Embed Size (px)

Citation preview

Internal Audit Data Analytics

ISACA September 2016

Timothy Tham – Risk Analytics Director – EY UK&I

1

Page 2

Agenda

► The changing data landscape

► The IA analytics journey and the role of IA

► A framework for getting started

► Covering the basics

► A taste of the more advanced

► Questions / Discussion

Page 3

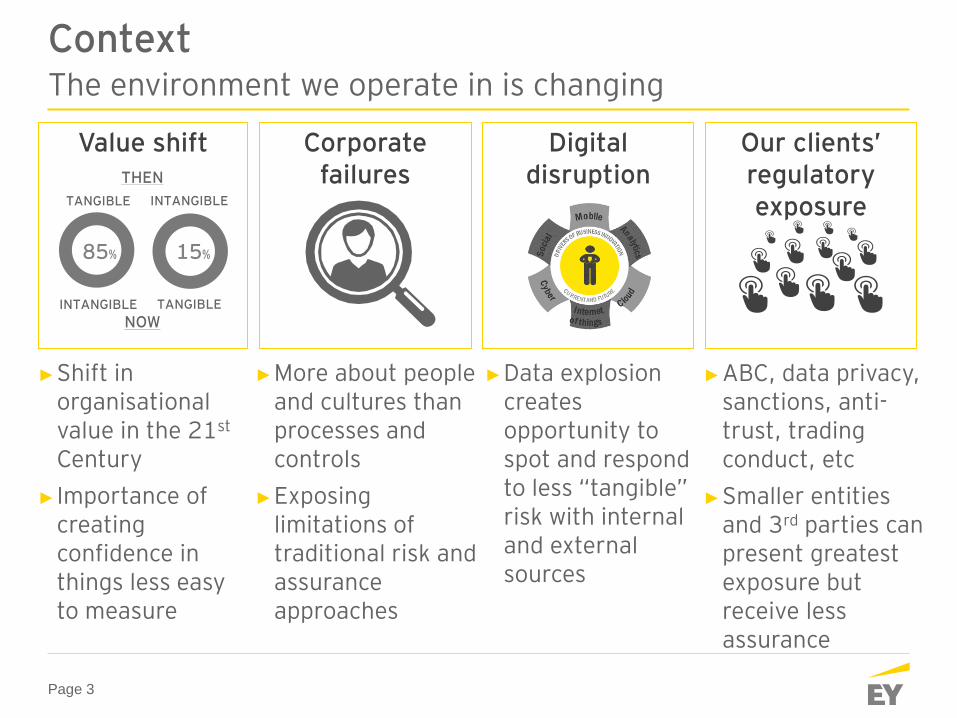

The environment we operate in is changing

Context

Corporate failures

Value shift

►More about people and cultures than processes and controls

►Exposing limitations of traditional risk and assurance approaches

►Shift in organisational value in the 21st Century

► Importance of creating confidence in things less easy to measure

Digital disruption

Our clients’ regulatory exposure

85% 15%

THEN

TANGIBLE INTANGIBLE

NOW INTANGIBLE TANGIBLE

►Data explosion creates opportunity to spot and respond to less “tangible” risk with internal and external sources

►ABC, data privacy, sanctions, anti-trust, trading conduct, etc

►Smaller entities and 3rd parties can present greatest exposure but receive less assurance

