Embed Size (px)

Citation preview

International Federation of Accountants

April 26, 2009

Transitioning to One World in Accounting Education

Robert Bunting, IFAC President

The Higher Education Accounting Forum

Global Economic Crisis

Global Economic Crisis

Demonstrates depth of international interdependencies (i.e., G20 Summit)

Highlights importance of finding international solutions

Underscores need for one set of global standards across the financial system

Reinforces need for high ethical standards and stronger corporate governance

Places greater pressure on public institutions

IFAC and the Financial Crisis

Reemphasizing and restating the urgency of convergence

Expediting development of standards and guidance on key issues, i.e., going concern, fair value, financial instruments, and corporate governance

Providing global resources for implementation and compliance monitoring

Supporting OECD corporate governance principles

Speaking with a global voice to international regulators, standard setters, and others

IFAC addresses the crisis by:

What IFAC Does

Sets international standards for:

– Auditing

– Ethics

– Accounting Education

– Public Sector Financial Reporting

Supports adoption and implementation of all global standards

Speaks for the global auditing and accounting profession

Liaises with regulators & other standard setters

The IFAC Family

157 members and associates in 122 countries and jurisdictions

2.5 million accountants in all segments of the profession:

– public practice

– education

– government service

– industry and commerce

Regional accountancy bodies

Global Networks of Audit Firms (21)

Globalization

Credentials becoming a global stamp of quality

International marketing by accountancy bodies, like the AICPA

Standards are overwhelmingly global

Accelerating pace at which globalization will impact accounting and auditing in universities

Academic programs

Business offices

Shaping the Accountancy Profession

How IFAC Can Help NACUBO

Vehicle for NACUBO access/influence on international issues

Academic access to standard setting

Provides corporate governance and ethical guidance

Offers sustainability guidance

Facilitates research and information exchange among academics

Addresses risk management, public sector performance, and other relevant issues

Why International Standards Matter

GASB

FASAB

GAO “Yellow Book”

FASB

AICPA ASB

IPSASB

IASB

IAASB

INTOSAI

IPSASB

U.S. International

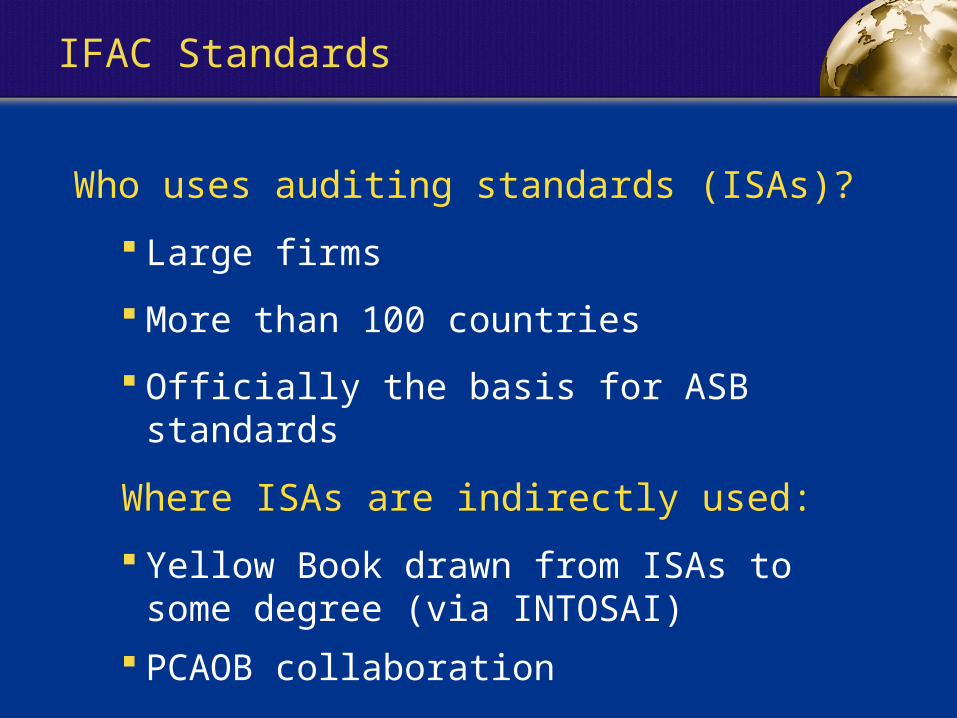

IFAC Standards

Who uses auditing standards (ISAs)?

