Embed Size (px)

Citation preview

Interaction of Mortgages and Leases

Why would a mortgagee want possession of “income property” prior to foreclosure? To stop waste or to make repairs. To rent out the premises (if vacant) To intercept the rents and apply them to

the debt and repairs.

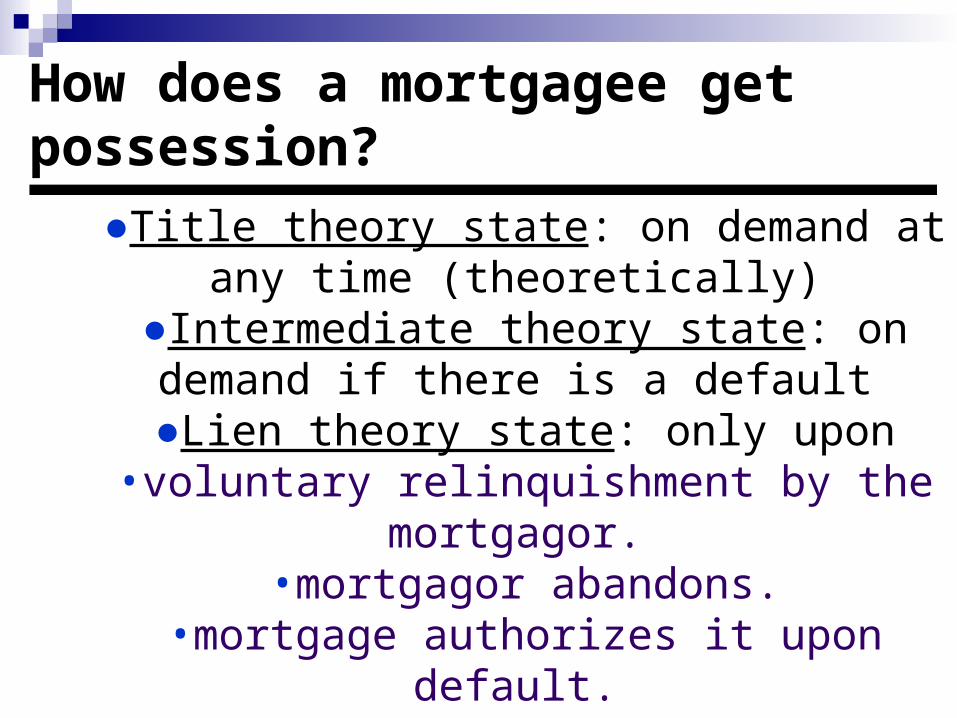

How does a mortgagee get possession?

●Title theory state: on demand at any time (theoretically)

●Intermediate theory state: on demand if there is a default

●Lien theory state: only upon•voluntary relinquishment by the mortgagor.

•mortgagor abandons.•mortgage authorizes it upon default.

•(Nearly all lien theory states accept this.)

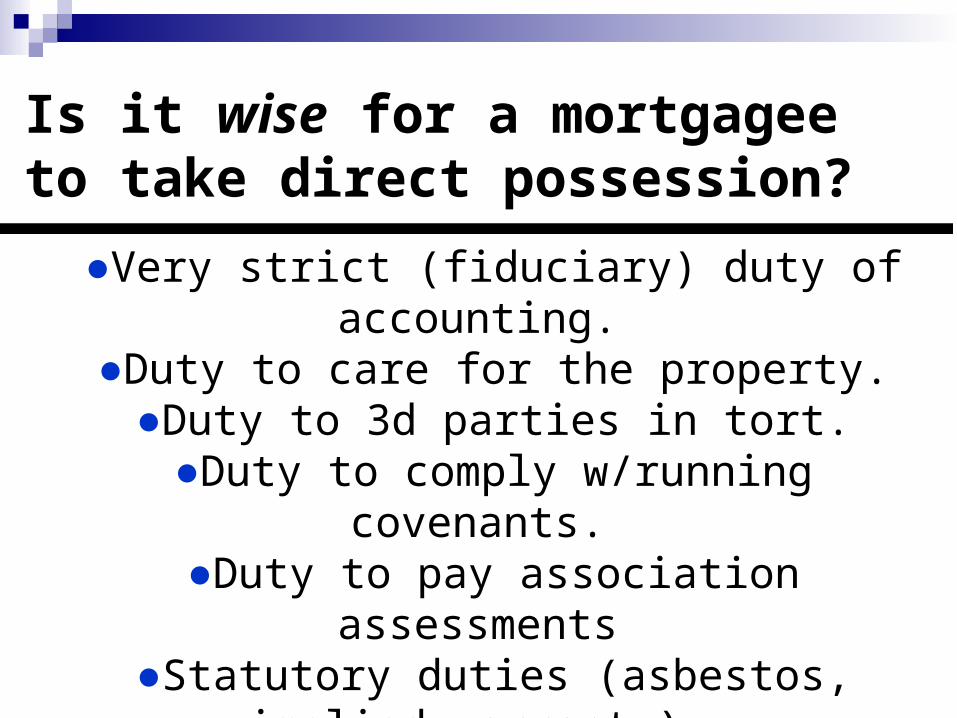

Is it wise for a mortgagee to take direct possession?

●Very strict (fiduciary) duty of accounting.●Duty to care for the property.

●Duty to 3d parties in tort.●Duty to comply w/running covenants.●Duty to pay association assessments

●Statutory duties (asbestos, implied warranty).

●Doing so may terminate junior leases (in “title theory” states).

