Embed Size (px)

Citation preview

International Accounting StandardsFinancial Reporting in Hyperinflationary EconomiesUnderstanding IAS 29

PricewaterhouseCoopers (www.pwcglobal.com), is the world’s largest professional services organisation. Drawing on theknowledge and skills of 150,000 people in 150 countries, we help our clients solve complex business problems andmeasurably enhance their ability to build value, manage risk and improve performance. PricewaterhouseCoopers refers tothe member firms of the worldwide PricewaterhouseCoopers organisation.

PricewaterhouseCoopers 1

International Accounting Standards (IAS) areincreasingly popular with enterprises raisinginternational capital through debt or equity. Thisincludes many enterprises in emerging markets andfast developing economies – which may behyperinflationary environments.

IAS 29 “Financial Reporting in HyperinflationaryEconomies” is an integral and mandatory part of theIAS body of standards. It requires the IAS financialstatements of any enterprise reporting in the currencyof a hyperinflationary economy to take full accountof the effects of inflation using a current purchasingpower approach.

The requirements of IAS 29 also need to beconsidered by any enterprise located outside thehyperinflationary environment preparing IAS

consolidated financial statements that include aforeign entity (such as a subsidiary, associate, jointventure or branch) which reports in the currency ofa hyperinflationary economy.

Preparation of financial statements using a currentpurchasing power approach requires both anunderstanding of the underlying economic concepts and a complex series of procedures andreconciliations to ensure accurate results.

This guide has been prepared to serve as a practical aid for those enterprises applying IAS 29.PricewaterhouseCoopers has helped manyenterprises to apply this difficult standard. Ourexperience and our proven methodology, describedin this guide, will make applying IAS 29 lessburdensome for your company.

Preface

Other publications on IASThe following publications on International Accounting Standards have been published byPricewaterhouseCoopers and are available from your nearest PricewaterhouseCoopers office:

International Accounting Standards – A Pocket Guide – 2001International Accounting Standards – Disclosure Checklist – 2001International Accounting Standards – Illustrative Corporate Financial Statements – 2001International Accounting Standards – Illustrative Bank Financial Statements – 2001International Accounting Standards – Illustrative Fund Financial Statements – 2001International Accounting Standards – Understanding IAS 39 International Accounting - Similarities & Differences – IAS, US GAAP and UK GAAP

and on wider aspects of international reporting:Audit Committees – Good Practices for Meeting Market ExpectationsReporting Progress – Good Practices for Meeting Market ExpectationsYou can find latest news, discussions and publications on our website athttp://www.pwcglobal.com/extweb/corprep.nsf/docid/

Contents

2 PricewaterhouseCoopers

Chapter 1

Chapter 2 Applying the standard 9

Overview 9

Selection of the price index 9

Segregation of monetary and non-monetary items 10

Restatement of non-monetary items 11

Income statement 11

The calculation of monetary gain or loss 12

Cash flow statement 12

Restatement of corresponding figures 12

Disclosures 13

Economies ceasing to be hyperinflationary 13

Chapter 3 Restatement procedures for non-monetary balance sheet items 15

Introduction 15

Non-monetary items at fair value or NRV 15

Prepaid expenses 15

Advances paid on purchases 16

Inventories 16

Investments in associates 16

Property, plant and equipment and accumulated depreciation 17

Intangible assets 18

Advances received 18

Deferred income (for instance grants) 19

Deferred tax assets and liabilities 19

Restatement of shareholders’ equity 19–20

Introduction 5

Why is this guide needed? 5

Inflation or changes in the general purchasing power of money 5

Characteristics of hyperinflation 5

Benefits of purchasing power adjusted financial statements 6

Objectives of IAS 29 6

Who must apply IAS 29 6

Reporting in a stable currency 6

Intra-group reporting 7

Contents

PricewaterhouseCoopers 3

Chapter 4 Restatement of the income statement 21

Revenue 21

Cost of goods sold 21

Depreciation, amortisation of intangible assets and realisation of prepaid expenses and deferred income (grant) 22

Other items included in the income statement 22

Adjustments and/or reclassifications made to statutory financial statements in order to arrive at IAS historic financial statements 22

Taxation on income 22

Monetary gain/loss 23

Chapter 6

Chapter 5 Monetary gain or loss 25

Proof – average monetary position method 25

Proof – statement of sources and application of net monetary assets and liabilities method 25–27

Cash flows 29–30

Chapter 7 Practical example of IAS 31

4 PricewaterhouseCoopers

PricewaterhouseCoopers 5

Why is this guide needed?IAS 29 is based on current purchasing powerprinciples and requires that financial statementsprepared in the currency of a hyperinflationaryeconomy be stated in terms of the value of money at the reporting balance sheet date.

This straightforward requirement needs anunderstanding of complex economic concepts, athorough knowledge of the enterprise’s financialand operating patterns and a detailed series ofprocedures to implement. It represents a realchallenge for enterprises and auditors.

The guide provides an overview of the concepts inthe standard, descriptions of the necessaryprocedures and a detailed worked example. Thischapter of the implementation guide covers theeconomic concepts, the objectives of the standardand who must apply it.

Inflation or changes in the generalpurchasing power of moneyThe purchasing power of money declines as thegeneral level of prices of goods and services rises. In an inflationary environment, the generalpurchasing power of money and the general pricelevel are interdependent.

Financial statements unadjusted for inflation in mostcountries are prepared on the basis of historic costwithout regard to changes in the general level ofprices. Consequently, the individual assets,liabilities, shareholders’ equity, revenue, expenses

and gains and losses are stated at cost at the timethese items originated. The impact of inflation isthus ignored. This produces a meaningful resultprovided that there are not dramatic changes in thepurchasing power of money.

Significant changes in the purchasing power ofmoney mean that financial statements unadjustedfor inflation are likely to be misleading. Amounts arenot comparable between periods and the gain orloss in general purchasing power that arises in thereporting period is not recorded. Financial statementsunadjusted for inflation do not reflect an accurateposition of the company at the balance sheet date or the results of its operations or cash flows.

Inflation adjusted financial statements are anextension to and not a departure from historic costaccounting. IAS 29 seeks to overcome thelimitations of historic cost financial reporting inhyperinflationary conditions.

Characteristics of hyperinflationIAS 29 does not provide an absolute definition ofhyperinflation. The general characteristics identifiedin IAS 29 are the following:

• people accumulate wealth in non-monetary assetsor in a stable foreign currency;

• monetary amounts are expressed in terms of arelatively stable foreign currency. Prices (forexample, rent, wages and capital goods) may bequoted in that currency;

Introduction

Chapter 1

• prices for credit sales and purchases are calculatedto compensate for the expected loss of purchasingpower during the credit period, even for shortterm credit;

• interest rates, wages and prices are linked to aprice index; and

• the cumulative inflation rate over three years isapproaching, or exceeds, 100%.

Other characteristics not mentioned in the standard,but which can be useful in determining thepresence of hyperinflation, include:

• severe exchange controls to protect the localcurrency; and

• frequent Central Bank intervention in the currency.

Benefits of purchasing poweradjusted financial statementsFinancial statements that are expressed in ameasuring unit current at the balance sheet dateunder IAS 29 provide several intrinsic benefits:

• they give comparable information from period toperiod to management, shareholders and otherusers as to the underlying results of operations,capital maintenance and trends in performance;

• they enable management to make more reliabledecisions on capital investment plans as thefinancial statements are more relevant; and

• the financial statements become more useful tointernational investors and other users of accountsin that they are comparable with other companiesthe same industry.

Objectives of IAS 29The IAS 29 approach is to restate all balancesrecorded in the financial statements (includingcomparative numbers) to the year-end generalpurchasing power of the reporting currency. Theeffects of the IAS 29 restatement on the financialstatements will depend on the magnitude ofinflation and the composition of the assets andliabilities of the company.

The remeasurement process requires theapplication of judgement as well as certain requiredprocedures. The standard explicitly states: “Theconsistent application of these procedures andjudgements from one period to another is moreimportant than the precise accuracy of the resultingamounts included in the restated financialstatements”.

Who must apply IAS 29Compliance with IAS 29 is mandatory for anycompany presenting IAS financial statements in the currency of a hyperinflationary economy, andnotably in connection with any application by such a company for listing on an international stock exchange.

The standard applies to the financial statements ofany enterprise from the beginning of the reportingperiod in which it identifies the existence ofhyperinflation in the country of its reporting currency.

Reporting in a stable currencyThe restatement process outlined in IAS 29specifically applies to those situations where acompany prepares its IAS financial statements in the currency of a hyperinflationary economy. IAS 29 does not address the situation where acompany operating in a hyperinflationary economyprepares its IAS financial statements in a stablecurrency (for example the US dollar).

When an enterprise reports in a stable currency, itshould ensure that the financial statements have

Chapter 1 Introduction

6 PricewaterhouseCoopers

If the cumulative inflation in an economydeemed to be hyperinflationary dropsbelow 100% in a three-year period, hashyperinflation ceased?

Probably, the economy has ceased to behyperinflationary. However, this quantitativemeasure needs to be evaluated in the contextof overall economic developments and trend.

Although judgement is involved indetermining when an economy is no longerhyperinflationary, all entities should cease toapply IAS 29 from the same date to ensurefinancial statements are comparable fromentity to entity.

Frequently asked questions

appropriately dealt with the impact ofhyperinflation. Enterprises should restate the localcurrency IAS financial statements in accordancewith IAS 29. The year-end exchange rate is used totranslate the financial statements into the stablecurrency for all periods presented.

Intra-group reportingA foreign entity operating in a hyperinflationaryeconomy may be required for group purposes toreport to its overseas parent in a stable currency,usually the parent’s reporting currency.

IAS 21 states that the foreign entity must restate itslocal currency IAS financial statements inaccordance with IAS 29 before translation into theparent’s reporting currency.

A foreign operation’s activities may be an integralpart of those of the reporting enterprise, wheresubstantially all its transactions are in the currencyof its parent. An integral foreign operation locatedin a hyperinflationary economy reporting to itsparent in a stable currency, treats all local currencytransactions as if they are foreign currencytransactions in accordance with IAS 21 p9.

Chapter 1 Introduction

PricewaterhouseCoopers 7

8 PricewaterhouseCoopers

PricewaterhouseCoopers 9

OverviewApplication of IAS 29 requires the restatement of thefinancial statements, including the cash flowstatements, into current purchasing power at thebalance sheet date. This requires a number ofprocedural steps plus the application of judgement.Consistent application of procedures is moreimportant than the precise accuracy of the results.

In outline form, the restatement procedures consistof the following:

• selection of a general price index,

• segregation of monetary and non-monetary items,

• restatement of non-monetary items,

• restatement of the income statement,

• calculation and proof of the monetary gain or loss,

• preparation of the cash flow statement withrecognition of inflationary effects, and

• restatement of corresponding figures

This chapter gives an overview of the restatementprocess. Further chapters provide detailed guidanceon complex areas. An extensive worked example isshown in the second half of this publication.

Selection of the price indexIAS 29 requires the use of a general price index toreflect changes in purchasing power. Mostgovernments issue several periodic price indicesthat vary in their scope.

The standard does not indicate which index to use.It is preferable that all enterprises that report in thecurrency of the same economy use the same index.

The most reliable indicators of changes in generalprice levels are the consumer price index and thewholesale price index. In some countries, becauseof differences in the scope and the weighting ofitems included, the two indices may indicate slightlydifferent rates of inflation in the short-term. Over thelong-term, however, the two indices should showapproximately the same rate of inflation.

Applying the Standard

Chapter 2

The most important attributes for a reliablegeneral price index are:

• wide range of reference, such as inclusionof most of the goods and services producedin the economy, in order to reflect varyingprice fluctuations;

• accurate reflection of price changes;

• availability of prior year indices as well asthose of the current year;

• regular, preferably monthly, updating; and

• consistency, uniformity and continuity.

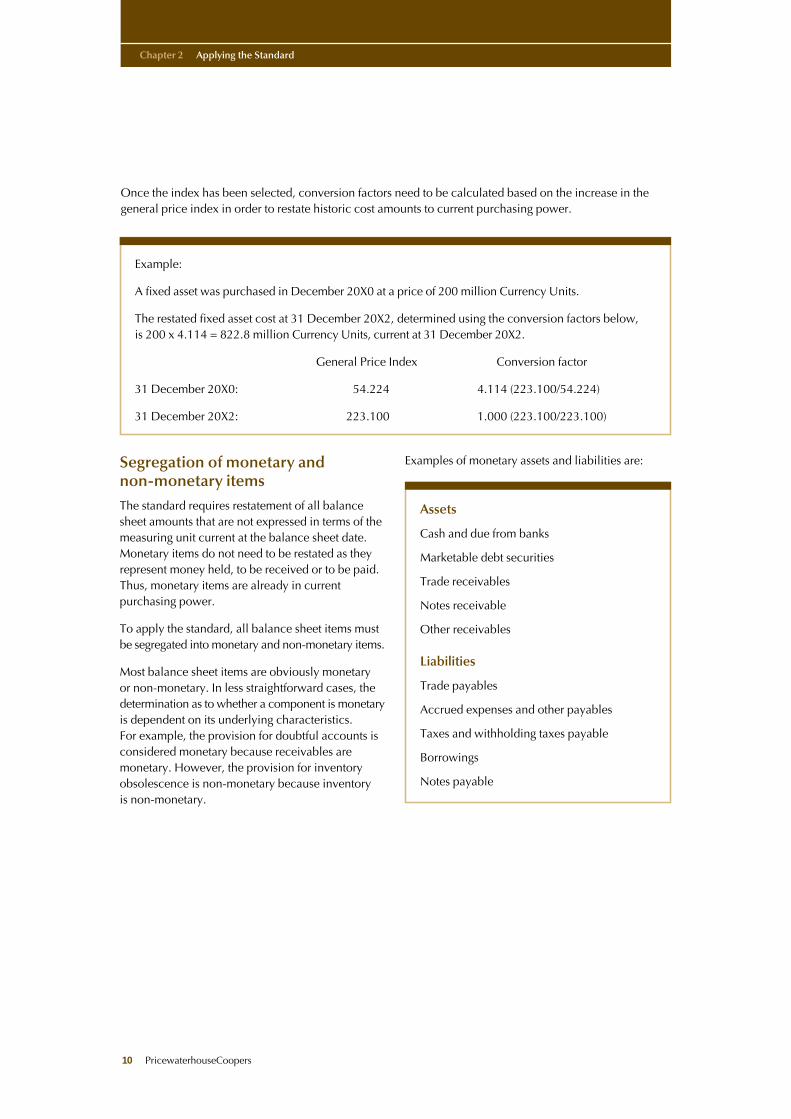

Once the index has been selected, conversion factors need to be calculated based on the increase in thegeneral price index in order to restate historic cost amounts to current purchasing power.

Chapter 2 Applying the Standard

10 PricewaterhouseCoopers

Example:

A fixed asset was purchased in December 20X0 at a price of 200 million Currency Units.

The restated fixed asset cost at 31 December 20X2, determined using the conversion factors below, is 200 x 4.114 = 822.8 million Currency Units, current at 31 December 20X2.

General Price Index Conversion factor

31 December 20X0: 54.224 4.114 (223.100/54.224)

31 December 20X2: 223.100 1.000 (223.100/223.100)

Segregation of monetary and non-monetary itemsThe standard requires restatement of all balancesheet amounts that are not expressed in terms of themeasuring unit current at the balance sheet date.Monetary items do not need to be restated as theyrepresent money held, to be received or to be paid.Thus, monetary items are already in currentpurchasing power.

To apply the standard, all balance sheet items mustbe segregated into monetary and non-monetary items.

Most balance sheet items are obviously monetary or non-monetary. In less straightforward cases, thedetermination as to whether a component is monetaryis dependent on its underlying characteristics. For example, the provision for doubtful accounts isconsidered monetary because receivables aremonetary. However, the provision for inventoryobsolescence is non-monetary because inventory is non-monetary.

Examples of monetary assets and liabilities are:

Assets

Cash and due from banks

Marketable debt securities

Trade receivables

Notes receivable

Other receivables

Liabilities

Trade payables

Accrued expenses and other payables

Taxes and withholding taxes payable

Borrowings

Notes payable

Assets and liabilities other than monetary items are called non-monetary items. Once paid in oraccumulated, all elements of shareholders’ equityare non-monetary.

Examples of non-monetary items are:

Restatement of non-monetary itemsNon-monetary assets and liabilities are restated interms of the measuring unit current at the balancesheet date, using the increase in the general priceindex from the transaction date, when they arose, to the balance sheet date.

Specific issues arise when restatement increases the carrying amount of assets beyond the netrealisable value or if non-monetary assets arecarried at fair value.

Detailed guidance on these issues and on therestatement of non-monetary items is included inthe balance sheet found in Chapter 3.

Income statement

The historic cost income statement generally reportsrevenues and costs that were current whenever theunderlying transaction or event occurred. IAS 29requires that all items in the income statement beexpressed in terms of the measuring unit current atthe balance sheet reporting date. Therefore, allamounts need to be restated by applying the changein the general price index for the dates when theitems of income and expenses originated.

Income statements are normally restated on amonthly basis.

Income statement items, such as interest incomeand expense, and foreign exchange differencesrelated to invested or borrowed funds are alsoassociated with the net monetary position. Theseitems are adjusted for inflation and, along with themonetary gain or loss, presented as separate linesunder the non-operating items caption in theincome statement. These items may be subtotalledwithin the non-operating caption as financingincome or expenses.

Detailed guidance on restatement of the incomestatement is found in Chapter 4.

Chapter 2 Applying the Standard

PricewaterhouseCoopers 11

Assets

Prepaid expenses

* Advances paid on purchases Inventories

Marketable equity investments

Investments in associates

Property, plant and equipment

Intangible assets

Deferred tax assets

Liabilities

*Advances received on sales

Deferred income (for example, grants)

Deferred tax liabilities

Shareholders’ equity

* Advances paid or received are considerednon-monetary if they are linked to specificpurchases or sales, otherwise they should be considered monetary.

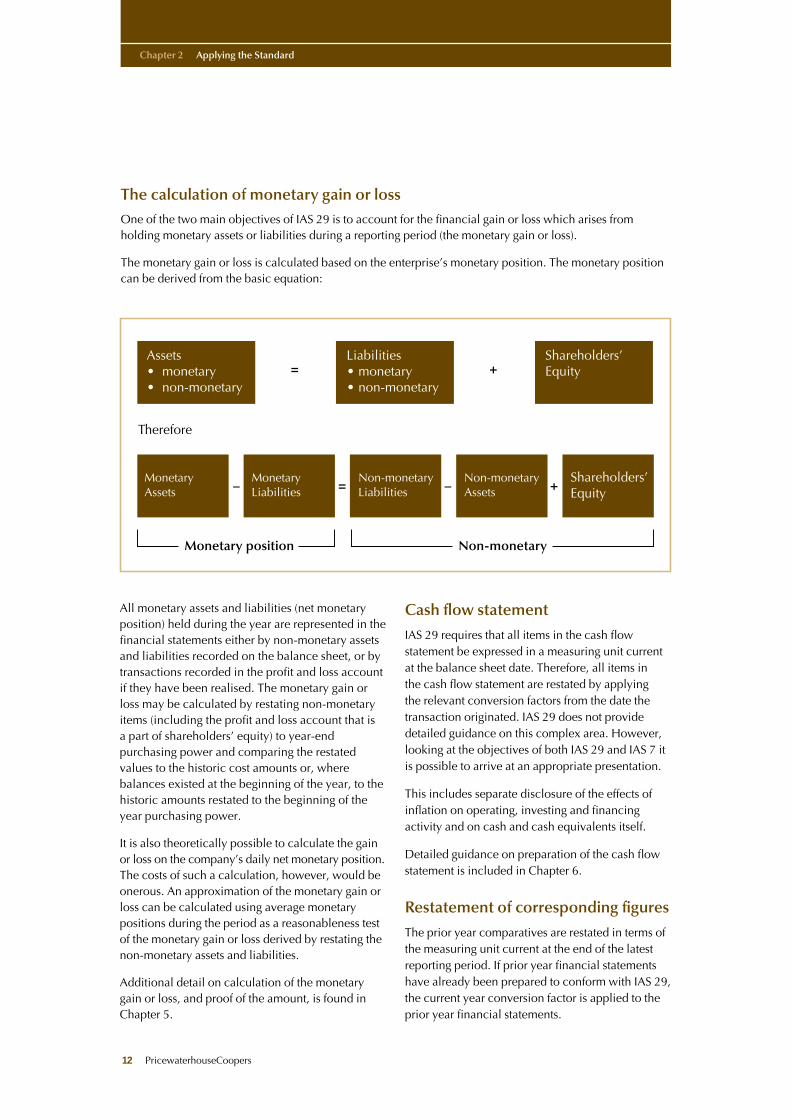

The calculation of monetary gain or lossOne of the two main objectives of IAS 29 is to account for the financial gain or loss which arises fromholding monetary assets or liabilities during a reporting period (the monetary gain or loss).

