Embed Size (px)

Citation preview

Interest Hedging in Times of Uncertainty

Annual Conference of theCroatian Association of Corporate Treasurers,

September 2009Mag. Martina Kranzl

2

Agenda

Interest Hedging in Times of Uncertainty

Basic Instruments

Participation in Money Market Rates

Participation in Capital Market Rates

Initial Situation

Appendix

3

Agenda

Interest Hedging in Times of Uncertainty

Basic Instruments

Participation in Money Market Rates

Participation in Capital Market Rates

Initial Situation

Appendix

4

Initial Situation

The purpose of this material is to present you with ideas to control your interest rate risks. On this basis, further possible solutions for you can be discussed.

The following example is precisely tailored to a specific initial situation. Modified solutions are naturally available for an altered initial situation.

I assume the following:

1. The coverage of your EUR financing needs for the next 5 years will be met by taking out a variable loan based on the 3M Euribor.

2. The interest rate will be stipulated at the beginning of every 3-month period based on the current 3M Euribor whereas the interest payment will take place in arrears on the last day of the respective period.

3. You would like to secure yourself against an unlimited increase in your interest load. For this hedging you do not want to pay a premium.

5

Agenda

Basis Instruments

Participation in Money Market Rates

Participation in Capital Market Rates

Initial Situation

Interest Hedging in Times of Uncertainty

Appendix

6

Current Market Environment

A historically low interest rate environment prevails in the Eurozone with low capital market interest rates and even lower money market interest rates.

On the one hand, low capital market interest rates offer the chance of entering into an attractive fixed-rate agreement.

7

Current Market Environment

On the other hand, a significant premium in the form of a spread will be required for this hedging, particularly in an economically strained environment.

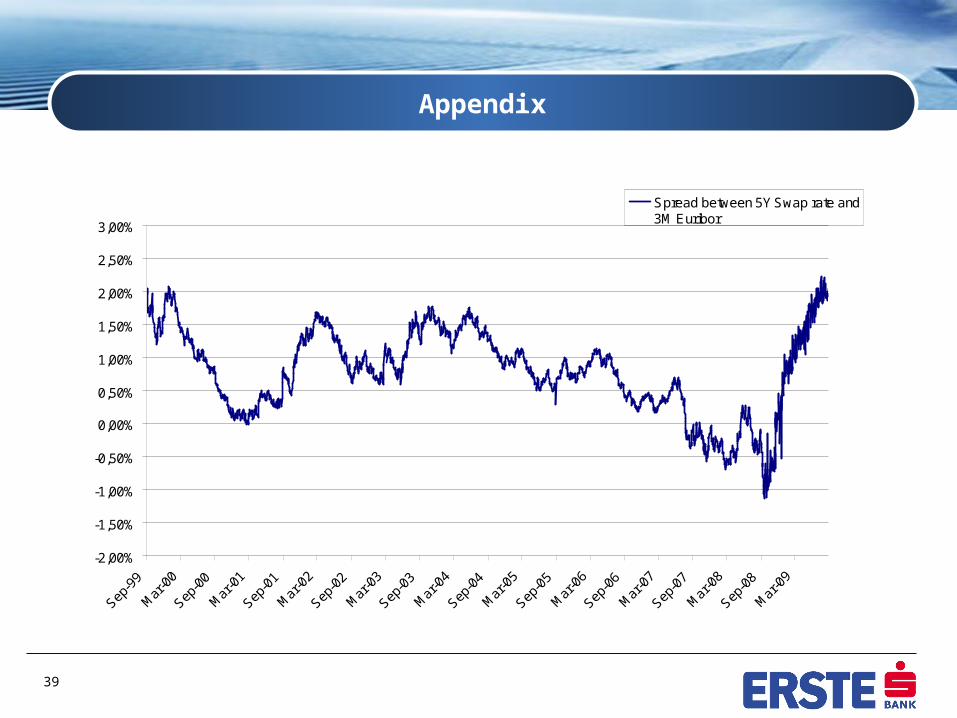

The 5Y swap rate is currently more than three times as high as the 3M Euribor (0.762%). Therefore, more will be calculated for the interest hedge than for the financing (excluding financing margin). The interest rate difference between the 5Y swap rate and the 3M Euribor reached its 5-year high at 2.0380%. (see appendix)

In addition to the fact that it is quite unattractive to pay a substantial premium, particularly in a period of weak economic growth, a 5Y interest rate swap does not fulfill the requirement for flexibility.

