Embed Size (px)

Citation preview

International Bar Association ConferenceReal Estate Investment TrustsPanel 2 - REIT formation

17 October 2007

Singapore9142562_1

2

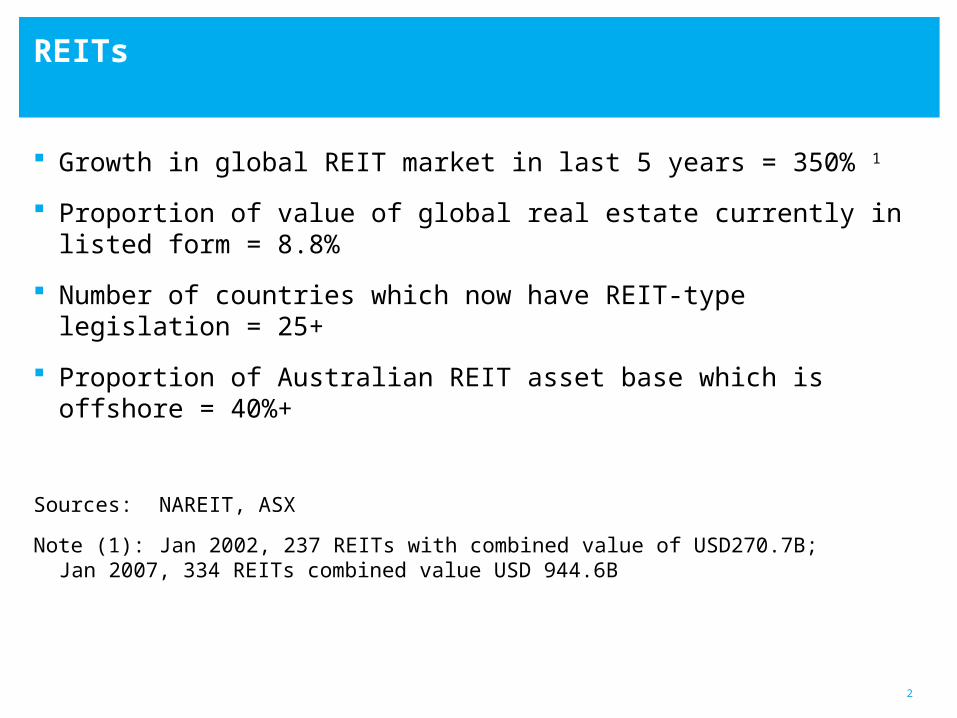

REITs

Growth in global REIT market in last 5 years = 350% 1

Proportion of value of global real estate currently in listed form = 8.8%

Number of countries which now have REIT-type legislation = 25+

Proportion of Australian REIT asset base which is offshore = 40%+

Sources: NAREIT, ASX

Note (1): Jan 2002, 237 REITs with combined value of USD270.7B;Jan 2007, 334 REITs combined value USD 944.6B

3

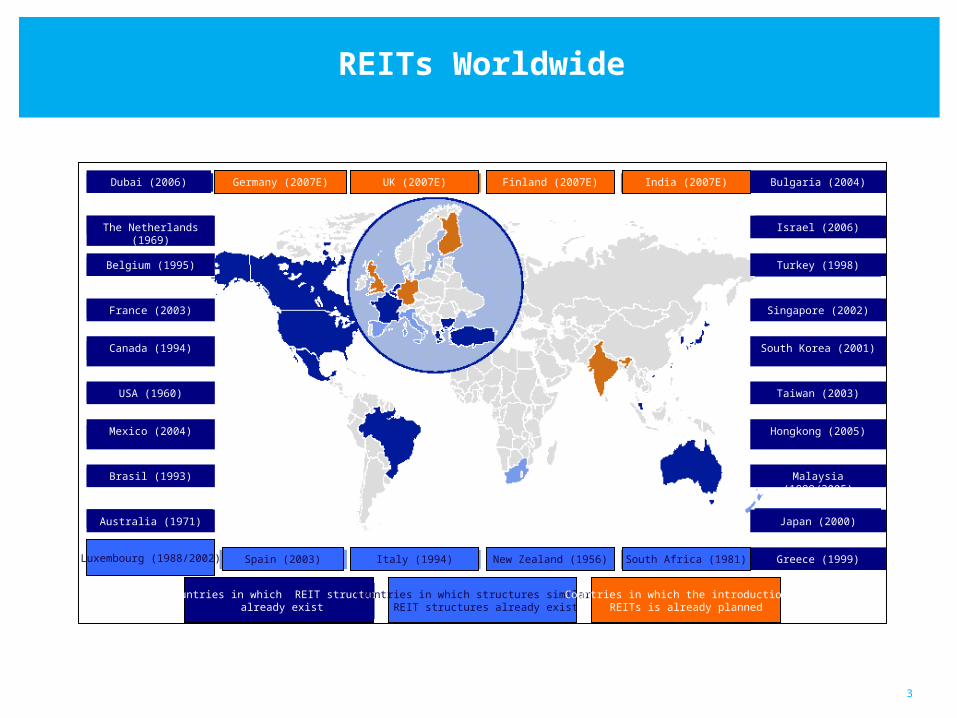

REITs Worldwide

Luxembourg (1988/2002)

Brasil (1993)

Australia (1971)

Mexico (2004)

USA (1960)

Canada (1994)

France (2003)

Belgium (1995)

The Netherlands (1969)

Germany (2007E)Dubai (2006) UK (2007E) Finland (2007E) India (2007E) Bulgaria (2004)

Israel (2006)

Turkey (1998)

Singapore (2002)

South Korea (2001)

Taiwan (2003)

Hongkong (2005)

Malaysia (1989/2005)

Japan (2000)

Greece (1999)South Africa (1981)New Zealand (1956)Italy (1994)Spain (2003)

