Embed Size (px)

Citation preview

INTERNAL MODELS WITHIN NON-LIFE INSURANCEOlov Dahlberg & Johan Bergström

AGENDA

Who are we?

Introduction

Modelling one risk at a time

Modelling through a cash flow approach

Excel Example

WHO ARE WE?

… and the short story about Trygg-Hansa

SEEMINGLY RANDOM NUMBERS

41

13, 10, 9, 0

33

15

11

6

1

INTRODUCTION

5

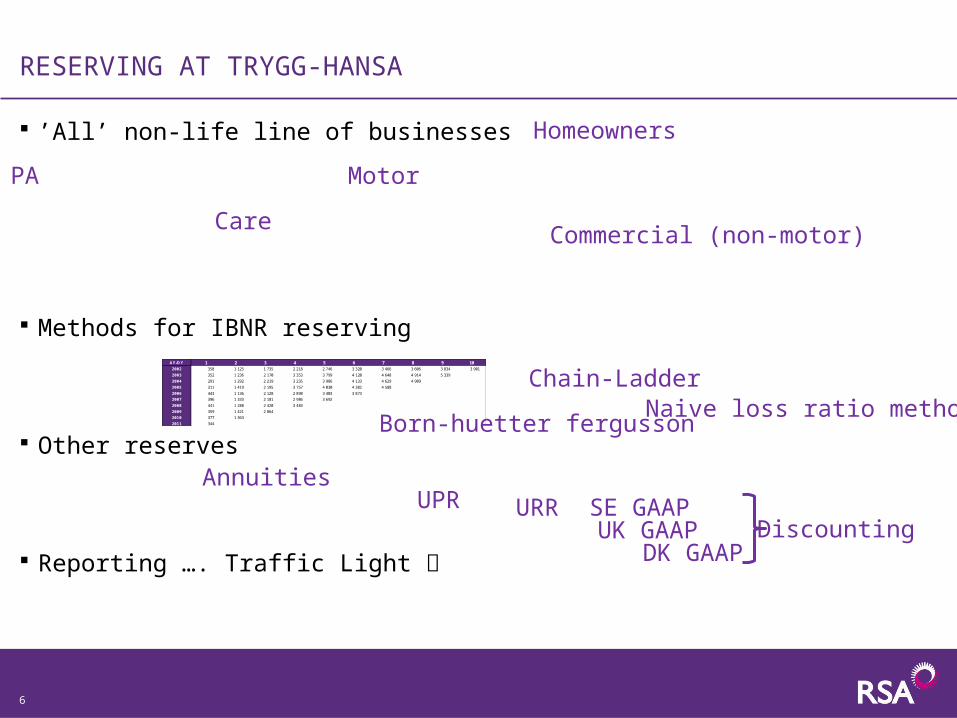

RESERVING AT TRYGG-HANSA

’All’ non-life line of businesses

Methods for IBNR reserving

Other reserves

Reporting …. Traffic Light

PA Motor

Homeowners

Commercial (non-motor)Care

Chain-LadderAY/DY 1 2 3 4 5 6 7 8 9 10

2002 358 1 125 1 735 2 218 2 746 3 320 3 466 3 606 3 834 3 901

