Embed Size (px)

Citation preview

Thursday,

July 12, 2001

Part II

Federal FinancialInstitutionsExamination CouncilCommunity Reinvestment Act;Interagency Questions and AnswersRegarding Community Reinvestments;Notice

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00001 Fmt 4717 Sfmt 4717 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36620 Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

FEDERAL FINANCIAL INSTITUTIONSEXAMINATION COUNCIL

Community Reinvestment Act;Interagency Questions and AnswersRegarding Community Reinvestment

AGENCY: Federal Financial InstitutionsExamination Council.ACTION: Notice.

SUMMARY: The Consumer ComplianceTask Force (we) of the Federal FinancialInstitutions Examination Council(FFIEC) is supplementing, amending,and republishing its InteragencyQuestions and Answers RegardingCommunity Reinvestment. TheInteragency Questions and Answershave been prepared by staff of the Officeof the Comptroller of the Currency(OCC), the Board of Governors of theFederal Reserve System (Board), theFederal Deposit Insurance Corporation(FDIC), and the Office of ThriftSupervision (OTS) (collectively, theagencies) to answer frequently askedquestions about communityreinvestment. These InteragencyQuestions and Answers containinformal staff guidance for agencypersonnel, financial institutions, andthe public.DATES: Effective Date of AmendedInteragency Questions and Answers onCommunity Reinvestment: July 11,2001.FOR FURTHER INFORMATION CONTACT:OCC: Karen Tucker, National BankExaminer, Community and ConsumerPolicy Division, (202) 874–4446; orMargaret Hesse, Special Counsel,Community and Consumer LawDivision, (202) 874–5750, Office of theComptroller of the Currency, 250 EStreet, SW., Washington, DC 20219.

Board: Catherine M.J. Gates, SeniorReview Examiner, (202) 452–3946; orKathleen C. Ryan, Senior Attorney,(202) 452–3667, Board of Governors ofthe Federal Reserve System, 20th Streetand Constitution Avenue, NW.,Washington, DC 20551.

FDIC: Robert W. Mooney, AssistantDirector, Division of Compliance andConsumer Affairs, (202) 942–3378;Stephanie Caputo, Senior Fair LendingSpecialist, Division of Compliance andConsumer Affairs, (202) 942–3413; or A.Ann Johnson, Counsel, Legal Division,(202) 898–3573, Federal DepositInsurance Corporation, 550 17th Street,NW., Washington, DC 20429.

OTS: Theresa A. Stark, ProjectManager, Compliance Policy, (202) 906–7054; or Richard R. Riese, Director,Compliance Policy, (202) 906–6134,Office of Thrift Supervision, 1700 GStreet, NW., Washington, DC 20552.

SUPPLEMENTARY INFORMATION:

BackgroundIn 1995, the agencies revised the

Community Reinvestment Act (CRA)regulations by issuing a joint final rule,which was published on May 4, 1995(60 FR 22156). See 12 CFR parts 25, 228,345 and 563e, implementing 12 U.S.C.2901 et seq. The agencies publishedrelated clarifying documents onDecember 20, 1995 (60 FR 66048) andMay 10, 1996 (61 FR 21362).

The revised regulations areinterpreted primarily through‘‘Interagency Questions and AnswersRegarding Community Reinvestment,’’which provide informal staff guidancefor use by agency personnel, financialinstitutions, and the public, and whichare supplemented periodically. Wepublished our most recent guidance onApril 28, 2000 (2000 InteragencyQuestions and Answers). 65 FR 25088.In addition to issuing the 2000Interagency Questions and Answers, were-proposed revisions to one questionand answer, as well as a conformingamendment to another question andanswer, in the accompanyingsupplementary information. Theproposed revised question and answeraddressed whether there must be adirect benefit from communitydevelopment loans and services andqualified investments to an institution’sassessment area. We specificallyrequested comment addressing theproposed revised question and answer,as well as general comments andquestions regarding the CRAregulations. 65 FR at 25090–92.

We received 17 letters in response toour request for comments in the 2000Interagency Questions and Answers.Comments came from financialinstitutions or financial institutionholding companies (7), communityorganizations (2), financial institutiontrade associations (4), one state agency,and others (3). This documentsupplements, revises, and republishesthe 2000 Interagency Questions andAnswers based, in part, on questionsand comments received from examiners,financial institutions, and otherinterested parties, and on commentsreceived in response to our request forcomments.

As discussed below, this documentadopts the revisions to the question andanswer about whether there must be adirect benefit to an institution’sassessment area for an activity to benefitthe assessment area that we proposed inApril 2000, along with conformingchanges to another existing questionand answer, which addresses what ismeant by a ‘‘regional area.’’ We are also

making slight clarifying revisions toeight existing questions and answersand adopting six new questions andanswers.