Page 4

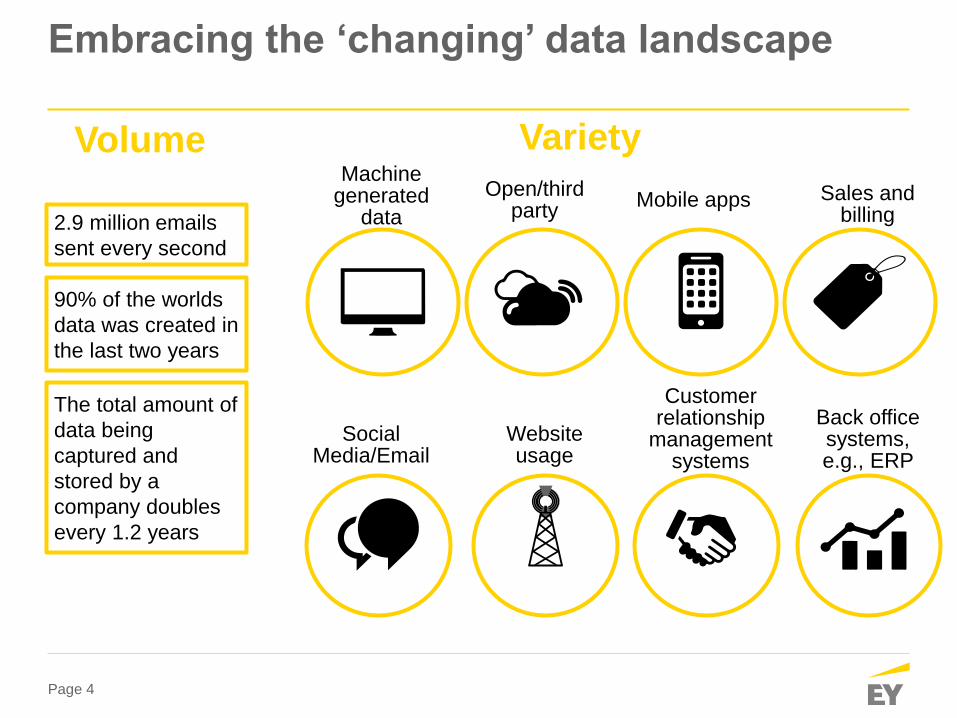

Embracing the ‘changing’ data landscape

The total amount of

data being

captured and

stored by a

company doubles

every 1.2 years

2.9 million emails

sent every second

90% of the worlds

data was created in

the last two years

Machine generated

data

Open/third party

Mobile apps Sales and billing

Social Media/Email

Website usage

Customer relationship

management systems

Back office systems, e.g., ERP

Volume Variety

Page 5

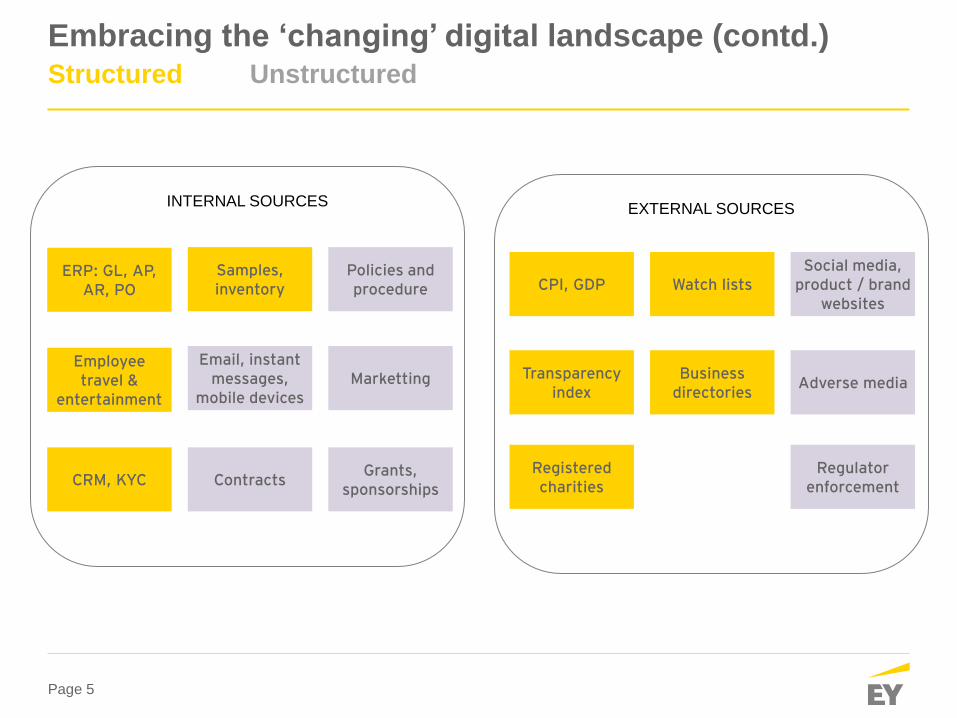

Embracing the ‘changing’ digital landscape (contd.) Structured Unstructured

INTERNAL SOURCES EXTERNAL SOURCES

ERP: GL, AP, AR, PO

Marketting

Policies and procedure

Employee travel &

entertainment

Email, instant messages,

mobile devices

CRM, KYC Contracts

Samples, inventory

Grants, sponsorships

CPI, GDP

Transparency index

Regulator enforcement

Social media, product / brand

websites

Business directories

Registered charities

Watch lists

Adverse media

Page 6

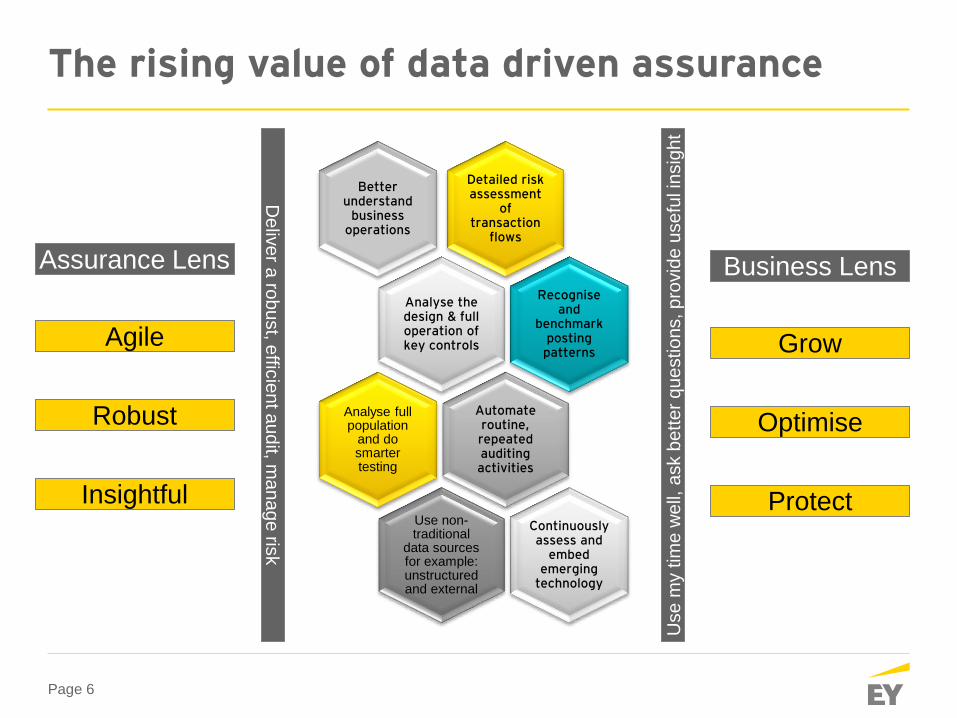

The rising value of data driven assurance

Detailed risk assessment

of transaction

flows

Better understand

business operations

Analyse the design & full operation of key controls

Recognise and

benchmark posting patterns

Automate routine, repeated auditing activities

Analyse full population

and do smarter testing

Use non-traditional

data sources for example: unstructured and external

Continuously assess and

embed emerging

technology

Agile

Assurance Lens

Robust

Insightful

Grow

Business Lens

Optimise

Protect

Use

my t

ime

we

ll, a

sk b

ett

er

qu

estio

ns, p

rovid

e u

se

ful in

sig

ht

De

live

r a ro

bu

st, e

fficie

nt a

ud

it, ma

na

ge

risk

The better the question. The better the answer.�The better the world works.

