Embed Size (px)

Citation preview

Internship Report

On

Service Quality Dimensions of Foreign

Exchange Operations

A Study on

SOCIAL ISLAMI BANK LIMITED

Service Quality Dimensions of Foreign

Exchange Operations

A Study on

SOCIAL ISLAMI BANK LIMITED

Topic: “Service Quality Dimensions of Foreign Exchange Operations

A Study on

Social Islami Bank Limited”

Submitted to:

Dr. Md. Zakir Hossain Bhuiyan

Professor

Department of Marketing

Faculty of Business Studies

University of Dhaka.

Submitted by:

Provakar Ghose

Roll: 165, 17th Batch

Department of Marketing

Faculty of Business Studies

University of Dhaka.

Submission Date: April 7, 2015

Letter of Transmittal

April 7, 2015

Dr. Md. Zakir Hossain Bhuiyan

Professor

Department of Marketing

University of Dhaka

Subject: Submission of the internship report

Honorable Sir,

I am very pleased to submit my report on “Service Quality Dimensions of Foreign Exchange

Operations: A Study on Social Islami Bank Limited”.

I have tried my best to make it as worthwhile as possible. Despite time constraint and thorough

knowledge, I have put my best effort to represent it well. Please accept my sincerest apology for

misrepresentation, if any.

If you have any queries about this report please feel free to ask me.

I hope your kind consideration to the matter & oblige thereby.

Yours Sincerely,

Provakar Ghose

Department of Marketing

University of Dhaka

CERTIFICATE OF APPROVAL

I am glad to certify that the Internship Report on “Service Quality Dimensions of Foreign

Exchange Operations: A Study on Social Islami Bank Limited” conducting by Provakar

Ghose is bearing roll no: 165 , Batch 17th of the Department of Marketing, University of Dhaka

have been approved for viva-voce. Under my supervision Provakar Ghose worked with Social

Islami Bank Limited, one of the prominent commercial bank in Bangladesh. I am pleased to

hereby certify that the data the findings presented in the report are the authentic tasks of Provakar

Ghose.

It has indeed been a great pleasure working with him. I wish him all success in life.

-------------------------------

Supervisor

Dr. Md. Zakir Hossain Bhuiyan

Professor

Department of Marketing

University of Dhaka

ACKNOWLEDGEMENT

This is a matter of great pleasure that the “Internship Programme” done by me in leading

commercial bank “Social Islami Bank Limited” and the report on the internship programme

submitted to Dr. Md. Zakir Hossain Bhuiyan , Professor of Department of Marketing, University

of Dhaka.

I would like to convey my gratitude to the honorable internship supervisor Dr. Md. Zakir

Hossain Bhuiyan for providing all necessary help in the process of preparing this report and

analysis. I have learned so many diversified areas regarding service quality dimensions of

foreign exchange operations, practices by Social Islami Bank Limited.

My sincere thanks go to Md. Tareik Morshed, Head of Principal Branch, Social Islami Bank

Limited; Md. Moinuddin Hossain, Officer in charge of Export, Social Islami Bank limited; Md.

Asiqur Rahman, Head of Back to Back, Social Islami Bank Limited; Sudeb Ghosh, officer, Back

to Back, Social Islami Bank Limited for extending their support in collection information for

analysis and for giving their valuable time while the report was prepared.

Documents, Journals, Reports, Data that directly related with the “Foreign Exchange’s Service

Quality” taken as “Literature Review” for the purpose of the report. And all those documents are

attached on the part of Appendix.

Executive summary

“Service Quality Dimensions on Foreign Exchange Operation” this is a study on Social Islami

Bank Limited. This study attempted to understand the value of service quality dimensions of the

bank which help to measure the customer perceptions and satisfaction level while dealing with

this bank. The broad objective of this study is to know about the service quality dimensions on

foreign exchange operations of Social Islami Bank Limited. The specific objectives are, to know

about the reliability, assurance, empathy, tangibility, and responsiveness dimensions of service

quality and to make recommendations for improving the quality of different foreign exchange

services provided to the customers. The study has been conducted based on both the primary and

secondary sources of information. This research is descriptive in nature. Service quality

dimensions are evaluated through taking SERVQUAL model into consideration. A structured

questionnaire has been designed and used to collect data from the customers. Likert scaling

technique has been used to justify the dimensions of service quality of foreign exchange

operations. In the analysis of data, to test each dimension of the SERVQUAL model, more than

one statement taken into consideration. Hence, to find-out the mean value that actually represents

the each dimension, the individual mean value of all statements under each dimension are

summed-up and the summed-up value of the statements is divided by the number of statements.

The mean value of each dimension shows the extent of attitude that belongs to customers

regarding the service quality. The higher the mean value than the value of neutral which is 3, the

higher the respondents are agreed with and express positive attitude toward the each dimension

of service quality. In this study it is found that Social Islami Bank Limited is ensuring reliability

in moderately effective way, and tangibility, empathy & responsiveness in effective way. On the

other hand, it is maintaining the service in terms of assurance dimension in excellent way. So, it

is desired that if the bank authority takes proper actions on the basis of findings and provided

recommendations of this study, it will be able to achieve excellence in all aspects of its service

quality of the operations that ultimately satisfy the actual customers and attract the potential

customers.

ACRONYMS

SIBL : Social Islami Bank limited

IT : International Trade

SME : Small and Medium Enterprise

L/C : Letter of Credit

BB L/C : Back to Back Letter of Credit

B/L : Bill of Lading

B/E : Bill of Exchange

UCPDC: Uniform Customs and Practice for Documentary Credit IRC : Import Registration Certificate

ERC : Export Registration Certificate

EXP : Export Forms

ECC : Export Cash Credit

PC : Packing Credit

LIM : Loan against Imported Merchandise

PDC : Post-dated Cheque

CSR : Corporate Social Responsibilities

LLID : Loan Locator Identification Number

CAD : Cash against Document

EFT : Electronic Fund Transfer

Table of contents

Item No Particulars Page No

Letter of Transmittal i

Certificate of Approval ii

Acknowledgement iii

Executive Summery iv

Acronyms v

Chapter 01 (INTRODUCTION)

1.1 Literature Review 02

1.2 Statement of the Problem 03

1.3 Objectives of the Report 03

1.4 Sources of Data Collection 03

1.5 Methodology 04

1.6 Scope of the Report 05

1.7 Limitations of the Study 05

Chapter 02 (AN OVERVIEW OF THE BANK)

2.1 SIBL Vision 07

2.2 SIBL Mission 07

2.3 Strategic Objectives 07

2.4 Commitments 07

2.5 SIBL Core Values 07

2.6 Functions of SIBL 08

2.7 Performance of the Bank on 2014 08

Chapter 03 (FOREIGN EXCHANGE OPERATIONS)

3.1 Foreign Exchange Departments 09-11

3.1.1 Import Departments 10

3.1.2 Import Procedure of SIBL 10

3.1.3 Import Financing 11

3.2 Export Department 12-14

3.2.1 Export Procedure 12

3.2.2 Export L/C 13

3.2.3 Export Financing 13

3.2.4 Advance Against Bill under Collection 14

3.2.5 Checking and Advising of Export L/C 14

3.2.6 Processing and Opening of BB L/C 14

3.3 Foreign Remittance 15

Chapter 04 (ANALYSIS OF DATA & INTERPETATION)

