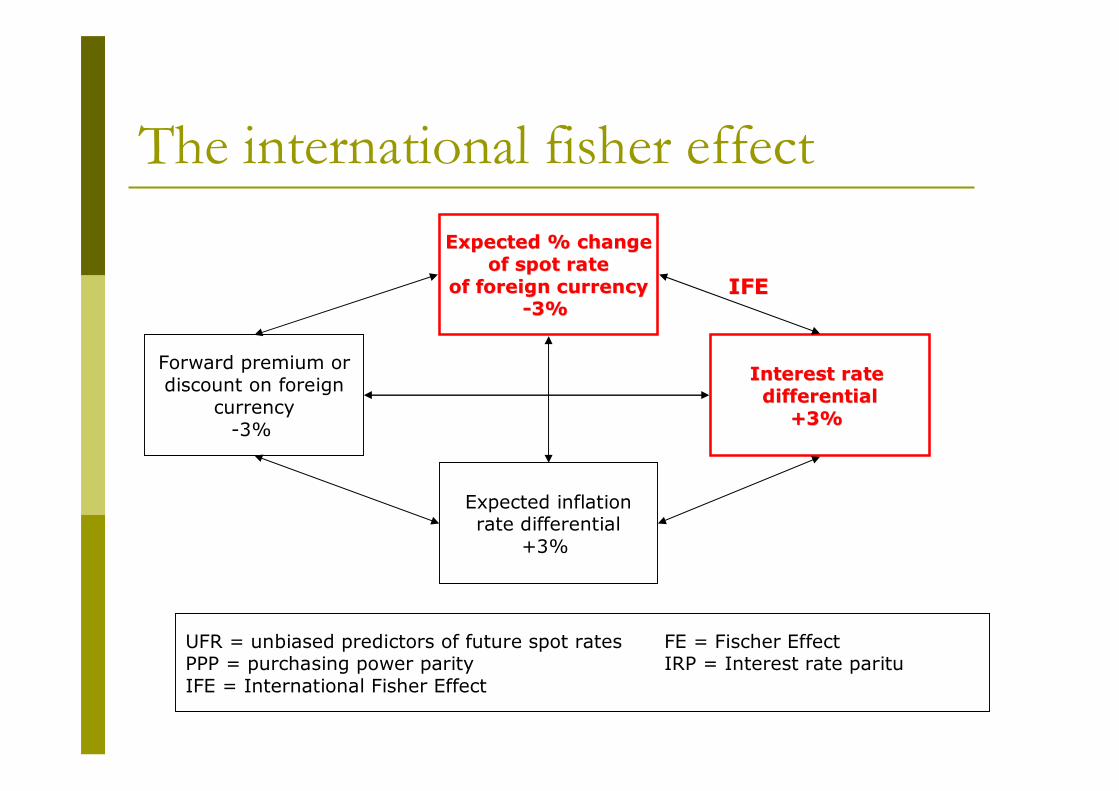

The international fisher effectExpected % changeExpected % change

of spot rateof spot rateof foreign currencyof foreign currency

--3% 3%

Interest rate Interest rate differentialdifferential

+3% +3%

Expected inflationrate differential

+3%

Forward premium ordiscount on foreign

currency-3%

IFEIFE

UFR = unbiased predictors of future spot rates FE = Fischer EffectPPP = purchasing power parity IRP = Interest rate parituIFE = International Fisher Effect

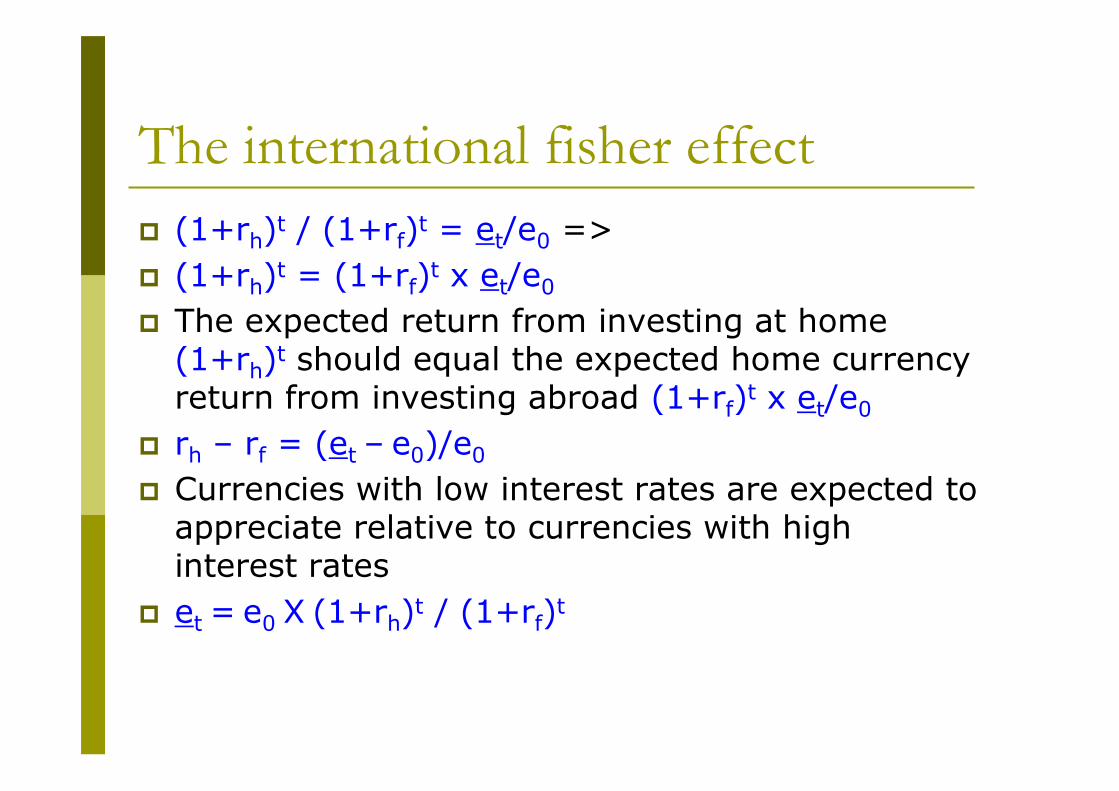

The international fisher effect(1+rh)t / (1+rf)t = et/e0 => (1+rh)t = (1+rf)t x et/e0

The expected return from investing at home (1+rh)t should equal the expected home currency return from investing abroad (1+rf)t x et/e0

rh – rf = (et – e0)/e0

Currencies with low interest rates are expected to appreciate relative to currencies with high interest rates et = e0 X (1+rh)t / (1+rf)t

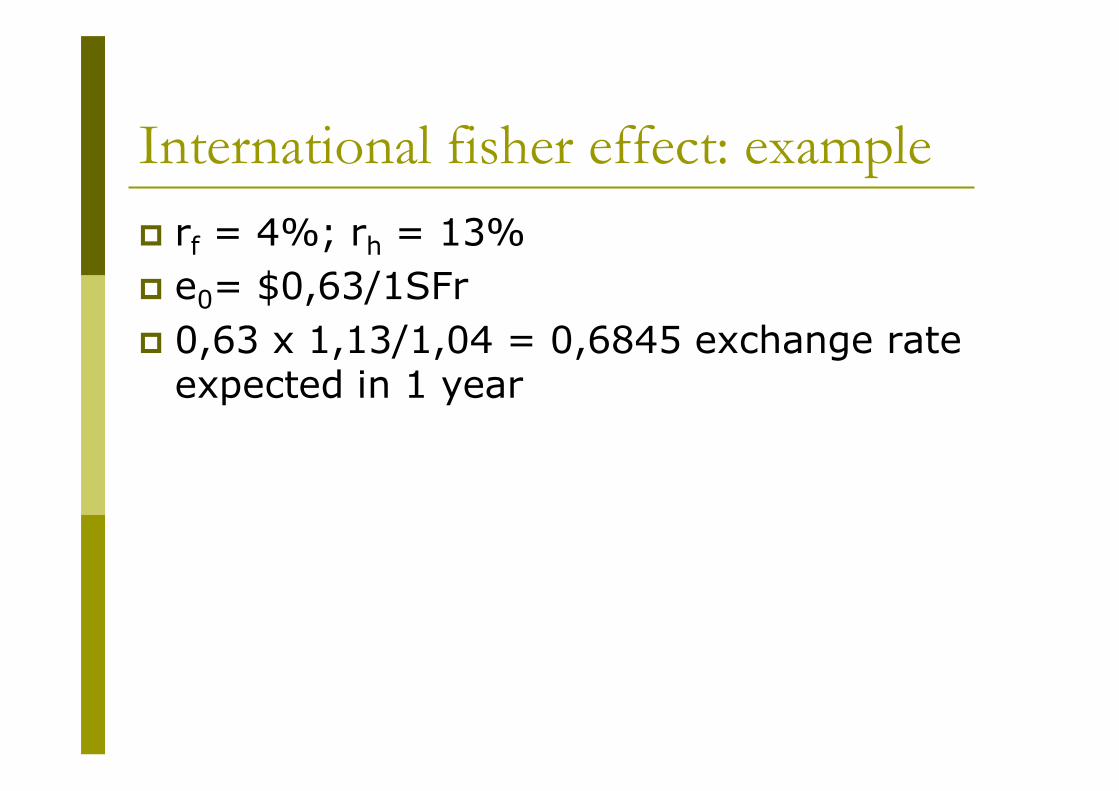

International fisher effect: examplerf = 4%; rh = 13% e0= $0,63/1SFr0,63 x 1,13/1,04 = 0,6845 exchange rate expected in 1 year

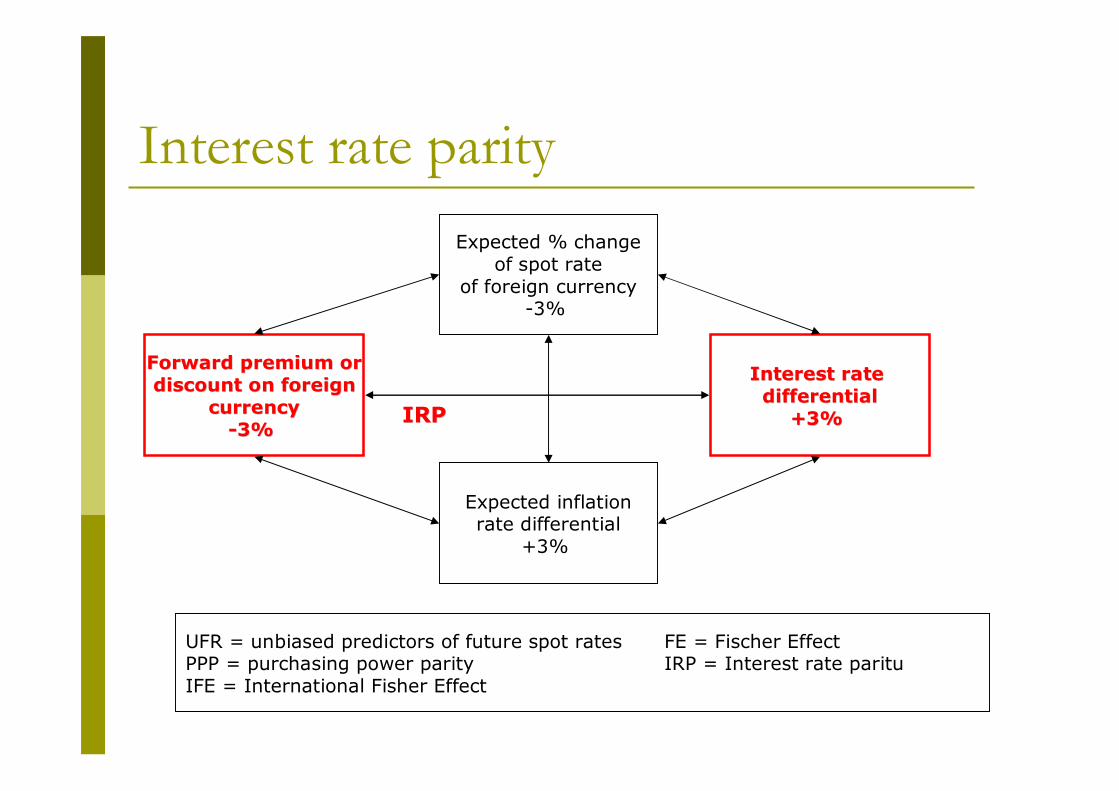

Interest rate parityExpected % change

of spot rateof foreign currency

-3%

Interest rate Interest rate differentialdifferential

+3% +3%

Expected inflationrate differential

+3%

Forward premium orForward premium ordiscount on foreigndiscount on foreign

currencycurrency--3% 3%

IRPIRP

UFR = unbiased predictors of future spot rates FE = Fischer EffectPPP = purchasing power parity IRP = Interest rate parituIFE = International Fisher Effect

Interest rate parityThe currency of the country with a lower interest rate should be at forward premium in terms of the currency of the country with the higher rate.The return on a hedged (or covered) foreign investment will just equal the domestic interest rate on investments of identical risk

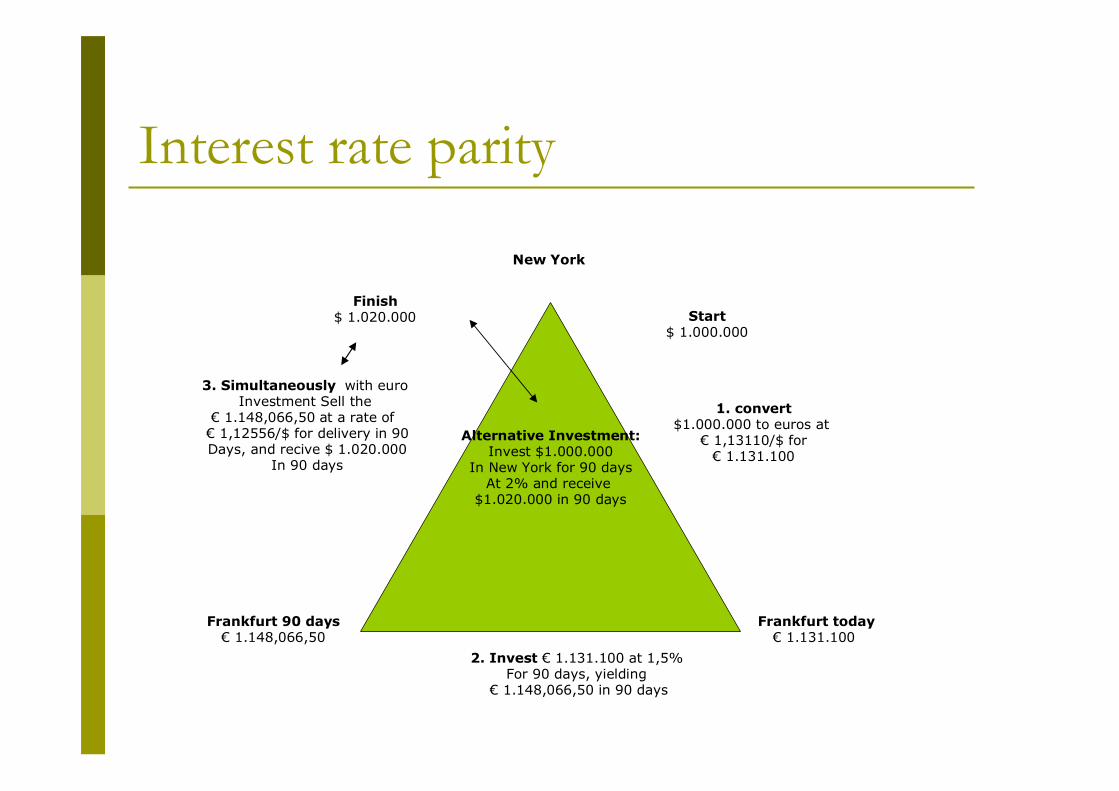

Interest rate parity

Alternative Investment:Invest $1.000.000

In New York for 90 daysAt 2% and receive

$1.020.000 in 90 days

1. convert$1.000.000 to euros at € 1,13110/$ for€ 1.131.100

Frankfurt today€ 1.131.100

Frankfurt 90 days€ 1.148,066,50

3. Simultaneously with euro Investment Sell the

€ 1.148,066,50 at a rate of € 1,12556/$ for delivery in 90Days, and recive $ 1.020.000

In 90 days

Finish$ 1.020.000 Start

$ 1.000.000

New York

2. Invest € 1.131.100 at 1,5% For 90 days, yielding

€ 1.148,066,50 in 90 days

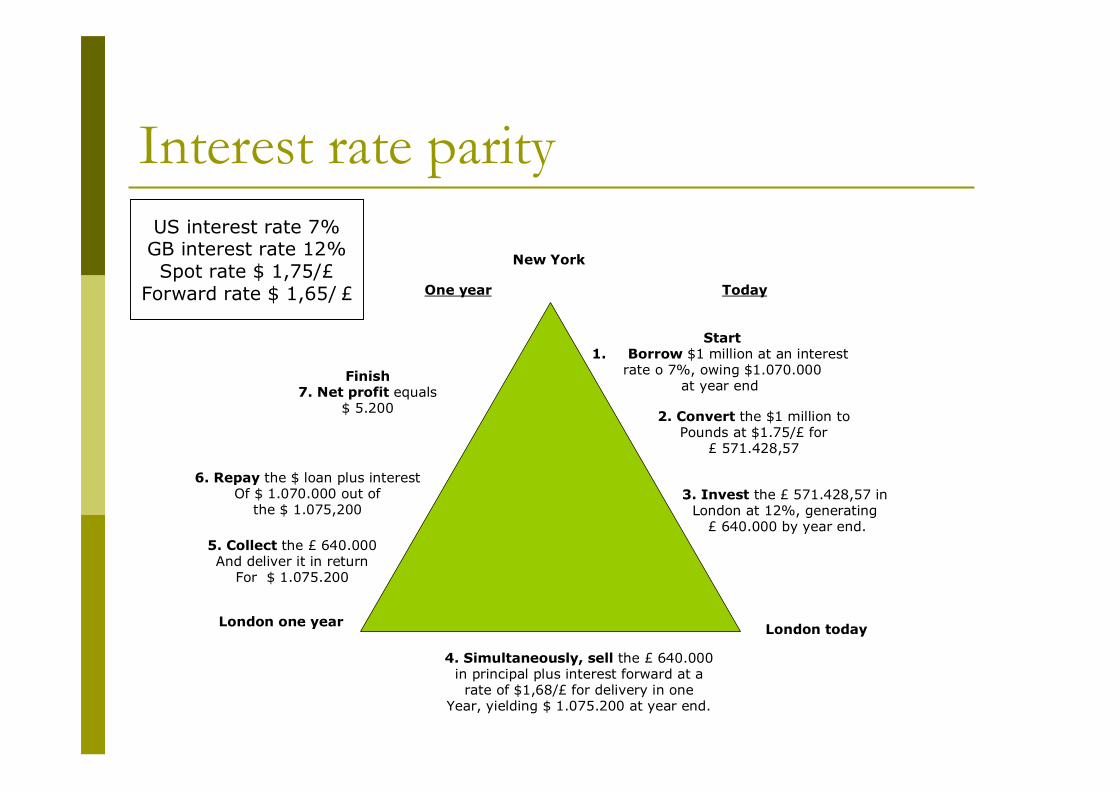

Interest rate parity

2. Convert the $1 million toPounds at $1.75/£ for

£ 571.428,57

London todayLondon one year

Finish7. Net profit equals

$ 5.200

3. Invest the £ 571.428,57 in London at 12%, generating

£ 640.000 by year end.5. Collect the £ 640.000And deliver it in return

For $ 1.075.200

6. Repay the $ loan plus interestOf $ 1.070.000 out of

the $ 1.075,200

One year

Start1. Borrow $1 million at an interest

rate o 7%, owing $1.070.000at year end

New York

4. Simultaneously, sell the £ 640.000in principal plus interest forward at a

rate of $1,68/£ for delivery in oneYear, yielding $ 1.075.200 at year end.

Today

US interest rate 7%GB interest rate 12%Spot rate $ 1,75/£

Forward rate $ 1,65/ £

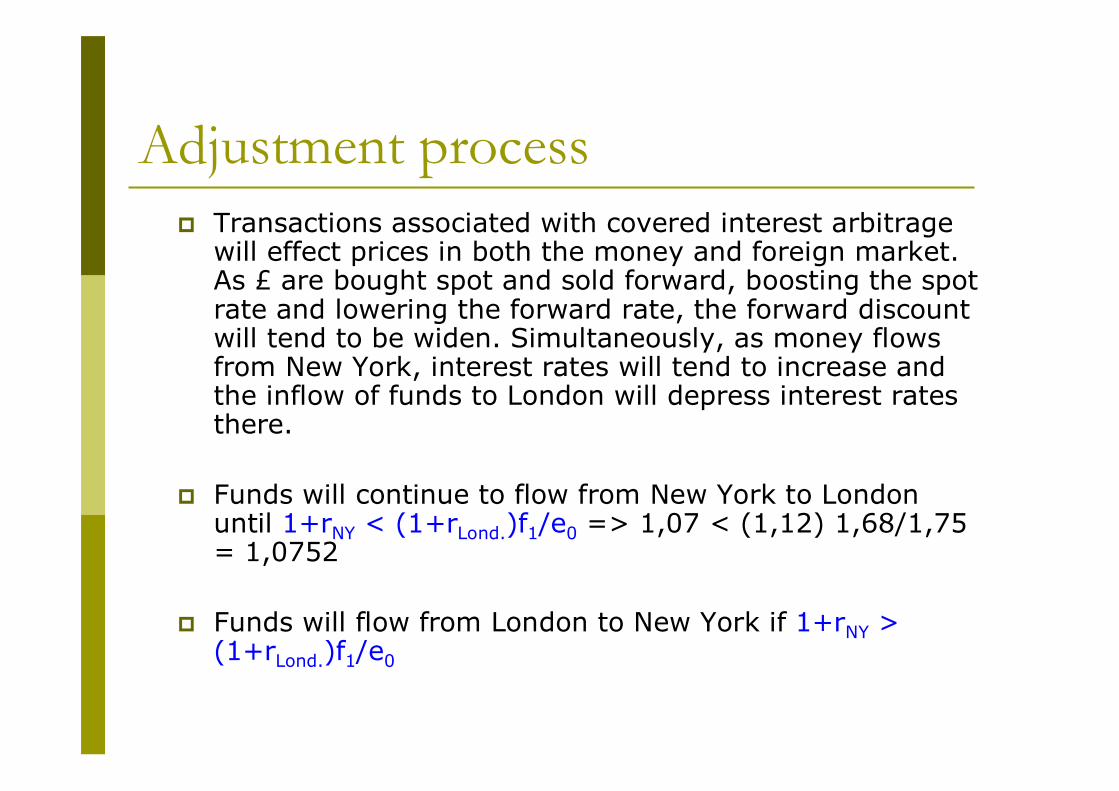

Adjustment processTransactions associated with covered interest arbitrage will effect prices in both the money and foreign market. As £ are bought spot and sold forward, boosting the spot rate and lowering the forward rate, the forward discount will tend to be widen. Simultaneously, as money flows from New York, interest rates will tend to increase and the inflow of funds to London will depress interest rates there.

