Embed Size (px)

DESCRIPTION

a prsentation on interest swaps

Citation preview

Interest rate swaps

Swap

• Derivative in which two counterparties exchange cash flows of one party's financial instrument for those of the other party's financial instrument.

• For example, in a swap involving two bonds, cash flows can be the periodic interest (coupon) payments associated with such bonds.

Swap

• Two counterparties agree to exchange one stream of cash flows against another stream.

• These streams are called the legs of the swap.• The swap agreement defines the dates when the cash

flows are to be paid and the way they are accrued and calculated.

• Usually at the time when the contract is initiated, at least one of these series of cash flows is determined by a random or uncertain variable such as a floating interest rate, foreign exchange rate, equity price, or commodity price.

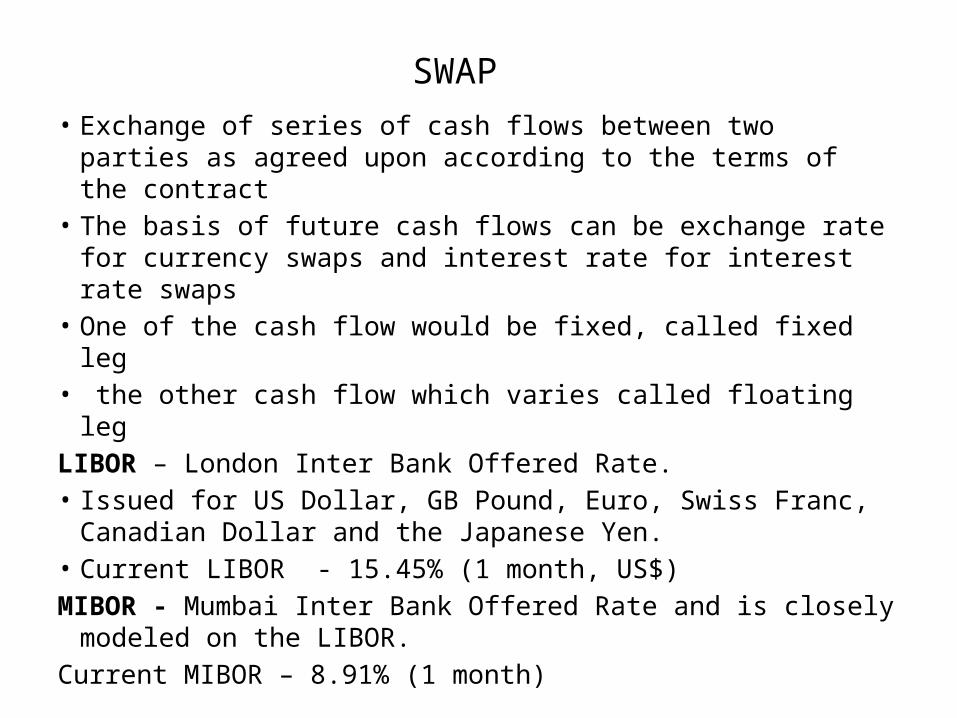

SWAP• Exchange of series of cash flows between two parties as

agreed upon according to the terms of the contract• The basis of future cash flows can be exchange rate for

currency swaps and interest rate for interest rate swaps• One of the cash flow would be fixed, called fixed leg• the other cash flow which varies called floating legLIBOR – London Inter Bank Offered Rate. • Issued for US Dollar, GB Pound, Euro, Swiss Franc,

Canadian Dollar and the Japanese Yen.• Current LIBOR - 15.45% (1 month, US$)MIBOR - Mumbai Inter Bank Offered Rate and is closely

modeled on the LIBOR. Current MIBOR – 8.91% (1 month)