The monetary gain or loss is calculated based on the enterprise’s monetary position. The monetary positioncan be derived from the basic equation:

Chapter 2 Applying the Standard

12 PricewaterhouseCoopers

Shareholders’Equity

Assets• monetary• non-monetary

Liabilities• monetary• non-monetary

MonetaryAssets

MonetaryLiabilities

Non-monetaryAssets

Shareholders’Equity

Monetary position Non-monetary

Therefore

= +

Non-monetary Liabilities– = – +

All monetary assets and liabilities (net monetaryposition) held during the year are represented in thefinancial statements either by non-monetary assetsand liabilities recorded on the balance sheet, or bytransactions recorded in the profit and loss accountif they have been realised. The monetary gain orloss may be calculated by restating non-monetaryitems (including the profit and loss account that isa part of shareholders’ equity) to year-endpurchasing power and comparing the restatedvalues to the historic cost amounts or, wherebalances existed at the beginning of the year, to thehistoric amounts restated to the beginning of theyear purchasing power.

It is also theoretically possible to calculate the gainor loss on the company’s daily net monetary position.The costs of such a calculation, however, would beonerous. An approximation of the monetary gain orloss can be calculated using average monetarypositions during the period as a reasonableness testof the monetary gain or loss derived by restating thenon-monetary assets and liabilities.

Additional detail on calculation of the monetarygain or loss, and proof of the amount, is found inChapter 5.

Cash flow statement

IAS 29 requires that all items in the cash flowstatement be expressed in a measuring unit currentat the balance sheet date. Therefore, all items in the cash flow statement are restated by applying the relevant conversion factors from the date thetransaction originated. IAS 29 does not providedetailed guidance on this complex area. However,looking at the objectives of both IAS 29 and IAS 7 itis possible to arrive at an appropriate presentation.

This includes separate disclosure of the effects ofinflation on operating, investing and financingactivity and on cash and cash equivalents itself.

Detailed guidance on preparation of the cash flowstatement is included in Chapter 6.

Restatement of corresponding figures

The prior year comparatives are restated in terms ofthe measuring unit current at the end of the latestreporting period. If prior year financial statementshave already been prepared to conform with IAS 29,the current year conversion factor is applied to theprior year financial statements.

DisclosuresEnterprises should describe in their accountingpolicy note the methodology used in applying IAS29. The following specific information should bedisclosed in accordance with IAS 29:

• the fact that the financial statements and thecorresponding figures for previous periods havebeen restated for the changes in the generalpurchasing power of the reporting currency and,as a result, are stated in terms of the measuringunit current at the balance sheet date;

• the identity and level of the price index at thebalance sheet date and the movement in theindex during the current and the previousreporting period; and

• whilst not required by the standard it is useful todisclose the three-year cumulative inflation rate atthe balance sheet date for each period presentedin the financial statements.

Economies ceasing to behyperinflationaryWhen an economy ceases to be hyperinflationaryand a company discontinues the preparation andpresentation of financial statements in accordancewith IAS 29, it should treat the amounts expressedin the measuring unit current at the end of theprevious reporting period as the basis for the carryingamounts in its subsequent financial statements.Practically speaking, an enterprise will continue touse the restated amounts as the cost basis of thenon-monetary items in the balance sheet.

Enterprises preparing IAS accounts for the first time in economies which have ceased to behyperinflationary will need to make a cumulativeadjustment to the non-monetary items in the balancesheet. All adjustments to non-monetary items willbe charged or credited to retained earnings.

Although IAS 29 is no longer applicable in thissituation, an enterprise may, if it wishes, providesupplementary information reflecting the effects ofchanging prices using the guidance in IAS 15.

Chapter 2 Applying the Standard

PricewaterhouseCoopers 13

14 PricewaterhouseCoopers

PricewaterhouseCoopers 15

IntroductionAll non-monetary components of the balance sheet,excluding retained earnings, are restated by applyinga general price index from the dates on which theitems arose at the first application of IAS 29. Restatedretained earnings, excluding current year earnings,are the balancing figure derived from all the otheramounts in the opening restated balance sheet.

This chapter describes the detailed procedures forrestating non-monetary assets and liabilities.

Non-monetary items at fair value or net realisable valueSome non-monetary assets may be carried at fairvalue at the balance sheet date such as fixed assetsrevalued by an independent appraiser as allowedunder IAS 16, marketable equity securities fairvalued under IAS 39 and investment propertiescarried at fair value under fair value model ofIAS 40. The historic cost amounts should be restatedin order to obtain the appropriate monetary gain orloss. The restated carrying amount should then becompared to the “current” values and thedifference, if any, charged or credited to the incomestatement or shareholders’ equity in accordancewith the appropriate IAS.

The net realisable value of an asset may be less than its restated amount. Application of the normal“lower of cost and market value” rule wouldtherefore result in a write-down to net realisablevalue in the restated financial statements, even if

no write-down of the asset was required in thehistoric cost financial statements.

Prepaid expenses• Obtain the ageing of prepaid expenses.

• Restate prepaid expenses from the date of thepayments to the balance sheet date.

Restatement procedures for non-monetarybalance sheet items

Chapter 3

Marketable Securities

Should equity securities that are carried atfair value be restated?

Equity securities classified as either held fortrading assets or available-for-sale assets arecarried at fair value on the balance sheetunder IAS 39. Fair value gains and losses onheld for trading assets are recognisedimmediately in the income statement wherefair value gains and losses on available-for-sale assets are recognised, under a one-timepolicy choice, either in equity or in theincome statement. Fair value gains and lossesdeferred in equity are recycled to the incomestatement on disposal or impairment.

The treatment for IAS 29 requires the historiccost of the equity securities be restated. Thedifference between the fair value of the equitysecurities and the restated historic cost of theequity securities is the fair value gain or loss.

Frequently asked questions

Advances paid on purchases• Obtain a breakdown of advances paid ensuring

that where appropriate, the relevant specificadvances have already been netted off againstaccounts payable.

• For advances paid in respect of purchases offuture inventories or fixed assets, obtain theageing of advances, including the amounts andpayment dates.

• Restate advances according to the ageing schedulefrom the payment dates to the balance sheet date.

• When the inventory or fixed asset is received therestated carrying value of the advance should beadded to the restated cost base of the asset.

Inventories

Raw materials

• Obtain the historic cost prices and acquisitiondates of raw materials. If a detailed ageing ofinventory cannot be obtained, the average ageingof items could (subject to materiality considerations)be estimated using inventory turnover.

• If the FIFO or moving average method is used,restate raw materials inventories based on theageing of the related items using the increase inthe general price index for the period from thepurchase dates to the balance sheet date.

• If a yearly average is used, restate raw materialsusing the yearly average increase in the generalprice index.

Semi-finished/finished goods

• Obtain the ageing of semi-finished and finishedgoods.

• Deduct the historic depreciation expense ofproperty, plant and equipment that is included incost of semi-finished goods as this will bereplaced with the restated depreciation expense.

• If the FIFO or moving average method is used,restate the balance of semi-finished goods, basedon the ageing of the composition of cost elementsincluded in inventories. If yearly average costingis used, restate using the yearly average increasein the general price index.

• After completion of the restatement as mentionedabove, add back to inventory the attributabledepreciation calculated by reference to therestated property, plant and equipment balances.

• After the inventory has been restated, review therestated balances to determine the need for anynet realisable value provisioning.

Investments in associates• Obtain the historic cost prices and acquisition

dates of investments according to the purchasedate and cost of purchase.

• Restate the balance of investments, using theincrease in the general price index from thepurchase date to the balance sheet date.

• Compare the restated investment balance with the market value, and adjust the investmentbalance, if necessary, based on the lower ofrestated cost and market value.

Chapter 3 Restatement procedures for non-monetary balance sheet items

16 PricewaterhouseCoopers

Inventory

Will the costing method of inventory (forexample FIFO, LIFO, or weighted average)have an impact on the IAS 29 restatement?

The costing method should have no impacton the final restated value of the inventoryif there are no price changes in real terms.For example under both the FIFO and LIFOinventory costing methods, the historic cost of the inventory would be restated to year-endpurchasing power. In practice, there is likelyto be slightly different results as the changesin the cost of inventory may not be exactlyequal to the change in the general price index.

How are inventory and the related provisionfor impairment treated when the inventoryis subsequently sold or disposed of?

Inventory, and any provision against thecarrying value, is a non-monetary item. Assuch, the carrying value of both the inventoryand the provision should be inflated up to thedate of the sale or disposal.

Frequently asked questions

Chapter 3 Restatement procedures for non-monetary balance sheet items

PricewaterhouseCoopers 17

Property, plant and equipment andaccumulated depreciation• Obtain the original historic cost prices and

acquisition dates of property, plant andequipment. The restatement should be based onthe original purchase date of the asset, not thecapitalisation date.

• If existing, eliminate from the IAS historicfinancial statements any revaluation ofconstruction in progress, property, plant andequipment and the associated accumulateddepreciation that does not meet the conditionsof IAS 16.

• Restate the original purchase cost of property,plant and equipment from the date of thepurchase of each item to the balance sheet date,using the general price index.

• Calculate the depreciation charge for the periodon the basis of the restated property, plant andequipment. Opening accumulated depreciation isalso calculated on the basis of restated property,plant and equipment.

• For disposals determine the original date ofpurchase and the historic cost. Calculate and thendeduct the restated property, plant and equipmentbalance that has been disposed of and itsaccumulated depreciation.

• Historic depreciation charges included in generaladministrative expenses, idle time expenses, costof goods sold and inventory balances should bereplaced with the depreciation expensecalculated on the basis of the restated property,plant and equipment balances.

Subsidiaries and associates

What exchange rates should be used whenconsolidating a foreign subsidiary of an entityreporting in a hyperinflationary economy?

If the foreign subsidiary is operating in aneconomy that is not experiencing hyperinflationthe income statement should be translated usingthe historic exchange rates (in practice averageexchange rates may be used). The incomestatement items should then be restated inaccordance with IAS 29 from the date of thetransaction (which would be the same date usedto translate the foreign currency into the localhyperinflationary currency). This will facilitatethe elimination of any inter-companytransactions as the transactions will be on thesame basis of accounting and thus be comparable.

The balance sheet should be translated into thehyperinflationary currency using the closing ratemethod. The investor’s share of net assets in thesubsidiary at the beginning of the year (ascalculated by the equity method of accounting)should be adjusted for current year inflation.The difference between the parent’s share of theclosing net assets and the opening balance and

earnings for the period both adjusted for inflationas described above should be charged to equityas a translation adjustment.

What exchange rates should be used whenequity accounting for a foreign associate of anentity reporting in a hyperinflationaryeconomy?

The investor’s share of the results of operationswould be translated into the reporting entitiescurrency at the dates the earnings accrued. Theearnings would then be restated to year-endpurchasing power in accordance with IAS 29 in theconsolidated accounts from the date of translation.

The opening investment balance accounted forusing the equity method at opening exchangerates should be adjusted for inflation to year-endpurchasing power. To calculate the netinvestment in the associate, the investee’sbalance sheet should be translated into thereporting currency at year end rates, which formsthe basis for carrying value of the investment.The difference between the carrying value andthe opening balance plus earnings for the period,both adjusted for inflation, should be charged toequity as a translation adjustment.

Frequently asked questions

• Obtain the historic cost prices and acquisitiondates of the construction in progress balance andrestate the balances by applying indicesaccording to transaction date. When theconstruction in progress is subsequentlytransferred to fixed assets the related inflationadjustment should be transferred and applied tothe asset.

• If the company capitalises interest in accordancewith IAS 23, the part of the capitalised borrowingcost that compensates for the inflation during thesame period should be recognised as an expensein the period in which those costs were incurred.

• If the company capitalises exchange losses inaccordance with the allowed alternativetreatment in IAS 21, such exchange losses should(for the purpose of IAS 29) be recognised as anexpense in the period in which they arise.

• For the initial year of adopting the IAS 16 alternativetreatment for measurement, the historic cost of thefixed asset would be restated in accordance withIAS 29 in order to obtain the correct monetarygain or loss in the income statement. The carryingvalue would then be replaced with the appraisedvalue, the difference should be treated inaccordance with IAS 16.39 or 16.40.

• Assess for impairment in accordance with IAS 36.

Intangible assets• Intangible assets, including goodwill, are inflated in

the same manner as property, plant, and equipment.

Advances received• Obtain a breakdown of advances received

ensuring that, where appropriate, the relevantspecific advances have been netted off against the relevant accounts receivable.

• Obtain the ageing of advances received.

• Restate advances according to the ageing andincrease in the general price level from the date of receipt to the balance sheet date.

• When the sale is realised the restated advancesreceived should be added to the sales value.

Deferred income (for instance grants)• Obtain the ageing of deferred income according

to the date of receipt.

• Restate the original amount of deferred incomereceived from the transaction date to the balancesheet date.

• Calculate accumulated amortisation and currentperiod amortisation on the basis of the restateddeferred income balance.

• Replace historic amortisation credited to theincome statement with the amortisation calculatedon the basis of the restated deferred income.

Chapter 3 Restatement procedures for non-monetary balance sheet items

18 PricewaterhouseCoopers

Property, plant, and equipment

What indices are used to restate constructionin progress (CIP)? How does the restatementof CIP affect the future value of fixed assets?

CIP should be restated from the date thepayment was made. An asset or project withinCIP should be restated within CIP. Whencapitalised, the related inflation adjustmentshould be transferred to fixed assets and addedto the cost base of the item being transferred.

When an entity is initially adopting IAS 29where the economy of the reporting entity hasbeen experiencing hyperinflation in previousyears, it is important to consider the inflationeffect on fixed assets which were previouslyheld in CIP

Frequently asked questions

▼

How are assets that have been remeasuredby an independent appraiser in accordancewith IAS 16 treated when restating the fixedassets in accordance with IAS 29?

If assets are revalued during a year ofrestatement the historic cost should be restatedin order to arrive at the correct monetary gainor loss. The restated cost would then becompared to the appraised amount, thedifference would be treated as noted in IAS 16.In subsequent years the appraised carryingamount and the revaluation reserve (unless itis first year of IAS 29 application wheneliminated) would be restated.

Deferred tax assets and liabilities• See “Taxation on income” on page 22.

Restatement of shareholders’ equity• At the beginning of the first period of application

of IAS 29, the components of shareholders’ equityin the opening balance sheet, excluding retainedearnings, are restated by applying a general priceindex from the dates on which the items arose. Anyrevaluation surplus that arose in previous periods iseliminated. Restated retained earnings is thebalancing figure derived from all the other restatedamounts in the restated opening balance sheet.

• At the end of the first period and in subsequentperiods, all components of shareholders’ equityare restated by applying a general price indexfrom the beginning of the period, or the dates onwhich the items arose if later. This restatementforms part of the monetary gain or loss calculation.

• Any statutory revaluation surplus (that is not inaccordance with IAS 16) arising in subsequentperiods is eliminated against the related assetsrevalued.

• Current year restated net income is added to thebalance of the restated opening retained earnings.

• For the purpose of the statement of changes inshareholders’ equity, dividends paid during aperiod should be restated by applying a general

price index from the date when the shareholders’right to receive payment is established to thebalance sheet date.

Chapter 3 Restatement procedures for non-monetary balance sheet items

PricewaterhouseCoopers 19

Provisions for liabilities and charges

Are provisions for liabilities and chargesmonetary or non-monetary items, forexample should we recognise a gain as aresult of holding provision or not?

Provisions for liabilities and charges could bemonetary, monetary but inflation linked, ornon-monetary. Their classification dependson the nature of liability exposed. If warrantyobligations are limited to a defined originalamount, the warranty provision is monetary.If the enterprise’s liability is specified as arepair or exchange of the item under warranty,the liability is non-monetary.

Frequently asked questions

Equity

What are the components of shareholders’equity that need to be restated? Which datesshould be used for the restatement?

All components of shareholders’ equity shouldbe restated, with certain exceptions forrevaluation reserves. Legal and extraordinaryreserves are generally become a part ofretained earnings in IAS accounts. Thesereserves are not considered for restatementpurposes. It may be beneficial to disclose thehistoric statutory reserves in the footnotes tothe financial statements.

Capital increases should be restated from the date the consideration was received. If consideration was received in the form of anon-monetary contribution (such as fixedassets contributed), the fair value of the assetshould be used as the historic cost.

How is the revaluation reserve in equity treated?

Very often statutory regulations for countriesoperating in a hyperinflationary economyallow companies to increase the carrying valueof fixed assets based on prescribed rules, with acorresponding increase to the equity – usuallycalled the revaluation reserve. Generally, thesestatutory revaluation adjustments are not inaccordance with IAS 16, Property Plant, andEquipment, and, should be eliminated from theIAS accounts.

If a revaluation has been performed at year-endin accordance with IAS 16, the revaluationreserve would be the difference between the historic values restated in accordancewith IAS 29 and the revalued amounts per IAS16. There would be no need to inflate therevaluation reserve, as it would be current atyear-end. In subsequent years the revaluationreserve would be inflated.

Frequently asked questions

▼

Chapter 3 Restatement procedures for non-monetary balance sheet items

20 PricewaterhouseCoopers

Equity – continuedHow should a share capital increase by way of a transfer from the statutory revaluation surplusbe treated?

As noted above, the statutory revaluationsurplus is eliminated from the IAS restatedfinancial statements. Thus, a share capitalincrease by way of a transfer from the statutoryrevaluation surplus is not considered incalculating the restated paid-in capital. Theincrease of the share capital will be offset by areduction of retained earnings. The amount ofthe increase to be disclosed is the restatedamount of statutory increase inflated as from thedate of increase authorisation.

How are dividends payable treated?

A dividend payable is a monetary liability thatwill result in a monetary gain for the company.Therefore, the dividend amount should beexcluded from retained earnings at the date thedividend becomes payable.

Should unpaid capital that the shareholdershave committed to pay be inflated?

The treatment of the unpaid share capital dependson whether the shareholder is legally bound to

pay-up the capital or whether the commitmentis nothing more than an unbinding promiseto pay.

If the shareholder has no legal obligation to paythis capital there would be no receivablerecorded in the company’s books. The unpaidcapital and commitment would be disclosed inthe footnotes at the historic amounts which isthe consideration expected to be received bythe company. There is no effect on monetarygain or loss, as the company does not have anenforceable receivable.

However, if the capital increase is legallybinding, and approved by the generalassembly, the company would show areceivable from shareholders with acorresponding increase in share capital (thefact that the share capital has not been paid-upwould be disclosed in the footnotes). The sharecapital would be restated to account for anysubsequent changes in inflation that creates amonetary loss in the income statement fromholding the receivable.

PricewaterhouseCoopers 21

All items in the income statement should be restatedby applying the change in the general price indexfrom the dates when the items of income andexpense were originally recorded.

Provided inflation is occurring at a relatively stablerate during the year, most enterprises will restateactivity on a monthly average basis, with alltransactions presumed to occur evenly throughout therelevant period. This chapter describes the detailedprocedures for restating the income statement.

Revenue• Obtain a monthly break down of revenue.

Restate each period using the appropriate indicesto year-end.

Cost of goods sold• Obtain the monthly breakdown of the items

included in production costs.

• Restate all components of production costs,except depreciation and raw materials, from the month when the costs were incurred to theyear-end.

• Calculate raw material used in the productionprocess through the reconciliation of restatedopening raw materials and closing raw materials balances.

• Calculate depreciation related to production costs on the basis of the restated property, plantand equipment, as explained on balance sheetsection, and replace the historic depreciation with this restated depreciation.

• Restate opening and closing historic finished andsemi-finished goods as explained on balancesheet section.

• The restated cost of goods sold figure is obtainedby adding to purchases and other productioncosts restated from the date when the cost was

Restatement of the Income Statement

Chapter 4

Selection of the indexWhat is the correct index to be used torestate the income statement?

The items within the income statement shouldbe restated from the date of the transaction.Having said this, it is generally not practical torestate the items from the date of the transaction,therefore, average indices may be used as approx-imations. The average indices to use woulddepend on the frequency of the transaction (in other words sales earned evenly throughoutthe period) and whether inflation wasrelatively constant throughout the period.

Frequently asked questions

▼

If the income statement transactions occurredevenly throughout the year, without seasonalfluctuations, and inflation was relativelyconstant during the year, the yearly averageindex may be used for the restatement. Inpractical terms, this is never the case and useof monthly indices is more appropriate.

incurred the restated opening finished and semi-finished goods and deducting the restatedclosing finished and semi-finished goods. The restated opening finished goods and semi-finished goods is derived by:

– Restating amounts to the prior balance sheet datepurchasing power, and

– Inflating the restated cost of opening amounts ascalculated above by the conversion factor for theentire year.