Funds will continue to flow from New York to London until 1+rNY < (1+rLond.)f1/e0 => 1,07 < (1,12) 1,68/1,75 = 1,0752

Funds will flow from London to New York if 1+rNY > (1+rLond.)f1/e0

Interest rate parity Interest rate parity holds when there are no covered interest arbitrage opportunity No arbitrage condition can be stated as follow: (1+rh)/(1+rf)= f1/e0

rh – rf = (f1 – e0)/e0

High interest rates on a currency are offset by forward discounts; low interest rates on a currency are offset by forward premium

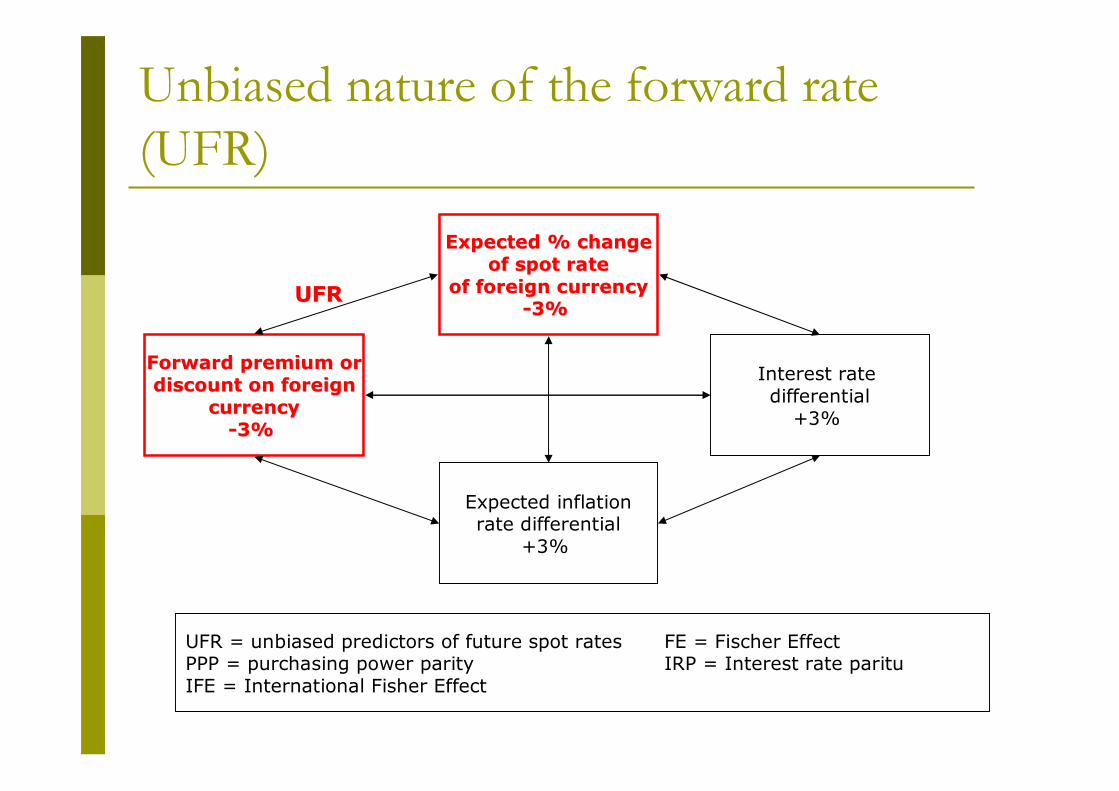

Unbiased nature of the forward rate (UFR)

Expected % changeExpected % changeof spot rateof spot rate

of foreign currencyof foreign currency--3% 3%

Interest rate differential

+3%

Expected inflationrate differential

+3%

Forward premium orForward premium ordiscount on foreigndiscount on foreign

currencycurrency--3% 3%

UFRUFR

UFR = unbiased predictors of future spot rates FE = Fischer EffectPPP = purchasing power parity IRP = Interest rate parituIFE = International Fisher Effect

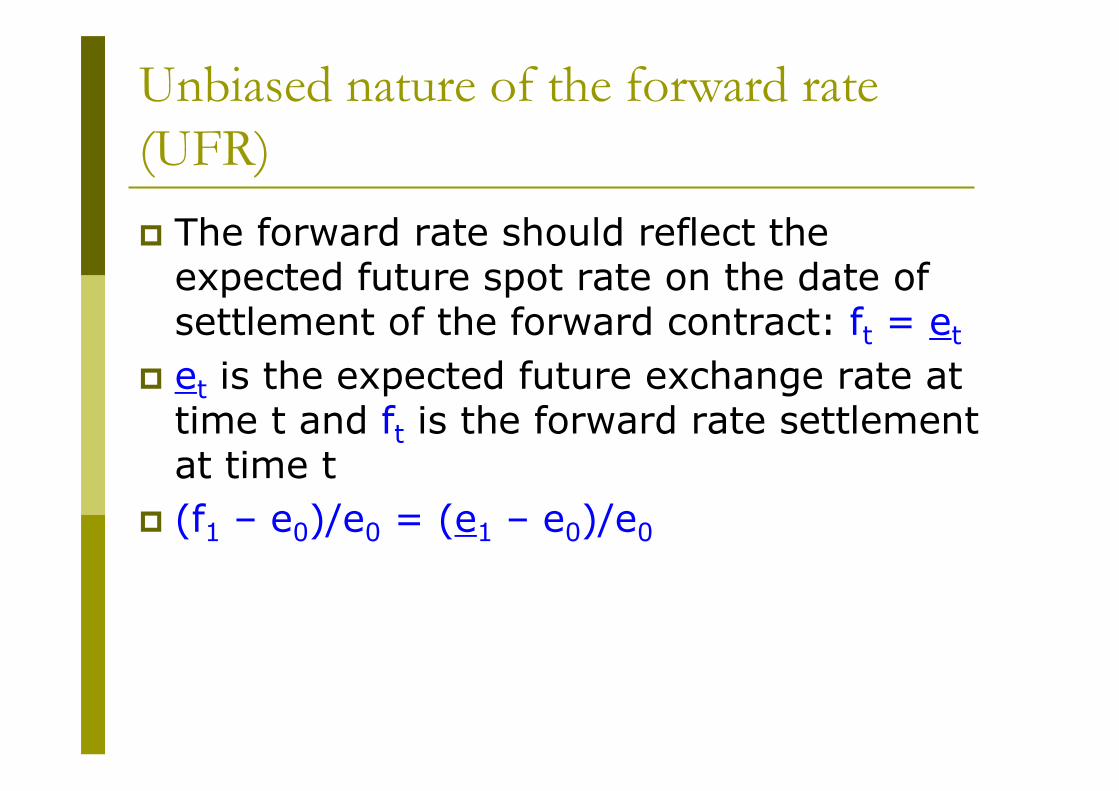

Unbiased nature of the forward rate (UFR)

The forward rate should reflect the expected future spot rate on the date of settlement of the forward contract: ft = et

et is the expected future exchange rate at time t and ft is the forward rate settlement at time t(f1 – e0)/e0 = (e1 – e0)/e0

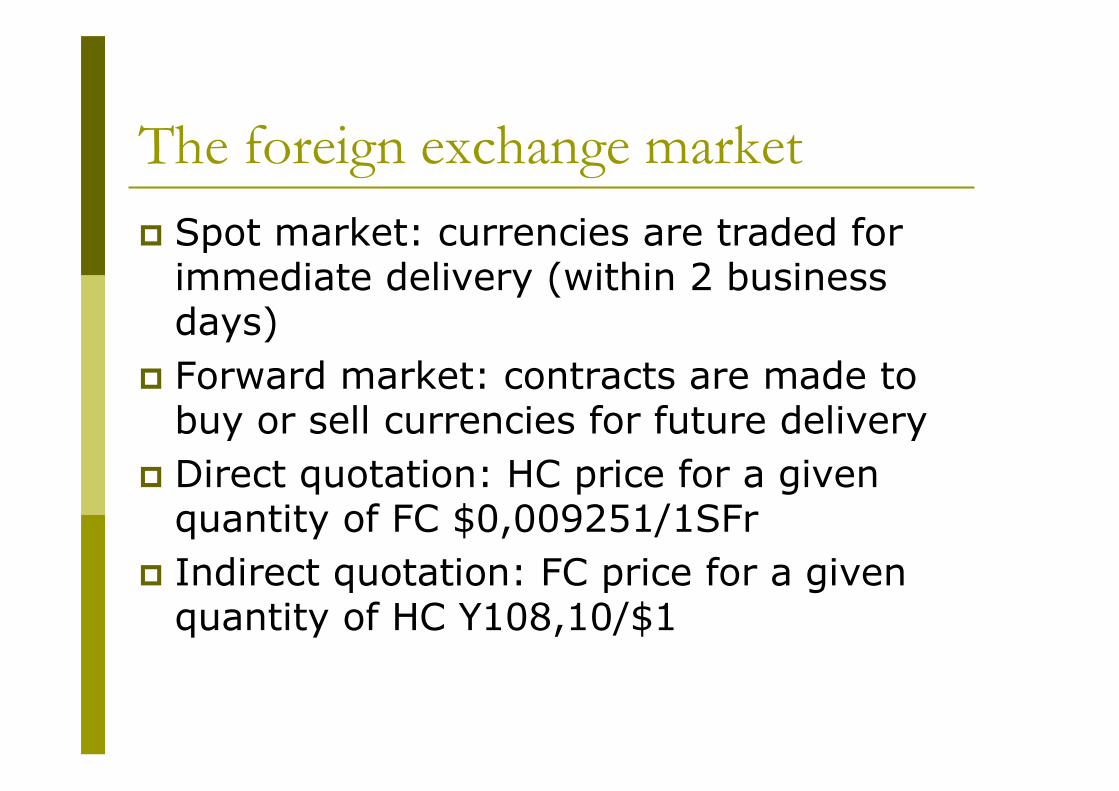

The foreign exchange market

The foreign exchange marketSpot market: currencies are traded for immediate delivery (within 2 business days)Forward market: contracts are made to buy or sell currencies for future deliveryDirect quotation: HC price for a given quantity of FC $0,009251/1SFrIndirect quotation: FC price for a given quantity of HC Y108,10/$1

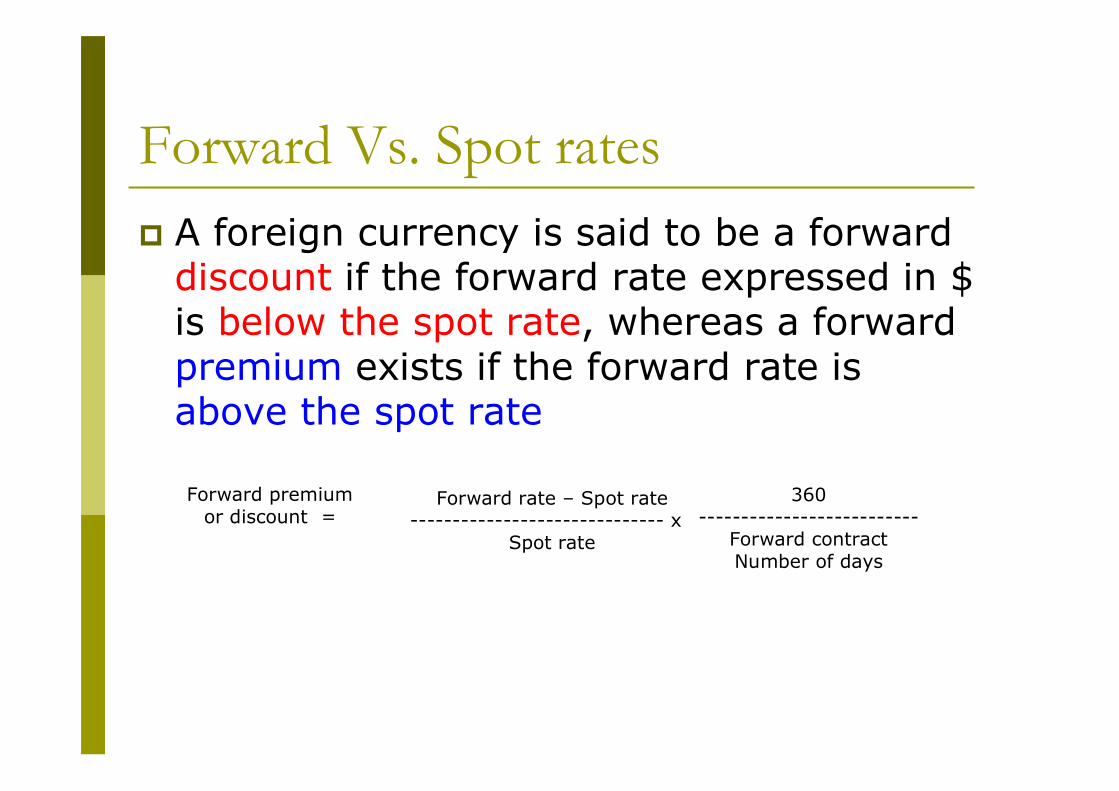

Forward Vs. Spot rates A foreign currency is said to be a forward discount if the forward rate expressed in $ is below the spot rate, whereas a forward premium exists if the forward rate is above the spot rate

Forward premium or discount =

Forward rate – Spot rate------------------------------ x

Spot rate

360--------------------------

Forward contractNumber of days

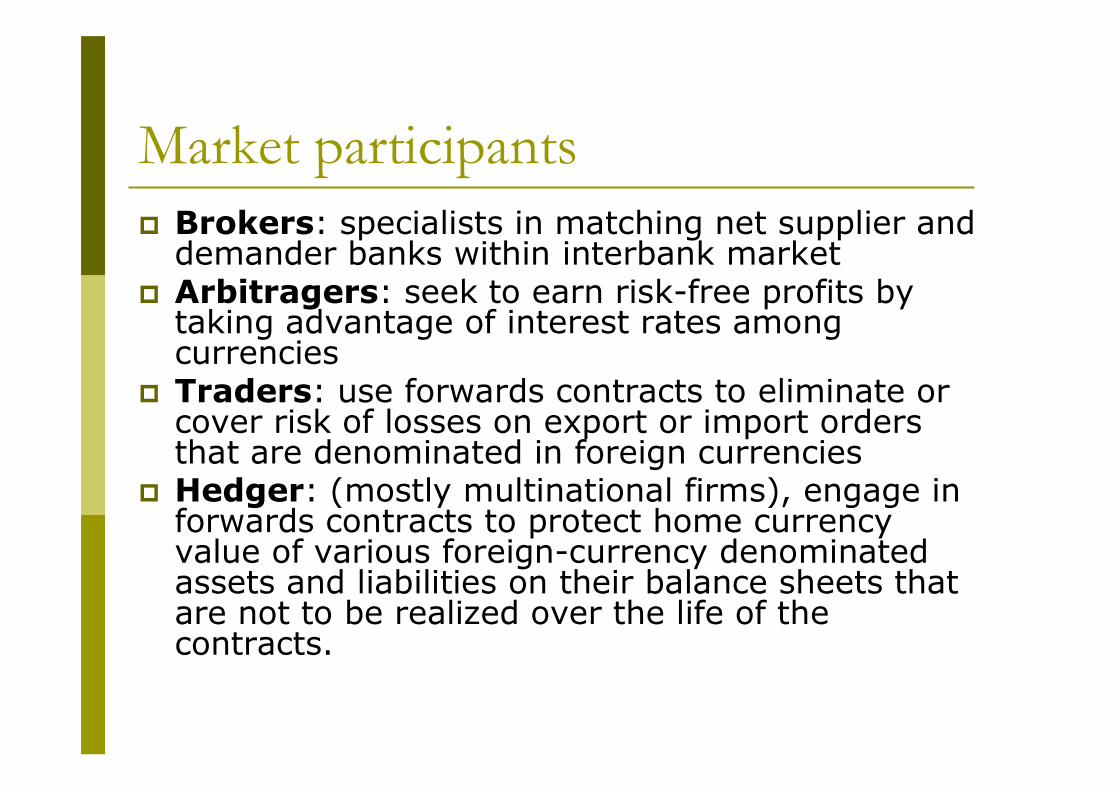

Market participantsBrokers: specialists in matching net supplier and demander banks within interbank marketArbitragers: seek to earn risk-free profits by taking advantage of interest rates among currencies Traders: use forwards contracts to eliminate or cover risk of losses on export or import orders that are denominated in foreign currenciesHedger: (mostly multinational firms), engage in forwards contracts to protect home currency value of various foreign-currency denominated assets and liabilities on their balance sheets that are not to be realized over the life of the contracts.

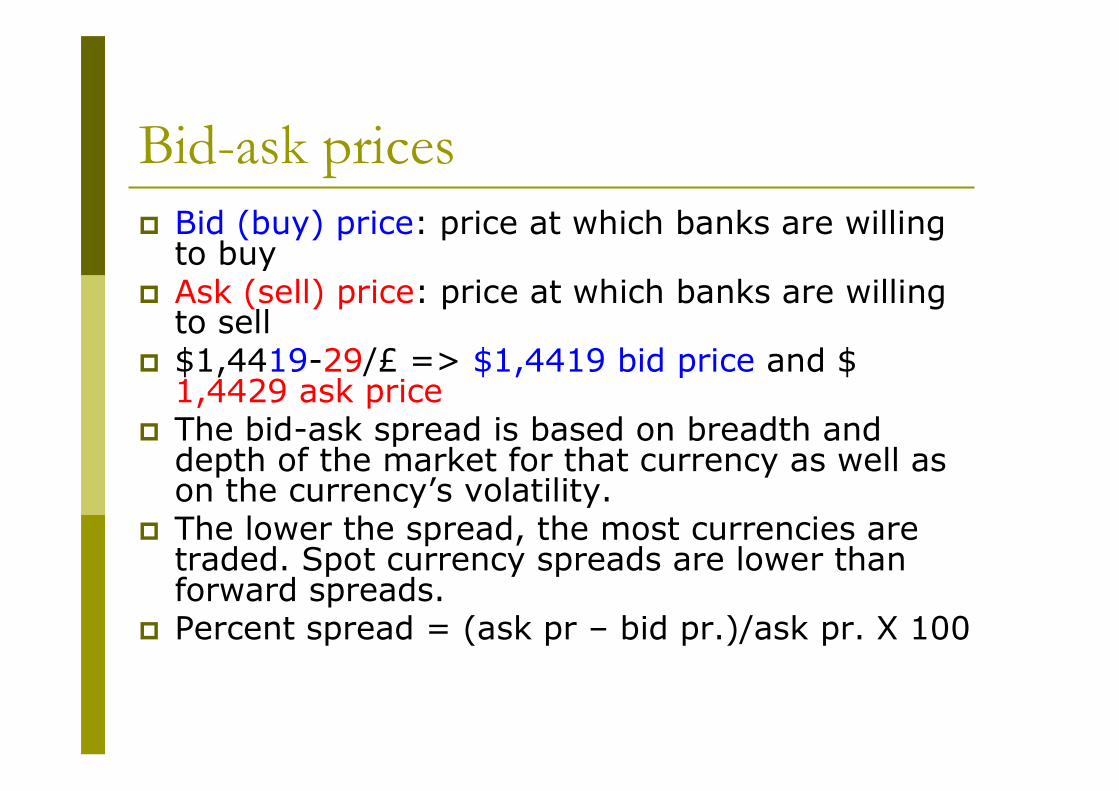

Bid-ask pricesBid (buy) price: price at which banks are willing to buyAsk (sell) price: price at which banks are willing to sell$1,4419-29/£ => $1,4419 bid price and $ 1,4429 ask priceThe bid-ask spread is based on breadth and depth of the market for that currency as well as on the currency’s volatility.The lower the spread, the most currencies are traded. Spot currency spreads are lower than forward spreads.Percent spread = (ask pr – bid pr.)/ask pr. X 100

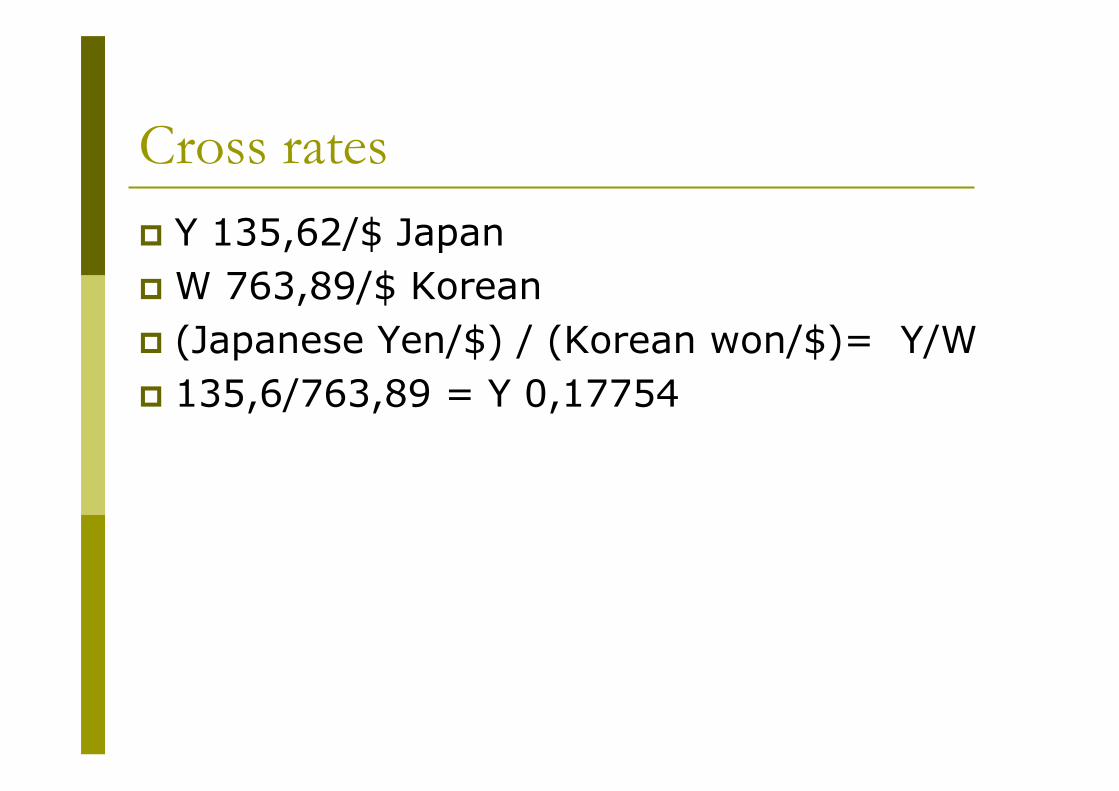

Cross ratesY 135,62/$ JapanW 763,89/$ Korean(Japanese Yen/$) / (Korean won/$)= Y/W135,6/763,89 = Y 0,17754

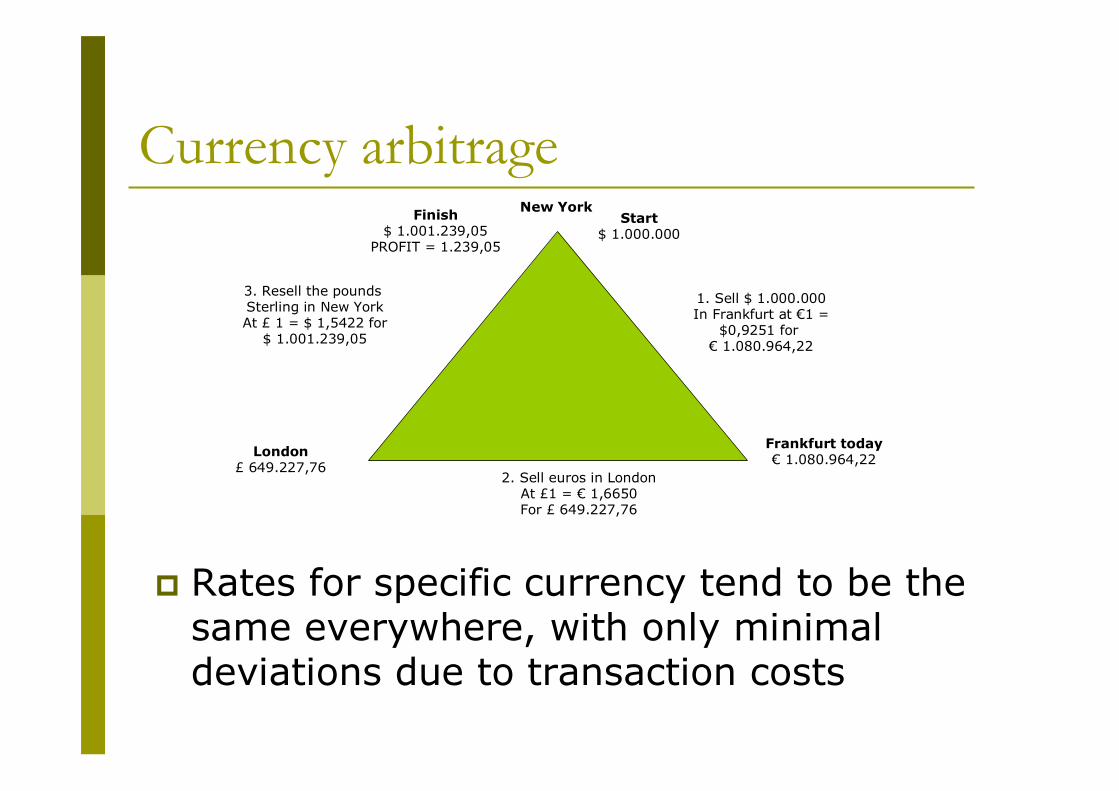

Currency arbitrage

1. Sell $ 1.000.000In Frankfurt at €1 =

$0,9251 for € 1.080.964,22

Frankfurt today€ 1.080.964,22London

£ 649.227,76

3. Resell the pounds Sterling in New YorkAt £ 1 = $ 1,5422 for

$ 1.001.239,05

Finish$ 1.001.239,05

PROFIT = 1.239,05

Start$ 1.000.000

New York

2. Sell euros in LondonAt £1 = € 1,6650For £ 649.227,76

Rates for specific currency tend to be the same everywhere, with only minimal deviations due to transaction costs

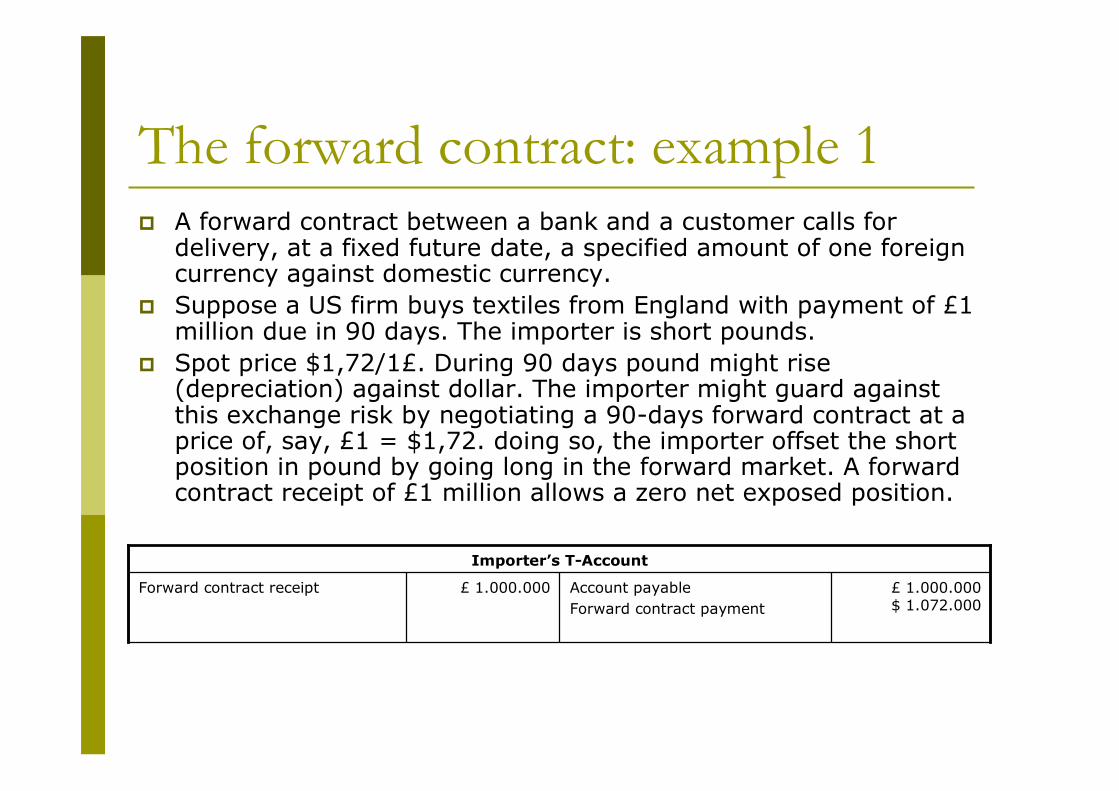

The forward contract: example 1A forward contract between a bank and a customer calls for delivery, at a fixed future date, a specified amount of one foreign currency against domestic currency.Suppose a US firm buys textiles from England with payment of £1 million due in 90 days. The importer is short pounds.Spot price $1,72/1£. During 90 days pound might rise (depreciation) against dollar. The importer might guard against this exchange risk by negotiating a 90-days forward contract at a price of, say, £1 = $1,72. doing so, the importer offset the short position in pound by going long in the forward market. A forwardcontract receipt of £1 million allows a zero net exposed position.