2003 352 1 236 2 170 3 353 3 799 4 120 4 648 4 914 5 339

2004 291 1 292 2 219 3 235 3 986 4 133 4 629 4 909

2005 311 1 419 2 195 3 757 4 030 4 382 4 588

2006 443 1 136 2 128 2 898 3 403 3 873

2007 396 1 333 2 181 2 986 3 692

2008 441 1 288 2 420 3 483

2009 359 1 421 2 864

2010 377 1 363

2011 344 Born-huetter fergussonNaive loss ratio method

AnnuitiesUPR URR

UK GAAPSE GAAP

DK GAAPDiscounting

6

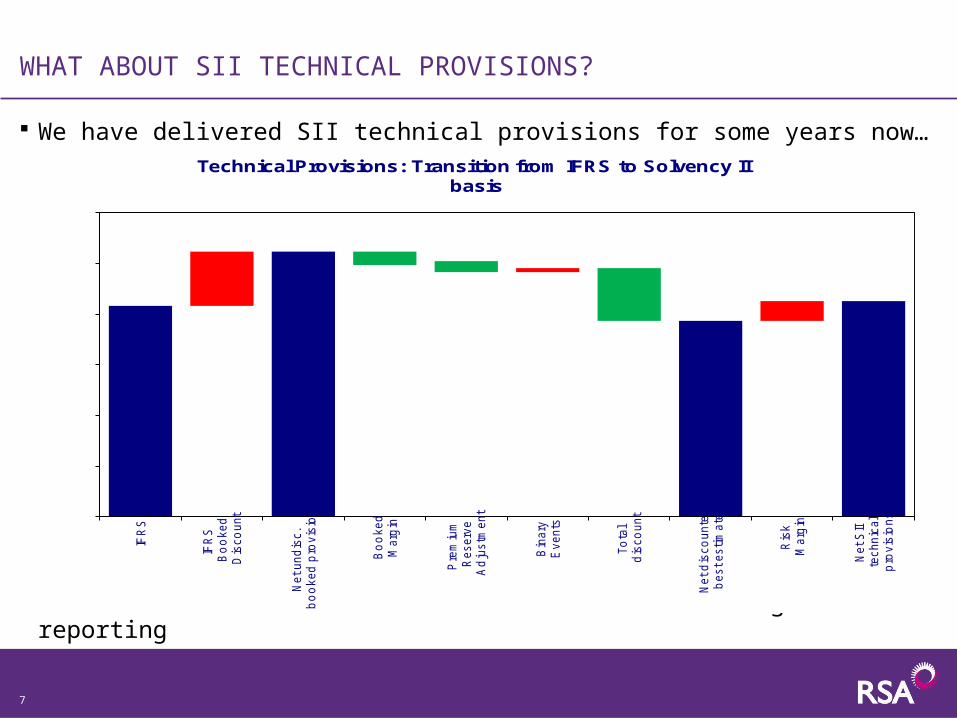

WHAT ABOUT SII TECHNICAL PROVISIONS?

We have delivered SII technical provisions for some years now…

…. several of above features are used in Traffic Light reporting

7

0

5 000

10 000

15 000

20 000

25 000

30 000

IFR

S

IFR

S

Bo

oked

Dis

co

unt

Net und

isc.