The 5Y swap rate exceeds the 3M Euribor because the financial markets expect, on average, an economic recovery and consequently for the ECB to react with a series of rate hikes in key interest rates in order to control inflation.

8

Current Market Environment

However, an economic recovery and a steady increase in money market rates is only one possible future scenario.The swap rate should be interpreted as an average of a wide range of market expectations (equilibrium price of supply and demand). It does not imply that this one particular possible future development will actually occur.

In times of robust economic growth, the range of market expectations concerning the future course of interest rates is relatively narrow. In light of present day uncertainties, current expectations are much more diverse.

On the next slides two extreme scenarios for economic development will be presented. I will elaborate on which form of interest rate hedging would meet the needs of a regular pro-cyclical customer.

9

Interest Rate vs. Economic cycle

It is assumed that the demands of a business entity will be best met if the interest payments on debt capital are sustainable i.e. if they adjust simultaneously with the economic cycle. This is the primary condition.

Once the primary condition is met, we can turn our attention to the secondary condition: a low rate of interest.

10

Recovery Scenario

The recovery from the recession, already presumed on the equity markets, continues steadily. During the following year, at the latest, the Eurozone economy will post positive growth rates.

The positive sentiment is reflected by sharply rising commodity prices and expectations for a rapid tightening by the ECB. The 3M Euribor is expected to exceed the level of the current 5Y swap rate by the middle of next year.

This recovery scenario makes clear that the lack of interest hedging would lead to a higher interest load and/or higher hedging costs.

11

Recovery Scenario

In a recovery scenario, an entity making use of an interest rate hedge would be better off due to two factors:

– Fully hedged and immunised to increasing interest rates.

– No upfront premium.

It should also be noted that a pro-cyclical business entity could presumably sustain these higher interest costs. The improvement of the business outlook justifies a higher interest load. After all, new projects would have to be financed at a higher level.

12

Weakness Scenario

Although many market participants anticipate an early recovery, some predict a much slower recovery and even long-term economic weakness cannot be excluded.

In this scenario, the financial market continues to be overwhelmed by ever-increasing uncertainty and consumer confidence decreases further, even in stable economies like Germany.

Improvements in sentiment prove to have been too optimistic. Many companies are put under severe pressure as their production capacities which were increased in recent years can no longer be exploited or sustained.

At the same time, governments are obliged to reform social aid and increase tax income to satisfy lenders and avoid a rise in financing costs putting the private sector under additional pressure.

13

Weakness Scenario

This scenario clearly points out how essential it is for a company to choose a variable loan that adjusts to the economic cycle at least for a portion of the financing requirement.

In a weakness scenario, an entity making use of variable financing would better off due to two factors:

– In comparison to the swap, no “premium“ in the form of a spread has to be paid to the 3M Euribor.

– The entity can fully participate in a further declining 3M Euribor.

Therefore, at least some of the demand-side shocks can be buffered by lower financing costs.

Moreover, interest management contributes to flexibility under the constraints of a tight financial situation in times of an economic crisis.

14

Smoothing Results via Variable Financing

Presented below is the smoothing effect of matching the interest costs with the development of the sales revenues by means of variable financing.

The gross profit and operating profit (EBITDA) will remain unaffected by the smoothing effect of variable financing but the fluctuation in annual profit can be minimised by adjustable interest costs.

Sales Revenues- Cost of Production_________________ Gross Profit

- Distribution Cost- Administration Cost_____________________ Operating profit (EBITDA)

- Interest Costs- Write-offs- Taxes+/- Extraordinary Earnings/Expenditure Net Income of the Year

Bear Market:Declining sales revenues absorbed by decreasing interest costs.

Bull MarketRising interest costs compensated by higher sales revenues.

15

Interim Conclusion

If the recovery scenario occurs, a fixed rate swap may well have been a reasonable solution in hindsight. This will not be the case with the weakness scenario. The possibility of retaining at least some sort of participation in lower interest rates and keeping financing costs flexible remains unutilized.

This leads to two recommendations regarding interest hedging:

– Don`t miss the chance to secure a maximum interest rate level to take advantage of current low interest levels. (Hedging)

– Maintain participation in low 3M Euribor interest rates for as long as the economic recovery is delayed. (Participation)

Below are various adjustable interest hedging solutions calculated with the expressed recommendations “Hedging and Participation“. All structures are free of premium. The following conditions are reference points on which a dialogue should be built.

