Embed Size (px)

Citation preview

Interest Rates and Business Cycles Interest Rates and Business Cycles

Fluctuations: a Focus on Higher MomentsFluctuations: a Focus on Higher Moments

By Andrea Beccarini, By Andrea Beccarini,

University of L’Aquila, Italy.University of L’Aquila, Italy.

Two Stylised Facts:Two Stylised Facts:

- Non Linearity and Regimes in the Interest Rates process

- Non Linearity and Regimes in the Business Cycles Variables

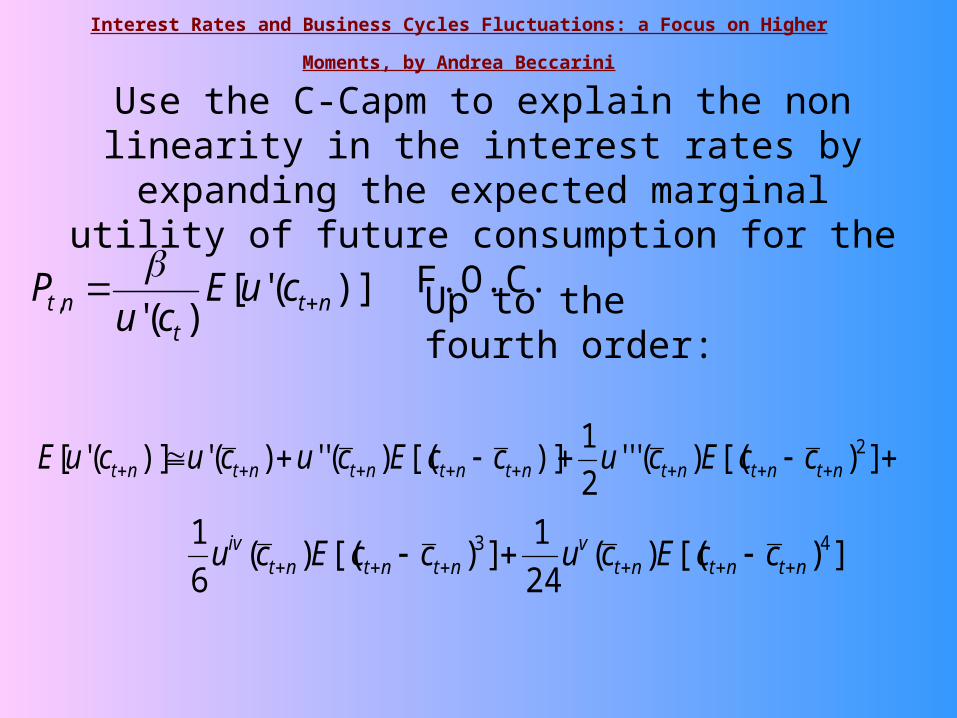

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

Use the C-Capm to explain the non linearity in the interest rates by expanding the expected marginal utility

of future consumption for the F.O.C.

])[()('''2

1)][()('')(')]('[ 2

ntntntntntntntnt ccEcuccEcucucuE

])[()(24

1])[()(

6

1 43ntntnt

vntntnt

iv ccEcuccEcu

)];('[)(', nt

tnt cuE

cuP

Up to the fourth order:

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

This is consistent with:

- Rationality assumption of the C-Capm:

the representative agent is an optimiser; all information must be exploited for the agent to be rational.

- Non linearity of the Business Cycles variables:

the alternation of phases of recessions and expansions make non-normal the

distribution of the total output.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

The theoretical moment links interest rates with moments up to the fourth of the consumption

(Business Cycles variable)

Hence, non linearity in the interest rates may depend on the higher moments of Business Cycles i.e.

asymmetry and kurtosis.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

Furthermore,

By testing the above model one may also verify:

- Rationality of financial markets, implicit in the maximization problem and in the use of all available information.

- Market risk aversion, represented by higher order utility function.

