Embed Size (px)

Citation preview

INTE

RIM

SH

ORT

RE

PORT

For the six months ended 31 December 2015

Henderson European Smaller Companies Fund

2 Henderson European Smaller Companies Fund

Henderson European Smaller Companies Fund

Short ReportFor the six months ended 31 December 2015

Investment Fund Managers

Ollie Beckett and Rory Stocks

Other information

Please note with effect from 1 August 2015 Ollie Beckett and Rory Stocks took over management of the fund from the Henderson Pan European Equity Team.

Investment objective and policy

To aim to provide capital growth by investing primarily in European Smaller Companies, excluding the United Kingdom.

Risk and reward profile

The fund currently has 2 types of share class in issue; A accumulation and I accumulation.

Each share class has the same risk and reward profile which is as follows:

Typically Lower potential risk/reward

Typically Higher potential risk/reward

Lower Risk Higher Risk

1 2 3 4 5 6 7

The Synthetic Risk and Reward Indicator (SRRI) is calculated based on historical volatility over a rolling 5 year period, it is reviewed monthly and updated if volatility has changed materially to cause a movement in the SRRI level. The SRRI is an indicator and may not accurately reflect future volatility and market conditions.

The value of an investment in the fund can go up or down. When you sell your shares they may be worth less than you paid for them.

The risk/reward rating above is based on medium-term volatility. In the future, the fund’s actual volatility could be higher or lower and its rated risk/reward level could change.

The lowest category does not mean risk free.

The fund’s risk level reflects the following:

• As a category, smaller companies are more volatile than larger.

• The fund focuses on a single region.

• Fluctuations in exchange rates may cause the value of your investment to rise or fall.

The rating does not reflect the possible effects of unusual market conditions or large unpredictable events. Under normal market conditions the following risks may apply:

Counterparty risk The fund could lose money if a counterparty with which it transacts becomes unwilling or unable to meet its obligations to the fund.

Focus risk The fund’s value may fall where it has concentrated exposure to an issuer or type of security that is heavily affected by an adverse event.

Liquidity risk Certain securities could become hard to value or sell at a desired time and price.

Management risk Investment management techniques that have worked well in normal market conditions could prove ineffective or detrimental at other times.

The full list of the fund’s risks are contained in the “Risk Warnings” section of the fund’s prospectus.

There have been no changes to the risk rating in the period.

The SRRI conforms to the ESMA guidelines for the calculation of the SRRI.

Investment review

European equity markets started the period in a volatile fashion, with the decision by the Chinese government to let the yuan devalue (although by a small amount) increasing investors’ nervousness about global risk assets. We found the immediate panic a little surprising, given the fact that China has been recording slower growth for some

Henderson European Smaller Companies Fund 3

time. Some more reassuring data from the global economy then led to a period of relative calm before December, when the expected year-end rally failed to materialise. The market seemed disappointed by the extent of the latest measures by the European Central Bank and unsettled by the first increase in interest rates by the US Federal Reserve (Fed).

The fund saw a positive contribution from auto component supplier Plastic Omnium. The company should benefit from the Volkswagen scandal through its nitrogen oxide emission reduction system for diesel engines. We also saw good returns from real estate design software company Nemetschek, as management increased guidance and recently announced the acquisition of quality assurance provider Solibri. Positive contributors to performance also included Faiveley Transport (railway equipment), which was subject to a bid at a significant premium of 41% to the share price. We also had good returns from Finnish online retailer Verkkokauppa.com. The company is increasing its market share in the Finnish market thanks to its e-commerce focus and low prices. These attributes are supported by lower fixed costs compared with its main competitors.

Aareal Bank was among the biggest detractors from performance. The company’s shares sold off as a result of investor fears that regulators will increase the capital requirements for all European banks, limiting near-term dividends. Competition also seems to have heightened, with net interest margins potentially coming under pressure.

We continue to like the conservative approach of management and believe these fears are overdone, as margin pressures can be offset by lower loan loss provisions. Oerlikon was also weak, as Chinese orders in the manmade fibres division fell short of expectations. This issue was not helped by a poor roadshow led by the company chairman.

During the quarter, we bought a position in Thule Group. Thule is the market leader in car roof racks, which are increasing in popularity as we see strong trends towards more active lifestyles. Thule’s dominant position gives the company a competitive advantage over its smaller competitors, which struggle to keep pace in product development. We also see opportunity for the company to leverage on the strong brand and enter adjacent categories. Additionally, we bought Swedish defence company Saab, as we see the geopolitical uncertainty driving a defence investment cycle across Europe. We also initiated a position in Irish hotel company Dalata. The recovery in Ireland is taking hold and a shortage of hotel rooms is resulting in a strong trading environment. We exited our position in Braas Monier (building materials) and Nordic auto seller Bilia, following a period of strong performance from both stocks.

