Embed Size (px)

Citation preview

1

EUROPEAN COMMISSION Executive Agency for Small and Medium-sized Enterprises (EASME)

INTELLIGENT ENERGY EUROPE II

2007 - 2013

GRANTS

FINANCIAL GUIDELINES

Version 8 - January 2015

2

CONTENT

I ROLE OF COORDINATOR ________________________________________ 3

II INTERESTS YIELDED BY PRE-FINANCING ____________________________ 4

III COST REIMBURSEMENT ________________________________________ 4

IV WHAT ARE ELIGIBLE COSTS? _____________________________________ 4

V WHAT ARE NOT ELIGIBLE COSTS? _________________________________ 8

VI COST CATEGORIES _____________________________________________ 9

VI.1 STAFF COSTS ________________________________________________ 9

VI.2 SUBCONTRACTING (external services) ___________________________ 14

VI.3 TRAVEL AND SUBSISTENCE ALLOWANCES ________________________ 17

VI.4 DURABLE EQUIPMENT _______________________________________ 17

VI.5 OTHER SPECIFIC COSTS _______________________________________ 18

VI.6 ELIGIBLE INDIRECT COSTS _____________________________________ 19

VI.7 BUDGET TRANSFERS _________________________________________ 20

VI.8 REVENUE __________________________________________________ 20

VII FINANCIAL GUARANTEES ______________________________________ 21

VIII CHECKS, and AUDITS __________________________________________ 22

IX AMENDMENTS ______________________________________________ 24

X HOW TO AVOID FREQUENT MISTAKES____________________________ 25

3

PURPOSE OF GUIDELINES These guidelines have been prepared to help co-ordinators and co-participants (hereafter referred to as “the participants”1) to understand the financial provisions of the IEE grant agreement (GA). Participants should read the guidelines carefully together with the submitted model grant agreement and its special and general terms and conditions. The grant agreement referenced below refers to the model grant agreement for Intelligent Energy - Europe II (IEE II) actions. If the guidelines conflict with the provisions of the agreement, the latter shall prevail. We also would like to refer to our website where additional information/documents can be found for the day-to-day management of you project and which are useful when preparing the interim/final financial reports or amendment requests: http://ec.europa.eu/energy/intelligent/managing-projects/day-to-day-management/index_en.htm I ROLE OF COORDINATOR There is always only one project coordinator who is responsible for the tasks defined in Article I.3.1 of the GA and who represents the consortium vis-à-vis the Agency. The tasks attributed by the GA to the coordinator in the above-mentioned article cannot be subcontracted or outsourced to a third party. Coordination tasks are part of the "management tasks"; however, "management tasks" include tasks beyond those of coordination of the project, and those tasks can be performed by participants other than the coordinator. In this sense, some management tasks will be performed by other participants. Principles of calculation of the EU contribution and transfer of funds to participants:

• The EU contribution shall be calculated by reference to the costs of the project as a whole and its reimbursement shall be based on the accepted costs of each participant; • The contribution shall be determined by applying the upper funding limits indicated in Article I.4.3 per participant to the actual eligible costs accepted by the Agency; • The EU contribution cannot give rise to any profit; • The total amount of payments by the Agency shall not exceed in any circumstances the maximum amount of the EU contribution referred to in Article I.4.3 of the GA, even if the consortium decides to increase the work on the project or to add new participants with the approval of the Agency; • Where designated the sole recipient of payments on behalf of all of the participants, the coordinator is responsible for making all the appropriate payments and/or recoveries to/from the co-participants within 30 days upon receipt of the funds paid by the Agency,

1 NB! Subcontractors are not participant to the grant agreement.

4

unless there is a justified delay. Payments to the coordinator will discharge the Agency from its payment obligation.

II INTERESTS YIELDED BY PRE-FINANCING For projects under call 2012 and 2013, the Article II.16.4 of the GA was cancelled, in order to be in line with the new Article 8.4 of the Financial Regulation, and replaced by the former Article II.16.5. Thus, participants of EU funds, under these two calls, are no longer obliged to lodge the pre-financing on interest bearing bank accounts, and to declare the interest yielded by the pre-financing on these accounts. This modification applies, from 01 January 2013, as follows:

Situation as from 1/1/2013 Grant agreements signed before 31/12/2012

The former rules continue to apply: the interest on pre-financing has to be declared and reimbursed to the Commission by the Coordinator

Grant agreements signed as from 1/1/2013 (Call 2012 and 2013 only)

No obligation to open an interest yielding bank account or to declare the interest generated by the pre-financing.

III COST REIMBURSEMENT Funding is based on cost-sharing grant agreements. This means that the EASME contributes up to a maximum of 75% of the eligible costs incurred for the performance of the work defined in the grant agreement. The contribution shall be determined by applying the upper funding limits indicated in Article I.4.3, and up to a maximum of 75%, per participant to the actual eligible costs accepted by the Agency.

IV WHAT ARE ELIGIBLE COSTS? To be eligible all costs must

relate to the purpose of the action; be included in the estimated budget annexed to the grant agreement; be necessary for the fulfilment of the action which is the subject of the grant; be generated during the duration of the action (except for costs relating to final reports

and audit certificates when incurred within a maximum period of two months following the completion of the action).

In addition, direct eligible costs must:

be reasonable, justified, consistent with the usual internal rules of the participant, and in accordance with the principle of sound financial management, especially cost-effectiveness and “value for money”;

be identifiable, verifiable and determined in accordance with the relevant accounting principles;

5

be actually incurred by the participant and recorded in the accounts of the participant no later than the grant agreement completion date;

be compliant with the requirements of applicable tax and social legislation; be substantiated by proper evidence allowing identification and checking (except for the

flat rate indirect costs). Actual costs as opposed to budgeted costs: "Budgeted" costs are used for establishing a budget estimate only (Cfr. Contract Preparation Forms, which finally resulted in Annex II to the grant agreement, i.e. the estimated budget of the action). Once the project has started "actual" costs incurred and only actual costs must be used as a basis for completing the financial statements. All costs claimed, with the exception of applicable flat rate, should be based on the actual costs incurred. They must be supported by evidence that they are real (recorded in the accounts of the participant and supported by invoices for example), paid (supported by bank statements for example), and linked to the funded project. As a general rule, neither estimated amounts, nor budgeted amounts, are acceptable. Where these conditions are not met the amounts will be deemed to be ineligible. Supporting documents All participating organisations must keep proper accounts and supporting documents to justify as necessary all costs incurred and generated by the action. This includes also all supporting documents demonstrating the compliance with the awarding of contracts when purchasing services, goods or equipment needed to carry out the action. Original documents, especially accounting and tax records, or in exceptional and duly justified cases, certified copies of original documents relating to the agreement (stored on any appropriate medium that ensures their integrity in accordance with the national legislation) must be kept for five years after the date of payment of the balance of the Union contribution. Evidence of costs, explanations and justifications, must be readily available for inspection by the Executive Agency for Competitiveness and Innovation (EASME) and/or the European Commission and their authorised representatives, as well as by the European Anti-fraud Office (OLAF) and the European Court of Auditors. Please note that the flat rate indirect costs do not need to be supported by accounting documents. In order to substantiate the time worked on an IEE II project, participants must have daily records of all hours spent by a given person (i.e. the timesheet shall not only record the time spent on a specific project, but shall reconcile the total working time of each person, say for example 1700 hours per year).