£ 1.000.000$ 1.072.000

Account payableForward contract payment

£ 1.000.000Forward contract receipt

Importer’s T-Account

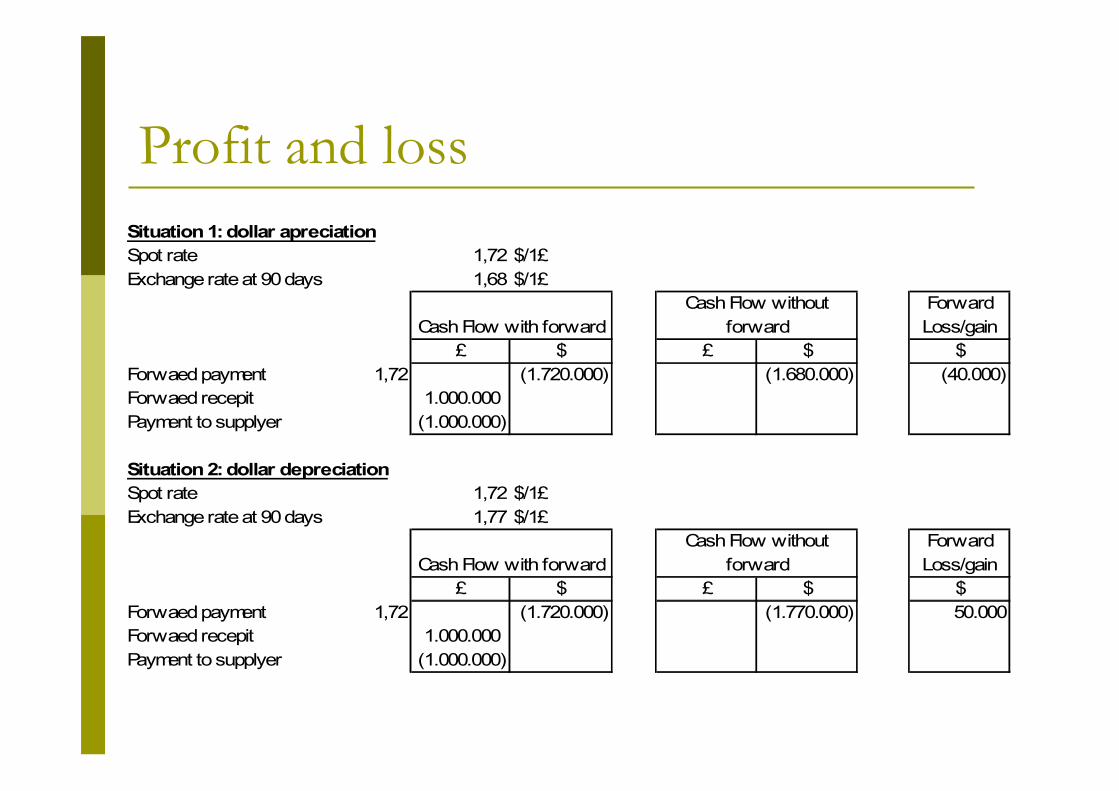

Profit and lossSituation 1: dollar apreciationSpot rate 1,72 $/1£Exchange rate at 90 days 1,68 $/1£

Forward Loss/gain

£ $ £ $ $Forwaed payment 1,72 (1.720.000) (1.680.000) (40.000)Forwaed recepit 1.000.000 Payment to supplyer (1.000.000)

Situation 2: dollar depreciationSpot rate 1,72 $/1£Exchange rate at 90 days 1,77 $/1£

Forward Loss/gain

£ $ £ $ $Forwaed payment 1,72 (1.720.000) (1.770.000) 50.000Forwaed recepit 1.000.000 Payment to supplyer (1.000.000)

Cash Flow with forwardCash Flow without

forward

Cash Flow with forwardCash Flow without

forward

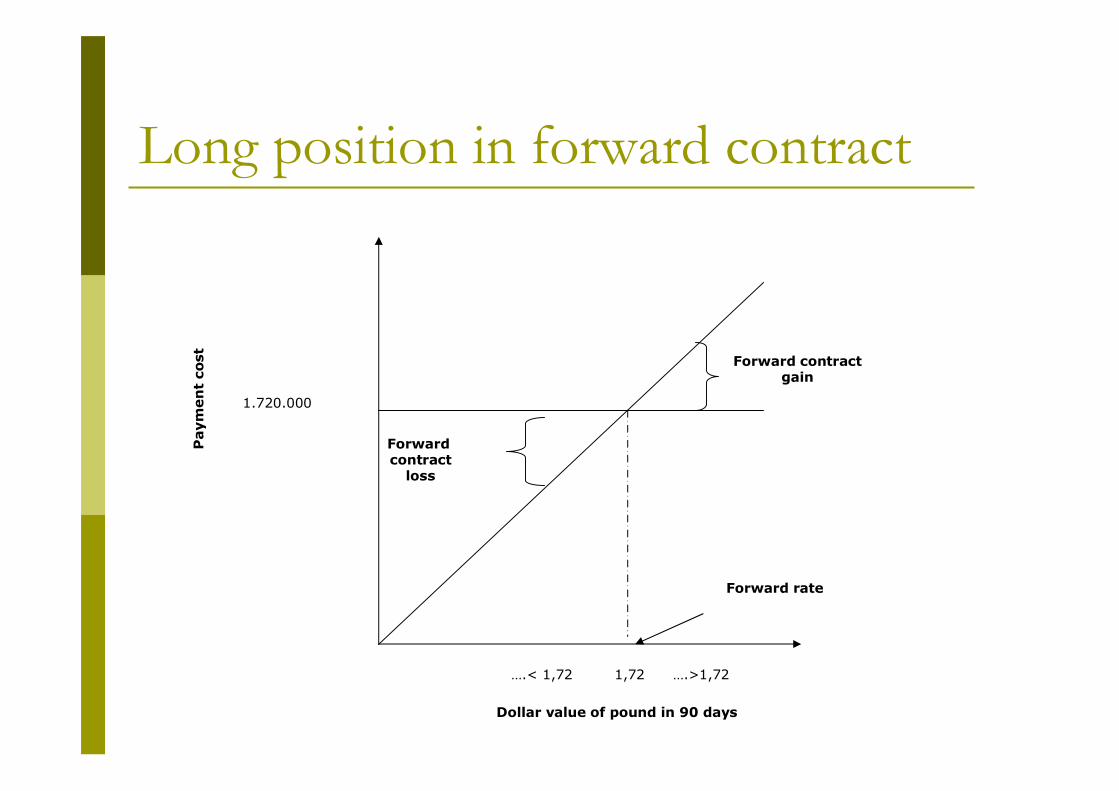

Long position in forward contract

Dollar value of pound in 90 days

….< 1,72 1,72 ….>1,72

1.720.000

Paym

en

t co

st

Forward rate

Forward contractgain

Forward contract

loss

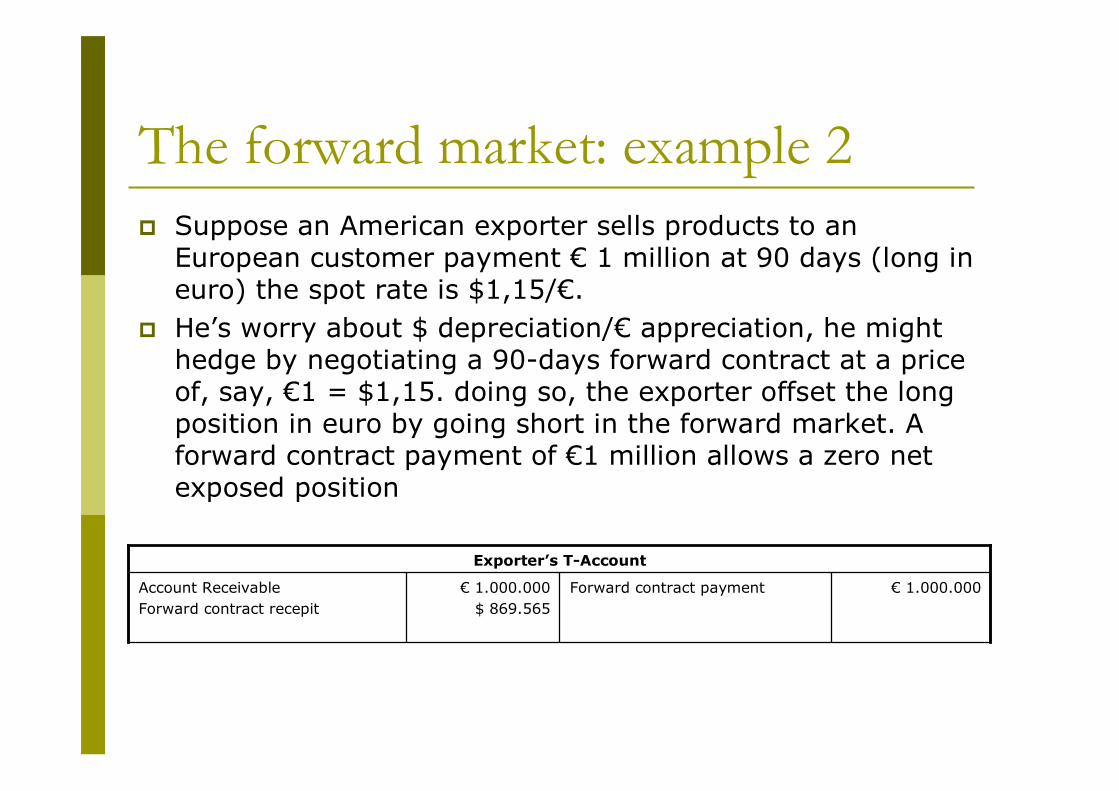

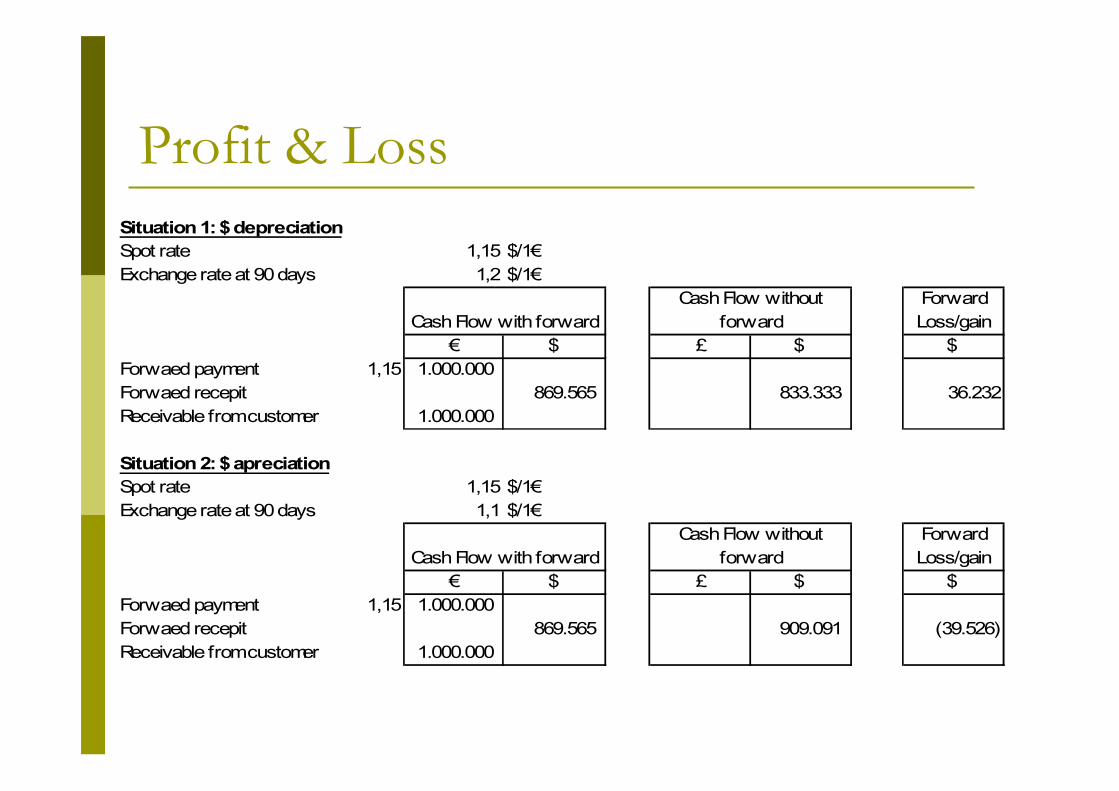

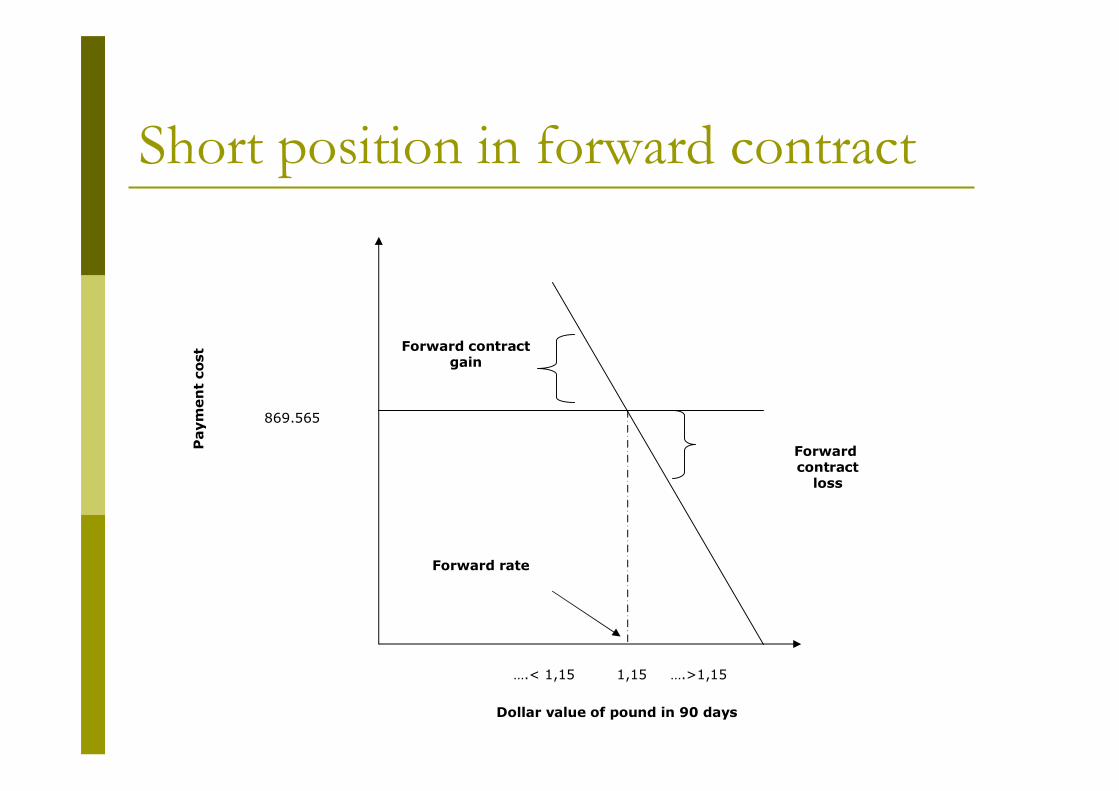

The forward market: example 2Suppose an American exporter sells products to an European customer payment € 1 million at 90 days (long in euro) the spot rate is $1,15/€. He’s worry about $ depreciation/€ appreciation, he might hedge by negotiating a 90-days forward contract at a price of, say, €1 = $1,15. doing so, the exporter offset the long position in euro by going short in the forward market. A forward contract payment of €1 million allows a zero net exposed position

€ 1.000.000Forward contract payment€ 1.000.000$ 869.565

Account Receivable Forward contract recepit

Exporter’s T-Account

Profit & LossSituation 1: $ depreciationSpot rate 1,15 $/1€Exchange rate at 90 days 1,2 $/1€

Forward Loss/gain

€ $ £ $ $ Forwaed payment 1,15 1.000.000 1.000.000 Forwaed recepit 869.565 833.333 36.232Receivable from customer 1.000.000 1.000.000

Situation 2: $ apreciationSpot rate 1,15 $/1€Exchange rate at 90 days 1,1 $/1€

Forward Loss/gain

€ $ £ $ $ Forwaed payment 1,15 1.000.000 1.000.000 Forwaed recepit 869.565 909.091 (39.526)Receivable from customer 1.000.000 1.000.000

Cash Flow with forwardCash Flow without

forward

Cash Flow with forwardCash Flow without

forward

Short position in forward contract

Dollar value of pound in 90 days

….< 1,15 1,15 ….>1,15

869.565

Paym

en

t co

st

Forward rate

Forward contractgain

Forward contract

loss

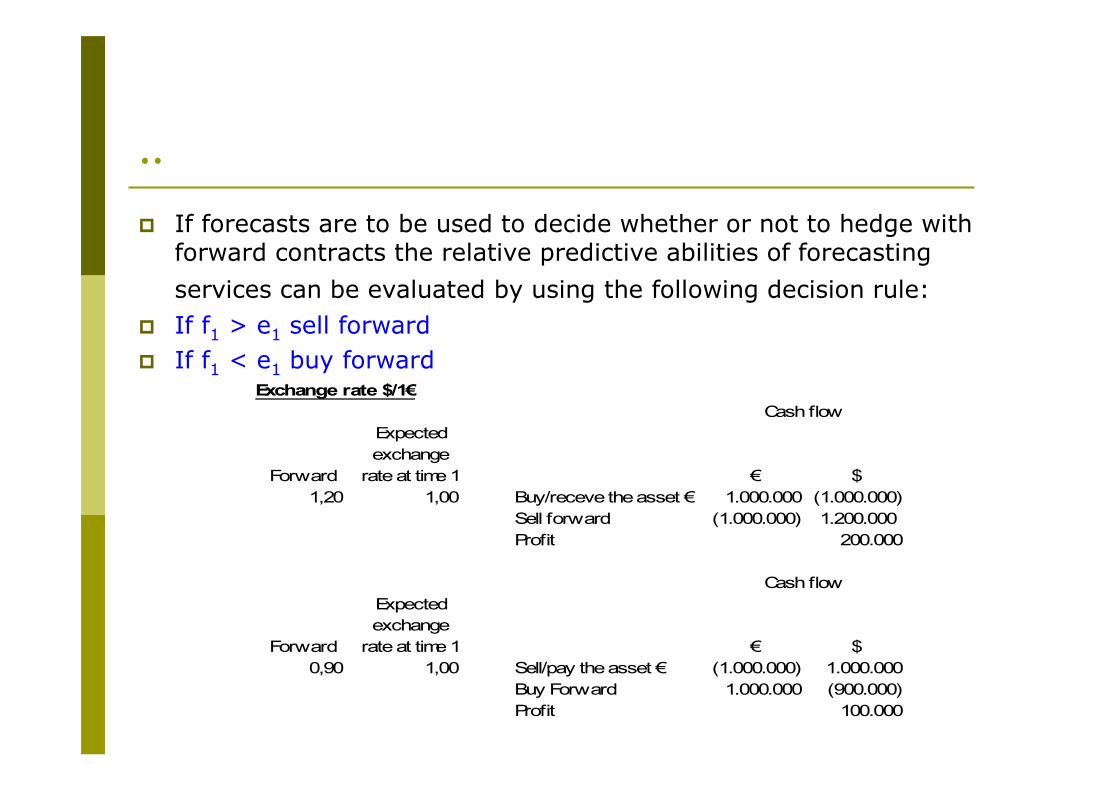

..If forecasts are to be used to decide whether or not to hedge with forward contracts the relative predictive abilities of forecasting services can be evaluated by using the following decision rule:If f1 > e1 sell forwardIf f1 < e1 buy forward

Exchange rate $/1€

Forward

Expected exchange

rate at time 1 € $1,20 1,00 Buy/receve the asset € 1.000.000 (1.000.000)

Sell forward (1.000.000) 1.200.000 Profit 200.000

Forward

Expected exchange

rate at time 1 € $0,90 1,00 Sell/pay the asset € (1.000.000) 1.000.000

Buy Forward 1.000.000 (900.000)Profit 100.000

Cash flow

Cash flow

Futures and option markets

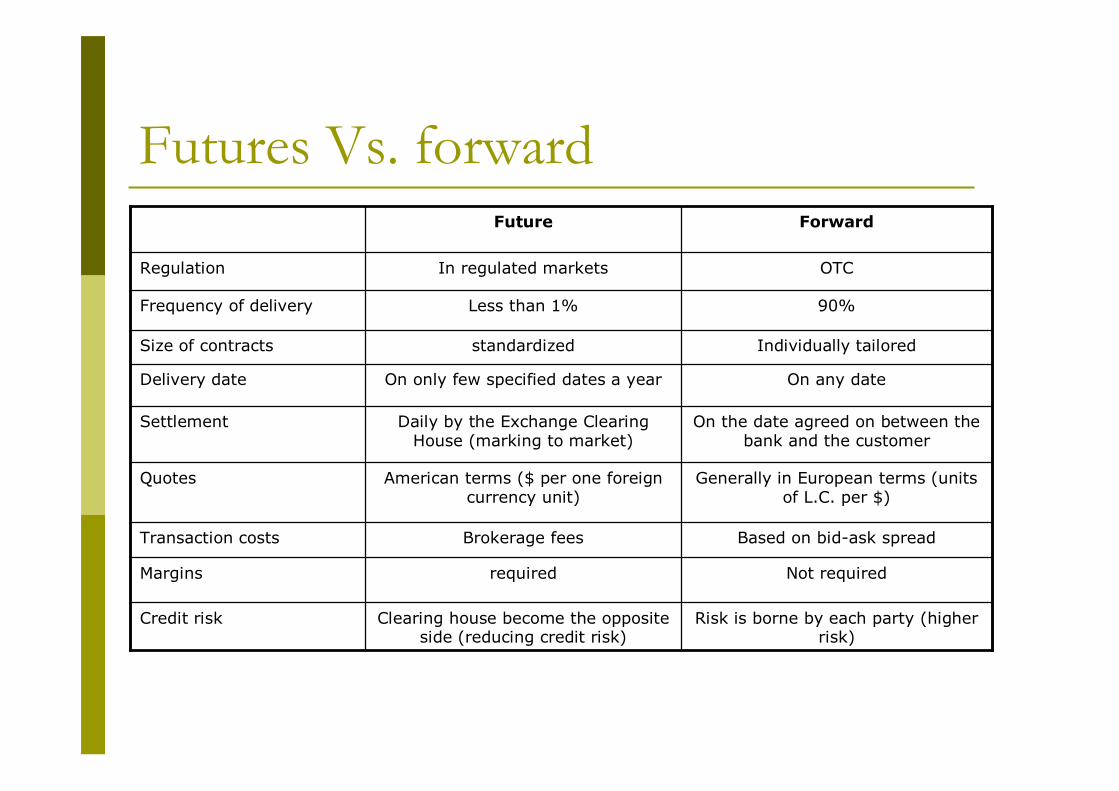

Futures Vs. forward

Risk is borne by each party (higher risk)

Clearing house become the opposite side (reducing credit risk)

Credit risk

Not requiredrequiredMargins

Based on bid-ask spreadBrokerage feesTransaction costs

On the date agreed on between the bank and the customer

Daily by the Exchange Clearing House (marking to market)

Settlement

On any dateOn only few specified dates a yearDelivery date

Individually tailored standardizedSize of contracts

Generally in European terms (units of L.C. per $)

American terms ($ per one foreign currency unit)