SWAP - Example

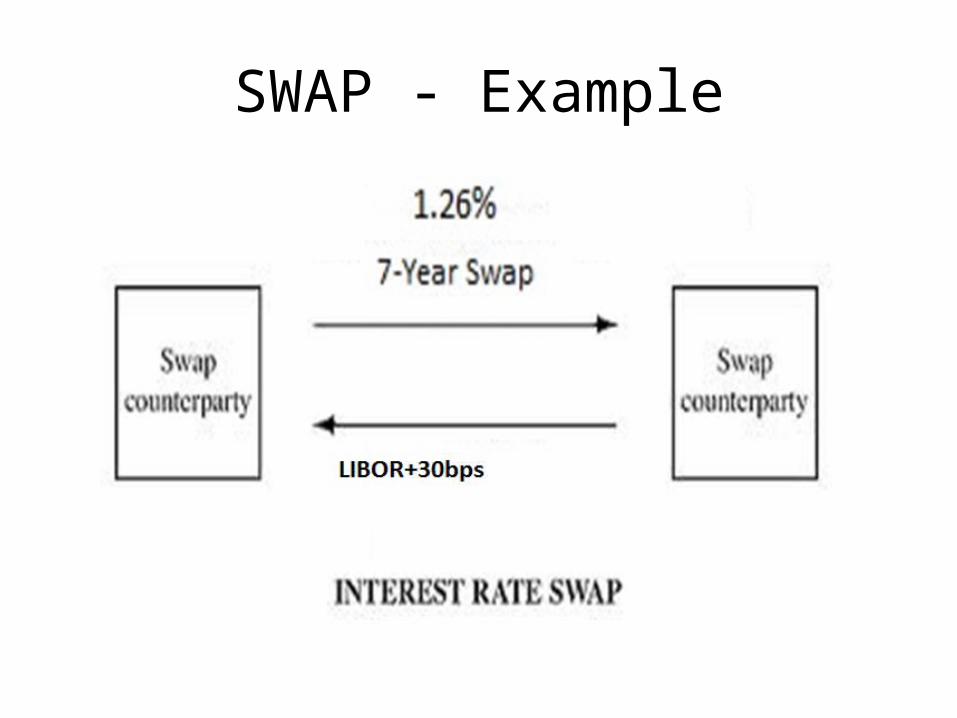

• A company enter into a SWAP contract to pay a fixed rate of 1.26% for 7 years and in return they would receive interest payments based on the 1-month LIBOR rate.

• The borrower’s interest payments would be fixed while the money they received from the swap would be variable based on the 1-month LIBOR rate.

• LIBOR - the average interest rate that they would be charged if borrowing from other banks, or estimated by leading banks in London.

• It is the primary benchmark for short-term interest rates around the world.

SWAP - Example

SWAP - Types

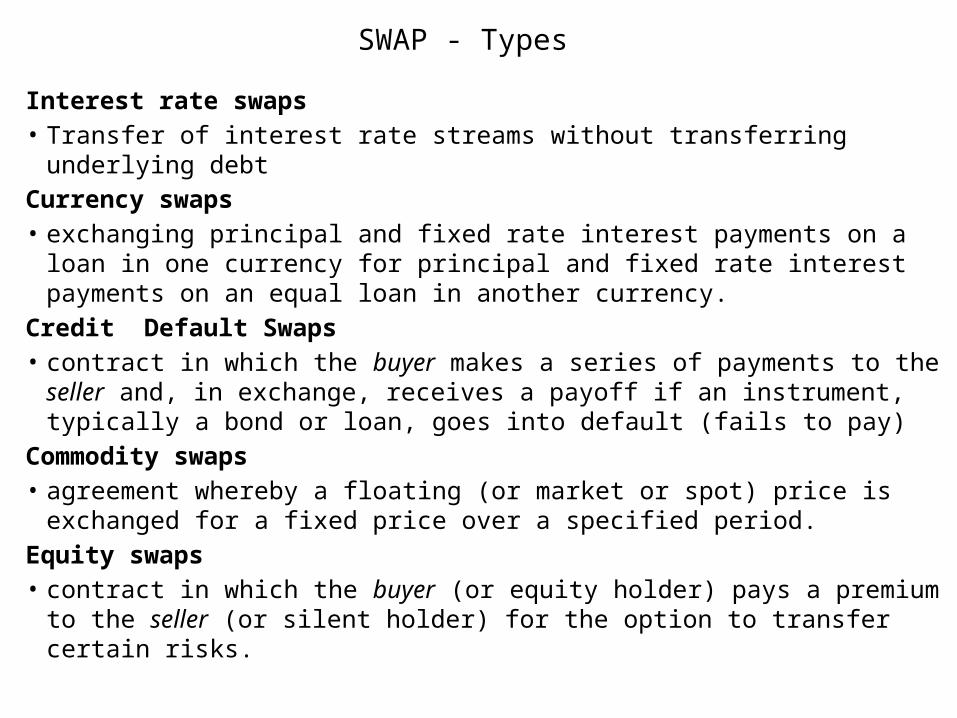

Interest rate swaps• Transfer of interest rate streams without transferring underlying debtCurrency swaps • exchanging principal and fixed rate interest payments on a loan in one

currency for principal and fixed rate interest payments on an equal loan in another currency.

Credit Default Swaps• contract in which the buyer makes a series of payments to the seller and, in

exchange, receives a payoff if an instrument, typically a bond or loan, goes into default (fails to pay)

Commodity swaps• agreement whereby a floating (or market or spot) price is exchanged for a

fixed price over a specified period.Equity swaps• contract in which the buyer (or equity holder) pays a premium to the seller

(or silent holder) for the option to transfer certain risks.