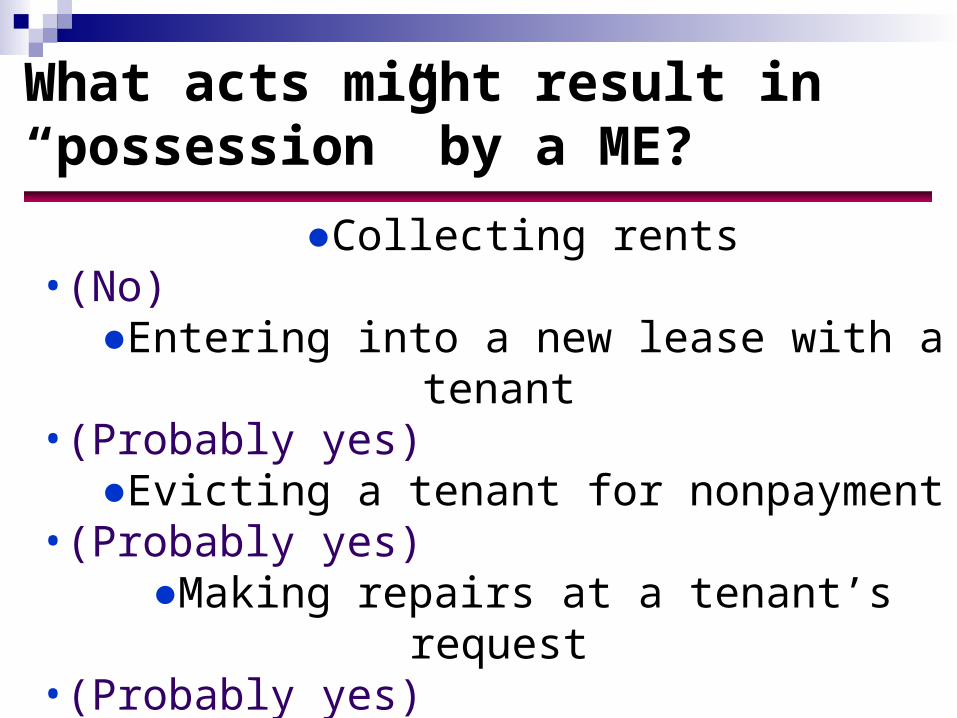

What acts might result in “possession” by a ME?

●Collecting rents• (No)

●Entering into a new lease with a tenant• (Probably yes)

●Evicting a tenant for nonpayment• (Probably yes)

●Making repairs at a tenant’s request• (Probably yes)

●Cultivating or harvesting crops• (Yes)

Most lenders are reluctant to become “mortgagees in

possession.” As an alternative, they usually prefer to have a receiver

appointed by a court.

What happens to existing leases when a mortgage is

foreclosed?

The answer depends on the relative priority of the

mortgage and the lease.

If lease has priority:

●Foreclosure purchaser has no right to terminate lease.

●Tenant has no right to terminate lease.●Tenant must attorn to foreclosure purchaser

(just as if MR had sold the property).

MR Tenant

MR ME Purch.Forecl.