Quotes

90%Less than 1%Frequency of delivery

OTCIn regulated marketsRegulation

ForwardFuture

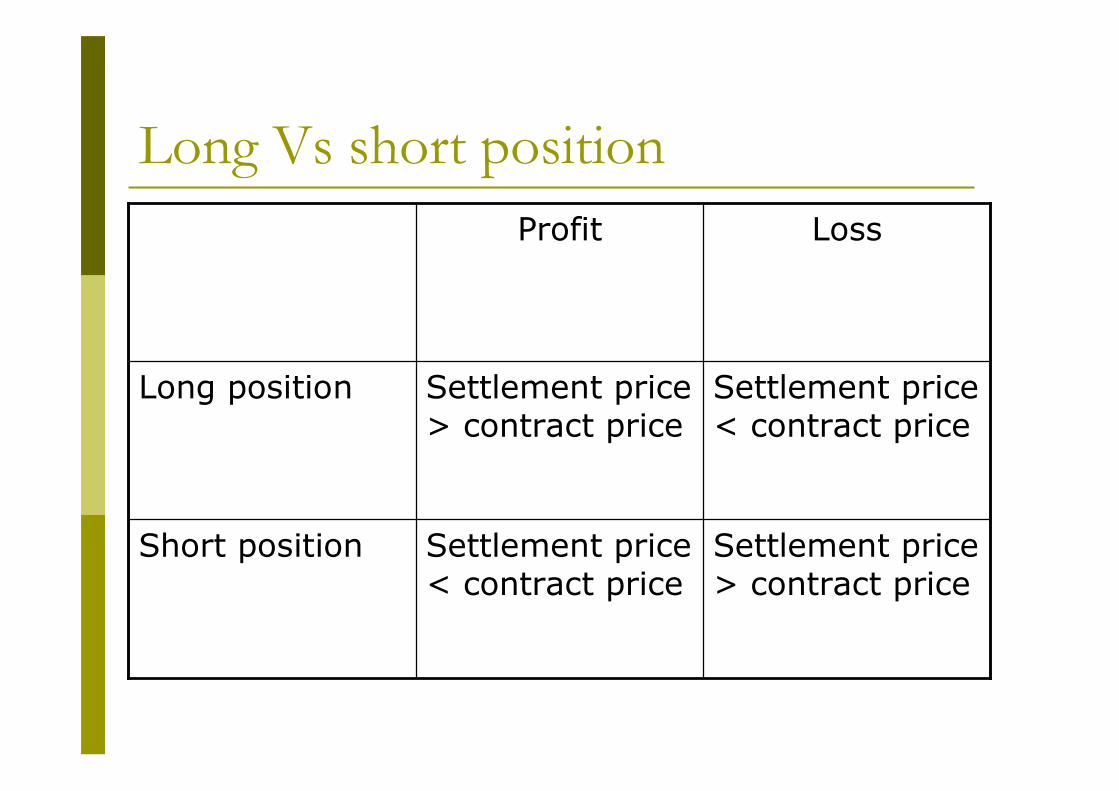

Long Vs short position

Settlement price > contract price

Settlement price < contract price

Short position

Settlement price < contract price

Settlement price > contract price

Long position

LossProfit

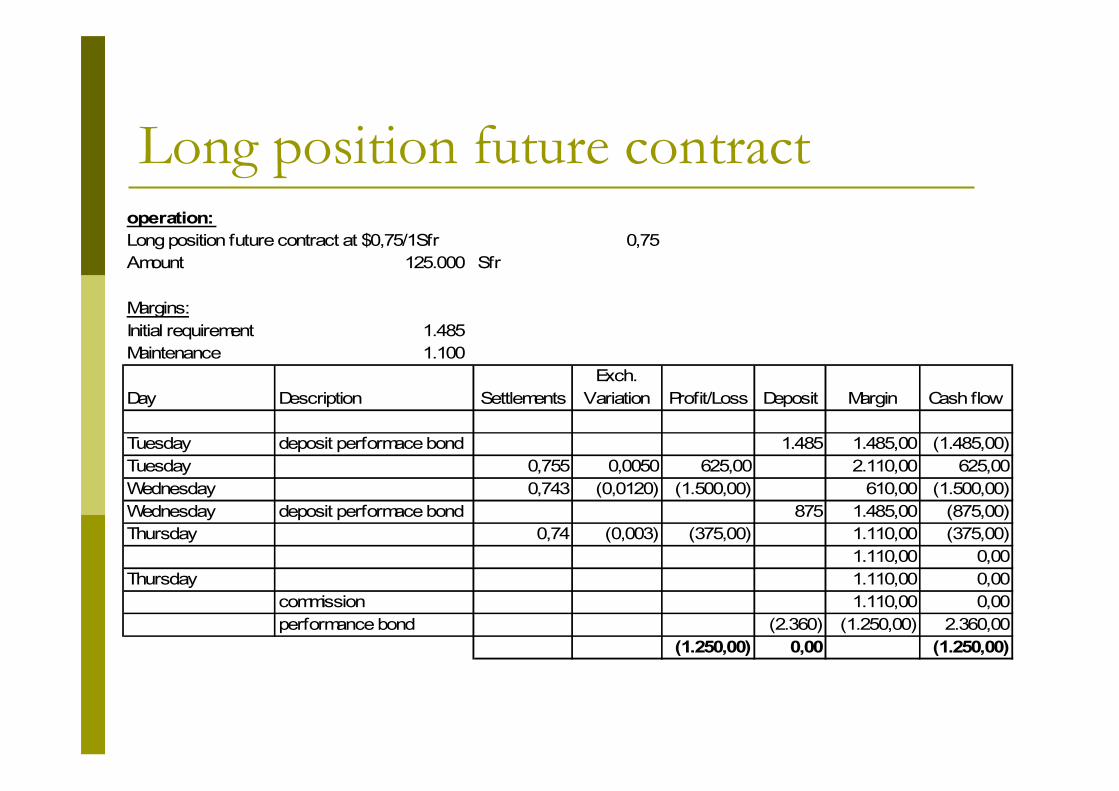

Long position future contractoperation: Long position future contract at $0,75/1Sfr 0,75Amount 125.000 Sfr

Margins:Initial requirement 1.485 Maintenance 1.100

Day Description SettlementsExch.

Variation Profit/Loss Deposit Margin Cash flow

Tuesday deposit performace bond 1.485 1.485,00 (1.485,00)Tuesday 0,755 0,0050 625,00 2.110,00 625,00Wednesday 0,743 (0,0120) (1.500,00) 610,00 (1.500,00)Wednesday deposit performace bond 875 1.485,00 (875,00)Thursday 0,74 (0,003) (375,00) 1.110,00 (375,00)

1.110,00 0,00Thursday 1.110,00 0,00

commission 1.110,00 0,00performance bond (2.360) (1.250,00) 2.360,00

(1.250,00) 0,00 (1.250,00)

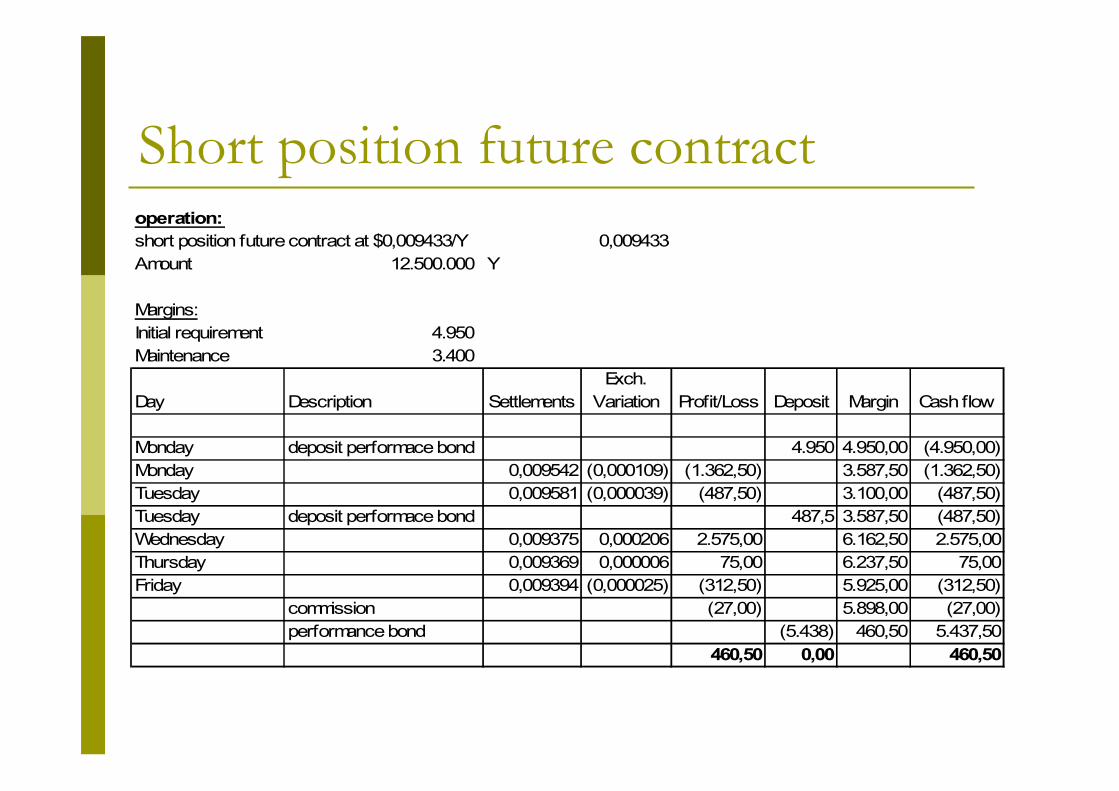

Short position future contractoperation: short position future contract at $0,009433/Y 0,009433Amount 12.500.000 Y

Margins:Initial requirement 4.950 Maintenance 3.400

Day Description SettlementsExch.

Variation Profit/Loss Deposit Margin Cash flow

Monday deposit performace bond 4.950 4.950,00 (4.950,00)Monday 0,009542 (0,000109) (1.362,50) 3.587,50 (1.362,50)Tuesday 0,009581 (0,000039) (487,50) 3.100,00 (487,50)Tuesday deposit performace bond 487,5 3.587,50 (487,50)Wednesday 0,009375 0,000206 2.575,00 6.162,50 2.575,00Thursday 0,009369 0,000006 75,00 6.237,50 75,00Friday 0,009394 (0,000025) (312,50) 5.925,00 (312,50)

commission (27,00) 5.898,00 (27,00)performance bond (5.438) 460,50 5.437,50

460,50 0,00 460,50

Call/Put Option

A call (put) option is the right to buy (sell) the underlying asset at a given exercise (strike) price during an agreed upon period of time

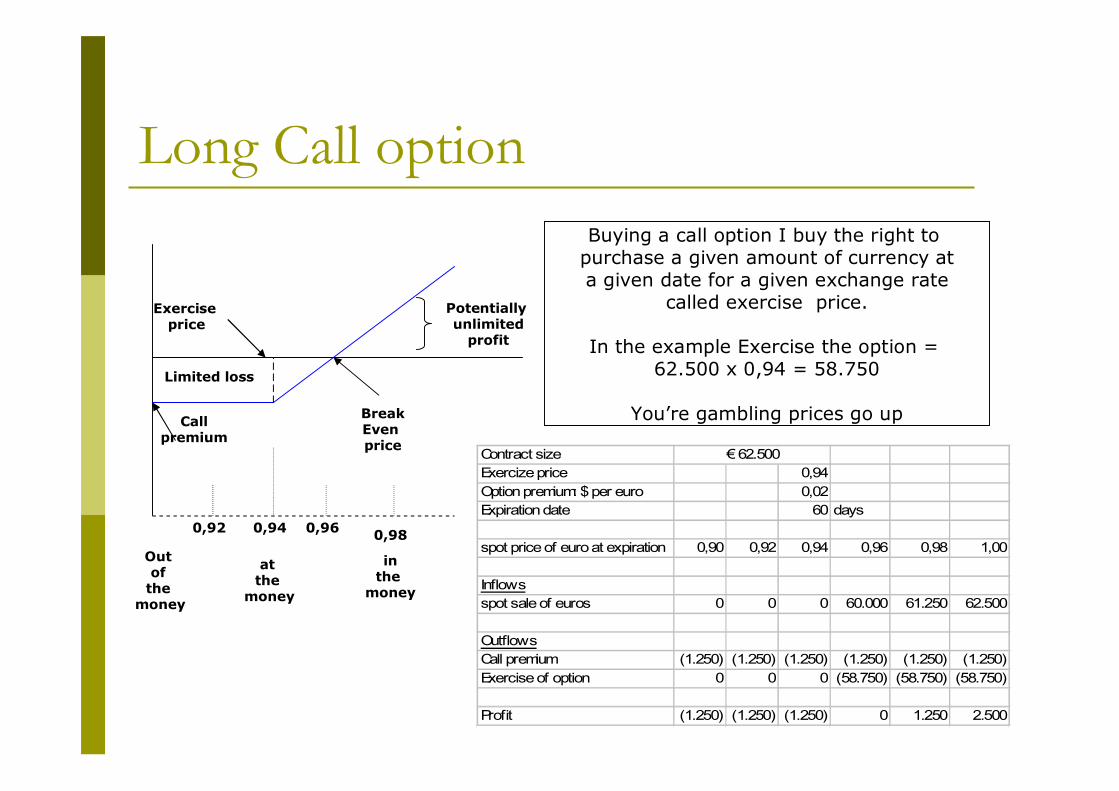

Long Call option

Potentially unlimited

profit

Limited loss

BreakEven price

Exercise price

Callpremium

0,92 0,94 0,96 0,98

Out of

the money

at the

money

inthe

money

Buying a call option I buy the right to purchase a given amount of currency at a given date for a given exchange rate

called exercise price.

In the example Exercise the option = 62.500 x 0,94 = 58.750

You’re gambling prices go up

Contract sizeExercize price 0,94Option premium: $ per euro 0,02Expiration date 60 days

spot price of euro at expiration 0,90 0,92 0,94 0,96 0,98 1,00

Inflowsspot sale of euros 0 0 0 60.000 61.250 62.500

OutflowsCall premium (1.250) (1.250) (1.250) (1.250) (1.250) (1.250)Exercise of option 0 0 0 (58.750) (58.750) (58.750)

Profit (1.250) (1.250) (1.250) 0 1.250 2.500

€ 62.500

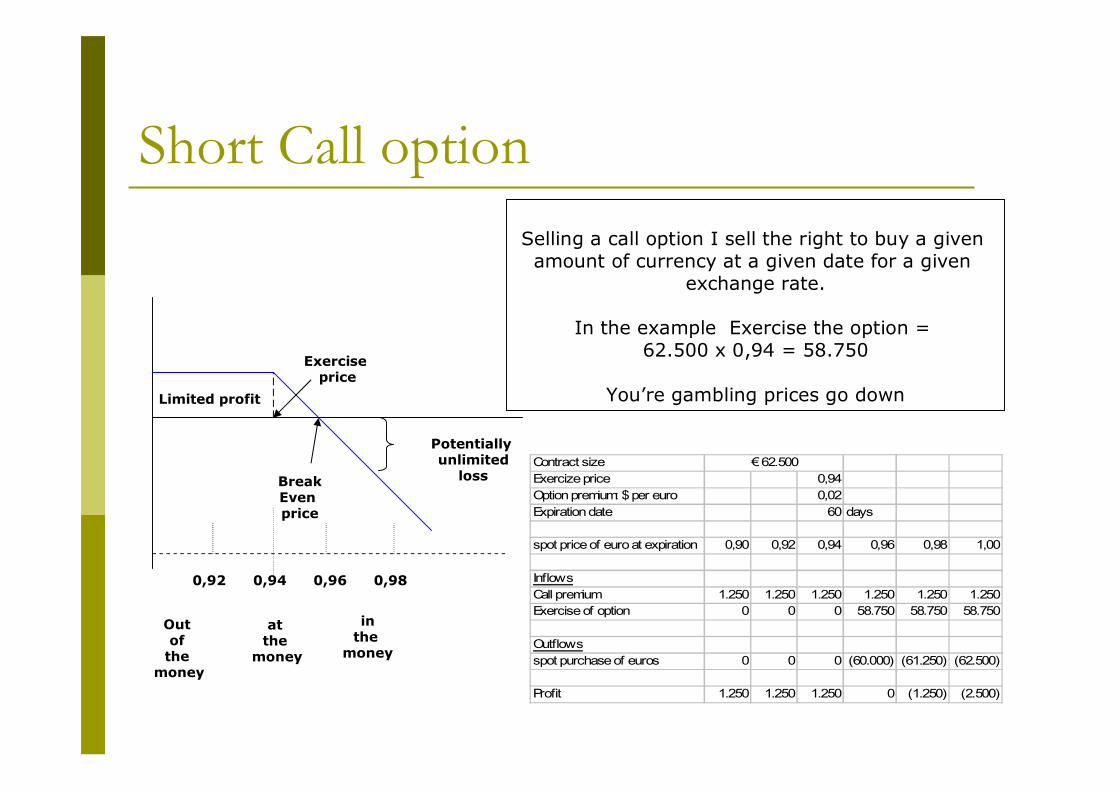

Short Call option

Potentially unlimited

loss

Limited profit

BreakEven price

Exercise price

0,92 0,94 0,96 0,98

Out of

the money

at the

money

inthe

money

Selling a call option I sell the right to buy a given amount of currency at a given date for a given

exchange rate.

In the example Exercise the option = 62.500 x 0,94 = 58.750

You’re gambling prices go down

Contract sizeExercize price 0,94Option premium: $ per euro 0,02Expiration date 60 days

spot price of euro at expiration 0,90 0,92 0,94 0,96 0,98 1,00

InflowsCall premium 1.250 1.250 1.250 1.250 1.250 1.250Exercise of option 0 0 0 58.750 58.750 58.750

Outflowsspot purchase of euros 0 0 0 (60.000) (61.250) (62.500)

Profit 1.250 1.250 1.250 0 (1.250) (2.500)

€ 62.500

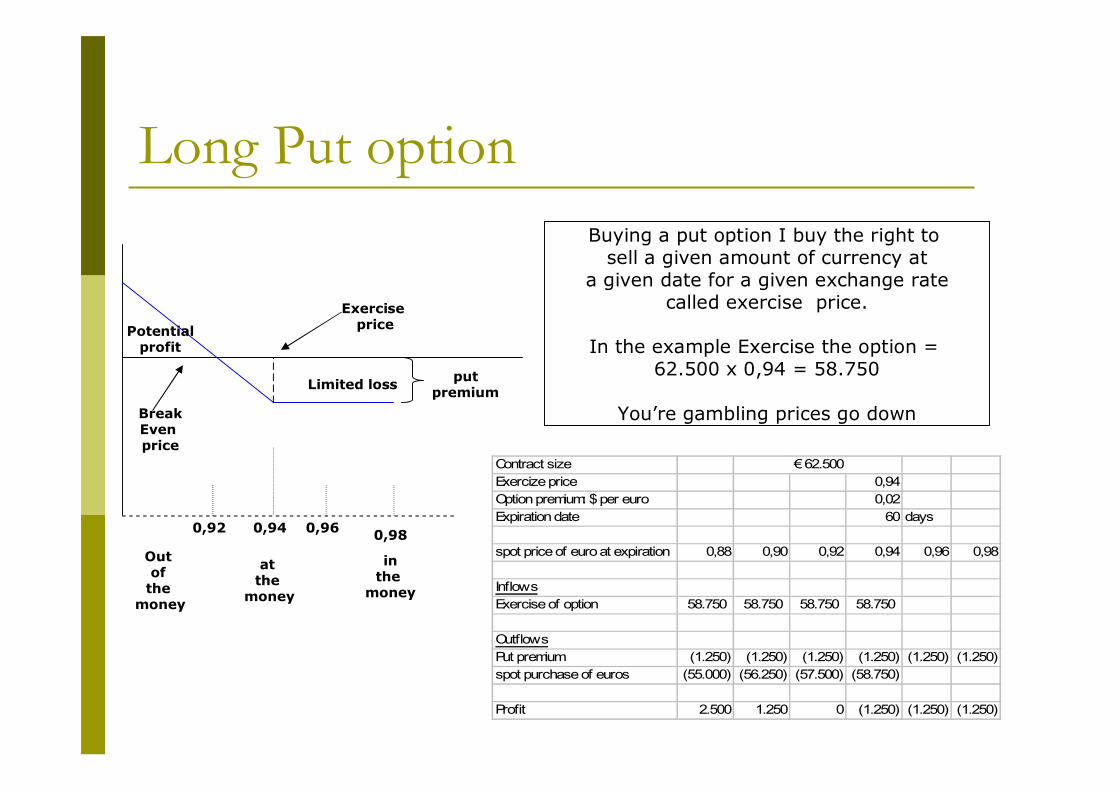

Long Put option

Potentialprofit

Limited loss

BreakEven price

Exercise price

0,92 0,94 0,96 0,98

Out of

the money

at the

money

inthe

money

Buying a put option I buy the right to sell a given amount of currency at

a given date for a given exchange ratecalled exercise price.

In the example Exercise the option = 62.500 x 0,94 = 58.750

You’re gambling prices go down

Contract sizeExercize price 0,94Option premium: $ per euro 0,02Expiration date 60 days

spot price of euro at expiration 0,88 0,90 0,92 0,94 0,96 0,98

InflowsExercise of option 58.750 58.750 58.750 58.750

OutflowsPut premium (1.250) (1.250) (1.250) (1.250) (1.250) (1.250)spot purchase of euros (55.000) (56.250) (57.500) (58.750)

Profit 2.500 1.250 0 (1.250) (1.250) (1.250)

€ 62.500

putpremium

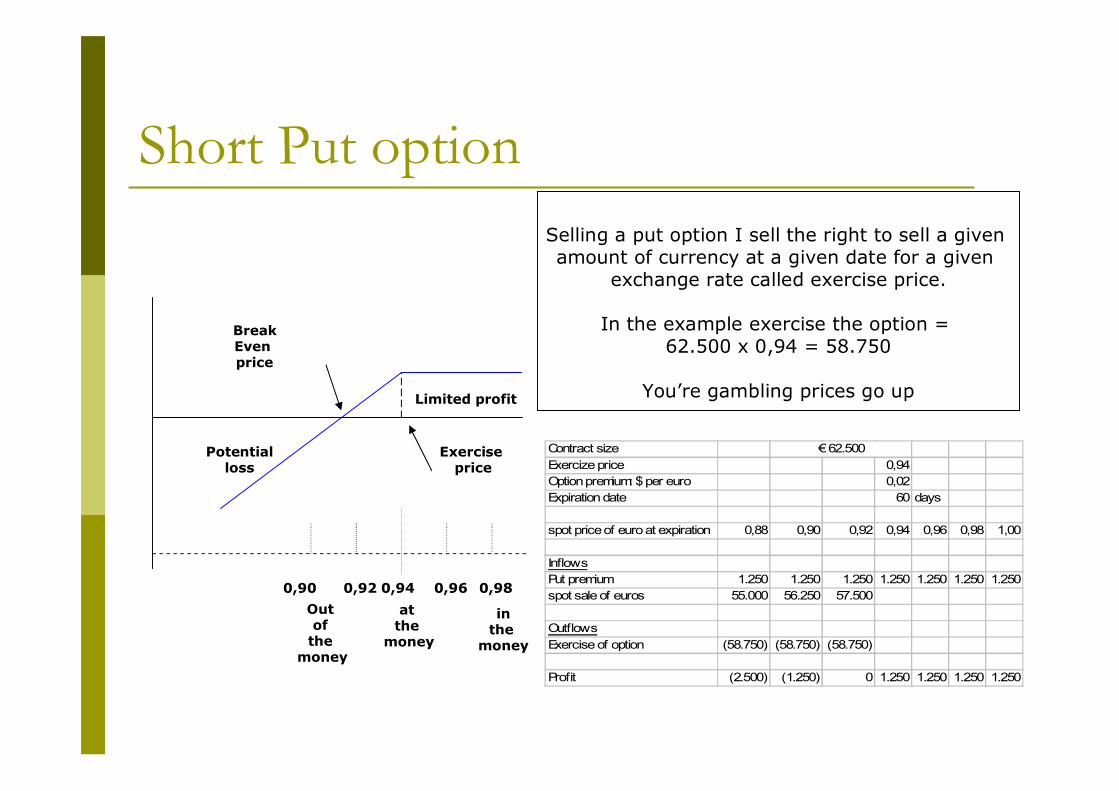

Short Put option

Potentialloss

Limited profit

BreakEven price

Exercise price

0,92 0,94 0,980,96

Out of

the money

at the

money

inthe

money

Selling a put option I sell the right to sell a given amount of currency at a given date for a given

exchange rate called exercise price.