4.1 Descriptive Analysis and Frequency Distribution 16

4.2 Descriptive Analysis 16

4.3 Frequency Distribution 16

4.4 Service Quality Dimensions Analysis 16-21

4.4.1 The SERVQUAL Instrument 17

4.4.2 Research Framework 17

4.5 Total Responses over the Dimensions 22-23

Chapter 05 (FINDINGS OF THE STUDY & RECOMMENDATIONS)

5.1 Findings of the Study 24-25

5.2 Recommendations 26

5.3 Conclusion 27

APPENDICES

References I-II

Appendix: 1 Questionnaire III-IV

Appendix:2 Data Analysis VI-XIV

Letter of Internship Placement XV

Letter of Declaration XVI

CHAPTER 1: INTRODUCTION

All over the world the dimension of banking has been changing rapidly due to deregulation,

technological innovation and globalization. Banking in Bangladesh has to keep pace with the

global change. In the market place, now banks must compete with local institutions as well as

foreign ones. To survive and thrive in such a competitive banking world, two important

requirements are development of appropriate financial infrastructure by the central bank and

development of “professionalism” in the sense of developing an appropriate manpower structure

and its expertise and experience. To introduce skilled banker, only theoretical knowledge in the

field of banking studies is not sufficient. An academic course of the study has a great value when

it has practical application in real life situation. In a simple word, excellence is the capacity of

producing desired result. So, Excellence of customer is, how customers perceive services, how

they assess whether they have experienced quality services and whether they are satisfied or not.

When it refers to excellence of customer, we assume that the dimensions of services and the

ways in which customers evaluate services are similar where the customer is internal & external

of the organization. In this report service quality dimensions of foreign exchange operations on

SIBL have been evaluated.

1.1 Literature Review

This study attempted to understand the customer perceptions on different service quality dimensions and

their satisfaction while dealing with SIBL. Service quality is defined as customer perception of how does

a service meets or exceeds their expectations (Czepiel, 1990). Several practitioners define service quality

as the difference between customer’s expectations for the service encounter and the perceptions of the

service received (Munusamy et al., 2010). Customer expectation and perception are the two main

ingredients in service quality. Customers judge quality as “low” if performance (perception) does not

meet up their expectation and quality as „high‟ when performance exceeds expectations according to

Oliver (1980).To measuring the sevice quality the most popular model is the SERVQUAL (service

quality) model developed by Parasuraman et al. The SERVQUAL model of Parasuraman et al. (1988)

proposed a five dimensional construct of perceived service quality tangibles, reliability, responsiveness,

assurance and empathy as the instruments for measuring service quality (Parasuramanet el al., 1988;

Zeithamlet el al., 1990). With a view to providing better service to the customers, the bankers need to

apply the technology in banking; islami sharia based banking system and customized customer service.

Ahmed, Feroz and Islam, Md. Tarikul (2008)observed that adopting e-banking services, banks in

developing countries are faced with strategic options between the choice of delivery channels and the

level of sophistication of services provided by these delivery channels. The profit growth of any bank

depends on the service quality of the bank. And now days, better quality service depends on technology.

Mohammad Anisur and Debnath, Nitai Chandra (2007) commented that the banking sector in Bangladesh

is clearly recognizing the importance of information technology to their continued success. Shamsuddoha

(2008) argued that in Bangladesh, banking industry is mature to a great extent than earlier period. It has

developed superb image in their various activities including electronic banking. Now modern banking

services have launched by some multinationals and new local private commercial banks. Electronic

banking is one of the most demanded and latest technologies in banking sector. Nyangosi , Arora , Singh

(2009) argued that banking through electronic channels has gained increasing popularity in recent years.

This system, popularly known as 'e-banking', provides alternatives for faster delivery of banking services

to a wide range of customers. It can be different types of loan like car loan, study loan etc and lower

interest for loan, increase the interest rate for deposits. By considering the those recommendations the

SIBL can improve their service quality and satisfied their customers with effectively and efficiency and

makes them loyal customers of SIBL considering the volume of operation and limitations of resources

and proper management the bank is doing better than many modern banks.

1.2 Statement of the Problem

In the current study, dimensions like reliability, responsiveness, assurance, tangibility and

empathy have been used to find out the customer service quality of SIBL.

1.3 Objectives of the Report

The objectives of the study are as follows:

1.3.1 Broad Objective:

The broad objective of the report is to know about the service quality dimensions of

foreign exchange operation on Social Islami Bank Ltd.

1.3.2 Specific Objective:

To know about the reliability, responsiveness, assurance on service quality of SIBL.

To know about the customers’ empathy, tangibility, satisfaction on service quality of

SIBL.

To make recommendations for improving the quality of different services provided to the

customers by SIBL.

1.4 Sources of Data Collection

The study has been conducted based on both the primary and secondary sources of information.

1.4.1 Primary Data

Primary data has been gathered from the customers when they came for services at the office

of SIBL. Questionnaire has been provided to those customers who are interested in

participating in the survey.

1.4.2 Secondary Data

Annual reports of SIBL, Previous report on foreign exchange, online articles/website of

SIBL. Bangladesh Bank’s publications have been used as a secondary dada.

1.5 Methodology

1.5.1 Research Design

This research is descriptive in nature. The topic has selected and at first made an exploratory

research. Then data collected for making the report. Here, Likert scaling technique has been

used for measuring service quality dimensions.

1.5.2 Population

The questionnaires have been distributed to those customers who have taken any kind of

services from this bank, whether they are L/C holder or account holder of this bank. The

Branch total population is more then 500. For conducting this research 30 sample are taken

from the population.

1.5.3 Survey Method

Questionnaire has used for this survey. Required data are collected both from secondary

source and primary source.

1.5.4 Sample Size

For conducting this research total sample size is 30.

1.5.5 Sampling Technique

For customer interview here non probability convenience sampling technique has been used.

1.5.6 Scaling Technique

From different scaling technique, in this study Likert scale has been used to collect data.

Typically, each scale item has five response categories, ranging from “strongly disagree to

strongly agree”.

Strongly Agree = 5

Agree = 4

Neutral = 3

Disagree = 2

Strongly Disagree = 1

1.5.7 Statistical Tool

Here the descriptive statistics has been used. Microsoft Excel is used to get the output of

those data. Followed the following steps to prepare the report:

Defined the problem.

Development of an approach to the problem.

Research design formulation.

Gathering the data.

Processing and analyzing the data.

Report preparation and presentation.

1.6 Scope of the Report

This report is going to show details about foreign exchange operations of SIBL. This study is

also going to identify the customer service quality of SIBL, considering key dimensions such

as reliability, responsiveness, assurance, empathy, and tangibles.

1.7 Limitations of the Study

Secrecy or confidentiality is a crucial matter in this organization. As an intern it was

not possible to reach those secret topics.

Not able to collect information from all the clients.

Limited service hour.