Depreciation, amortisation ofintangible assets and realisation ofprepaid expenses and deferredincome (grant)• Depreciation of property, plant and equipment,

amortisation of intangible assets and realisation of prepaid expenses and deferred income iscalculated on the basis of the restated asset and/orliability balance.

Other items included in the incomestatement• Obtain the monthly breakdown of all items.

• Restate all items for each month using theincrease in the general price index from therelated month or quarter until the year-end.

• Certain non-monetary items being included in theopening balance sheet could be realised throughthe income statement for the period, for exampleinventory and disposed property, plant andequipment. In that case the restatement should beapplied with taking into account the restatementsurplus accumulated whilst the item wasrecognised on the balance sheet.

Adjustments and/or reclassificationsmade to statutory financialstatements in order to arrive at IAShistoric financial statements• If the adjustment and/or reclassification made in

accordance with IAS is related to a specific period or specific date, the adjustment and/orreclassification calculated in historic terms shouldbe restated for the related time period, using theincrease in the general price index from thespecific date to the balance sheet date.

Taxation on income

Current taxation

• Obtain details of monthly or quarterly taxationcalculated on the basis of the monthly or quarterlytaxable income of the company. Restate monthlyor quarterly tax expenses for each month orquarter in terms of balance sheet date purchasingpower, using the increase in the general priceindex from the related month or quarter until thereporting date.

Chapter 4 Restatement of the Income Statement

22 PricewaterhouseCoopers

Foreign exchange

Should interest income or expense andforeign exchange gains or losses be restated?

IAS 29.26 states that all items in the incomestatement should be restated. There are noexceptions to this rule.

Frequently asked questions

Bad debts

If the bad debt expense is inflated themovement schedule of the provision does not reconcile. How then does the openingand closing balance reconcile?

At the time the debt is considered bad it isprovided against. The provision is a monetaryitem as the underlying asset it relates to ismonetary. Therefore a monetary gain willresult from carrying this provision (whichactually offsets the monetary loss beingincurred as a result of holding the receivable).The bad debt expense is inflated from the date the provision was made.

To ensure the reconciliation of the provisionaccount, all items must be in terms of themeasuring unit current at the balance sheetdate. The difference between the restatedopening balance, restated current periodexpense (net of any restated provision reversals)and the closing balance is a monetary gain.

Frequently asked questions

Deferred taxation

• Calculate deferred tax expense/income anddeferred tax liability/asset with reference tohistoric adjustments made (if any) in moving fromthe tax accounts to the IAS historic financialstatements.

• Calculate deferred tax in relation to temporarydifferences arising from the restatement of non-monetary assets and liabilities. According to IAS 12 (revised) deferred tax is calculated in fullon the temporary differences arising from therestatement of non-monetary assets and liabilities.

• As the closing deferred tax position is calculatedas the difference between the tax base and the IAS 29 adjusted financial statements (that is to saymeasuring unit current at the balance sheet date)there is no need to adjust the closing deferred taxbalance for inflation. The difference between theopening deferred tax balance, adjusted to year-end purchasing power, and the closing deferredtax balance is the deferred tax expense or creditfor the period.

Monetary gain/loss

• The gain or loss on the net monetary position arisesfrom holding monetary assets and liabilities, andis reported as a separate item in the restated incomestatement (see Chapter 5 for additional detail onthe monetary gain or loss). The monetary gain orloss is derived from restating the closing balancesheet (less the inflation adjustments to the openingbalance sheet in prior year-end purchasingpower) and the items in the income statement.

• The derived amount may need additional nettingoff with the indexation differences occurred in theincome statement on those monetary items thatare linked to inflation index and as such, beingnot subject to inflationary risks or holdingbenefits, such as monetary gains or losses.

Chapter 4 Restatement of the Income Statement

PricewaterhouseCoopers 23

24 PricewaterhouseCoopers

PricewaterhouseCoopers 25

Calculation and proof of the monetary gain or loss isan important element of applying IAS 29. This chaptercontains several methods to prove the accuracy ofthe monetary gain or loss arising from restatement.

The monetary gain or loss may be estimated byapplying the change in a general price index to theweighted average difference between monetaryassets and monetary liabilities. The weightedaverage of the opening monetary position and themonetary position at year-end may be used for thepurpose of this calculation. It is possible, however,that a large difference may arise between themonetary gain or loss in the income statement andthe estimate as calculated by the proof if themonetary position has not been relatively constantthroughout the year.

Therefore, if the monetary position is changingsignificantly a more accurate proof of the monetarygain or loss would be obtained by using thequarterly or monthly weighted average monetaryposition in the proof calculation.

Proof – average monetary position methodA simple example with a constant monetaryposition is set forth below. In this example it wouldbe appropriate to use the weighted average of theopening and closing monetary position.

Proof – statement of sources andapplication of net monetary assetsand liabilities methodIn addition, a statement of source and application of net monetary assets or liabilities is often preparedas alternative proof of the net monetary gain or loss(see below). The items which cause changes in themonetary assets/liabilities are analysed, and the net balance of the monetary assets/liabilities isdetermined as if there were no changes first, andthen you should adjust for current year movements.Restatements are performed and the comparisonwith the actual net balance and movements ofmonetary assets or liabilities enables the monetarygain or loss to be approximated.

Monetary gain or loss

Chapter 5

Chapter 5 Monetary gain or loss

26 PricewaterhouseCoopers

Procedures for preparation of a statement ofsource and application of net monetary assetsand liabilities are as follows:

Historic column:1. Calculate the net monetary position at the

beginning of the period under restatement.

2. Identify all items that caused changes in themonetary position during the period. Theseshould be the actual or uninflated changes inthe monetary position. These items can beobtained from the historic cost incomestatement and/or cash flow statement.

3. Arrive at the monetary position at the end ofthe period by adding or subtracting thechanges as identified. Check that monetaryposition as calculated is equal to the actualmonetary position at the end of the period.

Restated column:4. Calculate the net monetary position at the

beginning of the period as in step 1 above, but restate it for inflation for the entire period.The inflation adjustment restates the openingmonetary position as if there were no monetarygain or loss, in other words by adjusting theopening monetary position as if the openingmonetary assets and liabilities were not erodedas a result of inflation.

5. Inflate the changes in the monetary position(step 2 above) but restate as if there were no

monetary gain or loss, for example adjustingthe changes in monetary position for inflationrestates the monetary changes as if themonetary assets and liabilities obtained ordisposed of during the period were not erodedas a result of inflation. These items may beobtained from the inflation adjusted incomestatement and/or cash flow statement.

6. Determine the net monetary position restatedat period end as if inflation had not effectedthe monetary assets and liabilities. Note thatthe real monetary position does not change asa result of the inflation adjustment.

Proof:7. Compare the actual net monetary position at

the end of the period included in the “historic”column with the restated net monetary positionat the end of the period in the “restated”column. The difference between the actualposition and the restated monetary position is the estimate of the monetary gain or loss.This estimate should be compared to theactual gain or loss in the income statement.

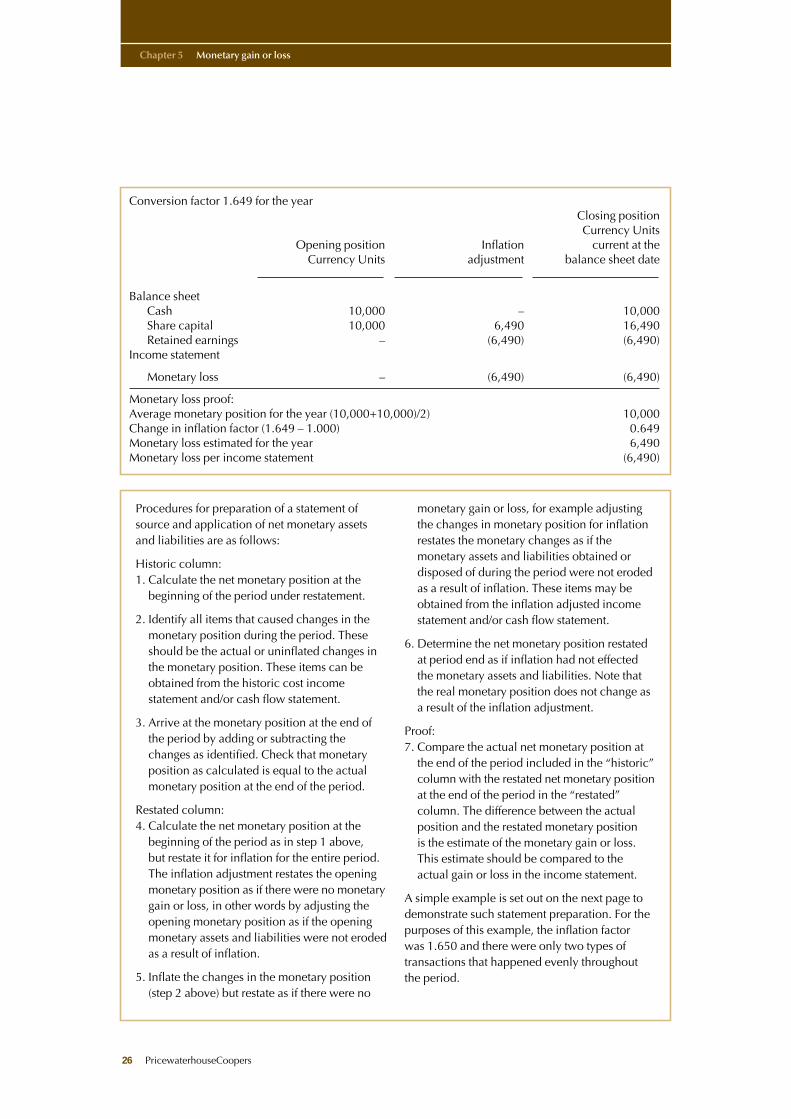

A simple example is set out on the next page todemonstrate such statement preparation. For thepurposes of this example, the inflation factor was 1.650 and there were only two types oftransactions that happened evenly throughoutthe period.

Conversion factor 1.649 for the yearClosing positionCurrency Units

Opening position Inflation current at theCurrency Units adjustment balance sheet date

Balance sheetCash 10,000 – 10,000Share capital 10,000 6,490 16,490Retained earnings – (6,490) (6,490)

Income statement

Monetary loss – (6,490) (6,490)

Monetary loss proof:Average monetary position for the year (10,000+10,000)/2) 10,000Change in inflation factor (1.649 – 1.000) 0.649Monetary loss estimated for the year 6,490Monetary loss per income statement (6,490)

Closing positionat period end

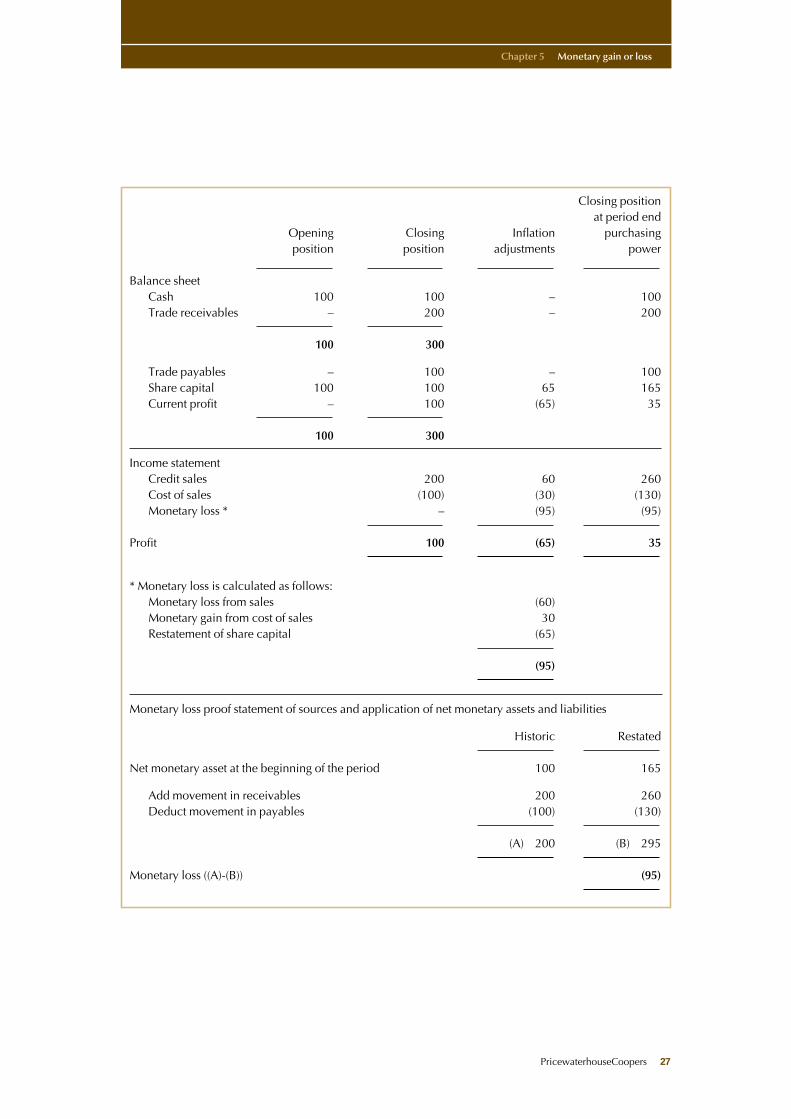

Opening Closing Inflation purchasingposition position adjustments power

Balance sheetCash 100 100 – 100Trade receivables – 200 – 200

100 300

Trade payables – 100 – 100Share capital 100 100 65 165Current profit – 100 (65) 35

100 300

Income statementCredit sales 200 60 260Cost of sales (100) (30) (130)Monetary loss * – (95) (95)

Profit 100 (65) 35

* Monetary loss is calculated as follows:Monetary loss from sales (60)Monetary gain from cost of sales 30Restatement of share capital (65)

(95)

Monetary loss proof statement of sources and application of net monetary assets and liabilities

Historic Restated

Net monetary asset at the beginning of the period 100 165

Add movement in receivables 200 260Deduct movement in payables (100) (130)

(A) 200 (B) 295

Monetary loss ((A)-(B)) (95)

Chapter 5 Monetary gain or loss

PricewaterhouseCoopers 27

28 PricewaterhouseCoopers

PricewaterhouseCoopers 29

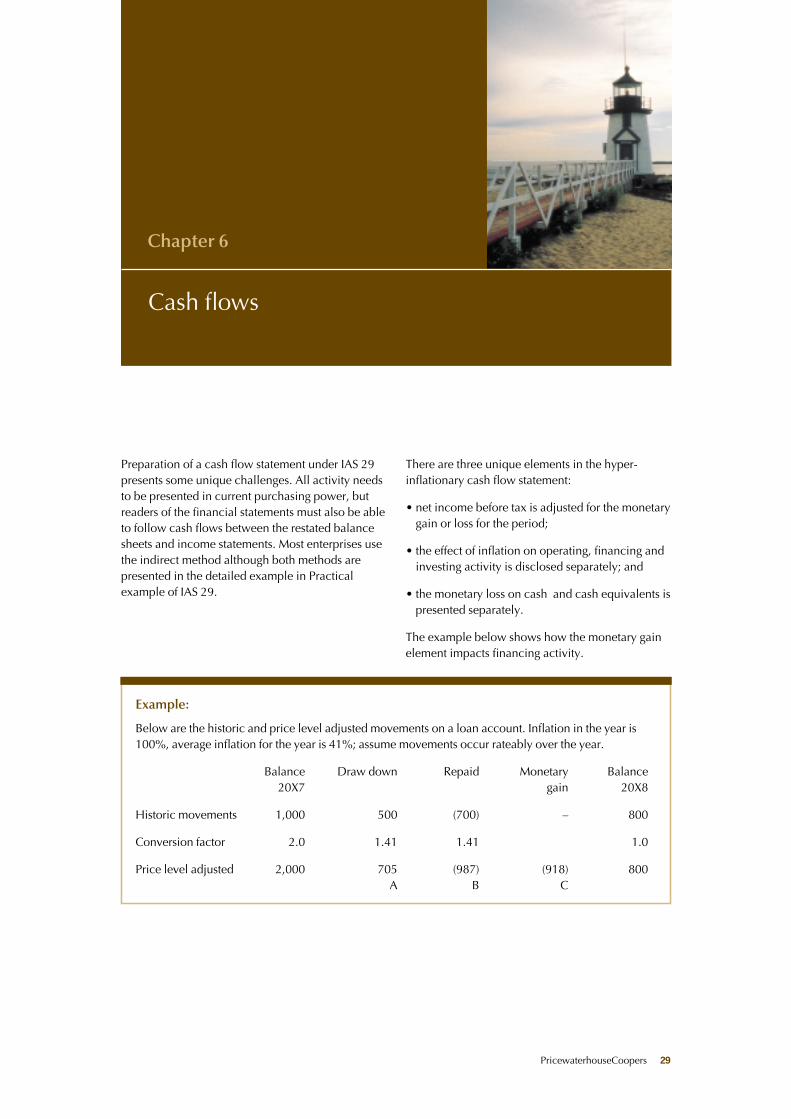

Preparation of a cash flow statement under IAS 29presents some unique challenges. All activity needsto be presented in current purchasing power, butreaders of the financial statements must also be ableto follow cash flows between the restated balancesheets and income statements. Most enterprises usethe indirect method although both methods arepresented in the detailed example in Practicalexample of IAS 29.

There are three unique elements in the hyper-inflationary cash flow statement:

• net income before tax is adjusted for the monetarygain or loss for the period;

• the effect of inflation on operating, financing andinvesting activity is disclosed separately; and

• the monetary loss on cash and cash equivalents ispresented separately.

The example below shows how the monetary gainelement impacts financing activity.

Cash flows

Chapter 6

Example:

Below are the historic and price level adjusted movements on a loan account. Inflation in the year is100%, average inflation for the year is 41%; assume movements occur rateably over the year.

Balance Draw down Repaid Monetary Balance20X7 gain 20X8

Historic movements 1,000 500 (700) – 800

Conversion factor 2.0 1.41 1.41 1.0

Price level adjusted 2,000 705 (987) (918) 800A B C

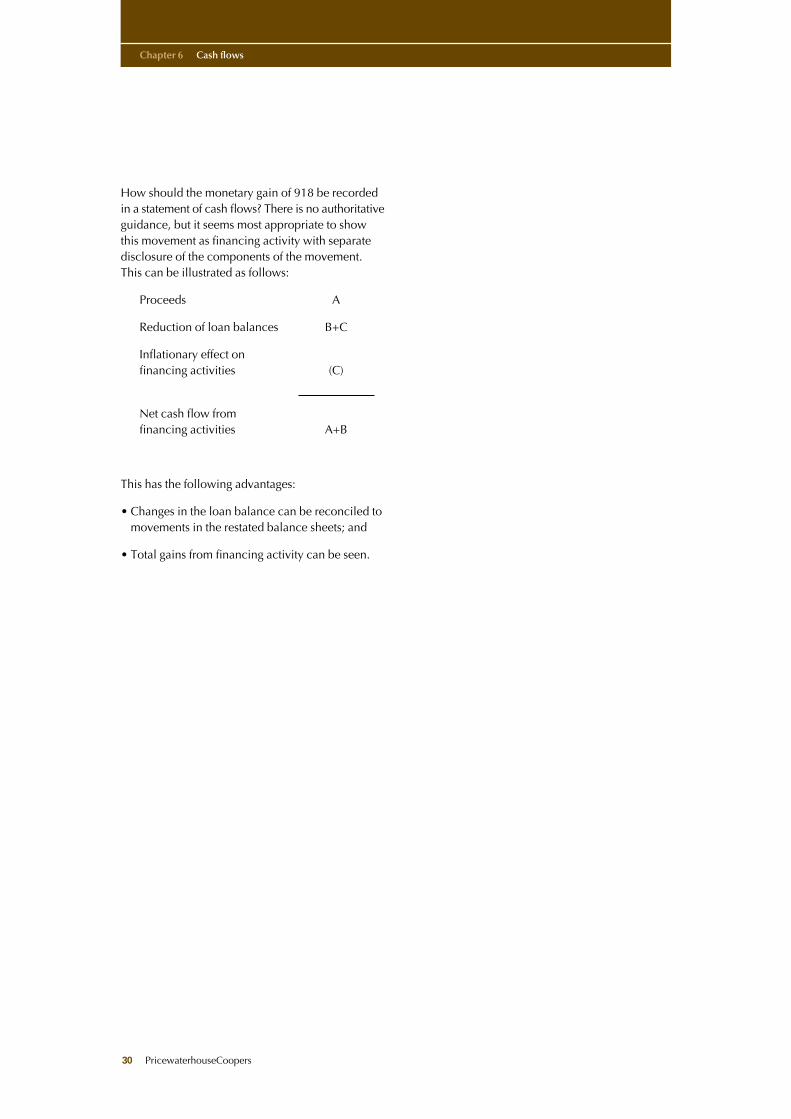

How should the monetary gain of 918 be recordedin a statement of cash flows? There is no authoritativeguidance, but it seems most appropriate to showthis movement as financing activity with separatedisclosure of the components of the movement.This can be illustrated as follows:

Proceeds A

Reduction of loan balances B+C

Inflationary effect on financing activities (C)

Net cash flow from financing activities A+B

This has the following advantages:

• Changes in the loan balance can be reconciled tomovements in the restated balance sheets; and

• Total gains from financing activity can be seen.

