Embed Size (px)

Citation preview

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update

Tony Christian

Director, Cambashi

www.cambashi.com

COFES 2011

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Factors

2

Commodity Prices

Food Prices

Political turmoilOil prices

Trade deficits

Sovereign debt

Japanese tragedy

Inflation

QE

Stimulus packages

Financial system unknowns

Eurozone tensions

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

3

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

4

Introduction

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

5

Introduction

Tracking The Technical Applications Software Market

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

6

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

7

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

8

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

9

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

10

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Cambashi

11

Founded in 1984 in Cambridge, UK, US subsidiary opened Boston, MA in 2008

Worldwide network of associates

Studying the use of IT in industry

Business reasons for IT investment decisions

Technology that addresses these issues

Market mechanisms that bring users and vendors together

Impact of deployment of applications and infrastructure

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

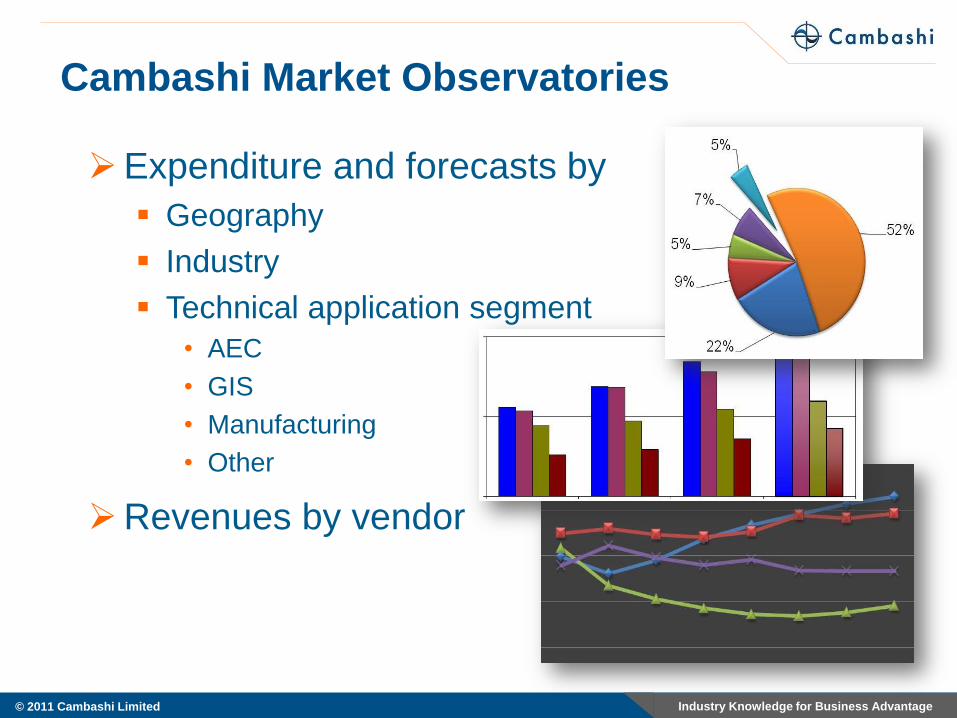

Cambashi Market Observatories

Expenditure and forecasts by

Geography

Industry

Technical application segment

• AEC

• GIS

• Manufacturing

• Other

Revenues by vendor

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

13

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

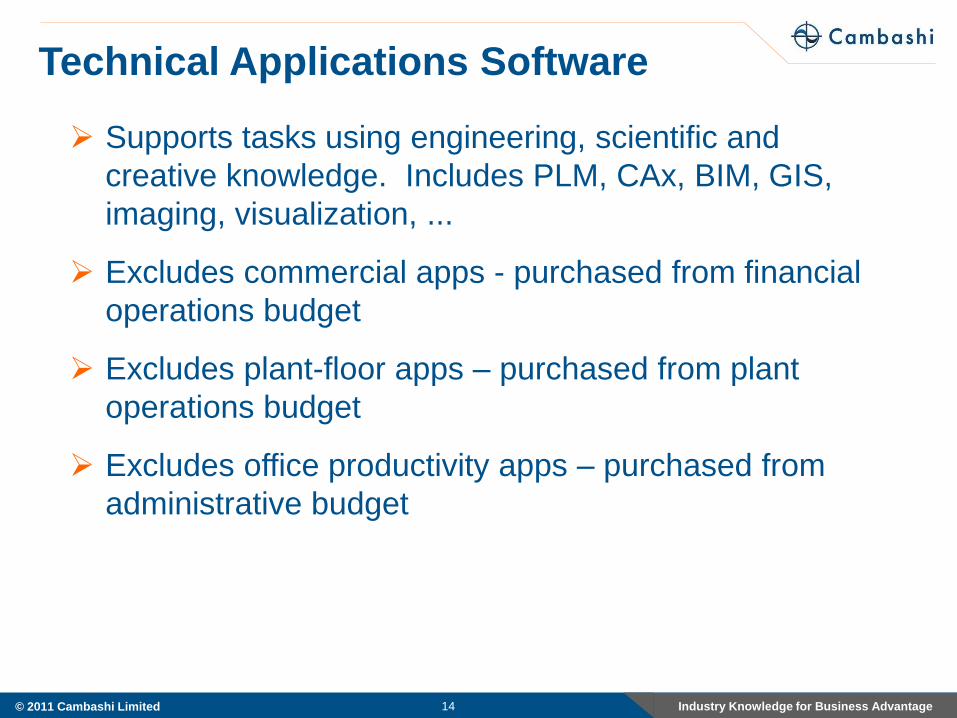

Supports tasks using engineering, scientific and

creative knowledge. Includes PLM, CAx, BIM, GIS,

imaging, visualization, ...