bo

oked

pro

vis

ions

Bo

oked

Marg

in

Pre

miu

m

Reserv

e

Ad

justm

ent

Bin

ary

Events

To

tal

dis

co

unt

Net d

isco

unte

d

best estim

ate

Ris

k

Marg

in

Net S

II

technic

al

pro

vis

ions

Technical Provisions: Transition from IFRS to Solvency IIbasis

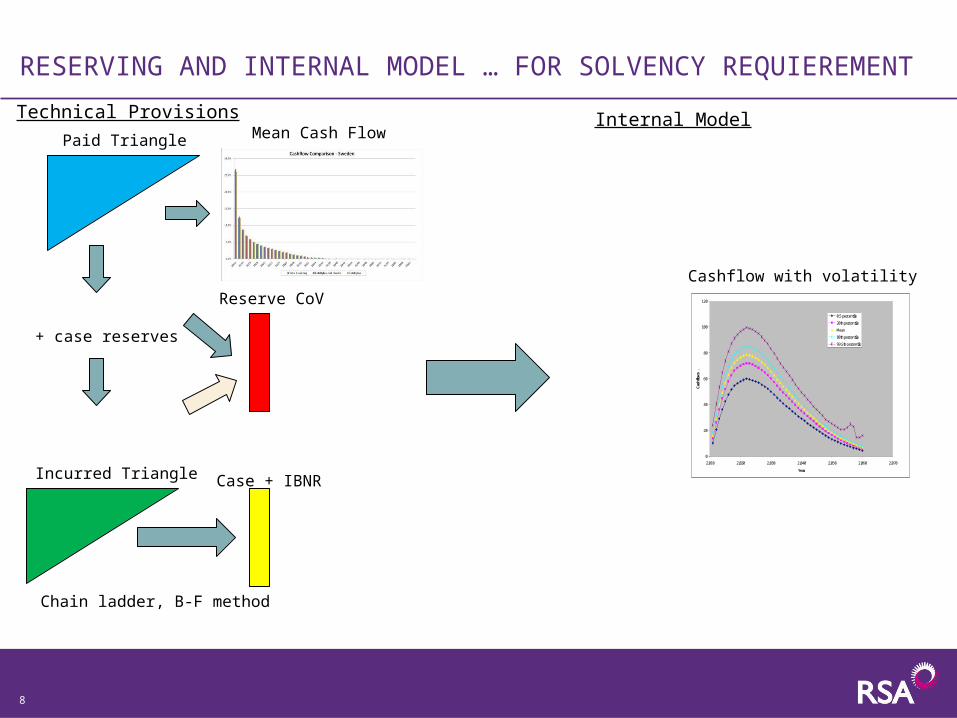

RESERVING AND INTERNAL MODEL … FOR SOLVENCY REQUIEREMENT

Technical Provisions

Paid Triangle

+ case reserves

Incurred Triangle

Mean Cash Flow

Chain ladder, B-F method

Case + IBNR

Reserve CoV

Internal Model

0

20

40

60

80

100

120

2,010 2,020 2,030 2,040 2,050 2,060 2,070

Year

Cas

hflo

ws

.

0.5 percentile

20th percentile

Mean

80th percentile

99.5th percentile

Cashflow with volatility

8

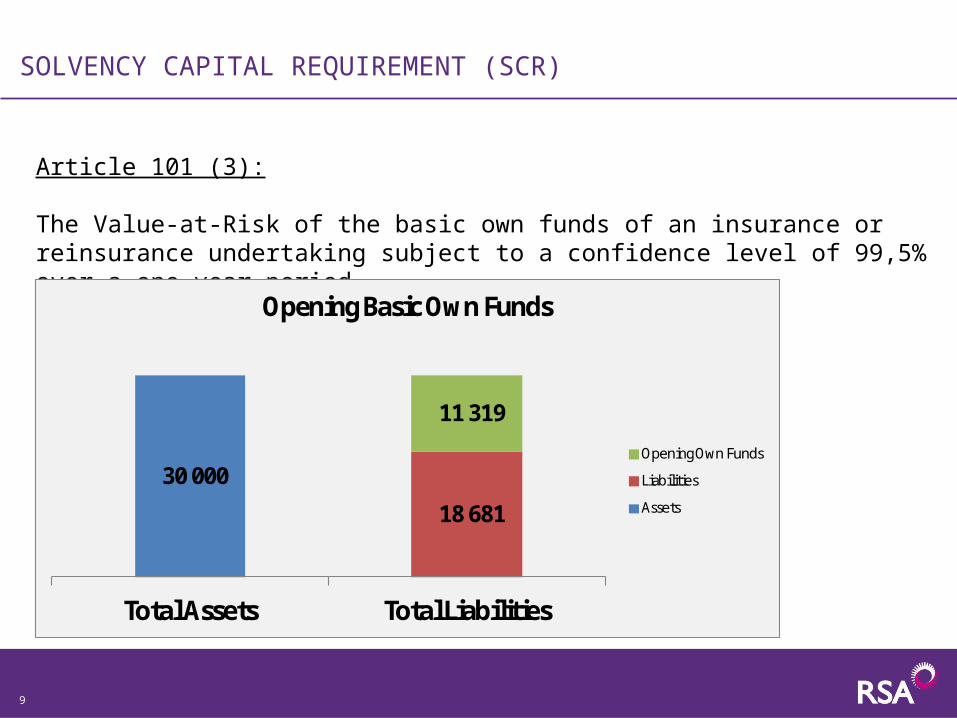

SOLVENCY CAPITAL REQUIREMENT (SCR)

Article 101 (3):

The Value-at-Risk of the basic own funds of an insurance or reinsurance undertaking subject to a confidence level of 99,5% over a one-year period.