In the example exercise the option = 62.500 x 0,94 = 58.750

You’re gambling prices go up

0,90

Contract sizeExercize price 0,94Option premium: $ per euro 0,02Expiration date 60 days

spot price of euro at expiration 0,88 0,90 0,92 0,94 0,96 0,98 1,00

InflowsPut premium 1.250 1.250 1.250 1.250 1.250 1.250 1.250spot sale of euros 55.000 56.250 57.500

OutflowsExercise of option (58.750) (58.750) (58.750)

Profit (2.500) (1.250) 0 1.250 1.250 1.250 1.250

€ 62.500

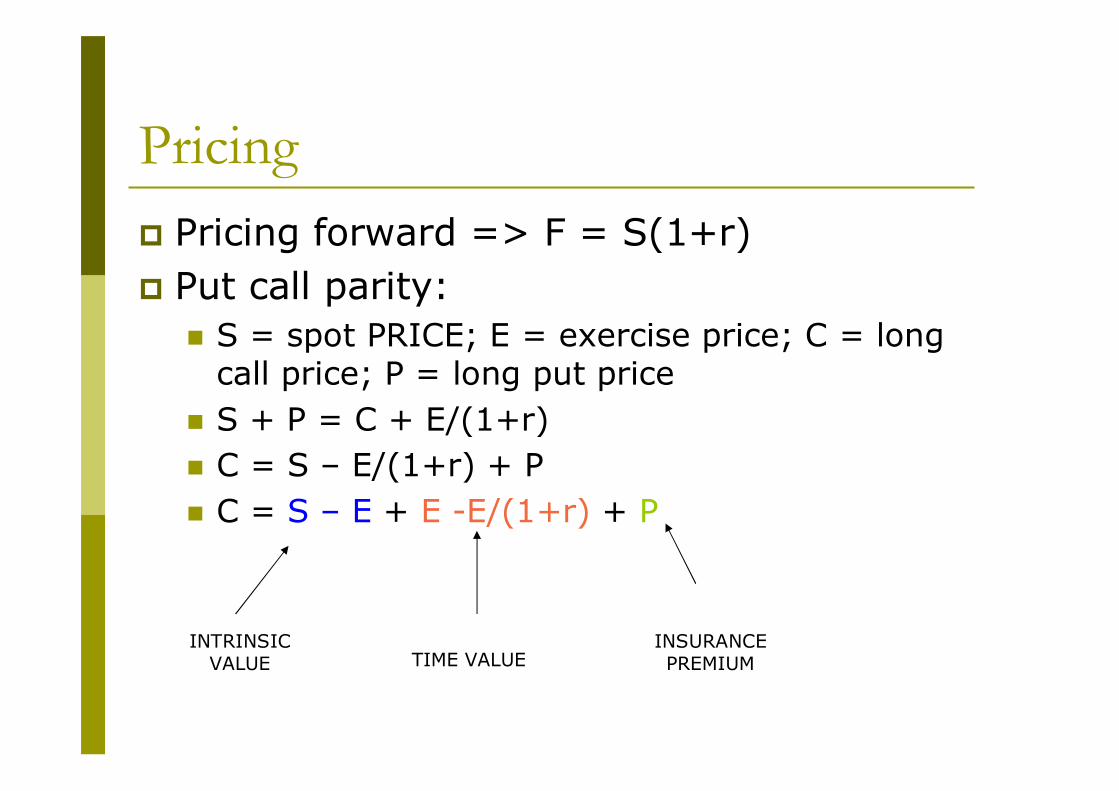

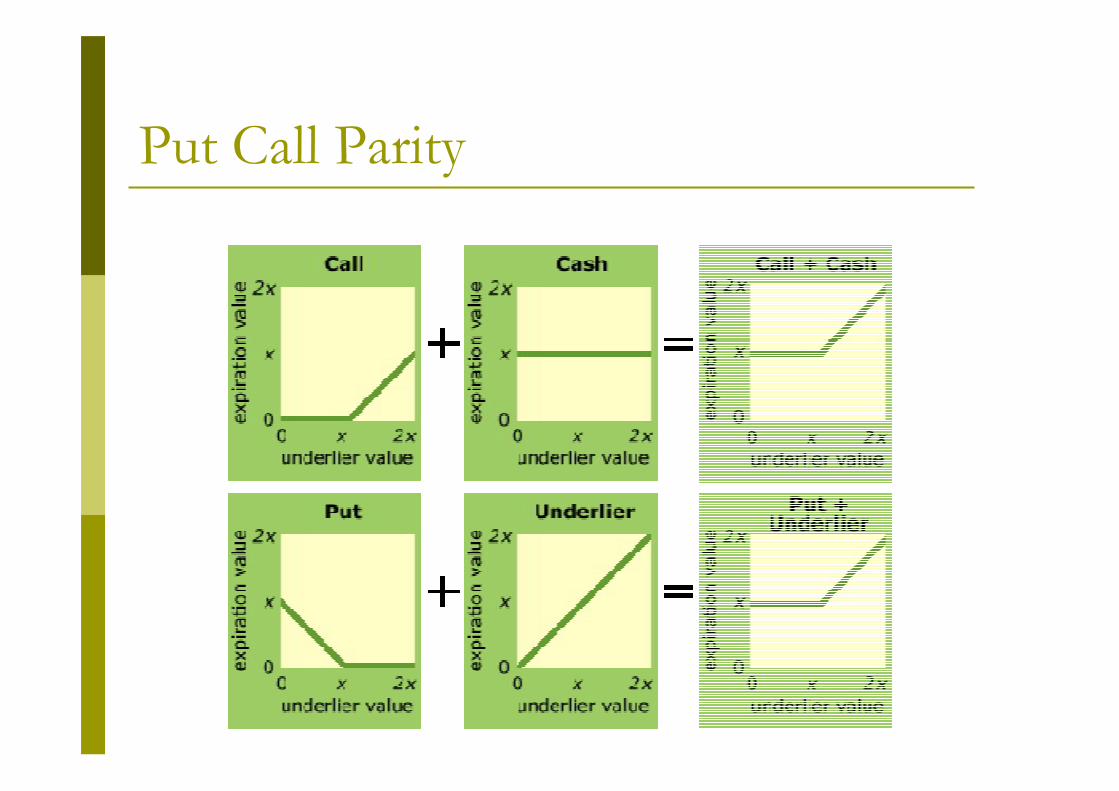

Pricing Pricing forward => F = S(1+r)Put call parity:

S = spot PRICE; E = exercise price; C = long call price; P = long put price S + P = C + E/(1+r)C = S – E/(1+r) + PC = S – E + E -E/(1+r) + P

INTRINSIC VALUE TIME VALUE

INSURANCEPREMIUM

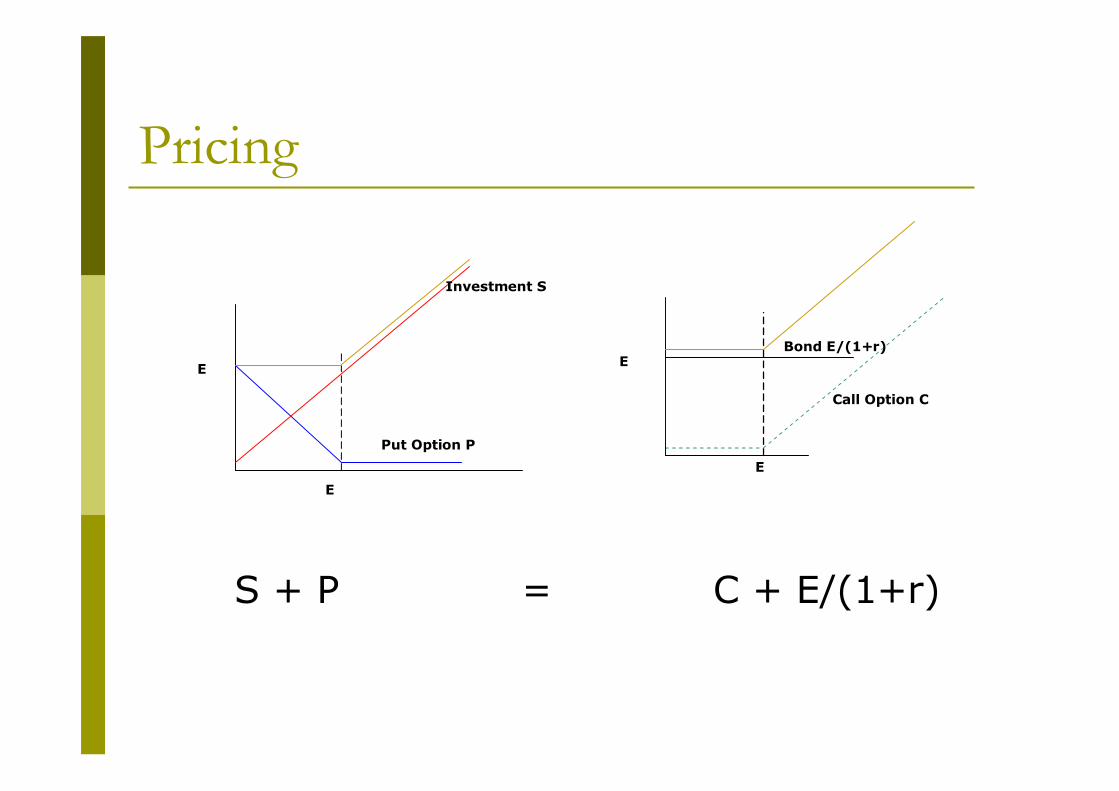

Pricing

Call Option C

Investment S

E

E

Put Option P

E

EBond E/(1+r)

S + P = C + E/(1+r)

Put Call Parity

AgendaBalance of paymentParity conditions in International FinanceThe foreign exchange marketFutures and option marketsSwaps and interest derivatives

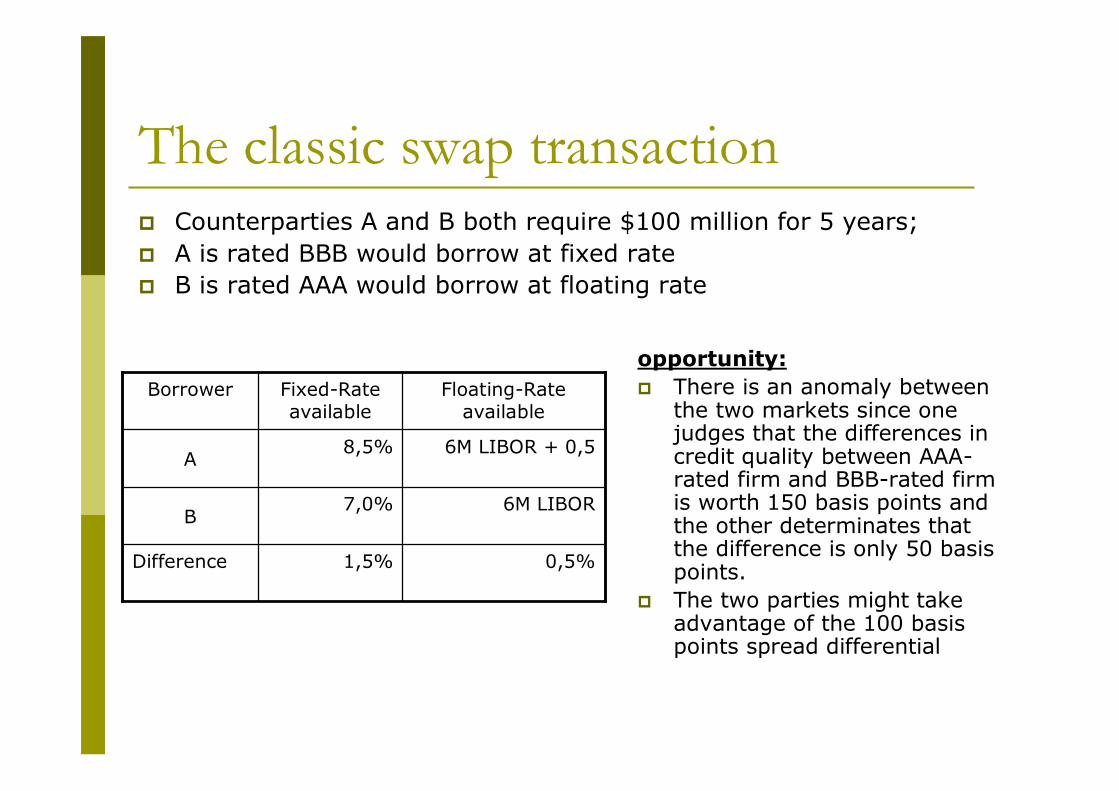

The classic swap transactionCounterparties A and B both require $100 million for 5 years; A is rated BBB would borrow at fixed rateB is rated AAA would borrow at floating rate

0,5%1,5%Difference

6M LIBOR7,0%B

6M LIBOR + 0,58,5%A

Floating-Rate available

Fixed-Rate available

Borroweropportunity:

There is an anomaly between the two markets since one judges that the differences in credit quality between AAA-rated firm and BBB-rated firm is worth 150 basis points and the other determinates that the difference is only 50 basis points. The two parties might take advantage of the 100 basis points spread differential

Interest rate swapsIt is an agreement between two parties to exchange interest payments for a specific maturity on an agreed upon notional amountNotional => theoretical principal underlying the swap; it is a reference amount against which the interest is calculated.In a coupon swap one party pays a fixed rate calculated at the time of trade as a spread to a particular treasury bond, and another side pays a floating rate that resets periodically through the life of the deal against a designed indexIn a basis swap, two parties exchange floating interests payments based on different references rates.

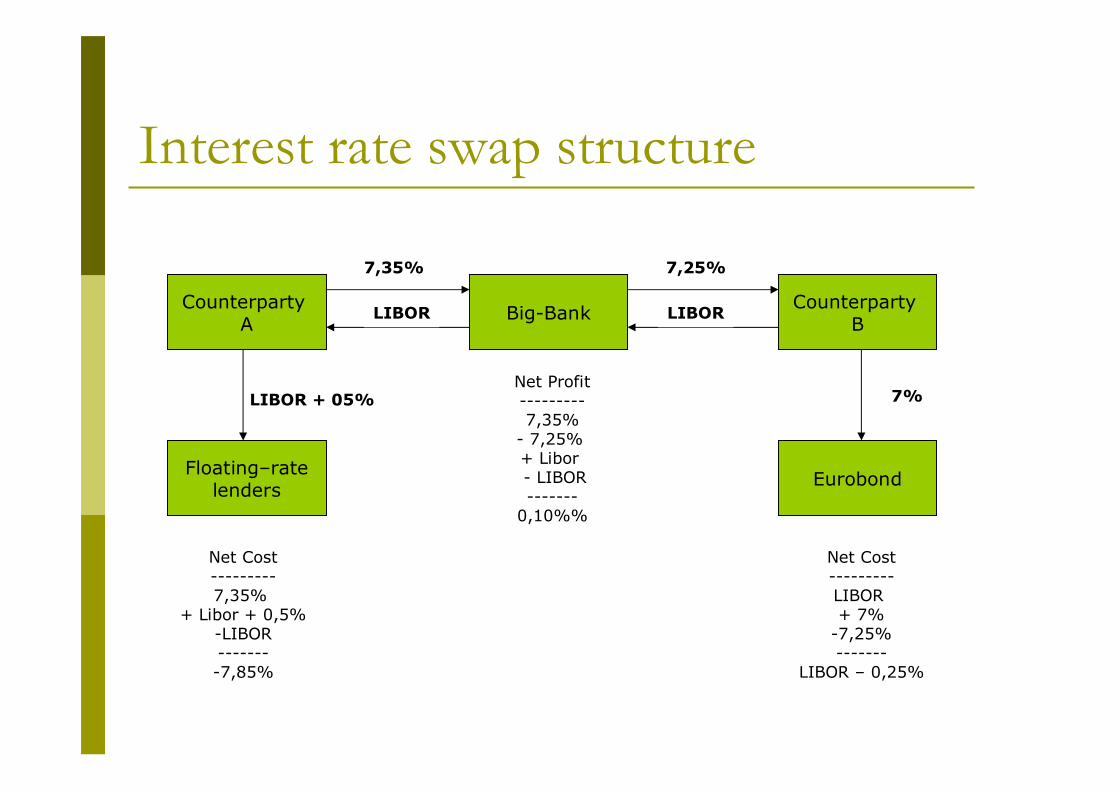

Interest rate swap structure

Counterparty A

Floating–ratelenders

Big-Bank Counterparty B

Eurobond

7,35% 7,25%

LIBOR LIBOR

LIBOR + 05% 7%

Net Cost---------LIBOR + 7%

-7,25%-------

LIBOR – 0,25%

Net Cost---------7,35%

+ Libor + 0,5%-LIBOR--------7,85%

Net Profit---------7,35%

- 7,25% + Libor - LIBOR-------

0,10%%

Currency swapsIt is an exchange of debt-service obligations denominated in one currency for the service on an agreed upon principal amount of debt denominated in another currency By swapping their future cash-flows obligations, the counterparties are able to replace cash flows denominated in one currency with cash flows in a more desired currency

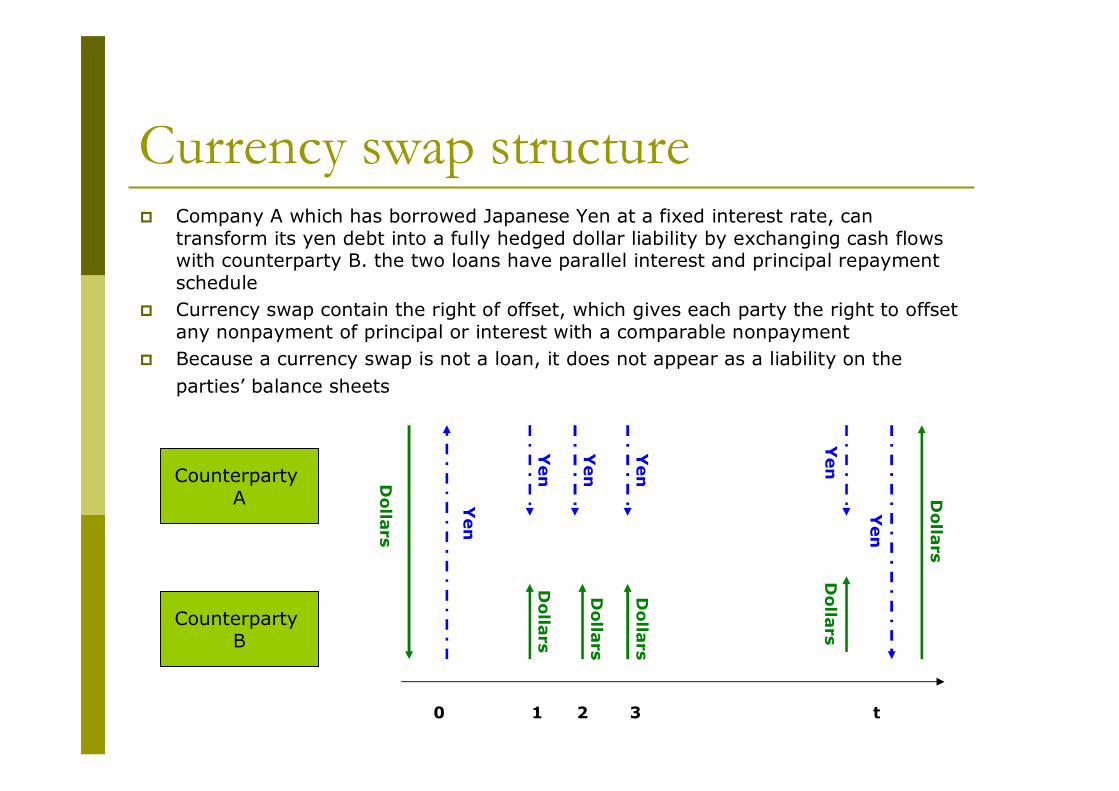

Currency swap structureCompany A which has borrowed Japanese Yen at a fixed interest rate, can transform its yen debt into a fully hedged dollar liability by exchanging cash flows with counterparty B. the two loans have parallel interest and principal repayment scheduleCurrency swap contain the right of offset, which gives each party the right to offset any nonpayment of principal or interest with a comparable nonpayment Because a currency swap is not a loan, it does not appear as a liability on the parties’ balance sheets

Counterparty A

Counterparty B

Dolla

rs

Yen

0 1 2 3 t

Dolla

rs

Dolla

rs

Dolla

rs

Yen

Yen

Yen

Yen

Yen

Dolla

rs

Dolla

rs

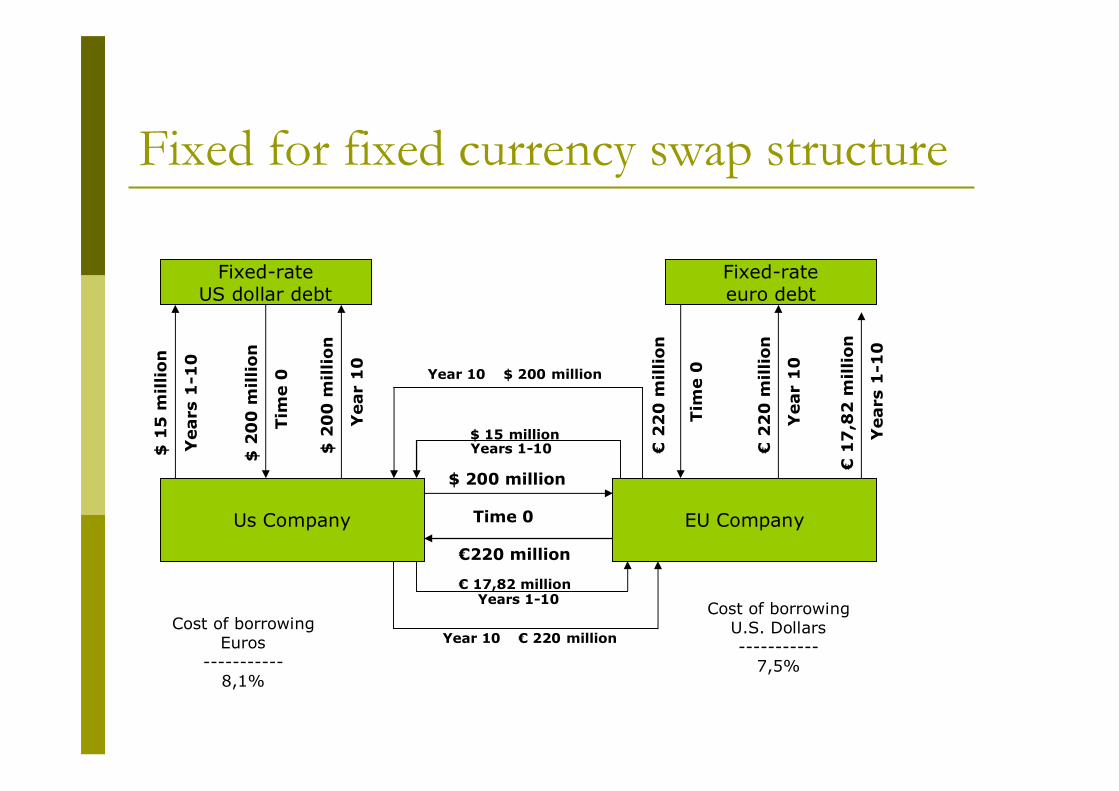

Fixed for fixed €/$ currency swapUS company is looking to hedge some of its euro exposure by borrowing in euros. At the same time EU company is seeking $ to finance additional investment in the US market.Both want the equivalent of $200 million in fixed-rate financing for 10 years (€1,1/$ = €220). US company can issue $-denominated debt at a coupon rat of 7,5% or €-denominated rate of 8,25%.Equivalent rates for the EU company are 7,7% and 8,1% respectively

Fixed for fixed currency swap structure

Us Company

Fixed-rateUS dollar debt

$ 1

5 m

illion

Years

1-1

0

$ 2

00

million

Tim

e 0

$ 2

00

million

Year

10

EU Company

Fixed-rateeuro debt

€2

20

million

Tim

e 0

Year

10

Years

1-1

0

€2

20

million

€1

7,8

2 m

illion

Time 0

$ 200 million

€220 million

$ 15 millionYears 1-10

Year 10 $ 200 million

Years 1-10€ 17,82 million

Year 10 € 220 millionCost of borrowing

Euros-----------

8,1%

Cost of borrowingU.S. Dollars-----------

7,5%

Dual currency bond swapIt is the case when one has the issue’s proceeds and interest payments stated in foreign currency and the principal repayment stated in domestic currency. Example: FNMA issued on October 1, 1985 10-year 8% coupon debentures in the amount o Yen 50 billion (Y237.5479/$1). In return Fannie Mae agreed to pay interest averaging about $21 million annually and to redeem these bonds at the end of 10 years at a cost of $240,4 millionThe net effect for FNMA was an all-in dollar cost of 10,67% annually regardless of what happened to the yen/dollar exchange rate

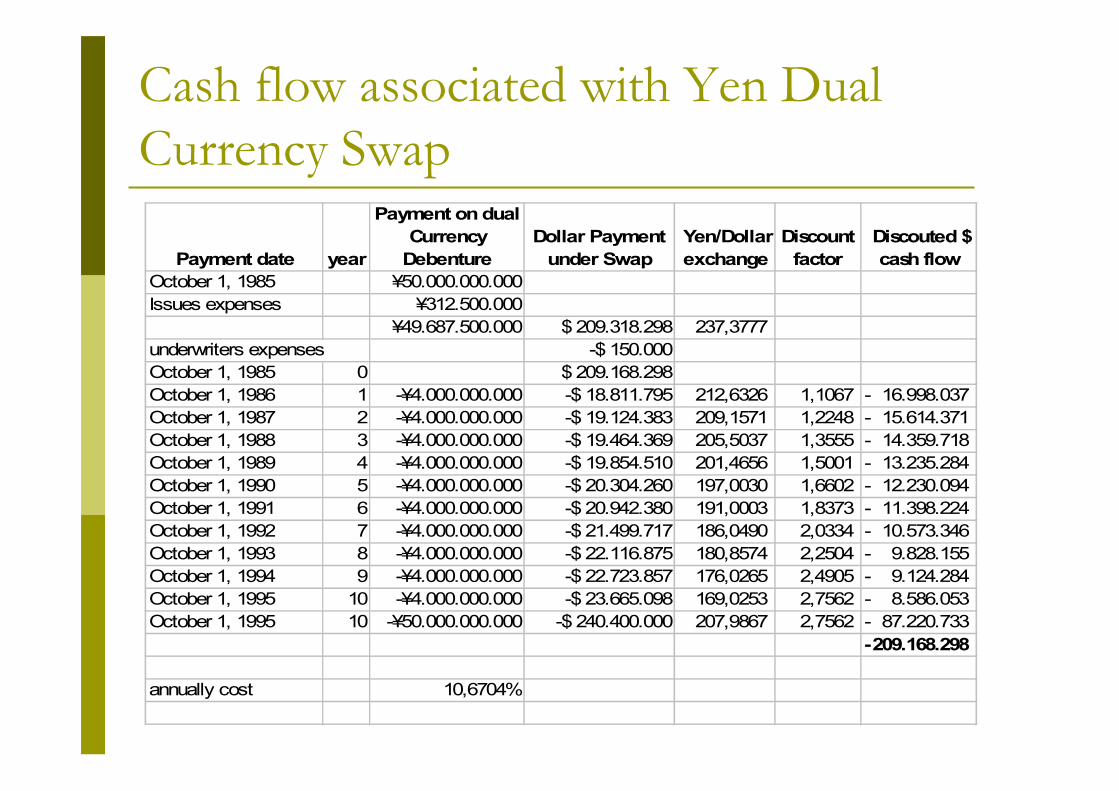

Cash flow associated with Yen Dual Currency Swap

Payment date year

Payment on dual Currency

DebentureDollar Payment

under Swap Yen/Dollar exchange

Discount factor

Discouted $ cash flow

October 1, 1985 ¥50.000.000.000Issues expenses ¥312.500.000

¥49.687.500.000 $ 209.318.298 237,3777 underwriters expenses -$ 150.000October 1, 1985 0 $ 209.168.298October 1, 1986 1 -¥4.000.000.000 -$ 18.811.795 212,6326 1,1067 16.998.037- October 1, 1987 2 -¥4.000.000.000 -$ 19.124.383 209,1571 1,2248 15.614.371- October 1, 1988 3 -¥4.000.000.000 -$ 19.464.369 205,5037 1,3555 14.359.718- October 1, 1989 4 -¥4.000.000.000 -$ 19.854.510 201,4656 1,5001 13.235.284- October 1, 1990 5 -¥4.000.000.000 -$ 20.304.260 197,0030 1,6602 12.230.094- October 1, 1991 6 -¥4.000.000.000 -$ 20.942.380 191,0003 1,8373 11.398.224- October 1, 1992 7 -¥4.000.000.000 -$ 21.499.717 186,0490 2,0334 10.573.346- October 1, 1993 8 -¥4.000.000.000 -$ 22.116.875 180,8574 2,2504 9.828.155- October 1, 1994 9 -¥4.000.000.000 -$ 22.723.857 176,0265 2,4905 9.124.284- October 1, 1995 10 -¥4.000.000.000 -$ 23.665.098 169,0253 2,7562 8.586.053- October 1, 1995 10 -¥50.000.000.000 -$ 240.400.000 207,9867 2,7562 87.220.733-

209.168.298-

annually cost 10,6704%

Interest rate forwards and futures: forward forward

A forward forward is a contract that fixes an interest rate today on a future loan or deposit. The contract specifies the interest rate, the principal amount the start and ending dates of the future interest rate period.