INTEREST RATE SWAPS

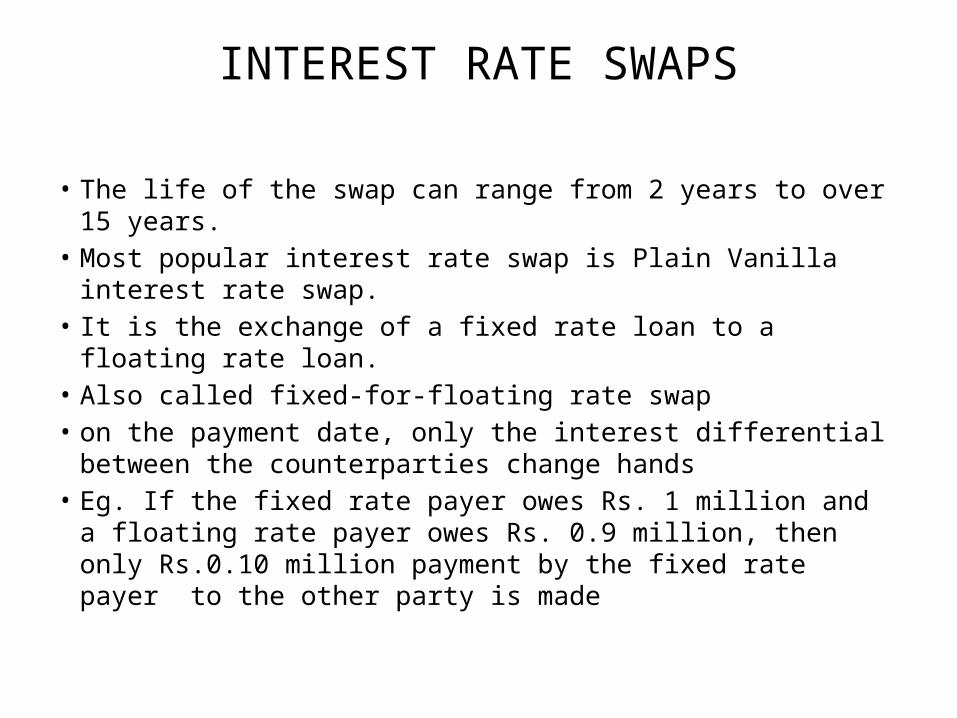

• The life of the swap can range from 2 years to over 15 years.

• Most popular interest rate swap is Plain Vanilla interest rate swap.

• It is the exchange of a fixed rate loan to a floating rate loan. • Also called fixed-for-floating rate swap• on the payment date, only the interest differential between

the counterparties change hands• Eg. If the fixed rate payer owes Rs. 1 million and a floating

rate payer owes Rs. 0.9 million, then only Rs.0.10 million payment by the fixed rate payer to the other party is made

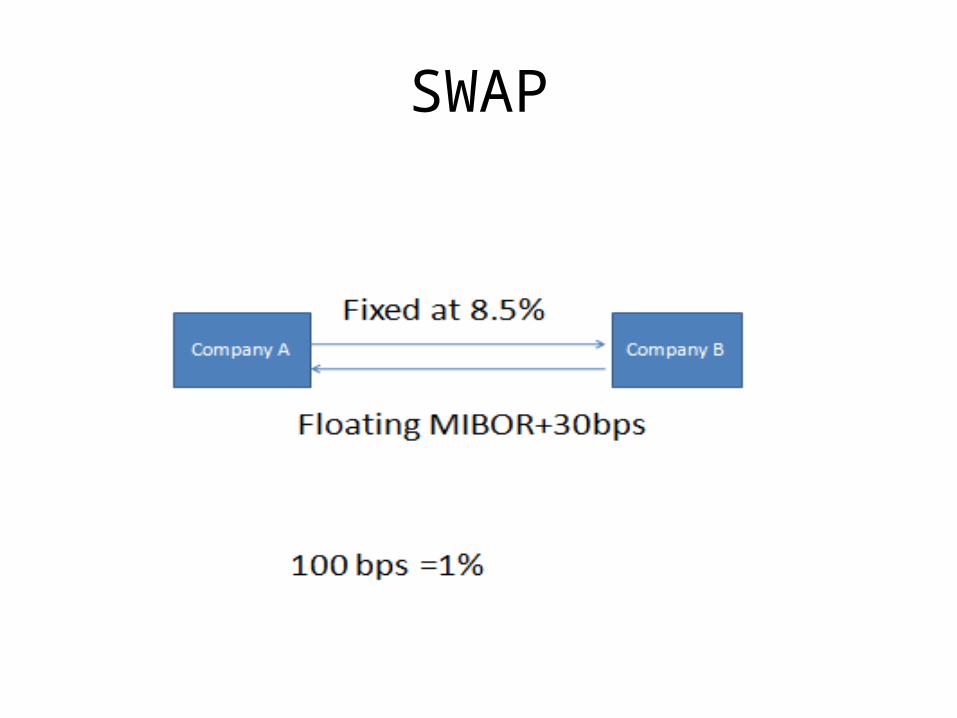

Plain Vanilla interest rate swap example

• Company B makes periodic interest payments to Company A based on a variable interest rate of MIBOR +30 basis points. Company A in return makes periodic interest payments based on a fixed rate of 8.5%.

• Fixed to floating swap

SWAP

Motives for SWAPs

• Offsetting needs among counterparties• Comparative advantage

Need for swap intermediary

• Difficulties in finding a matching counterparty can be reduced

• Assume counter party risk• Promote market development by matching of

needs, warehousing etc.

Warehousing• Banks play the role of market makers in swap• Example: one party looks for interest rate swap for Rs.

