Embed Size (px)

Citation preview

5/14/2014

1

1

Interest Rate Hedging:Unveiling Market Complexities

May 28, 2014

New York Cash Exchange

Amanda Breslin, CFA

2

Disclaimer

TRANSACTIONS IN OVER‐THE‐COUNTER DERIVATIVES (OR “SWAPS”) HAVE SIGNIFICANT RISKS, INCLUDING, BUT NOT LIMITED TO, SUBSTANTIAL RISK OF LOSS. YOU SHOULD CONSULT YOUR OWN BUSINESS, LEGAL, TAX AND ACCOUNTING ADVISERS WITH RESPECT TO PROPOSED SWAP TRANSACTION AND YOU SHOULD REFRAIN FROM ENTERING INTO ANY SWAP TRANSACTION UNLESS YOU HAVE FULLY UNDERSTOOD THE TERMS AND RISKS OF THE TRANSACTION, INCLUDING THE EXTENT OF YOUR POTENTIAL RISK OF LOSS. THIS MATERIAL HAS BEEN PREPARED BY A SALES OR TRADING EMPLOYEE OR AGENT OF CHATHAM HEDGING ADVISORS AND COULD BE DEEMED A SOLICITATION FOR ENTERING INTO A DERIVATIVES TRANSACTION. THIS MATERIAL IS NOT A RESEARCH REPORT PREPARED BY CHATHAM HEDGING ADVISORS. IF YOU ARE NOT AN EXPERIENCED USER OF THE DERIVATIVES MARKETS, CAPABLE OF MAKING INDEPENDENT TRADING DECISIONS, THEN YOU SHOULD NOT RELY SOLELY ON THIS COMMUNICATION IN MAKING TRADING DECISIONS.

5/14/2014

2

3

The Chatham Difference ‐ independent hedging advisor

Interest Rate Hedging FX Hedging Commodity Hedging Hedge Accounting Advisory Regulatory Advisory Debt & Capital Advisory

Full web‐based platform Financial risk mgt modules Debt management modules Covered by SSAE 16 audit

Serving 1200+ clients annually $2.5 trillion notional transacted 6 Locations globally inU.S., Europe, and Asia

4

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

Today’s Agenda

5/14/2014

3

5

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

Mar‐04 Mar‐05 Mar‐06 Mar‐07 Mar‐08 Mar‐09 Mar‐10 Mar‐11 Mar‐12 Mar‐13 Mar‐14

USD 5Y LIBOR Swap Rate

3M LIBOR

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Mar‐12 Sep‐12 Mar‐13 Sep‐13 Mar‐14

Source: Bloomberg

Current Interest Rate Landscape3M LIBOR and 5‐year swap rates have been volatile and are currently historically low

6

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 7 Yr 9 Yr 10 Yr

2010

2015

2014

2013

Current Interest Rate LandscapeInterest Rate Swap Yield Curves

5/14/2014

4

7

Pre-Crisis Post-Crisis

Large pool of market dealers

Abundant Liquidity

Less strict bank regulation

Minimum cost of funds among banks

More concentrated pool of market dealers

Constrained credit capacity

Stringent bank regulation

Higher cost of funds among banks.

Efficient execution costs

Close to zero funding charges

Credit and capital charges were flexible

Documentation and KYC requirements were light

Higher execution costs

Meaningful funding charges

Significant credit and capital charges

LIBOR no longer a good proxy for funding cost

Current Interest Rate Landscape

8

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%90.0%

100.0%

86%

44%

71%

86%

44% 50%

88%

58%

81%

96%

59%

81%

92%

39%55%

85%

35%

82%

89%

36%

85%

94%

32%

94%

89%

48%

75%

Source: The State of Financial Risk Management: Quantitative Benchmark Report – Chatham Financial’s independent study of more than 1,000 US, public companies examining their risk exposures, hedging, and hedge accounting practices.