Where are you on the IA analytics journey?

Page 8

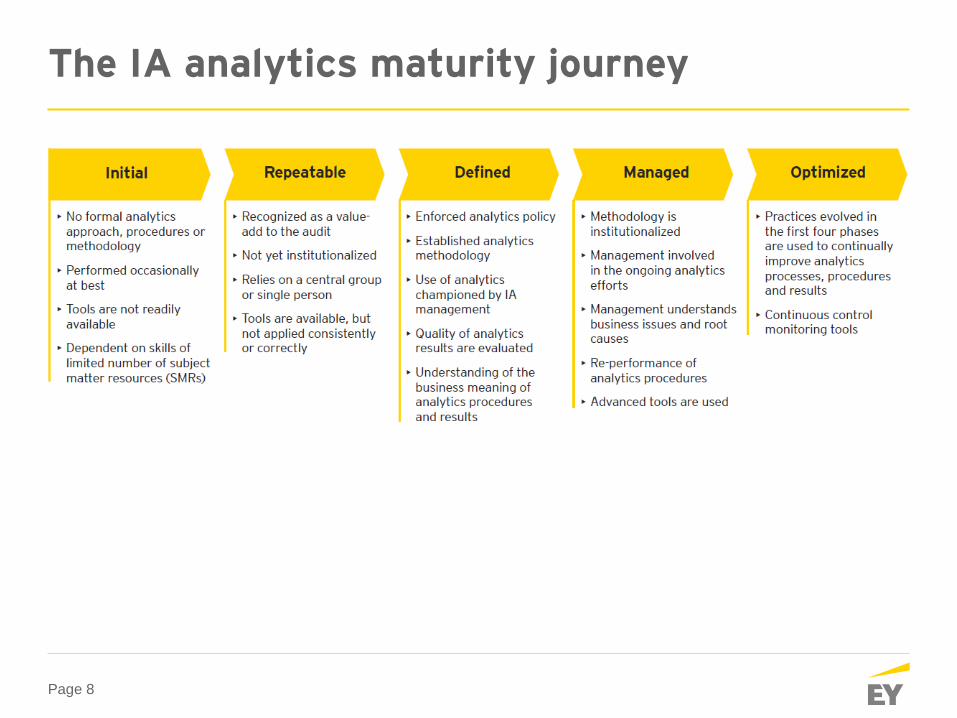

The IA analytics maturity journey

The better the question. The better the answer.�The better the world works.

The role of IA? Champion Catalyst Owner

Page 10

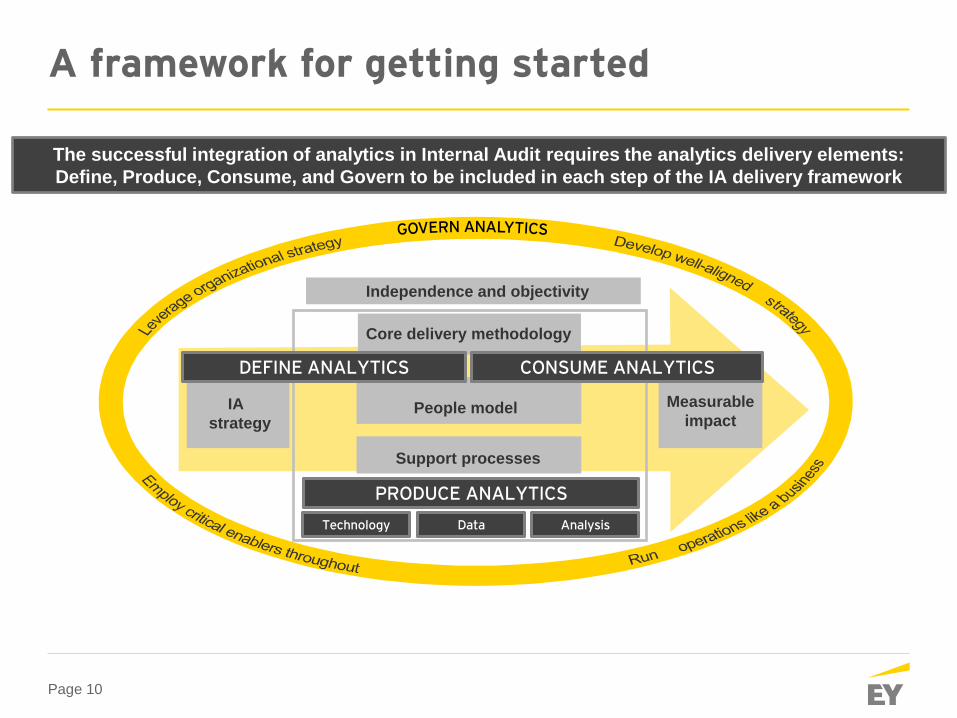

A framework for getting started

Independence and objectivity

Core delivery methodology

People model

Support processes

IA

strategy

Measurable

impact

PRODUCE ANALYTICS

Technology Analysis Data

DEFINE ANALYTICS CONSUME ANALYTICS

The successful integration of analytics in Internal Audit requires the analytics delivery elements:

Define, Produce, Consume, and Govern to be included in each step of the IA delivery framework

Page 11

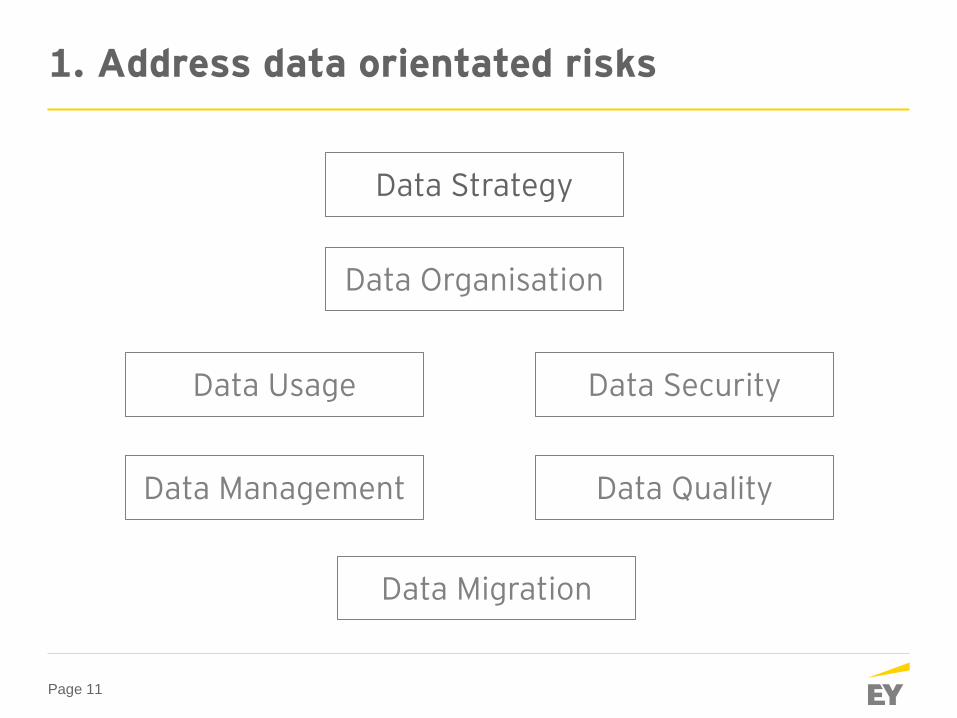

1. Address data orientated risks

Data Strategy

Data Security Data Usage

Data Management Data Quality

Data Organisation

Data Migration

Page 12

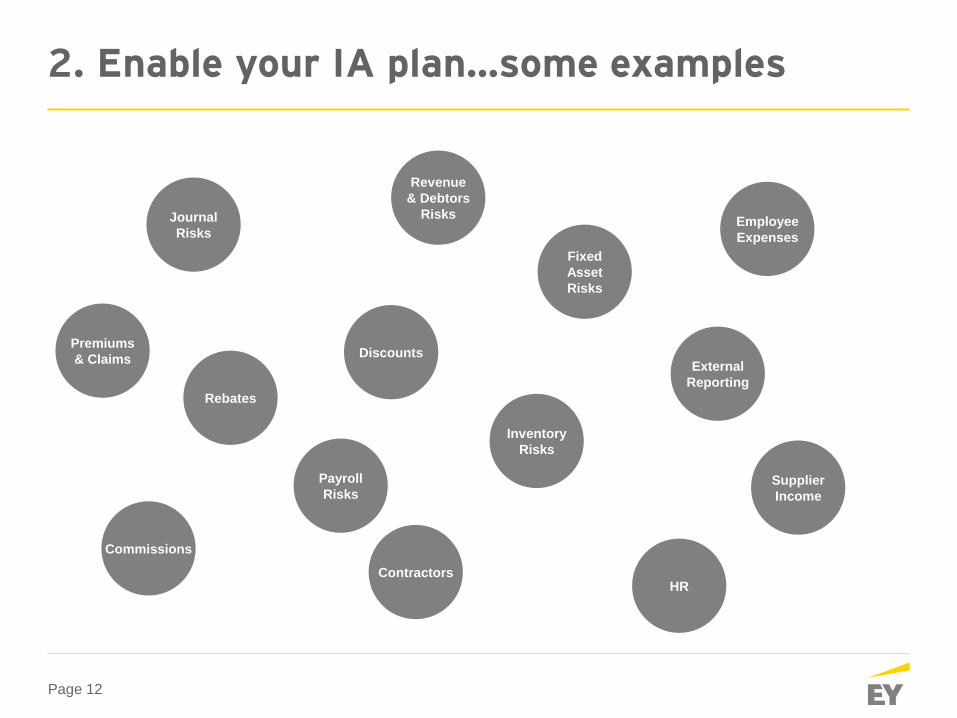

2. Enable your IA plan…some examples

Commissions

Revenue

& Debtors

Risks

Inventory

Risks

Discounts

Journal

Risks

Fixed

Asset

Risks

Employee

Expenses

External

Reporting

HR Contractors

Rebates

Supplier

Income

Payroll

Risks

Premiums

& Claims

Page 13

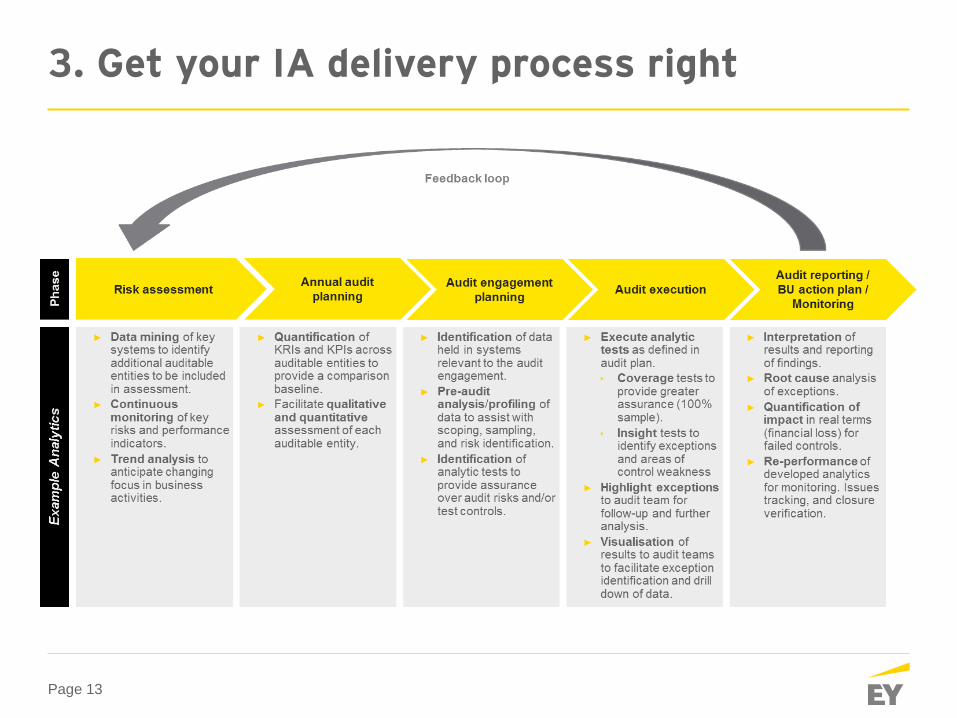

3. Get your IA delivery process right

Page 14

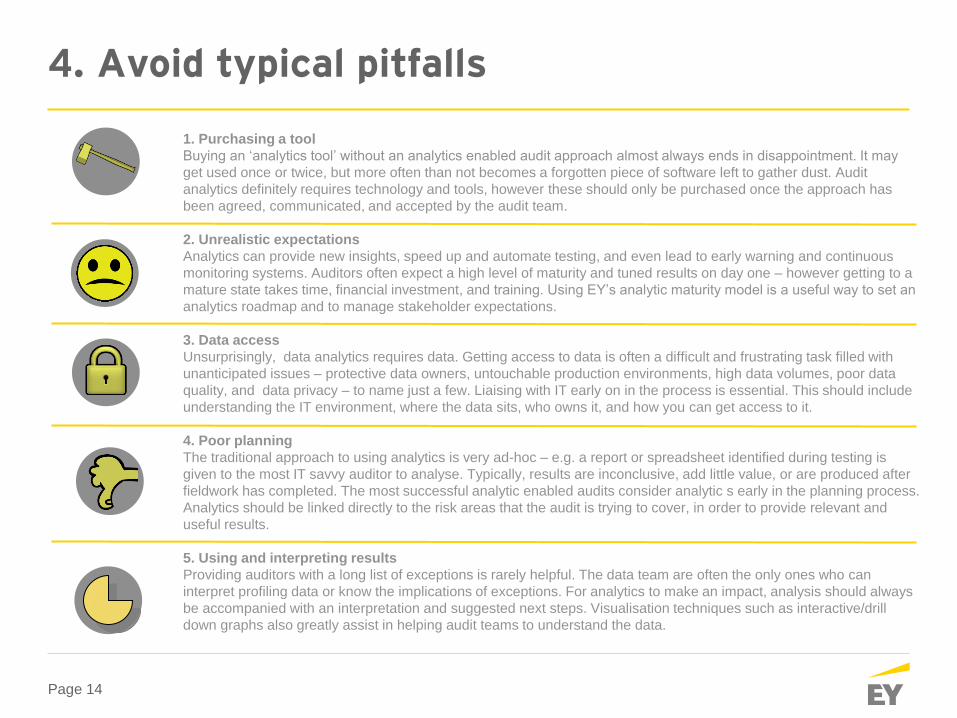

4. Avoid typical pitfalls

1. Purchasing a tool

Buying an ‘analytics tool’ without an analytics enabled audit approach almost always ends in disappointment. It may

get used once or twice, but more often than not becomes a forgotten piece of software left to gather dust. Audit

analytics definitely requires technology and tools, however these should only be purchased once the approach has

been agreed, communicated, and accepted by the audit team.

2. Unrealistic expectations

Analytics can provide new insights, speed up and automate testing, and even lead to early warning and continuous

monitoring systems. Auditors often expect a high level of maturity and tuned results on day one – however getting to a

mature state takes time, financial investment, and training. Using EY’s analytic maturity model is a useful way to set an

analytics roadmap and to manage stakeholder expectations.

3. Data access

Unsurprisingly, data analytics requires data. Getting access to data is often a difficult and frustrating task filled with

unanticipated issues – protective data owners, untouchable production environments, high data volumes, poor data

quality, and data privacy – to name just a few. Liaising with IT early on in the process is essential. This should include

understanding the IT environment, where the data sits, who owns it, and how you can get access to it.