CHAPTER 2: AN OVERVIEW OF THE BANK

The SOCIAL ISLAMI BANK LTD (SIBL), a second-generation bank, operating since 22

November, 1995 based on Shariah Principles, has now 100 branches all over the country with

two subsidiary companies - SIBL Securities Ltd. & SIBL Investment Ltd. Targeting poverty,

Social Islami Bank Limited is indeed a concept of 21st century participatory three sector banking

model in one. In the formal sector, it works as an Islamic participatory commercial bank with

human face approach to credit and banking on the profit and loss sharing: it is a Non-formal

banking with informal finance and credit package that empowers and humanizes real poor family

and create local income opportunities and discourages internal migration; it is a development

bank intended to monetize the voluntary sector and management of Waqf, Mosque properties

and introducing cash Waqf system for the first time in the history. In the formal corporate sector,

this bank would, among others, offer the most up to date banking services through opening of

various types of deposit and investment accounts, financing trade, providing letters of guarantee,

opening letters of credit, collection of bills, leasing of equipment and consumers' durable, hire

purchase and installment sale for capital goods, investment in low-cost housing and management

of real estates, participatory investment in various industrial, agricultural, transport, educational

and health projects and so on.

SIBL is a pioneer in introducing on-line banking among all the Islami banks of the country with

state-of-the-art banking software, which will enable the bank to perform as any branch real time

banking service to the clients. The state-of-the-art banking software of the bank will enable to

perform as any branch real time banking service to the clients. SIBL is supported by core

banking solutions and products & services are strongly backed by IT infrastructure, which are

upgraded & expanded on continuous basis.

SIBL lays emphasis on employment generated, environment friendly and green banking based

investment keeping an eye on equitable distribution of resources over geographical territory for

sustainable growth of macro economy of the country.

The bank's continuous effort has been to increase the shareholders' value, and be valued as a

compliant organization. The corporate governance systems in SIBL ensure transparency and

accountability at all levels in conducting business. SIBL in its journey towards continuous

excellence has changed its brand logo recently. Bank takes pride in their new logo.

2.1 SIBL Vision:

Working together for a caring society.

2.2 SIBL Mission

Transformation to a service oriented technology driven profit earning bank.

Empowering real poor families and creating local income opportunities.

Fast, accurate and satisfactory customer service.

Providing support for social benefit organizations by way of mobilizing funds and social

services.

2.3 Strategic Objectives

Transformation into a service-oriented technology-driven profit earning bank.

Ensure fast, accurate and best-in-class customer services with customers’ satisfaction.

To achieve global standards in Islamic Banking.

2.4 Commitments

to the Shariah

to the Shareholders

to the Customers

to the Employees

to the other Stakeholders

to the Environment

2.5 SIBL Core Values

Towards the Journey of Excellence, SIBL has changed its brand logo. The new logo depicts

bird’s wings with 9 feathers to represent its core values- comfortable and safe tying in the

economic sky of the country connecting it with the global sky by passing the territorial boundary.

2.6 Functions of SIBL

Deposit procurement & management under Shariah Principles.

Foreign Exchange Services i.e. Letter of Guarantee, Money Transfer etc.

Corporate Social Responsibilities (CSR).

Investment using Islamic Financial Contract.

2.7 Performance of the Bank on 2014

Fig in Million Taka

Honesty

Efficency

Accountability Transparency

Flexibility

Innovation Religiousness

Security

Technology

Indicators Target 2014

Actual 2014

Actual 2013

Achievement %

Growth %

Deposits 150,000.00 109,040.63 95,984.8 72.69% 13.60% Investments 120,000.00 107,899.96 85,922.33 89.92% 25.58% Foreign Exchange 230,000.00 139,910.00 132,374.70 60.83% 5.69% Operating Profit 5,500.00 3,964.27 2,894.06 72.08% 36.98%

CHAPTER 3: FOREIGN EXCHANGE OPERATIONS

Foreign exchange covers all business activities relating to import, export, inward and outward

remittance and buying and selling of currency. One of the largest businesses carried out by the

commercial bank is foreign trading. The trade among various countries falls for close link

between the parties dealing in trade International trade demands a flow of goods from seller to

buyer and of payment from buyer to seller. In this case the bank plays a vital role to bridge

between the buyer and seller.

Year 2010 2011 2012 2013 2014

Import 39459.50 68198.50 76985.60 73859.40 79024.20

Export 21372.20 34975.00 42712.20 51775.30 53044.90

Remittance 1099.40 5134.90 6822.10 6740.00 7839.90

Total 61931.00 108308.30 126519.90 132374.70 139910.00

(Fig in Million Taka)

SIBL foreign exchange business stood at Tk. 139910.00 million in 2014 against Tk. 132374.70

million in 2013, which is sharp increase of 16.32%.

In Social Islami Bank Ltd. (Principal Branch) foreign exchange division has one part which is

foreign trade.

3.1 Foreign Exchange Departments

Foreign exchange division includes the following departments

Import Department

Export Department

Foreign Remittance Department

3.1.1 Import Department

To bring in, from abroad, something in kind of goods or services (to behave lawfully) is

import. Import trade finance by SIBL rose to BDT 79024.20 million in 2014 compared with

BDT 73859.40 million in 2013. The growth rate is increased by 6.73%. In reporting year

2014 the Bank opened a total number of 113,260 LCs. Large LCs were opened mainly for

importing old ships, rice, wheat, edible oil, fertilizer, capital machinery, fabrics and

accessories, petroleum products and other consumer products.

Year 2010 2011 2012 2013 2014

Import 39459.50 68198.50 76985.60 73859.40 79024.20

3.1.2 Import Procedure of SIBL

Import means purchasing products from other countries for further process or to sell in local

market. Social Islami Bank Ltd plays a vital role in import financing system. There are some

different steps in whole import process. These are as follows:

LC Opening

Document Negotiate

Payment Clear

Bill of entry

File closed

L/C opening:

A letter of credit is a financing instrument opened by a foreign buyer with a bank in her/his

locality. The letter of credit stipulates the purchase price agreed upon by the buyer and seller, the

quantity of merchandise to be shipped and the type of insurance coverage to protect the

merchandise during shipment. The letter of credit names the seller as beneficiary (that is, you are

the party who gets paid) and identifies the definite time period, the terms remain in force. The

letter of credit authorized the buyers to pay when all the stipulated conditions have been met. A

letter of credit gives some assurance to the seller that the buyer is solvent.

Opening of LC is the first requirement of import. The importer must have account in the certain

bank. Some of the most essential documents of LC are described as follows:

Import Registration Certificate (IRC)

Invoice

Bank charged documents:

Bank charges some documents to the exporter on behalf of the party or importer. These

documents are:

i. LC Application form

ii. IMP from

iii. DP Note/ Promissory Note

iv. Additional guarantee letter etc

3.1.3 Import Financing

Loan against Imported Merchandise (LIM):

Loan against Imported Merchandise (LIM) is a facility provided by the Bank to the importers

who are in shortage of fund to retire the import bills and thus to clear the goods from the post

authority. In other works it may be referred as an advance against merchandise.