Lease

Mortgage

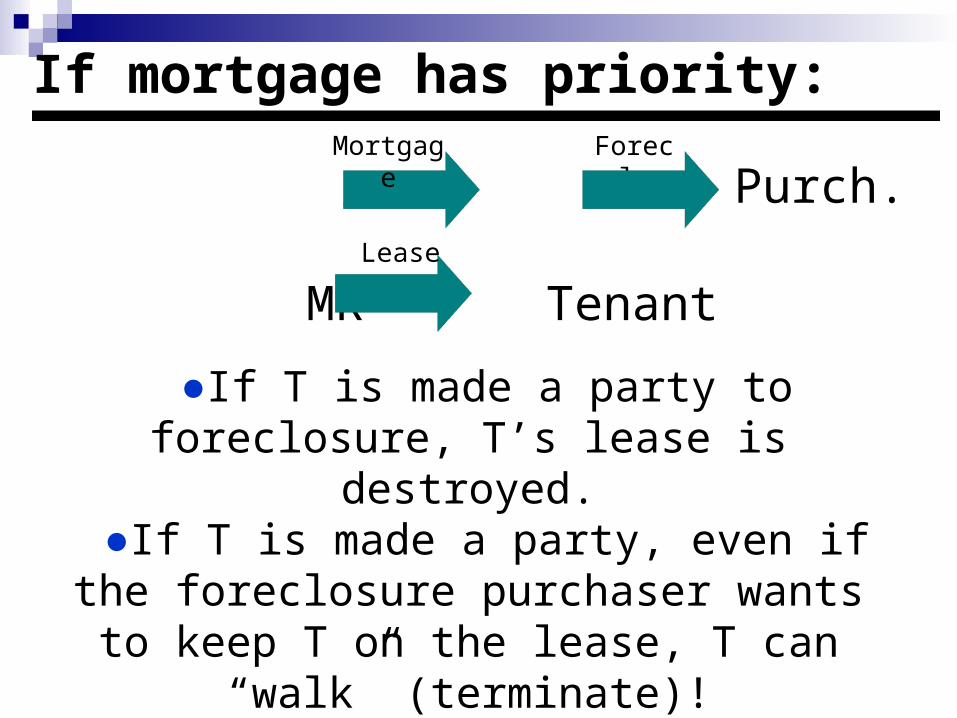

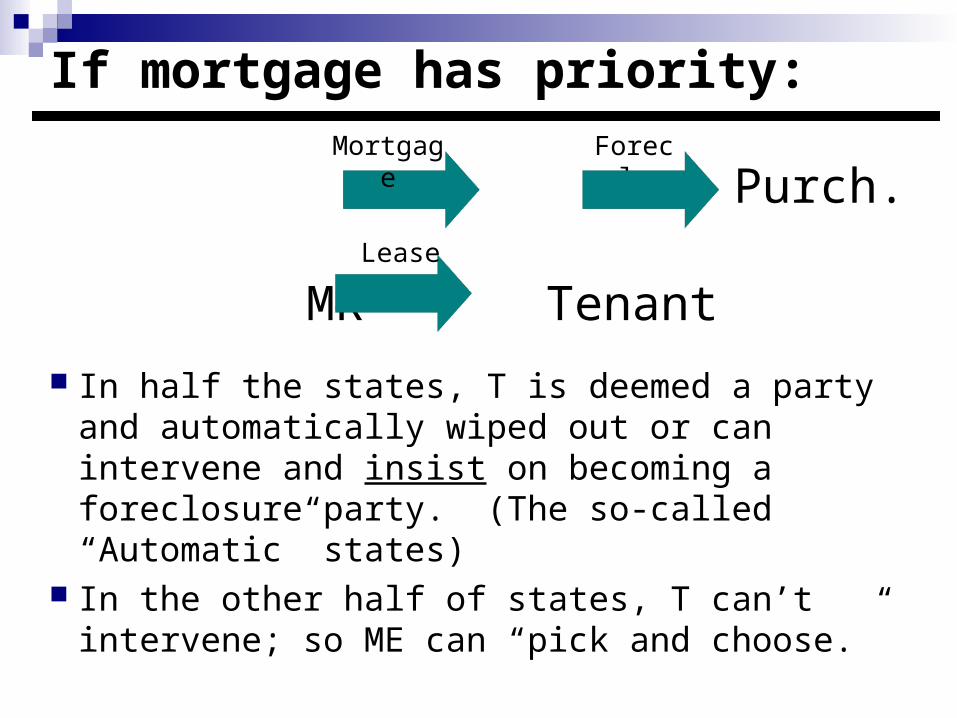

If mortgage has priority:

●If T is made a party to foreclosure, T’s lease is destroyed.

●If T is made a party, even if the foreclosure purchaser wants to keep T on the

lease, T can “walk” (terminate)!●Texas agrees: Med Center Bank v.

Fleetwood, 854 S.W.2d 278(Tex.App.-Austin,1993)

MR ME

MR Tenant

Forecl.

Lease

Mortgage

Purch.

If the tenant doesn’t want the lease terminated… Would the tenant have a claim against the

landlord-mortgagor for damages, for its failure to make the mortgage payments?

What theory would the tenant use? Texas denied such a tenant’s claim, where

the lease expressly stated that it was “subject to” existing mortgages. See HTM Restaurants, Inc. v. Goldman, Sachs & Co., 797 S.W.2d 326 (Tex.App.1990)

Was this correctly decided?

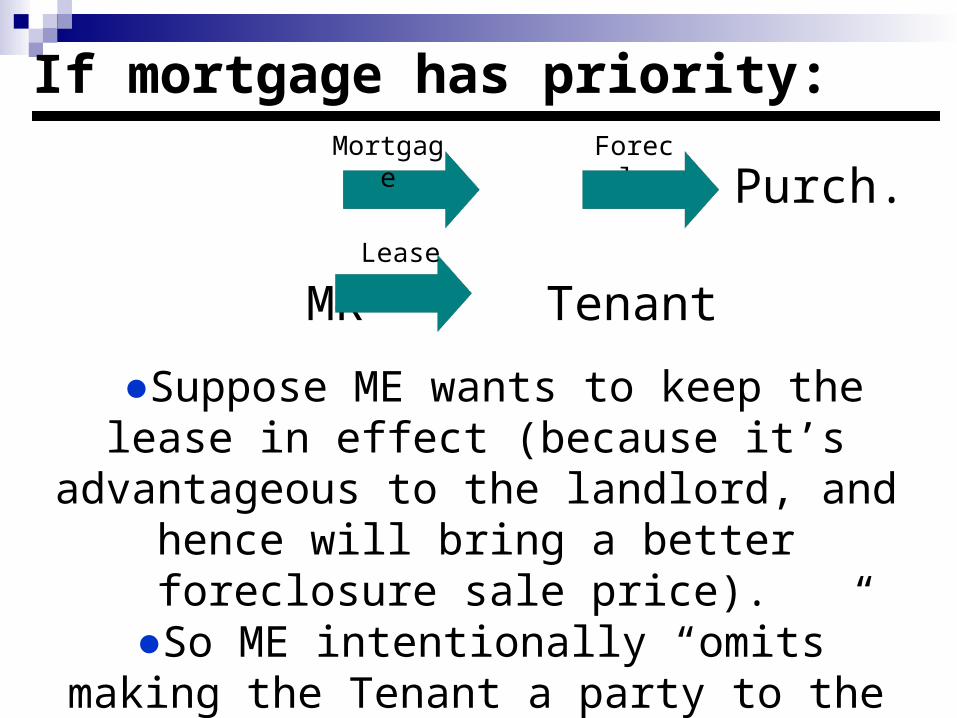

If mortgage has priority:

●Suppose ME wants to keep the lease in effect (because it’s advantageous to the landlord, and hence will bring a better

foreclosure sale price). ●So ME intentionally “omits” making the

Tenant a party to the foreclosure? Will this work to preserve the lease?

MR ME

MR Tenant

Forecl.

Purch.Lease

Mortgage

If mortgage has priority:

In half the states, T is deemed a party and automatically wiped out or can intervene and insist on becoming a foreclosure party. (The so-called “Automatic” states)

In the other half of states, T can’t intervene; so ME can “pick and choose.”