Excludes commercial apps - purchased from financial

operations budget

Excludes plant-floor apps – purchased from plant

operations budget

Excludes office productivity apps – purchased from

administrative budget

Technical Applications Software

14

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

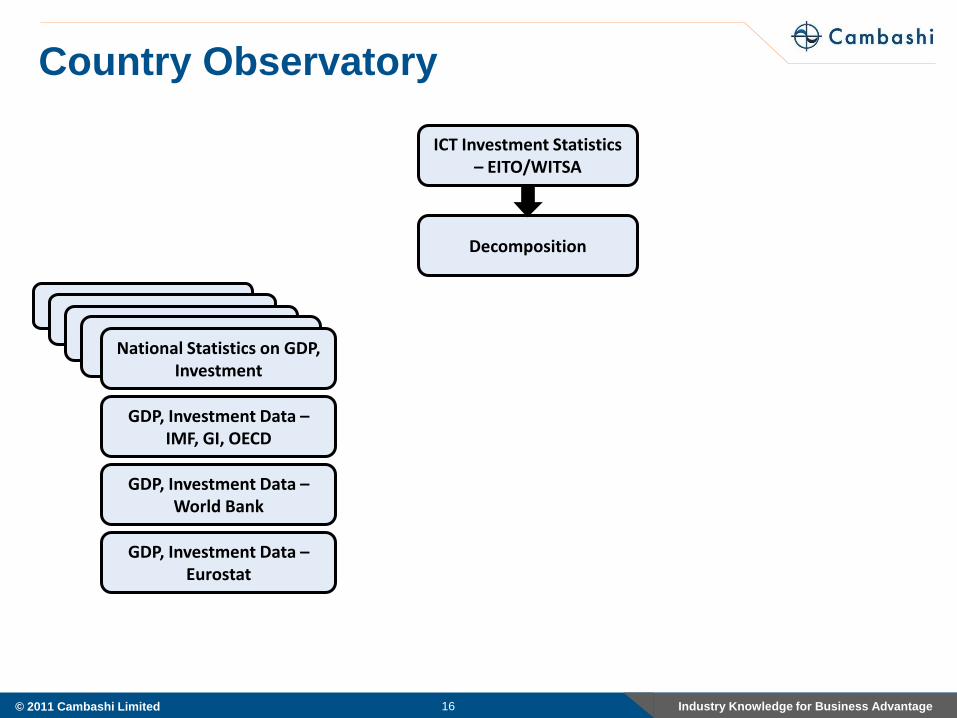

Country Observatory

Product Observatory

Industry Observatory

Employment Observatory

Cambashi’s 4 Views of the Market

15

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Country Observatory

GDP, Investment Data –IMF, GI, OECD

16

National Statistics on GDP, Investment

GDP, Investment Data –World Bank

GDP, Investment Data –Eurostat

ICT Investment Statistics – EITO/WITSA

Decomposition

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

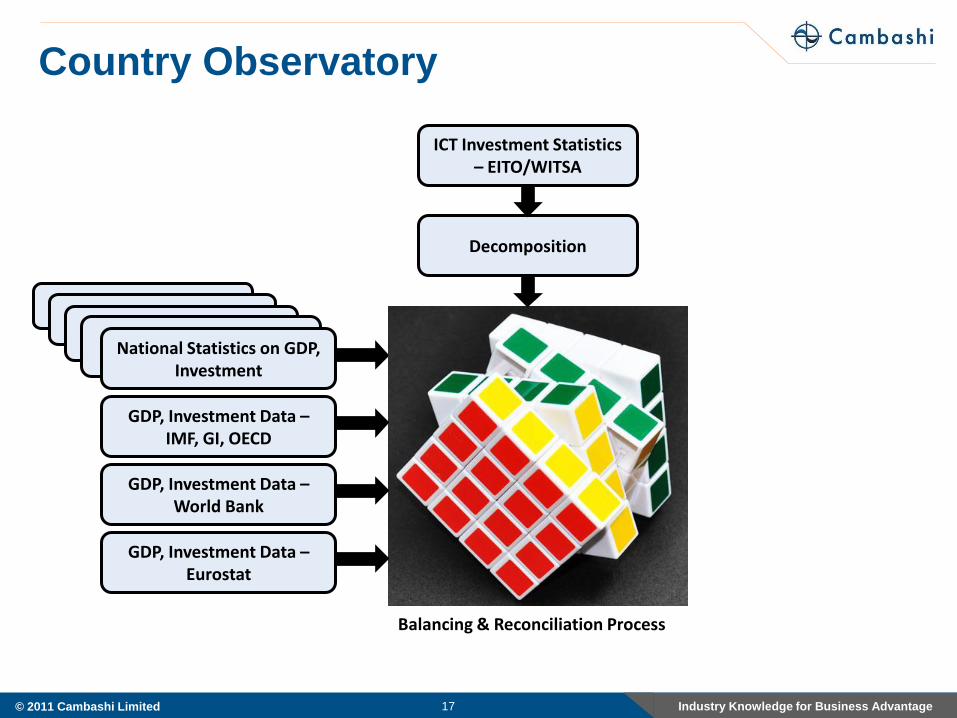

Country Observatory

GDP, Investment Data –IMF, GI, OECD

17

National Statistics on GDP, Investment

GDP, Investment Data –World Bank

GDP, Investment Data –Eurostat

ICT Investment Statistics – EITO/WITSA

Decomposition

Balancing & Reconciliation Process

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

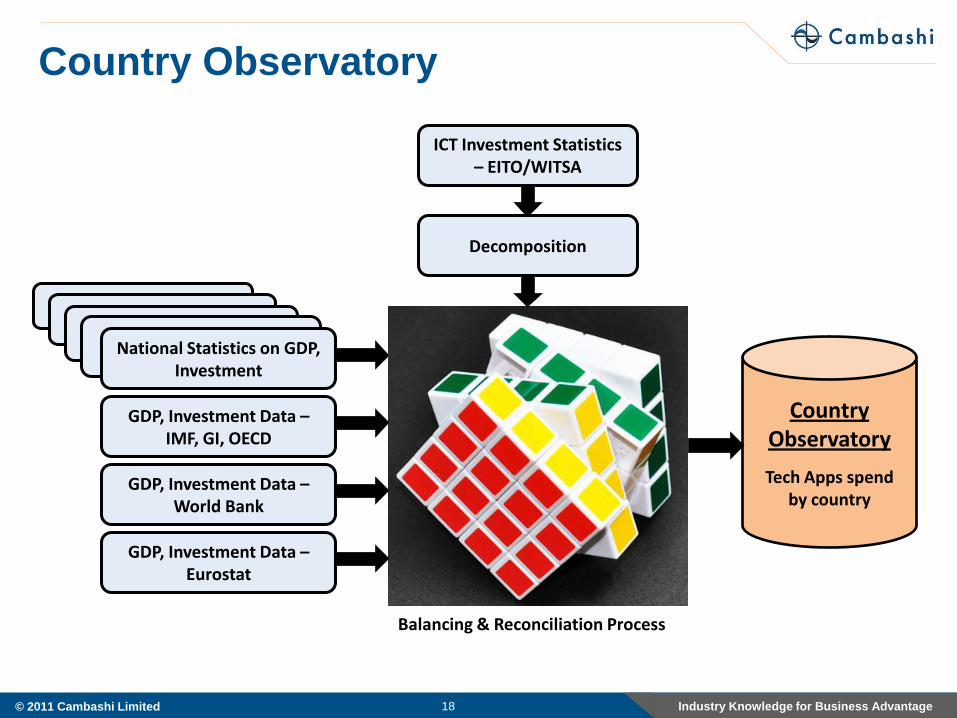

Country Observatory

GDP, Investment Data –IMF, GI, OECD

18

National Statistics on GDP, Investment

GDP, Investment Data –World Bank

GDP, Investment Data –Eurostat

ICT Investment Statistics – EITO/WITSA

Decomposition

Balancing & Reconciliation Process

Country Observatory

Tech Apps spendby country

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

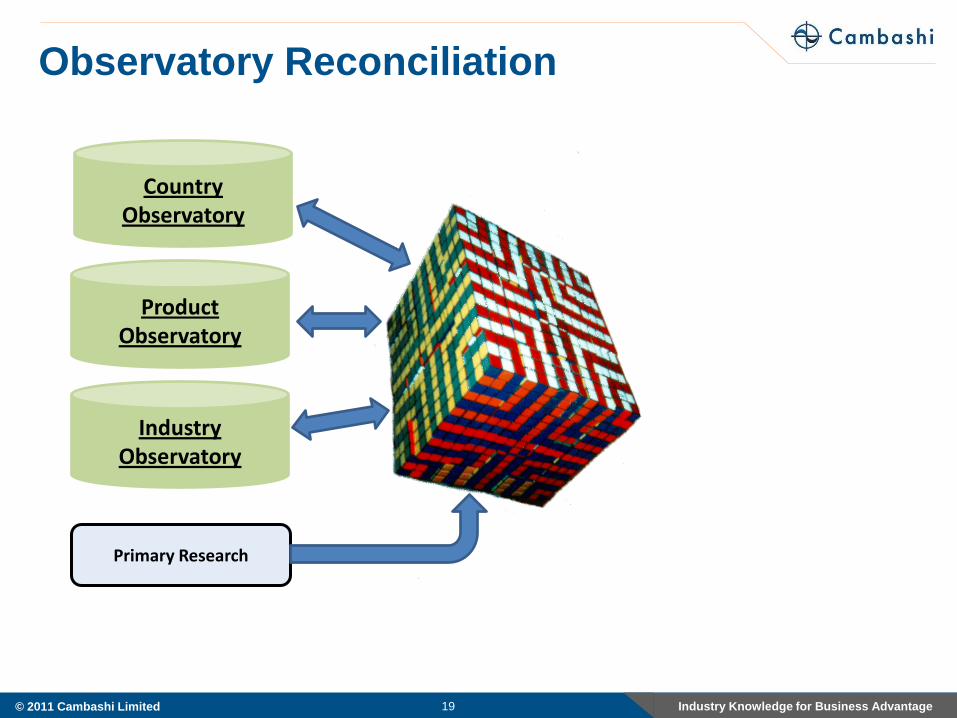

Observatory Reconciliation

Country Observatory

19

Product Observatory

Industry Observatory

Primary Research

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

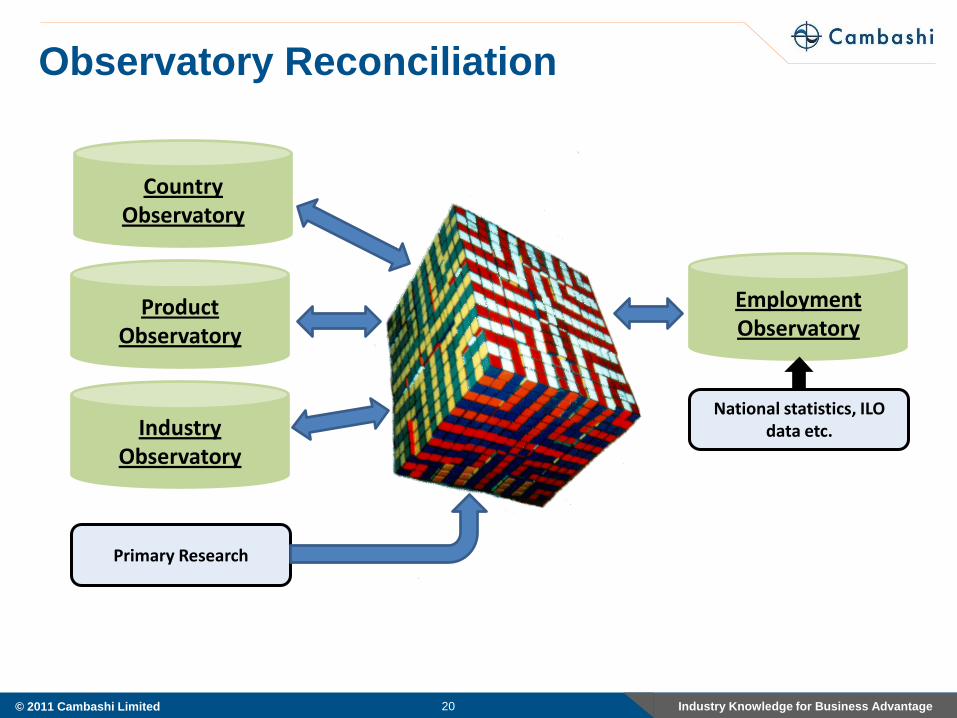

Observatory Reconciliation

Country Observatory

20

Product Observatory

Industry Observatory

Primary Research

Employment Observatory

National statistics, ILO data etc.

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

21

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

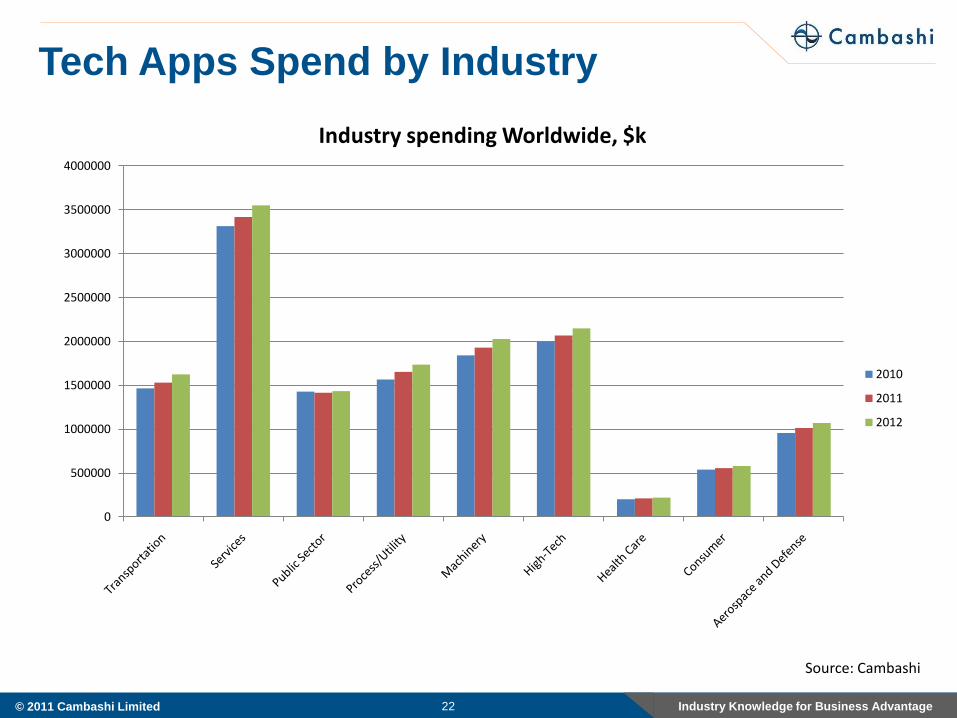

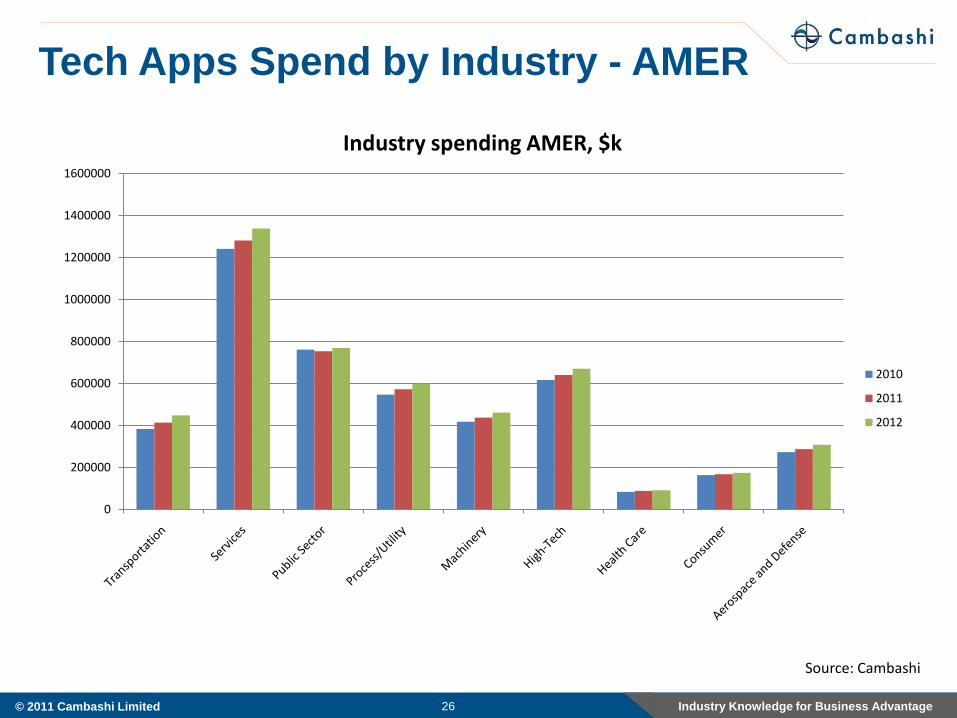

Tech Apps Spend by Industry

22

Source: Cambashi

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Industry spending Worldwide, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

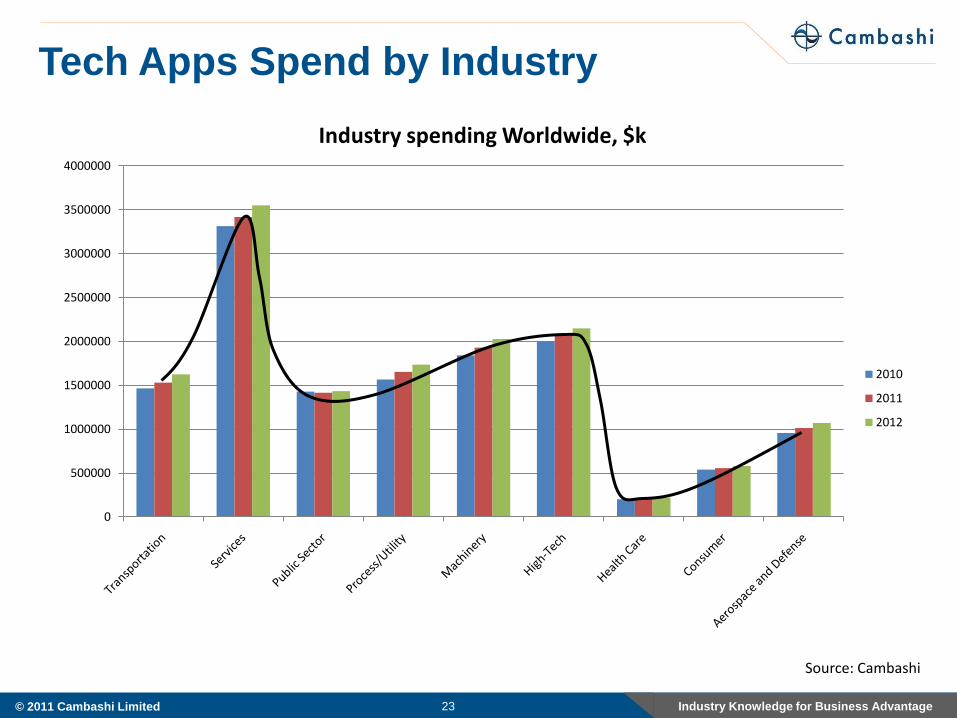

Tech Apps Spend by Industry

23

Source: Cambashi

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

Industry spending Worldwide, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