16

Agenda

Initial Situation

Interest Hedging in Times of Uncertainty

Participation in Money Market Rates

Participation in Capital Market Rates

Basic Instruments

Appendix

17

Interest Rate Swap

You enter into an interest rate swap which allows for the exchange of 3 month Euribor (3M Euribor) of your funding against the payment of the fixed interest rate of 2.8000% p.a. for the period of 5 years.

The 3M Euribor will be used to service the underlying funding; this interest rate provision is not dependent on your funding. The fixed rate of 2.8000% p.a. plus your individual funding margin will be your total interest load of the swap. For the remainder of the document this will be your comparison rate.

Alternative indications: 2.2000% p.a. for 3 years; 3.5500% p.a. for 10 years Rewards: fixed calculation rate, no upfront costs Risk: no participation in low Euriborrates

Client

3M-Euribor

2.8000% p.a.

3M-EuriborLoan

18

Interest rate Cap

Your interest load is based on the 3M Euribor and you want to maintain your interest load on a floating basis.

You pay a premium of 2.5000% p.a. to guarantee a maximum interest rate on the 3M Euribor at 3.5000% p.a. for the period of 5 years.

Alternative indications: Maximum interest rate at 2.7500% p.a. for 3 years; upfront premium: 1.5000% of

the notional amount Maximum interest rate at 5.0000% p.a. for 10 years; upfront premium: 3.9000% of

the notional amount Rewards: full participation in low Euriborrates, hedge against rising interest rates Risk: upfront costs

Client

3M-Euribor

3M-Euribor, maximum rate 3.5000% p.a. Premium: 2.5000%

3M-EuriborLoan

19

Agenda

Initial Situation

Interest Hedging in Times of Uncertainty

Basic Instruments

Participation in Capital Market Rates

Participation in Money Market Rates

Appendix

20

Libor Factor with Cap

Market Expectations: Slightly rising or falling 3M-Euribor.

Term: 5 Years, bullet

Interest Mode: quarterly, act/360, mod. foll.

Customer Receives: 3M-Euribor

Customer Pays: Liborfactor rate: 1.25 x 3M-Euribor

i.a.*, max. 4.0000% p.a.

* Interest rate determination at the end of a period (in arrears)

Alt. Fixed Rate: 2.8000% p.a.

3M-Euribor: 0.762% p.a.

Stand Still: 0.9525% p.a.Savings: 1.8475% p.a.

Worst Case: 4.0000% p.a.Best Case: 0.000% p.a.

Client

3M-Euribor

Liborfactor rate: 1.25 * 3M-Euribor, max. 4.0000% p.a.

3M-EuriborLoan

21

Libor Factor with Cap

You enter into an interest rate swap which allows for the exchange of 3 month Euribor (3M Euribor) of your funding against the payment Liborfactorrate.

The 3M Euribor will be used to service the underlying funding; This interest rate provision is not dependent on your funding. The liborfactor rate plus your individual funding margin will be your total interest load of the swap.

22

Libor Factor with Cap

RISKS The factor of 1.25 leads to commensurately higher interest load. The maximum rate is 1.2000% p.a. higher than the alternative rate. In case of increasing Euriborrates the fixing in arrears leads to a higher interest rate

load.

REWARDS You can participate in low Euribor rates. You have secured a maximum rate at no upfront premium. In case of falling Euriborrates the fixing in arrears leads to a lower interest rate load.

23

Interest Swap with Contingent Fixed Rate

Market Expectations: Slightly rising or falling 3M-Euribor

Term: 5 Years, bullet

Interest Mode: quarterly, act/360, mod. foll.

Customer Receives: 3M-Euribor

Customer Pays: 3M-Euribor i.a.*

as long as 3M-Euribor i.a.* < 2.6000% p.a.,

otherwise 4.7000% p.a. until the end of the Term

* Interest rate determination at the end of a period (in arrears)

Alt. Fixed Rate: 2.8000% p.a.3M-Euribor: 0.762% p.a.

Stand Still: 0.762% p.a.Savings: 2.0380% p.a.

Worst Case: 4.7000% p.a.Best Case: 0.0000% p.a.

Client

3M-Euribor

3M-Euribor i.a. or 4.7000% p.a.

3M-EuriborLoan

24

Interest Swap with Contingent Fixed Rate

You enter into an interest rate swap which allows for the exchange of the 3-month Euribor against the payment of the participation interest rate for the period of 5 years. This interest rate provision is not dependent on your funding. The participation interest rate plus your funding margin will be your total interest load of the swap.

