Embed Size (px)

Citation preview

Interest Rate Swaps

Jordan Heller

Chris Schubothe

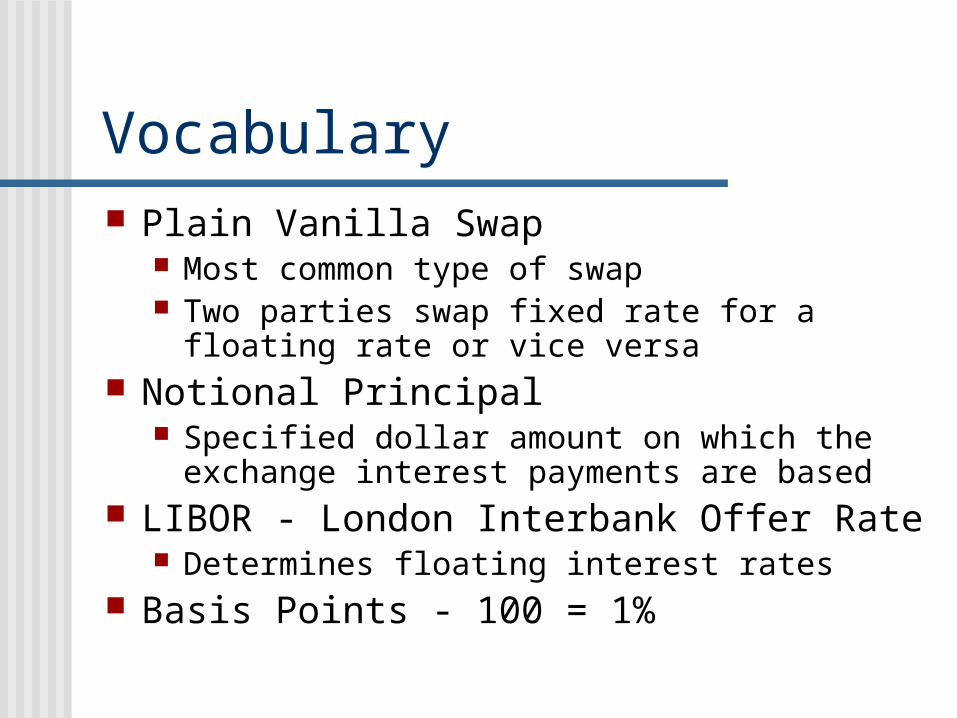

Vocabulary Plain Vanilla Swap

Most common type of swap Two parties swap fixed rate for a floating rate or vice

versa Notional Principal

Specified dollar amount on which the exchange interest payments are based

LIBOR - London Interbank Offer Rate Determines floating interest rates