Countries in which REIT structures already exist

Countries in which structures similar to REIT structures already exist

Countries in which the introduction ofREITs is already planned

4

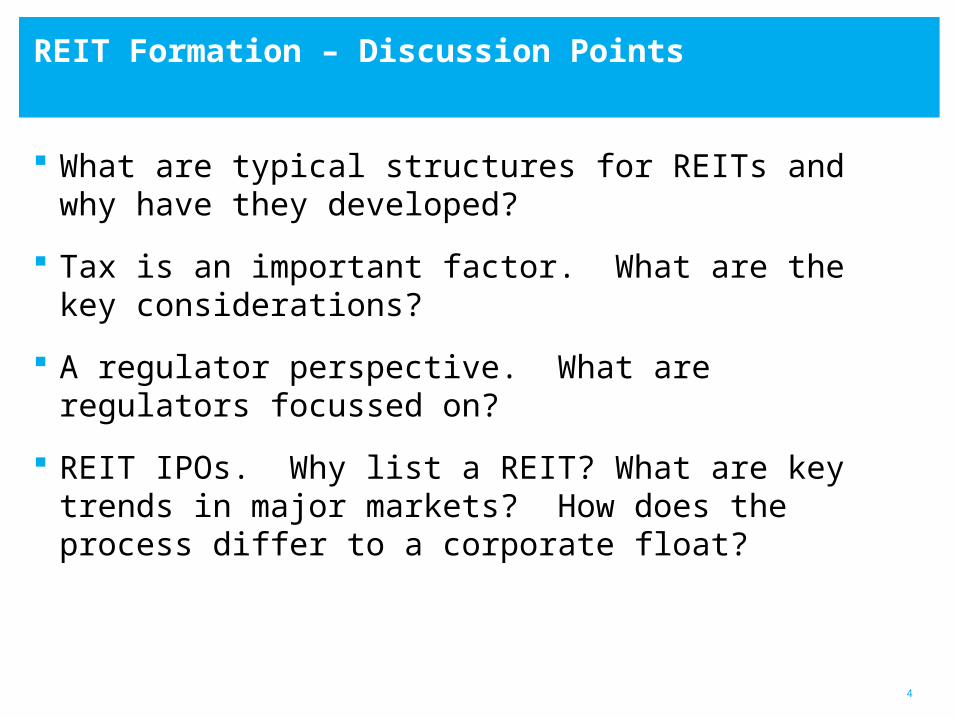

What are typical structures for REITs and why have they developed?

Tax is an important factor. What are the key considerations?

A regulator perspective. What are regulators focussed on?

REIT IPOs. Why list a REIT? What are key trends in major markets? How does the process differ to a corporate float?

REIT Formation – Discussion Points

5

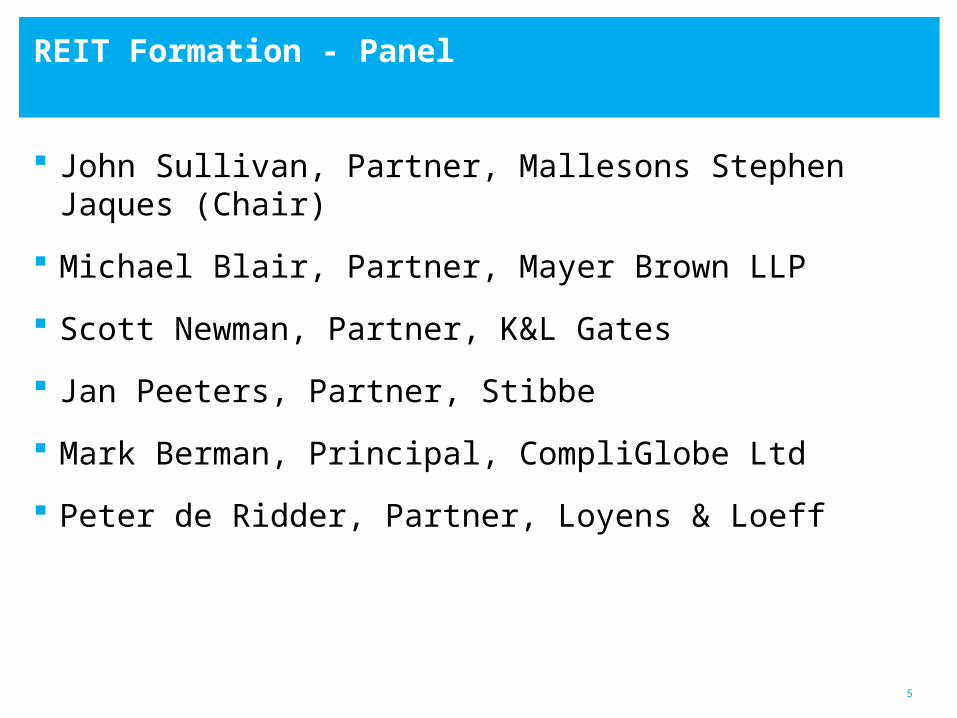

John Sullivan, Partner, Mallesons Stephen Jaques (Chair)

Michael Blair, Partner, Mayer Brown LLP

Scott Newman, Partner, K&L Gates

Jan Peeters, Partner, Stibbe

Mark Berman, Principal, CompliGlobe Ltd

Peter de Ridder, Partner, Loyens & Loeff

REIT Formation - Panel

6

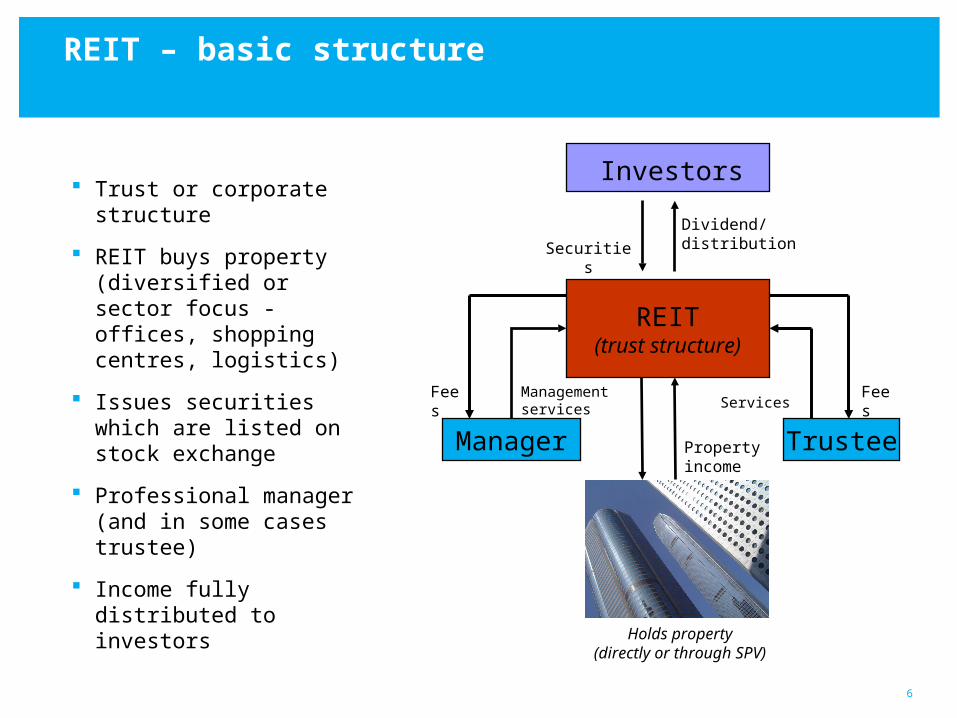

REIT – basic structure

Trust or corporate structure

REIT buys property (diversified or sector focus - offices, shopping centres, logistics)