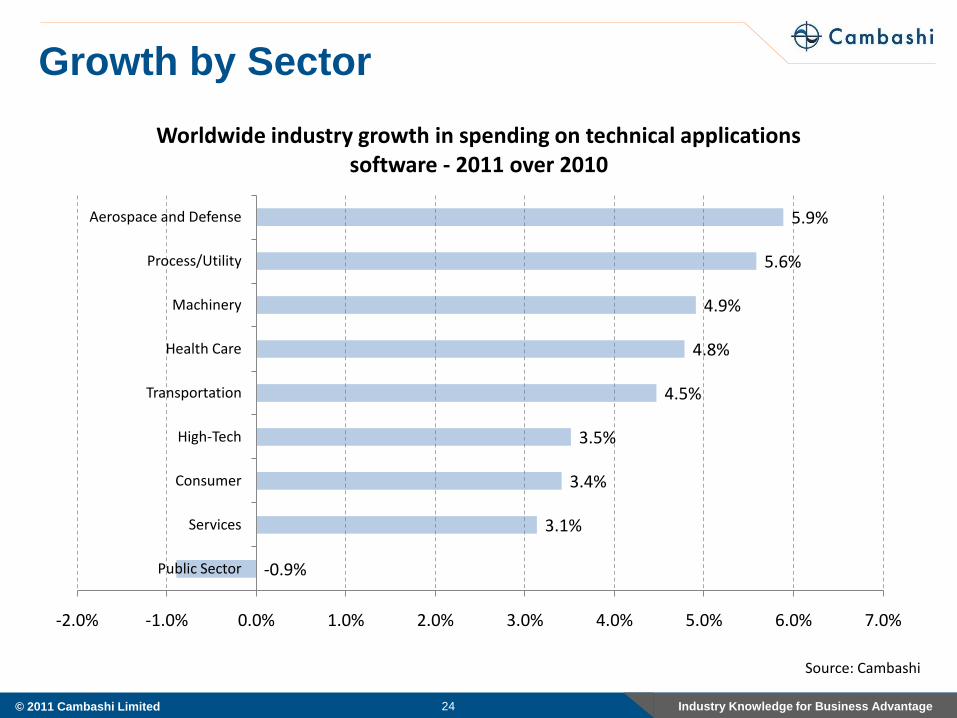

Growth by Sector

24

-0.9%

3.1%

3.4%

3.5%

4.5%

4.8%

4.9%

5.6%

5.9%

-2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0%

Public Sector

Services

Consumer

High-Tech

Transportation

Health Care

Machinery

Process/Utility

Aerospace and Defense

Worldwide industry growth in spending on technical applications software - 2011 over 2010

Source: Cambashi

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

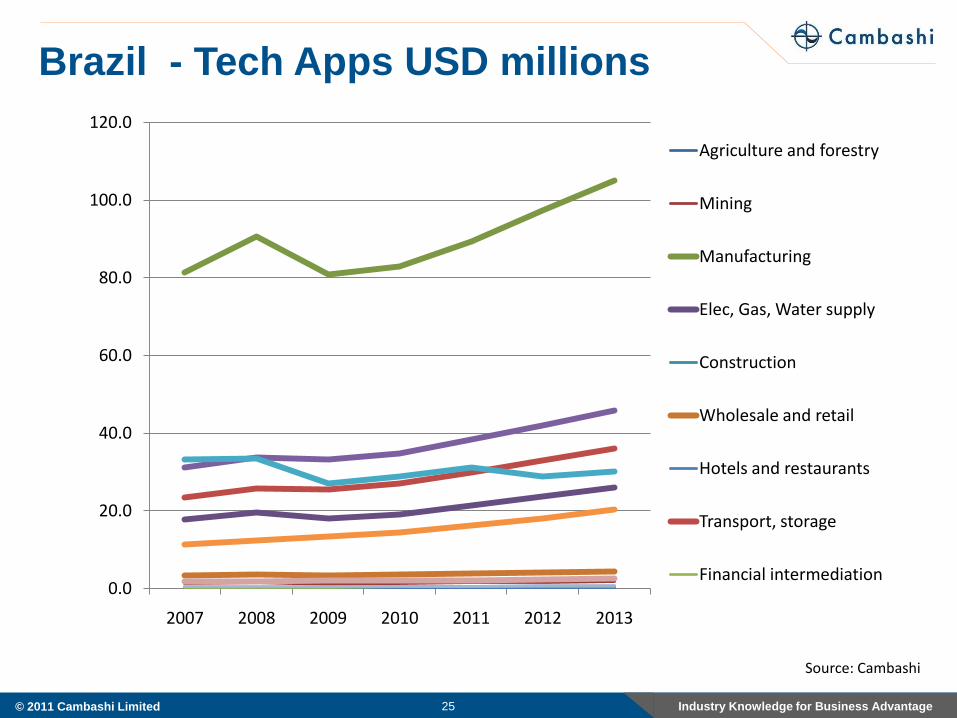

Brazil - Tech Apps USD millions

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2007 2008 2009 2010 2011 2012 2013

Agriculture and forestry

Mining

Manufacturing

Elec, Gas, Water supply

Construction

Wholesale and retail

Hotels and restaurants

Transport, storage

Financial intermediation

25

Source: Cambashi

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 26

Source: Cambashi

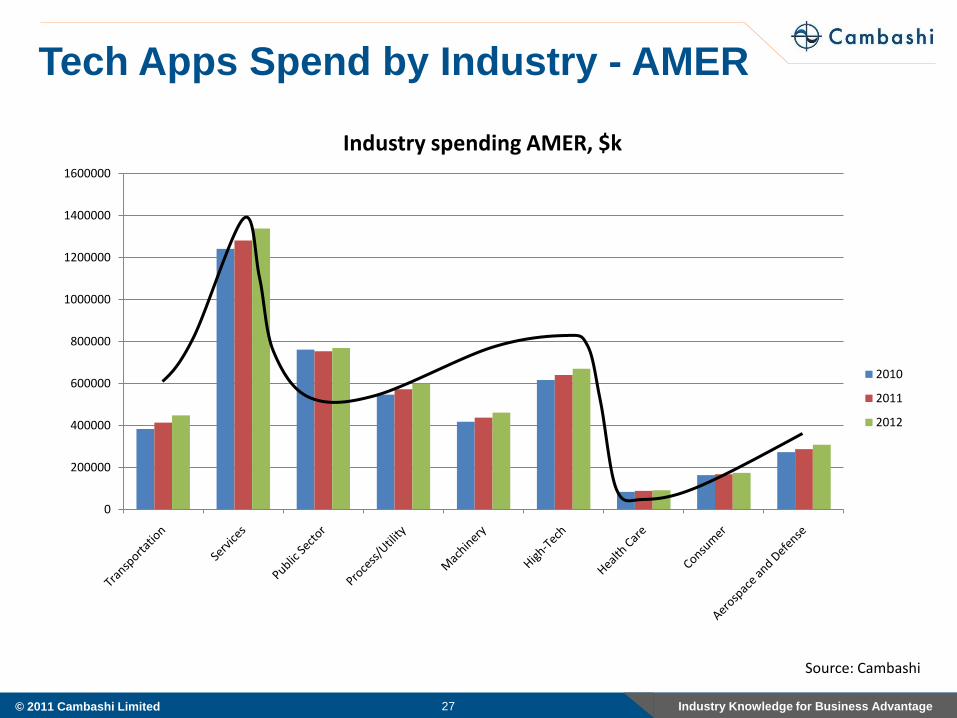

Tech Apps Spend by Industry - AMER

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Industry spending AMER, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 27

Source: Cambashi

Tech Apps Spend by Industry - AMER

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

Industry spending AMER, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 28

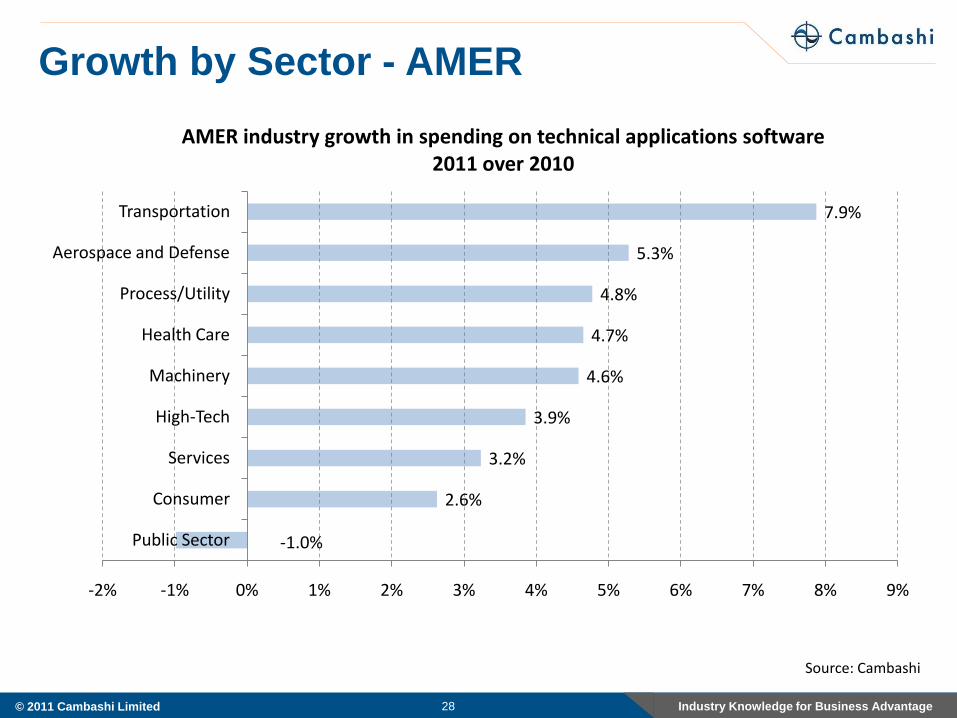

-1.0%

2.6%

3.2%

3.9%

4.6%

4.7%

4.8%

5.3%

7.9%

-2% -1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Public Sector

Consumer

Services

High-Tech

Machinery

Health Care

Process/Utility

Aerospace and Defense

Transportation

AMER industry growth in spending on technical applications software2011 over 2010

Growth by Sector - AMER

Source: Cambashi

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 29

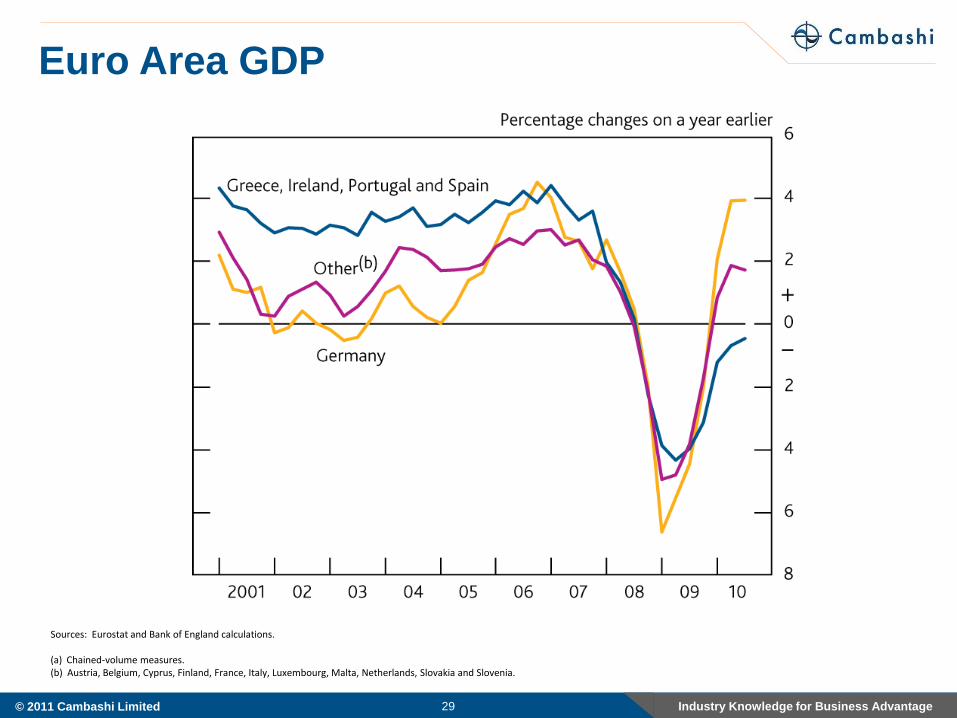

Sources: Eurostat and Bank of England calculations.