MR ME

MR Tenant

Forecl.

Purch.Lease

Mortgage

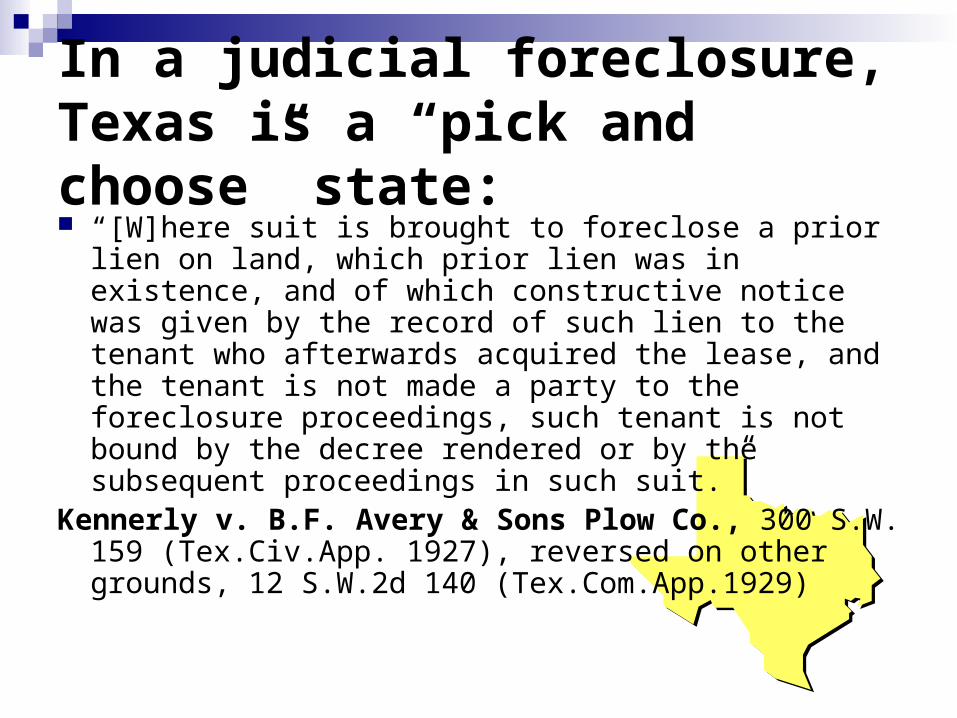

In a judicial foreclosure, Texas is a “pick and choose” state: “[W]here suit is brought to foreclose a prior lien on land,

which prior lien was in existence, and of which constructive notice was given by the record of such lien to the tenant who afterwards acquired the lease, and the tenant is not made a party to the foreclosure proceedings, such tenant is not bound by the decree rendered or by the subsequent proceedings in such suit.”

Kennerly v. B.F. Avery & Sons Plow Co., 300 S.W. 159 (Tex.Civ.App. 1927), reversed on other grounds, 12 S.W.2d 140 (Tex.Com.App.1929)

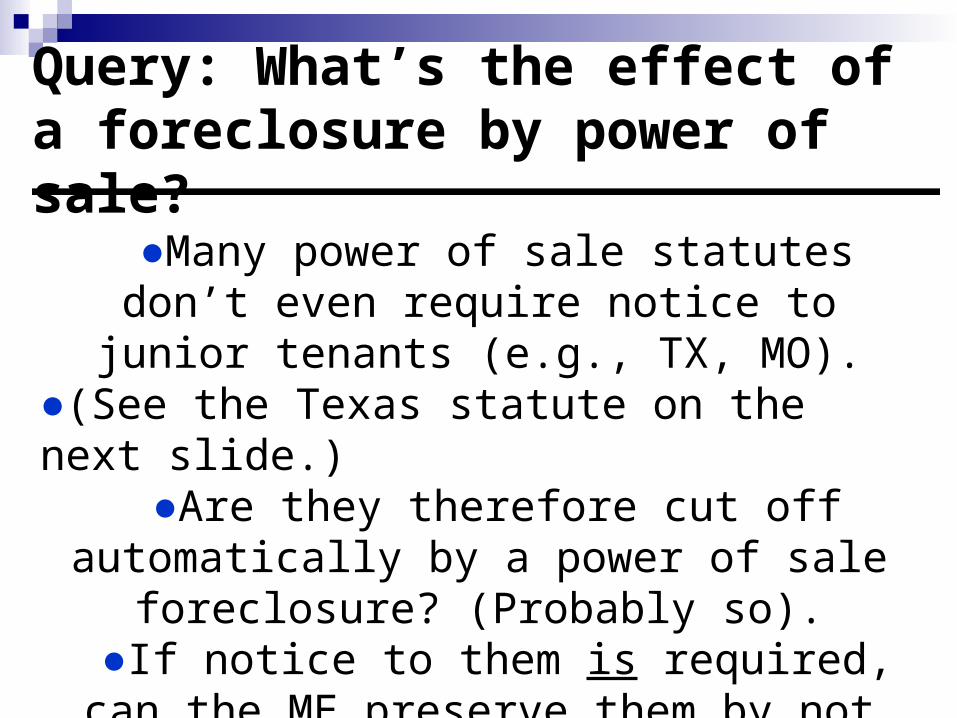

Query: What’s the effect of a foreclosure by power of sale?

●Many power of sale statutes don’t even require notice to junior tenants (e.g., TX, MO).●(See the Texas statute on the next slide.)

●Are they therefore cut off automatically by a power of sale foreclosure? (Probably so).