Issues securities which are listed on stock exchange

Professional manager (and in some cases trustee)

Income fully distributed to investors

Investors

REIT(trust structure)

TrusteeManager

Securities

Holds property(directly or through SPV)

Fees

Management services

Property income

Dividend/ distribution

ServicesFees

7

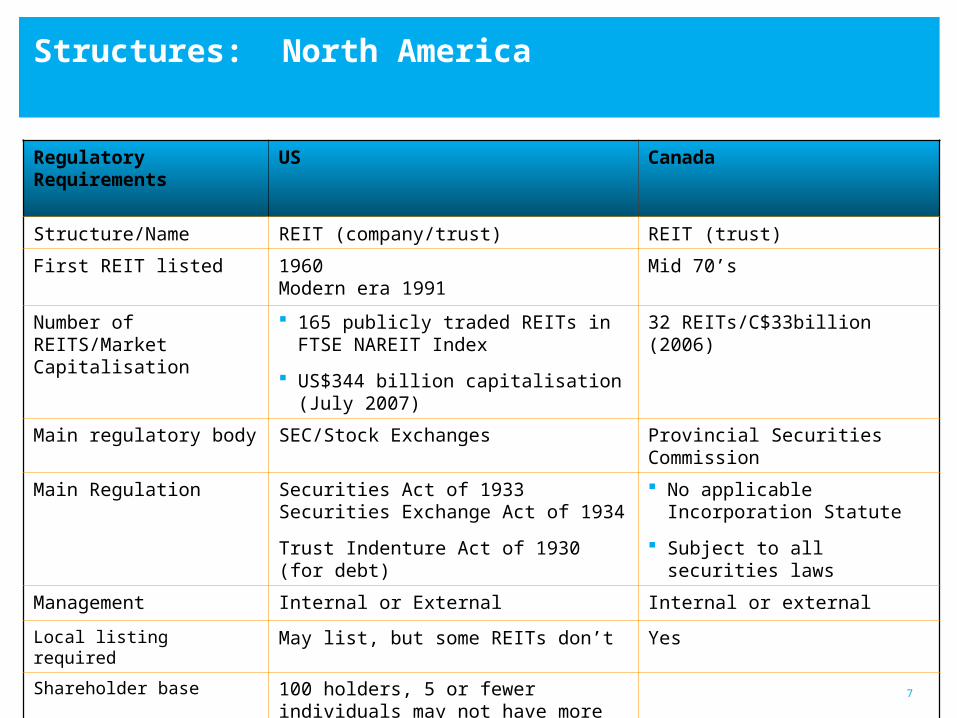

Structures: North America

Regulatory Requirements

US Canada

Structure/Name REIT (company/trust) REIT (trust)

First REIT listed 1960Modern era 1991

Mid 70’s

Number of REITS/Market Capitalisation

165 publicly traded REITs in FTSE NAREIT Index

US$344 billion capitalisation (July 2007)

32 REITs/C$33billion (2006)

Main regulatory body SEC/Stock Exchanges Provincial Securities Commission

Main Regulation Securities Act of 1933Securities Exchange Act of 1934

Trust Indenture Act of 1930 (for debt)

No applicable Incorporation Statute

Subject to all securities laws

Management Internal or External Internal or external

Local listing required May list, but some REITs don’t Yes

Shareholder base 100 holders, 5 or fewer individuals may not have more than 50% in value