An 'example' of a timesheet template can be found under the following link:

http://ec.europa.eu/energy/intelligent/files/implementation/doc/template_timesheet_en.xls

6

Incurred by the participant Supporting documents proving occurrence, the bookkeeping and the payment of the costs by the participants must be kept for all costs and for up to five years after the payment of the balance. Incurred during the duration of the project, with the exception of costs relating to final reports and audit certificates Only costs generated during the lifetime of the project can be eligible; as a result the period during which the project starts determines the beginning of the period of eligibility of the corresponding costs (Article I.2 of the GA – Duration and start date of the project). Determined according to the usual accounting and management principles and practices of the participant, identifiable and verifiable

Costs must be determined according to the applicable accounting rules of the country where the participant is established and "according to the usual accounting and management principles and practices of the participant". However, this principle is not absolute; it must be considered together with the other eligibility criteria, and therefore could not be invoked in order to deviate from other provisions of the GA. Used for the sole purpose of achieving the objectives of the project and its expected results, in a manner consistent with the principles of economy, efficiency and effectiveness

These costs must be essential for the performance of the project and would not be incurred if the project did not take place. The participant must be able to justify the resources used to attain the objectives set. The EU grant must not be diverted to finance other projects or other activities. The principles of economy, efficiency and effectiveness: refers to the standard of “good housekeeping” in spending public money effectively. Economy can be understood as minimising the costs of resources used for an activity (input), having regard to the appropriate quality and can be linked to efficiency, which is the relationship between the outputs and the resources used to produce them. Effectiveness is concerned with measuring the extent to which the objectives have been achieved and the relationship between the intended impact and the actual impact of an activity. Cost effectiveness means the relationship between project costs and outcomes, expressed as costs per unit of outcome achieved. Costs must be reasonable and comply with the principles of sound financial management, with the objectives of the project and with the formal aspects of the reporting of this expenditure, including the follow-up of the budget in terms of budget allocation and schedule of the cost. Recorded in the accounts of the participant and, in the case of any contribution from third parties (affiliates, members…), recorded in the accounts of the third parties

Associations and affiliates (if applicable to you, please see under Art. I.11 of the grant agreement + Annex I) Please note that 'natural persons' cannot be considered as a member, only legal entities.

7

Where an association participating in the action involves its members or a participating company involves its affiliates to carry out the work or parts thereof, the costs incurred by the members or the affiliates can be accepted provided they can be verified as being 'actual' and follow the guidance below. (a) For members of an association / European Economic Interest Group The participant (association) shall • Provide a clear description and evidence of the association's structure including the membership list; • Ensure that the contractual provisions applicable to him, especially those related to the eligibility of costs and the checks and audit that the EASME and/or the European Commission may carry out, are also applicable to its members; • Retain sole responsibility to carry out the action and for compliance with the provisions of the grant agreement. The member(s) involved in the action shall be clearly identified and their activities duly described in the work programme (Annex I to the grant agreement). (b) For affiliate(s) The participant ('Mother Company') shall • Provide a clear description and evidence of the ownership structure showing the affiliation with the affiliate(s); • Provide clear evidence that the costs are recharged and therefore incurred by the participant; The affiliate will execute the tasks in relation to the project on behalf of the participant at no additional financial cost and without profit. When submitting the final technical implementation report, the participant (Association/Mother Company) shall identify the work performed and resources deployed by each member/affiliate involved in the action. In addition, the participant (Association/Mother Company) shall, besides its own financial statement, also provide an individual financial statement from each member/affiliate involved in the action and a summary financial statement consolidating the sum of eligible costs borne by the participant (Association/Mother Company) and each member/affiliate involved in the action, as stated in their individual financial statements. Exchange Rates to be used in financial statements For participants of non-EURO countries there are two options to choose, i.e. any conversion of actual costs into euro shall either be made

1. at the monthly accounting rate established by the Commission and published on its website applicable on the day when the cost was incurred

8

or 2. at the monthly accounting rate established by the Commission and published on its

website applicable on the first working day of the month following the period covered by the financial statement concerned.

Website: http://ec.europa.eu/budget/inforeuro/index.cfm?fuseaction=home&Language=en Cost categories:

Eligible costs must be split into direct and indirect costs. They shall be presented in Annex II of the grant agreement as well as in the financial statements under the following headings:

Direct Costs Indirect Costs

1. Staff Costs 6. Indirect eligible costs 2. Subcontracting 3. Travel costs and Subsistence Allowances for Staff 4. Purchase Costs for Equipment 5. Other specific costs

V WHAT ARE NOT ELIGIBLE COSTS? Costs calculated in accordance with other conventions e.g. "current costs", "notional rents", "opportunity costs", etc. are not eligible. Therefore, no notional costs should be charged, e.g. in respect of revaluation of buildings or capital equipment, estimated or imputed interest, estimated rentals, etc. Other costs which are not eligible include in particular:

• value of contributions in kind, e.g. if a party who is not a signatory to the grant agreement provides expertise, meeting rooms, brochures etc. free of charge as their contribution to the action, the value of these cannot be included as part of the eligible costs nor be claimed, as no cost is incurred by a participant to the Agreement;

• "return on capital employed", including dividends and other distributions of profits; • provisions for losses or possible future losses or charges; • debt and debt service charges; • interest owed; • provisions for doubtful debts; • resources made available to a participant free of charge; • unnecessary or ill-considered expenses, excessive or reckless expenditure; • VAT, unless the participant can show that he is unable to recover it;2 • any cost incurred or reimbursed in respect of another Union grant; • exchange losses,

2 In such a case the participant must provide the EASME with proof from his national tax authorities.

9

VI COST CATEGORIES

VI.1 STAFF COSTS

The cost of staff assigned to the action, comprising actual salaries plus social charges and other statutory costs included in the remuneration, provided that this does not exceed the average rates corresponding to the participant’s usual policy on remuneration. Please note that costs which are not defined in the employment contract cannot be considered eligible.