Current Interest Rate LandscapeInterest Rate Hedging by Industry

5/14/2014

5

9

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

10

‐1%

1%

3%

5%

7%

9%

11%

13%

Mar‐14 Mar‐15 Mar‐16 Mar‐17 Mar‐18 Mar‐19 Mar‐20 Mar‐21

68% Probability

95% Probability

Current Interest Rate EnvironmentCurrent Interest Rate Environment

5/14/2014

6

11

95% Probability

‐1%

1%

3%

5%

7%

9%

11%

13%

Mar‐14 Mar‐15 Mar‐16 Mar‐17 Mar‐18 Mar‐19 Mar‐20 Mar‐21

5y Swap

5y Swap 1y Fwd+/‐ 2 SD

Current Interest Rate EnvironmentCurrent Interest Rate Environment

12

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

10yr Treasury Swap spread BBB corp spread

Market ApproachFunding Environment

5/14/2014

7

13

‐4.00%

‐2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2013

2014

3yr Swap Rates

Bias 1yr Forward Actual Average Bias

Market ApproachForward Curve is an imperfect forecaster

14

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

5/14/2014

8

15

Fixed

Floating

Credit Ratios and Covenant Restrictions

Business profile

Rates & Volatility

Capital Structure

Peer ComparisonRates and Volatility

Strategic ApproachFixed & Floating Mix Considerations

16

Maintain/ Improve Ratings

Maintain/ Improve Ratings

Meet Investor Requirements Meet Investor Requirements

Manage Covenants Manage Covenants

Board Risk Appetite Board Risk Appetite

0

1

2

3

4

5

6

7

8

Breach Covenant

1 Std Dev “Cushion”

2 Std Dev “Cushion”

2014 2015

Projected Net Debt / EBITDA

Strategic ApproachFinancial Metrics Restrictions and Risk Appetite

5/14/2014

9

17

COMPANY B Yr1 Yr2 Yr3Cash 100 150 50Floating debt 250 250 250Fixed Debt 750 750 750Total Debt 1,000 1,000 1,000Net Debt 900 850 950Fixed Exposure 83% 88% 79%

COMPANY A Yr1 Yr2 Yr3Cash 250 200 200Floating debt 250 250 250Fixed Debt 750 750 750Total Debt 1,000 1,000 1,000Net Debt 750 800 800Fixed Exposure 100% 94% 94%

Strategic ApproachLiability Management and Cash Reserves

18

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

5/14/2014

10

19

Mid‐market Level

Credit Value Adjustment (CVA) Cost

Swap Profit

Execution Cost

Funding Cost

All‐In Swap Level

Transparent

Reasonably

transparent and can be estimated

Not transparent

Pricing DynamicsSwap Rate Components

20

Example: 10‐year, 3M LIBOR swap rates using different discounting methods

LIBORdual‐curve stripping

LIBORdual‐curve stripping

LIBORtraditional bootstrapping

LIBORtraditional bootstrapping

OISdual‐curve stripping

OISdual‐curve stripping

Discounting MethodDiscounting Method

3.079%3.079% 3.092%3.092% 3.092%3.092%Mid‐marketMid‐market

Source: Bloomberg and Chatham proprietary valuation model. Rates as of March 20, 2014.

(1.3 bps)(1.3 bps) marketmarket marketmarketEarly TerminationEarly Termination

3.100% 3.100% 3.100%

Pricing DynamicsOIS Discounting

5/14/2014

11

21

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Mar‐14 Sep‐14 Mar‐15 Sep‐15 Mar‐16 Sep‐16 Mar‐17 Sep‐17 Mar‐18 Sep‐18

Swap Rate

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Mar‐14 Sep‐14 Mar‐15 Sep‐15 Mar‐16 Sep‐16 Mar‐17 Sep‐17 Mar‐18 Sep‐18

Offsetting Cash Flow Net Cash Flow Paid Net Cashflow Received

Swap Rate

Floor

Example: Vanilla 5‐year swap rate is 1.81%5‐year swap rate with embedded 1% floor: 2.09%