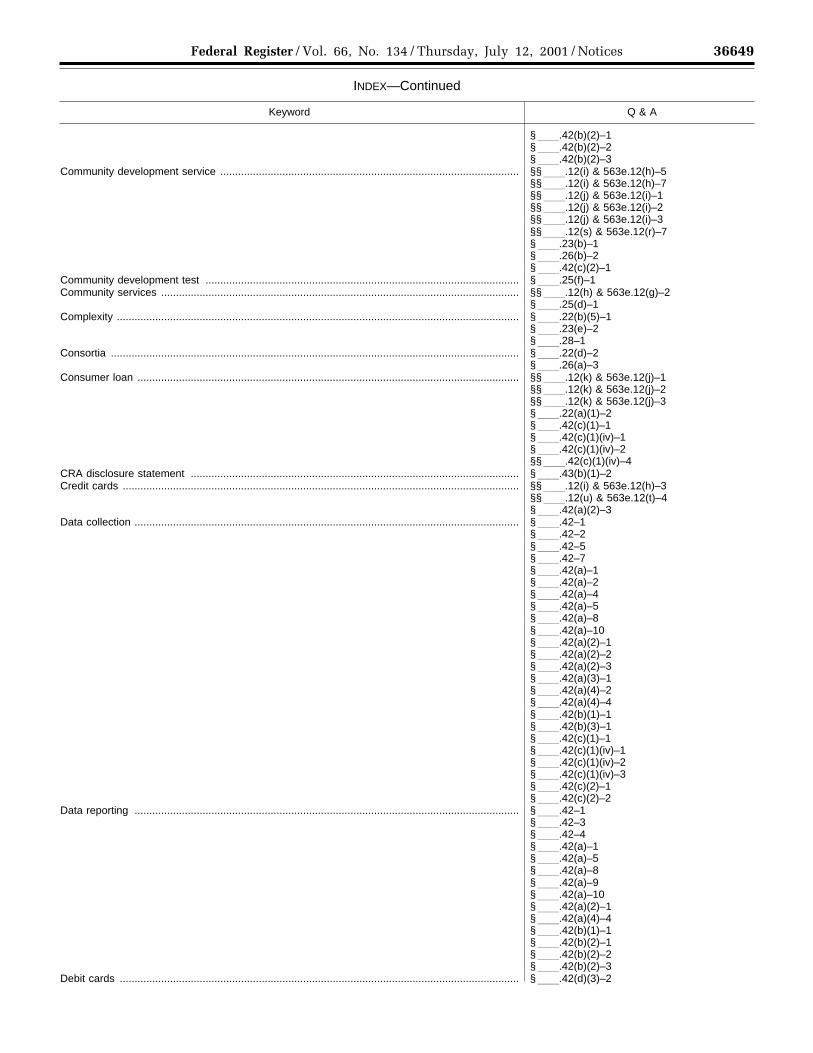

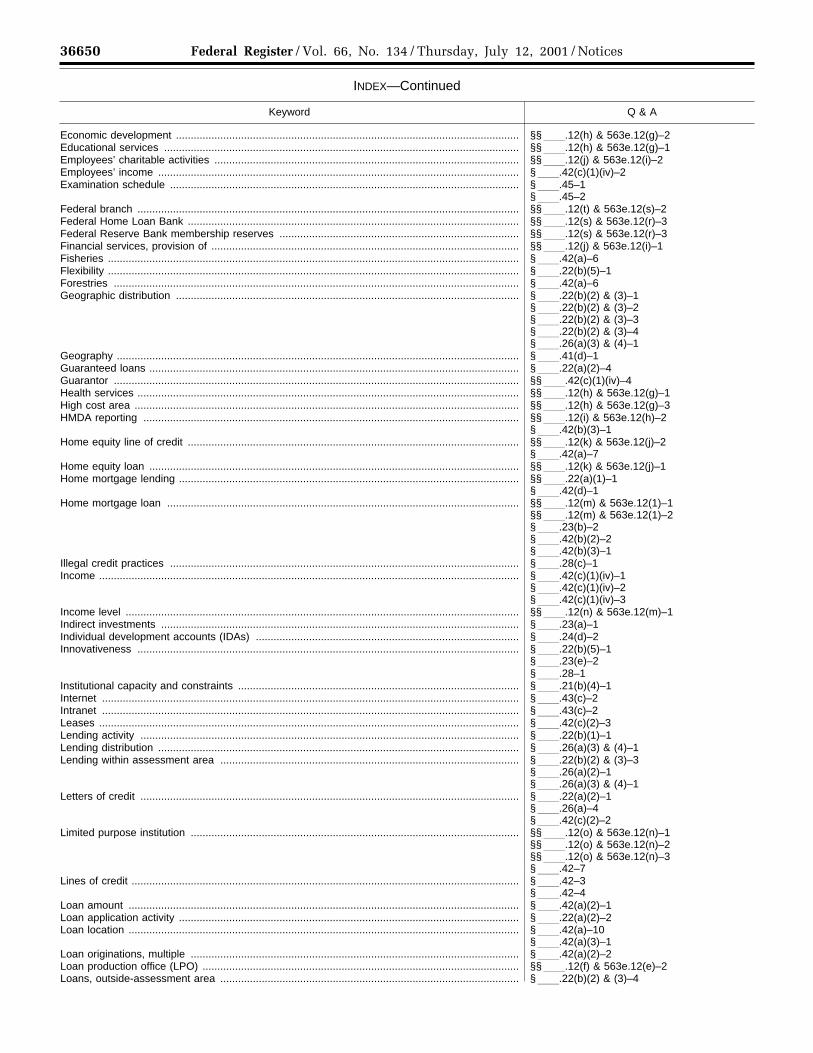

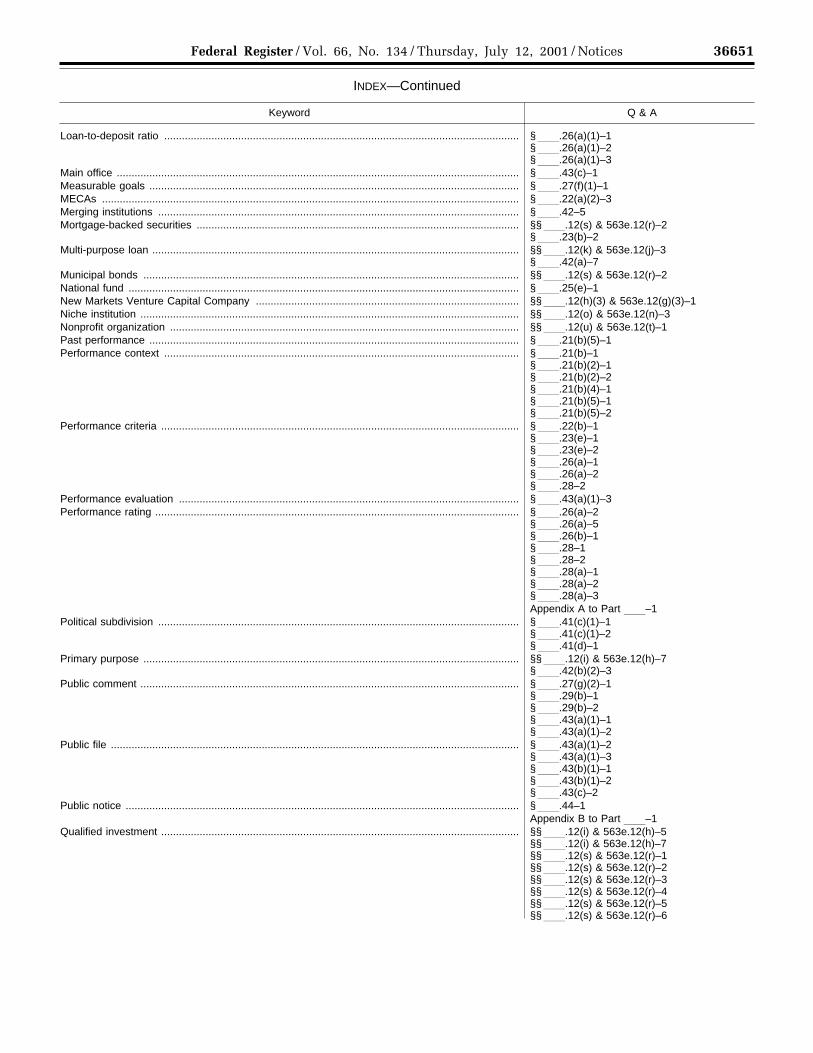

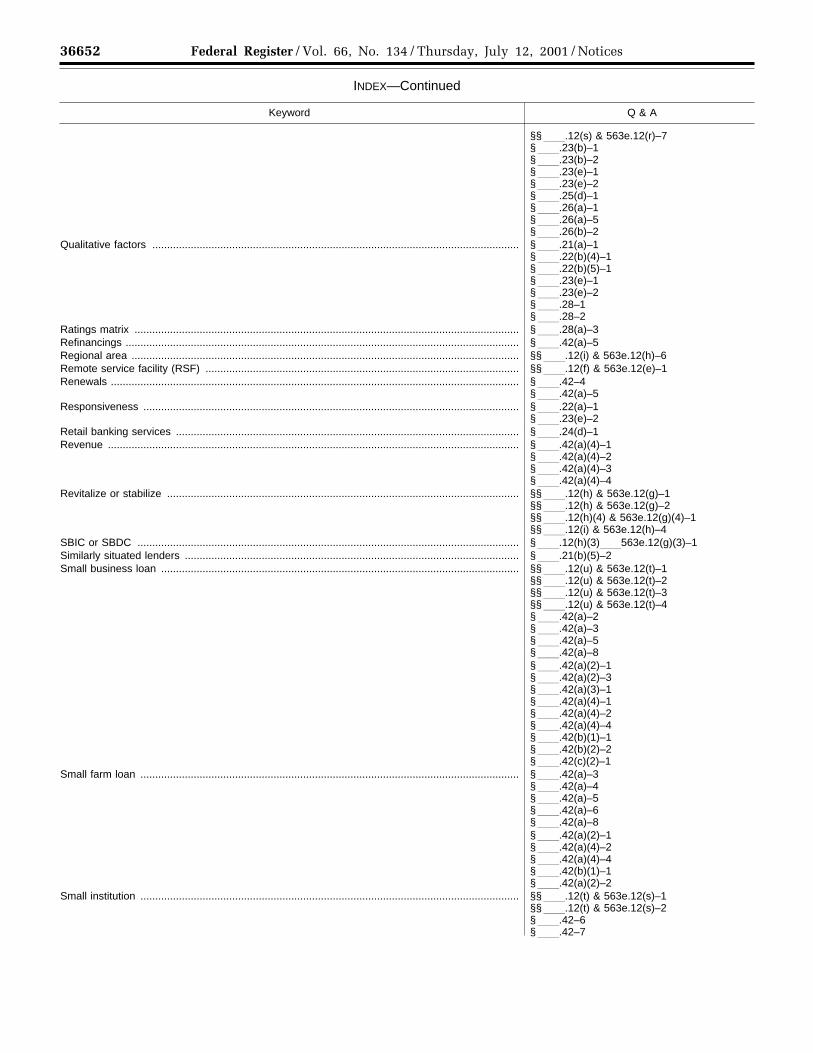

The Interagency Questions andAnswers has an index to aid readers inlocating specific information in thedocument. The index containskeywords, listed alphabetically, alongwith numerical indicators of questionsand answers that relate to that keyword.The list of questions and answersaddressing each keyword in the index isnot intended to be exhaustive. Wewelcome suggestions for additionalentries to the index. Further, when thisnew version of the InteragencyQuestions and Answers is madeavailable on the agencies’ and theFFIEC’s World Wide Web sites, theindex question and answer numberswill be linked by hypertext to thequestions and answers in the documentto facilitate quick reference to relevantinformation.

Questions and answers are groupedby the provision of the CRA regulationsthat they discuss and are presented inthe same order as the regulatoryprovisions. The Interagency Questionsand Answers employ an abbreviatedmethod to cite to the regulations.Because the regulations of the fouragencies are substantially identical,corresponding sections of the differentregulations usually bear the same suffix.Therefore, the Interagency Questionsand Answers typically cite only to thesuffix. For example, the small bankperformance standards for nationalbanks appear at 12 CFR 25.26; forFederal Reserve System member bankssupervised by the Board, they appear at12 CFR 228.26; for nonmember statebanks, at 12 CFR 345.26; and for thrifts,at 12 CFR 563e.26. Accordingly, thecitation in this document would be to§ll.26. In the few instances in whichthe suffix in one of the regulations isdifferent, the specific citation for thatregulation is provided. The questionnumbering system consists of theregulatory citation (as described above)and a number, connected by a dash. Forexample, the first question addressing§ll.21(a) would be identified as§ll.21(a)–1.

Adopting Question and Answer Re-Proposed in April 2000 and ConformingRevisions to One Question and Answer

We are adopting the revisions that were-proposed in April 2000 to thequestion and answer about whetherthere must be a direct benefit to aninstitution’s assessment area for anactivity to benefit the assessment area.We are also adopting conformingrevisions to another existing question

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00002 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36621Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

and answer to provide consistency withthe amended question and answer.

Must There Be Some Immediate orDirect Benefit to the Institution’sAssessment Area(s) To Satisfy theRegulations’ Requirement ThatQualified Investments and CommunityDevelopment Loans or Services Benefitan Institution’s Assessment Area(s) or aBroader Statewide or Regional AreaThat Includes the Assessment Area(s)?

The fifth question and answeraddressing §§ll.12(i) and 563e.12(h)(§§ll.12(i) & 563e.12(h)–5) addresseswhether there must be an immediate ordirect benefit to an institution’sassessment area(s) to satisfy theregulations’ requirement that qualifiedinvestments and communitydevelopment loans or services benefitan institution’s assessment area(s) or abroader statewide or regional area thatincludes the assessment area(s). Thisquestion and answer currently statesthat an institution’s assessment area(s)need not receive an immediate or directbenefit from the institution’s specificparticipation in the broader statewide orregional organization or activity,provided the purpose, mandate, orfunction of the organization or activityincludes serving geographies orindividuals located in the assessmentarea(s).

In May 1999, we first proposedrevising this question and answer topermit consideration of support forcommunity development organizationsor activities serving individuals orgeographies located somewhere in thebroader statewide or regional area thatincludes the institution’s assessmentarea. This consideration would be giveneven if the organization or activity didnot have the purpose, mandate orfunction of serving geographies orindividuals within the institution’sassessment area(s). Most commentersresponding to the 1999 proposalappeared to favor the original proposedrevision, as it would provide increasedflexibility in engaging in communitydevelopment activities. However, itappeared that a number of thosecommenters did not recognize therevised answer as an expansion ofexisting options for institutions toengage in community developmentactivities outside their assessmentarea(s). Therefore, we re-proposed forpublic comment a slightly revisedquestion and answer to ensure that thepublic understood that the revisedquestion and answer expands thecurrent guidance.