The corresponding salary costs of personnel of national administrations (incl. local, regional administrations) are eligible to the extent that they relate to the cost of activities which the relevant public authority would not carry out if the project concerned were not undertaken.

Only costs related to the actual hours worked by the persons directly carrying out the technical, analytical, promotional and dissemination work under the action may be charged to the grant agreement (Management, administrative, financial and secretarial staff are deemed to be covered in the indirect costs.).

Such persons must be

• directly employed by the participant in accordance with national law;

• under the participant’s sole technical supervision (in essence the technical output must belong to the participant);

• remunerated in accordance with the normal practices of the participant provided these are acceptable to the EASME.

Staff Costs are calculated as follows:

The following three elements must be known in order to calculate the total staff costs that can be charged to the action:

• Working time must be recorded (“timesheets”) throughout the duration of the action.

You must be able to produce evidence to support the number of hours that each person has worked on the project. This can be by the use of a reliable time recording system or adequate alternative evidence giving an equivalent level of assurance. We have regularly identified time charged to the project while the staff member is on leave or attending conferences unrelated to the project, which puts into question the reliability of the time recording system as a whole. For each person involved in the project, participants must have daily records of all hours spent by a given person (i.e. the timesheet shall not only record the time spent on a specific project, but shall reconcile the total working time of each person, say for example 1700 hours per year).The records should be certified at least once per month by the person in charge of the work ('project manager'). Estimates of hours worked are not acceptable If timesheets are used, please ensure that they are completed in good time and are properly authorised. A timesheet template can be found at: http://ec.europa.eu/energy/intelligent/files/implementation/doc/template_timesheet_en.xls

10

• Remuneration costs charged should be taken from the payroll account and should be

the total gross remuneration plus the employer's portion of social charges (e.g. holiday pay, pension contributions, health insurance and social security payments, see table below). Remuneration costs can be calculated individually for each employee or as an average by category of staff (the method should fairly represent actual labour costs).

Eligibility of taxes and charges related to personnel

(Presented per country and in alphabetical order). This list is not comprehensive and will be updated whenever necessary.

Eligible: Legal basis:

Indemnité de départ à la retraite

Eligibility within the limits set by law or mandatory collective agreement (FR)

Code du Travail

Intéressement des salariés à l'entreprise (FR) Code du TravailParticipation des salariés aux résultats de l'entreprise (FR)

Code du Travail

Taxe d'apprentissage (FR) Code général des impôts Participation à la formation professionnelle continue (FR)

Code du Travail

Taxe sur les salaires (FR) Code général des impôts Versement Transport (VT) (FR) Code général des collectivités territoriales Non-domestic property tax ("business rate") (UK - England and Wales)

UK Local Government Finance Act 1988

Partially eligible: Legal Basis: Fixed Term Workers Act, FTWA: any related provision will be considered eligible up to the rate provided for in the 2008 implementation rules of the Act (IRL)

Protection of Employees (Fixed-Term Work) Act 2003

Allocation d'assurance pour les travailleurs involontairement privés d'emploi (FR) (also known as Provision Perte Emploi, Allocation Retour à l'Emploi or Allocation Perte d'Emploi). When employers have entrusted the management of the insurance benefit to an external entity (ie pôle emploi), eligibility is limited to the proportion of payments actually made to this entity during a given year. When employers manage themselves the insurance benefit, eligibility is limited to the proportion of payments actually made during a given year

Code du Travail

Ineligible: Legal Basis: Crédit d'impôt recherche (FR) Code général des impôts Taxe professionnelle (FR) Code général des impôts Participation à l'effort à la construction (FR) Code général des impôts Imposta Regionale sulle Attività Produttive, IRAP (IT)

Decreto Legislativo 15 dicembre 1997, n. 446

11

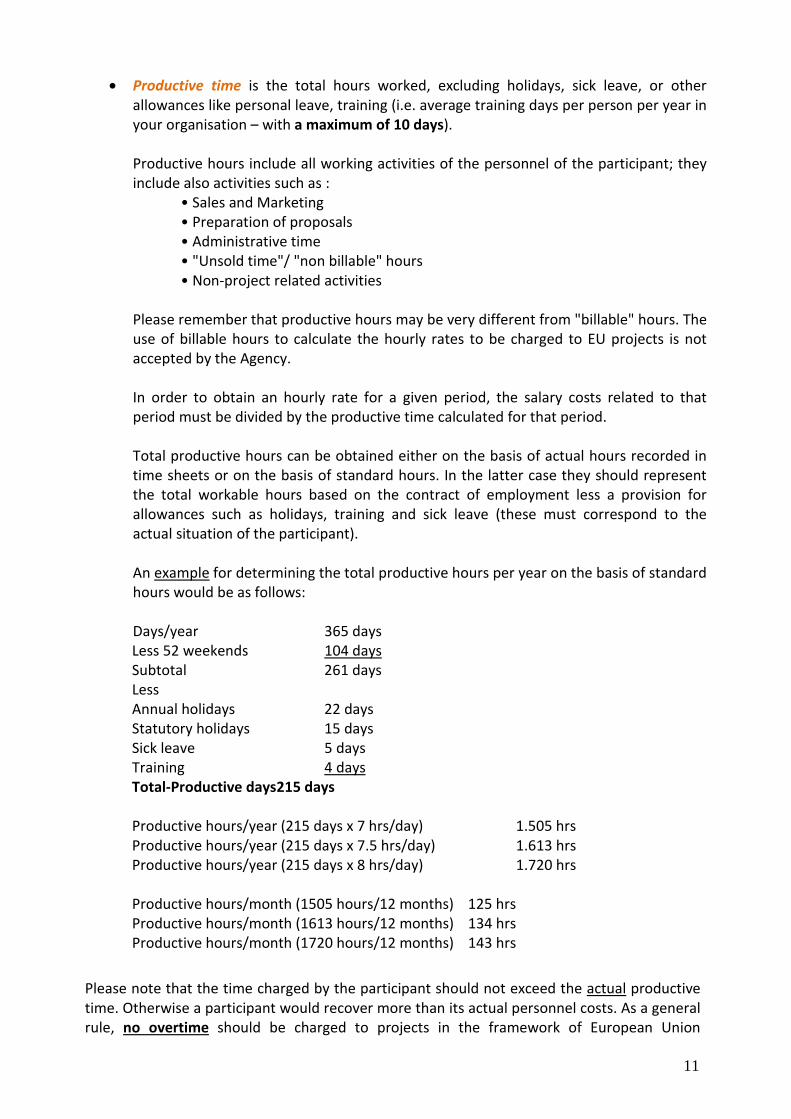

• Productive time is the total hours worked, excluding holidays, sick leave, or other allowances like personal leave, training (i.e. average training days per person per year in your organisation – with a maximum of 10 days). Productive hours include all working activities of the personnel of the participant; they include also activities such as :