30 000

18 681

11 319

Total Assets Total Liabilities

Opening Basic Own Funds

Opening Own Funds

Liabilities

Assets

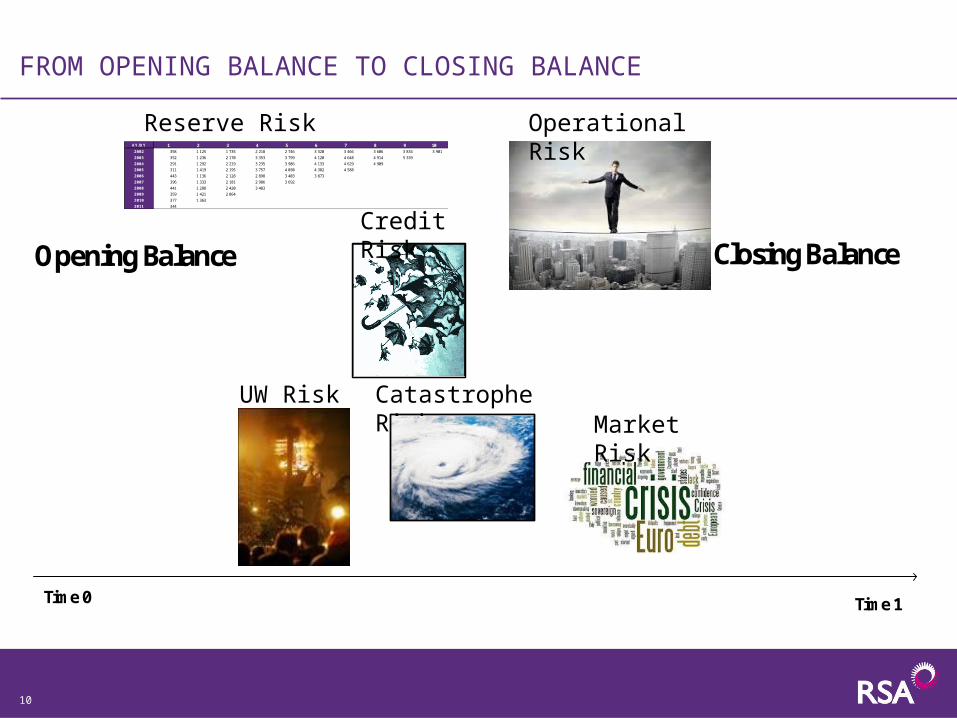

9

Time 0 Time 1

Opening Balance Closing Balance

FROM OPENING BALANCE TO CLOSING BALANCE

AY/DY 1 2 3 4 5 6 7 8 9 10

2002 358 1 125 1 735 2 218 2 746 3 320 3 466 3 606 3 834 3 901

2003 352 1 236 2 170 3 353 3 799 4 120 4 648 4 914 5 339

2004 291 1 292 2 219 3 235 3 986 4 133 4 629 4 909

2005 311 1 419 2 195 3 757 4 030 4 382 4 588

2006 443 1 136 2 128 2 898 3 403 3 873