The question and answer, as it was re-proposed in April 2000, contained twoapproaches to determine whether

qualified investments and communitydevelopment loans or services benefitan institution’s assessment area(s) or abroader statewide or regional area thatincludes the institution’s assessmentarea(s). First, as the agencies havealways maintained, if an activitysupports an organization or programthat benefits the institution’s assessmentarea or a broader statewide or regionalarea that is larger than, but includes, theassessment area(s), the activity will beconsidered if the purpose, mandate, orfunction of the organization or activityincludes serving the assessment area(s).Second, if, in light of its performancecontext, an institution has adequatelyaddressed the community developmentneeds of its assessment area(s),examiners will consider communitydevelopment activities that benefit low-and moderate-income individuals orgeographies somewhere in the broaderstatewide or regional area that includesthe assessment area(s), even if thoseactivities do not have a purpose,mandate, or function of benefiting theinstitution’s assessment area(s).

The following example explained thetwo approaches. An institution islocated in Chicago. Its assessment areais the Chicago metropolitan area. Itscommunity development activitiesinclude loans, investments, and servicesin organizations and projects located inand benefiting Chicago, its assessmentarea. These activities would beconsidered under the first approach.The institution’s communitydevelopment activities also includeloans and investments in severalprojects that benefit the entire state ofIllinois, including Chicago. Theseactivities also are considered under thefirst approach. In addition, theinstitution participated in a communitydevelopment activity that benefits theentire Great Lakes region, including theChicago metropolitan area. This activitywould also be considered under the firstapproach. Assume that, afterconsidering its performance context,examiners have determined that theinstitution has adequately addressed thecommunity development needs of itsassessment area through loans,investments or services consideredunder the first approach. Examinersthen would also consider theinstitution’s investment in a communitydevelopment organization located inDecatur, IL, that will serve only theDecatur area—with no potential that itwill ever benefit Chicago, theinstitution’s assessment area. Decatur, ofcourse, is in the statewide area (Illinois)that includes the institution’sassessment area. The institution would

receive consideration for this activityunder the second approach.

The agencies received 14 letterscommenting on the proposed questionand answer. All of the commenters weregenerally in favor of the proposedquestion and answer. As one financialinstitution commenter stated, ‘‘Webelieve that community developmentorganizations and programs that operateon a local, statewide, or even multi-statebasis ultimately provide benefit to allsurrounding areas. Such initiatives helpstabilize these markets and provide aripple effect on neighboringgeographies. As the capacity of one areagrows, it is possible to leverage thateffort to build community developmentmomentum.’’

The agencies are adopting theamended question and answer,§§ll.12(i) & 563e.12(h)–5, as it wasproposed in April 2000.

What Is Meant by the Term ‘‘RegionalArea’’?

In addition, the agencies are alsoadopting the conforming amendment toquestion and answer, §§ll.12(i) &563e.12(h)–6, which was also proposedin April 2000. This revised question andanswer is necessary so that, in caseswhere an institution has alreadyadequately addressed the communitydevelopment needs of its assessmentarea(s), examiner discretion does notunduly impede the broader choice andjudgment permitted to institutions forperforming community developmentactivities in the relevant statewide orregional area. This conformingamendment clarifies that, if aninstitution has adequately addressed thecommunity development needs of itsassessment area(s), examiners willconsider its community developmentactivities that benefit geographies orindividuals located somewhere withinthe broader statewide or regional areathat includes the institution’sassessment area(s), even if thoseactivities do not benefit its assessmentarea(s).

New Questions and AnswersThe agencies are adopting six new

questions and answers, which arediscussed below.

Revitalize and Stabilize Low- andModerate-Income Areas

Financial institutions and examinershave asked us about the types ofactivities that are considered torevitalize and/or stabilize low- andmoderate-income areas. In response, theagencies are adopting a new questionand answer, §§ll.12(h)(4) &563e.12(g)(4)–1, which provides

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00003 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36622 Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

guidance about such activities. It statesthat activities that revitalize or stabilizea low- or moderate-income geographyare activities that help to attract andretain businesses and residents.Examiners will presume that an activityrevitalizes or stabilizes a low- ormoderate-income geography if theactivity has been approved by thegoverning board of an EnterpriseCommunity or Empowerment Zone(designated pursuant to 26 U.S.C. 1391)and is consistent with the board’sstrategic plan. They will make the samepresumption if the activity has receivedsimilar official designation as consistentwith a federal, state, local, or tribalgovernment plan for the revitalization orstabilization of the low- or moderate-income geography. To determinewhether other activities revitalize orstabilize a low- or moderate-incomegeography, examiners will evaluate theactivity’s actual impact on thegeography, if information about this isavailable. If not, examiners willdetermine whether the activity isconsistent with the community’s formalor informal plans for the revitalizationand stabilization of the low- ormoderate-income geography.

Types of Lending Activities That MayWarrant Favorable Consideration asActivities Responsive to the CreditNeeds of an Institution’s Community

Credit needs vary from community tocommunity. However, there are somelending activities that are likely to beresponsive in helping to meet the creditneeds of many communities. Theagencies are adopting a new questionand answer, §ll.22(a)–1, whichidentifies the following activities asbeing responsive to the needs of aninstitution’s assessment area:

• Providing loan programs thatinclude a financial educationcomponent about how to avoid lendingactivities that may be abusive orotherwise unsuitable;

• Establishing loan programs thatprovide small, unsecured consumerloans in a safe and sound manner (i.e.,based on the borrower’s ability to repay)and with reasonable terms;

• Offering lending programs, whichfeature reporting to consumer reportingagencies, that transition borrowers fromloans with higher interest rates and fees(based on credit risk) to lower-costloans, consistent with safe and soundlending practices. Reporting toconsumer reporting agencies allowsborrowers accessing these programs theopportunity to improve their credithistories and thereby improve theiraccess to competitive credit products.Examiners may consider favorably such

lending activities, which have featuresaugmenting the success andeffectiveness of the institution’s lendingprograms.

Indirect Community DevelopmentServices

The agencies are adopting a newquestion and answer, §ll.24(e)–1,that addresses the conditions underwhich an institution may receiveconsideration for communitydevelopment services offered byaffiliates or third parties. The guidancestates that, at an institution’s option, theagencies will consider servicesperformed by an affiliate or by a thirdparty on the institution’s behalf underthe service test if the services providedenable the institution to help meet thecredit needs of its community. Indirectservices that enhance an institution’sability to deliver credit products ordeposit services within its communityand that can be quantified may beconsidered under the service test ifthose services have not been consideredalready under the lending or investmenttest. For example, an institution thatcontracts with a communityorganization to provide homeownership counseling to low- andmoderate-income home buyers as part ofthe institution’s mortgage program mayreceive consideration for that indirectservice under the service test. Incontrast, donations to a communityorganization that offers financialservices to low- or moderate-incomeindividuals may be considered underthe investment test, but would not alsobe eligible for consideration under theservice test. Services performed by anaffiliate will be treated the same asaffiliate loans and investments made inthe institution’s assessment area andmay be considered if the service is notclaimed by any other institution.

Credit Card Banks’ ActivitiesThe agencies are adopting a new

question and answer, §ll.25(a)–1,that applies only to credit card banksthat are exempt from the definition of‘‘bank’’ in the Bank Holding CompanyAct (BHCA), as amended by theCompetitive Equality Banking Act of1987 (CEBA credit card banks). Thisnew guidance explains how a CEBAcredit card bank (if designated as alimited-purpose institution) can meet itscommunity’s credit needs withoutlosing its exemption from the definitionof ‘‘bank.’’ This guidance memorializesa letter issued in 1996 by staff at theBoard of Governors of the FederalReserve System to the president of theAssociation of Financial ServicesHolding Companies. The guidance

clarifies that, although the BHCArestricts CEBA credit card banks tocredit card operations, a CEBA creditcard bank can engage in communitydevelopment activities without losingits exemption under the BHCA. A CEBAcredit card bank could providecommunity development services andinvestments without engaging inoperations other than credit cardoperations. For example, the bank couldprovide credit card counseling, or thefinancial expertise of its executives, freeof charge, to community developmentorganizations. In addition, a CEBAcredit card bank could make qualifiedinvestments, as long as the investmentsmeet the guidelines for passive andnoncontrolling investments provided inthe BHCA and the Board’s Regulation Y.Finally, although a CEBA credit cardbank cannot make any loans other thancredit card loans, under §ll.25(d)(2)(community development test— indirectactivities), the bank could elect to havepart of its qualified passive andnoncontrolling investments in a third-party lending consortium considered ascommunity development lending,provided that the consortium’s loansotherwise meet the requirements forcommunity development lending. Whenassessing a CEBA credit card bank’sCRA performance under the communitydevelopment test, examiners will takeinto account the bank’s performancecontext. In particular, examiners willconsider the legal constraints imposedby the BHCA on the bank’s activities aspart of the bank’s performance contextin §ll.21(b)(4).