• Sales and Marketing • Preparation of proposals • Administrative time • "Unsold time"/ "non billable" hours • Non-project related activities

Please remember that productive hours may be very different from "billable" hours. The use of billable hours to calculate the hourly rates to be charged to EU projects is not accepted by the Agency. In order to obtain an hourly rate for a given period, the salary costs related to that period must be divided by the productive time calculated for that period. Total productive hours can be obtained either on the basis of actual hours recorded in time sheets or on the basis of standard hours. In the latter case they should represent the total workable hours based on the contract of employment less a provision for allowances such as holidays, training and sick leave (these must correspond to the actual situation of the participant). An example for determining the total productive hours per year on the basis of standard hours would be as follows: Days/year 365 days Less 52 weekends 104 days Subtotal 261 days Less Annual holidays 22 days Statutory holidays 15 days Sick leave 5 days Training 4 days Total-Productive days 215 days Productive hours/year (215 days x 7 hrs/day) 1.505 hrs Productive hours/year (215 days x 7.5 hrs/day) 1.613 hrs Productive hours/year (215 days x 8 hrs/day) 1.720 hrs Productive hours/month (1505 hours/12 months) 125 hrs Productive hours/month (1613 hours/12 months) 134 hrs Productive hours/month (1720 hours/12 months) 143 hrs

Please note that the time charged by the participant should not exceed the actual productive time. Otherwise a participant would recover more than its actual personnel costs. As a general rule, no overtime should be charged to projects in the framework of European Union

12

Programmes, unless this element has been taken into account in the calculation of the total productive hours and overtime is reimbursed specifically by the participant, and the overtime is necessary to the project and in conformity with the participant's national legislation, and it is the policy of the participant to pay overtime. Only the hours worked on the project can be charged. The hourly rate applicable to these "overtime" hours has to be taken into account separately from the standard working hours and there must be a system that allows the identification of the productive hours worked for the project.

Parental leave of personnel assigned to the action: the amount of this allowance may be an eligible cost under certain conditions, in proportion to the time dedicated to the project. Participants who deduct time for parental leave from the standard annual productive time are already compensated for such costs and therefore are not allowed to charge costs related to individual employees' parental leave to the specific IEE project. Participants who do not deduct time for parental leave from the standard annual productive time may charge such costs in proportion to the time dedicated to the project provided that they are mandatory under national law (e.g. statutory maternity pay), that the participant has effectively incurred such costs, and that they are not compensated by the national or regional authorities. Only costs related to personnel who worked on the project before the parental leave may be eligible. Bonus payments: As a general rule, payment of bonuses that are not an employer's obligation arising from the national regulation relating to labour law or even from the employment contract and that are within its discretion may not be considered as part of normal remuneration, even though identified as a payment on the payroll, and their eligibility may be questioned (in particular with respect to the criterion of necessity for carrying out the project). However, if such payments are part of the normal salary and benefit package of an employee they could be considered as part of the normal personnel costs. Nevertheless, these costs have to be compliant with the eligibility criteria of Article II.14 of the GA, in this case the most important of which will be the criterion of economy and coherence with the participant's usual accounting practices. The costs must be in conformity with the usual behaviour of the participant. The following criteria must be applied to the “bonus payments” to be considered eligible. Failing to meet one of these criteria means, in principle, rejection of the "bonus payments":

1) The bonus scheme must be provided for in the internal regulations and/or practices of the organisation (calculation method, category of employees falling under this scheme, maximum amount, etc); 2) The bonus scheme must apply to all projects (EU and non-EU projects, national and international) of the same kind; i.e. the bonus must be given to all international (EU and non EU) or to all national projects. Bonus schemes should be implemented in a consistent manner for the same type of activities/projects. 3) The bonus payments must not result in a level of remuneration inconsistent with the current market conditions for a worker of the same category/grade/experience;

13

4) The bonus payments must be recorded in the accounts of the contractor as personnel costs and must be subject to taxes and social security charges applicable to salaries or specifically exempt from such taxes and/or charges. 5) These bonuses can only be paid as part of the employee's gross remuneration. The criteria (qualitative or financial targets, research activities carried out, contractor's profitability, etc.) used to calculate the amount of the bonus can be accepted provided they are of general application within the participant's organisation and are objective.

• Special case: Companies' owners not receiving a salary: There must be a clear distinction depending on whether or not a salary is paid and accounted for as such in the books of the participant. When no salaries are paid, there is a problem on how to measure the value of the contribution of these persons to the project. Remuneration Cost: as remuneration cost the agency will consider the average income (dividends are not considered eligible costs) as declared in the annual tax return, over the last three years. Productive time: 1720 hours based on 215 workable days and 8 hours working day. This means that, independently from the actual number of productive hours of the person concerned, the only figure to be used for this concept (productive hours) is set at 1720 hours. This applies only for the calculation of this formula for this special case of SME owners not receiving a salary. In the other cases (declaration of personnel costs on the basis of actual costs) the usual rules for productive hours detailed before in these guidelines apply. Furthermore, and also for this special case of SME owners/natural persons not receiving a salary, the maximum number of hours claimed by the same SME owner/natural person when adding all the hours worked for EU projects in the same year cannot be superior to 1720.

• Please remember that:

Hourly rates included in the 'Contract Preparation Forms' do not constitute 'agreed' hourly rates, they are only to be considered as 'estimates'. The financial statements to be submitted at the time of the interim/final report on the action should present the actual costs incurred and therefore use the actual rates, recalculated on the basis of the real staff costs paid. These actual costs need to be evidenced by the corresponding payslips, bank transfers, etc. - evidence which might be requested by the EASME on a case by case basis.

Only costs can be reimbursed and not prices (price = staff cost + commercial uplift) that would normally be charged to customers when engaging in commercial activities. Staff costs will only be considered eligible if they are reasonable and justified, and if they accord with the principles of sound financial management (i.e. (i) they may not unnecessarily increase the cost of the project and (ii) substantial deviations from the average cost of similar labour in the country concerned must be justified).