Basis Points - 100 = 1%

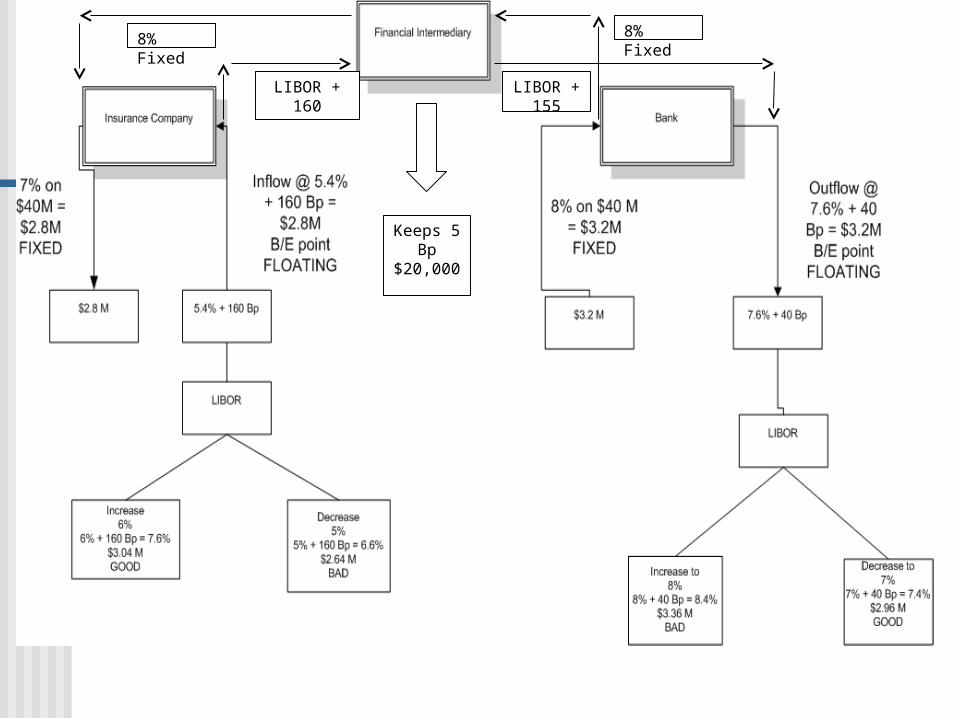

Insurance Company ($40M N.P.)

Pays Out

Claims - Actuarially computed Law of large numbers

7% on $40 Million = $2.8 Million Fixed rate

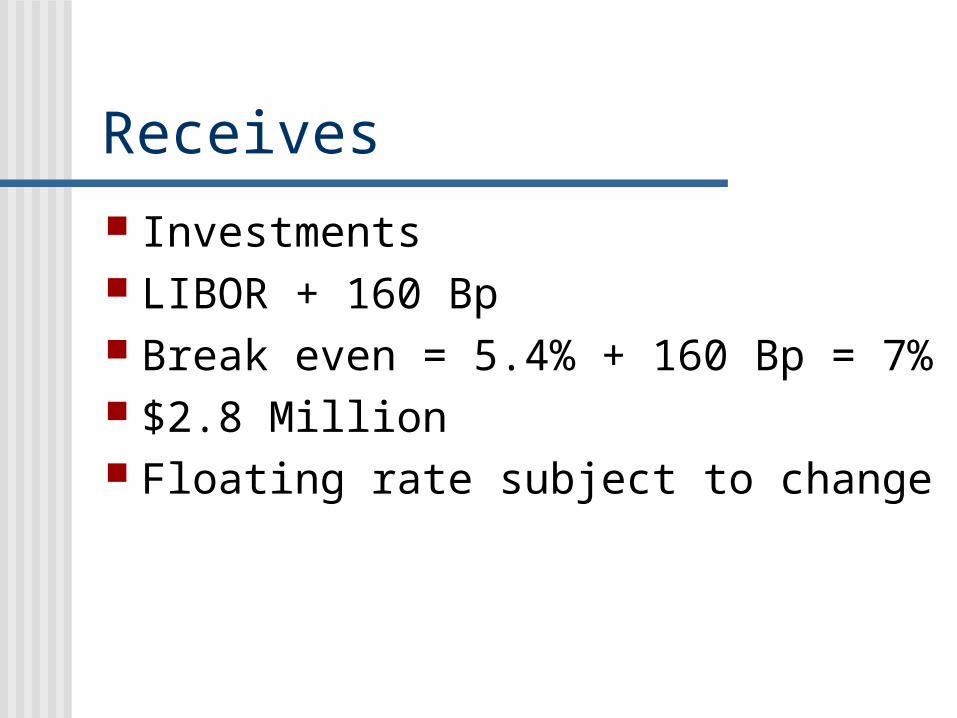

Receives

Investments LIBOR + 160 Bp Break even = 5.4% + 160 Bp = 7% $2.8 Million Floating rate subject to change