Effect of Evidence of Other Illegal CreditPractices

Section ll.28(c) of our regulationsstates that evidence of discriminatory orother illegal credit practices adverselyaffects the evaluation of an institution’sperformance. The agencies are adoptinga new question and answer addressingthis provision. The new question andanswer, §ll.28(c)–1, discusses whatis meant by ‘‘discriminatory or otherillegal credit practices.’’ It explains thatan institution engages in discriminatorycredit practices if it discourages ordiscriminates against credit applicantsor borrowers on a prohibited basis, inviolation, for example, of the FairHousing Act or the Equal CreditOpportunity Act (as implemented byRegulation B). Examples of other illegalcredit practices inconsistent withhelping to meet community credit needsinclude violations of:

• The Truth in Lending Act regardingrescission of certain mortgagetransactions and regarding disclosuresand certain loan term restrictions in

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00004 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36623Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

connection with credit transactions thatare subject to the Home Ownership andEquity Protection Act;

• The Real Estate SettlementProcedures Act regarding the giving andaccepting of referral fees, unearned feesor kickbacks in connection with certainmortgage transactions; and

• The Federal Trade Commission Actregarding unfair or deceptive acts orpractices.

Examiners will determine the effect ofevidence of illegal credit practices as setforth in examination procedures and§ll.28(c) of the regulations.

Violations of other provisions of theconsumer protection laws generally willnot adversely affect an institution’s CRArating, but may warrant the inclusion ofcomments in an institution’sperformance evaluation. Thesecomments may address the institution’spolicies, procedures, training programs,and internal assessment efforts.

Electronic Public Files

Some financial institutions haveinquired whether it is acceptable tomaintain the required public fileinformation electronically on anintranet or the Internet. The agenciesbelieve that an institution may keep allor part of its public file on an intranetor the Internet, provided that theinstitution maintains all of theinformation, either in paper orelectronic form, that is required in§ll.43 of the regulations. Aninstitution that opts to keep part or allof its public file on an intranet or theInternet must follow the rules in§ll.43(c)(1) and (2) as to whatinformation is required to be kept at amain office and at a branch. Theinstitution must also ensure that theinformation required to be maintainedat a main office and branch, if keptelectronically, can be readilydownloaded and printed for anymember of the public who requests ahard copy of the information.

The agencies are adopting a newquestion and answer, §ll.43(c)–2,which addresses maintaining publicfiles on an intranet or the Internet.

Revised Questions and AnswersThe agencies are revising eight

existing questions and answers, whichare discussed below.

New Markets Venture CapitalCompanies

The Consolidated Appropriations Actof 2001 (Pub. L. 106–554), enactedDecember 21, 2000, included the NewMarkets Venture Capital Program Act of2000. The New Markets Venture CapitalProgram, which is administered by the

Small Business Administration (SBA),allows the SBA to designate NewMarket Venture Capital companies(NMVCCs). NMVCCs are investmentfunds that will promote economicdevelopment and create wealth and jobopportunities in low-incomegeographies and among individualsliving in such areas through equity-typeinvestments in smaller enterpriseslocated in those low-incomegeographical areas.

Based on the statutory mandate forNMVCCs, the agencies will presumethat any loan to or lawful investment inNMVCCs will promote economicdevelopment. Therefore, we are revising§ll.12(h)(3)–1 to reflect thispresumption.

Reporting Loans With a BusinessPurpose That Are Secured byResidential Real Estate

The agencies are adopting revisions totwo existing questions and answers toaccommodate the difference intreatment between the Call Report andThrift Financial Report (TFR)instructions concerning loans securedby residential real estate that have abusiness purpose. Under the Call Reportinstructions, loans secured by nonfarmresidential real estate that are used tofinance small businesses must bereported as ‘‘loans secured by realestate’’ unless the security interest inthe nonfarm residential real estate istaken only as an abundance of caution.The TFR instructions, however, allowan institution to classify a loan thatmeets the definition of a mortgage loan,but that is used to finance smallbusinesses, as a mortgage loan or as anonmortgage loan according to thepurpose of the loan, at the option of thereporting institution. As a result,institutions that file Call Reports andthose that file TFRs may treat loanssecured by nonfarm residential realestate, but that are for the purpose offinancing a small business, in differentways.

The agencies are revising§§ll.12(u) & 563e.12(t)–3 and§ll.42(c)(2)–1 to be consistent withguidance provided in the Call Reportand TFR instructions. The agencies arebifurcating the answer to §§ll.12(u) &563e.12(t)–3 to account for the differenttreatment in the Call Report and TFRinstructions. The guidance states that,for banks filing Call Reports, loanssecured by nonfarm residential realestate to finance small businesses willtypically not be included as ‘‘loans tosmall businesses’’ for Call Reportpurposes, unless the security interest inthe property is taken only as anabundance of caution. The agencies

recognize that many small businessesare financed by loans that would nothave been made or would have beenmade on less favorable terms had theynot been secured by residential realestate. If these loans have a primarypurpose of community development, asdefined in the regulations, they may bereported as community developmentloans. Otherwise, at an institution’soption, the institution may collect andmaintain data separately concerningthese loans and request that the data beconsidered in its CRA evaluation as‘‘Other Secured Lines/Loans forPurposes of Small Business.’’

For institutions that file TFRs,depending on how a loan is classified,it is possible that a loan secured bynonfarm residential real estate thatfinances a small business will bereported as a ‘‘small business loan.’’Loans secured by nonfarm residentialreal estate to finance small businessesmay be reported as small business loansif they are reported on the TFR asnonmortgage, commercial loans.Otherwise, loans that meet thedefinition of mortgage loans, for TFRreporting purposes, may be classified asmortgage loans. These loans may bereported as community developmentloans, if appropriate, or collected as‘‘Other Secured Lines/Loans forPurposes of Small Business.’’

The guidance provided in§ll.42(c)(2)–1 is being revised to beapplicable only to banks that file CallReports. This question and answer isinapplicable to thrifts that file TFRs.The question and answer reiterates thatbanks that make loans to finance smallbusinesses, which are secured bynonfarm, residential real estate, and forwhich the security interest was nottaken only as an abundance of caution,may either report the loans ascommunity development loans, ifappropriate, or may collect andmaintain loan information as ‘‘OtherSecured Lines/Loans for Purposes ofSmall Business.’’

Clarification of §ll.21(b)(5)–1Addressing Assigned Ratings BeingAdversely Affected by Poor PastPerformance

The agencies are clarifying thewording of the answer to this question.We intend no substantive change.

Home Mortgage Loan Modification,Extension, and ConsolidationAgreements (MECAs)

In several states, financial institutionsuse MECAs as an alternative torefinancings for their customers.Existing guidance §ll.22(a)(2)–3states that an institution may receive

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00005 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36624 Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

consideration under CRA as ‘‘other loandata’’ for MECAs, in which it obtainsloans from other institutions withoutactually purchasing or refinancing theloans. The agencies are clarifying thisguidance to indicate that it applies onlyto home mortgage loans.

Reporting Lines of Credit

The agencies have received inquiriesfrom examiners and our institutionsabout how institutions should reportincreases to small business or smallfarm lines of credit once the total lineexceeds the $1 million or $500,000 limitfor reporting a loan to a small businessor a loan to a small farm, respectively,as described in the Call Report or TFRinstructions. Because the Call Reportand TFR no longer consider lines ofcredit that have exceeded the $1 millionor $500,000 thresholds as loans to smallbusinesses or loans to small farms,respectively, such lines would also nolonger be considered small business orsmall farm loans for CRA purposes.

The agencies are revising existingquestion and answer §ll.42–3 toclarify this view.

Clarification of §ll.42(a)–5Addressing Reporting Data onRefinancings and Renewals of SmallBusiness and Small Farm Loans

In the 2000 Interagency Questions andAnswers, the agencies adopted a revisedversion of §ll.42(a)–5, whichdiscusses collection and reporting ofdata on small business and farm loansthat are refinanced or renewed. The2000 guidance suggests that if a renewalof $15,000 and new money of $5,000 areprovided in connection with the sameloan to the same borrower, the twoamounts should be reported separatelyas two separate originations. In responseto several communications frominstitutions indicating that their datasystems may not allow such atransaction to be reported as twooriginations, the agencies are clarifyingthat institutions may report the twooriginations (the renewal and theincrease in the line) together as a singleorigination. In the example above, aninstitution may report one origination of$20,000.

We have also deleted from the answerto this question information that wasrelevant to data collected in the year2000 and reported in 2001. Because thisdata should have been reported byMarch 1, 2001, this portion of theanswer is no longer pertinent. Theremaining answer is applicablebeginning with data on small businessand small farm collected in 2000 andreported in 2001.

Updating §ll.42–4

Consistent with the deletion of theout-dated portion of the answer to§ll.42(a)–5, we are also deleting thepart of the answer to §ll.42 ‘‘ – thatwas relevant only to data that wascollected in 2000 and reported in 2001.The remaining answer is applicablebeginning with data about renewals oflines of credit collected in 2000 that willbe reported in 2001.

Small Business Regulatory EnforcementFairness Act of 1996 (SBREFA)

The SBREFA requires an agency, foreach rule for which it prepares a finalregulatory flexibility analysis, to publishone or more compliance guides to helpsmall entities understand how tocomply with the rule.

Pursuant to section 605(b) of theRegulatory Flexibility Act, the agenciescertified that their proposed CRA rulewould not have a significant economicimpact on a substantial number of smallentities and invited public comments onthat determination. See 58 FR 67478(Dec. 21, 1993); 59 FR 51250 (Oct. 7,1994). In response to public comment,the agencies voluntarily prepared a finalregulatory flexibility analysis for thejoint final rule, although the analysiswas not required because it supportedthe agencies’ earlier certificationregarding the proposed rule. Because aregulatory flexibility analysis was notrequired, section 212 of the SBREFAdoes not apply to the final CRA rule.However, in their continuing efforts toprovide clear, understandableregulations and to comply with thespirit of the SBREFA, the agencies havecompiled the Interagency Questions andAnswers. The Interagency Questionsand Answers serve the same purpose asthe compliance guide described in theSBREFA by providing guidance on avariety of issues of particular concern tosmall banks and thrifts.