- Precautionary Saving Hypothesis, represented by the significance of the second moment.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

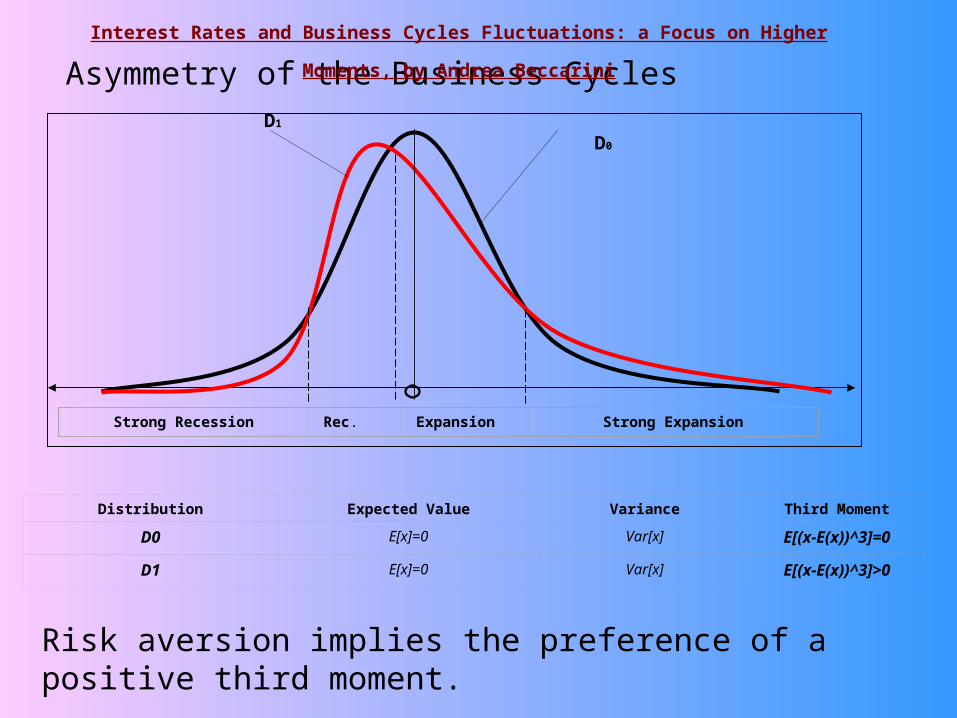

Asymmetry of the Business Cycles D1 D0

Strong Recession

Rec. Expansion

Strong Expansion

Distribution Expected Value Variance Third Moment

D0 E[x]=0 Var[x] E[(x-E(x))^3]=0

D1 E[x]=0 Var[x] E[(x-E(x))^3]>0

Risk aversion implies the preference of a positive third moment.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