8

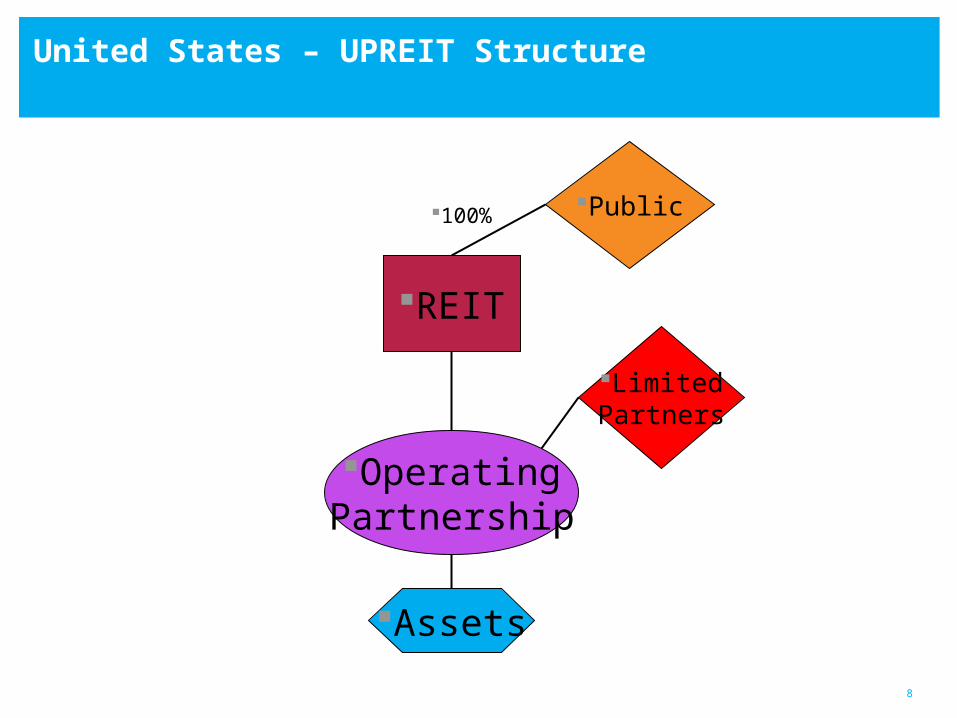

United States – UPREIT Structure

REIT

OperatingPartnership

Public

LimitedPartners

100%

Assets

9

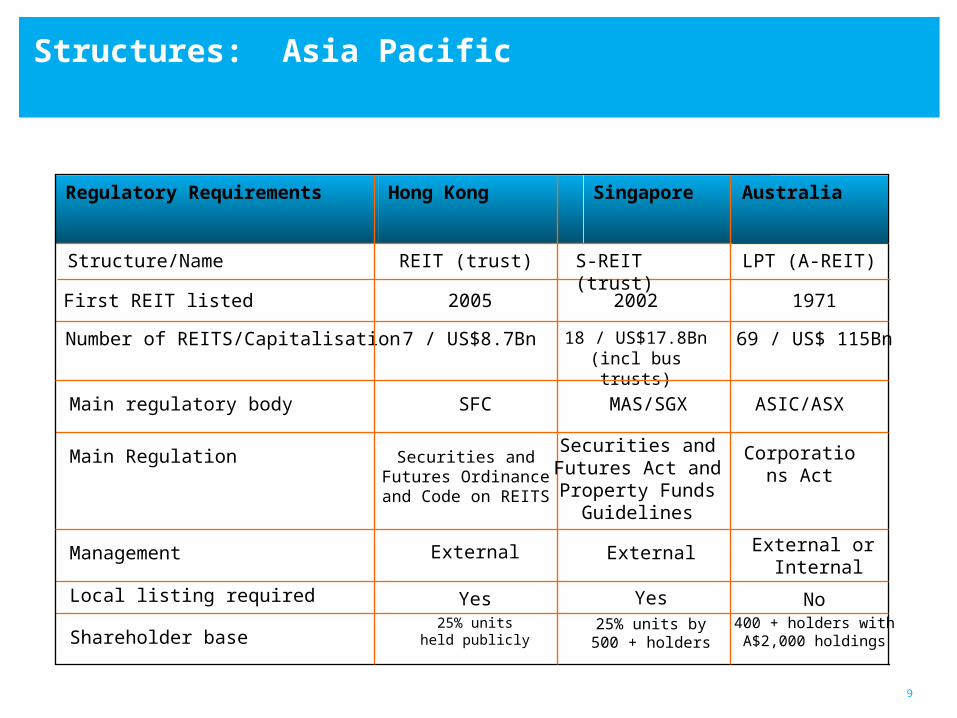

Structures: Asia Pacific

20022005First REIT listed

18 / US$17.8Bn (incl bus trusts)

7 / US$8.7BnNumber of REITS/Capitalisation

ExternalExternalManagement

SingaporeHong KongRegulatory Requirements Australia

External or Internal

69 / US$ 115Bn

1971

Main regulatory body SFC MAS/SGX ASIC/ASX

Main Regulation Securities and Futures Ordinance

and Code on REITS

Securities and Futures Act and Property Funds

Guidelines

Corporations Act

Local listing required Yes Yes No

Shareholder base25% units held

publicly25% units by 500 + holders

400 + holders with A$2,000 holdings

Structure/Name REIT (trust) S-REIT (trust) LPT (A-REIT)

10

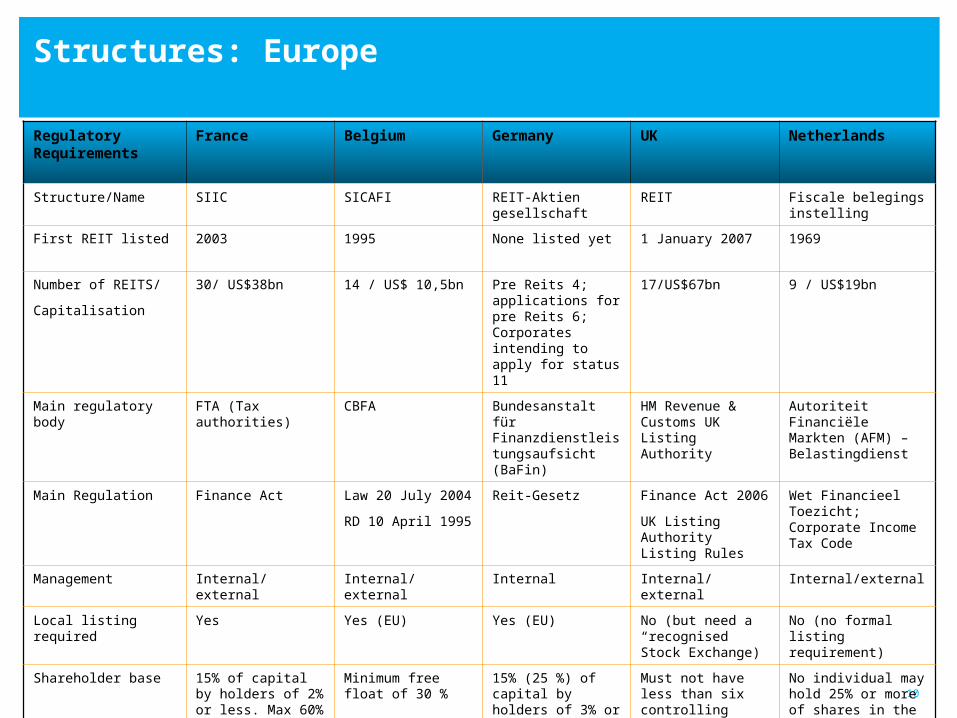

Structures: Europe

Regulatory Requirements

France Belgium Germany UK Netherlands

Structure/Name SIIC SICAFI REIT-Aktien gesellschaft

REIT Fiscale belegings instelling

First REIT listed 2003 1995 None listed yet 1 January 2007 1969

Number of REITS/

Capitalisation

30/ US$38bn 14 / US$ 10,5bn Pre Reits 4; applications for pre Reits 6; Corporates intending to apply for status 11

17/US$67bn 9 / US$19bn

Main regulatory body FTA (Tax authorities) CBFA Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin)

HM Revenue & Customs UK Listing Authority

Autoriteit Financiële Markten (AFM) – Belastingdienst

Main Regulation Finance Act Law 20 July 2004

RD 10 April 1995

Reit-Gesetz Finance Act 2006

UK Listing Authority Listing Rules

Wet Financieel Toezicht; Corporate Income Tax Code

Management Internal/external Internal/external Internal Internal/external Internal/external

Local listing required Yes Yes (EU) Yes (EU) No (but need a “recognised Stock Exchange)

No (no formal listing requirement)

Shareholder base 15% of capital by holders of 2% or less. Max 60% any holder/group.