The text of the Interagency Questionsand Answers follows:

Interagency Questions and AnswersRegarding Community Reinvestment

§ll.11—Authority, Purposes, andScope

§ll.11(c) Scope

§§ll.11(c)(3) & 563e.11(c)(2) CertainSpecial Purpose Institutions

§§ll.11(c)(3) & 563e.11(c)(2)–1: Isthe list of special purpose institutionsexclusive?

A1. No, there may be other examplesof special purpose institutions. Theseinstitutions engage in specializedactivities that do not involve grantingcredit to the public in the ordinary

course of business. Special purposeinstitutions typically serve ascorrespondent banks, trust companies,or clearing agents or engage only inspecialized services, such as cashmanagement controlled disbursementservices. A financial institution,however, does not become a specialpurpose institution merely by ceasing tomake loans and, instead, makinginvestments and providing other retailbanking services.

§ll.11(c)(3) & 563e.11(c)(2)–2: Tobe a special purpose institution, mustan institution limit its activities in itscharter?

A2. No. A special purpose institutionmay, but is not required to, limit thescope of its activities in its charter,articles of association or other corporateorganizational documents. Aninstitution that does not have legallimitations on its activities, but hasvoluntarily limited its activities,however, would no longer be exemptfrom Community Reinvestment Act(CRA) requirements if it subsequentlyengaged in activities that involvegranting credit to the public in theordinary course of business. Aninstitution that believes it is exemptfrom CRA as a special purposeinstitution should seek confirmation ofthis status from its supervisory agency.

§ll.12—Definitions

§ll.12(a) Affiliate

§ll.12(a)–1: Does the definition of‘‘affiliate’’ include subsidiaries of aninstitution?

A1. Yes, ‘‘affiliate’’ includes anycompany that controls, is controlled by,or is under common control withanother company. An institution’ssubsidiary is controlled by theinstitution and is, therefore, an affiliate.

§§ll.12(f) & 563e.12(e) Branch

§§ll.12(f)–563e.12(e) & 1: Do thedefinitions of ‘‘branch,’’ ‘‘automatedteller machine (ATM),’’ and ‘‘remoteservice facility (RSF)’’ include mobilebranches, ATMs, and RSFs?

A1. Yes. Staffed mobile offices thatare authorized as branches areconsidered ‘‘branches’’ and mobileATMs and RSFs are considered ‘‘ATMs’’and ‘‘RSFs.’’

§§ll.12(f) & 563e.12(e)–2: Are loanproduction offices (LPOs) branches forpurposes of the CRA?

A2. LPOs and other offices are not‘‘branches’’ unless they are authorizedas branches of the institution throughthe regulatory approval process of theinstitution’s supervisory agency.

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00006 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36625Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

§§ll.12(h)–563e.12(g) CommunityDevelopment

§§ll.12(h) & 563e.12(g)–1: Arecommunity development activitieslimited to those that promote economicdevelopment?

A1. No. Although the definition of‘‘community development’’ includesactivities that promote economicdevelopment by financing smallbusinesses or farms, the rule does notlimit community development loansand services and qualified investmentsto those activities. Communitydevelopment also includes community-or tribal-based child care, educational,health, or social services targeted tolow- or moderate-income persons,affordable housing for low- or moderate-income individuals, and activities thatrevitalize or stabilize low- or moderate-income areas.

§§ll.12(h) & 563e.12(g)–2: Must acommunity development activity occurinside a low- or moderate-income areain order for an institution to receiveCRA consideration for the activity?

A2. No. Community developmentincludes activities outside of low- andmoderate-income areas that provideaffordable housing for, or communityservices targeted to, low- or moderate-income individuals and activities thatpromote economic development byfinancing small businesses and farms.Activities that stabilize or revitalizeparticular low- or moderate-incomeareas (including by creating, retaining,or improving jobs for low- or moderate-income persons) also qualify ascommunity development, even if theactivities are not located in these low-or moderate-income areas. One exampleis financing a supermarket that serves asan anchor store in a small strip malllocated at the edge of a middle-incomearea, if the mall stabilizes the adjacentlow-income community by providingneeded shopping services that are nototherwise available in the low-incomecommunity.

§§ll.12(h) & 563e.12(g)–3: Does theregulation provide flexibility inconsidering performance in high-costareas?

A3. Yes, the flexibility of theperformance standards allowsexaminers to account in theirevaluations for conditions in high-costareas. Examiners consider lending andservices to individuals and geographiesof all income levels and businesses ofall sizes and revenues. In addition, theflexibility in the requirement thatcommunity development loans,community development services, andqualified investments have as their‘‘primary’’ purpose community

development allows examiners toaccount for conditions in high-costareas. For example, examiners couldtake into account the fact that activitiesaddress a credit shortage among middle-income people or areas caused by thedisproportionately high cost of building,maintaining or acquiring a house whendetermining whether an institution’sloan to or investment in an organizationthat funds affordable housing formiddle-income people or areas, as wellas low- and moderate-income people orareas, has as its primary purposecommunity development.

§§ll.12(h)(1) & 563e.12(g)(1)Affordable Housing (IncludingMultifamily Rental Housing) for Low- orModerate-Income Individuals

§§ll.12(h)(1) & 563e.12(g)(1)–1:When determining whether a project is‘‘affordable housing for low- ormoderate-income individuals,’’ therebymeeting the definition of ‘‘communitydevelopment,’’ will it be sufficient to usea formula that relates the cost ofownership, rental or borrowing to theincome levels in the area as the onlyfactor, regardless of whether the users,likely users, or beneficiaries of thataffordable housing are low- ormoderate-income individuals?

A1. The concept of ‘‘affordablehousing’’ for low- or moderate-incomeindividuals does hinge on whether low-or moderate-income individuals benefit,or are likely to benefit, from thehousing. It would be inappropriate togive consideration to a project thatexclusively or predominately housesfamilies that are not low- or moderate-income simply because the rents orhousing prices are set according to aparticular formula.

For projects that do not yet haveoccupants, and for which the income ofthe potential occupants cannot bedetermined in advance, or in otherprojects where the income of occupantscannot be verified, examiners willreview factors such as demographic,economic and market data to determinethe likelihood that the housing will‘‘primarily’’ accommodate low- ormoderate-income individuals. Forexample, examiners may look at medianrents of the assessment area and theproject; the median home value of eitherthe assessment area, low- or moderate-income geographies or the project; thelow- or moderate-income population inthe area of the project; or the pastperformance record of theorganization(s) undertaking the project.Further, such a project could receiveconsideration if its express, bona fideintent, as stated, for example, in a

prospectus, loan proposal or communityaction plan, is community development.

§§ll.12(h)(3) & 563e.12(g)(3)Activities That Promote EconomicDevelopment by Financing Businessesor Farms That Meet Certain SizeEligibility Standards

§ll.12(h)(3) & 563e.12(g)(3)–1:‘‘Community development’’ includesactivities that promote economicdevelopment by financing businesses orfarms that meet certain size eligibilitystandards. Are all activities that financebusinesses and farms that meet thesesize eligibility standards considered tobe community development?

A1. No. To be considered as‘‘community development’’ under§§ll.12(h)(3) and 563e.12(g)(3), aloan, investment or service, whethermade directly or through anintermediary, must meet both a size testand a purpose test. An activity meetsthe size requirement if it financesentities that either meet the sizeeligibility standards of the SmallBusiness Administration’s DevelopmentCompany (SBDC) or Small BusinessInvestment Company (SBIC) programs,or have gross annual revenues of $1million or less. To meet the purposetest, the activity must promoteeconomic development. An activity isconsidered to promote economicdevelopment if it supports permanentjob creation, retention, and/orimprovement for persons who arecurrently low- or moderate-income, orsupports permanent job creation,retention, and/or improvement either inlow- or moderate-income geographies orin areas targeted for redevelopment byFederal, state, local or tribalgovernments. The agencies willpresume that any loan to or investmentin a SBDC, SBIC, or New MarketsVenture Capital Company promoteseconomic development.

In addition to their quantitativeassessment of the amount of a financialinstitution’s community developmentactivities, examiners must makequalitative assessments of aninstitution’s leadership in communitydevelopment matters and thecomplexity, responsiveness, and impactof the community developmentactivities of the institution. In reachinga conclusion about the impact of aninstitution’s community developmentactivities, examiners may, for example,determine that a loan to a smallbusiness in a low- or moderate-incomegeography that provides needed jobsand services in that area may have agreater impact and be more responsiveto the community credit needs thandoes a loan to a small business in the

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00007 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36626 Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

same geography that does not directlyprovide additional jobs or services tothe community.

§§ll.12(h)(4) & 563e.12(g)(4)Activities That Revitalize or StabilizeLow- or Moderate-Income Geographies

§ll.12(h)(4) & 563e.12(g)(4)–1:What are activities that revitalize orstabilize a low- or moderate-incomegeography?

A1. Activities that revitalize orstabilize a low- or moderate-incomegeography are activities that help toattract and retain businesses andresidents. Examiners will presume thatan activity revitalizes or stabilizes alow- or moderate-income geography ifthe activity has been approved by thegoverning board of an EnterpriseCommunity or Empowerment Zone(designated pursuant to 26 U.S.C. 1391)and is consistent with the board’sstrategic plan. They will make the samepresumption if the activity has receivedsimilar official designation as consistentwith a federal, state, local or tribalgovernment plan for the revitalization orstabilization of the geography. Todetermine whether other activitiesrevitalize or stabilize a low- ormoderate-income geography, examinerswill evaluate the activity’s actual impacton the geography, if information aboutthis is available. If not, examiners willdetermine whether the activity isconsistent with the community’s formalor informal plans for the revitalizationand stabilization of the low- ormoderate-income geography. For moreinformation on what activities revitalizeor stabilize a low- or moderate-incomegeography, see §§ll.12(h) &563e.12(g)–2 and §§ll.12(i) &563e.12(h)–4.