100 crore on semi-annual basis for 3 years, while the counter party want swap for Rs.80 crore on quarterly basis for 2.5 years only

• Bank takes the exposure of Rs.20 crore in expectation of finding another party

• Bank takes the risk of interest rate fluctuations till a matching counter party is found

• The risk is usually covered through interest rate futures

Applications of SWAPs

• Transforming the floating rate liability to fixed rate liability and vice versa

• transform floating rate asset to fixed rate asset and vice versa

• Hedge against fluctuating interest rates• Reduce cost of funds

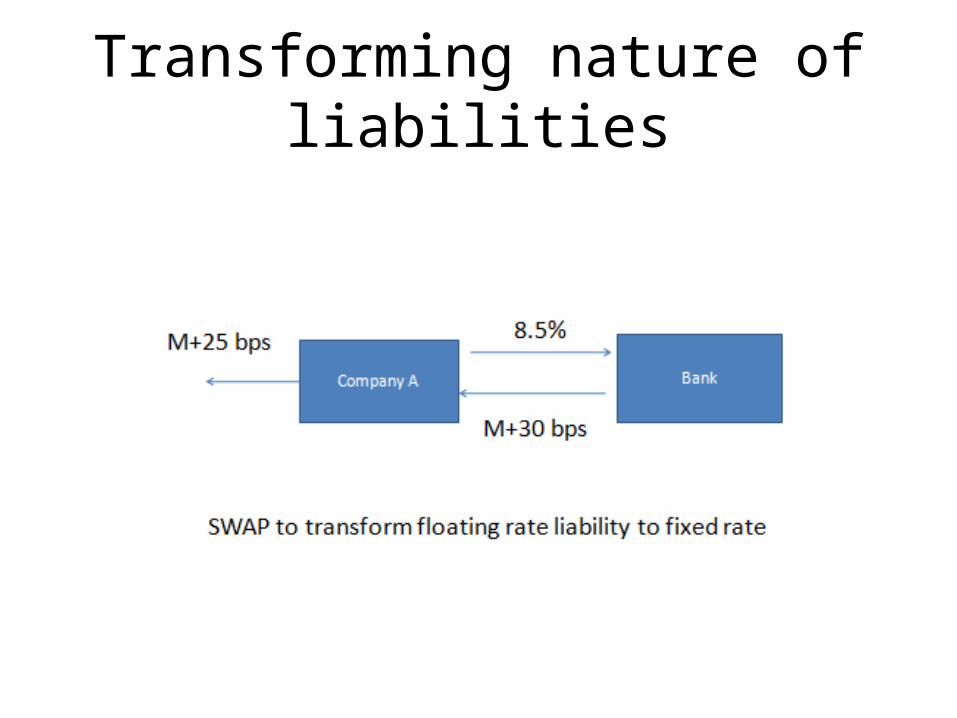

Transforming nature of liabilities

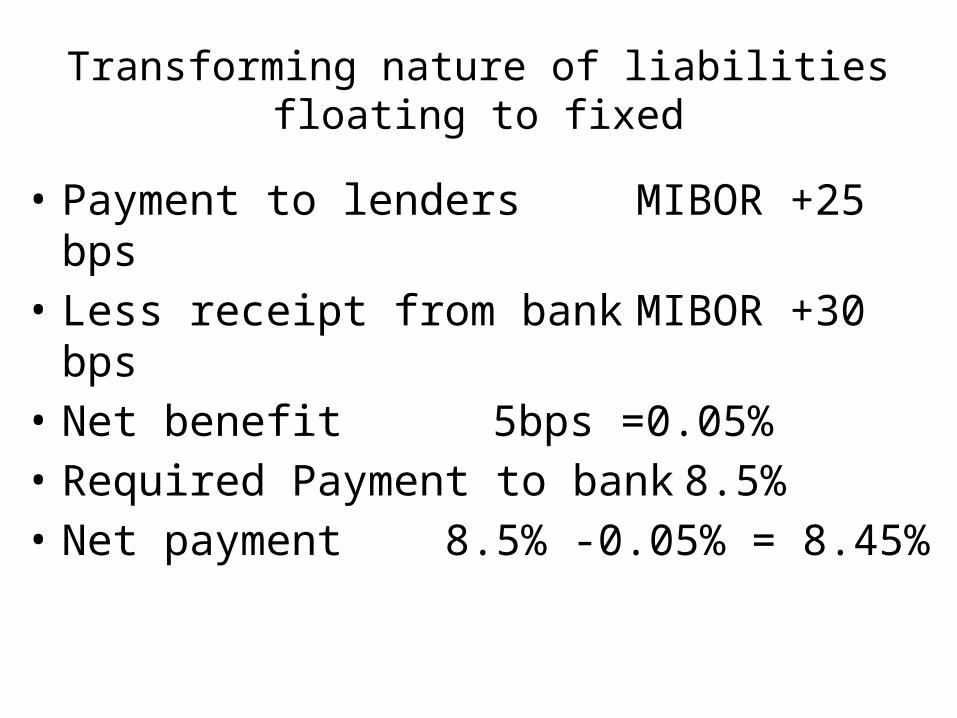

Transforming nature of liabilitiesfloating to fixed

• Payment to lenders MIBOR +25 bps• Less receipt from bank MIBOR +30 bps • Net benefit 5bps =0.05%• Required Payment to bank 8.5%• Net payment 8.5% -0.05% = 8.45%