The participation interest rate will be the 3M Euribor fixed at the end of every quarter (in arrears), as long as the 3M Euribor in arrears is fixed below the level of 2.6000% p.a. If the 3M Euribor is fixed above the level of 2.6000% p.a. you have to pay the Maximum rate of 4.7000% p.a. for this period and the rest of the tenor.

25

Interest Swap with Contingent Fixed Rate

RISKS The maximum rate of 4.7000% p.a. is 1.9000% p.a. above the comparison rate. Once the 3M Euribor is fixed above the level of 2.6000% p.a. you will pay the

maximum rate of 4.7000% p.a. for this period and the rest of the tenor. The fixing in arrears can lead to a higher Interest load and a sooner change into the

fixed rate of 4.7000% p.a.

REWARDS You have secured a maximum rate and therefore a fixed calculation basis. As long as the 3M Euribor is fixed below the interest rate level of 2.6000% p.a., you

can fully participate in low Euriborrates. You do not have to pay a premium for this hedging instrument.

26

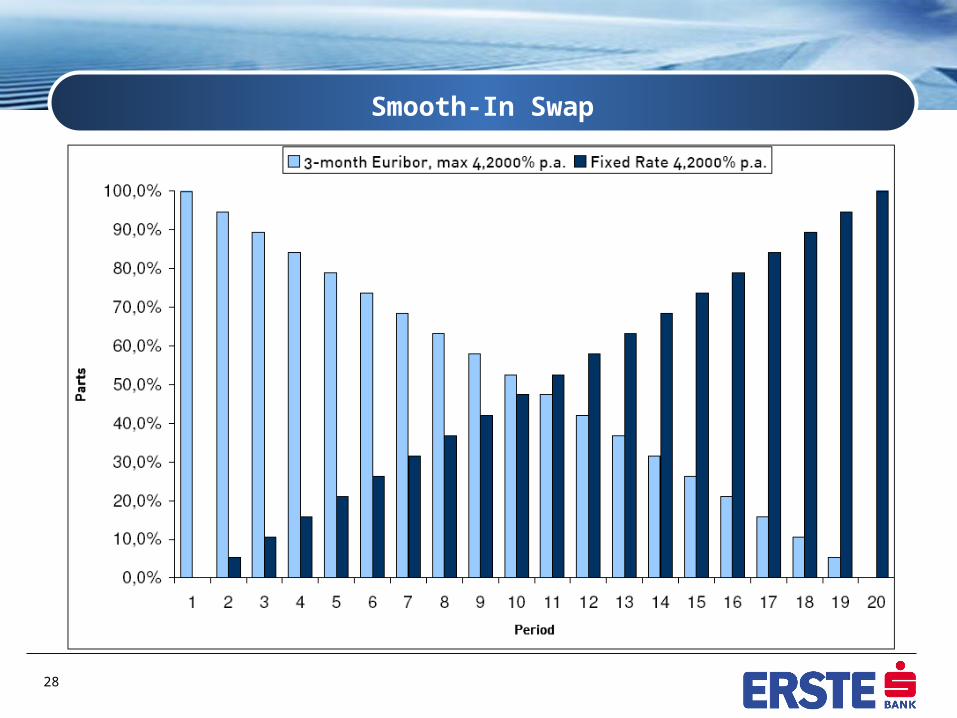

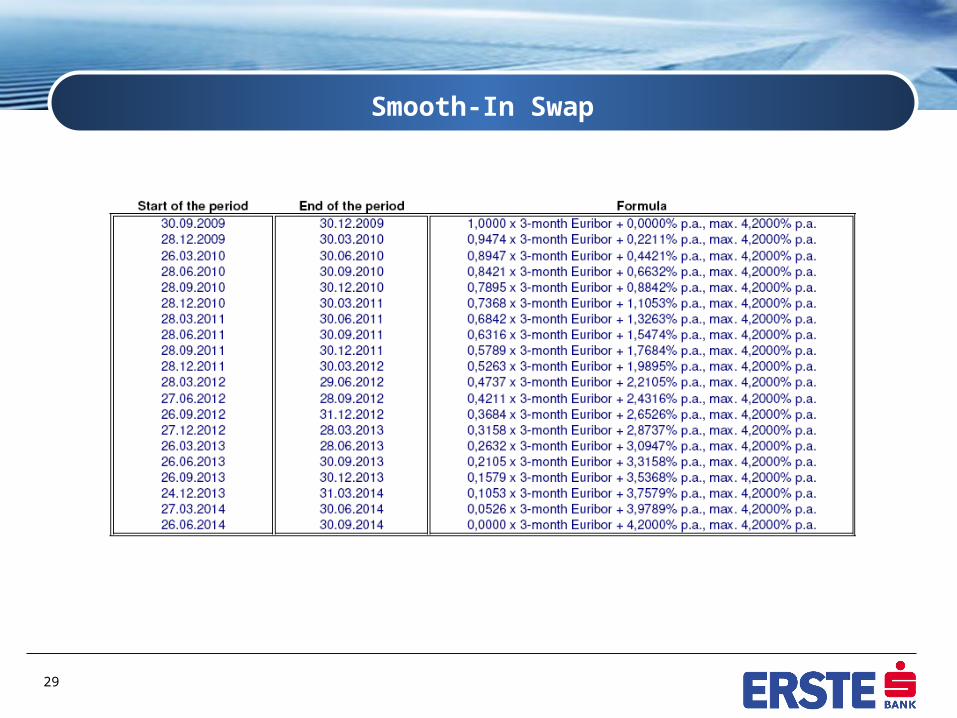

Smooth-In Swap

Market Expectations: Falling or constant 3M-Euribor in the beginning and

increasing later on

Term : 5 Years, bullet

Interest Mode: quarterly, act/360, mod. foll.

Customer Receives: 3M-Euribor

Customer Pays: Euribor Share + fixed portion

Euribor Share: 3M-Euribor i.a.*, max. 4.2000% p.a.

initially 100%, decreasing by 5.26% points per period (finally reaching 0%)

Fixed portion: 4.2000% p.a.

initially 0%, increasing by 5.26% points per period (finally reaching 100%)

* Interest rate determination at the end of a period (in arrears)

Alt. Fixed Rate: 2.8000% p.a.3M-Euribor: 0.762% p.a.

Stand Stillin Period 1: 0.762% p.a.

Stand Stillin Period 20: 4.2000% p.a.

Worst Case: 4.2000% p.a.Best Case: 0.0000% p.a.

27

Smooth-In Swap

You enter into an interest rate swap which allows for the exchange of the 3-month Euribor against the payment of the Smooth-in rate for the period of 5 years. This interest rate provision is not dependent on your funding. The Smooth-in rate plus your funding margin will be your total interest load of the swap.