2007 396 1 333 2 181 2 986 3 692

2008 441 1 288 2 420 3 483

2009 359 1 421 2 864

2010 377 1 363

2011 344

Reserve Risk

Catastrophe Risk

Credit Risk

Market Risk

Operational Risk

UW Risk

10

FROM OPENING BALANCE TO CLOSING BALANCE

Time 0 Time 1

11

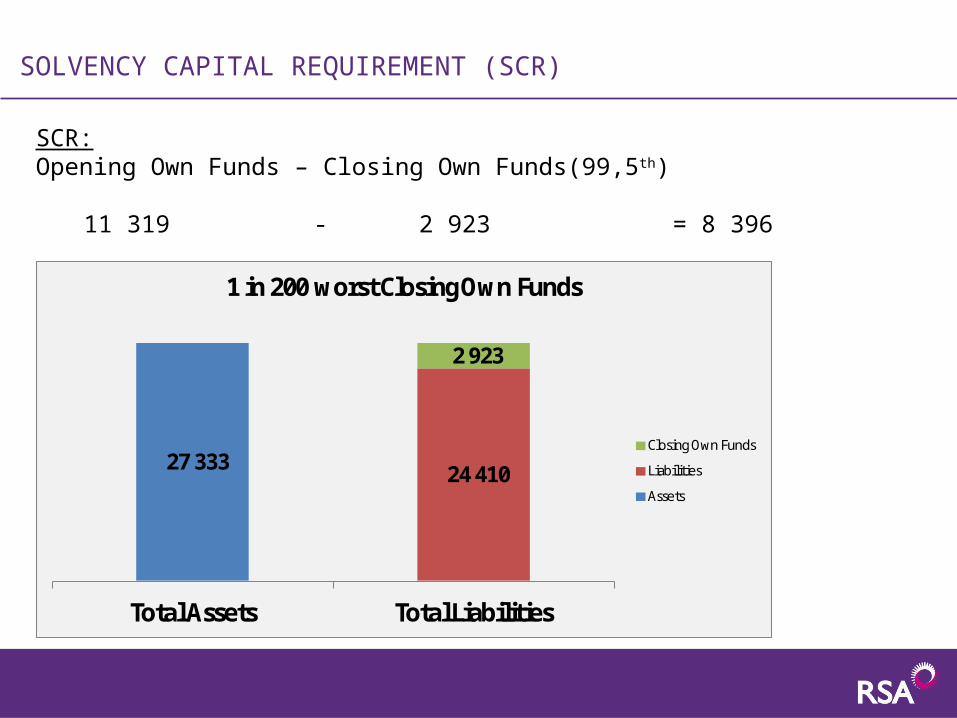

SOLVENCY CAPITAL REQUIREMENT (SCR)

27 333 24 410

2 923

Total Assets Total Liabilities

1 in 200 worst Closing Own Funds

Closing Own Funds

Liabilities

Assets

SCR:Opening Own Funds – Closing Own Funds(99,5th)