●If notice to them is required, can the ME preserve them by not giving them notice?●Or does that make the foreclosure void?

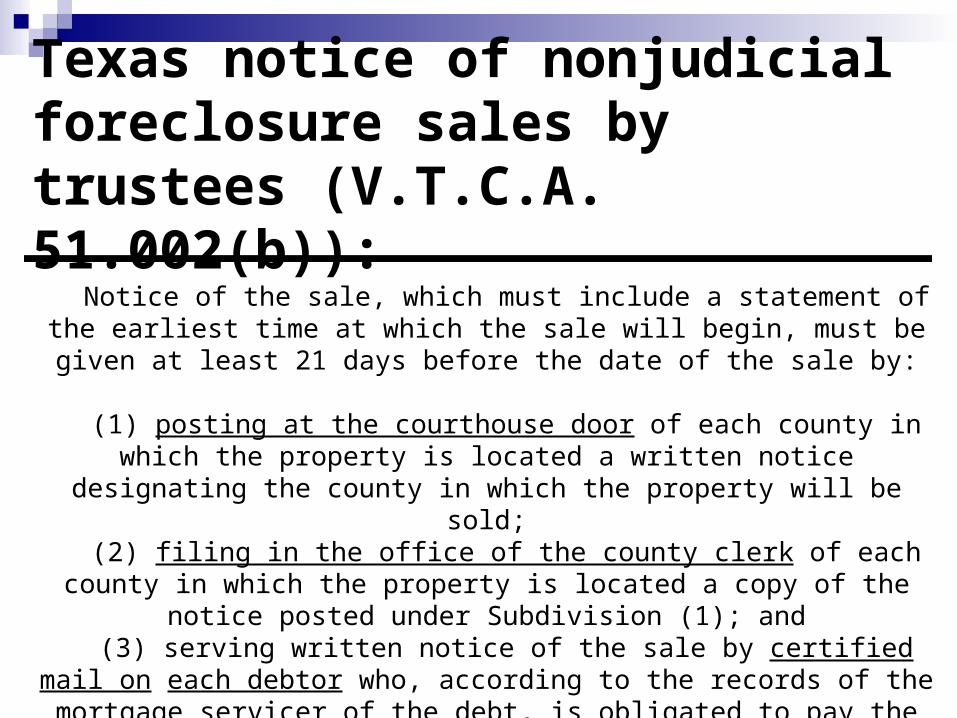

Texas notice of nonjudicial foreclosure sales by trustees (V.T.C.A. 51.002(b)):

Notice of the sale, which must include a statement of the earliest time at which the sale will begin, must be given at least 21 days before the date of

the sale by:

(1) posting at the courthouse door of each county in which the property is located a written notice designating the county in which the property will be

sold;(2) filing in the office of the county clerk of each county in which the

property is located a copy of the notice posted under Subdivision (1); and(3) serving written notice of the sale by certified mail on each debtor who,

according to the records of the mortgage servicer of the debt, is obligated to pay the debt.

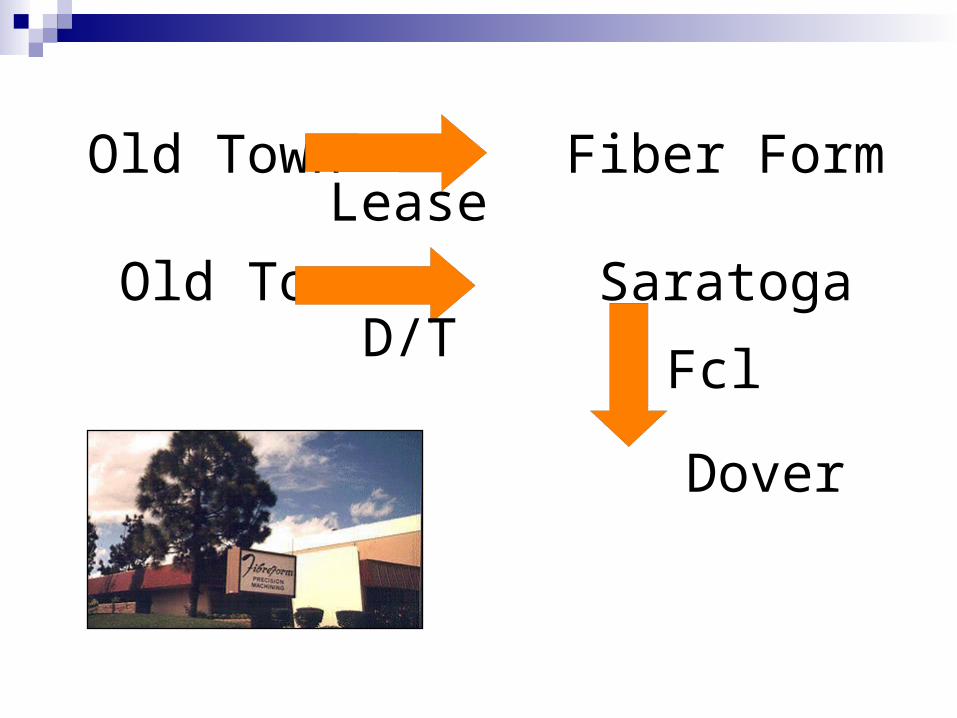

Old Town Fiber Form

Old Town Saratoga

Dover

Lease

D/TFcl

What would the priority between the lease and mortgage have been,

absent any lease clause?

What was the effect of the lease clause dealing with priority?

Priorities:

“Tenant agrees that this Lease shall be subordinate to any deeds

of trust that may hereafter be placed upon the premises.”