Example: Vanilla 5‐year swap rate is 1.81%5‐year swap rate with embedded 1% floor: 2.09%

Pricing DynamicsEmbedded Floors

22

‐$12,000,000

‐$10,000,000

‐$8,000,000

‐$6,000,000

‐$4,000,000

‐$2,000,000

$0

$2,000,000

$4,000,000Expected Exposure and Forward MTM

Forward MTM

Expected exposure

‐2 Standard deviations

Pricing DynamicsCredit Exposure of a Swap

5/14/2014

12

23

DerivativesDesk

Collateralized Market

Borrow Collateral

Pricing DynamicsFunding Value Adjustment (FVA)

End‐User

Dealer Bank

UncollateralizedTrade

Collateralized Hedge

Funding Desk

24

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

5/14/2014

13

25

Affiliate Transfers

Novation Rights

Events of Default Provisions

Valuation Disputes

MTM Reset Triggers

Credit Breaks

Mutual Breaks

Ability to Deliver Multiple Currencies

in Collateral

Embedding Options

ACCOUNTING

Step‐up Swaps

Index Choice

Documentation and Structuring Complexities

26

vs.

Cancellable Swap

Deferred Premium

Cap

Annuitized Premium

Cap

Swap w/ Embedded

Floor

Step‐Up Swap

Swaption

Swap

Collar

Cap

Documentation and Structuring ComplexitiesProduct Choice

5/14/2014

14

27

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

28

Banks 2008 Current

Morgan Stanley Aa3 Baa2

Bank of America Aa1 Baa2

Citibank Aa3 Baa2

Deutsche Bank Aa1 A2

Societe Generale Aa2 A2

Royal Bank of Scotland Aa2 Baa2

Unicredit Aa3 Baa2

Barclays A1 A3

BBVA Aa1 Baa2

Counterparty ConsiderationsBank Senior Unsecured Credit Ratings

5/14/2014

15

29

60+ HOURSto get set up for clearing…

or Policy, Board Review, Resolutions

60+ HOURSto get set up for clearing…

or Policy, Board Review, Resolutions

Constant EvolutionConstant Evolution

40+QUESTIONS

per trading entity in pre‐trade documentation

40+QUESTIONS

per trading entity in pre‐trade documentation

Increased Documentation & Operational Complexity

Regulatory ClassificationsHedging Entity

Counterparties

Product Choice

Regulatory ClassificationsHedging Entity

Counterparties

Product Choice

You decide to hedge

End‐User Exception

ISDA Schedules & CSAs

Portfolio Reconciliation & Reporting

FCM & Give‐Up Documentation

Dodd‐Frank & EMIR Protocols

Reporting & RecordkeepingReporting &

Recordkeeping

Collateral ManagementCollateral

Management

Daily ValuationsDaily ValuationsCompliance Measures

Clearing/End‐User Exception

Portfolio Reconciliation

Reporting

Compliance Measures

Clearing/End‐User Exception

Portfolio Reconciliation

Reporting

Reporting & Recordkeeping

Counterparty ConsiderationsRegulatory Complexities

30

Current IR Landscape

Common Approachesa. Market approachb. Strategic approach

Unveiling Complexitiesa. Pricing dynamicsb. Documentation and Structuringc. Counterparty considerations