§§ll.12(i) & 563e.12(h) CommunityDevelopment Loan

§§ll.12(i) & 563e.12(h)–1: What areexamples of community developmentloans?

A1. Examples of communitydevelopment loans include, but are notlimited to, loans to:

• Borrowers for affordable housingrehabilitation and construction,including construction and permanentfinancing of multifamily rental propertyserving low- and moderate-incomepersons;

• Not-for-profit organizations servingprimarily low- and moderate-incomehousing or other communitydevelopment needs;

• Borrowers to construct orrehabilitate community facilities thatare located in low- and moderate-income areas or that serve primarilylow- and moderate-income individuals;

• Financial intermediaries includingCommunity Development FinancialInstitutions (CDFIs), CommunityDevelopment Corporations (CDCs),minority- and women-owned financialinstitutions, community loan funds orpools, and low-income or communitydevelopment credit unions thatprimarily lend or facilitate lending topromote community development.

• Local, state, and tribal governmentsfor community development activities;and

• Borrowers to finance environmentalclean-up or redevelopment of anindustrial site as part of an effort torevitalize the low- or moderate-incomecommunity in which the property islocated.

The rehabilitation and construction ofaffordable housing or communityfacilities, referred to above, may includethe abatement or remediation of, orother actions to correct, environmentalhazards, such as lead-based paint, thatare present in the housing, facilities, orsite.

§§ll.12(i) & 563e.12(h)–2: If a retailinstitution that is not required to reportunder the Home Mortgage DisclosureAct (HMDA) makes affordable homemortgage loans that would be HMDA-reportable home mortgage loans if itwere a reporting institution, or if a smallinstitution that is not required to collectand report loan data under CRA makessmall business and small farm loansand consumer loans that would becollected and/or reported if theinstitution were a large institution, maythe institution have these loansconsidered as community developmentloans?

A2. No. Although small institutionsare not required to report or collectinformation on small business and smallfarm loans and consumer loans, andsome institutions are not required toreport information about their homemortgage loans under HMDA, if theseinstitutions are retail institutions, theagencies will consider in their CRAevaluations the institutions’ originationsand purchases of loans that would havebeen collected or reported as smallbusiness, small farm, consumer or homemortgage loans, had the institution beena collecting and reporting institutionunder the CRA or the HMDA. Therefore,these loans will not be considered ascommunity development loans.Multifamily dwelling loans, however,may be considered as communitydevelopment loans as well as homemortgage loans. See also §ll.42(b)(2)–2.

§§ll.12(i) & 563e.12(h)–3: Dosecured credit cards or other credit cardprograms targeted to low- or moderate-

income individuals qualify ascommunity development loans?

A3. No. Credit cards issued to low- ormoderate-income individuals forhousehold, family, or other personalexpenditures, whether as part of aprogram targeted to such individuals orotherwise, do not qualify as communitydevelopment loans because they do nothave as their primary purpose any of theactivities included in the definition of‘‘community development.’’

§§ll.12(i) & 563e.12(h)–4: Theregulation indicates that communitydevelopment includes ‘‘activities thatrevitalize or stabilize low- or moderate-income geographies.’’ Do all loans in alow- to moderate-income geographyhave a stabilizing effect?

A4. No. Some loans may provide onlyindirect or short-term benefits to low- ormoderate-income individuals in a low-or moderate-income geography. Theseloans are not considered to have acommunity development purpose. Forexample, a loan for upper-incomehousing in a distressed area is notconsidered to have a communitydevelopment purpose simply because ofthe indirect benefit to low- or moderate-income persons from construction jobsor the increase in the local tax base thatsupports enhanced services to low- andmoderate-income area residents. On theother hand, a loan for an anchorbusiness in a distressed area (or anearby area), that employs or servesresidents of the area, and thus stabilizesthe area, may be considered to have acommunity development purpose. Forexample, in an underserved, distressedarea, a loan for a pharmacy thatemploys, and provides supplies to,residents of the area promotescommunity development.

§§ll.12(i) & 563e.12(h)–5: Mustthere be some immediate or directbenefit to the institution’s assessmentarea(s) to satisfy the regulations’requirement that qualified investmentsand community development loans orservices benefit an institution’sassessment area(s) or a broaderstatewide or regional area that includesthe institution’s assessment area(s)?

A5. No. The regulations recognize thatcommunity development organizationsand programs are efficient and effectiveways for institutions to promotecommunity development. Theseorganizations and programs oftenoperate on a statewide or even multi-state basis. Therefore, an institution’sactivity is considered a communitydevelopment loan or service or aqualified investment if it supports anorganization or activity that covers anarea that is larger than, but includes, theinstitution’s assessment area(s). The

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00008 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36627Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

institution’s assessment area(s) need notreceive an immediate or direct benefitfrom the institution’s specificparticipation in the broader organizationor activity, provided that the purpose,mandate, or function of the organizationor activity includes serving geographiesor individuals located within theinstitution’s assessment area(s).

In addition, a retail institution that,considering its performance context, hasadequately addressed the communitydevelopment needs of its assessmentarea(s) will receive consideration forcertain other community developmentactivities. These communitydevelopment activities must benefitgeographies or individuals locatedsomewhere within a broader statewideor regional area that includes theinstitution’s assessment area(s).Examiners will consider these activitieseven if they will not benefit theinstitution’s assessment area(s).

§§ll.12(i) & 563e.12(h)–6: What ismeant by the term ‘‘regional area’’?

A6. A ‘‘regional area’’ may be as smallas a city or county or as large as amultistate area. For example, the ‘‘mid-Atlantic states’’ may comprise a regionalarea.

Community development loans andservices and qualified investments tostatewide or regional organizations thathave a bona fide purpose, mandate, orfunction that includes serving thegeographies or individuals within theinstitution’s assessment area(s) will beconsidered as addressing assessmentarea needs. When examiners evaluatecommunity development loans andservices and qualified investments thatbenefit a regional area that includes theinstitution’s assessment area(s), theywill consider the institution’sperformance context as well as the sizeof the regional area and the actual orpotential benefit to the institution’sassessment area(s). With larger regionalareas, benefit to the institution’sassessment area(s) may be diffused and,thus less responsive to assessment areaneeds.

In addition, as long as an institutionhas adequately addressed thecommunity development needs of itsassessment area(s), it will also receiveconsideration for communitydevelopment activities that benefitgeographies or individuals locatedsomewhere within the broaderstatewide or regional area that includesthe institution’s assessment area(s), evenif those activities do not benefit itsassessment area(s).

§§ll.12(i) & 563e.12(h)–7: What ismeant by the term ‘‘primary purpose’’ asthat term is used to define whatconstitutes a community development

loan, a qualified investment or acommunity development service?

A7. A loan, investment or service hasas its primary purpose communitydevelopment when it is designed for theexpress purpose of revitalizing orstabilizing low-or moderate-incomeareas, providing affordable housing for,or community services targeted to, low-or moderate-income persons, orpromoting economic development byfinancing small businesses and farmsthat meet the requirements set forth in§§ll.12(h) or 563e.12(g). Todetermine whether an activity isdesigned for an express communitydevelopment purpose, the agenciesapply one of two approaches. First, if amajority of the dollars or beneficiaries ofthe activity are identifiable to one ormore of the enumerated communitydevelopment purposes, then the activitywill be considered to possess therequisite primary purpose.Alternatively, where the measurableportion of any benefit bestowed ordollars applied to the communitydevelopment purpose is less than amajority of the entire activity’s benefitsor dollar value, then the activity maystill be considered to possess therequisite primary purpose if (1) theexpress, bona fide intent of the activity,as stated, for example, in a prospectus,loan proposal, or community actionplan, is primarily one or more of theenumerated community developmentpurposes; (2) the activity is specificallystructured (given any relevant market orlegal constraints or performance contextfactors) to achieve the expressedcommunity development purpose; and(3) the activity accomplishes, or isreasonably certain to accomplish, thecommunity development purposeinvolved. The fact that an activityprovides indirect or short-term benefitsto low-or moderate-income persons doesnot make the activity communitydevelopment, nor does the merepresence of such indirect or short-termbenefits constitute a primary purpose ofcommunity development. Financialinstitutions that want examiners toconsider certain activities under eitherapproach should be prepared todemonstrate the activities’qualifications.

§§ll.12(j) & 563e.12(i) CommunityDevelopment Service

§§ll.12(j) & 563e.12(i)–1: Inaddition to meeting the definition of‘‘community development’’ in theregulation, community developmentservices must also be related to theprovision of financial services. What ismeant by ‘‘provision of financialservices’’?

A1. Providing financial servicesmeans providing services of the typegenerally provided by the financialservices industry. Providing financialservices often involves informingcommunity members about how to getor use credit or otherwise providingcredit services or information to thecommunity. For example, service on theboard of directors of an organizationthat promotes credit availability orfinances affordable housing is related tothe provision of financial services.Providing technical assistance aboutfinancial services to community-basedgroups, local or tribal governmentagencies, or intermediaries that help tomeet the credit needs of low-andmoderate-income individuals or smallbusinesses and farms is also providingfinancial services. By contrast, activitiesthat do not take advantage of theemployees’ financial expertise, such asneighborhood cleanups, do not involvethe provision of financial services.

§§ll.12(j) & 563e.12(i)–2: Arepersonal charitable activities providedby an institution’s employees ordirectors outside the ordinary course oftheir employment consideredcommunity development services?

A2. No. Services must be provided asa representative of the institution. Forexample, if a financial institution’sdirector, on her own time and not as arepresentative of the institution,volunteers one evening a week at a localcommunity development corporation’sfinancial counseling program, theinstitution may not consider thisactivity a community developmentservice.

