Embed Size (px)

Citation preview

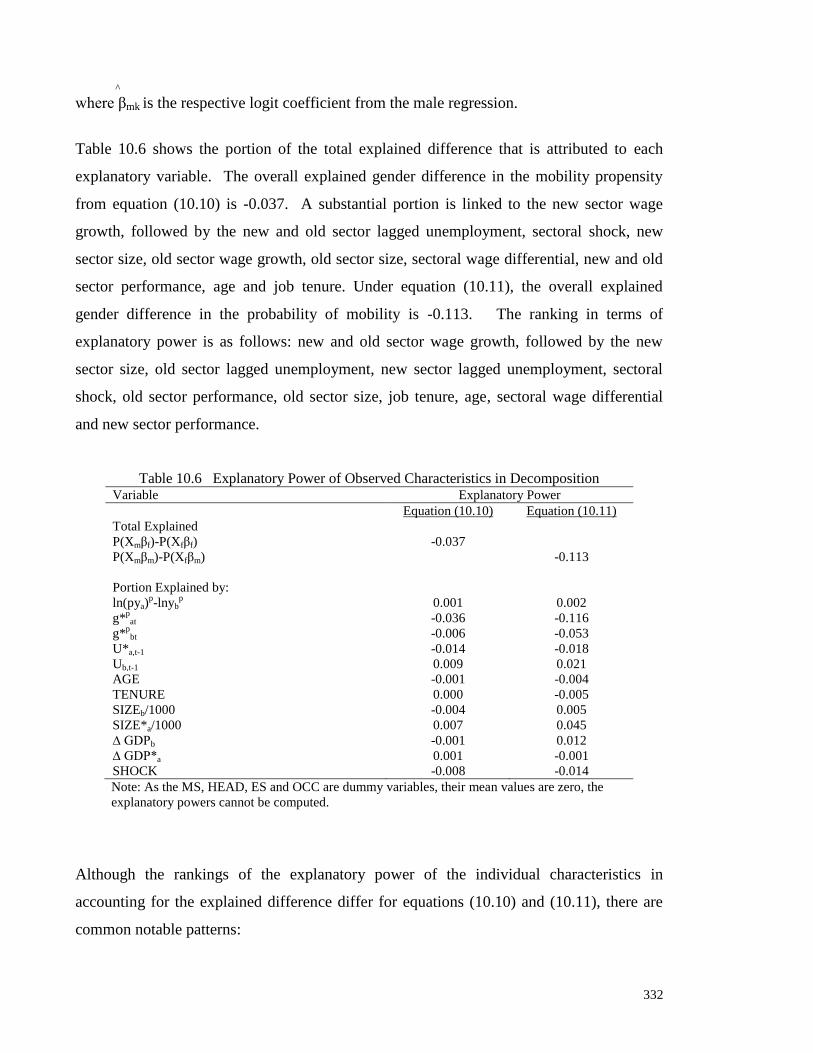

INTER-SECTORAL LABOUR MOBILITY IN KOREA:

ITS ORIGINS AND RELATIONSHIP WITH UNEMPLOYMENT

by

Fiona Ai Lin Tan

Bachelor of Economics (Hons) (UWA)

This thesis is presented for the degree of Doctor of Philosophy of

The University of Western Australia

Business School

University of Western Australia

September 2008

i

ABSTRACT

The Asian Financial Crisis was a wake-up call to the South Korean economy that a change

to its economic structure was needed. Prior to the Crisis, South Korea enjoyed healthy

economic growth and low unemployment. With the onset of the Crisis, Korea experienced

severe recession. Unemployment levels soared and turnover in the labour market became

commonplace. The Korean government enacted a series of policies and succeeded in

combating unemployment in the short-term. To the present time, unemployment levels

have been lowered, albeit with job instability and insecurity. A more effective longer-term

solution is needed to increase the resilience of this NIE.

The role of inter-sector labour mobility as a policy tool to combat unemployment using the

relevant determinants of mobility has not been explored in Korea (Asia), although it has

been debated at length in the West since the 1980s. Part of the reason for this lies in the

lack of longitudinal data to facilitate appropriate research. Recently, such data have been

made available by the Korean Labour Institute (KLI). This thesis extends research into the

labour mobility-unemployment relationship to South Korea. The priority is to establish

whether a mobility-unemployment relationship exists in Korea, and to obtain a thorough

understanding of the factors affecting sectoral mobility in this country in order to facilitate

the crafting of potential tools for addressing the unemployment problem.

The thesis is organised into two parts. Prior to the main study, however, the economic

history of Korea is outlined and sectoral labour reallocation patterns are associated with

economic growth. This preliminary work establishes the potential for the detailed research

for the Korean labour market that follows to make contribution to policy solutions to the

unemployment problem along the lines of the earlier research undertaken in Western

countries. Part I, entitled ‘Sectoral Mobility and Unemployment’, details the theoretical

hypotheses and empirical evidence concerning sectoral mobility and unemployment, and

extends the empirical application to Korea. The general finding is that whilst the

hypotheses [Sectoral Shift Hypothesis (SSH), Aggregate Demand Hypothesis (ADH) and

stage-of-the-business-cycle effect] are not relevant for Korea in the pre-Crisis era (1970-

1997), they have some support in the post-Crisis period (1998-2001). However, data

limitations, in the form of the short time period available for analysis, prevent strong

conclusions from being formed. The tentative conclusion is that a new mobility-

ii

unemployment relationship may exist for Korea in the post-Crisis period, thereby giving

rise to the potential for mobility as a policy tool for controlling unemployment. The in-

depth understanding of the factors of sectoral mobility required to implement such policy

provides the basis for the remainder of the thesis.

Part II, titled ‘The Factors Affecting Mobility’, develops a theoretical model for sectoral

mobility, and provides a literature review on other forms of labour mobility (union/non-

union, public-private and rural-urban mobility) as well as an empirical review of sectoral

mobility. These chapters set the stage for the empirical analysis of the determinants of

sectoral mobility for Korea. For the overall workforce, the main conclusion is that sectoral

mobility is a multi-facetted phenomenon involving a spread of factors. Of significance are

the expected and lifetime incomes, which are the pull factors of mobility, the deterrent

effect of the new sector’s unemployment rate and the direct effects of unanticipated sectoral

shocks. The multi-dimensional nature of these factors is replicated in the separate analyses

undertaken for males and females. The main finding is that whilst the monetary variables

and worker/industry characteristics impact male and female mobility differently, sectoral

unemployment and sectoral shock affect male and female mobility similarly.

The thesis is summarised and some policy measures provided in the sypnosis. It is argued

that the ‘new’ mobility-unemployment phenomenon appears to have emerged in Korea

after the Crisis, whereas it had been a feature of Western economies in much earlier time

periods. Traditional monetary and fiscal policies are inadequate when it comes to

combating unemployment in the presence of this mobility-unemployment phenomenon. A

combination of macro-policies, given the relevance of the ADH, and micro-policies, given

the validity of the SSH, is required. The multi-dimensional nature of mobility implies that

the micro policies to control or reduce mobility rates using the relevant variables (to

alleviate unemployment) should cover measures related to monetary wages, labour market

groups and sector performance. The sypnosis notes a dearth of Asian studies on sectoral

mobility, possibly due to the lack of longitudinal data. The collection of quality

longitudinal data for other Asian countries, so that research along the lines conducted in the

thesis could be undertaken for other NIEs, was seen as being of vital importance. With

such data, the standard of research on Asian economies can be at par with that of the

Western countries, and the apparently considerable potential benefits of microeconomic

policies via sectoral mobility for Asia could be realised.

iii

TABLE OF CONTENTS

Page

Abstract

Table of Contents

List of Tables

List of Figures

List of Common Acronyms

Acknowledgements

i

iii

xi

xii

xiii

xv

Chapter

Description

1

1.1

1.1.1

1.1.2

1.1.3

1.1.4

1.2

1.3

INTRODUCTION

Aims of Thesis

Definition of Sectoral Mobility

The Empirical Studies

Sectoral Mobility vis-à-vis Unemployment

The Factors Motivating Mobility

Organisation of the Thesis

Contributions to Labour Economics

1

1

1

1

2

4

5

7

2

2.1

2.2

2.2.1

2.2.2

2.2.3

2.2.4

2.2.5

2.2.6

2.3

2.3.1

2.3.2

2.3.3

2.4

2.4.1

2.4.2

2.4.3

2.5

ECONOMIC HISTORY OF SOUTH KOREA

Introduction

Korea’s Economic History

The Three Kingdoms

Koryo Dynasty

Choson Dynasty (1392-1910)

Japanese Colonial Rule (1910-1945)

Korean War (1950-1953)

Post-war South Korea

Korea’s Economic History in the Post-War Era

The 1970s

The 1980s

The 1990s

Economic Growth, Sectoral Changes and Labour Mobility

The Three Decades: 1970-2000

The 1998-2001 Period

Possible Structural Break during Asian Financial Crisis

Concluding Remarks

10

10

11

11

12

13

13

14

14

15

15

18

19

20

20

25

28

28

iv

Chapter Description Page

PART I:

SECTORAL MOBILITY AND UNEMPLOYMENT

PREAMBLE

29

29

3

3.1

3.2

3.2.1

3.2.2

3.2.3

3.3

3.3.1

3.3.2

3.4

3.5

3.5.1

3.5.2

3.6

3.6.1

3.6.2

3.6.3

3.7

3.7.1

3.7.2

3.7.3

3.8

3.9

THEORETICAL HYPOTHESES CONCERNING

SECTORAL MOBILITY AND UNEMPLOYMENT

Introduction

The Sectoral Shift Hypothesis

Impact of Sectoral Mobility on Aggregate Unemployment

SSH and Supply Shocks

SSH and the Natural Unemployment Rate

Aggregate Demand Hypothesis

U-V Relationship

The σ-U Co-movement Approach

Predicted and Unpredicted Mobility Indices

The Reallocation Timing Hypothesis and Stage-of-the-

Business-Cycle Effect

The Reallocation Timing Hypothesis

The Stage-of-the-Business-Cycle Effect

Conceptual Differences Between the SSH, ADH and RTH

Source of Sectoral Mobility

Chain of Causation

Nature of Unemployment

Methodological Differences

Methods to Test the SSH

Methods to Test the ADH

Methods to Test the RTH and Stage-of-the-Business-Cycle

Effect

Critique of the Mobility Indices

Summary

31

31

32

32

34

36

38

38

40

42

46

46

48

49

49

49

50

50

50

51

54

54

58

v

Chapter

4

4.1

4.2

4.2.1

4.2.2

4.2.3

4.2.4

4.3

4.3.1

4.3.2

4.4

4.4.1

4.4.2

4.4.3

4.5

4.6

4.6.1

4.6.2

4.6.3

4.6.3.1

4.6.3.2

4.6.3.3

4.6.4

4.6.4.1

4.6.4.2

4.6.5

4.6.6

4.6.7

4.7

4.8

Description

THE IMPACT OF SECTORAL MOBILITY ON

UNEMPLOYMENT: A REVIEW OF THE EMPIRICAL

LITERATURE

Introduction

Empirical Review on the SSH

The Raw Lilien Index

The Index Generated by Supply-side Disturbances

Pure Sectoral Shift Measures

The Natural Unemployment Rate Approach

Empirical Findings on the ADH

The Predicted Mobility Indices

The U-V Relationship

Findings on the RTH and Stage-of-the-Business-Cycle

The Horizon Covariance Index

Interaction Variables

Labour Reallocations and Foregone Production

Summary of Empirical Findings

Empirical Application

Type and Frequency of Data

Time Period

Model Estimation

Single-Equation Models

2-Stage Least Squares (2SLS)

Dual-Equation Models

Model Specification

Dependent Variable

Explanatory Variables

Number of σ’s in the Regression Equation

Natural Unemployment Rate Approach

Sectoral Mobility and Gender Unemployment

Summary of Empirical Application

Links with Research on Determinants of Mobility

Page

60

60

60

61

62

62

65

67

67

68

69

69

70

70

71

72

72

73

73

73

80

80

84

84

84

88

89

92

93

94

vi

Chapter Description

Page

5

5.1

5.2

5.2.1

5.2.2

5.3

5.3.1

5.3.2

5.3.3

5.3.4

5.4

5.4.1

5.4.1.1

5.4.1.2

5.4.2

5.4.2.1

5.4.2.2

5.4.3

5.4.3.1

5.4.3.2

5.4.3.3

5.4.3.4

5.4.3.5

5.4.4

5.5

5.5.1

5.5.2

5.6

5.6.1

5.6.2

5.6.3

5.6.4

5.7

SECTORAL MOBILITY AND UNEMPLOYMENT: AN

EMPIRICAL EXAMINATION FOR KOREA

Introduction

Trends in Aggregate and Sectoral Unemployment

Aggregate and Sectoral Unemployment

Sector-specific Employment and Unemployment

Model Framework

Baseline Model

Methodology

Descriptive Statistics

Stationarity

Dual-Equation Modelling

Estimation of Money Growth Equation

Review of Empirical Studies Estimating DMRt

Application to the Korean Case

Specification of Unemployment Equation

Unrestricted to Restricted Models

Preliminary Model Estimation

Structural Change

Prior Knowledge on Korean Unemployment

Tests for Model Stability

Phase I and Phase II

Phase II and Phase III

Accommodation of Structural Change

Re-specification of Unemployment Models

Final Model Estimation

Treatment for Serial Correlation

Sectoral Mobility during the Pre-Crisis Period (1971-1997)

Validity of the Hypotheses

Validity of the SSH

Relevance of the ADH

Applicability of the RTH

Sectoral Movements and Stage-of-the-Business-Cycle Effect

Concluding Remarks

97

97

98

98

98

100

100

100

101

105

106

106

106

108

111

111

114

116

116

116

120

120

123

125

127

127

129

130

131

134

135

136

138

vii

Chapter Description Page

PART II:

THE FACTORS AFFECTING SECTORAL MOBILITY

143

PREAMBLE

143

6

6.1

6.2

6.3

6.3.1

6.3.2

6.3.3

6.4

6.5

6.5.1

6.5.2

6.5.3

6.5.4

6.5.5

6.6

THE THEORETICAL AND CONCEPTUAL ISSUES IN

LABOUR/SECTORAL MOBILITY

Introduction

What is Labour Mobility

Theories of Sectoral/Industrial Mobility

Worker-Employer Mismatch Theory

Sectoral Shock Theory

Bridging Theory

Model of Labour Mobility

Empirical Models of Sectoral Mobility

Probability Choice Models

Simultaneous Equation Models

Vector Auto-regression Models

Sectoral Shock Measures

Time Periods

Summary: Model Application for Current Research

145

145

145

149

149

150

151

151

157

158

162

163

163

164

164

7

7.1

7.2

7.3

7.4

7.5

REVIEW OF THE EMPIRICAL LITERATURE ON

OTHER FORMS OF LABOUR MOBILITY

Introduction

Union versus Non-Union Mobility

Public versus Private Sector Mobility

Rural-Urban Mobility

Summary: Salient Points for Empirical Model

166

166

166

173

179

184

viii

Chapter

Description Page

8

8.1

8.2

8.3

8.3.1

8.3.2

8.3.3

8.3.4

8.4

8.5

8.6

8.7

8.8

EMPIRICAL EVIDENCE: FACTORS MOTIVATING

SECTORAL/INDUSTRIAL MOBILITY

Introduction

Sectoral/Industrial Mobility

Determinants under the Mismatch Theory

Monetary Wages

Macroeconomic Factors

Worker Characteristics

Job/Industry Characteristics

Determinants under Sectoral Shock Theory

Determinants under Bridging Theory

Assessment of Empirical Studies of Sectoral Mobility for

Modelling

Summary of Empirical Studies of Sectoral Mobility

Summary of Lessons Drawn from the Literature

186

186

186

188

194

198

203

220

226

230

231

233

237

9

9.1

9.2

9.2.1

9.2.2

9.2.3

9.2.3.1

9.2.3.2

9.2.3.3

9.2.3.4

9.3

9.4

9.4.1

9.4.1.1

9.4.1.2

9.4.1.3

9.4.2

EMPIRICAL STUDY ON THE DETERMINANTS OF

SECTORAL/INDUSTRIAL MOBILITY IN KOREA

Introduction

Data Sources, Concepts and Coverage

KLIPS Data

Korea NSO Data

The Role of Interim State of Unemployment

Sectoral Labour Flows

Missing Industry Information

Missing Survey Information

Interim States of Unemployment

Generic Model of Sectoral/Industrial Mobility

Descriptive Statistics

Survey Weights

Wave 1 Weights and the Population

Weights for Sample Attrition

Weights for New Entrants

Descriptive Statistics: Complex Statistics

240

240

241

241

245

245

245

247

249

250

251

252

253

254

255

255

256

ix

Chapter

9.5

9.5.1

9.5.2

9.5.3

9.6

9.6.1

9.6.2

9.6.3

9.6.4

9.6.5

9.7

9.7.1

9.7.2

9.8

Description

Derivation of Predicted/Recomputed Variables

Predicted Sectoral Wages

Sector-level Variables

Descriptive Statistics of Predicted/Recomputed Variables

Empirical Analysis: Determinants of Sectoral Mobility

Monetary Variables

Macroeconomic Variables

Worker Characteristics

Industry Characteristics

Sectoral Shock

Extensions of the Model

A Focus on the Initial Industry

Empirical Test: Theories of Sectoral Mobility

Summary

Page

261

262

269

274

275

280

282

283

289

290

291

291

292

298

10 10.1 10.2 10.3 10.4 10.5 10.5.1 10.5.2 10.5.3 10.5.4 10.5.5 10.6 10.6.1 10.6.2 10.6.3 10.7 10.7.1 10.7.2 10.7.3 10.7.4 10.8

GENDER DIFFERENCES IN SECTORAL/MOBILITY IN KOREA Introduction Model and Sample Dataset Validity of Pooling the Dataset Descriptive Statistics for Males and Females Gender Differences in the Determinants of Sectoral Mobility Monetary Variables Macroeconomic Variables Worker Characteristics Industry Characteristics Sectoral Shock A Gender Perspective on Theories of Sectoral Mobility Worker-Employer Mismatch Theory Sectoral Shock Theory Bridging Theory Decomposition Analysis An Overview of the Standard Decomposition Technique Application to Logit Models Decomposition Results Explanatory Power of Observed Variables Concluding Remarks

303 303 304 305 307 311 312 315 316 320 322 323 323 323 324 325 326 327 329 331 334

x

Chapter

Description

Page

11 11.1 11.2 11.3 11.4 11.4.1 11.4.2 11.4.3 11.5

THE SYPNOSIS Introduction Part I: Sectoral Mobility and Unemployment Part II: The Factors Affecting Sectoral Mobility The Policy Implications Policy Measures in Post-Crisis Period Assessment of Policy Measures and Current Situation Policy Recommendations Direction for Future Research

337 337 337 342 354 354 355 356 362

REFERENCES

364

LIST OF APPENDICES* 388

* Available on enclosed CD.

xi

LIST OF TABLES

Table Description Page

Table 2.1 Annual % Change in GDP, CPI and Employment (EMP) and 16

Unemployment Rate (UR)

Table 2.2 GDP by Sector, 1970-2000 21

Table 2.3 Employed Persons by Sector, 1970-2000 23

Table 2.4 GDP at Current Prices by Sector, 1998-2001 26

Table 2.5 Employed Persons by Sector, 1998-2001 27

Table 4.1 Studies on the Impact of Sectoral Mobility on Aggregate 63

Unemployment in the U.S.