Minimum free float of 30 %

15% (25 %) of capital by holders of 3% or less. Max 9.99% any holder.

Must not have less than six controlling members. Max 10% any holder.

No individual may hold 25% or more of shares in the listed entity.

Other restrictions apply

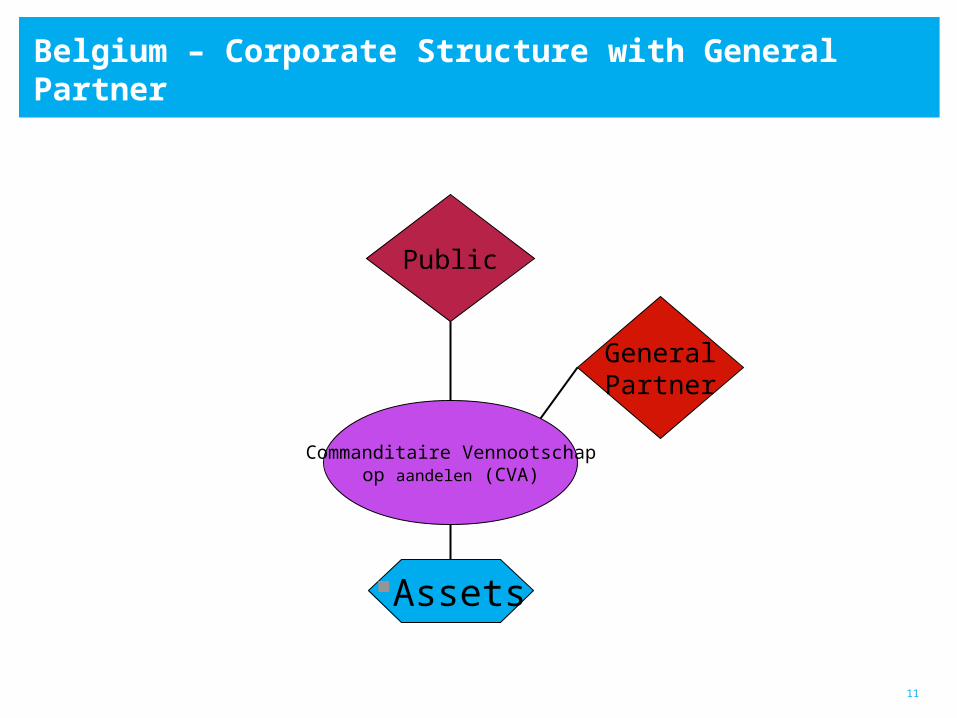

11

Belgium – Corporate Structure with General Partner

Commanditaire Vennootschapop aandelen (CVA)

Public

GeneralPartner

Assets

12

Trust, Limited Partnership or Limited Liability Company in order to achieve tax neutrality concept of the REIT?

Capitalisation of the REIT: equity and debt/borrowings – does it matter for tax purposes?

Investor home tax considerations and structuring opportunities

Tax considerations

13

REIT Formation – U.S. Tax Requirements

REIT provisions initially enacted by the U.S. in 1960

Designed to allow individual investors to invest in real estate through a public, liquid vehicle as if such investors had invested directly in the underlying real estate

If properly structured and operated, REIT is a “conduit” for purposes of U.S. income taxation (i.e., no corporate level tax and only one level of tax imposed at the shareholder level)

U.S. REITs: Equity versus Mortgage

Can be a corporation, trust or association, provided the following conditions are met:

⇒Managed by one or more trustees or directors

⇒Beneficial ownership of which is evidenced by transferable shares, or by transferable certificates of beneficial interest

⇒Would be taxable as a domestic corporation if not a REIT

14

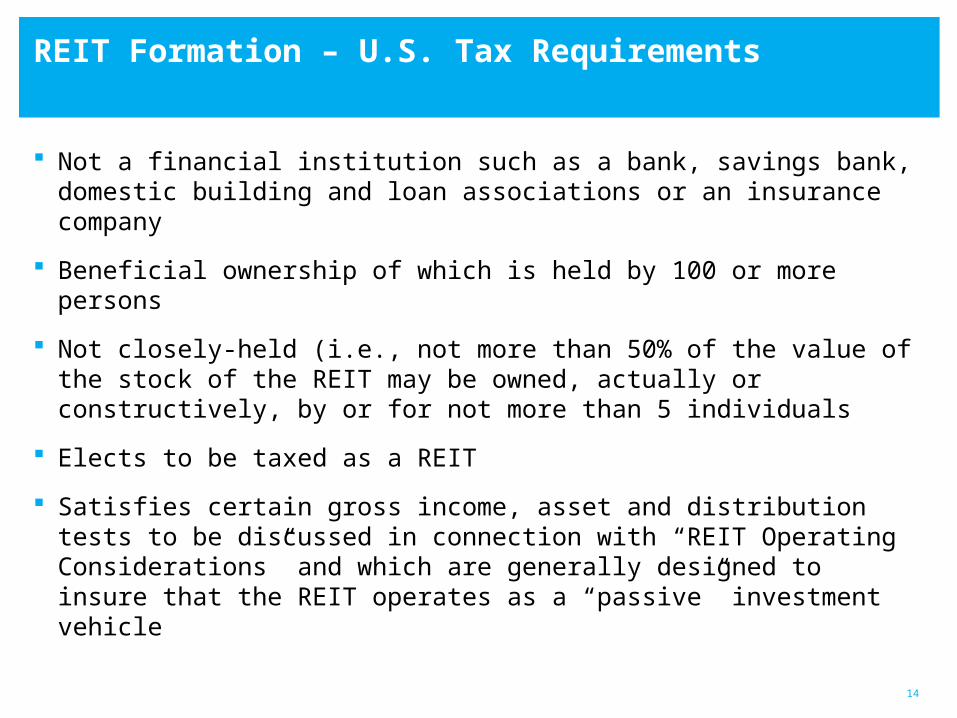

REIT Formation – U.S. Tax Requirements

Not a financial institution such as a bank, savings bank, domestic building and loan associations or an insurance company

Beneficial ownership of which is held by 100 or more persons

Not closely-held (i.e., not more than 50% of the value of the stock of the REIT may be owned, actually or constructively, by or for not more than 5 individuals

Elects to be taxed as a REIT

Satisfies certain gross income, asset and distribution tests to be discussed in connection with “REIT Operating Considerations” and which are generally designed to insure that the REIT operates as a “passive” investment vehicle