The Smooth-in Interest Rate will be calculated from the sum of the fixed rate portion which will increase during the strategys maturity and the 3-month Euribor, multiplied by a simultaneously decreasing factor. For the first period the smooth-in rate consists of 100% of the 3M Euribor, maximum 4.2000% p.a.; for the last period the smooth-in rate consists 100% of the fixed rate of 4.2000% p.a.

28

Smooth-In Swap

29

Smooth-In Swap

30

Smooth-In Swap

RISKS The maximum rate of 4.2000% p.a. is 1.4000% p.a. higher than your comparison

rate of 2.8000% p.a. The participation in low 3-month Euribor rates decreases over time.

REWARDS

Based on the current 3-month Euribor, you would pay an interest rate of 0.7620% p.a. for the first period, which corresponds to an interest reduction of 2.0380% p.a. in relation to the comparison rate.

You will have the opportunity to participate in low 3-month Euribor rates. The floating interest portion will reduce during the maturity of the strategy. Thus

your fixed rate portion will become more important and your interest load more calculable.

No premium payment

31

Combi-Swap

Market Expectations: Slightly rising or falling 3M-Euribor

Term : 5 Years, bullet

Interest Mode: quarterly, act/360, mod. foll.

Customer Receives: 3M-Euribor

Customer Pays: 0.5* 3M-Euribor + 1.9000% p.a.,

max. 3.8000% p.a.

Alt. Fixed Rate: 2.8000% p.a.3M-Euribor: 0.7620% p.a.

Stand Still: 2.2810% p.a.

Worst Case: 3.8000% p.a.Best Case: 1.9000% p.a.

Client

3 month Euribor

Combi-Swaprate, max. 3.8000% p.a.

3 month EuriborLoan

32

Combi-Swap

You enter into an interest rate swap which allows for the exchange of the 3-month Euribor against the payment of the Combi-Swaprate for the period of 5 years. This interest rate provision is not dependent on your funding. The Combi-Swaprate plus your funding margin will be your total interest load of the swap.