China remains the focus for investors following some average manufacturing numbers and huge stock market volatility, although an imminent hard landing still seems unlikely. Instead, our greater worry is that Fed chair Janet Yellen is tightening (via increased interest rates) into a slowdown in the US. If things hold together, and the global economy remains on its moderate path of expansion, we see few places offering better growth or value than European smaller companies.

4 Henderson European Smaller Companies Fund

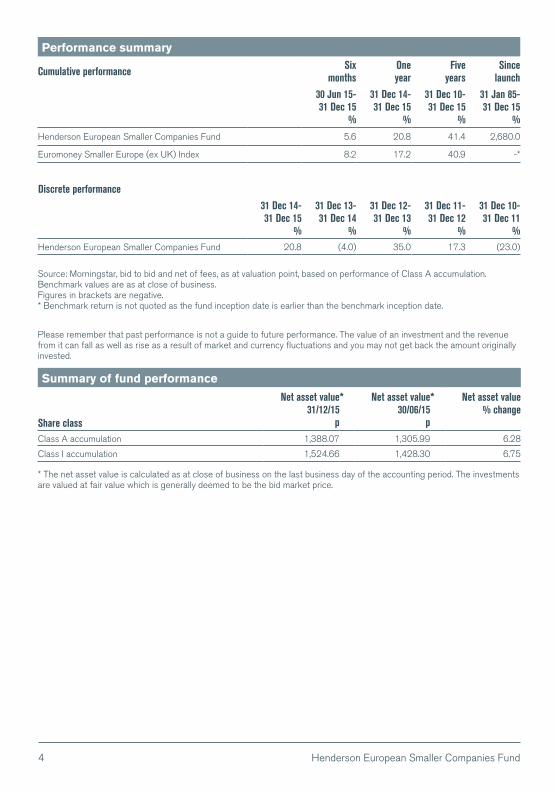

Source: Morningstar, bid to bid and net of fees, as at valuation point, based on performance of Class A accumulation.Benchmark values are as at close of business.Figures in brackets are negative.* Benchmark return is not quoted as the fund inception date is earlier than the benchmark inception date.

Please remember that past performance is not a guide to future performance. The value of an investment and the revenue from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested.

Performance summary

Cumulative performance Six months

One year

Five years

Since launch

30 Jun 15-31 Dec 15

%

31 Dec 14-31 Dec 15

%

31 Dec 10-31 Dec 15

%

31 Jan 85-31 Dec 15

%

Henderson European Smaller Companies Fund 5.6 20.8 41.4 2,680.0

Euromoney Smaller Europe (ex UK) Index 8.2 17.2 40.9 -*

Discrete performance

31 Dec 14- 31 Dec 15

%

31 Dec 13- 31 Dec 14

%

31 Dec 12- 31 Dec 13

%

31 Dec 11- 31 Dec 12

%

31 Dec 10- 31 Dec 11

%Henderson European Smaller Companies Fund 20.8 (4.0) 35.0 17.3 (23.0)

Summary of fund performance

Share class

Net asset value 31/12/15

p

*

Net asset value 30/06/15 p

*

Net asset value % change

Class A accumulation 1,388.07 1,305.99 6.28

Class I accumulation 1,524.66 1,428.30 6.75

* The net asset value is calculated as at close of business on the last business day of the accounting period. The investments are valued at fair value which is generally deemed to be the bid market price.