Large firms

More than 100 countries

Officially the basis for ASB standards

Where ISAs are indirectly used:

Yellow Book drawn from ISAs to some degree (via INTOSAI)

PCAOB collaboration

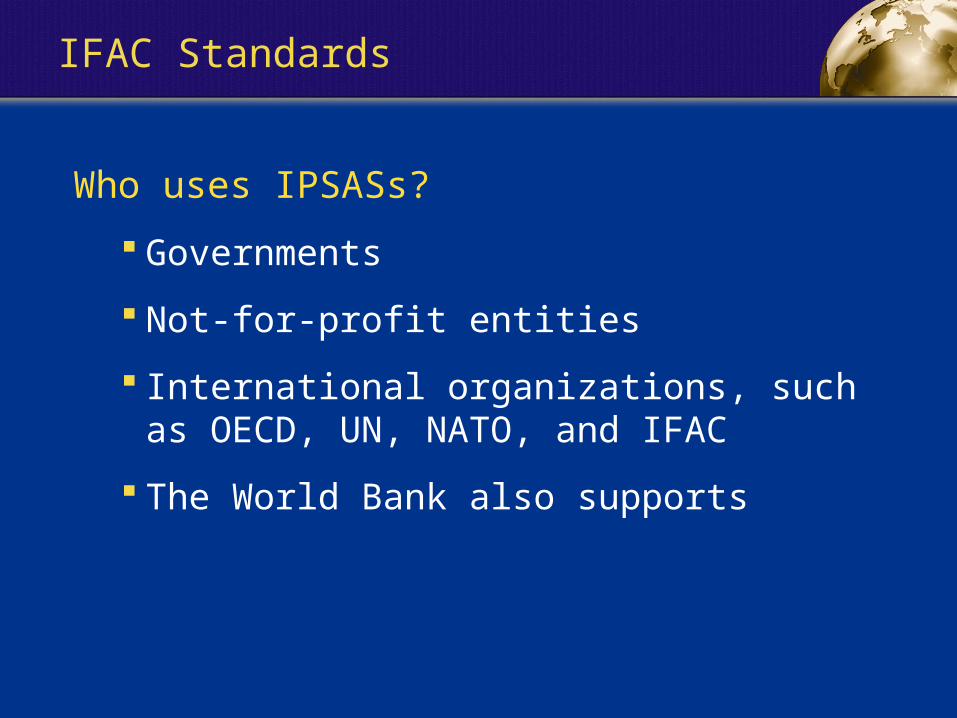

IFAC Standards

Who uses IPSASs?

Governments

Not-for-profit entities

International organizations, such as OECD, UN, NATO, and IFAC

The World Bank also supports

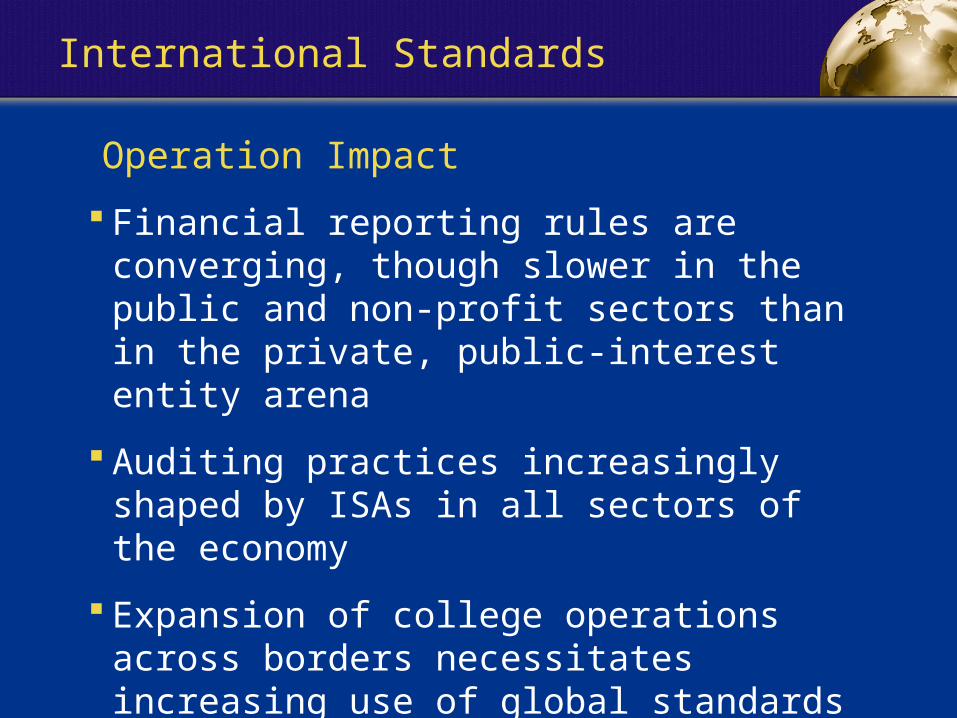

International Standards

Financial reporting rules are converging, though slower in the public and non-profit sectors than in the private, public-interest entity arena