Chapter 6 Cash flows

30 PricewaterhouseCoopers

PricewaterhouseCoopers 31

This section of the guide provides a detailedpractical example of the application of IAS 29. The term ‘restated’ is used to describe financialstatements after the application of IAS 29. Theterm ‘historic’ is used to describe financialstatements before restatement to currentpurchasing power. This example is prepared forillustrative purposes only, income statement,statement of changes in shareholders’ equity andstatement of cash flows are presented for one year.

Under IAS 1 comparative figures of thesestatements are required to be disclosed by thereporting enterprise.

This example does not cover all possiblecircumstances, nor does it take account of anyspecific legal framework. Depending on thecircumstances, further specific information may berequired in order to ensure fair presentation underInternational Accounting Standards.

Practical example of IAS 29

Chapter 7

A Historical Financial Statements (without notes)A.I Historical Balance Sheets as at 31 December 2003 and 2002 34A.II Historical Income Statement for the year ended 31 December 2003 35A.III Historical Statement of Cash Flows for the year ended 31 December 2003 36–37A.IV Historical Statement of Changes in Equity for the year ended

31 December 2003 38

B Additional Historical Information Required for IAS 29 RestatementB.I Property, Plant and Equipment 39B.II Investments

B.II.1 Investment in associated undertaking 40B.II.2 Other long-term investments 40B.II.3 Trading investments 40

B.III Inventories and Production Expenditures IncurredB.III.1 Inventory movements for the year 41B.III.2 Analysis of production costs incurred within the period 41B.III.3 Holding period of inventory 41

B.IV EquityB.IV.1 Share capital 42B.IV.2 Dividends 42

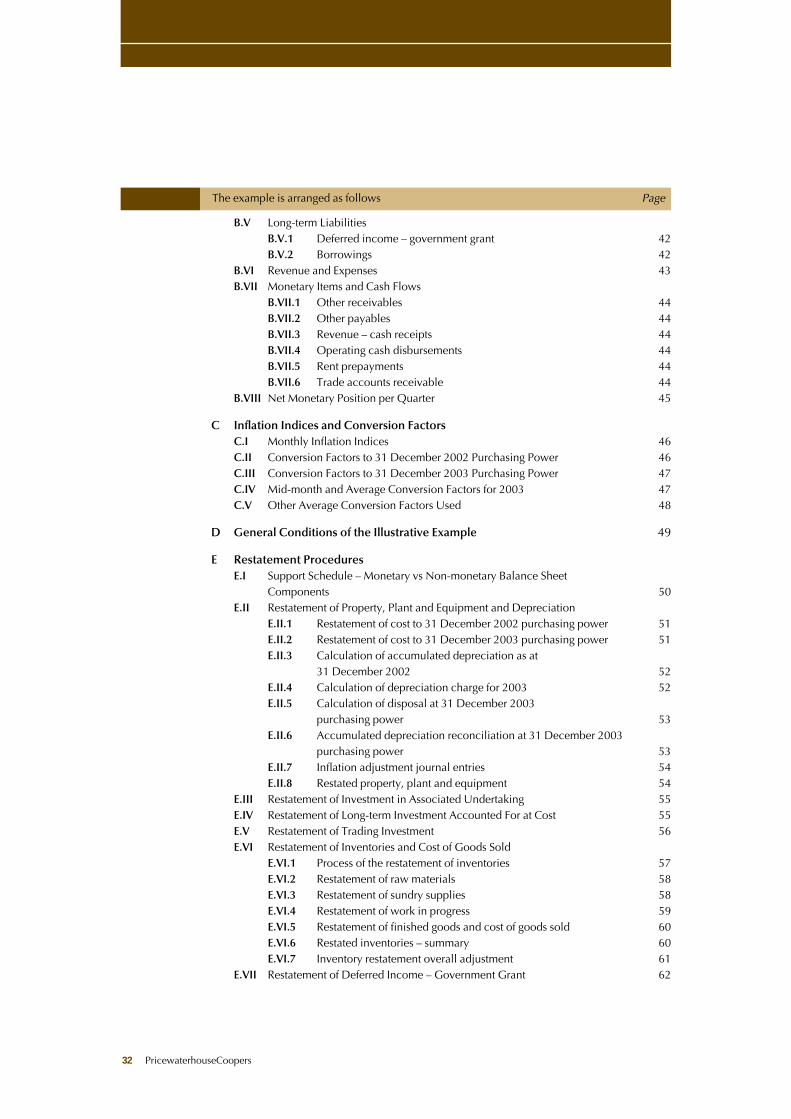

The example is arranged as follows Page

B.V Long-term LiabilitiesB.V.1 Deferred income – government grant 42B.V.2 Borrowings 42

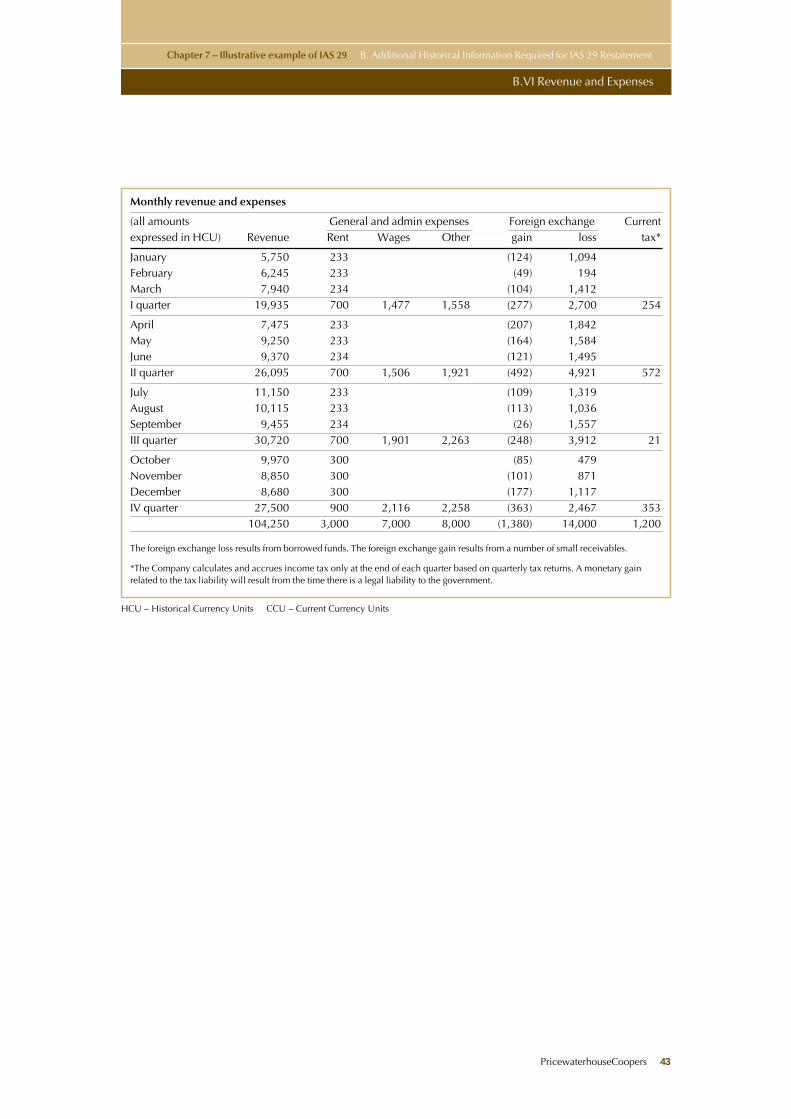

B.VI Revenue and Expenses 43B.VII Monetary Items and Cash Flows

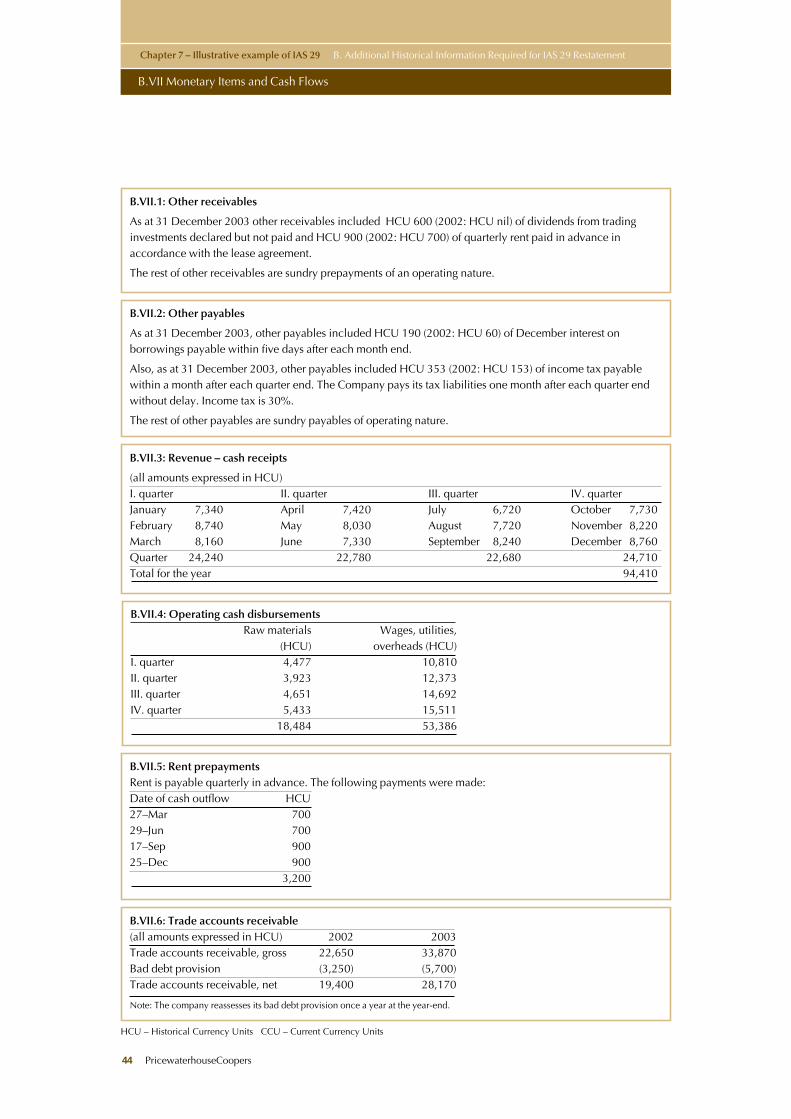

B.VII.1 Other receivables 44B.VII.2 Other payables 44B.VII.3 Revenue – cash receipts 44B.VII.4 Operating cash disbursements 44B.VII.5 Rent prepayments 44B.VII.6 Trade accounts receivable 44

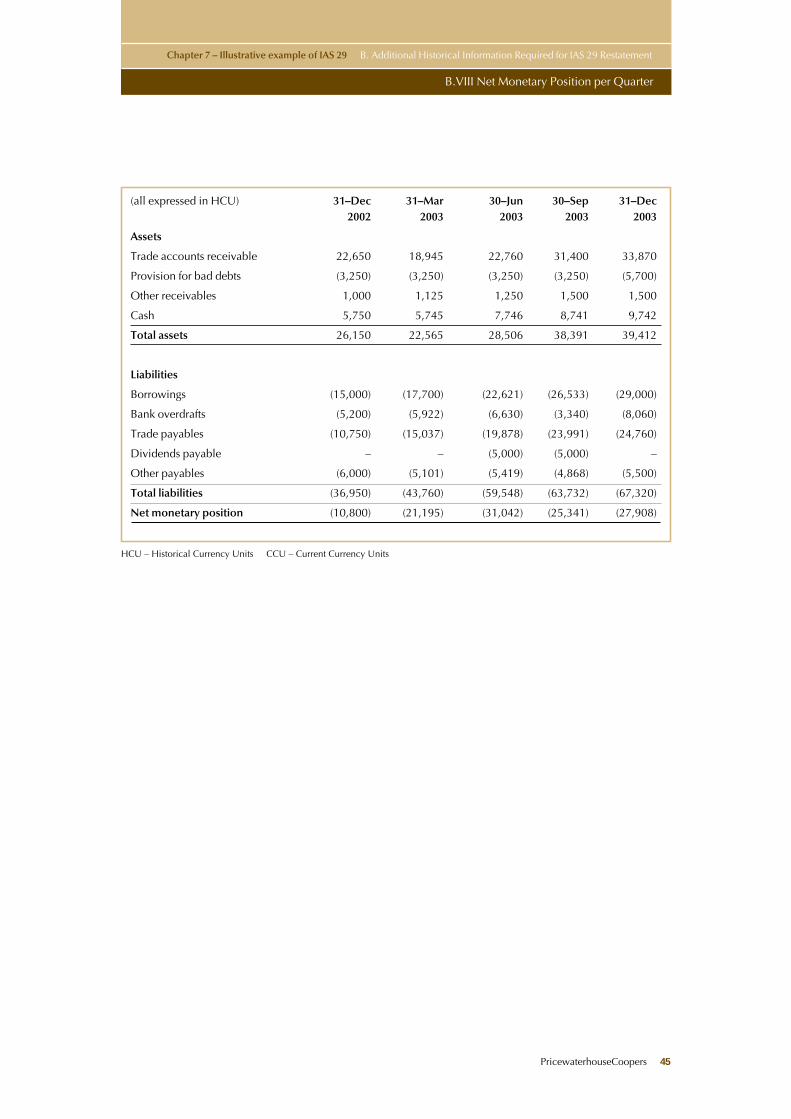

B.VIII Net Monetary Position per Quarter 45

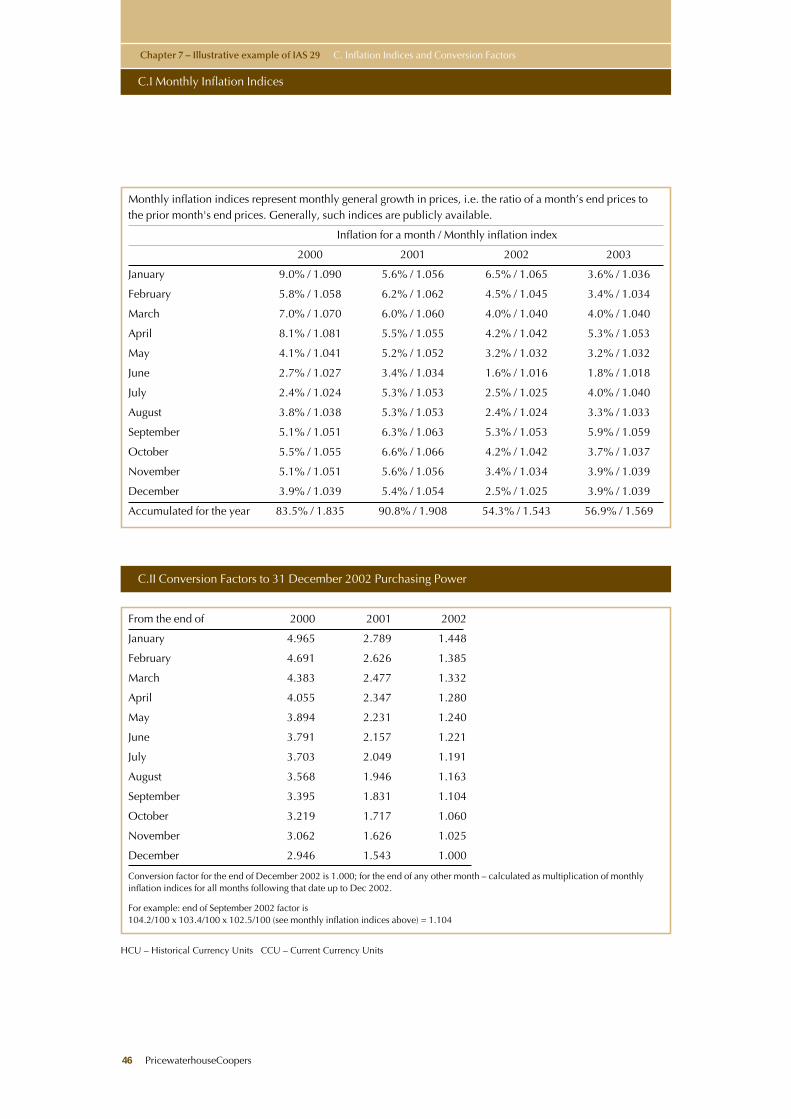

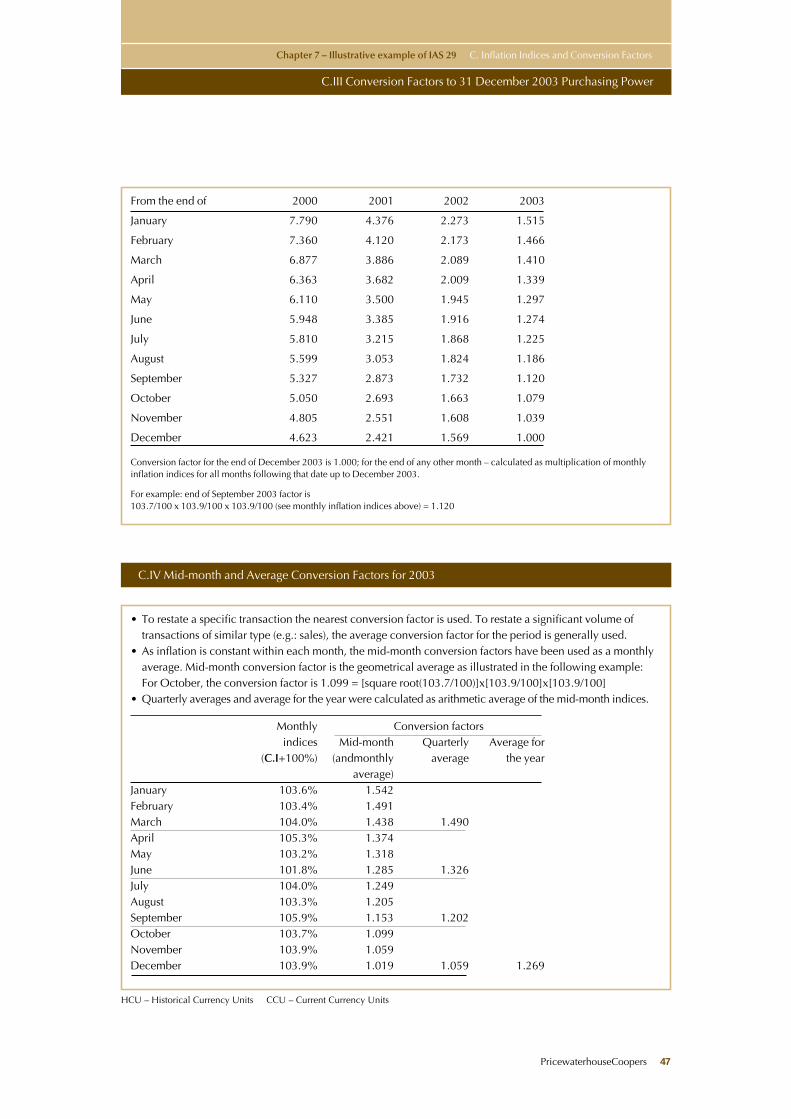

C Inflation Indices and Conversion FactorsC.I Monthly Inflation Indices 46C.II Conversion Factors to 31 December 2002 Purchasing Power 46C.III Conversion Factors to 31 December 2003 Purchasing Power 47C.IV Mid-month and Average Conversion Factors for 2003 47C.V Other Average Conversion Factors Used 48

D General Conditions of the Illustrative Example 49

E Restatement ProceduresE.I Support Schedule – Monetary vs Non-monetary Balance Sheet