(a) Chained-volume measures.(b) Austria, Belgium, Cyprus, Finland, France, Italy, Luxembourg, Malta, Netherlands, Slovakia and Slovenia.

Euro Area GDP

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

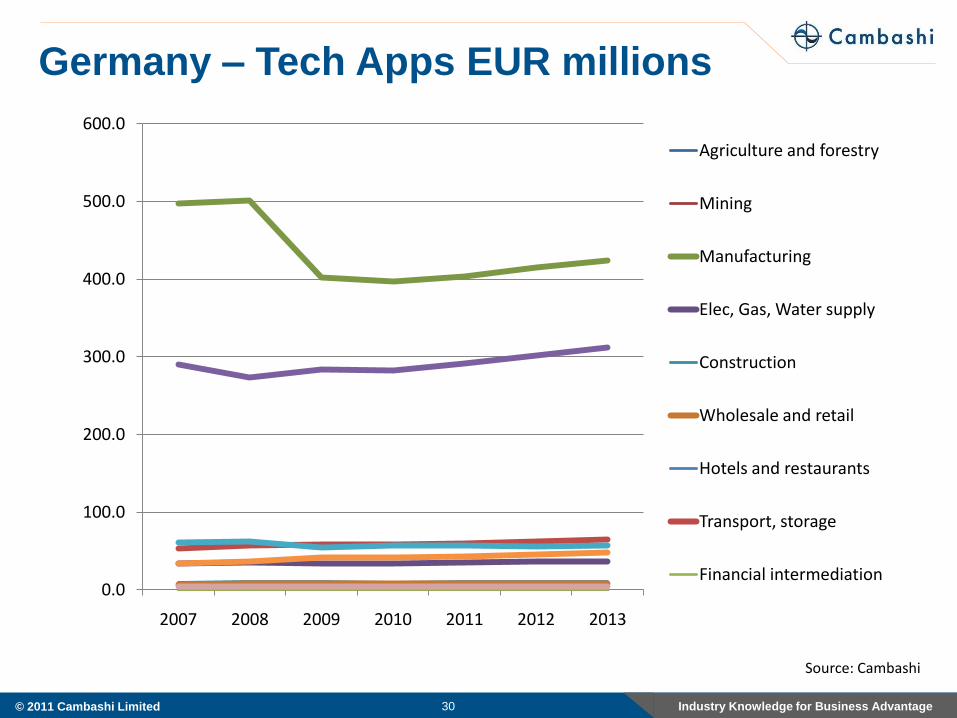

Germany – Tech Apps EUR millions

0.0

100.0

200.0

300.0

400.0

500.0

600.0

2007 2008 2009 2010 2011 2012 2013

Agriculture and forestry

Mining

Manufacturing

Elec, Gas, Water supply

Construction

Wholesale and retail

Hotels and restaurants

Transport, storage

Financial intermediation

30

Source: Cambashi

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

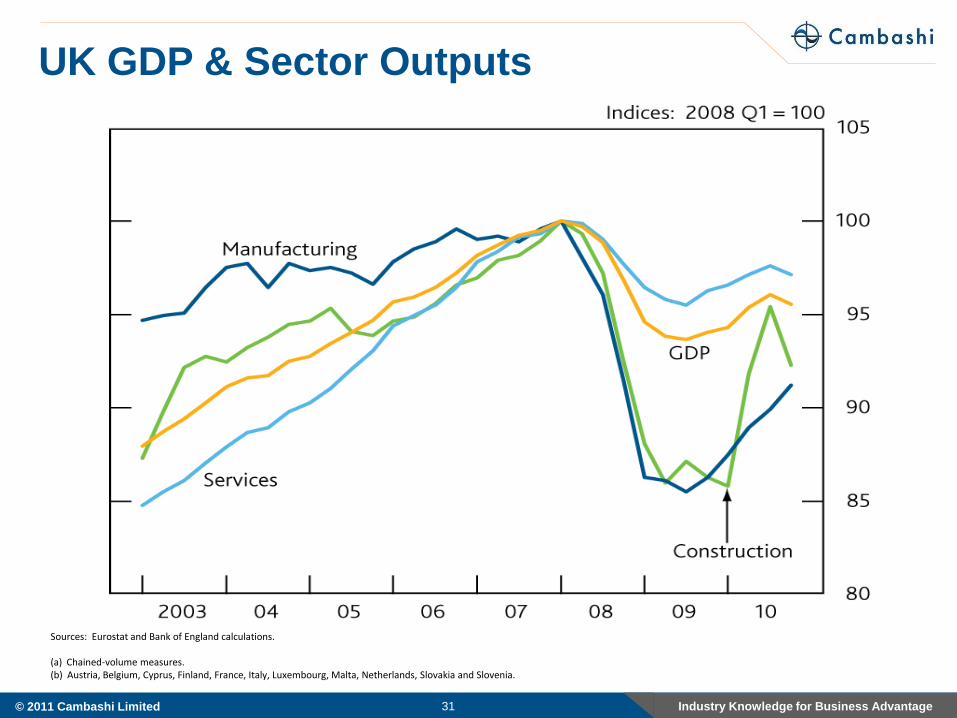

UK GDP & Sector Outputs

31

Sources: Eurostat and Bank of England calculations.

(a) Chained-volume measures.(b) Austria, Belgium, Cyprus, Finland, France, Italy, Luxembourg, Malta, Netherlands, Slovakia and Slovenia.

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

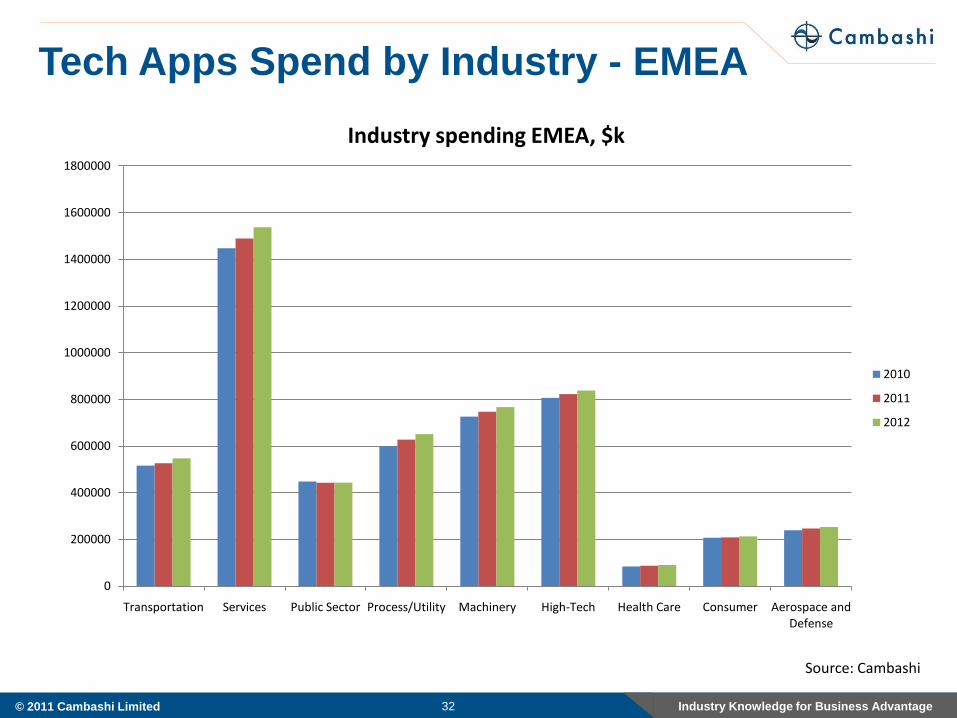

Tech Apps Spend by Industry - EMEA

32

Source: Cambashi

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

Transportation Services Public Sector Process/Utility Machinery High-Tech Health Care Consumer Aerospace and Defense

Industry spending EMEA, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

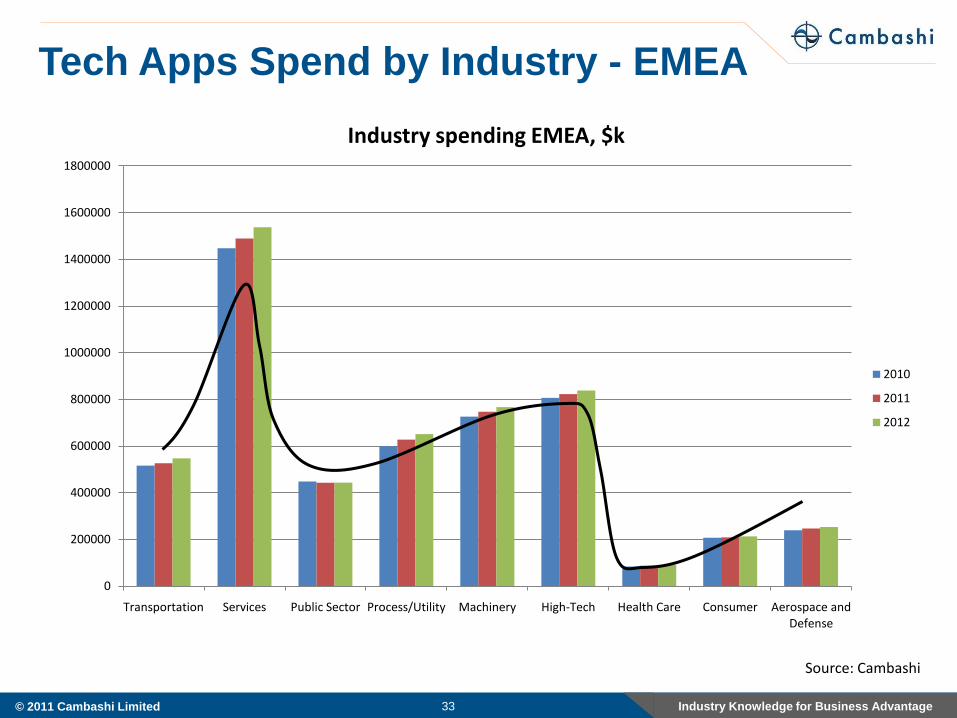

Tech Apps Spend by Industry - EMEA

33

Source: Cambashi

0

200000

400000

600000

800000

1000000

1200000

1400000

1600000

1800000

Transportation Services Public Sector Process/Utility Machinery High-Tech Health Care Consumer Aerospace and Defense

Industry spending EMEA, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

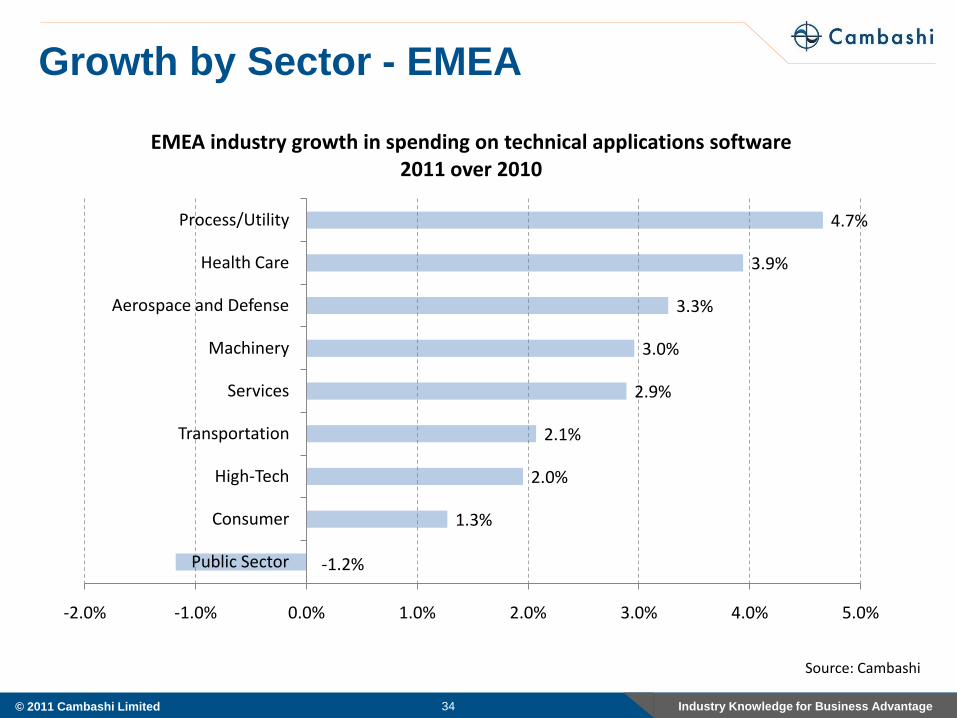

Growth by Sector - EMEA

34

-1.2%

1.3%

2.0%

2.1%

2.9%

3.0%

3.3%

3.9%

4.7%

-2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0% 5.0%

Public Sector

Consumer

High-Tech

Transportation

Services

Machinery

Aerospace and Defense

Health Care

Process/Utility

EMEA industry growth in spending on technical applications software2011 over 2010