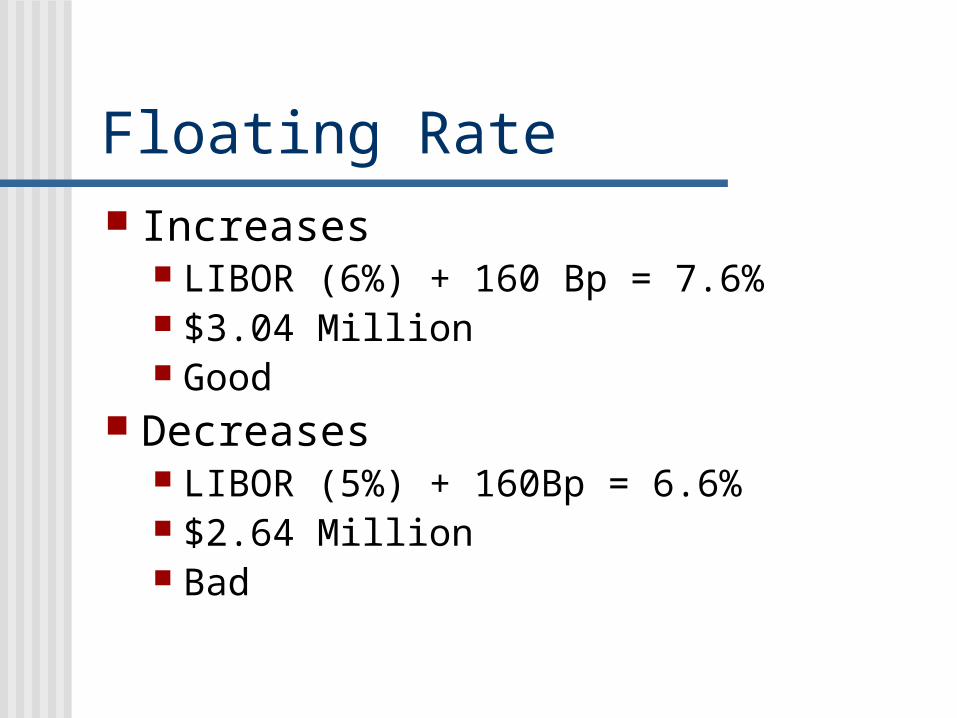

Floating Rate Increases

LIBOR (6%) + 160 Bp = 7.6% $3.04 Million Good

Decreases LIBOR (5%) + 160Bp = 6.6% $2.64 Million Bad

Bank ($40M N.P.)