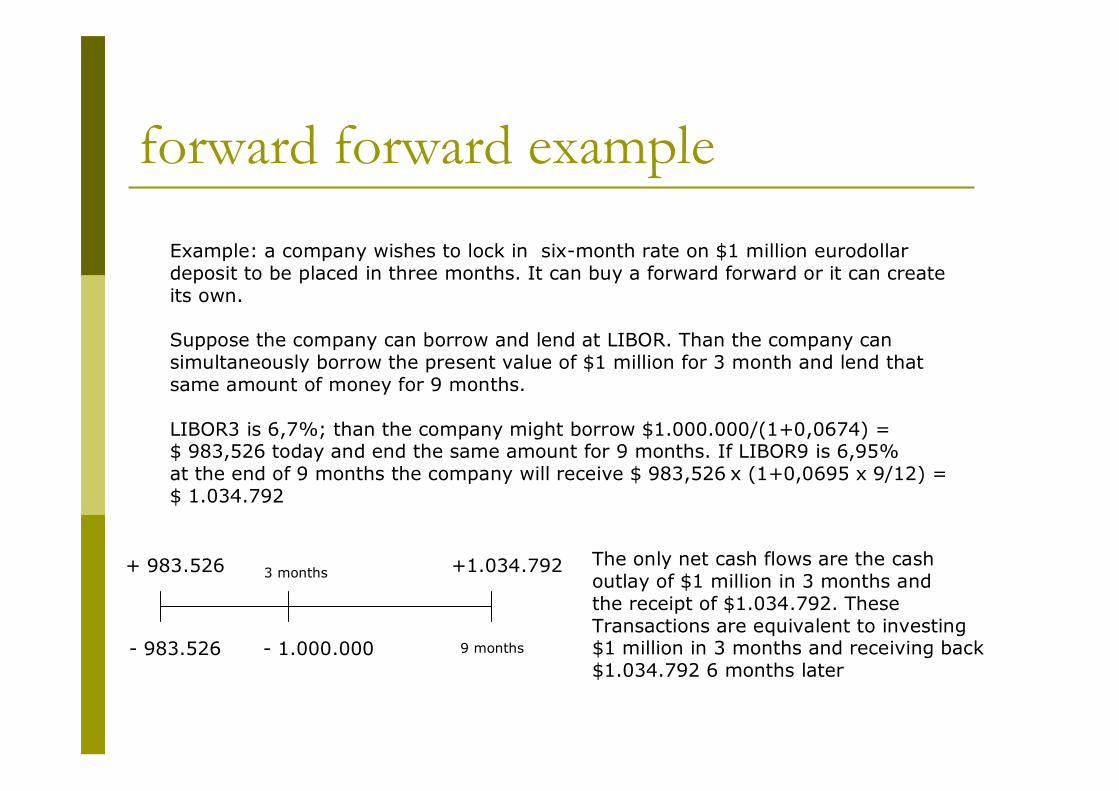

forward forward example

Example: a company wishes to lock in six-month rate on $1 million eurodollardeposit to be placed in three months. It can buy a forward forward or it can create its own.

Suppose the company can borrow and lend at LIBOR. Than the company can simultaneously borrow the present value of $1 million for 3 month and lend that same amount of money for 9 months.

LIBOR3 is 6,7%; than the company might borrow $1.000.000/(1+0,0674) = $ 983,526 today and end the same amount for 9 months. If LIBOR9 is 6,95%at the end of 9 months the company will receive $ 983,526 x (1+0,0695 x 9/12) =$ 1.034.792

- 983.526

+ 983.526

- 1.000.000

+1.034.7923 months

9 months

The only net cash flows are the cash outlay of $1 million in 3 months andthe receipt of $1.034.792. These Transactions are equivalent to investing$1 million in 3 months and receiving back$1.034.792 6 months later

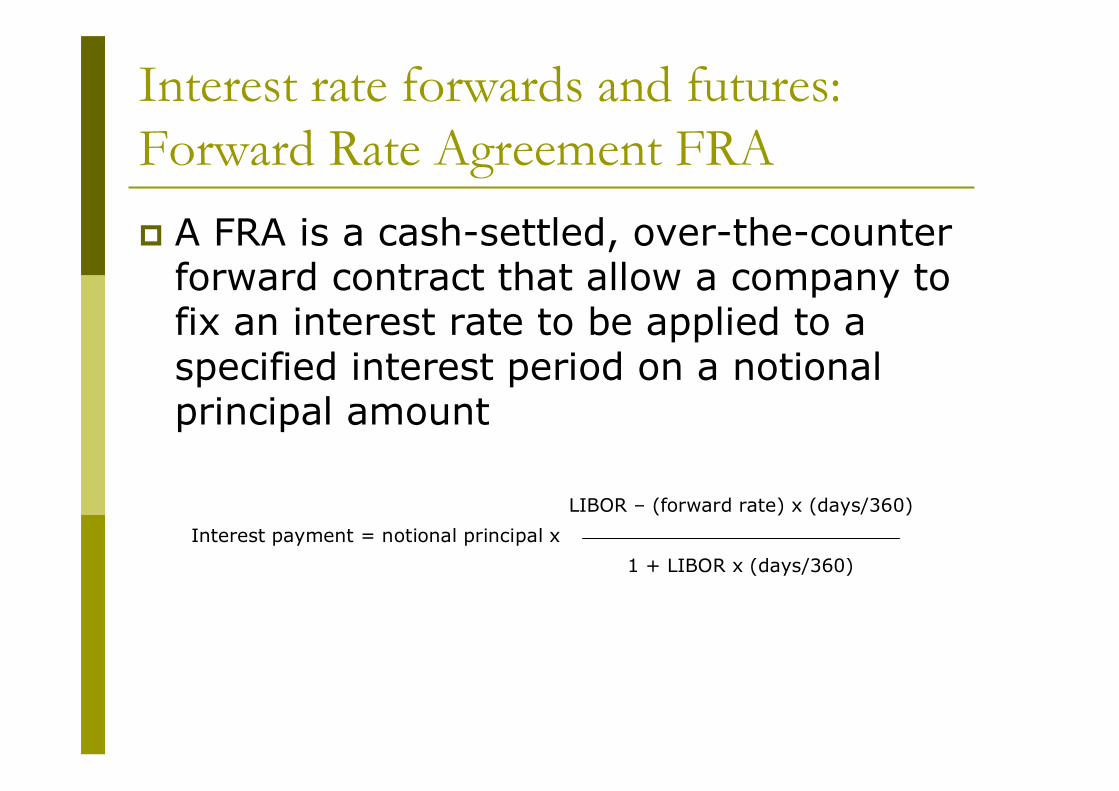

Interest rate forwards and futures: Forward Rate Agreement FRA

A FRA is a cash-settled, over-the-counter forward contract that allow a company to fix an interest rate to be applied to a specified interest period on a notional principal amount

LIBOR – (forward rate) x (days/360)

1 + LIBOR x (days/360)Interest payment = notional principal x

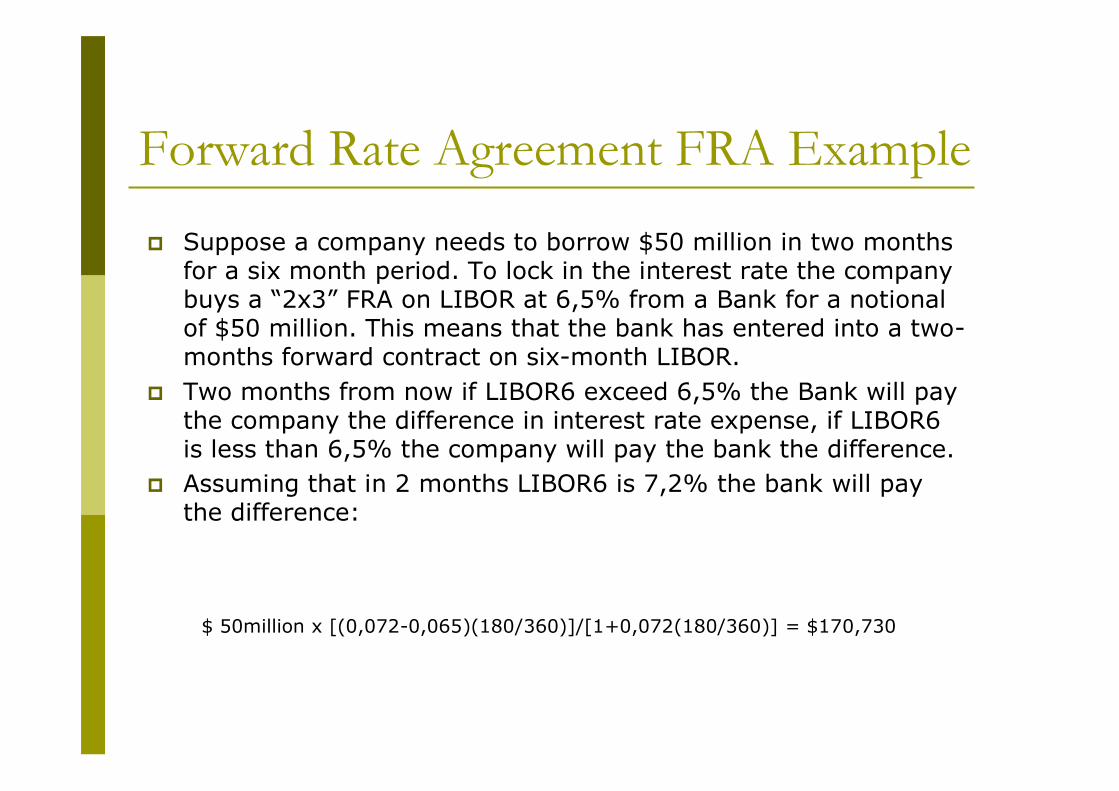

Forward Rate Agreement FRA Example

Suppose a company needs to borrow $50 million in two months for a six month period. To lock in the interest rate the companybuys a “2x3” FRA on LIBOR at 6,5% from a Bank for a notional of $50 million. This means that the bank has entered into a two-months forward contract on six-month LIBOR.Two months from now if LIBOR6 exceed 6,5% the Bank will pay the company the difference in interest rate expense, if LIBOR6 is less than 6,5% the company will pay the bank the difference.Assuming that in 2 months LIBOR6 is 7,2% the bank will pay the difference:

$ 50million x [(0,072-0,065)(180/360)]/[1+0,072(180/360)] = $170,730

Measuring and managing translation and transaction

exposure

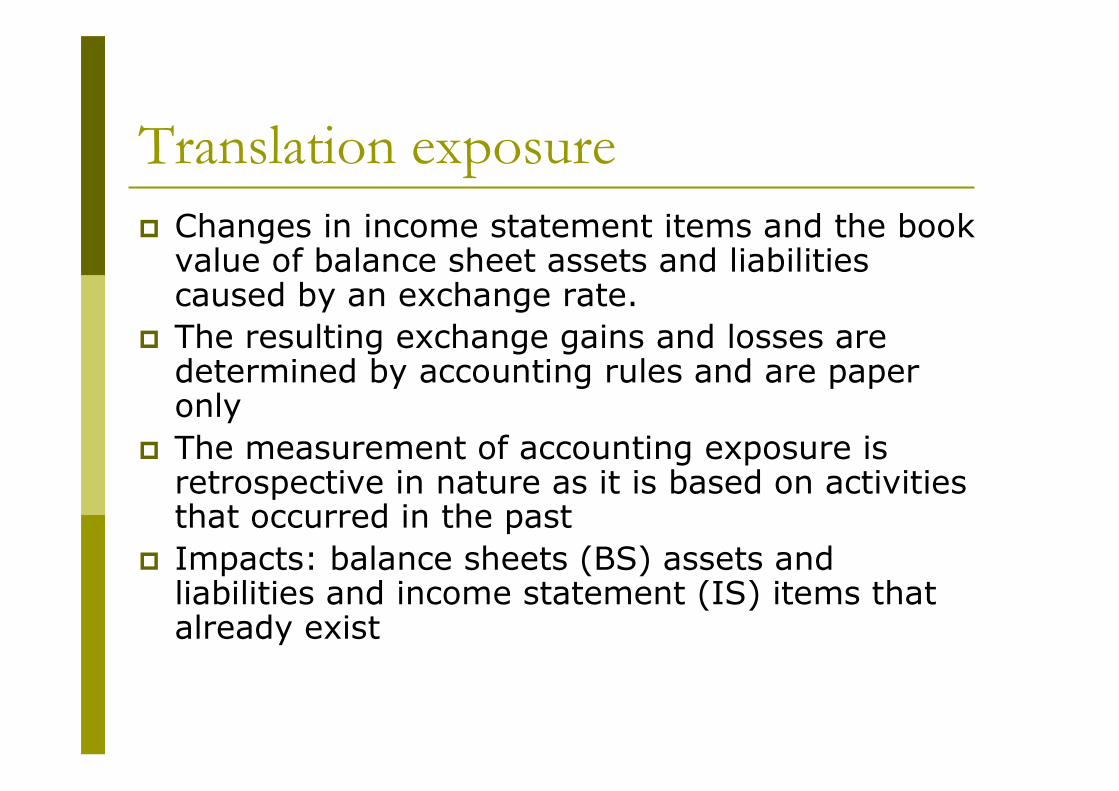

Translation exposureChanges in income statement items and the book value of balance sheet assets and liabilities caused by an exchange rate.The resulting exchange gains and losses are determined by accounting rules and are paper only The measurement of accounting exposure is retrospective in nature as it is based on activities that occurred in the pastImpacts: balance sheets (BS) assets and liabilities and income statement (IS) items that already exist

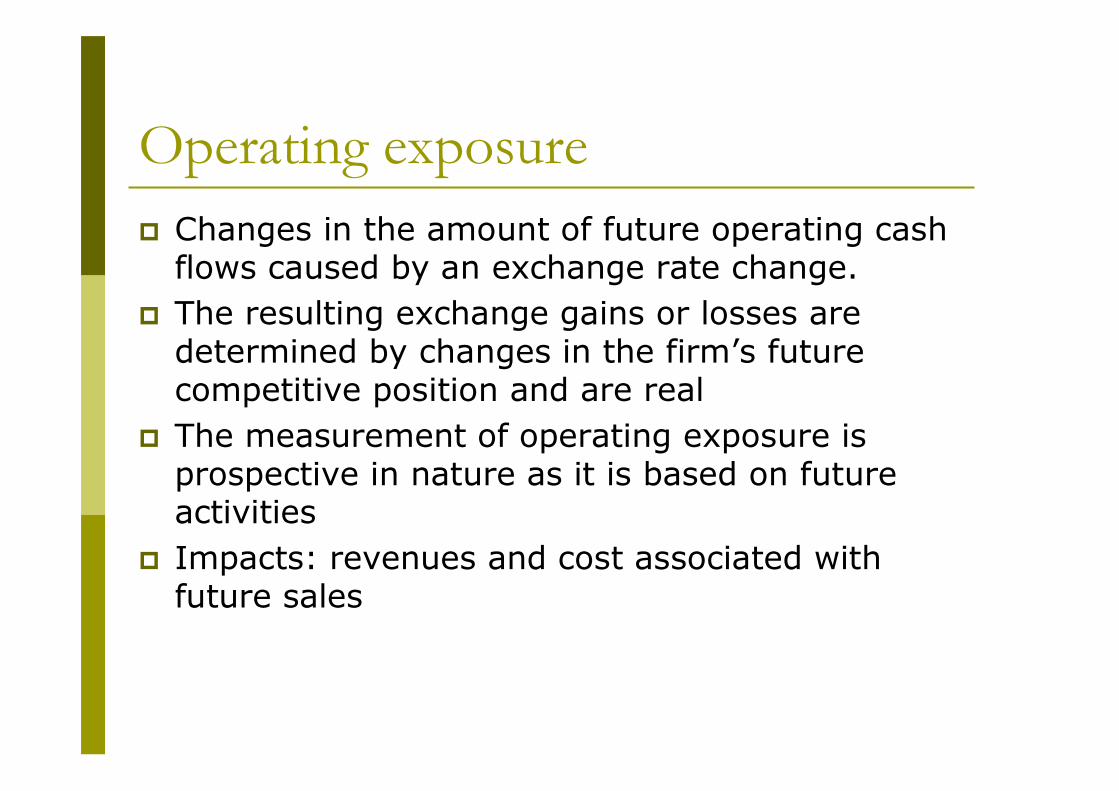

Operating exposureChanges in the amount of future operating cash flows caused by an exchange rate change. The resulting exchange gains or losses are determined by changes in the firm’s future competitive position and are realThe measurement of operating exposure is prospective in nature as it is based on future activitiesImpacts: revenues and cost associated with future sales

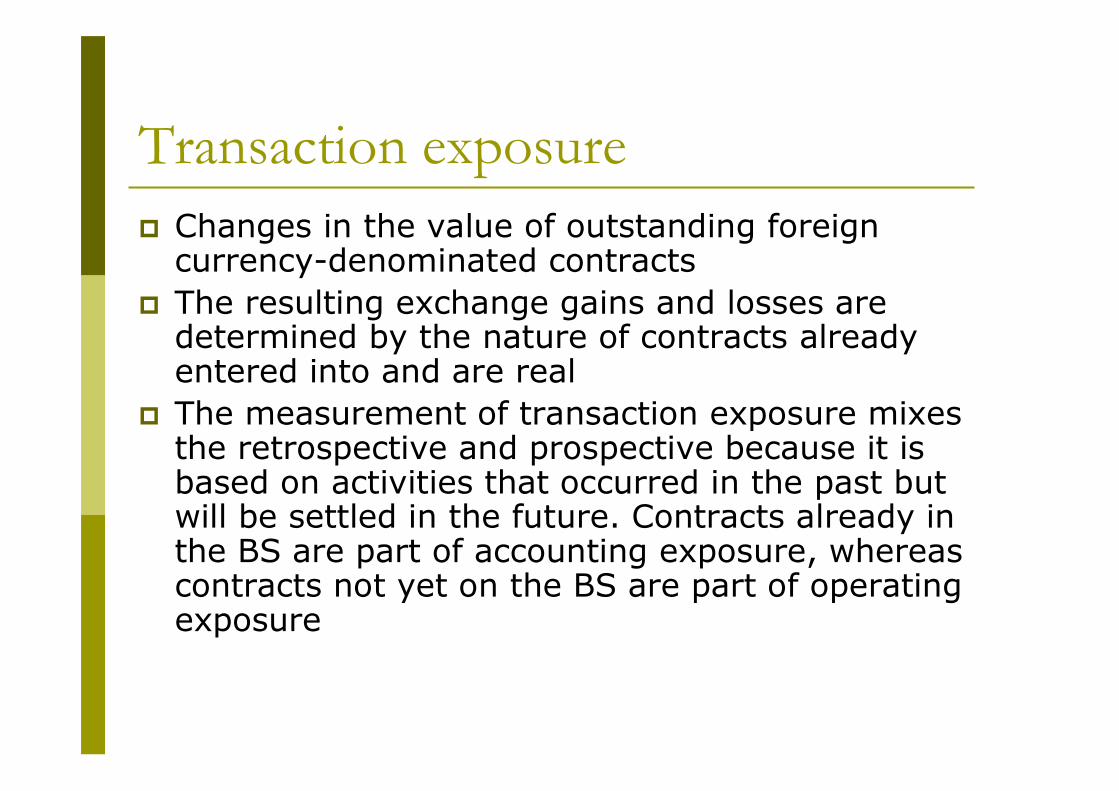

Transaction exposureChanges in the value of outstanding foreign currency-denominated contractsThe resulting exchange gains and losses are determined by the nature of contracts already entered into and are realThe measurement of transaction exposure mixes the retrospective and prospective because it is based on activities that occurred in the past but will be settled in the future. Contracts already in the BS are part of accounting exposure, whereas contracts not yet on the BS are part of operating exposure

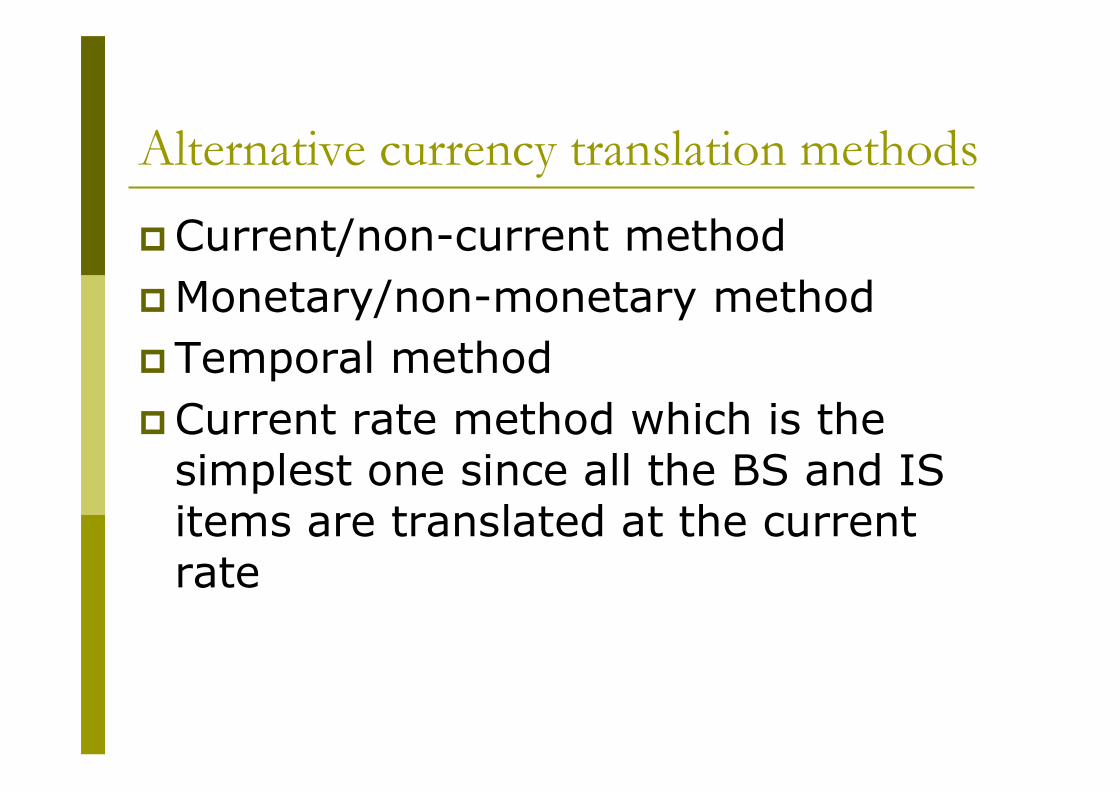

Alternative currency translation methods

Current/non-current methodMonetary/non-monetary methodTemporal methodCurrent rate method which is the simplest one since all the BS and IS items are translated at the current rate