Components 50E.II Restatement of Property, Plant and Equipment and Depreciation

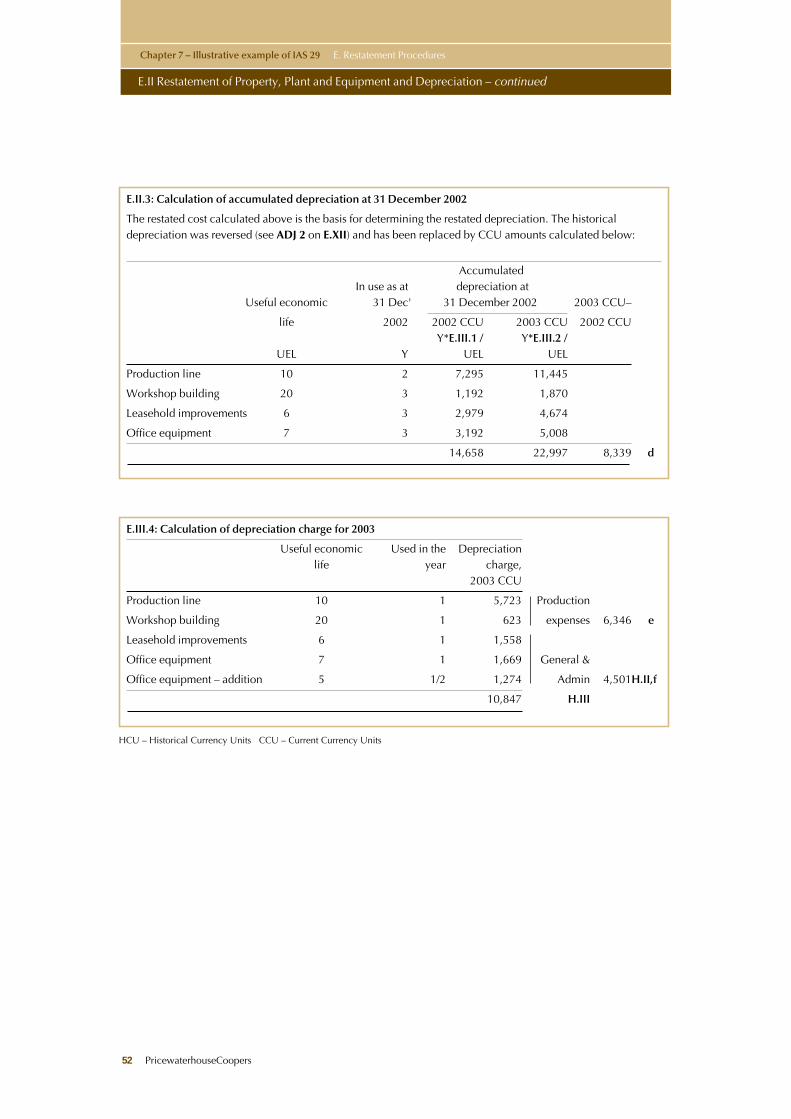

E.II.1 Restatement of cost to 31 December 2002 purchasing power 51E.II.2 Restatement of cost to 31 December 2003 purchasing power 51E.II.3 Calculation of accumulated depreciation as at

31 December 2002 52E.II.4 Calculation of depreciation charge for 2003 52E.II.5 Calculation of disposal at 31 December 2003

purchasing power 53E.II.6 Accumulated depreciation reconciliation at 31 December 2003

purchasing power 53E.II.7 Inflation adjustment journal entries 54E.II.8 Restated property, plant and equipment 54

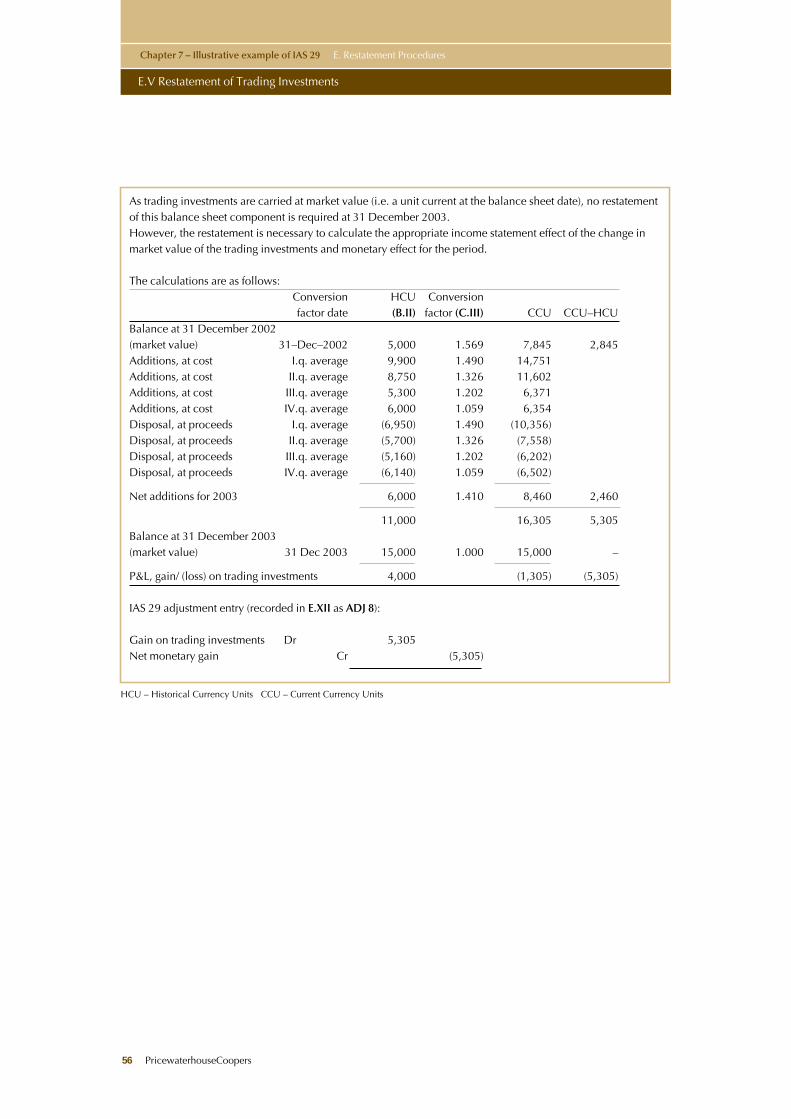

E.III Restatement of Investment in Associated Undertaking 55E.IV Restatement of Long-term Investment Accounted For at Cost 55E.V Restatement of Trading Investment 56E.VI Restatement of Inventories and Cost of Goods Sold