14

VI.2 SUBCONTRACTING (external services) The general rule is that participants shall implement the action and shall have the necessary resources to that end. However, it is accepted that, when the GA provides for it accordingly, and as an exception certain parts of the work may be subcontracted. A subcontractor is a type of third party, i.e. a legal entity which is not a participant of the GA, and is not a signatory to it. It appears in the project because one of the participants appeals to its services to carry out part of the work, usually for specialised jobs that it cannot carry out itself or because it is more efficient to use the services of a specialised organisation (e.g. setting up a website for the project). The subcontractor is defined by certain characteristics:

• The agreement is based on "business conditions"; this means that the subcontractor charges a price, which usually includes a profit for the subcontractor. This makes it different from other third parties' contributions where the third party charges only for the costs of the activity. • The subcontractor works without the direct supervision of the participant and is not hierarchically subordinate to the participant (unlike an employee). • The subcontractor carries out parts of the work itself • The subcontractor's motivation is pecuniary, not the action itself. It is a third party whose interest in the project is only the profit that the commercial transaction will bring. A subcontractor is paid in full for its contribution made to a project by the participant with whom it has a subcontract. As a consequence subcontractors do not have any IPR rights on the foreground of the project. • The responsibility vis-à-vis the EU for the work subcontracted lies fully with the participant. The work that a subcontractor carries out under the project belongs to the participant in the GA. A subcontractor has no rights or obligations vis-à-vis the Commission, the Agency, or the other participants, as it is a third party. However, the participant must ensure that the subcontractor can be audited by the Commission, the Agency or the Court of Auditors.

In principle, the participant should not subcontract part of the work to its affiliates. These should be identified as third parties linked to a participant and included in the GA via a special clause (see affiliates section, page 7 above). Accordingly, subcontracting between participants of the same consortium is not permitted under any circumstances. All participants by definition contribute to and are interested in the project, and where one participant needs the services of another in order to perform its part of the work, it is the second participant who should declare and charge the costs for that work. Subcontracting costs are direct costs. They have to be identified during the negotiations of the project, and be set out in Annex I ("Description of the Action") and Annex II ("Estimated budget of the action") to the grant agreement. Otherwise any amounts claimed will generally not be eligible. According to Article II.9.2, any subcontracting during the course of the action, which was not foreseen or identified in the Description of the Action, is subject to prior written approval by the Agency. If you wish to use sub-contractors that are not yet included in Annex I, you should send an amendment request through the project coordinator to the Agency service that signed

15

the grant agreement. If this request is approved your grant agreement will be amended and the costs will then be eligible for inclusion in your cost claims. Subcontracting may only cover the execution of a limited part of the action. Subcontracts must be awarded in accordance with the conditions set out in Article II.9 of the grant agreement. Where the implementation of the action requires the purchase of goods, or services, the participants shall award the contract to the tender offering best value for money, or as appropriate to the tender offering the lowest price. In doing so, they shall avoid any conflict of interest. Please note that EASME does not impose specific procurement rules on the participants. All participants in the agreement shall act in accordance with the European and national procurement rules and regulations applicable to their organisation and their own internal procedure on procurement, as long as this respects the criteria on 'best value for money or lowest price' and 'absence of conflict of interest'. In all cases and even when the participant does not organise a formal tendering process, this should be substantiated with supporting documents. The participants must ensure that their agreements with subcontractors mention in particular that the EASME and/or the European Commission may at any time during the grant agreement and up to five years from the date of payment of the balance, arrange for audits to be carried out by the EASME and/or the European Commission or any other outside body authorised by them as well as by the European Court of Auditors and the European Anti-fraud Office (OLAF). Copies of the three highest invoices for subcontracting must be submitted to the EASME with the corresponding financial statement. Copies of the other invoices (if any) may however, be requested on a case by case basis. In general, supporting documentation should be kept in the participant’s files and provided at the EASME's request. All copies of invoices for subcontracting must (where possible) make reference to the grant agreement or action but in any case to the concrete tasks and services concerned.

• Work contracts

In-house consultants deliver 'external services' and are to be considered under the 'subcontracting' cost category.

However : costs of consultants (i.e. natural (physical) persons) who join the participant's project team may be classified under staff costs, regardless of whether the consultants are self-employed or employed by a third party, if the criteria listed below are fulfilled (in addition to the general eligible cost criteria of the grant agreement).

Persons delivering services under 'civil contracts' (a form of service contract under private law with the obligation to deliver results in a specified timeframe) are to be considered under the 'subcontracting' cost category. However, if the persons join the participant's project team the costs may be classified under staff costs if every single of the 7 criteria listed below is fulfilled (in addition to the general eligible cost criteria of the grant agreement).

16

THE CRITERIA:

(1) The consultant/person has a contract to work for the participant and (some of) that work involves tasks to be carried out under the IEE grant agreement

(2) The consultant/person works under direct instructions/supervision of the participant

(3) The consultant/person works in the premises of the participant as a member of the project team

(4) The output of the work belongs to the participant

(5) The costs of employing the consultant/person are reasonable, are in accordance with the normal practices of the participant (provided that these are acceptable to the EASME) and are not significantly different from the personnel costs of employees of the same category working under a labour law contract for the participant

(6) Travel and subsistence costs related to the participation of the consultant/person in project meetings or other travel relating to the project is directly paid by the participant. The applicable tax and social security costs related to the consultant are paid by himself/herself, the applicable tax and social security costs related to the person working under a civil contract are paid by the participant.

(7) The consultant/person MUST be a user of the participant's infrastructure (i.e. user of the 'indirect costs')

Please note that teleworking may only be allowed if the standard working conditions applicable to the employees of the participant allow it (such an opportunity should be offered to the personnel of the organisation as a whole regardless the employment status -employees and in-house consultants- and clear rules should be available for the purpose of an audit), and if there is a system that allows the identification of the productive hours worked for the project and the above mentioned criteria are still respected. A copy of the standard working conditions might be requested by EASME on a case by case basis.

Remuneration cost:

=> in the case of "in-house consultants", the costs (excluding VAT when applicable), should be taken from the invoice received for the work performed. Invoices should indicate the project on which the persons have worked, the tasks carried out and the hours spent. => in the case of "persons working under a civil contract", the costs (excluding VAT when applicable) should be taken from the payroll account and should be the total gross remuneration plus the employer's portion of social charges (e.g. holiday pay, pension contributions, health insurance and social security payments) in line with the amounts agreed in the civil contract. DISCLAIMER : The participant should make sure that he/she complies with the legislation in force in his/her Member State related to the use of consultants (self-employed or employed by a third party). The legislation may prohibit or restrict the use of such consultants. The participant remains responsible for checking, prior to the allocation of such consultants to the project and taking into account the aforementioned conditions, that he/she does not infringe this legislation.