§§ll.12(j) & 563e.12(i)–3: What areexamples of community developmentservices?

A3. Examples of communitydevelopment services include, but arenot limited to, the following:

• Providing technical assistance onfinancial matters to nonprofit, tribal orgovernment organizations serving low-and moderate-income housing oreconomic revitalization anddevelopment needs;

• Providing technical assistance onfinancial matters to small businesses orcommunity development organizations,including organizations and individualswho apply for loans or grants under theFederal Home Loan Banks’ AffordableHousing Program;

• Lending employees to providefinancial services for organizationsfacilitating affordable housingconstruction and rehabilitation ordevelopment of affordable housing;

• Providing credit counseling, home-buyer and home-maintenancecounseling, financial planning or other

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00009 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36628 Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

financial services education to promotecommunity development and affordablehousing;

• Establishing school savingsprograms and developing or teachingfinancial education curricula for low-ormoderate-income individuals;

• Providing electronic benefitstransfer and point of sale terminalsystems to improve access to financialservices, such as by decreasing costs, forlow- or moderate-income individuals;and

• Providing other financial serviceswith the primary purpose of communitydevelopment, such as low-cost bankaccounts, including ‘‘Electronic TransferAccounts’’ provided pursuant to theDebt Collection Improvement Act of1996, or free government check cashingthat increases access to financialservices for low- or moderate-incomeindividuals.

Examples of technical assistanceactivities that might be provided tocommunity development organizationsinclude:

• Serving on a loan reviewcommittee;

• Developing loan application andunderwriting standards;

• Developing loan processingsystems;

• Developing secondary marketvehicles or programs;

• Assisting in marketing financialservices, including development ofadvertising and promotions,publications, workshops andconferences;

• Furnishing financial servicestraining for staff and management;

• Contributing accounting/bookkeeping services; and

• Assisting in fund raising, includingsoliciting or arranging investments.

§§ll.12(k) & 563e.12(j) ConsumerLoan

§§ll.12(k) & 563e.12(j)–1: Arehome equity loans considered‘‘consumer loans’’?

A1. Home equity loans made forpurposes other than home purchase,home improvement or refinancing homepurchase or home improvement loansare consumer loans if they are extendedto one or more individuals forhousehold, family, or other personalexpenditures.

§§ll.12(k) & 563e.12(j)–2: May ahome equity line of credit be considereda ‘‘consumer loan’’ even if part of theline is for home improvement purposes?

A2. If the predominant purpose of theline is home improvement, the line mayonly be reported under HMDA and maynot be considered a consumer loan.However, the full amount of the line

may be considered a ‘‘consumer loan’’ ifits predominant purpose is forhousehold, family, or other personalexpenditures, and to a lesser extenthome improvement, and the full amountof the line has not been reported underHMDA. This is the case even thoughthere may be ‘‘double counting’’ becausepart of the line may also have beenreported under HMDA.

§§ll.12(k) & 563e.12(j)–3: Howshould an institution collect or reportinformation on loans the proceeds ofwhich will be used for multiplepurposes?

A3. If an institution makes a singleloan or provides a line of credit to acustomer to be used for both consumerand small business purposes, consistentwith the Call Report and TFRinstructions, the institution shoulddetermine the major (predominant)component of the loan or the credit lineand collect or report the entire loan orcredit line in accordance with theregulation’s specifications for that loantype.

§§ll.12(m) & 563e.12(l) HomeMortgage Loan

§§ll.12(m) & 563e.12(l)–1: Does theterm ‘‘home mortgage loan’’ includeloans other than ‘‘home purchaseloans’’?

A1. Yes. ‘‘Home mortgage loan’’includes a ‘‘home improvement loan’’ aswell as a ‘‘home purchase loan,’’ as bothterms are defined in the HMDAregulation, Regulation C, 12 CFR part203. This definition also includesmultifamily (five-or-more families)dwelling loans, loans for the purchase ofmanufactured homes, and refinancingsof home improvement and homepurchase loans.

§§ll.12(m) & 563e.12(l)–2: Somefinancial institutions broker homemortgage loans. They typically take theborrower’s application and performother settlement activities; however,they do not make the credit decision.The broker institutions may alsoinitially fund these mortgage loans, thenimmediately assign them to anotherlender. Because the broker institutiondoes not make the credit decision,under Regulation C (HMDA), they donot record the loans on their HMDA–LARs, even if they fund the loans. Mayan institution receive any considerationunder CRA for its home mortgage loanbrokerage activities?

A2. Yes. A financial institution thatfunds home mortgage loans butimmediately assigns the loans to thelender that made the credit decisionsmay present information about theseloans to examiners for considerationunder the lending test as ‘‘other loan

data.’’ Under Regulation C, the brokerinstitution does not record the loans onits HMDA–LAR because it does notmake the credit decisions, even if itfunds the loans. An institution electingto have these home mortgage loansconsidered must maintain informationabout all of the home mortgage loansthat it has funded in this way.Examiners will consider this other loandata using the same criteria by whichhome mortgage loans originated orpurchased by an institution areevaluated.

Institutions that do not providefunding but merely take applicationsand provide settlement services foranother lender that makes the creditdecisions will receive consideration forthis service as a retail banking service.Examiners will consider an institution’smortgage brokerage services whenevaluating the range of servicesprovided to low-, moderate-, middle-and upper-income geographies and thedegree to which the services are tailoredto meet the needs of those geographies.Alternatively, an institution’s mortgagebrokerage service may be considered acommunity development service if theprimary purpose of the service iscommunity development. An institutionwishing to have its mortgage brokerageservice considered as a communitydevelopment service must providesufficient information to substantiatethat its primary purpose is communitydevelopment and to establish the extentof the services provided.

§§ll.12(n) & 563e.12(m) IncomeLevel

§§ll.12(n) & 563e.12(m)–1: Wheredo institutions find income level datafor geographies and individuals?

A1. The income levels forgeographies, i.e., census tracts and blocknumbering areas, are derived fromCensus Bureau information and areupdated every ten years. Institutionsmay contact their regional CensusBureau office or the Census Bureau’sIncome Statistics Office at (301) 763–8576 to obtain income levels forgeographies. See Appendix A of theseInteragency Questions and Answers fora list of the regional Census Bureauoffices. The income levels forindividuals are derived frominformation calculated by theDepartment of Housing and UrbanDevelopment (HUD) and updatedannually. Institutions may contact HUDat (800) 245–2691 to request a copy of‘‘FY [year number, e.g., 1996] MedianFamily Incomes for States and theirMetropolitan and NonmetropolitanPortions.’’

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00010 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36629Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

Alternatively, institutions may obtaina list of the 1990 Census Bureau-calculated and the annually updatedHUD median family incomes formetropolitan statistical areas (MSAs)and statewide nonmetropolitan areas bycalling the Federal Financial InstitutionExamination Council’s (FFIEC’s) HMDAHelp Line at (202) 452–2016. A freecopy will be faxed to the caller throughthe ‘‘fax-back’’ system. Institutions mayalso call this number to have ‘‘faxed-back’’ an order form, from which theymay order a list providing the medianfamily income level, as a percentage ofthe appropriate MSA ornonmetropolitan median family income,of every census tract and blocknumbering area (BNA). This list costs$50. Institutions may also obtain the listof MSA and statewide nonmetropolitanarea median family incomes or an orderform through the FFIEC’s home page onthe Internet at <http://www.ffiec.gov>.

§§ll.12(o) & 563e.12(n) LimitedPurpose Institution

§§ll.12(o) & 563e.12(n)–1: WhatConstitutes a ‘‘Narrow Product Line’’ inthe Definition of ‘‘Limited PurposeInstitution’’?

A1. An institution offers a narrowproduct line by limiting its lendingactivities to a product line other than atraditional retail product line requiredto be evaluated under the lending test(i.e., home mortgage, small business,and small farm loans). Thus, aninstitution engaged only in makingcredit card or motor vehicle loans offersa narrow product line, while aninstitution limiting its lending activitiesto home mortgages is not offering anarrow product line.

§§ll.12(o) & 563e.12(n)–2: Whatfactors will the agencies consider todetermine whether an institution that, iflimited purpose, makes loans outside anarrow product line, or, if wholesale,engages in retail lending, will lose itslimited purpose or wholesaledesignation because of too much otherlending?

A2. Wholesale institutions mayengage in some retail lending withoutlosing their designation if this activity isincidental and done on anaccommodation basis. Similarly, limitedpurpose institutions continue to meetthe narrow product line requirement ifthey provide other types of loans on aninfrequent basis. In reviewing otherlending activities by these institutions,the agencies will consider the followingfactors:

• Is the other lending provided as anincident to the institution’s wholesalelending?

• Are the loans provided as anaccommodation to the institution’swholesale customers?

• Are the loans made onlyinfrequently to the limited purposeinstitution’s customers?

• Does only an insignificant portionof the institution’s total assets andincome result from the other lending?

• How significant a role does theinstitution play in providing that type(s)of loan(s) in the institution’s assessmentarea(s)?

• Does the institution hold itself outas offering that type(s) of loan(s)?

• Does the lending test or thecommunity development test present amore accurate picture of theinstitution’s CRA performance?

§§ll.12(o) & 563e.12(n)–3: Do‘‘niche institutions’’ qualify as limitedpurpose (or wholesale) institutions?

A3. Generally, no. Institutions that arein the business of lending to the public,but specialize in certain types of retailloans (for example, home mortgage orsmall business loans) to certain types ofborrowers (for example, to high-endincome level customers or tocorporations or partnerships of licensedprofessional practitioners) (‘‘nicheinstitutions’’) generally would notqualify as limited purpose (orwholesale) institutions.