The Combi-Swaprate consists of the 3-month Euribor multiplied by the factor of 0.5000 plus a fixed rate of 1.9000% p.a. You will pay a maximum rate of 3.8000% p.a.

33

Combi-Swap

RISKS The maximum rate of 3.8000% p.a. is 1.0000% p.a. higher than your comparison

rate of 2.8000% p.a. Participation in low 3-months Euriborrates only with 50% of your interest load.

REWARDS You may participate in low 3-month Euriborrates with 50% of your interest load. Based on the current 3-month Euribor you would pay an interest rate of 2.2810%

p.a. for the first period, which is an interest reduction of 0.5190% p.a. in relation to the comparison rate.

You have hedged a maximum interest rate. You do not have to pay a premium for this hedging instrument. Your best case of 1.9000% p.a. in case the 3-months Euribor fixes at 0.000% p.a. is

0.9000% p.a. below your comparison rate.

34

Agenda

Initial Situation

Interest Hedging in Times of Uncertainty

Basic Instruments

Participation in Money Market Rates

Appendix

Participation in Capital Market Rates

35

CMS-Libor Factor with Cap

Market Expectations: Slightly rising or falling 2Y-EUR CMS rate. (see appendix)

Term: 5 Years, bullet

Interest Mode: quarterly, act/360, mod. foll.

Customer Receives: 3M-Euribor

Customer Pays: CMS Factor rate: 1.20 x 2Y-EUR CMS i.a.*

max. 4.00% p.a.

* Interest rate determination at the end of a period (in arrears)

Alt. Fixed Rate: 2.8000% p.a.3M-Euribor: 0.762% p.a.2Y-EUR CMS: 1.686% p.a.

Stand Still: 2.0232% p.a.Savings: 0.7768% p.a.

Worst Case: 4.000% p.a.Best Case: 0.000% p.a.

Client

3M-Euribor

CMS Factor rate: 1.20 * 2Y EUR CMS i.a., max. 4.00% p.a.

3M-EuriborLoan

36

CMS-Libor Factor with Cap

You enter into an interest rate swap which allows for the exchange of 3 month Euribor (3M Euribor) of your funding against the payment CMS Factor rate.

The 3M-Euribor will be used to carry forward to the underlying funding; This interest rate provision is not dependent on your funding. The CMS Factor rate plus your individual funding margin will be your total interest load of the swap.

37

CMS-Libor Factor with Cap

RISKS The factor of 1.2 leads to commensurately higher interest load. The maximum rate is 1.2000% higher than the alternative rate. In case of increasing CMS-rates the fixing in arrears leads to a higher interest rate

load. Your minimum interest load is at 0.0000%

REWARDS You can participate in low CMS-rates. You have secured a maximum rate at no upfront premium. In case of falling CMS-rates the fixing in arrears leads to a lower interest rate load.

38

Agenda

Initial Situation

Interest Hedging in Times of Uncertainty

Basic Instruments

Participation in Money Market Rates

Appendix

Participation in Capital Market Rates

39

Appendix

-2,00%

-1,50%

-1,00%

-0,50%

0,00%

0,50%

1,00%

1,50%

2,00%

2,50%

3,00%

Sep-9

9

Mar

-00

Sep-0

0

Mar

-01

Sep-0

1

Mar

-02

Sep-0

2

Mar

-03

Sep-0

3

Mar

-04

Sep-0

4

Mar

-05

Sep-0

5

Mar

-06

Sep-0

6

Mar

-07

Sep-0

7

Mar

-08

Sep-0

8

Mar

-09

Spread between 5Y Swap rate and3M Euribor

40

What does CMS stand for?

CMS is the abbreviation for “Constant Maturity Swap“. With a CMS Swap, a long-term swap rate will be used as the reference rate instead of a short-term rate (e.g. EURIBOR).

How is the fixing of the Capital Market Rate determined?

The fixing is carried out by the independent organization ISDA (International Swaps and Derivatives Association). Quoted swap rates from a panel of various reference banks are used to establish an average. The fixing for the EUR swap rate is published on the Reuters page ISDAFIX.

Frequently Asked Questions

Contact

Maja Crnec Mag. Martina KranzlErste&Steiermärkische Bank d.d. LPA GmbHFinancial Markets and Investment Banking

Zagreb I.Lučića 2 Frankfurt am MainTel.: +385 (0)62 37 1548

Email: [email protected] Email: [email protected]