Table 4.2 R2 between Actual Unemployment Rate and Natural Unemployment 66

Rate

Table 4.3 Contemporaneous Correlations between Labour Reallocation 71

and Average Value Proxies of Foregone Production

Table 4.4 Unemployment and Money Growth Equations used in Selected 74

Studies of Sectoral Mobility

Table 5.1 Employment and Unemployment By Sector 99

Table 5.2 Symbols of Sectoral Mobility 102

Table 5.3 Descriptive Statistics of Ut, DMRt and σ 103

Table 5.4 Initial Parameter Estimates of σ 115

Table 5.5 Phases in the Korean Labour Market from the CUSUMSQ Test 118

Table 5.6 F- and Harvey-Collier Statistics from Tests of Structural Change 122

Table 5.7 Final Model: Parameter Estimates of σ, D and σD and LM statistic 128

Table 5.8 1971-1997: Parameter Estimates of σ 130

Table 5.9 Parameter Estimates of σ, σSt and/or σStD 137

Table 7.1 Selected Studies of Union/Non-Union Mobility 168

Table 7.2 Selected Studies of Public-Private Sector Mobility 175

Table 7.3 Selected Studies of Rural-Urban Sector Mobility 181

Table 8.1 Probability Choice Studies of Sectoral/Industrial Mobility under 190

Worker-Employer Mismatch Theory

Table 8.2 Wages and Sectoral/Industrial Mobility 197

Table 8.3 Unemployment, Employment, GNP and Sectoral/Industrial Mobility 202

Table 8.4 Age and Sectoral/Industrial Mobility 204

Table 8.5 Gender and Sectoral/Industrial Mobility 206

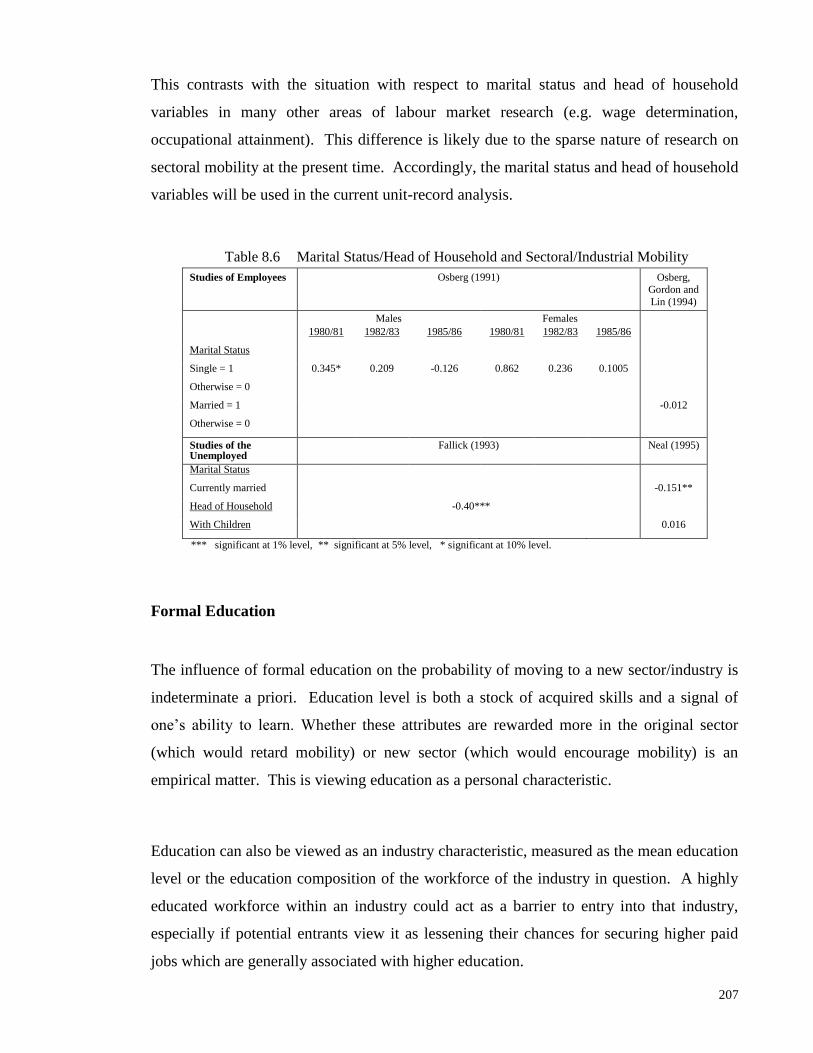

Table 8.6 Marital Status/Head of Household and Sectoral/Industrial Mobility 207

Table 8.7 Education and Sectoral/Industrial Mobility 208

Table 8.8 On-the-job Training and Sectoral/Industrial Mobility 213

Table 8.9 Occupation and Industrial Mobility 217

Table 8.10 Initial Industry and Industrial Mobility 218

Table 8.11 Employment Status and Industrial Mobility 220

Table 8.12 Working Hours, Product Similarity, Work Similarity and Industrial 223

Mobility

Table 8.13 Sectoral Performance Indicators and Sectoral/Industrial Mobility 226

Table 8.14 Sectoral Shocks and Sectoral/Industrial Mobility under Sectoral Shock 229

Theory

Table 8.15 Assessment of the Explanatory Variables 235

xii

Table Description Page

Table 9.1 Gross and Net Labour Flows based on Sample of 29,474 Observations 246

Table 9.2 Gross and Net Labour Flows based on Sample of 29,474 Observations 248

and the Interim State of Unemployment

Table 9.3 Industry Breakdown of 29,474 Sample with/without Survey Information 249

Table 9.4 Gross and Net Labour Flows based on Sample of 10,691 Observations 251

Table 9.5 Wave 1 Weights 254

Table 9.6 Means and Standard Deviations for Korean workers, Aged 20-64 years 258

Table 9.7 Actual versus Predicted Monetary Variables 269

Table 9.8 Means and Standard Deviations for Predicted and Recomputed

Variables 275

Table 9.9 Unrestricted Model: Logit Regression on Probability of

Sectoral/Industrial Mobility 278

Table 9.10 Main Model: Logit Regression on Probability of Sectoral/Industrial

Mobility 281

Table 9.11 Logit Regression on Probability of Sectoral/Industrial Mobility:

A Focus on the Initial Industry, Selected Coefficients 292

Table 9.12 Logistic Regression of Sectoral/Industrial Mobility on Wages and

Alternative Measures of Sectoral Shock, Selected Coefficients 296

Table 10.1 Logistic Regression of ‘Full’ Model 306

Table 10.2 Means and Standard Deviations for Male and Female workers, Aged

20-64 years 308

Table 10.3 Logistic Regression of Sectoral/Industrial Mobility by Gender 314

Table 10.4 Logistic Regression of Sectoral/Industrial Mobility on the Standard

Error of Wage Distribution and Sectoral Shock for Males and Females 324

Table 10.5 Decomposition Results 330

Table 10.6 Explanatory Power of Observed Characteristics in Decomposition 332

Table 11.1 Micro-policy Targets for Korea 360

LIST OF FIGURES

Figure Description Page

Figure 1.1 Lilien Index (σt) and Annual Unemployment Rate (Ut) 3

Figure 2.1 Korea’s Historical Timeline 11

Figure 2.2 Annual % Change in GDP, 1970-2001 17

Figure 2.3 Annual % Change in Employment and Unemployment Rate, 17

1970-2001

Figure 2.4 Annual % Change in CPI, 1970-2001 18

Figure 5.1 DMRt series 110

Figure 9.1 Probability of Sectoral Mobility and Age 284

Figure 9.2 Probability of Sectoral Mobility and Tenure 285

xiii

LIST OF COMMON ACRONYMS

ABS Australian Bureau of Statistics

ACGR Average Annual Compound Growth Rate

AD Aggregate Demand

ADH Aggregate Demand Hypothesis

APEC Asia-Pacific Economic Cooperation

AR Auto-regression

BLS Bureau of Labor Statistics

CILSS Cöte d’Ivoire Living Standards Survey

CO Cochrane-Orcutt

CPI Consumer Price Index

CPS Current Population Survey

CSO Central Statistical Organisation

CSV Cross-Section Volatility

CUSUM Cumulated Sum of Residuals

CUSUMSQ Cumulated Sum of Squared Residuals

DMR Unanticipated Money Growth

DME Anticipated Money Growth

DOLS Dynamic Ordinary Least Squares

DWS Displaced Workers Survey

ECM Error Correction Models

EP Energy Price Index

ESS Error Sum of Squares

GDP Gross Domestic Product

GIC Government Investment Corporation

GNP Gross National Product

HC Harvey-Collier

HILDA Household, Income and Labour Dynamics in Australia

ILO International Labor Organisation

IMF International Monetary Fund

IQ Intelligence Quotient

IT Information Technology

IV Instrumental Variables

KLI Korean Labor Institute

KLIPS Korea Labor Income Panel Study

LM Lagrange Multiplier

LMAS Labour Market Activity Survey

MLE Maximum Likelihood Estimation

NHWI National Help-Wanted Index

NIE Newly Industrialised Economy

NILF Not In Labour Force

NLS National Labor Survey

NSO National Statistical Office

NSW New South Wales

OECD Organisation for Economic Cooperation and Development

OLS Ordinary Least Squares

PID Personal Identification

PPI Producer Price Index

PSC Post-School Certificate

PSID Panel Study of Income Dynamics

RTH Reallocation Timing Hypothesis

SA South Australia

xiv

SSH Sectoral Shift Hypothesis

SME Small and Medium-sized Enterprises

TSM Time-Series Models

TQ Trade Qualification

UI Unemployment Insurance

U-V Unemployment-Vacancies

VAR Vector-autoregression

WA Western Australia

2SE 2-Step Estimation

2SLS 2-Stage Least Squares

σ-U Mobility-Unemployment

σ-V Mobility-Vacancies

Note: Excludes annotations for variables and mathematical symbols.

xv

ACKNOWLEDGEMENTS

This thesis has moved with me through three continents, seven houses and varied states of

employment. It’s a wonder it is finished. I have several people to be grateful for.

My principal supervisor, Professor Paul Miller; who was instrumental in the evolution of

this thesis. His expertise on the area of labour economics and excellent supervision

throughout the thesis will be treasured. His suggestions on modelling and empirical issues,

conscientious attention in reviewing the hundreds of drafts and empirical results, and clear

suggestions in the written drafts are valued, considering that the study was done long-

distance with minimal face-to-face contact. He is the ideal supervisor one could have.

My coordinating supervisor in my initial country of residence, Dr Chai Tai Tee, from the

Government of Singapore Investment Corporation, who gave direction on the choice of

topic and data collection. He sketched a realistic picture on the effort involved and was

willing to give the moral backup outside of the university.

The Korea Labor Institute for their assistance in the execution of the KLIPS software and in

explaining the survey questionnaires and data items which initially appeared in the Korean

language onscreen. The UWA Economics Programme for providing me with the necessary

resources during my residency at the university. A note of appreciation to Ms Derby Voon

for going through my list of references.

Special thanks to my family. To my mother who has been there for me these years; her

perfect blend of kindness and wisdom never ceases to amaze me. To my husband whose

job stint in the Middle East made this study possible and who became the IT helpdesk at

home. To my brother who assisted in the merging of several datasets. To ‘Moses’, my

little Maltese, my source of fun and amusement.

I thank God, too, for bringing these people to me, for without them, this thesis would not be

complete.

1

CHAPTER 1

INTRODUCTION

1.1 AIMS OF THESIS

1.1.1 Definition of Sectoral Mobility

Labour mobility is an area of labour economics that has generated considerable attention in

studies across the world. It involves labour movements across sectors, and can take various

forms, including between union and non-union sectors, public and private sectors, and rural

and urban sectors. This study examines labour mobility across industries or sectors of the

economy. Such labour movements are termed as „industrial‟, „inter-industrial‟, or more

simply „intersectoral‟ or „sectoral‟ mobility.

1.1.2 The Empirical Studies

There has been widespread interest in the study of sectoral mobility, from the perspective

of its causes and consequences. The latter has been particularly popular as a research topic,

with many studies looking at the links between sectoral mobility and employment and

unemployment. These links have been examined for the U.S. [Lilien (1982), Abraham and

Katz (1986), Blanchard and Diamond (1989), Parker (1992), Palley (1992), Brainard and

Cutler (1993), Davis (1987), Mills, Pelloni and Zervoyianni (1995), Loungani (1986),

Murphy and Topel (1987a) and Lu (1996)], Canada [Neelin (1987) and Samson (1985)],

Europe [Saint-Paul (1997) for France, Garonna and Sica (2000) for Italy], and Asia [Prasad

(1997) for Japan]. The seminal paper was Lilien (1982) on the relationship between

sectoral mobility and unemployment1. The subsequent development of this led to several

hypotheses, namely, the Sectoral Shift Hypothesis (SSH), Aggregate Demand Hypothesis

(ADH), Reallocation Timing Hypothesis (RTH) and stage-of-the-business-cycle effect.

This research has policy significance, as if the underlying relationship holds, inter-sector

mobility could be an instrument in combating unemployment via adjustments of its relevant

determinants2. Putting it figuratively, this is analogous to sculpting a new tool to solve an

old problem.

2

Given the links between mobility and unemployment, and the potential of mobility as a

policy tool, the need to understand the factors that motivate it emerges. Interest in these

only followed nearly a decade later, in the late 1980s and 1990s. The studies covering this

topic are for the U.S. [Loungani and Rogerson (1989), Jovanovic and Moffitt (1990),

McLaughlin and Bils (2001), Brainard and Cutler (1993), Fallick (1993), Thomas (1996b),

Neal (1995), Clark (1998) and Kim (1998)], Canada [Osberg (1991), Osberg, Gordon and

Lin (1994), Vanderkamp (1977) and Altonji and Ham (1990)], Europe [Ottersen (1993) for

Sweden and Gulde and Wolf (1998) for the European Union (France, Italy, Germany and

Spain)] and Asia [Prasad (1997) for Japan and Jayadevan (1997) for India]. Though the

number of studies is by no means sparse, given its belated entry into the field of labour

economics, sectoral mobility can be considered to be an infant topic of research.

1.1.3 Sectoral Mobility vis-à-vis Unemployment

The empirical basis for the research into the links between sectoral mobility and

unemployment can be seen for several continents/countries, namely, Oceania (Australia),

North America (U.S. and Canada), Europe (U.K., Sweden and Finland), and Asia (Japan,

South Korea and Singapore). The indicator of unemployment is its rate (Ut). Inter-sector

labour movements can be represented by the raw Lilien index (ζt), the derivation of which

will be outlined in chapter 33. Inter-sector labour movements and the unemployment rate

both fluctuate for each country over the 1970-2001 period4 (see country charts under Figure

1.1). Of relevance is South Korea, where sectoral mobility moved in tandem with

unemployment, especially during the 1998-20015 post-Crisis period where unemployment

reached 7% in 1998, the highest since 1970.

The various empirical investigations into data like that presented in Figure 1.1 suggest that

a mobility-unemployment relationship exists in most Western countries. The first review

of the aggregate-level data in Figure 1.1 suggests that a mobility-unemployment

relationship may also exist for Korea. Given the potential for this relationship to be

exploited in unemployment policy in Korea, it is important to establish more formally its

strength, and to determine how it arises. Part I of this thesis addresses these issues.

3

Figure 1.1 Lilien Index (ζt) and Annual Unemployment Rate (Ut)

Australia U.S.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Canada U.K.

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

Note: Methodology for 1999 revised; data not strictly comparable.

Finland Sweden

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Note: Methodology for 1989 revised; data not strictly comparable. Note: Methodology for 1993 revised; data not strictly comparable.

ζt*100

Ut

Ut

ζt*100

Ut

ζt*100

ζt*100

Ut

Ut

ζt*100

ζt*100

Ut

4

Japan Singapore

0.00

1.00

2.00

3.00

4.00

5.00

6.00

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000

0.00

2.00

4.00

6.00

8.00

10.00

12.00

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Note: Sector employment data not available for 1971-1973.

South Korea

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Note: For all charts, the x-axis is the year. The y-axis either represents the unemployment rate in percent terms or the

value of the Lilien index. The Lilien index is a measure of sectoral mobility, and it is the most commonly-used index in

empirical studies that focus on sectoral mobility.

1.1.4 The Factors Motivating Mobility

Where a mobility-unemployment relation exists and is to be used by policy makers, the

factors that determine this mobility need to be understood. Part II is dedicated to enhancing

such understanding for Korea for the recent 1998-2001 post-Crisis period. A range of

determinants of worker mobility have been identified in the empirical literature, covering

monetary and macroeconomic variables, worker/job characteristics and unanticipated

ζt*100 Ut

Ut

ζt*100

Ut

ζt*100

5

sectoral shocks. Study of the Korean labour market will include these, and there will be

emphasis on measuring these separately for the different sectors.

If these determinants can be identified formally, there arises the potential for policy to

control mobility via the relevant variables to alleviate unemployment. This thesis therefore

aims to: (i) establish the relationship between mobility and unemployment for Korea; and

(ii) enable a thorough understanding of the determinants of sectoral mobility in order to

provide a sound basis for policy in this area.