§§ll.12(s) & 563e.12(r) QualifiedInvestment

§§ll.12(s) & 563e.12(r)–1: Does theCRA regulation provide authority forinstitutions to make investments?

A1. No. The CRA regulation does notprovide authority for institutions tomake investments that are not otherwiseallowed by Federal law.

§§ll.12(s) & 563e.12(r)–2: Aremortgage-backed securities ormunicipal bonds ‘‘qualifiedinvestments’’?

A2. As a general rule, mortgage-backed securities and municipal bondsare not qualified investments becausethey do not have as their primarypurpose community development, asdefined in the CRA regulations.Nonetheless, mortgage-backed securitiesor municipal bonds designed primarilyto finance community developmentgenerally are qualified investments.Municipal bonds or other securitieswith a primary purpose of communitydevelopment need not be housing-related. For example, a bond to fund acommunity facility or park or to providesewage services as part of a plan toredevelop a low-income neighborhoodis a qualified investment. Housing-related bonds or securities mustprimarily address affordable housing(including multifamily rental housing)

needs in order to qualify. See also§ll.23(b)–2.

§§ll.12(s) & 563e.12(r)–3: AreFederal Home Loan Bank stocks andmembership reserves with the FederalReserve Banks ‘‘qualified investments’’?

A3. No. Federal Home Loan Bank(FHLB) stock and membership reserveswith the Federal Reserve Banks do nothave a sufficient connection tocommunity development to be qualifiedinvestments. However, FHLB memberinstitutions may receive CRAconsideration for technical assistancethey provide on behalf of applicants andrecipients of funding from the FHLB’sAffordable Housing Program. See§§ll.12(j) & 563e.12(i)–3.

§§ll.12(s) & 563e.12(r)–4: What areexamples of qualified investments?

A4. Examples of qualifiedinvestments include, but are not limitedto, investments, grants, deposits orshares in or to:

• Financial intermediaries (including,Community Development FinancialInstitutions (CDFIs), CommunityDevelopment Corporations (CDCs),minority- and women-owned financialinstitutions, community loan funds, andlow-income or community developmentcredit unions) that primarily lend orfacilitate lending in low- and moderate-income areas or to low- and moderate-income individuals in order to promotecommunity development, such as aCDFI that promotes economicdevelopment on an Indian reservation;

• Organizations engaged in affordablehousing rehabilitation and construction,including multifamily rental housing;

• Organizations, including, forexample, Small Business InvestmentCompanies (SBICs) and specializedSBICs, that promote economicdevelopment by financing smallbusinesses;

• Facilities that promote communitydevelopment in low- and moderate-income areas for low- and moderate-income individuals, such as youthprograms, homeless centers, soupkitchens, health care facilities, batteredwomen’s centers, and alcohol and drugrecovery centers;

• Projects eligible for low-incomehousing tax credits;

• State and municipal obligations,such as revenue bonds, that specificallysupport affordable housing or othercommunity development;

• Not-for-profit organizations servinglow- and moderate-income housing orother community development needs,such as counseling for credit, home-ownership, home maintenance, andother financial services education; and

• Organizations supporting activitiesessential to the capacity of low- and

VerDate 11<MAY>2000 13:14 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00011 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm01 PsN: 12JYN2

36630 Federal Register / Vol. 66, No. 134 / Thursday, July 12, 2001 / Notices

moderate-income individuals orgeographies to utilize credit or tosustain economic development, such as,for example, day care operations and jobtraining programs that enable people towork.

§§ll.12(s) & 563e.12(r)–5: Will aninstitution receive consideration forcharitable contributions as ‘‘qualifiedinvestments’’?

A5. Yes, provided they have as theirprimary purpose communitydevelopment as defined in theregulations. A charitable contribution,whether in cash or an in-kindcontribution of property, is included inthe term ‘‘grant.’’ A qualified investmentis not disqualified because aninstitution receives favorable treatmentfor it (for example, as a tax deductionor credit) under the Internal RevenueCode.

§§ll.12(s) & 563e.12(r)–6: Aninstitution makes or participates in acommunity development loan. Theinstitution provided the loan at below-market interest rates or ‘‘bought down’’the interest rate to the borrower. Is thelost income resulting from the lowerinterest rate or buy-down a qualifiedinvestment?

A6. No. The agencies will, however,consider the innovativeness andcomplexity of the communitydevelopment loan within the bounds ofsafe and sound banking practices.

§§ll.12(s) & 563e.12(r)–7: Will theagencies consider as a qualifiedinvestment the wages or othercompensation of an employee ordirector who provides assistance to acommunity development organizationon behalf of the institution?

A7. No. However, the agencies willconsider donated labor of employees ordirectors of a financial institution in theservice test if the activity is acommunity development service.

§§ll.12(t) & 563e.12(s) SmallInstitution

§§ll.12(t) & 563e.12(s)–1: How arethe ‘‘total bank and thrift assets’’ of aholding company determined?

A1. ‘‘Total banking and thrift assets’’of a holding company are determined bycombining the total assets of all banksand/or thrifts that are majority-ownedby the holding company. An institutionis majority-owned if the holdingcompany directly or indirectly ownsmore than 50 percent of its outstandingvoting stock.

§§ll.12(t) & 563e.12(s)–2: How areFederal and State branch assets of aforeign bank calculated for purposes ofthe CRA?

A2. A Federal or State branch of aforeign bank is considered a small

institution if the Federal or State branchhas less than $250 million in assets andthe total assets of the foreign bank’s orits holding company’s U.S. bank andthrift subsidiaries that are subject to theCRA are less than $1 billion. Thiscalculation includes not only FDIC-insured bank and thrift subsidiaries, butalso the assets of any FDIC-insuredbranch of the foreign bank and theassets of any uninsured Federal or Statebranch (other than a limited branch ora Federal agency) of the foreign bankthat results from an acquisitiondescribed in section 5(a)(8) of theInternational Banking Act of 1978 (12U.S.C. § 3103(a)(8)).

§§ll.12(u) & 563e.12(t) SmallBusiness Loan

§§ll.12(u) & 563e.12(t)–1: Areloans to nonprofit organizationsconsidered small business loans or arethey considered communitydevelopment loans?

A1. To be considered a small businessloan, a loan must meet the definition of‘‘loan to small business’’ in theinstructions in the ‘‘ConsolidatedReports of Conditions and Income’’ (CallReport) and ‘‘Thrift Financial Reports’’(TFR). In general, a loan to a nonprofitorganization, for business or farmpurposes, where the loan is secured bynonfarm nonresidential property andthe original amount of the loan is $1million or less, if a business loan, or$500,000 or less, if a farm loan, wouldbe reported in the Call Report and TFRas a small business or small farm loan.If a loan to a nonprofit organization isreportable as a small business or smallfarm loan, it cannot also be consideredas a community development loan,except by a wholesale or limitedpurpose institution. Loans to nonprofitorganizations that are not small businessor small farm loans for Call Report andTFR purposes may be considered ascommunity development loans if theymeet the regulatory definition.

§§ll.12(u) & 563e.12(t)–2: Areloans secured by commercial real estateconsidered small business loans?

A2. Yes, depending on their principalamount. Small business loans includeloans secured by ‘‘nonfarmnonresidential properties,’’ as defined inthe Call Report and TFR, in amountsless than $1 million.

§§ll.12(u) & 563e.12(t)–3: Areloans secured by nonfarm residentialreal estate to finance small businesses‘‘small business loans’’?

A3. Applicable to banks filing CallReports: Typically not. Loans securedby nonfarm residential real estate thatare used to finance small businesses arenot included as ‘‘small business’’ loans

for Call Report purposes unless thesecurity interest in the nonfarmresidential real estate is taken only as anabundance of caution. (See Call ReportGlossary definition of ‘‘Loan Secured byReal Estate.’’) The agencies recognizethat many small businesses are financedby loans that would not have been madeor would have been made on lessfavorable terms had they not beensecured by residential real estate. Ifthese loans promote communitydevelopment, as defined in theregulation, they may be considered ascommunity development loans.Otherwise, at an institution’s option, theinstitution may collect and maintaindata separately concerning these loansand request that the data be consideredin its CRA evaluation as ‘‘Other SecuredLines/Loans for Purposes of SmallBusiness.’’

Applicable to institutions that fileTFRs: Possibly, depending how the loanis classified for TFR purposes. Loanssecured by nonfarm residential realestate to finance small businesses maybe included as small business loansonly if they are reported on the TFR asnonmortgage, commercial loans. (SeeTFR Q&A No. 62.) Otherwise, loans thatmeet the definition of mortgage loans,for TFR reporting purposes, may beclassified as mortgage loans.

§§ll.12(u) & 563e.12(t)–4: Arecredit cards issued to small businessesconsidered ‘‘small business loans’’?

A4. Credit cards issued to a smallbusiness or to individuals to be used,with the institution’s knowledge, asbusiness accounts are small businessloans if they meet the definitionalrequirements in the Call Report or TFRinstructions.

§§ll.12(w) & 563e.12(v) WholesaleInstitution

§§ll.12(w) & 563e.12(v)–1: Whatfactors will the agencies consider indetermining whether an institution is inthe business of extending homemortgage, small business, small farm, orconsumer loans to retail customers?

A1. The agencies will considerwhether:

• The institution holds itself out tothe retail public as providing suchloans; and

• The institution’s revenues fromextending such loans are significantwhen compared to its overalloperations.

A wholesale institution may makesome retail loans without losing itswholesale designation as describedabove in §§ll.12(o) & 563e.12(n)–2.

VerDate 11<MAY>2000 16:31 Jul 11, 2001 Jkt 194001 PO 00000 Frm 00012 Fmt 4701 Sfmt 4703 E:\FR\FM\12JYN2.SGM pfrm04 PsN: 12JYN2