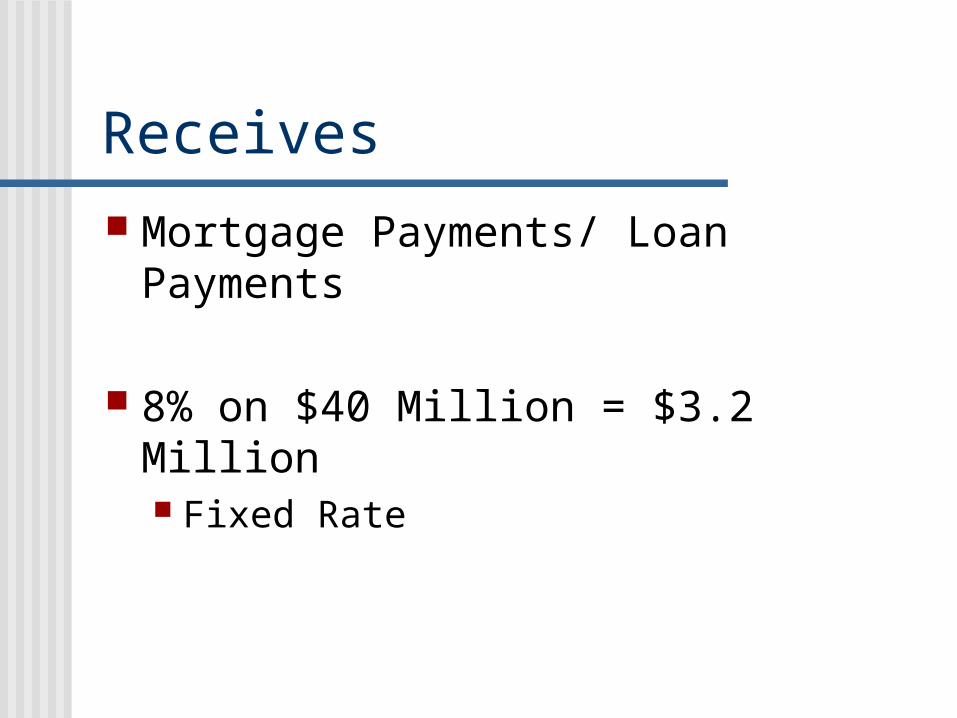

Receives

Mortgage Payments/ Loan Payments

8% on $40 Million = $3.2 Million Fixed Rate

Pays Out

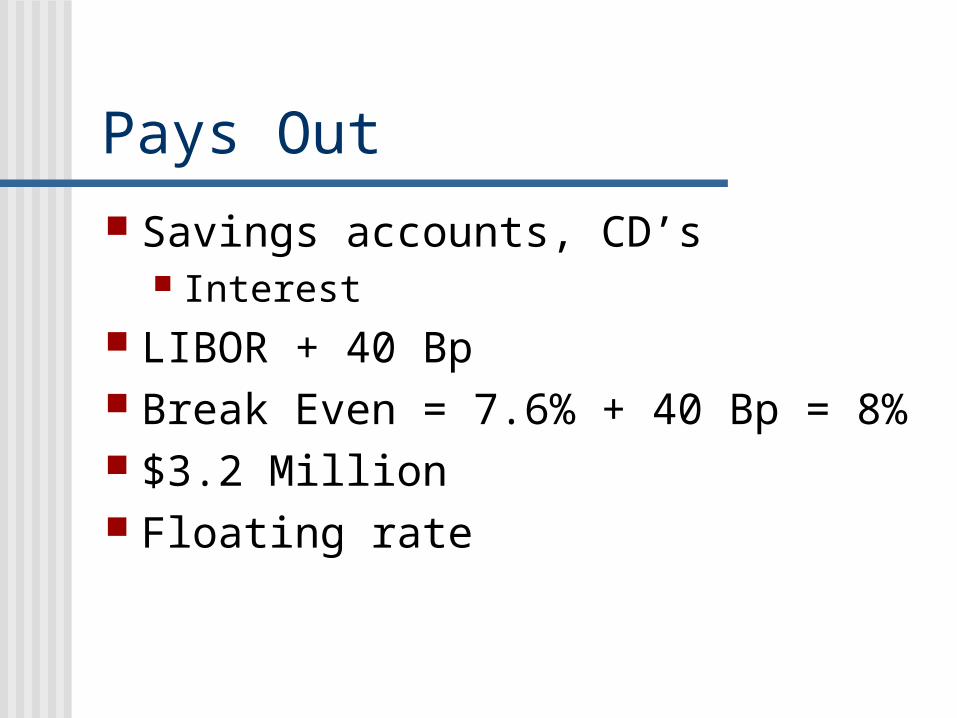

Savings accounts, CD’s Interest

LIBOR + 40 Bp Break Even = 7.6% + 40 Bp = 8% $3.2 Million Floating rate