1.2 ORGANISATION OF THE THESIS

The thesis consists of an introduction (chapter 1), a prelude (chapter 2), the main body of

research (Parts I and II), and a conclusion (chapter 11). Chapter 2, on „The Economic

History of South Korea‟, introduces the lesser-researched country of Korea and

demonstrates the importance of sectoral mobility in relation to economic growth. Part I

focuses on the issue of sectoral mobility vis-a-vis unemployment and Part II concentrates

on the determinants of sectoral mobility.

Part I, entitled „Sectoral Mobility and Unemployment‟, contains 3 chapters. Chapter 3

outlines theoretical perspectives on hypotheses concerning sectoral mobility and

unemployment. Chapter 4 covers empirical evidence on these hypotheses. An empirical

application to Korea is undertaken in the last chapter of Part I.

The theoretical hypotheses on sectoral mobility and unemployment presented in chapter 3

are the SSH, ADH, RTH and stage-of-the-business-cycle. The chapter documents the

different methods of testing these hypotheses. Conceptual differences among the

hypotheses, in terms of the source of sectoral mobility, the chain of causation, and the

nature of the resultant unemployment, are identified.

The empirical review of the impact of sectoral mobility on unemployment in chapter 4

focuses on findings, modelling techniques, model specification and the set of mobility

6

indices and explanatory variables. This is considered to be the preparatory work for the

empirical application carried out in chapter 5.

Chapter 5 estimates the impact of sectoral mobility on aggregate unemployment for Korea

in the context of the hypotheses outlined in chapter 3. The empirical model is subjected to

stringent econometric testing procedures. Two periods are distinguished in the empirical

work, the pre- and post-Crisis periods. For the earlier period, the main findings show a lack

of relevance of the SSH, ADH and stage-of-the-business-cycle effect for Korea. The

relevance of the RTH could not be ascertained owing to measurement issues associated

with the primary variable used, the horizon covariance index. For the post-Crisis period,

the findings favour the SSH, ADH and stage-of-the-business-cycle effect, but the limited

number of observations in the aggregate-level annual data prevents strong conclusions from

being drawn. Nonetheless, as the findings have revealed that the SSH and ADH could

apply to Korea, sectoral mobility could be a potential policy tool for addressing the

unemployment problem. Knowledge of the determinants of sectoral mobility is needed.

Part II is devoted to providing this information.

The second part of the thesis, entitled „The Factors Affecting Sectoral Mobility‟, contains

the literature review on labour/sectoral mobility and an empirical study of sectoral mobility

in the context of the Korean labour market. It contains five chapters, chapter 6 through to

chapter 10. Chapter 6 highlights the theoretical and conceptual issues in the study of

labour mobility and develops the empirical model. Chapter 7 reviews the literature on the

forms other than sectoral mobility, i.e. union/non-union, public-private and rural-urban

mobility, to extract findings useful for the current work in terms of econometric techniques,

data banks and relevant research questions. Finally, chapter 8 reviews the empirical

evidence on the factors associated with sectoral mobility. Together, chapters 6, 7 and 8 set

the stage, in terms of identifying a model, conceptual issues, econometric techniques,

appropriate explanatory variables and data to be used, for the empirical analysis of the

determinants of sectoral mobility for Korea.

The last two chapters in Part II contain the empirical application for Korea. Chapter 9

presents the generic model of sectoral mobility, descriptive statistics of the explanatory

variables, selected predicted/recomputed monetary and sector-level variables, and empirical

7

results of the determinants of sectoral mobility. The conclusion is that sectoral mobility is

a multi-dimensional phenomenon involving a range of factors. Of special interest are the

expected and lifetime incomes, which act as pull factors of mobility, the deterrent effect of

the new sector‟s unemployment rate and the positive impact of the unpredictable sectoral

shock. Having established the findings for the total workforce, separate analyses are

conducted for males and females in chapter 10.

Chapter 10 provides within- and across-gender group comparisons in terms of mobility

behaviour. The conclusion is that whilst the monetary variables and worker/industry

characteristics affect the mobility of males and females differently, sectoral unemployment

and sectoral shocks impact male and female mobility similarly. The multi-dimensional

nature of these determinants established for the workforce as a whole in chapter 9 is

similarly reflected in the separate analyses for men and women.

The synopsis is chapter 11. The key findings of the empirical work are summarized, and

links between Parts I and II of the research are drawn. Some policy implications

concerning labour mobility are provided and possible avenues for further research for

Korea are suggested.

1.3 CONTRIBUTIONS TO LABOUR ECONOMICS

The major contributions to labour economics can be succinctly stated. These cover

conceptual and empirical issues. On the impact of sectoral mobility on unemployment (i.e.

Part I), the contributions are:

a) The consolidation of the extensive information available on hypotheses on the

mobility-unemployment relationship, including the varied indices used in

empirical research and the way the hypotheses are tested;

b) Development of empirical research through the use of a comprehensive

specification, sophisticated econometric testing, and accommodation of

structural changes to the economy; and

8

c) Conducting research for Asia (Korea in this case), which has been

underrepresented in analyses of the sectoral mobility-unemployment

relationship.

The more notable contributions found in Part II on the determinants of sectoral mobility

include:

a) Raising the sophistication of research on the determinants of sectoral mobility.

This is made possible by drawing out lessons from the study of other forms of

labour mobility for empirical modelling, having a pooled, time-series cross-

sectional dataset at the micro-level, developing a conceptually-advanced model

and having a comprehensive list of variables in the estimating equation.

b) Filling the gap in the research into the determinants of worker mobility for Asia.

The existing studies for Asia are inadequate in quantity (i.e. conducted only for

Japan and India) and quality (i.e. conducted using aggregate-level datasets with

few explanatory variables). The new research in this area applies the lessons

learnt from the West to Korea. The availability of the micro-level dataset

ensures that the research can be carried out to the desired level of sophistication,

comparable with that of recent studies of the developed countries.

c) Extending the coverage of the research by conducting separate analyses for

males and females. This is an important contribution as there are only a few

gender studies, and these only cover the developed countries (e.g. Osberg (1991)

and Osberg, Gordon and Lin (1994) for Canada, and Jovanovic and Moffitt

(1990), Neal (1995) and Thomas (1996b) for the U.S.).

These contributions make the current study a pioneering effort in terms of coverage (to

Asia and the separate male and female labour markets) and the quality of research. It sets

the research on sectoral mobility for South Korea on par with that of the developed

countries.

9

Endnotes:

1. An earlier paper by Vanderkamp (1977) focused on the factors that determine sectoral mobility. Since this

paper did not generate much interest until the late 1980s/early 1990s, the Lilien (1982) paper on the impact of

sectoral mobility is considered to be the origin of the debate.

2. There are many economic, social and political problems associated with unemployment, including loss of

national output and personal hardship. These have been documented elsewhere and will not be discussed here.

3. Aggregate-level employment statistics sourced from the International Labour Organisation (ILO) are used

to compute the raw Lilien index. The Lilien index has been scaled up 100 times to make it comparable to the

unemployment rate in value terms. For all countries except Singapore, the Lilien index has been estimated

over the same nine major industries as that for Korea. The index for Singapore was estimated over 7

industries, with agriculture, mining and utilities being grouped together since 2000-2001 sector employment

data are not available for these industries.

4. The data period is chosen to synchronise with that for the empirical work undertaken in chapter 5.

5. This data period is consistent with that used in the empirical work undertaken on the impact and

determinants of sectoral mobility.

10

CHAPTER 2

THE ECONOMIC HISTORY OF SOUTH KOREA

2.1 INTRODUCTION

South Korea is classified as a Newly Industrialised Economy (NIE), alongside the

economies of Japan, Singapore, Hong Kong and Taiwan. It has experienced phenomenal

economic growth during the post war era, emerging from humble beginnings as a

developing country with a low per capita Gross Domestic Product (GDP) of U.S.$279 in

1970 to attaining developed country status in 1996, with a per capita GDP of U.S.$14,265

in 2004. Its spectacular growth did not come without obstacles, as it had to encounter the

global oil and food crises in the 1970s and it was one of the hardest-hit Asian countries

when the Asian Financial Crisis occurred in the last decade. The country‟s adeptness in

responding to changing economic conditions through industrialisation, protectionism,

financial reform, globalisation and seeking emergency assistance from international bodies

has contributed to its reputation as a dynamic and growing economy. As of 2004, it was

ranked as the world‟s tenth largest economy in gross domestic product1.

This chapter describes the economy of South Korea and traces its economic history. It also

demonstrates the importance of sectoral mobility in relation to economic growth. Whilst the

first aim is for the benefit of readers in providing background information on Korea‟s

economic history and labour market situation, which is imperative for this lesser-researched

Asian country, the second aligns the significance of the study of sectoral mobility itself to

the South Korean economy. The approach is chronological, with the period 1970-2000

categorised into decades, followed by a year-by-year analysis in the more recent period

covering 1998-2001. The purpose of this more detailed coverage of 1998-2001 is to provide

a better understanding of the data period used in the empirical study in chapters 5, 9 and 10.

The chapter is structured as follows. Section 2.2 sketches the history and economy of

Korea up to around 1970. The economic history post-1970 is presented in section 2.3, with

a separate account for each decade. Finally, in section 2.4, it is demonstrated that economic

growth not only depends on the changes in importance of the various sectors of the

11

economy but also on inter-sectoral labour mobility. Hence, labour movements between the

various sectors are tracked together with sectoral economic growth.