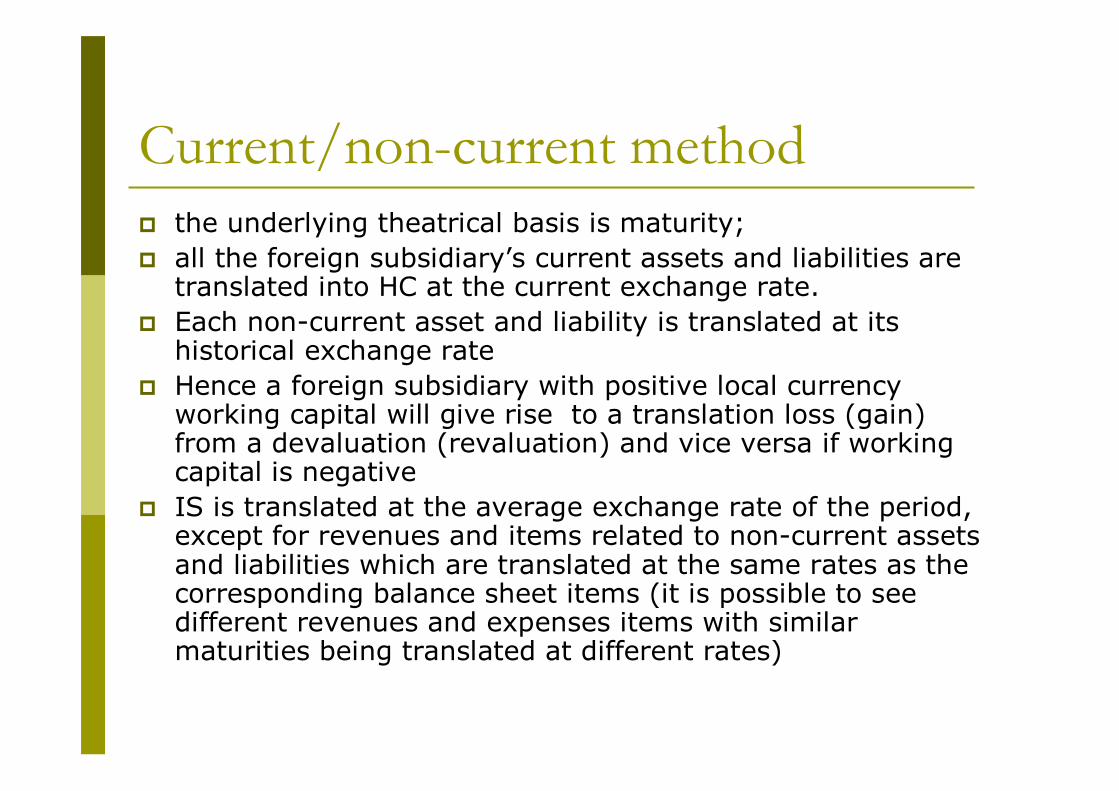

Current/non-current methodthe underlying theatrical basis is maturity;all the foreign subsidiary’s current assets and liabilities are translated into HC at the current exchange rate.Each non-current asset and liability is translated at its historical exchange rateHence a foreign subsidiary with positive local currency working capital will give rise to a translation loss (gain) from a devaluation (revaluation) and vice versa if working capital is negativeIS is translated at the average exchange rate of the period, except for revenues and items related to non-current assets and liabilities which are translated at the same rates as the corresponding balance sheet items (it is possible to see different revenues and expenses items with similar maturities being translated at different rates)

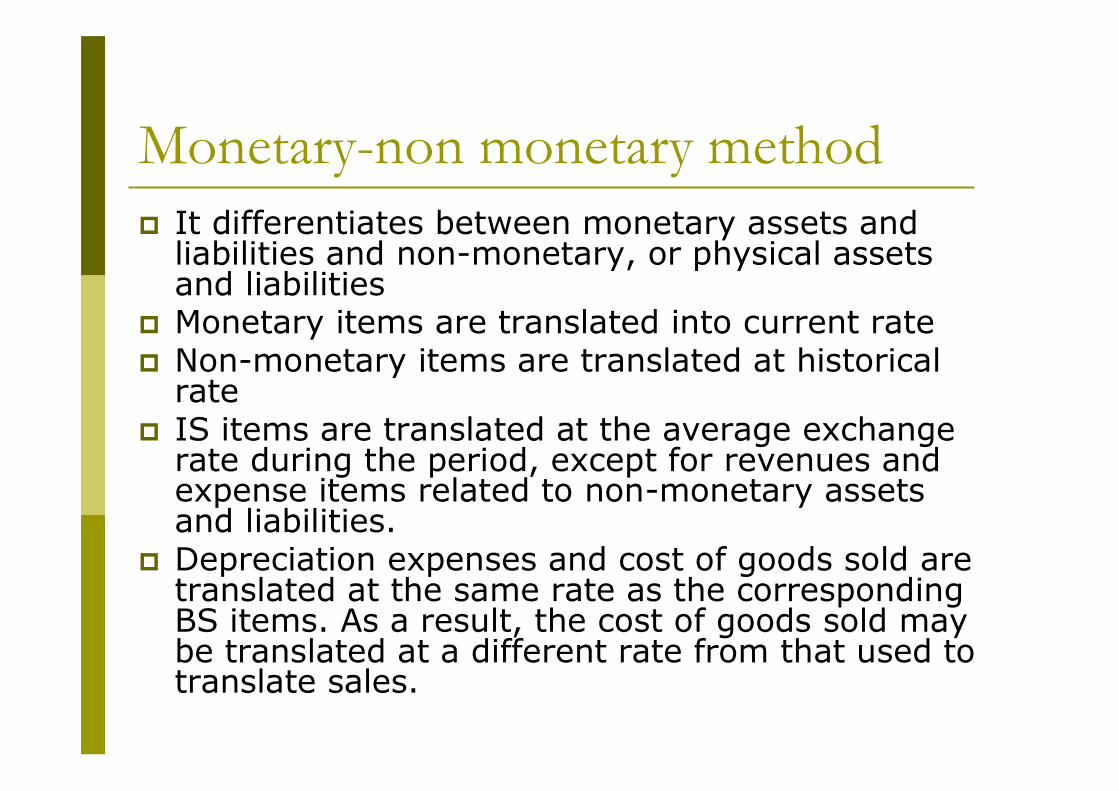

Monetary-non monetary methodIt differentiates between monetary assets and liabilities and non-monetary, or physical assets and liabilitiesMonetary items are translated into current rateNon-monetary items are translated at historical rateIS items are translated at the average exchange rate during the period, except for revenues and expense items related to non-monetary assets and liabilities. Depreciation expenses and cost of goods sold are translated at the same rate as the corresponding BS items. As a result, the cost of goods sold may be translated at a different rate from that used to translate sales.

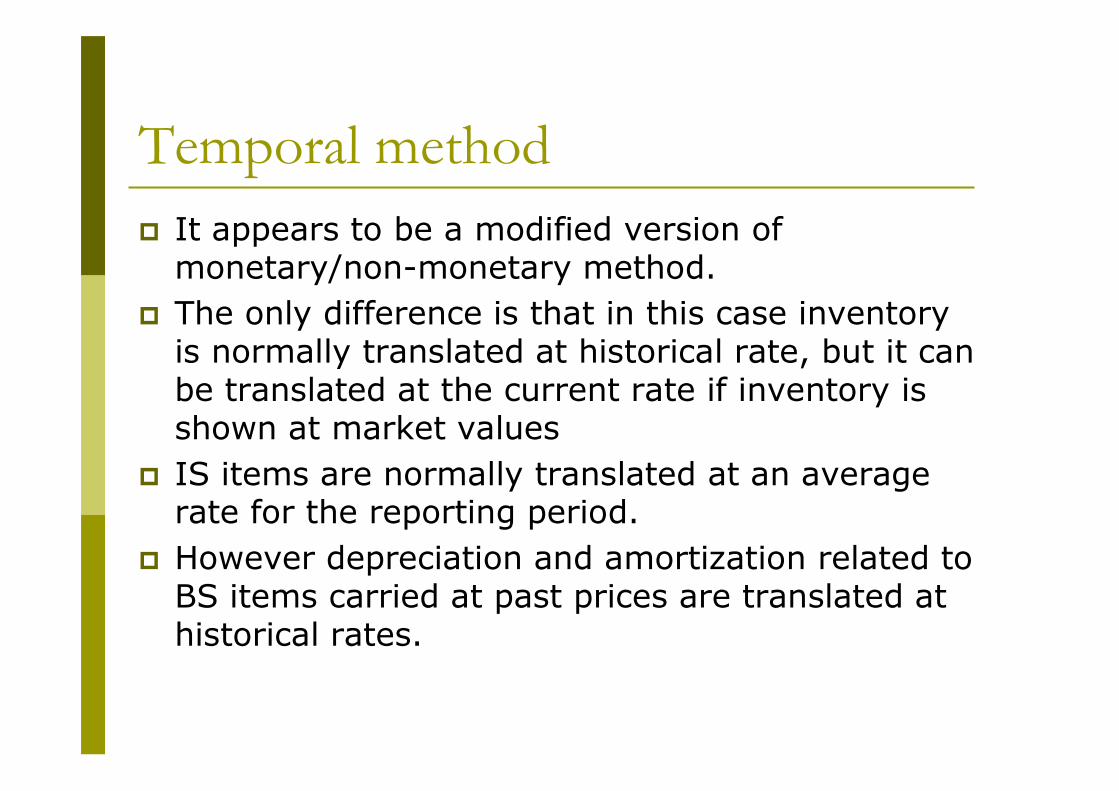

Temporal methodIt appears to be a modified version of monetary/non-monetary method. The only difference is that in this case inventory is normally translated at historical rate, but it can be translated at the current rate if inventory is shown at market valuesIS items are normally translated at an average rate for the reporting period.However depreciation and amortization related to BS items carried at past prices are translated at historical rates.

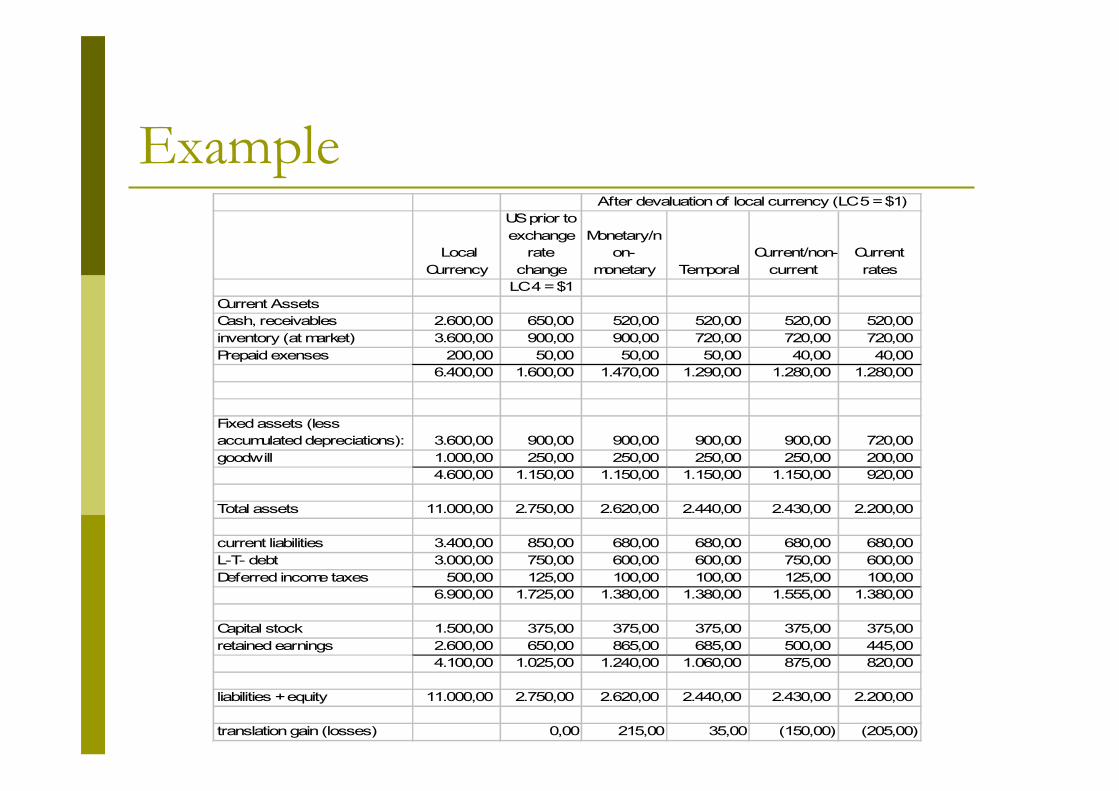

Example

Local Currency

US prior to exchange

rate change

Monetary/non-

monetary TemporalCurrent/non-

currentCurrent rates

LC 4 = $1Current AssetsCash, receivables 2.600,00 650,00 520,00 520,00 520,00 520,00 inventory (at market) 3.600,00 900,00 900,00 720,00 720,00 720,00 Prepaid exenses 200,00 50,00 50,00 50,00 40,00 40,00

6.400,00 1.600,00 1.470,00 1.290,00 1.280,00 1.280,00

Fixed assets (less accumulated depreciations): 3.600,00 900,00 900,00 900,00 900,00 720,00 goodwill 1.000,00 250,00 250,00 250,00 250,00 200,00

4.600,00 1.150,00 1.150,00 1.150,00 1.150,00 920,00

Total assets 11.000,00 2.750,00 2.620,00 2.440,00 2.430,00 2.200,00

current liabilities 3.400,00 850,00 680,00 680,00 680,00 680,00 L-T- debt 3.000,00 750,00 600,00 600,00 750,00 600,00 Deferred income taxes 500,00 125,00 100,00 100,00 125,00 100,00

6.900,00 1.725,00 1.380,00 1.380,00 1.555,00 1.380,00

Capital stock 1.500,00 375,00 375,00 375,00 375,00 375,00 retained earnings 2.600,00 650,00 865,00 685,00 500,00 445,00

4.100,00 1.025,00 1.240,00 1.060,00 875,00 820,00

liabilities + equity 11.000,00 2.750,00 2.620,00 2.440,00 2.430,00 2.200,00

translation gain (losses) 0,00 215,00 35,00 (150,00) (205,00)

After devaluation of local currency (LC 5 = $1)

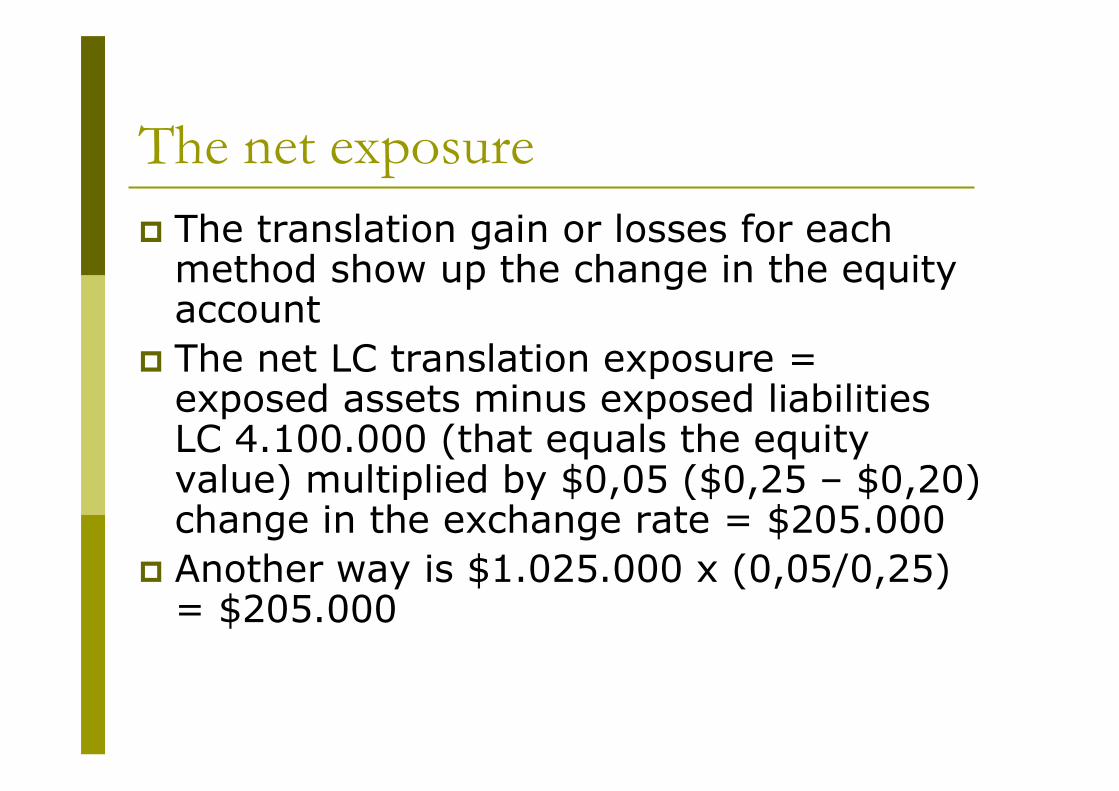

The net exposureThe translation gain or losses for each method show up the change in the equity accountThe net LC translation exposure = exposed assets minus exposed liabilities LC 4.100.000 (that equals the equity value) multiplied by $0,05 ($0,25 – $0,20) change in the exchange rate = $205.000Another way is $1.025.000 x (0,05/0,25) = $205.000

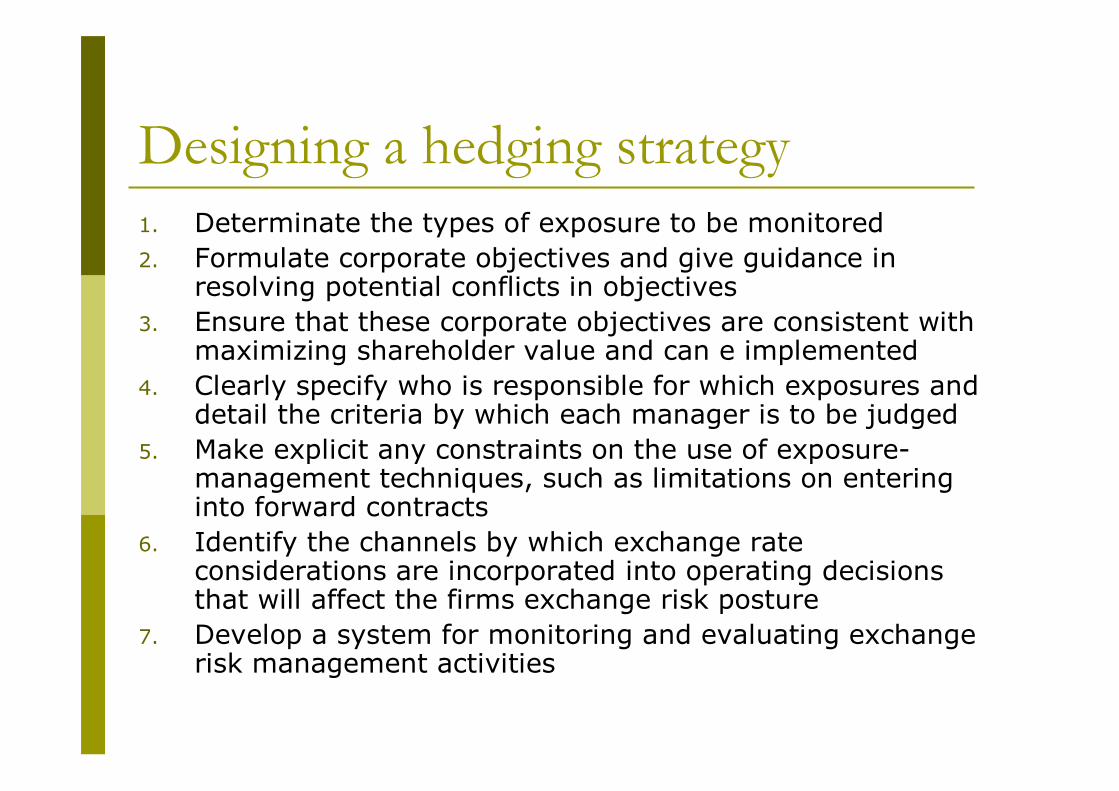

Designing a hedging strategy1. Determinate the types of exposure to be monitored2. Formulate corporate objectives and give guidance in

resolving potential conflicts in objectives3. Ensure that these corporate objectives are consistent with

maximizing shareholder value and can e implemented4. Clearly specify who is responsible for which exposures and

detail the criteria by which each manager is to be judged 5. Make explicit any constraints on the use of exposure-

management techniques, such as limitations on entering into forward contracts

6. Identify the channels by which exchange rate considerations are incorporated into operating decisions that will affect the firms exchange risk posture

7. Develop a system for monitoring and evaluating exchange risk management activities

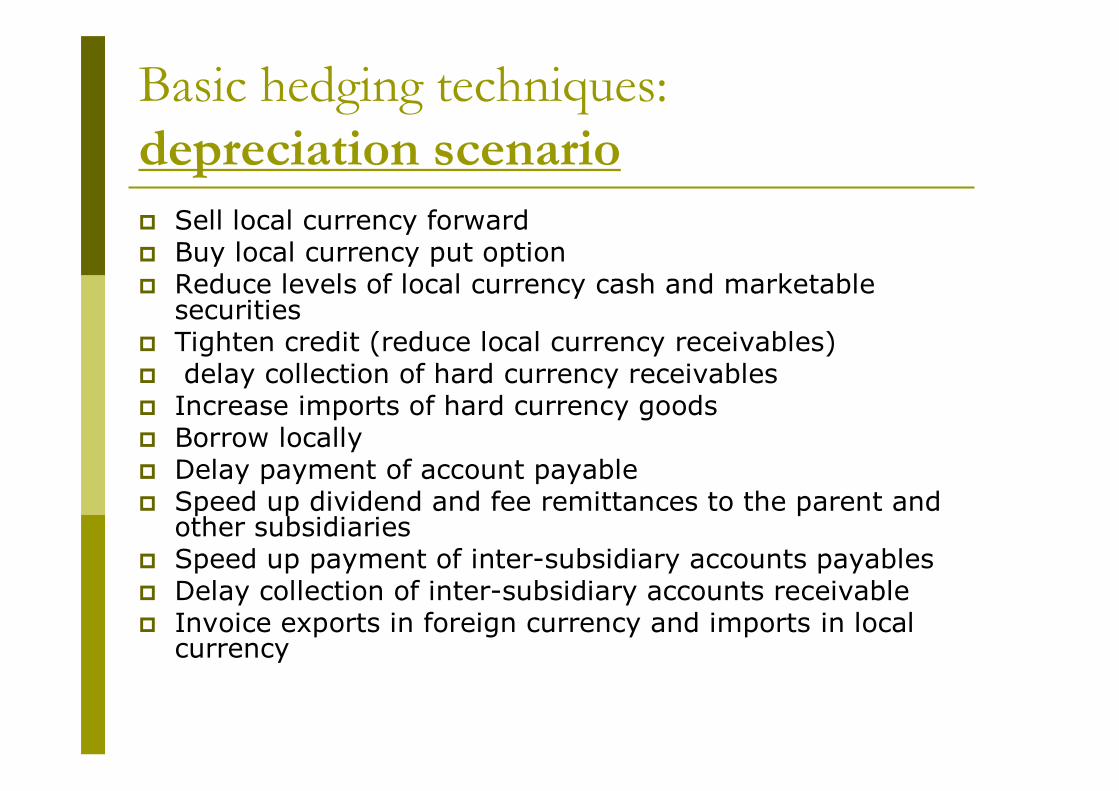

Basic hedging techniques: depreciation scenario

Sell local currency forwardBuy local currency put optionReduce levels of local currency cash and marketable securitiesTighten credit (reduce local currency receivables)delay collection of hard currency receivablesIncrease imports of hard currency goodsBorrow locallyDelay payment of account payableSpeed up dividend and fee remittances to the parent and other subsidiaries Speed up payment of inter-subsidiary accounts payablesDelay collection of inter-subsidiary accounts receivableInvoice exports in foreign currency and imports in local currency