LIM Accounts may be created in the following two cases:-

LIM Account on importer’s request:

Forced LIM Account

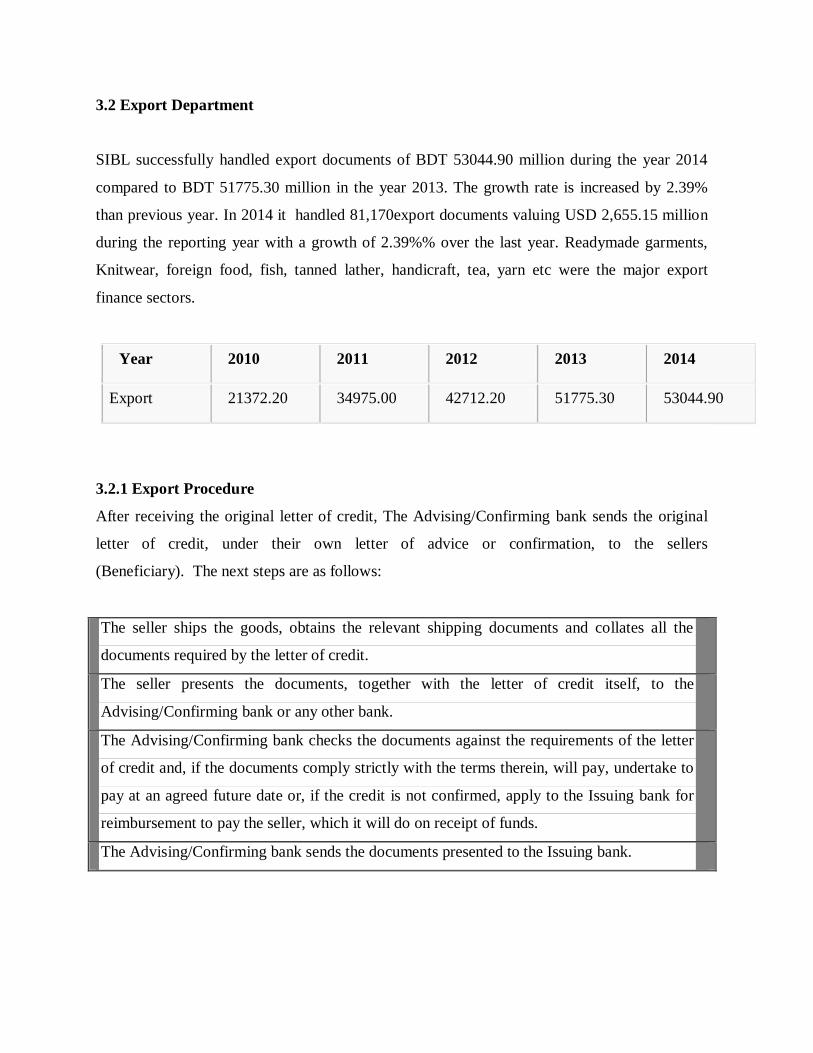

3.2 Export Department

SIBL successfully handled export documents of BDT 53044.90 million during the year 2014

compared to BDT 51775.30 million in the year 2013. The growth rate is increased by 2.39%

than previous year. In 2014 it handled 81,170export documents valuing USD 2,655.15 million

during the reporting year with a growth of 2.39%% over the last year. Readymade garments,

Knitwear, foreign food, fish, tanned lather, handicraft, tea, yarn etc were the major export

finance sectors.

Year 2010 2011 2012 2013 2014

Export 21372.20 34975.00 42712.20 51775.30 53044.90

3.2.1 Export Procedure

After receiving the original letter of credit, The Advising/Confirming bank sends the original

letter of credit, under their own letter of advice or confirmation, to the sellers

(Beneficiary). The next steps are as follows:

The seller ships the goods, obtains the relevant shipping documents and collates all the

documents required by the letter of credit.

The seller presents the documents, together with the letter of credit itself, to the

Advising/Confirming bank or any other bank.

The Advising/Confirming bank checks the documents against the requirements of the letter

of credit and, if the documents comply strictly with the terms therein, will pay, undertake to

pay at an agreed future date or, if the credit is not confirmed, apply to the Issuing bank for

reimbursement to pay the seller, which it will do on receipt of funds.

The Advising/Confirming bank sends the documents presented to the Issuing bank.

3.2.2 Export L/C

There are a number of formalities, which an exporter has to fulfill before and after shipment of

goods. These formalities or procedures are enumerated as follows –

1. Obtaining Export Registration Certificate (ERC)

2. Securing the order

3. Obtaining EXP

4. Signing of the contract Receiving the Letter of Credit

5. Procuring the materials

6. Endorsement on EXP

7. Disposal of Export Forms

8. Shipment of goods

9. Presentation of export documents for negotiation

10. Cash against document (CAD) Contract

11. Examination of document

12. Negotiation of export documents

3.2.3 Export Financing

Export of services and goods constitute an important part for long-term development prospect

of a country. Exports are, therefore, listed in priority sector and government always provides

different sorts of incentive or subsidies for growth of export. The government and banks give

the financing support to the exporters through the following channels:

I) Pre-shipment Financing,

II) Post-shipment financing,

Pre-shipment Financing:

In order to assist the exporters to ship the goods to foreign buyers, the banks make pre-

shipment finance to the exporters in the following ways:

Export Cash Credit (ECC)

Packing Credit (PC)

Post-shipment Financing:

The advance given to an exporter after the shipment is made is post-shipment finance.

They are given in the following manners

Negotiation of documents under L/C.

Negotiation under reserve or guarantee.

.

3.2.4 Advance against Bill under Collection

It sometime happens that the exporter has sufficient financial support of his own and

presented the document against exports L/C to bank for collection. But all on a sudden he

may require fund for meeting emergency need. In such a situation the exporter may approach

bank for finance against bill sent for collection awaiting remittance. In such a situation, bank

may allow overdraft up to a certain percentage (Say maximum 80%) of the value of the bill

under collection. In addition to the export bill as security, bank may ask for collateral security

by way of third party guarantee or mortgage of property.

3.2.5 Checking and Advising of Export L/C

On receipt of Export L/C is to be recorded in the banks inward Register and then the signature

o the Export L/C or test number for telex L/C is to be verified by an authorized officer of a

bank and finally it is to be forwarded to the beneficiary under forwarding schedule.

3.2.6 Processing and Opening of BB L/C

An exporter desired to have an import L/C limit under Back to Back arrangement. In that case

the following papers and documents are required:

1. Full particulars if bank account

2. Balance sheet

3. Statement of Assets & Liabilities

4. Trade license

5. Valid bonded warehouse license

6. Membership certificate

7. Income tax declaration

8. Memorandum & Articles of Association

9. Partnership deed

10. Resolution

11. Photographs (All Directors)

On receipt of above documents and papers the back to back L/C opening section will prepare a

credit report. Branch must obtain sanction from Head Office for opening of BB L/C.

3.3 Foreign Remittance

Social Islami Bank Ltd has remittance arrangement with different banks and exchange homes

in various countries throughout the world. The bank has earned the confidence and reputation

as a reliable organization of paying hard-earned money of the expatriate Bangladeshis to their

beneficiaries in the country safely and quickly.

Year 2010 2011 2012 2013 2014

Remittance 1099.40 5134.90 6822.10 6740.00 7839.90

The bank handled BDT 7839.90 million remittances in 2014 showing an increase of

BDT1099.90 million the previous year 2013which registered an attractive growth of 14%.