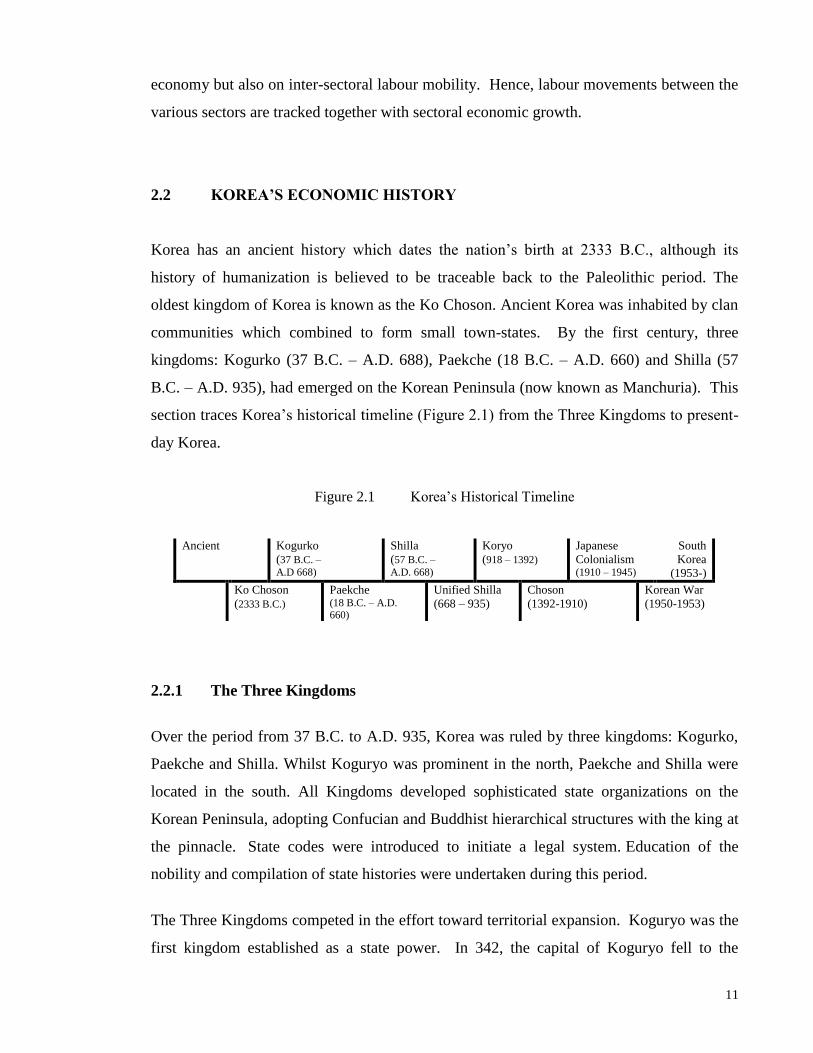

2.2 KOREA’S ECONOMIC HISTORY

Korea has an ancient history which dates the nation‟s birth at 2333 B.C., although its

history of humanization is believed to be traceable back to the Paleolithic period. The

oldest kingdom of Korea is known as the Ko Choson. Ancient Korea was inhabited by clan

communities which combined to form small town-states. By the first century, three

kingdoms: Kogurko (37 B.C. – A.D. 688), Paekche (18 B.C. – A.D. 660) and Shilla (57

B.C. – A.D. 935), had emerged on the Korean Peninsula (now known as Manchuria). This

section traces Korea‟s historical timeline (Figure 2.1) from the Three Kingdoms to present-

day Korea.

Figure 2.1 Korea‟s Historical Timeline

Ancient Kogurko

(37 B.C. –

A.D 668)

Shilla

(57 B.C. –

A.D. 668)

Koryo

(918 – 1392)

Japanese

Colonialism (1910 – 1945)

South

Korea

(1953-)

Ko Choson

(2333 B.C.)

Paekche (18 B.C. – A.D. 660)

Unified Shilla

(668 – 935)

Choson

(1392-1910)

Korean War

(1950-1953)

2.2.1 The Three Kingdoms

Over the period from 37 B.C. to A.D. 935, Korea was ruled by three kingdoms: Kogurko,

Paekche and Shilla. Whilst Koguryo was prominent in the north, Paekche and Shilla were

located in the south. All Kingdoms developed sophisticated state organizations on the

Korean Peninsula, adopting Confucian and Buddhist hierarchical structures with the king at

the pinnacle. State codes were introduced to initiate a legal system. Education of the

nobility and compilation of state histories were undertaken during this period.

The Three Kingdoms competed in the effort toward territorial expansion. Koguryo was the

first kingdom established as a state power. In 342, the capital of Koguryo fell to the

12

Chinese. After this Paekche amassed power and came into conflict with Koguryo in the

late fourth century. Subsequently Shilla managed to defeat the other two kingdoms, but

was initially unable to control the entire territories of Koguryo and Paekche, which were

under Chinese rule. Eventually Shilla defeated the Chinese in A.D. 676, and became a

unified state covering most of the Korean Peninsula.

The Unified Shilla kingdom (668-935) reached its peak of power and prosperity in the

middle of the eighth century. Education flourished in the government service, the equitable

distribution of land for peasants was put into practice in 722, reservoirs were erected for

rice field irrigation and taxation in kind was collected. Learning was encouraged, resulting

in a new transcription system of Korean words by the use of Chinese characters. However,

in the ninth century, Shilla was troubled by intra-clan conflict around the throne and in

district administration.

2.2.2 Koryo Dynasty

Shilla was destroyed by rebel leaders: Kyon Hwon in 900, Kung Ye in 901 and Wang Kon,

the last rebel of Shilla and founder of the Koryo Dynasty (918-1392). During the Koryo

dynasty, diplomatic relations with the former Shilla aristocracy were maintained, state

defence was strengthened, internal conflicts among royalties were discouraged, the

emancipation of slaves in 956 was instituted, a civil service examination system to recruit

officials by merit was enforced and land allocation to officials was put into practice. These

policies enabled the Dynasty to become a centralized government with the power to make

admonitions to the throne on the part of officials and censorship of royal decisions. With

such internal order, Koryo was long able to withstand frequent invasions by the Liaos (old

tribal league) in the 900s. However, in 1238 the Mongolians invaded Korea. When the

Mongol Empire collapsed in the middle of the 14th

century, the Koryo dynasty was faced

with internal problems, e.g. animosity between Buddhism and Confucianism, opposition to

land reform by land owners and raiding by Japanese pirates in the country.

13

2.2.3 Choson Dynasty (1392-1910)

In 1392, King Kongyang (of the Koryo Dynasty) was forced to abdicate his throne and

General Yi took over. This marked the start of the Choson dynasty (1392-1910). During

the early Choson period (till the 17th century), Confucian ethics were promoted. The early

Choson era was noted for progressive ideas in administration, phonetics, national script,

economics, science, music, medical science and humanistic studies, historical geography,

increases in learning and writing of books, an increasing number of schools as well as the

introduction of the Korean alphabet.

The Choson maintained its political independence and cultural and ethnic identity in spite

of a number of foreign invasions. However, these invasions brought about destruction of

government records, cultural objects and historical documents, the devastation of land,

decrease in population, and the loss of artisans and technicians. The late Choson period

witnessed much social and economic upheaval. Following a particularly destructive war

with Japan in 1592, there were activities to reconstruct, provide medical relief and print

books destroyed during the war. The era also saw the rise of mercantilism, upward social

mobility, introduction of agro-managerial production methods, privatized factories, higher

production of goods for trade and a rise in commercial farming.

2.2.4 Japanese Colonial Rule (1910-1945)

Towards the late 19th

century, Korea became the focus of intense competition among

imperialist nations: China, Japan and Russia. In 1910, Japan annexed Korea. The Japanese

remained in the peninsula until the end of World War II and instituted militarized colonial

rule. Anti-Japanese resistance was evident. These sentiments came to the fore on March 1

1919 with a nationwide demonstration declaring Independence for Korea in the face of

intolerable aggression and oppression by the Japanese colonialists. The demonstration was

forcefully suppressed by the Japanese occupiers.

At the height of the independence movement, a provisional government of Korea was

established in Vladivostok on March 21, in Shanghai on April 11, and in Seoul on April 21.

The provisional government in Seoul proclaimed Korean independence, asking Japan to

withdraw its occupation forces from Korea. It called upon the Korean people to refuse

14

payment of taxes to the Japanese government, reject trials by Japanese courts, and avoid

employment at colonial offices. The Vladivostok, Shanghai and Seoul groups attempted to

integrate and form the Provisional Government on November 4. The Provisional

Government, despite financial difficulties, attempted to fulfill the international obligations

of the Korean people for 27 years until World War II. It declared war on Japan and

cooperated with the Allied Powers during war.

2.2.5 Korean War (1950-1953)

The Japanese surrender in 1945 brought many challenges in Korea. Korea was then faced

with a conflict in ideology. Korea was divided by the U.S. and U.S.S.R., which occupied

the north and south of the 38th

parallel, respectively. The ideological confrontation

inevitably gave rise to a tense military confrontation. North Korean troops invaded and

defeated the unprepared South across the 38th parallel in 1950. South Korea appealed to the

U.N. In response, the Security Council passed a resolution ordering North Korea to

withdraw to the 38th parallel and encouraged all member countries to give military and

medical support to the Republic. This was provided by the U.S. and 15 other nations.