15

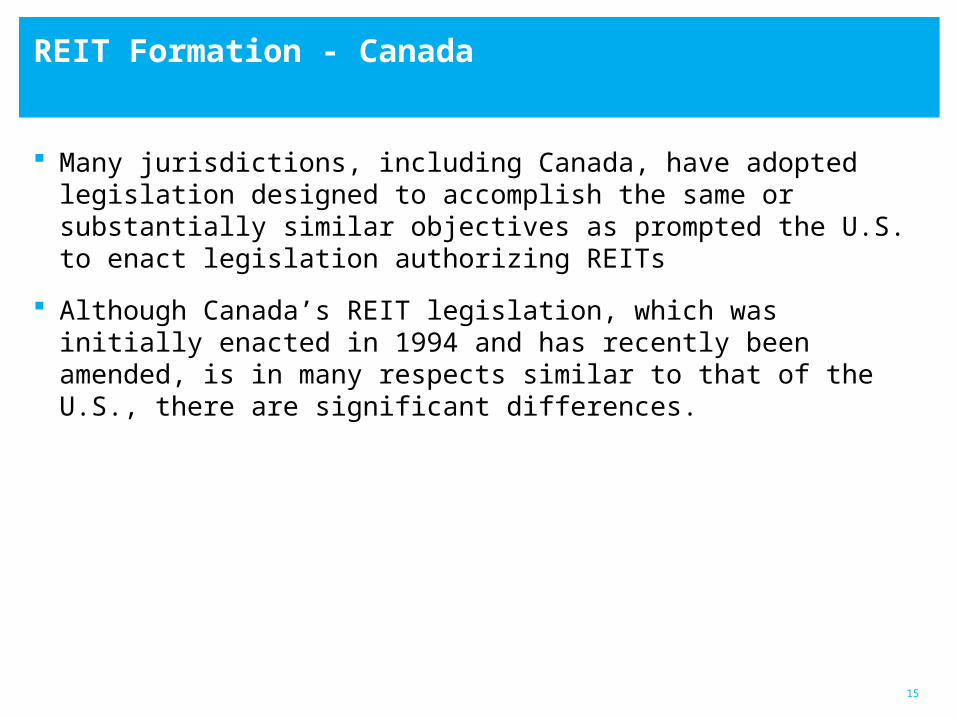

REIT Formation - Canada

Many jurisdictions, including Canada, have adopted legislation designed to accomplish the same or substantially similar objectives as prompted the U.S. to enact legislation authorizing REITs

Although Canada’s REIT legislation, which was initially enacted in 1994 and has recently been amended, is in many respects similar to that of the U.S., there are significant differences.

16

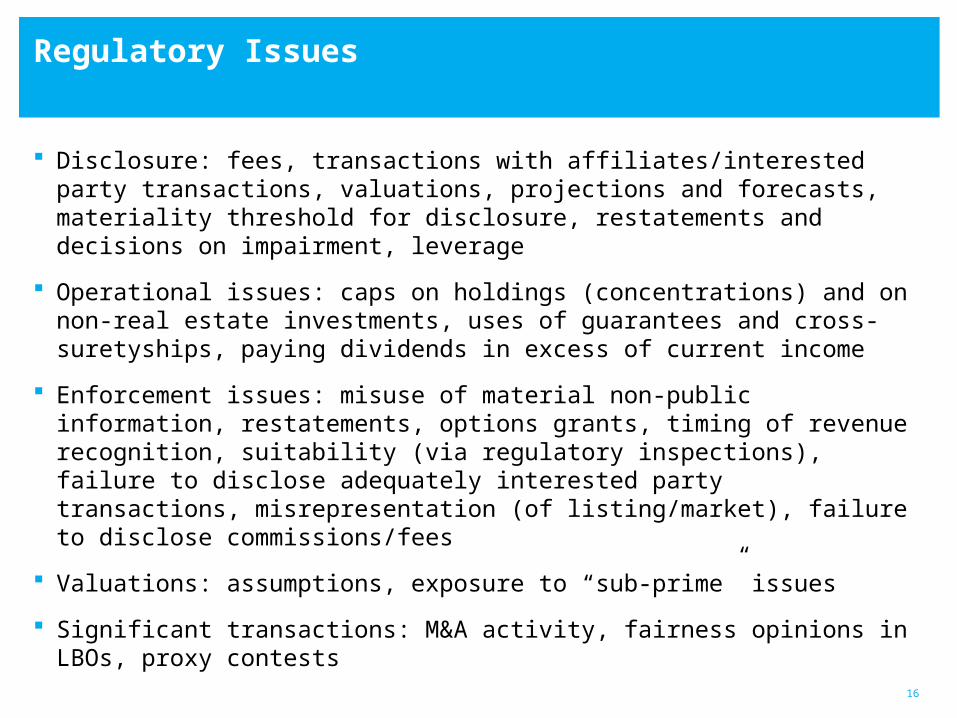

Regulatory Issues

Disclosure: fees, transactions with affiliates/interested party transactions, valuations, projections and forecasts, materiality threshold for disclosure, restatements and decisions on impairment, leverage

Operational issues: caps on holdings (concentrations) and on non-real estate investments, uses of guarantees and cross-suretyships, paying dividends in excess of current income

Enforcement issues: misuse of material non-public information, restatements, options grants, timing of revenue recognition, suitability (via regulatory inspections), failure to disclose adequately interested party transactions, misrepresentation (of listing/market), failure to disclose commissions/fees

Valuations: assumptions, exposure to “sub-prime” issues

Significant transactions: M&A activity, fairness opinions in LBOs, proxy contests