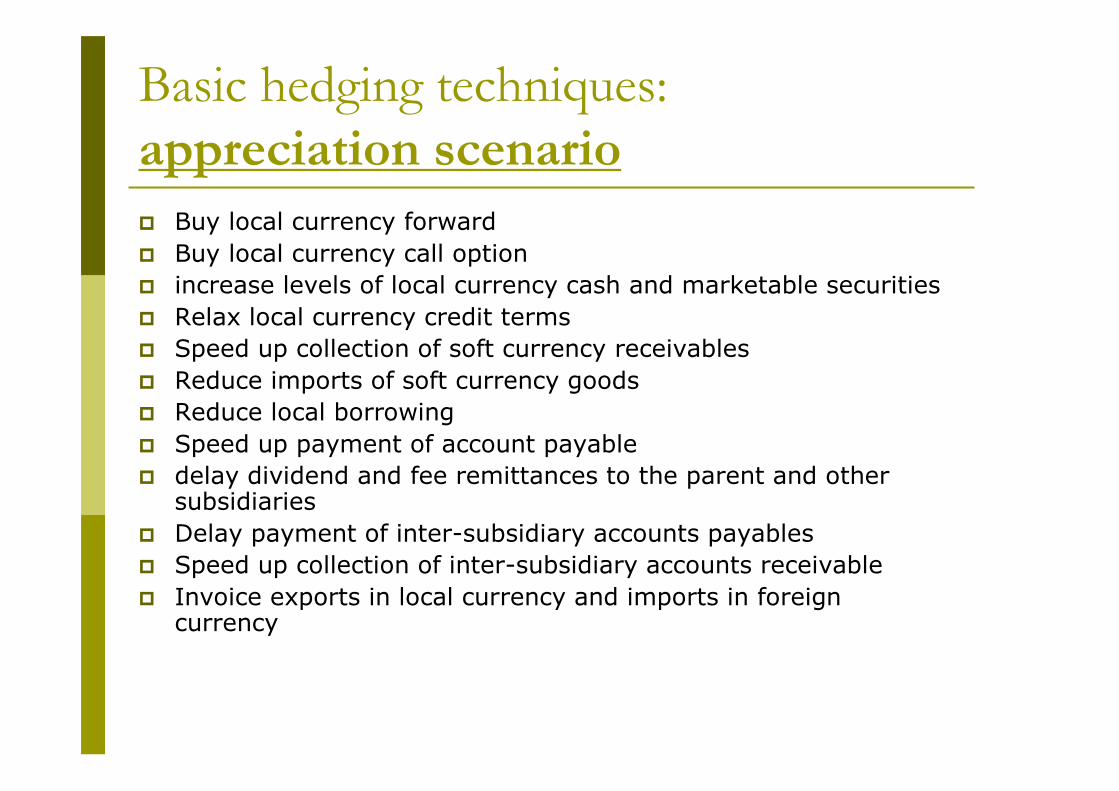

Basic hedging techniques: appreciation scenario

Buy local currency forwardBuy local currency call optionincrease levels of local currency cash and marketable securitiesRelax local currency credit termsSpeed up collection of soft currency receivablesReduce imports of soft currency goodsReduce local borrowingSpeed up payment of account payabledelay dividend and fee remittances to the parent and other subsidiaries Delay payment of inter-subsidiary accounts payablesSpeed up collection of inter-subsidiary accounts receivableInvoice exports in local currency and imports in foreign currency

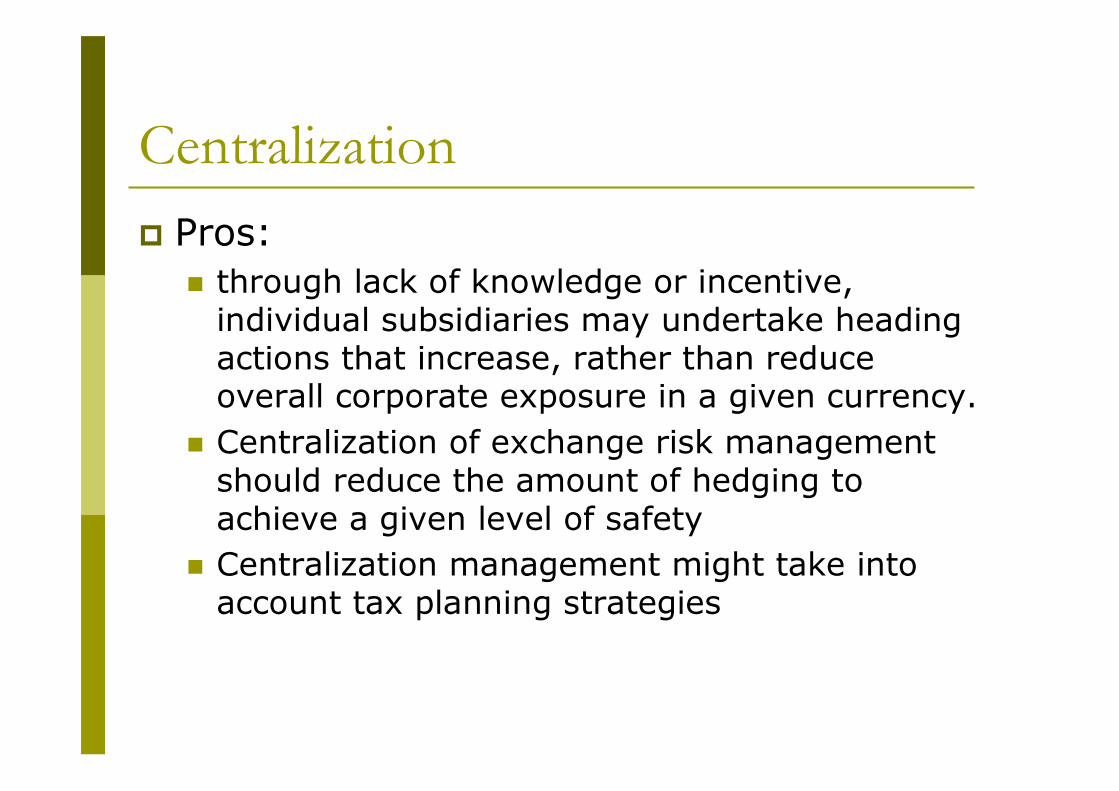

CentralizationPros:

through lack of knowledge or incentive, individual subsidiaries may undertake heading actions that increase, rather than reduce overall corporate exposure in a given currency. Centralization of exchange risk management should reduce the amount of hedging to achieve a given level of safetyCentralization management might take into account tax planning strategies

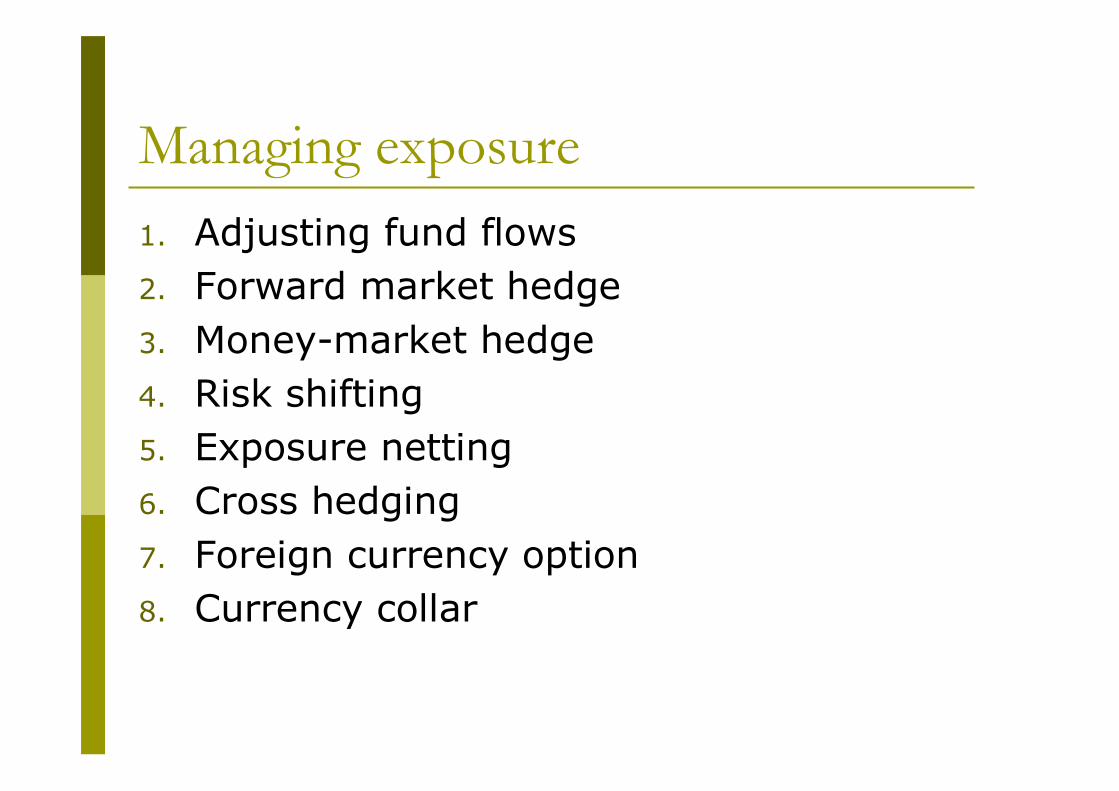

Managing exposure1. Adjusting fund flows 2. Forward market hedge3. Money-market hedge4. Risk shifting 5. Exposure netting 6. Cross hedging7. Foreign currency option8. Currency collar

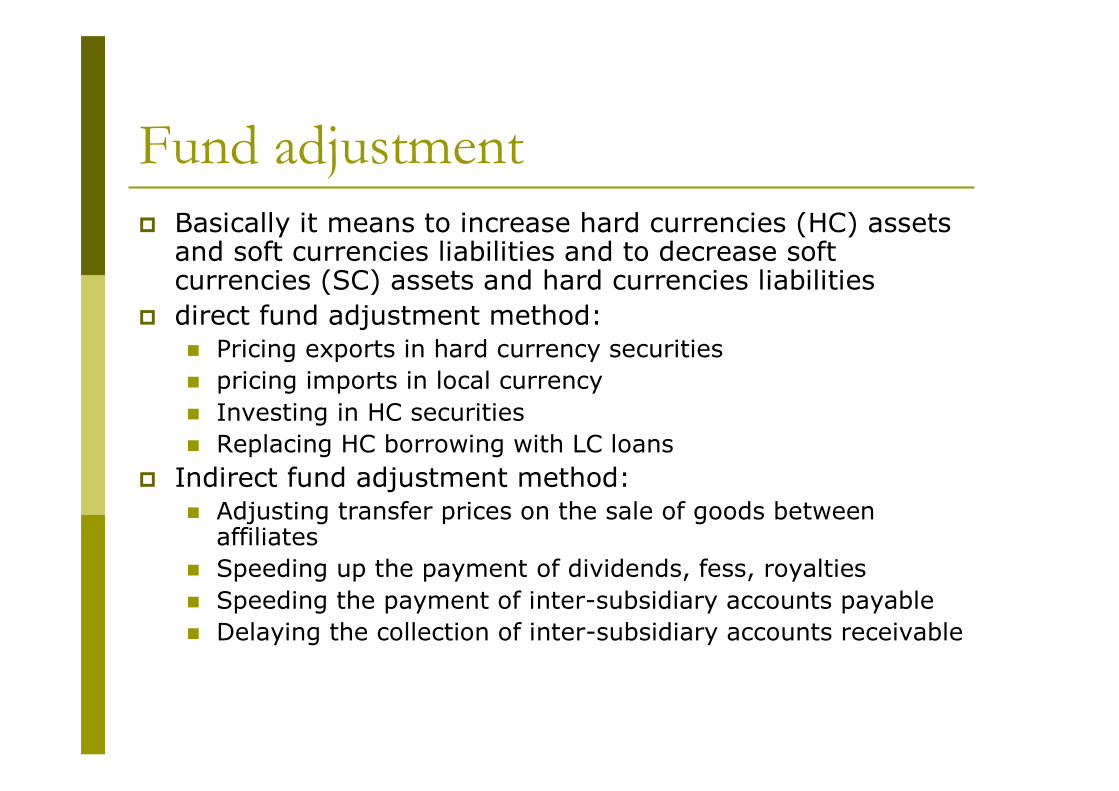

Fund adjustment Basically it means to increase hard currencies (HC) assets and soft currencies liabilities and to decrease soft currencies (SC) assets and hard currencies liabilitiesdirect fund adjustment method:

Pricing exports in hard currency securitiespricing imports in local currencyInvesting in HC securitiesReplacing HC borrowing with LC loans

Indirect fund adjustment method:Adjusting transfer prices on the sale of goods between affiliatesSpeeding up the payment of dividends, fess, royaltiesSpeeding the payment of inter-subsidiary accounts payableDelaying the collection of inter-subsidiary accounts receivable

Forward market hedgeIf you’re long a currency, hedge by selling forward if the currency is at forward premium (f1 > e0); if the currency is at forward discount (f1 < e0) do not hedgeIf you’re short a currency, hedge by buying forward if the currency is selling at a forward discount (f1 < e0); if the currency is at a forward premium (f1 > e0) do not hedge

Money-market hedgeIt is an alternative to forward market hedgeIt involve simultaneous borrowing and lending activities in two different countries to lock in the domestic currency value of a future foreign currency cash flow

Forward and money-market hedge: example

On Jan. 1, GE is awarded a contract to supply to LufthansaOn Dec. 31 GE will receive payment of € 10 million The most direct way for GE is to sell € 10 million forward contract for delivery in one year. Spot price $1,00/€; 1 year forward rate $0,0957/€Alternatively it can use a monetary-market hedge, which would involve borrowing €10 million for one year, converting into $, investing the proceed in security maturing on Dec. 31. suppose Euro and US interest rates are 15% and 10% respectively

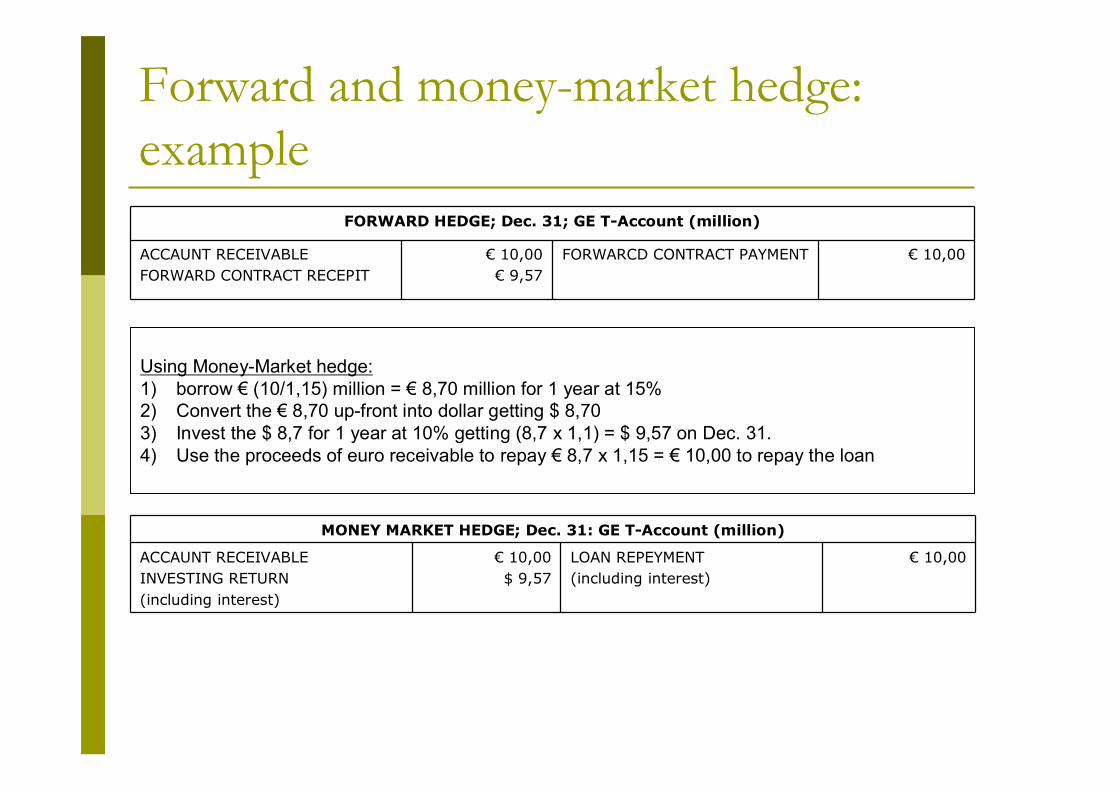

Forward and money-market hedge: example

€ 10,00FORWARCD CONTRACT PAYMENT€ 10,00€ 9,57

ACCAUNT RECEIVABLEFORWARD CONTRACT RECEPIT

FORWARD HEDGE; Dec. 31; GE T-Account (million)

€ 10,00LOAN REPEYMENT(including interest)

€ 10,00$ 9,57

ACCAUNT RECEIVABLEINVESTING RETURN(including interest)

MONEY MARKET HEDGE; Dec. 31: GE T-Account (million)

Using Money-Market hedge:1) borrow € (10/1,15) million = € 8,70 million for 1 year at 15% 2) Convert the € 8,70 up-front into dollar getting $ 8,70 3) Invest the $ 8,7 for 1 year at 10% getting (8,7 x 1,1) = $ 9,57 on Dec. 31.4) Use the proceeds of euro receivable to repay € 8,7 x 1,15 = € 10,00 to repay the loan

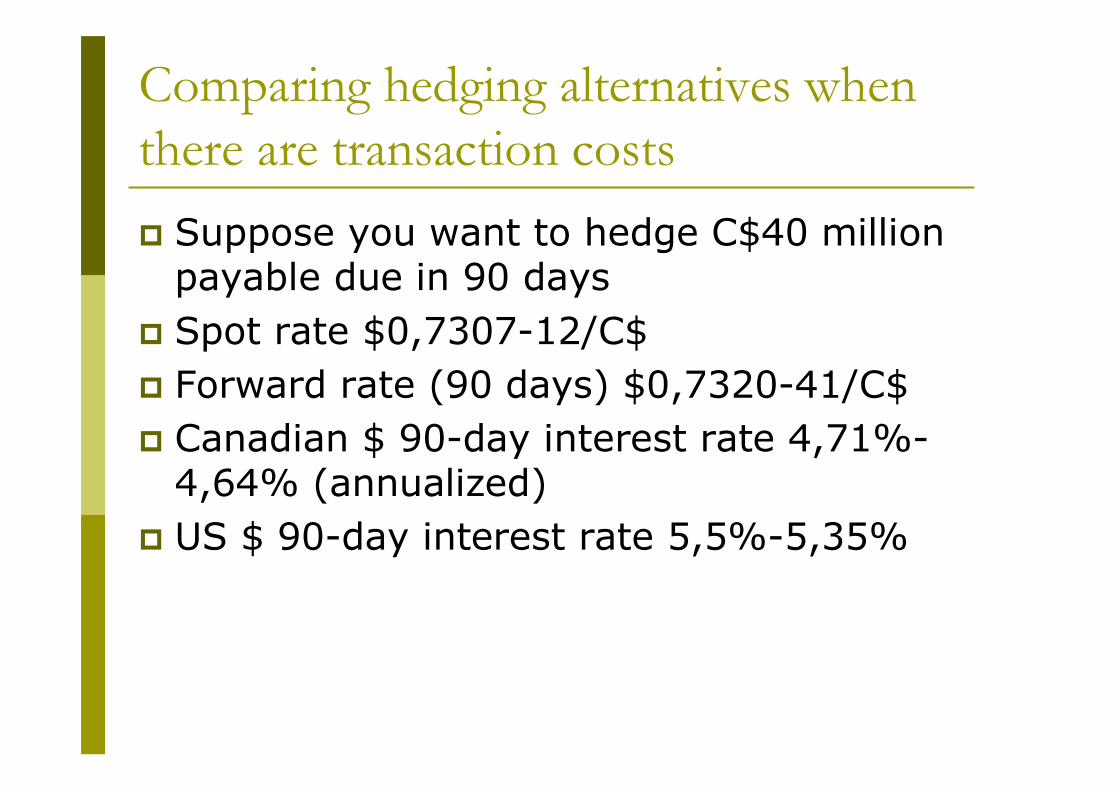

Comparing hedging alternatives when there are transaction costs

Suppose you want to hedge C$40 million payable due in 90 daysSpot rate $0,7307-12/C$Forward rate (90 days) $0,7320-41/C$Canadian $ 90-day interest rate 4,71%-4,64% (annualized)US $ 90-day interest rate 5,5%-5,35%

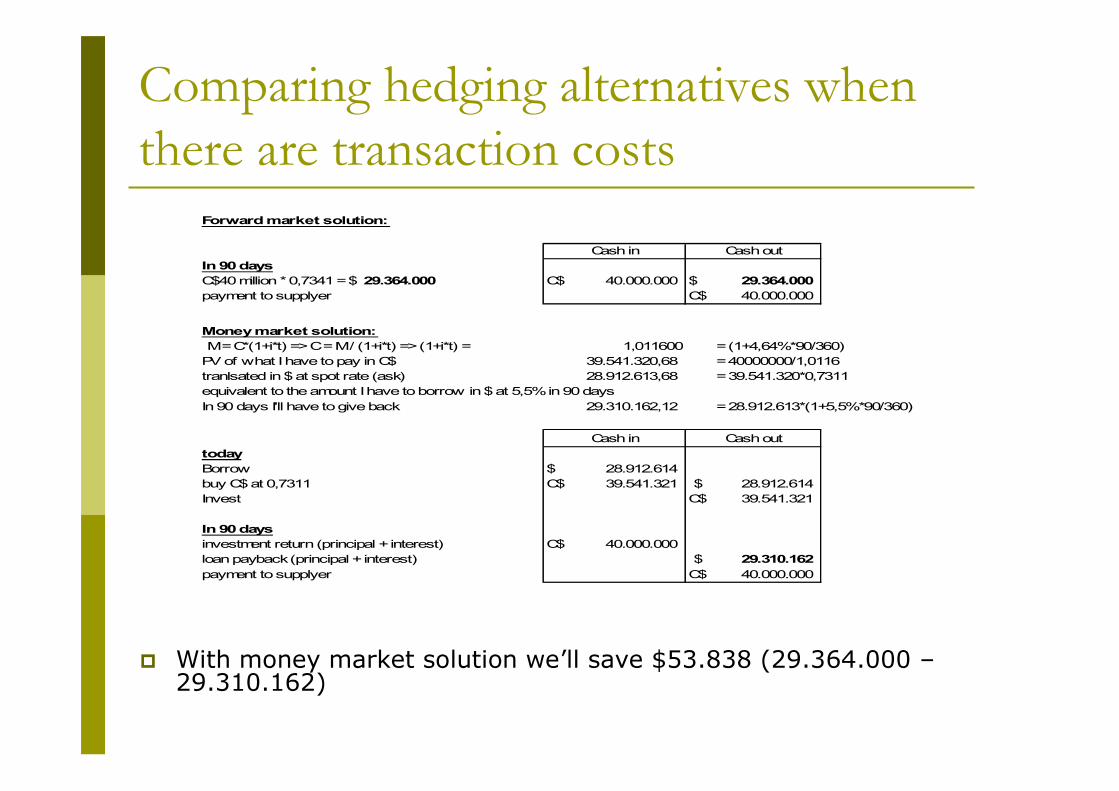

Comparing hedging alternatives when there are transaction costs

With money market solution we’ll save $53.838 (29.364.000 –29.310.162)

Forward market solution:

In 90 daysC$40 million * 0,7341 = $ 29.364.000 C$ 40.000.000 $ 29.364.000 payment to supplyer C$ 40.000.000

Money market solution: M = C*(1+i*t) => C = M / (1+i*t) => (1+i*t) = 1,011600 = (1+4,64%*90/360)

PV of what I have to pay in C$ 39.541.320,68 = 40000000/1,0116tranlsated in $ at spot rate (ask) 28.912.613,68 = 39.541.320*0,7311equivalent to the amount I have to borrow in $ at 5,5% in 90 daysIn 90 days I'll have to give back 29.310.162,12 = 28.912.613*(1+5,5%*90/360)

todayBorrow $ 28.912.614 buy C$ at 0,7311 C$ 39.541.321 $ 28.912.614 Invest C$ 39.541.321

In 90 daysinvestment return (principal + interest) C$ 40.000.000 loan payback (principal + interest) $ 29.310.162 payment to supplyer C$ 40.000.000

Cash in Cash out

Cash in Cash out

Pricing and risk shiftingInvoicing in domestic currency allow shifting the risk to the customer but this can work with not-informed customer;(alternatively) pricing on forward rate. In the precedent example, in order to be sure to get $10 million, GE should have priced at €10 million/0,957 = € 10,45 millionAdopting price adjustment clauses setting a neutral zone representing the currency range in which risk is not shared

Exposure nettingIt involves offsetting exposures in one currency with exposures in the same or another currency, where exchange rates are expected to move in a way such that losses (gains) on the first exposed position will be offset by gains (losses) on the second currency exposure

A firm can offset a long position in a currency with a short position in the same currencyIf the exchange rate movements of two currencies are positively correlated, than the firm can offset a long position in one currency and a short position in the otherIf the currency movements are negatively correlated, than short (or long) positions can be used to offset each otherIn exposure netting you’ve to take into account different maturities of assets and liabilities

Cross-hedgingHedging with future is very similar to hedging with forward contracts. However the exact future contract required might be unavailable.Future contracts on another currency that is correlated with the one of interest might be used.The resulting regression coefficient tells us the sign and approximate the size of the futures/forward position we should take in the related currency

Foreign currency optionIn the precedent example G can buy for $100.000 the right to sell to Citigroup €10 million on Dec. 31 at a price of $0,957/€.Instated of a straight put option, GE could use a futures put option. This would entail GE buying a put option on a December futures contract with the option expiring in April.If the put were in-the-money on April 1, GE would exercise it and receive a short position in a euro futures contract plus a cash amount equal to the strike price minus the Dec. futures price as of April 1.

Currency collarsA currency collar is a combination of option contracts allowing to create a range so that the holder of the collar can exercise the contract if at the expiring date the currency is settled within this range. Beyond the range protection is assured

Option Vs. forward contractsThe ideal use of forward contracts is when the exposure has a straight risk-reward profile; forward contract gains or losses are exactly by the losses or gains on the underlying transactionIf the transaction exposure is uncertain (the volume or the foreign currency prices of the items being bought or sold are unknown), currency option are preferred