4. Poor planning

The traditional approach to using analytics is very ad-hoc – e.g. a report or spreadsheet identified during testing is

given to the most IT savvy auditor to analyse. Typically, results are inconclusive, add little value, or are produced after

fieldwork has completed. The most successful analytic enabled audits consider analytic s early in the planning process.

Analytics should be linked directly to the risk areas that the audit is trying to cover, in order to provide relevant and

useful results.

5. Using and interpreting results

Providing auditors with a long list of exceptions is rarely helpful. The data team are often the only ones who can

interpret profiling data or know the implications of exceptions. For analytics to make an impact, analysis should always

be accompanied with an interpretation and suggested next steps. Visualisation techniques such as interactive/drill

down graphs also greatly assist in helping audit teams to understand the data.

The better the question. The better the answer.�The better the world works.

Industry 4.0… Innovation… Big Data… Where could (will?) the journey go?

Page 16

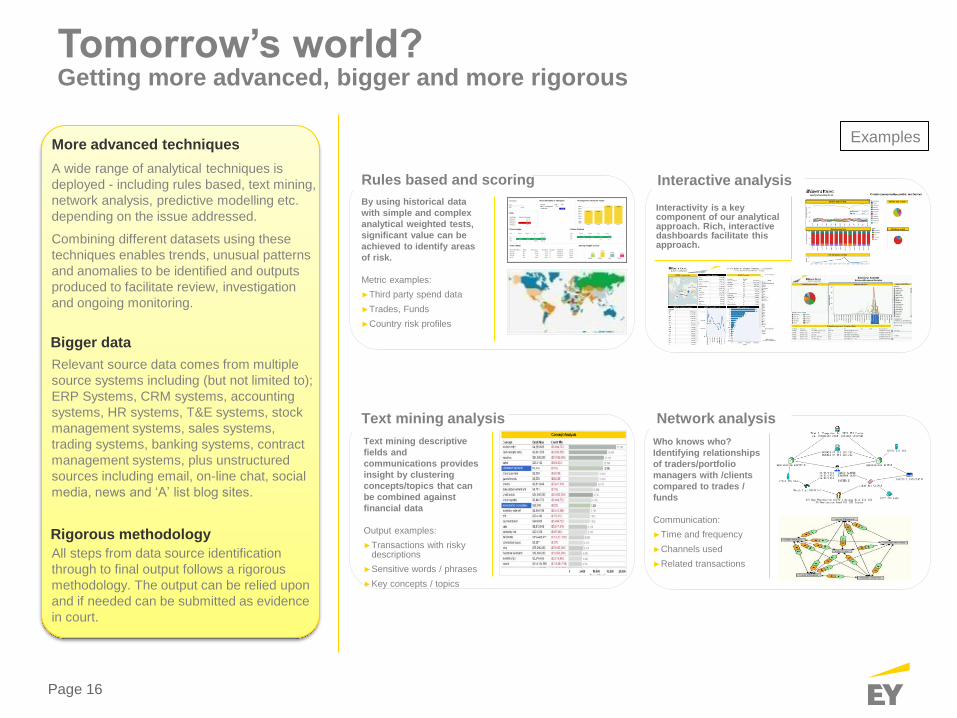

Relevant source data comes from multiple

source systems including (but not limited to);

ERP Systems, CRM systems, accounting

systems, HR systems, T&E systems, stock

management systems, sales systems,

trading systems, banking systems, contract

management systems, plus unstructured

sources including email, on-line chat, social

media, news and ‘A’ list blog sites.

By using historical data

with simple and complex

analytical weighted tests,

significant value can be

achieved to identify areas

of risk.

Metric examples:

►Third party spend data

►Trades, Funds

►Country risk profiles

Rules based and scoring

Bigger data

Interactive analysis

Network analysis

Who knows who?

Identifying relationships

of traders/portfolio

managers with /clients

compared to trades /

funds

Communication:

►Time and frequency

►Channels used

►Related transactions

Interactivity is a key component of our analytical approach. Rich, interactive dashboards facilitate this approach.

More advanced techniques

A wide range of analytical techniques is

deployed - including rules based, text mining,

network analysis, predictive modelling etc.

depending on the issue addressed.

Combining different datasets using these

techniques enables trends, unusual patterns

and anomalies to be identified and outputs

produced to facilitate review, investigation

and ongoing monitoring.

Text mining analysis

Text mining descriptive

fields and

communications provides

insight by clustering

concepts/topics that can

be combined against

financial data

Output examples:

►Transactions with risky descriptions

►Sensitive words / phrases

►Key concepts / topics

All steps from data source identification

through to final output follows a rigorous

methodology. The output can be relied upon

and if needed can be submitted as evidence

in court.