17

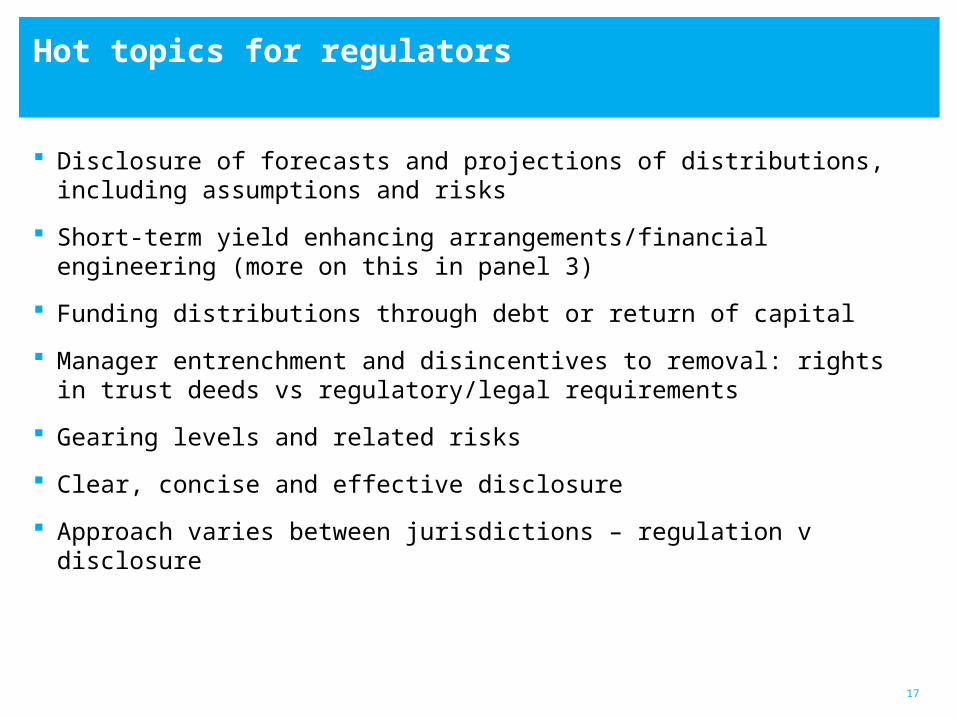

Hot topics for regulators

Disclosure of forecasts and projections of distributions, including assumptions and risks

Short-term yield enhancing arrangements/financial engineering (more on this in panel 3)

Funding distributions through debt or return of capital

Manager entrenchment and disincentives to removal: rights in trust deeds vs regulatory/legal requirements

Gearing levels and related risks

Clear, concise and effective disclosure

Approach varies between jurisdictions – regulation v disclosure

18

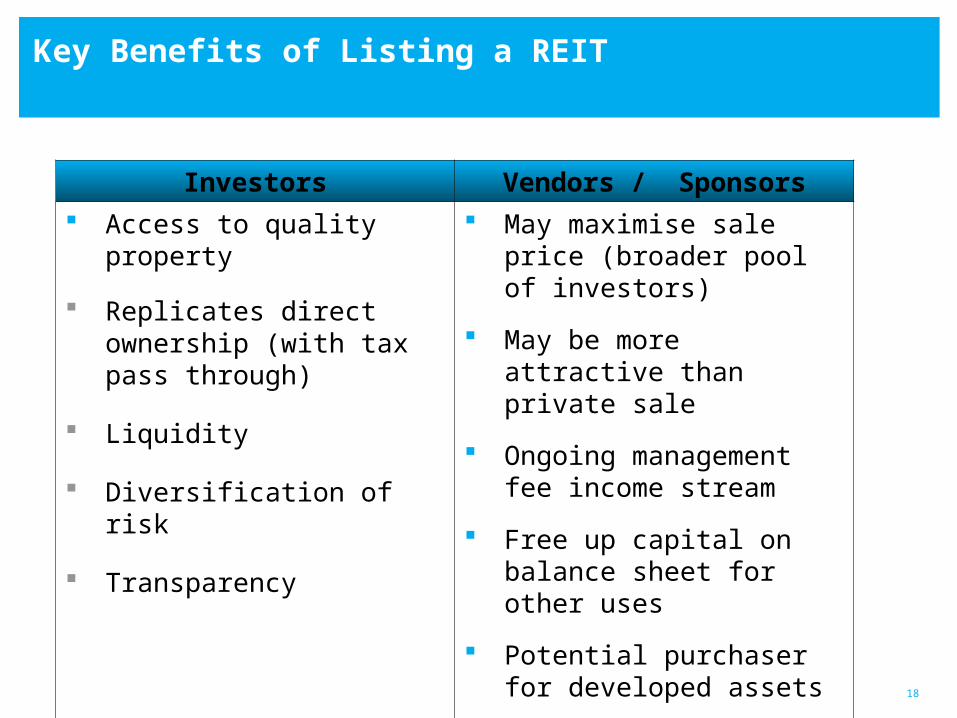

Key Benefits of Listing a REIT

Investors Vendors / Sponsors

Access to quality property

Replicates direct ownership (with tax pass through)

Liquidity

Diversification of risk

Transparency

May maximise sale price (broader pool of investors)

May be more attractive than private sale

Ongoing management fee income stream

Free up capital on balance sheet for other uses

Potential purchaser for developed assets

Potential value uplift in REIT structure

19

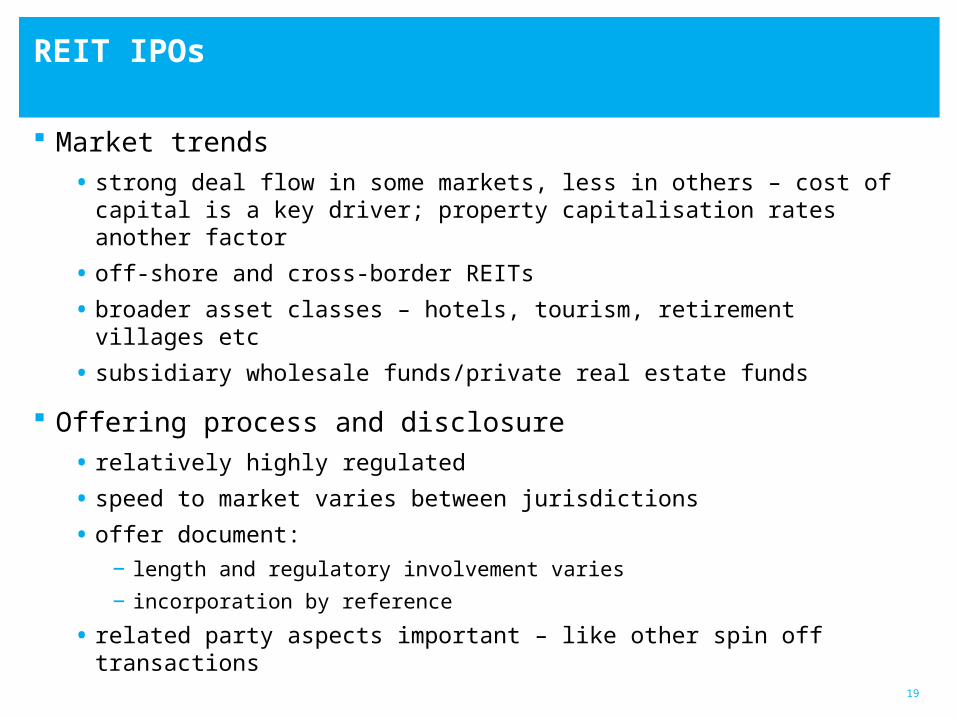

Market trends

• strong deal flow in some markets, less in others – cost of capital is a key driver; property capitalisation rates another factor