Although the Allied forces initially pushed the North Koreans out of South Korea and

advanced into the north, they were soon forced to retreat by the Communist Chinese in

January 1951. The U.N. forces mounted a counterattack, retaking Seoul on March 12. A

stalemate was reached in the area along the 38th parallel, where the conflict had begun. At

this point, the Soviet Union called for truce negotiations, which began in July 1951, and

dragged on for two years before an agreement was reached on July 27, 1953.

2.2.6 Post-war South Korea

By the time the war ended, two million people had died and the country had been officially

divided between the north and the south. The Republic of Korea in the south has a

democratic government, whilst the Democratic People‟s Republic of Korea in the north is

ruled by a Communist regime. From this point, the research focuses on the Republic of

Korea.

The start of the Republic of Korea‟s growth began in the early 1960s with the introduction

of the First Five-Year Economic Development Plan. A conscious effort was made to turn

15

from inward-looking import substitution to an outward-looking strategy of export

promotion. South Korea exported light manufactured goods, in which the country had a

comparative advantage owing to its low labour costs. Other measures included maintaining

high interest rates to increase domestic savings and encouraging the inflow of foreign

investment. Thus, Korea was a growing economy when it entered the 1970s.

2.3 KOREA’S ECONOMIC HISTORY IN THE POST-WAR ERA

The Korean economy has experienced astounding growth in the past three decades. Owing

to its sophisticated industrial structure and globalisation efforts, it was admitted into the

Organisation for Economic Cooperation and Development (OECD) in 1996, signaling the

country‟s entry into the rank of advanced economies. Double-digit growth has been

consistently recorded: 30% in 1970-1980, 17% in 1980-1990 and 11% in 1990-2000.

Corresponding to high economic growth, employment has been rising steadily, by 4%, 3%

and 2%, over the same periods.

2.3.1 The 1970s

Korea‟s economic performance in the 1970s can be described as phenomenal, with high

economic growth and inflation but stable unemployment. There was an economic boom in

this decade, with GDP increasing at astounding rates of between 24% and 41% (see Table

2.1 and Figure 2.2). This boom in fact started in the mid-1960s when Korea made policy

changes to promote a free trade regime for exports and combined this with selective

protection in the import competing sectors. As a result of the food shortage of 1973 and oil

price shock in 1974, Korea‟s balance of payments deteriorated and she responded by

restructuring exports to higher value-added sophisticated products and diversifying her

trading partners. Moreover, industrial restructuring towards heavy and chemical products

led to a rising demand for investment by firms as well as increased demand for skilled

workers in the urban areas. There was consequently a transfer of labour from agriculture to

industry. Employment grew rapidly from 3.6% in 1970 to 6.2% in 1976, although the

growth slowed to 1% by the end of the decade (Figure 2.3). With the growth in

16

employment, the unemployment rate was kept at reasonably stable levels, and actually

decreased slightly, from 5% in 1970 to 4% in 1979.

Table 2.1 Annual % Change in GDP, CPI and Employment (EMP)

and Unemployment Rates (UR) GDP CPI EMP UR

1970 27.9 16.0 3.6 4.5

1971 24.0 13.5 3.4 4.5

1972 23.5 11.7 4.4 4.5

1973 28.9 3.2 5.4 4.0

1974 41.2 24.3 4.4 4.1

1975 34.6 25.2 2.4 4.1

1976 36.9 15.3 6.2 3.9

1977 28.2 10.1 3.2 3.8

1978 35.0 14.5 4.7 3.2

1979 28.1 18.3 1.4 3.8

1980 21.8 28.7 0.6 5.2

1981 25.4 21.4 2.5 4.5

1982 14.9 7.2 2.5 4.4

1983 17.3 3.4 0.9 4.1

1984 14.3 2.3 -0.5 3.8

1985 11.4 2.5 3.7 4.0

1986 16.7 2.8 3.6 3.8

1987 17.2 3.1 5.5 3.1

1988 18.8 7.1 3.1 2.5

1989 12.2 5.7 4.1 2.6

1990 20.6 8.6 3.0 2.4

1991 21.1 9.3 3.1 2.3

1992 13.5 6.2 1.9 2.4

1993 12.9 4.8 1.2 2.8

1994 16.5 6.3 3.2 2.4

1995 16.7 4.5 2.9 2.0

1996 10.9 4.9 2.2 2.0

1997 8.3 4.4 1.7 2.6

1998 -2.0 7.5 -6.0 6.8

1999 8.6 0.8 1.8 6.3

2000 8.1 2.3 4.3 4.1

2001 5.7 4.1 2.0 3.0 Source: Data on CPI, Employment and UR are from the ILO LaborStat database.

Data on GDP are from the Korea National Statistical Office.

17

Figure 2.2 Annual % Change in GDP, 1970-2001

-8

-4

0

4

8

12

16

20

24

28

32

36

40

44

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

Figure 2.3 Annual % Change in Employment and Unemployment Rates, 1970-2001

-8

-4

0

4

8

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

EMPG

UR

Annotation: EMPG: Annual % Employment Growth Rate

UR: Unemployment Rate

%

%

year

year

18

Figure 2.4 Annual % Change in CPI, 1970-2001

0

4

8

12

16

20

24

28

32

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

This economic progress came at the cost of high inflation (Figure 2.4). Moreover, the

industrial structure was distorted by over-investment in heavy industries and under-

investment in light industries. There was also a high degree of government control which

distorted prices and stifled competition.

2.3.2 The 1980s

Compared to the previous decade, the 1980s was a decade with lower growth, less inflation

and reduced unemployment. The growth in GDP slowed, from 22% in 1980 to 12% in

1989. Inflation rates dropped significantly, from 29% to 6%, over the same period. These

changes were the result of active steps undertaken to reduce inflation, rectify the structural

imbalance in the economy and to promote competition in the 1970s. Many restructured

industrial firms (power-generating, automobile, electrical, electronics, shipping, overseas

construction industries) were forced to merge to reduce excess capacity. There was also a

financial restructuring in the 1980s, as many commercial banks privatized, barriers to entry

into the financial sector were reduced, and financial services were diversified and

streamlined. On the labour front, employment levels rose, with about 2.8 million new jobs

being created during the decade. The rate of unemployment sank to the unprecedented

level of 2.6% by 1989.

%

year

19

2.3.3 The 1990s

The third decade can be categorized into two phases, with the first (1990-1997)

characterized by high growth, high inflation and low unemployment, and the second (1998-

1999) by low growth, inflation and high unemployment. In the first phase, GDP continued

to grow at double-digit rates and unemployment was at relatively low rates of 2-3%. This

was attributed to Korea‟s regionalization and globalization policy, i.e. “segyehwa policy”,

in which the country reformed its financial sector and participated in international activities

through trade talks in the Uruguay Round, membership in the Asia-Pacific Economic

Cooperation (APEC) and accession to the OECD in 1996. The rising income levels that

followed from the robust economy induced excessive private spending and speculation, and

caused inflation rates to escalate again in the first half of the 1990s.

The Asian Financial Crisis was a turning point for the otherwise healthy Korean economy.

The export success of Korea from the late 1980s led Japanese firms to withdraw key inputs

from the top financial conglomerates „chaebol‟, which eroded Korea‟s export drive. There

was overdependence on the chaebol which were using their profits for speculative rather

than productive investments. By 1998, the chaebol recorded drastically reduced profits and

several went into bankruptcy. By this time South Korea had accumulated foreign debt of

billions of dollars2. GDP and employment growth rates plunged, to negative 2% and 6%,

respectively. The rate of unemployment registered an all-time high of 7%. To prevent the

total collapse of the economy, the government sought an emergency loan from the

International Monetary Fund (IMF). Following the Crisis, there was a series of reforms in

the financial, corporate and labour sectors aimed at promoting sustainable growth, reducing

debt and increasing labour market flexibility. By 1999, the Korean economy had recovered

from the Crisis. GDP rebounded to 9% growth and employment started to show signs of

growth. However, unemployment rates were still relatively high and this presented a

challenge for the government which wanted to reduce unemployment in order to maintain

social stability.

20

2.4 ECONOMIC GROWTH, SECTORAL CHANGES

AND LABOUR MOBILITY

The previous section highlighted that Korea has undergone several phases of boom and

recession in recent times. These have been associated with changes in the importance of

various sectors of the economy. This section illustrates the associations between economic

growth, sectoral changes and labour mobility on a decade-by-decade basis, from 1970 to

2000, with special attention on 1998-2001 to coincide with the period of data collection for

the dataset used in the study of worker mobility in Part II of this thesis. The major

sectors/industries comprise agriculture, mining, manufacturing, utilities, construction,

commerce, transport, storage and communications, financial, business services and real

estate, and community, social and personal services. The classification of these nine

sectors/industries follows that of the empirical study to be undertaken in Part II of this

thesis.