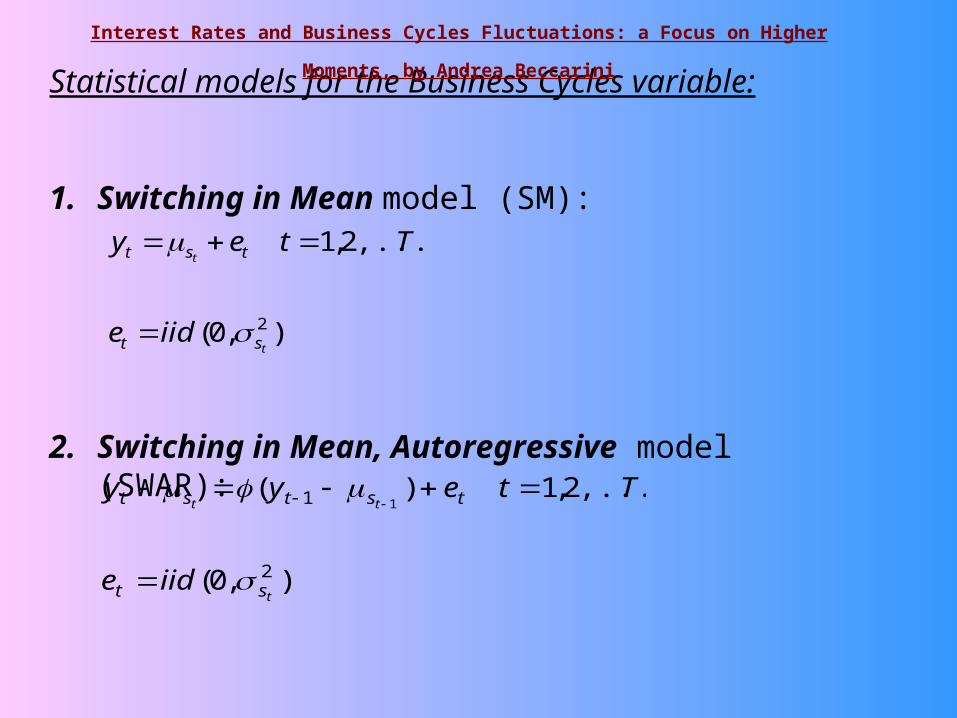

Statistical models for the Business Cycles variable:

1. Switching in Mean model (SM):

2. Switching in Mean, Autoregressive model (SWAR):

),0(

,...,2,1

2

t

t

st

tst

iide

Ttey

),0(

,...,2,1)(

2

1 1

t

tt

st

tstst

iide

Tteyy

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

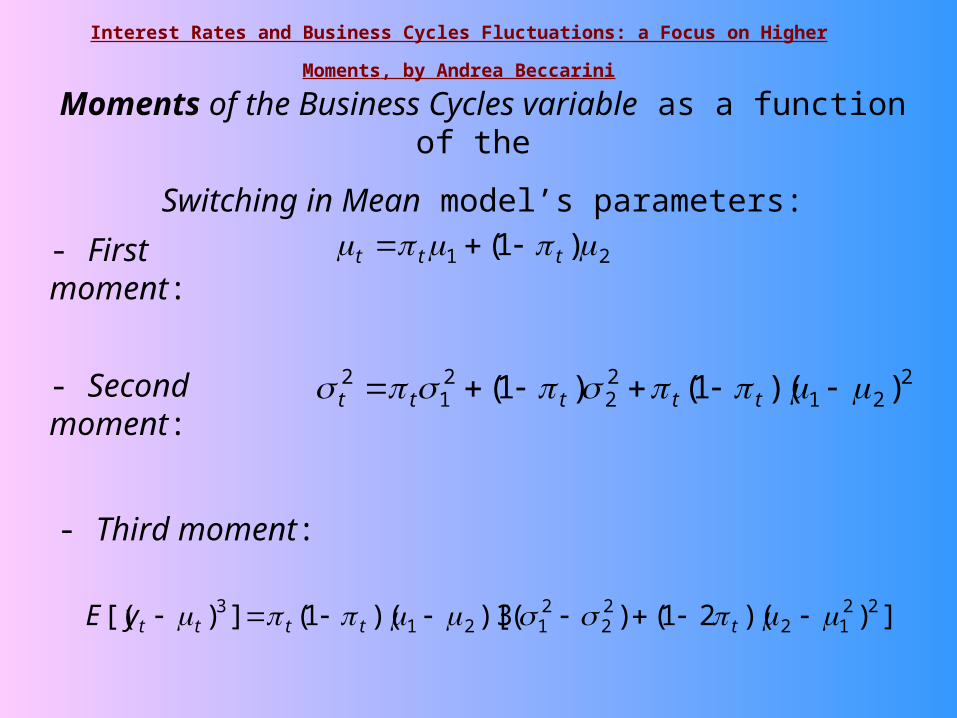

Moments of the Business Cycles variable as a function of the

Switching in Mean model’s parameters:

21 )1( ttt

221

22

21

2 ))(1()1( ttttt

]))(21()(3)[)(1(])[( 2212

22

2121

3 tttttyE

- First moment:

- Second moment:

- Third moment:

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

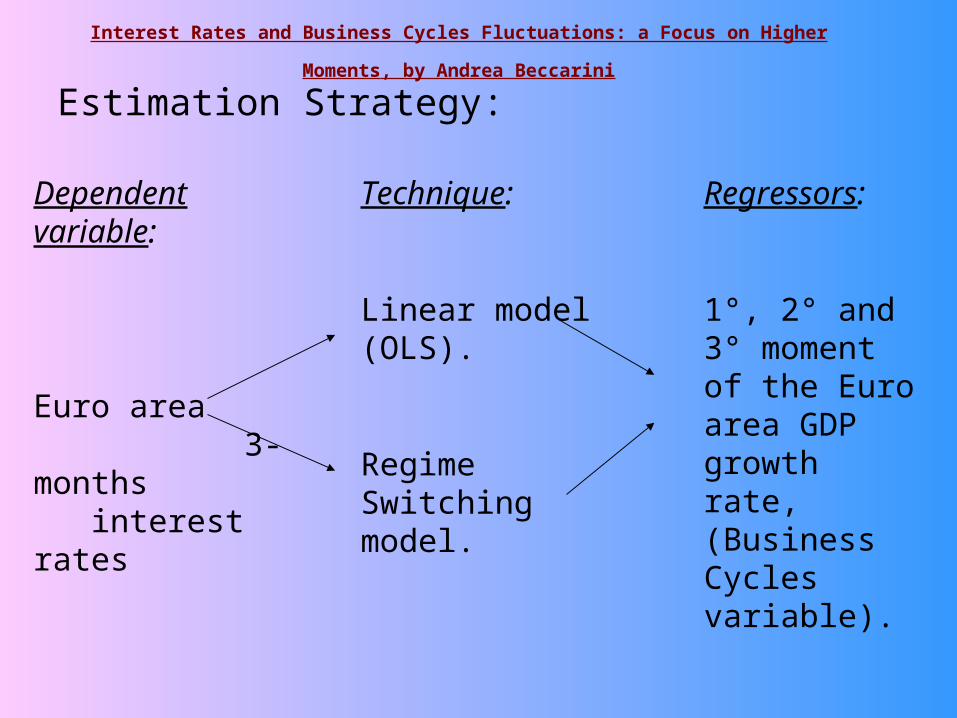

Estimation Strategy:

Dependent variable:

Euro area 3-months interest rates

Technique:

Linear model (OLS).

Regime Switching model.

Regressors:

1°, 2° and 3° moment of the Euro area GDP growth rate, (Business Cycles variable).