Auditing practices increasingly shaped by ISAs in all sectors of the economy

Expansion of college operations across borders necessitates increasing use of global standards

Statutory audits for local authorities

Reporting with IFRS (versions)

Operation Impact

International Standards

Academic Impact – Need to Broaden Curriculum

Teaching only U.S. GAAP handcuffs students to U.S. economy. Must incorporate ISAs IPSASs, and IFRSs in curriculum.

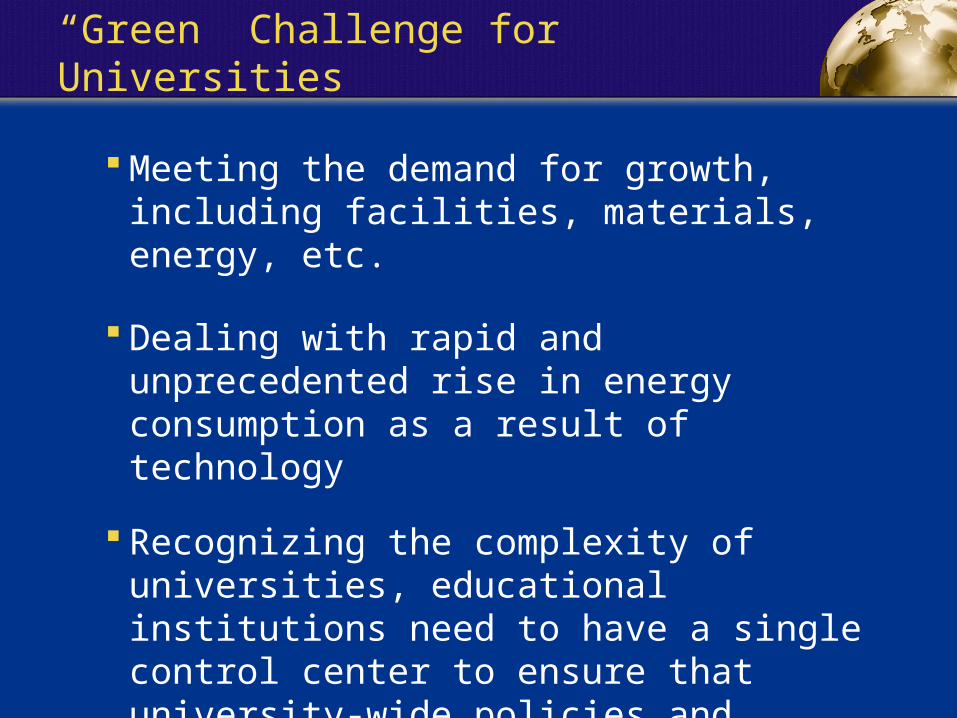

“Green” Challenge for Universities

Meeting the demand for growth, including facilities, materials, energy, etc.

Dealing with rapid and unprecedented rise in energy consumption as a result of technology

Recognizing the complexity of universities, educational institutions need to have a single control center to ensure that university-wide policies and procedures are implemented effectively and consistently

“Green” Solutions

Need ownership and coordination at the top

Need to identify clear green and social goals with stakeholder engagement

Need to identify broader set of measures of performance to include environmental and social issues

Start with relatively simple energy efficiency and waste minimization and better procurement initiatives

IFAC Sustainability Framework offers pointers for accountants and university business officers to sustainably manage their organizations.

“Green” Solutions

Engage All Stakeholders

What does this all mean?

Up-skilling/recruitment of staff in international accounting and auditing

– Accentuates the serious problem of shortage of accounting PhDs

Need to “internationalize” curricula and textbooks

International Education Standards can help

Means that you are “future-proofing” your students

Academic

What does this all mean?

Financial constraints are increasing

– Endowments and income declining

– Funding under pressure

Need to monitor and desirably influence the development of standards

Need for a single set of high-quality standards (US)

Competitive role in international credentialing?

Operational

The time for

study may be

passing

quickly.

Thinking

globally must

be paired with

acting

globally.

Moving Ahead

We are moving

rapidly to “one

world” in

accounting,

auditing, and

corporate

governance.

The Future

Observation vs. Mindful Purpose

Is there a role for NACUBO in shaping global policy?

International Federation of AccountantsInternational Federation of Accountants

www.ifac.orgwww.ifac.org