Introduction of products like Home Delivery Scheme, Electronic Fund Transfer (EFT) and

different instant payment system and modern technologies like SWIFT and inline services

have strengthened the position of the bank in channeling remittance proceeds. The remittance

cell at the Head Office is working for smooth and speedy delivery of remittances to all the

branches through online system. Beneficiaries are also informed through SMS regarding their

remittances.

All these efforts have propelled bank to a higher position with the support of 106 branches at

home, 38 Exchange Companies/Banks abroad and a vast network of Western Union all over the

world.

CHAPTER 4: ANALYSIS OF DATA & INTERPRETATION

This report is analyzed in a descriptive way. Excel software has been used to complete this report

so the data which are given is reliable and perfectly analyzed. Different groups of customers are

asked questions to collect information for this research.

4.1 Descriptive Analysis and Frequency Distribution

To analyze respondents answer, I have done descriptive analysis and frequency distribution.

4.2 Descriptive Analysis

It refers the transformation of raw data into a form that makes easy to understand and interpret;

rearranging, ordering, manipulating data to provide descriptive information.

4.3 Frequency Distribution

It refers a set of data organized by summarizing the number of times a particular value of a

variable occurs. Here targeted sample size is 30. The main target of this report is to know service

quality dimensions of SIBL. By using descriptive analysis and frequency distribution, we can

assume about the total population.

4.4 Service Quality Dimension Analysis and Discussion

In the changing banking scenario of 21st century, the banks had to have a vital identity to

provide excellent services. Banks nowadays have to be of world-class standard, committed to

excellence in customer’s satisfaction. The purpose of banking operations has been supposed to

be to progress the quality of life for the overall society not just the maximization of shareholders'

wealth.

Service quality has been defined as the overall assessment of a service by the customers while

other studies defined it as the extent to which a service meets customer’s needs or expectations.

4.4.1 The SERVQUAL Instrument

The SERVQUAL instrument developed by Parasuraman et al (1991) has proved popular, being

used in many studies of service quality. This is because it has a generic application and is a

practical approach to any area. I have applied the SERVQUAL model to measure service quality

dimensions of SIBL.

There are five dimensions by which service quality can be measured. If those dimensions are

positive to customers, the overall service quality can meet satisfaction level of customers, if not

customer will be dissatisfied with their current service.

4.4.2 Research Framework

Reliability Dimensions

Reliability depends on handling customers' service problems; performing services right the first

time; provide services at the promised time and maintaining error-free record. Furthermore, they

SERVQUAL

Reliability

Responsiveness

Empathy

Tangibility

Assurance Customer

Satisfaction

stated reliability as the most important factor in conventional service. Reliability also consists of

accurate order fulfillment; accurate record; accurate quote; accurate in billing; accurate

calculation of commissions; keep services promise. Reliability is the most important factor in

banking services.

Statements Average Likert

Scores (ALS)

Mean of Reliability

=∑(ALS)/N

The bank performs the service right the first time. 2.63

3.23

The bank promises to do something by a certain

time, it does so.

3.80

If you have a problem, the bank shows an

insincere interest in solving it.

3.27 (reversed)

Total numbers of Statement (N) =3 ∑(ALS) = 9.70

The average Likert scores for statements (Appendix:2), right service at first time is 2.63 which is

below the neutral (3), for the bank promises to do something by a certain time is 3.80 which is

above the neutral (3), and the bank shows an insincere interest in solving the problem by

reversed coding its average score is 3.27 which is also above the neutral (3).That means

customers support with the last two statements, and disagree with the first statement.

The higher the mean the higher the respondents agree with the reliability. The mean of reliability

is 3.23 which show that customers are positive with reliability service dimension of SIBL. So the

mean indicate that SIBL is ensuring reliability of service quality properly.

Assurance Dimensions

Assurance is a knowledge and courtesy of employees and their ability to inspire trust and

confidence. In SIBL assurance means the polite and friendly staff, provision of financial advice,

interior comfort, eases of access to account information and knowledgeable and experienced

management team.

Statements Average Likert

Scores (ALS)

Mean of Assurance

=∑(ALS)/N

You feel safe in foreign transactions with the

bank.

4.83

4.215 The behavior of employees is confident,

trustworthy & knowledgeable.

3.60

Total numbers of Statement (N) =2 ∑(ALS) = 8.43

The average Likert scores for statements (Appendix:2), customer feel safe in foreign transactions

with the bank, the behavior of employees is confident, trustworthy & knowledgeable, are 4.83 &

3.60. All of statements are above the neutral Likert scores 3. That means customers support with

the statements.

The higher the mean the higher the respondents agree with the assurance. The mean of assurance

is 4.215, which is closest to highest Likert scaling point 5. So we can say that SIBL is able to

fulfill the assurance which is more than minimum expectation of the customers.

Tangibility Dimensions

Tangibility is the appearance of physical facilities, equipment, personnel, and written materials.

Tangibility in their study of private sector banks is modern looking equipment, physical facility,

employees are well dressed and materials are visually appealing.

Statements Average Likert

Scores (ALS)

Mean of Tangibility

=∑(ALS)/N

SIBL has traditional and outdate looking

equipment.

3.37 (reversed)

3.67

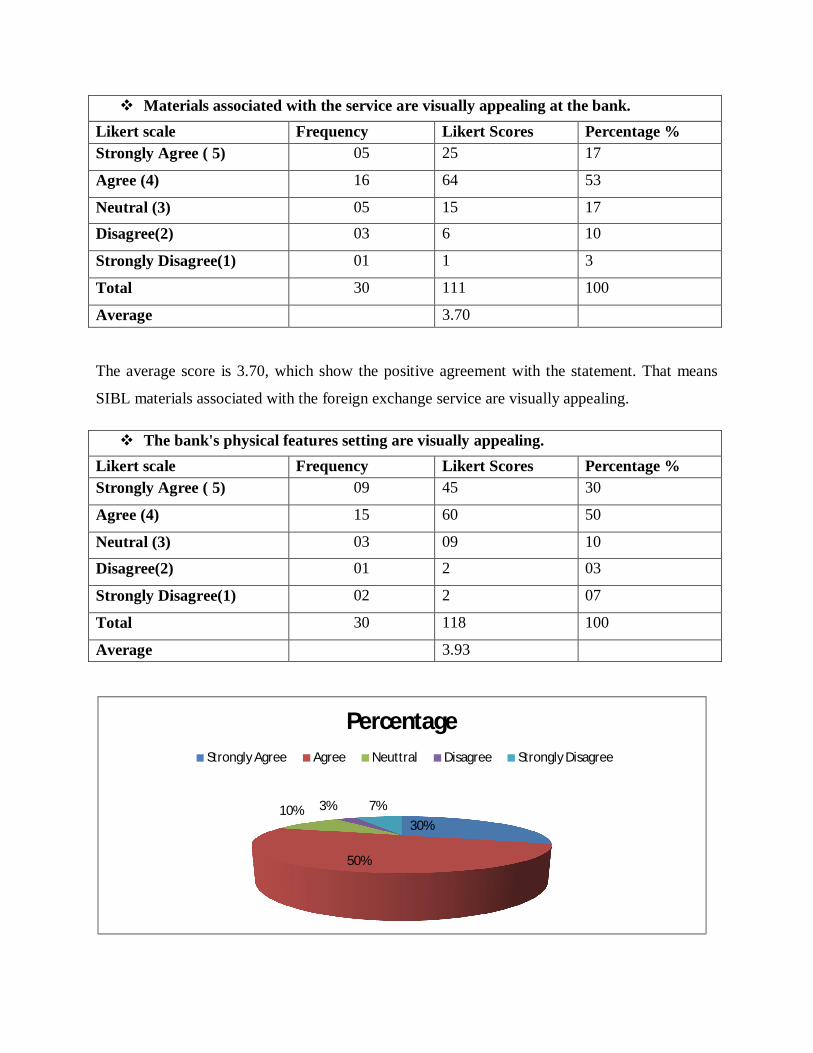

Materials associated with the service are visually

appealing at the bank.