2.4.1 The Three Decades: 1970-2000

The Korean economy at the start of the 1970s was dominated by three sectors: agriculture,

manufacturing and commerce. Together, these sectors contributed more than three-fifths of

total GDP in 1970, with the share of total output for agriculture, manufacturing and

commerce at 29%, 18% and 17%, respectively. At the end of the first decade, as a

consequence of the 1970s oil and food crises, the share of output due to agriculture and

commerce had declined considerably, to 16% and 14%, respectively. Corresponding to

their lower share in total output, the average annual GDP growths of agriculture and

commerce over the first decade were lower, at 22% and 28%, respectively. In comparison,

the share of manufacturing output rose to 24% and the sector experienced a strong average

annual growth of 34% over the decade. The services sector‟s contribution to GDP rose,

especially due to growth in the transport, storage and communications industry (share rose

from 7% to 8%), and the financial, business services and real estate industry (share rose

from 7% to 12%), with the average annual growths at 32% and 36%, respectively. These

high growth rates are reflective of the success of Korea‟s export-oriented policy and the

protectionism in the import sector. Thus, Korea‟s economic growth in the first decade was

associated mainly with strong growth in the manufacturing and services sectors.

21

Table 2.2 GDP by Sector, 1970-2000 1970 1980 1990 2000 1970-1980 1980-1990 1990-2000

% Distribution by Sector Average Annual Growth (%)

Total Gross Value-

Added at Basic Prices1 100.0 100.0 100.0 100.0 29.9 17.1 11.9 Agriculture 29.2 16.2 8.9 4.9 22.4 10.4 5.3 Mining 1.8 1.9 0.8 0.4 31.2 7.6 3.8 Manufacturing 17.8 24.4 27.3 29.4 34.1 18.4 12.7 Utilities 1.4 2.2 2.1 2.6 36.1 17.0 13.9 Construction 5.1 8.0 11.3 8.4 35.9 21.3 8.5 Commerce 16.8 14.2 13.0 10.8 27.7 16.1 9.8 Transport, Storage &

Communications 6.7 8.0 6.8 7.0 32.2 15.3 12.2 Financial, Business

Services & Real Estate 7.3 11.5 14.9 20.1 35.9 20.3 15.3 Community, Social &

Personal Services 13.9 13.7 14.8 16.5 29.7 18.1 13.1

Source: Korea NSO.

1. Whilst overall GDP comprises gross value-added at basic prices plus taxes less subsidies on products, the

latter does not have a sectoral breakdown. As such, „Total‟ refers to total gross value-added at basic prices. This

facilitates the computation of sectoral contributions.

By the second decade, the adverse effects of the global oil and food crises spilled over to

the agricultural and commerce sector where their shares of output declined to 9% and 13%,

respectively. Reflecting the diversification towards heavy and chemical industries during

the post-Crisis period, manufacturing‟s share of output continued to grow steadily, to 27%.

In the services sector, the contribution to GDP was the result of the increases in the

financial, business services and real estate industry (share rose from 12% to 15%) and

community, social and personal services industry (share rose from 14% to 15%). For the

financial industry, the availability of investment funds made the growth in the industry

possible.

In the third decade, the rising importance of services, particularly financial, business

services and real estate, and community, social and personal services industries, was

evident. The share of GDP increased from 15% to 20% for the former and from 15% to

17% for the latter. The success in the financial, business services and real estate industry

was attributed to financial restructuring and globalization efforts. The manufacturing sector

managed to sustain its high share of 29%, and this was probably due to lower costs

associated with the amalgamation of manufacturing industries in the late 1980s. In

contrast, agriculture‟s share of total output continued to fall, to a meager 5%. The

22

commerce sector also registered a declining share of GDP over the decade, although its

drop in relative importance was not as pronounced as the drop in the rural sector.

In terms of sectoral labour shifts, Korea‟s labour force moved from the rural and services

sectors to the manufacturing, construction and commerce sectors over the first decade. The

share of agricultural employment declined from 50% to 34%, whilst notable increases

occurred in manufacturing (13% to 22%), construction (3% to 6%) and commerce (12% to

19%). The proportion of employment remained fairly stable in the other sectors/industries

over the first decade.

Between 1980 and 1990, the composition of the labour force shifted from agriculture to the

manufacturing, commerce and services sectors. Whilst the employment share continued to

drop in agriculture (34% to 18%), it rose in the manufacturing sector, from 22% to 27%,

and from 19% to 22% in the commerce sector. Each of the services industries also

recorded rising shares of employment during the decade.

By the third decade, the sectoral shifts were mainly in the form of movements from the

agricultural and manufacturing sectors towards the commerce and services sectors. The

first two sectors witnessed proportionate declines in the employment whilst the latter two

experienced increases in their relative employment.

Table 2.3 Employed Persons by Sector, 1970-2000

1970 1980 1990 2000 000s % 000s % 1970-1980 growth 000s % 1980-1990 growth 000s % 1990-2000 growth

Total 9,745 100.0 13,683 100.0 3.5 18,085 100.0 2.8 21,156 100.0 1.6

Agriculture 4,916 50.4 4,654 34.0 -0.5 3,237 17.9 -3.6 2,243 10.6 -3.6

Mining 111 1.1 124 0.9 1.1 79 0.4 -4.4 17 0.1 -14.2

Manufacturing 1,284 13.2 2,955 21.6 8.7 4,911 27.2 5.2 4,293 20.3 -1.3

Utilities 25 0.3 44 0.3 5.8 70 0.4 4.8 64 0.3 -0.9

Construction 284 2.9 843 6.2 11.5 1,346 7.4 4.8 1,580 7.5 1.6

Commerce 1,213 12.4 2,625 19.2 8.0 3,945 21.8 4.2 5,752 27.2 3.8

Transport, Storage &

Communications 350 3.6 619 4.5 5.9 923 5.1 4.1 1,260 6.0 3.2

Financial, Business Services &

Real Estate 0.0 332 2.4 945 5.2 11.0 2,113 10.0 8.4

Community, Social & Personal

Services 1,562 16.0 1,489 10.9 -0.5 2,638 14.6 5.9 3,814 18.0 3.8

Source: ILO LaborStat database. No employment data are available for financial, business services and real estate in 1970.

24

It should be noted that the Table 2.3 data illustrate the net mobility across sectors, and

include the impact of individuals moving from outside the labour market into employment,

and of individuals leaving employment for non-labour market activities. For example,

between 1970 and 1980, there was an increase in employment of 1,671,000 in Korea‟s

manufacturing sector. This is accompanied by employment growth in the mining, utilities,

construction, commerce and services sectors, and a decline in employment in the

agricultural sector. The 1,671,000 people who, on net, joined the manufacturing sector

over this period will generally comprise:

(i) inflows into manufacturing from outside the labour market, Iolm, and from

agriculture (Ia), mining (Im), utilities (Iu), construction (Ict), commerce (Ic) or

services (Is)3;

(ii) outflows from manufacturing to either non-labour market activities, Oolm, or to

work in either agriculture (Oa), mining (Om), utilities (Ou), construction (Oct),

commerce (Oc) or services (Os).

These individual inflows and outflows are the gross flows that combine to generate the net

flows illustrated in Table 2.3.

Hence,

1,671,000 = Inflows – Outflows

= (Iolm + Ia + Im + Iu + Ict + Ic + Is)

- (Oolm + Oa + Om + Ou + Oct + Oc + Os)

Clearly, inflows exceed outflows, and the number of employed persons in the

manufacturing sector has risen. While knowledge of the individual flows would assist

understanding the dynamics of the Korean labour market, the net movements provide a

useful measure of the relative strengths of the various economic sectors.

It can be seen that the growth in the Korean economy not only depends on changes in the

significance of the various sectors but on labour movements between sectors. The data

reveals that the sectoral flows of workers occur in the same direction as that of economic

growth. In the first decade, there was a net movement of labour from the agriculture and

services sectors to the manufacturing4, construction and commerce sectors. The net labour

25

flows were from agriculture to the manufacturing, commerce and services sectors in the

second decade. In the third decade net labour flows occurred mainly from the agricultural

and manufacturing sectors to the commerce and services sectors.

2.4.2 The 1998-2001 period

Throughout 1998-2001, the sectoral shares of GDP (at current prices) and employment

have remained fairly stable. The major contributors to overall GDP have been the

manufacturing sector and financial services industry, with a combined contribution of about

half of the total. In contrast, the mining and utilities sectors contributed a meager share of

less than 5%. In terms of overall employment, whilst the manufacturing remained one of

the largest contributors, and the mining and utilities sectors the lowest, the commerce sector

emerged to have the largest share, displacing the financial industry in this regard.

As compositional changes are not usually obvious within a short span of 4 years, sectoral

changes for 1998-2001 will also be examined using growth data. The earlier section

revealed that the Asian Financial Crisis was associated with a deterioration in both

economic and employment growth, to negative 2% and 6%, respectively, in 1998. Many

sectors recorded declines in GDP, including agriculture, mining, construction and

commerce. Correspondingly, three out of these four sectors with adverse economic

performance experienced declining employment5.

The series of reforms after the Crisis led to rises of 9% in GDP and 2% in employment. All

sectors except mining and construction experienced improvements in economic

performance. In the labour market, it was these two same two sectors, along with the

agricultural sector, where employment failed to recover. The situation in the agricultural

sector probably reflects the continued outflow of surplus labour from the rural to urban

sectors.

Economic recovery continued in 2000, and GDP rose by 8% and employment by 4%. The