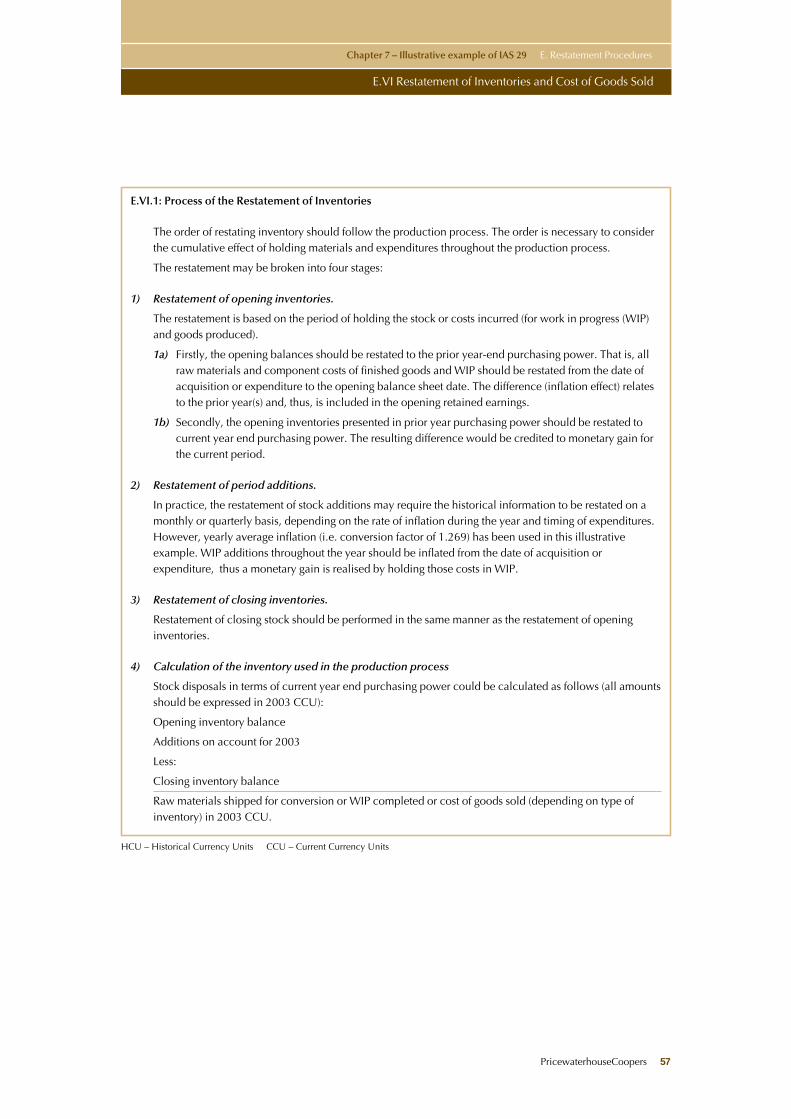

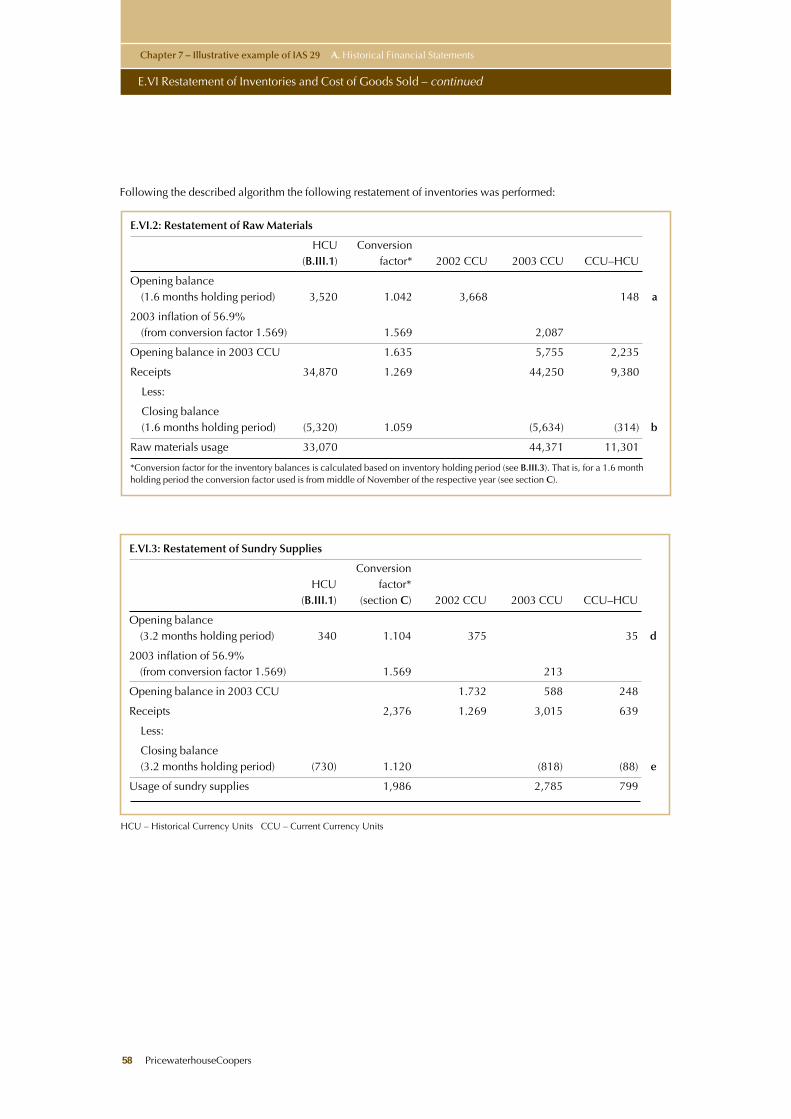

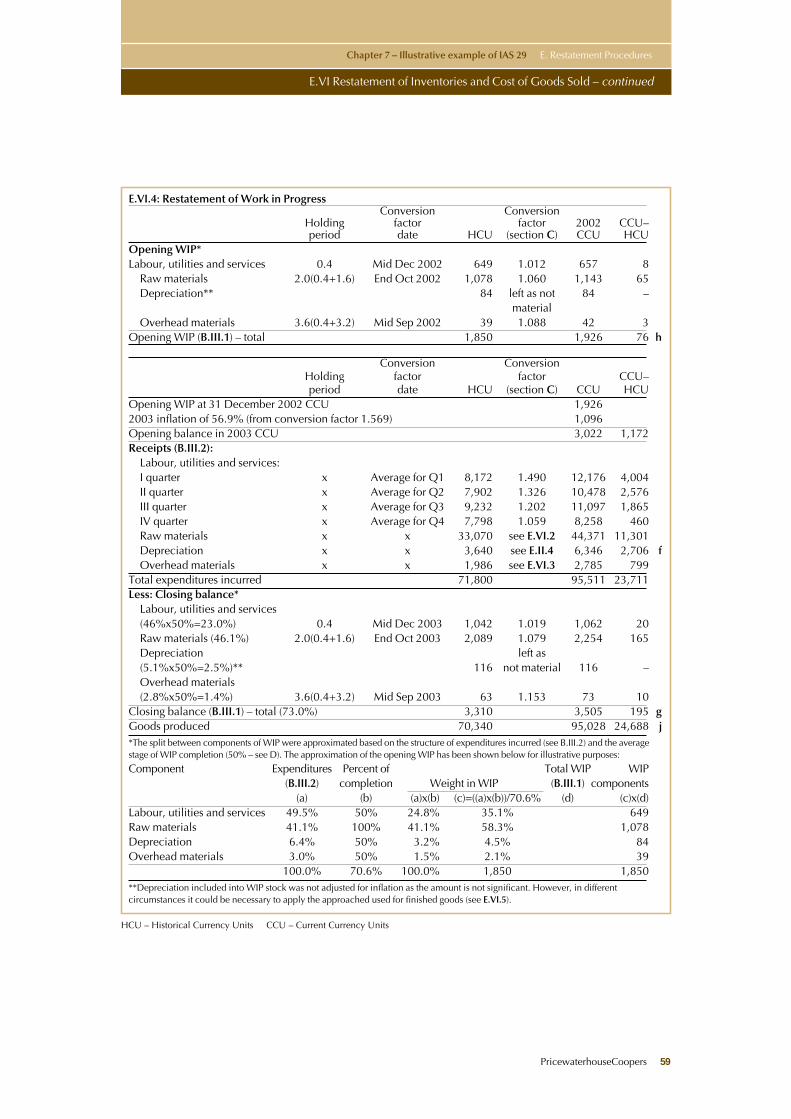

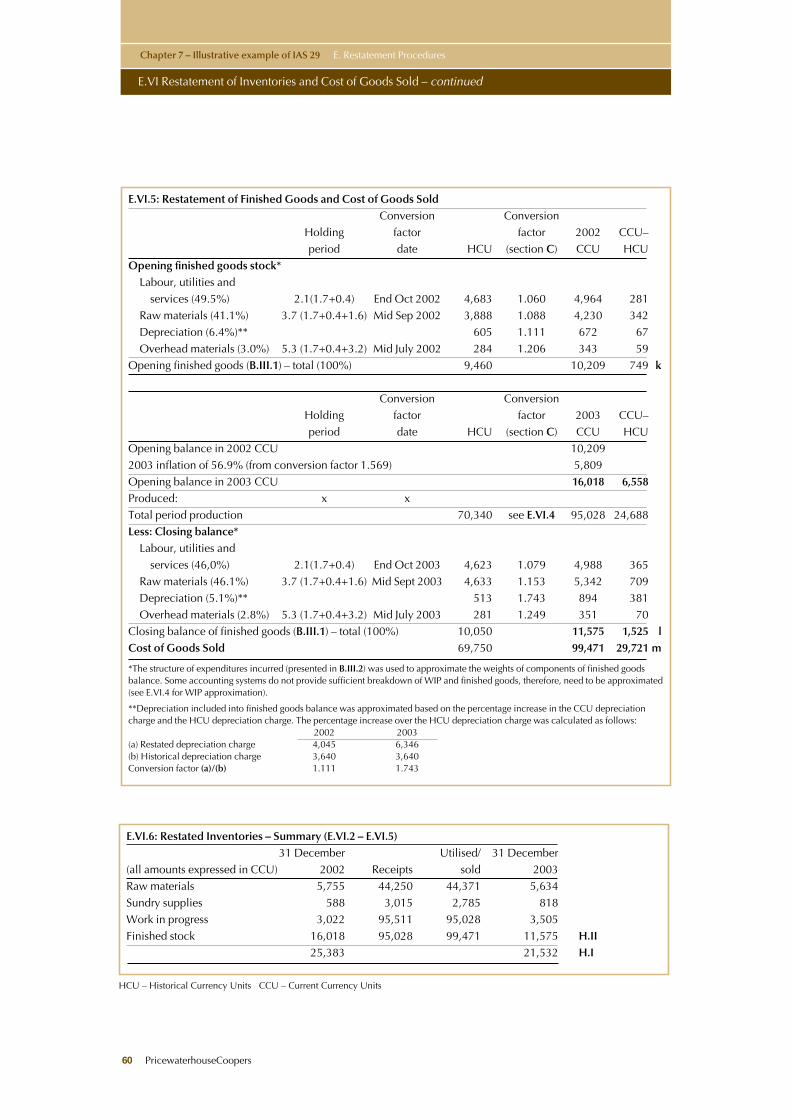

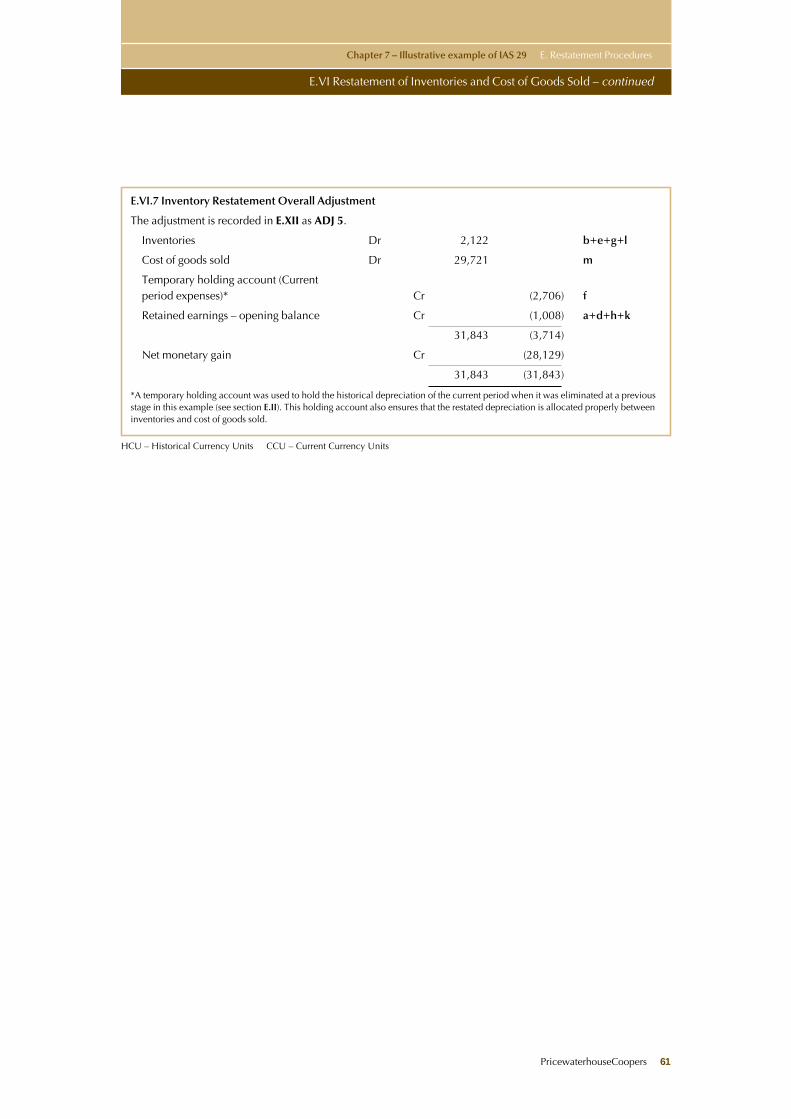

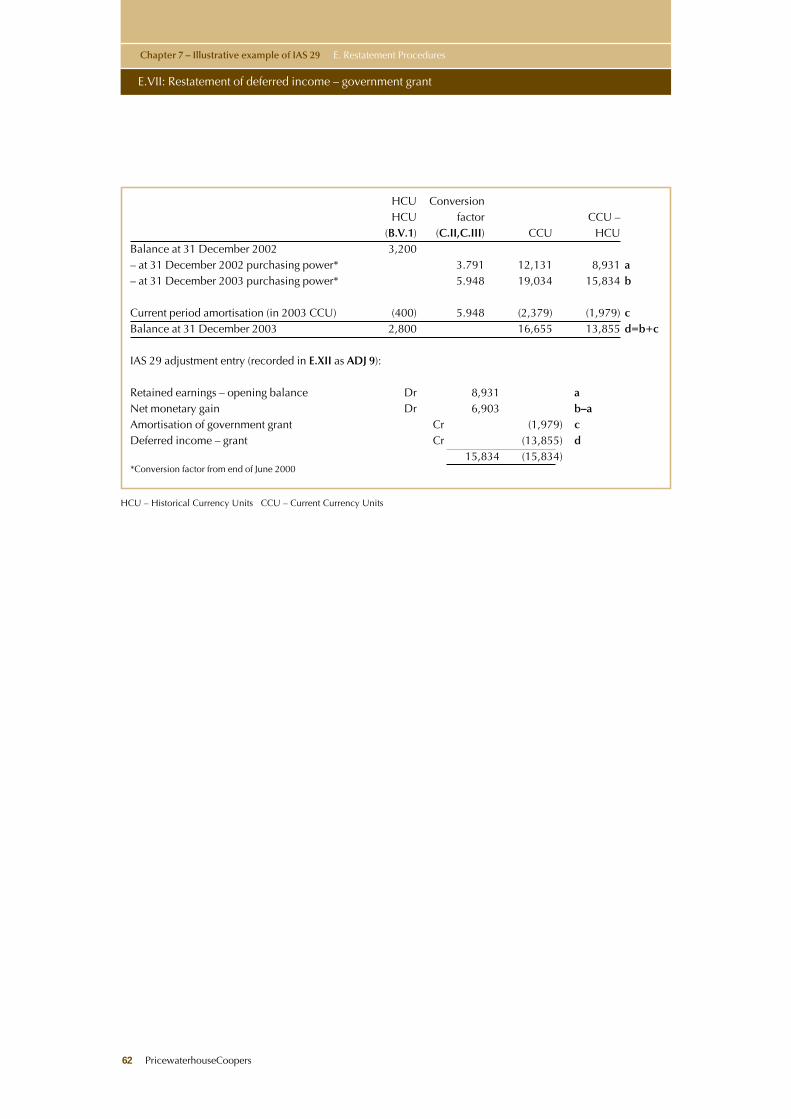

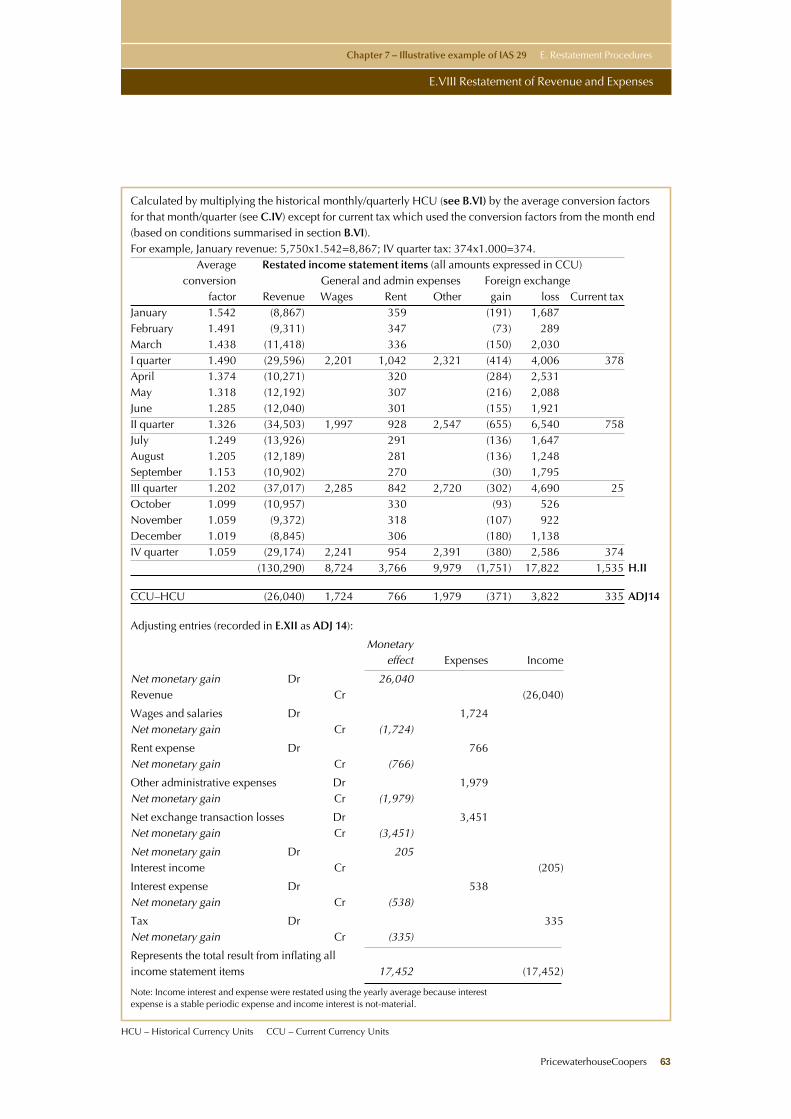

E.VI.1 Process of the restatement of inventories 57E.VI.2 Restatement of raw materials 58E.VI.3 Restatement of sundry supplies 58E.VI.4 Restatement of work in progress 59E.VI.5 Restatement of finished goods and cost of goods sold 60E.VI.6 Restated inventories – summary 60E.VI.7 Inventory restatement overall adjustment 61

E.VII Restatement of Deferred Income – Government Grant 62

32 PricewaterhouseCoopers

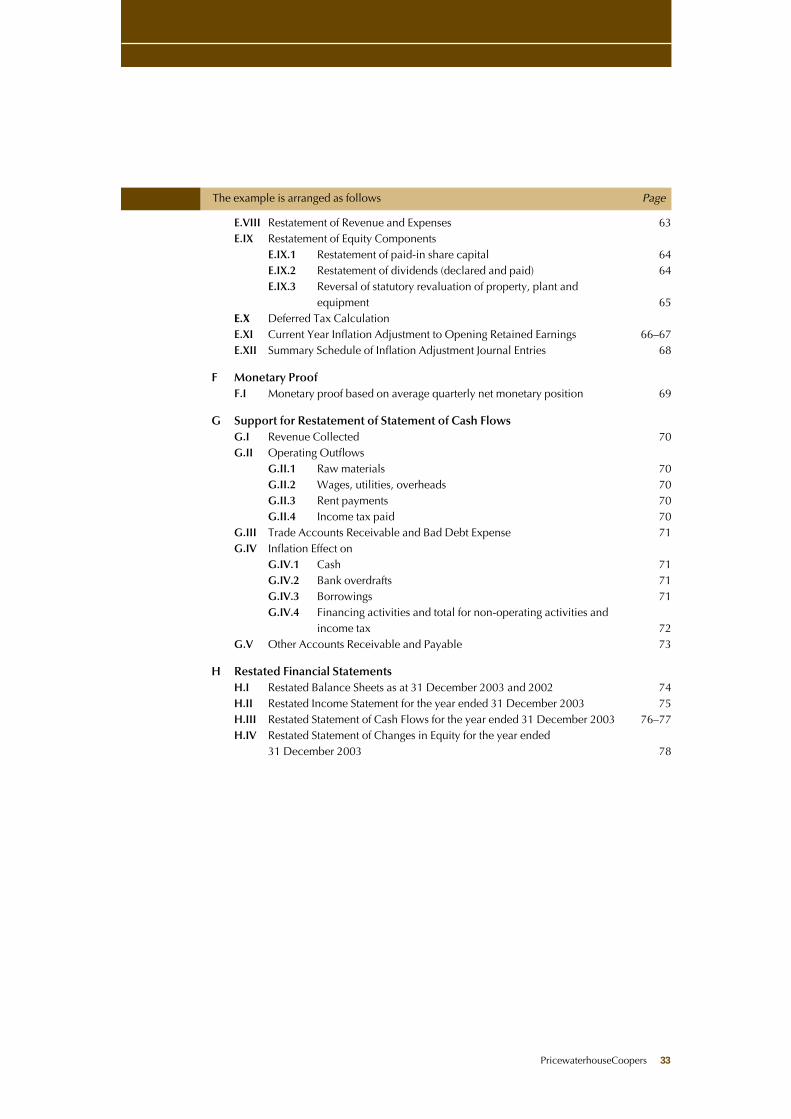

The example is arranged as follows Page

E.VIII Restatement of Revenue and Expenses 63E.IX Restatement of Equity Components

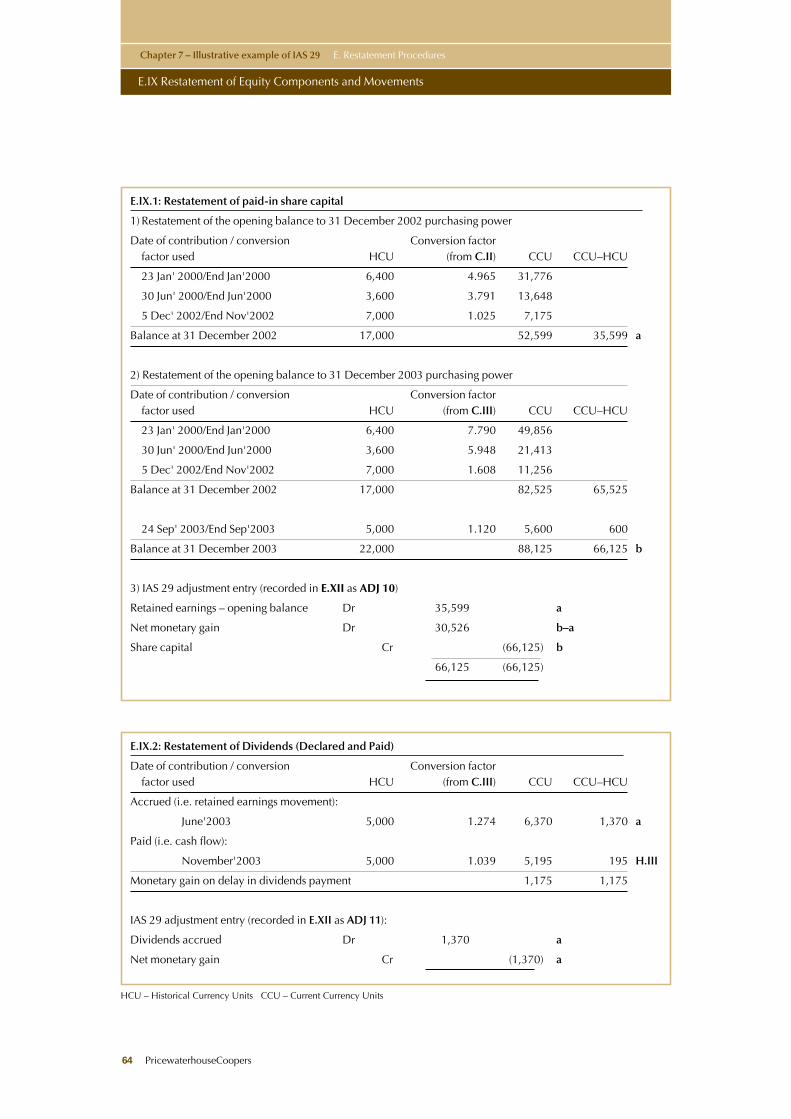

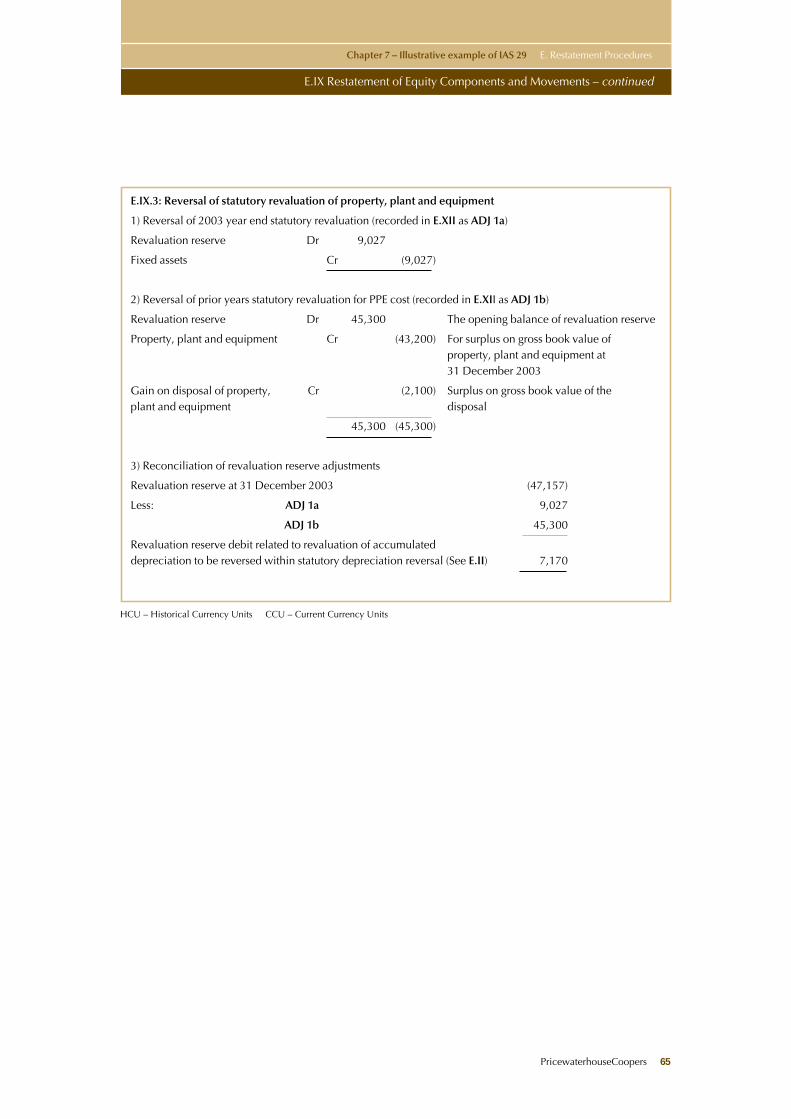

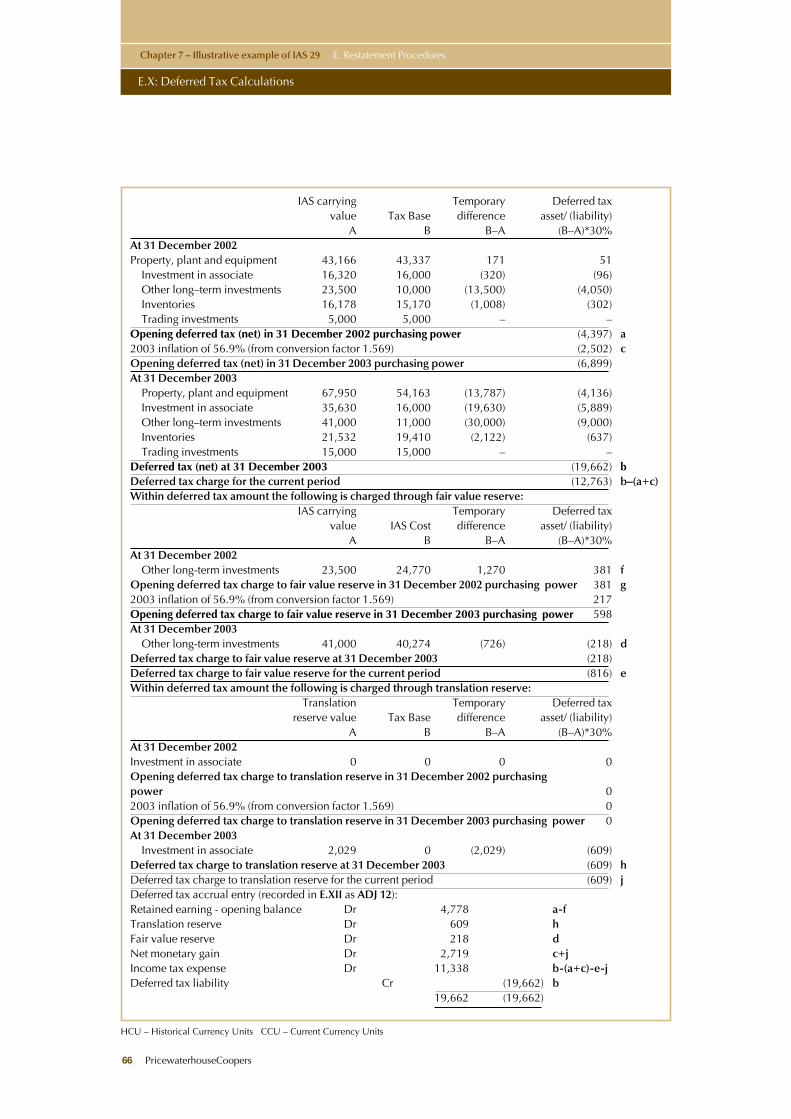

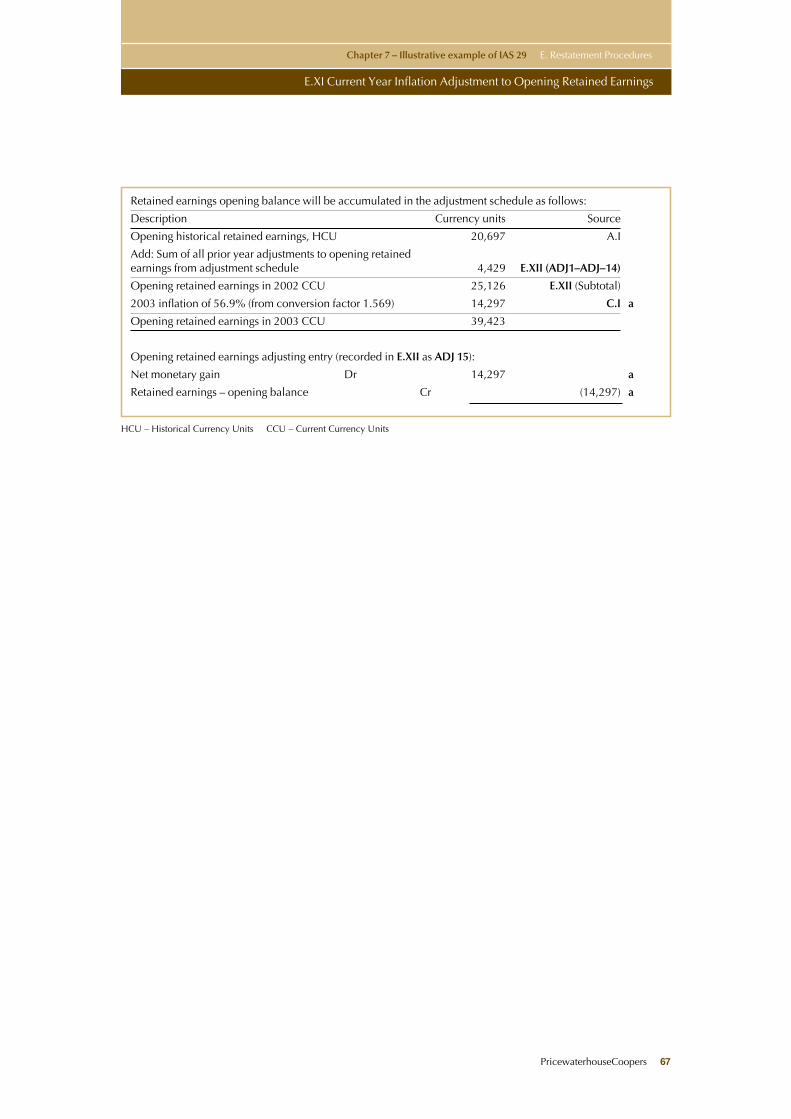

E.IX.1 Restatement of paid-in share capital 64E.IX.2 Restatement of dividends (declared and paid) 64E.IX.3 Reversal of statutory revaluation of property, plant and

equipment 65E.X Deferred Tax CalculationE.XI Current Year Inflation Adjustment to Opening Retained Earnings 66–67E.XII Summary Schedule of Inflation Adjustment Journal Entries 68

F Monetary ProofF.I Monetary proof based on average quarterly net monetary position 69

G Support for Restatement of Statement of Cash FlowsG.I Revenue Collected 70G.II Operating Outflows

G.II.1 Raw materials 70G.II.2 Wages, utilities, overheads 70G.II.3 Rent payments 70G.II.4 Income tax paid 70