Best Practices:Case Study

5/14/2014

16

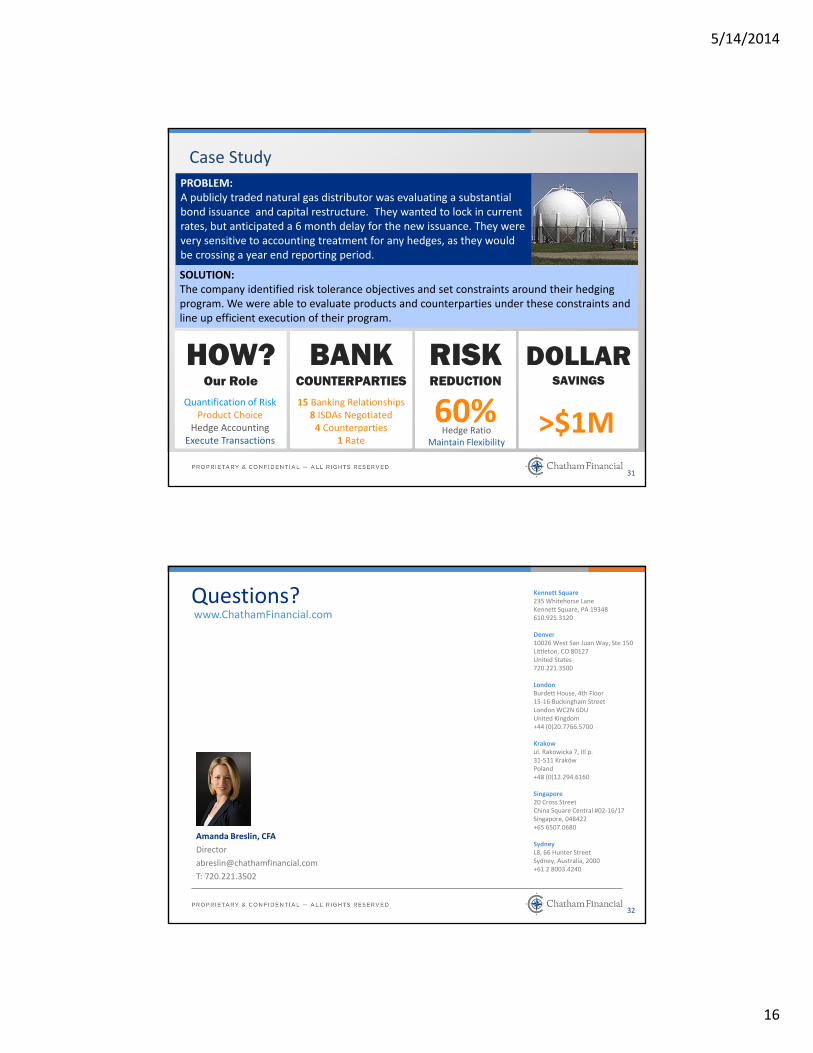

31

DOLLARSAVINGS

RISKREDUCTION

60%

PROBLEM:A publicly traded natural gas distributor was evaluating a substantial bond issuance and capital restructure. They wanted to lock in current rates, but anticipated a 6 month delay for the new issuance. They were very sensitive to accounting treatment for any hedges, as they would be crossing a year end reporting period.

SOLUTION:The company identified risk tolerance objectives and set constraints around their hedging program. We were able to evaluate products and counterparties under these constraints and line up efficient execution of their program.

HOW?Our Role

BANKCOUNTERPARTIES

15 Banking Relationships8 ISDAs Negotiated4 Counterparties

1 Rate

Quantification of RiskProduct Choice

Hedge Accounting Execute Transactions

Case Study

Hedge RatioMaintain Flexibility

>$1M

32

Questions?www.ChathamFinancial.com

Amanda Breslin, CFA

Director

T: 720.221.3502

Kennett Square235 Whitehorse LaneKennett Square, PA 19348610.925.3120

Denver10026 West San Juan Way, Ste 150Littleton, CO 80127United States720.221.3500

LondonBurdett House, 4th Floor15‐16 Buckingham StreetLondon WC2N 6DUUnited Kingdom+44 (0)20.7766.5700

Krakowul. Rakowicka 7, III p.31‐511 KrakówPoland+48 (0)12.294.6160

Singapore20 Cross StreetChina Square Central #02‐16/17Singapore, 048422+65 6507.0680

SydneyL8, 66 Hunter StreetSydney, Australia, 2000+61 2 8003.4240