11 319 - 2 923 = 8 396

ONE RISK AT A TIME APPROACH

13

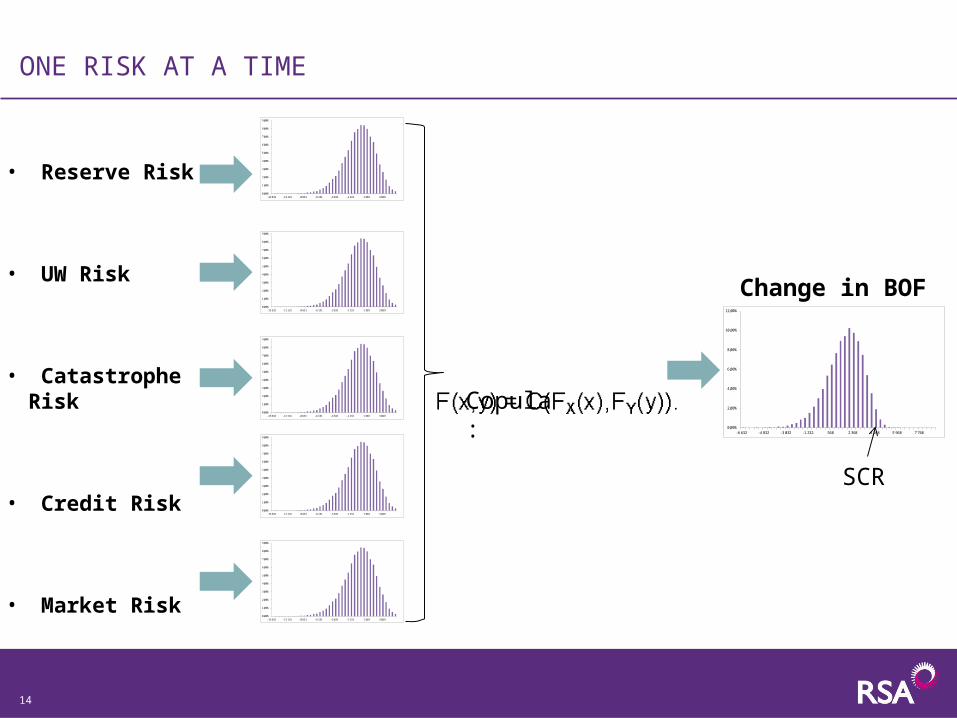

ONE RISK AT A TIME

• Reserve Risk

• UW Risk

• Catastrophe Risk

• Credit Risk

• Market Risk

Copula:

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

- 6 632 - 4 832 - 3 032 - 1 232 568 2 368 4 168 5 968 7 768

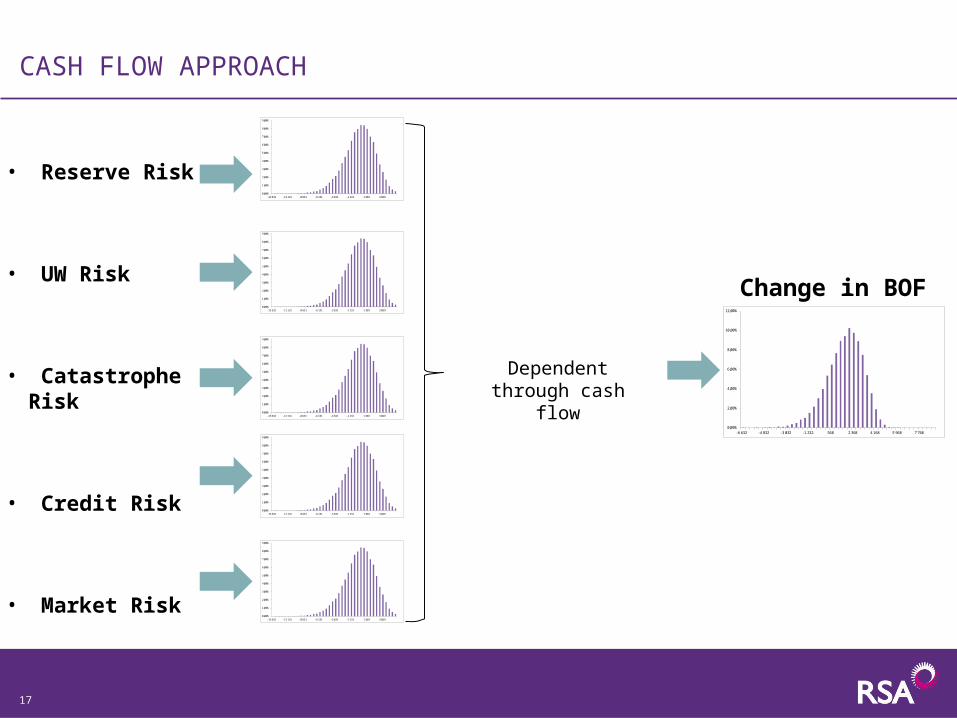

Change in BOF

14

SCR

CASH FLOW APPROACH

15

IGLOO

16

CASH FLOW APPROACH

• Reserve Risk

• UW Risk

• Catastrophe Risk

• Credit Risk

• Market Risk

Dependent through cash flow

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

1,00%

2,00%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

- 13 631 - 11 131 - 8 631 - 6 131 - 3 631 - 1 131 1 369 3 869

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

- 6 632 - 4 832 - 3 032 - 1 232 568 2 368 4 168 5 968 7 768

Change in BOF

17

QUESTIONS?