“Any beneficiary, at its option, may elect to have this Lease superior to

its deed of trust.”

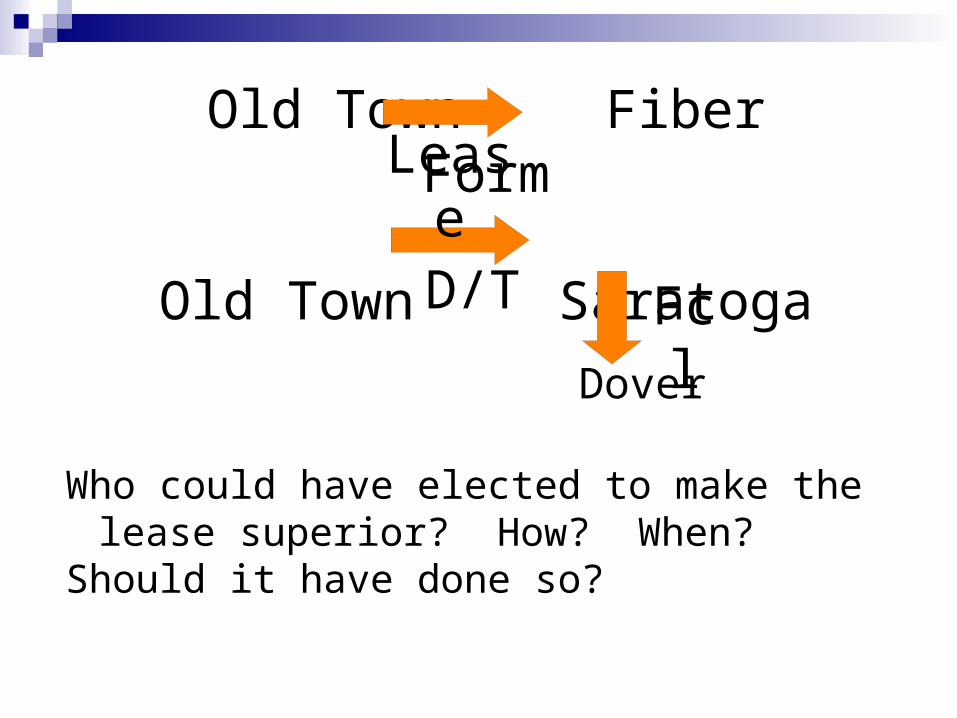

Old Town Fiber Form

Old Town Saratoga

Lease

D/T FclDover

Who could have elected to make the lease superior? How? When?

Should it have done so?

Old Town Fiber Form

Old Town Saratoga

Lease

D/T FclDover

Could Saratoga have preserved the lease by “omitting” FiberForm from the foreclosure?

Could they in a Texas D/T nonjudicial foreclosure? (Apparently not; there’s no mechanism for doing so.)

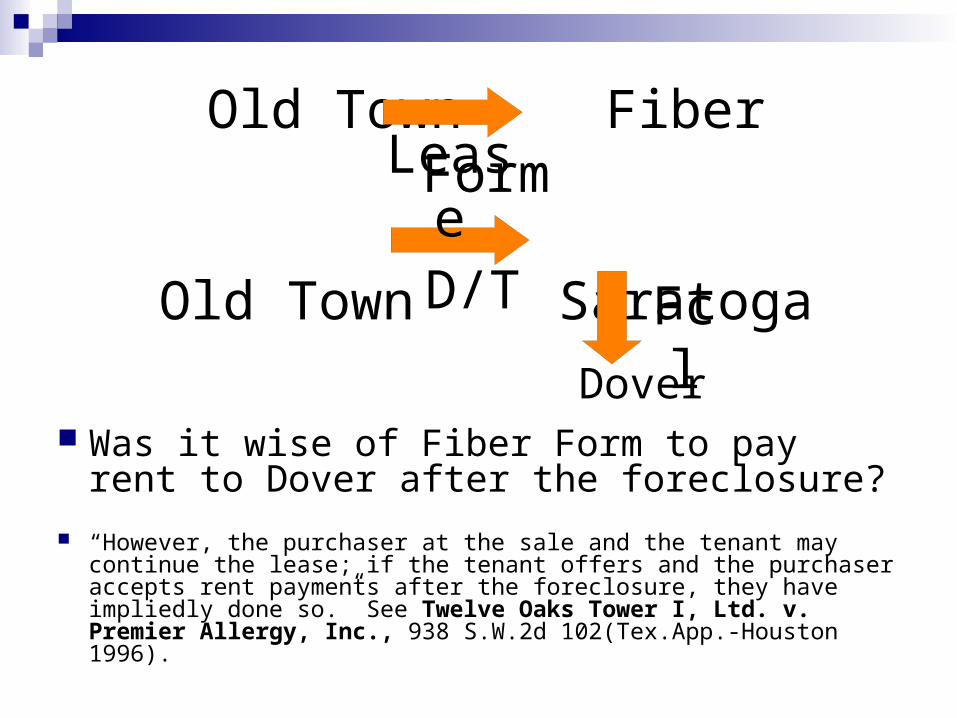

Old Town Fiber Form

Old Town Saratoga

Lease

D/T FclDover

Was it wise of Fiber Form to pay rent to Dover after the foreclosure?

“However, the purchaser at the sale and the tenant may continue the lease; if the tenant offers and the purchaser accepts rent payments after the foreclosure, they have impliedly done so.” See Twelve Oaks Tower I, Ltd. v. Premier Allergy, Inc., 938 S.W.2d 102(Tex.App.-Houston 1996).