• off-shore and cross-border REITs

• broader asset classes – hotels, tourism, retirement villages etc

• subsidiary wholesale funds/private real estate funds

Offering process and disclosure

• relatively highly regulated

• speed to market varies between jurisdictions

• offer document:

− length and regulatory involvement varies

− incorporation by reference

• related party aspects important – like other spin off transactions

REIT IPOs

20

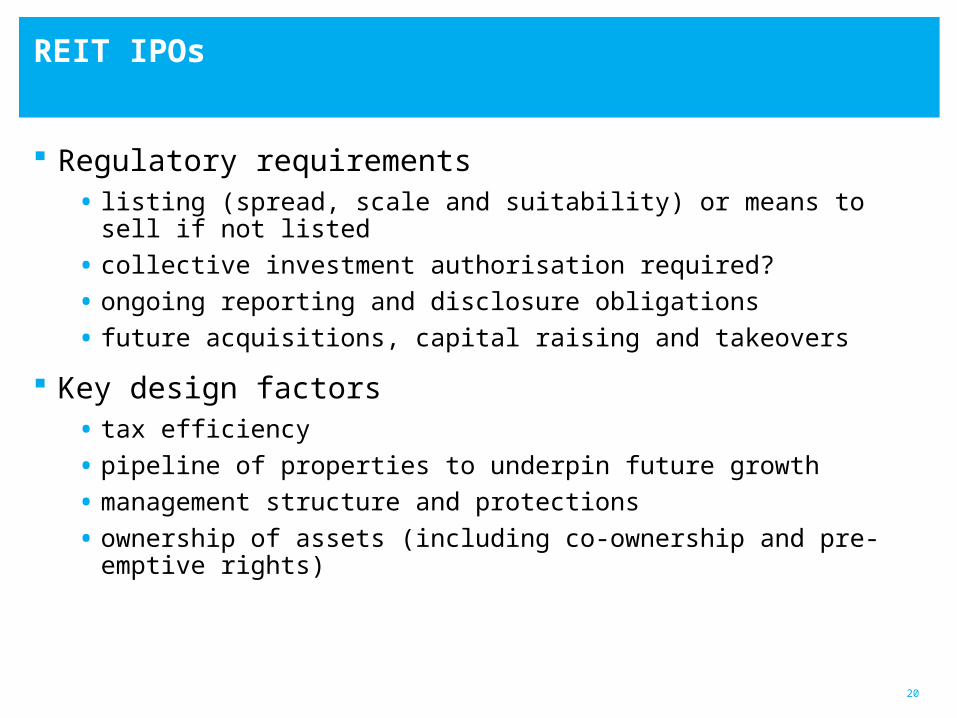

REIT IPOs

Regulatory requirements• listing (spread, scale and suitability) or means to sell if not listed

• collective investment authorisation required?

• ongoing reporting and disclosure obligations

• future acquisitions, capital raising and takeovers

Key design factors• tax efficiency

• pipeline of properties to underpin future growth

• management structure and protections

• ownership of assets (including co-ownership and pre-emptive rights)

21

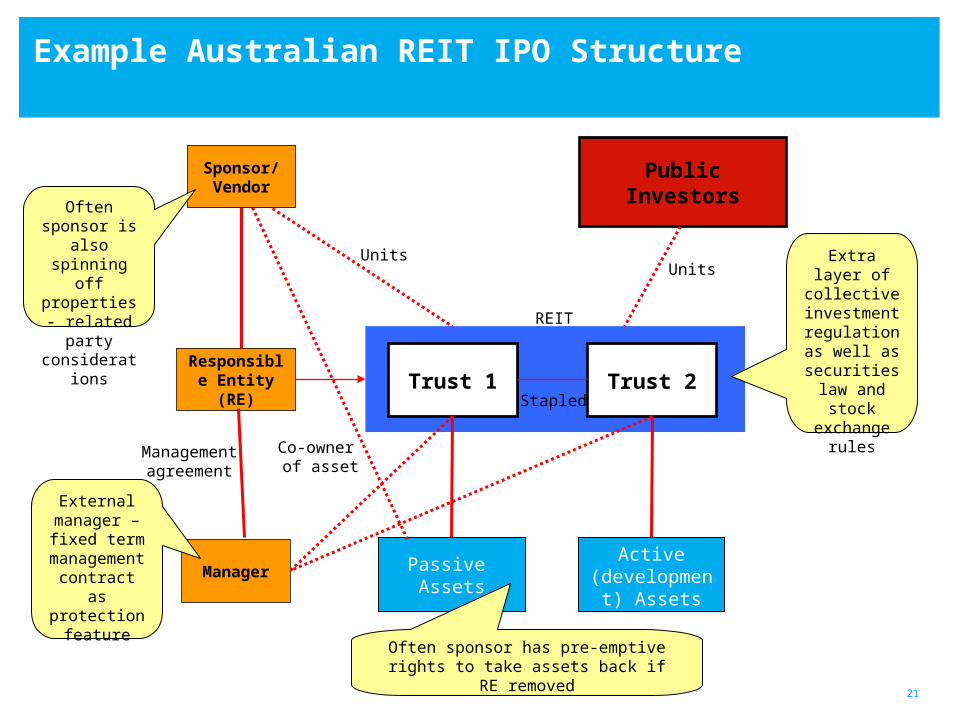

Example Australian REIT IPO Structure

Passive Assets

Public Investors

Trust 1 Trust 2Responsible Entity (RE)

ManagerActive

(development) Assets

Extra layer of collective

investment regulation as

well as securities law

and stock exchange

rules

Often sponsor has pre-emptive rights to take assets back if RE removed

External manager – fixed term

management contract as protection

feature

Units

REIT

Co-owner of asset

Management agreement

Sponsor/Vendor

Often sponsor is also

spinning off properties - related party consideration

s

Units

Stapled

International Bar Association ConferenceReal Estate Investment TrustsPanel 2 - REIT formation

17 October 2007

Singapore9142562_1