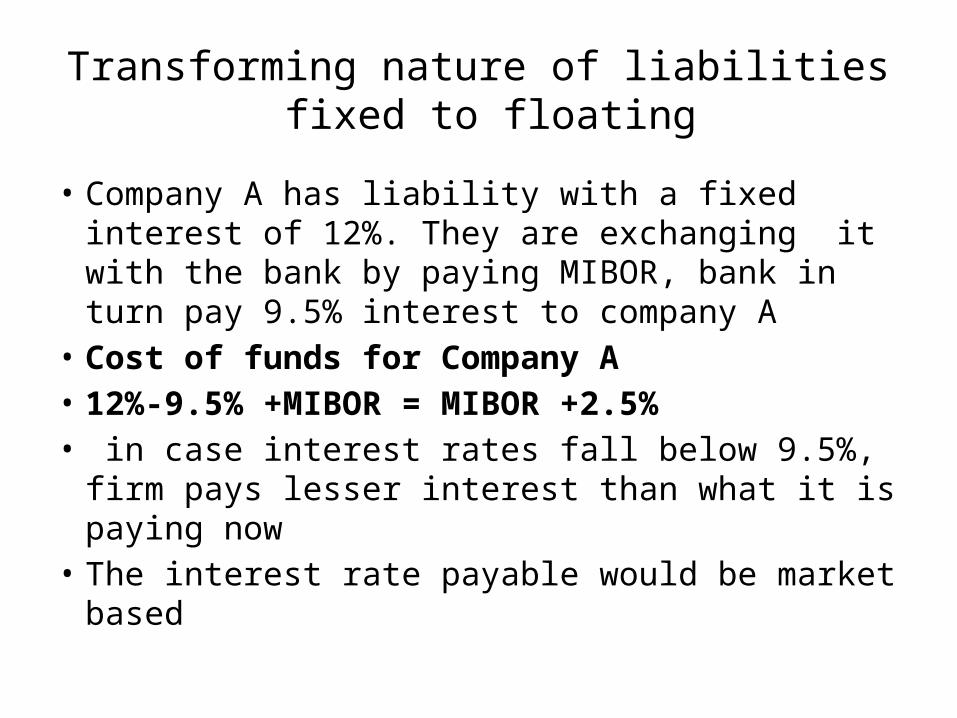

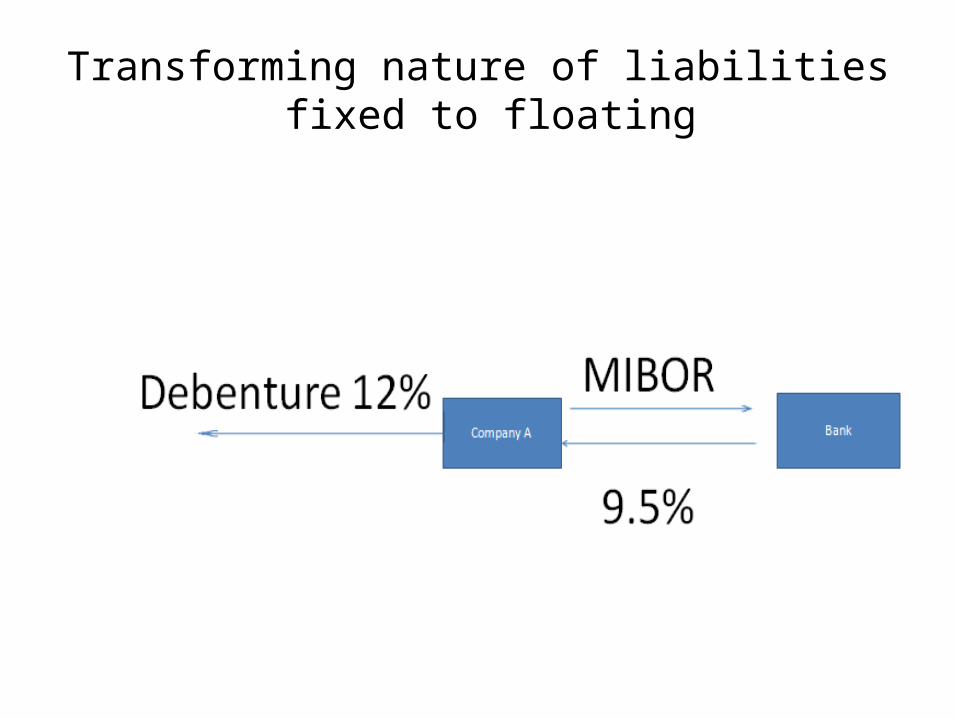

Transforming nature of liabilities fixed to floating

• Company A has liability with a fixed interest of 12%. They are exchanging it with the bank by paying MIBOR, bank in turn pay 9.5% interest to company A

• Cost of funds for Company A• 12%-9.5% +MIBOR = MIBOR +2.5%• in case interest rates fall below 9.5%, firm pays

lesser interest than what it is paying now• The interest rate payable would be market based