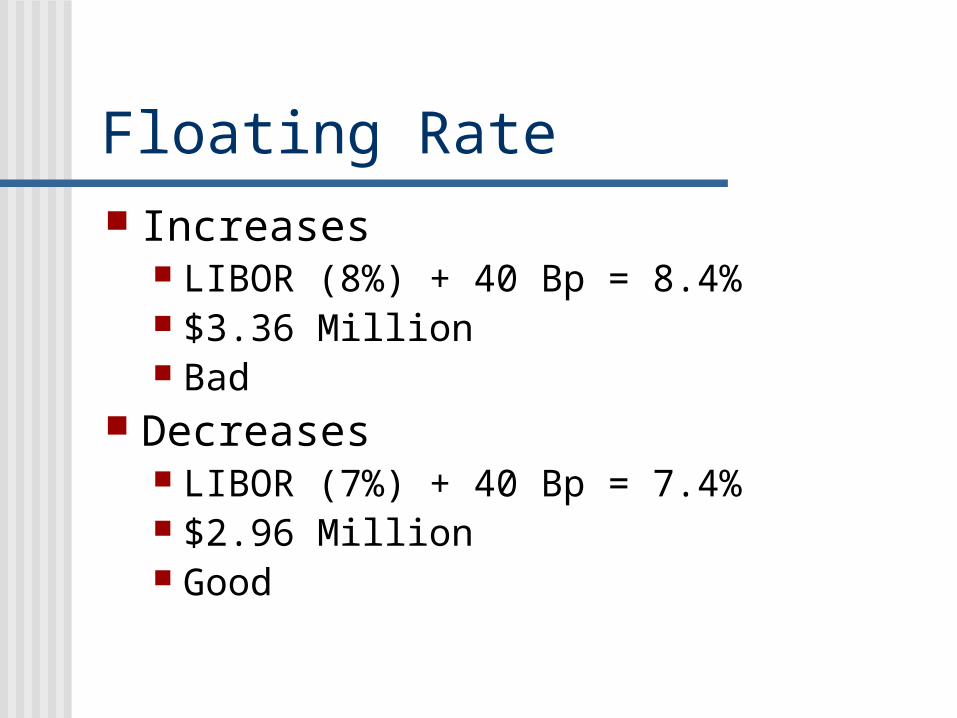

Floating Rate Increases

LIBOR (8%) + 40 Bp = 8.4% $3.36 Million Bad

Decreases LIBOR (7%) + 40 Bp = 7.4% $2.96 Million Good

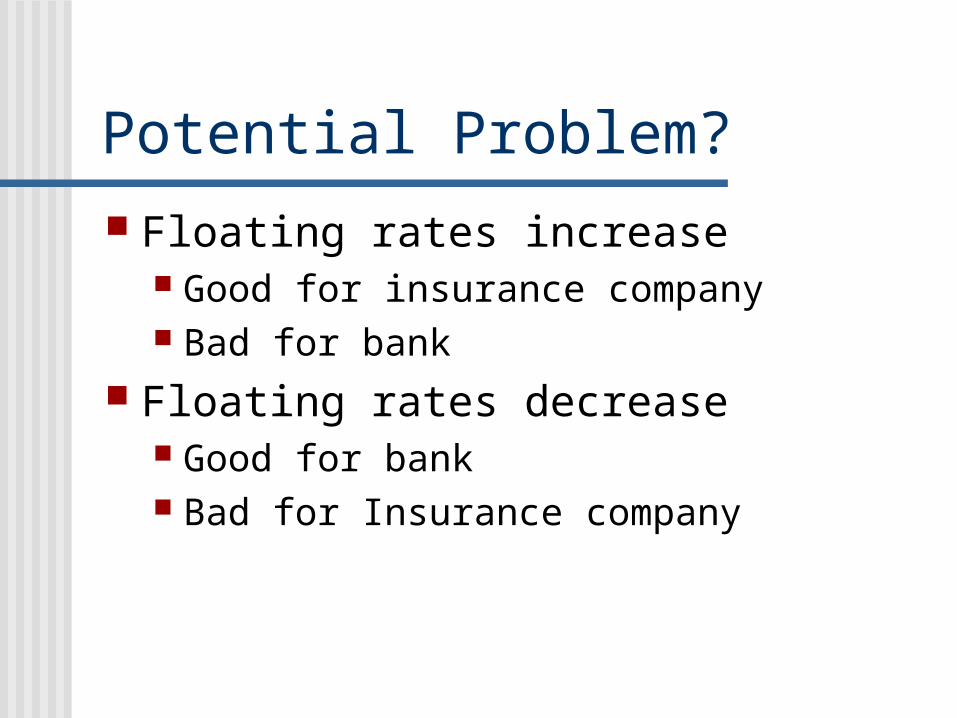

Potential Problem?