Any of three different (but similar) types of clauses might have let Saratoga keep FiberForm’s lease…

“Optional unsubordination” (the actual case)(Could ME unsubordinate without a clause?

See Mortgages Restatement § 7.7) “Attornment” clause. “New Lease” clause.

Must the clause be in the lease? What about putting it in the mortgage?

Most printed form commercial leases contain one of these clauses. Why? They give the lender (existing or future) all the

“marbles.” Hence, they make the landlord’s interest highly

“financible.” But a powerful tenant would

never sign one of these forms!

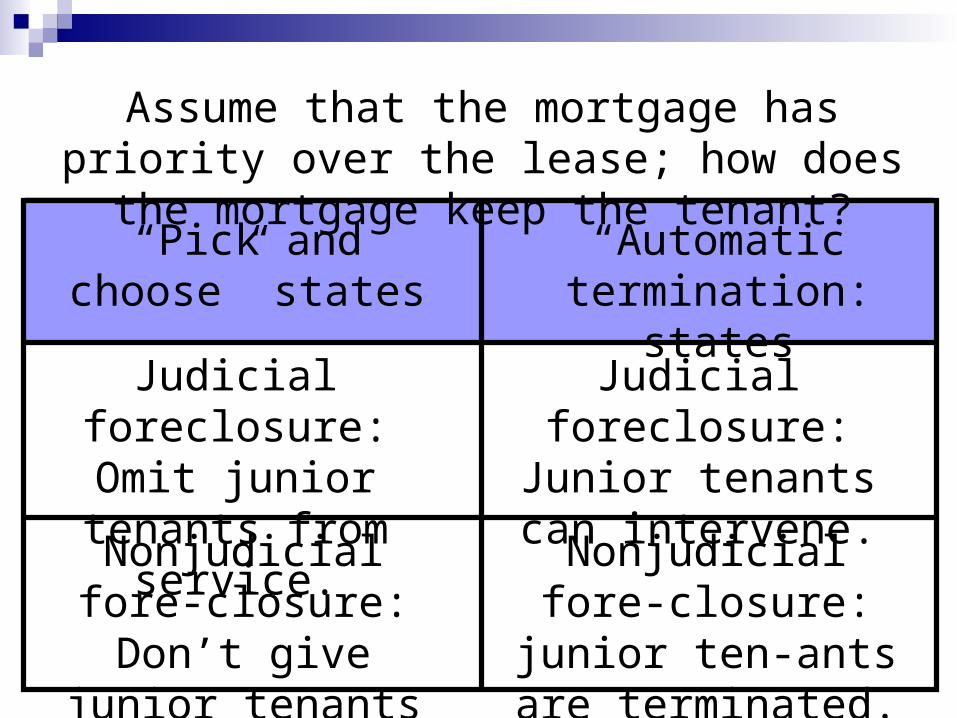

Assume that the mortgage has priority over the lease; how does the mortgage keep the tenant?

“Pick and choose” states

“Automatic termination: states

Judicial foreclosure: Omit junior tenants

from service.

Nonjudicial fore-closure: Don’t give

junior tenants notice

Judicial foreclosure: Junior tenants can

intervene.

Nonjudicial fore-closure: junior ten-

ants are terminated.

Assuming they have a choice, how do foreclosing mortgagees (and foreclosure purchasers) evaluate whether a lease should be preserved?

1. Characteristics of the tenant and the lease.

2. Debt service coverage ratio. 3. Estoppel statements from the tenants.

Characteristics of the tenant and the lease: T’s financial condition & rent payment record Rent and rent escalation clauses Landlord’s financial duties Casualty loss/rebuilding Renewals & extensions Exclusive clauses Assignment/subletting rights Duty to operate (“lights on”)

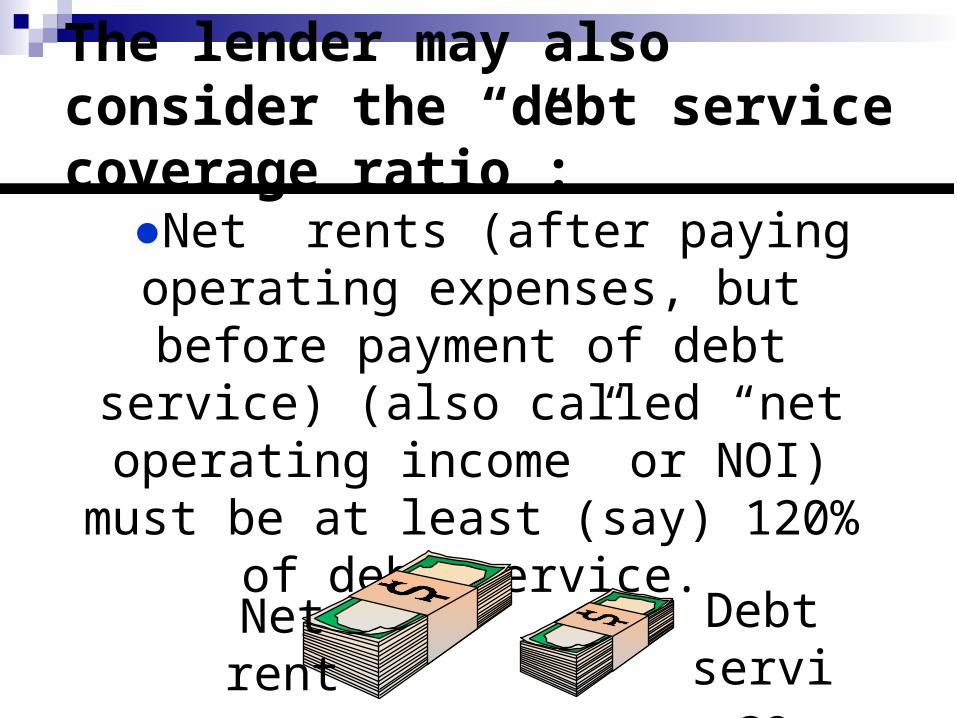

The lender may also consider the “debt service coverage ratio”:

●Net rents (after paying operating expenses, but before payment of debt

service) (also called “net operating income” or NOI) must be at least (say)

120% of debt service.