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

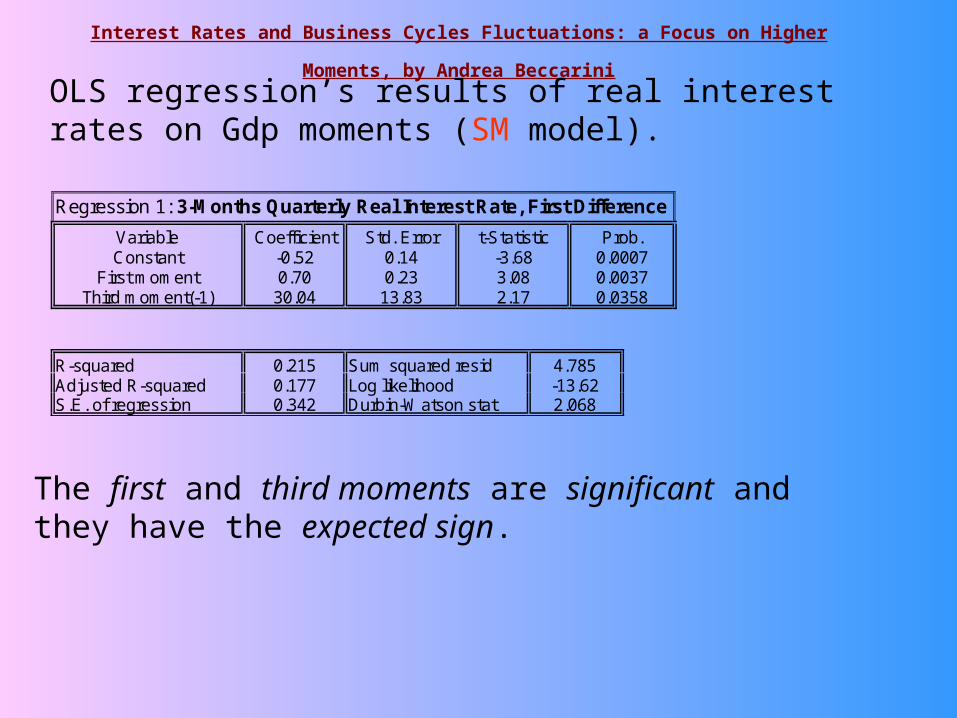

Regression 1: 3-Months Quarterly Real Interest Rate, First Difference

Variable Coefficient Std. Error t-Statistic Prob. Constant -0.52 0.14 -3.68 0.0007

First moment 0.70 0.23 3.08 0.0037 Third moment(-1) 30.04 13.83 2.17 0.0358

R-squared 0.215 Sum squared resid 4.785 Adjusted R-squared 0.177 Log likelihood -13.62 S.E. of regression 0.342 Durbin-Watson stat 2.068

OLS regression’s results of real interest rates on Gdp moments (SM model).

The first and third moments are significant and they have the expected sign.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

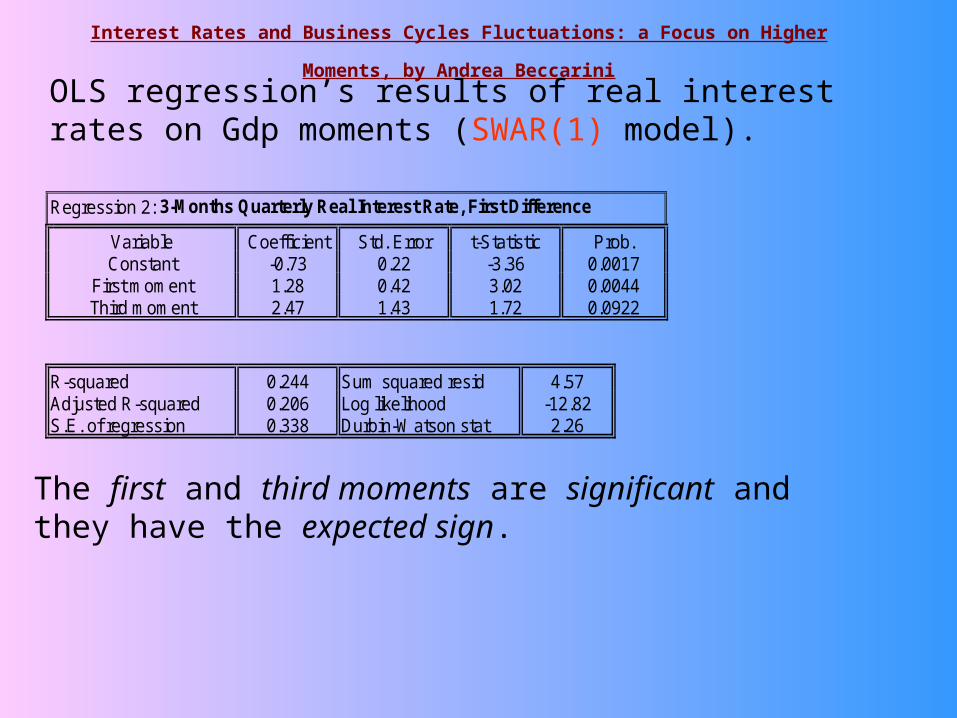

OLS regression’s results of real interest rates on Gdp moments (SWAR(1) model).