Floating rates increase Good for insurance company Bad for bank

Floating rates decrease Good for bank Bad for Insurance company

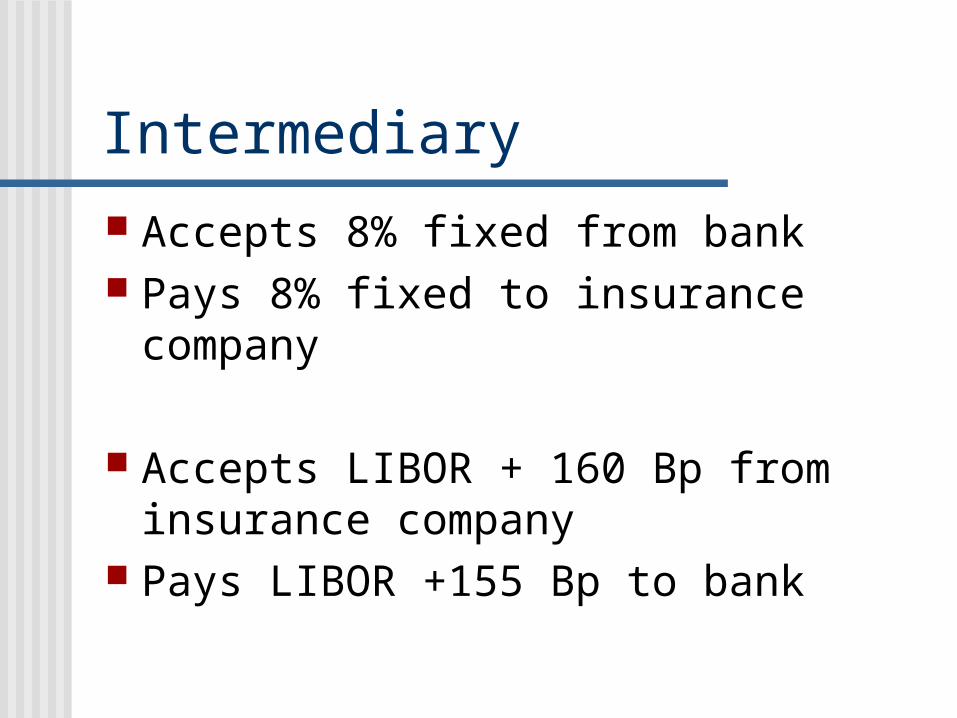

Intermediary

Accepts 8% fixed from bank Pays 8% fixed to insurance company

Accepts LIBOR + 160 Bp from insurance company

Pays LIBOR +155 Bp to bank

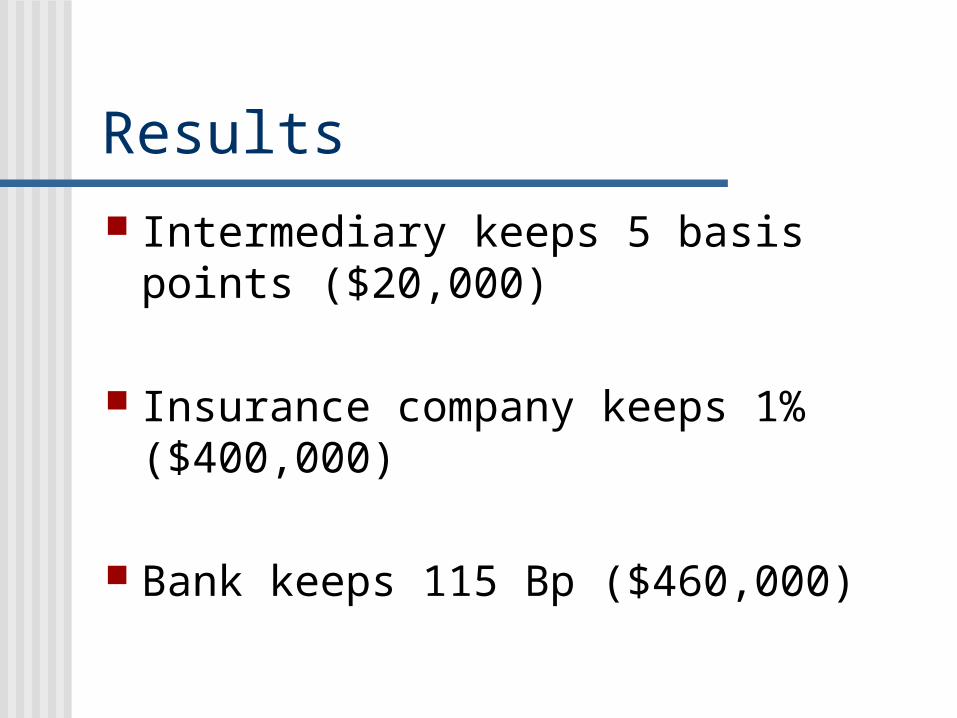

Results

Intermediary keeps 5 basis points ($20,000)

Insurance company keeps 1% ($400,000)

Bank keeps 115 Bp ($460,000)

LIBOR + 160

LIBOR + 155

8% Fixed8% Fixed

Keeps 5 Bp

$20,000

Intermediaries

Intermediaries key to the swap Match two companies with similar needs Different notional principles - Intermediary

takes a position to fill swap

Questions?