3.70

The bank's physical features setting are visually

appealing.

3.93

Total numbers of Statement (N) =3 ∑(ALS) = 11.00

The mean of tangibility is 3.67.Which is above the neutral Likert scores and closest to highest

point 5. So the service quality of SIBL is tangible to customers.

Empathy Dimension

Empathy is the caring and individual attention the firm provides its customers. It involves giving

customers individual attention and employees who understand the needs of their customers and

convenience business hours. Empathy in this study on SIBL is giving individual attention;

convenient operating hours; giving personal attention; best interest in heart and understands

customer’s specific needs.

Statements Average Likert

Scores (ALS)

Mean of Empathy

=∑(ALS)/N

The employees of SIBL understand your specific

needs.

4.20

3.50 The bank has not operating hours convenient to

all its customers.

3.27 (reversed)

The bank gives you individual attention. 3.03

Total numbers of Statement (N) =3 ∑(ALS) = 10.50

The average Likert scores for statements (Appendix:2), the employees of SIBL understand

customers specific needs is 4.20, for the bank has not operating hours convenient to all its customers by

reversed coding its average is 3.27, and SIBL gives you individual attention is 3.03. All of statements

have above the neutral scores 3.That means customers support with the statements.

The mean of empathy is 3.50, which is above the neutral Likert scores and closest to highest

point 5. Thus SIBL acquire empathy in their service.

Responsiveness Dimension

Responsiveness defined as the willingness or readiness of employees to provide service. It

involves timeliness of services. It is also involves understanding needs and wants of the

customers, convenient operating hours, individual attention given by the staff, attention to

problems and customers‟ safety in their transaction.

Statements Average Likert

Scores (ALS)

Mean of Responsiveness

=∑(ALS)/N

The bank tells you exactly when the services

will be performed.

3.13

3.55

Employees in the bank are never too busy to

respond to your request.

3.40

Employees in the bank are always willing to

help you.

4.13

Total numbers of Statement (N) =3 ∑(ALS) =10.66

The average Likert scores for statements (Appendix:2), the bank tell you exactly when the

services will be performed is 3.13, for employees in the bank are never too busy to respond to

your request is 3.40. All of statements have above neutral Likert scores 3. That means customers

support with the statements.

The higher the mean the higher the respondents agree with the assurance. The mean of

responsiveness is 3.55 which are closest to highest point 5. So the bank is able to confirm its

responsiveness to the customers for gaining the customer satisfaction.

4.5 Total Responses over the Dimensions

On the dimension of reliability, 50% respondents have shown positive attitude towards the

foreign exchange operations of SIBL, 31% have seen it negatively and 19% respondents have

seen it neither good nor bad.

For the dimension of assurance, 82% respondents have shown positive attitude towards the

foreign exchange operations of SIBL, 6.5% have seen it negatively and 11.5% respondents have

seen it neither good nor bad.

DIMENSIONS

Reliability

Assurance

Tangibility

Empathy

Responsiveness

Totally positive

Totally Negative

Neutral

50%

82%

66.7%

57%

54.3%

31%

11.5% 6.5%

13%

20.7%

12.3%

19%

20.3%

22.3%

33.3%

66.7% respondents have shown positive attitude towards the foreign exchange operations of

SIBL, 13% have seen it negatively and 20.3% respondents have seen it neither good nor bad on

the dimension of tangibility.

On the dimension of empathy, 57% respondents have shown positive attitude towards the

foreign exchange operations of SIBL, 20.7% have seen it negatively and 22.3% respondents have

seen it neither good nor bed.

On the dimension of responsiveness, 54.3% respondents have shown positive attitude towards

the foreign exchange operations of SIBL, 12.3% have seen it negatively and 33.3% respondents

have seen it neither good nor bed.

CHAPTER 5: FINDINGS OF THE STUDY & RECOMMENDATIONS

5.1 Findings of the Study

From the overall output of this research work it is clearly stated that the customer satisfaction

level and service quality towards foreign exchange division of SIBL is enough satisfied.

It has been pointing out some focusing area from the respondent’s view according to objectives

that shows below:

Service Quality Dimensions Mean

Reliability 3.23

Assurance 4.215

Tangibility 3.67

Empathy 3.50

Responsiveness 3.55

Service quality dimensions of foreign exchange operations of SIBL are more appropriate to

satisfy their customers. More than 50% respondents have shown positive attitude towards service

quality. The mean of all service quality dimensions are more than indifferent point (3) which

focus service quality dimensions have ability to satisfy customers.

Most of the clients in SIBL are satisfied with Foreign exchange service of giving

statement.

The Reliability dimension of service quality is not better as compared to other

dimensions. Still the score is low. Customers of the bank hesitate to rely on the bank.

As score for Assurance is at first place in the dimensions, so the customers of SIBL are

very confident and feel safe while transacting with the bank. Moreover the employees of

the bank have proved to be trustworthy. Employees are also educated enough to answer

all the questions.

The score of Tangibility dimension of service quality of SIBL is the 3.67. This indicates

that the physical structure of SIBL neither so modern nor so outdated.

The score of Empathy is not so satisfactory but not so unsatisfactory also.

In SIBL, the score of Responsiveness is 3.55 so they are focusing on prompt service,

employees are willing to help the customers and say the exact time when the services will

be performed.

All the officers are so much helpful and have a friendly working environment. They help

each other, when any officer falls in trouble.

The top executives and officers are very helpful to the clients. Some of our businessmen

do not know the exact procedures of international trade. The officers of SIBL help them

to properly execute their business.

SIBL provide little assistance in relation with foreign exchange to the small entrepreneur

comparing to large business houses. Small entrepreneur has to keep higher margin,

sometimes 100%, regarding opening a L/C.

SIBL has limited promotional activities about foreign exchange services to increase

motivate its present and potential investment client.

The presence of modern data processing and communication equipments is inadequate in

SIBL. This cause considerable disagree of inefficiency in the bank’s performance,

especially in the foreign exchange department.

5.2 Recommendations

This complementary study recommends that SIBL to expand their foreign exchange Services in a

planned and well articulated strategy for the long run, in order to have customer satisfaction and

increase in banks profitability. I had the practical exposure in SIBL for just two months. On the

basis of my observation I would like to present the following recommendations-

SIBL should offer some services to attract the foreign remittance. As Bangladesh has a

high number of non residential, collecting remittances can be a good way of generating

revenue for the company.