G.III Trade Accounts Receivable and Bad Debt Expense 71G.IV Inflation Effect on

G.IV.1 Cash 71G.IV.2 Bank overdrafts 71G.IV.3 Borrowings 71G.IV.4 Financing activities and total for non-operating activities and

income tax 72G.V Other Accounts Receivable and Payable 73

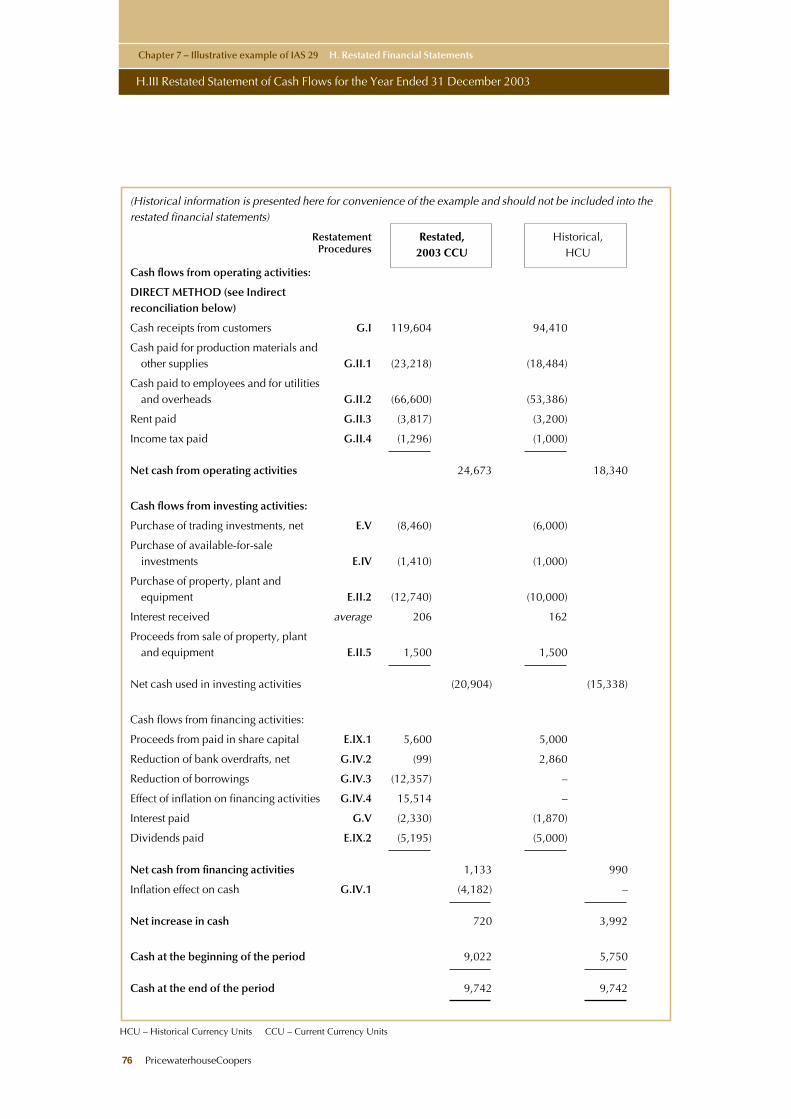

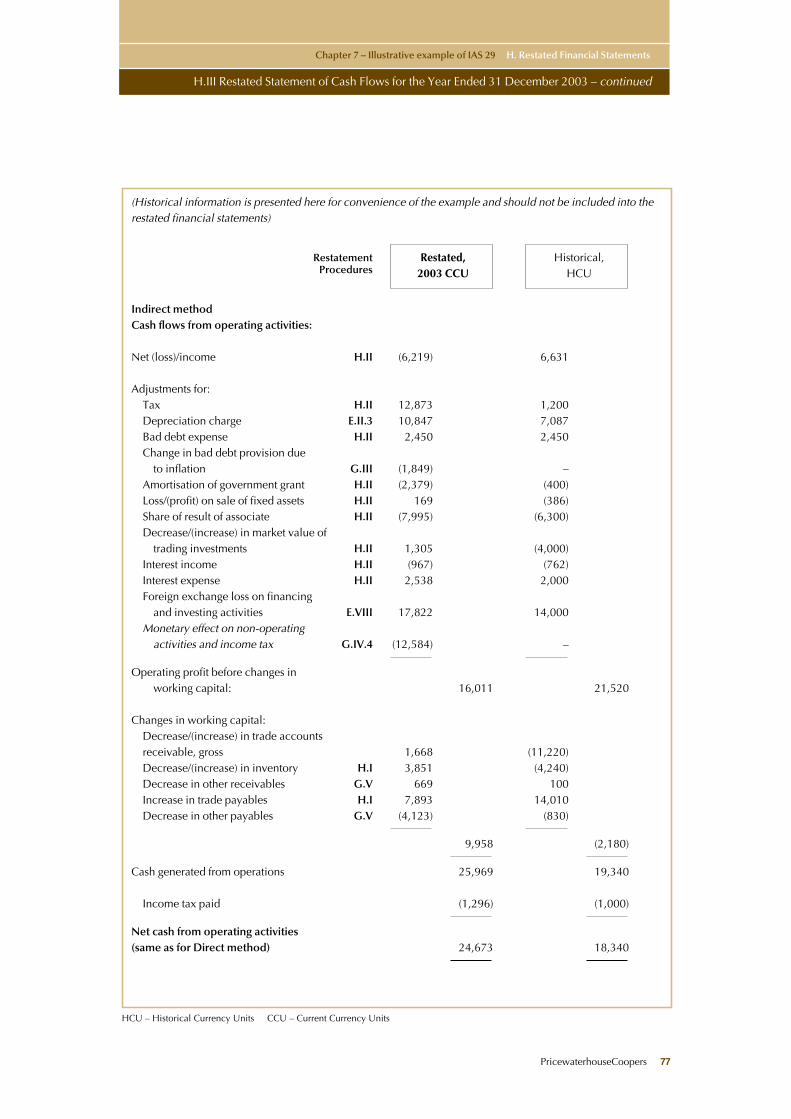

H Restated Financial StatementsH.I Restated Balance Sheets as at 31 December 2003 and 2002 74H.II Restated Income Statement for the year ended 31 December 2003 75H.III Restated Statement of Cash Flows for the year ended 31 December 2003 76–77H.IV Restated Statement of Changes in Equity for the year ended

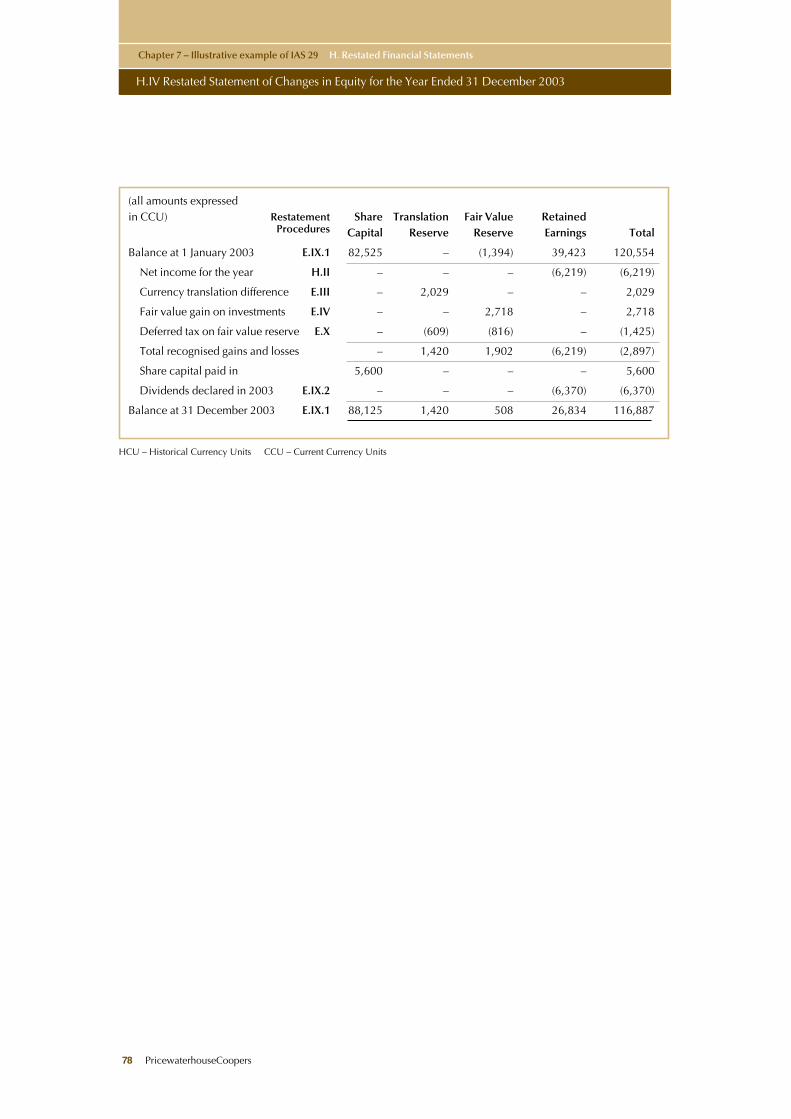

31 December 2003 78

PricewaterhouseCoopers 33

The example is arranged as follows Page

x

34 PricewaterhouseCoopers

HCU – Historical Currency Units CCU – Current Currency Units

Chapter 7 – Practical example of IAS 29 A. Historical Financial Statements

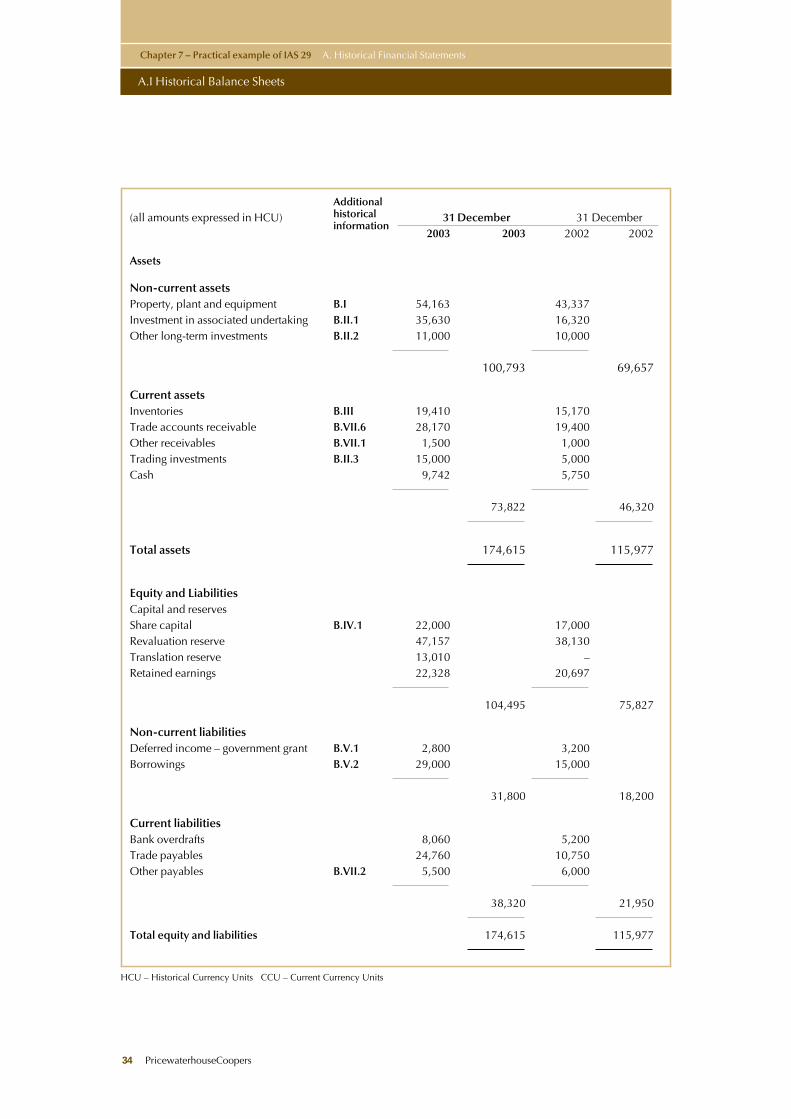

A.I Historical Balance Sheets

Additional

(all amounts expressed in HCU) historical 31 December 31 Decemberinformation

2003 2003 2002 2002

Assets

Non-current assetsProperty, plant and equipment B.I 54,163 43,337 Investment in associated undertaking B.II.1 35,630 16,320Other long-term investments B.II.2 11,000 10,000

100,793 69,657

Current assetsInventories B.III 19,410 15,170Trade accounts receivable B.VII.6 28,170 19,400Other receivables B.VII.1 1,500 1,000Trading investments B.II.3 15,000 5,000Cash 9,742 5,750

73,822 46,320

Total assets 174,615 115,977

Equity and LiabilitiesCapital and reservesShare capital B.IV.1 22,000 17,000Revaluation reserve 47,157 38,130Translation reserve 13,010 –Retained earnings 22,328 20,697

104,495 75,827

Non-current liabilitiesDeferred income – government grant B.V.1 2,800 3,200Borrowings B.V.2 29,000 15,000

31,800 18,200

Current liabilitiesBank overdrafts 8,060 5,200Trade payables 24,760 10,750Other payables B.VII.2 5,500 6,000

38,320 21,950

Total equity and liabilities 174,615 115,977

PricewaterhouseCoopers 35

HCU – Historical Currency Units CCU – Current Currency Units

Chapter 7 – Illustrative example of IAS 29 A. Historical Financial Statements

A. II Historical Income Statement

Additional

(all amounts expressed in HCU) historical Year endedinformation

31 December 2003

Sales B.VI 104,250Cost of sales (69,750)

Gross Profit 34,500

General and administrative expenses:Wages and salaries B.VI (7,000)Depreciation expense (3,447)Rent expense B.VI (3,000)Bad debt expense (2,450)Other administrative expenses B.VI (8,000)Amortisation of government grant B.V.1 400Profit on sale of property, plant and equipment B.I 386

(23,111)

Operating profit 11,389

Share of result of associate B.II.1 6,300

Finance costs:Gain on trading investments B.II.3 4,000Interest income 762Interest expense (2,000)Net foreign exchange transaction losses B.VI (12,620)

(9,858)

Profit before tax 7,831

Tax B.VI (1,200)

Net income 6,631

HCU – Historical Currency Units CCU – Current Currency Units

Chapter 7 – Illustrative example of IAS 29 A. Historical Financial Statements

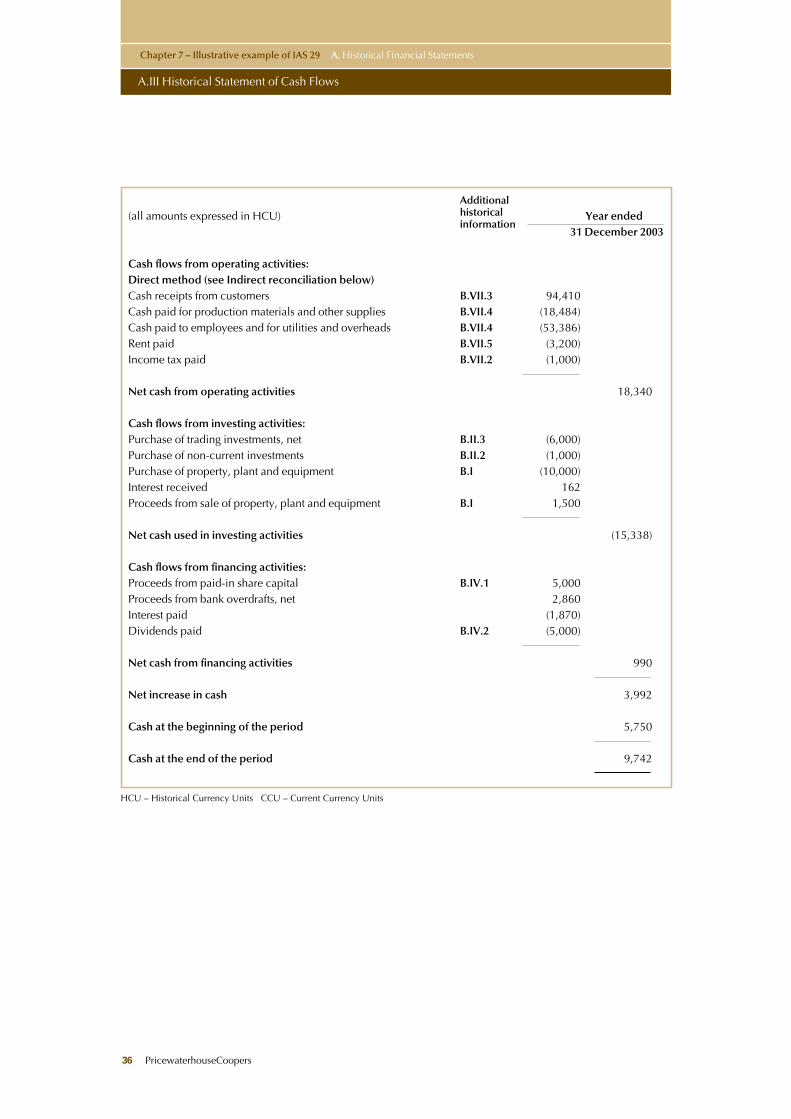

A.III Historical Statement of Cash Flows

36 PricewaterhouseCoopers

Additional

(all amounts expressed in HCU) historical Year endedinformation

31 December 2003

Cash flows from operating activities:Direct method (see Indirect reconciliation below)Cash receipts from customers B.VII.3 94,410Cash paid for production materials and other supplies B.VII.4 (18,484)Cash paid to employees and for utilities and overheads B.VII.4 (53,386)Rent paid B.VII.5 (3,200)Income tax paid B.VII.2 (1,000)

Net cash from operating activities 18,340

Cash flows from investing activities:Purchase of trading investments, net B.II.3 (6,000)Purchase of non-current investments B.II.2 (1,000)Purchase of property, plant and equipment B.I (10,000)Interest received 162Proceeds from sale of property, plant and equipment B.I 1,500

Net cash used in investing activities (15,338)

Cash flows from financing activities:Proceeds from paid-in share capital B.IV.1 5,000Proceeds from bank overdrafts, net 2,860Interest paid (1,870)Dividends paid B.IV.2 (5,000)

Net cash from financing activities 990

Net increase in cash 3,992

Cash at the beginning of the period 5,750

Cash at the end of the period 9,742

Chapter 7 – Illustrative example of IAS 29 A. Historical Financial Statements

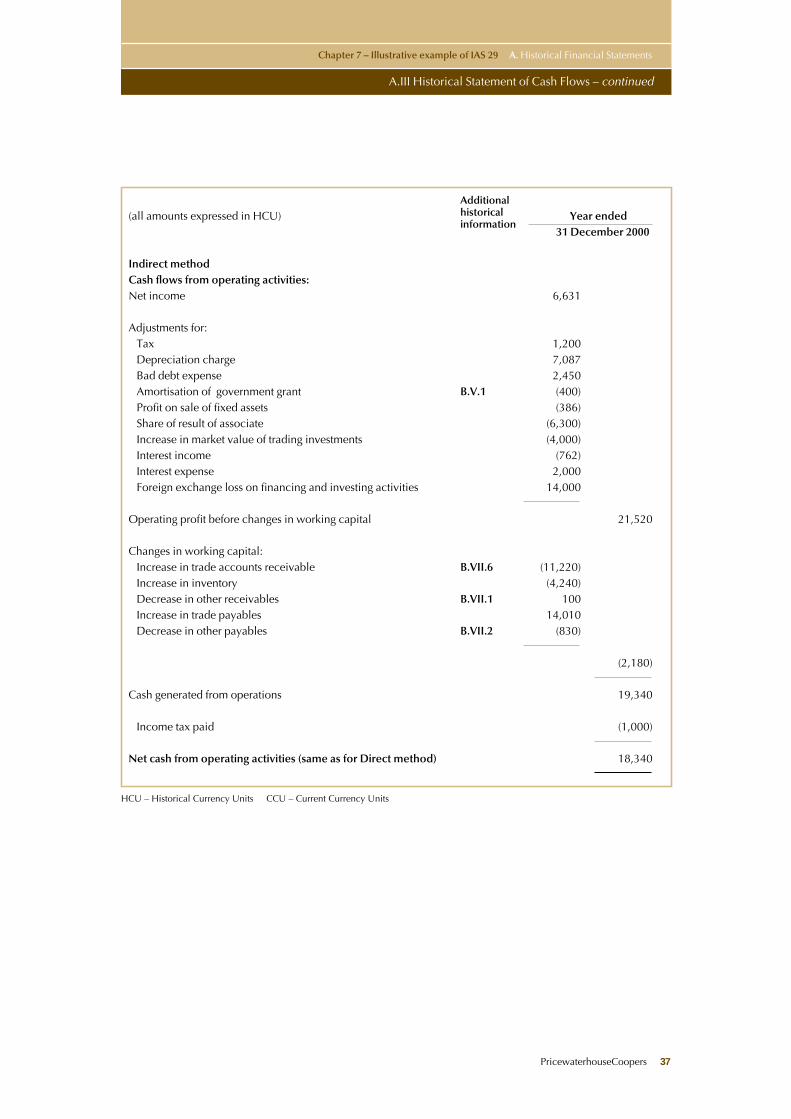

A.III Historical Statement of Cash Flows – continued

Additional

(all amounts expressed in HCU) historical Year endedinformation

31 December 2000

Indirect methodCash flows from operating activities:Net income 6,631

Adjustments for:Tax 1,200Depreciation charge 7,087Bad debt expense 2,450Amortisation of government grant B.V.1 (400)Profit on sale of fixed assets (386)Share of result of associate (6,300)Increase in market value of trading investments (4,000)Interest income (762)Interest expense 2,000Foreign exchange loss on financing and investing activities 14,000