Regression 2: 3-Months Quarterly Real Interest Rate, First Difference

Variable Coefficient Std. Error t-Statistic Prob. Constant -0.73 0.22 -3.36 0.0017

First moment 1.28 0.42 3.02 0.0044 Third moment 2.47 1.43 1.72 0.0922

R-squared 0.244 Sum squared resid 4.57 Adjusted R-squared 0.206 Log likelihood -12.82 S.E. of regression 0.338 Durbin-Watson stat 2.26

The first and third moments are significant and they have the expected sign.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

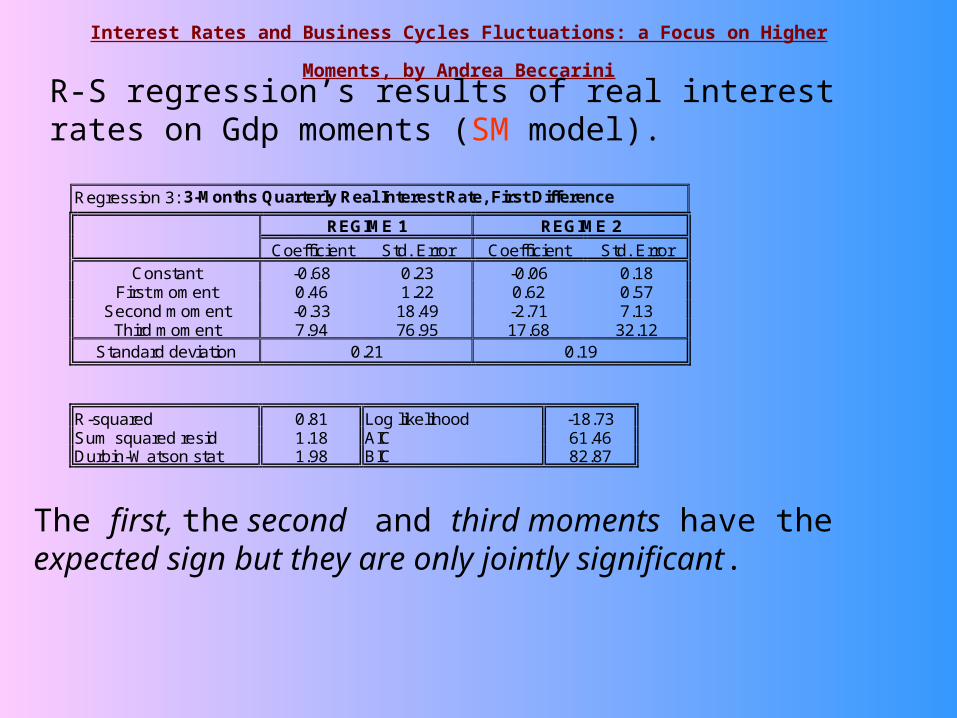

R-S regression’s results of real interest rates on Gdp moments (SM model).

Regression 3: 3-Months Quarterly Real Interest Rate, First Difference

REGIME 1 REGIME 2

Coefficient Std. Error Coefficient Std. Error

Constant -0.68 0.23 -0.06 0.18 First moment 0.46 1.22 0.62 0.57

Second moment -0.33 18.49 -2.71 7.13 Third moment 7.94 76.95 17.68 32.12

Standard deviation 0.21 0.19

R-squared 0.81 Log likelihood -18.73 Sum squared resid 1.18 AIC 61.46 Durbin-Watson stat 1.98 BIC 82.87

The first, the second and third moments have the expected sign but they are only jointly significant.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

R-S regression’s results of real interest rates on Gdp moments (SWAR(1) model).