SIBL needs to improve reliability dimensions of their services like, right at first time

services, fast services, error free services and sincere interest about customer’s problems.

Modern equipments, new improved technology should be replaced with the old ones.

Bank employees would be encouraged to learn to recognize these regular customers,

learn their names, and begin to identify their basic service requirements.

Evening banking allowance may be increased.

SIBL should improve their integrated marketing activities.

Reducing existing charges can successfully attract a huge number of customers to SIBL if

charges are made considerable, SIBL can capture a big portion of middle class society

who can be proved to be better customer than any other class of the society. SIBL should

lower their charges immediately so as to prevent the loss of customers.

The bank should move to the fully automated banking system. This will save a lot of time

of personnel working here and will increase their and the bank’s performance thereby.

In case of exporting goods the bank should aware about under invoicing so that nobody

can get chance to avoid Tax, Vat, and Duty.

The Gap between customer expectation & employee perception is to be reduced so as

maintain a smooth transaction between staffs & customers.

The five-dimensional structure could possibly serve as a meaningful framework for

tracking a banks service quality performance over time and comparing it against the

performance of competitors.

5.3 Conclusion

Growing influence of globalization on the Bangladeshi banking industry, a number of global and

local banks are coming into the Bangladeshi banking industry. In such a dynamic environment

the banks need to be more quality conscious since the products offered are almost similar by all

the banks in the industry. The bank needs to take serious efforts to make it competitive and stable

in the dynamic market situation by focusing on the service quality dimensions.

SIBL actively takes place in foreign exchange especially in export and import. Every year bank

earns a lot of money by issuing letter of credit and its growth rate increase at in increasing rate.

Through the import, export and foreign operations, this department is making a great

contribution to the bank and the economy as a whole. In this study it is found that SIBL has

reached the position by its commitment, people’s love and dedicated human resource SIBL has

been shown supremacy in all kind of banking operations in our country.

To conclude I must say that Social Islami Bank it has immense potential in Bangladesh. It can

play vital role in bringing revolutionary changes in our life with both material and moral world

and in individual and collective level.

REFERENCES

Books

Malhotra, K, Naresh, Dash, Satyabhushan, 2010, marketing research: an applied orientation, 6th

edition, pp.68-384, Prentice Hall of India private limited.

Mudie Peter, Cottam Angela , 2011, Management and Marketing of Services, 2nd edition, pp. 34

67 , Routledge , Milton Park ,New York.

Journal & Articles

Berry, L., Parasuraman, A. and Zeithaml, V., 1994, “Improving service quality in America:

lessons learned”, Academy of Management Executive.

Czepiel, J., 1990, “Managing Relationships with Customers: A Differentiation Philosophy of

Marketing,” in Service Management Effectiveness, D. E. Bowen, R. B. Chase, and T. G.

Cummings, eds. San Francisco: Jossey-Bass, pp.299-323.

Kaynak, E., Kucukemiroglu, O., 1992, “Bank and Product Selection: Hong Kong” The

International Journal of Bank Marketing, Vol 10, No. 1. – pp. 3-17.

Social Islami Bank Limited, 2014, Annual Report, pp.5-41.

Wisniewski, M. and Donnelly, M., 1996, "Measuring service quality in the public sector: the

potential for SERVQUAL", Total Quality Management, Vol. 7, No. 4, pp. 357-365.

Yang, Z. and Fang, X., 2004, "Online service quality dimensions and their relationships with

satisfaction: A content analysis of customer reviews of securities brokerage services",

International Journal of Service Industry Management, Vol. 15 Issue: 3, pp.302 – 326.

Zeithaml, V. A., Parasuraman, A., and Berry, L., 1990, Delivering quality service: Balancing

customer perceptions and expectations. New York, NY: Free Press.

Zeithaml, V., 2000, “Service quality, profitability and the economic worth of customers: What

we know and what we need to learn”, Journal of the Academy of Marketing Science, Vol. 28 No.

1, pp. 67- 85.

Zeithaml, V., Berry, L. and Parasuraman, A., 1996, “The behavioral consequences of service

quality”, Journal of Marketing, Vol. 60, April, pp. 31-46.

Web sites

www.sibl.bd.com. 2015. Institutional Banking remittance. [ONLINE] Available at:

http://www.siblbd.com/home/crpu. [Accessed 24 March 15].

www.ukessays.com. 2015. Essay. [ONLINE] Available at: http://www.ukessays.com/ essays /

marketing/the-five-dimensions-of-service-quality-measured-marketing essay. [Accessed 18

March 15].

Appendix: 1 Questionnaire

Questionnaire on

Foreign Exchange Services of

Social Islami Bank Limited Name :

Occupation :

Address :

I. Which area of foreign exchange you deal with SIBL? o Export o Import o Foreign money transfer o All of above

II. Are you a current customer of Social Islami Bank Ltd.? o Yes. o No.

III. Frequency of coming to Social Islami Bank Ltd.? o More than once in a week. o Once in a week. o Once in 15 days. o Once in a month.

Put the cross mark (×) on your desired answer

Reliability Dimension of Service Quality Judgment:

Statements Strongly Disagree

Disagree Neutral Agree Strongly Agree

The bank performs the service right the first time.

1 2 3 4 5

The bank promises to do something by a certain time, it does so.

1 2 3 4 5

If you have a problem, the bank shows an insincere interest in solving it.

1 2 3 4 5

Assurance Dimension of Service Quality Judgment:

Statements Strongly Disagree

Disagree

Neutral Agree Strongly Agree

You feel safe in your foreign transactions with the bank.

1 2 3 4 5

The behaviors of employees are confident, trustworthy & knowledgeable.

1 2 3 4 5

Tangibility Dimension of Service Quality Judgment:

Statements Strongly Disagree

Disagree Neutral Agree Strongly Agree

SIBL has traditional and outdate looking equipment.

1 2 3 4 5

Materials associated with the service are visually appealing at the bank.

1 2 3 4 5

The bank's physical features setting are visually appealing.

1 2 3 4 5

Empathy Dimension of Service Quality Judgment:

Statements Strongly Disagree

Disagree Neutral Agree Strongly Agree

The employees of SIBL understand your specific needs.

1 2 3 4 5

The bank has not operating hours convenient to all its customers.

1 2 3 4 5

The bank gives you individual attention. 1 2 3 4 5

Responsiveness Dimension of Service Quality Judgment:

Statements Strongly Disagree

Disagree Neutral Agree Strongly Agree

The bank tells you exactly when the services will be performed.

1 2 3 4 5

Employees in the bank are never too busy to respond to your request.

1 2 3 4 5

Employees in the bank are always willing to help you.

1 2 3 4 5

THANK YOU

Appendix: 2 DATA ANALYSIS

Reliability Dimension

The bank performs the service right the first time. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 01 5 3 Agree (4) 04 16 13 Neutral (3) 10 30 34 Disagree(2) 13 26 43 Strongly Disagree(1) 02 2 7 Total 30 79 100 Average 2.63

Table shows that 13% of the respondents are agreed and 3% are strongly agree that they get

quick service of foreign exchange in SIBL. 34% is neutral, where 43% disagreed and 7%

strongly disagreed with the statement.