Source: Cambashi

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

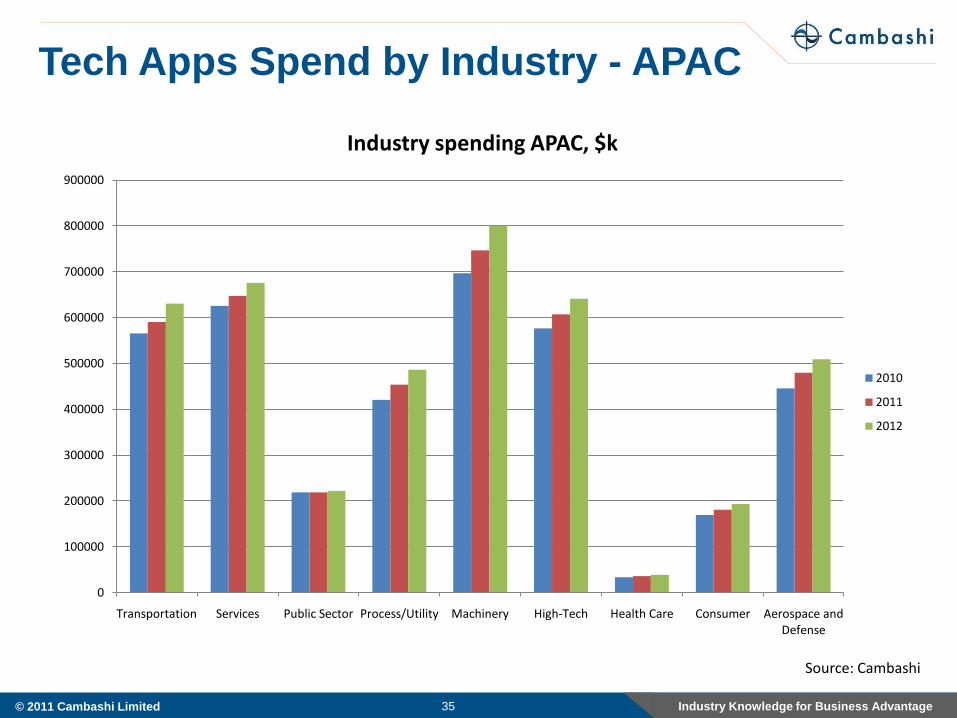

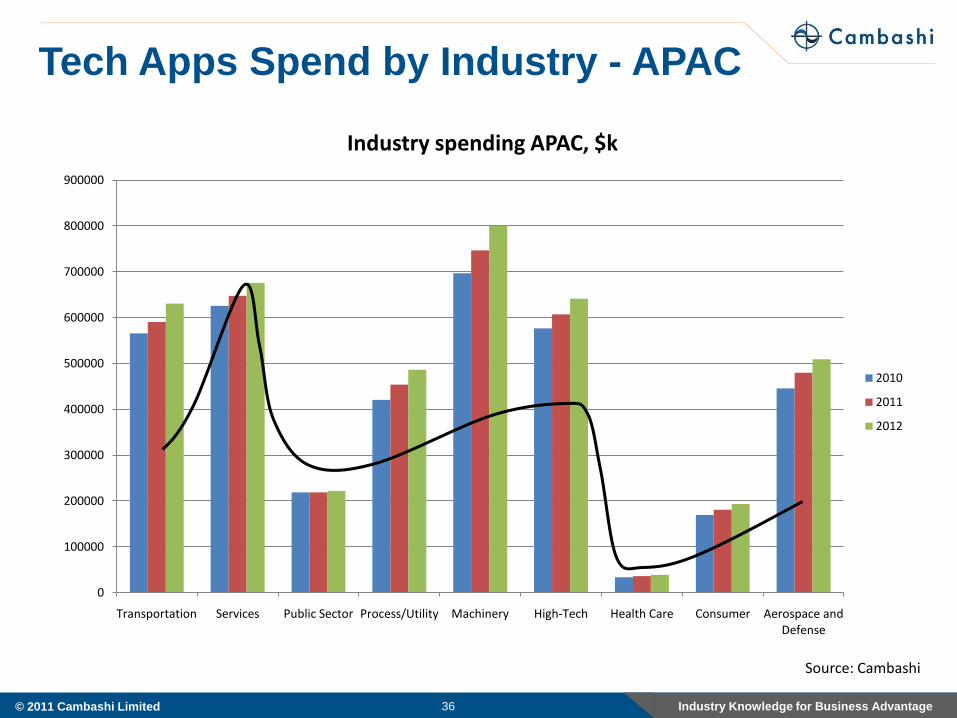

Tech Apps Spend by Industry - APAC

35

Source: Cambashi

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

Transportation Services Public Sector Process/Utility Machinery High-Tech Health Care Consumer Aerospace and Defense

Industry spending APAC, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Tech Apps Spend by Industry - APAC

36

Source: Cambashi

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

Transportation Services Public Sector Process/Utility Machinery High-Tech Health Care Consumer Aerospace and Defense

Industry spending APAC, $k

2010

2011

2012

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

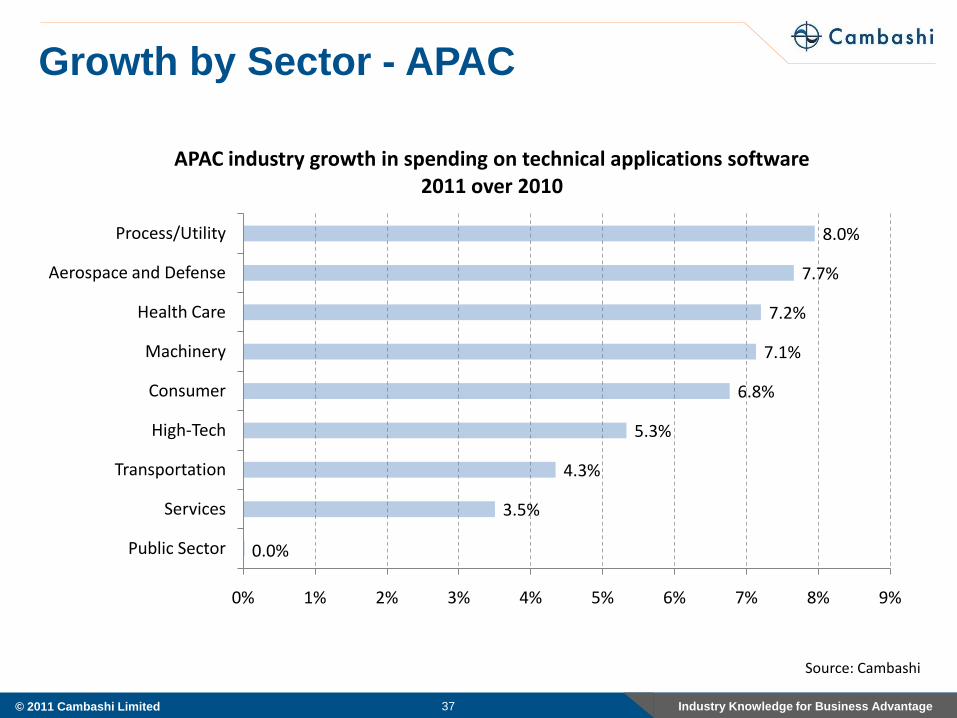

Growth by Sector - APAC

37

0.0%

3.5%

4.3%

5.3%

6.8%

7.1%

7.2%

7.7%

8.0%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

Public Sector

Services

Transportation

High-Tech

Consumer

Machinery

Health Care

Aerospace and Defense

Process/Utility

APAC industry growth in spending on technical applications software2011 over 2010

Source: Cambashi

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

38

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

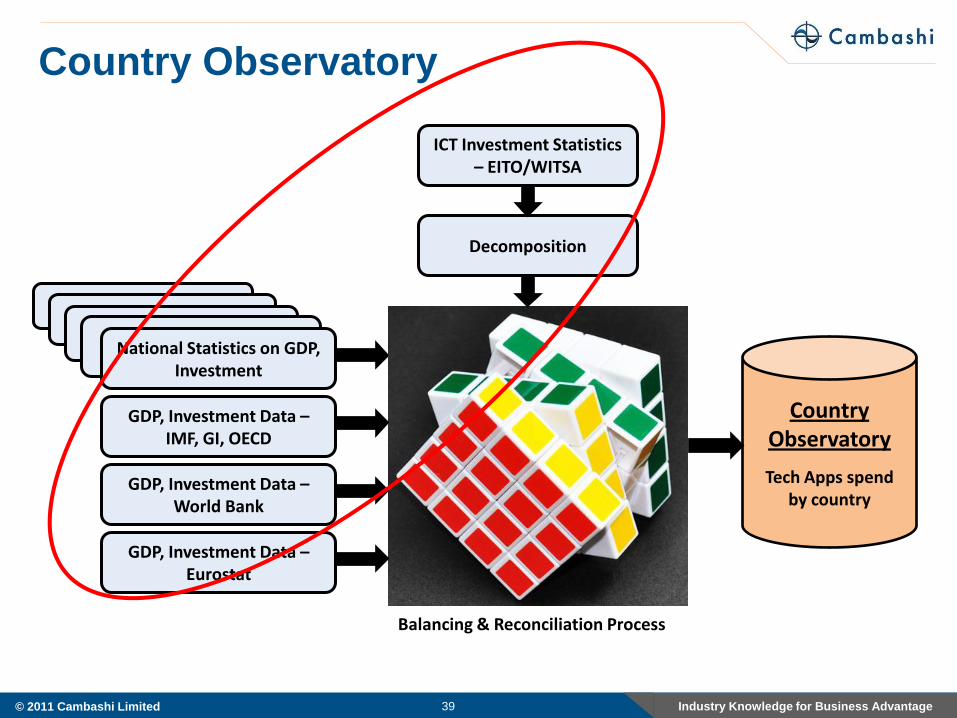

Country Observatory

Balancing & Reconciliation Process

GDP, Investment Data –IMF, GI, OECD

39

National Statistics on GDP, Investment

GDP, Investment Data –World Bank

GDP, Investment Data –Eurostat

ICT Investment Statistics – EITO/WITSA

Decomposition

Country Observatory

Tech Apps spendby country

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

40

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

41

Financial System – Blinding with Complexity!

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

42

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

43

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

China – The Main Driver?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

44

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

China – The Main Driver?

Commodities – Who Will be Able to Afford Them?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

45

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

China – The Main Driver?

Commodities – Who Will be Able to Afford Them?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

How did we get here?

46

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

How did we get here?

47

Failure of regulation

Securitization

The scale of the problem

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

How did we get here?

48

Mortgage

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

How did we get here?

49

Mortgage

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

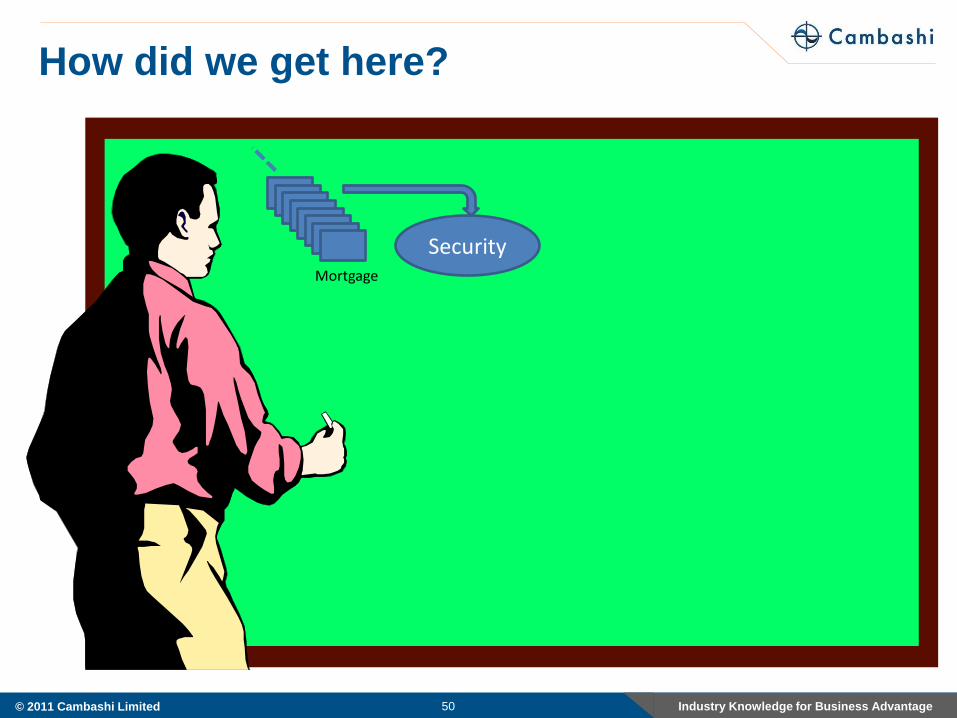

How did we get here?