Henderson European Smaller Companies Fund 5

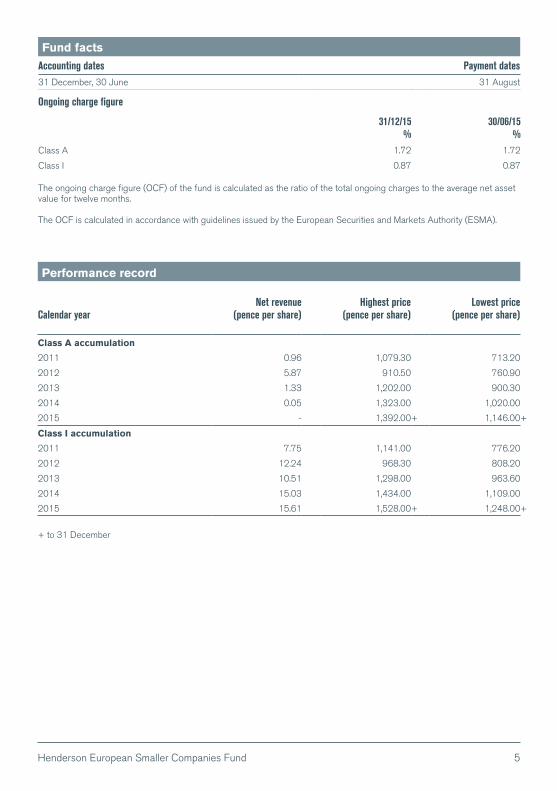

Fund facts

Accounting dates Payment dates31 December, 30 June 31 August

Ongoing charge figure

31/12/15 %

30/06/15 %

Class A 1.72 1.72

Class I 0.87 0.87

The ongoing charge figure (OCF) of the fund is calculated as the ratio of the total ongoing charges to the average net asset value for twelve months.

The OCF is calculated in accordance with guidelines issued by the European Securities and Markets Authority (ESMA).

Performance record

Calendar year

Net revenue (pence per share)

Highest price (pence per share)

Lowest price (pence per share)

Class A accumulation

2011 0.96 1,079.30 713.20

2012 5.87 910.50 760.90

2013 1.33 1,202.00 900.30

2014 0.05 1,323.00 1,020.00

2015 - 1,392.00+ 1,146.00 +

Class I accumulation

2011 7.75 1,141.00 776.20

2012 12.24 968.30 808.20

2013 10.51 1,298.00 963.60

2014 15.03 1,434.00 1,109.00

2015 15.61 1,528.00+ 1,248.00 +

+ to 31 December

6 Henderson European Smaller Companies Fund

Past performance is not a guide to future performance

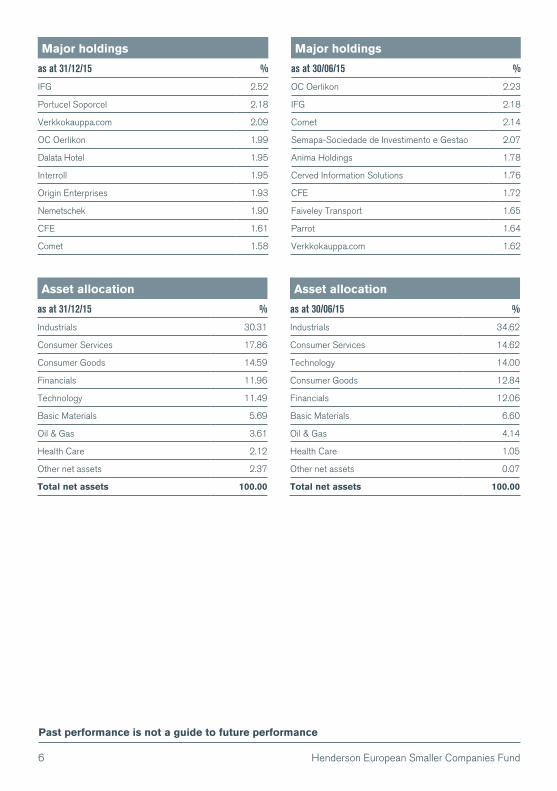

Major holdings Major holdings

as at 31/12/15 % as at 30/06/15 %

IFG 2.52 OC Oerlikon 2.23

Portucel Soporcel 2.18 IFG 2.18

Verkkokauppa.com 2.09 Comet 2.14

OC Oerlikon 1.99 Semapa-Sociedade de Investimento e Gestao 2.07

Dalata Hotel 1.95 Anima Holdings 1.78

Interroll 1.95 Cerved Information Solutions 1.76

Origin Enterprises 1.93 CFE 1.72

Nemetschek 1.90 Faiveley Transport 1.65

CFE 1.61 Parrot 1.64

Comet 1.58 Verkkokauppa.com 1.62

Asset allocation Asset allocation

as at 31/12/15 % as at 30/06/15 %

Industrials 30.31 Industrials 34.62

Consumer Services 17.86 Consumer Services 14.62

Consumer Goods 14.59 Technology 14.00

Financials 11.96 Consumer Goods 12.84

Technology 11.49 Financials 12.06

Basic Materials 5.69 Basic Materials 6.60

Oil & Gas 3.61 Oil & Gas 4.14

Health Care 2.12 Health Care 1.05

Other net assets 2.37 Other net assets 0.07

Total net assets 100.00 Total net assets 100.00

Henderson European Smaller Companies Fund 7

Issued by:Henderson Investment Funds LimitedRegistered office: 201 Bishopsgate, London EC2M 3AEMember of The Investment Association and authorised and regulated by the Financial Conduct Authority.Registered in England No 2678531

Shareholder AdministratorInternational Financial Data Services (UK) LimitedIFDS HouseSt. Nicholas LaneBasildon SS15 5FS

DepositaryNational Westminster Bank Plc135 BishopsgateLondon EC2M 3UR

AuditorPricewaterhouseCoopers LLP 141 Bothwell Street Glasgow G2 7EQ

Report and accountsThis document is a short report of the Henderson European Smaller Companies Fund for the six months ended 31 December 2015.