Transforming nature of liabilities fixed to floating

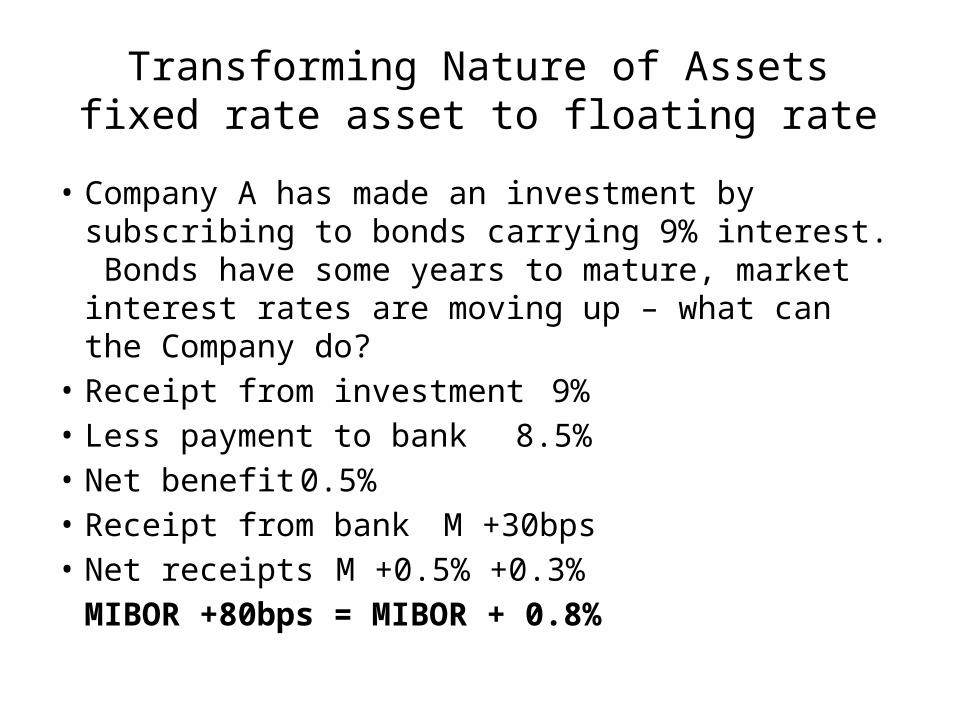

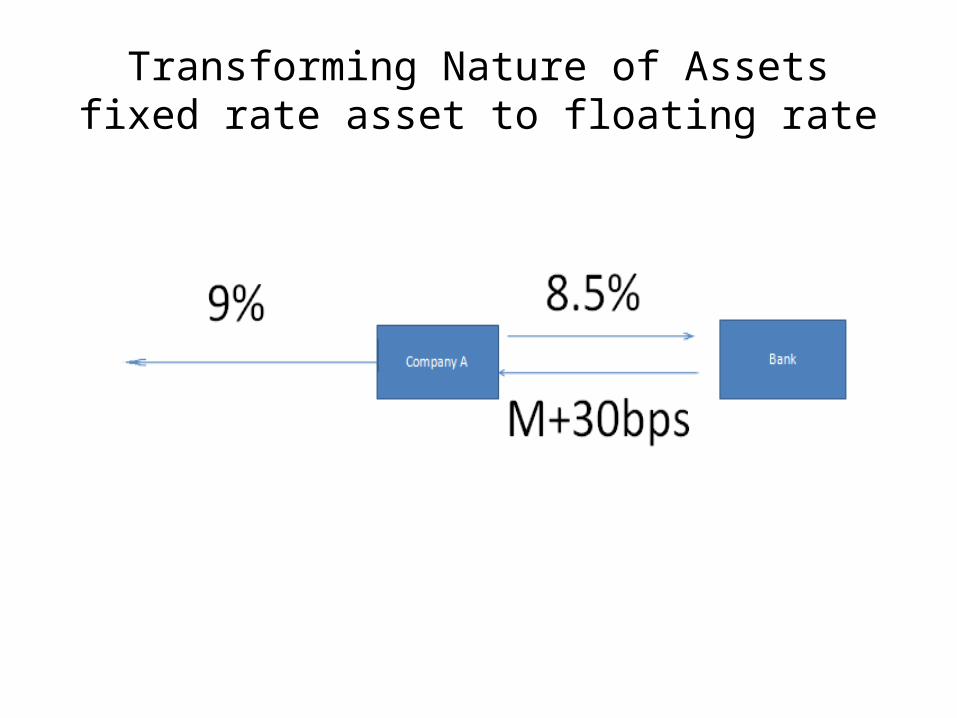

Transforming Nature of Assetsfixed rate asset to floating rate

• Company A has made an investment by subscribing to bonds carrying 9% interest. Bonds have some years to mature, market interest rates are moving up – what can the Company do?