50

Mortgage

Security

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

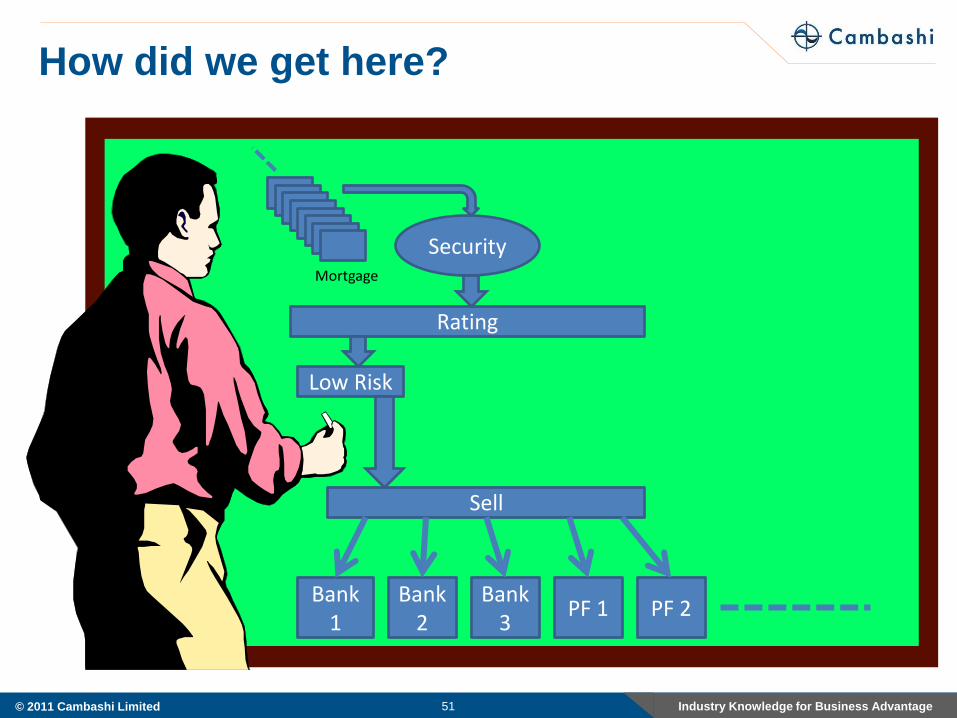

How did we get here?

51

Mortgage

Security

Sell

Bank 1

Bank 2

Bank 3

PF 1 PF 2

Rating

Low Risk

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

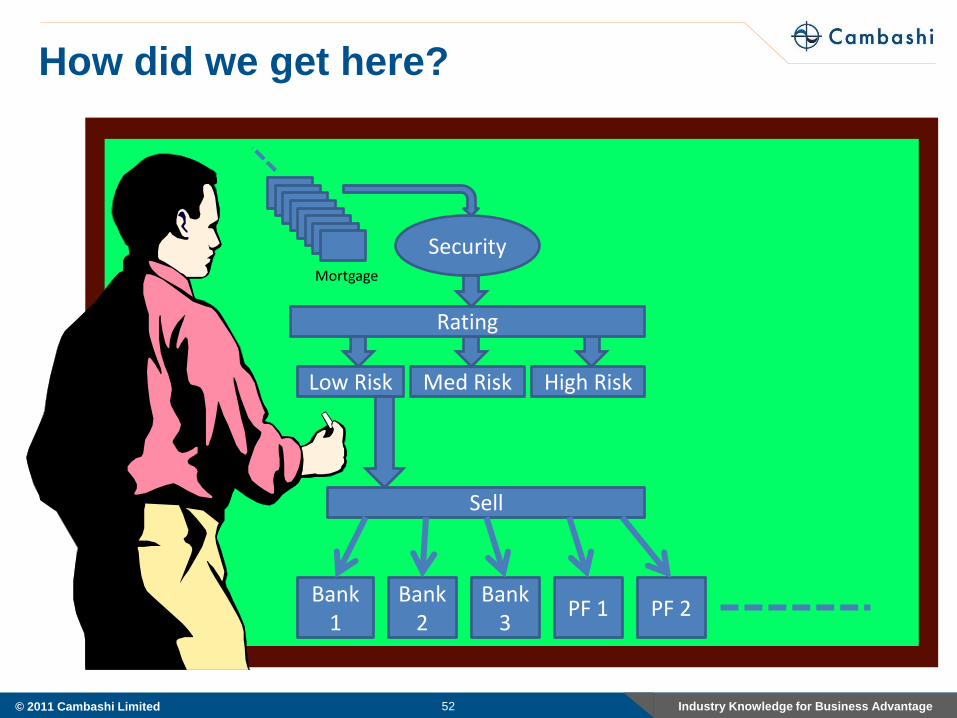

How did we get here?

52

Mortgage

Security

Med Risk High Risk

Sell

Bank 1

Bank 2

Bank 3

PF 1 PF 2

Rating

Low Risk

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

How did we get here?

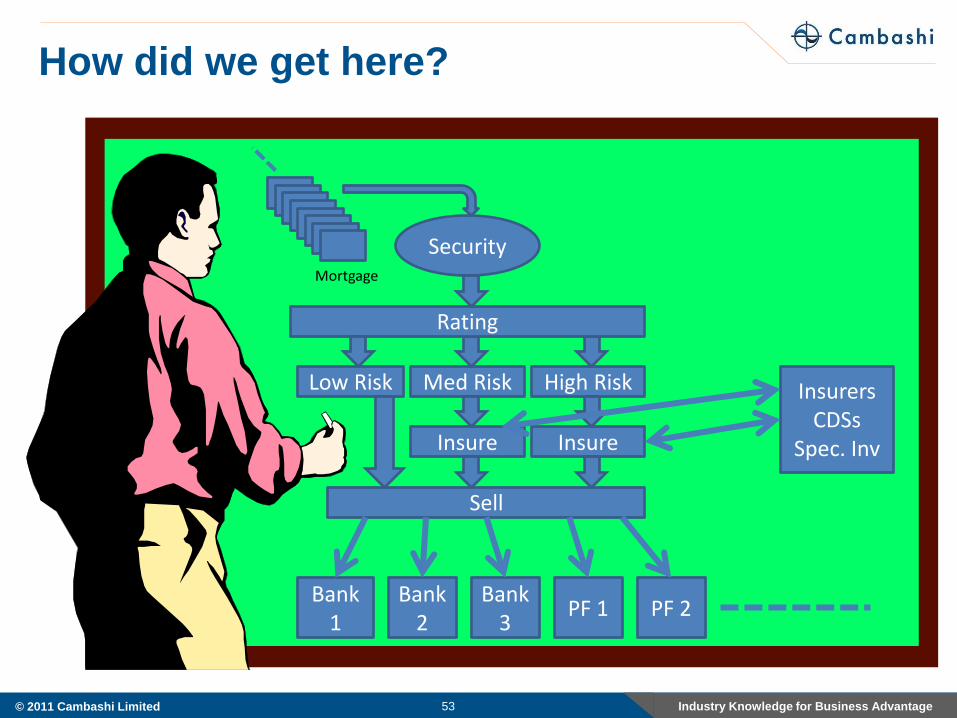

53

Mortgage

Security

Med Risk High Risk

Insure Insure

InsurersCDSs

Spec. Inv

Sell

Bank 1

Bank 2

Bank 3

PF 1 PF 2

Rating

Low Risk

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

How did we get here?

54

Mortgage

Security

Med Risk High Risk

Insure Insure

InsurersCDSs

Spec. Inv

Sell

Bank 1

Bank 2

Bank 3

PF 1 PF 2

Rating

Low Risk

Sell

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

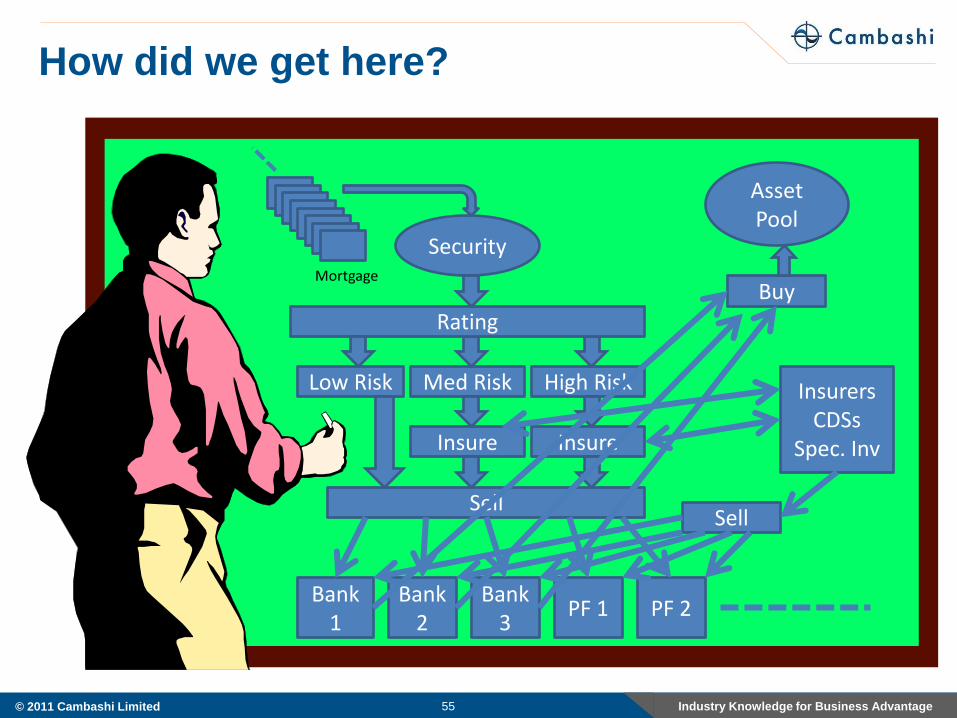

How did we get here?

55

Mortgage

Security

Med Risk High Risk

Insure Insure

InsurersCDSs

Spec. Inv

Sell

Bank 1

Bank 2

Bank 3

PF 1 PF 2

Rating

Low Risk

Sell

Asset Pool

Buy

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

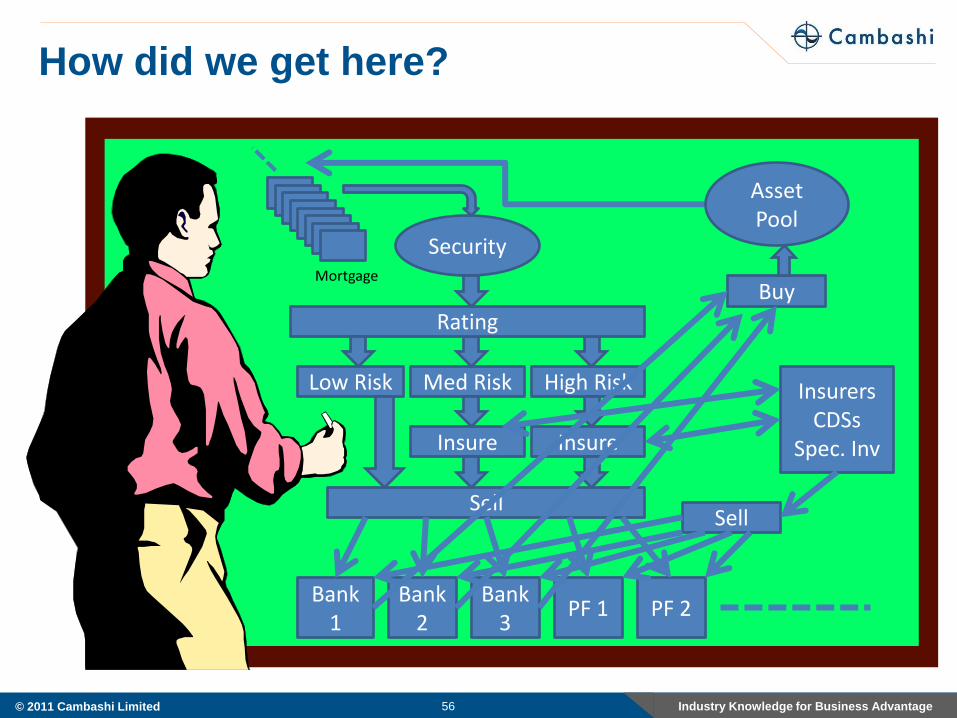

How did we get here?