Regression 4: 3-Months Quarterly Real Interest Rate, First Difference

REGIME 1 REGIME 2

Coefficient Std. Error Coefficient Std. Error

Constant -0.65 0.34 -0.35 0.31 First moment 0.58 1.56 1.07 0.68

Second moment -0.06 4.08 -0.42 1.73 Third moment 0.57 3.66 2.07 1.93

Standard deviation 0.27 0.20

R-squared 0.77 Log likelihood -25.57 Sum squared resid. 1.39 AIC 55.15 Durbin-Watson stat 2.27 BIC 76.56

The first, the second and third moments have the expected sign but they are only jointly significant.

Main Results:

- The positive relationship between the first moment of Gdp and the first difference of interest rates, consistently with basic C-Capm.

- The negative relationship between the second moment of Gdp and the first difference of interest rates, hence Precautionary Saving motivations.

- The positive relationship between the third moment of Gdp and the first difference of interest rates, consistently with the presence of relevant information in higher moments.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

Other Results:

- The importance of fitted moments of the Gdp rather than the row time series.

- The evidence of the rational expectation formation rather than the adaptive formation.

- The Precautionary Saving hypothesis rather than the Permanent Income Hypothesis.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

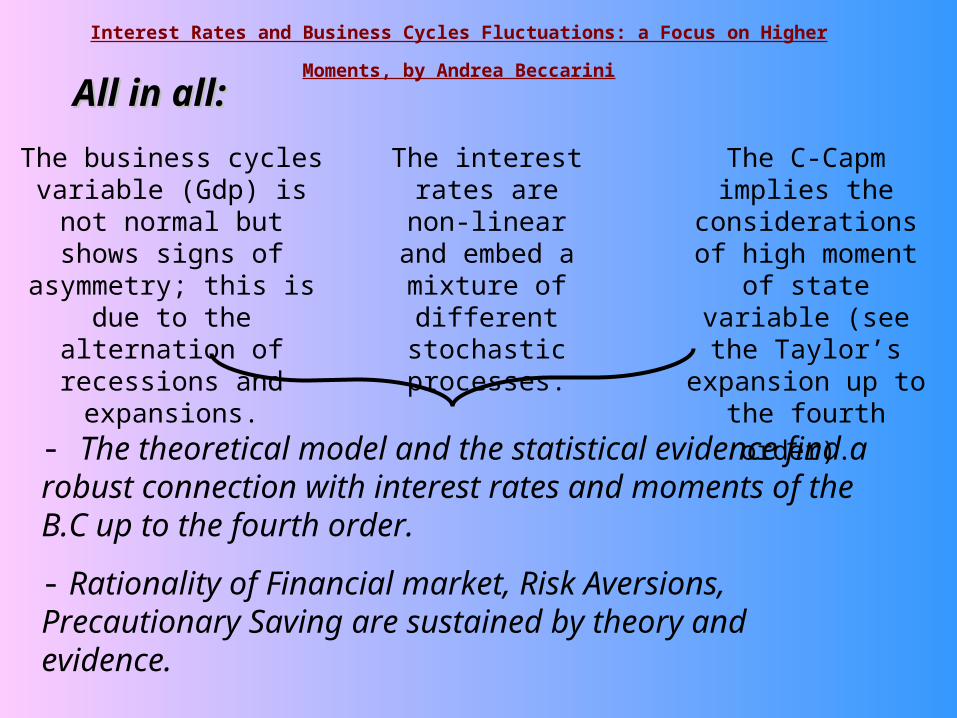

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

The business cycles variable (Gdp) is not normal but

shows signs of asymmetry; this is due to the alternation

of recessions and expansions.

The C-Capm implies the considerations of high moment of state

variable (see the Taylor’s expansion up

to the fourth order).

All in all:All in all:

- The theoretical model and the statistical evidence find a robust connection with interest rates and moments of the B.C up to the fourth order.

- Rationality of Financial market, Risk Aversions, Precautionary Saving are sustained by theory and evidence.