• Receipt from investment 9%• Less payment to bank 8.5%• Net benefit 0.5%• Receipt from bank M +30bps• Net receipts M +0.5% +0.3%

MIBOR +80bps = MIBOR + 0.8%

Transforming Nature of Assetsfixed rate asset to floating rate

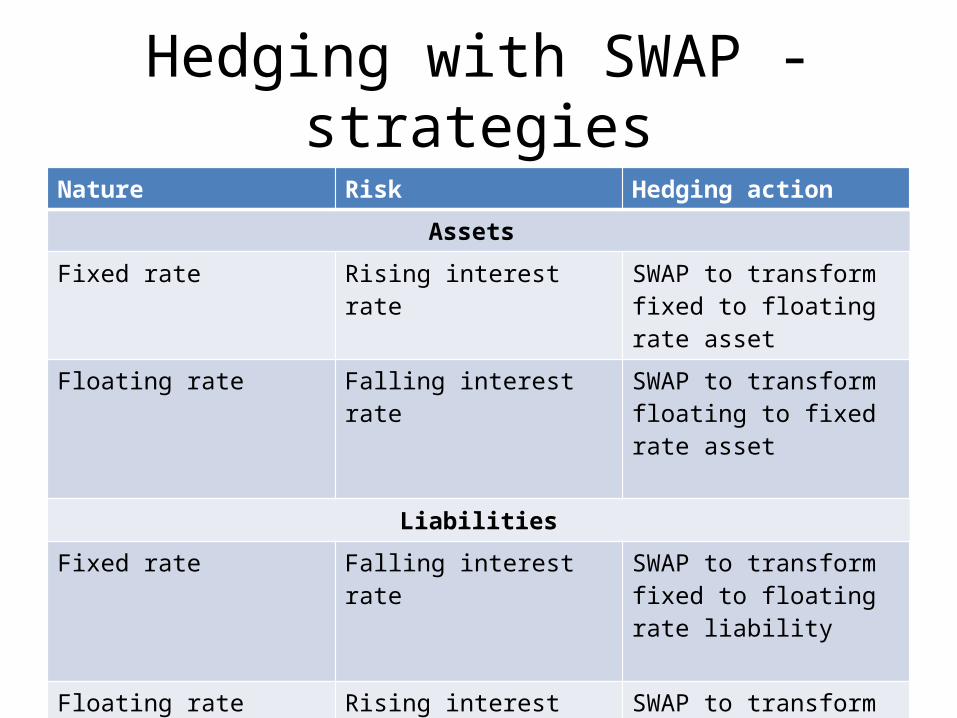

Hedging with SWAP - strategiesNature Risk Hedging action

Assets

Fixed rate Rising interest rate SWAP to transform fixed to floating rate asset

Floating rate Falling interest rate SWAP to transform floating to fixed rate asset

Liabilities

Fixed rate Falling interest rate SWAP to transform fixed to floating rate liability

Floating rate Rising interest rate SWAP to transform floating to fixed rate liability