Operating profit before changes in working capital 21,520

Changes in working capital:Increase in trade accounts receivable B.VII.6 (11,220)Increase in inventory (4,240)Decrease in other receivables B.VII.1 100Increase in trade payables 14,010Decrease in other payables B.VII.2 (830)

(2,180)

Cash generated from operations 19,340

Income tax paid (1,000)

Net cash from operating activities (same as for Direct method) 18,340

HCU – Historical Currency Units CCU – Current Currency Units

PricewaterhouseCoopers 37

HCU – Historical Currency Units CCU – Current Currency Units

Chapter 7 – Illustrative example of IAS 29 A. Historical Financial Statements

A.IV Historical Statement of Charges in Equity

38 PricewaterhouseCoopers

Additional

(all amounts expressed in HCU) historical Share Revaluation Translation Retained Totalinformation

Capital Reserve Reserve Earnings

Balance at 1 January 2003 B.IV.1 17,000 38,130 – 20,697 75,827

Share capital paid in B.IV.1 5,000 – – – 5,000

Net profit for the year – – – 6,631 6,631

Revaluation of property, plant and equipment B.I – 9,027 – – 9,027

Currency translation differences B.II.1 – – 13,010 – 13,010

Dividends declared in 2003 B.IV.2 (5,000) (5,000)

Balance at 31 December 2003 22,000 47,157 13,010 22,328 104,495

PricewaterhouseCoopers 39

HCU – Historical Currency Units CCU – Current Currency Units

Chapter 7 – Illustrative example of IAS 29 B. Additional Historical Information Required for IAS 29 Restatement

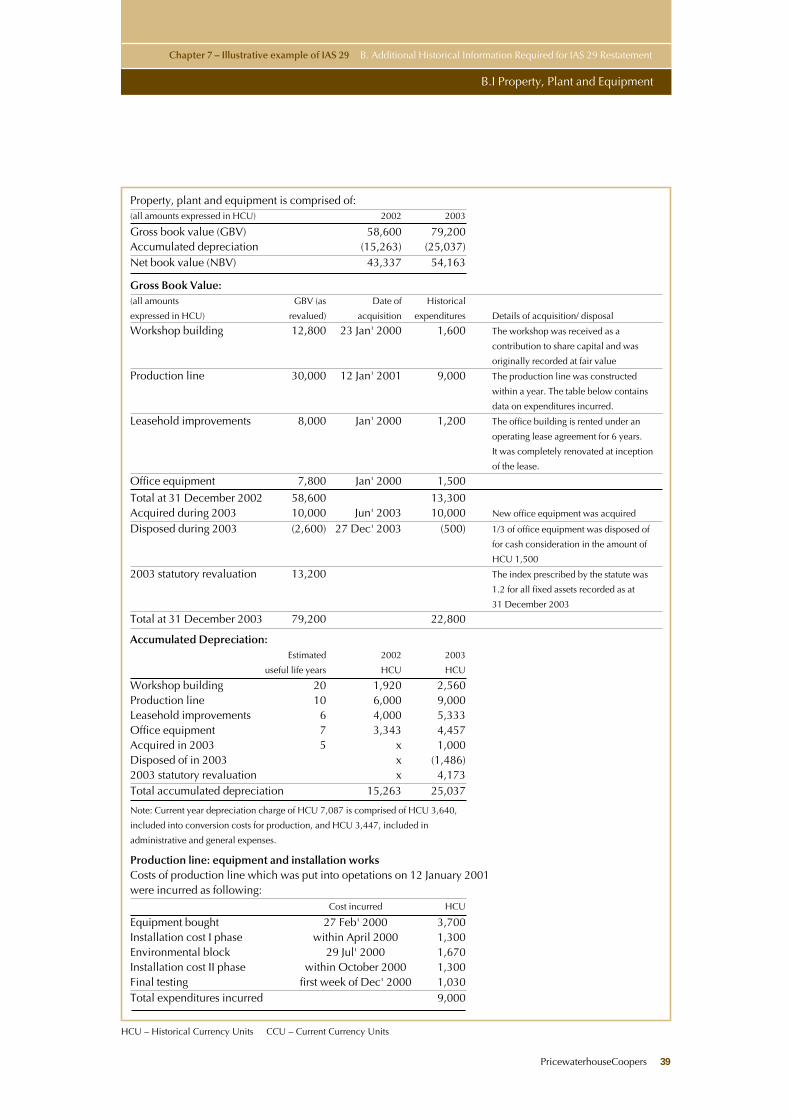

B.I Property, Plant and Equipment

Property, plant and equipment is comprised of:(all amounts expressed in HCU) 2002 2003

Gross book value (GBV) 58,600 79,200Accumulated depreciation (15,263) (25,037)Net book value (NBV) 43,337 54,163

Gross Book Value:(all amounts GBV (as Date of Historical

expressed in HCU) revalued) acquisition expenditures Details of acquisition/ disposal

Workshop building 12,800 23 Jan' 2000 1,600 The workshop was received as a

contribution to share capital and was

originally recorded at fair value

Production line 30,000 12 Jan' 2001 9,000 The production line was constructed

within a year. The table below contains

data on expenditures incurred.

Leasehold improvements 8,000 Jan' 2000 1,200 The office building is rented under an

operating lease agreement for 6 years.

It was completely renovated at inception

of the lease.

Office equipment 7,800 Jan' 2000 1,500

Total at 31 December 2002 58,600 13,300Acquired during 2003 10,000 Jun' 2003 10,000 New office equipment was acquired

Disposed during 2003 (2,600) 27 Dec' 2003 (500) 1/3 of office equipment was disposed of

for cash consideration in the amount of

HCU 1,500

2003 statutory revaluation 13,200 The index prescribed by the statute was

1.2 for all fixed assets recorded as at

31 December 2003

Total at 31 December 2003 79,200 22,800

Accumulated Depreciation:Estimated 2002 2003

useful life years HCU HCU

Workshop building 20 1,920 2,560Production line 10 6,000 9,000Leasehold improvements 6 4,000 5,333Office equipment 7 3,343 4,457Acquired in 2003 5 x 1,000Disposed of in 2003 x (1,486)2003 statutory revaluation x 4,173Total accumulated depreciation 15,263 25,037

Note: Current year depreciation charge of HCU 7,087 is comprised of HCU 3,640,

included into conversion costs for production, and HCU 3,447, included in

administrative and general expenses.

Production line: equipment and installation worksCosts of production line which was put into opetations on 12 January 2001 were incurred as following:

Cost incurred HCU

Equipment bought 27 Feb' 2000 3,700Installation cost I phase within April 2000 1,300Environmental block 29 Jul' 2000 1,670Installation cost II phase within October 2000 1,300Final testing first week of Dec' 2000 1,030Total expenditures incurred 9,000

HCU – Historical Currency Units CCU – Current Currency Units

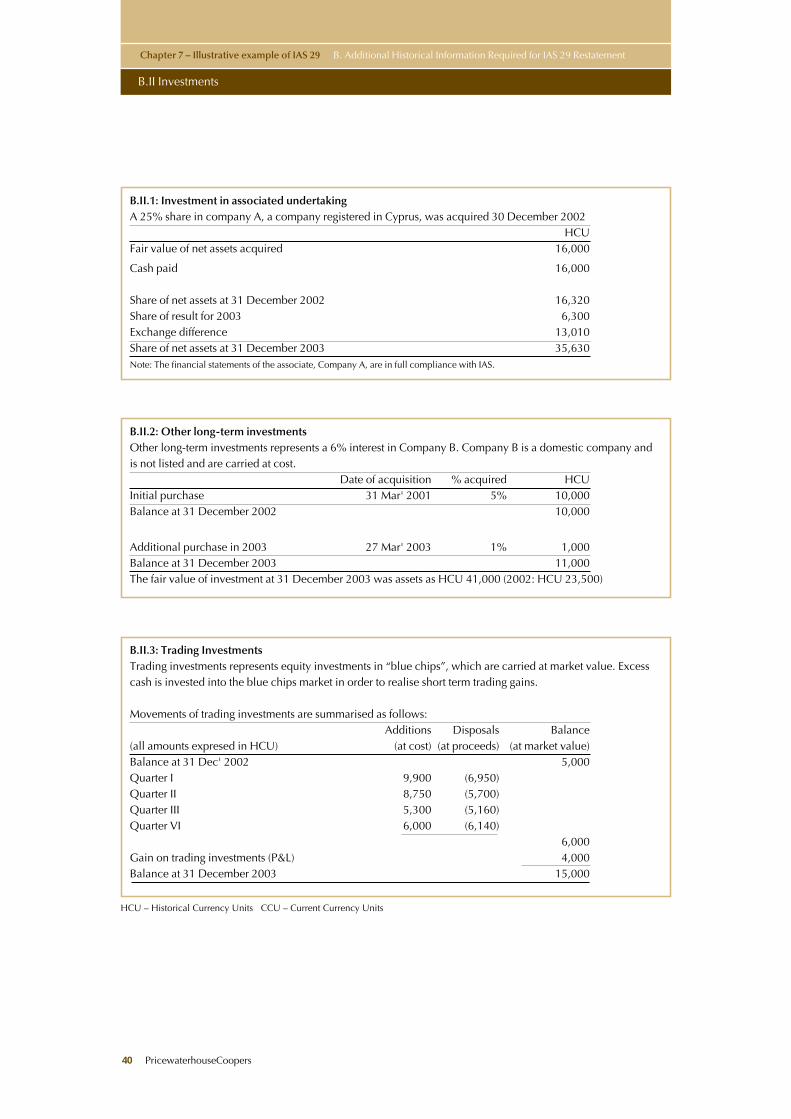

B.II.1: Investment in associated undertakingA 25% share in company A, a company registered in Cyprus, was acquired 30 December 2002

HCUFair value of net assets acquired 16,000

Cash paid 16,000

Share of net assets at 31 December 2002 16,320Share of result for 2003 6,300Exchange difference 13,010Share of net assets at 31 December 2003 35,630Note: The financial statements of the associate, Company A, are in full compliance with IAS.

B.II.2: Other long-term investmentsOther long-term investments represents a 6% interest in Company B. Company B is a domestic company andis not listed and are carried at cost.

Date of acquisition % acquired HCUInitial purchase 31 Mar' 2001 5% 10,000Balance at 31 December 2002 10,000

Additional purchase in 2003 27 Mar' 2003 1% 1,000Balance at 31 December 2003 11,000The fair value of investment at 31 December 2003 was assets as HCU 41,000 (2002: HCU 23,500)

B.II.3: Trading InvestmentsTrading investments represents equity investments in “blue chips”, which are carried at market value. Excesscash is invested into the blue chips market in order to realise short term trading gains.

Movements of trading investments are summarised as follows:Additions Disposals Balance

(all amounts expresed in HCU) (at cost) (at proceeds) (at market value)Balance at 31 Dec' 2002 5,000Quarter I 9,900 (6,950)Quarter II 8,750 (5,700)Quarter III 5,300 (5,160)Quarter VI 6,000 (6,140)

6,000Gain on trading investments (P&L) 4,000Balance at 31 December 2003 15,000

Chapter 7 – Illustrative example of IAS 29 B. Additional Historical Information Required for IAS 29 Restatement

B.II Investments

40 PricewaterhouseCoopers

PricewaterhouseCoopers 41

HCU – Historical Currency Units CCU – Current Currency Units

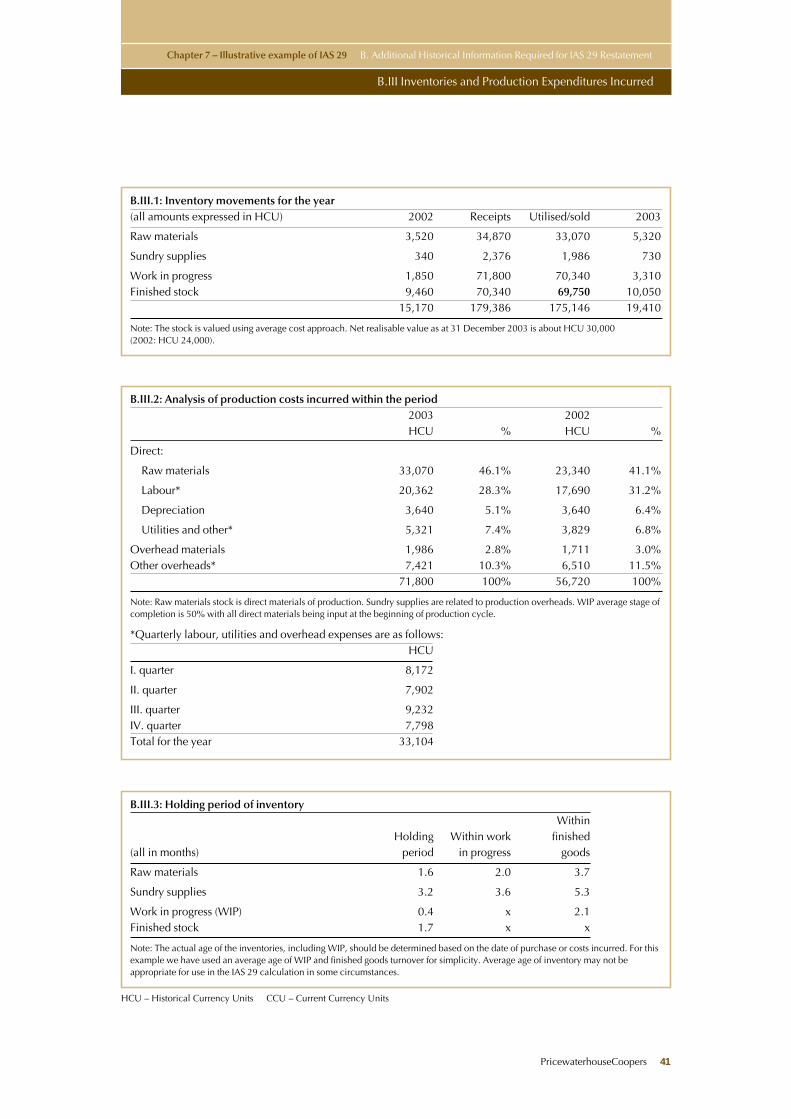

B.III.1: Inventory movements for the year(all amounts expressed in HCU) 2002 Receipts Utilised/sold 2003

Raw materials 3,520 34,870 33,070 5,320

Sundry supplies 340 2,376 1,986 730

Work in progress 1,850 71,800 70,340 3,310Finished stock 9,460 70,340 69,750 10,050

15,170 179,386 175,146 19,410

Note: The stock is valued using average cost approach. Net realisable value as at 31 December 2003 is about HCU 30,000(2002: HCU 24,000).

B.III.3: Holding period of inventoryWithin

Holding Within work finished (all in months) period in progress goods

Raw materials 1.6 2.0 3.7

Sundry supplies 3.2 3.6 5.3

Work in progress (WIP) 0.4 x 2.1Finished stock 1.7 x x

Note: The actual age of the inventories, including WIP, should be determined based on the date of purchase or costs incurred. For thisexample we have used an average age of WIP and finished goods turnover for simplicity. Average age of inventory may not beappropriate for use in the IAS 29 calculation in some circumstances.

B.III.2: Analysis of production costs incurred within the period2003 2002HCU % HCU %

Direct:

Raw materials 33,070 46.1% 23,340 41.1%

Labour* 20,362 28.3% 17,690 31.2%

Depreciation 3,640 5.1% 3,640 6.4%

Utilities and other* 5,321 7.4% 3,829 6.8%

Overhead materials 1,986 2.8% 1,711 3.0%Other overheads* 7,421 10.3% 6,510 11.5%

71,800 100% 56,720 100%

Note: Raw materials stock is direct materials of production. Sundry supplies are related to production overheads. WIP average stage ofcompletion is 50% with all direct materials being input at the beginning of production cycle.

*Quarterly labour, utilities and overhead expenses are as follows:HCU

I. quarter 8,172

II. quarter 7,902

III. quarter 9,232IV. quarter 7,798Total for the year 33,104

Chapter 7 – Illustrative example of IAS 29 B. Additional Historical Information Required for IAS 29 Restatement

B.III Inventories and Production Expenditures Incurred

HCU – Historical Currency Units CCU – Current Currency Units

Chapter 7 – Illustrative example of IAS 29 B. Additional Historical Information Required for IAS 29 Restatement

B.IV: Equity

BV: Long-Term Liabilities

42 PricewaterhouseCoopers

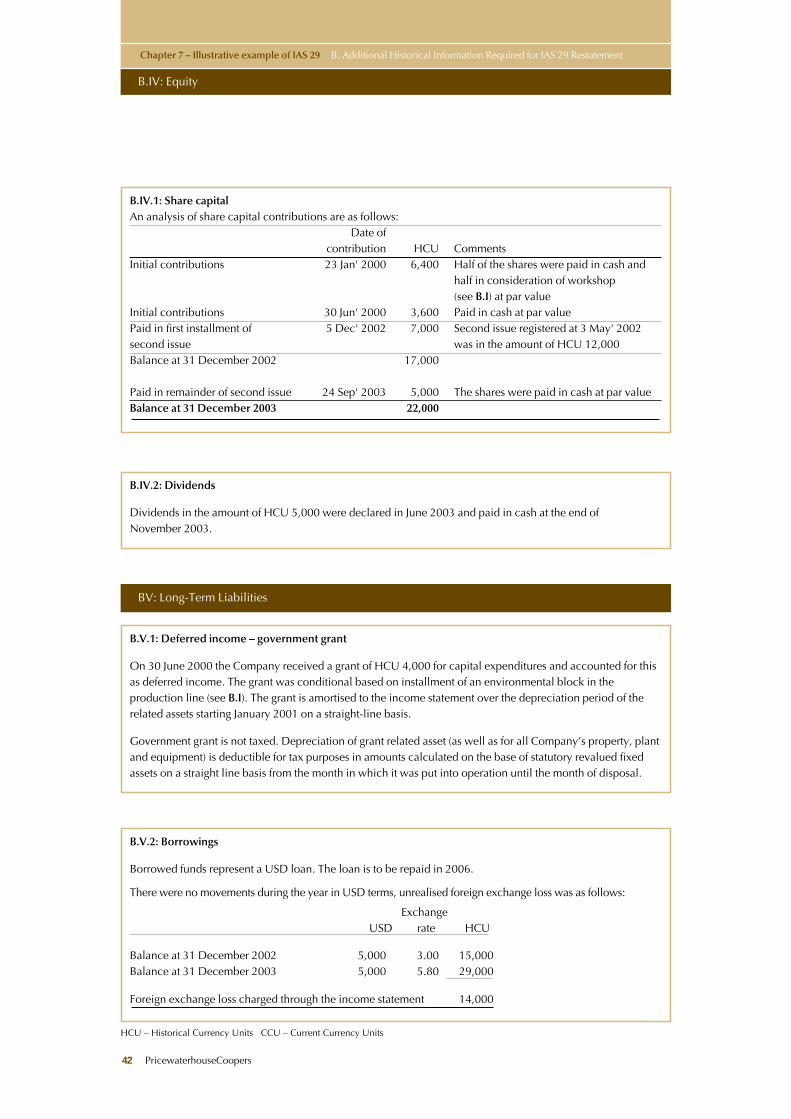

B.IV.1: Share capitalAn analysis of share capital contributions are as follows:

Date ofcontribution HCU Comments

Initial contributions 23 Jan' 2000 6,400 Half of the shares were paid in cash and half in consideration of workshop (see B.I) at par value

Initial contributions 30 Jun' 2000 3,600 Paid in cash at par valuePaid in first installment of 5 Dec' 2002 7,000 Second issue registered at 3 May' 2002 second issue was in the amount of HCU 12,000Balance at 31 December 2002 17,000

Paid in remainder of second issue 24 Sep' 2003 5,000 The shares were paid in cash at par valueBalance at 31 December 2003 22,000

B.IV.2: Dividends

Dividends in the amount of HCU 5,000 were declared in June 2003 and paid in cash at the end ofNovember 2003.

B.V.2: Borrowings

Borrowed funds represent a USD loan. The loan is to be repaid in 2006.

There were no movements during the year in USD terms, unrealised foreign exchange loss was as follows:

ExchangeUSD rate HCU

Balance at 31 December 2002 5,000 3.00 15,000Balance at 31 December 2003 5,000 5.80 29,000

Foreign exchange loss charged through the income statement 14,000

B.V.1: Deferred income – government grant