Rigorous methodology

Examples

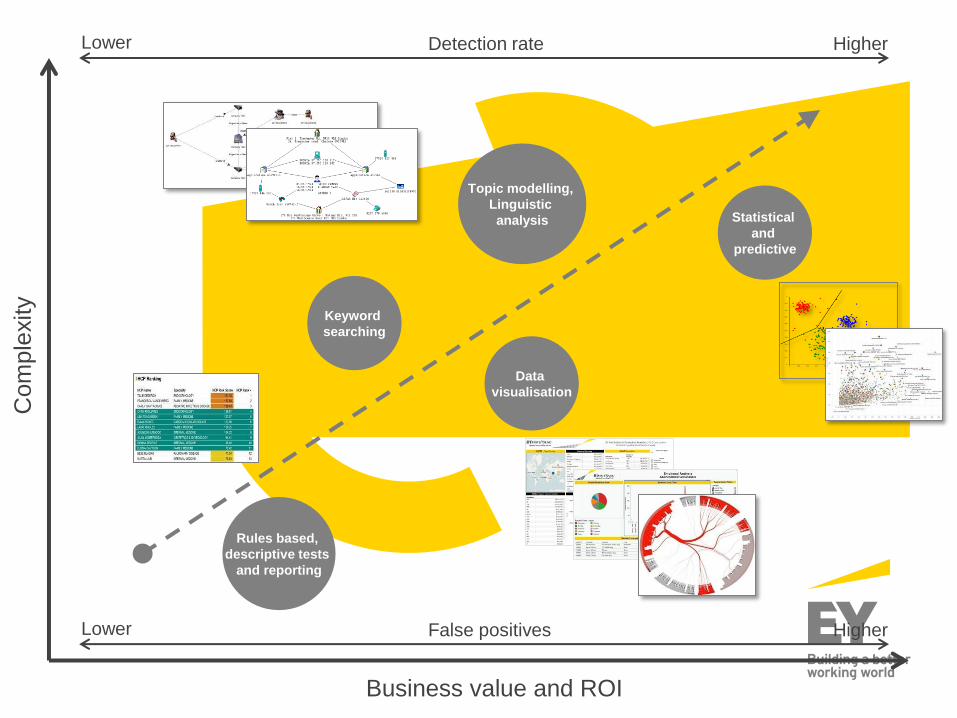

Tomorrow’s world? Getting more advanced, bigger and more rigorous

Data

visualisation

Topic modelling,

Linguistic

analysis

Keyword

searching

Rules based,

descriptive tests

and reporting

Statistical

and

predictive

Com

ple

xity

Business value and ROI

Detection rate Lower Higher

False positives Lower Higher

Page 18

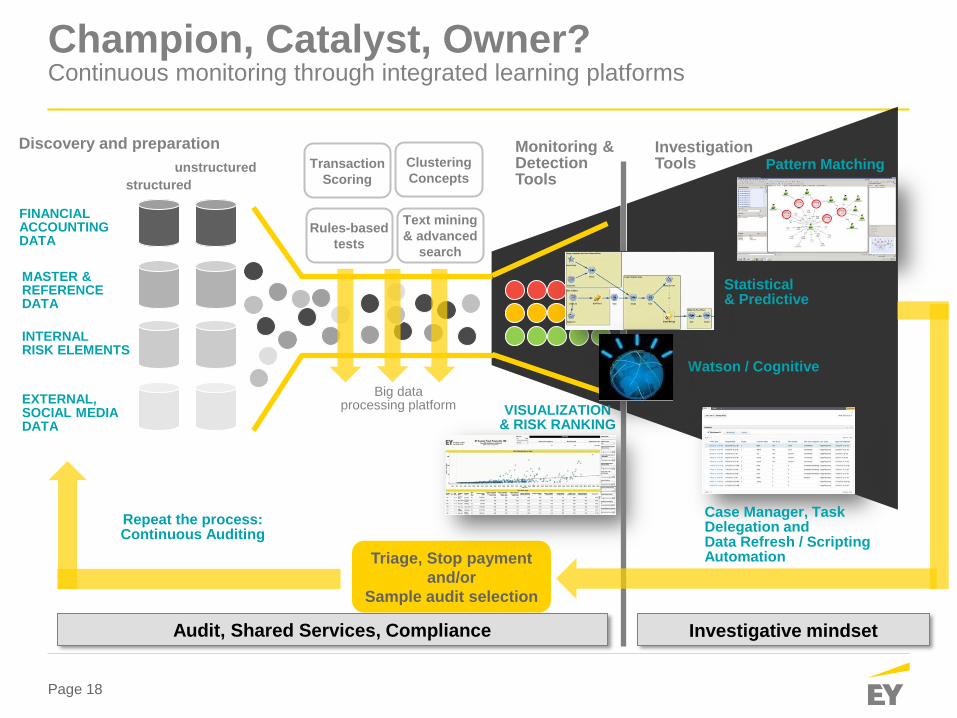

Champion, Catalyst, Owner? Continuous monitoring through integrated learning platforms