56

Mortgage

Security

Med Risk High Risk

Insure Insure

InsurersCDSs

Spec. Inv

Sell

Bank 1

Bank 2

Bank 3

PF 1 PF 2

Rating

Low Risk

Sell

Asset Pool

Buy

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Current situation

57

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Current situation

58

Mark to Model

Stress Tests

Locating „assets‟

Valuation

Reform

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

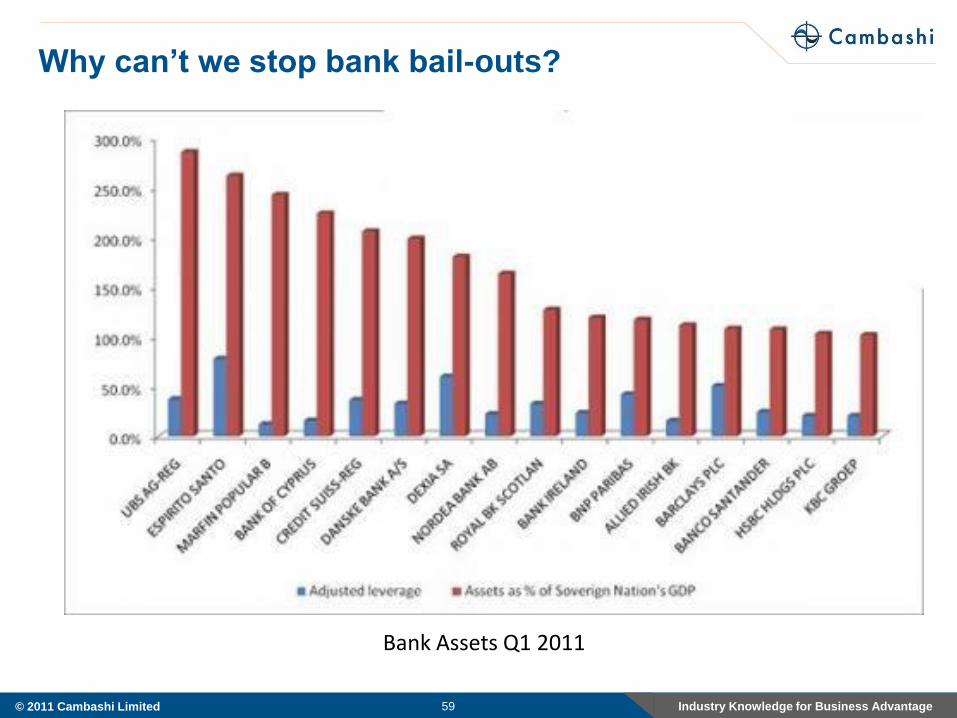

Why can’t we stop bank bail-outs?

59

Bank Assets Q1 2011

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 60

Progress on Bank Lending

Banking Innovations for 2011 – The 5-Minute Loan

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

61

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

China – The Main Driver?

Commodities – Who Will be Able to Afford Them?

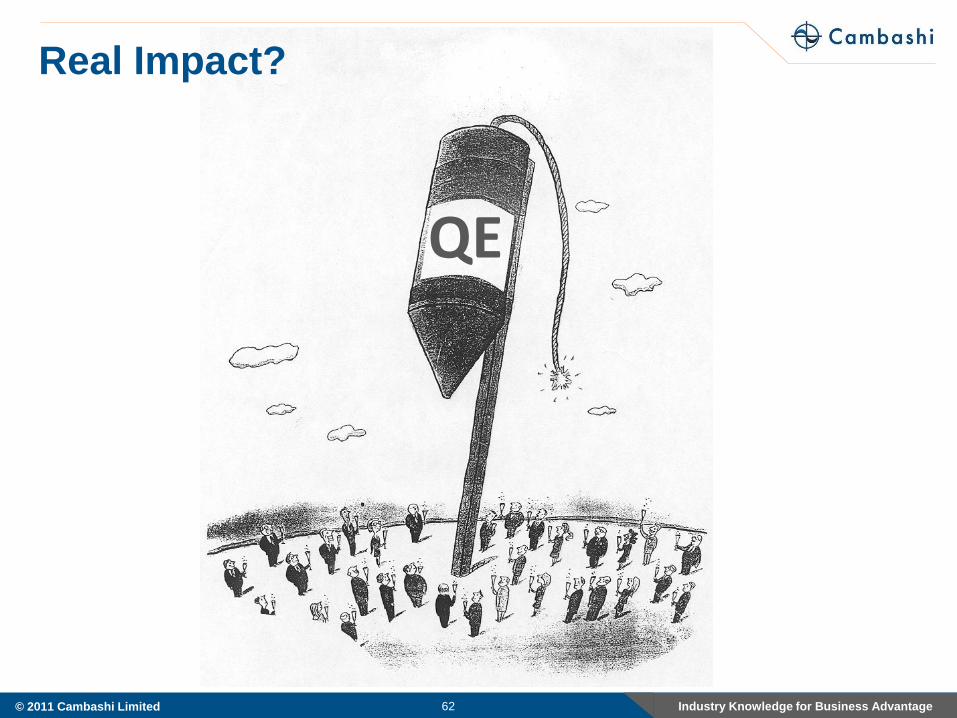

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 62

QE

Real Impact?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

The Options

63

Forget austerity, we must continue to stimulate the economy – more QE!

It’s essential to address our deficits now

What the economic experts say:

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

The Options

64

Forget austerity, we must continue to stimulate the economy – more QE!

It’s essential to address our deficits now

Sovereign Debt

Inflation/deflation

What the economic experts say:

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

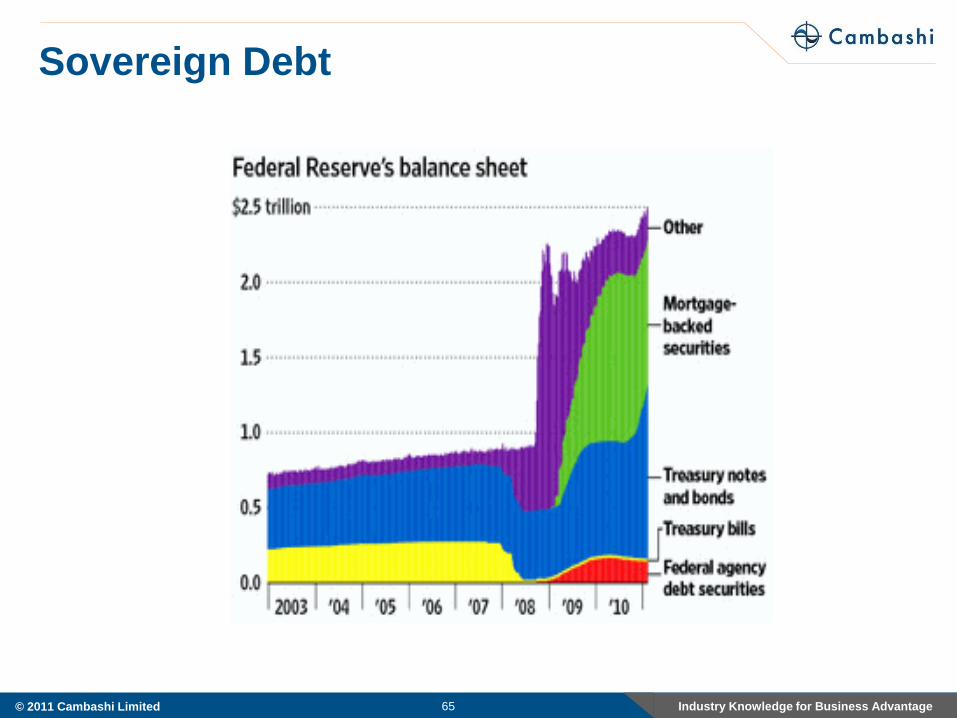

Sovereign Debt

65

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

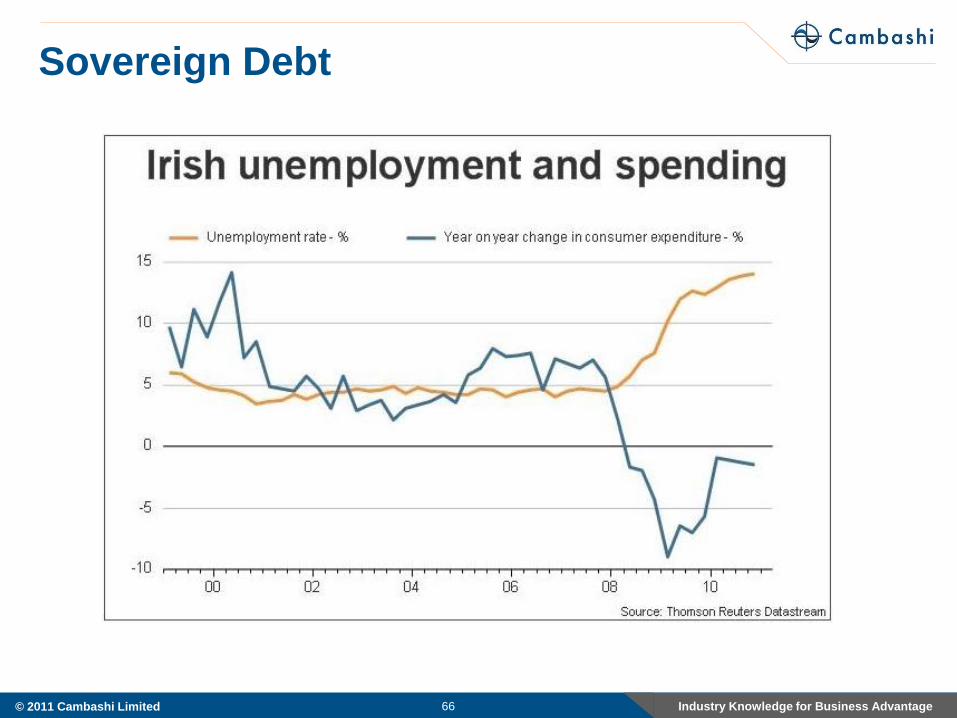

Sovereign Debt

66

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

67

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

China – The Main Driver?

Commodities – Who Will be Able to Afford Them?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

China’s Economy

68

2010 gross domestic product (GDP) growth 10%;

2011 est. 8.7%

50-year "Go West" campaign

Auto sales in China 20 million in 2011 (Booz & Co)

Some recent evidence of over-inventory?

Record month

Inflation?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

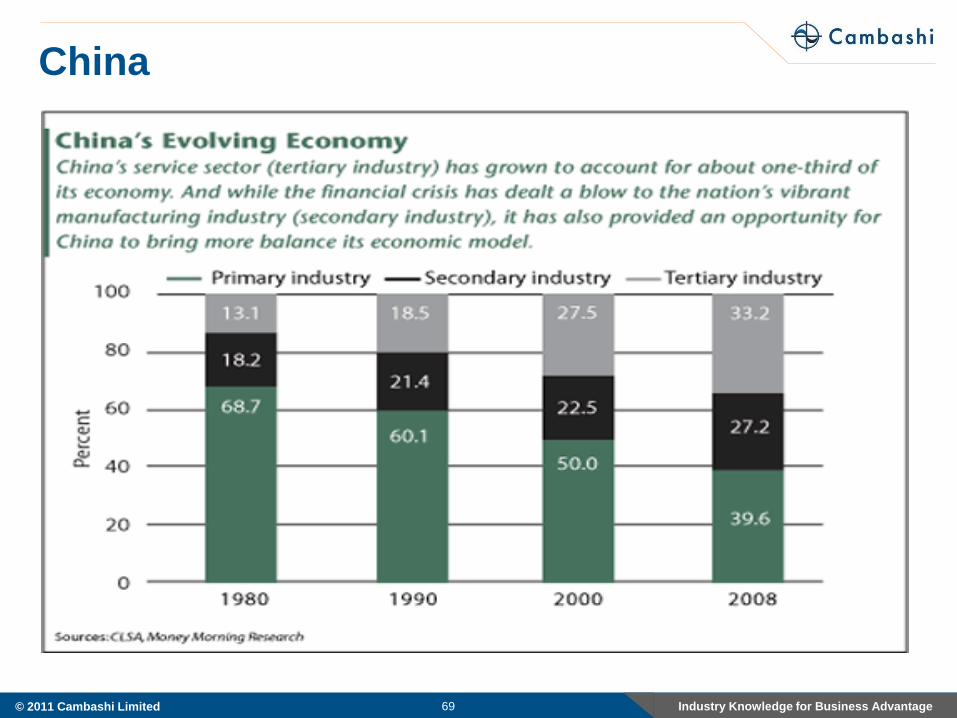

China

69

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Global Economy – Reasons to be Cautious

70

Financial System – Blinding with Complexity!