Netrent

Debtservice

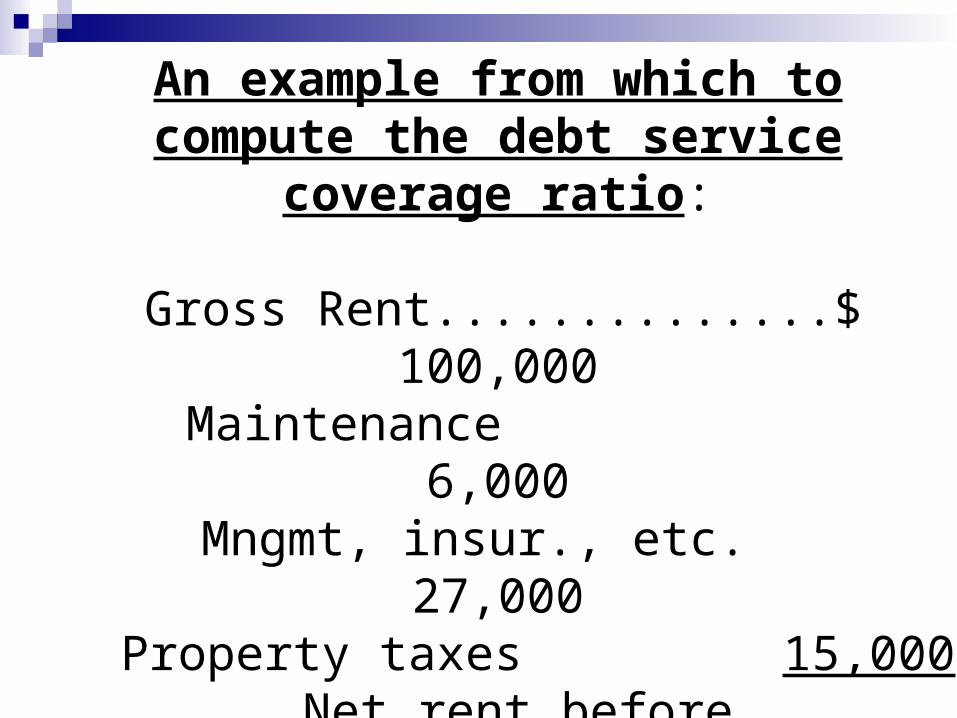

An example from which to compute the debt service coverage ratio:

Gross Rent..............$ 100,000Maintenance 6,000Mngmt, insur., etc. 27,000Property taxes 15,000

Net rent before debt service (NOI)..$ 52,000Debt service.............$ 40,000Net cash flow............$ 12,000

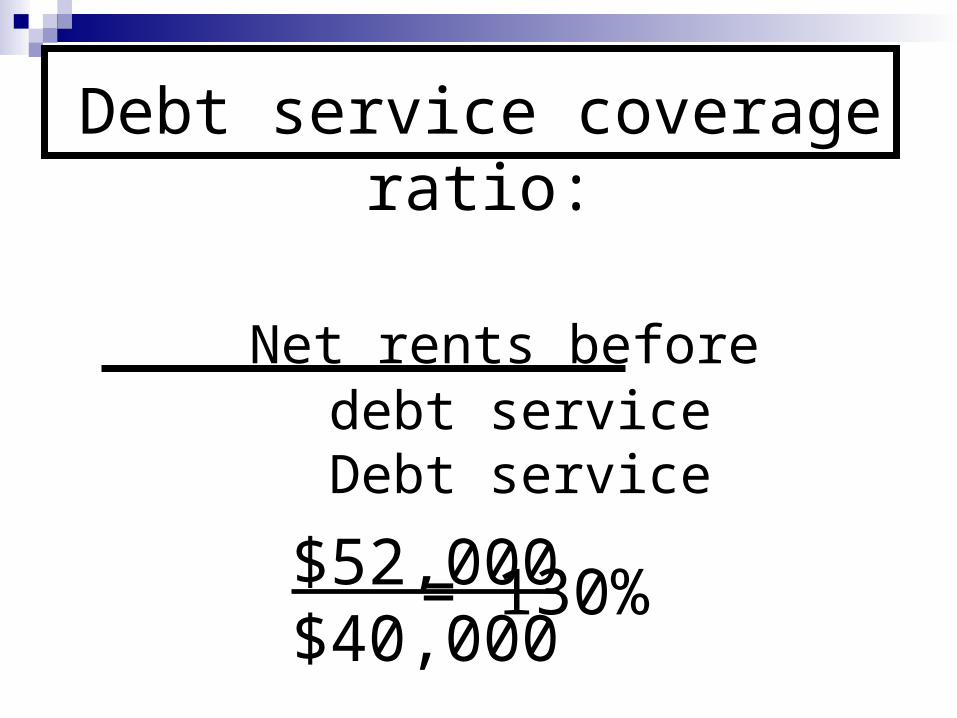

Debt service coverage ratio:

Net rents before debt serviceDebt service

$52,000$40,000

= 130%