Copies of the annual and half yearly long form report and financial statements of this fund are available on our website www.henderson.com or contact client services on the telephone number provided.

Other informationThe information in this report is designed to enable you to make an informed judgement on the activities of the fund during the period it covers and the results of those activities at the end of the period.

Risk warningPlease remember that past performance is not a guide to future performance. The value of an investment and the revenue from it can fall as well as rise as a result of market and currency fluctuations and you may not get back the amount originally invested.

Imp

ort

an

t In

form

ati

on

Hen

ders

on G

loba

l Inv

esto

rs is

the

nam

e un

der w

hich

Hen

ders

on G

loba

l Inv

esto

rs L

imite

d (r

eg. n

o. 9

0635

5), H

ende

rson

Fun

d M

anag

emen

t Lim

ited

(reg

. no.

260

7112

), H

ende

rson

Inve

stm

ent

Fund

s Li

mite

d (r

eg. n

o. 2

6785

31),

Hen

ders

on In

vest

men

t M

anag

emen

t Li

mite

d (r

eg. n

o. 1

7953

54),

Alp

haG

en C

apita

l Lim

ited

(reg

. no.

962

757)

, Hen

ders

on E

quity

Par

tner

s Li

mite

d (r

eg.

no. 2

6066

46),

Gar

tmor

e In

vest

men

t Lim

ited

(reg

. no.

150

8030

), (e

ach

inco

rpor

ated

and

regi

ster

ed in

Eng

land

and

Wal

es w

ith re

gist

ered

off

ice

at 2

01 B

isho

psga

te, L

ondo

n E

C2M

3A

E) a

re

auth

oris

ed a

nd re

gula

ted

by th

e Fi

nanc

ial C

ondu

ct A

utho

rity

to p

rovi

de in

vest

men

t pro

duct

s an

d se

rvic

es. T

elep

hone

cal

ls m

ay b

e re

cord

ed a

nd m

onito

red.

Ref

: 34V

Unl

ess

othe

rwis

e st

ated

, all

data

is s

ourc

ed b

y H

ende

rson

Glo

bal I

nves

tors

.

H0

20

73

3/0

11

6

Ch

an

ges

of

ad

dre

ss -

reg

ula

tory

req

uir

em

en

tsFC

A re

gula

tion

requ

ires

us to

sen

d th

is re

port

mai

ling

to th

e ad

dres

s he

ld o

n fil

e on

the

acco

untin

g da

te o

f 31

Dec

embe

r 20

15

. If y

ou h

ave

conf

irmed

a c

hang

e of

ad

dres

s w

ith u

s si

nce

that

dat

e w

e w

ill e

nsur

e al

l fut

ure

corr

espo

nden

ce w

ill b

e se

nt to

you

r new

add

ress

.

Onl

ine

valu

atio

nsY

ou c

an v

alue

you

r Hen

ders

on E

urop

ean

Sm

alle

r Com

pani

es F

und

at a

ny ti

me

by lo

ggin

g on

to w

ww

.hen

ders

on.c

om. S

elec

t ‘P

erso

nal I

nves

tor’

and

then

acc

ess

‘Val

uatio

ns’ f

rom

the

Tool

s M

enu.

Sim

ply

sele

ct th

e fu

nd y

ou h

old

and

ente

r the

ap

prop

riate

num

ber o

f sha

res.

Any

que

stio

ns?

Furt

her i

nfor

mat

ion

abou

t the

act

iviti

es a

nd p

erfo

rman

ce o

f the

fund

for t

his

and

prev

ious

per

iods

can

be

obta

ined

from

the

Inve

stm

ent M

anag

er. I

f you

hav

e an

y qu

estio

ns p

leas

e ca

ll ou

r Clie

nt S

ervi

ces

Team

on

08

00

83

2 8

32

or e

mai

l su

ppor

t@he

nder

son.

com

.

Co

nta

ct u

sC

lien

t S

erv

ices

0800

832

832

H

ead

Off

ice a

dd

ress

:w

ww

.hen

ders

on

.co

m

201

Bis

ho

psg

ate

, Lo

nd

on

EC

2M 3

AE