17

VI.3 TRAVEL AND SUBSISTENCE ALLOWANCES Actual travel costs and related subsistence allowances for staff taking part in the action may be charged to the action provided they comply with the participant’s established internal rules and usual practice. Travel costs must be needed for the work in the project, or for activities related to it (e.g. presentation of a paper explaining the results of the project in a conference). Travel costs related to a conference where no specific project-related work will be performed or presented by the participant would not be eligible. Travel costs should be limited to the necessity for the project; any extension of the travel for other professional or private reasons is not an eligible cost. Travel costs of subcontractors, if applicable, are to be included in their subcontracts. Travel expenses of experts participating on punctual basis in the project (i.e. attendance to specific meetings) are not travel costs; however, they may be considered direct eligible costs and be booked under the "other specific costs" section, provided the participation of those experts is duly foreseen in Annex I. These costs may be reimbursed to the experts by the participant or the participant may directly deal with the travel arrangements (and therefore be directly invoiced). Subscription fees to conferences or events, where relevant, should be charged under “other specific costs” (see point V.5 below). Missions to any destination outside the Member States and the third countries eligible to participate in the programme should be reasonable and justifiable as necessary for the fulfilment of the action (see definition of eligible costs). Depending on the financial impact of the travel it might be convenient to discuss it with the Project Advisor. Please note that each participant, according to their internal travel rules, should claim less daily allowance if dinner (or lunch) costs are paid by the organising participant.

VI.4 DURABLE EQUIPMENT Durable equipment charged to the grant agreement must be specifically required for the purpose of the action, have an expected life equal to or greater than the duration of the work under the grant agreement and must be entered in the inventory of capital expenditure of the participant according to the relevant accounting principles. It must be acquired during the duration of the action. Utilisation of existing equipment and installations are deemed to be included in the budget via the indirect costs. It must be depreciated in accordance with the tax and accounting rules applicable to the participant and generally accepted for items of the same kind. Only the portion of the equipment’s depreciation corresponding to the duration of the action and the rate of actual use for the purpose of the action may be taken into account by the EASME.

18

Due to the type of actions (non-technological), equipment costs will only be accepted under exceptional circumstances and only with prior written approval from the EASME.

VI.5 OTHER SPECIFIC COSTS Other specific costs, are those costs arising directly from requirements imposed by the agreement (dissemination of information, specific evaluation of the action, audits, translations, reproduction, etc.), including the costs of any financial services (especially the cost of financial guarantees). Such costs may also include specific costs incurred by the coordinator when fulfilling his responsibilities in relation to the overall management of the action and the co-ordination of the participants. All other specific costs, which cannot be included under the previous classifications of direct costs, may only be charged either with the prior written approval of the EASME or alternatively if these costs were foreseen and clearly specified in the Description of the Action (Annex I of the grant agreement). These costs may include items such as,

- costs of organising seminars, workshops, conferences (unless a subcontract has been concluded with a service provider, in which case these costs should be charged under “Subcontracting”);

- subscription fees for conferences and events; - travel and subsistence allowances of persons who are not on the payroll of the

participants foreseen in the Description of the Action (Annex I of the grant agreement); - charges for financial guarantees required by the agreement; - costs of audit certificates required by the agreement; - bank charges of the co-ordinator related to opening a specific bank account for the

agreement or re-distributing the payments from the EASME to other participants. Direct costs internally invoiced: Sometimes facilities are shared between different departments of the same legal entity, and the costs of their use are charged through internal invoices. This type of costs may be eligible if their use for the project and the usage is properly recorded. In such case, the costs claimed must represent a fair apportionment and be based on objective, measurable and auditable criteria's. The costs arising from internal invoices delivered by units or groups which belong to the same legal entity are eligible as long as the other eligibility requirements are met (Art II.19 of the grant agreement) and there has been no attempt to 'subcontract' within a single entity by charging market prices (i.e. with a commercial margin). Internally invoiced overheads are not eligible as direct project costs, as this is already covered by the indirect costs. Intra-group invoices:

19

The same principle as for internal invoices here above applies to a participant being charged by a different legal entity ("sister company") making part of the same group as the participant: Cross Invoicing: A participant is invoiced by another participant of the same IEE project. This practice shall be avoided. It is the participant who is going to incur the costs that should register and charge the costs to the project and not charge its costs to other participants.

Dinner costs When participants organise project meetings, the costs for the organisation of one dinner per meeting can be accepted under 'Other Specific Costs'. The maximum eligible number of persons to be included in the dinner costs is twice the number of participants in the consortium (this is deemed to cover also invited external experts). The maximum dinner price per person should not exceed 40€. Any deviations should be explained when submitting the financial statements. Where a dinner is paid by one of the participants, the subsistence allowance of the participants is to be reduced accordingly when claiming the travel cost (to avoid double funding). Participation in events The participation in events (conferences, exhibitions etc.) is often already included in Annex 1 and the CPF's. If not, participants should apply the definition of eligible direct costs – the participation in an event must be reasonable and necessary for the fulfilment of the action. If participants have doubts they might consult the EASME prior to the event in question. Participation in events should normally be by one person and be limited to two persons per project consortium.

VI.6 ELIGIBLE INDIRECT COSTS The indirect costs incurred in carrying out the action are only eligible for flat-rate funding fixed at 60% of the participants total eligible direct staff costs. Indirect costs do not need to be supported by accounting documents. Energy Management Agencies created under the IEE programmes may only claim indirect costs as of the moment that they are no longer part of an ongoing IEE Grant Agreement in which their agency was established. Equally, any organisation receiving an operating grant from the EU for the period of the action or parts of the period cannot claim the 60% indirect costs for the period in question. Indirect costs are deemed to cover (non-exhaustive list, examples only) :

- secretarial/administrative/financial/managerial etc…costs (Exceptions could occur when tasks outlined in the action justify a distinct role of such staff, which then also has to be recorded in time sheets, and on condition that these costs are directly booked to the project) - Consumables : Toner, office supplies, paper, photocopies, etc... - Bank charges (except bank charges incurred by coordinator as specified under V.5)

20

- Postal services except when it concerns courier services (e.g. DHL, UPS, TNT) necessary for the action or in case of mass mailings. The latter should then be registered as a direct cost for the project. - Utilisation of existing equipment and installations

VI.7 BUDGET TRANSFERS The budget sets the maximum acceptable amount per cost category and per participant. It is under the responsibility of the coordinator to adjust the budget of the project, and request, in due time, its modification. The budget should be set up in the best possible way before the beginning of the action. Nevertheless, changes in budget between partners and/or between categories can be expected during the cause of the action. However, budget transfers shall remain limited. An amendment to the grant agreement through a supplementary agreement is necessary in the event where:

• The amount to be transferred between participants exceeds 20% of the total budget of the receiving participant (i.e. the participant receiving the extra budget) and/or

• The amount to be transferred between cost categories of a given participant exceeds 20% of the total budget of this participant and/or

• The adjustment of expenditure affects the implementation of the action Any transfer of budget exceeding the above thresholds or affecting the implementation of the action must be proposed to EASME by the coordinator. He/she shall submit to the Agency a written request substantiating the need for the budget transfer for himself and/or for the co-participants concerned together with a new version of Annex II (including the updated Contract Preparation Forms). Failure to submit a written request to the EASME in good time, and at the latest 30 days before the end of the action, will result in the costs being limited to the original budgeted level per participant and per cost category. The EASME should be informed in writing, at the latest at the moment of the final report, on budget transfers below the 20% thresholds which did not substantially affect the implementation. No new request for the implementation of a budget transfer between cost categories and/or between participants can be accepted after the approval or rejection, by the Agency, of the final report.