Likert scores are calculated by multiplying each frequency by Likert scale score ranging from

5 = strongly agree to 1= strongly disagree and total score is divided by sample size that is 30 to

get the average score. The higher the score the higher the respondents are agree with the

statement. Here the average score is 2.63 which show the negative agreement of the respondents.

That means the bank does not perform the services right at first time.

0%10%20%30%40%50%

Strongly Agree

Agree Neuttral Disagree Strongly Disagree

Percentage

Percentage

When the bank promises to do something by a certain time, it does so. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 02 10 7 Agree (4) 23 92 77 Neutral (3) 02 6 6 Disagree(2) 03 6 10 Strongly Disagree(1) 00 00 00 Total 30 114 100 Average 3.8

Table shows that 77% of the respondents are agreed and 7% are strongly agree that they get

convenient transaction hour in SIBL. 6% is neutral, where 10% disagreed with the statement.

Here the average score is 3.8 which show the positive agreement of the respondents.

If you have a problem, the bank shows an insincere interest in solving it.

Likert scale (reversed coding)

Frequency Likert Scores Percentage %

Strongly Agree ( 1) 01 1 3 Agree (2) 09 18 30 Neutral (3) 05 15 17 Disagree (4) 11 44 37 Strongly Disagree (5) 04 20 13 Total 30 98 100 Average 3.27

0%

50%

100%

Strongly Agree

Agree Neuttral Disagree Strongly Disagree

Percentage

Percentage

Table shows that 30% of the respondents are agreed and 3% are strongly agree that they get

pleasant environment. 17% is neutral, where 37% disagreed and 13% strongly disagreed with the

statement.

It is a negative statement that why used revers coding. Here the average score is 3.27 which

show the positive agreement of the respondents. That means the bank shows an sincere interest

in solving the problems of customer.

Assurance dimension:

You feel safe in foreign transactions with the bank.

Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 25 125 83

Agree (4) 05 20 17

Neutral (3) 00 00 00

Disagree(2) 00 00 00

Strongly Disagree(1) 00 00 00

Total 30 145 100

Average 4.83

3%

30%

17%37%

13%

PercentageStrongly Agree Agree Neuttral Disagree Strongly Disagree

Table shows that 17% of the respondents are agreed and 83% are strongly agree that they get

pleasant environment. Here the average score is 4.83 which show the positive agreement of the

respondents.

The behaviors of employees are confident, trustworthy & knowledgeable. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 04 20 14

Agree (4) 15 60 50

Neutral (3) 07 21 23

Disagree(2) 04 08 13

Strongly Disagree(1) 00 00 00

Total 30 109 100

Average 3.6

83%

17%0.00% 0% 0.00%0%

20%40%60%80%

100%

Strongly Agree Agree Neuttral Disagree Strongly Disagree

Percentage

14%

50%

23.00%

13%

0.00%

Strongly Agree Agree Neuttral Disagree Strongly Disagree

Table shows that 50% of the respondents are agreed and 14% are strongly agree that they get

pleasant environment. 23% is neutral, where 13% disagreed with the statement.

Here the average score is 3.6 which show the positive agreement of the respondents.

Tangibility Dimension:

SIBL has traditional and outdate looking equipment. Likert scale (reversed) Frequency Likert Scores Percentage % Strongly Agree ( 1) 01 1 3

Agree (2) 04 8 13

Neutral (3) 10 30 34

Disagree (4) 13 52 43

Strongly Disagree(5) 02 10 7

Total 30 101 100

Average 3.37

Table shows that 13% of respondents are agreed and 3% are strongly agree that they get quick

service. 34% is neutral, where 43% disagreed and 7% strongly disagreed with the statement.

The average score is 2.63, which show the negative agreement with the statement. That means

SIBL has modern looking equipment.

0%20%40%60%

Strongly Agree

Agree Neuttral Disagree Strongly Disagree

Percentage

Percentage

Materials associated with the service are visually appealing at the bank. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 05 25 17

Agree (4) 16 64 53

Neutral (3) 05 15 17

Disagree(2) 03 6 10

Strongly Disagree(1) 01 1 3

Total 30 111 100

Average 3.70

The average score is 3.70, which show the positive agreement with the statement. That means

SIBL materials associated with the foreign exchange service are visually appealing.

The bank's physical features setting are visually appealing. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 09 45 30

Agree (4) 15 60 50

Neutral (3) 03 09 10

Disagree(2) 01 2 03

Strongly Disagree(1) 02 2 07

Total 30 118 100

Average 3.93

30%

50%

10% 3% 7%

PercentageStrongly Agree Agree Neuttral Disagree Strongly Disagree

The average score is 3.93, which show the positive agreement with the statement. That means SIBL’s physical features setting are visually appealing.

Empathy Dimension

The employees of SIBL understand your specific needs. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 15 75 50

Agree (4) 08 32 27

Neutral (3) 05 15 17

Disagree(2) 02 4 6

Strongly Disagree(1) 00 00 00

Total 30 126 100

Average 4.2

The average score is 4.2, which show the respondents are strongly agreed with the statement.

That means SIBL’s employees understand your specific needs.

The bank has not operating hours convenient to all its customers. Likert scale (Reveres coding)

Frequency Likert Scores Percentage %

Strongly Agree ( 1) 3 3 7

Agree (2) 4 8 47

Neutral (3) 7 21 23

Disagree (4) 14 56 13

Strongly Disagree (5) 2 10 10

Total 30 98 100

Average 3.27

The average score is 4.2, which show the respondents are strongly agreed with the statement.

That means SIBL’s has operating hours convenient to all its customers

The bank gives you individual attention. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 00 00 00

Agree (4) 12 48 40

Neutral (3) 8 24 27

Disagree(2) 9 18 30

Strongly Disagree(1) 1 1 3

Total 30 91 100

Average 3.03

Here the average score is 3.03 which show the positive agreement of the respondents.

Responsiveness Dimension

The bank tells you exactly when the services will be performed. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 01 05 3

Agree (4) 09 36 30

Neutral (3) 15 45 50

Disagree(2) 03 06 10

Strongly Disagree(1) 02 02 7

Total 30 94 100

Average 3.13

0% 40%

27%

30% 3%

PercentageStrongly Agree Agree Neuttral Disagree Strongly Disagree

The average score is 3.13, which show the respondents are strongly agreed with the statement.

That means SIBL tell you exactly when the services will be performed.

Employees in the bank are never too busy to respond to your request. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 04 20 13

Agree (4) 11 44 37

Neutral (3) 09 27 30

Disagree(2) 05 10 17

Strongly Disagree(1) 01 01 03

Total 30 102 100

Average 3.40

Here the average score is 3.40 which show the positive agreement of the respondents.

Employees in the bank are always willing to help you. Likert scale Frequency Likert Scores Percentage % Strongly Agree ( 5) 10 50 33

Agree (4) 14 56 47

Neutral (3) 06 18 20

Disagree(2) 00 00 00

Strongly Disagree(1) 00 00 00

Total 30 124 100

Average 4.13

The average score is 4.13, which show respondents are the strongly agreed with the statement.

That means employees in the bank are always willing to help you.