Stimulus Measures – Unintended Consequences?

China – The Main Driver?

Commodities – Who Will be Able to Afford Them?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Oil

71

We can bring the oil price under control by simply producing more

We are past Peak Oil; OPEC doesn’t have any more

What the economic experts say:

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Oil

72

We can bring the oil price under control by simply producing more

We are past Peak Oil; OPEC doesn’t have any more

What the economic experts say:

Supply and Demand

Role of Speculation

EROI

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

73

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Western governments and CBs must adopt a realistic

view of pace of recovery and the balance of the

economy

Nature of GDP; consumer-driven GDP growth?

Challenges for Growth

74

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

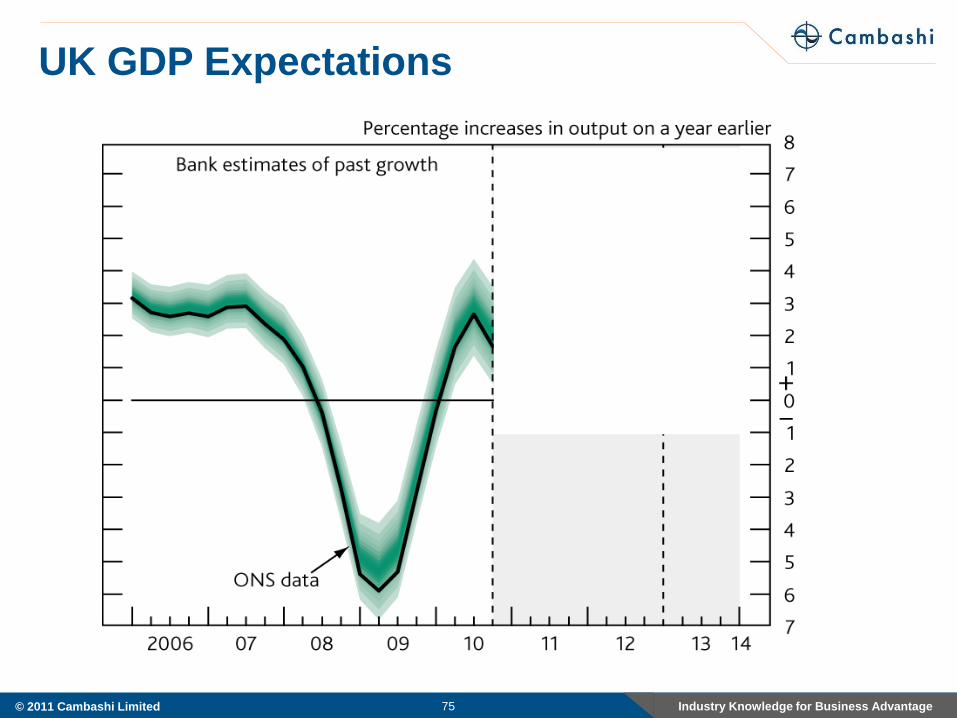

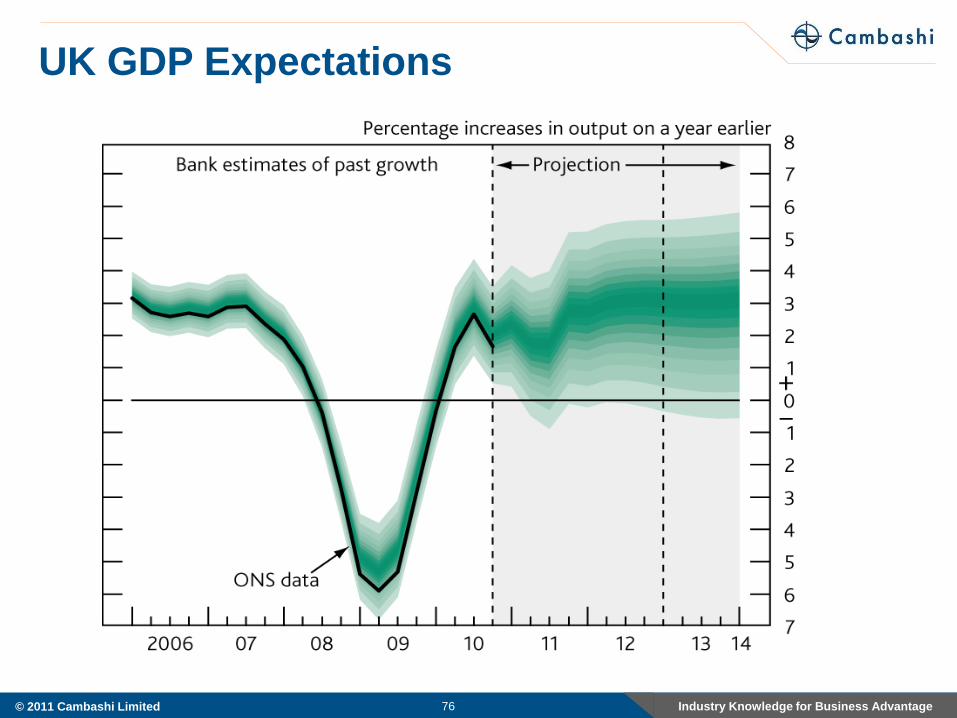

UK GDP Expectations

75

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

UK GDP Expectations

76

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

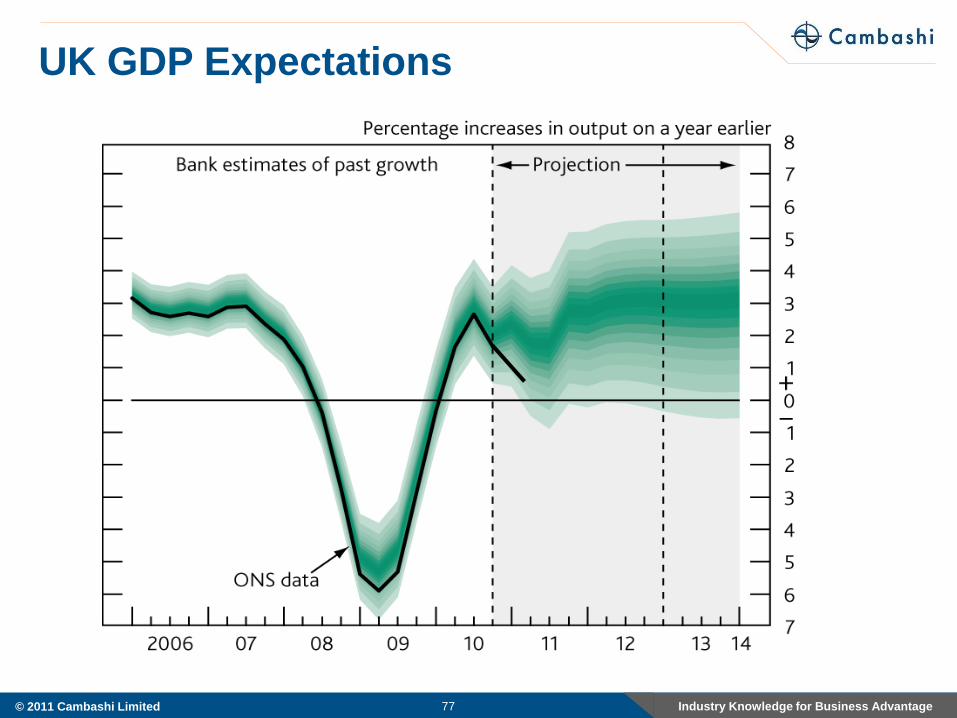

UK GDP Expectations

77

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Western governments and CBs must adopt a realistic view of pace of recovery and the balance of the economy

Nature of GDP; consumer-driven GDP growth?

Jobless recovery?

Demographic and affordability problem - was old out, young in, now it‟s old still there, young.....?

Dangers lurking in the financial system

Financialisation – TBTF, SIFI – banks are getting bigger!

Convergence

Challenges for Growth

78

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 79

Extreme Caution

Not at all sure what’s ahead

Challenges for manufacturers

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Challenges for manufacturers

Cost control

Quality

Reliable scheduling

Faster to market with innovative, competitive products

Efficient asset and resource usage

Global sourcing and sales

New competitors with new brand values

Share customer‟s project/risk

Responsive customization

Handle late changes

Be able to prove compliance

Plan for and manage more “real-time” parameters (price of power, ...)

80

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

BRIC and other emerging nations dominate?

BRIC provided half of world GDP growth between 2000 and

2008.

Not yet the balance of developed economies, but moving fast

How to develop long term sustainable manufacturing

capabilities?

How to exploit Engineering Software?

Tipping point?

81

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 82

Engineering Software

Key to future competitiveness or leveler (global

convergence) ?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

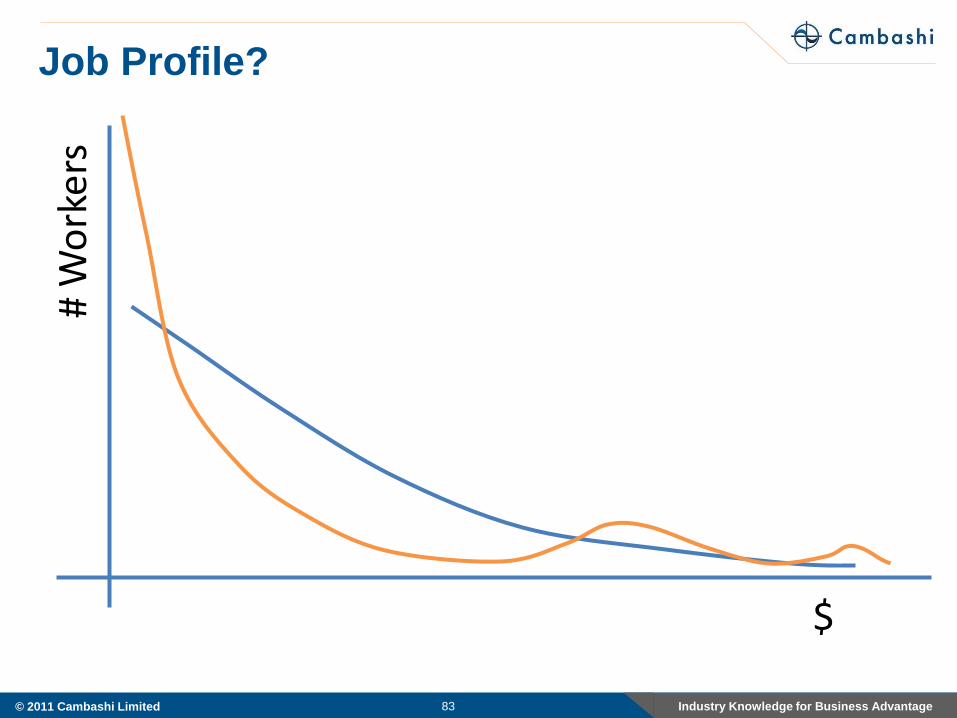

Job Profile?

83

$

# W

ork

ers

Industry Knowledge for Business Advantage© 2011 Cambashi Limited 84

Engineering Software

Key to future competitiveness or leveler – global

convergence ?

Can ES providers help manufacturers achieve a more beneficial balance?

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

International Business Update - Agenda

85

Introduction

Tracking The Technical Applications Software Market

What is the Market Looking Like?

The Wider Picture - Black Swan Spotting

Manufacturing Matters – More Than Ever

Summary

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Summary

86

In the near term Tech Apps market is fine, BUT

Further financial system crises are likely inevitable

Western governments MUST address the balance of

economy problem

Manufacturing is the only way to drive sustainable

growth

The way in which ES is exploited is key

Industry Knowledge for Business Advantage© 2011 Cambashi Limited

Thanks for listening

www.cambashi.com

+44 1223 460439

![Investors' Presentation - Q3FY 16 Business Update [Company Update]](https://img.pdfslide.us/doc/110x75/577ca5831a28abea748b9124/investors-presentation-q3fy-16-business-update-company-update.jpg)

![Investors' Presentation - Q2FY 16 Business Update [Company Update]](https://img.pdfslide.us/doc/110x75/577ca70d1a28abea748c2bc2/investors-presentation-q2fy-16-business-update-company-update.jpg)