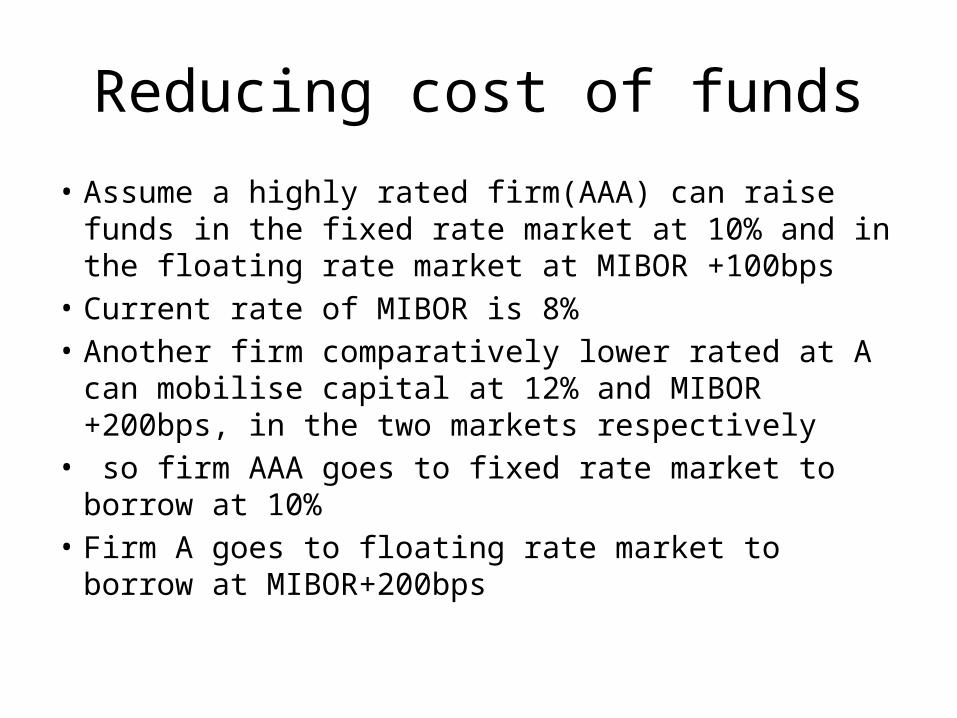

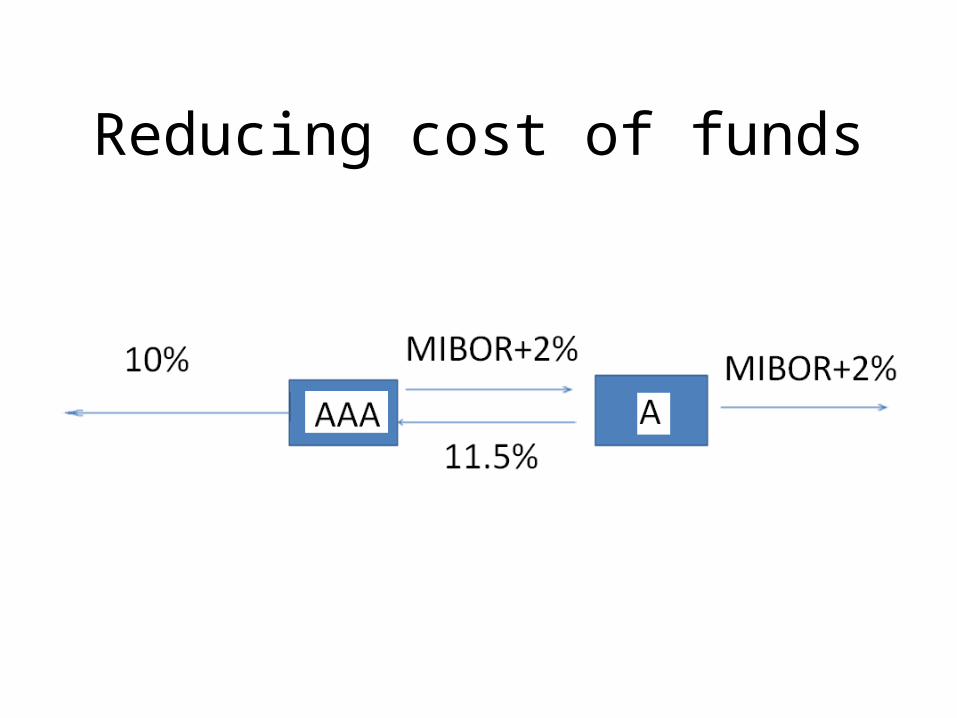

Reducing cost of funds

• Assume a highly rated firm(AAA) can raise funds in the fixed rate market at 10% and in the floating rate market at MIBOR +100bps

• Current rate of MIBOR is 8%• Another firm comparatively lower rated at A can

mobilise capital at 12% and MIBOR +200bps, in the two markets respectively

• so firm AAA goes to fixed rate market to borrow at 10%• Firm A goes to floating rate market to borrow at

MIBOR+200bps

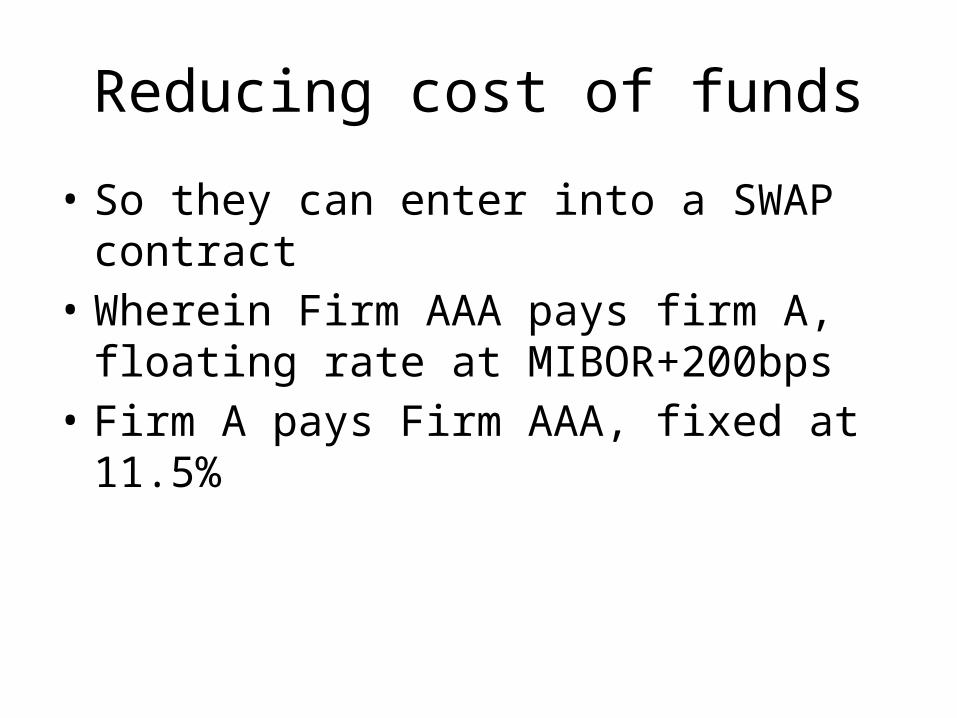

Reducing cost of funds

• So they can enter into a SWAP contract• Wherein Firm AAA pays firm A, floating rate at

MIBOR+200bps• Firm A pays Firm AAA, fixed at 11.5%

Reducing cost of funds

Types of interest rate Swaps

• Fixed –to-floating• Floating-to-fixed• Basis Swap – both legs on floating rate basis

when parties are tied to one assets or liabilities based on one reference rate and want to convert the same to another reference rate

• Eg. A firm having liabilities based on T-bills rate wants to convert it to MIBOR based rate, then it can enter into a basis swap

![John Hull �L�T[Interest rate, Swap]](https://img.pdfslide.us/doc/110x75/55362e014a7959ba1e8b48c1/john-hull-ltinterest-rate-swap.jpg)