VI.8 REVENUE Any revenue generated by the action needs to be recorded and must be reported to the EASME in the final Financial Statement. Account must be taken of revenue which is

21

- established (revenue that has been collected and entered in the accounts),

- generated or confirmed (revenue that has not yet been collected but which has been generated or for which the participant has a commitment or written confirmation) on the date when the request for payment of the balance of the grant is established.

Revenue can be, for example, financial transfers or their equivalent to the participant from third parties, income generated by the project and "co-financing". The grant shall be limited to the amount necessary to balance the action's receipts and expenditures; it may not in any circumstances produce a profit for the participants (i.e. any surplus of total actual receipts over the total actual costs). Any surplus shall result in a corresponding reduction in the amount of the grant.

VII FINANCIAL GUARANTEES Where required by the special conditions of the grant agreement, the participant concerned shall provide a financial guarantee from a bank or an approved financial institution established in one of the Member States of the European Union. The financial guarantee shall be drawn up in accordance with the model letter to be provided by the EASME, linked here below, http://ec.europa.eu/energy/intelligent/files/call_for_proposals/doc/easme-2013-model-bank-guarantee_en.doc and shall indicate that the guarantor stands as first call guarantor who shall not require the Agency to have recourse against the principal debtor (i.e. the participant concerned). The financial guarantee shall remain in force until the Agency proceeds with the payment of the balance of the grant pursuant to the provisions of Article I.5.3. The Agency undertakes to release the guarantee within sixty (60) days following that date. EASME will return the original financial guarantee to the coordinator who shall be responsible to return the financial guarantee immediately to the co-participant. a) When to submit the financial guarantee?

Once the coordinator has received the duly completed and original financial guarantee(s) from the consortium partner(s), he/she will submit it/them, in any case within 60 days from the date of entry into force of the agreement as provided for in Article I.5.1 second paragraph.

b) Where to submit the financial guarantee?

The coordinator shall submit the financial guarantee(s) to the EASME to the address indicated in the grant agreement.

22

c) How to avoid frequent mistakes?

• The amount of the pre-financing should be correctly calculated. It must equal exactly 30% (two decimals accuracy) of the Union financial contribution of the participant concerned.

• Do not add any calendar date indicating the end of validity of the financial guarantee. This will result in the rejection of the financial guarantee.

• The financial guarantee shall be governed by the law applicable to the grant agreement; if modified this will result in the rejection of the financial guarantee.

VIII CHECKS, and AUDITS a) Audit Certificates An audit certificate on the financial statements and underlying actions’ accounts is required from each private body participating in the action whose total EU contribution exceeds EUR 225,000 for calls up to 2012, and EUR 325,000 for call 2013 only (please refer to Article I.5.3 of the grant agreement,). It shall be provided by an independent external auditor, chosen by the participant. The external auditor shall issue the audit certificate for the attention of the participant and not for the attention of the EASME and/or the European Commission. Please refer to the template and guidelines available under section "audit certificate", on http://ec.europa.eu/energy/intelligent/managing-projects/day-to-day-management/index_en.htm, With a view to avoiding delays in the submission of external audit certificates, participants should select and contract the external auditor well before the final financial statement is due. The cost of obtaining an audit certificate is eligible (excluding VAT when applicable) only when incurred by the participants within a maximum period of two months following the completion of the action, and should be declared under the Other Specific Costs category. b) Purpose of Audits The Agency and/or The Commission may, at any time during the implementation of the project, and up to five years from the date of the payment of the final balance, arrange for financial audits to be carried out. The audits may cover:

• financial aspects • systemic aspects • other aspects such as accounting and management principles.

23

c) Participants' rights and obligations In order to permit a complete, true and fair verification that the project and the grant are (have been) properly managed and performed, participants are required to:

• keep the originals, or in exceptional cases, where the national legislation accepts or contemplates this possibility, duly authenticated copies – including electronic copies – of all documents relating to the grant agreement for up to five years from the date of the payment of the final balance of the project.

In principle: - documents received should be kept on the medium on which they arrived. - documents created should be kept on the medium on which they were compiled. This implies that documents received or created on paper form should be kept in their original paper form. Documents received or created only in electronic form should be kept in their original electronic form. No paper copy is required of original electronic documents.

For cases where the relevant national authorities/law allows the participant to destroy the original documents for the transfer to other reliable support, this support is considered as a duly authenticated copy. • ensure that the Agency and/or the Commission's services, and/or any external body(ies) authorised by it, have on-the-spot access at all reasonable times, notably to the participant's offices where the project is being or has been carried out, to its computer data, to its accounting data and to all the information needed to carry out those audits, including information on individual salaries of persons involved in the project. They shall ensure that the information is readily available on the spot at the moment of the audit and, if so requested, that data be handed over in an appropriate form. • make available directly to the agency and/or the Commission all the detailed data that it may request, • ensure that the rights of the Agency and/or the Commission and the European Court of Auditors to carry out audits are extended to the right to carry out any such audit or control on any third party whose costs are reimbursed in full or in part by the EU contribution, on the same terms and conditions. • Ensure the right of the Agency and/or the Commission to interview people working or having worked on the IEE project.

d) Audits may be carried out by

• The Agency and/or the Commission (its own departments – including the anti-fraud office, OLAF – or by any of its duly authorised representatives (including external auditors appointed by the Agency and/or the Commission)). • The European Court of Auditors (by its own departments or by any of its duly authorised representatives).

24

e) Reports

• A provisional report shall be drawn up on the basis of the findings made during the financial audit and sent to the participant audited. • The participant may make observations within one month of receiving the report. The Agency and/or the Commission may decide not to take into account observations or documents sent after that. • The final report shall be sent within two months of expiry of this deadline.

On the basis of the conclusions of the audit, the Agency and/or the Commission may issue recovery orders and apply sanctions including financial penalties. f) Financial penalties Any participant found to have seriously failed to meet its obligations under the GA shall be liable to financial penalties of:

• between 2% and 10% of the value of the EU contribution received by that participant; • between 4% and 20% of the value of the EU contribution received by that participant in the event of a repeated offence in the five years following the first infringement.