The interest rates are non-linear and embed a mixture

of different stochastic processes.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

Annex 1: Estimated parameters of the SM (switching in mean) model:

)11(.71.0)13(.8.0)015(.03.ˆ)02(.06.ˆ

)05(.23.ˆ)06(.76.ˆ

221122

21

21

pp

R e s i d u a l s u m o f S q u a r e s : 1 . 4 1 7 D W - s t a t i s t i c : 1 . 4 9

L o g - L i k e l i h o o d v a l u e : - 2 0 . 9 3 R s q v a l u e : 0 . 7 2 3

The average rate of growth of the Gdp during expansions is 0.76; during recessions is 0.23.

The probability of remaining in the expansion phase is 0.81. The probability of remaining in the recession phase is 0.71.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

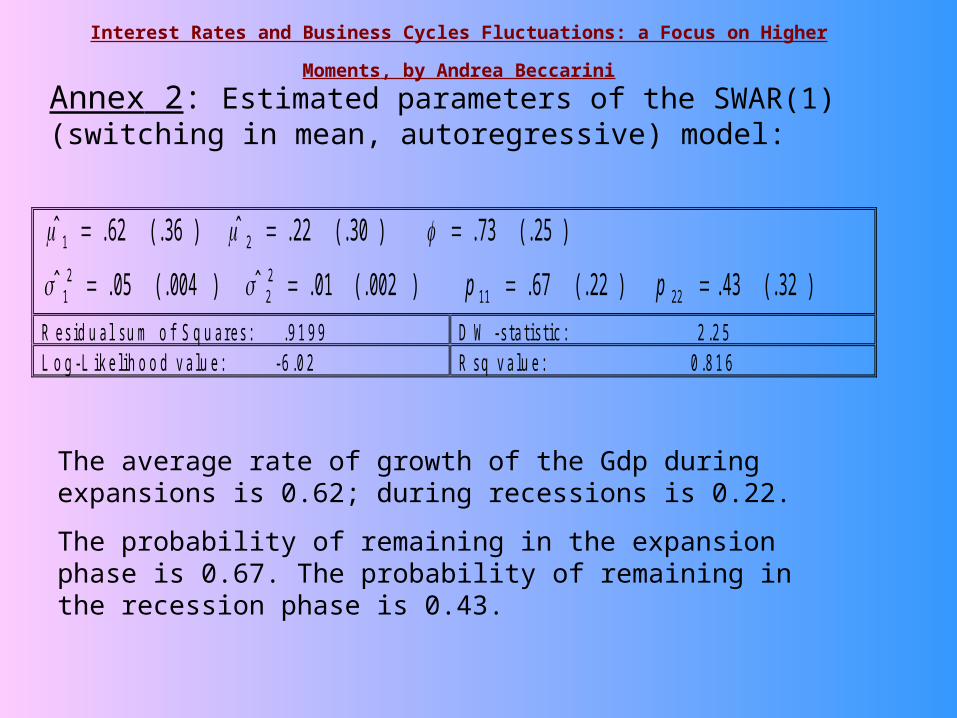

Annex 2: Estimated parameters of the SWAR(1) (switching in mean, autoregressive) model:

)32(.43.)22(.67.)002(.01.ˆ)004(.05.ˆ

)25(.73.)30(.22.ˆ)36(.62.ˆ

221122

21

21

pp

R e s i d u a l s u m o f S q u a r e s : . 9 1 9 9 D W - s t a t i s t i c : 2 . 2 5 L o g - L i k e l i h o o d v a l u e : - 6 . 0 2 R s q v a l u e : 0 . 8 1 6

The average rate of growth of the Gdp during expansions is 0.62; during recessions is 0.22.

The probability of remaining in the expansion phase is 0.67. The probability of remaining in the recession phase is 0.43.

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

The end of the presentation titled:

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments

By Andrea Beccarini,

University of L’Aquila, Italy.

E-mail address: [email protected]

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini

Interest Rates and Business Cycles Fluctuations: a Focus on Higher Moments, by Andrea Beccarini