FINANCIAL ACCOUNTING DATA

MASTER & REFERENCE DATA

INTERNAL RISK ELEMENTS

EXTERNAL, SOCIAL MEDIA DATA

Rules-based

tests

Text mining

& advanced

search

VISUALIZATION & RISK RANKING

Triage, Stop payment

and/or

Sample audit selection

Big data processing platform

structured

unstructured

Statistical & Predictive

Pattern Matching

Case Manager, Task Delegation and Data Refresh / Scripting Automation

Monitoring & Detection Tools

Investigation Tools

Repeat the process: Continuous Auditing

Audit, Shared Services, Compliance

Watson / Cognitive

Investigative mindset

Discovery and preparation

Transaction

Scoring

Clustering

Concepts

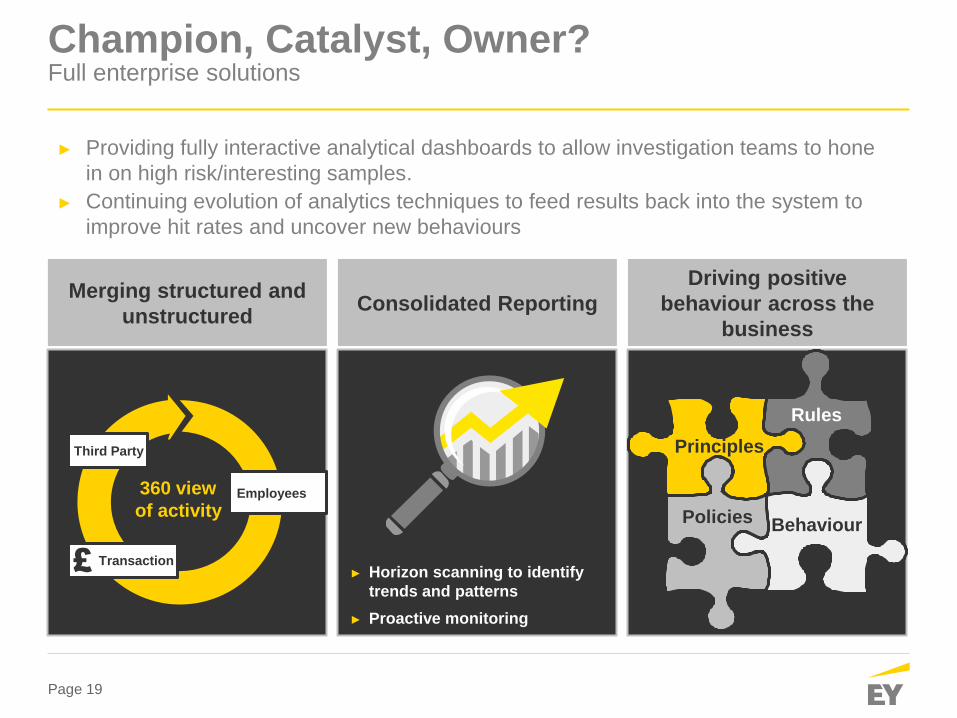

Page 19

Merging structured and

unstructured Consolidated Reporting

Driving positive

behaviour across the

business

360 view

of activity Employees

Transaction

Third Party

► Providing fully interactive analytical dashboards to allow investigation teams to hone

in on high risk/interesting samples.

► Continuing evolution of analytics techniques to feed results back into the system to

improve hit rates and uncover new behaviours

► Horizon scanning to identify

trends and patterns

► Proactive monitoring

Principles

Behaviour

Rules

Policies

Champion, Catalyst, Owner? Full enterprise solutions

Page 20

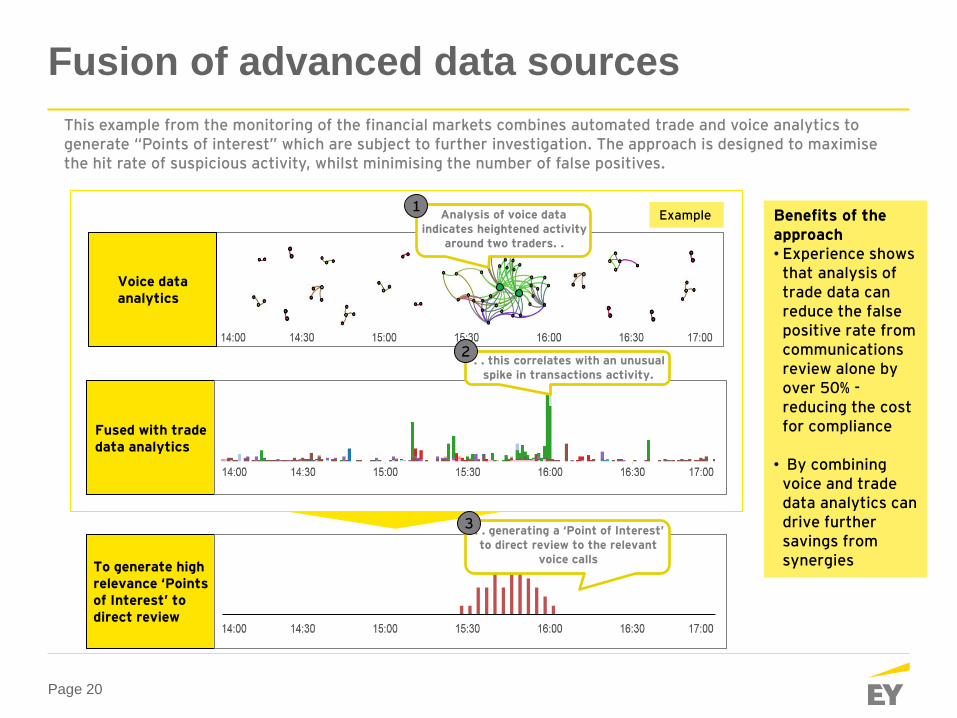

Fusion of advanced data sources

Example Benefits of the approach • Experience shows

that analysis of trade data can reduce the false positive rate from communications review alone by over 50% - reducing the cost for compliance

• By combining voice and trade data analytics can drive further savings from synergies

Voice data analytics

Fused with trade data analytics

Analysis of voice data indicates heightened activity

around two traders. .

To generate high relevance ‘Points of Interest’ to direct review

This example from the monitoring of the financial markets combines automated trade and voice analytics to generate “Points of interest” which are subject to further investigation. The approach is designed to maximise the hit rate of suspicious activity, whilst minimising the number of false positives.

. . this correlates with an unusual spike in transactions activity.

1

2

. . generating a ‘Point of Interest’ to direct review to the relevant

voice calls

3

The better the question. The better the answer.�The better the world works.

Questions / Discussion What’s your next step?