Example: It is determined that a participant has seriously failed to meet its obligations under the GA. According to the report(s) to the Agency on the distribution of the EU financial contribution between participants, this participant has received an EU financial contribution of EUR 700,000. According to the audit’s findings, it is the first serious failure of this participant’s in actions supported by the Commission in the last five years. This participant may be subject to additional financial penalties of between EUR 14,000 and EUR 70,000= (2%-10%) of EUR 700,000. This is in addition to the recovery of the amount overpaid (unjustified financial contribution). The provision also applies to participants who have been guilty of making false declarations. In both cases, the participant will also be excluded from all grants financed by the EU for a maximum period of two years from the date the infringement is established. IX AMENDMENTS

During the lifetime of a project, situations may occur that require the modification of the grant agreement. In order to make the process transparent and efficient, we have developed a form called 'Modification to the Grant Agreement'.

This form contains two parts: one part that needs to be completed by the coordinator and a second part in which the documents that need to be submitted together with the modification form are listed.

25

You can download it from: http://ec.europa.eu/energy/intelligent/files/implementation/doc/modification_grant_agreement_template_en.xls

X HOW TO AVOID FREQUENT MISTAKES As a participant of grant support, under the IEE 2 programme, it is in your interest to make sure that your claims for cost reimbursement are reliable, correct, and accurate. This will considerably speed-up repayment of your eligible project costs, and should prevent you having to pay back some or all of the EU financial contribution received, should errors be detected during the course of financial audits, controls or checks. These refunds may be subject to financial penalties. In fact, the vast majority of mistakes arise from misunderstandings of the rules or a lack of attention to the detail of the provisions of the grant agreements and associated guidelines. Here below are listed the most frequently recurring errors along with some explanatory notes. A. Costs claimed that are not substantiated or are not linked to the project All costs claimed, with the exception of applicable flat rate, should be based on the actual costs incurred. They must be supported by evidence that they are actual (recorded in the accounts of the participant and supported by invoices for example), paid (supported by bank statements for example), and linked to the funded project. As a general rule, neither estimated amounts, nor budgeted amounts, are acceptable. Where these conditions are not met the amounts will be deemed to be ineligible. B. Sub-contracting The use of sub-contractors should be identified during the negotiations of the project, and be set out in Annex I ("Description of the action") to the grant agreement. Otherwise any amounts claimed will not be eligible. If you wish to use sub-contractors that are not yet included in Annex I, you should send an amendment request through the project coordinator to the Agency service that signed the grant agreement. If this request is approved your grant agreement will be amended and the costs will then be eligible for inclusion in your financial statement. Please note that EASME does not impose specific procurement rules on the participants. All participants in the agreement shall act in accordance with the European and national procurement rules and regulations applicable to their organisation and their own internal procedure on procurement, as long as this respects the criteria on 'best value for money or lowest price' and 'absence of conflict of interest'. In all cases and even when the participant does not organise a formal tendering process, this should be substantiated with supporting documents. In addition, it is underlined that sub-contracting between partners of the consortium is not permitted under any circumstances.

26

C. Depreciation If you purchase equipment for your project then you are not, in general, entitled to claim the full cost of the equipment immediately. Rather, you are entitled to charge to the project the corresponding depreciation of the equipment over the part of its useful economic life that falls within the project. The amounts that you can claim annually should be based on the amount of depreciation that is incurred annually for the equipment. You should use your usual depreciation policy. Moreover, only the part of the equipment (percentage used and time of use) dedicated to the project may be charged. For example, a participant participates in a project that lasts for 3 years. In the second year of the project it acquires a machine that costs €100,000, and has a useful economic life of 5 years. The normal accounting policy of the participant is to apply "straight line" depreciation. The eligible amount would be €40,000, reflecting the depreciation charge for the 2 remaining years until the end of the project. The residual value of €60,000 cannot be charged to the project since it falls outside the project's period. D. Personnel costs - Calculation of productive hours The calculation of actual personnel costs requires the establishment of the productive hours for personnel. Productive hours should include all the time that the employee is available to undertake activities for the organisation (project and non-project activities). It should exclude weekends and holidays, but should include for instance administrative time, meetings, etc. Please remember that productive hours may be very different from "billable" hours. The use of billable hours to calculate the hourly rates to be charged to EU projects is not accepted by the Agency. For example, staff at a participant were contracted to work 36 hours per week. The calculation of cost charged to customers assumed 30 billable hours per week, and the 30 hours were used as the basis for calculating hourly rates. However, the 36 hours contracted per week should be used as the basis for calculating rates charged to EU projects. E. Personnel costs - charging of hours worked on the project Participants must be able to produce evidence to support the number of hours that each person has worked on the project. This can be by the use of a reliable time recording system or adequate alternative evidence giving an equivalent level of assurance. We have regularly identified time charged to the project while the staff member is on leave or attending conferences unrelated to the project, which puts into question the reliability of the time recording system as a whole. If timesheets are used, please ensure that they are completed in good time and are properly authorised. F. In-House consultants claimed under direct staff costs In-house consultants deliver 'external services' and are to be considered under the 'subcontracting' cost category. However : costs of consultants who join the participant's project team may be classified under staff costs, regardless of whether the consultants are self-employed or employed by a third

27

party, if every single of the 7 criteria listed below is fulfilled (in addition to the general eligible cost criteria of the grant agreement). (1) The consultant/person has a contract to work for the participant and (some of) that work involves tasks to be carried out under the IEE grant agreement (2) The consultant/person works under direct instructions/supervision of the participant (3) The consultant/person works in the premises of the participant as a member of the project team (4) The output of the work belongs to the participant (5) The costs of employing the consultant/person are reasonable, are in accordance with the normal practices of the participant (provided that these are acceptable to the EASME) and are not significantly different from the personnel costs of employees of the same category working under a labour law contract for the participant (6) Travel and subsistence costs related to the participation of the consultant/person in project meetings or other travel relating to the project is directly paid by the participant. The applicable tax and social security costs related to the consultant are paid by himself/herself, the applicable tax and social security costs related to the person working under a civil contract are paid by the participant. (7) The consultant/person MUST be a user of the participant's infrastructure (i.e. user of the 'indirect costs'). G. Value Added Tax VAT is not an eligible cost. Please ensure that VAT is always excluded from cost claims (unless the participant attached together with the financial report the relevant documents substantiating that it cannot recover VAT). H. Budget Transfer Too often, participants do not adjust their budget per cost categories and see their declared costs being limited, at the time of the final report, to this upper limit sets in the Annex II of the GA. It is under the responsibility of the coordinator to adjust the budget of the project, in order to cover as much as possible the declared costs, and request to the Agency, in due time, its modification. No new request for the implementation of a budget transfer between cost categories and/or between participants can be accepted after the approval, by the Agency, of the final report.